Page 1

XAVIER INSTITUTE OF MANAGEMNET, BHUBANESWAR

INDIVIDUAL RESEARCH PROECT

Topic:

A comparative analysis of advance towards priority sector lending

and customer satisfaction in public and private sector banks.

FACULTY GUIDE:

Dr. P Mishra, Professor

Economics and Strategic Management Area

XIMB

Submitted by:

Monika Poddar

Roll No. 31, PGDM (RM)-II

XIMB

Page 3

3

ACKNOWLEDGEMENT

I am grateful to Xavier Institute of Management, Bhubaneswar for giving me an opportunity to work on

Individual research project. It was a great experience for me to learn how to measure customer

satisfaction in both public and private banks. It also gave me opportunity to work on the trend analysis of

advances towards the priority sector lending by public and private banks.

The project gave us very valuable insights about the tools used in research studies. My experience

from this project is ineffable and it has certainly broadened my knowledge arena by introducing us to the

practical exposure in the research field. It also helped me in learning new techniques to be used with the

help of SPSS and also interpretation of the same.

All this had been possible only due to the constant support and guidance given by my guide Dr. P

Mishra, Professor, Economics and strategic management Area, for helping me out in every possible way

to conduct the research study. I feel indebted to my SRC guides Prof. Biswa Swarup Misra, Associate

Professor, Economics Area and Prof Sandip Anand, Assistant Professor, Marketing Area for their

wholehearted guidance throughout my project work.

I would like to thank Prof C Shambu Prasad for his help. I would also like to thank entire XIMB

family who has either directly or indirectly contributed in the successful completion of this project.

I cannot end without thanking my family, on whose constant encouragement and love I have

relied throughout my time at the Academy. I am also grateful to my father for his unflinching courage and

conviction which has always inspired me. It is to them that I dedicate this work.

Monika Poddar

Page 4

4

TABLE OF CONTENTS

EXECUTIVE SUMMARY:.....................................................................................................................6

INTRODUCTION:..................................................................................................................................7

RESEARCH OBJECTIVE: .....................................................................................................................9

PART I: PRIORITY SECTOR LENDING:..............................................................................................9

Categories of priority sector ...............................................................................................................11

Weaker sections within the priority sector: .........................................................................................11

Trends in the priority sector lending: ..................................................................................................12

Bank group wise credit to priority sector advances .............................................................................12

1. Public sector Banks:....................................................................................................................12

2. Private sector banks: ...................................................................................................................13

Methodology adopted:........................................................................................................................13

Analysis of the advances towards the priority sector lending:..............................................................14

Private Banks: ................................................................................................................................15

Public banks ...................................................................................................................................16

Conclusion:........................................................................................................................................21

PART II: CUSTOMER SATISFACTION IN BANKS:..........................................................................22

State Bank of India:............................................................................................................................22

Punjab National Bank:........................................................................................................................23

ICICI Bank: .......................................................................................................................................23

HDFC Bank: ......................................................................................................................................24

Need for customer satisfaction: ..........................................................................................................24

Current Scenario: ...............................................................................................................................25

Literature Review:..............................................................................................................................25

Methodology:.....................................................................................................................................27

The questionnaire formation and pretesting:....................................................................................28

Data analysis:.....................................................................................................................................28

Customer satisfaction in banks:.......................................................................................................28

Page 5

5

Section1: Demographic profile of customers: .....................................................................................29

Section 3: Regression Analysis:..........................................................................................................44

Section 4: Factor Analysis: ................................................................................................................52

Findings: ............................................................................................................................................59

CONCLUSION: ....................................................................................................................................60

References:............................................................................................................................................61

ANNEXURES.......................................................................................................................................62

Annexure 1: Questionnaire .................................................................................................................62

Annexure 2: Advances to priority sector lending by public and private sector banks in India...............66

Annexure 3: Factor Analysis……………………………………………………………………………67

Page 6

6

EXECUTIVE SUMMARY:

Customer satisfaction in banks plays a very important role in today’s competitive world. With a line of

various public and private banks coming into picture every year has given lots of importance to

understand what exactly a customer seek before he approaches a bank for its service. Customer

satisfaction is a post purchase experience that a customer gets after consumption of products and

services and becomes deciding factor for customer to make rational decision of repurchase and to

recommend it to others. But in a purely service industry service is provided, consumed and analyzed at

the point of consumption of service.

This study focuses on measurement of customer satisfaction related to Service offered and rendered by

public and private banks and also contribution of banks towards the priority sector as both are the

important stakeholders to bank as a whole. Any bank has responsibilities to give satisfaction to its

customers and also towards the society especially providing access to credit to the underprivileged ones.

Since Indian economy is a developing economy, every bank needs to cater a minimum of 40% of its net

bank credit towards the priority sector. Through this study we tried to see how these two sets of banks are

able to cater the needs of its customers and its society esp. priority sectors.

The trend analysis of the priority sector lending is done with the help of secondary data available at

www.indiastat.com and for customer satisfaction; a survey had been conducted online with a sample of

200 respondents across India. A structured questionnaire was prepared and administered and the data so

collected was analyzed both by percentages and statistical methods. Extensive use of SPSS (Statistical

Package for Social Sciences) software was incorporated for getting the analytical report. Tools like

univariate analysis, bivariate analysis, regression analysis and factor analysis has been used to analyse the

customer satisfaction survey.

The result showed that public sector banks have higher contribution towards the priority sectors as

compare to public sector banks. But in case of customer satisfaction private sector banks has higher score.

Better customer service on part of private banks can be better appreciated as their functions are fully

automated and they serve a narrowed exclusive clientele. Public sector banks on the other hand has a vast

network of branches in the rural areas and larger customer base with greater access to all cross section of

the society perhaps are not in the position to cater to its customers growing needs. Technology infusion

in the PSBs in the days to come perhaps would be able to improve their customer service.

Page 7

7

INTRODUCTION:

Banks play a very important role in economic development of every modern state. Indian banking sector

consist of a Reserve Bank of India, which is the central bank, commercial banks and cooperative banks.

Again commercial banks are divided into two types; the first one is schedule banks which have been

included in the Second Schedule of Reserve Bank of India (RBI) Act 1934 and nonscheduled banks.

"Non-scheduled bank in India" means a banking company as defined in clause (c) of section 5 of the

Banking Regulation Act, 1949 (10 of 1949), which is not a scheduled bank". Currently, India has 88

scheduled commercial banks (SCBs) - 27 public sector banks (that is with the Government of India

holding a stake), 29 private banks (these do not have government stake; they may be publicly listed and

traded on stock exchanges) and 31 foreign banks.

The oldest bank in existence in India is the State Bank of India, which originated in the Bank of Calcutta

in June 1806. By the 1900s, the market expanded with the establishment of banks such as Punjab National

Bank, in 1895 in Lahore and Bank of India, in 1906, in Mumbai - both of which were founded under

private ownership. In 1991, when Govt. embarked the policy of liberalization, that gave license to small

number of private banks. So in early nineties, six private sector banks were set up viz. UTI Bank ltd (now

Axis Bank), Oriental Bank of Commerce, ICICI Banking Corporation ltd, Global Trust Bank ltd,

Centurion Bank ltd and HDFC Bank ltd.

When we talk about the priority sector lending for these banks, the Reserve Bank's credit policy for the

year 1967-68 always come as the starting point. It caused an enunciation of the need to channelize the

flow of credit to certain sectors of the economy, known as the priority sectors, in the larger interests of the

country. Due to the severe imbalances which had developed in the economy in the preceding two years as

a result of shortfalls in agricultural output and slowing down of industrial production, credit policy for the

slack season 1967 was liberalized on a selective basis with a view, among other purposes, to enlarging the

flow of credit to the priority sectors such as agriculture, exports and small-scale industries (SSI). After lot

of reform and changes in the percentage of contribution made by the RBI towards the priority sector,

presently 40% of total net bank credit should be dedicated towards the priority sector lending.

