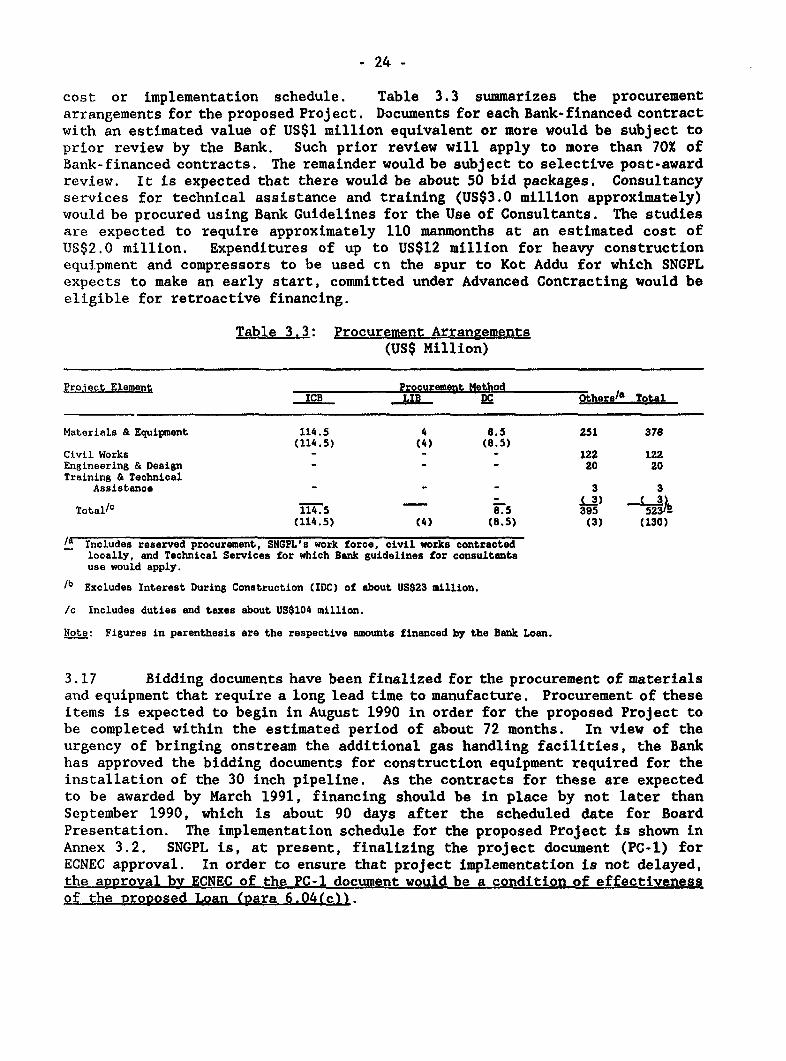

Document of The World Bank FOR OFFICIAL USE ONLY \9c/42 Report No.7407-PAK STAFF APPRAISAL REPORT PAKISTAN SUI NORTHERN GAS PIPELINESLIMITED (SNGPL) CGtPORATE RESTRUCTURING AND SYSTEM EXPANSION PROJECT JULY 12, 1990 Energy Operations Division Country Department I Europe, Middle East and North Africa Regional Office This document has a restricteddistribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

Document of

The World Bank

FOR OFFICIAL USE ONLY

\9c/42 Report No.7407-PAK

STAFF APPRAISAL REPORT

PAKISTAN

SUI NORTHERN GAS PIPELINES LIMITED (SNGPL)

CGtPORATE RESTRUCTURING AND SYSTEM EXPANSION PROJECT

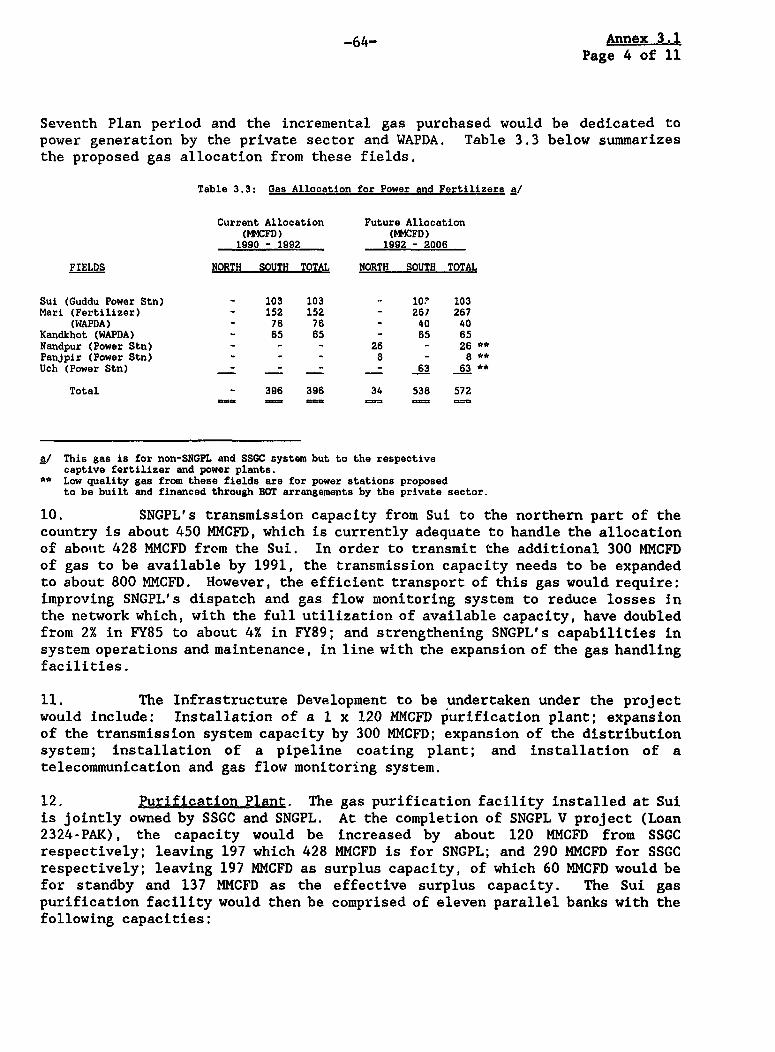

JULY 12, 1990

Energy Operations DivisionCountry Department IEurope, Middle East and North Africa Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENT

Currency Unit Pakistan Rupee (Rs)US$1.00 - Rs 21.50

MEASURES AND EOUIVALENTS

1 barrel (bbl) - 0.159 cubic meters1 metric ton of oil (0.85 specific gravity) - 7.4 bblMCF = 1,000 cubic ft.MMCF = 1 million cubic ft.MMCFD = 1 million cubic ft. daily1 BCF = 1 billion cubic ft.1 TCF = 1 trillion cubic ft.1 ton of crude oil equivalent (toe) = 1.0 ton of crude oil

ADB - Asian Development BankARL - Attock Refinery LimitedBOC - Burmah Oil CompanyBOT - Build-Operate-TransferCDWP - Central Development Working PartyCIP - Core Investment ProgramDGG - Directorate General of GasERG - Energy Review GroupESL I - Energy Sector Loan I (Loan 2552-PAK)ESL II - Energy Sector Loan II (Loan 3107-PAK)ECC - Economic Coordination CommitteeECNEC - Executive Cormnittee of the National Economic CouncilFY - Fiscal YearGDS - Gas Development SurchargeGOP - Government of PakistanICB - International Competitive BiddingIMF - International Monetary FundKESC - Karachi Electric Supply CompanyLES - Long-Term Energy StrategyLIB - Limited International BiddingMPNR - Ministry of Petroleum and Natural ResourcesMPD - Ministry of Planning and DevelopmentMOP - Ministry of ProductionMWP - Ministry of Water and PowerNDFC - National Development Finance CorporationNEPC - National Energy Policy CommitteeNFL - National Petroleum LimitedNRL - National Refinery LimitedOGDC - Oil and Gas Development CorporationPEPA - Pakistan Environmental Protection AgencyPERAC - Pakistan Refinery and Petrochemicals CorporationPFP - Policy Framework PaperPGCL - Pirkoh Gas Company LimitedPIDC - Pakistan Investment Development CorporationPMDC - Pakistan Mineral Development CorporationPOL - Pakistan Oilfields LimitedPPL - Pakistan Petroleum LimitedPRL - Pakistan Refinery LimitedPSEDF - Private Sector Energy Development FundPSO - Pakistan State Oil LimitedSCADA - Supervisory Control and Data AcquisitionSNGPL - Sui Northern Gas Pipelines LimitedSSGC - Sui Southern Gas CompanyWAPDA - Water and Power Development Authority

GOP's Fiscal Year (FY)

July 1 - June 30

FOR OFFICIAL USE ONLY

PAKISTAN

SUI NORTHERN GAS PIPELINES LIMITED (SNGPL)

CORPORATE RESTRUCTURING AND SYSTEM EXPANSION PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

LOAN AND PROJECT SUMMARY .............................. i

I. ENERGY SECTOR .............................. 1

A. The Economy ....................................... 1

B. Sectoral Setting .................................. 2

C. Developments in the Sector, FY79-FY88 .............. 4

D. Natural Gas Subsector ............................. 5

E. Bank Group's Role in the Energy Sector andExperience with Past Lending .................... 10

II. THE BORROWER .11

III. THE PROJECT ..................... 15

IV. FINANCIAL ASPECTS .27

V. ECONOMIC JUSTIFICATION .33

VI. AGREEMENTS REACHED AND RECOMMENDATIONS .36

This report was prepa.ed by Messrs. A. Oduolowu (Senior PetroleumSpecialist), M. Sharma (Economist), C. Schroeder (Senior Financial Analyst),M. Shirazi (Senior Gas Specialist) and M. Mengesha (Procurement Specialist-Consultant). Secretarial assistance was provided by Mmes. Anne Haldar,Young Hong and Hannah Pratt.

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ANNEXES

Page No.

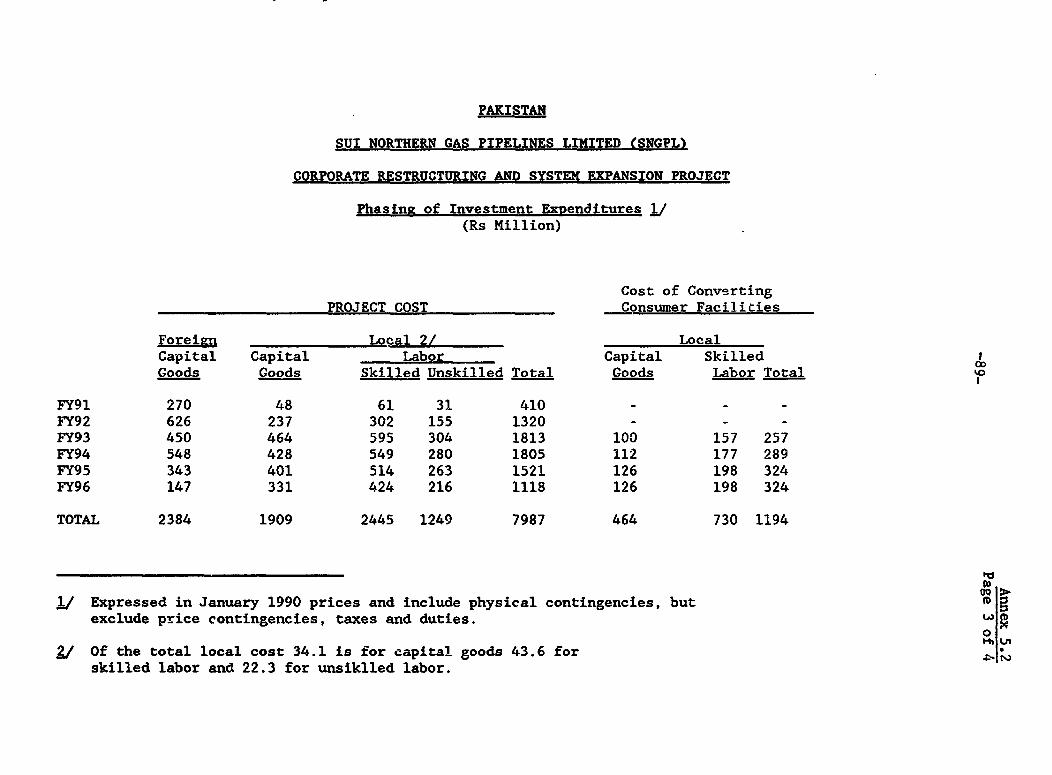

1.1 Organization of the Energy Sector .......................... 401.2 Details Relating to Long-Term Energy Strategy (LES) ........ 411.3 Proven Gas Reserve Estimates ............................... 511.4 Summary of Probable Gas Reserves ........................... 521.5 Summary of Gas Analysis .................................... 531.6 Historical Trends in the Consumption of Gas by Sectors ...... 541.7 Historical Developments in the Consumption

