DocumeIt aI The World Bank FOR OMCIUL USE ONLY Cp. 1/?S3 -. 2,4 Report No. 6310-ZA STAFF APPRAISAL REPORT ZAMBIA THIRD DEVELOPMENT BANKOF ZAMBIAPROJECT November 17, 1986 Industrial and Development Finance Division Eastern and Southern AfricaRegion This document ha a mtetncted disttibution and maybe used by recipients only in the performance of ofllcial dutiea Its contents maynot othenrse be discloW without WoddBankauthorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

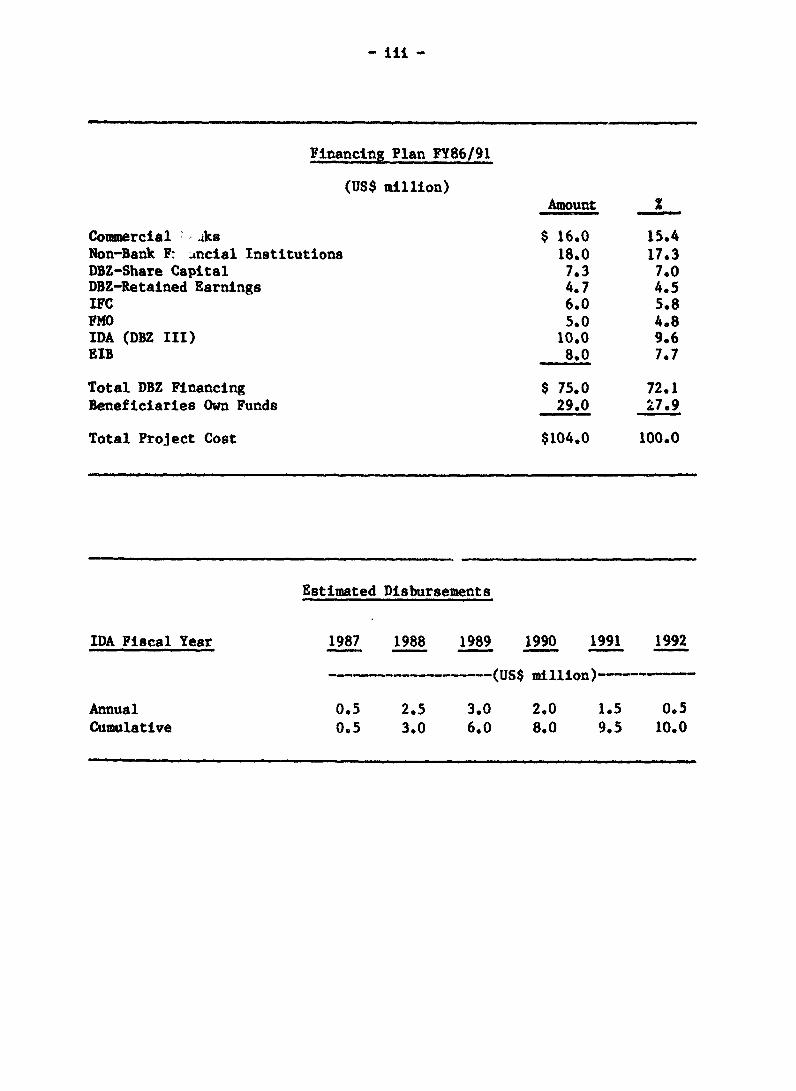

DocumeIt aI

The World BankFOR OMCIUL USE ONLY

Cp. 1/?S3 -. 2,4

Report No. 6310-ZA

STAFF APPRAISAL REPORT

ZAMBIA

THIRD DEVELOPMENT BANK OF ZAMBIA PROJECT

November 17, 1986

Industrial and Development Finance DivisionEastern and Southern Africa Region

This document ha a mtetncted disttibution and may be used by recipients only in the performanceof ofllcial dutiea Its contents may not othenrse be discloW without Wodd Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURAENCY EQUIVALENTS

Currency Unit - Kwacha (K)JS$1 - K 6.87US$0.1456 - K 1.00

The US Dollar/Zambian Kwacha exchange rate is determined by weeklyauction. The exchange rate shown above is the result of the auction heldon August 30, 1986.

WEIGHTS AND MEASURES

1 meter (m) = 3.28 feet (ft)1 kilometer (km) 0.62 miles1 sq kilometer (km2) 0 0e386 sq miles1 metric ton (tonne) - 1,000 kg - 2,204.6 pounds1 liter - 1.057 US quarts = 0.22 Imp. Gallon

ACRONYMS AND ABBREVIATIONS

ADB - African Development BankAFC = Agriculture Finance CompanyBOZ = Bank of ZambiaDBZ U Development Bank of Zambia,EG Deutsche Gesellschaft fur Wirtschaftliche Zusammenarbeit

Entwicklungsgesellschaft (German Finance Company for EconomicCooperation)

DRA 5 Debt Recovery Action PlanEAS Equator Advisory ServicesEIB = European Investment BankFMO Nederlandse Financierings Maatschappij Voor Ontwikkelingsladen

N.V. (Netherlands Finance Company for Developing Countries)GDP Gross Domestic ProductINDECO = Industrial Development CorporationMBA - Master of Business AdministrationMIS = Management Information SystemNORAD - Norwegian Agency for International DevelopmentNSCB = National Savings and Credit BankPTA = Preferential Trade AreaSEP = Small Scale Enterprise Promotion Ltd.SSE = Small Scale EnterprisesT-Bill = Treasury BillZADB - Zambian Agriculture Development BankZCCM = Zambian Consolidated Copper Mines LimitedZIMCO - Zambia Industrial and Mining CorporationZNBS - Zambia National Building SocietyZNCB = Zambla National Commercial BankZNPF a Zambia National Provident FundZSIC = Zambia State Insurance Corporation

FISCAL YEAR

April 1 - March 31

FOX OMCIAL USE ONLYSTAFF APPRAISAL REPORT

ZAMBIA

THIRD DEVELOPMENT BANK OF ZAMBIA PROJECT

Table of Contents

Page No.

Credit and Project Summary ................................... i - iii

Basic Data ............................. iv -vi

I. INTRODUCTION

A. The Industrial Sector .............................. 1Sector Background I............. ......,.,,, , .. 1Structure of Industry ...................,.,........ 2Employment, Labor Productivity and Wages ........... 3The Policy Framework .................ee....e.e..c 3

Background 3.................. ... oeee.. 3The New Industrial Policy Regime ............... 4Foreign Exchange Regime ...........e............ 4Import Regime .................................. 5Export Promotion ...... te.eeeeeeeeeC 5Investment Act ............................Public Sector Investment in Industry ........... 5

Recent Industrial Performance ...... ................ 6Resource Allocation 6........................* 6Effect of Policy Changes ....................... 6Capacity Utilization ........ e. 6

B, The Financial Sector .. a eec ........ c cc... 7Financial Institutions ......... eec 7

The Bank of Zambia (BOZ) ....................... 7The Commercial Banks ....... 7ee...... e 7

Specialized Parastatal Financial Institutions ...... 7Agricultural Development Banks ..... ................ 8Structure of Banking System Lending ................ 8Monetary Policy Developments ... .................... 9

Money, Credit, Inflation and Devaluation .....t.. 9Interest Rates .... 9.eee.e ....... .. ee 9Effect of the Foreign ExchangeAuction on Interest Rates .................... 9

This report is based on the findings of an appraisal mission to Zambia inMarch-April 1986, composed of Neil C. Hughes, Godfrey Tumusiime andJoseph Owen of RAPID.

This document has a retricted distrbution and may be used by reipients only in the perfowmanceof their ofki duties. Its contents may not otherwis be disclosed without World Bank authoriation.

Page No.

II. DEVELOPMENT BANK OF ZAMBIA ....... ...................... 10

Origin, Objectives and Role .........................,., 10Ownership ........................ 10

Board of Directors 00*e*00*S ........ .......... 11Organization and Management ............................ 11Staff Development and Training ......................... 12Operating Policies and Procedures .................... 12

Accounting, Financial Managementand Information Systems *.......................... 13

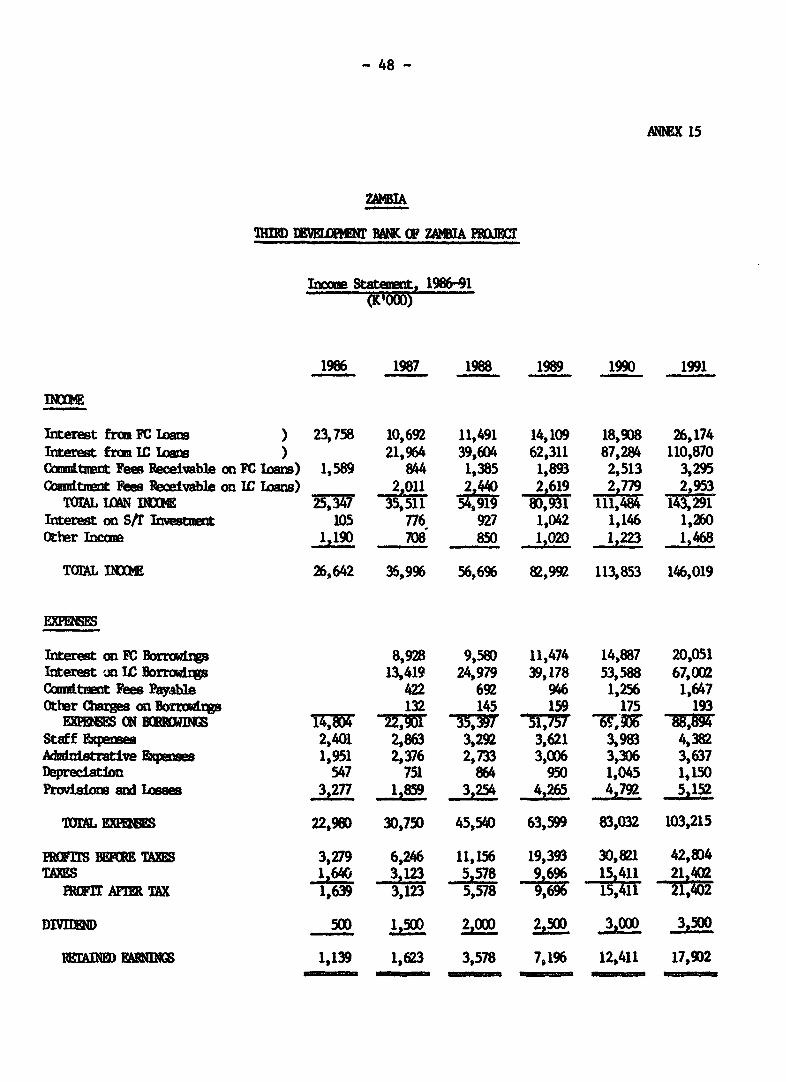

Procurement 0000000000000000000000000000000000000000000. 14Interest Rate Structure *.................. ........ 15Operations .... 0....... 0 15Quality of DBZ's Portfolio .................. ..... 15Resources ....................... , , 17Financial Results and Condition ........................ 18Projected Operations and Financing ..................... 19New Capital Increase ... ,....................,.......... 20Projected Financial Performance ... o .................... 21

III_ THE PROJECT *2***1*.....,...............,............ 21

Bank Group Experience with DBZ ......................... 21Project Justification and Objectives ...... ............. 22Project Description **0000@000000 0050000000 0000000o...... 23

Project Benefits and Risks ......................... 25

IVe AGREEMENTS REACHED AT NEGOTIATIONS ... , .................. 26

ANNEXES

1. ZAMBIA: Structure of Interest Rates .,.........,.,.... 282. DBZ: List of Shareholders ...... ........................ 293. DBZ: Organizational Chart ...... ........................ 304. DBZ: Statement of Operating Policies ..... .............. 31-33

Page No.