In order to measure the customer satisfaction in the banks, we need to understand what the customers

looks for and what services does he expects from it. Customer satisfaction is increasingly becoming a

corporate goal as more and more companies strive for quality in their products and services Customer

Page 8

8

satisfaction is the feeling or attitude of a customer towards a product or service after it has been used and

is generally described as the full meeting of one's expectations.

The major differentiating parameter that distinguishes these private banks from public banks is the quality

of services that are offered to the customers. A number of studies clearly point out that these new

generation banks focus on the customer—understanding his needs, preempting him and consequently

delighting him with various configurations of benefits and a wide portfolio of products and services

(Arora, 2000; and Gani and Mustaq, 2003).

In this study, we have addressed the two aspects viz. the performance of the public banks and private

sector banks with respect to priority sector lending. It mainly focuses on measurement of customer

satisfaction related to services offered and rendered by public and private sector banks and also

contribution of banks towards the priority sector as both are the important stakeholders to the bank as a

whole. Banks in the developing economy has the responsibilities both to its customers and the society at

large. They have responsibilities to provide satisfaction to its customers and also towards the society

especially providing access to credit to the underprivileged ones. According to RBI norms, every bank

needs to cater a minimum of 40% of its net bank credit towards the priority sector. Through this study we

tried to see how these two sets of banks are able to cater the needs of its customers and the society

especially priority sectors.

In view of the above entire study has been divided into two parts:

Part 1 deals with the trend analysis of the advances towards the priority sector lending of both public and

private sector banks from 2001-2007.

Part 2 deals with the customer satisfaction survey w.r.t to various service offered by public and private

banks.

Page 9

9

RESEARCH OBJECTIVE:

1. To understand the amount of money being diffused towards the priority sector lending

(agriculture, exports and small-scale industries) by public and private sector banks and its

implications.

2. To study the ratio of total lending and lending to the priority sector (rural sector) by both the

categories of banks.

3. To study level of customer satisfaction between public and private sector bank with respect to

several services provided by them.

PART I: PRIORITY SECTOR LENDING:

An enunciation of the need to channelize the flow of credit to certain sectors of the economy, known as

the priority sectors, in the larger interests of the country, can be traced to the Reserve Bank's credit policy

for the year 1967-68. In view of the severe imbalances which had developed in the economy in the

preceding two years as a result of shortfalls in agricultural output and slowing down of industrial

production, credit policy for the slack season 1967 was liberalized on a selective basis with a view,

among other purposes, to enlarging the flow of credit to the priority sectors such as agriculture, exports

and small-scale industries (SSI).

The nationalization of the 14 major commercial banks in July 1969 led to a considerable reorientation of

bank lending, especially to the priority sectors of the economy, which had not previously received

sufficient attention from the commercial banks. It gave an impetus to the process of reallocation of

banking resources to suit the socio-economic needs of the country. There was a greater involvement of

banks in these and other socially desirable sectors. Moreover, institutional credit facilities at reasonable

rates of interest were extended to a large number of borrowers of small means such as small farmers,

small-scale manufacturers, retail traders, road transport operators, small businessmen, professionals and

self-employed persons, and also for education. One of the objectives of nationalization of 14 major

commercial banks was to ensure that no viable productive endeavor should falter for lack of credit

support, irrespective of the fact whether the borrower was big or small. Thus, the concept of priority

Page 10

10

sector lending was evolved further to ensure that assistance from the banking system flowed in an

increasing measure to the vital sectors of the economy and according to national priorities.

Government of India, viz., that banks should aim at raising the proportion of their advances to the priority

sector from 33 1/3 per cent to 40 per cent by 1985, and that the banks should actively promote the

implementation of the 20-Point Programme which aimed at improving the lot of the weaker sections of

the population. The Group identified the categories of beneficiaries requiring assistance from the banking

system in pursuance of the 20-Point Programme and spelt out the manner in which assistance could be

rendered. As most of the beneficiaries under the Programme fell in the relatively under-privileged group

within the priority sector, the Group suggested certain changes in the approach to priority sector lending.

In particular, it introduced the concept of 'weaker sections' within the priority sector and recommended

separate sub-targets for lending to the weaker sections in the two main categories of the priority sector,

namely, agriculture and SSI, within the overall enhanced target of 40 per cent for lending to the priority

sector. Housing loans upto Rs 5,000 for construction of houses for SC/ST and weaker sections, assistance

to any governmental agency for construction of houses for SC/ST and low-income groups (where loan

component does not exceed Rs 5000 per unit) and pure consumption loans granted to the weaker sections

under the Consumption Credit Scheme were recommended for inclusion in priority sector.

Currently, the targets and sub-targets set under priority sector lending for domestic and foreign banks

operating in India are furnished below:

Domestic banks (both public

sector and private sector

banks)

Foreign banks operating in

India

Total Priority Sector advances 40 percent of NBC 32 percent of NBC

Total agricultural advances 18 percent of NBC No target

SSI advances No target 10 percent of NBC

Export credit Export credit does not form part

of priority sector

12 percent of NBC

Advances to weaker sections 10 percent of NBC No target

Page 11

11

CATEGORIES OF PRIORITY SECTOR

1. Agriculture (direct and indirect finance)

2. Small scale industries (including setting up of industrial estates)

3. Small road and water transport operators (owning upto 10 vehicles).

4. Small business (Original cost of equipment used for business not to exceed Rs 20 lakh)

5. Retail trade (advances to private retail trader’s upto Rs.10 lakh)

6. Professional and self-employed persons (borrowing limit not exceeding Rs.10 lakh of which

not more than Rs.2 lakh for working capital; in the case of qualified medical practitioners setting

up practice in rural areas, the limits are Rs 15 lakh and Rs 3 lakh respectively and purchase of one

motor vehicle within these limits can be included under priority sector)

7. State sponsored organisations for Scheduled Castes/Scheduled Tribes

8. Education (educational loans granted to individuals by banks)

9. Housing [both direct and indirect – loans upto Rs.5 lakhs (direct loans upto Rs 10 lakh in urban/

metropolitan areas), Loans upto Rs 1 lakh and Rs 2 lakh for repairing of houses in rural/ semi-

urban and urban areas respectively].

10. Consumption loans (under the consumption credit scheme for weaker sections)

11. Micro-credit provided by banks either directly or through any intermediary; Loans to self help

groups (SHGs) / Non Governmental Organisations (NGOs) for onlending to SHGs.

12. Loans to the software industry (having credit limit not exceeding Rs 1 crore from the banking

system)

13. Loans to specified industries in the food and agro-processing sector having investment in plant

and machinery up to Rs 5 crore.

14. Investment by banks in venture capital (venture capital funds/ companies registered with

SEBI)

Weaker sections within the priority sector:

1. Small and marginal farmers with land holding of 5 acres and less and landless labourers, tenant

farmers and share croppers.

