27

1 Yale School of Management Price Impact Costs and the Limit of Arbitrage Zhiwu Chen Werner Stanzl Masahiro Watanabe

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 0 times |

1

Yale School of Management

Price Impact Costs and the Limit of Arbitrage

Zhiwu ChenWerner Stanzl

Masahiro Watanabe

Arbitrageur PriceAnomalies

3

Yale School of Management

Market Anomalies

Size effect (Banz, 1981; Fama & French, 1993)Smaller size, larger returns Long small-size & short big-size stocks

B/M (value) effect (Basu, 1983; FF 1993Lakonishok et al., 1994; LaPorta et al.,

1997)Higher B/M, greater returns Long high-B/M & short low-B/M stocks

Momentum (Levy, 1967; Jegadeesh & Titman, 1993 & 2001)Return continuation Long past winners & short past losers

4

Yale School of Management

Empirical Price Impact Literature

Linear Price ImpactBreen, Hodrick & Korajczyk (2001)Sadka (2002)

Nonlinear (Concave) Price ImpactHasbrouck (1991)Hausman, Lo & MacKinlay (1992)Keim and Madhavan (1996)Knez and Ready (1996)

5

Yale School of Management

Data

TAQ Price impact estimation1/1993-6/1993: Oldest available

CRSP Return & portfolio formation7/1963-12/2001: Covers Fama & French(1993) and Jegadeesh & Titman (1993)

Compustat Accounting information4th Quarter, 1962 - 4th Qtr, 2001

TASSEstimation of actual hedge fund sizeCovers 1330 hedge funds as of 5/2000

6

Yale School of Management

Estimation of Price-Impact Function

Price Impact

where Qt = Quote midpoint at transaction time t

Vt = Dollar trading volume at t

Nonlinearity b/w log ( = 0) & linear ( = 1) functions inclusive

The only method that can be applied to almost all stocks without overfitting to outliers

Nonlinear least squares, purchases and sales separately

Matching & trade direction: Lee & Ready (1991) Method

Discard the top one-percentile trades

tt

t

ttt

Vba

Q

QQPI

11

7

Yale School of Management

Overfitting problem except for the Box-Cox model

Example: FHTFigure 1

8

Yale School of Management

Estimated Price ImpactsFigure 2

9

Yale School of Management

GE KO BONT CSII S INGR MIKE

(a) BuysNobs 23,265 23,157 518 1,212 10,826 2,329 4,704 aB (×10-3) -0.020 -0.060 -5.28 -3.89 -0.13 -0.49 -0.78

(-1.34) (-3.71) (-2.75) (-5.11) (-3.07) (-1.99) (-6.69)bB (×10-4) 0.00308 0.0109 6.53 4.91 0.0379 0.770 0.940

(2.27) (3.20) (3.04) (5.69) (2.27) (2.77) (7.91)B 0.468 0.410 0.000 0.000 0.302 0.000 0.000

(12.51) (15.05) (--) (--) (7.97) (--) (--)

(b) SellsNobs 25,543 25,029 523 692 16,368 1,710 4,362 aS (×103) 0.018 -0.020 -1.37 -2.83 -0.030 -0.87 -0.30

(2.49) (-1.50) (-0.70) (-2.47) (-1.65) (-3.05) (-2.36)bS (×104) 0.000774 0.00406 2.74 3.72 0.00392 1.20 0.47

(1.95) (3.13) (1.30) (3.01) (2.38) (3.83) (3.68)S 0.575 0.499 0.000 0.000 0.502 0.000 0.000 (13.17) (18.11) (--) (--) (13.79) (--) (--)

Estimates for Individual StocksTable 2

10

Yale School of Management

Box-Cox vs. Linear PI FunctionsFigure 3

11

Yale School of Management

Linear vs. Nonlinear PI FunctionsTicker Symbol

GE KO BONT CSII S INGR MIKENobs

23,265

23,157

518

1,212

10,826

2,329

4,704

B (×10-4) 0.614 0.822 3.464 1.288 1.394 1.467 1.200

(24.22) (21.81) (1.11) (1.16) (23.12) (3.57) (6.83)

B (×10-8) 0.0455 0.0829 1.075 2.657 0.0631 0.2690 0.0403

(37.04) (42.43) (0.90) (4.02) (27.56) (1.77) (1.64)

