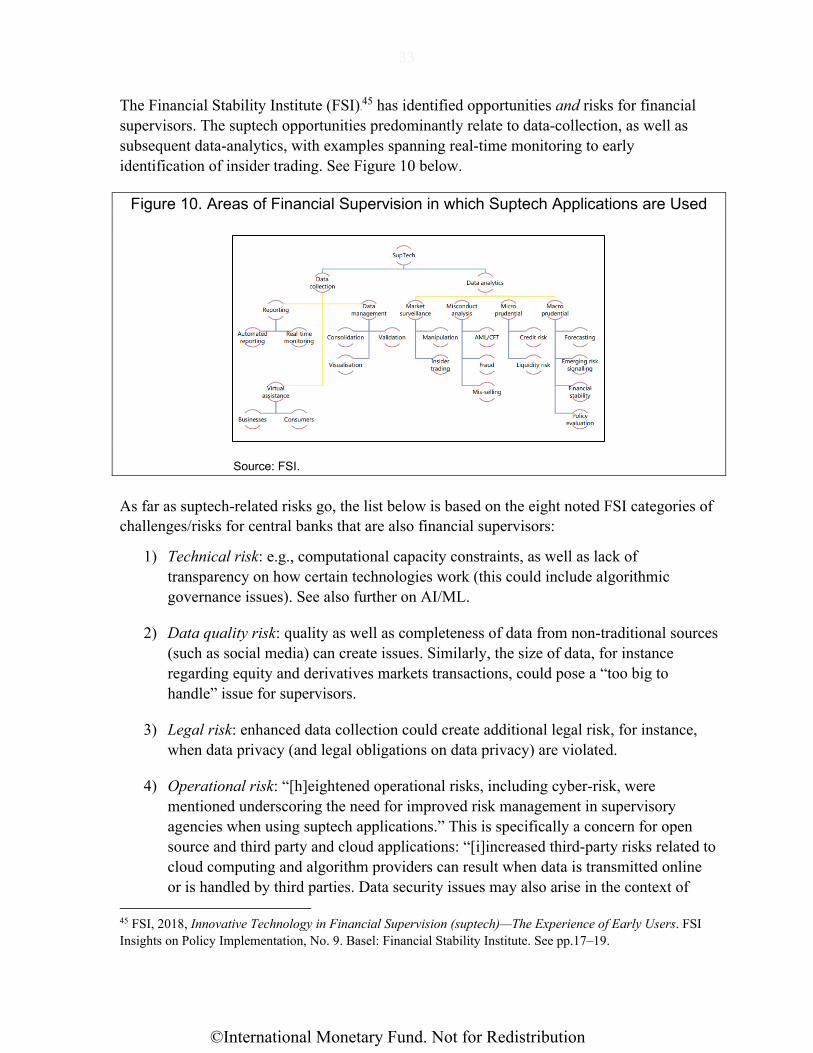

76

0

WP/21/105

Central Bank Risk Management, Fintech, and Cybersecurity

by Ashraf Khan and Majid Malaika

IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

©International Monetary Fund. Not for Redistribution

1

© 2021 International Monetary Fund WP/21/105

IMF Working Paper

Monetary and Capital Markets Department and Information Technology Department

Central Bank Risk Management, Fintech, and Cybersecurity

Prepared by Ashraf Khan and Majid Malaika

Authorized for distribution by Jihad Alwazir and Herve Tourpe

April 2021

Abstract Based on technical assistance to central banks by the IMF’s Monetary and Capital Markets Department and Information Technology Department, this paper examines fintech and the related area of cybersecurity from the perspective of central bank risk management. The paper draws on findings from the IMF Article IV Database, selected FSAP and country cases, and gives examples of central bank risks related to fintech and cybersecurity. The paper highlights that fintech- and cybersecurity-related risks for central banks should be addressed by operationalizing sound internal risk management by establishing and strengthening an integrated risk management approach throughout the organization, including a dedicated risk management unit, ongoing sensitizing and training of Board members and staff, clear reporting lines, assessing cyber resilience and security posture, and tying risk management into strategic planning.. Given the fast-evolving nature of such risks, central banks could make use of timely and regular inputs from external experts.

JEL Classification Numbers: G32, G34, G38, E50, E58, K23, O30.

Keywords: fintech, cybersecurity, central banking, financial supervision, law, technical assistance

Authors’ Email Addresses: [email protected], [email protected]

The authors are grateful for input from Ricky Satria, Yosamartha, Ronggo Gundala, Irman Pardede (Bank Indonesia), Ralph Ansumana (Bank of Sierra Leone), Jean Goetzinger (Central Bank of Luzembourg), Roman Hartinger (National Bank of Ukraine), review comments from Ben Norman (Bank of England), Gabriel Andrade (Bank of Portugal), Paul Woods (Central Bank of Ireland), Jihad Alwazir, Herve Tourpe, Bachir Boukherouaa, Gani Gerguri, Sanjeev Matai, Elie Chamoun, Lott Chidawaya, Stephen Swaray, Rudy Wytenburg, Parma Bains, Rangachary Ravikumar, Inutu Lukonga, Tanai Khiaonarong, Ryan Rizaldy, Gabriel Soderberg, Marianne Bechara, Juan Sebastian Viancha, Kathleen Kao, Nadine Schwartz, Victoria Bakhtina (IMF), and data assistance from Marc Engher. Danica Owczar provided invaluable administrative assistance. All remaining errors are our own.

IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

©International Monetary Fund. Not for Redistribution

2

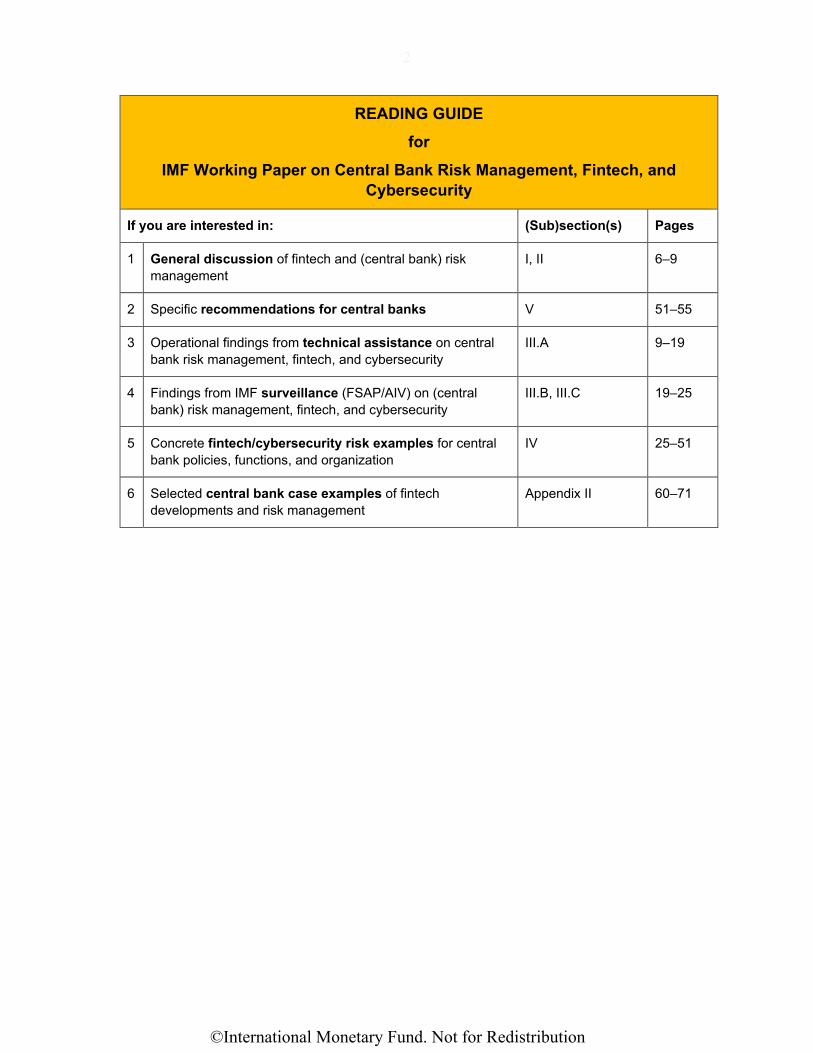

READING GUIDE for

IMF Working Paper on Central Bank Risk Management, Fintech, and Cybersecurity

If you are interested in: (Sub)section(s) Pages

1 General discussion of fintech and (central bank) risk management

I, II 6–9

2 Specific recommendations for central banks V 51–55

3 Operational findings from technical assistance on central bank risk management, fintech, and cybersecurity

III.A 9–19

4 Findings from IMF surveillance (FSAP/AIV) on (central bank) risk management, fintech, and cybersecurity

III.B, III.C 19–25

5 Concrete fintech/cybersecurity risk examples for central bank policies, functions, and organization

IV 25–51

6 Selected central bank case examples of fintech developments and risk management

Appendix II 60–71

©International Monetary Fund. Not for Redistribution

3

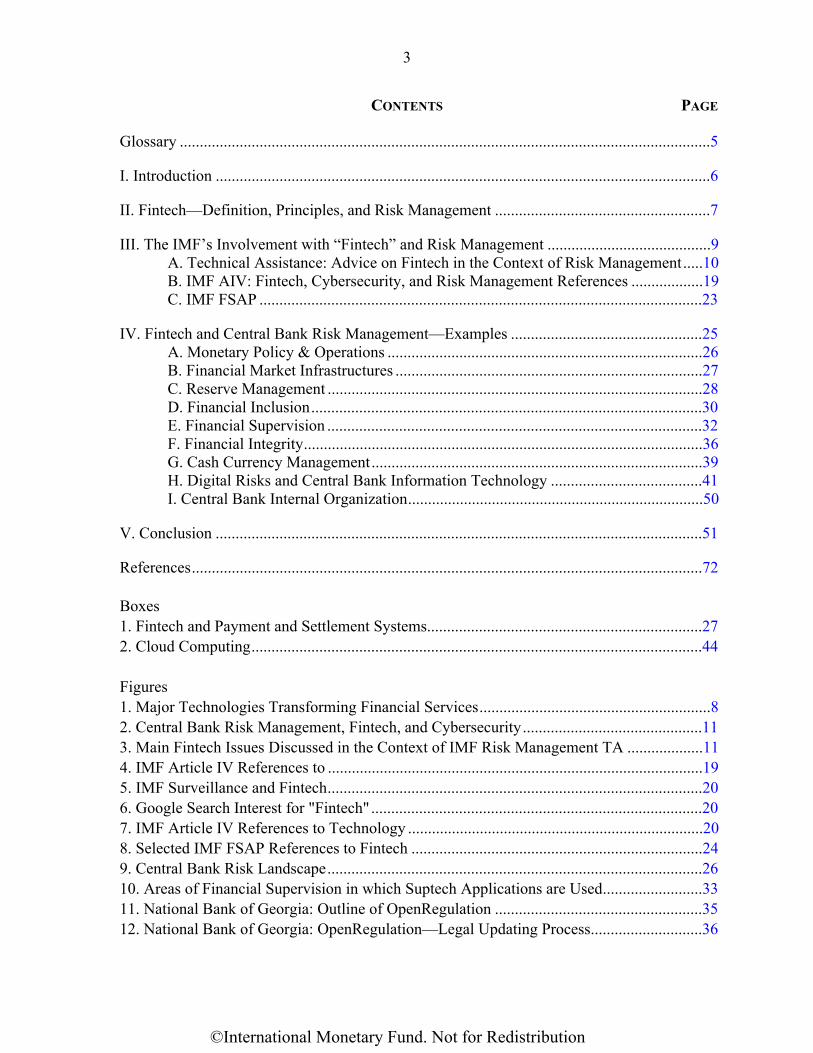

CONTENTS PAGE

Glossary .....................................................................................................................................5

I. Introduction ............................................................................................................................6

II. Fintech—Definition, Principles, and Risk Management ......................................................7

III. The IMF’s Involvement with “Fintech” and Risk Management .........................................9 A. Technical Assistance: Advice on Fintech in the Context of Risk Management .....10 B. IMF AIV: Fintech, Cybersecurity, and Risk Management References ..................19 C. IMF FSAP ...............................................................................................................23

IV. Fintech and Central Bank Risk Management—Examples ................................................25 A. Monetary Policy & Operations ...............................................................................26 B. Financial Market Infrastructures .............................................................................27 C. Reserve Management ..............................................................................................28 D. Financial Inclusion ..................................................................................................30 E. Financial Supervision ..............................................................................................32 F. Financial Integrity ....................................................................................................36 G. Cash Currency Management ...................................................................................39 H. Digital Risks and Central Bank Information Technology ......................................41 I. Central Bank Internal Organization ..........................................................................50

V. Conclusion ..........................................................................................................................51

References ................................................................................................................................72

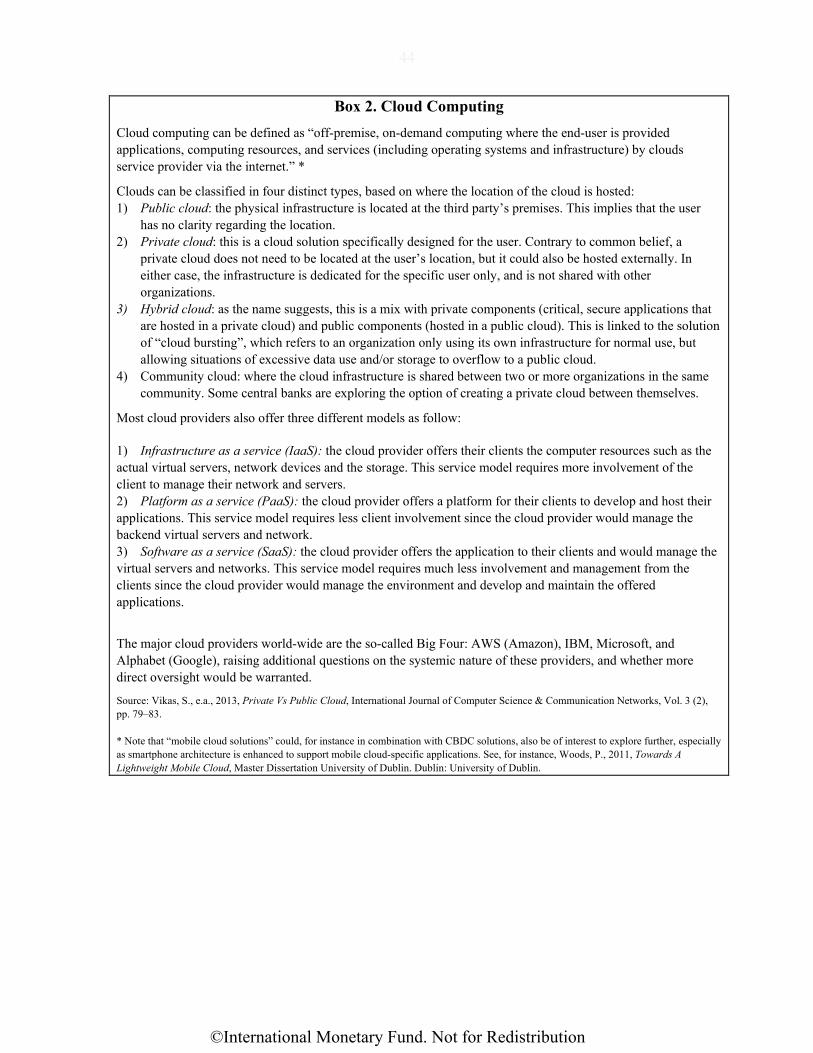

Boxes 1. Fintech and Payment and Settlement Systems.....................................................................27 2. Cloud Computing .................................................................................................................44

Figures 1. Major Technologies Transforming Financial Services ..........................................................8 2. Central Bank Risk Management, Fintech, and Cybersecurity .............................................11 3. Main Fintech Issues Discussed in the Context of IMF Risk Management TA ...................11 4. IMF Article IV References to ..............................................................................................19 5. IMF Surveillance and Fintech ..............................................................................................20 6. Google Search Interest for "Fintech" ...................................................................................20 7. IMF Article IV References to Technology ..........................................................................20 8. Selected IMF FSAP References to Fintech .........................................................................24 9. Central Bank Risk Landscape ..............................................................................................26 10. Areas of Financial Supervision in which Suptech Applications are Used .........................33 11. National Bank of Georgia: Outline of OpenRegulation ....................................................35 12. National Bank of Georgia: OpenRegulation—Legal Updating Process............................36

©International Monetary Fund. Not for Redistribution

4

13. Cash Currency and CBDC—Transfer of Possession .........................................................39 14. Countries Where Retail CBDC is Being Explored ............................................................40 15. Digital Risks to IT Systems ...............................................................................................42 16. Fintech and Central Bank Operational Resilience .............................................................45 17. Cyber Risk Management....................................................................................................50 18. Fintech and Central Bank Risk Management—Example of a Risk Matrix .......................55

Tables 1. Example: IMF TA Recommendations on Central Bank Risk Management, .......................14 2. Example: IMF TA Recommendations on Central Bank Strategic Planning, RiskManagement and Cybersecurity ..............................................................................................15 3. Example: IMF TA Recommendations on Central Bank Strategic Planning, ......................16

Appendices I. Bali Fintech Agenda .............................................................................................................56 II. Case Examples ....................................................................................................................60

©International Monetary Fund. Not for Redistribution

5

GLOSSARY

AI Artificial Intelligence AIV IMF Article IV surveillance AML/CFT Anti-Money Laundering/Combatting the Financing of Terrorism API Application Programming Interface BCBS Basel Committee on Banking Supervision BCL Banque Centrale du Luxembourg BCM Business Continuity Management BFA Bali Fintech Agenda BI Bank Indonesia BIS Bank for International Settlements BSL Bank of Sierra Leone CBDC Central Bank Digital Currencies CBLD Central Bank Legislation Database CER Committee on Emerging Risks (of IOSCO) DeFi Decentralized Finance DLT Distributed Ledger Technology ECB European Central Bank ELA Emergency Liquidity Assistance ERM Enterprise-wide Risk Management FATF Financial Action Task Force FIU Financial Intelligence Unit FMI Financial Market Infrastructure FSAP Financial Sector Assessment Program FSB Financial Stability Board FSI Financial Stability Institute GFC Global Financial Crisis GRC Governance, Risk, and Compliance GSC Global Stablecoin HR Human Resources IMF International Monetary Fund IOSCO International Organization of Securities Commissions IT Information Technology ITD Information Technology Department LIC Low-Income Countries LOLR Lender of Last Resort MCM Monetary and Capital Markets Department, IMF ML Machine-Learning NBG National Bank of Georgia NBU National Bank of Ukraine OECD Organisation for Economic Co-operation and Development ORM Operational Risk Management PF Proliferation Financing PFMI Principles for Financial Markets Infrastructures RBI Reserve Bank of India RCSA Risk Control Self-Assessment RMD Risk Management Department RTGS Real-Time Gross Settlement SME Small and Medium Enterprises SOC Security Operation Center SRA Strategic Risk Assessment TA Technical Assistance UMP Unconventional Monetary Policies

©International Monetary Fund. Not for Redistribution

6

I. INTRODUCTION

Effective risk management of central banks is imperative for managing a wide variety of increasing financial and nonfinancial risks. Central banks0F

1 across the globe have undergone an expansion of the risks that they run. This includes financial risks resulting from policy decisions, especially those in unconventional times, including during the COVID-19 pandemic—varying from asset purchase operations that have significantly expanded the balance sheets of central banks in, for instance, the United States, the United Kingdom, the European Union, and Japan, to central banks actively pursuing more aggressive, yield-increasing asset management strategies due to the low interest environment.