2. Artisans, village and cottage industries where individual credit limits do not exceed Rs. 50,000/-

3. Beneficiaries of Swarnjayanti Gram Swarojgar Yojana (SGSY)

Page 12

12

4. Scheduled Castes and Scheduled Tribes

5. Beneficiaries of Differential Rate of Interest (DRI) scheme

6. Beneficiaries under Swarna Jayanti Shahari Rojgar Yojana (SJSRY)

7. Beneficiaries under the Scheme for Liberation and Rehabilitation of Scavengers (SLRS).

8. Self Help Groups (SHGs)

If the banks fail to achieve the required lending to priority sector then the following are taken by the RBI:

i. Domestic scheduled commercial banks having shortfall in lending to priority sector / agriculture

are allocated amounts for contribution to the Rural Infrastructure Development Fund (RIDF)

established in NABARD. Details regarding operationalisation of the RIDF such as the amounts to

be deposited by banks, interest rates on deposits, period of deposits etc., are decided every year

after announcement in the Union Budget about setting up of RIDF. They can also contribute their

shortfall in SIDBI or buy special bonds from state financial corporations.

TRENDS IN THE PRIORITY SECTOR LENDING:

According to a study made by RBI rural planning and credit department the credit advanced to the

priority sector by scheduled commercial banks recorded an average annual growth rate of 18.4 per cent

during the period from 1995 to 2004, which was marginally higher than the average annual growth of

18.0 per cent observed in aggregate bank credit. However, the share of priority sector advances as a

percentage of NBC had shown undulating trends during the period. During 1995-1996, it fell from 33.7

per cent to 32.8 per cent, but remained steady at around 35 per cent during the years 1997 to 2000.

Thereafter, it dipped sharply to 31.0 per cent in 2001 recovered to 35.1 per cent in 2003 and further to

36.8 per cent in 2004.

Bank group wise credit to priority sector advances

1. Public sector Banks:

The outstanding priority sector advances of PSBs increased by 21 per cent in 2003-04 as against an

increase of 18.6 per cent during 2002-03. During the period 1995-2004, the average annual growth rate of

advances to priority sector by public sector banks was 17.6 per cent as compared to average growth rate

Page 13

13

of NBC at 16.7 per cent in the same period. The higher growth in priority sector advances of PSBs during

the above period was primarily due to 28.8 per cent average growth rate recorded by other priority sectors

which compensated for the low average growth rate in credit to SSI (9.3 per cent) and direct agriculture

credit (15.7 per cent). The share of priority sector advances in NBC of PSBs increased to 44 per cent in

2003-04 from 42.5 per cent in 2002-03. The growth in priority sector advances of PSBs was fuelled by

the surge in the loans and advances to various other priority sectors and robust growth of credit to the

agriculture sector. Advances to agriculture constituted 15.4 per cent of NBC of PSBs as on the last

reporting Friday of March 2003. The share of advances to other priority sectors in NBC of PSBs

increased to 17.0 per cent in 2003-04 from 15.0 per cent in 2002-03. The number of accounts covered

under various major segments (agriculture, SSI and other priority sectors) of priority sector declined over

the period.

2. Private sector banks:

Private sector banks’ lending to priority sector as a percentage of their NBC has been showing an

increasing trend. The share of their advances to priority sector in NBC had increased from 44.4 per cent in

2002-2003 to 47.4 per cent in 2003-04. During the period from 1997 to 2004, average annual growth rate

of priority sector advances of private sector banks was 29.5 per cent which was mainly contributed by the

growth in lending to other priority sectors (44.7 per cent) and agriculture (37.4 per cent). In comparison,

the average annual growth rate for advances to SSI was at 8.4 per cent. In absolute terms, credit to

agriculture, SSI and other priority sectors had increased. The share of credit to other priority sector

category was the highest at 23.1 per cent of NBC, followed by advances to agriculture and SSI. The

lending of private sector banks to agriculture sector had increased to 12.3 per cent of their net bank credit

in 2003-04, higher by 1.1 per cent over that in 2002-03.

Methodology adopted:

The data for the advances towards the priority sector lending for the last seven years has been taken from

2001-2007. The trend analysis using univariate tool has been done to analyse the flow of credit towards

the priority sector.

Page 14

14

Analysis of the advances towards the priority sector lending:

The table showing the details of the advances towards the priority sector lending in the last seven years

are given in Annexure 2.

Page 15

15

From the graph we can see that though the contribution towards the priority sector has been increasing by

both public sector and private sector but if we see in absolute number terms we find that public banks has

contributed in fairly large amounts as compared to private sector banks.

Private Banks:

There is an increasing trend in the advances to agriculture sector by the private banks upto 2004 but it has

not reached the required 18% target in any of the last seven years.

The advances to the Small Scale Industries has decline over a period of seven years. Though there is no

fixed target for Small Scale Industries but the contribution towards this sector has decreased.

Advances in the other priority sectors including export credit, contribution to weaker section and DRI

advances has increased from 2001 to 2004, then again it has shown a slow declining trend till 2007.

The total priority sector advances has increased from 2001 to 2004 and has crossed the minimum target of

40% towards priority sector. But after 2004 there has been again a declining trend at a slow pace.

Page 16

16

Public banks

There is a decreasing trend in the advances to agriculture sector by the public banks from 2001 to 2003

then an increasing trend from 2004 to 2007 but still it has not achieved the required 18% target in any of

the last seven years.

The advances to the Small Scale Industries has decline over a period of seven years. Though there is no

fixed target for Small Scale Industries but the contribution towards this sector has decreased.

Advances in the other priority sectors including export credit, contribution to weaker section and DRI

advances has been showing an increasing and decreasing trend on year to year basis from 2001 to 2007

The total priority sector advances has decreased from 2001 to 2003 but it has crossed the minimum target

of 40% towards priority sector. The contribution increased from 2003 to 2004 but after 2004 there has

been again a declining.

The increase in the contribution to priority sector in the initial years was mainly due to the inclusion of

funds provided to Regional Rural Banks by their sponsoring banks, that were eligible to be treated as

priority sector advances.

Page 17

17

Private Banks: The % net bank credit for agriculture in 2001 is 9.6% (as compared to min target - 18%).

SSI contributes 13.8% to total net bank credit. Other priority sector contributed 12.3% of total net bank

credit. The total priority sector lending is 36.7% (as compared to min target of 40%).

Public Banks: The % net bank credit for agriculture in 2001 is 15.7% (as compared to min target - 18%).

SSI contributes 14.2% to total net bank credit. Other priority sector contributed 12% of total net bank

credit. The total priority sector lending is 43.7% (which is higher than the min target of 40%).

Page 18

18

Private Banks: The % net bank credit for agriculture in 2002 is 8.5% (as compared to min target - 18%).

SSI contributes 13.7% to total net bank credit. Other priority sector contributed 14.4% of total net bank

credit. The total priority sector lending is 40.9% (reached the min target of 40%).

Public Banks: The % net bank credit for agriculture in 2002 is 14.8% (as compared to min target - 18%).

SSI contributes 13.8% to total net bank credit. Other priority sector contributed 15% of total net bank

credit. The total priority sector lending is 43.5% (again higher than the min target of 40% but less than

previous year).

Private Banks: The % net bank credit for agriculture in 2003 is 12% (as compared to min target - 18%).

SSI contributes 9.7% to total net bank credit, less than previous year. Other priority sector contributed

22.5% of total net bank credit. The total priority sector lending is 44.1% (crossed the min target of 40%).

Public Banks: The % net bank credit for agriculture in 2003 is 14.5% (as compared to min target - 18%).

SSI contributes 10.8% to total net bank credit, less than previous year. Other priority sector contributed

14.7% of total net bank credit. The total priority sector lending is 41.2% (crossed the min target of 40%).

Page 19

19

Private Banks: The % net bank credit for agriculture in 2004 is 14.2% (as compared to min target -

18%). SSI contributes 7.3% to total net bank credit, less than previous year. Other priority sector

contributed 24.9% of total net bank credit. The total priority sector lending is 47.3% (crossed the min

target of 40%).