(a) Price impact from $50,000 trade (bp) Linear 0.84 1.24 8.84 14.57 1.71 2.81 1.40 Box-Cox 0.83 1.62 17.85 14.23 1.87 3.43 2.37 Difference 0.01 -0.38 -9.01 0.35 -0.16 -0.62 -0.97

(b) Price impact from $300,000 trade (bp) Linear 1.98 3.31 35.72 80.99 3.29 9.54 2.41 Box-Cox 2.20 4.05 29.55 23.02 4.24 4.81 4.05 Difference -0.22 -0.74 6.17 57.97 -0.96 4.73 -1.65

Table 3

12

Yale School of Management

Table 4

For both buys and sells,Slope coefficient b decreases with sizeConcavity coefficient has a U-shape

Portfolio PI Functions by Size

Size aB(x10-3) bB(x10-4) B aS(x10-3) bS(x10-4) SSmall -1.98 4.56 0.245 -0.16 2.41 0.285

2 -1.95 3.15 0.198 -1.16 2.29 0.206

3 -1.69 2.48 0.155 -1.13 2.03 0.160

4 -1.65 2.53 0.121 -1.13 2.03 0.157

5 -1.53 2.44 0.113 -1.10 2.00 0.148

6 -1.59 2.33 0.108 -1.41 2.26 0.108

7 -1.52 2.10 0.108 -1.24 1.89 0.137

8 -1.22 1.49 0.133 -1.19 1.61 0.119

9 -1.00 1.11 0.168 -0.99 1.21 0.162

Big -0.19 0.22 0.268 -0.25 0.35 0.239

13

Yale School of Management

Figure 4

Buy trades have positive price impacts, sells negativeAbsolute price impact increases with the size of tradePrice impact monotonically decreases with firm size

Price Impacts by Size Decile

14

Yale School of Management

Implementation of Strategies

Set up a long-short portfolio based on each strategyMeasure excess return after cost, where volume to

compute PIs converted to year 1993 dollarsSince price impact increases in fund size, there is a

maximal fund size at which

excess return after cost = 0The maximal fund size reported in year 2001 dollars

15

Yale School of Management

Portfolios are formed annually, semiannually, or quarterly

Value of long position = Value of short position

Rebalance when stocks are either added to or dropped from a

portfolio; also when weights change

Commisions: 15 bp for purchases and sales

25 bp for short-selling

Short-sale rebate: 80% of Fed Fund Rate

Maximum $ volume / trade: 1% of market cap

Maximum holding: 5% of market cap

Investment Strategy Criteria

16

Yale School of Management

Initial fund size: 0

At the beginning of period t1, investbt = t-1 – PILt – PISt – TCLt – TCSt

Volume to compute PIs converted to year 1993 dollarsAt the end of period t,

t = (1 + rl,t – rs,t+ 0.8 rFF,t) bt Excess return after cost

Rt = t / t-1 – 1 – rFF,t Break-even fund size

Below, 0 is reported in year 2001 dollars

}0)(RT

1|0sup{

1 0t0 T

t

Portfolio Accounting

17

Yale School of Management

Size StrategyMean

Excess Standard Sharpe Return (t-stat) Deviation Max / Min Ratio

Size 0.067 (1.36) 0.265 0.733 / -0.369 0.252Strategy [0.058] [(1.46)] [0.247] [0.733 / -0.369] [0.236]CRSP 0.092 (1.67) 0.295 0.972 / -0.473 0.311

Equally Weighted [0.093] [(2.24)] [0.259] [0.972 / -0.473] [0.358]

Arbitrage MeanFund Excess Standard Sharpe Mean Price Mean Mean Price Mean Size Return (t-stat) Deviation Max / Min Ratio Impact Turnover Impact Turnover1M 0.059 (1.21) 0.263 0.722 / -0.373 0.225 0.004 0.661 0.001 0.542

[0.051] [(1.28)] [0.245] [0.722 / -0.373] [0.207] [0.004] [0.649] [0.001] [0.530]10M 0.053 (1.10) 0.261 0.714 / -0.376 0.204 0.008 0.663 0.001 0.544

[0.045] [(1.14)] [0.244] [0.714 / -0.376] [0.185] [0.008] [0.651] [0.001] [0.533]100M 0.043 (0.90) 0.259 0.698 / -0.381 0.167 0.016 0.667 0.002 0.549