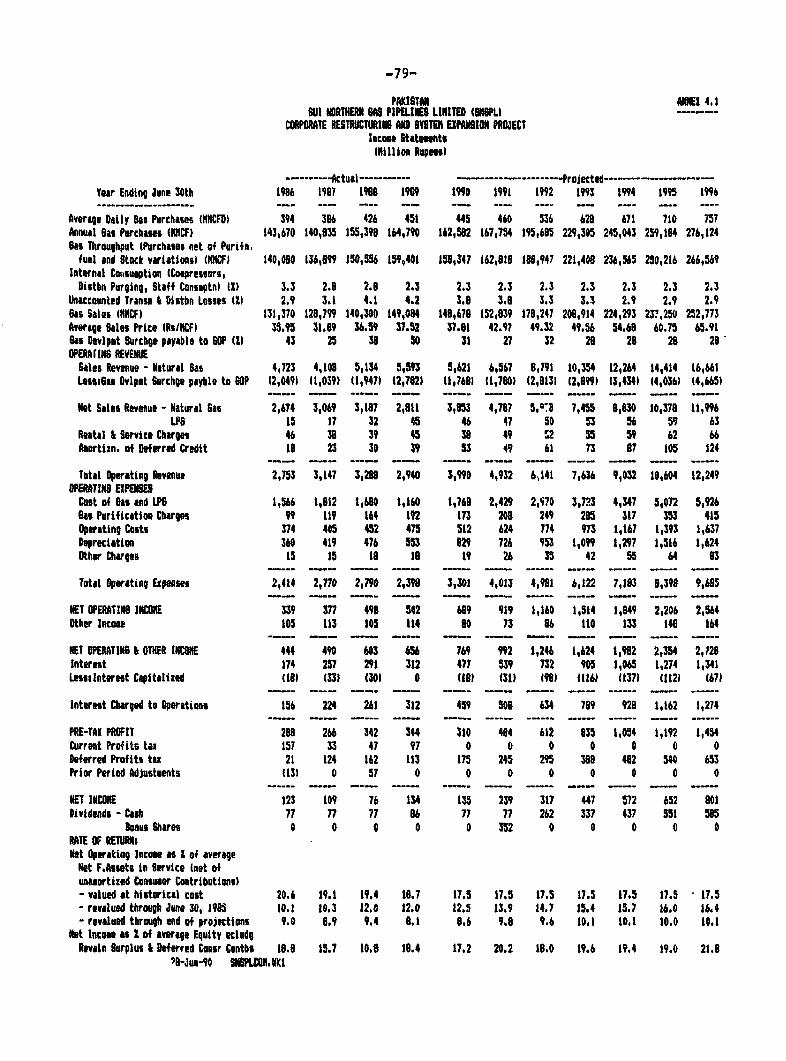

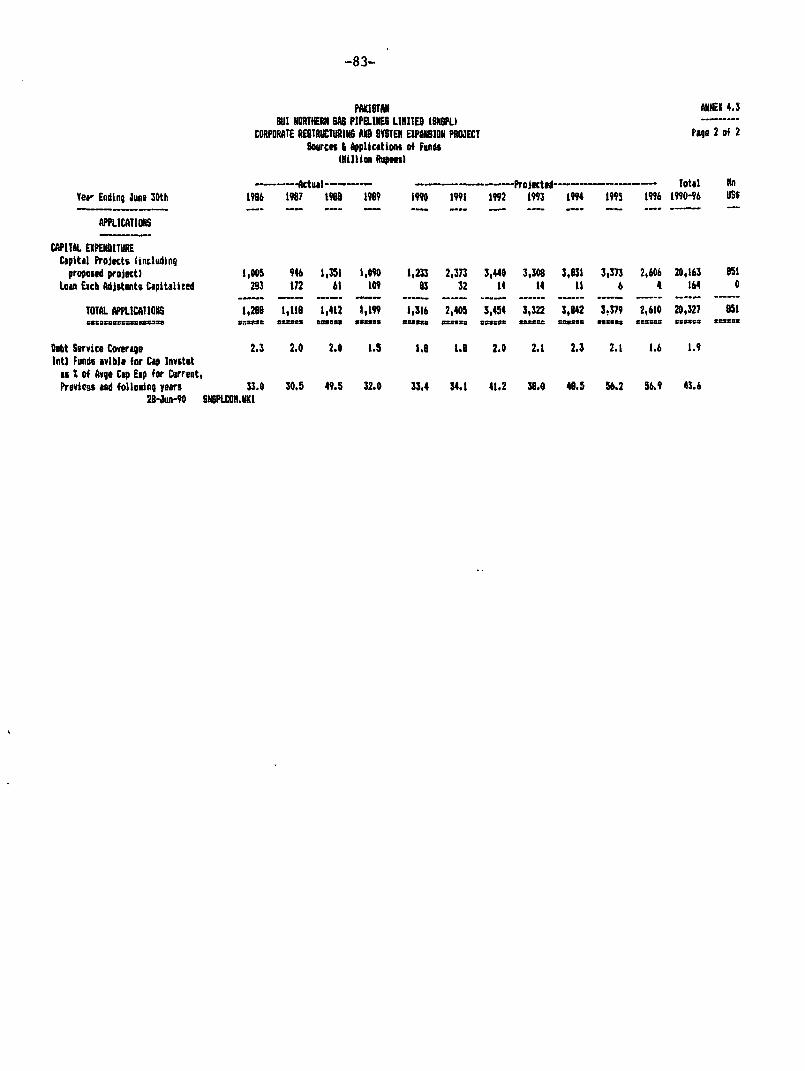

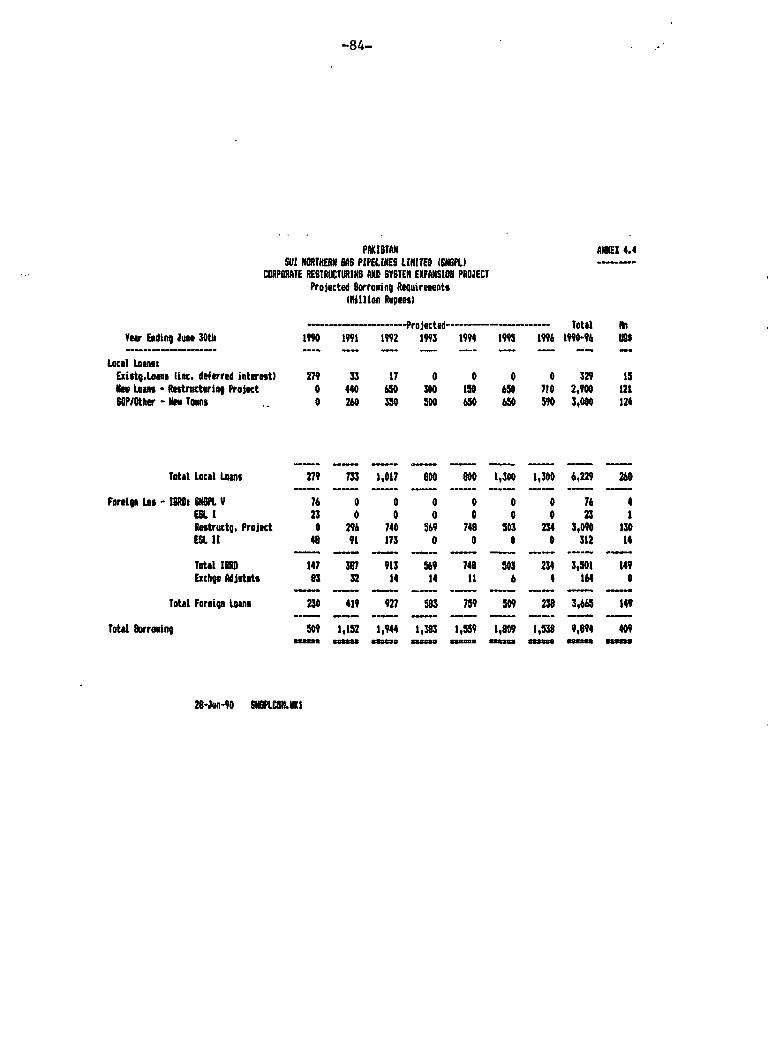

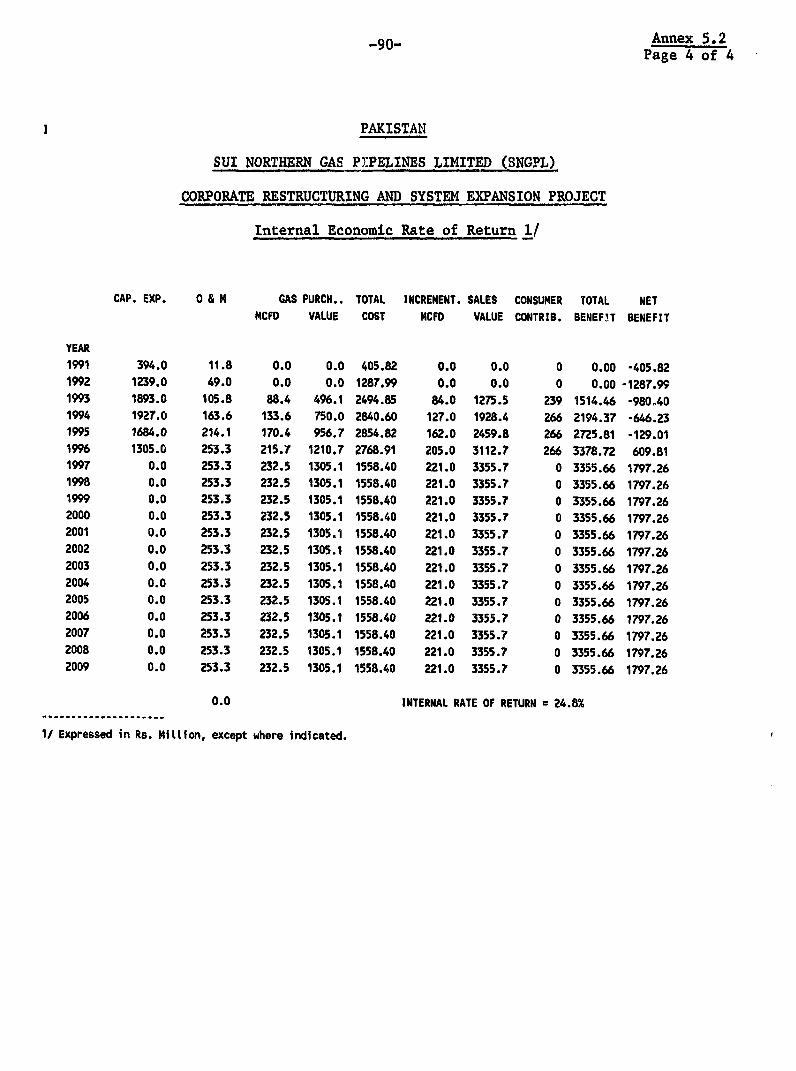

of Gas (1971-1989) ........................................ 551.8 Production Forecast by Fields ............................... 561.9 Forecast of Transmission System Requirements of Gas ......... 582.1 Composition of SNGPL's Equity Ownership ..................... 592.2 SNGPL - Organization Chart .................................. 603.1 Detailed Project Description ................................ 613.2 Implementation Schedule ..................................... 723.3 Project Cost ................................................ 733.4 Disbursement Schedule ....................................... 753.5 Bank Supervision Input Into Key Activities ................. 764.1 Income Statements ........................................... 794.2 Balance Sheets ............................................. 804.3 Sources & Applications of Funds ............................. 824.4 Projected Borrowing Requirements ................... ........ 844.5 Projected Investment Program ................................ 855.1 SNGPL's Actual and Forecast Sales of Gas .................... 865.2 Assumptions and Calculation for the Rate of Return .......... 876.0 Selected Documents in Project File .......................... 91

MAP IBRD No. 20961R1

- i -

PAKISTAN

SUI NORTHERN GAS PIPELINES LIMITED (SNGPL)

CORPORATE RESTRUCTURINIG AND SYSTEM EXPANSION PROJECT

LOAN AND PROJECT SUMNARY

Borrower: Sui Northern Gas Pipelines Limited (SNG't)

Guaranto_: Islamic Republic of Pakistan

Amount: US$130 million equivalent

Terms: Twenty years, including a five-year grace period, atthe Bank's standard variable interest rate.

