Document of The World Bank FOR OFFICIAL USE ONLY Report No. 11682-MAG STAFF APPRAISAL REPORT REPUBLIC OF MADAGASCAR FINANCIAI. INSTITUTIONS DEVELOPMENT TECHNICAL ASSISTANCE PROJECT APRIL 28, 1993 Industry and Energy Operations Division South-Central and Indian Ocean Department Africa Regional Office This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 11682-MAG

STAFF APPRAISAL REPORT

REPUBLIC OF MADAGASCAR

FINANCIAI. INSTITUTIONS DEVELOPMENT TECHNICAL ASSISTANCE PROJECT

APRIL 28, 1993

Industry and Energy Operations DivisionSouth-Central and Indian Ocean DepartmentAfrica Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EOUIVALENTS

Currency Unit = Malagasy Franc (FMG)USS 1 1,899 FMG (March 1993)

= 1,833 FMG (average for 1992)

WEIGHTS AND MEASURES

Metric BritishtUS Eauivalent

1 meter (m) = 3.28 foet1 square meter (sq. m) = 10.76 square feet1 kilometer (km) = 0.62 mile1 square kilometer (sq. km) = 0.39 square mile

ABBREVIATIONS AND ACRONYMS

AON = Appels d'Offres Negatives (Liquidity Withdrawal)AOP = Appels d'Offres Positives (Liquidity Injection)BCRM = Banque Centrale de la Republique Malgache (Central Bank)BFV = Banky Fampandrosoana ny Varotra (State-Owned Commercial Bank)BITS = Swedish Agency for International Technical and Economic CooperationBMOI = Banque Malgache de l'Ocean Indien (Private Commercial Bank)BNI = Bankin'ny Indostria (Private Commercial Bank)BTA = Bon du TrEsor par Adjudication (Short-Term Treasury Bill)BTC = Bon du TrEsor Classique (Medium-Term Treasury Bond)BTM = Bankin'ny Tantsana Mpamokatra (Stae-Owned Commercial Bank)CCBEF = Commission de Contr6le des Banques et Etablissements Financiers

(Financial Supervisory Commission)CCP = Compte de Chequer Postaux (Postal Checking Institution)CD = Certificates of depositCEM = Caisse d'Epargne de Madagascar (Postal Savings Institution)CNAPS = Caisse Nationale de Prevoyance Sociak (Social Security Fund)CNFPB = Centre National de Formation de la Profession Bancaire (School of Banking Training)CPI = Consumer Price IndexIASC = Intenational Accounting Standards CommitteeIFAC = Intenational Federation of AccountantsINSCAE = Institut National des Sciences Comptabia et de l'Administration des Entreprises

(School of Business Management and Accounting)NGO = Non-govemmental OrganizationNPCB = Nouveau Plan Comptable Bancaire (New Banking Chart of Accounts)PCM = Plan Comptable Malgache (1987 General Chart of Accounts)PIT = Postal and Teleommunications ServicesSA = Societe Anonyme (Private Limited Company)SDP = Plan StratEgique de DEveloppement (Strategic Development Plan of BCRM and

CCBEF)SILI = Syst&me d'Importations Liberalis&a (Open General License)SME = Small and Medium Enterprises

FISCAL YEAR

January 1 - Deenmber 31

FOR OFFICIAL USE ONLYSTAFF APPRAISAL REPR

MADAGASCAR

FINANCIAL INSTITUTIONS DEVELOPMENT TECHNICAL ASSISTANCE PROJECT

TABLE OF CONTENTS

Page No.

CREDIT AND PROJECT SUMMARY ...................... (i)

I. INTRODUCTION .......................................... 1

II. THE FINANCIAL SYSTEM ....................................... 2

B. The Financial Sector ......................................... 4- Recent Developments ......................................... 4- Required Institutional and Policy Reforms ........ .................... 6- Financial Sector Strategy ....................................... 7

C. The BCRM (Central Bank) ........................................ 9D. The CCBEF (Financial Supervisory Commission) ......................... 13E. The Commercial Banks ......................................... 14F. The Insurance Sector ......................................... 14G. The Social Security Fund. 15H. Postal Financial Services ............................. 15I. The Payments System ............................. 16J. Financial Markets ............................. 16K. Accounting and Audit Framework .............................. 16

III. THE PROJECT ............................. 18

A. Project Objectives and Scope ............................. 18B. Rationale for IDA Involvement . ............................. 19

This report is based on the findings of a Bank appraisal mission which visited Madagascar from Pebruary 20, 1993, to March5, 1993, comprising of Messrs/MMme Govindan Nair, financial economist, (AF31E - mission leader and task manager); SimonGray, economist, (AF31E); Maud Borg (consultant, central bank mauagement); and Ake Andolf (consultant, informationsystems). Mr. Khalid Siraj (ASTlF) was Iead reviewer and Mr. P"cal Bouvier (IMF) was peer reviewer. Contributions areacknowledged from Mrs. Claudine Morin, lawyer (LEGAF), and Mr. Colin Lyle, auditing and accounting specialist (AFTCP).Messrs. Stokes and Thomet, respectively consultants for USAID and the Swiss Government, also participated in various aspectsof the appraisal mission. Bilingual seretarial support was provided by Mrs. Franqoise Schatten, staff assistant, (AF31E).Messrs. Francisco Aguirre-Sacasa (AF3DR) and Michael N. Sarris (AP31E) are respectively the Department Director and themanaging Division Chief for the operation.

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

C. Project Description ....................... .... .... ..... .... .. . 191. Restructuring BCRM ........... ............................. 192. Strengthening CCBEF .......... ............................. 233. Improving the Accounting and Audit Framework ....................... 244. Support to State Bank Privatization ............................... 25

D. Project Costs. 25E. Project Financing .26F. Project Implementation, Monitoring and Mid-Term Review .26G. Procurement .27H. Disbursements .29I. Accounting, Auditing and Reporting .30J. Project Supervision .30

IV. PROJECT BENEFITS AND RISKS ................................. 31

V. AGREEMENTS TO BE REACHED AND RECOMMENDATIONS .. 32

ANNEXES

1. Statement of Financial Sector Reform and Development Policy2. Madagascar: Monetary Survey, 1986-19923. Main Technical Assistance and Training Activities:

Summary Description of First Year Tasks.4. BCRM Informatics Program5. Project Costs6. Estimated Disbursement Profile7. Implementation Schedule for Key Project Components8. Monitorable Actions under the Project9. Project Supervision Plan10. Terms of Reference for BCRM Coordinator of Strategic

Planning and Development

MADAGASCAR

FINANCIAL INSTITUTIONS DEVELOPMENT TECHNICAL ASSISTANCE PROJECT

CREDIT AND PROJECT SUMMARY

Boffower: Republic of Madagascar.

Beneficiaries: Central Bank of the Republic of Madagascar (BCRM), Financial Supervisory Commission(CCBEF), Ministry of Finance.

Amount: SDR 4.6 million (US$6.3 million equivalent).

Terms: Standard IDA terms with 40-year maturity.

PRelending Government passes SDR 3.5 million of the Credit toITrms: BCRM on a grant basis.

Objectives: The project objective is to facilitate investment and growth in the productive sectors byimproving the functioning of the financial system. This is in line with the Bank's countryassistance strategy which emphasizes increased private sector savings and investment asengines for future growth. The project aims at strengthening key financial institutions andmarkets in Madagascar (including privatization of the two remaining state banks), therebyenhancing public trust in them and enabling them to mobilize savings to meet theinvestment financing needs of the private sector. The project will be implemented in thecontext of the Government's Statement of Financial Sector Reform and DevelopmentPolicy adopted in March 1993. Specifically, the project would aim at: (i) enhancing theCentral Bank's (BCRM) ability to formulate and conduct monetary policy based onindirect instruments; (ii) improving the prudential supervision environment through thestrengthening of the Financial Supervisory Commission (CCBEF); (iii) formulating andenforcing accounting audit and financial disclosure standards based on internationalnorms; and (iv) supporting the privatization of state banks.

