Page 1

64

X

Financial Market

1. An Overview

In August 2007, the reverberations of the US sub-prime mortgage and credit crisis

have been felt across the global equity markets as market participants turned risk averse and

there has been flight to safety leading to huge volatility. FIIs have been net sellers on the

domestic stock exchanges on most of the trading sessions of the month leading to bearish

sentiments, but due to the net purchase positions of domestic financial institutions, the market

has remained positive. Yet, the market has been expecting a correction, as the rally in the

stock markets in July had been rather rapid defying the emerging weaknesses in the export

and manufacturing sectors. Moreover, though the domestic inflation rate remained subdued,

international crude oil prices continued to surge cautioning the market sentiments. Following

the RBI imposing restriction on the ECB borrowings, the rupee depreciated much to the relief

of exporters. Also, the surprise US FED rate cut has turned the markets buoyant, as a measure

to avert the emerging liquidity crisis in US. The political uncertainty arising out of the

proposed nuclear deal with the USA did have some bearish effects on the market but rather

for a short period. With the quarterly GDP figures exhibiting sustained growth momentum,

the markets again surged ahead.

In the short-term money market, call rates have reverted to rule within the informal

corridor set by reverse repo and repo rates. Despite the hike in CRR rates, the consequent

surge in interest rates has been contained as the Finance Minister urged the banks to hold the

rates steady. In the commodities market, the turnover continued to surge but lower than that

in the pervious year. In the forex market, the rupee rate vis-à-vis the US dollar depreciated in

response to the RBI placing limits on ECB borrowings and deepening US sub-prime

mortgages crisis evoking risk averse behaviour among international investors towards

emerging markets.

Page 2

65

2. Trends in the Equity Market

i) Primary Issues

The volatility in the

stock market appears to have

affected public issue mop-ups

in August. The companies have

mobilised only about Rs 1,877

crore from IPOs and follow-on

public offerings (FPOs) during

August, a drop of almost 82

per cent from the July level,

but above the year’s low seen in May. There have been five IPOs during the month— Take

Solutions, KPR Mill, Motilal Oswal Financial Services, Indowind Energy and Magnum

Ventures were issued through book building process — while the month’s sole FPO by

Dagger Forst Tools raised Rs 16.23 crore from the market.

Real Estate Company, Puravankara Projects, has extended its initial public offering

subscription period from August 3 to August 8 and reduced its price band from Rs 500- 525

to Rs 400-450 a share. The offer opened on July 31. The director of the company said that the

decision was taken in view of the volatility of the global and Indian markets and, with due

respect to investor sentiment, who expressed a deep desire to invest in their company but also

pointed out the market condition. Apparently, poor response has forced the company to

extend the IPO. Total bids received were 76,26,010 and those at cut-off price were 30,33,200.

However, this is not the first time that IPOs had to cut price and extend the offer period.

When the market was witnessing adverse conditions in May-June 2006, issues such as Air

Deccan, Abhishek Mills, Bluplast and Vigneshwara Exports were also forced to resort to

similar measures.

On August 31, lack of interest from retail investors had forced IT People (India), a

provider of manpower to IT and BPO industry, to withdraw its ongoing FPO, resulted in its

stocks plunging by 9.88 per cent to Rs 31 on the BSE. The company said that while the FPO

had received favourable response from Qualified Institutional Buyers (QIBs) and High

Networth Individuals (HNIs), the absence of adequate interest from retail investors (in spite

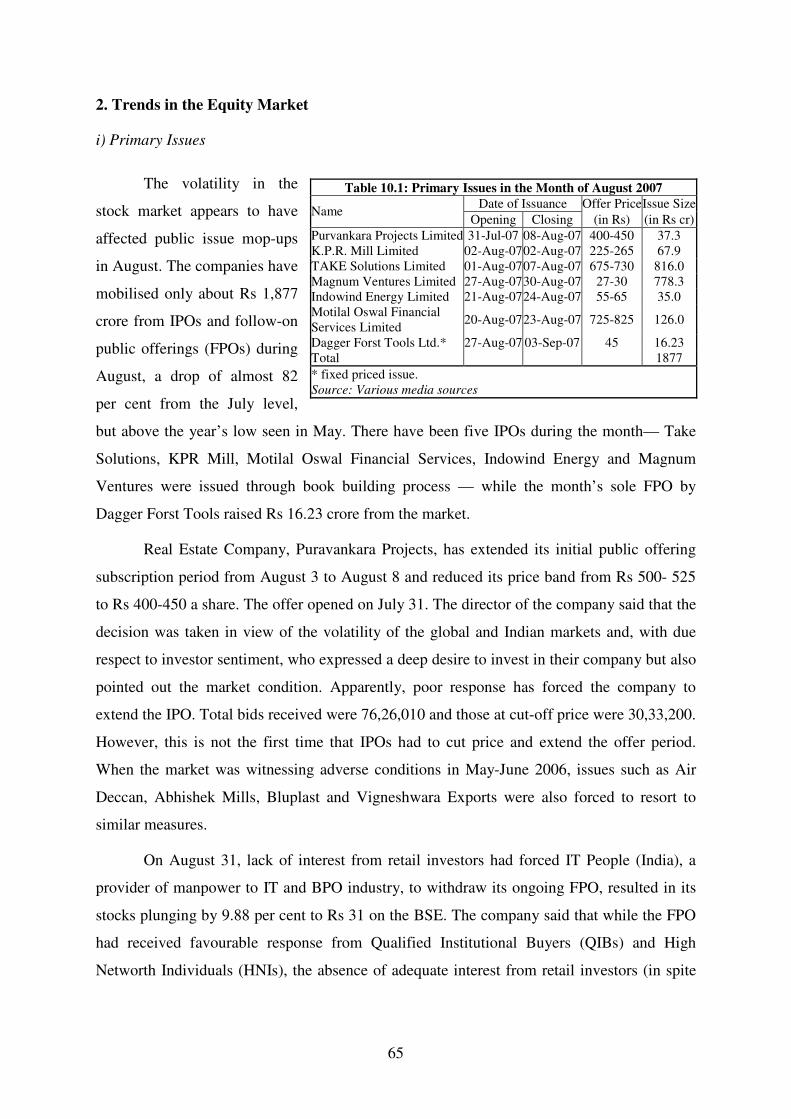

Table 10.1: Primary Issues in the Month of August 2007

Date of Issuance Offer Price Issue Size Name

Opening Closing (in Rs) (in Rs cr)

Purvankara Projects Limited 31-Jul-07 08-Aug-07 400-450 37.3 K.P.R. Mill Limited 02-Aug-07 02-Aug-07 225-265 67.9 TAKE Solutions Limited 01-Aug-07 07-Aug-07 675-730 816.0 Magnum Ventures Limited 27-Aug-07 30-Aug-07 27-30 778.3 Indowind Energy Limited 21-Aug-07 24-Aug-07 55-65 35.0 Motilal Oswal Financial Services Limited

20-Aug-07 23-Aug-07 725-825 126.0

Dagger Forst Tools Ltd.* 27-Aug-07 03-Sep-07 45 16.23 Total 1877

* fixed priced issue. Source: Various media sources

Page 3

66

of the issue being completely underwritten by the Book Running Lead Managers) led the

company to withdraw its issue.

There has been a rise of 140 per cent in the

resource mobilisation during April-July 2007 over the

corresponding period in the previous financial year.

During April-July 2007, the largest resource mobilisation

has been by cement and construction sector (Rs 13,466

crore) and banks/financial institutions (Rs 10,879 crore).

New share listings in August have borne the brunt

of the market turmoil with five of the 14 companies debuting at a discount to the issue price.

Market experts say that perception about the pricing and the subscription garnered are two

important factors that influence the performance of an issue on listing day and thereafter.

Most issues including IVR Prime Urban, Alpa Laboratories, KPR Mills and Puravankara

Projects that listed at a discount are trading in red territory. Only SEL Manufacturing

Company has managed to lift itself up after a weak opening.

The Securities and Exchange Board of India (Sebi) has put equity float by large-cap

companies on the fast track. A new scheme called the ‘fast track share issuance programme’

says companies with a three-year listing track record on the National Stock Exchange and the

Bombay Stock Exchange, and with free-float market capitalisation of at least Rs 10,000

crore, can raise funds through rights and follow-on issues, without having to wait for the

regulator’s clearance. There are only 35 companies listed on the BSE and NSE having a free

float market cap of Rs 10,000 crore or above. The list includes Reliance Industries, ICICI

Bank, Infosys Technologies, Larsen & Toubro, Bharti Airtel, HDFC, ITC, Reliance Capital,

among others.

ii) Secondary Market

The secondary market has witnessed huge volatility as a number of factors such as the

international factors: weaknesses in US sub-prime mortgages spreading across different parts

of the world, FIIs turning aggressive net sellers as they turned risk averse and surging

international crude oil prices and domestic factors: emerging threat to political stability over

the nuclear deal issue. Besides, the market remained concerned about the possible margin

calls in the wake of volatile movements in prices. However, the subdued inflation, good

Table 10.2: Resources Raised through Public and Rights Issues

April-July

2007 April-July

2006

No Amount

(Rs crore)No

Amount (Rs crore)

Public Issues 35 27225 15 11261 IPOs 33 16636 11 10553 FPOs 2 10589 4 708 Rights Issues 3 342 12 219 Total 38 27567 27 11480

Source: Sebi Bulletin, August 2007

Page 4

67

prospects of corporate earnings, depreciation of the rupee domestic financial institutions

remaining net buyers and good first quarter GDP results contributed to the positive

sentiments.