Public Banks: The % net bank credit for agriculture in 2004 is 15.1% (as compared to min target - 18%).

SSI contributes 10.3% to total net bank credit, less than previous year. Other priority sector contributed

17.1% of total net bank credit. The total priority sector lending is 43.6% (crossed the min target of 40%).

Private Banks: The % net bank credit for agriculture in 2005 is 13.5% (as compared to min target -

18%). SSI contributes 5.4% to total net bank credit, less than previous year. Other priority sector

Page 20

20

contributed 24.2% of total net bank credit. The total priority sector lending is 43.6%, which is less than

the previous year but crossed the min target of 40%.

Public Banks: The % net bank credit for agriculture in 2005 is 15.3% (as compared to min target - 18%).

SSI contributes 9.5% to total net bank credit, less than previous year. Other priority sector contributed

17.4% of total net bank credit. The total priority sector lending is 42.8%, which is less than the previous

year but crossed the min target of 40%.

Private Banks: The % net bank credit for agriculture in 2006 is 13.6% (as compared to min target -

18%). SSI contributes 4.2% to total net bank credit, still less than previous year. Other priority sector

contributed 23.2% of total net bank credit. The total priority sector lending is 42.8%, which is less than

the previous year but crossed the min target of 40%.

Public Banks: The % net bank credit for agriculture in 2006 is 15.3% (as compared to min target - 18%).

SSI contributes 8.1% to total net bank credit, still less than previous year. Other priority sector

contributed 16.1% of total net bank credit. The total priority sector lending is 40.3%, which is less than

the previous year but crossed the min target of 40%.

Page 21

21

Private Banks: The % net bank credit for agriculture in 2007 is 12.8% (as compared to min target -

18%). SSI contributes 3.9% to total net bank credit, still less than previous year. Other priority sector

contributed 22.9% of total net bank credit. The total priority sector lending is 42.7%, which is bit less

than the previous year but crossed the min target of 40%.

Public Banks: The % net bank credit for agriculture in 2007 is 15.6% (as compared to min target - 18%).

SSI contributes 8% to total net bank credit, still less than previous year. Other priority sector contributed

15.3% of total net bank credit. The total priority sector lending is 39.6%, which is bit less than the

previous year but crossed the min target of 40%.

CONCLUSION:

The trend analysis of the priority sector shows that the public banks have always been contributing more

towards the priority sector in absolute terms. The public banks have always contributed higher in the

agriculture sector in the last 7 years as compared to private banks. This shows that the public banks have

higher score in providing credit advances to the priority sector. Later the private banks were able to

increase its contribution towards priority sector by increasing their contribution more towards other

priority sectors like export credit, contribution to weaker section and DRI advances etc.

Page 22

22

PART II: CUSTOMER SATISFACTION IN BANKS:

Banks play a very important role in economic development of every modern state. Indian banking sector

consist of a Reserve Bank of India, which is the central bank, commercial banks and cooperative banks.

Again commercial banks are divided into two types; the first one is schedule banks which have been

included in the Second Schedule of Reserve Bank of India (RBI) Act 1934 and nonscheduled banks.

"Non-scheduled bank in India" means a banking company as defined in clause (c) of section 5 of the

Banking Regulation Act, 1949 (10 of 1949), which is not a scheduled bank". Currently, India has 88

scheduled commercial banks (SCBs) - 27 public sector banks (that is with the Government of India

holding a stake), 29 private banks (these do not have government stake; they may be publicly listed and

traded on stock exchanges) and 31 foreign banks.

The oldest bank in existence in India is the State Bank of India, which originated in the Bank of Calcutta

in June 1806. By the 1900s, the market expanded with the establishment of banks such as Punjab National

Bank, in 1895 in Lahore and Bank of India, in 1906, in Mumbai - both of which were founded under

private ownership.

In 1991, when Govt. embarked the policy of liberalization, that gave license to small number of private

banks. So in early nineties, six private sector banks were set up viz. UTI Bank ltd (now Axis Bank),

Oriental Bank of Commerce, ICICI Banking Corporation ltd, Global Trust Bank ltd, Centurion Bank ltd

and HDFC Bank ltd.

STATE BANK OF INDIA:

State Bank of India (SBI) is the largest bank in India. It is measured by the number of branch offices and

employees as the largest bank in the world. Established in 1806 as Bank of Bengal, it remains the oldest

commercial bank in the Indian Subcontinent and also the most successful one providing various domestic,

international and NRI products and services, through its network of 13,908 branches, including 4,731

associate banks' branches in India and overseas. It also provides financial services, such as life insurance,

merchant banking, mutual funds, credit card, factoring, security trading and primary dealership in the

money market. With an asset base of $126 billion and its reach, it is a regional banking behemoth. The

Page 23

23

bank was nationalized in 1955 with the Reserve Bank of India having a 60 percent stake. It has laid

emphasis on reducing the huge manpower through Golden handshake schemes and computerizing its

operations.

It also has non-banking subsidiaries and joint ventures, such as SBI Capital Markets Ltd., SBI DFHI Ltd.,

SBI Funds Management Pvt Ltd., SBI Factors & Commercial Services Pvt Ltd. and SBI Life Insurance

Company Ltd. Effective from April 20, 2005; it acquired a 51 percent stake in Indian Ocean International

Bank Ltd.

PUNJAB NATIONAL BANK:

Punjab National Bank (PNB), was registered on May 19, 1894 under the Indian Companies Act with its

office in Anarkali Bazaar Lahore. The Bank, founded by Dyal Singh Majithia and Lala Harkishen Lal, is

the second largest government-owned commercial bank in India with about 4,500 branches across 764

cities. It serves over 37 million customers. The bank has been ranked 248th biggest bank in the world by

Bankers Almanac, London. Total Business of the bank for financial year 2007 is estimated to be

approximately US$60 billion. It has a banking subsidiary in the UK, as well as branches in Hong

Kong and Kabul, and representative offices in Almaty, Shanghai, and Dubai.

ICICI BANK:

ICICI Bank (formerly Industrial Credit and Investment Corporation of India) is India's largest private

sector bank and second largest overall. ICICI Bank has total assets of about USD 56 Billion (end-Mar

2006), a network of over 619 branches and offices, and about 2400 ATMs. ICICI Bank offers a wide

range of banking products and financial services to corporate and retail customers through a variety of

delivery channels and through its specialized subsidiaries and affiliates in the areas of investment

banking, life and non-life insurance, venture capital and asset management. ICICI Bank's equity shares

are listed in India on stock exchanges at Kolkata and Vadodara, the Stock Exchange, Mumbai and the

National Stock Exchange of India Limited and its ADRs are listed on the New York Stock Exchange

(NYSE). Between 2004 and 2007, its balance sheet has grown at more than 40% every year. It has also

aggressively expanded its overseas presence in past few years, setting up shop in 18 countries and

building $25 billion (Rs1.1 trillion) of assets, roughly one-fourth of its book.

Page 24

24

HDFC Bank:

HDFC Bank is one of the first, new generation, tech-savvy commercial banks of India, was incorporated

in August 1994. The Bank was promoted by the Housing Development Finance Corporation Limited, a

premier housing finance company (set up in 1977) of India. Currently HDFC Bank has 1,500 branches

and over 1,716 ATMs, in 325 cities in India, and all branches of the bank are linked on an online real-

time basis. The bank offers many innovative products & services to individuals, corporates, trusts,

governments, partnerships, financial institutions, mutual funds, insurance companies.

In 2007 HDFC Bank acquired Centurion Bank of Punjab taking its total branches to more than 1,000.