ProjectDescription: The project consists of:

(a) restructuring BCRM, the Central Bank, principally through improvements in itsresearch, open market, treasury, internal audit and accounting operations, andthrough the implementation of information technology and human resourcedevelopment plans;

(b) strengthening CCBEF, the Financial Supervisory Commission, with technicalassistance to create an effective supervision structure, training for inspectors andequipment for on- and off- site surveillance;

(c) improving the accounting and audit enviroment, through two sets of activities:(i) training and technical assistance activities to accelerate the development of the

- ii -

accounting profession and to ensure the availability of reliable financialinformation on enterprises based on international standards; and (ii) specifictechnical assistance and training to bankers, auditors and other professionals toestablish, disseminate and implement transparent international accounting andaudit procedures for commercial banks and financial institutions; and

(d) supporting the privatization of banks in the context of an ongoing process ofprivatizing one of the two state banks, BTM, and a Government commitment toa similar process for the other state bank, BFV, by supporting specializedconsultant services such as for valuation and placement of these banks withprivate investors.

The Credit would finance technical assistance, training, equipment and vehicles.

Benefits: The major benefits of the project will derive from its contribution to the establishmentof an efficient financial system, with an effective banking system at its core, which isessential for the development of a market-oriented economy. The project will helpimplement an overall strategy for market oriented financial reforms, particularly instrengthening the framework for prudential supervision, accounting and audit. In turna sound financial system will facilitate productive investments and contribute toaccelerated economic growth and the creation of employment opportunities which are keyfactors in poverty alleviation. Specifically, the project is expected to: (i) enhance theeffectiveness of BCRM to conduct monetary policy; (ii) strengthen the prudentialsupervision role of CCBEF and over time engender greater confidence in the use ofindirect controls rather than direct controls to allocate resources; (iii) enhance the securityand efficiency of financial transitions and the quality of financial intermediation througha greater stimulus for financial savings and more efficient allocation of capital; and (iv)help avert future financial crises rather than simply react to them.

Risks: The major risks of the project stem from the possible impact of the present transitionalpolitical decision-making structure on effective implementation. Successfulimplementation is predicated on political will being maintained to preserve the authorityof BCRM and CCBEF, respectively, to formulate and execute monetary policy and toexercise prudential oversight of banks. At the same time, the institutional developmentgoals for BCRM and CCBEF are complex and ambitious, including significantlyredefined business objectives and extensive use of information technology, and could besubject to implementation slippages. These risks are mitigated by: (i) the high level ofcommitment to project objectives and to the project's urgency expressed by a broadspectrum of political figures and technicians; (ii) limiting the project core to BCRMwhich has demonstrated continuity in its institutional capacity; (iii) the progress alreadymade, by BCRM and CCBEF themselves, towards preparing this project, indicating earlyownership and internalization of project design and objectives; and (iv) up-frontagreement and implementation of key organizational and institutional changes necessaryto execute the project.

Rate of return: Not Applicable

- iii -

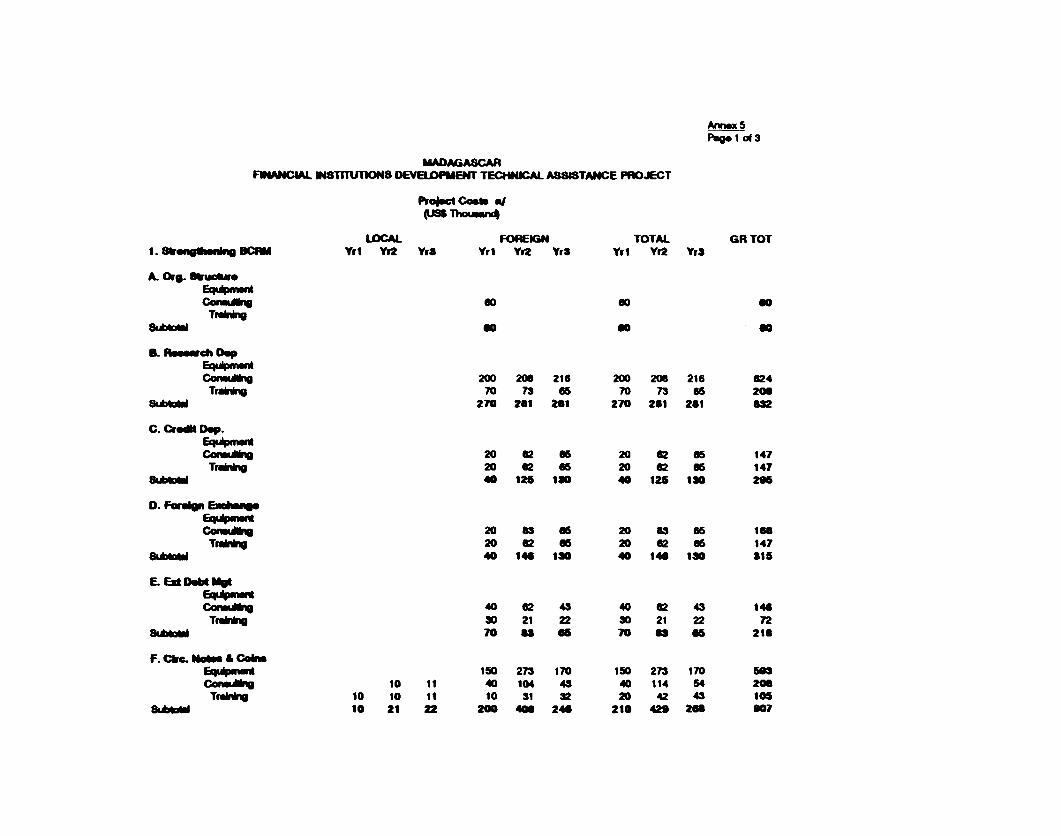

SUMMARY PROJECT COSTS ESTIMATES f(USS thousand)

ESTIMATED PROJECT COSTS: L l gll ~~~~~~~~~~~~~~~~LoOcal Foreign Total

1. Strengthening BCRM T TAdvisory Services for Central Bank Organization - 60.0 60.0

Research Department - 832.0 832.0

Credit Departmnt - 295.0 295.0

Foreign Exchange - 315.0 315.0

External Debt Management - 218.0 218.0

Planning & Management of Circulation of Notes & Coins 53.0 854.0 907.0

Accounting 82.0 499.0 581.0

Internal Audit 26.0 307.0 333.0

Information Systems 345.0 4,014.0 4,359.0

Human Resources 144.0 380.0 524.0

Project Management Assistance - 502.0 502.0

Sub-Total 650.0 827 892.0

2. Strengthening CCBEF 21.0 556.0 577.0

3. Improving the Audit & Accounting Framework 204.0 456.0 660.0

4. Supporting the Privatization of State Banks - 200.0 200.0

TOTAL _.488.5 D0.360

a The incremental staff and operating costs under the project will be borne by the implementingagencies concerned, mainly BCRM.

k/ Includes annual physical contingencies of 5%, and annual price contingencies of 4% in US$.

FINANCIAL INSTITUTONS DEVELOPMENT TCNCAL ASSISTANCE PROJECT

STAF APPRAISALRE R

L.INTRODUCTO

1.1 In 1991, a number of economic reforms were abandoned as Madagascar entered into a periodof political turbulence. Fundamental weaknesses in the financial sector had severely undermined thecapacity of the authorities to execute structural adjustment programs and as a consequence theirsustainability was thwarted. Madagascar is still in a period of political transition with limited authorityto undertake a comprehensive structural adjustment program. This period of transition does, however,present the opportunity to strengthen key financial institutions in preparation for the resumption of broadeconomic reforms and economic recovery and growth.

1.2 Significant strengthening of the Central Bank (BCRM) and the Financial Supervisory Commission(CCBEF) is indispensable for mobilizing savings to meet the investment financing needs of the privatesector and to laying the foundations for sustainable economic growth. The proposed project will beimplemented in the context of a Government Statement of Financial Sector Reform and Development.The core of the project is centered on BCRM which has demonstrated continuity in its institutionalcapacity over the transition period.

1.3 The project will specifically: (i) reinforce the institutional capacity of BCRM so that it caninitiate and sustain financial sector reform through more effective formulation and execution of monetarypolicy; (ii) develop CCBEF so that it can effectively execute its prudential supervision functions andconsequently engender greater confidence in the use of indirect controls in allocating financial resources;(iii) improve financial accounting and audit in enterprises and in the financial sector, specifically thebanking system, by basing them on internationally accepted standards; and (iv) help complete the processof privatizing the remaining two state banks.