After the government curtailed overseas borrowings by companies, Finance Minister

Shri P Chidambaram, said there were no plans to regulate participatory notes. One of the

purposes is to moderate the inflow of capital and the claim that the curbs will hurt

investments is exaggerated, he said. The notes, which are typically derivatives that change in

value depending on the performance of the underlying securities, allow hedge funds to invest

in the country without having to register with the stock market regulator.

The total turnover on BSE declined sharply to Rs 1,06,042 crore from Rs 1,25,041

crore in July for all securities, yet the total market capitalisation increased to Rs 45,38,006

crore from Rs 45,29,772 crore due to increase in market capitalisation of S group, T group

and Z group shares. Similarly, the total equity turnover on NSE has dipped to Rs 2,31,241

crore from Rs 2,67,227 crore in July.

As per Sebi bulletin, in July 2007, the daily average volatility was the highest for the

BSE metal index (1.94 per cent), followed by capital goods index (1.92 per cent), CNX IT

index (1.36 per cent) and BSE Oil and Gas (1.31 per cent). The highest volatility in current

financial year so far until July was recorded for Bank Nifty index (1.66 per cent), BSE Metal

index (1.64 per cent), BSE Bankex index (1.52 per cent) and BSE capital goods index (1.49

per cent). Among the international indices, highest daily volatility has been was recorded for

South Korea Kospi (1.55 per cent), Thailand SET index and germany Dax index. On an

annualised basis, volatility has been the hightest for S&P CNX nifty (11.9 per cent) & BSE

sensex (10.3 per cent)

The Securities and Exchange Board of India chairman, M Damodaran, has stated that

subprime crisis was not the only reason for the market volatility and also ruled out any

separate regulation for hedge funds. Damodaran has stated that there exists no single category

as hedge funds and Sebi would prefer them to enter the Indian markets directly rather than

through some offshore derivatives. Further, he stated that registration of hedge funds with the

Sebi, as in the case of foreign institutional investors, was enough. He pointed out that the

Sebi was not worried about the large number of players coming into India because their entry

presupposes the constant returns being offered by the Indian markets besides a sound market

regulatory mechanism. He also mentioned the Sebi would soon issue guidelines for setting up

Page 5

68

a self-regulatory organisation (SRO) for investment advisers comprising representatives of all

sections including brokers and print and electronic media.

Despite rising interest rates and appreciating rupee, capital investments by Indian

companies in the current fiscal could exceed last year’s level, according to a study by the

Reserve Bank of India. Indian corporates expect to spend Rs 1,48,207 crore in capital

expenditure in the current fiscal in projects already appraised and sanctioned by banks and

financial institutions. This is against the total investments of Rs 2,06,460 crore in 2006-07.

Transmission of Securities

A SEBI-appointed group studying the issues relating to difficulties faced by investors,

while dealing with transmissions of securities in physical and dematerialised mode, has

recommended a threshold limit up to which the listed companies would require only an

Affidavit, Deed of Indemnity and No Objection Certificate from other legal heirs. Standard

format of these documents have also been recommended. The threshold limit should be fixed

at holding of 200 shares or Rs 1 lakh in value, whichever is higher. Also, the prescribed

threshold limit shall be the basic minimum limit to be adhered to by all the listed companies.

The companies having higher threshold shall continue to do so, and also can set liberal

threshold.

CBDT Clarifications

The Central Board of Direct Taxes (CBDT) has clarified that lending and borrowing

of shares for short selling in equities will not attract capital gains tax. With this clarification

one of the important hurdles in the way of permitting short selling on the stock exchanges has

been cleared. According to the sources, the short selling of securities will also not attract

securities transaction tax (STT) as is prevalent in case of physical sale and purchase of equity

shares. This is because securities offered under lending and borrowing does not amount to

transfer of shares and hence it is exempt from capital gains tax. Short selling is backed by a

scheme of lending and borrowing of shares which will help in settlement of transactions

through physical delivery. This is otherwise known as covered short sale.

Observations from RBI Annual Report

The RBI Annual Report, stated that further deterioration in sub-prime delinquencies

could lead to reassessment of risk by investors across products and markets and retrenchment

of capital from the emerging market economies (EMEs), given the contagion and herd

mentality. As a growing number of hedge funds invest in the country, the capital inflow can

Page 6

69

be volatile, given the nature of the funds. Private equity funds, another major source of

capital for EMEs, are sensitive to interest changes. Therefore, any monetary tightening in the

major economies could lead to a slowdown of investment from private equity funds, the RBI

pointed out. Further, the report stated that while its monetary policy stance would continue to

be that of maintaining price stability and anchoring inflation expectations, in this context,

financial stability would assume greater importance in the months to come.

Trading at HSE

Trading at Hyderabad Stock Exchange (HSE) came to a halt for the second

consecutive day on August 30 as it is now de-recognised as per the Securities Contracts

Regulations 2006 notified by Sebi. The 64-year-old HSE was required to complete the

demutualisation scheme on or before August 28 and it failed to do so because of lack of

response from investors to its offloading of 51 per cent of outstanding share capital.

According to HSE officials the exchange had not received any formal communication from

Sebi on its status. But as per the Act, HSE was automatically deregistered from August 29

and Sebi is not required to communicate the same immediately.

IIISS 2007 Findings

Invest India Income and Savings Survey 2007 produced by IIMS Dataworks suggests

that just around 15 per cent of the country’s equity investors are speculators, entering and

exiting the market several times during a year. Almost 75 per cent of them have been there

since 2003, that is, they have ridden out many ups and downs in the past. And around a sixth

of the investment made by individuals directly in the country’s stock markets is made by

individuals who earn under Rs 20,000 a month- a twentieth is invested by those earning less

than Rs 8,000 a month.

Apart from giving valuable insights into the investment habits of investors, the

findings are especially relevant in the context of the plethora of stories that talk of the small

investor losing thousands of crore each time the market crashes. According to the survey,

there are at present a little over 7.2 million individuals in India with equity market positions.

Over half of them have only mutual fund investments’ in either balanced or mainly equity

funds. Nearly two million have equity positions only, and the rest have investments in mutual

funds as well as directly in the market. At the time of the survey, around four months ago, the

aggregate financial savings and investment portfolio of these 7.2 million investors stood at

roughly Rs 400,000 crore while their aggregate equity portfolio value stood at Rs120,000

Page 7

70

crore (29.7 per cent of their total portfolios). In other words, around 2 per cent to 3 per cent of

the total market capitalisation is held by small investors, while promoters hold around 50 per

cent to 60 per cent of outstanding shares, FIIs hold another 15 per cent to 20 per cent,

banks/mutual funds/insurance firms hold the rest. . IIMS Dataworks’ survey asked questions

about why investors entered the market and those classified as speculators answered in the

affirmative to questions such as ‘I don’t want to miss out on a boom, ‘I like to speculate’, and

so on. Collectively, the equity portfolio of the speculator group is around Rs 26,000 crore,

according to the survey.

NSDL to act as CRA

The Sebi has put several eligibility conditions for National Securities Depository Ltd

(NSDL) to act as the Central Recordkeeping Agency (CRA) for pension funds, under the new

pension scheme for central and state government employees. According to the decision,

NSDL could act as the CRA only through a separate strategic business unit (SBU). Further,

the depository will have to hive off other activities within three years to a separate entity

without any financial and legal links with NSDL. Another eligibility condition is that

NSDL’s other activity should not erode the net worth required for carrying out the NSDL’s

activity in securities. NSDL is required to get the approvals from its board and sponsor for

carrying on other activities. Sebi stipulations also require NSDL to get additional insurance

cover for risks, if any, of other activities. The depository will also have to meet other

financial conditions, if required, in the interest of beneficial owners, said sources. Earlier,

Sebi had expressed its reservations on NSDL acting as a recordkeeper for pension funds. The

regulator had stated that the new responsibility will be outside the assigned role as a

depository, and that the Depository Act prohibited such activities.