5. DBZ: Debt Recovery Action Plan Methodology ............. 346. DBZ: Summary of Operations, December 31, 1985 .......... 357. DBZ: Analysis of Loan Approvals, December 31, 1985 36-378. DBZ: Balance Sheets, 1982-86 ........................... 389. DBZ: Income Statements, 1982-86 3910, DBZ: Assumptions Underlying Financial Projections 40-4311. DBZ: Projected Operations, 1987-91 4412. DBZ: Projected Sources and Uses of Funds, 1987-91 ...... 4513. DBZ: Projected Net Cash Generation *,,,,,,,**,**,**,,,. 4614. DBZ: Projected Balance Sheets, 1987-91 ................. 4715. DBZ: Projected Income Statements, 1987-91 ...... ....... 4816. DBZ: Projected Financial Ratios, 1987-91 ............... 4917. DBZ: Proposed Capital Structure, 1987-91 o.o.o..o....... 5018. DBZ: Schedule of Disbursements ., 51

ZAMBIA

THIRD DEVELOPMWEN BANK OF ZAMBIA PROJECT

Credit and Project Summary

Borrower: Republic of Zambia

Beneficiary% Development Bank of Zambia (DBZ)

Amount: SDR 8.3 million (US$10.0 million equivalent)

Terms: Standard IDA terms

Terms of Relending: The borrower would onlend the about US$8.9 millioninvestment component of the credit to DBZ at aninterest rate equal to the Bank rate at the time ofnegotiations (i.e. 8.23%), for subloans denominatedin foreign currency, and at a variable rate equal tothe treasury bill (T-bill) rate plus 22 for subloansdenominated in Kwacha. DBZ would repay the Credit tothe borrower in accordance with the aggregate of therepayment schedules for subloans. Subloans would notexceed 15 years with appropriate grace periods not toexceed 4 years. DBZ would provide sub-borrowers withthe option of denominating the subloan repayments (i)in US dollars at a fixed rate equal to the Bank rateplus a 4% spread; (ii) in kwacha at a variable rateequal to the sum of the 1-bill rate plus a 2% foreignexchange risk premium, plus a spread of not less than4%. The borrower would pass on the US$1.1 milliontechnical assistance portion of the credit to DBZ asa long-term subordinated loan, which would beconsidered as quasi-equity for the purpose ofcalculating DBZ's debt-to-equity ratio. Retroactivefinancing up to an amount of SDR 250,000 would bemade available for expenditures made before the dateof loan signing but after October 31, 198f, under thetechnical assistance component.

Project Description: The credit would finance the long-term foreignexchange portion of the capital investment require-ments of productive sector subprojects approved byDBZ, for modernization, expansion or restructuring ofexisting enterprises, and to a lesser degree for newinvestment subprojects. The credit would alsofinance the establishment of a computerized financialand management information system at DBZ, technicalassistance to Implement the new system and trainstaff in its use, as well as staff training inproject evaluation and supervision, both in Zambiaand abroad.

- il -

Project Benefitsand Risks: The propcsed project would provide term resources to

the productive sectors in Zambia to rehabilitateindustrial and agro-industrial enterprises, developmanufactured and other non-traditional exports, andincrease production in all productive sectors. Itwould thus help accelerate growth and increaseemployment in Zambia and would complement thepositive impact of the policy reforms already takenby the Government and supported by IDA. Theinvestment component of US$8.9 million Is expected tosupport productive investments totalling about US$20million. The project would also enable IDA to helpDBZ, the main term-lending institution in Zambia, toincrease its effectiveness as a term-lendinginstitution by mobilizing additional resources,upgrading the quality of its portfolio, andincreasing the effectiveness of financial andmsnagement decision-making. Continued IDA supportwould enhance DBZ's capability to mobilize additionalforeign capital and other resources from bilateralinstitutions and would enable it to play a moresignificant role in assisting the recovery ofZambia's productive sectors.

There are two major risks to this project. One isthe possible deterioration of Zambia's economicsituation. Such a risk is, however, limited, so longas Zambia continues to follow the stabilizationprogram supported by the IMF and the policy reformsand actions envisaged by IDA and other donors toincrease the resource transfer and accelerateeconomic growth in Zambia. A second risk is acontinued deterioration of DBZ'a arrears position.This risk is being reduced as DBZ takes the actionssupported by the proposed credit to improve loancollections and to resolve its portfolio problems.These should insure that DBZ will remain an effectiveterm-lending institution that promotes economicallysound investment projects.

16. Arrears as % of TotalPortfolio - 7.8 13.1 10.8 10.0

17. Loan Collections as %of Total Bil'lings - - 66.0 86.5 105.0

8. Resource Position (as of December 31, 1985)K'000

Local Foreign Total

Resources Available for Disbursement 3,395 38,476 41,871Less: Undisbursed Commitments 13,673 34,100 47,773

Resources Available for Commitments (10,278) 4,376 (5,902)Less: Uncommitted Approvals 15,620 2,715 18,335

Resources Available for Approvals (25,898) 1,661 (24,237)

a/ Line 3 - Line 4tr/ Line 13 - Line 14

STAFF APPR.AISAL REPORT

ZAMBIA

THIRD DEVELOPMENT BANK OF ZAMBIA PROJECT

I. THE INDUSTRIAL AND FINANCIAL SECTORS

A. The Industrial Sector

Sector Background 1/

1.01 Zambia's manufacturing sector is relatively large compared toother sub-Saharan African countries, contributing over US$600 million toGDP in 1983, and employing nearly 60,000 workers (16% of employment in themodern sector). The 20% share of manufacturing in Zambia's GDP is secondonly to Zimbabwe, and only Zimbabwe and the Ivory Coast in sub-Saharar.Africa have higher levels of manufacturing GDP per capita.

1.02 Manufacturing was the fastest growing sector of the economy inthe first decade after independence. From 1965 to 1974, manufacturingvalue added grew at 10% per annum in real terms while total GDP was growingat about 3.3% p.a. The rapid growth of manufacturing during the 1960s andearly 1970s was due to: (i) growing demand for consumer goods because ofgrowing incomes; (ii) increased demand for equipment and metal fabricationlinked to the mining sector; and (iii) the Government's policy of accele-rated industrialization through import substitution and public sectorinvestments in manufacturing. The sector's growth continued at high ratesuntil 1975 when, in response to the sharp fall in copper earnings and theresulting economic recession, industrial output fell dramatically by 15% inreal terms between 1975 and 1980. Despite some recovery in 1981, thegeneral picture remained one of decline in industrial output, with manufac-

/ A detailed analysis of the performance and main policy issues facingZambia's industrial sector was presented in the report: Zambia:Industrial Policy and Performance IDA. Report No. 4436-ZA, from whichthis section is taken.

- 2 -

turing value added in 1985 about three quarters the 1976 level. Depresseddemand as well as increasing difficulties in obtaining imported inputs dueto foreign exchange scarcity were mainly responsible for this situation.

Structure of Industry

1.03 Industrial production in Zambia has become increasingly diver-sified over the years, moving from a predominance of consumer goods to agreater share of output in intermediate and capital goods (chemicals, metalproducts, machinery etc.). Between 1965 and 1975, the share of food,beverages, tobacco, textiles, clothing and leather in gross manufacturingoutput dropped from 59% to 40% whereas the share of intermediate productsand equipment increased from 32% to 49%. The spatial distribution ofZambia's industry is unusual in Africa because it is not concentrated inthe administrative/commercial capital. Rather, about half the establish-ments and employment are located in cities along the line of rail to thenorth in the Copperbelt Province, and in the Southern Province, with onlyaround a third in the Central and Lusaka Provinces. The remaining five ofthe country's nine provinces have less than 3% of the firms and less than1% of industrial employment.

1.04 The degree of government intervention in the industrial sectorhas been substantial. Between 1970 and 1980, the public sector, repre-sented primarily by the Industrial Development Corporation (INDECO), grewat rates exceeding those for the economy as a whole and those for privatemanufacturing. By 1980, public enterprises accounted for more than halfof gross manufacturing output and more than 40% of manufacturing employ-ment. Government policies with respect to licensing, tariffs and invest-ment incentives created an environment in which competition was limited andindustry grew as an import-substituting activity behind high protectivebarriers. In addition, the choice of public sector investments coupledwith distortions in factor prices combined to create a highly capital andimport-intensive structure.

1.05 The shortage of foreign exchange to purchase imported inputs andspare parts, on which Zambian manufacturers are heavily dependent, led tolow levels of capacity utilization resulting in decreasing efficiency andincreasing average costs. Results of a 1981 survey 2/ of 24 firmsrevealed that, on average, firms imported about 50% of their inputs. Onlyfood, textiles and footwear industries import less than half their inputs,while metal products are the most import-intensive, with imports accountingfor 81% of all inputs. Chemicals, wood and paper products also have highimport shares in total inputs.

1.06 Despite a relatively large and more advanced industrial sectorcompared to other sub-Saharan African countries, Zambia's manufacturedexports are exceptionally small. The highest amount of manufacturedexports achieved was US$3.3 million in 1974, which was greater than onlyeight out of 34 African countries for which data was available. Manufac-tured goods made up only 1.3% of Zambia's exports in 1977 and 0.7% in1980. The depreciation of the kwacha, beginning in 1983, foliowed by the

2/ Ibid.

drastic drop in the kwacha following the introduction of the foreignexchange auction in 1985, have helped to bring about a small but signifi-cant increase in manufactured exports. A survey 31 of about twentyprivate firms in early 1986 indicates that exports for these firms areexpected to increase ten-fold this year (i.e. to about US$2 million).Manufacturing exports are largely limited to cement, molasses, coppercable, clothing, crushed stone and lime, and explosives. As the productbase is enlarged, through the implementation of appropriate policies,manufactured exports can become significant contributors to the balance ofpayments in the 1990s.

