FILE COPY DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use Report No. 259a-IRN APPRAISAL OF THE INDUSTRIAL AND MINING DEVELOPMENT BANK OF IRAN January 15, 1974 This report was prepared for officialuse only by the Bank Group. It may not be published, quoted or cited without BankGroup authorization. The Bank Group does not accept responsibilityfor the accuracyor completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

FILE COPY

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENTINTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

Report No. 259a-IRN

APPRAISAL OF

THE INDUSTRIAL AND MINING DEVELOPMENT BANK OF

IRAN

January 15, 1974

This report was prepared for official use only by the Bank Group. It may not be published, quotedor cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit = Iranian Rial

Up t6 Feb. 18, 1973 : US$1 = Rials 76.5

1 Rial = US$0.01307

1 million Rials = US$13,070

After Feb. 18, 1973 : uts1 = Rials 68.85

1 Rial = US$0.01452

1 million zlals US$14,520

From June 9, 1973, the Bank Melli Iran's selling rate for U.S. dollarshas been Rials 67.75 per US$1.

Note

1) The Iranian year runs from March 21 - March 20. FY71 is theyear March 21, 1970 - March 20, 1971. The Iranian year 13h9is the Gregorian year March 21, 1970 - March 20, 1971.

2) The Fourth Five Year Plan covers the period March 1968 - M4arch 1973The Fifth Five Year Plan covers the period March 1973 - March 1978

This report was prepared by Messrs. Bernardus H. PottkerHenry B. Thomas and George C. Maniatis, following their visitto Iran, July 7 - 18, 1973.

APPRAISAL OF

THE INDUSTRIAL AND MINING DEVELOPMENT BANK OF IRAN

TABLE OF CONTENTS

Page No.

BASIC DATA ........................... a-b

SIh?ARY .................................... i-i

I. INTRODUCTION .........................

II. THE ENVIRONMENT .................... * 1

Industrial Development ........ ...................... . 1Industrial Finance and the Role of IMDBI ...... .. ...... 3Character and Development Impact of IMDBI's Operations 4

III. INDBI'S ORGANIZATION, PROCEDURES AND RESOURCES ....... 7

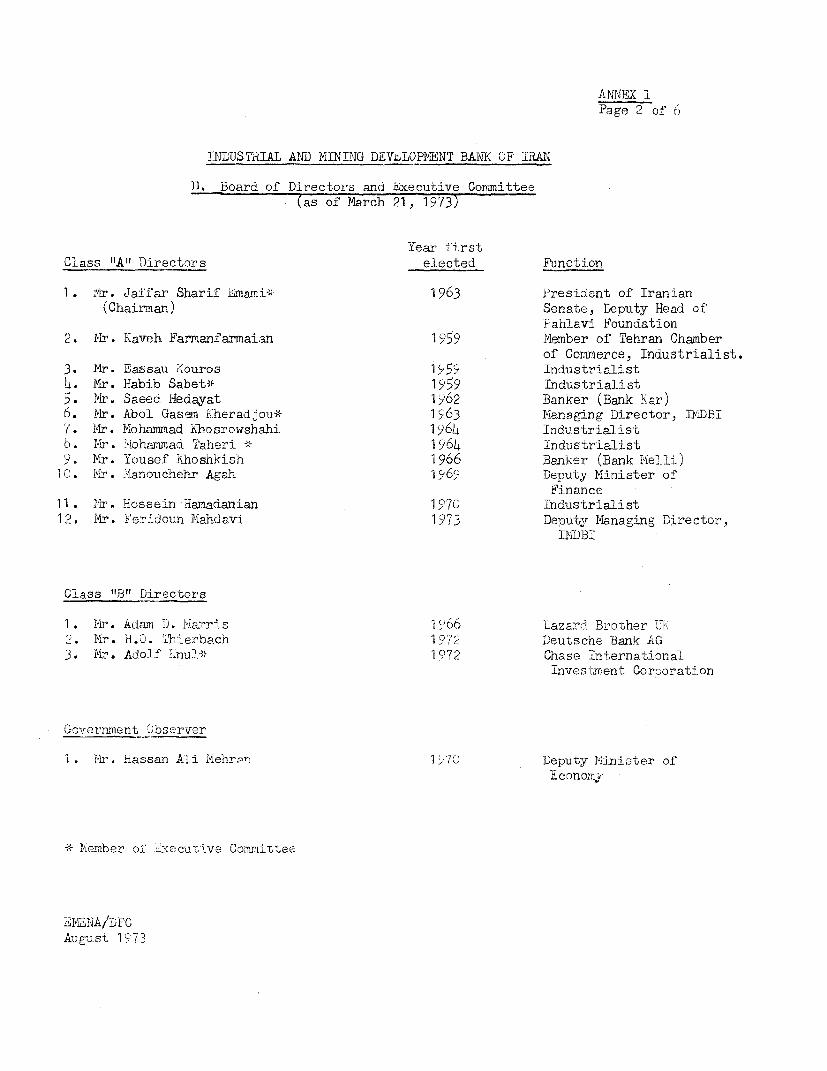

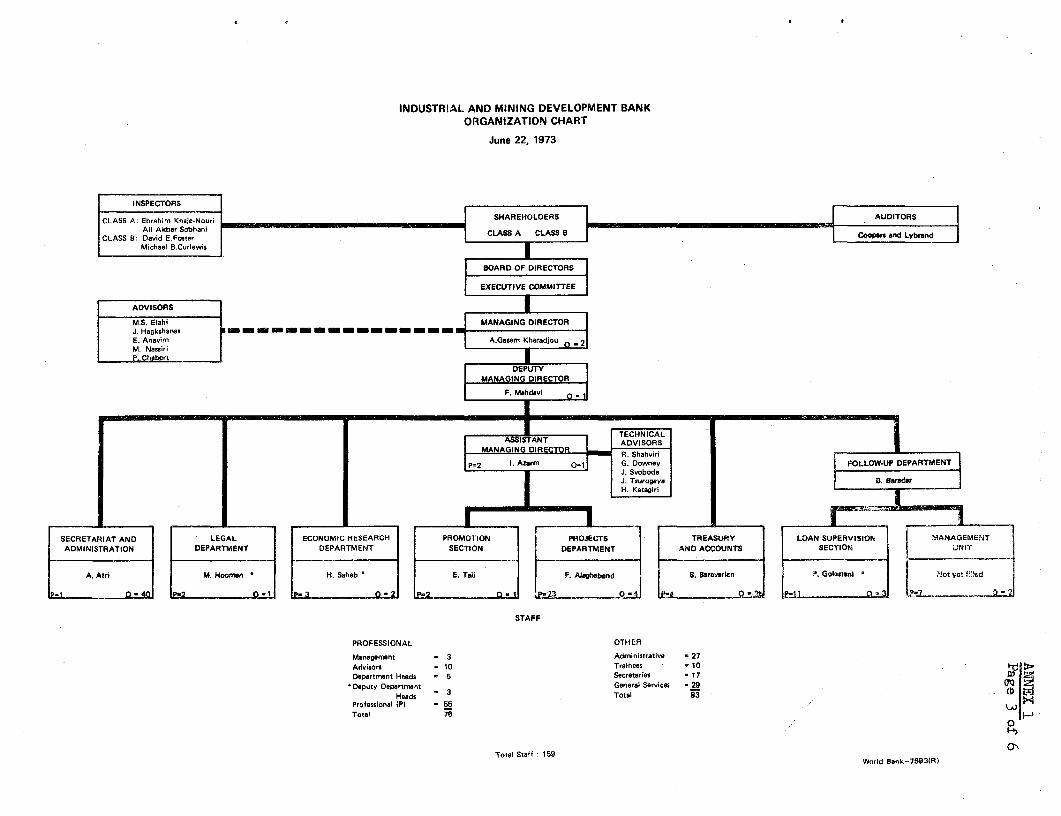

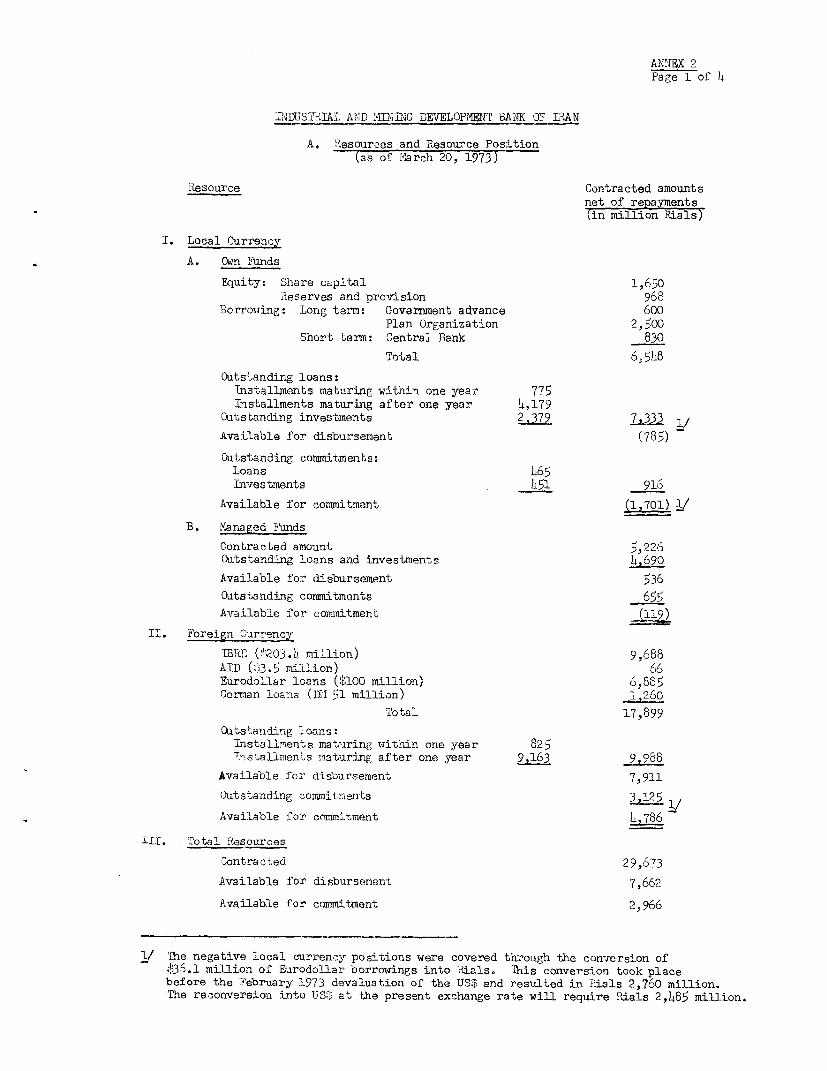

1. A. List of ShareholdersB. Board of Directors and Executive CommitteeC. Organization ChartD. Notes on Shareholders, Board of Directors and Organization