[0.036] [(0.91)] [0.242] [0.698 / -0.381] [0.148] [0.016] [0.655] [0.002] [0.538]500M 0.032 (0.68) 0.256 0.680 / -0.386 0.126 0.025 0.671 0.003 0.554

[0.025] [(0.66)] [0.239] [0.680 / -0.386] [0.107] [0.023] [0.659] [0.003] [0.543]1B 0.026 (0.56) 0.254 0.670 / -0.389 0.103 0.029 0.674 0.004 0.557

[0.020] [(0.52)] [0.237] [0.670 / -0.389] [0.084] [0.028] [0.661] [0.003] [0.546]5B 0.008 (0.18) 0.249 0.637 / -0.397 0.034 0.043 0.682 0.005 0.566

[0.004] [(0.10)] [0.233] [0.637 / -0.397] [0.016] [0.040] [0.668] [0.005] [0.554]7B 0.004 (0.08) 0.248 0.628 / -0.398 0.016 0.046 0.684 0.006 0.568

[0.000] [(-0.01)] [0.232] [0.628 / -0.398] [-0.001] [0.043] [0.670] [0.005] [0.556]9B 0.000 (0.01) 0.247 0.621 / -0.400 0.001 0.049 0.685 0.006 0.570

[-0.003] [(-0.09)] [0.231] [0.621 / -0.400] [-0.015] [0.045] [0.671] [0.005] [0.558]10B -0.001 (-0.03) 0.247 0.618 / -0.401 -0.005 0.050 0.686 0.006 0.570

[-0.005] [(-0.13)] [0.230] [0.618 / -0.401] [-0.021] [0.047] [0.672] [0.006] [0.559]

Long Portfolio Short Portfolio

(b) Equally Weighted, with Costs

(a) Equally Weighted, without Costs

Table 5

Huge, but is this really attainable?

18

Yale School of Management

Realistically implemented size strategies will not accommodate more than several hundred million dollars

Trading and Holding RestrictionsFigure 5

19

Yale School of Management

The potential benefit of “fine tuning” does not cover higher price impact costs

Higher Rebalancing FrequenciesFigure 6

20

Yale School of Management

Book-to-Market StrategyTable 7

MeanExcess Standard Sharpe Return (t-stat) Deviation Max / Min Ratio

B/M 0.093 (3.57) 0.139 0.320 / -0.234 0.664Strategy [0.093] [(3.76)] [0.152] [0.320 / -0.272] [0.610]CRSP 0.092 (1.67) 0.295 0.972 / -0.473 0.311

Equally Weighted [0.093] [(2.24)] [0.259] [0.972 / -0.473] [0.358]

Arbitrage MeanFund Excess Standard Sharpe Mean Price Mean Mean Price Mean Size Return (t-stat) Deviation Max / Min Ratio Impact Turnover Impact Turnover1M 0.061 (2.30) 0.142 0.296 / -0.254 0.428 0.013 1.030 0.012 0.984

[0.061] [(2.45)] [0.153] [0.296 / -0.304] [0.397] [0.013] [0.970] [0.012] [0.985]10M 0.037 (1.37) 0.145 0.280 / -0.268 0.254 0.024 1.046 0.022 0.999

[0.038] [(1.53)] [0.155] [0.280 / -0.320] [0.248] [0.022] [0.985] [0.021] [0.999]50M 0.013 (0.45) 0.151 0.267 / -0.280 0.084 0.035 1.067 0.032 1.018

[0.017] [(0.64)] [0.159] [0.267 / -0.333] [0.104] [0.032] [1.001] [0.030] [1.014]90M 0.002 (0.07) 0.155 0.262 / -0.305 0.013 0.040 1.077 0.036 1.028

[0.007] [(0.28)] [0.162] [0.262 / -0.337] [0.045] [0.036] [1.010] [0.034] [1.022]100M 0.000 (0.00) 0.156 0.262 / -0.313 0.000 0.040 1.079 0.037 1.030

[0.006] [(0.21)] [0.163] [0.262 / -0.338] [0.035] [0.037] [1.012] [0.035] [1.023]300M -0.023 (-0.73) 0.170 0.254 / -0.418 -0.135 0.051 1.110 0.047 1.057

[-0.014] [(-0.48)] [0.174] [0.254 / -0.418] [-0.079] [0.046] [1.035] [0.043] [1.045]

