11

1 WPIE Digital Content Workshop: The Case of Music Sacha Wunsch-Vincent WPIE, 1 Dec. 2004

1

WPIE Digital Content Workshop:

The Case of Music

Sacha Wunsch-Vincent

WPIE, 1 Dec. 2004

2

Outline of the PaperI. MUSIC MARKET INDUSTRY: HISTORY, SIZE AND DIFFERENT

MUSIC CARRIERS

II. INDUSTRY STRUCTURE: TRANSFORMING VALUE CHAINS AND CHANGING BUSINESS MODELS1. Traditional Record Industry Value Chain, Business models and

Players2. Traditional record industry business model

3. New Online Music Industry Value Chain, Business models and Players

4. Digital Music Value Chain

III. FILE-SHARING DEVELOPMENTS1. The rapid rise of file-sharing and its relationship to broadband2. Evidence of the effect of file-sharing on music sales3. Actions of the Music Industry against file-sharing4. Commercial / legitimate uses of file-sharing in the music industry

IV. OBSTACLES AND POLICY ISSUES

ANNEX: for example: Legal cases involving Filesharing

3

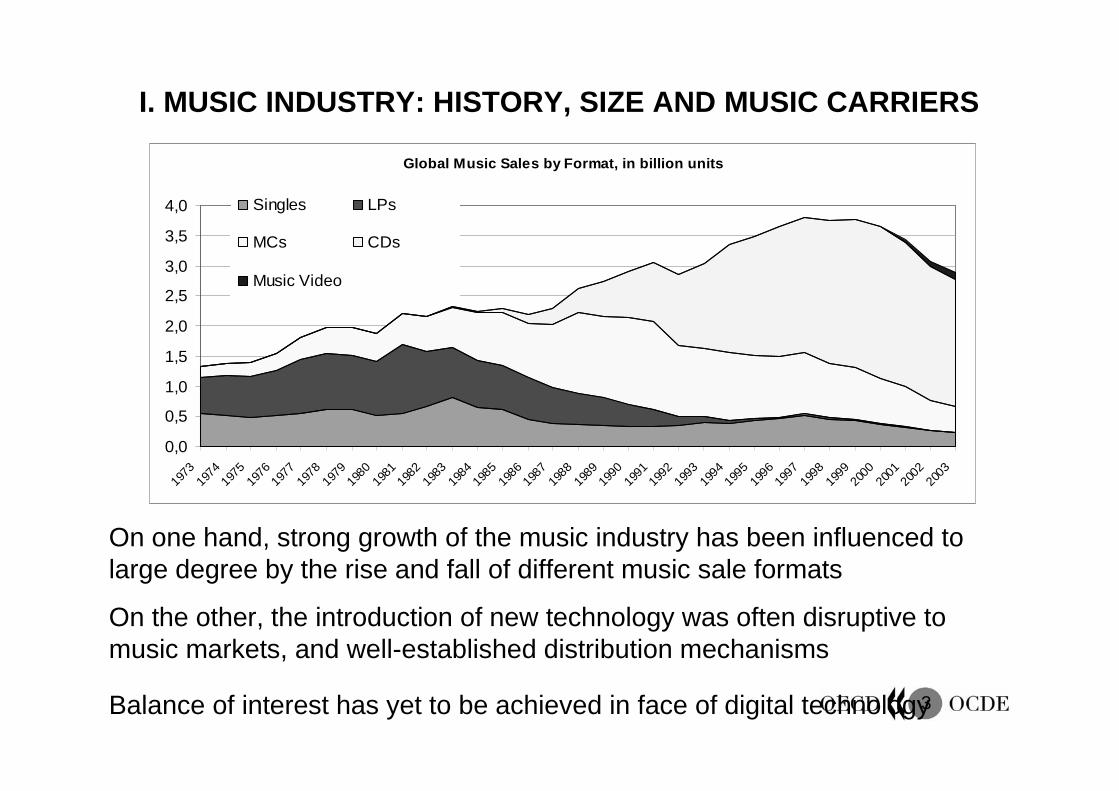

Global Music Sales by Format, in billion units

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Singles LPs

MCs CDs

Music Video

I. MUSIC INDUSTRY: HISTORY, SIZE AND MUSIC CARRIERS

On one hand, strong growth of the music industry has been influenced to large degree by the rise and fall of different music sale formats