Though, the official license was given to Centurion Bank of Punjab branches, to continue working as

HDFC Bank branches, on May 23, 2008. Over a decade of its operations, HDFC Bank has been

recognized, rated and awarded by a number of organizations. With a merger with Centurion bank of

Punjab the total no. of branches reach to more than 1500 branches

Need for customer satisfaction:

Customer satisfaction is an important theoretical as well as practical issue for most marketers and market

researchers. Customer satisfaction is increasingly becoming a corporate goal as more and more companies

strive for quality in their products and services Customer satisfaction is the feeling or attitude of a

customer towards a product or service after it has been used and is generally described as the full meeting

of one's expectations. Customer satisfaction is a major outcome of marketing activity whereby it serves as

a link between the various stages of consumer buying behavior. For instance, if customers are satisfied

with a particular service offering after its use, then they are likely to engage in repeat purchase and try

line extensions.

The major differentiating parameter that distinguishes these private banks from public banks is the quality

of services that are offered to the customers. A number of studies clearly point out that these new

generation banks focus on the customer—understanding his needs, preempting him and consequently

delighting him with various configurations of benefits and a wide portfolio of products and services

(Arora, 2000; and Gani and Mustaq, 2003). The Indian banking sector has never taken relationship

marketing seriously, which is a “new paradigm”. It is only after liberalization, banks are moving towards

a “customer-centric approach”. From 1992 onwards, the competition between the public and private

Page 25

25

sector banks started gaining momentum. People have shifted their focus from the public sector to the

private sector banks, which show that these new banks have generated trust, commitment and loyalty

among the customers (Dhillon et al., 2003).

Current Scenario:

The banking industry like many other financial service industries is facing a rapidly changing market,

new technologies, economic uncertainties, fierce competition and more demanding customers and the

changing climate has presented an unprecedented set of challenges. Banking is a customer oriented

services industry, therefore, the customer is the focus and customer service is the differentiating factors.

With the current change in the functional orientation of banks, the purpose of banking is redefined. The

main driver of this change is changing customer needs and expectations. Customers in urban India no

longer want to wait in long queues and spend hours in banking transactions. This change in customer

attitude has gone hand in hand with the development of ATMs, phone and net banking along with

availability of service right at the customer's doorstep. With the emergence of universal banking, banks

aim to provide all banking product and service offering under one roof and their endeavor is to be

customer centric. With the emergence of economic reforms in world in general and in India in particular,

private banks have come up in a big way with prime emphasis on technical and customer focused issues.

Literature Review:

Customer-centric banking services involved anticipation, identification, reciprocation and satisfaction of

the customers’ needs and wants effectively, efficiently and profitably. The competition between public

sector banks and private sector banks has put pressure on the banks to improve their customer service and

work for image building and branch equity. There are different authors who have studied these aspects

and have arrived at several conclusions. Some of the studies and findings of a few researchers which are

related to the present study have briefly been summarized in the following few paragraphs.

Luiz Moutinho, Douglas T. Brownlie (1989) in their work have examined customer satisfaction with bank

services using a Multidimensional Space Analysis. He found that respondents had high levels of

satisfaction with regard to the location and accessibility of branches and ATMs, and acceptance of the

current levels of banking fees; but expressed some caution in their evaluation of new and improved

services

Page 26

26

Fornell (1992) defined customer satisfaction as an overall evaluation of the total purchase experience

compared with pre-purchase expectations over time. Bitner and Hubbert (1994) defined service quality as

the customer’s overall impression about perceived superiority of a company and its products/services

while satisfaction is defined as the feeling of a customer after the usage and the purchase of a product or

service. Reichheld & Sasser (1990) argued that loyalty is directly connected with profitability.

Roger Hallowell (1996) has tried to examine the relationships of customer satisfaction, customer loyalty,

and profitability. In his empirical research, he has used relational measures to quantify the extent of

relationships between the said variables. He has found out that increase in customer satisfaction could

dramatically improve profitability of the bank.

Johnson & Mehra (2002), stated that handling and resolving customers’ complaints transform dissatisfied

customers into satisfied and loyal.

Aggrawal and Gupta (2003) have attempted to develop a Multilevel-Multidimensional model,

SERVQUAL (Service Quality) Model of service quality. The result shows that service quality of foreign

banks and new private banks is comparatively much better than those of government banks. The reason

was that these banks operated in a selected market and offered selected services along with the fact that

the customers are valued. Secondly, they are backed by state-of-the-art banking technology, which gives

them a competitive edge (Gani and Mustaq, 2003). The studies for customers’ perceptions of service

quality is also significant because a high-level of service quality is associated with several key

organizational outcomes including high market share, enhanced customer loyalty and improved

profitability relative to competitors (Debasish, 2003). The public and private bank employees differ

significantly on Customer Relationship Management (CRM) and customer orientation (Mittal et al.,

2003). This implies that private bank employees score high on CRM in general and specifically on

customer orientation. This further implies that it is highly essential for a bank to strive towards service

excellence to ensure that customers are not just satisfied but delighted with what banks do for them.

Anders Gustafsson (2008) had conducted a study on customer satisfaction with service recovery and

found out that competition in current scenario is fierce. More and more services include a technology

component that may limit customer/employee contacts and make services more complex. Retaining

customer has therefore become very important. Dhade and Mittal (2008) have mentioned in their work

that the phenomenal changes taking place in the banking industry indicate that the new private

Page 27

27

sector banks have gradually won the market with their customer-centric approach. The depleting market

share of the public sector banks poses a threat to them. They have concluded that banking business was

becoming more and more complex as a result of liberalization and globalization. They have also opined

that private banks are becoming more conscious of the needs of the customers. From their findings they

have mentioned that customer plays an important role in the selection of a particular bank. Now, proper

customer care, number of years in business and easy accessibility are considered as the important factors

that influence a customer’s choice of a bank.

As mentioned towards the beginning of this section, there are several researchers who have conducted

study on customer satisfaction, the profitability of the bank and determinant with respect to the customer

satisfaction and quite a few other issues relating to the services provided by the banks. In our present

study we have focussed on the differences between the customer satisfaction with respect to two sets of

bank namely public banks and private sector banks. In this connection, we have examined the previous

work of few authors in the area of differences in customer satisfaction in both the sets of banks. In our

brief literature mentioned above authors such as Dhade and Mittal (2008), Debasish,( 2003), Mittal et al.,(

2003), Gani and Mustaq,(2003), Aggrawal and Gupta (2003) have conducted research specifically on

comparative picture of customer satisfaction in public and private sector banks. Their brought conclusions

are basically revolves around finding out factors that determine the customer satisfaction in both the types

of banks. Keeping this in our mind we have tried to find out the factors for customer satisfaction taking

samples across the country which is a departure from some of the earlier studies.

METHODOLOGY:

To address the above objective the following methodology has been used. Needless to mention that the

present report is based on a survey research relating to the satisfaction level of the customers in two types

of banks namely public sector banks and private sector banks.

For the present study a sample of 200 respondents have been selected at random. However due to

limitation in identifying the universe/population, simple random sampling has not been adopted rather a

systematic accidental sampling has been adopted to select the samples. The selection of sample

respondents was done by sending an online questionnaire to customers of different banks across the

country. The responses relating to their willingness to participate were tabulated and a sample of 200

respondents was selected on the basis of region, occupation, gender etc. it may be pointed out here that

Page 28

28

although the selection process is accidental, we have tried to make the sample a representative of the

customers in two sets of banks, with respect to above variables. A structured questionnaire was prepared

and administered and the data so collected was analyzed both by percentages and statistical methods.