Mandatory Quarterly Investment Reports

The Securities and Exchange Board of India (Sebi) will soon make it mandatory for

international and domestic private equity (PE) and venture capital (VC) funds to submit

quarterly investment reports to the regulator. Currently, foreign and domestic venture capital

funds registered with Sebi have been voluntarily submitting quarterly investment reports to

the regulator. Market sources said foreign and domestic venture capital funds, generally, are

secretive about their investments, making it difficult for the regulator to keep a tab on their

investments in India. At present, there are about 80 foreign venture capital investors and 90

domestic venture capital funds registered with the Sebi. The reason cited for the new rules is

Page 8

71

that as a regulatory body there was a need for the maintaining reliable data on PE/VC

investments. Globally, private equities are neither regulated nor are their investments kept

track of by the regulators.

The Sebi set a cap of 10 per cent on overseas investments by venture capital funds in

India. This is part of the guidelines for venture capital funds, would be allowed only into

those foreign unlisted companies that have an Indian connection, such as companies which

have back office operations in India. Sebi said in a circular that the allocation of investment

limits would be done on a first come, first served basis, depending on the availability of the

overall limit of $500 million (Rs 2,000 crore). The VCFs can invest in equity and equity-

linked undertakings, within an overall limit of $500 million, for which they have to take Sebi

approval.

Margin Accounts of Brokers

The Securities Exchange Board of India (Sebi) has expressed reservations over the

transparency in transactions in the margin accounts of brokers. In its investigation, the Sebi

has observed that the securities maintained in these accounts are misused by brokers for

leveraging and pushing up trading volumes in particular shares. The securities under the

margin account are not earmarked client-wise and belong to brokers at any given point of

time. To curb market manipulation, the market regulator has directed the depositories to flag

off such margin accounts by asking brokers to identify accounts as their own (proprietary)

and that of the clients. Further, brokers will have to work out the volume of transactions and

furnish the data to the Sebi periodically.

Sectoral Indices

India Index Services & Products (IISL), a joint venture between NSE and CRISIL, ,

launched on August 7, 2007 a new sectoral index based on the infrastructure sector. The 25-

stock CNX Infrastructure Index includes companies belonging to the telecom, power, port,

air, roads, railways, shipping and other utility services providers. CNX Infrastructure Index

constituents represent about 21.01 per cent of the total market capitalisation as on 31 July

2007. The index is a market-capitalisation-weighted index with base date of 1 January 2004,

indexed to a base value of 1000.

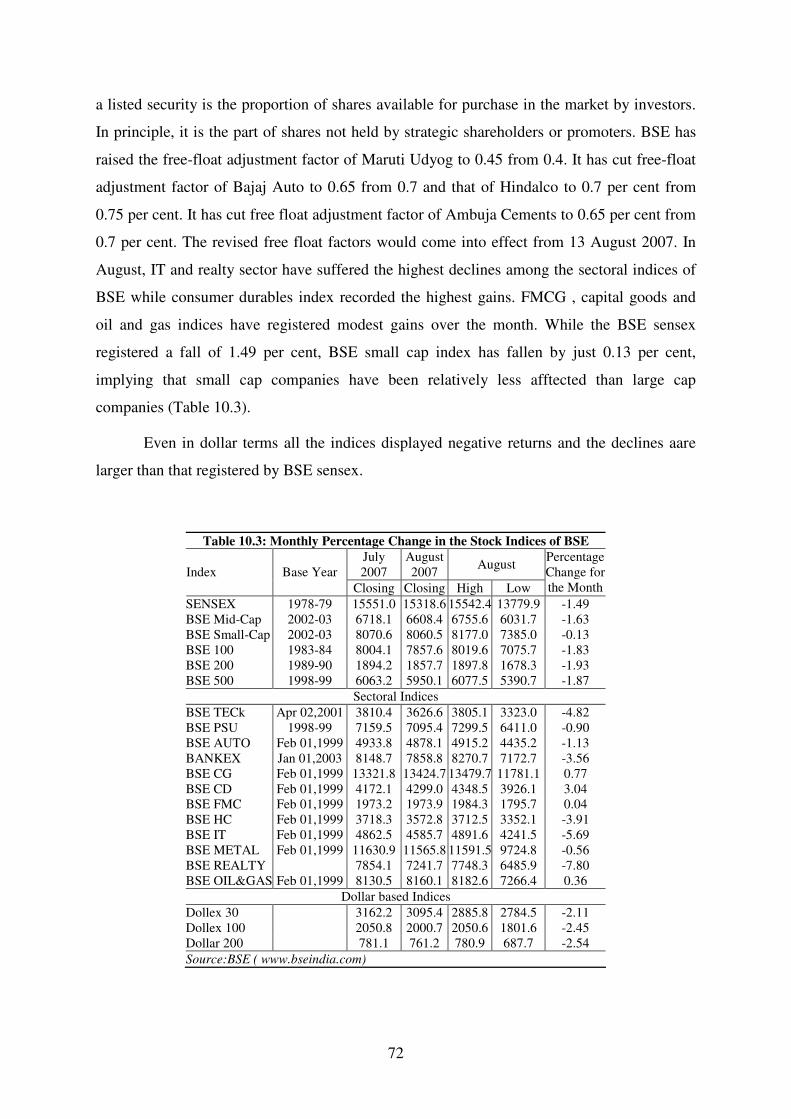

BSE has revised free-float adjustment factor of four constituents of BSE Sensex. Free

float adjustment factor is used for calculating a scrip’s weightage in Sensex. The free float of

Page 9

72

a listed security is the proportion of shares available for purchase in the market by investors.

In principle, it is the part of shares not held by strategic shareholders or promoters. BSE has

raised the free-float adjustment factor of Maruti Udyog to 0.45 from 0.4. It has cut free-float

adjustment factor of Bajaj Auto to 0.65 from 0.7 and that of Hindalco to 0.7 per cent from

0.75 per cent. It has cut free float adjustment factor of Ambuja Cements to 0.65 per cent from

0.7 per cent. The revised free float factors would come into effect from 13 August 2007. In

August, IT and realty sector have suffered the highest declines among the sectoral indices of

BSE while consumer durables index recorded the highest gains. FMCG , capital goods and

oil and gas indices have registered modest gains over the month. While the BSE sensex

registered a fall of 1.49 per cent, BSE small cap index has fallen by just 0.13 per cent,

implying that small cap companies have been relatively less afftected than large cap

companies (Table 10.3).

Even in dollar terms all the indices displayed negative returns and the declines aare

larger than that registered by BSE sensex.

Table 10.3: Monthly Percentage Change in the Stock Indices of BSE

July 2007

August 2007

August Index Base Year

Closing Closing High Low

Percentage Change for the Month

SENSEX 1978-79 15551.0 15318.6 15542.4 13779.9 -1.49 BSE Mid-Cap 2002-03 6718.1 6608.4 6755.6 6031.7 -1.63 BSE Small-Cap 2002-03 8070.6 8060.5 8177.0 7385.0 -0.13 BSE 100 1983-84 8004.1 7857.6 8019.6 7075.7 -1.83 BSE 200 1989-90 1894.2 1857.7 1897.8 1678.3 -1.93 BSE 500 1998-99 6063.2 5950.1 6077.5 5390.7 -1.87

Sectoral Indices

BSE TECk Apr 02,2001 3810.4 3626.6 3805.1 3323.0 -4.82 BSE PSU 1998-99 7159.5 7095.4 7299.5 6411.0 -0.90 BSE AUTO Feb 01,1999 4933.8 4878.1 4915.2 4435.2 -1.13 BANKEX Jan 01,2003 8148.7 7858.8 8270.7 7172.7 -3.56 BSE CG Feb 01,1999 13321.8 13424.7 13479.7 11781.1 0.77 BSE CD Feb 01,1999 4172.1 4299.0 4348.5 3926.1 3.04 BSE FMC Feb 01,1999 1973.2 1973.9 1984.3 1795.7 0.04 BSE HC Feb 01,1999 3718.3 3572.8 3712.5 3352.1 -3.91 BSE IT Feb 01,1999 4862.5 4585.7 4891.6 4241.5 -5.69 BSE METAL Feb 01,1999 11630.9 11565.8 11591.5 9724.8 -0.56 BSE REALTY 7854.1 7241.7 7748.3 6485.9 -7.80 BSE OIL&GAS Feb 01,1999 8130.5 8160.1 8182.6 7266.4 0.36

Dollar based Indices

Dollex 30 3162.2 3095.4 2885.8 2784.5 -2.11 Dollex 100 2050.8 2000.7 2050.6 1801.6 -2.45 Dollar 200 781.1 761.2 780.9 687.7 -2.54

Source:BSE ( www.bseindia.com)

Page 10

73

Similarly, the S & P CNX Nifty has also fallen of 1.4 per cent as against a gain of 6.1

per cent in July. Among the sectoral indices, CNX IT registered the highest fall of 5.4 per

cent and Bank nifty declined by 3.7 per cent (Table10.3)

Table 10.4: Monthly Percentage Change in the Stock Indices of NSE

July 2007

August 2007

August Index Base Year

Closing Closing High Low

Percentage change for the month

S&P CNX Nifty 1995 4528.9 4464.0 4532.9 4002.2 -1.43 CNX Midcap 2003 6177.7 6043.8 6183.3 5576.6 -2.17 CNX Nifty Junior 1996 8849.6 8632.8 8966.3 7700.2 -2.45 S&P CNX Defty 1995 3885.2 3776.2 3900.8 3331.7 -2.81 S&P CNX 500 1994 3783.9 3711.6 3793.9 3362.8 -1.91 CNX 100 4436.2 4366.1 4444.4 3920.6 -1.58 CNX IT 1996* 5086.7 4813.2 5093.4 4439.2 -5.38 BANK Nifty 2000 6928.5 6675.9 7110.6 6058.4 -3.65

Note:*the base value has been changed from 1000 to 100 with effect from May 24, 2004 Source: NSE ( www.nseindia.com)

Foreign Institutional Investors (FIIs) and Mutual Funds

In response to the reverberations in US sub-prime and credit markets, FIIs have been

net sellers to the extent of Rs 7,771 crore as against a net purchase position of Rs 22,609

crore the highest ever inflow in July. Also, the cumulative net FII investments slipped to US

$ 57,373 million from a peak of Rs 60,798 million in July (Chart 10A).