1.4 The proposed project was appraised in February 1993 by a World Bank mission consisting of:Messrs./Mme Govindan Nair, financial economist, (AF3IE - mission leader and task manager); SimonGray, economist (AF3IE); Claudine Morin, lawyer (LEGAF); Maud Borg, (consultant, central bankmanagement); and Ake Andolf (consultant, information systems). Contributions are acknowledged fromMr. Colin Lyle, accountant (AFTCP), and Messrs. Stokes and Thomet, respectively consultants forUSAID and the Swiss Government, who also participated in various aspects of the appraisal mission.

- 2 -

II. HE FINANCIAL YSTEM

A. Macroeconomic Context

Background

2.1 Madagascar, with a population of 12 million growing at 3 percent per year, and per capitaincome of about US$220, is one of the world's poorest countries. It is the fourth largest island on theplanet with wide variations in soils, topography and climate, and it features unique flora and fauna. Thecountry's staple is rice, and the major exports are coffee, vanilla, cloves and shellfish. In the early yearsof independence in the 1960s, Madagascar witnessed modest growth, followed by stagnation from 1970to 1980, and a severe downturn to 1982. Financial stabilization followed with limited economic growthfrom 1983 to 1987. Since 1988, the economic results were encouraging until 1990, shortly after whichthe country entered into a period of political turbulence in 1991.

2.2 In the period from 1983 to 1988, Madagascar implemented a comprehensive program ofstabilization and economic reform. The Government's deficit was slashed from 18 percent of GDP in1981 to just over 4 percent in 1989. Monetary creation slowed and so did inflation from a high of 31percent in 1981 to 9 percent in 1989. At the same time the external current account deficit (includingtransfers) dropped from 10 percent to 5 percent of GDP. In achieving these stabilization measuresMadagascar was supported by four IMF standby arrangements since 1985, which were subsequentlyreplaced by arrangements under the Enhanced Structural Adjustment Facility in 1989.

2.3 Actions, albeit slower than required, were also taken to reform the trade and exchange rateregimes. The exchange rate moved away from being fixed administratively to more flexibly managedwith significant depreciation of the real effective exchange rate. Complementary actions on tariff reformwere also implemented. All quantitative restrictions were lifted by 1988, followed by a four-year programinstituting ad valorem tariffs, rationalizing product import categories from 69 to 16, and introducingminimum and maximum tariffs of 5 percent and 80 percent, respectively.

2.4 In tandem with these trade reforms, structural adjustment was tackled on a number of differentfronts. Price controls were virtually eliminated over the decade with prices on agricultural commoditiesand the consumer price of rice being completely freed in 1985 and retail prices on 90 percent of valueadded in industry being decontrolled by the end of the decade. Over the same period, the Governmentrolled back the monopoly of public marketing authorities, most notably in coffee, clove and pepperexports and through the legalization of private trade in rice, pulses and groundnuts. Currently, only thevanilla trade remains controlled. The effect on the rice industry was immediate, with significant increasesin production in the 1987 season and a significant decline in import rice dependency to 1990.

2.5 Public expenditures underwent a fundamental reorientation in the 1986-90 Development Plan thatemphasized: maintenance and rehabilitation, improved utilization of capacity, a much reduced role of theState in manufacturing, and a major rationalization for agriculture. The first rolling triennial investmentprogram was formulated for 1989-1991 and was followed by further improvements in a subsequentprogram for 1990-1992, which included increased aggregate provision for counterpart funding forexternally assisted projects, and the beginning of a significant reorientation of current expenditurestoward priority needs in primary health, basic education and public safety.

2.6 The Government took initial steps to reform the completely state-owned banking sector. By theend of 1989, the loan portfolios of these banks had been cleaned of most non-performing and doubtfulassets. In 1990, a new full private bank with majority foreign capital started operations, and in 1991 oneof the state banks was privatized and another obtained minority private participation. Moreover, in 1990,Central Bank (BCRM) embarked upon a process of replacing direct credit allocation with a more flexiblesystem based on indirect market instruments.

2.7 BCRM losses, however, mounted over the 1980s which indicated a fundamental flaw in thefinancing of public expenditure. In taking direct liability for the exchange rate risk on governmentexternal debt, in addition to providing advances to the Government at well above the statutory limit andat near zero percent interest rates, BCRM registered operating losses which averaged 3 percent of GDPfrom 1985 to 1990 and resulted in accumulated losses equivalent to 9.6 percent of GDP in 1990. Limitedaction was taken to redress this situation in 1991 when it was decided to remunerate Treasury depositsand charge Treasury borrowing with the BCRM at money market rates.

2.8 Overall, the stabilization and subsequent structural reforms contributed to the resumption of percapita growth in early 1988. This supply response was, however, slower than desired partly because ofinadequate progress in institutional reforms in the financial sector. It was undermined by political eventsin 1991.

Recent Developments

2.9 In 1988-90, strong growth in agricultural production and new export-oriented manufacturingactivities (e.g., garments, leather, wood processing) led to modest per-capita GDP growth. Thedevelopments in 1990, however, demonstrated the fragility of the reform and recovery. Even prior to thepolitical turmoil, growth in agricultural production slowed to about 2 percent due to poor weather, whilethe secondary sector stagnated due to weak performance in the public sector textile and food industries,despite continued strong performance by the new manufacturing enterprises. The setback centered on thefailure of the authorities to effectively link and manage exchange rate policies and credit policies.Merchandise imports rose by 58 percent in nominal U.S. dollar terms as a result of an uncontrolledexpansion of credit (provided largely through BTM, the only remaining fully state-owned commercialbank), an appreciating real effective exchange rate, and an increased oil bill. This, together withstagnating merchandise exports in current dollar terms, due largely to the continued sharp decreases inthe prices of the country's major exports (in particular that of coffee), led to a trade deficit of 6 percentof GDP, compared to a small surplus in 1989. As a result, the external current account deficit widenedfrom 8.6 percent of GDP in 1989 to 11.7 percent in 1990. These developments, combined withlower-than expected aid inflows, caused foreign exchange reserves to decline from five months of importsat end-1989 to less than two months by end-1990.

2.10 The Government acted, albeit slowly, to restore financial equilibria by devaluing the FMG by16 percent in January 1991 and by severely tightening credit expansion between November 1990 and June1991. These measures and increased external support helped improve the country's external positionduring the first half of 1991, and the economy was on the way to another year of positive growth, whenpolitical turmoil broke out in the second half of 1991. As widespread demonstrations and strikesparalyzed public administration, economic activity was severely disrupted, and the adjustment processwent off-track.

- 4 -

2.11 Real GDP contracted by 6 percent in 1991; inflationary pressures built up; financial imbalanceswidened significantly; and large domestic and external payments arrears were accumulated. Politicaldisturbances in 1991 resulted in a shortfall in tax collection and the rise in the budget deficit to about 10percent of GDP; in 1992, tax collection did not improve and budgetary discipline worsened. The truesize of the fiscal deficit was masked by the quasi-fiscal operations of the Central Bank which since 1983has been assuming debt-servicing obligations once borne by the Treasury. The internal imbalances werereflected in a worsened external position of Madagascar, with the overall current account deficit reaching10 percent of GDP in 1992. The growing shortage of foreign exchange had led to the suspension of theOpen General License system in October 1991.

2.12 A transitional power-sharing arrangement, agreed in late October 1991 by all major politicalforces, became effective in January 1992. Under this arrangement, the President remained in office withgreatly curtailed executive powers; the National Assembly was dissolved and replaced by a High StateAuthority headed by a key opposition leader; and a government of national consensus was formed. Thenew Constitution was approved by referendum in August 1992, followed by presidential elections in lateNovember 1992 and February 1993. Legislative elections are scheduled for June 1993. Political andeconomic turmoil have exacerbated issues which were already adversely affecting Madagascar's projectimplementation performance. Notable among these is weak management, ill prepared to meet thechallenges of a market economy. While the political transition runs its course, institution building willbe critical to permit the timely and efficient return to private sector led growth.