Project Description: The proposed Project would cover three components:Corporate Restructuring of SNGPL, InfrastructureDevelopment, and Consultancy Services and Training.Corporate Restructuring of SNGPL would involve: (a)restructuring of SNGPL's ownership through issuance ofnew additional equity shares to dilute public sectorownership initially from 91% to 51%, and subsequentlyto at most 40%; (b) restructuring SNGPL's Board ofDirectors to reflect the new shareholding; (c)establishing financial performance criteria to improveits efficiency and ability to raise equity; and (d)reviewing the regulatory functiors of t1-: DirectorateGeneral of Gas. Infrastructure Developmeni. would providefor: (a) installation of a 1 x 120 MKCFD gaspurification plant at Sui; (b) expansion of thetransmission system capacity by about 300 MMCFD; (c)expansion of the distribution network to supply naturalgas by FY96 to new domestic, commercial, and industrialconsumers, 2 fertilizer plants and the power station atKot Addu; (d) installation of a linepipe coating plant;(e) installation of a telecommunication system formonitoring the operations of the network; and (f)procurement of compressors and construction equipmentrequired for the installation of the linepipe.Consultancv Services and Training would cover: (a)safety and hazard assessment survey of the transmissionand distribution system; (b) upgrading the capabilityof the Directorate General of Gas, and training of SNGPLstaff through a collaborative arrangement with a foreignprivate gas utility; (c) development of SNGPL's financialmanagement information systems and data processing andtraining in internal auditing of computerized accountingsystems; (d) designing the new formula for settingSNGPL's prices net of the Gas Development Surcharge and

- ii -

performance criteria; (e) services of financial advisersand an underwriter or consortium of underwriters tomanage the issuance of shares; and (f) design,engineering and supervision of high pressure pipelineconstruction at river crossings.

Benefits: The proposed Project would assist GOP in restructuringSNGPL with a view to increasing its autonomy and abilityto mobilize resources from the financial capital marketsand the general public, as well as expanding theutility's transmission and distribution network at leastcost. Specific benefits under the proposed Project areexpected from: (a) increased private sector investmentin SNGPL, supporting GOP's fiscal reforms by restrainingthe growth of public debt; (b) incremental sales of gasto new consumers; (c) incremental consumer investmentcontributions; and (d) substitution of gas for highervalue petroleum products which, at the margin, areimported.

Risks: The main risks associated with the proposed Project are:(a) inability of SNGPL to raise the required financialresources from the capital markets; (b) delays in theimplementation of the proposed Projen.t because of itsrelatively large size compared to past investmentsundertaken by SNGPL; (c) a decline in the productivityof the gas fields to a level lower than forecast; and(d) environmental impact from possible gas leakages.These risks are being addressed through the provisionof: (a) professional services of a financial adviserand underwziters tc assist SNGPL in managing themarketing of equity shares in the doLestic capitalmarket; (b) consultancy services for the engineering,design and supervision of the construction of the highpressure pipelines and the establishment of acollaborative arrangement with an experienced foreignprivate sector utility to assist SNGPL in projectimplementation, as well as train its staff in pipelineoperation and maintenance and establishment of adequatesafety measures including the installation of a new SCADAsystem to monitor gas flows and detect faults along thesystem; and (c) technical assistance and consultancyservices under ESL II for the development of the Lotifield, and under Pirkoh III Development Project, financedby the Asian Development Bank for the development of thePirkoh field, and assistance to OGDC under the proposedDomestic Resources Development Project, for theaccelerated development of new gas fields.

- iii -

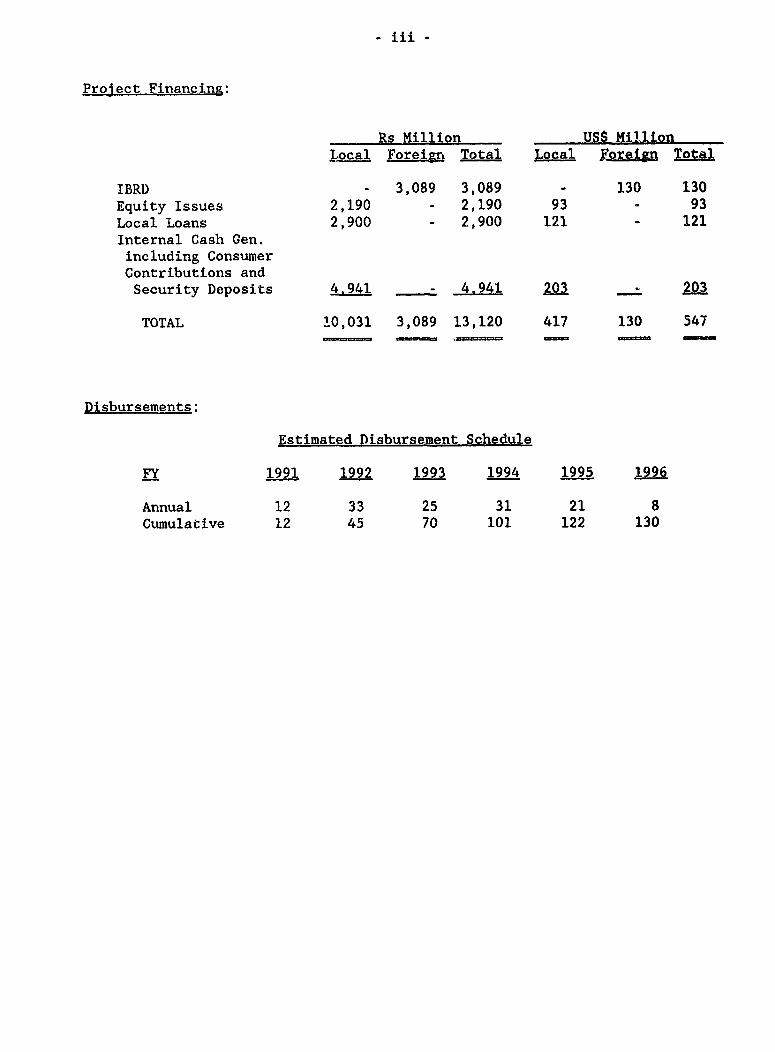

Project Financing:

Rs Million USS MillionLocal Foreign Total Local ForIign Total

CORPORATE RESTRUCTURING AND SYSTEM EXPANSION PROJECT

STAFF APPRAISAL REPORT

I. ENERGY SECTOR

A. The Economy

1.01 Pakistan's economic performance during the period FY79-88 comparesfavorably with that of many developing countries. Growth in GDP, averaging about6.5% annually, was accompanied by a steady docline in inflation from 10% in FY79to 6% in FY88. Despite these achievements, macroeconomic imbalances had becomea concern by FY88. Specifically, as public expenditures had increased fasterthan revenues in the 1980s, the fiscal deficit increased from 5% of GDP in FY80to 8.7% in FY88. Inflation also began to increase in that year, reaching 10%in FY89. While merchandise export volume continued to grow, a deterioration inthe terms of trade and geneially accommodative domestic credit contributed toan overall increase in the trade deficit. These developments together with thecontinuing erosion in remittances from Pakistanis abroad brought the currentaccount deficit to about 4.3% of GNP in FY88. More critically, the CentralBank's gross foreign reserves at end-FY88 were equivalent to less than two anda half weeks of annual imports of goods and services, and less than the externalshort-term liabilities of the banking system.

1.02 As the emerging imbalances were likely to become a major impediment tosustaining economic growth of about 5.5% or more annually, as was envisaged forthe Seventh Plan period (FY89-93), the Government of Pakistan (GOP), inconsultation with the International Monetary Fund (IMF) and the Bank, initiateda medium-term macroeconomic adjustment and structural reform program aimed atfostering strong economic growth while ensuring domestic and external financialstability. The key requirements of the program, which initially covered theperiod FY89-91, are: (a) a reduction of the fiscal deficit, through an enlargedsales tax and other measures to broaden the tax base and the substantialcontainment of the growth of expenditures; (b) implementation of additional tradepolicy reforms with significant liberalization of non-tariff barriers; and (c)initiation of reforms in key sectors, such as finance, agriculture and energy,that will be important to improving the efficiency and growth potential of theeconomy. In support of GOP's program, the IMF's Executive Board approved onDecember 28, 1989, a three-year arrangement under the structural adjustmentfacility for a cumulative amount of SDR 347 million and a first annualarrangement for SDR 109 million, as well as a 15-month stand-by arrangement foran amount of SDR 273 million. The Bank's Executive Directors, discussed thepolicy framework paper in December 1988. The Bank approved an AgriculturalSector Adjustment Loan for US$200 million in August 1988, a Financial SectorAdjustment Loan for US$150 million in March 1989, and a Second Energy Sector Loan(ESL II; Loan 3107-PAK) for US$250 million in June 1989. The proposed Projectfits into the overall framework of the ESL II program of structural reforms and

- 2 -

is designed to support the corporate restructuring of Sui Northern Gas PipelinesLtd. (SNGPL) and assist in expanding, at least cost, its transmission anddistribution capacity for the supply of gas to new consumers whose energyrequirements are currently being met by higher value petroleum products, the bulkof which are imported.

1.03 Implementation of the policy measures tinder the FY89 adjustment programhas been broadly on track with respect to the liberalization of the trade regime,tariff rationalization, industrial incentives, domestic credit restraint and theflexible management of the exchange rate. Tnese policies have contributed toan increase in private investment, a slowing of inflation toward the end of FY89,and an increase in export volumes despite the severe floods, disturbances inmajor industrial cities and the constraints on development expenditures.However, several economic problems surfaced in 1989. The external currentaccount deficit instead of declining from 4.3% of GNP in FY88 to 3.4% of GNP inFY89 as programmed, widened to 4.7%, and international reserves remained at avery low level, mainly as a result of a deterioration in the terms of trade.The fiscal deficit, while still falling from 8.3% of GDP to 7.3% of GDP in FY89,was higher than the target of 6.7%. Revenues increased as projected butexpenditures grew faster than originally foreseen, mainly because of increasesin subsidies linked to higher than projected import of wheat. Consequently,following a review in September 1989, the date for achieving the end-programmacroeconomic targets was extended by one year to FY92 with IMF and World Bankconcurrence, while the schedule for policy reforms remained unchanged.

1.04 During the first nine months of FY90, the second year of the program,the macroeconomic situation has generally improved. Overall economic growth willprobably exceed 5%, industrial output has recovered, private investments appearstrong and a good wheat crop is expected. Inflation has been reduced to below6%. Preliminary fiscal data reviewed by an IMF mission in May 1990 indicate thatthe budget deficit for FY90 is likely to exceed the target by about 0.5% of GDP,primarily because of larger than programmed defense spending. This expenditureoverrun is also expected to lead to a slightly larger external current accountdeficit than targeted (by about US$0.1 billion or less than 0.2% of GDP) onaccount of larger defense rela'Ued imports. Exports, other than rice and cotton,on the other hand, are expected to be on target. While the IMF mission in naywas unable to complete its work for the second review under the StandbyArrangement, the IMF's management has agreed to extend the scheduled review fromend-June to end-November 1990 as GOP has initiated measures to comply with thetwo end-March performance criteria and reiterated its commitment to achievingthe agreed overall fiscal deficit target of 5.5% of GDP in FY91.

B. Sectoral Setting

1.05 Energy Resources. Pakistan's commercially exploitable energy resourcesconsist of about 30,000 MW of hydropower potential, 16 trillion cubic feet (TCF)of proven and 6.3 TCF of probable reserves of natural gas, 175 millioin tons ofproven and 725 million tons of probable reserves of coal and lignite, and 54million tons of proven and 4 million tons of probable reserves of oil. Thecountry also has a relatively large base of traditional fuels in form of fuelwood

and agricultural and animal waste, which play a crucial role in meeting theenergy needs of the rural consumers. However, as the consumption of fuelwoodis already in excess of what can be replenished through reforestation and thesupplies of biomass are diminishing on a per capita basis, the share oftraditional fuels in the overall supply of energy is expected to decline relativeto that of commercial energy resources. As a consequence, and given the modestreserves of oil and the technical limits on the economic substitution of coaland gas for petroleum products, as well as the long lead time and substantialfinancial resources required to bring the major hydro sites on stream, Pakistanis expected to remain dependent on imported energy over the foreseeable future.The rate of growth of energy imports could be contained, however, by:restraining the growth of demand for energy through price and non-price measuresincluding rehabilitation and retrofitting of power plants, refineries and energyintensive industries; accelerating the development of smaller hydropower sitesand also of oil, gas and coal and encouraging the substitution of the latter aswell as that of imported coal for higher value petroleum products; andstrengthening implementation capabilities of entities involved in the sector.

1.06 Institutional Setting. Four ministries share the responsibility forthe energy sector: the Ministry of Petroleum and Natural Resources (MPNR), theMinistry of Water and Power (MWP), the Ministry of Production (MOP), and theMinistry of Planning and Development (MPD). Coordination between the ministrieson energy matters is provided by the Energy Wing of MPi, which acts as asecretariat for the National Energy Policy Committee (NEPC) and Energy ReviewGroup (ERG). NEPC is responsible for the formulation of GOP's overall energypolicy. The review of the investment plans of the sector and the approval ofenergy pricing proposals is under the Jurisdiction of the Economic CoordinationCommittee (ECC). The Executive Committee of the National S_onomic Council(ECNEC) and the Central Development Working Party (CDWP) review and approve majorproposals and projects for all sectors, including energy.