However, in addition to financial risks, central banks also run nonfinancial risks. These include strategy and policy risks, operational risks, and reputational risk in general. These risks can hold significant financial consequences for central banks. This has spurred an increasing number of central banks to try and quantify operational risks in particular.

However, nonfinancial risk management of central banks has traditionally not received as much attention as financial risks and their management. In an earlier IMF Working Paper,1F

2 we ascribed this to the fact that central banks’ mandates, objectives, and functions were more limited before the Global Financial Crisis (GFC), but that with the advent of the GFC those mandates got expanded further into areas beyond price stability.

Several developments over the past years have even further increased that awareness of nonfinancial risks for the central bank. The focus on topics such as climate change, economic development/employment, financial inclusion, and fintech, have led to central banks becoming public super-institutions—seemingly capable of solving most of a country’s economic and financial problems. Clearly, this has also led to central banks moving into areas that might be in the realm of the fiscal authorities—with significant consequences for central bank nonfinancial risks related to those newer areas as well.

This paper focuses on central bank nonfinancial risks specifically related to the surge of technological innovations dubbed “fintech,” including the related area of cybersecurity, and how fintech and cybersecurity strengthen the need for enhanced central bank risk management. Central banks need to carefully consider this interplay between the possible upsides of fintech, and the guaranteed downsides of cyber risks, when trying to achieve their (often multiple) objectives.

The paper draws on:

1 This paper predominantly looks at risk management of central banks. However, this includes functions such as microprudential supervision if the supervisor is incorporated into the organization of the central bank. 2 See Khan, A., 2016, Central Bank Governance and the Role of Nonfinancial Risk Management, IMF Working Paper 16/34. Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

7

1) Findings from nine (9) central bank technical assistance (TA) cases2F

3 from the IMF’s Monetary and Capital Markets Department (MCM, Central Bank Operations Division) and Information Technology Department (ITD, Digital Advisory Unit); and four (4) country cases (Indonesia, Luxembourg, Sierra Leone, and Ukraine);

2) Informal interactions on fintech with heads of risk management departments of several central bank members of the International Operational Risk Working Group (IORWG);

3) Participation in the EU’s Fintech Risk Management Project;3F

4 and

4) Findings from the IMF’s Article IV (AIV) database and from selected Financial Sector Assessment Programs (FSAP).

Section II will provide a definition and overview of “fintech” and related developments relevant for central bank risk management. Next, Section III will examine to what extent IMF technical assistance by MCM Central Bank Operations and ITD/Digital Advisory, as well as IMF surveillance has covered possible links between central bank risk management, fintech, and cybersecurity. Building on this, Section IV analyzes in more detail how specific fintech developments affect central bank risk management (focusing on strategy and policy risk, as well as operational risk). Finally, Section V draws conclusions and recommendations for central banks to consider.

Appendix I lists relevant risk management details of the Bali Fintech Agenda (BFA); Appendix II provides several country case examples.

II. FINTECH—DEFINITION, PRINCIPLES, AND RISK MANAGEMENT

Fintech, in the definition of the Bali Fintech Agenda (BFA), relates to “the advances in technology that have the potential to transform the provision of financial services spurring the development of new business models, applications, processes, and products.”4F

5 Similarly,

3 Due to the confidential nature of those TA cases, the names of the central banks involved are not mentioned. Instead, the paper has used anonymized findings from the TA reports, discussions with, and feedback from the respective central banks as the foundation for this paper. The TA cases took place between 2018 and 2020. The TA missions were all led by IMF HQ staff from MCM and ITD, and comprised external experts on risk management, strategic planning, governance and organization, from various central banks.

4 See https://www.fintech-ho2020.eu/. Staff from MCM participated in several meetings of the EU Fintech Risk Management Project, and engaged with participants (academic institutions, central banks, financial supervisors, and fintech firms).

5 BFA, p. 12.

©International Monetary Fund. Not for Redistribution

8

the Financial Stability Board (FSB)5F

6 defines fintech as “technologically enabled innovation in financial services that could result in new business models, applications, processes or products with an associated material effect on financial markets and institutions and the provision of financial services.” Both definitions cover the extensive use of data by (and technological advances to) financial services, and leverage the explosion of Big data on individuals and firms, advances in AI/ML, computing power, lowering capital cost, cryptography, distributed computing and the reach of the Internet. The strong complementarities among these technologies give rise to an array of new applications touching on services from payments to financing, asset management, insurance, and advice. This creates the possibility of entities driven by fintech emerging as competitive alternatives to traditional financial intermediaries, markets, and infrastructures.6F

7

Fintech-related technologies have broad effects on a range of financial services. Figure 1 below demonstrates how AI, Big data, Distributed Computing, cryptography, and mobile access internet influence financial services from payments, to saving and lending, risk management, and financial advice (the latter could include components of consumer protection and financial inclusion as well).

Figure 1. Major Technologies Transforming Financial Services

Source: IMF, 2017, Fintech and Financial Services: Initial Considerations. IMF Staff Discussion Note 17/05. Washington, D.C.: International Monetary Fund.

6 https://www.fsb.org/work-of-the-fsb/financial-innovation-and-structural-change/fintech/#:~:text=The%20FSB%20defines%20FinTech%20as,the%20provision%20of%20financial%20services.

7 IMF, 2017, Fintech and Financial Services: Initial Considerations. IMF Staff Discussion Note 17/05. Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

9

Risk management has been identified as relevant to fintech developments. The IMF/WB Bali Fintech Agenda (BFA)7F

8 highlights the necessity for central banks and supervisors to examine risk management components of fintech. BFA Principle IX (Ensure the Stability of Domestic Monetary and Financial Systems, see Appendix I) stresses that fintech “offers central banks the opportunity to explore new services, while having to consider new risks.” It focuses on policy aspects relating to Central Bank Digital Currencies (CBDC), payments systems, as well as financial stability aspects, including the lender of last resort-role of central banks.

The BFA includes a specific focus on risk management of fintech. Principle X (Develop Robust Financial and Data Infrastructure to Sustain Fintech Benefits, see Appendix I) stresses that “[e]ffective governance structures and risk-management processes are important to identify and manage risk associated with the use of fintech. The greater reliance on such technologies leads to new operational risks and more interdependencies among service providers… that may threaten the operational resilience of financial and data infrastructures.” This includes risks related to outsourcing, as Principle X refers to third-party service providers, and the fact that many of these providers “fall outside the regulatory perimeter,” which would require “increased emphasis on managing operational risks and ensuring robust outsourcing arrangements.” These risks may reach such significant levels that require the development of a specific vendor risk management framework.

Principles IX and X are focused on fintech-related risks for financial institutions. However, the risk management aspects of the principles hold for central banks to a large extent as well, as the next sections will explore.

III. THE IMF’S INVOLVEMENT WITH “FINTECH” AND RISK MANAGEMENT

The IMF has been involved with “fintech” over the past decades. Though the concept of “fintech” was not necessarily used as such, much of the IMF work in surveillance, policy development, and technical assistance relates to technological developments in and of the financial sector, including of central banks and their risk management.8F

9

IMF technical assistance (TA) covers all the areas that the IMF works on. As noted, this paper looks at TA provided by the IMF in the context of central bank operations (central bank risk management, governance, internal organization, and cash currency management) and digital advice (in particular, cybersecurity).

8 IMF/WB, 2018, The Bali Fintech Agenda. IMF Policy Paper. Washington, D.C.: International Monetary Fund. 9 The IMF, of course, also assists countries by providing financial support through loans. As part of these lending operations, the IMF’s Finance Department conducts Safeguards Assessments. The Assessments examine, i.a., the internal control framework (including risk management) of the central bank. However, given the highly confidential nature of Safeguards Assessments, this paper does not look at possible fintech and cybersecurity findings based on Safeguards Assessments.

©International Monetary Fund. Not for Redistribution

10

The paper also examines IMF surveillance findings. Surveillance involves the IMF monitoring risks to domestic and global stability. The Fund does so by means of consulting with its member states, which is often referred to as the Article IV (AIV) discussions. These discussions with country authorities focus on exchange rate issues, monetary, fiscal, and regulatory policies, as well as macro-critical structural reforms.

Lastly, the IMF also gauges stability and soundness of the financial sector and assesses the financial sector’s potential contribution to growth and development. The IMF does so by means of its Financial Sector Assessment Program (FSAP), of which selected findings are also presented in the paper

In these three modalities—TA, AIVs, FSAPs—attention for fintech and cybersecurity, and to a certain extent (central bank) risk management, is visible and made concrete, as the following subsections will highlight.

A. Technical Assistance: Advice on Fintech in the Context of Risk Management

TA by MCM and ITD on fintech and central bank risk management has increased since the publication of the BFA. In the period 2018–2020, MCM (in several cases together with ITD) provided central bank risk management TA, as well as bilateral advice to and discussions with central banks in all regions of the world, with a distinct fintech focus.

As Figure 2 shows, most TA and informal interactions in the period 2018–2020 on fintech and central bank risk management took place with central banks in the European and Middle East and Central Asia regions, and on the topics of (1) central bank risk management in general (including Business Continuity Management, BCM), followed by (2) fintech organization (i.e., relating to the central bank’s internal organization of fintech-related activities, for instance, by considering the setting up of a dedicated fintech unit), (3) central bank cybersecurity, and, in two cases, (4) developments of digital payments in the context of central bank risk management and cash currency management.9F

10

10 Of course, this is not indicative of IMF TA on digital payments separate from central bank risk management.

©International Monetary Fund. Not for Redistribution

11

Figure 2. Central Bank Risk Management, Fintech, and Cybersecurity

Source: authors.

The main categories of questions raised by the respective central banks related to the following fintech components (see Figure 3 below):

Figure 3. Main Fintech Issues Discussed in the Context of IMF Risk Management TA

Source: IMF staff.