Extensive use of SPSS (Statistical Package for Social Sciences) software was incorporated for getting the

analytical report. Univariate analysis, bivariate analysis, regression analysis and factor analysis has been

done.

The Bivariate analysis shows that the customers of private banks are more satisfied with the services

offered to hem at their banks as compared to customers of the public banks. The regression analysis

shows that there is a positive relationship between the overall satisfaction of the bank and the

The questionnaire formation and pretesting:

A questionnaire was formulated with respect to our objective mentioned above (Annexure 1). The

questionnaire was pretested with 15 respondents and a few corrections were made in the same on the

basis of their feedback. The questionnaire was finalised for final canvassing.

DATA ANALYSIS:

Customer satisfaction in banks:

To analyse the data, frequency tables, ratio and percentages and multivariate tools like factor and

regression analysis have been used.

To begin with we have started with the univariate analysis of age and occupation for the respondents.

Here the data has been taken for both private and public banks. Private Banks in this study includes

HDFC Bank and ICICI Bank. Public bank includes SBI and PNB. Only four banks have been taken for

study due to time constraints. 50 respondents from each bank have been taken to do the data analysis. A

total of 200 respondents have filled the questionnaire which has become the basis of analysis for customer

satisfaction in bank.

Page 29

29

The analysis has been divided into 4 sections. The first section deals with the univariate tools, second part

deals with the bivariate analysis, third part deals with regression analysis and the fourth part deals with

the factor analysis.

Section1: Demographic profile of customers:

Two parameters are taken i.e., gender and occupation is taken into consideration. The figure below shows

the gender distribution of the customers of both private and public banks.

On the basis of our samples the findings on gender distribution is that in Private Bank there are more male

customers, and less number of female customers. But reason of less female customers could be due to the

fact that the female customers may not like to come to bank and their male relatives operate their account

for them. Similarly in case of Public banks 59% customers are male and rest are female. Though here the

number is comparatively more females but still the overall emphasis is made on the basis of male

respondent.

Page 30

30

The figure shown below is related to the occupation of the respondents of both private and public banks.

It is understood from the above that 44% of the customers that are surveyed is doctors. The next higher

number of response came from student and software engineer. Professors are the next major customers in

our survey and lastly MBA graduate and Executive is also the part of the survey. This customers in this

survey is quite diversified and thus the analysis is done from the view point of the major chunks from the

society.

The respondents from the public banks are also diversified with people from medical field, executive,

MBA, student etc taking part in the survey. Majority of the respondents here are doctors and students.

Since we find most of the student having SBI loan account and as it one of our banks to be surveyed, we

found more response from the student side. 15% respondents are professors and 23% are software

engineers. This shows the sample is diversified from all sections of society.

Page 31

31

• Fig. 1 shows that 100% customers of private banks are either satisfied or very satisfied with efficient account handling by these banks.

They feel that private banks manage accounts efficiently without mistakes. In case of public banks 95% customers feel that these banks

manage accounts efficiently without mistakes. And 5% customers in public banks are dissatisfied with the accounts handling by the banks

and feel that. This makes private banks working more efficiently in handling accounts.

• Fig. 2 shows that almost 65% customers of private banks are satisfied and they say that they bank personnel ask apologies for their

mistakes. 21% are dissatisfied with this behavior and remaining 14% customers have no experience in this regard. In case of public banks

around 63% customers are satisfied and they say that they bank personnel ask apologies for their mistakes. 21% are dissatisfied with this

behavior and remaining 16% customers have no experience in this regard.

Section 2: Bivariate analysis

Managing accounts

In this section we have tried to relate a few variable and presented in graphs and distributions

Page 32

32

• Fig. 3 shows that in private banks, 65% customers claim that the charges are explained more efficiently regarding accounts and prevailing

in the market. Around 32% customers say they are dissatisfied and 3% have no experience regarding this. In case of public banks also 65

% customers’ feels satisfied and 27% feels that they are dissatisfied but 8% customers have no experience about it. This shows that private

banks customers less satisfied but they have at least experienced this more than public banks.

Page 33

33

Handling Queries:

• Fig. 4 shows that 68% customers of private banks are satisfied with the staff response in taking time to answer their call regarding queries.

24% customers say that they are dissatisfied with it and 8% have no experience in this regard. In case of public banks 63% customers says

that they are satisfied with the staff response in taking time to answer their call regarding queries. 31% customers say that they are

dissatisfied with it and 6% have no experience in this regard.

• Fig.5 shows that 79% customers of private banks are satisfied with the way in which staff answers their call. 15% are dissatisfied and 6%

customers have no experience regarding it. In case of public banks 67% customers are satisfied with the way in which staff answers their

call. 28% are dissatisfied and 5% customers have no experience regarding it.

This shows that private banks have higher satisfaction level in both time taken and way in which the staff answers the customer call.

Page 34

34

• Fig. 6 shows that in private banks, 76% customers say that the staff voice is more clear and are satisfied. 17% customers says that they are

dissatisfied and 7% says that they have not experienced this any time. In case of public banks, 69% customer says that that the staff voice

is more clear and are satisfied. 27% customers says that they are dissatisfied and 4% says that they have not experienced this any time.

• Fig. 7 shows that 62% customers in private banks say that they feel easy to approach the right person in bank and are satisfied. 32% says

that they are dissatisfied with this service and 6% says that they don have any experience related to it. In case of public banks 58%

customers says that they feel easy to approach the right person in bank and are satisfied. 40% says that they are dissatisfied with this

service and 2% says that they don have any experience related to it.

This shows that private banks are giving more satisfaction to customers in terms of staff clearness of voice and ease of reaching them.

Page 35

35

• Fig. 8 shows that a 71% customer of private banks feels that enquiry is understood by the staff easily and they are satisfied with it. 25%

customers are dissatisfied and 4% have no experience regarding it. In case of public banks 66% customers are satisfied with the quick

response in answering their enquiry. And rest 34% customers are dissatisfied. There is no customers who have not experienced this

service. This shows that in public banks enquiry is very frequent and customers are either satisfied with it or dissatisfied.

• Fig. 9 shows that in private banks around 58% customers are satisfied with the time responding to letters/mails. 29% customers are

dissatisfied and 13% customers have no experience in this regard. In case of public banks, 52% customers are satisfied with the time

responding to letters/mails. 31% customers are dissatisfied and 17% customers have no experience in this regard.

Page 36

36

• According to Fig. 10, 76% customers in private banks say that the letters are easily understood. 12% are dissatisfied and 12% have no

experience in it. But none of the respondents showed very high dissatisfaction in this regard. In case of public banks, 61% customers in

private banks say that the letters are easily understood. 23% are dissatisfied and 16% have no experience in it.

• According to fig. 11, 71% customers are satisfied and highly satisfied with the clarity in which the enquiry is answered. 19% are

dissatisfied with the service but very few are highly dissatisfied. 10% customers say that they have no experience in it. In case of public

banks, 54% customers say that they are satisfied and highly satisfied with the clarity in which the enquiry is answered. 29% are

dissatisfied with the service but very few are highly dissatisfied. 17% customers say that they have no experience in it.

This shows that in either of the services customers are not highly dissatisfied with the performance of the private banks.

Page 37

37

About the branch:

• Fig. 12 shows that 81% customers of private banks feels that level of privacy is high in their banks. Out of which 35% are very satisfied

with this service. 15% feels dissatisfied and 4% has no experience related to it. But no customers are very dissatisfied with this particular

parameter and are fine this service that their bank provides. In case of public banks we find that 82% customers feels that level of privacy

is high in their banks. 10% feels dissatisfied and 8% has no experience related to it. But no customers are very dissatisfied with this

particular parameter and are fine this service that their bank provides.