1.07 The day-to-day management and operation of the energy sector is vestedin a number of public and private sector entities. The public sector entitiesare: the Water and Power Development Authority (WAPDA), which is responsiblefor developing Pakistan's water resources and for the construction, operationand maintenance of power generation, transmission and distribution facilitiesthroughout the country, except the Karachi area; the Oil and Gas DevelopmentCorporation (OGDC) for exploration and development of oil and gas; the PakistanMineral Development Corporation (PMDC) for the exploration and development ofmineral resources; the State Petroleum Refinery and Petrochemical Corporation(PERAC) and the National Refinery Limited (NRL) for processing crude oil; andNational Petroleum Limited (NPL) for a proposed hydrocracker project. Alsoinvolved in the energy sector are a number of semi-autonomous entities in whichGOP has, either directly or through public financial institutions, a controllinginterest. These are: Karachi Electric Supply Corporation (KESC), which isresponsible for the construction, operation and maintenance of power generationfacilities, as well as the transmission and distribution for electricity supplyin the Karachi area; SNGPL and the Sui Southern Gas Corporation (SSGC) for thetransmission and distribution of natural gas; and Pakistan State Oil Limited(PSO) for marketing and distribution of petroleum products. Private sectorentities include: a large number of Pakistani coal mining companies; tworefineries, the Attock Refinery Limited (ARL) and Pakistan Refinery Limited

. 4 -

(PRL); and several oil and gas development companies including Pakistan PetroleumLimited (PPL), Pakistan Oilfields Limited (POL), the Fauji Foundation, UnionTexas, Occidental Petroleum Limited .id other international oil companies injoint ventures with OGDC. As shown in the organization chart of the energysector (Annex 1.1), all operational entities (public and semi-autonomous) areunder the jurisdiction of MPNR, except for WAPDA, KESC, NRL and PRL. MWP hasjurisdiction over WAPDA and KESC and MOP over NRI, and NPL. In addition, theDepartment of Forestry, in the Ministry of Agriculture is responsible forafforestation and the Pakistan Environmental Protection Agency for issuesrelating to the implementation of GOP's environmental policies.

C. Developments in the Sector. FY79-FY88

1.08 The Fifth Plan (FY79-FY83) ewphasized the accelerated development ofdomestic energy resources and rationalization of energy prices. Financial andimplementation constraints, however, impeded the achievement of the supplytargets for all energy products except natural gas. The largest shortfall wasin the oil and power subsectors where only 64% and 50% of the output targets,respectively, were achieved. These shortfalls, together with the rapid growthof consumption, precipitated by GOP's policy of underpricing energy in an effortto stimulate economic growth, increased the country's dependence on importedenergy. In recognition of the growing supply gap, GOP accorded high priorityto restructuring the sector during the Sixth Plan (FY84-FY88). Its objectiveswere to accelerate and rationalize the development of energy, correct distortionsin energy pricing, streamline the institutions and agencies in the sector andincrease private sector involvement in the development, production and deliveryof energy. However, as these objectives were not translated into concretepolicies and programs, in the first two years of the Plan, only one-half of theplanned investment program for the sector was implemented, energy prices wereallowed to decline in real terms, and the institutions in the sector remainedunresponsive to the pressing needs of the economy. These setbacks prompted GOPto formulate a Long-Term Energy Strategy (LES), covering the period 1986-2010.It calls for implementing integrated programs of structural reforms over five-year intervals, corresponding to the planning cycle, in the areas of: resourcedevelopment and energy investments; pricing, resource mobilization and demandmanagement; and institutional development.

1.09 To assist GOP in implementing the reforms called for by LES, a seriesof sector loans was envisaged by the Bank, each in support of a monitorable coreprogram of policy actions and priority investments, which would form the umbrellafor the Bank's lending for specific energy investments and for the more effectivecoordination of external financing for the sector. The first phase of thesereforms was implemented successfully under the first Energy Sector Loan (ESL I,Loan 2552-PAK) during the last three years of the Sixt'. Plan (FY86-88). Supportfor implementing the second phase, which constitutes an integral part of themedium-term structural adjustment and policy reform program, is being providedunder ESL II (para 1.02), covering the first three years of the Seventh Plan(FY89-92). Details relating to LES and review of the progress made in itsimplementation under ESL I and ESL II are presented in Annex 1.2.

- 5 -

D. Natural Gas Subsector

Organization of the Subsector

1.10 MPNR has overall responsibility for the development of the oil andnatural gas subsector. The downstream activities for the natural gas subsectorare discharged through the Directorate General of Gas (DGG), one of the fiveDirectorates in the Ministry. DGG functions as a regulatory body and, inaccordance with the Natural Gas Ordinance of 1967, is responsible for overseeingthe operations of the gas transmission and distribution companies which, interalia, include a review of their investment programs, as well as the harmonizationof their forecasts of demand for gas. DCG, together with the Ministry ofFinance, also reviews the financial performance of the transmission anddistribution companies and assists them in mobiliz.ng resources for theirinvestment programs. In addition, DGG recommends changes in the procedures forallocating gas to regions and consumer categories and in the level and structureof the consumer price of gas. These recommendations, however, require theapproval of ECC and the Cabinet prior to implementation (para 1.06).

1.11 Pakistan has two principal gas transmission systems, the northern andsouthern systems. The northern system, managed by SNGPL, supplies gas to thecities of Multan, Faisalabad, Lahore, Gujranwala, Islamabad and Peshawar fromthe Sui gas field and other gas fields in the Potwar area. The southern system,managed by SSGC, runs south from the Sui Field to serve both sides of the Indusriver valley and the major cities of Karachi and Hyderabad. In addition, thereare three smaller systems: (a) the Quetta pipeline, owned by SSGC, transportsgas from the Sui field to the city of Quetta; (b) the Mari system, ow;red by theFauji Foundation, supplies gas to three fertilizer plants; and (c) two separatepipelines owned by WAPDA transmit gas from the Sui, Mari and Kandkhot fields tothe Guddu power station.

Gas Reserves

1.12 Natural gas was first discovered at Sui in 1952. Since then severalother fields have been discovered, including the non-associated gas fields atMari, Khandkot, Pirkoh, Loti, Qadirpur and Kadanwari; the condensate fields atDhodak, Dhurnal, Dakhni and Adhi; and low quality gas fields at Uch, Panjpir andNandpur. As noted (para 1.05), proven recoverable reserves of gas are estimatedat about 16 TCF (400 mtoe) and probable reserves at about 6.3 TCF (156 mtoe)(Annexes 1.3 and 1.4). All of the non-associated gas fields are located aroundthe Sui region in the central part of the country. These fields account forabout 80% of total recoverable reserves. The quality of gas in Pakistan, interms of heating value, varies from field to field. The location of the maingas fields is shown on the attached map (IBRD No. 20961R1) and the averagecomposition of the gas from the major fields is given in Annex 1.5.

Historical Developments in the Consumption and Supply of Gas

1.13 Consumption of gas increased between FY71 and FY89 at an average annualrate of 7.5%, from 294 MMCFD to 1,081 MMCFD (Annex 1.6). However, the rate ofgrowth of consumption has declined significantly since FY82, from an average of9.3% between FY71 and FY82 to 4.7% between FY82 and FY89. This decline is

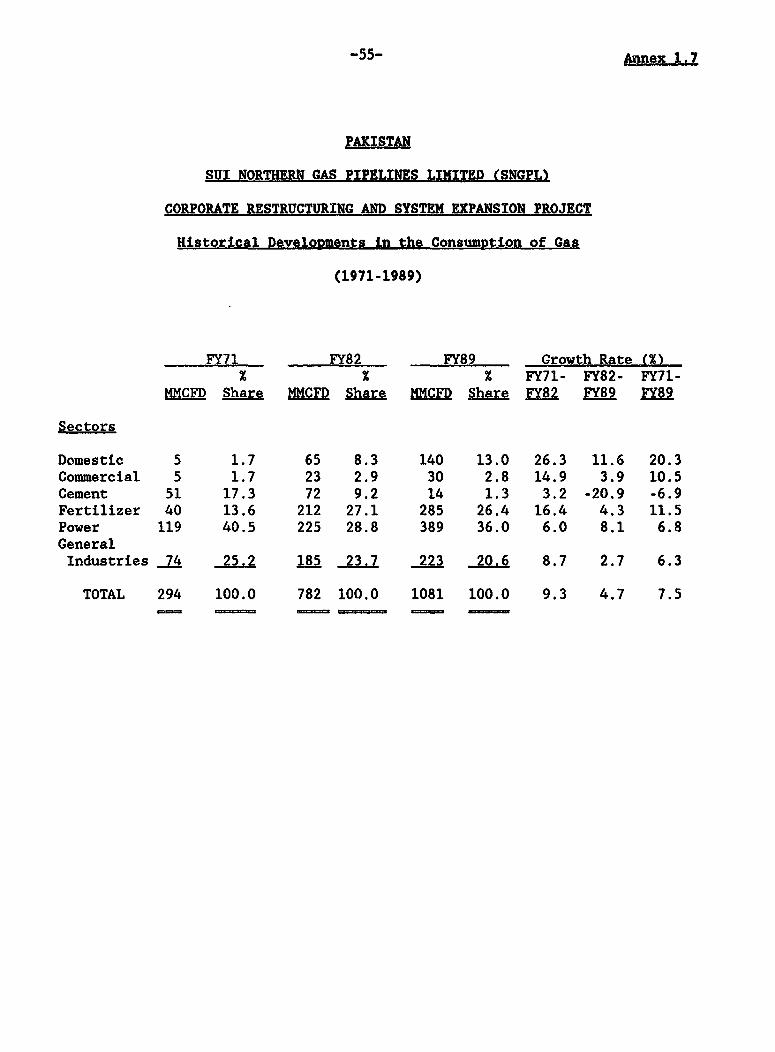

attributable to supply constraints caused by GOP's past policy of settingproducer prices for gas at levels which failed to provide producers theincentives needed to increase output from existing fields and bring intoproduction already discovered fields (para 1.19). Moreover, as GOP's consumerpricing policy was inappropriate for restraining the growth of demand, shortagesof gas started to emerge in 1981 (para 1.08). In response to these shortages,GOP initiated a number of measures aimed at rationalizing the consumption andsupply of gas. On the demand side, a gas allocation procedure was adopted topromote the substitudion of fuel oil and coal for gas. Accordingly, gas wasreleased from the cement industry for use by households and its supply to othernew industrial consumers was curtailed to nine months each year. The supply ofgas to the power subsector was also fixed as was the number of connections tobe provided to domestic and commercial consumers. The allocation of gas,together with a nearly three-fold increase in the consumer price of gas betweenFY81 and FY89 (para 1.20), resulted in a marked shift in the shares of gasconsumed by the main sectors of the economy, especially the residential sectorand the cement and power subsectors. As shown in Annex 1.7, between FY82 andFY89, the share of the cement subsector declined from 9.2% to 1.3%, while thoseof the residential sector and the power subsector increased from 8.3% and 28.8%to 13.0X and 36.0%, respectively. As for the other sectors, their shares haveremained virtually unchanged and as of FY89, these were about 2.8% for thecommercial sector; 26.4% for the fertilizer industry; and 21% for the industrialsector.

1.14 On the supply side, GOP concluded agreements on gas producer priceswith PPL and the Fauji Foundation in 1982 and 1984, respectively, to providethese producers additional incentives to increase their output from the Sui andMari gas fields. Under ESL I a new gas producer formula was adopted and athree-year Core Investment Program (CIP) for exploration and development wasoutlined (para 1.19). It covered three main elements: (a) the appraisal anddevelopment of fields to be undertaken by OGDC using its own resources andbudgetary allocations; (b) exploration and development activities to beundertaken through existing joint ventures; and (c) new joint ventures inprospective areas for which further effort was to be made in mobilizing privatesector participation. The joint ventures were intended to supplement OGDC'stechnical capabilities and mobilize resources for exploration and development.The implementation of these measures has enabled GOP to conclude twenty-one newjoint venture contracts; accelerate the development of Pirkoh, Loti, Dakhni,Nandpur and Panjpir fields; increase the recoverable reserves by about 4.63 TCF,and the output of gas from about 300 BCF (7.5 mtoe) in FY83 to about 395 BCF (9.5mtoe) in FY89. Moreover, in order to further encourage private sectorinvolvement in petroleum exploration and development in Pakistan, GOP promotedthe available acreages for exploration in December 1988 in Houston and London.As the response of private sector to the promotion was highly favorable, GOP hasfurther revised the gas producer price formula for new offshore concessions tosustain this momentum (para 1.19).