2. A. Resources and Resource PositionB. Note on Resources

3. Summary of Loan Agreements with Foreign Banks and Institutions

4. Policy Statement

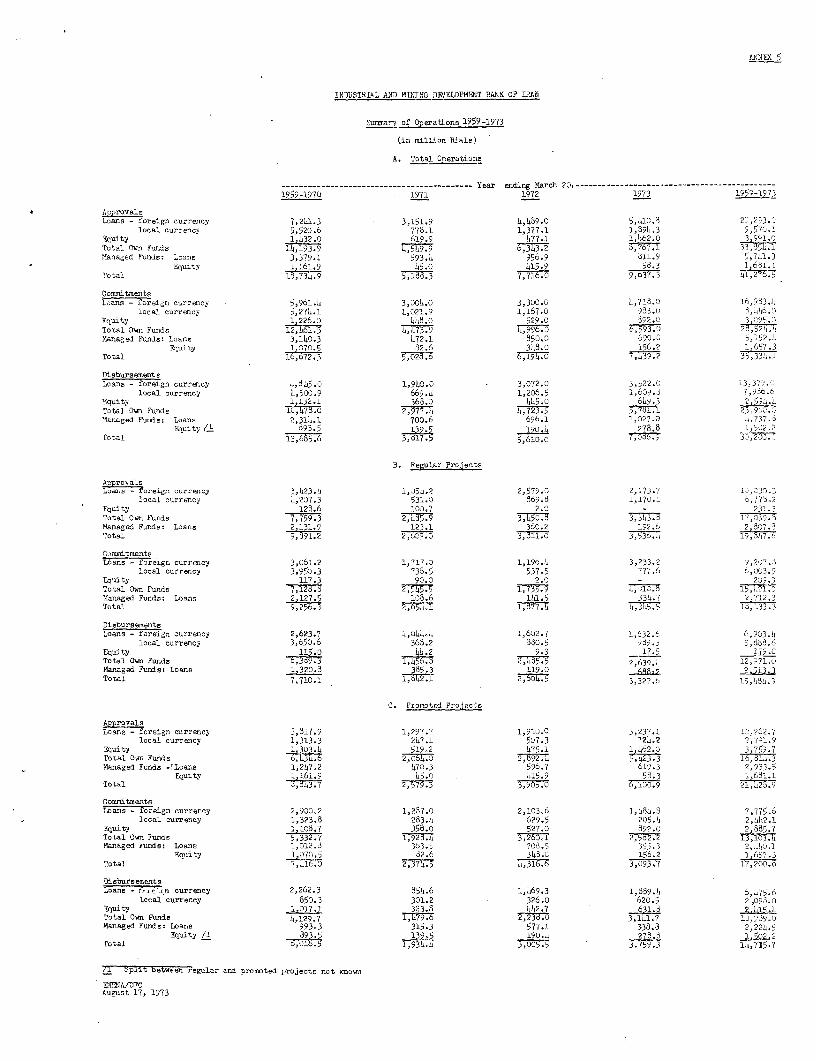

5. Summary of Operations, 1959 - 1973

6. Comparative Statement of Loans Signed, 1959 - 1971

7. Equity Portfolio as of March 20, 1973

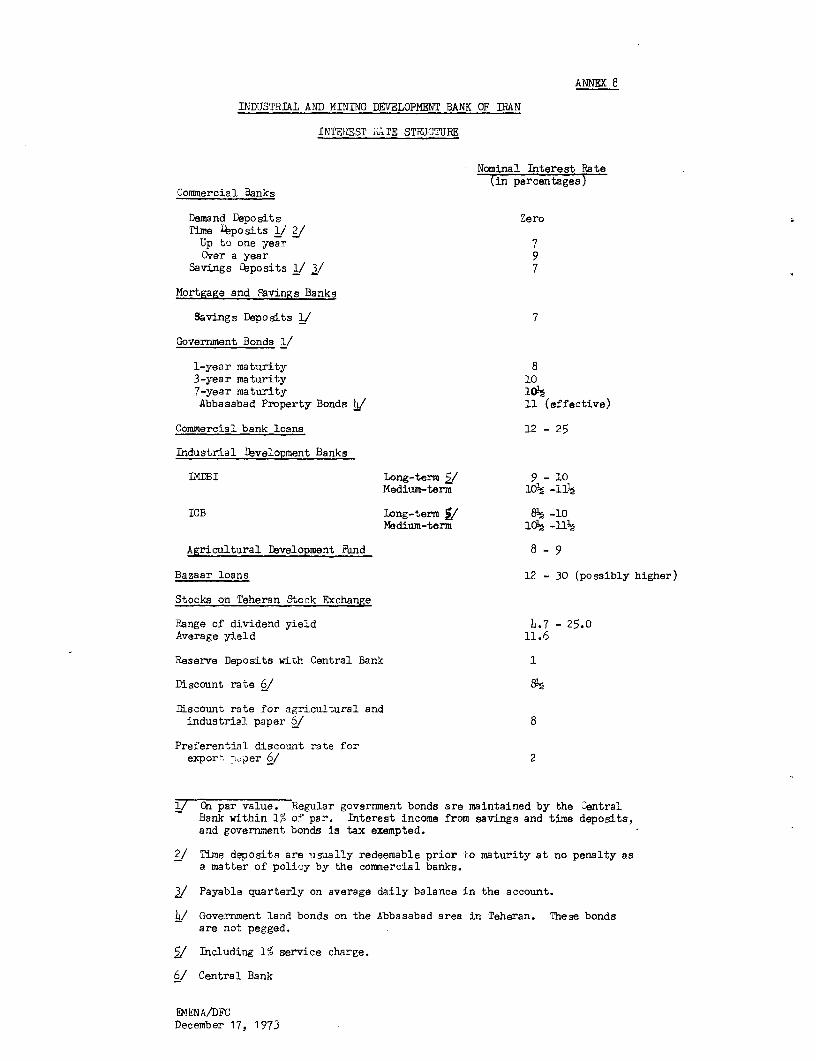

8. Interest Rate Structure

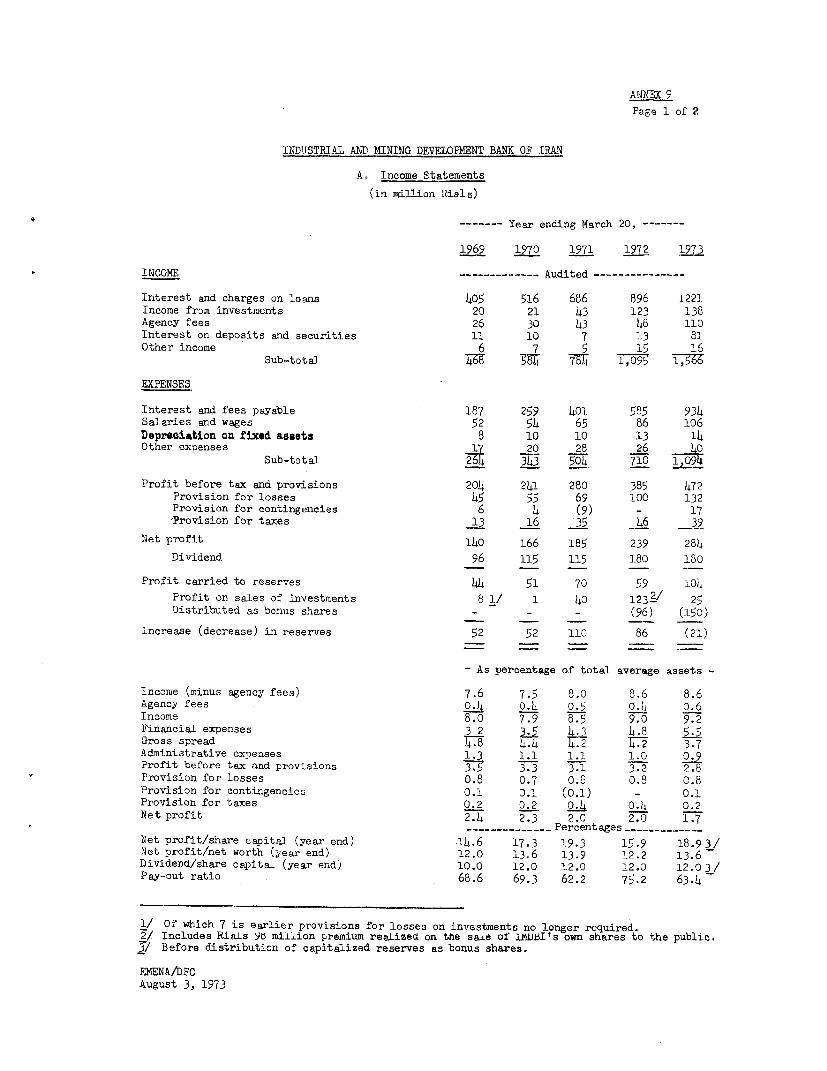

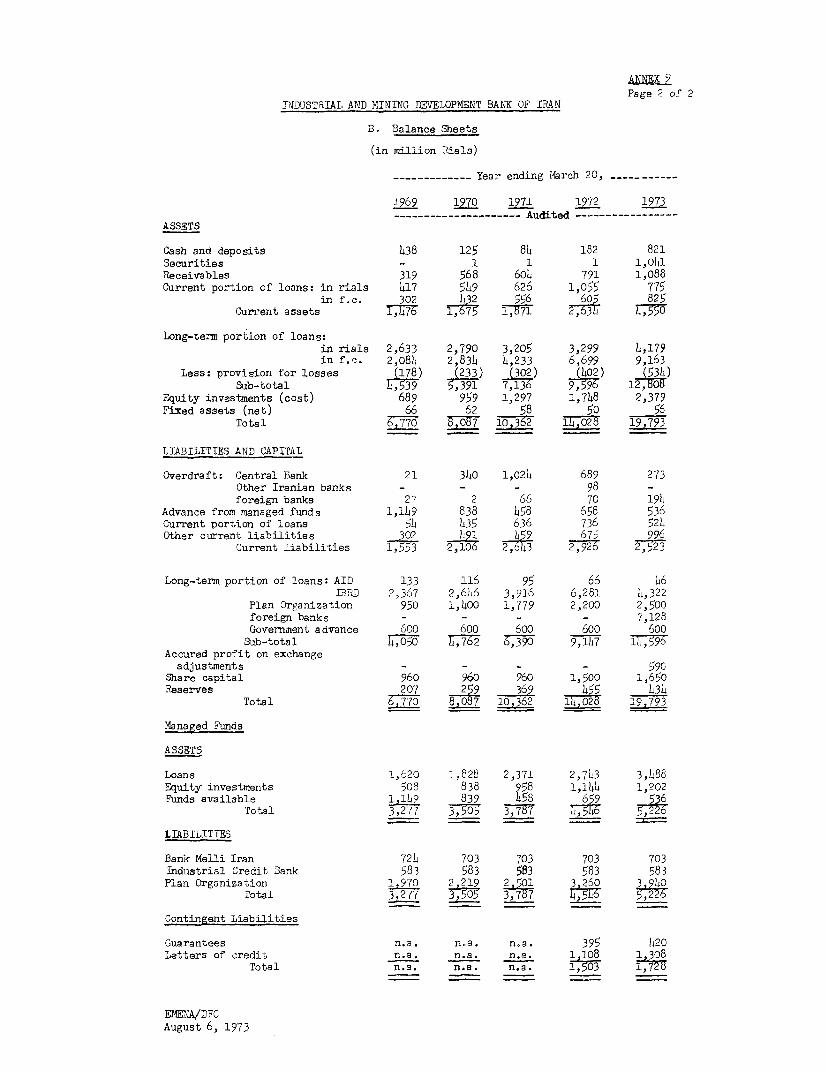

9. A. Income Statements, FY69-73B. Balance Sheets, FY69-73

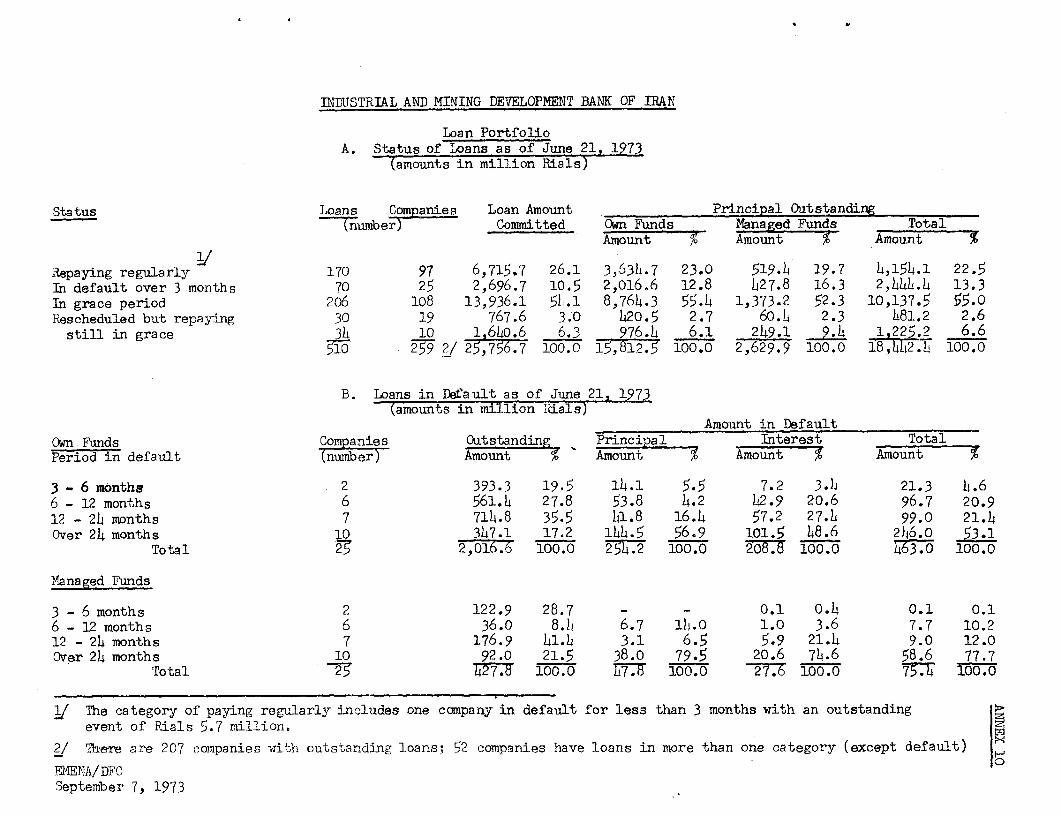

10. Loan Portfolio

A. Status of Loans as of June 21, 1973B. Loans in Default as of June 21, 1973