B. The Financial Sector

Recent Developments

2.13 In the second half of the 1980s, reforms in the financial sector centered on steps to strengthenthe banking sector, which was completely state-owned and experiencing severe financial problems. Bythe end of 1989, the loan portfolios of these banks had been cleaned of most non-performing and doubtfulassets. In 1990, a new, fully private bank with majority foreign capital started operations; in 1991, oneof the state banks was privatized and another obtained minority private participation while two privateforeign banks opened representative offices in Madagascar. In parallel with these actions, the CentralBank embarked upon a process of replacing direct credit allocation with a more flexible system based onindirect market instruments. These financial sector reforms have had mixed results. The new privatebanks and the majority privatization of one of the state banks has proved successful. Progress was lesssustainable, however, in maintaining the overall health of the banking system following the portfolioclean-up of 1989, because the two majority state banks have shown increasing weaknesses since 1991.These difficulties led to a virtual standstill in the interbank money market, jeopardizing the success of amarket-based system of interest rates introduced in November 1990. As discussed below, theestablishment of market-based interest rates was also undermined by the suspension of the Treasury Billmarket in mid-1991.

2.14 Problemns in establishing market-based interest rates. Direct refinancing operations by BCRMwere replaced in November 1990 by money market auction operations, to both inject and removeliquidity from the financial system. They were interrupted in June 1991 in the wake of political strife,but were reinstated again in November 1991. The root of this perturbation in the money market was there-emergence of macroeconomic instability in 1991, as outlined in paragraph 2.11. At the same time,institutional weaknesses in the two state banks have undermined the development of a money market.Specifically, in 1990/1991 a rapid expansion in credit by the largest state bank undermined monetary

stability, which was later compounded by a similar increase in credit in the other remaining state bankin 1992. It is noteworthy that while the two state banks have at various times exceeded their creditceilings for extended periods, the two private banks have generally kept within their credit ceilings.

2.15 Another reason the money market has not worked well has been the lack of clear objectives inmonetary policy which is partly reflected in an inability to coordinate money market operations withpublic financing operations of the Treasury. Currently the only treasury bills being issued are BTCs (Bonsdu Tresor Classiques), representing medium to long-term investments. Returns on this paper, becauseof up front interest payments and tax exemption, provide effective rates which have remained static overa two-year period and bear little relation to the prevailing market conditions. Since the money marketwas reinstated in November 1991, the market has been highly liquid, due to the suspension of the OGLimport system combined with lower tax recovery and increased government spending. BCRM has,therefore, been systematically removing liquidity from the system through the money market auctioninstrument "appel d'offres n6gatives' (AONs). To avoid wide fluctuations in rates that could result fromfiscal problems and weaknesses of state banks, BCRM openly or covertly attempts to regulate the marketwhich results in rigid interest rates, while basic policies of either removing or injecting li-uidity aremechanistically followed. Under these conditions, the Treasury has no incentive to issue short-, erm paper(BTAs) in lieu of borrowing from BCRM at money market rates.

2.16 The problems of state banks and lack of adequate coordination of monetary and fiscalmanagement have resulted in three indications of a lack of market-based interest rates. First, interest rateson both BCRM deposit and refinancing instruments have remained exceptionally static over the last twoyears despite a complete reversal in the money market situation from a highly illiquid market fromNovember 1990 to June 1991, to a highly liquid situation following the resumption of the market in 1991.Second, operations in the interbank market have been extremely modest, with most of the operationsoccurring between the two state banks, while the private banks, for reasons of confidence, prefer torefinance or place resources directly with BCRM. Third, the wide divergence in returns on savings isindicative of the of lack of market forces at play: sight deposits averaging 2.6 percent, term depositsaveraging 14 percent, AONs 8.75 percent, special deposits with BCRM 5 percent, and six-month treasurybills (Bons du Tresor par Adjudication, BTAs) 18 percent and with an effective return of 25 percent.

2.17 Problems of state banks. With regard to the banking system, despite the 1986 to 1988 portfolioclean up and the privatization moves referred to in paragraph 2.6, the authorities were unable tosatisfactorily control the growth of credit in 1990 and 1991. This inability to control credit centered oninstitutional weaknesses in one bank, the wholly state-controlled BTM, which witnessed a severedegradation of its loan portfolio over the 1990/1991 period. This was a major factor in the discontinuationof the OGL import system in September 1991. Remedial action was taken in February 1992 with thereplacement of BTM top management, which has led since April 1992 to the reduction of BTM loanportfolio to within the specified BCRM credit ceiling, and to a position where BTM reversed its normalrefinancing requirement with BCRM to a situation where it placed excess liquidity with BCRM as ofAugust 1992. While BTM's adverse impact on overall credit management appears to have now beencontained, the state of the bank's loan portfolio has worsened. Consequently, the profitability of the bankis declining while provisioning requirements for doubtful assets increase, making the prospects forimmediate privatization more remote.

2.18 Problems at BTM recently spilled over to the other remaining state bank, BFV. The 1991accounts for this bank could not be satisfactorily audited and the loan portfolio has significantlydeteriorated and, consequently, a large increase in provisions is required. Furthermore, since late 1991,

- 6 -

BFV has consistently failed to respect credit ceilings. While the two private banks have been in positionsof excess liquidity and BTM reduced its refinancing requirement, showing excess liquidity in August1992, BFV still had a net refinancing requirement with BCRM.

2.19 The problems of establishing market-based interest rates and of the state banks reflect two setsof weaknesses in the financial system. First, the lack of independence of the Central Bank (BCRM) andFinancial Supervisory Commission (CCBEF) has resulted in the conduct of monetary policy andprudential oversight being influenced by political factors. Second, the lack of independence of these keyinstitutions is compounded by inadequate capacity to formulate and execute monetary policy based onindirect instruments and the lack of concise and comparable information on the health of bankinginstitutions as well as inadequacies in the prudential supervision system, the accounting framework, andthe financial disclosure and audit standards for banks. All these factors have made early detection andcorrection of financial distress difficult.

Required Institutional and Policy Reforms

2.20 The Government and BCRM are conscious that a wide variety of monetary and financial reformsare required to develop a market oriented economy. Accordingly, the Government adopted a Statementof Financial Sector Reform and Development Policy in March 1993 containing a two-stage strategy forstrengthening the financial system (see Annex 1). The first phase of reform aims at the following priorityinstitutional reforms: (i) strengthening the independence and accountability of the Central Bank; (ii)enhancing the capacity of CCBEF in prudential supervision; (iii) improving the framework for audit andaccounting; and (iv) supporting the privatization of state banks. Some of the remaining reforms arepredicated on macroeconomic stability through fiscal prudence and clear policy decision with politicalstability. In many cases, however, the ground can be laid to facilitate the implementation of futurereforms while the necessary fiscal and political preconditions are in the process of being fulfilled. Indeed,the unsatisfactory results of earlier financial sector reforms underscore the urgency of institutionalstrengthening in order to allow macroeconomic reform to succeed.

2.21 On the monetary front, a number of improvements are required to the workings of the market.Chief among these is the implementation of a pure Dutch auction system for BCRM refinancing with theremoval of any BCRM limits on interest rates for auctions. In addition to this, the standardization ofmaturities and a well defined and publicized auctioning schedule for both refinancing and placing needsto be accomplished. Furthermore, alternative BCRM instruments to borrow and deposit funds whichundermine the auction system should be removed. This must be complemented with a well designedresearch capacity combined with improvements in the monetary programming in BCRM. Eventually, bankcredit ceilings and limits should be abolished once there is adequate progress towards: (i) the developmentof an active money market; (ii) a sound privatized banking system; and (iii) improvements in planningand financing public debt. This series of measures should begin to place the functioning of financialmarkets and conduct of monetary policy using market instruments on a more firm footing.

2.22 While progress has been made in developing reserve requirements into a fully fledged tool ofmonetary control, a number of measures are required to improve this instrument. These includeimproving the computing lag time, being more flexible on what constitutes reserves and not being undulysevere on the penalty when reserve requirements cannot be met. Again, capacity building measures inBCRM could overcome many of these shortcomings.