Employment, Labor Productivity and Wages

1.07 Zambia's manufacturing sector employs nearly 60,000 workers,which amounts to 16% of formal sector employment. Manufacturing employmentgrew at more than 11% per annum in the 1960s and 5.6% per annum during1970-74. Thereafter, employment continued to grow, albeit at only 1%annually, despite the sharp drop in the value of manufacturing output.This was due to the parastatal sector, in which employment was growing atan annual rate of 5% during 1975-80, more than twice the rate of growth ofparastatal production. In the private sector, both employment and valueadded fell at about 3% annually during this period. As a result of thesetrends, labor productivity in manufacturing declined, at an average ofabout 4% annually, between 1973-80. Real wages in manufacturing, whichrose substantially during the post-independence boom period, also followeda declining trend since 1973, falling at an average annual rate of 2%between 1975 and 1980. Wages in the formal manufacturing sector are nowbelow the average wages in mining, transport, communications and services.

The Policy Framework

1.08 Background. The Zambian economy has been in a continuing stateof contraction since 1975. Relying on a single primary commodity (copper)for the bulk of its export earnings and with both production andconsumption heavily dependent on imports, Zambia was vulnerable to thecombination of deteriorating export prices, increasing costs for importedgoods and raw materials, and regional unrest which occurred over the pastdecade. The country's external terms of trade fell by 70% during thisperiod causing a severe compression of imports and a sharp decline in GDP,All sectors of the economy were affected by the contraction on importswhich resulted in widespread underutilization of capacity. In addition,spare parts for maintenance became increasingly scarce leading to largeunmet rehabilitation and replacement requirements. The Government's fiscaland balance of payments performance, which had relied heavily on the miningindustry, deteriorated dramatically.

1.09 Zambia's difficulties were exacerbated by inappropriate economicpolicies and weakness in economic management. Continued economic deterio-ration, however, led the Government to recognize the permanent nature ofthe imbalance in its external accounts and the corresponding need fordeep-seated structural changes in the economy. In the past three years,

31 IDA Supervision mission for Industrial Reorientation Credit.

- 4 -

the Government, with Bank and IMF assistance and support, has undertaken arecovery program to stabilize Zambia's external accounts, restore growth,and lay the basis for restructuring the economy. The Government's long-term objectives are to diversify the economy through greater emphasis onincreasing agricultural output, restructuring industrial operations alongthe lines of comparative advantage, rationalizing the mining industry,rehabilitating existing infrastructure, and encouraging non-traditionalexports. In support of the Government's recovery program, recent Bankassistance to Zambia include a US$75 million Export Rehabilitation andDiversification loan for the mining sector in 1984, an Agricultural Rehabi-litation credit of US$25 million and an Industrial Reorientation credit ofUS$62 million in 1985, and a Recovery credit of US$50 million in 1986. Inaddition, stand-by arrangements were agreed with the IMP in 1983, 1984 and1986.

1.10 The New Industrial Policy Reglme. An immediate objective of theGovernment's new industrial strategy is to raise the level of capacityutilization in the sector by providing additional foreign exchange toefficient import-substitution and export-oriented industries. Increasedindustrial production will reduce the economic and social pressuresassociated with the economic stabilization and adjustment process, andgrowth in industrial exports will help to regain external equilibrium. Inthe longer term, the Government's objective is to increase the efficiencyand export orientation of the industrial sector, by instituting anincentive structure and a set of policies that encourage the flow ofinvestnent resources to the more productive industrial subsectors andenterprises. In order to attain these objectives the Government iscommitted to pursue a less protective, more outward-looking industrialstrategy, to rely increasingly on market forces to allocate resources, andto reduce the share and increase the efficiency of the public sector inmanufacturing.

1.11 The Government is aware that in addition to the provision offoreign exchange, controls and restrictions must be removed and the policyframework changed. Consequently, it has adopted a number of institutionaland policy reform measures that are being implemented with IDA assistancein the context of the Industrial Reorientation Project, and are designed toimprove the foreign exchange regime, reform the import regime, removedisincentives to exports, streamline and improve investment incentives,increase the efficiency of public enterprises and improve the publicsector's investment program in manufacturing.

1.12 Foreign Exc!an gime. A market determined exchange rate isthe cornerstone of the Government's new development strategy and of itsindustrial policy reform. The foreign exchange auction system, which hasbeen functioning effectively since October 1985, is based on a weeklyauction of foreign exchange at which the exchange rate which applies to allforeign exchange transactions is determined by the marginal bid whichexhausts the foreign exchange available for auction. At present, aboutUS$6-9 million is being auctioned every week. Although administrativeallocation, at the auction rate, continues for the fore.'gn exchangerequirements of the Government, the copper mining conglomerate (ZCCM),public debt service, and for imports of pharmaceuticals, books and, whennecessary, maize and fertilizer, the use of this mechanism is declining andwill be reduced to a minimum in the future.

-5 -

1.13 IMrtRegmime. The Government has adopted several policyreforms, beginning in October 1984, to shift the full weight of traderestrictions from an import licensing system to a tariff system. Themeasures adopted to date, which constitute a major step in the reform ofthe import regime, are: (a) elimination of import licensing and itsreplacement by a simple system of registration; (b) elimination of allimport prohibitions for protective purposes; (c) establishment of a 10%minimum tariff on all imports; (d) reduction of maximum tariff rates from150% to 100%; and (e) establishment of a 15% sales tax on all finaldomestic goods produced in significant quantities. The second phase of thetariff reform includes the establishment of a Tariff Commission to prepareand carry out further reforms of the tariff structure and indirect taxes inorder to decrease the level and increase the uniformity of effectiveprotection between sectors. The recommendations of the Tariff Commissionare expected to be implemented by the Government no later than June 30,1987.

1.14 Epr romotion. Given the limited prospects for copperexports, particularly beyond the year 2000, Zambia's future foreignexchange availability will depend on the development and growth of non-traditional exports. To provide incentives for non-traditional exports,the government has established a set of new incentives that include:(a) replacement of export licensing by a simple system of registration;(b) replacement of the complex system of individual duty drawbacks by asimpler system of average drawbacks for major groups of exports;(c) establishment of an autonomous export promotion board, with privatesector participation; (d) initiation of feasibility studies forestablishing export credit insurance and guarantee schemes.

1.15 Investment Act. In April 1986, the Government enacted a newInvestment Act to replace the Industrial Development Act of 1977. The oldAct failed in its objective to attract new private investment to manufac-turing because it was highly regulatory; did not provide any new incentivesthat were not already available to all manufacturers; access to incentiveswas arbitrary and finally it did not abandon the overall industrialstrategy of granting a dominant role to the public sector at the expense ofthe private sector. The new Act provides a uniform policy environment forpublic and private enterprises and improved incentives in the form ofincome tax deductions and grants for training and R&D, for enterprises thateither export, produce with high local input content, are located in arural areas, or are classified as small-scale enterprises (SSEs),

1.16 Public Sector Investment in Industry. Most public investment inmanufacturing is carried out by INDECO. In the past, the limited capabi-lity of INDECO to appraise projects and to assess the performance of esta-blished enterprises resulted in many uneconomic, capital-intensive andimport-dependent investments. The Government has committed itself toincrease the efficiency of the public sector and has commenced with a planof action to achieve this objective. In this context, INDECO's managementhas: (i) established an Economic Evaluation Unit to appraise new invest-ment projects and monitor the performance of existing enterprises usingsound economic criteria; (ii) initiated a review, with the assistance ofIDA, of the economic viability and operational efficiency of existingenterprises that will subsequently lead to the implementation of an action

- 6 -

plan to restructure some enterprises that are viable, and to phase outfirms or activities that are not viable; and (iii) prepared a three-yearinvestment program, which has been reviewed and approved by IDA.

Recent Industrial Performance

1.17 Resource Allocation. A study of the impact of the foreignexchange auction on the allocation of foreign exchange to the productivesectors, carried out in April 1986, reveals that the manufacturing sectoris receiving a similar amount and proportion of the foreign exchangeavailable to what it was receiving immediately prior to the auction.However, major changes are taking place in the allocation of foreignexchange within the industrial sector. The share of imports going to theprivate sector has increased significantly, from less than 50% immediatelybefore the auction to over 61% now, at the expense of parastatals. Withinparastatals, preliminary evidence suggests that the least efficient firmsare purchasing smaller amounts of foreign exchange, whereas others aregetting a higher share.

1.18 Effect of Policy Changes. The auction system, with its market-clearing exchange rate level, and the major trade policy and financialreforms (elimination of all non-tariff import restrictions, freeing ofInterest rates), has led to a significant change in the actual amounts offoreign axchange purchased by different sectors and subsectors and is alsohaving a positive impact on the efficiency of use of foreign exchange andother resources. In industry, increases are already taking place incapacity utilization, productivity of capital and labor, efficiency offoreign exchange use and exports. The differences in attitude on the partof parastatal and private sector management are striking when compared toearlier experiences. Since the changes in the economic and regulatoryenvironment of October 1985, managers interviewed during a supervisionmission of the Industrial Reorientation Project emphasized efficiency,labor productivity, competition and the profitability of exports, incontrast to the "cost-plus" complacency of the past.

1.19 Capacity utilization in industry is estimated to have increasedfrom 42% in early 1985 to 47% in 1986, the direct result of the significantrise in private sector capacity utilization from 38% to 54%. Capacityutilization declined in the parastatal sector from 45% to 41% mainly as aresult of the poor performance of five economically ineffiAiententerprises. The productivity of capital in industry has increased byapproximately 12% as a result of higher capacity utilization. Overall,labor productivity has increased significantly (by at least 15%) because ofthe higher production levels and reductions in the industrial labor force.Industrial parastatals, with few exceptions, have shed labor throughnatural attrition as a means of reducing costs.

1.20 Foreign exchange is also being utilized more efficiently. Basedon actual data from all INDECO firms and a sample 4/ of privateenterprises, it was found that each unit of foreign exchange is generatingabout 10% more value added than before the auction, because: (i) foreign

4/ Ibid.

- 7 -

exchange is being purchased by more efficient producers in the sector; and(ii) firms have implemented productivity improvement measures as a responseto the higher cost of foreign exchange.

B. The Financial Sector

Financial Institutions

1.21 Zambia has a well developed financial system which includes, inaddition to the Central Bank, nine commercial banks and six specializedparastatal financial institutions. The latter are under the control of theZambia Industrial and Mining Corporation (ZIMCO)--the Apex holding companyfor all state-controlled enterprises.

1.22 The Bank of Zambia (BOZ). The Central Bank was established in1965 to issue currency, regulate commercial banks, and establish andadminister national monetary and credit policies through the use of thediscount rate and reserve requirements. BOZ also manages Zambia's interna-tional reserves and is in charge of the country's foreign exchange controlsystem, which it administers in cooperation with the commercial banks.