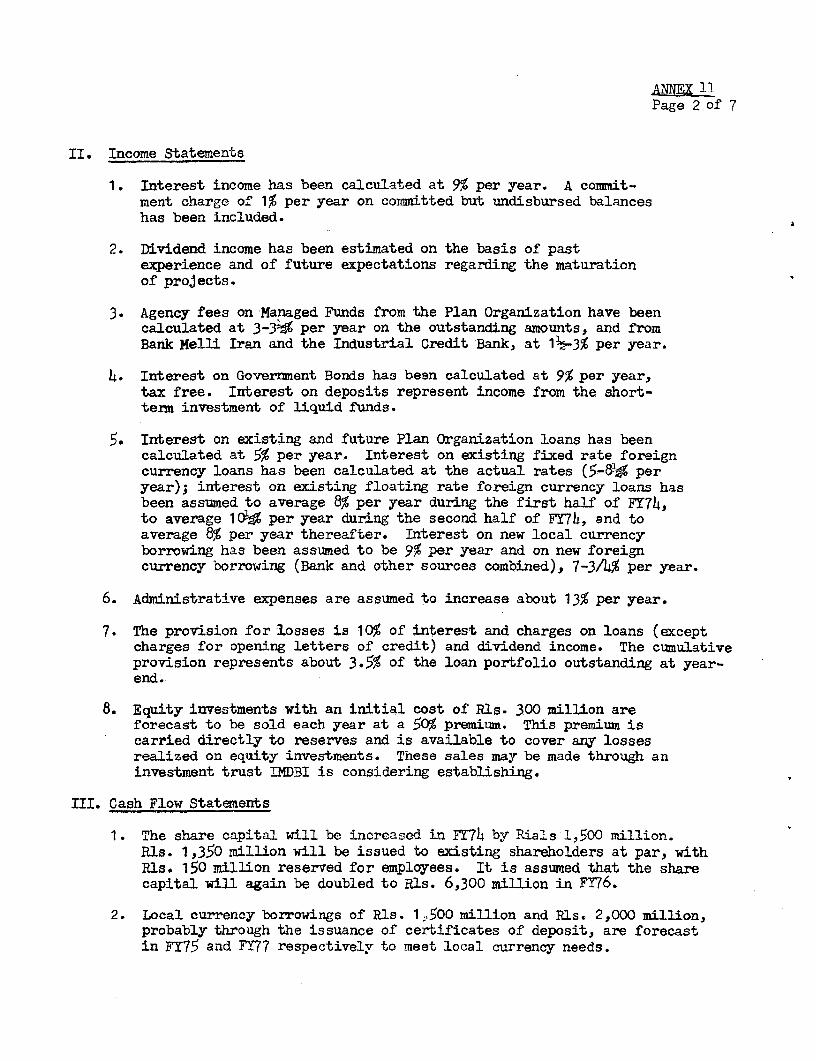

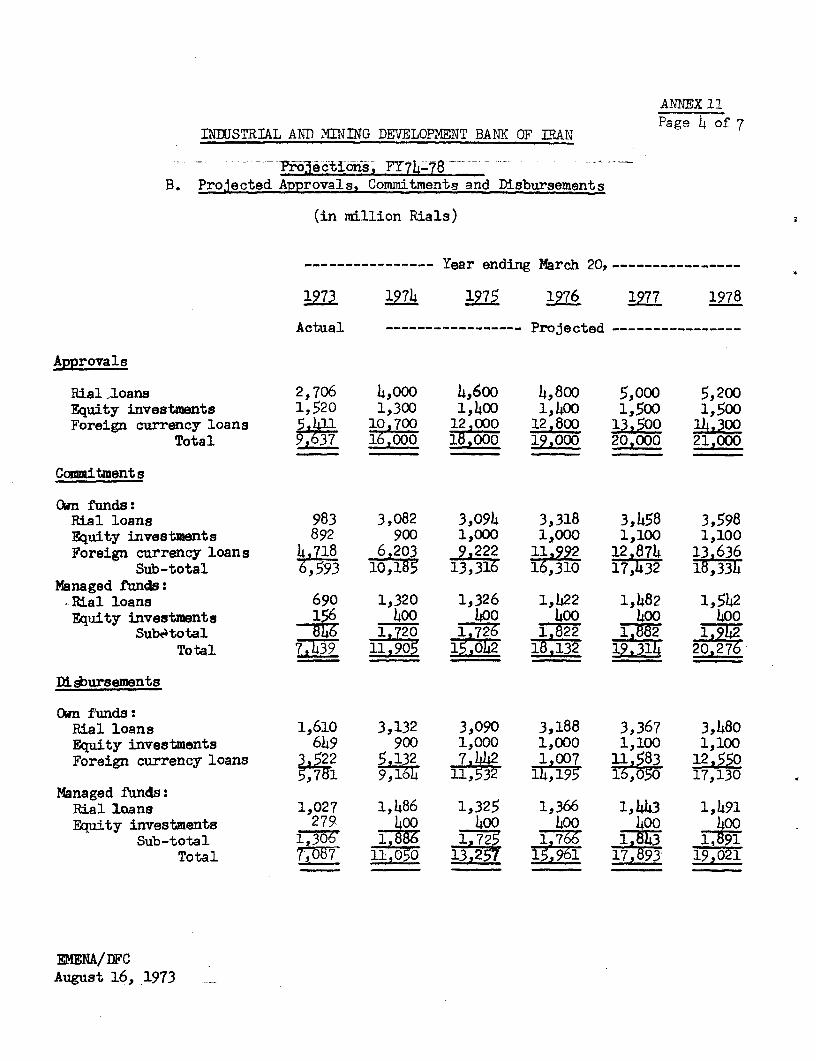

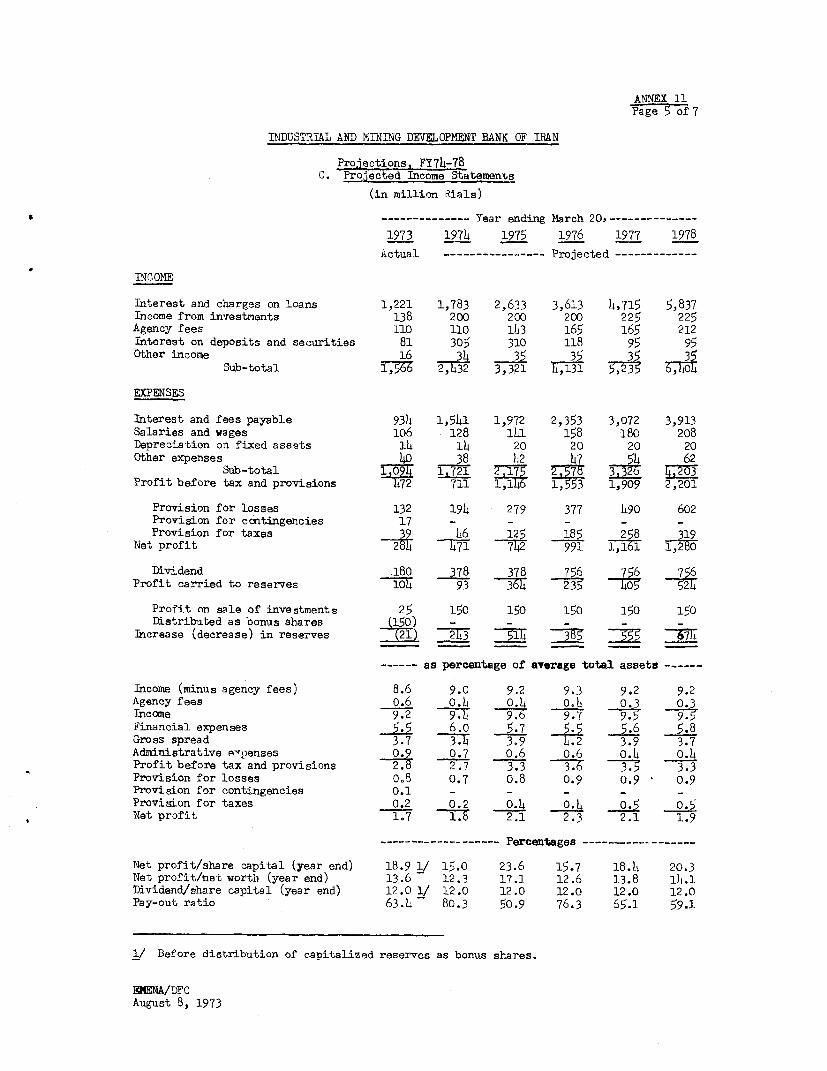

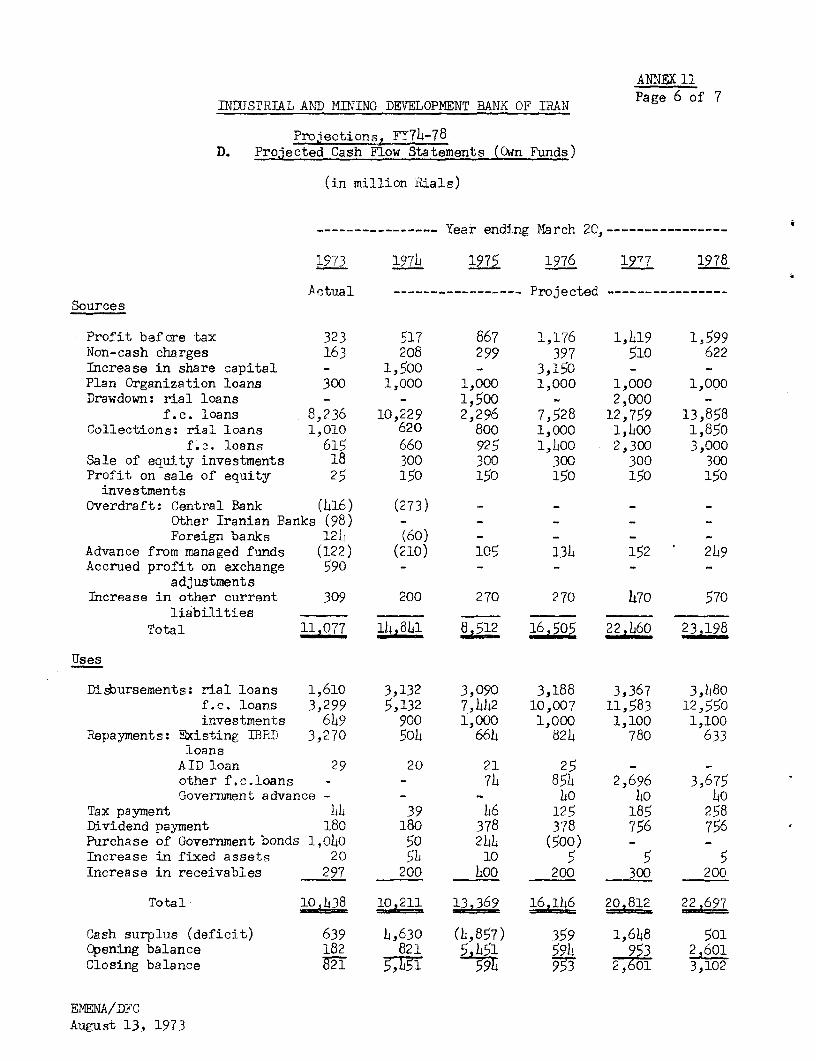

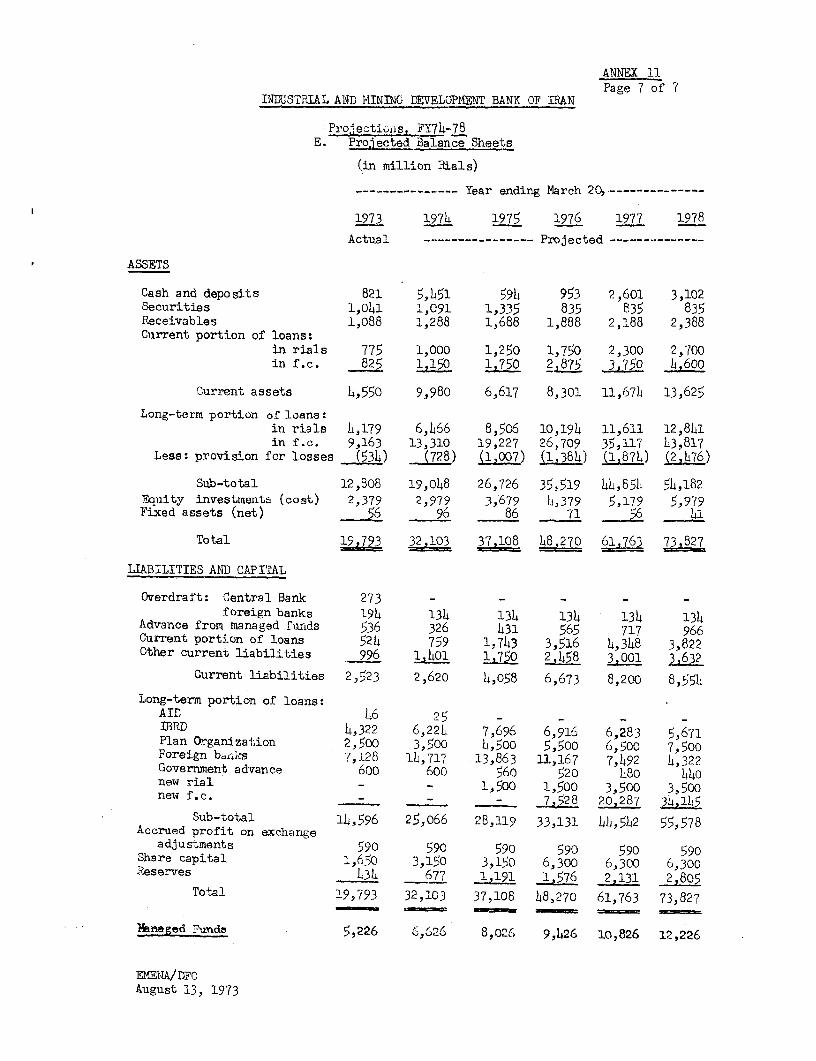

11. Projections, FY74-78

A. Major Assumptions Underlying the ProjectionsB. Projected Approvals, Commitments and DisbursementsC. Projected Income StatementsD. Projected Cash Flow Statements (Own Funds)E. Projected Balance Sheets

12. Projected Disbursement Schedule.

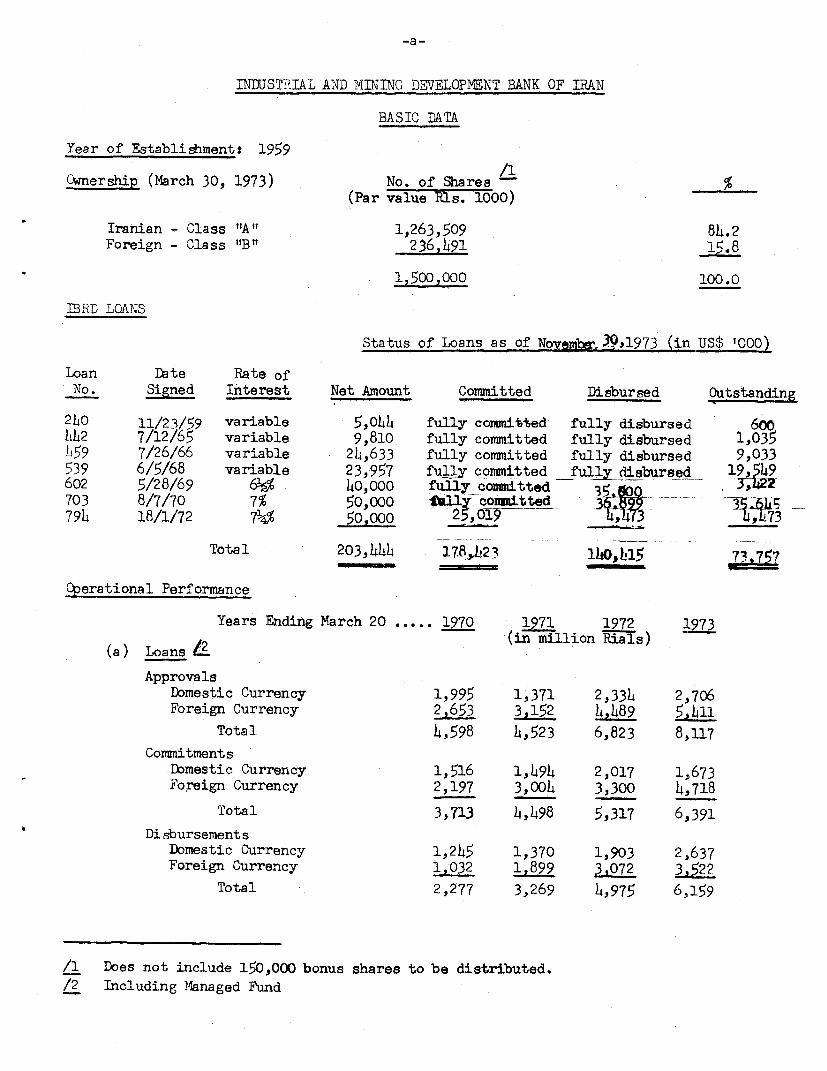

-a-

INDUSTRIAL AND MINING DEELOPENT BANK OF IRAN

BASIC DATA

Year of Establishment: 1959

Ownership (March 30, 1973) No. of Shares -L %(Par value Rls. 1000)