In August, barring a few

days, mutual funds have been net

buyers of equities supporting market

sentiments affected by the massive

FII outflows (Chart 10 B). Their net

purchases have been worth Rs 4,094

crore with Rs 16,676 crore and sales

of Rs 12,582 crore.

The Asset under management

(AUM) has declined in August to Rs

467,623 crore from Rs 486,646 crore

in July; though the inflows from

Chart10.A : Daily Investment of FIIs and Mutual

Funds (August 2007)

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

1-A

ug

8-A

ug

15

-Au

g

22

-Au

g

29

-Au

g

Net

FII

In

ves

tmen

t (R

s cr

ore

)

-400

-200

0

200

400

600

800

1000

Net

Mu

tual

Fu

nd

s In

ves

tmen

t (R

s

cro

re)

Net FII investment Net Mutual Funds Investment

Page 11

74

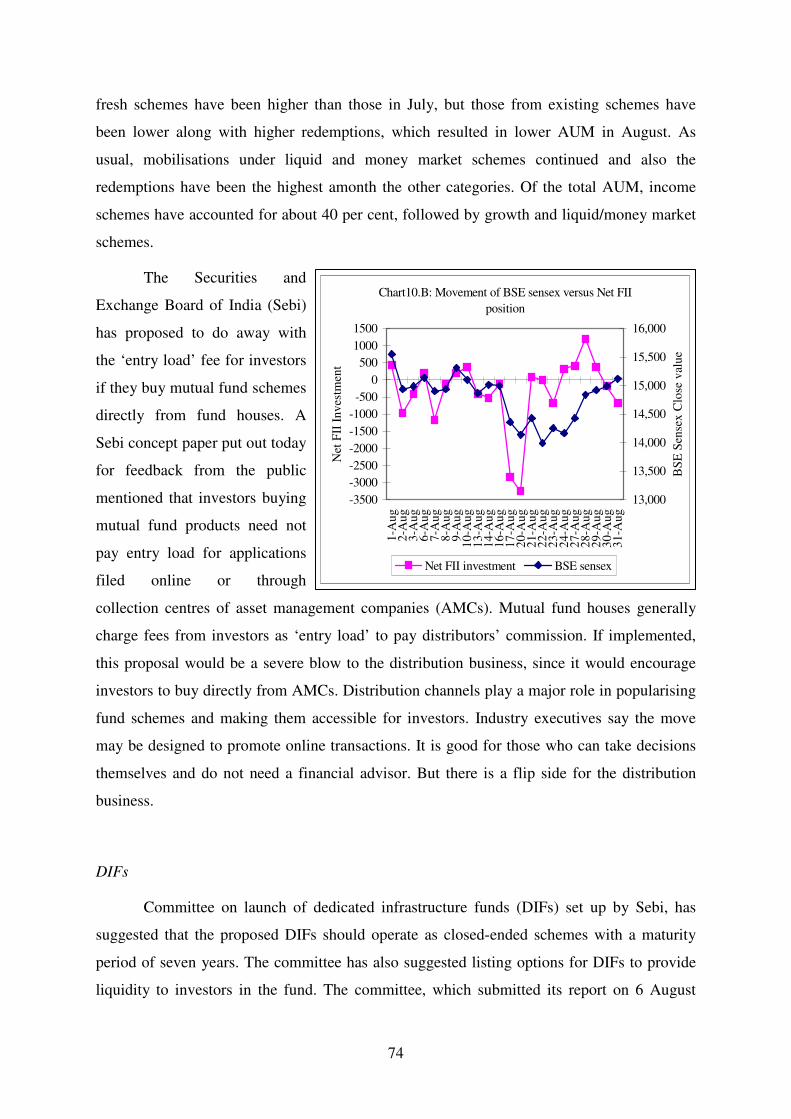

fresh schemes have been higher than those in July, but those from existing schemes have

been lower along with higher redemptions, which resulted in lower AUM in August. As

usual, mobilisations under liquid and money market schemes continued and also the

redemptions have been the highest amonth the other categories. Of the total AUM, income

schemes have accounted for about 40 per cent, followed by growth and liquid/money market

schemes.

The Securities and

Exchange Board of India (Sebi)

has proposed to do away with

the ‘entry load’ fee for investors

if they buy mutual fund schemes

directly from fund houses. A

Sebi concept paper put out today

for feedback from the public

mentioned that investors buying

mutual fund products need not

pay entry load for applications

filed online or through

collection centres of asset management companies (AMCs). Mutual fund houses generally

charge fees from investors as ‘entry load’ to pay distributors’ commission. If implemented,

this proposal would be a severe blow to the distribution business, since it would encourage

investors to buy directly from AMCs. Distribution channels play a major role in popularising

fund schemes and making them accessible for investors. Industry executives say the move

may be designed to promote online transactions. It is good for those who can take decisions

themselves and do not need a financial advisor. But there is a flip side for the distribution

business.

DIFs

Committee on launch of dedicated infrastructure funds (DIFs) set up by Sebi, has

suggested that the proposed DIFs should operate as closed-ended schemes with a maturity

period of seven years. The committee has also suggested listing options for DIFs to provide

liquidity to investors in the fund. The committee, which submitted its report on 6 August

Chart10.B: Movement of BSE sensex versus Net FII

position

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

1-A

ug

2-A

ug

3-A

ug

6-A

ug

7-A

ug

8-A

ug

9-A

ug

10

-Au

g1

3-A

ug

14

-Au

g1

6-A

ug

17

-Au

g2

0-A

ug

21

-Au

g2

2-A

ug

23

-Au

g2

4-A

ug

27

-Au

g2

8-A

ug

29

-Au

g3

0-A

ug

31

-Au

g

Net

FII

In

ves

tmen

t

13,000

13,500

14,000

14,500

15,000

15,500

16,000

BS

E S

ense

x C

lose

val

ue

Net FII investment BSE sensex

Page 12

75

2007, also suggested that retail investors investing in DIFs be given tax incentives. The

committee has, however, added that such tax benefits should be available only to the original

investors.

iii) Derivatives

Given the volatility in the cash market, the derivatives market witnessed surge in its

aggregate turnover to Rs 10,56,731 crore from Rs 10,15,077 crore in July. Also, the end of

day daily averages of has been at Rs 82,726 crore, yet the percentage of open interest to daily

average traded value has been lower at 172 per cent as against 176 per cent in July (Table

10.5).

The productwise turnover shows

that the share of stock futures has

declined from 64 per cent in July to 49

per cent in August and that of index

futures has increased from 24 per cent to

34 per cent. The turnover of index options

has increased from 9 per cent to 13 per

cent while that of stock options has

remained steady (Chart 10.D).

As per the data published by NSE, the share of retail investors has been declining in

the recent past while that of institutional investors has increased. The retail investors

accounted for 65 per cent of the total turnover in March 2007 has fallen to 60 per cent, while

that of institutional investors has risen from 11 per cent to 14 per cent over the same period.

Chart D: Productwise contribution to total

derivatives turnover

0

100000

200000

300000

400000

500000

600000

700000

Index

Futures

Stock

Futures

Index

Options

Stock

Options

Turn

over

(R

s cr

ore

)

July-07 August-07

Page 13

76

Table 10.5: Business Growth of F & O Segment of NSE.

Index Futures Stock Futures Index Options Stock Options Grand Total Month/

Year No. of contracts

Turnover (Rs. cr.)

No. of contracts

Turnover (Rs. cr.)

Total Futures Trading

No. of contracts

Turnover (Rs. cr.)

No. of contracts

Turnover (Rs. cr.)

Total Options Trading

No. of contracts

Turnover (Rs. cr.)

Average Daily

Turnover (Rs. cr.)