- 7 -

2.23 In the area of public finance and monetary policy, greater coordination between BCRM and theTreasury needs to be developed to ensure a more planned and systematic approach that avoids ad hoefinancing and increases the efficiency of public finance operations. BTAs issued for six months andtwelve months should be reintroduced. This will require concurrent flexibility in auction operations toguarantee that rigid auction rates do not undermine the attractiveness of BTAs. Increased research andmanagement capacities at BCRM are required to ensure that short-term liquidity management is integratedwithin a well formulated overall policy of monetary management and that returns on BTCs are more inline with the market, and to allow for the development of a secondary market for both types of treasurybills.

2.24 While prior credit approval has been abolished by BCRM, there remains a prior authorizationby BCRM of any individual loan that a bank uses to collateralize refinancing with BCRM. As capacitiesto enhance supervision of financial institutions in CCBEF improve, this requirement should be abolished.BCRM refinancing will become more a function of the commercial bank risk rather than the individualborrower risk, though provision could still be made to exclude loans to specific individual borrowers withinsufficient creditworthiness from being used as collateral for BCRM refinancing.

2.25 In the light of the present banking crisis and given the policy objective to shift to indirectmonetary controls, increased support for banking supervision and the upgrading of financial accountingand auditing standards is crucial. This will require strengthening the technical and legal capacity of theFinancial Supervisory Commission (CCBEF) in tandem with the dissemination and implementation of animproved and uniformly applicable chart of accounts for commercial banks, as well as the introductionof appropriate auditing procedures, both of which should reflect international norms.

2.26 Besides improved supervision, the key to solving present problems in the banking system is theprivatization or liquidation of the two state banks. The privatization route may necessitate theintroduction of interim management to turn these banks around and render them privatizable. In the eventthat it is concluded that the alternative of liquidation is the only feasible outcome, financial policy willdictate that all efforts are made to explore the possibility of selling the assets to another bank with a viewto maintaining the depth and range of financial services as is economically feasible.

2.27 In the process of restructuring the financial sector, policies which engender financial andeconomic autonomy and transparency of financial institutions, should be pursued to ensure that theyoperate in an efficient and self sustaining manner. This is a particularly important objective for BCRM,whose institutional and financial independence will also form an important policy objective. Furthermore,wherever feasible, policy to broaden and deepen the financial markets through the creation andstrengthening of existing institutions and instruments will be pursued.

Financial Sector Strategy

2.28 The strengthening of the financial sector is critical to sustaining the reforms embarked on in thelate 1980s, whose principal objective was to ensure the successful transition from a state to a privatesector-based market economy. The centerpiece of the financial strategy is to efficiently mobilize savingsto meet the investment fmancing needs of the private sector. The major constraint to increasing the levelof investment in Madagascar, particularly private sector investment, is the low level of domestic savings.Despite increases in domestic savings to 10 percent of GDP in 1989, Madagascar's gross domesticsavings rate is below the average for sub-Saharan Africa (12 percent). Equally, Madagascar's investmentrate has been below the sub-Saharan average at 10 percent of GDP between 1985 and 1989, against a sub-Saharan average of 14 percent. While the primary obstacle to mobilizing savings and increasing

investment remains a fiscal problem crowding out private investment and dampening incentive to save,a number of secondary problems are related to institutional capacities and the quality of financialintermediation.

2.29 To enable the financial sector to play its role in recovery and growth, a seven-part sector strategyhas been developed jointly with the Government. This strategy is the outcome of a dialogue which beganin January 1992 with discussions of the World Bank's Financial Sector Study (Report No. 9817-MAG).The various elements of this strategy are included in a Government Statement of Financial Sector Reformand Development Policy (See Annex 1). EiM, the Government will pursue a public expenditure programconsistent with a significant lowering of the budget deficit in the short to medium term, and will relieveBCRM of all its quasi fiscal obligations. Second, a full range of institutions, markets and instruments willbe developed over time to ensure that all segments of the population have access to financial services,which effectively mobilize financial savings and efficiently transfer them into the real economy. Financialdepth, M2/GDP, has hardly changed and remained below 25 percent of GDP in Madagascar since the1970s (1985-88 average: 22.5 percent), which is low when compared with other developing countries.Furthermore there is highly disparate availability of financial intermediation in Madagascar, dependingon geographical location and income group. The majority of the rural population has limited access tofinancial services, and these services have limited usefulness to a large part of the active populationbecause of the low level of incomes and the restricted and inflexible nature of the services offered. ThiW,over time the financial system will promote a market determined set of key prices, notably interest ratesthat would remain positive in real termns and, eventually, an exchange rate that is market determined.At present, despite monetary reforms, interest rates are extremely rigid and thus fluctuate in real termsfrom negative to positive without any reference to demand for and supply of resources. Removal of therigidities in interest rates is, therefore, key to the efficient allocation of resources. It is recognized,however, that this can only be achieved if macroeconomic stability is restored and fundamentalinstitutional weaknesses in the banking sector are resolved.

2.30 A fQ.gh element of the financial sector strategy is the development of a rigorous and effectiveprudential supervision which also implies an appropriate framework of accounting, auditing and financialdisclosure for financial institutions. At the core of many of the financial sector problems experienced inMadagascar over recent years has been the lack of reliable financial information, combined with adeficiency in the prudential supervision of financial institutions. A strategy to raise standards in financialinformation and strengthen supervision is, therefore, essential to the financial sector reform. Fifth, therewill be an eventual shift to indirect instruments of monetary control. sixth, state ownership and controlin all bank and non-bank financial institutions will be removed and a sound institutional framework withstrong and competitive financial institutions will be promoted. Finally, the appropriate financialinfrastructure (legal system, payments system) will ensure the efficiency and security of all financialtransactions (payments, deposits, loans, etc.).

2.31 The proposed project will help in the implementation of the overall sector strategy. It will focuson immediate priorities of reforms in BCRM and the CCBEF and improvements to accounting and audit.It will provide technical assistance, training, equipment and supplies to strengthen both BCRM andCCBEF. Furthermore, the project will strengthen the accounting and auditing environment by providingtechnical assistance and training for upgrading and disseminating improved accounting and auditingstandards in line with international norms. Experience with prior adjustment programs has demonstratedthat there are advantages to initiating institutional reforms as early as possible, because of the time it takesto bring them about. Having stronger institutions is a precondition for the application of effectivefinancial policies and structural reforms in the sector.

-9 -

2.32 IDA involvement in financial sector reforms: World Bank involvement in the financial sectordates back to the mid-1980s when the Government began to place limits on banking sector credits topublic enterprises. In 1987, state owned banks started restructuring their portfolios by provisioning moreaggressively against non-performing assets. In 1988, a new banking law allowed private sectorparticipation in the financial sector, which resulted in a new private commercial bank opening its doorsin 1989 and one of the three state banks being fully privatized and another partially. The World Bank'srole in these initiatives was complemented by the IMF which, inter alia, provided assistance in the designand launching of a new money market in Madagascar in 1989-1990. Bank/IMF collaboration includedIMF participation in the Bank's Financial Sector Study (Report No. 9817-MAG, March 1993).

2.33 The Government, conscious of the need to establish solid financial institutions as a vehicle forprivate sector development and the resumption of growth, requested in January 1991 assistance from theBank in preparing a series of operations designed to meet this objective. With regard to the proposedproject, the World Bank has been involved in a series of discussions with both the Government andBCRM, including seminars in three subsequent missions before appraisal in February/March 1993. Thesediscussions have been aimed at early ownership of the project by BCRM which created a project groupin August 1992 to draft a strategic development plan. In parallel with these discussions, the IMF reviewedBCRM and banking issues and reforms in May 1992, and provided advice on how the balance sheet ofBCRM could be restructured to eliminate all quasi fiscal obligations more properly attributed to the State.At the same time, the IMF has taken the lead in reviewing the statutes of BCRM and in helping defineappropriate steps for strengthening the supervisory role of CCBEF, including an IMF initiative to recruita foreign bank supervisor as technical adviser. These initiatives intimately complement those of theproject, and reflect the critical role the IMF has played in reviewing and defining the framework for thistechnical assistance operation.