On the other, the introduction of new technology was often disruptive to music markets, and well-established distribution mechanisms

Balance of interest has yet to be achieved in face of digital technology

4

Advent of digital technology: Opportunity and challenge for the music industry

Drop in music sales after 1999 which is not universally shared across all OECD marketsMusic industry reactions: Lawsuits, first commercial online music offerings and CD price cuts2003 continued fall in music sales but first signs of recovery2004 as year of turnaround of the music industry?Rise of the online music market– More than 130 online music stores / 150 million downloads through

Apple– Emerging as “meaningful revenue stream” Large additional revenues

accrue to third players – Impact of online music on artists and their discovery, and on users not

captured by these assessments. – Citizens interacting with content and information, making them active

participants in the whole chain of content creation, marketing and distribution (Krasilovsky, Shemel and Gross, 2003).

5

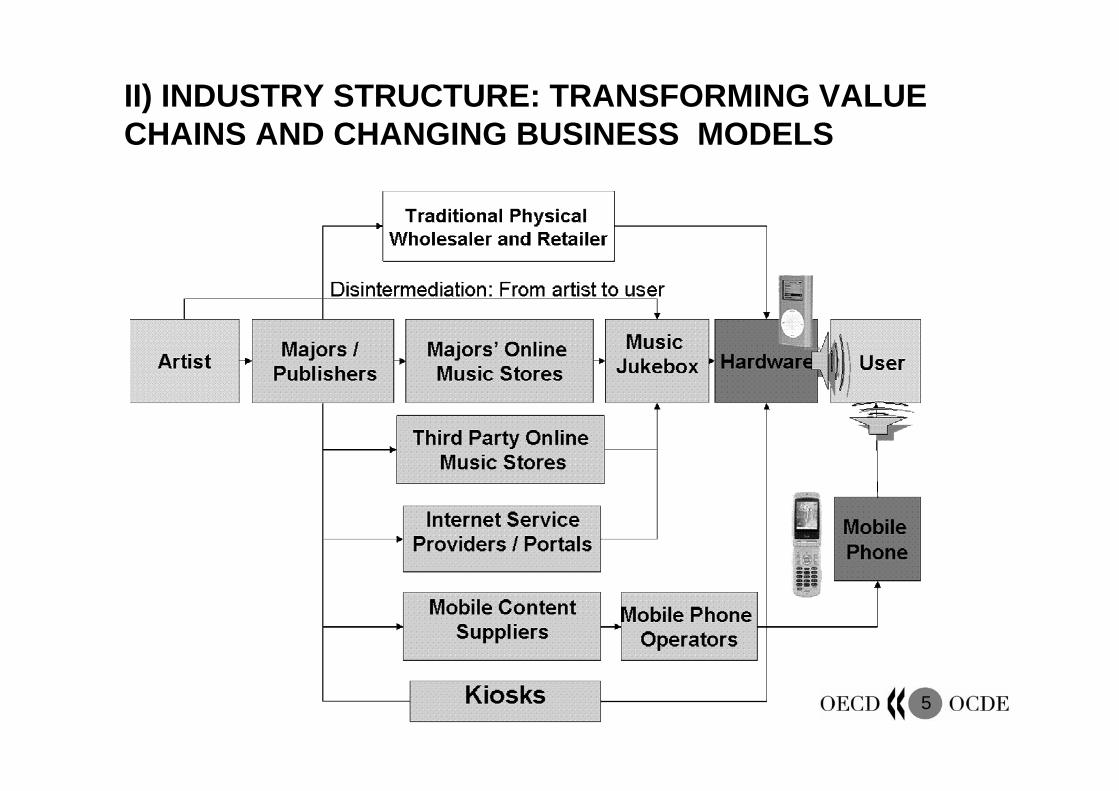

II) INDUSTRY STRUCTURE: TRANSFORMING VALUE CHAINS AND CHANGING BUSINESS MODELS

6

Player Ambition Majors and independent record labels

Trying to receive additional revenue through the digital sales format while avoiding revenue losses due to online piracy, cannibalisation of traditional revenue streams and the “commoditisation” of music.

Artists Trying to receive additional revenue through the digital sales format while avoiding revenue losses due to online piracy. Establish own distribution platforms to gain popularity or to sell music.

Hardware producers Use the interest in content to sell hardware allowing functionality and interoperability. White label services Maximize revenue by catering services to digital music stores solutions. Software producers Aiming to establish player and DRM software as standard for content delivery. ISPs Use the interest in content to attract customers into premium Internet services. Content portals Retain and leverage Internet audience to attract traffic and advertising revenues. Consumer brands Increase customer loyalty through music and use music for promotions. Credit card Earn revenues from fixed- and percentage-based transaction fees.