2002-03

2126763 43951 10676843 286532 330483 442241 9247 3523062 100134 109381 16768909 439864 1752

(10.0) (65.1) (75.1) (2.1) (22.8) (24.9)

2003-04

17191668 554462 32368842 1305949 1860411 1732414 52823 5583071 217212 270035 56886776 2130446 8388

(26.0) (61.3) (87.3) (2.5) (10.2) (12.7)

2004-05

21635449 772174 47043066 1484067 2256241 3293558 121954 5045112 168858 290812 77016465 2547053 10107

(30.3) (58.3) (88.6) (4.8) (6.6) (11.4)

2005-06

58537886 1513791 80905493 2791721 4305512 12935117 338469 5240776 180270 518739 157619271 4824251 19220

(31.4) (57.9) (89.2) (7.0) (3.7) (10.8)

2006-07

81487424 2539574 104955401 3830967 6370541 25157438 791906 5283310 193795 985701 216883573 7356242 29543

(34.5) (52.1) (86.6) (10.8) (2.6) (13.4)

April 07

10,383282 205,458 10647866 296,629 502087 4874462 97,150 635357 17,050 114200 26540967 616287 30814

(33.3) (48.1) (81.5) (15.8) (2.8) (18.5)

May 07

10383282 214,523 13350667 400,096 614,619 4055682 85,465 758306 23,358 108,823 28383804 723443 34450

(29.7) (55.3) (85.0) (11.8) (3.2) (15.0)

Jun 07 11407865 240797 14287983 451314.3 692,111 4340991 92503 694589 21928 114,431 30731428 806542 38407

(29.9) (56.0) (85.8) (11.5) (2.7) (14.2)

Jul 07 10605483 238577 18888008 647356 885933 4221585 94561 1022158 34582 129143 34737234 1015077 46140

(24) (64) (88) (12)

Note: Figures in bracket are per cent to total.

Source: www.nseindia.com

3. Corporate Debt Market

A major development, which may propel the corporates to mobilise more funds

through bonds in the domestic market, concerns the imposition of restrictions by RBI on

external commercial borrowings (ECBs). ECBs up to USD 20 million per borrowing

company per financial year have been permitted for foreign currency expenditures for

permissible end-uses under the Automatic Route; also these funds are to be parked overseas

and not to be remitted to India. Borrowers proposing to avail of ECB up to USD 20 million

for Rupee expenditure for permissible end-uses would require prior approval of the Reserve

Bank under the Approval Route. However, such funds have to be parked overseas until actual

requirement arise in India. Also, foreign currency convertible bonds (FCCBs) have been

losing investor interest due to rising interest rate costs, declining premia, lower conversion

into equity and volatility in stock and currency markets.

Page 14

77

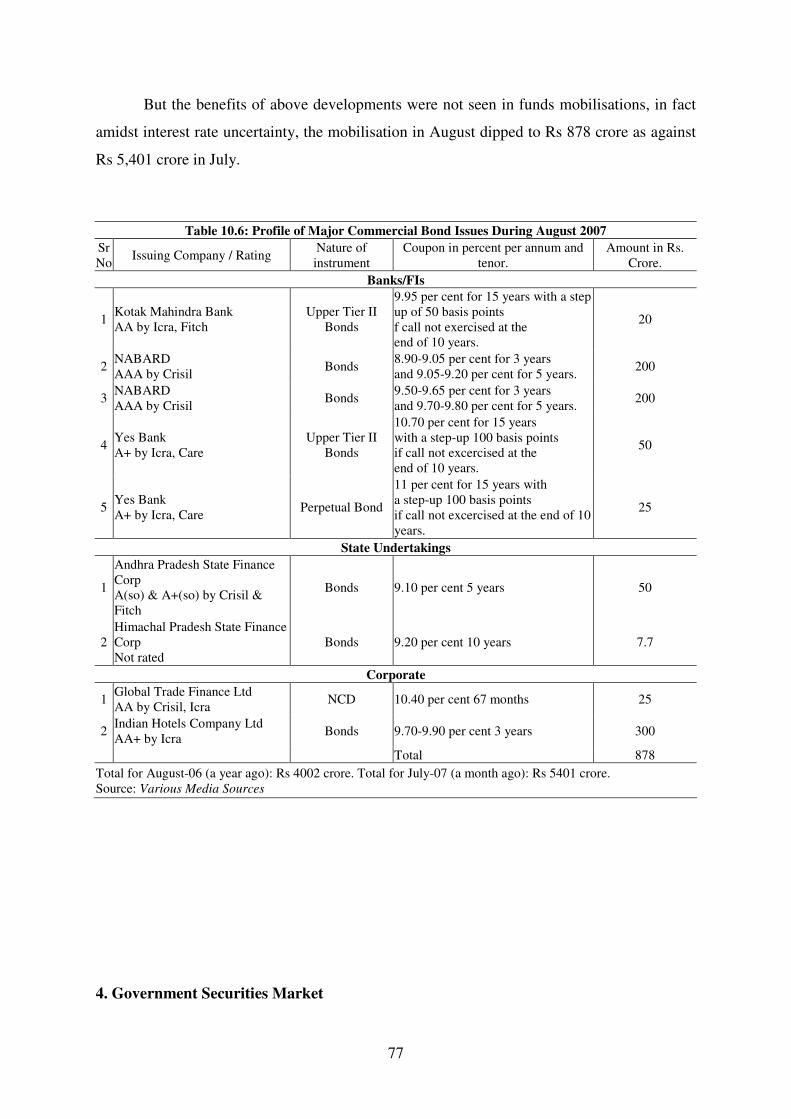

But the benefits of above developments were not seen in funds mobilisations, in fact

amidst interest rate uncertainty, the mobilisation in August dipped to Rs 878 crore as against

Rs 5,401 crore in July.

Table 10.6: Profile of Major Commercial Bond Issues During August 2007

Sr No

Issuing Company / Rating Nature of instrument

Coupon in percent per annum and tenor.

Amount in Rs. Crore.

Banks/FIs

1 Kotak Mahindra Bank AA by Icra, Fitch

Upper Tier II Bonds

9.95 per cent for 15 years with a step up of 50 basis points f call not exercised at the end of 10 years.

20

2 NABARD AAA by Crisil

Bonds 8.90-9.05 per cent for 3 years and 9.05-9.20 per cent for 5 years.

200

3 NABARD AAA by Crisil

Bonds 9.50-9.65 per cent for 3 years and 9.70-9.80 per cent for 5 years.

200

4 Yes Bank A+ by Icra, Care

Upper Tier II Bonds

10.70 per cent for 15 years with a step-up 100 basis points if call not excercised at the end of 10 years.

50

5 Yes Bank A+ by Icra, Care

Perpetual Bond

11 per cent for 15 years with a step-up 100 basis points if call not excercised at the end of 10 years.

25

State Undertakings

1

Andhra Pradesh State Finance Corp A(so) & A+(so) by Crisil & Fitch

Bonds 9.10 per cent 5 years 50

2 Himachal Pradesh State Finance Corp Not rated

Bonds 9.20 per cent 10 years 7.7

Corporate

1 Global Trade Finance Ltd AA by Crisil, Icra

NCD 10.40 per cent 67 months 25

2 Indian Hotels Company Ltd AA+ by Icra

Bonds 9.70-9.90 per cent 3 years 300

Total 878

Total for August-06 (a year ago): Rs 4002 crore. Total for July-07 (a month ago): Rs 5401 crore. Source: Various Media Sources

4. Government Securities Market

Page 15

78

i) Primary Market

Dated Securities

The government in August has mobilised Rs 17,000 crore through two instalments by

issuing two securities each. In the first instance on August 3, the government has re-issued

7.99 per cent 2017 and 7.95 per cent 2032 securities for notified amounts of Rs 6,000 crore

and Rs 4,000 crore, respectively. The cut-off yield for the 10-year paper has been set lower at

7.93 per cent against 7.99 per cent set in July, while the yield on 25-year security has been set

higher at 8.45 per cent against 8.34 per cent (Table 6).

On August 24, the government has re-issued 7.27 per cent 2013 and the 10-year

security auctioned earlier in the month for notified amounts of Rs 5,000 crore and Rs 2,000

crore, respectively. The yield on 6-year paper has been set at 7.87 per cent while for the 10-

year security the yield has been set at 7.91 per cent lower than that set earlier during the

month.

Eight state governments have tapped the market to mobilise Rs 3,484 crore by issuing

10-year state development loans (SDL) through a yield-based auction using multiple price

auction method on August 16. In the case of Madhya Pradesh, the green shoe option has

exercised and bids worth Rs 750 crore have been accepted instead of Rs 600 crore. The cut-

off yields have been set at the lowest for Tamil Nadu at 8.30 per cent and the highest for 8.90

per cent for Jammu and Kashmir (J&K) ; in the previous month, J&K offered on SDL 8.25

per cent for the same maturity.