1.23 The Commercial Banks. The first commercial bank was establishedin Zambia in the early part of this century. However, of the nine existingcommercial banks, five have been established during the last five years.The state-owned Zambia National Commercial Bank (ZNCB) handles the bulk ofcommercial banking business of parastatal organizations and otherGovernment agencies. Its assets amounted to K 1,305 million (US$186million equivalent) at December 31, 1985. Subsidiaries of two Britishbanks, Barclays Bank and Standard Chartered Bank, are next in size, withtotal assets of K 1,035 million and K 1,090 million, respectively. Oneforeign-owned middle-sized bank, the Bank of Credit and Commerce (totalassets of K 532 million), is followed by five smaller foreign bankb. withassets ranging from K 64 million to K 241 million. Zambian investorsrecently established a second local bank, the African Commercial Bank (nodata available). The commercial banking system is the major source ofmobilization of savings from the general public. At year-end 1985, totaldeposits amounted to K 1,964 million, equal to a real increase of 100% infive years. Three fourths (K 1,484 million) of these deposits were held bythe three largest barks. The five banks established since 1980, controljust one fifth of total deposits. Over one half of the total deposits(K 1,027 million) are demand deposits. Rates for time deposits have notprovided much incentive for savers to place their funds at term (Annex I).For small savers, bank deposits are the only means of saving for the futureand earning a reasonable return.

Specialized Parastatal Financial Institutions

1.24 Zambia National Provident Fund (ZNPF) was established in 1966 asa Government-owned entity to administer a mandatory retirement savingsscheme for non-civil service Zambian employees. The funds are channelledinto productive investments mainly through credit to the public sector. Asof March 31, 1984, the Fund's total assets were K 550.5 million. Zambia

- 8 -

State Insurance Corporation (ZSIC) was formed in 1967 after the merger andnationalization of all existing insurance companies. As of December 31,1985, the Corporation's resources totalled K 415.0 million, of which about80% were invested in Government bonds, loans and in industrial andcommercial investments. Zambia National Building Society (ZNBS) was formedafter the nationalization of three private societies in 1971, It obtainsfunds through savings shares and deposits from the general public andinstitutions. As of December 31, 1984, its assets totalled K 163.4million, of which four fifths were invested in mortgage loans mainly forresidential properties. National Savings and Credit Bank(NSCB) is thefinancial institution in Zambia with the largest network of branches(150). The bank caters to small savers, especially in the rural areaswhere no other banking facilities exist. At the end of 1984, its totalassets amounted to K 125 million, one half of which were loans to theGovernment and parastatals, and one half were deposits with ZNBS and ZNCB.

Agricultural Development Banks

1,25 Agriculture Finance Company (AFC) was established in 1970 as aparastatal holding company under the Ministry of Rural Development. Mostof AFC's lending is for seasonal loans to agriculture. The remainderconsists of medium-term agriculture financing and mortgage loans for thepurchase of farms. As of March 31, 1985, AFC had accumulated losses ofK 95.7 million on a share capital of K 43.5 million. AFC has had a veryhigh rate of default on its loans, is presently insolvent, and is stilloperating only because it is receiving Government financial support. It isexpected to be merged with the Zambian Agriculture Development Bank (ZADB)which was established in 1979 but only commenced operating in 1983. Thisinstitution is expected to gradually take over the activities of AFC and tobecome the main source of credit to the agriculture, fishing and agro-industrial sectors. ZADB had a net unimpaired share capital of K 3.8million and total assets of K 7.9 million as of December 31, 1984,

Structure of Banking System Lending

1.26 The commercial banks provide short- and medium-term (up to threeyears) credit, leaving long-term credit to specialized institutions.Although most banks are limited by their own internal controls to allocateonly 10-15% of their portfolio for medium-term lending, it was only afterthe establishment of the foreign exchange auction that they made any realeffort in this area. In effect, the banks responded to the needs of theirclients who wanted medium-term kwacha loans to purchase foreign exchange inthe auction to finance capital imports. They also made loans to DBZ, whichdid not have the local resources to attend to the similar needs of its ownclients. The composition of the banks portfolio is as follows: about 35%of commercial bank lending goes to agriculture; 20% to manufacturing; 15%to mining and 8% to commerce. The balance (22%) is lent to transport,construction, financial institutions, and individuals. At December 31,1985, 50% of total commercial bank loans and advances were granted to theprivate sector, 38% to parastatal entities and the balance of 12% to meetstatutory requirements. Since 1980, total outstanding loan portfolio hasincreased from K 431.6 million to K 1,146.6 million (an increase of about66% in real terms). About two thirds of lending by the private commercialbanks goes to the private sector, while four fifths of ZNCB lending isdirected to the public sector and parastatal organizations.

-9-

Monetary Policy Developments

1.27 Money, Credit, Inflation and Devaluation. During the 1980s,monetary policy has largely met the requirements of the Government's fiscalpolicy. Between 1980-82, monetary and credit policy accommodated thegrowing needs of an expansionary budget policy and an attempted recovery inthe productive sectors. Over the two-year period, when the consumer priceindex was increasing at a rate of 12% p.a., the money supply increased by22% annually, the net domestic assets of the banking system increased 30%p.a. and banking system credit to the government increased by 25% eachyear. Credit to the private sector grew even faster, averaging 40% p.a.Budgetary restraint in 1983 led to a sharp decline in the rate of growth ofnet banking system assets, the money supply, and banking system credit tothe Government, all of which grew by less than 10%. Private sector creditstill managed to grow by 14%, while the inflation rate increased to 18% andthe kwacha was devalued by 27%. All monetary indicators indicated growthrates of 18% or less in 1984, but meanwhile inflation had reached a rate of21% and the kwacha suffered a further 32% depreciation. With the openingup of the economy in 1985, a substantial monetary expansion occurred (42%),while banking system assets increased 29%. At the same time, the rate ofinflation rose 35%, fueled by major price increases in a whole range ofgoods and services following the 200% devaluation of the kwacha inOctober-November of that year. The monetary expansion continued in 1986,with the money supply increasing 24% between January and May (an annualrate of 58%).

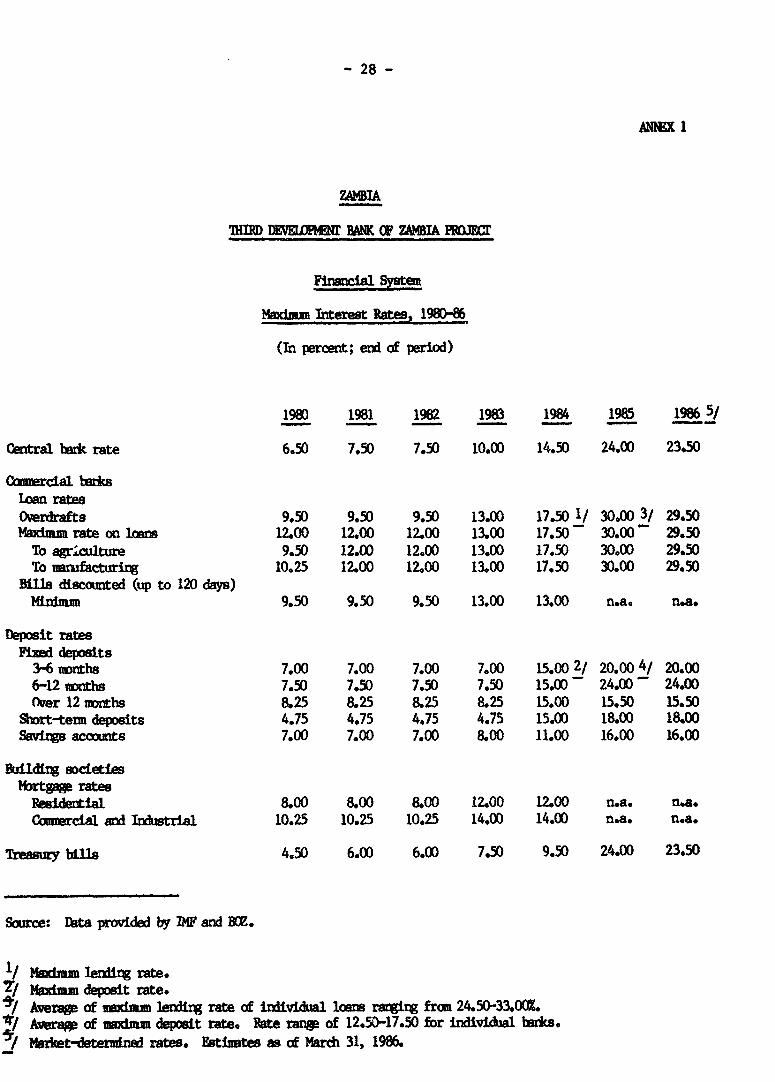

1.28 Interest Rates. Between 1982-85, BOZ raised interest rates in aseries of gradually larger steps (Annex 1), until in 1985, rates werecompletely freed and limits were set by market forces. In 1983, most rateswere raised between 1.5-3.5%. In 1984, most active and passive rates weresubstantially increased again, i.e., by 3-10.5%. However, these increasesdid not catch up with increasing inflation, and in real terms, ratesremained negative. The removal of all ceilings on interest rates inSeptember 1985 radically changed this situation, and resulted in almost afurther doubling of rates within a two-month period. An auction oftreasury bills was also introduced, which more than doubled the T-bill rateover the same period (i.e., from 13% to 23%). Under the new system, theBanks in practice establish a prime rate which is close to the T-billrate. The basic market option for the banks is to (i) invest deposits inT-bills, or (ii) make loans at rates reflecting the return on T-bills plustheir own loan administration costs of about 1% plus an additional profitmargin. In practice, the prime rate charged is about 2% above the T-billrate, which provides the banks with a 6% spread over the average cost ofdeposits. In effect, the T-bill auction established a market-oriented coststructure not only for government borrowing, but also for setting lendingrates throughout the banking system.

1.29 Effect of the Foreign Exchange Auction on Interest Rates. Whenthe T-bill remained at about 24%, the bank's prime rate was set at 1% to2% above the T-bill rate. Some borrowers had to pay as high as 33%, andthe average lending rate was about 30%. Because inflation in the past hasbeen much lower, low inflationary expectations have led to resistance tothese interest rates. This is also reflected in an increase in the

- 10 -

liquidity ratio (liquid assets as a percentage of deposit liabilities) ofthe commercial banking system, which was 70.6% at December 31, 1985, upfrom 63.1 at the end of 1984. As a result, even though real interest ratesbecame negative following the 1985 devaluation and subsequent priceinflation, they have recently become marginally positive as the rate ofinflation slowed during the course of 1986. Nevertheless, pressures arebuilding to limit further increases in interest rates. If low or evennegative rates persist, deposits are likely to go down, hampering resourcemobilization and leading to new upward pressures in the interest rate. Theprospects for future trends in interest rates and inflation depend largelyon the Government's success in controlling the latter. Assuming that theGovernment's economic program including market-oriented interest ratepolicy will be maintained, the outlook is for a return to an equilibriumsituation, resulting from a continued decline in the rate of inflation.Consequently, the market-determined interest rates are expected to become morepositive over the medium-term.