1

6

5

1

2

WHD EUR MCD APD AFR

6

8

4

2

FintechOrganization

RiskManagement(general) &

BCM

Cyber security DigitalPayments

0 2 4 6 8 10 12 14 16

Risk Management / (1) Role and Involvement of theRisk Management Department, (2) Cyber Security

Decision-making / Role and Involvement ofManagement and Board

Internal Organization / (1) Need for and role of apossible Fintech Unit, (2) training of staff, (3)information-sharing between departments

Cash Currency Management / development of digitalpayments

(a) Interactions (missions, advice, discussions) by region (2018-2020)

(b) Main topics of discussion (2018-2020)

AFR: Africa APD: Asia and Pacific EUR: European MCD: Middle East and Central Asia WHD: Western Hemisphere

©International Monetary Fund. Not for Redistribution

12

1) Risk Management: ensuring fintech risks that may affect the central bank are adequately covered by the central bank’s risk management department. In several cases, the central bank risk management departments were not fully aware of emerging fintech risks, for instance, related to cloud computing (see also Section IV (H))—even though risks related to the use of third-parties and outsourcing in general did exist (for instance, related to general procurement and use of service from third-parties). In another case, the risk management department arranged for a presentation by the central bank’s fintech department to the IMF TA mission and the risk management department itself. The presentation covered key domestic fintech developments among financial institutions. Subsequently, the discussion between the fintech department and the risk management department allowed for the risk managers to be further informed of key fintech developments, and be able to translate them into developments that might affect the central bank itself. In general, closer cooperation between the central bank’s (i) IT department, (ii) fintech department (where applicable), and (iii) financial supervision department (where applicable) proved to be beneficial, as often fintech-related knowledge was already available “in house,” but not necessarily available to the risk management department. This also included identifying cyber risks emerging from fintech developments and ensuring sufficiently strong central bank cyber resilience are in place/are being developed. Several TA missions also focused on details of central bank security posture, and whether the involvement of third-party vendors would be sound from a central bank risk management perspective. Experiences from other central banks were shared, including on how to set up a central bank Security Operation Center (SOC),10F

11 conduct cybersecurity assessments (including red, blue, and purple teaming exercises) mainly to examine the SOC’s effectiveness, and provide assurance to central bank decision-makers on cybersecurity arrangements.

2) Decision-making: ensuring the central bank’s decision-makers (i.e., senior management and Board) are adequately aware of fintech opportunities and risks in their jurisdiction and are aware of how these developments could feed into the central bank’s strategic planning process and its internal risk management. In most cases, the central bank’s key decision-makers (i.e., members of the decision-making body/bodies, such as the governor, deputy governors, and nonexecutive Board members—where applicable) were not fully informed of, or up to date on relevant fintech and cybersecurity developments and how these could affect the central bank’s risks (or provide opportunities), and no discussions had taken place in the context of the central bank’s risk appetite. Often this turned out to be a more systemic central bank governance issue, as in

11 SOC is a security operations center formed within an organization to handle security related events and incidents at the technical level. SOC rely on network traffic, node health and application behavior to monitor the network and systems for anomalies and are usually capable of responding and eliminating the threat.

©International Monetary Fund. Not for Redistribution

13

three cases the decision-making body was not at full strength, with in particular nonexecutive Board members’ position not yet being filled—even though especially nonexecutive Board members would have a key role to play in identifying strategic developments, including those relating to fintech, cybersecurity, and the role of and effect on the central bank. Additionally, some of these cases also highlighted internal silos, with a fintech department reporting to one specific decision-maker, and risk management reporting to another, without proper information-sharing arrangements.

3) Internal Organization: facilitating internal central bank discussions on whether there is a need and necessity to have a fintech unit, roles and responsibilities of such a unit, and place within the internal organization. In three cases, the central bank requested IMF advice on how to set up a fintech department, without it necessarily being clear what such an organizational unit would focus on. In most cases, the fintech department aimed at contributing to financial supervision by identifying fintech developments among financial institutions, examining licensing requirements—including in the context of a regulatory sandbox. In one other case, the fintech department was specifically set-up to contribute to financial inclusion, highlighting less of a focus on upholding prudential requirements, and more on deepening the financial market.

Other internal organization issues the respective TA missions provided support on, related to ensuring central bank staff (in particular financial supervisors, IT staff, risk management staff) had a proper understanding of relevant fintech developments, and were able to update their knowledge and expertise on a regular basis – in the case of one central bank, it moved to having regular, open meetings with fintech companies at the central bank’s premises, allowing them to showcase their products and services, facilitating interaction with central bank staff, and thereby enhancing the central bank’s staff’s understanding of relevant fintech developments. Cooperation with other involved agencies and donors, including the United Nations and the World Bank, proved to be helpful as well, with fintech experts from their sides providing training to central bank staff in specific fintech areas.

4) Cash Currency Management: discussions on the interaction between cash currency management and related risks, and the development of digital payments. In few cases, the risk management department and the currency department raised concerns about moving towards a more cashless society, and/or the increased practical use of digital payments. In one case this related to the use of SIM chips and money stored on those SIM chips, including questions on which agencies would be responsible for overseeing the respective telephone operators. In another case, the central bank presented its case on a (CBDC and how it had identified opportunities as well as risks for the central bank itself. In another example, the central bank was exploring the possibility of issuing a CBDC, and the IMF highlighted a number of operational issues and gaps within the central bank’s cyber resilience program to improve internal processes, technologies and skillset needed to maintain a high-level of assurance of their standing infrastructure,

©International Monetary Fund. Not for Redistribution

14

and to include the newly introduced CBDC ecosystem as well. One of the issues highlighted, which was raised by the central bank internal security team, was the lack of a SOC within the central bank to monitor their infrastructure and systems, capable of instantly responding to any threat or incident. Running a SOC capable of monitoring and responding 24/7/365 days to any security issue is fundamental to fintech services specially with more widely accessible systems such as CBDC in comparison to closed traditional payment systems with selective participants (usually commercial banks and credit unions). This is under the assumption that the central bank is maintaining the backend core-system.

Practical examples of IMF TA recommendations on central bank risk management and how fintech and cybersecurity (should) tie into risk management are provided below. Tables 1 and 2 below provide anonymized examples of recommendations from the IMF in two recent MCM TA missions.

Table 1. Example: IMF TA Recommendations on Central Bank Risk Management, Fintech, and Cybersecurity

# Theme Recommendation Actor(s) Time Frame 1 Risk

Management Diagnostic

Appoint remaining central bank Nonexecutive Board members (and provide support for their nonexecutive responsibilities), in line with IMF Safeguards Recommendations.

[Governor to highlight the necessity]

As soon as possible

2 Engage with central bank Nonexecutive Board members on strategic planning (initially, only focusing on strategic risk assessment, see below).

[Governor to highlight the necessity]

After appointment of remaining Nonexecutive Board members

3 Strategic Risk Management

Prepare for/conduct a Strategic Risk Assessment (SRA), built on Operational Risk Management ORM) achievements, complete a multilayered perspective to avoid risk blindsides.

Risk Management Department (RMD)

12-18 months

4 Develop Enterprise-wide Risk Management (ERM) to strengthen, streamline and integrate oversight and performance.

RMD 18-24 months

5 Fintech Integrate Fintech Unit’s (fintech risk) findings within the central bank’s risk management Framework.

RMD, Fintech Unit

1-6 months

6 Enhance fintech governance/compliance research with technologists within the RMD.

RMD 6-12 months

7 Conduct a cybersecurity gap assessment, addressing: a) Central bank cyber resilience; and b) Early security assurance research/activities

for fintech adoption.

RMD 6-18 months

Source: IMF.

©International Monetary Fund. Not for Redistribution

15

Table 2. Example: IMF TA Recommendations on Central Bank Strategic Planning, Risk Management and Cybersecurity

# Theme Recommendation Actor(s) Time Frame 1 Strategic

Planning Appoint central bank nonexecutive members (and provide support for their nonexecutive responsibilities), in line with IMF Safeguards Recommendations.

[Governor to highlight the necessity]

[asap]

2 Adjust the Strategic Objectives to express how the central bank intends to deliver the priorities in the Strategic Plan. Undertake a thorough review of the strategy planning and monitoring procedures based on the information shared by the mission and re-consider what strategic planning information is made public.

Governor (sponsor), Risk Management Department (RMD)

3-6 months 12-24 months

3 Have the central bank’s nonexecutive Board members monitor implementation of the Strategic Plan at a sufficient frequency and to a sufficient depth, to facilitate timely challenge and support by the nonexecutives.

Board Ongoing (after appointment)

4 Risk Management

Develop a Risk Management Framework and Risk Appetite.

RMD 12-15 months

5 Ensure empowerment and presence of the risk management function, including monitoring strategic plan progress and risks, and mandatory participation in the central bank’s key forums.

Governor (sponsor), RMD

Ongoing

6 Create further awareness of risk management and of the departmental risk champions.

RMD Ongoing

7 Conduct a Risk Control Self-Assessment (RCSA) of processes.

RMD 6-12 months

8 Set up the incident registration process. RMD 12-18 months 9 Incentivize risk management research and

benchmarking. RMD Ongoing

10 Cyber Security

Strengthen the cyber resilience and security posture.

RMD, IT Department (ITD)

24 months

11 Build and launch the Security Operations Center (SOC) capabilities and perform periodic evaluation exercises.

RMD, ITD 18-30 months

12 Enhance cybersecurity risk management and security assurance activities during the evaluation, development or acquisition of new and existing information technology projects and systems.

RMD, ITD Ongoing

13 Adopt a cloud computing strategy. RMD, ITD 24 months

Source: IMF.