Under MSS issuances, the RBI has issued 5.48 per cent 2009 for an aggregate amount

of Rs 17,000 crore through three weekly auctions wherein the yields offered have declined

from 7.74 per cent on August 1 to 7.72 per cent on August 8 and then jumped to 7.99 per cent

on August 16, thus exceeding the yield offered on the 10-year security auctioned during the

month. However, in the last auction of the month on August 22, it dipped to 7.92 per cent.

The government issued new marketable securities 8.08 per cent 2022 for an aggregate

amount of Rs. 2,969 crore, 8.26 per cent 2027 for Rs.1,427 crore and 8.32 per cent 2032 for

Rs. 2,434 crore to 11 nationalised banks on August 2, 2007 against their holdings

recapitalisation bonds.

Page 16

79

Table10.7: Details of Central Government Market Borrowing (Amount in Rs Crore)

Competitive Bids Received

Competitive Bids Accepted Date of

Auction Nomenclature

of Loan Type of Auction

Notified Amount

Number Amount Number Amount

Indicative YTM at cut-off price

Devolvement on Primary

Dealers

6-Jul-07 7.99 per cent

2017 Normal 6000 308 18088 101 5979

7.99 per cent

NA

6-Jul-07 8.33 per cent

2036 Normal 4000 215 8271 134 3985

8.45 per cent (Rs. 98.72)

NA

20-Jul-07 7.27 per cent

2013 Normal 6000 227 13973 114 5984

7.59 per cent (Rs. 98.47)

NA

20-Jul-07 7.95 cent

2032 Normal 3000 235 11285 40 2991

8.34 per cent (Rs. 95.82)

NA

18-Jul-07 6.65 per cent

2009 MSS 5000 204 20934 24 4995

7.08 per cent (Rs. 99.30)

NA

25-Jul-07 7.55 per cent

2010 MSS 2000 108 5505 26 1999

7.04 per cent (Rs 101.27)

NA

Source: RBI Press Releases

Treasury Bills

Table 10.8: Auctions of Treasury Bills

(Rs crore)

Bids Received Bids Accepted

Total Face Value No. Total Face Value Date of Auction

Date of Issue

Notified Amt

No. Competitive

Non-competitive

Competitive Non-

competitive

Weighted avg. price

Implicit yield

91-Day Treasury Bills

1-Aug 3-Aug 2000 97 4932 200 56 2000 200 98.43 6.48 8-Aug 10-Aug 2000 86 4295 2500 29 2000 2500 98.41 6.56

14-Aug 17-Aug 2000 94 3450 303 61 2000 303 98.37 6.73 22-Aug 24-Aug 2000 82 3991 2050 14 2000 2050 98.34 6.81 29-Aug 31-Aug 3500 104 7553 550 26 3500 550 98.28 7.10

182-Day Treasury Bills

8-Aug 10-Aug 1500 52 1985 500 47 1500 500 96.61 7.27 22-Aug 24-Aug 1500 69 2235 1500 54 1500 1500 96.45 7.47

364-Day Treasury Bills

1-Aug 3-Aug 2000 84 4675 - 43 2000 - 93.31 7.25 14-Aug 17-Aug 2000 104 4685 - 33 2000 - 93.1 7.49 29-Aug 31-Aug 2000 115 5415 33 39 2000 33 93.06 7.52

Source: Weekly Statistical Supplement, RBI

The pressure on liquidity arising from increased government borrowings has reflected

in the unusual firming up of treasury bill rates. The yield on 91-day TB has surged from 4.46

per cent on July 25 to 6.48 per cent on August 1, to 6.56 per cent on August 8 and then to

Page 17

80

6.73 per cent and to 6.81 per cent on August 22; finally it has breached the 7 per cent mark by

touching 7.10 per cent on August 29 (Table 10.8).

ii) Secondary Market

Given the pressure on liquidity and uncertainty, the secondary market turnover for

gilt-edged securities has declined and the weekly average turnover ranged between Rs 14,629

crore and Rs 35,912 crore as against a range of Rs 38,961 crore and Rs 55,324 crore in the

previous month. Following the announcement of the first review of credit policy, the market

sentiments have turned cautious and prices fell. However, as the RBI enhanced the MSS

limit, the sentiments again have remained cautious except for a brief spell. Further, though

the domestic inflation remained subdued, international crude oil prices continued to surge

causing firmness in yields. In the RBI’s annual report, concerns have been expressed about

inflation remaining a threat, and hence the sentiments remained cautious despite RBI

refraining from undertaking MSS issuances.

Table 10.9: Inter-Category Wise NDS Reported Outright Trade of Central Govt

(Buy side) August 2007

Sellers

Buyer Category Foreign Banks

Primary Dealers

Public Sector Banks

Private Sector Banks

Mutual Funds

Coop Banks

FIs Others Ins.Cos Total

Per cent of total market share

Foreign Banks 52.40 22.56 11.08 6.40 3.14 3.06 0.00 0.00 1.34 100 28.62 Primary Dealers 33.59 6.51 12.49 37.17 4.76 4.50 0.00 0.00 0.98 100 15.76 Public Sector Banks 51.79 14.60 6.85 11.01 12.67 1.37 0.00 0.00 1.71 100 18.55 Private Sector Banks 43.60 25.63 5.01 16.98 4.31 2.12 0.00 1.07 1.28 100 20.94 Mutual Funds 22.57 40.52 3.73 11.20 6.22 15.76 0.00 0.00 0.00 100 3.73 Coop Banks 28.08 23.45 10.74 8.63 22.57 5.97 0.00 0.00 0.55 100 2.88 FIs 0.00 0.00 0.00 100.00 0.00 0.00 0.00 0.00 0.00 100 0.04 Others 10.16 21.25 0.00 16.94 39.47 11.17 0.00 0.00 1.02 100 0.02 Ins.Cos 3.95 8.96 0.59 83.35 2.57 0.20 0.00 10.79 0.39 100 9.45

Source: CCIL Rakshitra - September 2007

As per the inter-category

data published by CCIL for NDS

reported trades, foreign banks have

been the dominant players in dated

securities reported on the NDS

platform of the RBI, followed by

private sector banks (Table 10.9).

Table10.10: Category-Wise Market Share

for the Month of August 2007

Category Outright Treasury Bills Reverse RepoRepo

Buy Sell Buy Sell

Primary Dealers 10.6519.72 7.90 24.50 0.39 21.22Public Sector Banks 12.93 8.20 24.50 17.06 0.84 1.11 Private Sector Banks 14.4020.85 11.52 14.81 2.76 33.82Foreign Banks 41.1740.92 28.33 25.01 11.07 43.69Mutual Funds 5.34 5.67 24.35 18.10 84.38 0.00 Co-op Banks 4.02 3.35 1.69 0.31 0.00 0.11 FIs 0.06 0.00 0.07 0.00 0.01 0.05 Ins.Cos 11.22 1.13 1.63 0.20 0.53 0.00 Others 0.22 0.15 0.00 0.00 0.01 0.00

Source: CCIL Rakshitra- September 2007

Page 18

81

Mutual funds have been the major lenders while foreign banks have been the major

borrowers of funds. Also mutual funds have been major buyers of treasury bills given the

huge cash surplus mobilised by them through the new offerings. In the outright market,

foreign banks have been dominating buy as well as sell side of trades by accounting for about

40 per cent of the total trades (Table 10.10).

5. Money Market

After a gap of about two months,

the overnight rates have begun hovering

around the informal corridor set by the

reverse repo and repo rates, that is, around

August 6 when the RBI removed the cap

imposed on absorptions under reverse repo

and withdrew second LAF (Table 10.11).

In sync with call rates, the market

repo (outside the LAF) and CBLO rates declined and continued to remain below the call rate.

Overnight call rates, market repo rates and CBLO rates have displayed close co-movements

during the month

Reverse Repo and Repo under RBI’s LAF

In the first quarter review of credit

policy, the RBI withdrew the ceiling of Rs

3000 crore on daily reverse repo

absorptions and also second LAF was

withdrawn from August 6, as the there was

shift in liquidity scenario necessitating

absorptions through reverse repo.

However, the aggregate reverse repo bids tendered in August dipped to Rs 11,21,405 crore as

against Rs 19,54,710 crore as the outflows towards dated and MSS securities auctions and

hike in CRR impinged the liquidity (Table 10.12).