II, DEVELOPMENT BANK OF ZAMBIA

Origin, Objectives and Role

2.01 The Developmet Bank of Zambia, established as a statutorycorporation by an Act o' Parliament in 1972, started operations in 1974.Its main objectives are provide medium- and long-term loans and equityfinancing for projects in idustry, agro-industry, construction, transport,power, tourism, mining and .arge-scale agriculture. DBZ is also authorizedto provide technical assistance and advisory services and to administerSpecial Funds on behalf of the Government. The World Bank Group assistedthe Government in establishing DBZ by participating in the feasibilitystudy that led to its creation, through an IFC equity investment ofUS$545,000 and by granting a US$15 million loan to DBZ in 1975 and anadditional US$15 million loan in 1980. Since inception, DBZ has maintainedits autonomy in making investment decisions, has become the major source ofterm financing for productive investments in Zambia and, despite thecountry's economic difficulties, has remained a basically sound financialinstitution.

Ownership

2.02 DBZ was established with an authorized share capital of K 10million consisting of 600 "Class A" shares and 400 'Class B" shares ofK 10,000 each. IFC subscribed 35 shares of the latter. In April 1979,Parliament authorized DBZ to increase its share capital by issuing a newclass of non-voting preferred interest-bearing shares designated "Class C"shares. However, none has as yet been issued. The "Class A" shares arereserved for the Government and its agencies and the "Class B" shares arereserved for local private shareholders and international banks orinstitutions, while there are no limitations on 'Class C" shares. DBZ'sauthorized share capital has been increased to K 30 million, and as ofMarch 31, 1986, DBZ's total paid-in capital amounted to K 18,950,000,including K 14,150,000 held by 6 "Class A" shareholders and K 4,800,000

- 11 -

held by 23 "Class B" shareholders. Total capital and reserves (includingsubordinated debt) amounted to K 35.5 million at March 31, 1986. The listof DBZ's shareholders is presented in Annex 2. A capitalization plan toraise an additional K 51 million in share capital to support the expectedincrease in DBZ's operations was accepted by DBZ's shareholders during itsJuly 1986 Board Meeting (para. 2.29).

Board of Directors

2.03 DBZ's Board of Directors consists of ten members, six of whom,including the chairman, are appointed by the Government to represent'Class A" shareholders while four members are appointed by "Class B" share-holders. The Directors appointed by the Government include the PermanentSecretary of the Ministry of Finance, who is the chairman, the Governor ofthe Bank of Zambia, the Special Assistant to the President of Zambia onEconomic Affairs, the Director of the Zambia National Provident Fund, DBZ'sManaging Director and a local businessman. The Directors appointed by"Class B" shareholders include an official of DEG, the Resident Director ofBeogradska Bank, ADB's Regional Representative 5/ and the Credit Managerof Grindlays Bank (Zambia) Limited. The Directors, who are appointed for aterm of four years, do not have alternates. The Board meets quarterly,takes an active interest in DBZ's activities, and has been instrumental inhelping DBZ maintain its autonomy and to develop into a sound, profitableinstitution. The contemplated share capital increase will result in are-distribution of "Class B" Board seats, to conform with new shareholdingrelationships. A new shareholder, FM0, which has agreed to subscribe atleast 10% of the total amount of share capital, w3uld receive one of theseats presently held by groups of shareholders who individually hold lessthan 10%.

Organization and Management

2.04 Except for a one-man office in the Northwestern Province (whichis responsible for implementing a small-scale enterprise program financedby the International Fund for Agricultural Development (IFAD)), all DBZ'sstaff are located in one building in Lusaka which DBZ owns. The appraisal,implementation and supervision of projects financed by DBZ entail extensivetravel by DBZ staff. The distances involved make it difficult for DBZ topromote, implement or supervise effectively some of these projects.Copperbelt, Northwestern, Northern and Luapula Provinces account for 31% ofthe number and 40% of the amount of DBZ's loans. DBZ has carried out adetailed feasibility study which assess the justification, costs andbenefits of establishing the proposed regional office, and recommends itsestablishment. DBZ management has decided, therefore, to establish aregional office in Ndola to handle the appraisal, implementation andsupervision of projects in this area.

2.05 Overall, DBZ's management is dedicated and effective. DBZ isheaded by a Managing Director who joined the institution in 1977.

5/ ADB and IPC have a rotation arrangement for representation on DBZ'sBoard, under which IPC Bits for two years followed by ADB for one year.

- 12 -

Previously, he had been Managing Director of ZNCB and had also occupied asenior position at BOZ. He is assisted by a General Manager who alsopreviously occupied senior positions at ZNCB and BOZ. DBZ's organizationstructure comprises six divisions responsible for project promotion,appraisal, supervision, personnel and administration, finance and internalaudit. Except for internal audit, each of the divisions comprises twodepartments. DBZ's organization structure is appropriate for its objec-tives and operations. Two expatriate advisors funded by the NorwegianAgency for International Development (NORAD) provide assistance in SSIdevelopment and project supervision. An organization chart is presented inAnnex 3. All managers in DBZ are Zambian nationals, All the divisions areadequately managed, but the Finance division needs to be strengthened byrecruiting an experienced Financial Advisor (para. 2.13).

Staff Development and Training

2.06 DBZ has a total staff of 182 consisting of 64 professional staffand 118 secretarial and general support staff. All management and almostall professional staff are university graduates with degrees mostly ineconomics, agriculture and business administration, and one quarter alsohold graduate degrees. More than one half of the professional staff havebeen with DBZ for more than five years. Overall, the professional staff isof good quality and is productive. Since 1982, staff increased by 67, from115 to 182 (a growth rate of 58%). Most of the increase (44) was innon-professional staff, while professional staff increased by 23. Asoperations were growing at a faster rate, staff costs as well as totaladministrative costs, remained low (para. 2.24). DBZ has been active intraining its staff through on-the-job training, and by sending selectedprofessional staff on training programs abroad. Due to lack of foreignexchange, however, DBZ has not attained its staff training targets for thepast two years (only two of the five staff originally expected to receiveexternal training were sent on short-term training programs). In thetechnical assistance component of the proposed credit, funds would beincluded to help DBZ carry out its staff training activities and prior toJune 30, 1987, DBZ would prepare a detailed staff tisining programsatisfactory to IDA (para. 3.08).

Operating Policies and Procedures

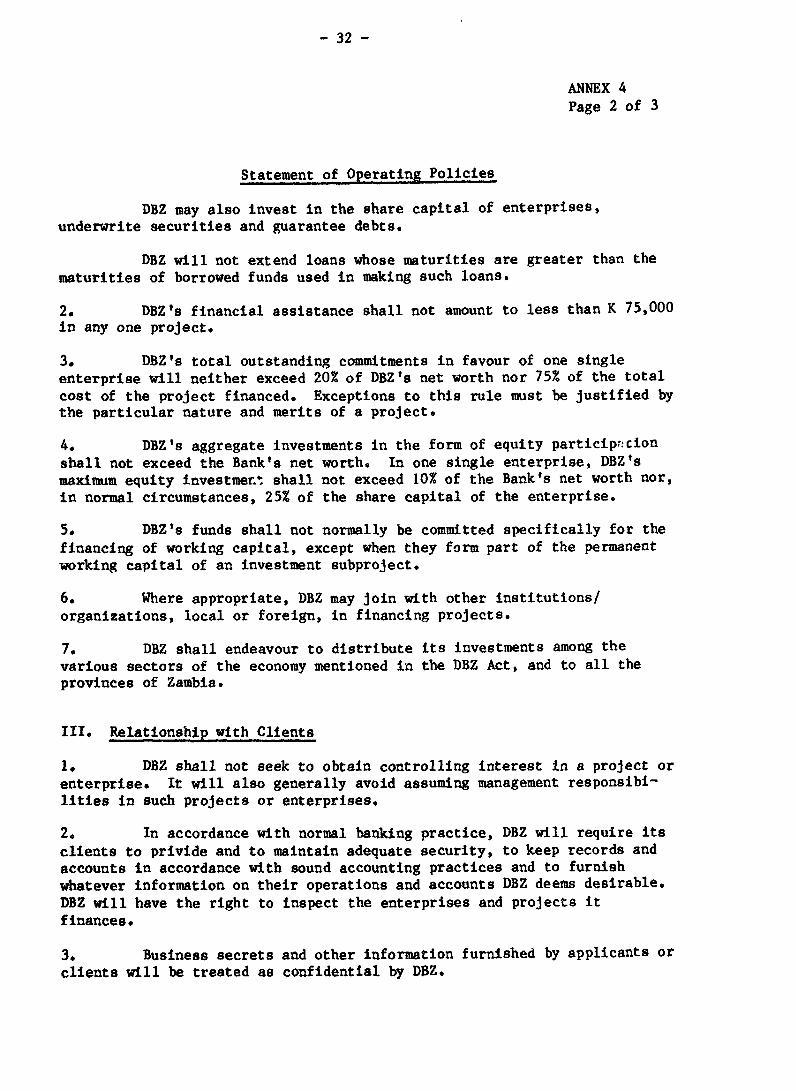

2.07 Policy Statement. The operating policies that govern DBZ'sactivities are set forth in a Statement of Operating Policies (Annex 4),which were established under the first Bank loan. This statement esta-blishes, inter alia, the financing of economically and financially viableprojects as DBZ's main objective, limits the DBZ's re-lending maturities tothe maturities of the borrowed funds utilized in making such loans,establishes a maximum exposure limit per client (20% of DBZ's equity andquasi-equity), and guidelines for equity investments (10% of DBVs equity)in viable enterprises. The policy statement also requires that DBZ bemanaged on sound and businesslike principles. In January 1986, DBZ adopteda specific policy for making adequate provisions for possible losses(para. 2.22). DBZ's policy statement, as previously reviewed and includingthe above amendment, provides a sound basis for operations under theproposed credit.

- 13 -

2.08 Promotion. Promotional activities in DBZ are carried out by theProjects Promotion Division which, at present, has a staff of five profes-sionals. The division's role is to develop project ideas using outsideconsultants financed out of a Special Fund for Technical Assistance fundedby the governments of Norway, Germany and Sweden and, where justified, toprepare pre-feasibility studies. After the studies are reviewed by DBZ'sLoan Committee, a detailed appraisal is carried out of projects with poten-tial, and in consultation with DBZ senior management, suitable uponsors areidentifiee. Over the past five years, this division has carried out 23feasibility studies of which 13 have been implemented by interested privateinvestors.