Iranian - Class "A" 1,263,509 84.2Foreign - Class "'B" 236,491 15.8

1,500,000 100 .0

BRD LOANS

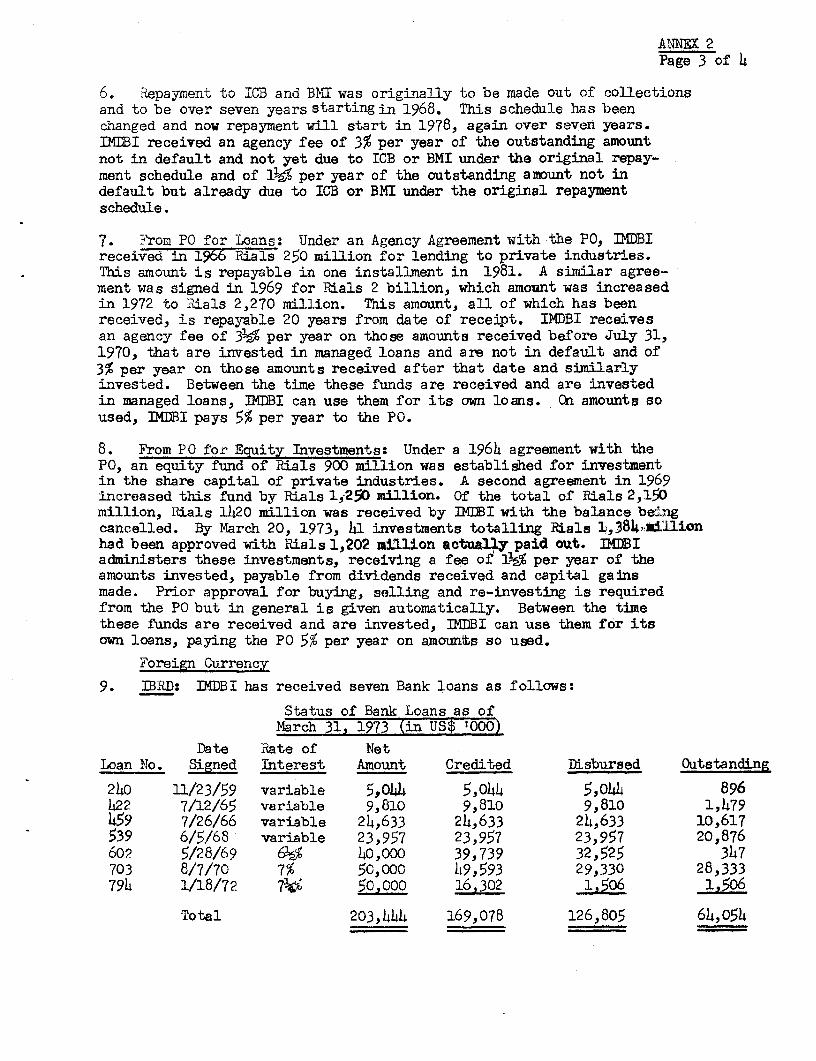

Status of Loans as of Noy 3mbr39,1973 (in US$ 0CO0)

Loan Date Rate ofNo. Signed Interest Net Amount Committed Disbursed Outstanding

Years Ending March 20 ..... 1970 1971 1972 1973(in million Ral s)

(a) Total assets 8,087 10,362 14,028 19,793of which loan portfolio (6,065) (8,620) (11,658) (14,942)

equity portfolio (959) (1,297) (1,748) (2,379)Net worth plus provisions 1,1452 1,631 2,357 2,618Long-term debt 5,197 7,026 9,883 15,120of which Government (2,000) (2,379) (2,820) (3,100)

IBRD (3,064) (4,531) (6,988) (4,826)

(b) Long-term debt/equity (times) 3.6 4.3 4.2 5.8Profits before tax and provisions

as % of average total assets 3.3 3.1 3.2 2.8Net profits as % of year endnet worth 13.6 13.9 12.2 13.6

Cost of term-debt as % of average 5term-debt outstanding 5.6 6.6 6.9 7.5

Reserves and provisions as % ofyear-end loan portfolio 7.4 7.8 7.4 6.5

(c) Book value as % of par value 151.3 169.9 157.1 174.5 /2Dividend as % of par value 12.0 12.0 12.0 12.0 /2Dividend pay-out ratio 6903 62.2 75.2 63.4,hare quotation (in Rials) 1,230 lj,460 1,500 1,740

/1 Excluding Managed Funds/2 Before distribution of 150,000 bons shares.

EMENA/DFCAugust 17, 1973

APPRAISAL OF

THE INDUSTRIAL AND MINING DEVELOPMENT BANK OF IRAN

SUMMARY

i. The Industrial and Mining Development Bank of Iran (IMDBI) has re-ceived seven loans from the Bank totalling $203.4 million. Commitment of thelast loan, granted in January 1972, was temporarily slowed during the unset-tled monetary situation earlier in 1973. Commitments have since picked upand the loan is expected to be fully committed early in 1974. IMDBI isnow seeking another loan from the Bank.

ii. The Iranian economy is growing at an impressive pace, with indus-try playing a leading role. For some years Iran has aimed at creating an in-dustrial sector, based on modern technology, that would ultimately be compe-titive internationally and would provide increasing employment. The shareof manufacturing aiid mining in non-oil GDP has risen from 13% in 1960 to 19%in 1970 while exports of non-traditional manufactures grew at a 42% annualrate from FY68 to FY73, amounting to $100 million or 22% of the total exports(excluding oil) in the latter year.

iii. IMDBI and the Industrial Credit Bank (ICB) remain the major Iraniansources of long-term institutional finance for industry. While IMDBI has con-centrated on the larger scale, modern manufacturing sector, ICB has cateredto the smaller, more traditional enterprises. The local capital market isstill underdeveloped with a scarcity of public companies whose shares arelisted. This situation is changing, however. Turnover of securities ismainly in Government bonds which have a privileged position in the market.The Government's public debt and interest rate policies continue to affectthe market for fixed interest securities, making it nearly impossible forprivate entrepreneurs or institutions to borrow long-term directly.

iv. IMDBI has been a dynamic institution, actively participating inseeking out industrial projects. Its projects show in the main a satisfac-tory economic rate of return and have provided employment to 45,000 workersin the period 1968-1972. Their export performance is good and the exportpotential is increasing. Besides assisting established industrialists andnew entrepreneurs, an important feature of IMDBI's operation is to promoteprojects on its own. IMDBI's high level of activity reflects Iran's economicgrowth; over half of its financial assistance has been approved in the lastthree years of its 15 year existence.

v. Financing IMDBI's increasing level of activity has been a challenge.Unable to raise local currency resources on the local market, IMDBI has reliedon loans from the Government and successive increases in its share capital.Until 1972, IMDBI's foreign exchange resources came almost exclusively fromthe Bank. During 1972 and early 1973, however, IMDBI was able to raise sub-stantial sums in Europe, with the result that at the end of FY73 Bank fundsrepresented only some 55% of total foreign currency resources. This develop-ment had the Bank's encouragement. IMDBI anticipates relying even less inthe future on the Bank for funds, and hopes to be able to raise some limitedamounts on the local market.

- il -

vi. Though recent foreign borrowings have dramatically eased IMDBI'sliquidity problem, they have raised a new problem; DMDBI now has a foreignexchange exposure. Because of IMDBI's maturity and strong financial position,some such exposure is acceptable. An arrangement has been worked out forIMDBI to set up specific provisions and to establish appropriate risk para-meters depending on the level of provisions and the number of currencies inwhich IMDBI is exposed.

vii. IMDBI has enjoyed continued stability of top management. IMDBI'sinternal organization is relatively informal, giving it flexibility to ab-sorb new staff as well as additional business. Its appraisal of projectsremains of good quality, but there are some problems which still need to beworked out. These are especially related to appraising economic aspects.IMDBI's supervision work has improved considerably since the Bank's lastappraisal, though there remains room for improvement.

viii. IMDBI remains financially sound and profitable. Its loan portfoliois of good quality with the arrears situation showing distinct improvementover the past two years. Its equity portfolio is gradually maturing, provid-ing IMDBI with a 9.5% return during FY73.

ix. IMDBI is a very competent institution, though it still has someflaws caused essentially by its rapid growth. It should be capable of deal-ing with these problems. IMDBI deserves continued Bank support even on alarge scale to move it nearer to achieving Independence from Bank financing,a stage which it should be able to achieve In the 1970s.

x. The prospects for the economy and IDBI 's business are good. Com-mitments from own funds are forecast to total Rials 10.2 billion ($148 mil-lion) in FY74, a 54% increase over FY73. This forecast is based on the levelof business already achieved during the first part of the year and on the pipe-line of projects under study, and is considered reasonable if not conservative.Commitments in the following four years are forecast to increase by an annualaverage of about 16%. Foreign exchange commitments through the end of FY76are projected to total some $400 million. Existing resources at the beginningof FY74 and foreign borrowings already arranged during the year total $166million, leaving a gap of $234 million. A Bank loan of $75 million is recom-mended to fill part of this gap. The loan would be made on the normal con-ditions of Bank loans made to dfcs except that the loan should have a fixedamortization schedule. It is also recommended that only those projects whichneed more than $4 million of IMDBI's resources, including Bank loan funds,should require the approval of the Bank.

APPRAISAL OF

THE INDUSTRIAL AND MINING DEVELOPMENT BANK OF IRAN

I. INTRODUCTION

1.01 Since its establishment in 1959 the Industrial and Mining DevelopmentBank of Iran (IMDBI) has received seven loans from the Bank, totalling $203.4million net of cancellations. IMDBI has approached the Bank for an eighthloan. This report appraises IMDBI in connection with this request and recom-mends that a loan in the amount of $75 million be extended.

1.02 The report focuses on IMDBI's overall performance and its role inthe industrial development of Iran since the last Bank appraisal of IMDBI(DB-82a dated December 2, 1971). Information on industry is contained in thereport "Industrial Policies and Priorities in Iran" (SA-27a dated March 1,1972), while the "Memorandum on Current Economic Developments in Iran" (Re-port No. 49a-IRN dated March 14, 1973) updates the report entitled "CurrentEconomic Prospects of Iran" (SA-23a dated May 18, 1971). This report incor-porates the findings of these reports as appropriate.

II. THE ENVIRONMENT

Industrial Development

2.01 During the 1960s the Government made a major effort to acceleratethe pace of industrialization and to diversify the Iranian economy. The mainobjective of the official policy has been to create an industrial sector,based on modern technology, that would ultimately be competitive internation-ally, and would provide employment to an increasing part of the population.Private initiative was encouraged to engage in import substitution by meansof high protection (high tariffs and quantitative restrictions) and generousincentives (duty free import of capital goods and tax concessions). Thispolicy succeeded in stimulating investment in the consumer goods and in someproducer goods industries. The favorable investment climate led also to aconsiderable growth of direct foreign investment. Manufacturing (includingmining) grew at 12% in real terms annually during the 1960s, while its sharein non-oil GDP rose from 13% in 1960 to 19% in 1970. There has also been asignificant increase in efficiency, particularly of the large and modern in-dustrial firms; this contributed to the rapid increase in value added in in-dustry in more recent years (14% per annum during the Fourth Plan).

2.02 The Government's industrialization strategy for the 19708 is inline with the Bank's views. It tries to cope with the existing frictionsand problems in the industrial sector. It mainly emphasizes further in-creases in efficiency; promotion of intermediate and capital goods and export-oriented industries; minimum economic size and competitiveness of the newplants; progressive decentralization of industry away from the Tehran area;greater attention to small and medium size industry; transfer of certain

-2-

State-owned enterprises to private hands; and the broadening of the owner-ship base through the sale of shares of industrial enterprises to workersand the public at large. Several policy tools are being employed which arediscussed below.

2.03 By using the import licensing and duty systems more flexibly, theGovernment expects to increase efficiency and keep domestic prices competitivewith international prices. Protection on most products has already been sub-stantially reduced, helped by price increases abroad. The industrial licensingsystem has recently been liberalized for certain industries and is now mainlyused as a tool to influence location and economic size of production. A moveis afoot not to allow, on a selective basis, imports of capital goods whoselocal production the Government is willing to stimulate because the rapidgrowth of the domestic market makes the establishment of economically viableunits increasingly feasible in Iran. Since 1970 there has been a new packageof export incentives. Foreign firms establishing a plant in Iran are in mostcases obligated to export. These measures have begun to bear fruit: exportsof non-traditional manufactures grew at 42% annually during the Fourth Plan,totalling $100 million in FY73 or 22% of total non-oil exports - against $25million and 11% in FY69.