Table 10.11: Comparison of Call, Overnight CBLO and Repo rates

Weighted

Average Rates Daily Average Volumes

(in per cent) (Rs. crore)

Overnight

Overnight

Week Ending

Call

CBLO

Repo

Call

CBLO

Repo

3-Aug-07 0.63 0.08 0.32 8914 15314 9079 10-Aug-07 6.08 5.00 5.71 14994 30748 16839 17-Aug-07 7.12 6.01 5.89 12980 26196 17687 24-Aug-07 6.41 6.09 6.12 15476 27306 17350 31-Aug-07 6.13 5.74 6.05 12821 28085 17389 Source: CCIL Weekly Updates, Various Issues

Table10.12: Repo/Reverse Repo Amount

Tendered under RBI's LAF

(Amount in Rs Crore)

Week Repo Reverse Repo Outstanding

Amount

TenderedAccepted TenderedAccepted

Apr-07 166175 166175 174000 22919 -17245 May-07 151005 151005 305420 28983 26798 Jun-07 19370 19370 1432535 54979 -8895 Jul-07 0 0 1954710 56941 2992

Aug-07 0 0 1121405 488317 16855

Source: RBI Weekly Statistical Supplement (WSS)

Page 19

82

6. Foreign Exchange Market

The month of August

saw huge volatility across

global stock markets as well as

currency markets amidst the US

subprime crisis, turmoil in

global credit markets and high

crude oil prices. But the rupee

has been resilient amidst all

these skirmishes. In correcting

the earlier appreciation, it

depreciated not only against the

US dollar and Chinese Yuan,

but also against some of the

south East Asian currencies such as Hong kong dollar and Singaporean dollar, along with

marginal appreciations against South Korean won, Malaysian Ringgit and Indonesian

Ruphiah. Interestingly, this has happened when the US dollar itself was depreciating against

most of the currencies in the wake of deepening sub-prime mortgage crisis and spreading

contagion effect. Also, there were unwinding of yen carry trades as a part of global risk

aversion. There were FII outflows from the domestic equities market to the extent of Rs

7,771 crore during August as it implied that the investors’ penchant for emerging markets

appeared to have waned albeit temporarily and the rupee-dollar exchange rate depreciated

below the Rs 41-mark. After the US fed unexpectedly effected a cut in its benchmark rate and

as the domestic stock markets recovered, the rupee firmed up. However, again in the wake of

political uncertainty over nuclear deals along with firm international crude oil prices, the

rupee reverted to below the Rs 41-mark. The market sentiments for the rupee were influenced

by the Chinese central bank raising its lending and deposit rates and internally, the RBI

imposing constraints on ECB borrowings.

RBI has notified that the reporting platform developed by CCIL for capturing the

transactions in OTC interest rate derivatives (Interest Rate Swaps and Forward Rate

Agreements (IRS/FRA)), would be operationalised by August 30, 2007. All banks and

primary dealers are required to report all their IRS/FRA trades on the reporting platform

within 30 minutes from the deal time.

Chart 10.C:Daily Net FII Inflows and Rupee-Dollar

Exchange Rate (Aug 2007)

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

1-A

ug

3-A

ug

7-A

ug

9-A

ug

13-A

ug

16-A

ug

20-A

ug

22-A

ug

24-A

ug

28-A

ug

30-A

ug

Net

FII

Infl

ow

s (R

s cr

ore

)

40

40.1

40.2

40.3

40.4

40.5

40.6

40.7

Rupee

-doll

ar E

xch

ange

Rat

e

Net FII investment Rupee-Dollar Exchange Rate

Page 20

83

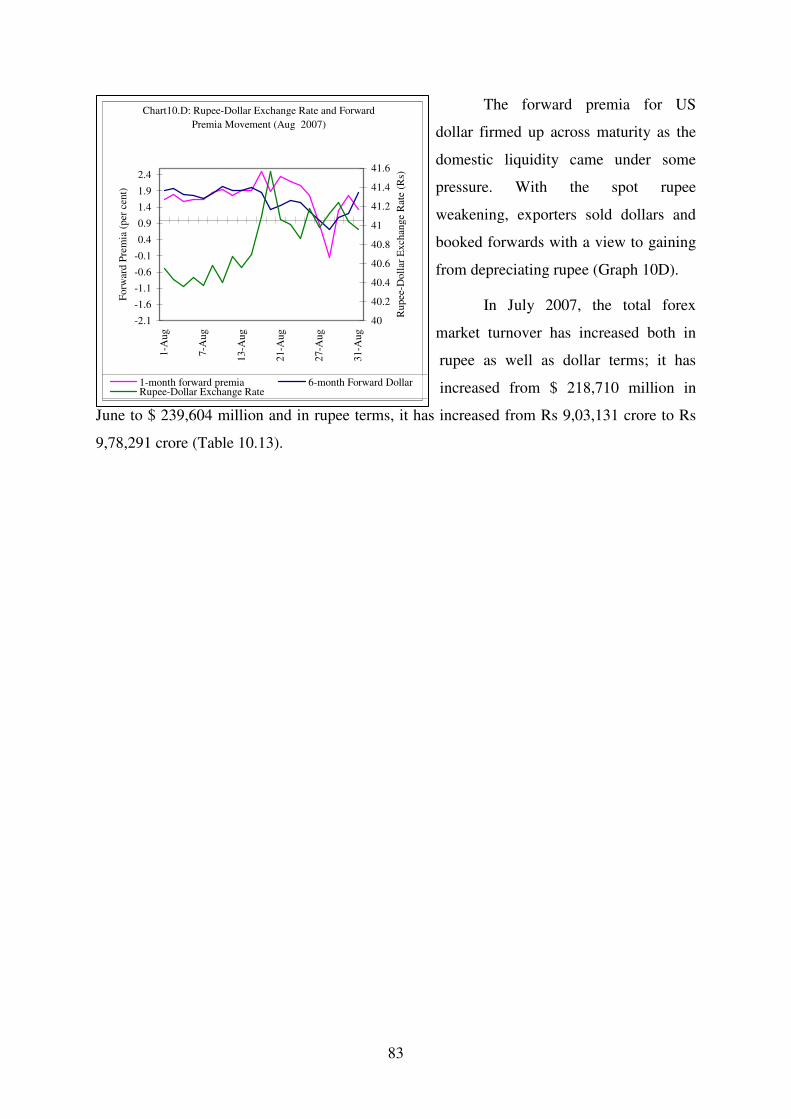

The forward premia for US

dollar firmed up across maturity as the

domestic liquidity came under some

pressure. With the spot rupee

weakening, exporters sold dollars and

booked forwards with a view to gaining

from depreciating rupee (Graph 10D).

In July 2007, the total forex

market turnover has increased both in

rupee as well as dollar terms; it has

increased from $ 218,710 million in

June to $ 239,604 million and in rupee terms, it has increased from Rs 9,03,131 crore to Rs

9,78,291 crore (Table 10.13).

Chart10.D: Rupee-Dollar Exchange Rate and Forward

Premia Movement (Aug 2007)

-2.1

-1.6

-1.1

-0.6

-0.1

0.4

0.9

1.4

1.9

2.41-A

ug

7-A

ug

13-A

ug

21-A

ug

27-A

ug

31-A

ug

Forw

ard P

rem

ia (

per

cen

t)

40

40.2

40.4

40.6

40.8

41

41.2

41.4

41.6

Rupee

-Doll

ar E

xch

ange

Rat

e (R

s)

1-month forward premia 6-month Forward DollarRupee-Dollar Exchange Rate

Page 21

84

Table 10.13: Category-Wise Settlement Volume in Forex Market for the Month of August 2007

Cash Tom Spot Forward Total Average Settlement period

(N) (A) (B) (N) (A) (B) (N) (A) (B) (N) (A) (B) (N) (A) (B) (N) (A) (B)

2002-03 - - - - - - 74423 96483 462370 25809 39619 195665 100232 136102 658035 1101 1496 7231

2003-04 1036 5951 26861 1555 9150 41335 251258 354541 1627644 76668 131700 622691 330517 501342 2318531 1425 2161 9994

2004-05 8747 69882 312311 16178 112750 504325 356382 533015 2389936 85020 184133 835863 466327 899782 4042435 1976 3813 17129

2005-06 12946 154626 6861604 21307 199621 8855851 371059 585089 25942395 84337 240352 10736886 489649 1179688 5239674 2084 5020 22297

2006-07 14292 233010 1050413 25708 316585 1427018 481702 884740 3993765 85106 342646 762957 606808 1776981 8023078 2550 7466 33710

Apr-07 1503 25993 109763 2596 37177 157760 55509 131841 557876 8065 46902 208121 67673 241913 1033519 3562 12732 54396

May-07 1213 21579 88118 1997 27416 112115 52868 123237 503448 7163 37633 163896 63241 209865 867578 3162 10493 43379

Jun-07 1244 23761 96909 2078 32973 134494 50598 116061 473537 7872 45915 198193 61792 21871 903131 2942 10415 43006

Jul-07 1222 24387 98578 1952 27648 111750 50105 133051 538466 7743 54519 229497 61201 239604 978291 3051 11980 48915

Aug-07 1119 23805 97105 2367 37802 154054 55995 132831 542257 7994 55897 235261 67475 250335 1028677 3213 11921 48985

Note: N-No of Trades; A-Volume in USD Million; B-Volume in Rs Crore

Source: CCIL Rakshitra, CCIL Market Update, various issues

Page 22

85

7. Commodities Futures Market

During April- August 2007, the total commodities turnover has been Rs 14,83,273

crore as against Rs 15,63,096 crore in the corresponding period last year. MCX has continued

to account for more than 70 per cent of the total turnover while the share NCDEX has

declined from 22 per cent in July to 11 per cent in August. Also, the share of agricultural

commodities in total turnover has declined while that of non-agricultural commodities has

increased sharply (Table 10.14).

