World Bank Pension Reform Primer This note is part of the Pension Reform Primer series of the World Bank. It was written by Edward Whitehouse of Axia Economics, London. Please contact the Social Protection Advisory Service, World Bank 1818 H Street NW Washington DC 20433, telephone +1 202 458 5267, fax +1 202 614 0471, e-mail [email protected]. All of the notes are on the internet at www.worldbank.org/pensions. Supervision Building public confidence in mandatory funded pensions he regulation and supervision of individual pension accounts has been a neglected issue. In contrast, much has been written on financing the transition to funded pensions and the design of benefits. Yet effective regulation and efficient supervision are crucial to the success of pension reform. This note explores six issues in the design of a supervisory regime. It makes some comparisons between the performance of agencies in different countries and looks at four important areas of supervision: institutional and financial controls, and membership and benefits procedures. A new agency? Most of the activities of a pension supervisory agency are already carried out by existing authorities, such as central banks, tax collectors and capital-market regulators, such as securities and exchange commissions or insurance regulators. Grafting responsibility for the new pension system onto these existing agencies would be efficient. But a new, specialized agency might be more effective, for a number for reasons. First, the scheme is mandatory, unlike other kinds of savings. So the government has a greater responsibility to ensure that managers comply with basic rules and are carefully supervised. Secondly, pensions are more complicated than most other forms of savings. They are long-term contracts and there are complex interactions between capital markets, insurance and social security. Thirdly, consumers are often suspicious of the efficiency and transparency of existing supervisory agencies. Existing pensions in some reforming countries were under-regulated or even unregulated in the past. Public confidence in the new system would be undermined if the perceived inadequacies of existing supervision were carried over to the new system. However, a new agency alone will not be sufficient. The financial system is interwoven. Problems elsewhere, in the banking system, for example, are likely to damage the new pension regime. And the same problems are likely to develop in the pension fund supervisor unless the underlying causes of regulatory ineffectiveness are addressed. The relationship between pension-fund supervisors and other agencies in OECD countries is shown in Figure 1. In six — including two former-socialist countries, Hungary and Poland— and France and Italy—an independent, separate pension-fund agency has been established. Pension funds fall under the insurance regulator in seven countries, including Germany, and are part of a universal financial-services supervisor in a further six, including Canada and the United Kingdom. Finally, ministries of finance or labor supervise funds directly in six countries, including Japan and the United States. T

Transcript

World Bank Pension Reform Primer

This note is part of the Pension Reform Primer series of the World Bank. It was written by Edward Whitehouse ofAxia Economics, London. Please contact the Social Protection Advisory Service, World Bank 1818 H Street NWWashington DC 20433, telephone +1 202 458 5267, fax +1 202 614 0471, e-mail [email protected] of the notes are on the internet at www.worldbank.org/pensions.

SupervisionBuilding public confidence in mandatory funded pensions

he regulation and supervision of individualpension accounts has been a neglected issue.

In contrast, much has been written on financingthe transition to funded pensions and the design ofbenefits. Yet effective regulation and efficientsupervision are crucial to the success of pensionreform. This note explores six issues in the designof a supervisory regime. It makes somecomparisons between the performance of agenciesin different countries and looks at four importantareas of supervision: institutional and financialcontrols, and membership and benefitsprocedures.

A new agency?Most of the activities of a pension supervisoryagency are already carried out by existingauthorities, such as central banks, tax collectorsand capital-market regulators, such as securitiesand exchange commissions or insuranceregulators. Grafting responsibility for the newpension system onto these existing agencies wouldbe efficient. But a new, specialized agency mightbe more effective, for a number for reasons. First,the scheme is mandatory, unlike other kinds ofsavings. So the government has a greaterresponsibility to ensure that managers comply withbasic rules and are carefully supervised.