©International Monetary Fund. Not for Redistribution

16

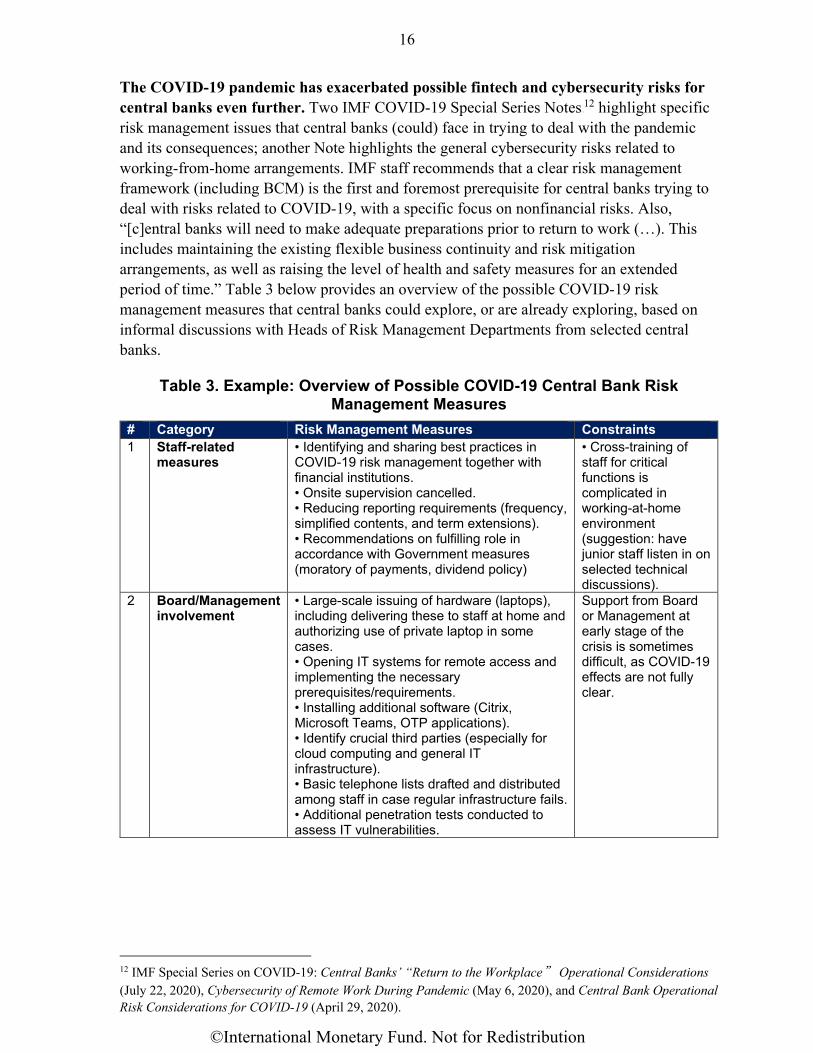

The COVID-19 pandemic has exacerbated possible fintech and cybersecurity risks for central banks even further. Two IMF COVID-19 Special Series Notes11F

12 highlight specific risk management issues that central banks (could) face in trying to deal with the pandemic and its consequences; another Note highlights the general cybersecurity risks related to working-from-home arrangements. IMF staff recommends that a clear risk management framework (including BCM) is the first and foremost prerequisite for central banks trying to deal with risks related to COVID-19, with a specific focus on nonfinancial risks. Also, “[c]entral banks will need to make adequate preparations prior to return to work (…). This includes maintaining the existing flexible business continuity and risk mitigation arrangements, as well as raising the level of health and safety measures for an extended period of time.” Table 3 below provides an overview of the possible COVID-19 risk management measures that central banks could explore, or are already exploring, based on informal discussions with Heads of Risk Management Departments from selected central banks.

Table 3. Example: Overview of Possible COVID-19 Central Bank Risk Management Measures

# Category Risk Management Measures Constraints 1 Staff-related

measures • Identifying and sharing best practices in COVID-19 risk management together with financial institutions. • Onsite supervision cancelled. • Reducing reporting requirements (frequency, simplified contents, and term extensions). • Recommendations on fulfilling role in accordance with Government measures (moratory of payments, dividend policy)

• Cross-training of staff for critical functions is complicated in working-at-home environment (suggestion: have junior staff listen in on selected technical discussions).

2 Board/Management involvement

• Large-scale issuing of hardware (laptops), including delivering these to staff at home and authorizing use of private laptop in some cases. • Opening IT systems for remote access and implementing the necessary prerequisites/requirements. • Installing additional software (Citrix, Microsoft Teams, OTP applications). • Identify crucial third parties (especially for cloud computing and general IT infrastructure). • Basic telephone lists drafted and distributed among staff in case regular infrastructure fails. • Additional penetration tests conducted to assess IT vulnerabilities.

Support from Board or Management at early stage of the crisis is sometimes difficult, as COVID-19 effects are not fully clear.

12 IMF Special Series on COVID-19: Central Banks’ “Return to the Workplace” Operational Considerations (July 22, 2020), Cybersecurity of Remote Work During Pandemic (May 6, 2020), and Central Bank Operational Risk Considerations for COVID-19 (April 29, 2020).

©International Monetary Fund. Not for Redistribution

17

Table 3. Example: Overview of Possible COVID-19 Central Bank Risk Management Measures (Continued)

• Increased staff awareness activities,

especially relating to phishing (all central banks) and information protection. • Central bank VPN monitored 24x7 by cyber security division.

3 Communication • Internal: avoiding fake news, boosting morale (videos or messages by Governor and by the Board) providing info on health care services, clear feedback from Board/Management. • External: public communication, as well as sharing information with stakeholders (ministries, other regulators). • In some cases, crisis communication actions were needed after a confirmed case was detected among bank’s staff, as well as to avoid fake news.

Difficult to keep up with continuously changing news; central bank needs to be proactive, fast, and accurate.

4 Interaction with financial sector

• Identifying and sharing best practices in COVID-19 risk management together with financial institutions. • Onsite supervision cancelled. • Reducing reporting requirements (frequency, simplified contents, and term extensions). • Recommendations on fulfilling role in accordance with Government measures (moratory of payments, dividend policy)

5 IT and cyber-security

• Large-scale issuing of hardware (laptops), including delivering these to staff at home and authorizing use of private laptop in some cases. • Opening IT systems for remote access and implementing the necessary prerequisites/requirements. • Installing additional software (Citrix, Microsoft Teams, OTP applications). • Identify crucial third parties (especially for cloud computing and general IT infrastructure). • Basic telephone lists drafted and distributed among staff in case regular infrastructure fails. • Additional penetration tests conducted to assess IT vulnerabilities. • Increased staff awareness activities, especially relating to phishing (all central banks) and information protection. • Central bank VPN monitored 24x7 by cyber security division.

• Almost no central bank had deployed or tested telework (working-at-home) in a large-scale in the past. • Cyber risk is biggest concern, especially with weak endpoints (e.g., private laptops, including for critical services), and limited data-protection measures. Phishing attacks on staff are on the increase. • Unclear whether IT infrastructure can support this situation in the mid- to long-run/cracks appearing.

©International Monetary Fund. Not for Redistribution

18

Table 3. Example: Overview of Possible COVID-19 Central Bank Risk Management Measures (Concluded)

6 Overall risk

management • Examining if existing legislation and measures are sufficient for (policy and operational) responses. • Increasing monetary policy risk tolerance to allow easier access to liquidity. • Examining overall effects of monetary policy measures on risk exposure of central bank • Reviewing risk appetite. • Strategic risk assessment needed to see if central bank can still achieve its (legal) mandate – need to reprioritize objectives, including postponing larger projects. • Risk Management Department (RMD) plays key role in collecting bank-wide information for Management & Board. In some cases, RMD powers are significantly expanded to collect risk data directly from departments without departmental management involved. • BCM planning were not sufficient (these kinds of extreme scenarios were never included/tested). Some banks had to define new strategies based on worst case scenarios. • Enhanced assessments of critical functions, and staff (when less than 6 people can perform a critical activity). For some central banks critical processes were expanded from the ‘normal’ 50 to currently 300 – due to predications based on an extended 90-day window for COVID-19 effects • Extension of BCM scope to all central bank activities, including those who were initially considered non-critical. • Development of new internal risk templates to minimize administrative burden on departments.

Legal and reputational risks emerging due to central banks conducting additional (policy) measures, changed public opinion, and effects on financial institutions.

7 Cash currency management

• Minimized interpersonal contacts by more shifts, social distancing, additional cleaning/sanitization of buildings and equipment including between shifts. • Quarantining of banknotes between 7 to 15 days. • Still some limited interaction with financial institutions in the form of cash deliveries; no more printing of new banknotes, no more sorting of banknotes and no more flights with banknotes. No sanitization of banknotes was carried out by central banks. • Strategic stock of banknotes in branches is increased to 3 months. • Active encouragement of electronic payments and online transactions (by reducing or eliminating usage fees during the crisis period)

Cash currency management is most sensitive area for new COVID-19 central bank infections.

Source: IMF, 2020, Central Bank Operational Risk Considerations for COVID-19. IMF Special Series on COVID-19 Note. Washington D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