Table 10.14: Monthly Turnover Of Commodity Exchanges

(Amount in Rs. crore)

Commodity Exchange April-Aug 07

turnover June-07

Turnover July-07

Turnover Aug-07

Turnover 1 1060455 208998 206111 225339

Multi Commodity Exchange of India Limited, Mumbai (71.5) (74.0) (73.0) (74.2)

2 9334 1329 1373 1391

National Multi-Commodity Exchange of India Limited, Ahmedabad

(0.6) (0.5) (0.5) (0.5)

3 221373 34173 64754 32854

National Commodity & Derivatives Exchange Ltd. Mumbai (14.9) (12.1) (22.9) (10.8)

4 7752 1770 1439 1186

Chamber of Commerce, Hapur

(0.5) (0.6) (0.5) (0.4)

5 34096 6752 6369 6615

National Board of Trade, Indore

(2.3) (2.4) (2.3) (2.2)

Total * 1483575 282550 282251 303508

Note: * Total includes the monthly turnover of the remaining 18 commodity exchanges. Figures in brackets denotes percentage share in the total turnover.

Source: FMC (www.fmc.gov.in)

Commodity-wise Turnover

Table10.15: Commodity-wise turnover

Jun-07 Jul-07 Aug-07

Commodity Trading on

all exchanges (Rs. Cr)

Percentage

to total turnover

Trading on all

exchanges (Rs. Cr)

Percentage

to total turnover

Trading on all

exchanges (Rs. Cr)

Percentage

to total t urnover

Metal

Gold 52998 18.76 56975 20.2 49346 16.3 Silver 42275 14.96 37345 13.2 44795 14.8 Copper 49032 17.35 39069 13.8 44577 14.7 Zinc 23622 8.36 22404 7.9 21756 7.2 Nickel 12325 4.36 10724 3.8 8910 2.9 Agricultural Product

Pepper 8958 3.17 8283 2.9 7808 2.6 Jeera 11191 3.96 5032 1.8 5246 1.7 Soy oil 13553 4.8 13750 4.9 11351 3.7 Gaur seed 8341 2.95 12878 4.6 17477 5.8 Chana 5942 2.1 7118 2.5 7225 2.4

Source: FMC (www.fmc.gov.in)

Page 23

86

In August, the share of gold has declined while that of silver and copper has

increased. Among the agricultural commodities, the trading in guar seed has increased while

that of pepper, chana, Jeera and Soya oil has declined (Table 10.15).

Entry of Corporates

Trading volumes on domestic commodity exchanges are rising with the entry of giant

corporates from across all sectors, especially in global commodities such as base metals,

precious metals, steel and energy. An increase in corporate volumes would stabilise prices

and help in anchoring the physical markets to the futures market. For effective price

discovery, it was important for speculators, hedgers and arbitrageurs to be present in the

market.

Anjani Sinha, director, MCX, has said that MCX cloaks the maximum market share in

metal futures in India, and traders would like to hedge on this platform where the cost is

lower because of higher liquidity. And hence, he said, the entry of corporates, especially for

metals on the MCX, would help them in better price discovery said. Although, the volume of

corporate hedgers has not reached a significant level, sources believe that within a short span

of time it would overtake the volume of small hedgers. In base metals, players like Binani

Zinc (BZL) has been keen, hedging approximately 2000 tonnes of zinc on the MCX.

Reportedly, Binani Zinc, the second-largest zinc producer in the country after Hindustan

Zinc, has traded to the value of Rs 1,500 crore and booked a profit of Rs 150 crore since it

started hedging on the MCX last year. Other players that are currently hedging on the

domestic exchanges include Essar and Polycab Wire, while metal and energy majors,

including Hindustan Copper (HCL), Indian Oil Corporation (IOC), Bharat Petroleum

Corporation (BPCL), and Hindustan Petroleum Corporation (HPCL), are in various stages of

negotiations to begin hedging in the near future. Many corporates hedge on global

commodity exchanges, with metal majors trading primarily on the London Metal Exchange

(LME) and the New York Mercantile Exchange (Nymex), and energy majors on the

Intercontinental Exchange (ICE), among others.

New Contracts

National Commodity and Derivatives Exchange is launching futures trading in

robusta coffee cherry AB variety on September 10, an official with the exchange said.

Page 24

87

NCDEX is launching five contracts expiring in January, March, May, July and September

2008. It has already secured approval from the market regulator Forward Markets

Commission to launch futures trading in robusta Cherry AB.

The recently introduced futures trading in raw jute on the Multi Commodity Exchange

(MCX) has come in for sharp criticism from the jute industry, with the latter urging the

Centre for an immediate ban on the futures. The industry’s appeal is currently being looked

into by the textile ministry. The ministry is already in discussion with the Ministry of

Consumer Affairs, Food and Public Distribution Department (FPD) and the Forward Markets

Commission (FMC).

National Commodity and Derivatives Exchange has launched a deliverable futures

contract in light sweet crude oil. Contracts for delivery in September, October and November

have begun trading. The Jawaharlal Nehru Port Trust has been designated as the delivery

centre. The trading unit will be 100 barrels, while the delivery unit is 50,000 barrels. The

exchange said that the buyer shall be responsible for the freight cost, insurance, import duty

and all other taxes and levies on actual basis. Traders have to give delivery intention during

the last three days of trading in the contract. The daily price fluctuation limit will be 6 per

cent, and if it reached intraday it would be extended by 3 per cent after 15 minutes. The

position limit for members has been set at 1.2 million barrels and that for a client will be

4,00,000 barrels.

Issues in Commodity Futures Market

Forward Markets Commission Chairman B C Khatua, stated that commodity futures

trading in the country is heading toward’s saturation levels due to bottlenecks in

infrastructure and operational constraints, lack of quality warehousing facilities as well as

uniform standards for benchmarking each commodity. Setting a uniform standard for a

commodity as far as possible will help in increasing the volume of trade as well as ensuring

better participation, he added. Turnover in commodity exchanges dropped 6-7 per cent in

April-July, 2007 compared with same period a year ago due to these problems, the Chairman

said. The Central government banning forward trading in high volume commodities, like

wheat a few months ago has also contributed to the fall in turnover, he said. Limits imposed

on open positions that could be held by individuals for near-month contract in commodities

like pepper and jeera has also affected the market, the chairman said. Rejecting suggestions

for a ban on futures trade, he said the market will achieve further growth by bringing more

Page 25

88

commodities under forward trading. Commodity futures trading in its present form is

relatively new in India and the depth of the market is limited at present, he said. But we could

resolve all these issues in consultations with various stakeholders in the market, Khatua said.

The chairman also stated his support for participation of banks and mutual funds in

commodity futures trading.

Issues in Jute Trading

According to the industry, futures trade in raw jute is a clear /fatka and dabba trade

perpetrated by unscrupulous brokers and market operators, who are mostly interested in

maximising gains. Such an action, the industry feels, can never be allowed to grow especially

on jute, which is an essential commodity and is governed by Jute and Jute Textile Control

Order (J&JTCO). The industry representatives mentioned that the recent raw jute speculation

on MCX showed compulsory deliveries despite the contract. The market speculators and

operators escape the practice through delivery/purchase by paying 5 per cent penalty as

mentioned in the penal provisions, they alleged. The penal margins being very low, the

speculators are deriving benefits out of these contracts, thereby marring prospects for the

industry. Moreover, the industry argued, with the Centre making packaging of sugar and food

grain compulsory in jute bags, the jute prices remaining stable is all the more necessary. The

Centre has recently made the order under the Compulsory Jute Packaging Act of 1987.

If prices of raw jute doesn’t remain within limits, the cost of production of bags would

shoot up, adversely affecting the operations of the food ministry, FCI and other state

agencies, who will then be forced to pack the materials well above the market regulated

prices and distribute through PDS,’said an industry representative. It has been pointed out to

the government that due to ‘speculative trade’ on the National Multi Commodity Exchange

(NMCE), Ahmedabad, in jute year 2005-06, the prices of raw jute rose exorbitantly and

hoarding became a common practice. At that point, jute was not available in the market,

forcing the industry to go in for ‘block closure’ of mills resulting in unemployment of almost

2.5 lakh workers and daily wage earners across the country.

The industry had then filed an FIR with the state police to investigate the whole

activities of the NMCE and its brokers/sub-brokers and agents. Following this, the Centre

took a series of steps such as fixing fresh prices of raw jute, registration of all dealers, traders

or agencies holding raw jute and launching of de-hoarding operations.