2.04 A value added ratio of at least 35% has been laid down as a pre-condition for a license to set up a new plant, though there are exceptions.To disperse industry, plants are not allowed to locate within a 120 kilometerradius of Tehran. The expansion of existing industries near Tehran is alsolimited and tax exemptions are used to influence the location of industry.

2.05 Until recently the Government has neglected small and medium sizeindustry. Incentives were generally not available to the smaller entrepreneurs.Neither were the development banks equipped to cater to this segment or willingto pay it attention. This situation is changing. The Government is now moreaware of the importance of small-scale industry. During the Fifth Plan aboutUS$160 million will be allocated from the Government budget for lending tosmaller entrepreneurs.

2.06 Ownership of large-scale industry is still mainly controlled byfamily groups. In Iranian circumstances this could create social friction;it may also affect the development of the capital market. In order to broadencompany ownership the Government has devised a scheme whereby workers and thepublic at large can participate up to 49% in the larger industrial enterprises.Tax and other incentives are offered to convert family-controlled firms intopublic companies. Already 85 companies are earmarked to become public in thenext two years; 15 companies 1/ have actually done so, including nine projectspromoted by IMDBI.

1/ These companies enabled their workers to take interest-free loans of upto a year's salary and repayable over five years to buy shares. Thescheme complements the benefits of the Profit Sharing Act of 1964, whichallocated 20% of profits to the employees.

-3-

Industrial Finance and the Role of IMDBI

2.07 The major sources of long-term institutional finance for industryremain IMDBI and ICB 1/, providing roughly 15% and 4% respectively of thetotal financial requirements for private, fixed capital formation in industryand mining. Sponsors typically supply another 40%, suppliers' credits andother foreign funds 25%, while the remainder comes from commercial banks,the bazaar and other institutions. In effect, because IMDBI and ICB provideon average about one-third of the overall capital requirements of the projectsthey finance, they are involved in about 50% and 10% respectively of allprivate industrial and mining projects. Whereas IMDBI has concentrated onthe larger scale, modern manufacturing sector, ICB caters to the somewhatsmaller scale, more traditional industries, which are generally more labor-intensive and resource-based. Yet over 50% of ICB's resources have beenallocated to relatively large enterprises 2/ and up to 1971 long-term loancommitments and equity investments amounted to only about Rials 1 billion ayear. Some long-term credit from commercial banks, particularly Bank Melli,is also available but this is usually granted in the form of highly collater-ized roll-over credits.

2.08 The market for equities and fixed interest securities is very thin.The Tehran Stock Exchange, sponsored by IMDBI, was established in 1968 andis still in its infancy, mainly because of widespread aversion to breakingup family control of companies. However, last year's turnover equalled thatof all the preceding years put together. Some 25 industrial and banking en-terprises are listed and the annual turnover in 1972 amounted to about US$17million, of which US$13 million were in Government bonds. When the afore-mentioned 85 companies have become public, the Exchange's role of mobilizingresources is expected to increase.

2.09 IMDBI has a keen interest in a more developed capital market spe-cifically because the majority of its promoted projects are included in the85 companies and generally because there would be a better opportunity toroll-over IMDBI's investments. Besides selling directly to the market IMDBIhas plans to promote an Investment Trust to which it could sell part of itsequity portfolio. The Trust (which would be a closed-end Mutual Fund) wouldenable the small investor to participate in the ownership of a larger numberof companies. IMDBI is also planning to promote a Securities Firm/BrokerageHouse. These are good initiatives as long as fMDBI takes only a minorityshareholding and does not get unduly involved in the ventures' management andpolicy making. Potential conflicts of interest also need to be guarded against.

2.10 The pre-emption of the bond market by the Government for many yearsmakes domestic borrowing virtually impossible even by such well establishedinstitutions as IMDBI. Government bonds were issued at 9% tax free, whichraised their effective yield to 12-13% per annum. Since the ceiling on banks'long-term lending rates was set by the Government at 9%, there was clearly a

1/ The Industrial Credit Bank (ICB) is a state-owned entity. A proposedBank loan to ICB is under consideration.

2/ Enterprises with fixed assets exceeding $1.5 million.

-4-

disincentive to IMDBI, or to any other institution for that matter, to issuebonds. In September 1973'the Government increased the Central Bank rate to8-1/2% and the interest rate on Government bonds to 10-1/2%. At the sametime IMDBI was allowed to increase its effective lending rate to 10%. Theseincreases are a reaction to inflationary pressures and are intended to bringdomestic rates more in line with interest rates abroad. But they will notsolve the problem for IMDBI arising from Iran's interest rate structure.Up to now interest rates have not played an important function in Iran inallocating resources. Rather, this role was performed by licensing, taxbenefits and access to low cost public utilities. However, with the increasedsophistication of the economy and the increasing freedom of the private sector,the capital market should become a more important instrument for allocatingand mobilizing resources.

2.11 Largely because commercial banks are inexperienced with industrialfinance - they traditionally finance trade - there has been for some time anacute shortage of short- and medium-term capital in industry despite rapidincreases in bank deposits. To meet the growing demand, four new banks wereestablished in the last year. IMDBI participates for 10% in the share cap-ital of two, while ICB participates in another for 5%. All four banks haveoffered a significant share of their initial capital to the public whichresponded enthusiastically. The banks are commercial banks though their mainfunction will be to satisfy the working capital needs of industrial enterprisesand the demand for consumer credit. They currently charge 10-112, which islower than the effective lending rates of many commercial banks. They expectthat higher efficiency and a smaller spread between borrowing and lendingshould make this lower rate possible. The situation is new. There are goodelements but there is the potential of overbanking. 1/

2.12 A new development bank, the Development and Investment Bank of Iran(DIBI), has just been established. It will specialize in long-term lending,equity investment and underwriting. Its share capital is Rials 2.1 billion;20% was subscribed by the public, 20% by foreign interests and the remainderby various industrial groups. DIBI will provide an alternative source oflong-term funds and will be competing with IMDBI. Given the level of invest-ments in private industry, the size of some projects which clearly exceedthe financial capacity of a single institution, and the virtually monopolisticposition of IMDBI, the entrance of DIBI into the market seems like a good de-velopment.

Character and Development Impact of IMDBI's Operations

2.13 In the last 10 years IMDBI made investments amounting to Rials 120billion, to which IMDBI itself contributed Rials 41 billion. IMDBI's devel-opment effort has been constantly directed to providing a modern industrial

1/ Not long ago, the Iran (Overseas) Investment Bank was established inLondon, sponsored by IMDBI, Bank Melli and eight other banks in Europe,the USA and Japan. Its main function will be to act as an agent forthe arrangement of loan syndicates for the Iranian Government and pub-lic and private corporations, including IMDBI itself.

-5-

base for Iran. This effort has found its main shape in IMDBI's promotionalwork. Beginning in the early 1960s IMDBI started to promote new projects inan environment which had little industrial tradition and industrial managementexperience. Although Government policies favored industrial development, itwas IMDBI that assumed the job of shaping projects, taking an active role ingetting the projects off the ground, and assuring their proper operation. Inthis respect IMDBI was an innovator: IMDBI brought entrepreneurs together,interested foreign participants, negotiated agreements, assured technicalassistance, worked as mediator between all parties, and through technical,financial and managerial advice, assured that projects were imnlemented andoperated in accordance with modern business practices. The first promotedprojects were mainly for manufacturing simple consumer goods like shoes, dairyproducts, sugar, tires, paper and glass. In the middle 1960s IMDBI startedpromoting more complicated projects like a rolling mill, a pipe mill and proj-ects producing telecommunications and electrical equipment. Later there weremore sophisticated projects, for example to manufacture ball bearings, com-pressors, diesel engines and projects related to the automotive industry.Now, IMDBI's promotions are spreading out in various directions, e.g. castiron foundries, expansions of the rolling and pipe mills, manufacture ofintermediate products for the textile, tire and metal industries, capitalgoods industries and agro-industries as well as into financial institutions,consulting services, industrial estates and even a business school. The dyna-mic promotional character of IMDBI, backed by favorable economic conditionsand Government policies, has made it possible for IMDBI to create its ownclientele. In this respect, ITDBI has been and is rather unique among thedfc's associated with the World Bank group. In spite of its heavy emphasison promotional work IMDBI has also helped many new or small entrepreneurs.Over half of its financing has gone to "regular projects".

2.14 A representative sample indicates that IMDBI's projects on theaverage have a satisfactory economic rate of return (exceeding 17%). Fi-nancial rates of return are not excessive, averaging 14% on total invest-ments and 17.5% on equity, although some projects have made returns exceed-ing 25%. During the Fourth Plan period IMDBI's projects generated directlyabout 45,000 jobs (about one-half of the total new employment in medium- andlarge-scale industry) at an average investment per worker of US$12,000. Thiscapital cost per new job compares favorably with the experience of other dfc'sin the region (ranging from $39,000 to $14,000), especially since there is noacute unemployment in Iran. It should be noted, however, that IMDBI's promotedprojects are relatively capital intensive, averaging US$25,000 investment perworker, but even this figure compares favorably with the average investmentper worker in the public sector (US$60,000). The aim of the promoted projectswas not primarily employment creation but rather to bring new technology andnew types of industry to Iran. Secondary employment creation is likely to beat least as important as the direct employment effect.

2.15 Seventy of IMDBI's projects up to March 1972 had foreign participa-tions amounting to US$78 million, or 14% of the project cost (US$557 million).Exports by IMDBI-financed projects rose by 73% between 1971 and 1972 andthere are good prospects of further increases in the coming years. Exportsfrom IMDBI's projects accounted for 19% of the country's non-traditionalexports in 1972 compared with 15% in 1971. Export potential is one of the

-6-

most important criteria for projects financed by INDBI at the moment. Ef-fective protection has not been at all as severe as the apprehension ex-pressed in past Bank appraisal reports. With increased efficiency and capac-ity utilization in IMDBI's projects, together with increasing prices abroadand a relative depreciation in Iran's exchange rate vis-a-vis Iran's majortrading partners, the competitiveness of IMDBI-financed projects has sub-stantially improved. Over 70% of IMDBI's projects are now likely to have aneffective rate of protection of below 30%; quite a few have none at all.

2.16 IMDBI has successfully promoted the establishment of industrialestates. IMDBI set up and financed the company which implemented the Alborz

Industrial Estate near Ghazvin. The Estate occupies 1,165 hectares and isdesigned to accommodate 135 industrial units, including residential areas for100,000 people and service areas. At present 28 industrial units are in oper-ation and another 26 are being built. Most of the remaining space of 80 unitshas been allocated. In addition, IMDBI has promoted two smaller estates inTabriz and Kermanshah. There are plans for three more estates, in Rasht,Esfahan and Mashad.

2.17 Firms partly or wholly owned by directors on the Board of IMDBI havereceived about 25% of IMDBI's total commitments for loans and equity invest-ments. Given the fact that a high proportion of large-scale industrial in-vestment in the past 15 years took place through the initiative of familygroups which are represented on IMDBI's Board this share is not consideredexcessive. Since well-conceived and financially sound projects have ori-ginated from this group, it would be unwise for IMDBI to dissociate itselffrom them altogether. However, IMDBI is well aware of the economic and so-cial dangers of too close an association with these important families andin Its promotions it allows them only minority holdings. DIMDBI, furthermore,encourages its promoted projects to go public in order to widen the ownershipin its companies. Most of DMBI's promoted projects are among the 85 companiesto go public in the next two years.

2.18 IMDBI has also been instrumental in mobilizing resources. The sharecapital of IMDBI has increased in the last seven years from Rials 400 millionto Rials 3.1 billion and the number of shareholders now stands at over 3,000.The resources IMDBI has attracted from abroad came originally from the WorldBank and to a small extent from AID. In the last two years, however, INDBIhas borrowed over US$165 million from the Eurodollar market, KfW and theGerman private bond market bringing the share of the Bank's funds in totalforeign resources to below 55%. At home IMDBI has been less successful forreasons explained in paragraph 2.10. It is therefore an important objectiveof IMDBI to develop the domestic capital market in order to mobilize thesavings of the country.

-7-

III. IMDBI's ORGANIZATION, PROCEDURES AND RESOURCES

Ownership, Management, Organization and Staff

3.01 A list of Shareholders, information on the Board of Directors andExecutive Committee, the Organization Chart and a Note giving factual infor-mation about these aspects is contained in Annex 1. Because of the Bank'sfamiliarity with IMDBI, history and description are kept to a minimum and,wherever possible, relegated to Annexes.

3.02 The Board and Executive Committee have largely remained the sameover the last five years. They consist mainly of industrialists, bankers andhigh public officials who have served IMDBI well and encouraged IMDBI's pro-motional activities. IMDBI's Managing Director, Mr. Kheradjou, is well knownto the Bank. He is also a member of IMDBI's Board. Except for one departure,the Head of the Economics Department, there have also been no changes in IMDBI'stop and middle management. This stability has greatly improved the continuityof the organization which in the past often experienced major changes in seniorstaff. The Managing Director has delegated considerable responsibilities tohis Deputy and Assistant Managing Directors, who have acted similarly vis-a-via their department heads. These developments have made IMDBI less vulnerableto an unexpected sudden departure of the Managing Director, who still remainsthe driving force behind the company.