This shows that the customers are satisfied with the level of privacy that the banks provides to them as this might be one reason before choosing to

open their account in a bank.

Page 38

38

• According to fig. 13, 85% customers of private banks are actually satisfied with the cleanliness that the bank maintains. 13% says that they

are not satisfied with this service and only 2% says that have not noticed it. In case of public banks, only 69% customers are satisfied with

the cleanliness activity of their banks. And remaining 31% customers are dissatisfied with this service.

• 63% customers of private banks are actually satisfied with the queuing system followed in their banks which consumes most of their time

normally. 29% customers are dissatisfied and 8% customers have not experienced it. In case of public banks only 42% customers feels that

they are satisfied with the queuing system followed in their banks which consumes most of their time normally. 57% customers are

dissatisfied and 1% customers have not experienced it.

This shows that customers of private sector banks are more happy with the cleanliness service and the queuing time which their bank provides.

Page 39

39

About the staff:

• Fig. 15 shows that 83% private bank customers feel that the staffs are knowledgeable about the services they offer. And remaining 17%

are dissatisfied with it. In case of public banks, 74% customers feel that the staffs are knowledgeable about the services they offer. 25%

are dissatisfied with it and 1% have customers have not experienced it.

• Fig. 16 shows that 71% customers of private banks feel that staffs are able to give good advice. 23% are dissatisfied with it and 6% have

not experienced it. In case of public banks, 65% customers are satisfied with staff giving good advice. 32% are dissatisfied and 3% have

not experienced it.

This shows that private banks again hold high in the customers mind in terms of their staff with good knowledge and ability to give good advice.

Page 40

40

• Fig. 17 shows that 65% customers of private banks are satisfied and highly satisfied with the staff giving 100% attention to them.

Remaining 35% are dissatisfied with it. In case of public banks, 47% customers of public banks feel that they are satisfied with the staff

giving 100% attention to them. Remaining 50% are dissatisfied with it.

• Fig. 18 shows that 76% customers of private banks feel that the staff is happy assisting them. 23% feel that they are dissatisfied and rest

1% have not noticed this before. In case of public banks, 55% customers feel that staff is happy assisting them. Remaining 45% feel that

they are dissatisfied.

This shows that again more number of customers of private banks are much satisfied with staff giving full attention and pleased in assisting them.

Page 41

41

• Fig. 19 shows that 75% customers of private banks feel that staffs are smart and professional whereas 24% feels dissatisfied with it and

1% have not noticed it. In case of public banks 52% customers say that staffs are smart and professional whereas 47% feels dissatisfied

with it and 1% have not noticed it.

• Fig. 20 shows that 79% customers of private banks are satisfied with the ATM service of their respective banks whereas 21% are

dissatisfied. Incase public banks 51% are satisfied and 49% are dissatisfied with it. This suggests that almost half of the customers of the

public banks are not satisfied with the ATM service of their bank.

Page 42

42

• Fig. 21 shows that 65% customers of private banks have actually recommended their bank to a friend or relative whereas in case of public

banks, 68% customers have actually recommended their bank to a friend or relative.

• Fig. 22 shows that 92% customers of private banks are satisfied with the overall bank services provided to them whereas only 8% are

dissatisfied with it. In case of public bank 84% customers are satisfied with the overall bank services provided to them whereas 16% are

dissatisfied with it.

Page 43

43

• Fig. 23 shows that 37% say that the services of private banks have got better in last few years. 57% say that it has stayed same and only

6% say that it has got worse in last few years. In case of public banks, 45% customers say that it has got better, 47% say that it has stayed

same and 8% say that it has got worse.

From the findings reported above using the bivariate analysis we find that the customers of the private banks are more satisfied with the services

provided by their private banks as compared to public banks so far as several services provided by the banks are concerned.

Page 44

44

Section 3: Regression Analysis:

In this section, we have used Regression analysis to examine the relationship between overall satisfaction

of the customers and few variables such as Staff being smart and professional, Staff giving full attention

to customers, Bank handling accounts efficiently & Satisfied with the bank’s ATM service

Regression analysis is done to find a possible relationship with the different variables used in the

customer satisfaction survey. To obtain a general linear equation for the variables, we have tried to do it

for all banks as a whole, then with private banks and then with public banks. The analysis has been shown

below.

All banks:

A priori reasoning: There is a positive relation with overall satisfaction of the customers with the bank

and few variables such as Staff being smart and professional, Staff giving full attention to customers,

Bank handling accounts efficiently & Satisfied with the bank’s ATM services.

Y is the Dependent variable and X is the Independent variable.

Y= Overall satisfaction with the bank service.

X1= Staff are smart and professional

X2= Staff give full attention to customers

X3= Bank handles accounts efficiently

X4= Satisfaction with the bank’s ATM service

After applying the data in SPSS we got the following result:

Page 45

45

The R square is found to be 0.388 which is low but it is positive and suggests that 38% of the variability

can be explained through this.

Page 46

46

The F value is 30 which says that there is a high degree of association between the overall satisfaction of

the banks services and the Staff being smart and professional, Staff giving full attention to customers,

Bank handling accounts efficiently & Satisfied with the bank’s ATM service.

The standardized beta coefficients for variable i.e., able to give full attention to customers and handling

accounts efficiently are higher which shows that they are having more explanatory power as compared to

others.

The significance level for the entire variables as shown in the coefficient table suggests that it is

significant (more that 0.1).

The equation formed is:

Y = 1.280 + 0.131 X1 + 0. .256 X2 + 0.258 X3 + 0.058 X4

PRIVATE BANKS:

A priori reasoning: There is a positive relation with overall satisfaction of the customers with the bank

and few variables such as Staff being smart and professional, Staff giving full attention to customers,

Bank handling accounts efficiently & Satisfied with the bank’s ATM services.

Same variable are been taken so as to make comparative analysis of all banks with each of private and

public banks.

Y is the Dependent variable and X is the Independent variable.

Y= Overall satisfaction with the bank service.

X1= Staff are smart and professional

X2= Staff give full attention to customers

X3= Bank handles accounts efficiently

Page 47

47

X4= Satisfaction with the bank’s ATM service

Page 48

48

The R square is found to be 0.357 which is low but it is positive and suggests that 35.7% of the variability

can be explained through this.

The F value is 13 which says that there is a little lower degree of association between the overall

satisfaction of the banks services and the Staff being smart and professional, Staff giving full attention to

customers, Bank handling accounts efficiently & Satisfied with the bank’s ATM service.

The standardized beta coefficients for variable i.e., able to give full attention to customers and handling

accounts efficiently are higher which shows that they are having more explanatory power as compared to

others

The significance level for the two variables that is Staff give full attention to customers and Bank handles

accounts efficiently are having significance level below 0.1 and says that they are significant enough to

explain the variability. Whereas two other variables have high significance level suggesting that they are

not significant.

Page 49

49

The equation formed is:

Y = 1.637 + 0.074X1 + 0.286 X2 + 0.228 X3 + 0.025X4

PUBLIC BANKS:

A priori reasoning: There is a positive relation with overall satisfaction of the customers with the bank

and few variables such as Staff being smart and professional, Staff giving full attention to customers,

Bank handling accounts efficiently & Satisfied with the bank’s ATM services.

Same variable are been taken so as to make comparative analysis of all banks with each of private and

public banks.

Y is the Dependent variable and X is the Independent variable.

Y= Overall satisfaction with the bank service.