2.09 Appraisal. During implementation of the second Bank loan, thequality of DBZ's project appraisals has continued to improve with thebuilding-up of staff experience and technical capabilities, and theadoption of an improved credit manual. The appraisal division at presenthas a staff of 12 professionals. Detailed appraisal is undertaken onlyafter an initiating project brief has been cleared by management.Appraisal reports are, in general, compreheasive, and cover the project'sfeatures in detail. However, except when required by the Bank, DBZ has notcalculated economic rates of return on all the projects it finances.Agreement was reached at negotiations that by December 31, 1986, economicrates of retirn would be calculated for all subprojects requiring DBZfinancing of US$250,000 equivalent or more, not just for Bank-financedsubprojects.

2.10 Supervision. The Supervision Division has a staff of 19 profes-sionals who visit most projects at least once a year (those facing pro-blems, more frequently). In the past, supervision has been hampered byunexperienced staff and a tendency to visit enterprises only after problemshad developed. DBZ has made efforts to train and obtain new personnel, andto establish procedures and guidelines, which were set out in a ProjectSupervision Manual adopted in 1980. However, although the manual lays outgeneral principles and sets guidelines, it lacks specificity. Partly as aresult of this, project supervision has not been systematic, sometimesfailing to determine the root cause of problems or to arrive at adequatesolutions for dealing with them. During preparation and appraisal of theproposed credit, DBZ agreed to establish a more systematic approach tosupervision, and to gear its supervision activities to achieving specificand realizable goals. For this purpose, it has established a Debt RecoveryAction (DRA) Plan to reduce arrears (Annex 5), and has developedappropriate collection targets (paras. 2.19 and 2.21).

Accounting, Financial Management and Information Systems

2.11 The quality of financial information prepared by DBZ andreflected in annual audits prepared by its auditors remains satisfactory.The growth of DBZ's volume of operations and size of portfolio, however,has outstripped the institution's manual capability to prepare and maintainaccurate, detailed, and up-to-date accounting, financial and portfolio dataand these processes are now very time consuming. Except for payroll, staffloans and a general ledger, which are processed on a small micro-computerwith little data processing capability, all other accounting, financial and

- 14 -

portfolio data are prepared manually. As a result, data preparationmanagement and retrieval are cumbersome; there are frequent delays inpreparation of key management reports, the flow of information is slow andinadequate, and there is lack of coordination between the Finance Divisionand the operating divisions, especially the Supervision Division, which isresponsible for portfolio management and therefore relies extensively oninformation generated by the Finance Division.

2.12 In an effort to alleviate the existing weaknesses, DBZ hascarried out, with the help of its auditors, a detailed review of thepresent accounting and management information practices, which includeddesigning an appropriate system to replace them. The first and secondstages of the review (assessment of the adequacy of existing practices anddesign specification and tendering of the new system) have been completed.A contract, satisfactory to IDA, is presently being negotiated between DBZand its auditors for the third stage (implementation of the system).

2.13 The weaknessses in DBZ's accounting and management informationsystems are also partly due to manpower constraints. The head of theFinance Division, a qunlified accountant, has limited experience to designnew systems and to manage DBZ's accounting and financial managementfunctions. DBZ has agreed to recruit a suitably qualified FinancialAdvisor for a three-year term. In view of the shortage of Zambiannationals with the necessary experience, DBZ would recruit an expatriate tooccupy this position. In addition, the Director of Finance would completea one-year intensive executive MBA (finance) program. In his absence, theFinancial Advisor would be Acting Director of Finance. Also, DBZ does nothave the qualified staff needed to develop and implement a managementinformation system (MIS). Training of DBZ staff in the operation of theMIS will be provided under the project. To help DBZ achieve theseobjectives, the required financing would be included under the technicalassistance component of the proposed credit (para. 3.08). The hiring ofthe Financial Advisor would be completed prior to March 31, 1987 (para.3.08). The initial salary and the part of the equipment cost associatedwith this component would be financed retroactively (para. 3.05).

Procurement

2.14 Procurement for DBZ-financed projects is made following regularcommercial practices in Zambia. DBZ policies require that clients obtainat least three quotations from three different suppliers or contractors.To be comparable, each quotation must include a complete itemization of thetotal price or cost, including suppliers' standard term of sale. Selectionof the winning quote is based on adherence to the following criteria, whichare closely monitored by DBZ: (i) price/cost competitiveness; (ii) trackrecord of the suppliers/contractors; (iii) availability of maintenanceservices in Zambia; (iv) availability of technical assistance services(i.e., training and installation); and (v) provision of warranties andperformance guarantees. In general, this procedure has worked well in thepast. Under the proposed project, DBZ will, in addition, require eachsub-borrower to submit a detailed written comparison of the quotationsreceived.

- 15 -

Interest Rate Structure

2.15 DBZ's present loan portfolio is almost evenly divided betweenforeign and local currency denominated loans. On foreign currency loans,DBZ has been charging a fixed annual interest rate of 15% and a commitmentfee of 3% due on the date of signing the contract and on the un'isbursedamounts on each subsequent anniversary of contract signing. Local currencyloans bear a semi-annual floating interest rate that carries apredetermined spread above the market-determined T-bill rate (prior toMarch 1984, loans in local currency had fixed interest rates). As ofMarch 31, 1986, the interest rate for loans for industrial projects was 28%p.a. and for agricultural projects 26%. Loans to SSEs bear a fixedinterest rate of 18%. A commitment fee of 2% is charged on local currencyloans. Folloving the adoption of the foreign exchange auction in October1985 and the recent decline in world interest rates, DBZ will establish alower interest rate for new foreign currency loans based on the Bank's rateplus an adequate spread (para. 3.06).

Operations

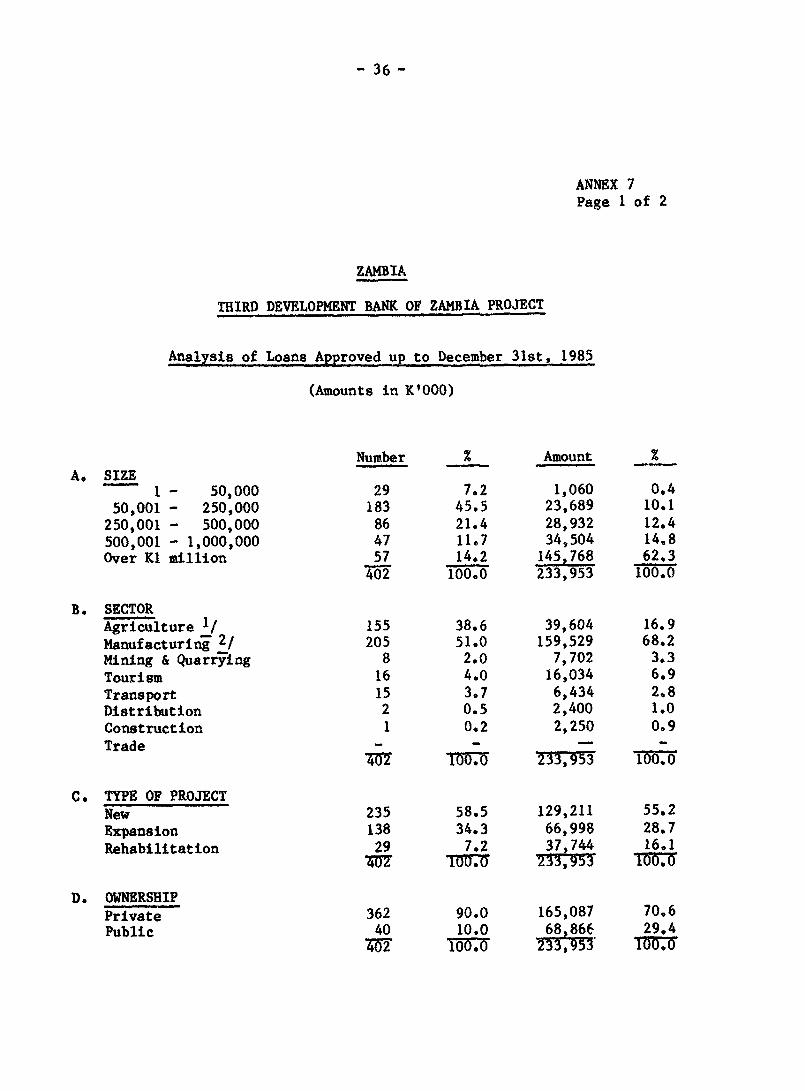

2.16 An analysis of DBZ's loan approvals since 1974 and a summary ofDBZ's operations over the last five years are presented in Annexes 6 and7. As of December 31, 1985, DBZ had approved 402 loans for a total ofK 233.9 million and 23 equity investments amounting to K 5.1 million. Loanapprovals in the last five years grew from K 24.9 million in 1982 to K 57.2million in 1986-a nominal average rate of growth of 24.0% p.a., or about2% p.a. in real terms. Both loan comsmitments and disbursements have keptpace with DBZ's approvals. In each of the past five years, loan commit-ments exceeded 80% of amounts approved and a disbursement rate of more than65% of the amount committed was achieved in each of the last five years.Most (86%) of the loans approved by DBZ since its establishment, were forless than K 1 million (US$142,887 at the current exchange rate). In termsof value, however, loans for less than K 1 million were just 38% of thetotal amount approved. The sectoral distribution of loan approvals shows aconcentration in manufacturing, with 51% of the number and 68% of theamount of loans approved. Agriculture accounts for 17% of the totalamount. Other sectors--mining, tourism, transport, trade andconstruction-account for the remaining 15%.

2.17 A substantial majority (84%) of the projects financed by DBZ areconcentrated along the line of rail, notably in the Copperbelt, ientral,Lusaka and Southern Provinces. About 55% of both the number ard amount ofloans approved since inception were for new projects. In recent years,however, DBZ has responded to a growing demand for expansion and rehabili-tation of existing enterprises. Although DBZ has no policy that givespreference to privately ownee projects, 90% of the number of loans it hasapproved to-date and 71% of the amounts approved were to the privatesector.