(a) Equally Weighted, without Costs

(b) Equally Weighted, with Costs

Long Portfolio Short Portfolio

21

Yale School of Management

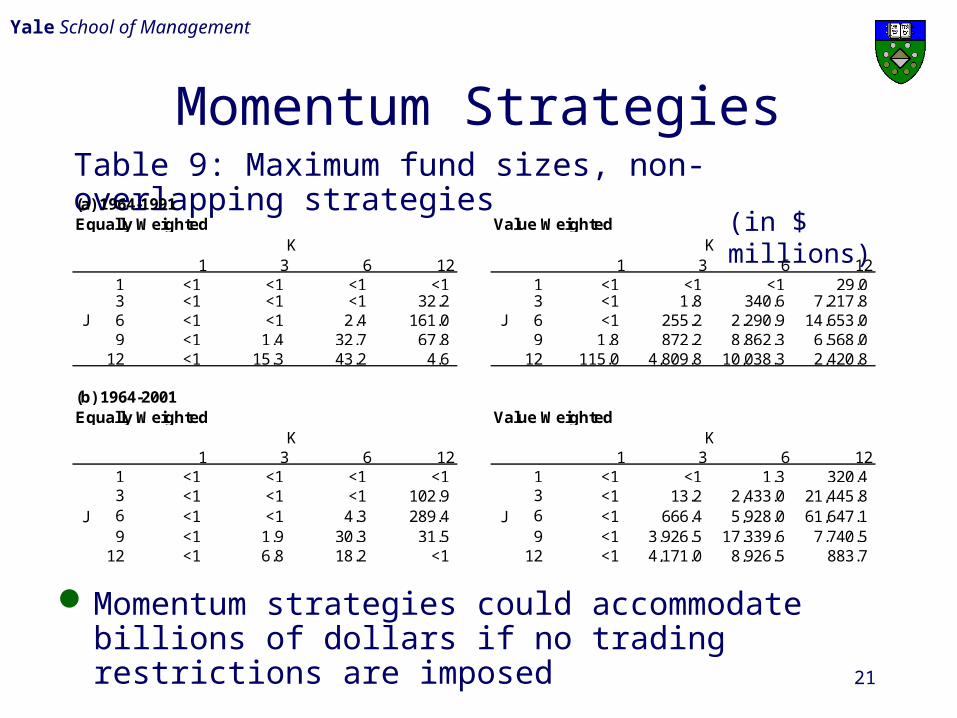

Momentum StrategiesTable 9: Maximum fund sizes, non-overlapping strategies

Momentum strategies could accommodate billions of dollars if no trading restrictions are imposed

(in $ millions)

1 3 6 12 1 3 6 121 <1 <1 <1 <1 1 <1 <1 <1 29.0 3 <1 <1 <1 32.2 3 <1 1.8 340.6 7,217.8

J 6 <1 <1 2.4 161.0 J 6 <1 255.2 2,290.9 14,653.0 9 <1 1.4 32.7 67.8 9 1.8 872.2 8,862.3 6,568.0

12 <1 15.3 43.2 4.6 12 115.0 4,809.8 10,038.3 2,420.8

1 3 6 12 1 3 6 121 <1 <1 <1 <1 1 <1 <1 1.3 320.4 3 <1 <1 <1 102.9 3 <1 13.2 2,433.0 21,445.8

J 6 <1 <1 4.3 289.4 J 6 <1 666.4 5,928.0 61,647.1 9 <1 1.9 30.3 31.5 9 <1 3,926.5 17,339.6 7,740.5

12 <1 6.8 18.2 <1 12 <1 4,171.0 8,926.5 883.7

KK

KValue WeightedEqually Weighted

(a) 1964-1991

Equally Weighted Value Weighted(b) 1964-2001

K

22

Yale School of Management

At a glance…Table 6 Rebalancing (in $ millions)

frequency Equally Weighted Value WeightedSize Strategy Annual 9,173.1 421.0

[6841.4] [129.8]Semiannual 3,812.7 173.2

[4384.0] [75.0]Quarterly 634.0 16.6

[827.3] [8.2]B/M Strategy Annual 100.17 <1

[158.5] [<1]Semiannual 25.78 <1

[69.2] [<1]Quarterly 12.01 <1

[23.0] [<1]Size-B/M Annual 768.6 758.9 Combined [1395.9] [636.5]Strategy Semiannual 294.6 208.6