Forecast of Supply and Demand for Gas

1.15 The gas supply and demand forecast for the period FY90-FY2006, preparedby GOP in the context of a gas utilization and demand management study completedin December 1987, was revised by GOP under ESL II to take into account the recent

- 7 -

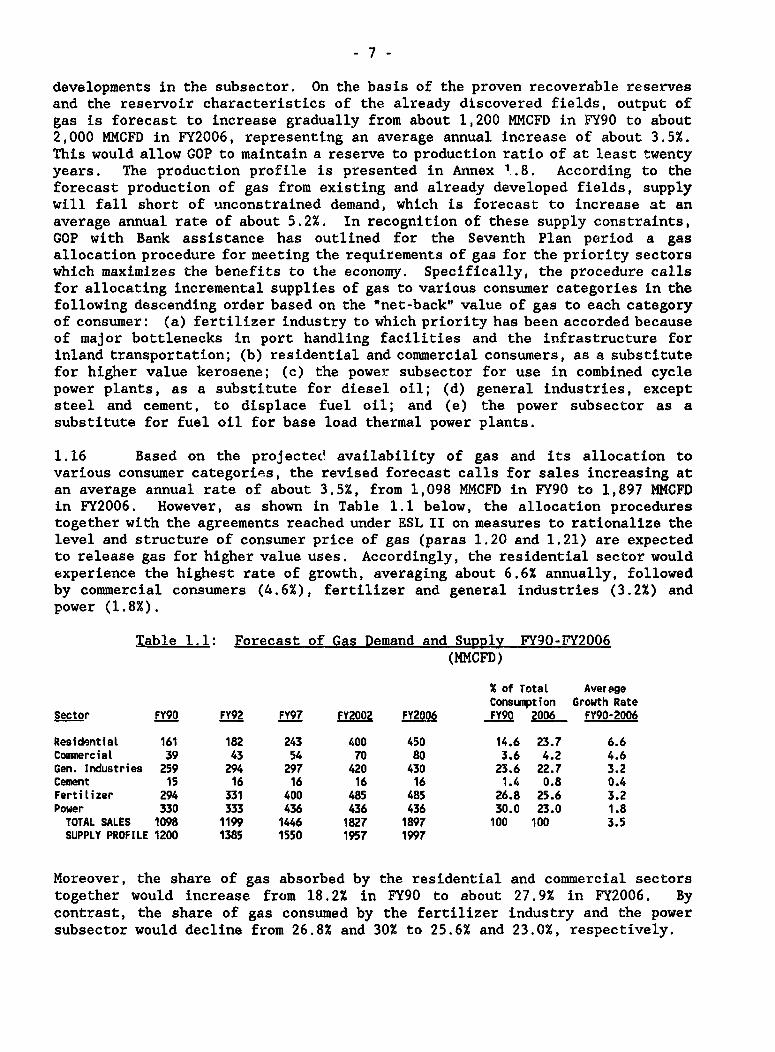

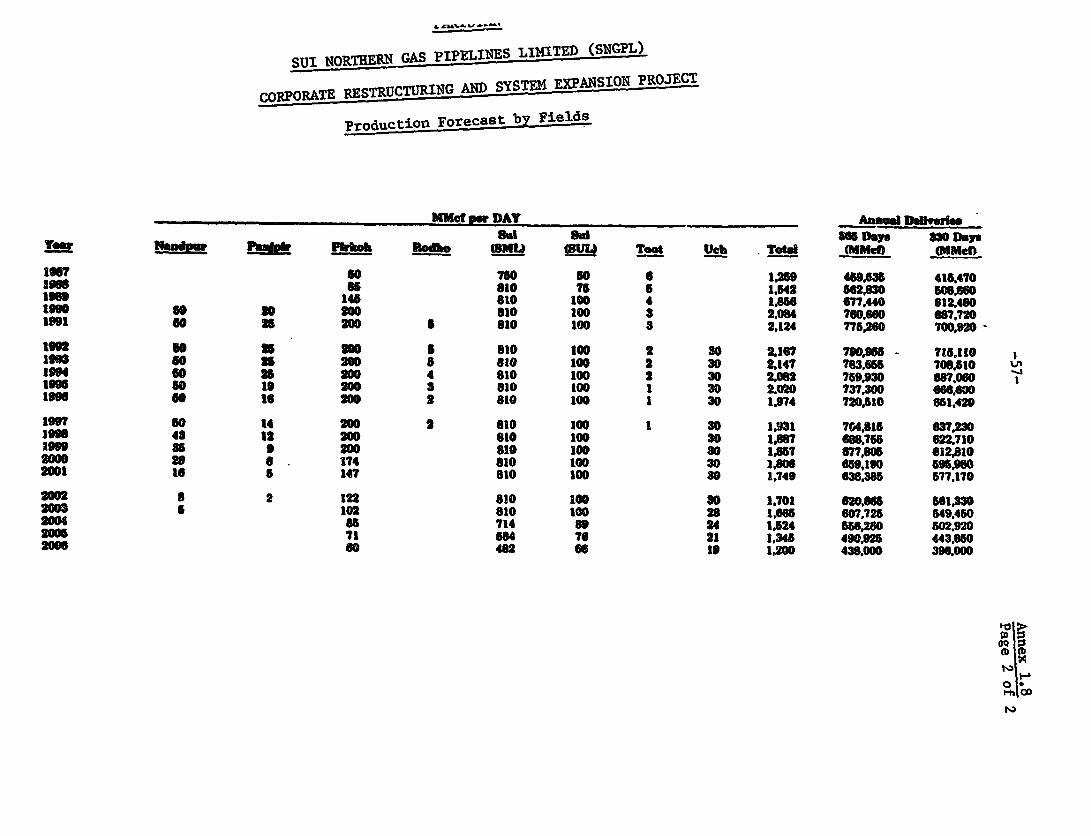

developments in the subsector. On the basis of the proven recoverable reservesand the reservoir characteristics of the already discovered fields, output ofgas is forecast to increase gradually from about 1,200 MMCFD in FY90 to about2,000 MMCFD in FY2006, representing an average annual increase of about 3.5%.This would allow GOP to maintain a reserve to production ratio of at least twentyyears. The production profile is presented in Annex 1.8. According to theforecast production of gas from existing and already developed fields, supplywill fall short of unconstrained demand, which is forecast to increase at anaverage annual rate of about 5.2%. In recognition of these supply constraints,GOP with Bank assistance has outlined for the Seventh Plan period a gasallocation procedure for meeting the requirements of gas for the priority sectorswhich maximizes the benefits to the economy. Specifically, the procedure callsfor allocating incremental supplies of gas to various consumer categories in thefollowing descending order based on the "net-back" value of gas to each categoryof consumer: (a) fertilizer industry to which priority has been accorded becauseof major bottlenecks in port handling facilities and the infrastructure forinland transportation; (b) residential and commercial consumers, as a substitutefor higher value kerosene; (c) the power subsector for use in combined cyclepower plants, as a substitute for diesel oil; (d) general industries, exceptsteel and cement, to displace fuel oil; and (e) the power subsector as asubstitute for fuel oil for base load thermal power plants.

1.16 Based on the projectec availability of gas and its allocation tovarious consumer categories, the revised forecast calls for sales increasing atan average annual rate of about 3.5%, from 1,098 MMCFD in FY90 to 1,897 MMCFDin FY2006. However, as shown in Table 1.1 below, the allocation procedurestogether with the agreements reached under ESL II on measures to rationalize thelevel and structure of consumer price of gas (paras 1.20 and 1.21) are expectedto release gas for higher value uses. Accordingly, the residential sector wouldexperience the highest rate of growth, averaging about 6.6% annually, followedby commercial consumers (4.6%), fertilizer and general industries (3.2%) andpower (1.8%).

Table 1 1: Forecast of Gas Demand and Supply FY9O-FY2006(MMCFD)

Moreover, the share of gas absorbed by the residential and commercial sectorstogether would increase from 18.2% in FY90 to about 27.9% in FY2006. Bycontrast, the share of gas consumed by the fertilizer industry and the powersubsector would decline from 26.8% and 30% to 25.6% and 23.0%, respectively.

-8-

Gas Development Program

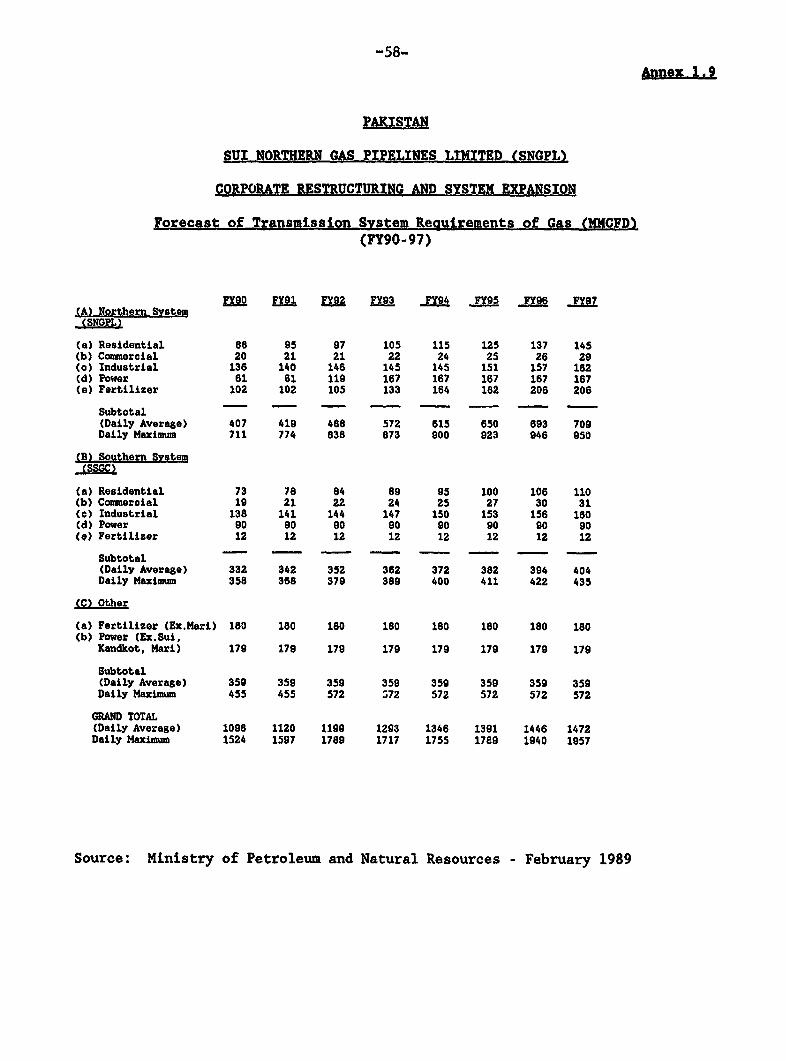

1.17 GOP's medium term development program for the gas subsector calls for:(a) drilling of about 250 wells by both the private and the public sectors toaccelerate the appraisal and development of the gas fields at Loti, Sui, Pirkoh,Khandkot, Bad.in Block, Mari, QadiPpur and Kadanwari, the condensate fields ofDhodak, Dakhni and Adhi, and the low quality gas fields of Uch, Panjpir andNandpur; and (b) expanding the infrastructure for the purification, transmissionand dist:ibution of gas. In particular, SNGPL's capacity would be increased toabout 800 MMCFD; transmission pipelines would be extended and reinforced to:(a) connect the Dhodak, Adhi and Dakhni fields; and (b) supply the combined cyclepower station at Kot Addu (paras 3.02 and 5.02). The capacity of SSGC'stransmission line on the right bank of the Indus would be increased to transportan additional 100 MMCFD of gas from the Badin fields. The projected gasrequirements for both the SNGPL and SSGC transmission systems are given in Annex1.9. The development program for the gas subsector which constitutes an integralpart of the CIP for the Seventh Plan, will receive priority in telms of resourceallocation and implementation will be monitored under ESL II (para 1.02).

1.18 To implement this program, Rs 38 billion would be invested during theSeventh Plan in the development of oil and gas subsector by both the public andprivate sectors for exploration drilling, appraisal and development of discoveredoil and gas fields, and the expansion of the gas transmission and distributionretwork. Investments amounting to Rs 14.9 billion would be undertaken by OGDC,Rs 4.4 billion by SSGC, and Rs 6.5 billion by the private sector. As for SNGPL,its investments are expected to amount to Rs 12.2 billion during the Seventh Planand about Rs 7.8 billion would be incurred between FY94-96 (para 4.08). Thisprogram includes, inter alia, about Rs 13 billion for the proposed Project, andabout Rs 3 billion for extending the distribution network which constitute a partof' the Government's social development program. The Bank has reviewed theinvestment program and advised GOP that it is large relative to the availabilityof resources and the implementation capacity of SNGPL and, hence, should bereviewed annually (para 4.06). Furthermore, in order to ensure that thedistribution network to connect new town is not extended in an ad hoc fashion,specific economic criteria are to be developed and reviewed with the Bank forthe selection of the new towns to be connected (para 3.11).

Gas Pricing and Demand Management

1.19 Producer Price of gas refers to the price per unit of gas at the well-head and covers the financial cost of extraction and a return to investors. Theformula for setting this price was changed under ESL I as the formula that hadbeen in place since 1981 had not succeeded in increasing the private sector'sinvolvement in the exploration and development of gas for two reasons: (a) the12% rate of return it guaranteed was low relative to the returns secured by theoil industry elsewhere; and (b) it required that the well-head price of gas beset after discovery, which entailed a higher risk for investors given thelikelihood of protracted negotiations once discovery was made. To address theseshortcomings, the new formula links the producer price of gas to two-thirds theborder price of fuel oil, less a discount to be negotiated prior to discoverybased on the geological and market conditions of the concession involved. In

- 9 -

1987, a year after it was adopted, GOP on its own accord, expanded theapplicability of this formula to cover not only new concessions but also thealready discovered fields, provided the concessionaires were willing torenegotiate their entire contract. The private sector has responded favorablyto these initiatives and so far exploration contracts have been signed for 21new onshore concessions and negotiations are underway for several others (para1.14). In addition, new gas fields have been discovered at Qadirpur by OGDC andat Kadanwari by the joint venture of OGDC and IASMO, and the production of gashas increased by about 25%, with OGDC doubling its output. Notwithstanding thesegenerally satisfactory developments, the downturn in the international price ofoil has made exploration in new high cost concession areas, particularly inremote and offshore areas, less attractive to the private sector under theprevailing producer price formula. Therefore, with the objective of providingadditional stimulus to the private sector to increase its involvement in theexploration and development of gas, under ESL II, GOP has revised the producerprice formula for new offshore concessions granted after July 1, 1989, by linkingthe well-head price of such gas to full parity with the border price of fuel oil,less a negotiated discount for geological and market conditions.