C. BCRM (Central Bank)

2.34 The core functions of the Central Bank of the Republic of Madagascar (BCRM) are consistentwith those of a modern central bank, namely: issuing legal tender and assuring economic growth withprice stability through appropriate monetary policy. However, as is the case with many countries in thedeveloping world, BCRM has taken on a number of other functions, notably quasi fiscal activities, whichare inconsistent with its development into an independent institution ensuring stability in money andfinancial markets. To better identify institutional development needs of BCRM, the scope and results ofits primary functions (domestic and foreign operations, credit, research), as well as support (accountingand audit, information systems, human resources) are reviewed below:

(a) Formulating and Executing Monetary Policy

2.35 As previously indicated, there are major weaknesses in the monetary operations of BCRM whichhave resulted in a rigid money market and the maintenance of a number of direct controls on the market.The first weakness is a lack of research capacity to formulate monetary policy based on an analysis ofdevelopments in the real and financial sectors (see paragraph 2.39 below). The second weakness is thelack of coordination with the Treasury on government financing and open market operations. Institutionalstrengthening through the development of (i) research capacities, (ii) open market operations and(iii) improved coordination with the government financial operations, would give BCRM more confidencein allowing the market to function. BCRM would, therefore, be better prepared to remove credit ceilings

- 10 -

and other direct controls, once macroeconomic stability has been established and fundamental institutionalweaknesses in the commercial banks resolved.

(b) Government Banker

2.36 Apart from acting as the Government's banker, BCRM has also been implicitly obliged tofinance the public sector deficit, which is illustrated by the mounting operating losses of BCRM in the1980s. This financing took three forms: (i) taking direct liability for the exchange rate risk onGovernment and private sector external debt during the London and Paris Club rescheduling negotiationsin the 1980s which, in the case of the Government, effectively meant recording losses on the balancesheet of BCRM that should have been ascribed to the national budget; (ii) providing advances to theGovernment well above the statutory limit; and (iii) providing the advances at virtually zero percentinterest until 1991. Since the Government does not systematically respect its obligations to compensateforeign exchange and operating losses, three fifths of BCRM operating assets represented unremuneratedclaims on the Government by the end of the 1980s.

2.37 The resolution of this problem centers on legally enshrining the independence of BCRM andrestructuring its balance sheet. Initiatives involving the IMF in both these areas are already underway.With regard to the independence of BCRM, revisions to the 1973 Ordinance setting forth BCRM'sStatutes have been prepared to: (i) clearly limit the objective of BCRM to the stability of the currency;(ii) increase its authority in formulating monetary policy; (iii) increase the independence of the Governorand Board through lengthened tenure, fixed-term appointments and clear dismissal criteria; and (iv) ensurethe regular publication of BCRM audited accounts. A first step towards the restructuring of the balancesheet was undertaken in 1992, when the non-interest earning assets of BCRM representing claims onGovernment and associated liabilities were recorded in specific new accounts outside of the balance sheetof BCRM, which now render these quasi fiscal operations more transparent.

2.38 Increased legal and financial independence of BCRM are key to general financial sector reformand critical to the successful application of any technical assistance provided to BCRM or CCBEF.Consequently the independence of BCRM and the elimination of its fiscal obligations constitute explicitobjectives of government policy for the financial sector which need to be forcefully pursued. (See theGovernment's Statement of Financial Sector Reform and Development Policy, Annex 1).

(c) Primary Functions

2.39 Research. A fully fledged research and statistics function does not exist in any significant senseat BCRM. Currently, a unit consisting of four staff is engaged in collecting macroeconomic data, mainlyin preparation for BankI/IMF missions. There is a multitude of research and policy-related data gatheringand processing efforts through BCRM which are uncoordinated and which result in numerous redundantdata requests from various departments of BCRM to the outside (commercial banks and financialinstitutions, ministries, etc.). The research function until very recently lacked a director and, as a result,the authority to coordinate and streamline data requests from the outside and data flows within BCRM.Consequently, no monetary programming is carried out. Furthermore, there is no strategic or policyresearch, for example for helping formulate monetary policy or better understanding links between thefinancial system and the real economy.

2.40 Credit. The credit department in BCRM has primary responsibility for the implementation ofdirect monetary controls, and in the last few years has been responsible for reforming a number of these

- 11 -

instruments and for implementing new money market instruments to manage the level of liquidity in themarket. While some progress has been made in dismantling some of the direct controls, notably inabolishing all prior credit approval and in developing reserve requirements as a tool of monetary control,the operation of the money market remains rigid (See para. 2.15) and credit is still micro-managed byBCRM. Notwithstanding that credit ceilings will need to be maintained until fiscal problems andinstitutional weaknesses in the commercial banks are resolved, a great deal of institutional strengtheningis required over the transition to improve the flexibility, responsiveness and effectiveness of the nascentmoney market and the new monetary instruments.

2.41 Foreign Exchange Operations. BCRM monitors all foreign currency operations and managesall foreign currency transactions on behalf of the Government. Until September 1991, when the OpenGeneral License System (OGL) was abolished, all foreign currency receipts had to be surrendered toBCRM. Currently the commercial banks are permitted to keep 60 percent of the foreign currency receiptswhile ceding 40 percent to BCRM, which maintains its role of monitoring all foreign currencytransactions. Given the existing foreign exchange shortage and the need for commercial banks to conductforeign exchange transactions at an overvalued official rate, this system effectively puts the burden ofrationing on commercial banks. A strategy, cognizant of present fiscal and monetary problems, needs tobe developed with the long term objective of BCRM playing a supervisory role in a market where foreigncurrency is freely traded. Furthermore institutional weaknesses in managing and monitoring foreigncurrency operations have to be addressed to prepare BCRM for the implementation of this strategy andto increase the efficiency of existing operations.

2.42 External Debt Management. BCRM manages all external public debt on behalf of theGovernment, and has been obliged to bear losses on external debt that should have been borne by theTreasury, notably exchange rate losses. A strategy to ensure that all obligations on foreign debt contractedby the Government are correctly attributed to the Treasury was developed in 1992 as part of the overallpolicy to eliminate quasi fiscal activities from BCRM balance sheet, referred to in paragraph 2.37. Thisresulted in the creation in early 1993 of a distinct department within BCRM to implement this strategyand to manage all external debt. Technical assistance is required to develop the capacities of thisdepartment to manage these external debt operations.

2.43 Circulation of Bank Notes. Activities associated with the circulation of bank notes at BCRMcenter on national currency management. BCRM is poorly equipped to monitor and manage the level ofnational currency in circulation due to: (i) limited operational capabilities within BCRM to forecast andcontrol demand for national currency; and (ii) poor communications with both BCRM domesticcorrespondents and the commercial banks. These problems need to be tackled in tandem with a reviewof the domestic payments system.

(d) Support Functions

2.44 Accounting. Whereas BCRM appears to have managed to maintain and prepare accounts on aregular basis, the internal organization of the accounting function suffers certain weaknesses. These result,principally from an unsatisfactory segregation of responsibilities, and the fact that there is no separate unitwhich is primarily responsible for accounting and for reporting on financial matters directly tomanagement. Currently, departments or units are not only initiating transactions but are also responsiblefor recording them, thus bypassing a fundamental principle of adequate internal control within theinstitution. Furthermore this situation inhibits the preparation and diffusion to general management ona timely basis, of the financial information necessary to effectively execute their managerial

- 12 -

responsibilities. The absence of regular external audits of BCRM accounts is an additional shortcomingin the overall control exercised over the bank's operations.

2.45 Internal Audit. Within BCRM the activities normally attributed to an internal audit office orunit are currently carried out by the Inspection Department. This includes routine verification and internalcontrol functions which are more properly handled by a separate accounts unit. The InspectionDepartment also carries out a variety of other activities (review of applications for the banking licenses,on-site and off-site inspection of financial institutions) which should now be the responsibility of CCBEF.Moreover, the Inspection Department is not directly responsible to the Board of Directors of BCRM anddoes not, therefore, enjoy the independence usually associated with the function of internal audit.

2.46 Information Technology. Information processing plays an important role in the day to dayoperations of BCRM, though a number of activities lack required computer support due to the scarcityof data processing resources. Likewise there is a need for more active general management participationin data processing planning and implementation. Furthermore, in a changing environment with aprogressive shift to using indirect instruments of monetary policy, the role of information technology willbecome increasingly important in attaining BCRM objectives. Strengthening strategic capacities in the areaof information technology is, therefore, a central part of BCRM development.