3.03 IMDBI has for most of its existence been a largely informally or-ganized company. Given the fast increase in IMDBI's business and the relatedrequirements for new staff, procedures have been adjusted and the organiza-tion has been changed frequently to suit the new circumstances. AlthoughIMDBI's management considers that there is need for more structuring, it alsofeels that for the time being the organization should remain flexible to ab-sorb both new staff as well as additional business. Improvements now beingconsidered concern better financial planning and forecasting. The account-ing department, with the help of a foreign advisor, is pursuing this.

3.04 INDBI has continued its recruitment effort; 26 new professionalstaff members were added in the last two years. In Iran, IMDBI is consid-ered an excellent training ground for later moves to other jobs in industry.Consequently IMDBI lost eight professional staff members in the same period.By providing training, including special courses in the Management Center 1/,IMDBI tries to improve the efficiency of its relatively new staff. It is alsostudying ways to more quickly assimilate new staff members so that they canmake a productive contribution earlier. Given the fast growth of IMDBI'soperations, staffing is one of rMDBI's greatest problems to which IMDBI'smanagement is giving urgent attention. IMDBIts plans were discussed duringnegotiations. Staff with more than five years service are now eligible toparticipate in a scheme whereby they can buy IMDBI shares at par. With theprospect of other financial rewards, IMDBI expects to decrease staff turnover.

1/ Sponsored by IMDBI and staffed in part by Harvard Business School.

-8-

Project Appraisal

3.05 The appraisal of "regular" (i.e. non-promoted) projects remains ofgood quality. IMDBI scrutinizes carefully the financial, technical and mar-ket aspects of these projects and helps entrepreneurs in overcoming problemsin the several stages of planning, implementation and operation. The choiceof technology, the type of machinery and financial plan are carefully checked.Still, there are cases where the fast increases in prices both of machineryimported from abroad and of local construction have resulted in substantialcost overruns. Some of the overruns might have been avoided if the appraisalhad taken into account recent price trends and if cost estimates had been dis-aggregated in more detail. DMDBI could perhaps also have avoided some of thefinancial problems if it had assured itself that the financial plan of theprojects included sufficient contingencies. IMDBI is now giving particularattention to cost estimates and the adequacy of contingencies.

3.06 Economic appraisal work has remained the weakest area of IMDBI'sappraisal, but is getting better as IMDBI has started calculating the economicrate of return (ERR) in addition to the partial economic analyses done hither-to. During negotiations IMDBI undertook to calculate the ERR of all projectssubmitted to the Bank. IMDBI has engaged consultants to advise it on how itcan best organize and train its economic staff.

3.07 In promoted projects, IMDBI goes about its project appraisal differ-ently. After a project has been identified by IMDBI itself, the Governmentor an entrepreneur, detailed technical and feasibility studies are made by re-putable firms, generally the same ones that are responsible for the implemen-tation and operation of the project. In view of IMDBI's experience that oncefeasibility studies are completed, it is difficult to make basic changes inthe proposal, DMDBI has decided that its staff will, in the future, activelyparticipate in the preparation of such studies. DMDBI hopes thus to getgreater control over the selection of technology and equipment. After comple-tion of the feasibility study and the selection of the foreign partner, agree-ments for technical services, management assistance and the use of patents andlicenses are prepared and negotiated. At this stage a financing proposal isprepared which is sent for appraisal to the Projects Department. nMDBI'sdual role of promotor and appraisor sometimes makes an objective appraisaldifficult.

3.08 Procurement. IMDBI's procedures for guiding and controlling pro-curement by its clients are well-designed and appropriate to the nature ofits business. For its promoted projects at least three bids are required,which are carefully examined; for regular projects, because of special re-quirements or the need to integrate new equipment into the existing plant,this procedure is not always followed. IMDBI supplements its analysis bycomparing the bids with cost estimates of previously financed projects.

Project Supervision

3.09 IMDBI's supervision work is handled by two sections: the LoanSupervision Section, which follows up on all regular projects, and the Man-agement Unit, which follows up on all promoted projects.

-9-

3.10 Loan Superision Section. IMDBI's supervision work, which was notwell organized a few years ago, has improved considerably over the last twoyears. Annual reports are now received from 80% of the customers. Plantvisits are made regularly, except to projects classified as "good", i.e. proj-ects that are repaying regularly and which in IMDBI's opinion have no financial,technical, market or managerial problems. Projects with major problems arevisited on average three times and reports are made and reviewed at leasttwice a year. Sometimes an IMDBI staff member is seconded to a severe prob-lem project to give technical and sometimes managerial assistance to over-come the problems. IMDBI's supervision of projects under construction isgood and includes regular visits and reports.

3el1 There is still room for improvement. IMDBI often encounters diffi-culties in collecting accurate information and in enforcing proper accountingand auditing practices. Reasons for the latter are some enterpreneurs' at-titudes and the lack of trained accountants and auditors in Iran. IMDBI'sown supervision reports are still mainly used as a means to ensure repaymentand not as a tool which can be used in the appraisal of new projects and toevaluate its economic impact. However, the reports are adequate for Xanage-ment's purpose of keeping itself informed on the progress and operation ofit client companies. It is expected that the Economic Research Department,which was recently created, will make sector and other economic studies towhich supervision reports will be a major input. The most important obstacleto further improve supervision is the lack of experienced staff, given thefast increase in the outstanding portfolio. Still, IMDBI needs to give thisaspect of its work the importance it deserves.

3.12 Management Unit. The follow-up on all promoted projects is assignedto this Unit. The Unit is to give particular attention to promoted projectswith problems and a few members from the Unit have been assigned the actualmanagement of projects in difficulties. Most reporting to management is doneorally instead of through written reports which can be circulated and usedfor later reference. Although the system has helped Management to keep it-self abreast of developments, quite a few of the staff have had little bene-fit from knowledge acquired from supervision. To a large extent, this defi-ciency is rectified because most of the promoted projects have come back forrepeater loans which required a re-appraisal of the company. Furthermore,through its seats on the Boards, IMDBI keeps in close contact with the man-agement of its promoted projects. Proper accounting, auditing and reportingis of great importance to IMDBI and except for three projects all promotedcompanies are audited. However, there remains much to be improved in thegeneral area of accounting and reporting. IMDBI's directors on the Boardsof companies could work more effectively if they made better use of the staffin the Management Unit.

3.13 Disbursement procedures. The procedures and checks regardingdisbursements for goods procured from abroad are thorough and ensure thatpayments are made only for approved machinery, equipment and services.Disbursements related to local construction, equipment and services are

- 10 -

only made following plant visits, at which time physical progress is care-fully estimated, the sponsor's contribution is ascertained, documents arechecked and actual and planned costs are compared. Due to cost increasesand delays in implementation, DMDBI is very careful to ensure adequate con-tributions from the project sponsors before INDBI reimburses for incurredexpenses. Overall, disbursement procedures and practices are satisfactory.

Resources

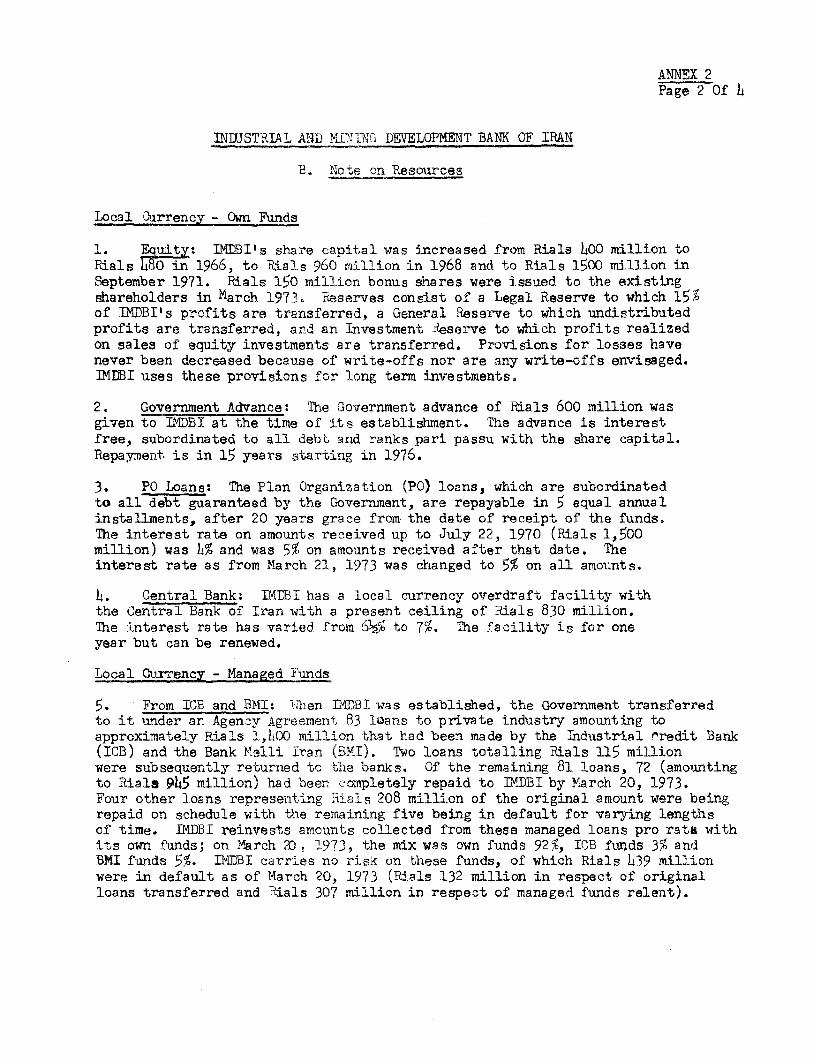

3.14 Annex 2 presents IMDBI's resource position as of March 20, 1973,and describes the several sources of funds.

3.15 Local Currency Resources. In the last two years the only increasesin IMDBI's own local currency resources resulted from a share capital increaseof Rials 540 million in September 1971 and from cash generation. Unless itwas to experience a negative spread, IMDBI was unable to borrow Rials long-term from sources other than the Government. The Government did not makeadditional funds available during these two years (Rials 720 million werepaid in on past commitments). Consequently, the share of local resourcesin total resources decreased from 36% in March 1971 to 26% in March 1973.This inhibited IMDBI from taking on new local currency business, for whichdemand exceeded supply. However, rMDBI's difficulties were alleviated whenit drew down large Eurodollar loans during FY73 and converted $36.1 millioninto Rials. This improvement in IMDBI's resource position has, however, re-sulted in a foreign exchange exposure (see paragraphs 3.19 - 3.22 below).

3.16 Managed Funds. These funds, coming from the Government and avail-able to IMDBI without risk, are described in Annex 2. The availability orthese funds has been important because they have provided flexibility by al-lowing IMDBI to lend a single enterprise amounts in excess of the exposurelimit stipulated in its policy statement (Annex 4). These funds have beendeclining and will continue to decline in importance due to the growth inIMDBI's net worth, and consequently in its absolute exposure limit. Theslight over-commitment of Managed Funds (Rials 119 million as of March 20,1973) will be covered by repayments and by new funds expected during theFifth Plan period. IMDBI has no separate investment criteria for itsManaged Funds and almost every project requiring local currency receivespiart of its financing from these funds. Loans from the Managed Funds aremade on the same terms and conditions as INDBI's own funds. Loan caait-ments from Managed Funds have fallen to 15% of total loan commitments, wixIis an indication of the declining importance of these funds.

3.17 Foreign Currency Resources. Up to the end of FY72, the Bank hadvirtually been IMDBI's only source of foreign currency resources. Thissituation has changed dramatically since then. The Government passed leg>i-latiorn in 1971 which enabled it to guarantee borrowing by IMDBI from souroznŽother than the Bank. In January 1972 IMDBI arranged two German lines ot eKdit (KfW and DEG) totalling DM 51 million, with Government guarantees. FuL-,-thermore the favorable conditions in the Eurodollar market made it posa'!.to borrow from that market without a Government guarantee. During FY73 fotnEurodollar loans amounting to $100 million were drawn down. These loano, p)uo

- 11 -

two others arranged early in FY74 (including the first private bond issue bya development finance company in the German market), are described in Annex 3.IMDBI has thus been highly successful in raising fresh foreign resources. Inthis respect it hi-s exceeded the expectations as expressed at the time of thelast loan presentation to the Board. The share of Bank funds in IMDBI's totalforeign currency resources at the end of FY73 had decreased to below 55% andin overall resources to below 33%.

3.18 A noteworthy feature of all but one of the Eurodollar loans is thefLexible interest rate, set every six months based on the current London interbank rate. When initially drawn down, the interest rates were in the neighbor-hood of 8%; when renewed in the middle of 1973 the rates were increased to, inmany cases, above 10%. While some of these funds have been lent as workingcapital loans at 10-11%, on others a 10% cost has lead to a negative spread.IMDBI expects that over the life of these loans the average spread will bepositive either because the Eurodollar interest rate will come down to morenormal levels or by charging higher interest rates to its own borrowers, whichit can do since this September. This expectation is plausible.