19

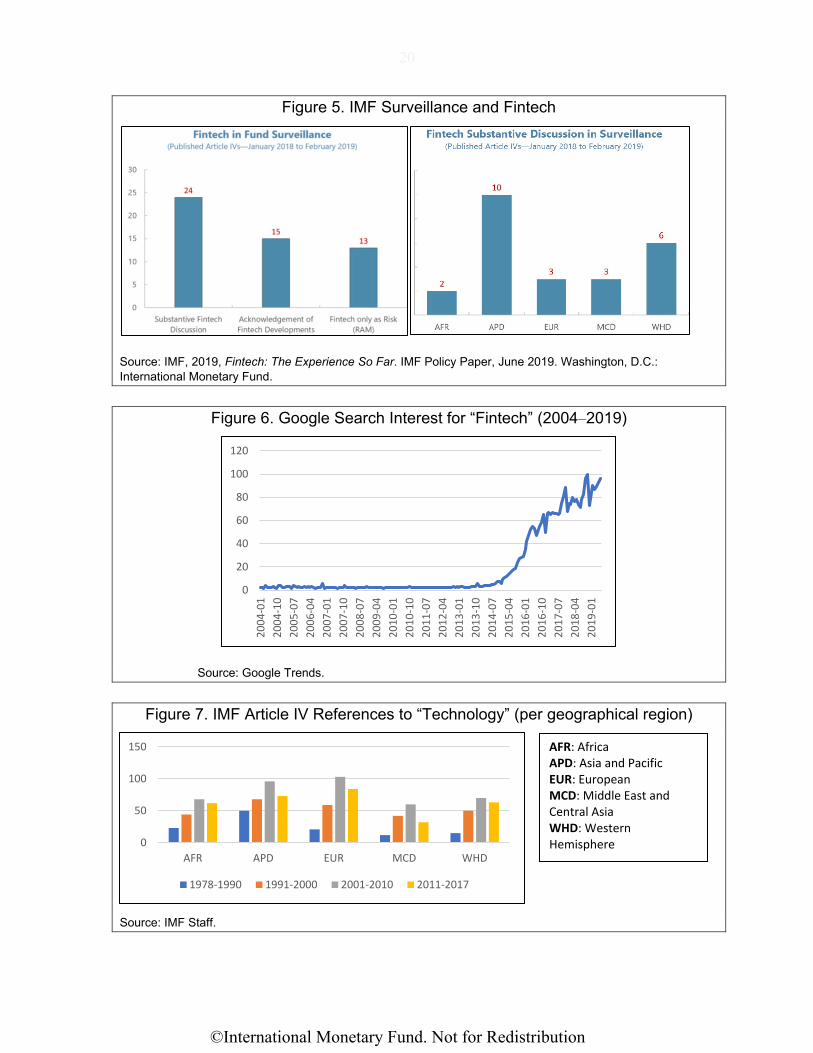

B. IMF AIV: Fintech, Cybersecurity, and Risk Management References

When examining the IMF’s Article IV (AIV) database, 1,095 unique hits12F

13 can be found relating to “technology,” spanning the period from 1978 until 2017.

Figure 4 below highlights the number of references per year for different time periods. Clearly, there has been a significant increase in AIV references to technology-related issues in/of the financial sector over the past years, with the period after 2011 showing the bulk of attention for technology-related issues in AIVs.

Figure 5 zooms in on fintech discussions in the one-year period between January 2018 and February 2019—where the majority of fintech issues which are classified as “substantive discussions,” followed by the more generic acknowledgement of fintech in the AIV (without further substantive discussion).

The geographical attention for technology-related issues between 1978–2017 is predominantly centered on the African and European regions (Figure 7); in the period January 2018–February 2019 this moved to Asia Pacific and (to a lesser extent) Western Hemisphere (Figure 5). This significantly increased attention coincides with the increase in general attention for “fintech,” as Figure 6 demonstrates (Google search for “fintech”).

Figure 4. IMF Article IV References to “Technology” (per time period, average per year, 1978–2017)

Source: IMF Staff.

13 A unique hit relates to an AIV report in a specific time period, for a specific country. One report can contain many references, but the entry is only counted as 1 for the purposes of this paper. Note that the IMF AIV database is an internal database consisting of AIV documents dating back to approximately 1978.

9.32.63 3.97

44

0

10

20

30

40

50

1978-1990 1991-2000 2001-2010 2011-2017

©International Monetary Fund. Not for Redistribution

20

Figure 5. IMF Surveillance and Fintech

Source: IMF, 2019, Fintech: The Experience So Far. IMF Policy Paper, June 2019. Washington, D.C.: International Monetary Fund.

Figure 6. Google Search Interest for “Fintech” (2004–2019)

Source: Google Trends.

Figure 7. IMF Article IV References to “Technology” (per geographical region)

Source: IMF Staff.

0

20

40

60

80

100

120

2004

-01

2004

-10

2005

-07

2006

-04

2007

-01

2007

-10

2008

-07

2009

-04

2010

-01

2010

-10

2011

-07

2012

-04

2013

-01

2013

-10

2014

-07

2015

-04

2016

-01

2016

-10

2017

-07

2018

-04

2019

-01

0

50

100

150

AFR APD EUR MCD WHD

1978-1990 1991-2000 2001-2010 2011-2017

AFR: Africa APD: Asia and Pacific EUR: European MCD: Middle East and Central Asia WHD: Western Hemisphere

©International Monetary Fund. Not for Redistribution

21

It should be noted that “finance and technology” references in the context of AIVs are understandably broader than the current scope of “fintech.” The AIV references to finance and technology, as well as cybersecurity, often relate to different sets of findings, such as:

a) General investment/foreign direct investment (FDI) policies;

b) Agricultural technology (including drilling and mining), and other application areas of technology (including space technology); and

c) Fiscal technology (i.e., to improve fiscal operations, including tax revenue collection).

However, within the search results of “finance and technology,” several subsets of areas of interest can be identified that could relate to central bank risk management as well, including:

a) Information (and communication) technology: references include the building of IT capacity at central banks and Y2K-related risks, which would come closest to the current concept of fintech;

b) Financial inclusion technology, which aligns with one of the key goals of fintech often mentioned by central banks—see below;

c) Digital development strategies: this includes government-wide strategies, as well as the building of technology hubs (in particular, around the turn of the century), which is similar to jurisdictions like Singapore, UAE, and Hong Kong SAR positioning themselves as fintech hubs and fintech innovation centers.

d) Telecommunications development;

e) In occasional cases, explicit references to “fintech” can already be found. In the case of one European country reference is made to “regtech” avant la lettre (2001), as is the case for “fintech” in another European country (2016); and

f) Cybersecurity: out of the 1,095 AIV search hits on technology, only three AIVs could be found with explicit references to cybersecurity. These AIVs all took place after 2015, and generally highlight the role of the authorities in bolstering resilience to cyber-attacks (with one explicit reference to the Bangladesh Bank cyber heist), including in commercial banks.

The IMF13F

14 notes that the most recent AIV cases where fintech was discussed, relate to links between digital payments and financial inclusion (for instance, Cambodia, Peru, and Tuvalu), as well as “setting up appropriate frameworks and safeguards to develop crypto-assets,

14 IMF, 2019, Fintech: The Experience So Far. IMF Policy Report. Washington, D.C.: International Monetary Fund, pp. 9-12.

©International Monetary Fund. Not for Redistribution

22

including digital currencies projects in small states (the Republic of Marshall Islands (RMI) and Curacao and Sint Maarten).” Additionally, fintech has been brought up in the AIV context regarding China’s fintech industry, and development of financial centers into so-called fintech hubs (such as Hong Kong SAR and Singapore).

On a side note, the links between finance and technology and climate change (risks) should also be noted. In several AIV cases, the links with climate change and the role of the financial sector are made explicit, highlighting how several of the IMF’s overarching policy areas and the accompanying macro-financial risks, are closely related. Examples include considerations on the introduction of low-carbon technologies and noting how the presence of only rudimentary technology has created vulnerabilities to climate change-related issues.

Specific risk management references in the context of “fintech” cover various areas. Most references14F

15 in the IMF’s AIV database relate to risk management in the context of operational risk for financial sector oversight, that is, in the context of financial supervision. Often, concerns are raised regarding outsourcing of specific activities by financial institutions, and whether third-party risk is managed properly. In those cases where outsourcing aspects of governmental services (including the outsourcing of supervisory functions, and the development of “e-government”) are identified, risk concerns are not often noted explicitly, or possibly overlooked. Instead, the upsides of cost-efficiency and higher operational efficiency are more predominant. There is some specific attention for risks of the central bank, especially in cases related to IT, as well as operational risks related to Financial Market Infrastructures (FMIs) and setting up and maintaining infrastructure for RTGS systems.

Central bank-related cybersecurity risks have emerged only more recently. Several AIV cases, predominantly after 2015, refer to “cyber” issues. This relates to initiatives to reinforce central bank cyber-security, especially after the Bangladesh Bank’s “cyber-heist” in February 2016—which is referred to in a couple of cases.

Concludingly, IMF attention for fintech will likely only continue to increase in its areas of surveillance, affecting most of the Fund’s membership. Earlier references in AIVs to finance and technology highlight that IMF staff are aware of opportunities and risks that countries—their central banks, supervisors, and other public agencies—might run because of technological developments. Attention has been given predominantly to IT, financial inclusion technology, digital development strategies, telecommunications development, and some initial “fintech” activities. The Fund stresses this increased attention by highlighting that further “advances in AI, digital identification and cybersecurity are enabling new models

15 Search terms that were used included “outsourcing” (for possible links to outsourcing of IT/technology components of the central bank) and “operational risk” (for possible links to operational risks that the central bank may run related to IT or other technological aspects)

©International Monetary Fund. Not for Redistribution

23

for managing risk for individuals, financial institutions, and regulators.”15F

16 Substantive discussions on fintech in AIVs are increasingly common, and authorities would do well to prepare for these discussions accordingly.

C. IMF FSAP

Attention for the links between risk management, fintech, and cybersecurity in IMF FSAPs is also increasing.

The Switzerland FSAP16F

17 stresses that “[r]isks in the rapidly growing fintech space may not be well understood due to data gaps, resource constraints, and the authorities’ liberal approach.” It recommends that the Swiss authorities, including the central bank and the financial supervisor, address data collection, analytical capacity, and resources for dealing with fintech-related challenges. This on its turn “should also inform development of fintech-related policies and legislation.”

The FSAP on Singapore17F

18 noted that “fintech developments hold the promise of having a far-reaching impact on the Singaporean financial services sector, bringing both opportunities and new risks,” for clients, financial institutions, and the financial system as a whole. This could include questions relating to (the applicability of) regulation and the absence of internationally agreed standards, forcing the authorities to “ensure an appropriate balance between opportunities and risks.” Though the FSAP mainly talks about financial institutions, its statement that “uncertainty surrounding technology” might pose challenges, could likely extend to the central bank (the Monetary Authority of Singapore) as well. Even more so as the main fintech risks are noted as operational and technology-related risks: “Execution risks to implement new strategies and manage business and technology risks are increasingly top risk priorities. Yet a complicating factor are banks’ legacy systems with older, slower, and less agile systems increasing banks’ inherent risk profile. Additionally, an increasing use and reliance on third-party service providers is evident in the sector” (underlining added). This would, as we have noted already, arguably also apply to central banks, in particular those that have not sufficiently invested in their internal organization, systems, and processes (though it should be stressed that this was not explicitly noted in the Singapore FSAP). Lastly, and importantly, the FSAP also notes that operating a fintech sandbox is not without risk to the central bank: “[t]he potential for reputational risk from the regulatory sandbox needs to be monitored. The sandbox is new, and [the Monetary Authority of Singapore] noted its benefits

16 IMF, 2019, Fintech: The Experience So Far. IMF Policy Report. Washington, D.C.: International Monetary Fund, p. 9.

17 IMF, 2019, Switzerland Financial Sector Assessment Program. IMF Country Report No. 19/183, June 2019. Washington, D.C.: International Monetary Fund.