2.47 Information processing at BCRM today relies on an outdated mainframe computer system forwhich the supplier has discontinued maintenance. Although spare parts can still be procured from placesas far away as Europe, it often entails a wait of up to ten days. This constitutes a considerable operationalrisk for some of the basic data processing functions. High priority is, therefore, being accorded to movingthe most important systems, accounting and payroll, to other hardware. Despite the relatively highquality of BCRM computer staff, compared to that of other countries at a similar stage of development,the number of qualified systems analysts and programmers is limited. Significant emphasis on trainingprograms is required to meet the information technology skills requirements of BCRM.

2.48 Human Resources. While the quality of staff in BCRM is quite high on average, there appearsto be a lack of broad-based understanding of the functions of central banking. Most staff have onlylimited knowledge of the operations of departments other than the one in which they are working. Thereis virtually no systematic planning for staff rotation or long-term training. BCRM senior managementhave also expressed the need to review the present system of classifying personnel to improve incentivesand prospects for horizontal and vertical mobility. BCRM is examining the possibility of introducing ofoccupational streams (economists, financial analysts, etc.) to guide future recruitment, training, andpromotion.

(e) Recent BCRM Reforms

2.49 BCRM senior management and staff have generally been conscious of the problems and the needfor improvements within the institution. A number of steps have been recently initiated to strengthenBCRM capabilities to more effectively meet its responsibilities in an increasingly market-based economy.A major initiative is the revision of the 1973 Statutes of BCRM, which will give BCRM a clearer andmore independent role in both the formulation and execution of monetary policy. The Government hasadopted the ordinance setting forth the revised Statutes, which were agreed at negotiations, and thepromulgation of this ordinance is a condition of Credit effectiveness.

- 13 -

2.50 Furthermore, BCRM began preparing in August 1992 a strategic development plan (SDP) whichwill constitute a business plan for its organizational development over a 3 to 5 year period. The plan hasfour elements described below: (i) a statement of key policy and business objectives; (ii) action plans fordepartment strengthening and restructuring BCRM; (iii) more effective application of informationtechnology systems; and (iv) human resource development. The SDP represents the beginnings of astrategic planning and development function in BCRM. Although the SDP will remain a workingdocument to be continually reviewed, a first completed version of the text was adopted by the Board ofBCRM in April 1993 to commit the institution to a more strategic approach to its organizationaldevelopment. In addition, to help institutionalize this new function, a new position of Coordinator forStrategic Planning and Development has been created in BCRM. The coordinator is expected to help thesenior management of BCRM to more effectively plan and co-ordinate organizational changes and the useof information technology. BCRM will also form a steering committee comprised of senior BCRMmanagement and department managers to continually review the implementation of the SDP and approveorganizational and information technology plans. The steering committee will continually consult withoutside advisors on worldwide organizational practices in central banking.

2.51 Under its SDP, BCRM statement of objectives are categorized into 'business objectives" and'institutional objectives". The business objectives comprise: (a) price stability through the pursuit ofmonetary policy, eventually based on indirect instruments, and (b) legal, administrative and financialindependence of the Central Bank through the revision of its statutes and the removal of all quasi fiscalobligations. Institutional objectives include: (i) strengthening the budget and internal control functionswithin BCRM through improved accounting systems and procedures and their harmonization with a newchart of accounts for banks; (ii) development of an internal audit function; (iii) development of a fully-fledged research and statistics department; (iv) strengthening of capacities in foreign exchangemanagement, with the Central Bank ultimately playing a supervisory rather than a clearing role in theforeign exchange market; (v) strengthening capacity to implement monetary policy through indirectinstruments and, ultimately, open market operations; (vi) increasing capacities to monitor credit-worthiness of banks going hand in hand with the elimination of the review of individual bank loans forBCRM refinancing; (vii) enhancing domestic currency management by improving planning andcommunication capacities; (viii) development of modern information systems for the generation,processing, storage, transmission, and retrieval of operational and management information in alldepartments; and (ix) improvement of human resource functions especially in the areas of recruitment,training, and promotion.

D. CCBEF (Financial Supervisory Commission}

2.52 The Financial Supervisory Commission (CCBEF) was established under the April 1988 BankingAct governing the banking sector. CCBEF which is not a legal entity is chaired by the Governor of theCentral Bank. The primary roles of CCBEF are to monitor and safeguard the financial health of allfinancial sector institutions and to ensure that these institutions respect all laws and regulations governingtheir operations. CCBEF also has the power to issue regulations regarding the management, accountingand other technical practices of these institutions.

2.53 The development of CCBEF since its inception has, however, been stunted. Consequently, itspresent available capacity is inconsistent with the demands of full regulatory and supervision functionsof financial institutions in an environment of greater reliance on indirect controls in the conduct ofmonetary policy and increased competition among banks on both sides of their balance sheets. CCBEF

- 14 -

has lacked full-time trained staff and, until recently, had only one full-time professional, its SecretaryGeneral. Instead, it has relied on the staff of the Inspection Department of BCRM on an ad hoc basis,which has impeded effective financial sector supervision. The principal reasons for this are: (i) thecontinued reliance by BCRM on direct controls, entailing review of individual bank loans for refinancing,rather than ensuring financial institution health through supervision activities. The Credit Department ofBCRM has thus also assumed responsibilities for off-site surveillance, and remains a major force withinBCRM for directing credit, while the function of monitoring commercial bank risk has secondaryimportance; (ii) the lack of distinction between the roles of the Inspection Department in BCRM andCCBEF; and (iii) the absence of accounting and auditing standards, particularly for banks, which reflectinternational norms. Rationalization of BCRM and CCBEF roles in on- and off-site supervision isrequired, with primary responsibility for supervision belonging to CCBEF. A systematic program oftraining under a seasoned bank supervisor is envisaged to strengthen CCBEF supervision capacities.

E. The Commercial Banks

2.54 In 1975, Madagascar's banking system was nationalized and in 1977 the five nationalized bankswere restructured into three commercial banks with the intention of each specializing in a sector of theeconomy, i.e., agriculture (BTM), industry (BNI) and commerce (BFV). Credit increased rapidly from1975 to 1980 and witnessed more modest growth thereafter. In 1985, following the first steps ofstructural adjustment, there was a rapid deterioration of the commercial banks' overall loan portfolio,with 40 percent considered doubtful. In the 1986 - 1989 period, through a process of revaluation of fixedassets, commercial banks loan portfolios were significantly cleaned up, reducing doubtful loans to 15percent of gross loans by the end of 1989. In May 1988, a new Banking Act paved the way for theprivatization of the banking sector. In August 1989, a new commercial bank, BMOI, opened its doorswith two major foreign investors, BNPI and SFOM. In February 1991, Credit Lyonnais acquired themajority shareholding and took over the management of BNI (now known as BNI-Credit Lyonnais), andInstituto Bancario San Paolo di Torino (IBSP) acquired a 22 percent stake in BFV in March 1991.

2.55 As previously indicated in paragraph 2.17, despite the 1986 to 1989 portfolio clean up and theprivatization achievements, the banking sector again finds itself in crisis, because of renewed deteriorationin the portfolios of the two remaining state controlled banks, BTM and BFV. BTM profitability isdeclining while provisioning requirements for doubtful assets increase, making the prospects forimmediate privatization more remote. However, as of mid-1992 BTM began keeping within its creditceilings and has reduced its refinancing requirement, which is not the case of the BFV. The BFV hasconsistently failed to respect credit ceilings since the strike of 1991, and while the other three commercialbanks had excess liquidity in August 1992, BFV still had a net refinancing requirement with BCRM.Moreover, the 1991 accounts for this bank could not be certified and the loan portfolio has deterioratedsignificantly. The two private commercial banks by contrast appear to be in a sound financial situationdespite the numerous political and economic problems witnessed in the years 1991/92. More encouraging,a fifth commercial bank with Mauritian and South African investors has recently opened its doors inMadagascar, and a sixth bank is currently in the process of being granted its banking license.