IMDBI's Foreign Exchange Exposure

3.19 At about the time IMDBI started to diversify its resources, the in-ternational fixed exchange rate system was abandoned. Because the Bank con-tinued to disburse other currencies than those IMDBI's borrowers required fortheir payments, IMDBI has been faced with difficulties in passing on the for-eign exchange risk to its borrowers; the Government is unwilling to assume it.INDBI, together with other well-established development finance companies,has argued that it should be allowed to carry some foreign exchange exposurearising from the normal business of the company. In fact, IMDBI was exposedfor $70.6 million on March 20, 1973. There were two main origins to thisexposure:

a) In view of the market expectations in 1972 for an appreciationof the Yen and the Deutsche Mark - two currencies which weremainly disbursed at that time by the Bank - IMDBI's borrowerswanted either to prepay their loans or to have them replacedby loans in currencies with less risk. Complaints were acutefrom borrowers who had procured machinery from countries otherthan Japan and Germany, but who had their loan accounts chargedwith Yens and DM's. In December 1972 IMDBI used $35 million ofits Eurodollar borrowings to prepay the outstanding amount ofLoan 602-IRN. It thereby replaced its obligation to the Bankin several currencies, but mainly Yens and DM's, for dollarobligations to other institutions. IMDBI expected to be ableto convert the currency liabilities of its borrowers, who hadutilized Loan 602-1=N, into dollars so that it would have noexposure. However, though it started to review the accountsof these borrowers and to arrange consultations with themimmediately after prepaying the Bank, this work required agreat deal of time and was not far advanced when the February1973 realignment of currencies (including an unexpected apprecia-tion of the Rial vis-a-vis the US dollar) took place. As a

- 12 -

result of this realignment many of IMBI's borrowers nolonger wanted to convert their loans. With the subsequentmovements in exchange rates it became impracticable to pursuethe conversion of these loans.

b) The second development was the conversion of some $36.1million of Eurodollar borrowings into Rials to meet itslocal currency needs (see paragraph 3.15). Of this, $10million equivalent has been invested in Government bondswith the exchange risk covered by Bank Melli under a con-tinuing agreement. Besides this $10 million cover IMDBIhas a reserve on its Balance Sheet labelled "Accrued profiton exchange adjustments" totalling some $8.6 million equiv-alent as of March 20, 1973; this item represents bookprofits resulting from exchange adjustments during FY73. 1/

3.20 IMDBIts exposure increased further in May 1973 as a result of itsDM 60 million bond issue. The proceeds of this issue, as required by theLoan Agreement and in line with measures by the German authorities to speedup capital outflows, had to be converted into Eurodollars immediately andtaken out of Germany. Subsequently, $15.4 million of the proceeds wereconverted into Rials with the remaining $4.9 million being used in normalforeign currency operations. Because DOBI's obligation is in DM's IMDBI'sexposure increased by about $11 million equivalent.

3.21 The above three developments expose IMDBI to risk of loss result-ing from changes in exchange rates. During negotiations agreement was reachedwith IMDBI on the steps it will take to protect itself from such a loss.Essentially these involve, besides arranging guarantees, purchasing forwardcover, etc., the establishment of a specific provision to cover possible ex-change losses and the limiting of the exposure to a prudent level in relationto the provision. The relation between exposure and the provision is deter-mined by the composition of the exposure, i.e. the number and relative impor-tance of the currencies in the exposure. A review of DMDBI's exposure atthe end of the first half of its FY74 (September 22, 1973) established thata prudent level would be up to seven times the provision or, looked at theother way around, that the provision should represent at least 14.3% of theexposure. It is expected that this relationship between the provision andthe maximum prudent exposure will continue in the future.

3.22 The provision would be made up of realized and unrealized profitsmade on the exposure (offset by realized and unrealized losses) and of alloca-tions from income. For FY74, 3-1/3% of gross income will be transferred tothis provision. In addition, a one-time transfer of about $3 million equiva-lent from the provision for bad debts will be made in the current fiscal year;the Bank and IMDBI's auditors agree with IMDBI that the remaining bad debtprovision will be more than adequate to cover any possible portfolio losses.As a result of these transfers, the provision for exchange losses is expectedto total some $12 million equivalent at the beginning of FY75, versus the ex-posure as of September 22, 1973, of about $87 million equivalent, $10 millionof which is covered by the Bank Melli exchange rate guarantee.

1/ By September 22, 1973, this book profit had been reduced to $8.0 millionequivalent due to exchange rate movements.

- 13 -

IV. OPERATIONS AND FINANCES

Operations

4.01 A summary of operations through the end of FY73 is given in Annex5. IMDBI has far exceeded the level of operations forecast in December 1971.The main reason has been a better foreign exchange resource position thanforeseen two years ago. This also enabled IMDBI to extend its activitiesinto, for instance, the granting of medium-term credit to client companieswith shortages of permanent working capital. As discussed before DMBI,through its promotions, to a large extent creates its own clientele; increasedsupply of funds, therefore, enabled it to step up its business. The betterforeign exchange resource position also allowed IMDBI to increase its equityinvestments in promoted projects.

4.02 IMDBI committed Rials 18.7 billion (US$272 million) in FY71-73,including Rials 9.8 billion for promoted projects. This three-year totalexceeded total commitments in the period FY59-70 (Rials 16.7 billion).Commitments have been growing at a steady rate of over 28% per year in thelast five years. Disbursements have kept up with this trend partially be-cause working capital loans are quickly disbursed and equity investmentsare paid in soon after being committed. However, disbursements from Bankloans were delayed, beginning in October 1972, because of the internationalmonetary situation. It is expected that, with a solution to the exchange riskproblem and greater stability in the international money markets, disbursementsfrom Bank loans will be speeded up. This is in fact already taking place.Of the $16.0 million disbursed since October 1972, $11.5 million was disbursedfrom August through November. For comparison, disbursements in the periodOctober 1971 - October 1972 were $29.5 million.

4.03 Loan Operations. Annex 6 gives a comparative statement of loanssigned. The following facts, derived from the annex, are significant andconfirm DMDBI's continued emphasis on relatively large-scale projects inthe modern sector:

(a) An increase in the size of loans and continued emphasis on themodern sectors of manufacturing: The average size of loanshas more than doubled in the period FY71-73, compared withthe years up to FY70, i.e., from Rials 45 million to Rials100 million. Despite this development, the number of loansbelow Rials 45 million account for more than 50% of all loans;medium-size enterprise remains therefore an important part ofIMDBI's business. In total, 98 loans were made to projectsproducing machinery, light metal, non-metallic minerals,textiles and paper. These projects accounted for over 70% ofthe amounts committed since March 1971. The average size ofloans to these sectors is large, particularly in paper (US$3.4million), followed by machinery and textiles (US$1.8 million),

- 14 -

non-metallic minerals (US$1.5 million) and light metal indus-tries (US$0.8 million). The heaviest concentration of commit-ments is to the machinery and equipment sector (23.9%). Com-mitments are, however, well spread over the various industrialactivities.

(b) An increase in the average maturity of the loans: The averagematurity weighted by amounts committed increased from 6.8years before FY71 to 8.8 years after FY71. Loans over tenyears increased from 4 to 22 in this period. The reason forthis development is the larger size of the projects requiringlonger gestation and amortization periods.

(c) Expansion projects have become relatively more important thannew projects. Many projects are coming back for repeater loansto increase the size of production to satisfy increased demand.The share of loan commitments to new projects dropped from 53.6%of total commitments made up to March 1971 to 41% in the periodFY71-73. Working capital loans, always made to existing proj-ects, increased their share from only 3% to over 10% in thisperiod.

(d) Continued concentration of commitments to projects located inTeheran. These still account for over 40% of total loan commi-tments. However, the high figure for FY73 (48%) is due mainlyto one automobile project 1/ which accounted for Rials 1.3billion.

4.04 IMDBI's promoted projects are a significant factor in these devel-opments. The average size of the loan commitments to promoted projects isRials 225 million (US$3.3 million); most of these loans have maturities ex-ceeding eight years, are in the intermediate and capital goods sector andalmost half of the promoted projects have received additional loans for ex-pansion. 55% of IMDBI's loan and equity investments are outstanding in pro-moted projects. IFC has invested in four of IDEBI's promoted projects. ParsPaper, IMDBI's largest project, has received a $10.22 million loan and an in-vestment of $1.95 million; Aliaf Nylon, a company producing Nylon 6 yarn, re-ceived a loan of $4.5 million 2/; Iran Carbon obtained a loan of $3.1 millionand an investment of $0.43 million; and Ahwaz Rolling and Pipe Mill, a $3million loan and $0.9 million investment. Except for Pars Paper, which hadits loans rescheduled, these projects are progressing satisfactorily and fur-ther expansions in all of them are contemplated.

1/ Iran National, not a promoted project, received a loan from IFC in FY73amounting to US$11 million. IMDBI made a $7.7 million loan to the com-pany and guaranteed part of the suppliers' credits.

2/ This loan has since been prepaid. IFC has under consideration a secondloan to, and an equity investment in, this company to help finance anexpansion project.

- 15 -

4.05 Eouity Investments, A list of companies in which IMDBI has takenan equity investment is attached as Annex 7. IMDBI has subscribed a total ofRials 3.1 billion to the share capital of 60 companies. Reflecting IMDBI'sgeneral operational orientation, equity subscriptions have mainly been madein tle modern sectors of industry, i.e., steel and basic metals (22.8%), ma-chinery and mechanical industries (16.5%) and electrical equipment (10.2%).Almnst 50% of IMDBI's total loan and equity commitments up to March 1973 hasbeen made to promoted projects. Managed Ftunds equity investments are partlyoutstanding in promoted projects and partly in projects in which the Govern-ment wanted to invest in order to renovate the company. Investments from Man-aged Funds as well as the sale thereof require Government approval.

4.06 Generally, DMDBI keeps its holdings in a company below 20% of theshare capital, but it always requires a seat on the Board. Through its equityinvestments IMDBI ensures an active role in the formulation, implementationand operation of the projects. IMDBI's equity participation helps ensuremajority Iranian holding, and when several sponsors are inxrolved IMDBI is re-garded as a neutral party whose advice is considered to be in the interest ofthe project itself. In almost all promoted projects, a foreign collaboratorparticipates in the equity of the company (except in the agro-food and theservices sectors where foreign skills are not required).

4.07 Considering the Stock Exchange's infancy, and the relatively un-seasoned state of DMDBI's equity portfolio, IMDBI has been quite successfulin rolling-over its equity portfolio. Sales have amounted in total to Rials217.5 million, of which Rials 40 million were in the last two years. Theplanned Investment Trust may absorb a considerable part of IMDBI's equityportfolio.

4.08 Working capital loans. IMDBI got into this field in response tothe dearth of short- and medium-term capital (paragraph 2.11). IMDBI makesthese loans to finance raw materials, work in progress, inventories and salesof companies which have previously received long-term loans from IMDBI. Theygenerally have a maturity of two and a half to five years. When projects haveincurred cost overruns and the implementation of the project has been delayed(see paragraph 3.05), original working capital provisions are often depletedand the companies face difficulties in starting operations. On the basis ofa separate appraisal, IKDBI has been willing to provide medium-term financeto overcome these difficulties, although it is not its policy to replacecommercial banks. Following the promotion of the Iran Industries Bank andthe establishment of several other institutions, IMDBI will likely provideless working capital loans in the future.

Financial Position and Performance

4.09 Audited income statements and balance sheets for the five yearsending March 20, 1973, are attached as Annex 9.

4.10 Income Statements. Gross income rose at an accelerating rate betweenFY69 and FY73; the annual increase averaged about 35%. These increases reflectthe growing loan portfolio, the increasing contribution of dividend income and,

- 16 -

in the most recent year, the large agency fees and income on deposits. Ex-penses, however, followed the same trend over the period, with an average an-nual increase of over 40%. FY73 expenses were some 50% higher than in theprevious year, due mainly to the utilization of higher cost Eurodollar loans.As a result, net profits have grown at an average rate of some 15% per yearover the period. Not included in the net profit figures are the gains real-ized on sales of equity investments. These gains, which are indicated inthe income statements, are carried directly to reserves.

4.11 Administrative expenses have increased in absolute terms but havedecreased as a percentage of average assets - less than 1% in FY73. Netprofit as a percentage of net worth increased in FY73 after a drop the prev-ious year caused by the share capital increase. Dividends have been main-tained since FY70 at 12% of share capital. This has resulted in a relativelyhigh pay-out ratio, though not dangerously so. The high level of dividendshas facilitated increases in IMDBI's share capital.

4.12 Balance Sheets. IMDBI's latest balance sheet (March 20, 1973) issignificantly different from earlier ones thanks to the major foreign borrow-ings which also caused a dramatic improvement in IMDBI's liquidity. Thecurrent ratio is now more than one for the first time in a number of years.IMDBI's debt/equity ratio, as defined in the latest Loan Agreement (794-IRN)(which now results in the same ratio as the conventional debt/equity ratio)was 5.8 as of March 20, 1973, versus the maximum level of debt allowed underthe Loan Agreement of seven times equity. IMDBI has a sound capital structure.

Portfolio

4.13 Details on IMDBI's loan portfolio are given in Annex 10, separatelyfor Own and Managed Funds. Because of the rapidly increasing commitments inthe last three years more than 50% of rMDBI's loan portfolio is still in grace.IMDBI's outstanding loan portfolio increased from Rials 9.0 billion in June1971 to Rials 15.8 billion in June 1973.

4.14 There has been a distinct improvement in IMDBI's loan portfoliosince the 1971 appraisal by the Bank. Only 25 companies, out of the 207active borrowers, had loans in arrears on June 21, 1973. The loan amountoutstanding affected by arrears was about 13% of IMDBI's total loan portfoliowhile the principal amount actually in arrears was only 1.6% of the totaloutstanding loan portfolio. The percentages were 16% and 2.4% in June 1971.Although the proportion of Managed Funds affected by arrears was slightlyhigher (16.6%) the principal amount actually in arrears was only 1.8% of theManaged Funds outstanding portfolio. The reason for the slightly worse sit-uation of the Managed Funds is found in two projects accounting for outstand-ing loans of Rials 250 million.

4.15 There are a number of reasons for the improvement. First, a fewcomplicated projects, which faced problems in implementation and start-up,overcame their problems. In some of these projects IMDBI's direct interven-tion in the management was instrumental in this turnaround. Second, someprojects' working capital situations have improved, in part because IMDBI

- 17 -

has begunr making loans for this purpose. In the past, some companies de-faulted on their loan repayments mainly for lack of liquidity. Third, com-panies have benefitted from the continued boom conditions in the country.Fourth, IMDBI rescheduled loans which should in the first place have beengiven longer grace or amortization periods. Further improvements are likelyin the next six months when five more companies, with an outstanding loanamount of about Rials 1.4 billion and principal amount in arrears of Rials106 million, should be able to repay their arrears.