Secondly, pensions are more complicated thanmost other forms of savings. They are long-termcontracts and there are complex interactions

between capital markets, insurance and socialsecurity.Thirdly, consumers are often suspicious of theefficiency and transparency of existing supervisoryagencies. Existing pensions in some reformingcountries were under-regulated or evenunregulated in the past. Public confidence in thenew system would be undermined if the perceivedinadequacies of existing supervision were carriedover to the new system.

However, a new agency alone will not besufficient. The financial system is interwoven.Problems elsewhere, in the banking system, forexample, are likely to damage the new pensionregime. And the same problems are likely todevelop in the pension fund supervisor unless theunderlying causes of regulatory ineffectiveness areaddressed.

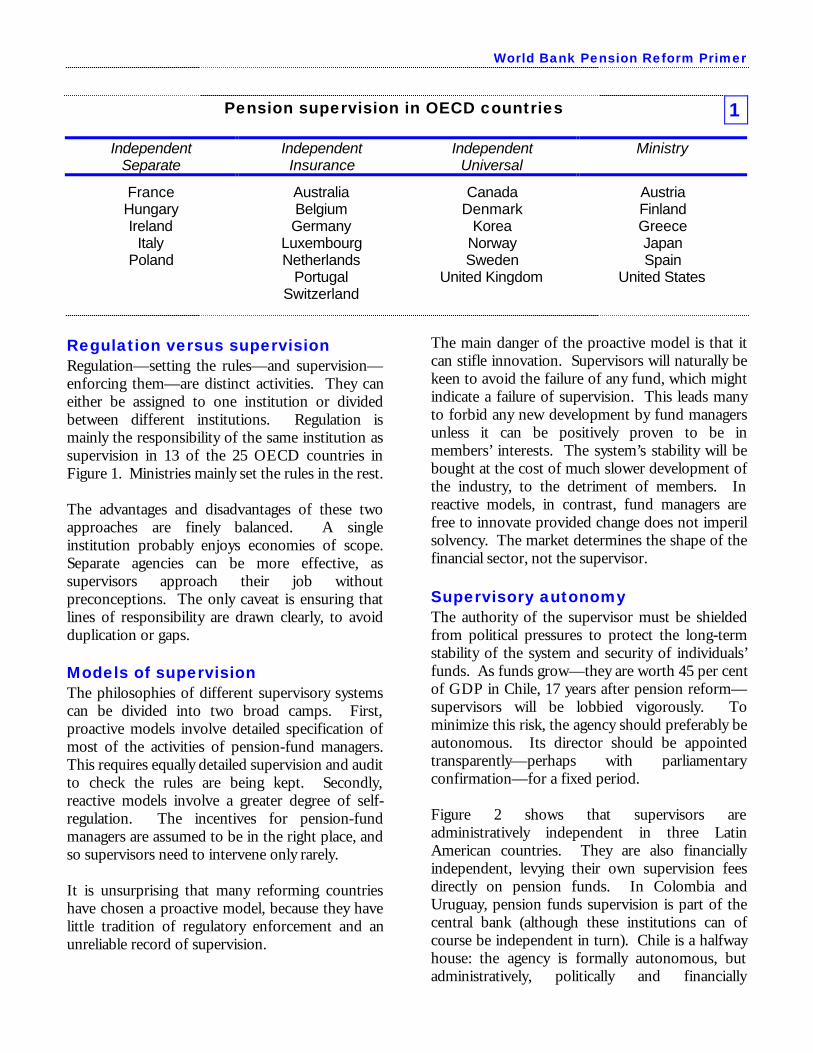

The relationship between pension-fundsupervisors and other agencies in OECD countriesis shown in Figure 1. In six — including twoformer-socialist countries, Hungary and Poland—and France and Italy—an independent, separatepension-fund agency has been established.Pension funds fall under the insurance regulator inseven countries, including Germany, and are partof a universal financial-services supervisor in afurther six, including Canada and the UnitedKingdom. Finally, ministries of finance or laborsupervise funds directly in six countries, includingJapan and the United States.