18 See IMF, 2019, Singapore Financial Sector Assessment Program Technical Note – Fintech: Implications for the Regulation and Supervision of the Financial Sector. Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

24

of facilitating innovation in a controlled environment. The main challenge is to strike a balance between the benefits of fintech firms experimenting in a live environment while mitigating potential downside risks.”

In the case of the FSAP on Canada18F

19, IMF staff noted that Canadian authorities were proactive in monitoring fintech developments, including through fintech research which was helpfully conducted to assess the impact on the financial system and the Bank of Canada’s core functions. The Canadian Department of Finance, additionally, worked on setting up a new retail payments oversight framework, and examine the possibilities of open banking. Lastly, a so-called “Heads of Agencies Crypto-Asset Working Group was established to coordinate efforts in monitoring developments in crypto-assets with the aim of developing a consistent and clear domestic regulatory framework.”

Most recently, in the FSAP on Korea,19F

20 it was noted that “even within an already highly technologically advanced, efficient, and inclusive financial sector, significant benefits can still be reaped from innovation in financial services.” However, “new risks could arise in time, such as increasing interconnectedness and complexity in the financial sector, the introduction of greater operational risk, and negative impact on the profitability of incumbent banks.”

Figure 8 below provides a schematic overview of the attention for fintech in the selected FSAPs mentioned above, and the specific attention for risks and risk management-related areas.

Figure 8. Selected IMF FSAP References to Fintech

Source: Authors.

19 See IMF, 2020, Canada Financial Sector Assessment Program Technical Note – Oversight of Financial Market Infrastructures and Fintech Development. Washington, D.C.: International Monetary Fund.

20 See IMF, 2020, Republic of Korea Financial Sector Assessment Program Technical Note – Technological Change, Legal Frameworks, and Implications for Financial Stability. Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

25

The relevance of IMF attention for finance and technology in AIVs and FSAPs will incentivize further awareness among central banks to ensure adequate understanding and identification of fintech-related risks that they themselves run. Legacy (IT) systems, the involvement of third parties (for instance, in the context of cloud computing—see Section IV. H and Box 2), and already identified nonfinancial risks (operational and reputational, in addition to legal risk), and the need to ensure sufficient resources (which on its turn requires proper strategic planning by the central bank) are key themes.

IV. FINTECH AND CENTRAL BANK RISK MANAGEMENT—EXAMPLES

Given the definition of fintech (Section II), and the emerging of attention for fintech in TA, AIVs, and FSAPs (Section III), it is important to examine in more detail how fintech developments could possibly affect a central bank’s risks and its risk management, by means of examples.

Fintech can hold policy risks related to several core central bank functions. Given the wide range of technologies flagged in Figure 1 above, fintech will likely affect central bank functions such as monetary policy, payments systems regulation, operations, and oversight, financial supervision (and other financial stability functions: macro prudential oversight, resolution, ELA/LOLR), cash currency management, and reserve management, as well as central bank functions in the areas of financial integrity and financial inclusion.

Figure 9 below provides an overview of central bank risks: strategy and policy risk (that are inherently the result of the central bank’s overall strategy and its policies), financial risk (as a result of financial operations), and operational risk (based on wide variety of risk categories, including IT infrastructure, cybersecurity, outsourcing, governance, and processes). Tying these together is reputational risk—a risk category that results from one or more of the other risks materializing. The subsections below will delve deeper into (i) policy risk emanating from selected central bank functions, as well as (ii) operational risk emanating from the central bank’s internal organization, to highlight how fintech and cybersecurity developments might offer opportunities to a central bank, but simultaneously also introduce or exacerbate existing central bank nonfinancial risks. This, on its turn, highlights the continued need for stronger central bank risk management, in particular as many of the highlighted risks overlap: central banks, therefore, should ensure an integrated fintech and cybersecurity analysis, including through the lens of central bank risk management.

©International Monetary Fund. Not for Redistribution

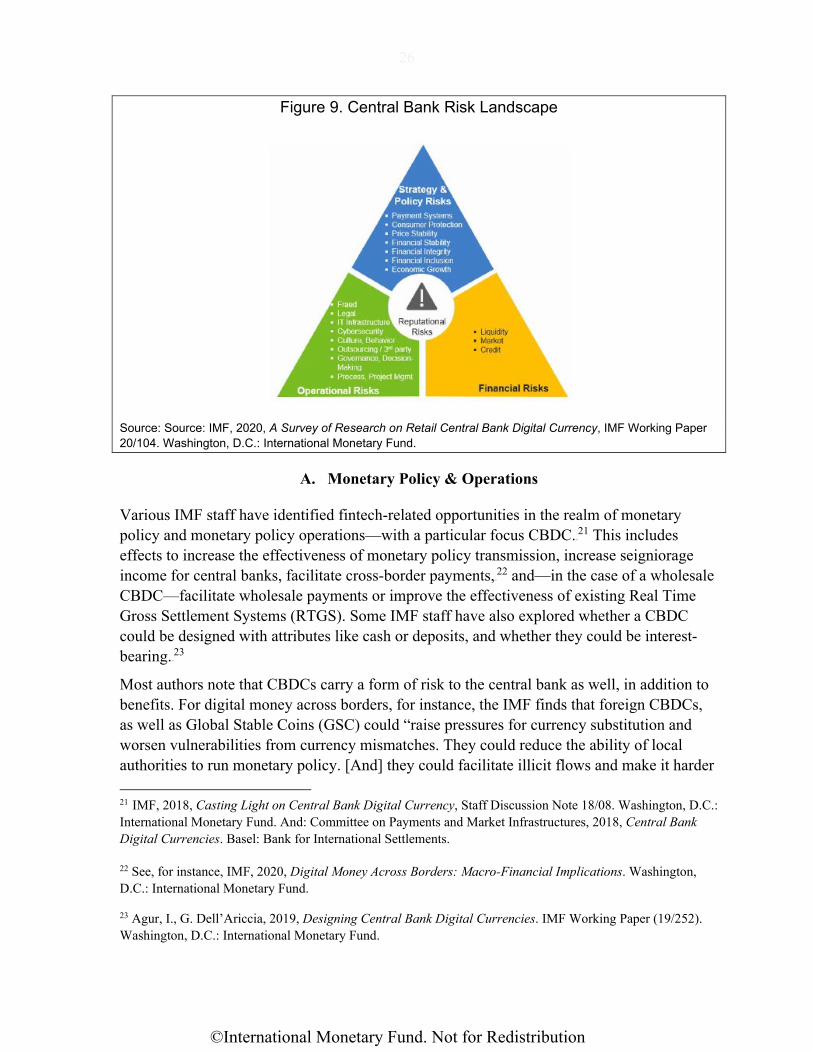

26

Figure 9. Central Bank Risk Landscape

Source: Source: IMF, 2020, A Survey of Research on Retail Central Bank Digital Currency, IMF Working Paper 20/104. Washington, D.C.: International Monetary Fund.

A. Monetary Policy & Operations

Various IMF staff have identified fintech-related opportunities in the realm of monetary policy and monetary policy operations—with a particular focus CBDC.20F

21 This includes effects to increase the effectiveness of monetary policy transmission, increase seigniorage income for central banks, facilitate cross-border payments,21F

22 and—in the case of a wholesale CBDC—facilitate wholesale payments or improve the effectiveness of existing Real Time Gross Settlement Systems (RTGS). Some IMF staff have also explored whether a CBDC could be designed with attributes like cash or deposits, and whether they could be interest-bearing.22F

23

Most authors note that CBDCs carry a form of risk to the central bank as well, in addition to benefits. For digital money across borders, for instance, the IMF finds that foreign CBDCs, as well as Global Stable Coins (GSC) could “raise pressures for currency substitution and worsen vulnerabilities from currency mismatches. They could reduce the ability of local authorities to run monetary policy. [And] they could facilitate illicit flows and make it harder

21 IMF, 2018, Casting Light on Central Bank Digital Currency, Staff Discussion Note 18/08. Washington, D.C.: International Monetary Fund. And: Committee on Payments and Market Infrastructures, 2018, Central Bank Digital Currencies. Basel: Bank for International Settlements.

22 See, for instance, IMF, 2020, Digital Money Across Borders: Macro-Financial Implications. Washington, D.C.: International Monetary Fund.

23 Agur, I., G. Dell’Ariccia, 2019, Designing Central Bank Digital Currencies. IMF Working Paper (19/252). Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

27

for regulatory authorities to enforce exchange restrictions and capital flow management measures.”23F

24 All of these issues are clearly contingent on the design of the CBDC, and the literature is very much in development.

Other relevant monetary policy aspects include broader issues relating to access to central bank money and its risk implication. That is, the provision of credit facilities, collateral and prefunding arrangements, and operational risk considerations. Central bank examples include, for example, the Bank of England’s access provision to TransferWise, as well as access to the non-bank switching company in the Australian National Payment Platform.

B. Financial Market Infrastructures

FMIs24F

25 play an important role in a country’s financial system at large. The 2012 Committee on Payments Market Infrastructures25F

26 Principles for Financial Markets Infrastructures (PFMI) were drafted precisely to help identify and mitigate risks related to this systemic nature of FMIs. FMIs “facilitate the clearing, settlement, and recording of monetary and other financial transactions [which] can strengthen the markets they serve and play a critical role in fostering financial stability.” Given this role, they could also “pose significant risks to the

24 IMF, 2020, Digital Money Across Borders: Macro-Financial Implications. Washington, D.C.: International Monetary Fund.

25 Which includes payments systems, Central Securities Depositories, Securities Settlement Systems, Central Counterparties, and Trade Repositories. 26 Previously: Committee on Payment and Settlement Systems, renamed in June 2014.