1.20 Consumer Price of gas refers to the price per unit of gas paid by theend-use consumers and covers the producer price, the utilities' costs oftransmission and distribution and their financial returns, as well as a gasdevelopment surcharge (GDS), which accrues to GOP as rent. GDS represents thedifference between the consumer price and the utilities' costs including theproducer price and returns. Prior to 1981, GOP maintained the consumer priceof gas at levels lower than those of its substitutes to encourage the use of gasand buffer the economy from the adverse impact of a higher bill for energyimports. As this was resulting in the uneconomic use of gas and was denying thesubsector the resources needed to implement an expanded exploration anddevelopment program, GOP agreed under the First Structural Adjustment Loan toraise the weighted average consumer price of gas to two-thirds the border priceof fuel oil, a commitment that was reaffirmed under ESL II. In keeping with thisagreement, gas prices were increased six times between FY81 and FY89 by anaverage of about 23% in nominal terms. As of December 1989, the weighted averageconsumer price of gas was slightly higher than the then prevailing border priceof fuel oil (Rs 41.6/MCF compared to Rs 40.7/MCF) and well above the target of66% originally agreed to with the Bank.

1.21 The progress made by GOP in adjusting the level of the consumer priceof gas, however, was not accompanied by corresponding realignments in itsstructure, where distortions were relatively widespread. Specifically, the priceof gas to consumers, other than general industries, the cement subsector and thecommercial sector, was lower than the price of petroleum products it wasdisplacing. The price paid by WAPDA in FY89 for pipeline quality gas was at fullparity with the domestic price of fuel oil, but for direct purchases of gas fromproducers it was only at 25% of fuel oil parity. Likewise, the 10% of thehouseholds in the country with access to gas were paying only 24% of the domesticprice of kerosene and only 22% of the domestic price of fuelwood, both of whichare used by the remaining 90% of the households. Unlike the general industrialconsumers and the cement subsector, the fertilizer industry was paying forpipeline quality gas only 32% of the domestic price of fuel oil. In view of theprevailing supply constraints, which augment the need for rationalizing the

- 10 -

consumption of gas and mobilizing financial resources for implementing thedevelopment program of the subsector, GOP agreed under ESL II to implementmeasures required to address these distortions, including increases in the priceof gas to households and the power subsector (para 4.06). As for the fertilizerindustry, which is a major consumer of gas and has important links to theagricultural sector, GOP agreed to complete by March 31, 1991, a study to assessthe impact of higher gas prices on the ex-factory prices of fertilizer andidentify investments in retrofitting and changes in technology to improve theefficiency of gas utilization.

1.22 The demand for gas in Pakistan varies significantly by time of day andseason. This, together with the supply constraints that have persisted since1981, has induced GOP to curtail the supply of gas to new industrial consumersto nine months each year (para 1.13). As a result, for the remaining threemonths, these consumers shift to the use of higher-value petroleum products suchas kerosene and diesel which, at the margin, are imported. As this is contraryto the objectives of LES, GOP needs to adopt a load management strategy thatwould balance the supply and demand of gas and promote allocative and operationalefficiency. Such a strategy would require storing the excess gas undergroundand producing it to meet peak demand. The Bank, in consultation with GOP andSNGPL, has ascertained that sufficient gas is available for storage particularlyduring the summer months. The Gas Utilization Study has identified the nowdepleted Dhtilian field as a suitable candidate for creating such a facility,subject to completion of a detailed feasibility study to assess its viability.Moreover, as the domestic price of diesel oil and kerosene is at presentsubstantially higher than that of gas, the willingness to pay of consumers whosubstitute the former for the latter during peak periods, is substantially higherthan what they are currently paying for pipeline quality gas. As the surpluscaptured by such consumers could be mobilized by GOP through better demandmanagement including the implementation of time of day and seasonal tariffs, GOPagreed under ESL II to recruit consultants under terms and conditionssatisfactory to the Bank to complete, by March 31, 1991, a study to: (a) assessthe potential for peak shaving of gas consumption; (b) formulate a structure oftariffs for gas which would promote peak shaving; and (c) prepare a timetablesatisfactory to the Bank for the implementation of the new tariff structure.

E. Bank Group's Role in the Energy Sector and Experience with Past Lending

1.23 The Bank Group's involvement in Pakistan's energy sector started in1955, with a loan to KESC for the construction of a thermal power station. Sincethen, it has assisted in the implementation of projects in all energy subsectors.Prior to 1985, the Bank Group had made 16 loans/credits to Pakistan for energyprojects: in the power subsector, the Bank participated in the Indus BasinDevelopment Projects, and provided a series of four credits/loans to KESC andthree to WAPDA; in the petroleum subsector, the Bank's involvement included fiveloans to SNGPL for the expansion of the infrastructure for the transmission anddistribution of gas, three to OGDC for exploration and development of oil andgas and one to NRL for improving its energy efficiency. All of these projectshave been or are about to be completed.

- 1i -

1.24 In addition to ESL I and ESL II, the Bank Group has made eight loansand a credit in the energy sector since 1985. These include: WAPDA IV (Loan2499-PAK) and WAPDA V (Loan 2556-PAK) for the least cost extension andreinforcement of the secondary and high voltage transmission grid; the PetroleumResource Joint Venture Project (Loan 2553-PAK) to assist GOP in mobilizingprivate sector involvement in exploration and development of oil and gas; theKot Addu Combined Cycle Project (Loan 2698-PAK) to add another 250 MW ofgenerating capacity through the conversion of combustion turbines to combinedcycle operation; the Power Plant Efficiency Improvement Project (Loan 2792-PAK)for the rehabilitation of existing power plants and conversion of combustionturbines to combined cycle operation; the Refinery Energy Conservation andmodernization Project (Loan 2842-PAK) for restructuring product output andstreamline existing systems; the Private Sector Energy Development Project (Loan2982-PAK), the first of its kind to be processed by the Bank with the objectiveof increasing private sector involvement in energy development; the TransmissionExtension and Reinforcement Project (Loan 3147-PAK) supports the continuationof work on least cost expansion of the high voltage transmission grid; and theRural Electrification Project (Credit 2078-PAK and Loan 3148-PAK) which is aimedat improving rural productivity and quality of life of the rural population.

1.25 The proposed Project would be the Bank's sixth operation with SNGPL.The first five have been completed successfully. The Bank through thisrelationship has contributed to expanding SNGPL's gas transmission anddistribution network and to strengthening its financial, management and technicalcapabilities. The Project Completion Report (PCR) for SNGPL IV Project (Loan1107-PAK), however, noted that separate financial and managerial objectives tobe developed for the Project's Department of the Company were not adopted fully.Likewise, the SNGPL V Project for which the PCR is under preparation has furtherconfirmed that, despite the autonomy granted so the corporation under theCompanies Act, GOP exercises substantial control in the day-to-day managementof SNGPL, including the appointment of senior staff. Such control is neithercorducive to the efficient operation of the company, nor does it fosteraccountability, issues that are likely to gain especial significance in view ofthe planned investments which would more than double the assets of the company.The measures to be implemented under the proposed Project are aimed at, interalia, restructuring SNGPL along commercial lines and increasing accountabilityand autonomy.

II. THE BORROWER

Background

2.01 SNGPL, the Borrower of the proposed Loan, was incorporated in 1963under the Companies Act as a private limited company and converted in 1964 toa public limited company. Originally established as a gas transmission anddistribution company, its activities have expanded and currently include theconstruction and operation of pipelines, both for itself and other organizations.It has an authorized capital of Rs 400 million, of which Rs 383 million has beenissued and paid up.

- 12 -

2.02 Until 1970, SNGPL's shares were held in equal proportions by Burmah Oi'LCompany (BOC), the Pakistan Industrial Development Corporation (PIDC) and thegeneral public. liowever, through equity contributions and subsequently throughthe acquisition of shares sold by BOC, GOP became in 1973 the majorityshareholder in SNGPL. As of May 1990, about 91% of SNGPL's shares were owned,directly or indirectly, by GOP, followed by BOC (6.7%) and the general public(2.3%). The company's shares are traded on the Karachi and Lahore stockexchanges. Details relating to the current ownership of SNGPL are presented inAnnex 2.1, and summarized below.

I %

GOP (direct holding) 51.0 51.0

Indirect Government Holdin&s

Pakistan Investment DevelopmentCorporation 9.7

State Life Insurance Corporation 5.3Pakistan Insurance Corporation 2.2National Development Finance

Other GOP controlled institutions _..2Subtotal 24.5

Other Public Sector Shareholding

National Investment Trust 9.0Investment Coiporation of Pakistan 6.5

Subtotal 15.5

Private Sector

Burmah Oil Company of UK 6.7General Public 2,3Subtotal 9.0

TOTAL 100.0

Organization and Management

2.03 As a public limited company, SNGPL operates under the provision ofthe Company Ordinance of 1984. Ownership is conferred through ordinaryshareholding, and control is exercised through a Board of Directors who areelected by the shareholders for a period of three years and are eligible forreapiointment. The Company Ordinance, however, provides for the appointment ofdirectors to the Board to protect creditors interests. Currently, SNGPL's Boardconsist of 14 members, 12 of whom are elected by the respective shareholders.As majority shareholder, GOP exercises the prerogative of appointing eightmembers to the Board including the Chairman. In addition, it appoints two otherdirectors who represent GOP controlled banks and development financeinstitutions, the creditors of the company. Of the remaining four directors,one is from the Pakistan Investment Development Corporation, a wholly-ownedgovernment enterprise; one each from the government-owned and controlled mutualfunds, the National Investment Trust and Investment Corporation of Pakistan; andone from the BOC. The Board is responsible for the formulation of long-termpolicy, though all major decisions currently require Government approval priorto implementation (para 1.10). Consequently, the day-to-day management and

- 13 -

decision making of the company are strongly influenced by the Government, andits investment program often reflects Government's priorities.

2.04 The Managing Director, who is appointed by resolution of the Board,after confirmation by GOP, is responsible for the day-to-day management of thecompany. He is assisted by three (financial, technical and commercial) GeneralManagers, and six senior managers, including managers for Telecommunications,Audit,. Corporate Planning, Data Processing, Systems and Procedures, the CompanySecretary and a Special Assistant. The ;nior management is qualified, competentand well-experienced. However, in light of the strong influence in the day-to-day running of the company by the government, the authority of the company'smanagement is limited, which is not conducive to quick decision-making and smoothoperation. The proposed Project, through the restructuring of the ownership andmanagement of the company would promote the autonomy and independence accordedto SNGPL under the Companies Act (paras 3.05 and 3.07). The current organizationchart is presented in Annex 2.2.