Regulation versus supervisionRegulation—setting the rules—and supervision—enforcing them—are distinct activities. They caneither be assigned to one institution or dividedbetween different institutions. Regulation ismainly the responsibility of the same institution assupervision in 13 of the 25 OECD countries inFigure 1. Ministries mainly set the rules in the rest.

The advantages and disadvantages of these twoapproaches are finely balanced. A singleinstitution probably enjoys economies of scope.Separate agencies can be more effective, assupervisors approach their job withoutpreconceptions. The only caveat is ensuring thatlines of responsibility are drawn clearly, to avoidduplication or gaps.

Models of supervisionThe philosophies of different supervisory systemscan be divided into two broad camps. First,proactive models involve detailed specification ofmost of the activities of pension-fund managers.This requires equally detailed supervision and auditto check the rules are being kept. Secondly,reactive models involve a greater degree of self-regulation. The incentives for pension-fundmanagers are assumed to be in the right place, andso supervisors need to intervene only rarely.

It is unsurprising that many reforming countrieshave chosen a proactive model, because they havelittle tradition of regulatory enforcement and anunreliable record of supervision.

The main danger of the proactive model is that itcan stifle innovation. Supervisors will naturally bekeen to avoid the failure of any fund, which mightindicate a failure of supervision. This leads manyto forbid any new development by fund managersunless it can be positively proven to be inmembers’ interests. The system’s stability will bebought at the cost of much slower development ofthe industry, to the detriment of members. Inreactive models, in contrast, fund managers arefree to innovate provided change does not imperilsolvency. The market determines the shape of thefinancial sector, not the supervisor.

Supervisory autonomyThe authority of the supervisor must be shieldedfrom political pressures to protect the long-termstability of the system and security of individuals’funds. As funds grow—they are worth 45 per centof GDP in Chile, 17 years after pension reform—supervisors will be lobbied vigorously. Tominimize this risk, the agency should preferably beautonomous. Its director should be appointedtransparently—perhaps with parliamentaryconfirmation—for a fixed period.

Figure 2 shows that supervisors areadministratively independent in three LatinAmerican countries. They are also financiallyindependent, levying their own supervision feesdirectly on pension funds. In Colombia andUruguay, pension funds supervision is part of thecentral bank (although these institutions can ofcourse be independent in turn). Chile is a halfwayhouse: the agency is formally autonomous, butadministratively, politically and financially

3 Supervision

dependent on the ministry of labor and socialsecurity.

FinancingA separate supervision fee is appealing comparedwith financing from the central budget. First, itbolsters the independence of the supervisoryagency. Secondly, it avoids cross-subsidies frompeople who do not participate in the new system.Argentina is a good example. The legislation sets abudget ceiling of 1.5 per cent of the pensionsystem’s total revenues. The agency then spendsas necessity dictates and takes periodic transfersfrom the managing companies (AFJPs) to coverexpenses. Budgeted costs have been below 0.5 percent of total revenues.

Supervision in Latin America 2

Government FundingAutonomousArgentina Labor ministry feeMexico Treasury fee (partial)Peru Economy ministry feeDependentBolivia Treasury feeChile Labor ministry budgetColombia Central bank feeUruguay Central bank budget

Staffing the supervisory agencyFinding the right staff for a new supervisoryagency can be a challenge. Professionals withbroadly relevant experience might be scarce. Andthe supervisory agency will be competing withpension-fund managers to hire qualified staff andto train others with the right aptitude.

It is important that the agency is able to attract andretain the right workforce, so it must be free tooffer competitive pay and benefits. This willprobably surpass the packages offered to othergovernment officials. But this is probablyunavoidable. In Argentina, for example, thepensions law requires that supervision employeesreceive a salary greater than or equal to the averagepaid by the 50 per cent of pension-fund managerswith the highest wages. This rule has the

advantage that salaries keep pace with the privatesector, where pay in financial services has tendedto increase more rapidly than in other industries.Other countries have set competitive salariesinitially, but these have eroded over time.