Box 1. Distributed Ledger Technology Experiments in Payments and Settlements

Distributed Ledger Technology (DLT) is a possible platform for enhancing payment systems by integrating and reconciliating settlement accounts and ledgers. Various central banks have conducted DLT research (and experiments with large-value interbank payments) to examine benefits, risks, limitations, and implementation challenges of DLT in the context of payments and settlements. This includes Brazil. Canada, the Euro area/Japan, Singapore, South Africa, and Thailand. Some central banks and private sector participants have also examined DLT for cross-border payments. Key risks of DLT, and other technologies, for payments and settlements include liquidity, credit, transaction delay, settlement finality, counterparty, and operational risks. The latter category includes cyber risk incidents. Even though these operational risks are not different from the standard computerized processing, it is the faster (real-time) environment that requires “very fast and highly automated error-handling processes to limit the volume of transactions affected by operational errors.” This, on its turn, “calls for improved monitoring systems and error-correction solutions.” Additionally, cyberattacks could “compromise data confidentiality, service availability, and systems integrity (…) [and] also affect established settlement finality rules and recovery time objectives.” The potential benefits of DLT therefore require careful consideration from a (central bank) risk management perspective. Source: Shabsigh, G., T. Khiaonarong, e.a., 2020, Distributed Ledger Technology Experiments in Payments and Settlements, IMF Fintech Note. Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

28

financial system and be a potential source of contagion, particularly in periods of market stress.”26F

27

Payments systems operations and oversight are closely linked to fintech developments. The use and operation of (real-time) settlement systems27F

28 are examined by several central banks from the viewpoint of increasing effectiveness, and/or security by applying distributed ledger technology (see Box 1). Not surprisingly, the Reserve Bank of India (RBI) recently indicated that payment and settlement systems are “technology-based substitutes for currency,” tying fintech developments in this area unequivocally to not only its FMI, but to its currency management and monetary policy functions.28F

29

The PFMI offer existing guidance on how to deal with fintech-related operational risks. Principle 17 expands on this and puts the key responsibility with the board of directors for defining operational risk (both roles and responsibilities, as well as endorsing the framework). It goes on to specify details on business continuity plans, policies relating to physical and information security, as well as outsourcing risks, and how monitoring should ideally take place. The PMFI highlight similarity with commercial risk management practices, stressing that commercial standards on information security, business continuity, and project management can be helpful for FMIs.

As an example, the RBI stresses in its recently updated Booklet on Payment Systems29F

30 regarding its FMI oversight framework that the payment landscape “has experienced extensive leveraging of advanced technology in facilitating processing of payment transactions by the PSOs [Payment Systems Operators] as well as their service providers/intermediaries/third party vendors and other entities in the payment ecosystem. On the other hand, the number, frequency and impact of cyber incidents/attacks have increased manifold.”

C. Reserve Management

As per the IMF definition,30F

31 central banks’ reserve management relates to ensuring that there are adequate official public sector foreign assets. These need to be readily available to, and

27 BIS, 2012, Principles for Financial Markets Infrastructures. Basel: Bank for International Settlement. See p.5. 28 A common case of a central bank acting as an FMI is the services it provides through the RTGS. In an RTGS, transfers from one bank to another take place in real time and on a gross basis. RTGS’ are essential for a smooth and efficient banking system. The central bank can provide the RTGS infrastructure. 29 RBI, 2018, Reserve Bank of India releases Dissent Note on Inter-Ministerial Committee for finalization of Amendments to PSS Act, RBI Press Release, October 19, 2018. 30 RBI, 2021, Booklet on Payment Systems (January 25, 2021). Mumbai: Reserve Bank of India; accessible via: https://m.rbi.org.in/scripts/PublicationsView.aspx?Id=20315#AP3.

31 IMF, 2013, Guidelines on FX Reserve Management. Washington, D.C.: International Monetary Fund.

©International Monetary Fund. Not for Redistribution

29

controlled by, the authorities for meeting their (pre-defined) objectives. Reserve management is clearly a central bank activity related to core policy decisions.31F

32 The buying, selling, and managing of the central bank’s foreign assets entail risk; not just financial, but also nonfinancial. “Reserve management should seek to ensure that (1) adequate foreign exchange reserves are available for meeting a defined range of objectives; (2) liquidity, market, credit, legal, settlement, custodial, and operational risks are controlled in a prudent manner; and (3) subject to liquidity and other risk constraints, reasonable risk-adjusted returns are generated over the medium to long term on the funds invested.”32F

33 (underlining added)

To contain/mitigate reserve management’s operational risks, proper internal governance arrangements are essential. The IMF Guidelines highlight, for instance, the need to “be guided by the principles of clear allocation and separation of responsibilities and accountabilities.” The central bank is advised to have “appropriate hierarchical levels”, a “committee structure”, and a clear separation/independence of the investment side from the risk control/management side to avoid improper incentives. Reserve management also requires checks and balances in the form of internal audits and well-trained staff. Most indicative of the operational risk effects that reserve management activities can have, is the statement that “it is important to identify the level of authority that would reconcile inconsistencies or interferences between reserve management activities and other central bank functions. Unwanted signaling effects from reserve management operations should be avoided.”33F

34

The IMF Guidelines on FX Reserve Management present34F

35 several clear examples of operational risks related to reserve management:

a) Control system failure risks: There have been a few cases of outright fraud, money laundering, and theft of reserve assets that were made possible by weak or missing control procedures, inadequate skills, poor separation of duties, and collusion among reserve management staff members.

b) Financial error risk: Incorrect measurement of the net foreign currency position has exposed reserve management entities to large and unintended exchange rate risks and led to large losses when exchange rate changes have been adverse. This has also occurred when risk has been measured only by reference to the currency composition of reserves directly under management by the reserve management unit and has not included other

32 Ibid., Article 50: “Reserve management strategies should be consistent with and supportive of a country’s or union’s specific policy environment, in particular it’s monetary and exchange arrangements.” 33 Ibid., Article 8. 34 Ibid., Section C, articles 24–33. 35 Ibid., p.26.

©International Monetary Fund. Not for Redistribution

30

foreign currency-denominated assets and liabilities on and off the reserve management entity’s balance sheet.

c) Financial misstatement risk: In measuring and reporting official foreign exchange reserves, some authorities have incorrectly included funds that have been lent to domestic banks or to foreign branches of domestic banks. Similarly, placements with a reserve management entity’s own foreign subsidiaries have also been incorrectly reported as reserve assets.

d) Loss of potential income: A failure to reinvest funds accumulating in clearing (nostro) accounts with foreign banks in a timely manner has given rise to the loss of significant amounts of potential revenue. This problem arises from inadequate procedures for monitoring and managing settlements and other cash flows and for reconciling statements from counterparts with internal records.

In all these examples, fintech could assist central banks to enhance their reserve management, for instance, by allowing machine learning applications to analyze financial patterns, identify possibly anomalies (such as related to fraud), and allow for enhanced data reporting to a central bank’s first and second lines of defense. The two most relevant fintech applications for asset management in general, as noted in a PWC study,35F

36 relate to (i) increased sophistication of data analytics to better identify and quantify risk, and (ii) automation of asset allocation. As such, PWC notes that “[m]achine learning technology is transforming risk management by enabling computers to identify patterns in market behavior and analyze transactions almost in real time.” It is not unimaginable that central bank reserve and asset managers would similarly benefit from fintech applications.

D. Financial Inclusion

Financial inclusion implies that individuals and businesses have access to useful and affordable financial products and services that meet their needs, and that are delivered in a secure, responsible, and sustainable way. Central banks increasingly have specific roles on, and responsibilities for (stimulating and/or supporting) financial inclusion, as noted above.

Fintech carries significant direct gains for financial inclusion by contributing to increased financial sector efficiency. Fintech could (1) facilitate access to credit, insurance, and pension products, (2) lower costs of cross-border transfers (including worker remittances), (3) stimulate tailored investment products, and (4) strengthen financial literacy and education. Relevant technologies relate to mobile access, API and Internet, Big data and AI, DLT, and cryptography. Indirect fintech gains could be found, for instance, by using DLT payment systems to enhance real-time payments—which could eventually help customers of

36 PWC, 2016, Beyond Automated Advice - How FinTech is Shaping Asset & Wealth Management. PWC Global FinTech Survey 2016.

©International Monetary Fund. Not for Redistribution

31

pay day lenders. Financial inclusion cases using fintech tools in one way or another can be found in different regions of the world.36F

37 Often, a combination of a high financial exclusion rate with a high cellphone penetration rate allows for leapfrogging in providing financial services to the unbanked and poorest parts of the population.

The IMF37F

38 (in the context of developments in Asia) stresses that fintech could support “growth and poverty reduction by strengthening financial development, inclusion, and efficiency,” supported by strong cellphone penetration in particular (see Zhang and Chen38F

39 for the case of China in particular). This would allow fintech applications in the areas of micro loans, as well as bookkeeping and accounting tools for Small- and Medium-Sized Enterprises.

Other central banks have indicated that they would want to enhance their decision-making on fintech and financial inclusion. The RBI, for instance, wants to “further deepen digital payments and enhance financial inclusion through FinTech… [by] appoint[ing] a five-member committee under the chairmanship of Shri Nandan Nilekani.”39F

40

Fintech could enhance financial inclusion by increased loan allocation, and lower rates—but also carries risks, including from a consumer protection perspective. See for instance Bazarbash,40F

41 who indicates that, in particular, fintech credit “has the potential to enhance financial inclusion and outperform traditional credit scoring by (1) leveraging nontraditional data sources to improve the assessment of the borrower’s track record; (2) appraising collateral value; (3) forecasting income prospects; and (4) predicting changes in general conditions.” This could lead to significantly shortened credit allocation times and lower loan rates.