Different players, Different motives

7

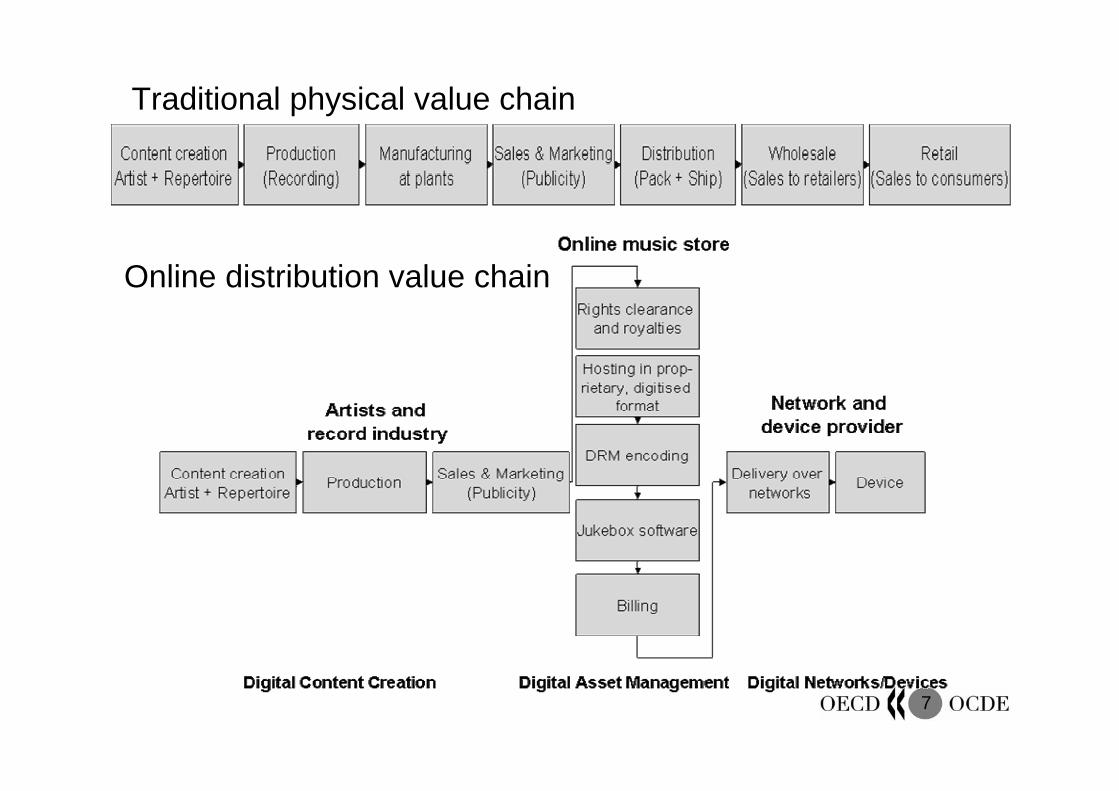

Online distribution value chain

Traditional physical value chain

8

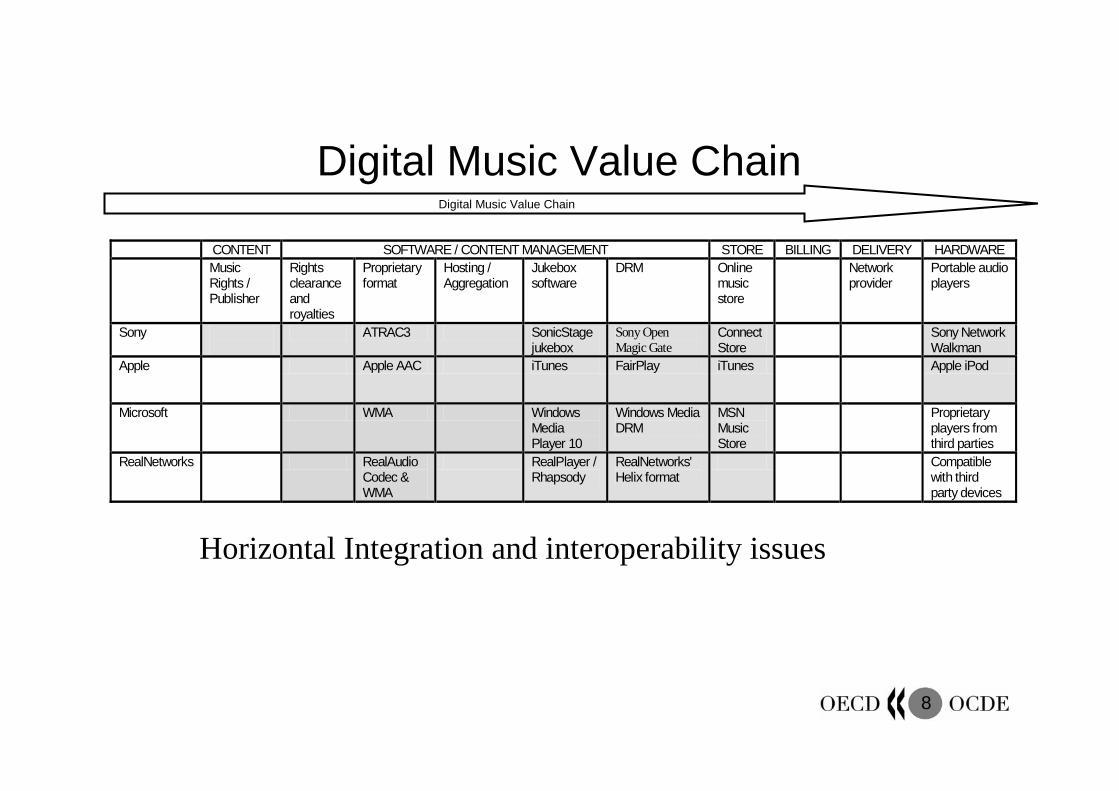

Digital Music Value Chain

CONTENT SOFTWARE / CONTENT MANAGEMENT STORE BILLING DELIVERY HARDWARE Music

Rights / Publisher

Rights clearance and royalties

Proprietary format

Hosting / Aggregation

Jukebox software

DRM Online music store