Although it might be tempting to staff the agencywith secondees from existing agencies anddepartments of government, this should beavoided. The agency will need a mix of staff withpublic- and-private sector experience. To ensurethat knowledge of the industry is kept up-to-date,there needs to be a continual flow of recruits fromthe fund-management industry, including at seniorlevels.

Supervisory ‘capture’The risk of a ‘revolving door’ between the fundmanagement companies and the supervisoryagency is that of industry capture, where thesupervisor puts the interests of the industry beforethe protection of pension-scheme members.

The best answer to this problem is a separation ofresponsibilities for the market as a whole fromindividual fund managers. Regulation and analysisof the system’s performance, where the damagefrom capture is large, can be separated fromprudential supervision, where detailed knowledgeof the industry is needed but the damage fromcapture is smaller.

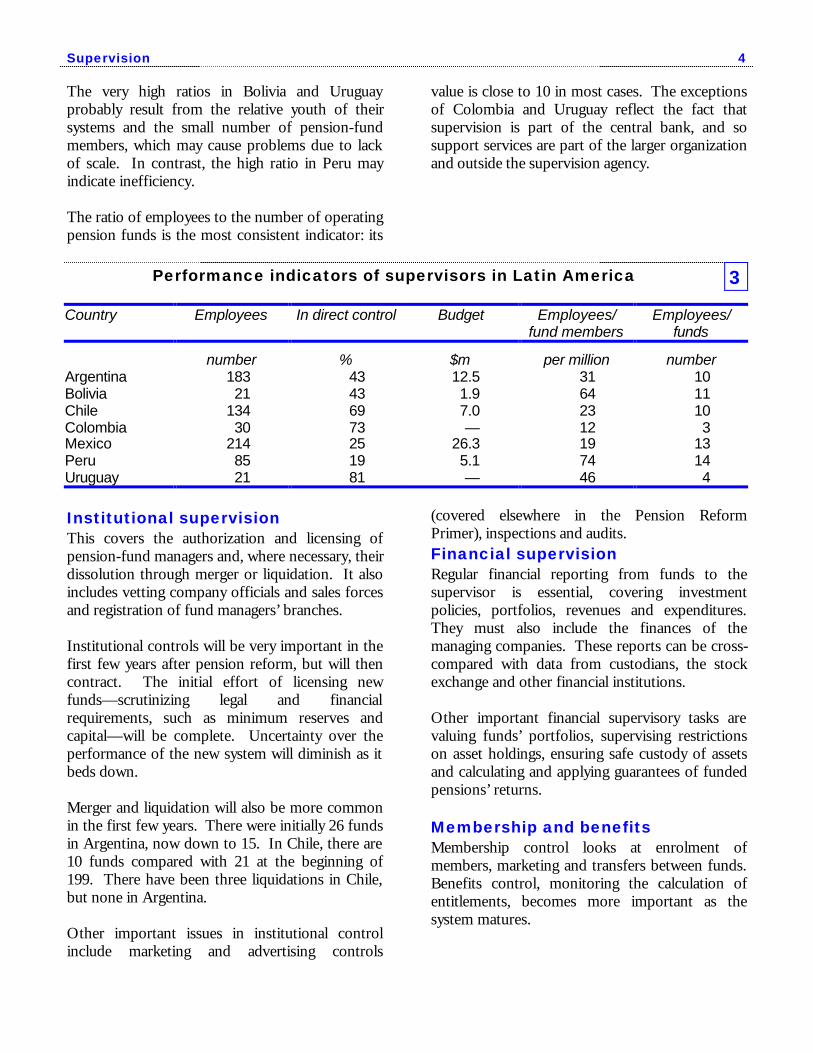

Supervisory performanceComparing different systems is complicatedbecause of their different characteristics. Figure 3concentrates on Latin America.

The Mexican agency is the largest and most costly,with 214 employees and a budget of $26 million.This probably reflects the fact that over 11 millionemployees are covered in Mexico, compared witharound 6 million in Argentina and Chile, 2½million in Colombia, just over 1 million in Peruand fewer than half a million in Bolivia andUruguay. Consequently, the ratio of supervisionemployees to pension-fund members is the secondlowest in Mexico, after Colombia.