4.16 Seven relatively small projects, committed in the early 1960's,with an outstanding loan amount of altogether $3.2 million (of which $0.8million from Managed Funds), have more structural problems. However, IMDBIdoes not expect anv losses in these companies and keeps them under closesupervision. Two of the companies have been under the management of theIndustrial Protection Board, an agency that takes over companies in severedifficulties, and no loan repayments are made by these companies. Againsttwo other companies legal action is being taken. Two promoted projects withoutstanding loans of $5.1 million, a paper tissue plant and a stationaryengine company, face more long-term problems but IMDBI and the managementof the companies are working hard to find solutions.

4.17 As of March 20, 1973 DMDBI had provisions against possible losseson its loan portfolio of Rials 534 million, equal to 4Z of the portfolio.Because no losses are foreseen on outstanding loans these provisions arebasically part of IMDBI's equity. The loan portfolio is of sufficientlygood quality to support the judgment that INDBI has a sound financial posi-tion.

4.18 IMDBI's equity portfolio is gradually maturing; 15 companies paiddividend in FY73 resulting in a yield of 6.6% on average outstanding port-folio during the year. Profits on the sales of shares and rights increasedthe return on 1973's average equity portfolio to 9.5%. Furthermore, IMDBIreceived bonus shares valued at Rials 66.3 million (at par). Given the mixbetween operating and non-operating companies, this return on equity is satis-factory. Conservatively valued at market value, net book value or at par (forcompanies under construction), the equity portfolio should be worth aboutRials 350 million more than the book value.

4.19 Audit. The independent accounting firm of Coopers and Lybrand hasbeen IMDBfrs auditors since inception and has always approved the financialstatements without qualification. The Bank receives a long-form audit reportand the auditor's letter to IMDBI's management regarding the maintenance ofaccounts and related matters. Following the Bank's suggestion, IMDBI's AnnualReport for FY73 included for the first time data on contingent liabilities.It did not, however, make any mention of the foreign exchange exposure. Theauditors agreed to cover this topic next year.

- 18 -

V, PROSPECTS

The Environment

5.01 The Five Year Plan (1973-78). Motivated by well supported expec-tations for rising oil revenues and improvements in Iran's absorptive capac-ity, the Government has approved the Fifth Plan which is expected to raiseper capita GDP, currently $580, by 75% to about $1,020 by 1978. GDP is pro-jected to grow at 11.4% per annum in real terms compared with roughly 11%during the Fourth Plan. The share of investment in GDP is expected to risefrom 22% to over 27% at the end of the Fifth Plan. Public investment is tobe maintained at high levels, reaching an estimated $22.7 billion (in con-stant prices) during the Plan period, while private investment is planned tobe $13.4 billion. Industry, including mining, would grow at 15% annually,the share of industry to non-oil GDP rising from 20% to 23% during the Planperiod. Exports of non-oil manufactures are expected to increase by 30% perannum. The proportion of the labor force employed in industry would growfrom 21% to 28% by 1978.

5.02 The shortage of skilled labor and managerial staff could conceivablybecome a constraint in the fulfilment of the Plant s targets. However, theGovernment is optimistic that through training programs, repatriation ofIranians working abroad and hiring of foreigners, this problem can be alle-viated. Also, the need to contain increasing inflationary pressures mayniecessitate monetary and fiscal policies restrictive of public and privatespending. Prices rose by 6% in 1972 and have probably increased more in 1973.However, the comfortable foreign exchange position affords the Government con-siderable flexibility in combatting inflation. Although ambitious, the targetsof the Fifth Plan seem to be feasible in light of projects being prepared andIran's track record in recent years.

5.03 The Government is expected to make large investments in the basicindustries (steel, mining, petrochemical, heavy engineering and ship-building).The Plan is already being revised and a larger share of planned industrialinvestments will be allocated to the private sector in order to free addition-al resources for agriculture and the social sectors. The original target ofprivate investment in industry of US$5 billion is being revised upward con-siderably in order to achieve the growth rates outlined in paragraph 5.01.Particularly a target annual growth rate of 15% in industrial value addedwill require large investments, taking into account the gestation period ofsome large scale investments in industry. During the Fourth Plan period,when the manufacturing sector grew on the average by 14% per year, fixedinvestments in private industry increased at an annual rate of 202 in realterms. To obtain an even higher growth rate in value added, private invest-ments in industry may have to increase by an average of 20-25% in real terms.The main challenge for Iran is to formulate and implement this high level ofinvestments. IMDBI's promotional work will be very important in this regard.

- 19 -

5.04 An important and welcome feature of the Fifth Plan is the emphasison the social sectors and especially on rural development. Overall expendi-tures in the social sectors, including agriculture, are planned to be 37% ofthe total planned Government expenditures. A rise in rural incomes shouldinter alia considerably broaden the market for industrial products. TheFifth Plan also lays emphasis on regional development. To encourage theprivate sector to invest in backward regions and contain labor emigrationto the large cities, additional financial and other incentives will be pro-vided. The Government's strategy is to create a number of growth poles alongthe East-West axis Mashad - Teheran - Ghazvin - Tabriz and along the North-South axis Tabriz - Arak - Esphahan - Abadan - Shiraz - Kerman - Bandar Abbas.The parallel development of natural resources (agriculture, oil and otherminerals) is also foreseen. The Fifth Plan envisages five times more ex-penditure for industrial development in the provinces than in the Fourth Plan.

IMDBI's Prospects for Business

5.05 In considering IMDBI's projections some aspects should be noted.First, the size of IMDBI's projects is increasing constantly; whereas a fewyears ago a US$10 million project was considered large, at the moment IMDBIhas under consideration projects requiring fixed investments of over US$50million. Second, IMDBI has had so far a virtual monopoly in the financing oflarge-scale industry. However, in the next five years this situation is likelyto change and the recently set up DIBI and stepped-up operations by ICB arelikely to bring more competition to IMDBI. These should be healthy develop-ments. IMDBI is by now well established in the market, has good relationswith both the Government and the business community, and has a momentum whichcan well stand some more competition. Third, IMDBI's scope for promotions isincreasing. Not only are there possibilities of backward integration into in-termediate products in several sectors (such as acrylic and polyester, diesand castings and parts for the automotive and household appliance industry)which will require large investments, but also the capital goods sector nowoffers great potential (for example, construction machinery, trucks, trainwagons and electromotors). The growing size of the consumer market makes itpossible on the other hand to enter into the production of more end-products,and finally construction and agricultural production is increasing which willrequire more construction materials and processing capacity. IMDBI is work-ing on all these fronts; it currently has under consideration about 30 proj-ects for promotion and another 50 regular projects.

5.06 Annex 11 presents operational and financial projections for IMDBIfor the next five-year period beginning with FY74. Approvals in FY74 areforecast to total Rials 16 billion, a two thirds increase over the Rials 9.6billion approved in FY73. This substantial increase is supported by some 60projects under active study by IMDBI in July 1973 that are likely to be ap-proved before the end of FY74, involving potential loans and equity invest-ments by IMDBI of Rials 12.7 billion. During the first;six months of FY74(i.e. up to September 22, 1973) loans and investments totalling Rials 7.3 bil-lion were approved; this is more than double the amount approved in thesame period the year before. Approvals in FY75 are forecast to increase by

- 20 -

12% to Rials 18 billion. IMDBI's share in Iran's total industrial fixedcapital formation is forecast to fall slightly from an average of 15% in thelast five years to 13% in the next five years.

5.07 On the basis of approved loans not yet committed and of IMDBI'spipeline, commitments are expected to amount to Rials 10.2 billion in FY74,a 54% increase over the Rials 6.6 billion committed in FY73. Commitmentsin the first six months of FY74 totalled Rials 6.8 billion, 82% higher thanin the same period the year before. Commitments in the following four yearsare forecast to increase by an annual average of about 16%. These forecastsfollow the forecast of approvals and are also in line with past trends. ThoughIMDBI has experienced some cancellations of approved loans, these have beenvery few and the forecast assumes that there will be none in the future.

5.08 With the expected increasing availability of local capital and in-termediate goods it is plausible that Rial lending should increase more thanlending in foreign exchange. Therefore, loan commitments in Rials from OwnFunds are projected to increase from the rather low level of commitments ofRials 983 million in FY73 to Rials 3,598 million in FY78. Equity investmentsfrom Managed Funds and Own Funds are projected to increase only slowly becauseIMDBI would otherwise exceed its policy limit on its aggregate exposure inequity. Thus the projections foresee a relative fall in equity operations inrelation to loan operations.

5.09 Given the feasible targets of the Fifth Plan and rMDBI's establishedrole in financing industrial projects, as well as its present pipeline, theseprojections are reasonable, if not conservative. A possible constraint inmeeting these forecasts is IMDBI's capacity to process this number of projects.Its engineering staff, currently numbering twelve, could be a bottleneck, butIMDBI is actively recruiting new engineers to strengthen the projects depart-ment.

Resource Requirement

5.10 To finance the volume of operations projected for the five-yearperiod FY74-78 IMDBI will need a total of Rials 75.6 billion (US$1.1 bil-lion) against which it had Rials 3.1 billion of uncommitted funds availableas of the beginning of FY74. IMDBI's total resource gap over these fiveyears includes Rials 23.4 billion to finance local currency expendituresand Rials 49.1 billion equivalent to finance imports. In addition, foreigncurrency loan repayments in FY77 and FY78 will exceed collection by Rials2.5 billion, reflecting the shorter term of the Eurodollar loans. The fi-nancing of these two aspects of the resource gap is considered in the fol-lowing paragraphs.

5.11 Local Currency Resources: A share capital increase of Rials 1.5billion took place in September of this year. Another share capital increaseof Rials 3,150 million is forecast in FY76. The forecast includes local bor-rowing by IMDBI from the market (Rials 1.5 and 2.0 billion for FY75 and FY77respectively). These would be the first efforts by IMDBI to develop the localfixed interest security market, and would depend on a change in the Government's

21-

attitude toward private borrowers (see paragraph 2.10). Although IMDBI doesnot yet know in what form it might be able to raise these local resourcesthe forecasts assumes four to five year paper with an interest rate of around9% tax free. (If IMDBI is unable in the event to borrow locally it will eitherhave to increase its dependency on Government funds, increase its share capi-tal further or curtail its local currency activities.) Plan Organizationborrowings on the same conditions as in the past, included in the Fifth Planat Rials 1.0 billion a year, will contribute about 20% of the additionalresources needed over the next five years. Internal cash generation, includingloan collections, are expected to cover the remaining local currency gap.

5.12 Foreign Currency Resources: IMDBI had available at the beginning ofFY74 $69.5 million of foreign exchange resources. Early in FY74 it drew downa $15 million Eurodollar loan and a DM 60 million ($21.5 million equivalent)bond issue which together with the $69.5 million could carry TMDBI until aboutMarch 1974. It had also arranged two further Eurodollar loans totalling $60million. Against these existing and planned resources of $166 million, pro-jected commitments through the end of FY76 total some $400 million, leaving anear-term gap of $234 million. Adding projected commitments for FY77 and PY78plus the excess of loan repayments over collections increases the gap for thewhole five-year period to over $650 million.

5.13 This gap is clearly too large for IMDBI to fill without the Bank'sassistance. IMDBI has therefore requested a Bank loan of $75 million to helpcover the near-term gap of $234 million. Against the balance of $25 millionavailable for commitment from existing Bank loans at the end of November,IMDBI has submitted to the Bank projects amounting to almost $38 million whichare being reviewed for our approval. Amounts that cannot be accomodated fromexisting loans would be authorized from the proposed new loan. In view ofIMDBI's present resource position and projected commitment level, the proposedBank loan should be available toward the end of IMDBI's FY74, i.e., in earlycalendar year 1974. IMDBI anticipates being able to borrow the rest of itsprojected foreign currency needs from other foreign sources. Given its pastsuccess in this regard, and assuming that foreign markets do not seriouslydeteriorate, it should be able to do so, even though the amounts envisaged arevery substantial. The alternative would be to reduce IMDBI's projected levelof operations.

5.14 In individual projects, the proposed Bank loan would be mixed withforeign currency from other lenders so that the size of individual projectcontributions from Bank funds would not normally exceed $4 million. Withoutsuch a mixing the Bank's contribution to a project could become inordinatelylarge as IMDBI takes on larger and larger projects. This mixing would alsoallow the longer term of a Bank loan to accommodate the expected shorter termof loans from other sources. In this way the Bank's funds would perform therole of a catalyst.

- 22 -

Financial Projections

5.15 Interest income is expected to increase by about 50% per year inthe next two years with the portfolio rising 40%. Furthermore, a small in-crease in the average interest rate charged on loans, primarily arising fromworking capital loans, is forecast. 1/ Interests and fees payable take intoaccount the higher cost of borrowings, particularly the higher cost of Euro-dollar loans. Interest costs are forecast to be 65% higher in FY74 comparedwith FY73. The projections assume that rates on Eurodollar loans will comedown from the record highs prevailing in 1973 but, because profits are quitesensitive to interest payable, the situation needs close watching in the future.Profits before tax and provisions are forecast to increase by 50% per year inthe next three years, coming down to a more moderate growth level of 20% there-after.

5.16 There should be a decline in administrative expenses, forecast todrop from 0.9% of average total assets in FY73 to 0.4% in FY78. Offsettingthis decline, however, is the increase forecast for taxes and provisions forlosses.

5.17 IMDBI proposes to maintain its dividend payment level at 12% ofshare capital. This is forecast to result in a pay-out ratio of 80% in FY74due to the share capital increase. With the growth in net profit, however,the pay-out ratio is expected to fall to about 50% in FY75, rising againthereafter due to the forecast increase in the share capital. Free reservesare expected to increase throughout the period at an average annual rate of45%.