F. The Insurance Sector

2.56 Madagascar's insurance industry, both non-life and life insurance, is in the early stages ofdevelopment. The ratio of gross insurance premiums to GDP (1987) was 0.05 percent, compared to that

- 15 -

in developed countries of 4.5 percent. There are two major insurance companies in Madagascar, AROand NY Havanana; these are joint-stock companies with majority interest held by the Government. Afurther two insurance companies are in quasi liquidation, and have no impact on the market. The natureof the industry is consequently highly oligopolistic, which includes provision for the sharing ofinformation and a non-competitive agreement between the two companies ensuring that one company willnot take a client from another. These barriers to competition have allowed these companies to dorelatively well even in harsh economic times, and as is the nature of the business they have accumulatedsubstantial reserves and thus are important investors. While strong arguments have been made to maintainthe duopolistic nature of the industry because of the small size of the market and the need to protectindividual savings, there is little rationale to defend continued government participation in theseindustries. The insurance sector could therefore have an important role to play in terms of both theprivatization process and the development of a securities market discussed in section J below.

G. The Social Security Fund

2.57 In Madagascar wage earners are covered by two systems of social security - a small governmentscheme for public sector employees through the Ministry of Finance and the social security fund, theCaisse Nationale de Prevoyance Sociale (CNAPS). CNAPS undertakes three social security functions,i.e., family benefits, workers' compensation, and retirement benefits. The fund, together with theinsurance companies, is one of the major mobilizers of term funds and an important institutional investorin Madagascar. However, its soundness as a financial institution has been under question. The WorldBank is financing under the APEX project a series of studies on CNAPS - a financial audit, anorganizational diagnosis, an actuarial study, and a study of investment policies - which are being executedsince October 1992 by the Social Security Department of the International Labor Organization (ILO).

H. Postal Financial Services

2.58 The Postal and Telecommunication Services (PTT) is made up of three entities, the Post Office,the postal checking institution (Comptes Cheques Postaux - CCP) and the postal savings institution, CEM.Although CEM was transformed into a savings bank in 1985 it continues to operate as a traditional postalsavings institution. It has a number of advantages in that, through the post office, it operates 220 windowsin 208 towns throughout Madagascar, with a high number of individual accounts. (e.g. every fourthresident of Antananarivo has an account). Its major weaknesses are: (a) its total dependence on theTreasury for financial management, which requires it to place all funds with the Treasury at below marketrates; and (b) the lack of financial transparency in the costing of services between the three PTT entities.In July 1992, the Government adopted a new policy for restructuring the post and telecommunicationssector. Besides proposing to commercialize the telecommunications entity, the new policy proposes toreorganize the Post Office and the two postal financial services as independent entities. A number ofproposals are currently being considered by the Minister of Post and Telecommunications to strengthenthe autonomy of postal financial services. One proposal is that the Post Office and the two postalfinancial services each be established as individual enterprises with independent boards which could inan initial phase be placed under a holding company. Subsequently, private capital should be allowed intoany one or all three of these entities. The Post Office should become a service provider on a fee basisto the new postal checking and postal savings entities and should structure contractual relationships forproviding services through its post office network to these entities.

- 16 -

I. The Payments System

2.59 The present system of effecting payments through financial instruments (checks, wire transfers,money orders, etc) is riddled with delays, risks and inefficiencies, particularly for out-of-towntransactions. Clearance and settlement of checks and transfers can in some instances take up to 90 days.Most of the delays are due to basic problems with road transport and inadequacies in the quality of publicnetwork telecommunications. The present institutional set-up includes 15 clearinghouses throughoutMadagascar for clearance of checks, in which all four banks, BCRM and the post office participate, andthe use of windows at about 220 post offices for payments through the postal checking system (CCP).Some improvements that have already been suggested to the Government are as follows: (i) introductionof a single clearing center in the capital for all out-of-town checks, to avoid the delays currently incurredthrough bilateral exchanges of checks among all 15 clearinghouses; (ii) development of either an expressmail system or a low-cost high-frequency radio network for data transmission, to expedite informationexchange; and (iii) introduction of new safety standards and procedures to allow clearing based onexchange of information rather than documents.

J. Financial Markets

2.60 In addition to the money markets described in para. 2.15, there is further potential for financialmarket deepening through the trade of equities and private debt instruments. One of the economic changesthat Madagascar is currently undergoing involves the privatization of state enterprises and thestrengthening and creation of private shareholding in a number of existing and new enterprises. Amechanism to facilitate the trading and transfer of equity would enhance this process of expanding privateownership. Analysis of the potential for a small securities exchange was undertaken in 1992 and it isenvisaged to be further developed in the near future, which will include the fiscal and legal changes thatwould be required to allow for an efficient system of share transfer. Furthermore public securitiescould also be traded in a secondary market, which could facilitate the reintroduction of BTAs (referredto in paragraph 2.23). Finally in the light of the weaknesses in the interbank market there is potentialto allow financial institutions (principally the banks and insurance institutions) to issue negotiablecertificates of deposit (NCDs). In broadening the market this would allow banks with excess liquidityanother form of investment apart from BCRM in which to place their surpluses, and provide alternativesources of refinancing (again apart from BCRM) for other financial institutions. All these aspects of thefinancial market require further analysis in preparation for regulatory and institutional reforms.

K. Accounting and Audit Framework

2.61 Accounting. Financial information in a concise and comparable form is not easily available inMadagascar. Outdated accounting principles continue to be applied by commercial banks, as Madagascarhas failed to revise its 1983 Bank Chart of Accounts or even ensure its universal application. This causesmajor problems in gaining an accurate interpretation of the financial position of banks and other financialinstitutions; specifically with regard to the provisioning of doubtful debts, income recognition, and theuse of suspense accounts. Therefore, difficulties are experienced in comparing the financial performanceof like organizations in Madagascar such as commercial banks. Consequently BCRM, concerned withinstitutional weaknesses and the veracity of financial information, has been reluctant to give up directmonetary controls. On the other hand, the implementation of indirect controls, such as reserverequirements, over the last two years has been accompanied by confusion on the part of the commercial

- 17 -

banks as to the exact nature of financial accounting required and the rationale behind BCRM demands.The lack of understanding on both sides has generally led to the implementation of an overly rigid systemwith penalties for reserves deficiencies that are unduly severe. This has neither inspired confidence inindirect controls nor in either BCRM or CCBEF capacity to effectively regulate the financial markets.

2.62 Although there have been some developments in accounting over recent years (the developmentof the 1987 General Chart of Accounts, PCGM-87, introduced with effect from January 1, 1989, and anew uniform chart of accounts for commercial banks, NPCB, for introduction with effect from January1st, 1994), two fundamental weaknesses in the accounting profession need to be addressed. These are(i) the limited number of professionally qualified accountants; and (ii) the lack of a regulatory frameworkto stimulate the development of a national accounting profession with standards and ethics at par withlevels accepted internationally. The absence of a suitable regulatory framework has been at the core ofthe problem although a professional body has been in existence since 1962. The IDA financed Accountingand Audit Organization and Management Training Project (Cr. 1 155-MAG), sought to establish legislativeand training requirements for the accounting profession and financed the National Institute for AccountingScience and Enterprise Administration (Institut National des Sciences Comptables et de l'Administrationdes Entreprises (INSCAE). INSCAE ongoing activities and development are currently being supportedunder the ongoing Accounting and Management Training Project (Cr. 1661-MAG). However, INSCAEis currently able to train to the level of accounting technician only.

2.63 Under new legislation governing the accounting and audit profession, a student who hassuccessfully completed the INSCAE program or who has obtained an equivalent diploma, can take examsfor admission as a trainee for the qualification of ExDert Comptable et Financier, as defined by this newlegislation, and thus become a fully fledged member of this professional body. Furthermore, there area number of transitory measures which will expand the admission to the profession of other practitioners,provided they can demonstrate an acceptable level of expertise. This new regulatory framework is a keytool in the development of the profession and in the introduction of accounting and auditing standardsacceptable internationally. The new legislation does, however, have fundamental flaws in that foreignaccounting and audit firms are discriminated against, and certain anomalies need to be resolved tofacilitate the development of international accounting standards. Allowing foreign nationals with theappropriate qualifications to compete freely with national firms in the local market is important instimulating future development in the profession.