Sources of Gas Supplies and Existing Facilities

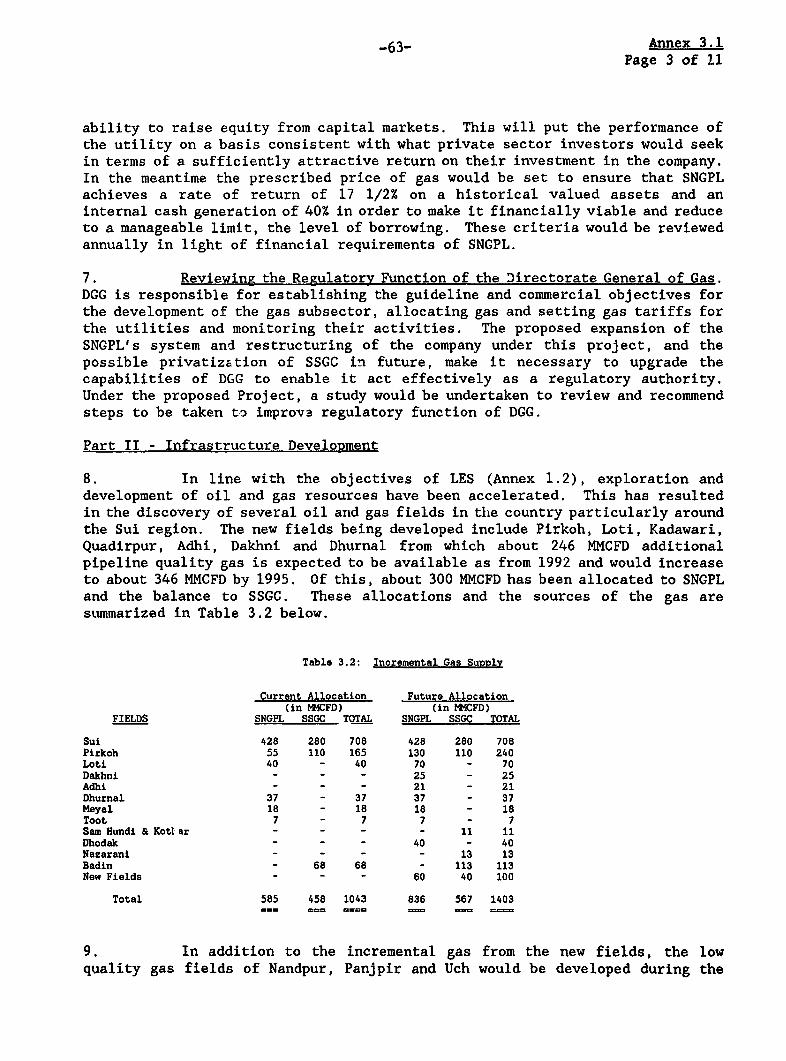

2.05 As of January 1990, the major source of 4as for SNGPL was the Suifield, which is operated by PPL with whom it has two long-term contracts withdedicated reserves: one for purchases of up to 428 MMCFD until the year 1999,and the other for purchases of up to 55 MMCFD until 1998 (para 3.06). Othersources of gas include about 7 MMCFD from the Toot field, operated by OGDC and18 MMCFD from Meyal field, operated by POL. SNGPL has also negotiated contractsfor additional gas supply with: OGDC for the purchase of about 225 MMCFD of gasfrom Pirkoh (130 MKCFD), Loti (70 MMCFD), and Dakhni fields (25 MMCFD); with thePOL/OGDC joint venture for the purchase of about 21 MMCFD from the Adhi field;and with the Oxy/OGDC Joint Venture for 37 hMCFD from the Dhurnal field (para3.14). Negotiations are also underway with: OGDC for 50 MMCFD from the Dhodakfield, and 40 MMCFD from Qadirpur; and the Lasmo/OGDC Joint Venture for 60 MMCFDfrom the Kadanwari field (Annex 3.1).

2.06 The main transmission and distribution system owned and operated bySNGPL consists of: (a) 2,446 km of high pressure pipeline of varying diameterto transmit the gas from Sui, Toot and Meyal field to cities in Punjab and theNorthwest Frontier Pi.ovince via Multan and Faisalabad; and (b) 8,722 km ofvarying diameter pipelines to distribute this gas to a large number of citiesand towns including Lahore, Faisalabad, Islamabad, Peshawar, Gujrat and Sialkot.In addition, SNGPL owns and operates several compressor stations (Map IBRD20961R1) to facilitate the movement of the gas along the system; purificationplants at Sui with a total capacity of 450 MMCFD; and an LPG plant at Dhurnal.SNGPL's existing system supplies gas to about 23,781 commercial consumers, about540,000 domestic consumers, and about 2,860 industrial consumers including 5fertilizer plants and WAPDA for power generation. Over the next six yearsSNGPL's system capacity is expected to be increased from 450 MMCFD to about 800MKCFD (para 3.14).

Corporate Planning

2.07 SNGPL's Corporate Planning Department is staffed by two seniorengineers and a junior accountant. The primary function of this department has

- 14 -

been to prepare SNGPL's medium-term investment program over a five year span onthe basis of gas allocated by the Government, and also project implementationand financing plans (generally referred to as PC-1) for the investment programfor goverrnment clearance and approval. It also liaises with financialinstitutions such as the Bank for identifying sources for financing itsinvestment program. In view of the envisaged expansion of SNGPL's activitiesto be undertaken under the proposed Project, the capability of the CorporatePlanning department would be strengthened in the areas of economics, financeand system planning (para 3.21).

Project Engineering and ImDlementation

2.08 SNGPL has a separate department for project design and implementation.It is headed by the Manager Projects, who reports to the Technical GeneralManager. The department has successfully implemented a number of projects,including the SNGPL IV Project (Loan 1107-PAK) and the SNGPL V Project (Loan2324-PAK), and those for other entities in Pakistan such as WAPDA. The companycarries out its own design, engineering and construction of transmission anddistribution pipelines, except for pipelines across large rivers for whichSNGPL's inhouse expertise is limited. As the prJposed Project involves theconstruction of pipelines across two rivers (Ravi and Sutlej rivers), consultantswill be recruited to assist SNGPL in the design, engineering and supervision ofthe construction of pipelines across rivers (para 3.10).

0rieration and Maintenance

2.09 SNGPL has competent personnel to operate and maintain its gastransmission and distribution network. Currently its methods and procedures foroperation and maintenance are satisfactory. However, with the expansion of thesystem, SNGPL would need to monitor more closely the gas supply flow patternwithin its system to respond more effectively to changes in demand, particularlyduring peak periods. This would require the installation of a modern SupervisoryControl And Data Acquisition (SCADA) system. The implementation of the firstphase of the SCADA system was initiated under ESL I and would be completed underESL II (para 1.02). The second phase of the SCADA system required for theenvisaged expansion of the network would be implemented under the proposedProject (para 3.02). In view of recent increases in losses due to pipelinecorrosion, there is a need for improving the procedures for the coating of thelinepipes, and upgrading SNGPL's procedures for monitoring safety and detectingpossible gas leakages. Provision has been made under the proposed Project, forthe installation of a new up-to-date coating plant and for a collaborativearrangement with an internationally reputable gas utility to undertake a safetyand hazard assessment survey of SNGPL's entire transmission and distributionsystem with the objective of establishing and implementing appropriate safetymeasures (para 3.21).

Personnel and Staffing

2.10 Personnel management and staffing is the responsibility of thePersonnel Manager, who reports to the Commercial General Manager. Since 1983,SNGPL has adopted a relatively cautious approach to recruitment and, as a result,its staff has increased annually by only about 2%, from 3,800 in 1983 to 4,352

- 15 -

by June 1990. This approach, in turn, has enabled SNGPL to substantially improvethe consumer-employee ratio which, in June 1990, was about 142:1 compared to101:1 in June 1983. On the basis of the configuration and level of complexityof the SNGPL's system, this ratio compares favorably with those of other welldeveloped gas distribution systems. Of the total staff employed by SNGPL, 381(9%) are engaged in project construction and the remaining 3,971 (91%) inoperations. SNGPL's clerical and support staff is represented by a union, whichnegotiates the terms and conditions of employment. A two-year contract, coveringthe period July 1, 1989 to June 30, 1991, was ratified by the Sui Northern GasEmployees Union and SNGPL on October 21, 1989. The overall relationship betweenlabor and management is good and the total package of wages and benefits offeredby SNGPL is considered attractive by local standards.

Training

2.11 Training of staff is the responsibility of the Personnel Manager andline managers. Under the Fourth and Fifth SNGPL Projects (Loans 1107-PAK and2324-PAK), the Bank assisted SNGPL in upgrading the technical and managerialcapabilities of its staff through overseas training in selected aspects of gasutility management and operations. SNGPL has recently appointed a full timeTraining Coordinator under the Personnel Manager for the coordination andimplementation of all training programs. However, given the growth and diversityof operations envisaged under the proposed Project, especially the shift fromsingle to multiple sources of gas supply, SNGPL has requested the Bank to financea collaborative arrangement with an internationally reputable private gasutility. Through this arrangement, assistance would be provided to SNGPL toupgrade its operational procedures and allow its staff to obtain on-the-jobtraining overseas or in Pakistan, in the areas of long term planning, operationand maintenance, inventory control, corporate planning, project implementation,safety and industrial emergency prevention (para 3.21).

III. THE PROJECT

Project Objectives

3.01 The objectives of the proposed Project are to: (a) assist GOP inrestructuring SNGPL's equity ownership to make the utility more autonomous andenhance its resource mobilization capability by enabling it to tap new sourcesof financing including private sector financing; (b) expand SNGPL'sinfrastructure for purification, transmission and distribution of gas at leastcost; (c) promote the substitution of gas for higher value petroleum productsin the northern part of the country; (d) rationalize the consumption and supplyof gas through pricing and demand management; and (e) strengthen SNGPL'scapabilities in long-term planning, project implementation, inventory control,operation and maintenance and safety.

- 16 -

Proiect DescriRtion

3.02 Over a period of six years, the proposed Project would support threecomponents, Corporate Restructuring of SNGPL, Infrastructure Development andConsultancy Services and Training. Details of the proposed Project are presentedin Annex 3.1 and summarized below:

A. CorRorate Restructuring of SNGPL. This would involve:

(a) Restructuring of SNGPL's Ownership: Presently, GOP owns directly about51% and indirectly, through GOP-owned institutions, about 40% ofSNGPL's shares. The restructuring of the ownership involves mobilizingresources from the private sector through issuance of additional equityshares, initially to dilute public sector ownership from 91% to 51%,and subsequently to at most 40% (para 3.05);

(b) Restructuring of SNGPL's Management, which would include thereconstitution of the Board of Directors of the company to reflect thenew shareholding in the company. In order to ensure reduced Governmentinvolvement in the management and decision making of the company, theChairman and Managing Director and other key personnel of the companywould be appointed by the Board of Directors (para 3.07);

(c) Establishment of Financial Performance Criteria to include a new basisfor setting SNGPL's prices net of the Gas Development Surchargecollected on behalf of GOP (Prescribed Prices) and providing for, interalia, the capping of SNGPL's prices rather than of its rate of returnon fixed assets, for the purpose of improving the efficiency of theborrower and enhancing its ability to raise equity from capital markets(para 4.03); and

(d) Reviewing the Regulatory Functions of the Directorate General of Gas(DGG). Currently, DGG is responsible for: establishing the guidelinesand commercial objectives for the development of the gas subsector;allocating gas and setting gas tariffs for the utilities and monitoringtheir activities. The planned expansion of the gas transmission anddistribution systems throughout the country and in particular theproposed expansion of the SNGPL system and restructuring of the Companyunder this Project, makes it necessary to upgrade the capabilities ofDGG to enable it to act effectively as a regulatory authority. Underthe proposed Project, the role of DGG would be reviewed andrecommendations made on how to improve its regulatory functions (para3.08).

B. Infrastructure DeveloRment. This would provide for:

(a) installation of a 1 x 120 MMCFD gas purification plant at Sui forpurifying the additional gas from Pirkoh, Loti, and the newlydiscovered gas fields of Kadanwari and Quadirpur;

(b) expansion of SNGPL's transmission system capacity by about 300 NMCFDincluding the construction of approximately 215 kms of 30-inch diameter

- 17 -

pipeline between Sui and Multan and installation of 6x4000 BHPcompressor units to enable SNGPL evacuate the additional gas from thegas fields in the Sui region;

(c) expansion of SNGPL's distribution system to supply gas to the powerstation at Kot Addu and two fertilizer plants to be constructed betweenSahiwal and Lahore, and to connect during FY93-96 approximately 330,000domestic, 6000 commercial and 400 industrial new consumers;

(d) installation of a linepipe coating plant, to improve the coatingprocess, extend the life of the linepipes and improve operationalsafety during construction;

(e) installation of a telecommunication system (SCADA) for monitoring theoperations of the transmission and distribution network; and

(f) procurement of compressors and construction equipment for installationof the linepipe.

C. Consultancy Services and Training. This would cover:

(a) a safety and hazard assessment survey of the transmission anddistribution system;

(b) upgrading the capability of the Directorate General of gas, andtraining of SNGPL staff in the areas of long-term planning, projectimplementation, pipeline system operations and maintenance, inventorycontrol and safety through a collaborative arrangement with a foreignprivate gas utility;

(c) further development of SNGPL's financial management information systemsand data processing including definition of its computer hardware andsoftware needs, and a review of its billing cycle; and training ininternal auditing of computerized accounting systems;

(d) designing the new formula for setting SNGPL's Prescribed Prices andperformance criteria referred to in the description of the CorporateRestructuring program in para 3.08;

(e) services of financial advisers and an underwriter or consortium ofunderwriters to manage the issuance of shares; and

(f) design, engineering and supervision of high pr'ssure pipeline at rivercrossings.

Project Cost

3.03 The total cost of the proposed Project, including physical and pricecontingencies and interest during construction, is estimated at US$546.5 millionequivalent, of which taxes and duties amount to about US$103.9 million. Of thetotal cost, about US$129.9 million would be in foreign exchange and aboutUS$416.6 million equivalent in local costs. The cost estimate is based on

- 18 -

quotations for similar works and equipment in Pakistan, and reflects January1990 prices. Physical contingencies have been estimated at 10% of the base cost.Price escalation for local costs has been assumed at 6.8% for FY91 and 6%thereafter. Price escalation for foreign costs has been assumed at 4.9X p.a.for FY91-95 and 4.3% for FY96. The resulting total local and foreign costs foreach year have been converted into/from USDollars at the estimated averageexchange rate for that year. The cost estimate for the proposed Project issummarized in Table 3.1 below.