Supervision 4

The very high ratios in Bolivia and Uruguayprobably result from the relative youth of theirsystems and the small number of pension-fundmembers, which may cause problems due to lackof scale. In contrast, the high ratio in Peru mayindicate inefficiency.

The ratio of employees to the number of operatingpension funds is the most consistent indicator: its

value is close to 10 in most cases. The exceptionsof Colombia and Uruguay reflect the fact thatsupervision is part of the central bank, and sosupport services are part of the larger organizationand outside the supervision agency.

Performance indicators of supervisors in Latin America 3

Country Employees In direct control Budget Employees/fund members

Employees/funds

number % $m per million numberArgentinaBoliviaChileColombiaMexicoPeruUruguay

18321

13430

2148521

43436973251981

12.51.97.0—

26.35.1—

31642312197446

1011103

13144

Institutional supervisionThis covers the authorization and licensing ofpension-fund managers and, where necessary, theirdissolution through merger or liquidation. It alsoincludes vetting company officials and sales forcesand registration of fund managers’ branches.

Institutional controls will be very important in thefirst few years after pension reform, but will thencontract. The initial effort of licensing newfunds—scrutinizing legal and financialrequirements, such as minimum reserves andcapital—will be complete. Uncertainty over theperformance of the new system will diminish as itbeds down.

Merger and liquidation will also be more commonin the first few years. There were initially 26 fundsin Argentina, now down to 15. In Chile, there are10 funds compared with 21 at the beginning of199. There have been three liquidations in Chile,but none in Argentina.

Other important issues in institutional controlinclude marketing and advertising controls

(covered elsewhere in the Pension ReformPrimer), inspections and audits.Financial supervisionRegular financial reporting from funds to thesupervisor is essential, covering investmentpolicies, portfolios, revenues and expenditures.They must also include the finances of themanaging companies. These reports can be cross-compared with data from custodians, the stockexchange and other financial institutions.

Other important financial supervisory tasks arevaluing funds’ portfolios, supervising restrictionson asset holdings, ensuring safe custody of assetsand calculating and applying guarantees of fundedpensions’ returns.

Membership and benefitsMembership control looks at enrolment ofmembers, marketing and transfers between funds.Benefits control, monitoring the calculation ofentitlements, becomes more important as thesystem matures.

5 Supervision

Conclusions and recommendations

q the professional expertise, transparencyand perceived independence ofsupervisory agencies is essential to thesuccess of pension reform

q in countries where existing regulation isweak or ineffective, a new, separateagency is probably best placed (but notcertain) to avoid repeating past failures

q a proactive model, with detailedspecification of funds activities might beneeded initially, but the system shouldmove towards reactive supervision overtime to avoid stifling innovation

q financial autonomy, with the agency’sbudget paid by pension funds rather thangeneral government revenues, willprotect supervision from undesirableshort-term political pressures

q administrative independence is similarlypreferable

q salaries must be competitive with theprivate sector (and remain so) to recruitqualified personnel from public andprivate sectors and to limit corruption risk

q separation of regulation and supervisioncan help limit the risk of regulatorycapture

Further readingDemarco, G. and Rofman, R. with Whitehouse,

E.R. (1998), ‘Supervising mandatory fundedpension systems: issues and challenges’, SocialProtection Discussion Paper no. 9816, WorldBank.

Rofman, R. and Demarco, G. (1999), ‘Collectingand transferring contributions in multipillarpension schemes’, Social ProtectionDiscussion Paper, forthcoming, World Bank.

Laboul, A. (1998), ‘Private pension systems:regulatory policies’, Ageing Working Paper no.2.2, OECD, Paris.

Vittas, D. (1998), ‘Regulatory controversies ofprivate pension funds’, in Institutional Investors inthe New Financial Landscape, OECD, Paris.