Quality of DBZ's Portfolio

2.18 DBZ's loan portfolio has increased from K 65.7 million at yearend 1982, to K 177.2 million (net of provisions), distributed among 288borrowers as of March 31, 1986. DBZ also had a total equity portfolio of

- 16 -

K 5.1 million in23 firms. DBZ's portfolio has been traditionally of highquality, with arrears of over three months considerably below 5% of thetotal portfolio until 1983, The portfolio started to deteriorate, however,when the Zambian economic crisis accelerated in the early 1980s, Many ofDBZ's clients, operating in an adverse economic environment and sufferingfrom reduced sales and profits, had to cut back production. Those whichhad received dollar-denominated subloans, began to suffer from theincreased financial burden resulting from the devaluation of the kwacha.Other firms, operating below their capacity levels, have not been able togenerate sufficient income to service air debt. Still others had todelay project implementation, often because foreign exchange was notavailable on time to make key investment purchases. This situation wascompounded by DBZ's initial inability to prepare and implement a systematicapproach to portfolio management and arrears collection. As a result, loanprincipal and interest in arrears over three months increased from 2.8% oftotal loan portfolio in 1982, to 4.4% in 1983, 7.8% in 1984 and 13.1% ayear later. Portfolio affected by arrears increased accordingly from 18.3%in 1982 to 46.9% in 1985. Meanwhile, collection ratios ranged from 60-75%of total billings, By December 31, 1985, arrears had reached 15.8% of loanportfolio, and affected portfolio amounted to 50% of the total. Thecollection ratio for the f1irt six months of FY86 was 61%. During projectpreparation, DBZ intensified its collection efforts, and the ratio rose to80% for the quarter ended December 31, 1985, and increased sharply to 144%for the quarter ended March 31, 1986. The recently completed annual auditfor the year ending March 31, 1986, indicates the success of these efforts,as arrears fe:l to 11,1% of portfolio, substantially ahead of the arrearsreduction targets agreed at negotiations (para. 2.21).

2.19 Improved collectioni were the result of additional efforts madeby DBZ, particularly in systematizing its approach to debt recovery. WithIDA's assistance, DBZ prepared a Debt Recovery Action (DRA) Plan to dealwith its more persistent arrears problems, based on the individual client'scapacity to repay (Annex 5). This plan consists of two phases. Phase onefocused on reducing arrears from the 40 clients with the largest arrearsexposure as of December 31, 1985. By concentrating initially on thisgroup, DBZ has applied a systematic recovery strategy with the objective ofrecovering 732 of its portfolio in arrears. By the end of September 1986,seven firms had repaid in full and 23 firms were in the process of repaying(through installment payments, sale of assets or liquidation). Inaddition, three firms which had demonstrated their capacity to repay overthe longer term have had their arrears rescheduled, and legal action isbeing taken against seven other firms with whom agreement was not reached.During negotiations, agreement was reached on the timing of phase two,which will commence not later than December 31, 1986, will follow the samemethodology as phase one, and vill concentrate on a second group of 40clients, comprising an additional 18% of total portfolio. Both phaseswould include about 90% of the arrears outstanding at the end of December1985. The existing staff in DBZ's Project Supervision Department issufficient to carry out this program.

2.20 The Government has also taken measures to reduce the impact ofthe devaluation on DBZ's portfolio. In particular, in October 1985, theBank of Zambia fixed the liability of the disbursed and outstandingportions of DBZ's dollar-denominated subloans at the exchange rate ineffect on the day before the initial auction (October 4, 1985). Thus,

- 17 -

repayments under subloans drawn down before the above date can be made atthe equivalent of K 2.2 to the US dollar. This step greatly eased thelocal currency cost of paying off dollar obligations for many of DBZ'sclients, and has paved the way for a much more vigorous collection efforton the part of DBZ. In addition, the implementation of the foreignexchange auction is enabling many firms to obtain the imported inputs andspare parts they need to increase capacity utilization and to generate theincome they need to service their debts, or to coap.ete the implementationof projects which have been held up.

2.21 As a means of establishing a monitorable basis for assessingDBZ's collection performance, DBZ agreed at negotiations to set preliminarysemestral targets for collections and arrears reduction over the next 18months, to include a collection ratio (total collections as a % of totalbillings) of not less than 100% at December 30, 1986, and June 30, 1987,and then declining to 90% at the end of December 1987. This collectiontarget would result in the arrears ratio (as a % of total loan portfolio)declining gradually to 12% in December 31, 1986, 101 by June 30, 1987 and9% by December 31, 1987.

2.22 Although provisions for doubtful loans were made after the end ofFY84 and FY85 (para. 2.25), DBZ had not adopted an explicit policy forestablishing such provisions. As its arrears situation worsened, DBZ'sBoard, in its January 1986 meeting, adopted a provisions policy thatenables it to anticipate prudently its potential losses on loan and equityinvestments. The main criteria of DBZ's provisions policy are: (i) a 100%provision on principal and interest in arrears over one year; (ii) a 50%provision against principal and interest in arrears 6 to 12 months; and(iii) a 100% provision against bad debts (i.e., non-recoverable principaland interest) after deducting the value of security as determined by DBZ'sauditors.

Resources

2.23 As of March 31, 1986, DBZ had mobilized long-term local currencyresources amounting to K 107.9 million consisting of paid-in share capitalof K 14.2 million, reserves and retained earnings of K 8.98 million andmedium- and long-term borrowings totalling K 79.97 million. DBZ has alsobeen successful in mobilizing resources from foreign institutions. As ofMarch 31, 1986, it had obtained foreign currency resources amounting toK 150.0 million. These included paid-in share capital of K 4.7 million,IBRD loans amounting to US$30 million and K 26.8 million from an OPEC Fundline of credit committed but not disbursed. Other lenders include ADB,EIB, BADEA, DEG and FMO. Local currency resources have been raised atinterest rates ranging from 6.25% to 24% with maturities between 3 to 24years. Foreign currency resources carry interest rates ranging from 1%(OPEC Fund) to 9.2% (IBRD) with maturities of 6 to 15 years. The weightedaverage cost of funds is 10,96%, with 8.75% on foreign currency resourcesand 13.7% on local currency resources. DBZ's resource position as ofDecember 31, 1985, showed a resource gap for commitments in local currencyof K 10.3 million and K 4.4 million in resources available for foreigncurrency loan commitments. Its plans for mobilizing additional resourcesto cover this gap and finance its future operations are outlined in paras.2.27-2.28.

- 18 -

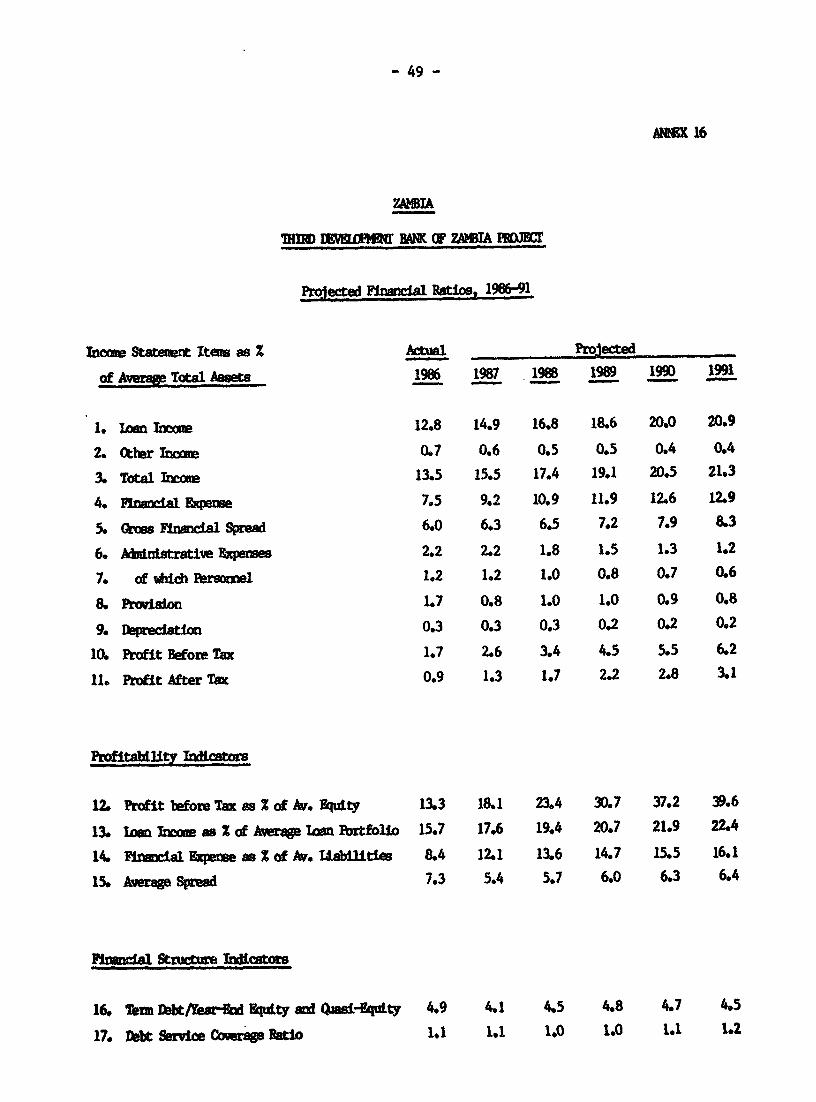

Financial Results and Condition

2.24 DBZ's income statements, balance sheets and main financial ratiosfor FY82-86 are summarized in Annexes 8 and 9. In spite of theincreasingly adverse economic circumstances of the last five years and theportfolio deterioration during 1985, DBZ has continued to be profitable andremains a sound development bank. Net profit before tax as a percentage ofaverage equity for the five-year period FY82-86 was 17%, and fairly stableduring the same period. Since 1982, DBZ's borrowing costs have been goingup steadily from 5.8% of average total assets to 8.4% in 1986, and DBZ hashad difficulty in maintaining its financial spread as it relent these fundsat fixed rates. Despite this increase in financial costs, the effect onprofitability was not significant because DBZ kept a tight lid onadministrative expenses which, at an average of 2% of average total assets,remain one of the lowest rates for DFC's in the ESA region. In March 1984,DBZ adopted a variable (during the life of the loan) lending rate policyfor local currency loans and its spread begun to improve again. DBZ'stotal assets have grown from K 68 million in 1982 to K 223 million in 1986,an annual growth rate of 33%. This growth is attributed to an increase inDBZ's lending activities as well as the upward revaluation of the foreignexchange component of its loan portfolio as a result of the depreciation ofthe kwacha beginning in 1983.

2.25 In 1985, DBZ substantially increased its provisions against badloans, in response to a deteriorating arrears situation, to K 4 millionfrom K 0.4 million in FY84. Total accumulated provisions at the end ofFY85 amounted to 3% of total portfolio or 6% of loans affected by arrears.The implementation of the new provisions policy (para. 2.22) in FY86 hasresulted in total provisions of K 7.1 million (4% of total loanportfolio and 8% of loans affected by arrears). Such a level of provisionsreflects adequately DBZ's portfolio risk at this time. Duringnegotiations, DBZ agreed not to distribute dividends unless provisions forbad or doubtful loans constitute at least 4% of total loan portfolio.