X1= Staff are smart and professional

X2= Staff give full attention to customers

X3= Bank handles accounts efficiently

X4= Satisfaction with the bank’s ATM service

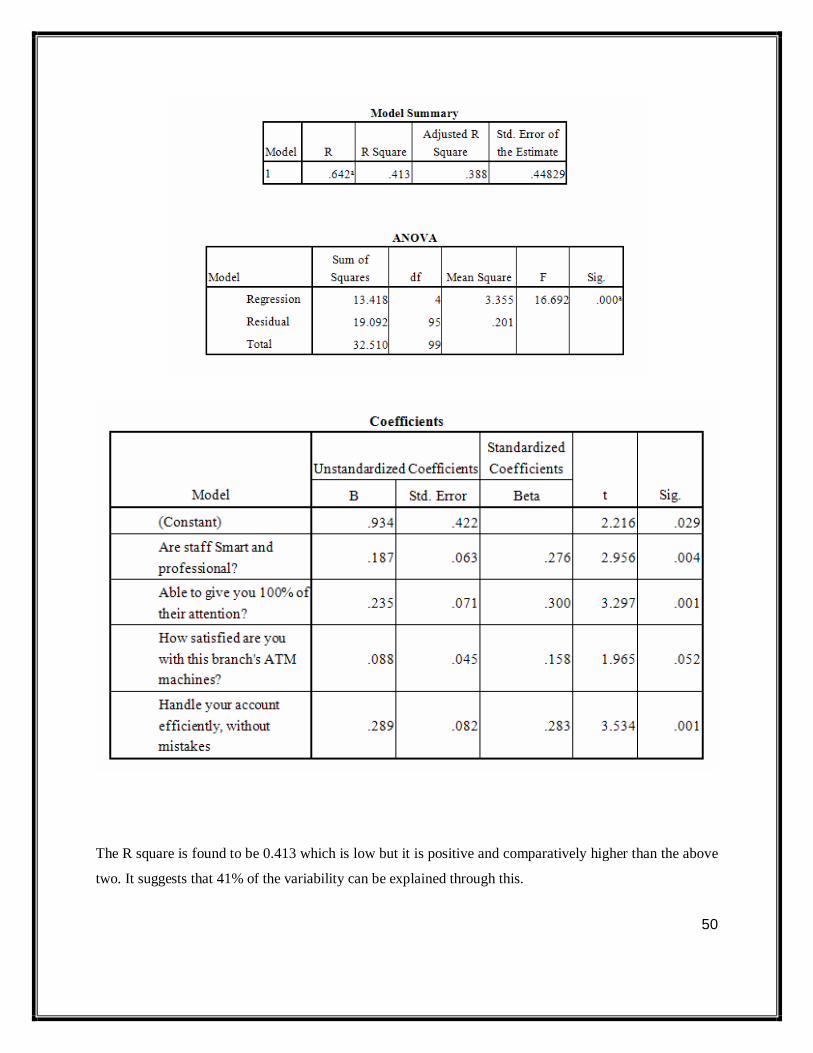

After applying the data in SPSS we found the following:

Page 50

50

The R square is found to be 0.413 which is low but it is positive and comparatively higher than the above

two. It suggests that 41% of the variability can be explained through this.

Page 51

51

The F value is 16 which says that there is a little lower degree of association between the overall

satisfaction of the banks services and the Staff being smart and professional, Staff giving full attention to

customers, Bank handling accounts efficiently & Satisfied with the bank’s ATM service.

The standardized beta coefficients for variable i.e., able to give full attention to customers and handling

accounts efficiently are higher which shows that they are having more explanatory power as compared to

others

The significance level for the entire variables as shown in the coefficient table suggests that it is

significant (more that 0.1).

The equation formed is:

Y = 0.934 + 0.187 X1 + 0.235 X2 + 0.289 X3 + 0.088 X4

CONCLUSION:

After doing the regression analysis of the overall banks and both private and public banks, we have

observed that in the two sets of banks the variables which determine the overall satisfaction are Staff are

smart and professional, Staff give full attention to customers, Bank handles accounts efficiently &

Satisfaction with the bank’s ATM service.

Page 52

52

Section 4: Factor Analysis:

In this section, we have tried to carve out a few factors (latent variables) from a set of manifest variables.

The questionnaire was canvassed with all the sample respondents to find out there perceptions on the

services of the banks. There perceptions were measured using a likert scale of 1 to 5 points. As many as

22 variables were included as manifest variables in the questionnaire. As mentioned earlier these data

were used to run a factor analysis with the principal component method. This suggested that the first

factor carved out in the analysis is the most important one and the other factors are relatively less

important in the descending order. This analysis was done for all the banks and the two sets of banks

separately. The results (output) of the factor analysis are appended in Annexure 3. However the summary

of the factor output is presented and analysed in the following:

Page 53

53

All Banks:

The Eigen value is taken as one and the cut off point for factors is 0.33. The factor loadings with respect

to each of the manifest variable is mentioned within brackets. The factor name has been suggested and

mention at the top of the table which are the latent variables (factors). There are 5 factors that are found

for all banks clubbing together. They are:

Page 54

54

1. Staff services in banks:

This factor suggest that people expect that staffs in banks should knowledgeable about the

services, able to give good advice, give full attention to customers, assist please fully and should

be smart & professional. All those criteria listed in the questionnaire are considered important by

the customers and they are satisfied by these services. It is true in fact that any customers will

need that they should get full attention, the bank staff should be knowledgeable and they should

give good advice and must be smart and professional.

2. Handling queries in bank:

This factor says that while any queries are being asked through phone, the customers looks at

time in which it is answered, way in which it is answered, clearness in its voice and if they want

to approach for any query, how easily the person is approachable. These were asked in the

questionnaire as handling queries and 8 variables were given but after doing the analysis we

found that customers feel that only these 4 variables are more impotant if we want to measure the

level of satisfaction in handling queries.

3. Responding to mails:

This factor shows that when a customer ask any query through mail or letters, he considers the

response time, easy in understanding mail, & Clarity in answering the enquiry. Though these

factor were under handling queries in the questionnaire but after doing the factor analysis we

found that customers considers these variables as different and it is more preferred if we consider

it separately. So we have named it as “responding to mails”.

4. In- the Branch services:

This factor shows what customers looks when he enters the branch. He likes to see the cleanliness

in branch, less queuing time, efforts to be made to reduce the queuing time (like token system),

and quick response of the cashier to the customers instructions. Though level of privacy was also

included in the questionnaire but the customers do not feel it important in the in-branch services.

Page 55

55

5. Privacy and managing accounts:

This factor says that customer also look for privacy in the bank. He looks for handling accounts

efficiently, apologies for mistakes and explaining charges more clearly. This factor makes the

customer more satisfied with the bank services with relation to managing accounts and level of

privacy.

PRIVATE BANKS:

The Eigen value is taken as one and the cut off point for factors is 0.33. The factor loadings with respect

to each of the manifest variable is mentioned within brackets. The factor name has been suggested and

mention at the top of the table which are the latent variables (factors). There are 5 factors that are found

for private banks clubbing together. They are:

Page 56

56

1. Staff services in banks:

This factor suggests that people expect that staffs in banks should knowledgeable about the

services, able to give good advice, give full attention to customers, assist please fully and should

be smart & professional. All those criteria listed in the questionnaire are considered important by

the customers and they are satisfied by these services. These factors are same as mentioned in the

overall bank factor analysis. This shows that the private banks customers who are the important

part of banking sector also look for these variables to see the staff services.

2. Handling queries in bank:

This factor suggests that while any queries are being asked through phone, the customers looks at

time in which it is answered, way in which it is answered & clarity in its voice These were asked

in the questionnaire as handling queries and 8 variables were given but after doing the analysis