[946.9] [325.0]Quarterly 44.4 17.7

[175.1] [37.4]Momentum Annual 4.6 2,420.8 Strategy [<1] [883.7]

Semiannual 2.4 2,290.9 [4.3] [5928.0]

Quarterly <1 1.8 [<1] [13.2]

23

Yale School of Management

Size-B/M Combined Strategy (Table 10)Smaller break-even fund sizes than the size-only strategy

because of higher turnover in the long positionBecause of this and the smaller # stocks in both the long

and short positions, the 1% trade-size and 5% position-size restrictions will make the fund sizes even smaller than those for size-only strategies in Figure 5

No-small-stock B/M Strategy (Table 11)Restricts the available stocks to only those in the biggest 5

decilesMediocre performance, due to much lower returns before

cost than with all stocks

Combined/No-small-stock Strategies

24

Yale School of Management

No-small-stock Momentum Strategy

Arbitrage MeanFund Excess Standard Sharpe Mean Price Mean Mean Price Mean Size Return (t-stat) Deviation Max / Min Ratio Impact Turnover Impact Turnover10M 0.036 (0.94) 0.203 0.486 / -0.387 0.178 0.006 1.798 0.006 1.786

[0.037] [(0.84)] [0.269] [0.809 / -0.816] [0.138] [0.006] [1.765] [0.006] [1.778]100M 0.026 (0.69) 0.201 0.469 / -0.395 0.130 0.011 1.805 0.010 1.794

[0.027] [(0.62)] [0.266] [0.795 / -0.818] [0.103] [0.010] [1.773] [0.010] [1.786]1B 0.004 (0.12) 0.199 0.442 / -0.462 0.022 0.020 1.826 0.020 1.816

[0.008] [(0.19)] [0.264] [0.777 / -0.820] [0.030] [0.019] [1.790] [0.019] [1.804]3B -0.025 (-0.66) 0.198 0.430 / -0.561 -0.124 0.033 1.857 0.034 1.847

[-0.014] [(-0.33)] [0.264] [0.774 / -0.821] [-0.055] [0.028] [1.813] [0.029] [1.828]

Long Portfolio Short Portfolio

(f) Value Weighted, with Costs and 1% Market-Capital Per-trade Restriction

Table 12, VW 12/12 non-overlapping strategy

Still works.Both the EW & VW strategies accommodate b/w $1

and 3 billions with the 1% trade-size restriction.

25

Yale School of Management

Actual Hedge Fund SizeTable 13

Size (in millions of dollars)Style #funds %total Mean Minimum Maximum SumTop down macro 362 27.4% 241.4 0.0147 4,122.0 87,396.0Bottom up approach 694 52.6% 195.0 0.1898 23,474.4 135,306.2Short selling 524 39.7% 201.1 0.0147 4,618.1 105,362.6Long bias 443 33.6% 181.1 0.3780 23,474.4 80,217.2

Market neutral 313 23.7% 152.0 0.0147 4,122.0 47,563.9Opportunities 498 37.8% 139.0 0.1100 23,474.4 69,206.0Relative value 360 27.3% 183.0 0.0147 10,194.0 65,862.1Arbitrage 408 30.9% 137.3 0.0602 23,474.4 56,018.6Discretionary 275 20.8% 101.1 0.0147 23,474.4 27,803.3Trend follower 201 15.2% 72.7 0.3384 3,958.9 14,603.4Technical 401 30.4% 74.9 0.0147 23,474.4 30,036.8Fundamental 702 53.2% 169.5 0.1898 4,618.1 118,957.1Systematic 323 24.5% 83.4 0.0602 10,194.0 26,940.0Diverse 354 26.8% 140.2 0.0147 23,474.4 49,646.3Other 153 11.6% 98.6 0.0147 23,474.4 15,087.2Total 1319 100.0% 139.9 0.0147 23,474.4 184,492.4

26

Yale School of Management

Price impact reduces returns substantially

For size and B/M strategies, only about one hundred million

dollars can be accommodated under realistic trading

restrictions

This is marginal compared to the actual hedge fund size

However, some momentum strategies may be implemented

profitably with about one billion dollars

Market is minimally efficient to allow for size & B/M

anomaly; persistence of momentum is still a challenge

Conclusions

27

Yale School of Management

“Working” the order

VWAP

Time variation in liquidity suggests change

in price impacts

Change in other costs (bid-ask spread, short

sale carry cost, transactions fees)

Future Research