Network provider

Portable audio players

Sony

ATRAC3 SonicStage jukebox

Sony Open Magic Gate

Connect Store

Sony Network Walkman

Apple

Apple AAC iTunes FairPlay iTunes Apple iPod

Microsoft

WMA Windows Media Player 10

Windows Media DRM

MSN Music Store

Proprietary players from third parties

RealNetworks RealAudio Codec & WMA

RealPlayer / Rhapsody

RealNetworks' Helix format

Compatible with third party devices

Horizontal Integration and interoperability issues

Digital Music Value Chain

9

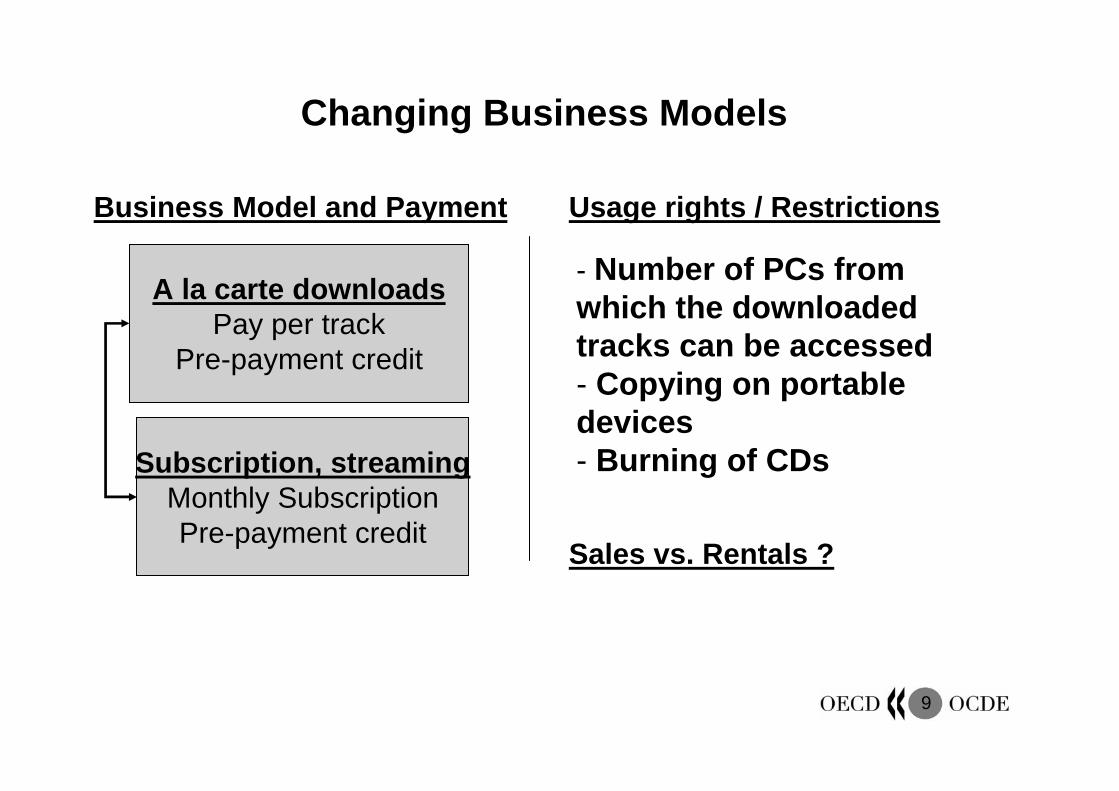

A la carte downloadsPay per track

Pre-payment credit

Subscription, streamingMonthly SubscriptionPre-payment credit

Business Model and Payment Usage rights / Restrictions

- Number of PCs from which the downloaded tracks can be accessed- Copying on portable devices- Burning of CDs

Changing Business Models

Sales vs. Rentals ?