Table 3.1: Summarv of Project Cost Estimate

Rs Million USS MillionL.C. F.C. Total L.C. F.C. Total

Of which Taxes & Duties 2,472 - 2,472 103.9 - 103.9

Project Financing

3.04 The financing plan for the proposed Project is based on the frameworkfor the restructuring of SNGPL which calls for reducing GOP's direct and indirectshareholding in SNGPL from 91% to at most 40% through share issues to the generalpublic (para 3.05). The proposed Loan in the amount of US$130 million equivalentwould cover the total foreign exchange required for the Project and would be madedirectly to SNGPL, with GOP as guarantor. SNGPL would cover the foreign exchangerisk. New equity issues and local loans would cover local costs of,respectively, US$93 million and US$121 million equivalent. The remaining localcosts, US$203 million equivalent, would be financed by SNGPL from internalsources, including customer contributions and security deposits. The financingplan for the proposed Project is summarized below in Table 3.2.

- 19 -

Table 3.2: Financing Plan

Rs Million USS MillionLocal Foreign Total Local Foreign Total

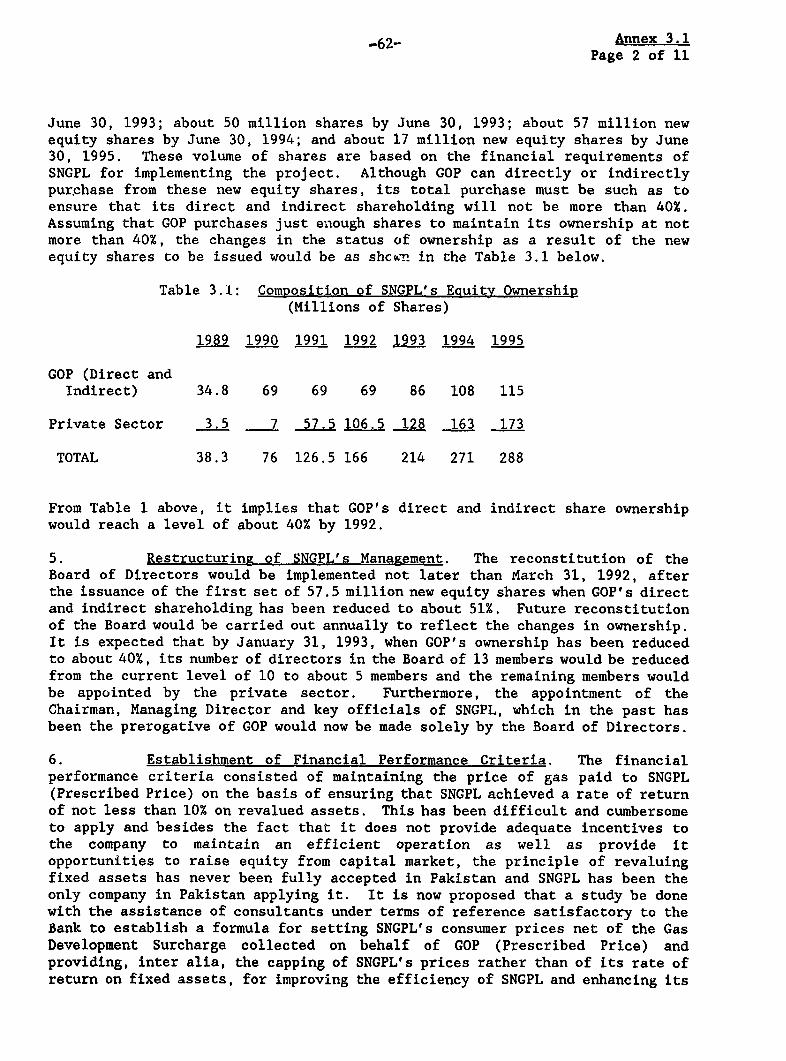

3.05 Restructuring of SNGPL's Ownership. The timetable and actions to beimplemented to achieve the corporate restructuring of the entity was discussedin relative detail by the Bank with the Government - the current ma'orityshareholder of SNGPL. It was agreed that the reduction of GOP's shareho'dingto not more than 40% would be by dilution through the issuance of about 219million new equity shares of SNGPL to the general public over a period of fiveyears (1991-1996) (Annex 3.1). The first issue of about 57.5 million new equityshares would be implemented not later than June 30, 1991. In order to achievethe reduction of GOP's direct and indirect shareholding from 91% to 51%, GOPmust refrain from purchasing directly or indirectly any of these shares. Theremaining shares would be issued in series annually depending on the financialrequirements of SNGPL to fund its investment program. Therefore GOP has agreedto reduce its direct and indirect shares in the company to not more than 51%through _he issuance of 57.5 million new eguity shares to be implemented notlater than June 30. 1991 and not exercise- its right to purchakse or otherwiseacquire. either directly or indirectly. any of the new eguity shares. if at anytime. the total of any such shares sought to be purchased or other-wise acquired.when added to GOP's direct and indirect shareholding in SNGPL would cause itsdirect and indirect shareholding to exceed 40% (Rara 6.01(a)). In addition.SNGPL has agreed to issue: (i) not later than June 30. 1291. 57.5 million newequity shares to the general public: (ii) not later than June 30, 1992. about37.5 million new eauitv shares: (iii) not later than June 30. 1993. about 50million new equity shares: (iv) not later than June 30. 1994. about 57 millionnew equity shares: and (v) not later than June 30. 1995 about 17 million neweauity shares (nara 6.03(a)!.

3.06 SNGPL's finance department will be responsible for implementing theissuance of new equity shares. However, before shares can be issued to thepublic, the issue must be authorized by SNGPL's board of directors andshareholders (increase of Authorized Capital) and by the Controller of Capitalissues. It should then be underwritten by one or several of the specialized

- 20 -

private sector financial institutions. As SNGPL has no experience in marketingsuch issues, it would require the assistance of a financial adviser to manageanG market the issues (para 3.05). In order to ensure that the process for theissuance of the equity shares is implemented in a timely fashion, SNGPL agreedto: (a) provide not later than December 31. 1990. evidence satisfactory to theBank that it has obtained all necessary consents and clearances for the marketingof the new equitv shares (nara 6,03(b)): and (b) aRpoint not later than January31, 1991. an underwriter or a consortium thereof. satisfactory to the Bank onafully committed basis to market the new eauity shares (6.03(c)). Of thesizeable local currency loans (US$121 milijon equivalent) required for theproject, SNGPL intends to contract loans totalling Rs 1.5 billion (approximatelyUS$70 million equivalent) from various local financial institutions in 1990.To ensure timely availability of the funds required for implementation of theproposed Project, the following have been set as conditions of effectivenessof the proposed Loan: (a) appointment by SNCPL of financial advisers, whoseoualifications. exgerience and terms of reference are satisfactory to the Bank.to manage and implement measures for raisinig the reguired resources througheauity issues and loans (para 6.04(a')): and (b) submission of evidence ofconcluded loan agreements totalling Rs 1.5 billion with local financialinstitutions (nara 6.04(b)).

3.07 Restructuring of SNGPL's Management. The reconstitution of the Boardof Directors would be implemented not later than March 31, 1992, after theissuance of the first set of new equity shares. In order to increase theautonomy of the management of the company, the appointment of the Chairman andManaging Directors and other key senior staff of SNGPL, which is currently theprerogative of GOP, is now to be made by the Board of Directors as provided forin the Company's Ordinance and, until such time that the Government shareholdingis reduced to a minority position, the Bank shall be given an opportunity tooffer its views on proposed appointments by the Board of Senior Staff.Furthermore, as part of the assistance to be provided under the collaborativearrangement between SNGPL and a reputable international private sector gasutility, the Corporate Planning Department and the operational management ofSNGPL would be reviewed with the intention of upgrading its capabilities.Therefore SNGPL has agreed: to appoint to the staff of the Corporate PlanningDepartment by not later than March 31. 1991, an economist. financial analyst andsystem planner all with approRriate gualifications and experience (Rara 6.03(d)):and (ii) reconstitute its Board of Directors not later than March 31. 1992. toreflect the new ownership of the Company (Rara 6.03(e)).

3.08 Review of the Regulatory Functions of DGG. As mentioned in para 3.02(A)(d), provision has been made under this project for GOP to undertake a study,with the objective of reviewing the regulatory role of DGG and recommendingactions to be taken to upgrade its capabilities. Therefore GOP has agreed toinitiate not later than October 1. 1991 and complete not later than March 31.1992. a study, under terms of reference satisfactory to the Bank. to upgrade theregulatory caRabilities of DGG: furnish to the Bank the findings andrecommendations of such study for review and comments: and thereafter taking intoaccount the Bank's comments. implement the findings and recommendations of suchstudy not later than March 31. 1993 (para 6.01(b)).

- 21 -

3.09 Design and Engineering. With regard to the expansion of thetransmission and distribution network, SNGPL undertook an in-house study in 1987,to identify the least cost option for increasing its transmission anddistribution capacity from about 450 M1ICFD to abeut 80) MMCFD by 1996, based ona GOP approved allocation of about 200 MUFD of additional gas from Pirkoh andLoti fields, and about 100 MMCFD from other new fields. Three pipeline optionswere evaluated by SNGPL for increasing the capacity of its system by 300 MMCFD.These include replacing the existing pipeline with either a 24-inch, 28-inch ora 30-inch pipeline. The combination of the length, size and associatedcompression required was optimized. The study concluded that the 30-inch optionis least cost for expanding the capacity to transport about 800 MMCFD of gaswithout compromising operational safety and flexibility. SNGPL has alreadyprepared the detailed design and technical specifications for this option. TheBank has reviewed the results of the optimization study and the design andtechnical specifications, and found them satisfactory.

3.10 As part of the high pressure 30-inch pipeline to be installed wouldcross two rivers, Ravi and Sutlej, consultants with proven expertise would berequired to assist in the design, engineering and supervision of constructionof the pipeline across these rivers (para 2.08). About 30 manmonths ofconsultancy services would be required. SNGPL has agreed to recruit consultantsby October 31. 1991. under terms and conditions satisfactory to the Bank. fo.the Rreparation of the detailed design and engineering and suRervision ofconstruction of the high pressure pipeline across rivers Ravi and Sutlei (Dara6.03(f)).

3.11 The distribution component of the proposed Project is part of SNGPL'splan for the development of the distribution network in the northern part of thecountry (para 5.02). The plan calls for connecting about 584,000 domestic,11,700 commercial and 800 industrial consumers, including the Kot Addu powerplant and two new fertilizer plants and, an estimated 150,000 consumers in newtowns between 1990 and 1997 (Annex 3.1). Of these, about 330,000 domestic, 6,000commercial and 400 industrial consumers, and the power plant at Kot Addu and twonew fertilizer plants to be built along the Multan-Sahiwal-Lahore route, wouldbe connected under the proposed Project during 1993-1996 (Annex 3.1). The Bankhas reviewed this component of the distribution plan, including the investmentrequired and the specifications of the equipment and materials to be procured,and found them satisfactory. This target is achievable, given SNGPL'sperformance in 1988 and 1989, when about 80,000 new consumers were connectedannually. With regard to the new towns, SNGPL is currently finalizing its mapof the new towns and developing economic criteria for the selection and rankingof the towns with regard to their nearness to the major transmission lines andthe numoer of consumers and amount of gas to be provided. These new towns willnot be financed under the proposed Project as GOP has promised to provide SNGPLabout Rs 3,000 million during FY91-96 for the new towns from the PeoplesDevelopment Fund (PDF) established for social development programs. However,in order to ensure that the distribution development plan is implementedsatisfactorily, SNGPL agreed to complete the Rlan for distribution of gas to newtowns and in consultation with GOP establish not later than June 30. 1991.criteria satisfactory to the Bank. for the ranking and selection of the new townsto be connected (Rara 6.03(g)).

- 22 -

3.12 SNGPL would utilize its Project and Distribution Departments for theimplementation of the system expansion component of the proposed Project. TheseDepartments would be responsible for the construction of the transmission anddistribution networks, design, engineering and application of cathodic protectionand for the inspection of the coating and wrapping of linepipes. Since most ofthis work would be carried out while the system is in operation, SNGPL would beassisted by consultants under the proposed collaborative arrangement to ensureclose coordination between construction and operating units of SNGPL and alsoto ensure that shutdowns and tie-ins to the existing system are carried outefficiently and with minimum disruption in gas supply. As the Project andDistribution Departments have acquired substantial experience in carrying outsuch work under similar operating conditions, especially through theirinvolvement in the Fourth and Fifth SNGPL projects (para 2.08), the proposedarrangement is satisfactory.

3.13 In addition to its own staff, SNGPL intends to utilize qualified localcontractors and consultants to undertake the civil works, such as trench diggingand backfilling, for the distribution network and to inspect pipeline welding,respectively. To complement its limited experience in the design, engineeringand construction of pipelines across river crossings, the proposed Projectprovides for consulting services for tile supervision of construction of pipelinesacross the rivers Ravi and Sutlej (para 3.10).