2.26 DBZ's financial structure remains sound. DBZ's liquidityposition is satisfactory and its current ratio has remained above 1.8 inrecent years (with a peak of 2.6 in 1985). DBZ's debt obligations haveoverall a longer duration than its portfolio loans. As a result, the ratioof its current maturities of portfolio loans to current maturities of termdebts averaged 2.0 for the period FY82-85. However, DBZ has recently hadto rely increasingly on local currercy resources to finance its investmentactivities, and its current maturities ratio fell to 1.4 in 1986. Much ofthis new funding has been obtained from commercial banks at three-yearmaturities, and DBZ has in turn relent these funds for up to five years tomeet the longer-term investment needs of its clients. This termtransformation was needed to fill a temporary financing gap, and DBZ hasnow agreed that it will cease this practice in the future (para. 2.07).While DBZ's debt service coverage ratio is expected to decline slightly inthe next few years (Annex 16), the projected capital increase will provideDBZ with an adequate liquidity margin. DBZ's financial structure remainssound. The term debt-to-equity ratio for the period FY82-84 remained belowthe recommended 4:1. By early 198', however, the debt-to-equity ratiojumped to 4.9:1 because of a subs'^atial revaluation of the foreignexchange component of its loan portfolio, and because share capital

- 19 -

subscriptions did not keep pace with DBZ's borrowing to meet the need of

its clients. However, the ratio has subsequently declined as additionalcapital was paid-in, to 4.4 as of October 31, 1986. Further capital

payments are expected to reduce the ratio even further, to 4.1 at the endof FY87.

Projected Operations and Financing

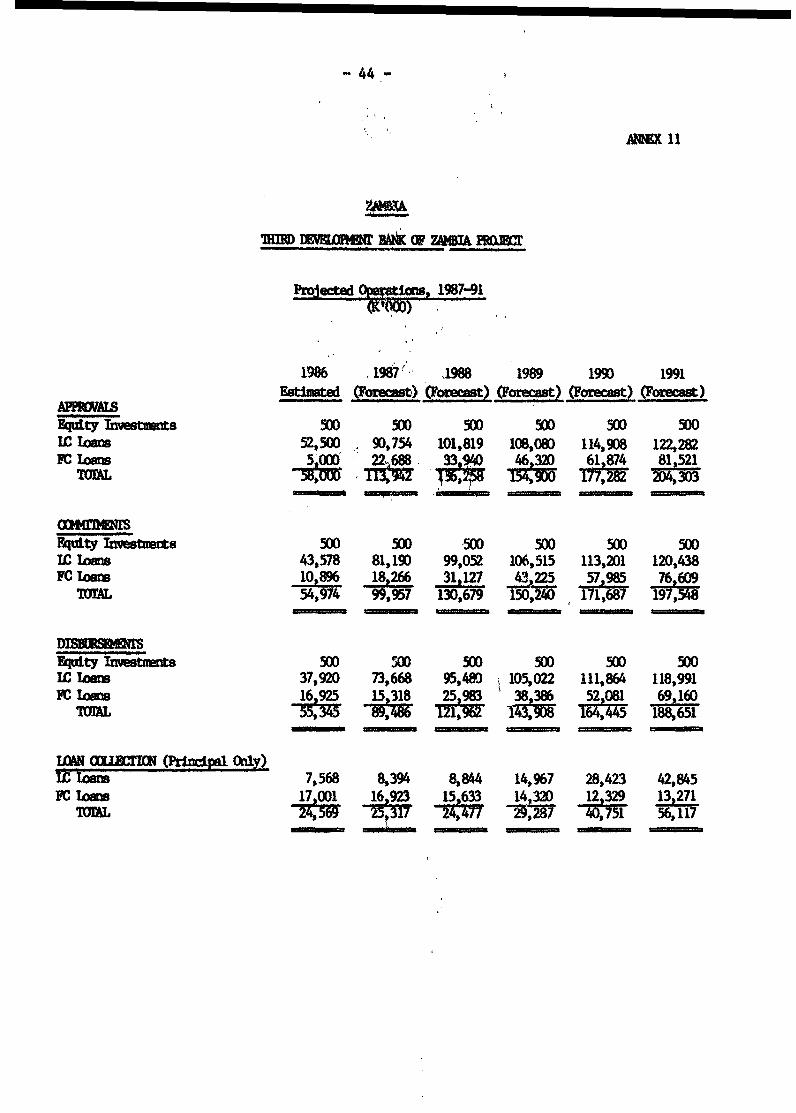

2.27 DBZ's operational forecast is based on a firm pipeline and a

cautious optimism that the recent economic policy measures undertaken bythe Government, with strong support from the IMF and the World Bank, willprovide a timely stimulus to the economy and generate a growth in demandfor investment financing. Total loan approvals expressed in current USdollars are expected to grow in nominal terms by 4% in FY87 increasing to10% in FY91. This implies negative real growth for FY87 followed byincreasing positive real growth rates through FY91. Commitments anddisbursements would follow the pace of approvals. To meet this expectedgrowth in operations, DBZ will require new resources in an amount of US$75million equivalent for the five-year period FY86-91. The direct andindirect foreign exchange component of this amount is estimated to be US$45million, of which about US$30 million would be required during thethree-year commitment period of the proposed credit. Roughly one half ofthe US$30 million represents financing of current requirements for sparesand medium-term fixed asset investment financing. The remaining US$15million represents long-term financing needs of investment projects,including fixed assets, associated working capital and related civil works.

2.28 Over one fifth of the US$75 million equivalent required to meetDBZ's five-year operational targets are expected to be supplied by local

commercial banks, with a maximum term of three years. About one fourth isexpected to be obtained in loans from parastatal non-bank financialinstitutions. In addition, DBZ plans to obtain one-sixth of its needs fromnew equity and retained earnings. Loans granted by FMO, EIB and possiblyIFC (which is presently appraising DBZ for a possible joint equityinvestment and loan), would provide an additional fifth. The proposed IDA

credit would fill the remaining gap during the middle three years of theperiod, and would play an important catalytic role in the new capitalincrease, since IDA's support to DBZ is critical in order to obtain theequity financing it needs. IDA, PMO and BIB (and possibly IFC) funds would

be DBZ's main sources of long-term financing, and would meet the foreignexchange long-term investment needs mentioned in para. 2.31. DBZ'spipeline of subprojects, which has been carefully reviewed on an individualbasis, supports this estimate. It reflects a potential three-year demandfor foreign exchange investment financing of US$20-30 million (including6-9 parastatal subprojects and 20-25 privately-owned enterprises),depending on whether a moderate or high probability of projectimplementation is projected, The expected contribution from each of theabove sources to DBZ's financing plan is the following:

2.29 As of March 31, 1986, DBZ's share capital totalled K 19 million.In order to meet its operational growth targets (paras. 2.27-2.28), DBZwill need to increase its share capital to about K 70 million by FY91.During FY86, DBZ increased its share capital from K 10 million to K 19million, of which "Class A" (domestic) shareholders hold 75%, while "ClassB" (foreign) shareholders presently hold 25%. Traditionally, therelationships between "Class A" and "B" shares has been 60:40, and thepresent imbalance results from the fact that "Class A" shareholdersresponded more quickly to the requested increase than did the "Class B"shareholders. In order to at least return to the 60:40 relationship, theforeign shareholders would have to subscribe a larger share of the K 70million target, and an additional K 51 million would have to be subscribed,of which K 23.1 million would have to be subscribed by "Class B"shareholders, and K 27.9 million by 'Class A shareholders.

2.30 DEG of Germany, FMO of the Netherlands, and EIB have indicatedtheir intentions to subscribe a substantial portion of the amount requiredfrom 'Class B" shareholders. They are expected to take a formal decisionshortly, following the clarification of DBZ's capital needs within thecontext of an accurate operational forecast of DBZ's potential for growth,which was prepared by DBZ with IDA assistance during appraisal. DEG, FMO,EIB and IFC have undertaken a joint appraisal of DBZ, following which theywill present proposals to their respective Boards.

2.31 The Government is having difficulties in providing additionalcapital because of fiscal constraints, bait it has agreed to channel a K 9million portion of a grant from the Dutch Government, to DBZ as part of theGovernment's "Class A" share contribution. IFC is also presently exploringwith the Government the possibility of restructuring DBZ's ownership togive more scope to non-Government shareholders, in connection with apossible increase in IFC's investment in DBZ. Based on tentativeagreements reached with its existing and potential new shareholders, DBZpresented a preliminary capitalisation plan totalling K 51 million to its

- 21 -

Board at the July 11, 1986, Board meeting. A final capitalization planwould be presented to DBZ's Board not later than September 30, 1987. Whilecommitment to subscribe will be firmed up as soon as possible, paying-in ofthe amounts subscribed would be phased according to a timetable related toDBZ's growth needs (Annex 14).

2.32 With the forecast operations and financing plan, DBZ will need toincrease its total debt-to-equity ratio from its present 4:1 limit to 5:1.The higher ratio is justified given DBZ's improved portfolio quality andfinancial performance, and its commitment to match the maturities of itsloans to those of its borrowings.

Projected Financial Performance

2.33 DBZ's financial projections for FY86-91 (Annexes 10-16) assumethat it will maintain an average spread of 4.5% on its foreign currencyborrowings and that its spread on local currency borrowings will increasefrom a projected 5.0% in FY87 to 7% in FY91 as new loans enter the variablelending rate pool. Also, DBZ's profitability is expected to increase as aresult of the implementation of the DRA Plan and improved collectionsrecord (paras. 2.18-2.19). Net income after tax is projected to grow fromabout US$0.2 million in FY86 to US$1.9 million in FY91 when it is expectedto represent about 20% of average equity, as compared to 8.0% for theperiod FY82-85. Total assets are projected to increase from US$32 millionin FY86 to US$68 million in FY91. DBZ's financial structure is expected tocontinue to remain sound, with the debt-to-equity ratio declining as thecapital increase is subscribed and paid-in.

III, THE PROJECT

Bank Group Experience with DBZ

3.01 The Bank Group's relationship with DBZ began in 1971 when theBank, on request of the Government, reviewed the need for a developmentbank in Zambia and recommended the establishment of DBZ to fulfil the mainfunctions of mobilizing resources and promoting and financing of viableprojects in the productive sectors. In addition, the Bank provided adviceon DBZ's organizational structure, operational policies and procedures andstaffing requirements. DBZ was subsequently established in December 1972and began operations in January 1974. To enable DBZ to fulfil its role,the Bank Group has helped DBZ to mobilize foreign exchange resourcesthrough an IFC equity investment and providing lines of credit to financeits operations. DBZ received a Bank loan (No. 1210-ZA) of US$15.0 millionand an IFC equity investment of K 550,000 in FY76, and a second Bank loan(No. 1923.-ZA) of US$15.0 million in FY80. Loan 1210-ZA was fullydisbursed in 1981, and Loan 1923-ZA was 100% committed and 99.9% disbursedas of October 31, 1986.

3.02 The objectives of the first Bank loan and the IFC investment wereto (a) pirovide appropriate mediumr- and long-term financing to medium- andlarge-seale projects which met sound economic, financial and technicalcriteria, rMnd (b) to build DBZ into an effective development financial

- i2 -