10

Emerging issues for government and other stakeholders

I. Infrastructure, innovation and technology• Broadband access and policies• R&D and new technologies• Human resources• Standards and Technical interoperability• (Micro)-Payment issuesII. Value chain and business model issues• Securing a competitive environment: Access to content and

networks• Difficult rights negotiationsIII. Business and regulatory environment• Protection of Intellectual Property Rights

– National copyright law and the ratification of WIPO Internet treaties– Government action plans towards piracy, counterfeiting and file-sharing– Efforts to compensate content right holders for unauthorized use– Digital Rights Management– Balance between copyright owners and users

• Fostering adequate legal frameworks• Value-added taxes

11

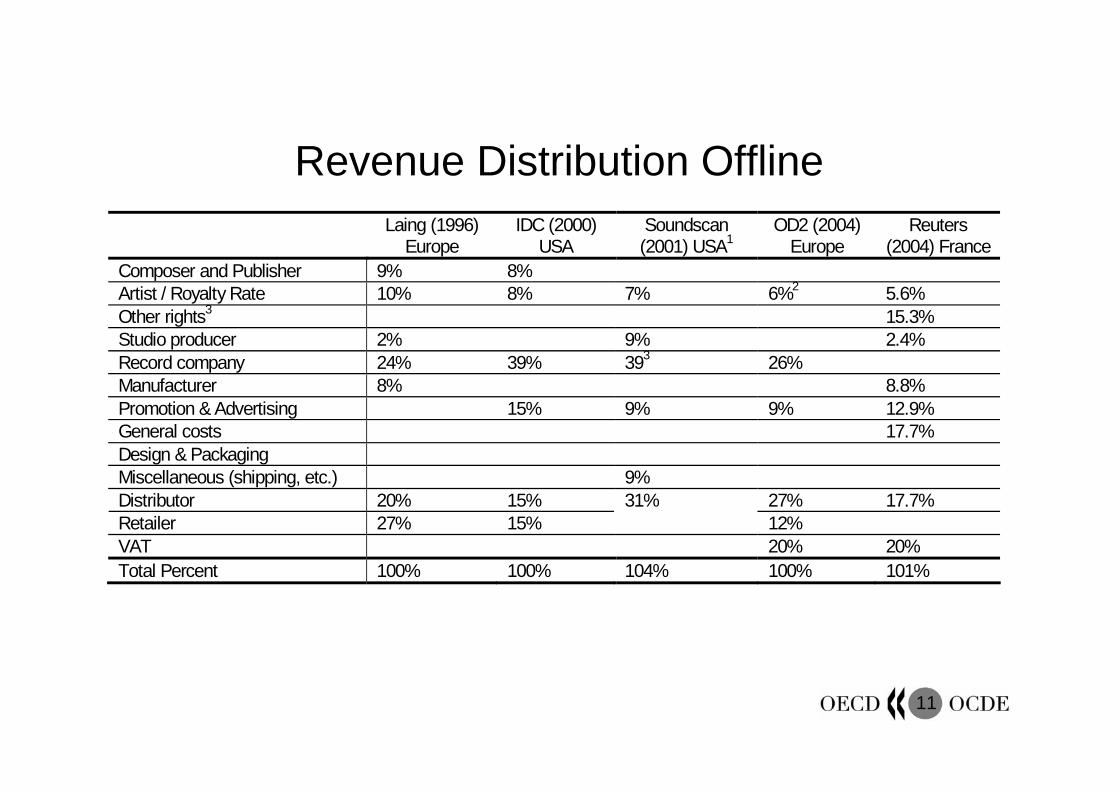

Revenue Distribution Offline Laing (1996)

Europe IDC (2000)

USA Soundscan (2001) USA1

OD2 (2004) Europe

Reuters (2004) France

Composer and Publisher 9% 8% Artist / Royalty Rate 10% 8% 7% 6%2 5.6% Other rights3 15.3% Studio producer 2% 9% 2.4% Record company 24% 39% 393 26% Manufacturer 8% 8.8% Promotion & Advertising 15% 9% 9% 12.9% General costs 17.7% Design & Packaging Miscellaneous (shipping, etc.) 9% Distributor 20% 15% 27% 17.7% Retailer 27% 15%

31% 12%

VAT 20% 20% Total Percent 100% 100% 104% 100% 101%