44

Yara International ASA 2018 first quarter results 20 April 2018

Yara International ASA 2018 first quarter results 20 April 2018

0

5

Jan'16 Mar May Jul Sep Nov Jan '17 Mar May July Sep Nov Jan'18 Mar'18

TRI (Total recordable injuries 12-month rolling)1

Safe operations is our first priority

1) TRI: Total recordable injuries, lost time (absence from work), restricted work and medical treatment cases per one million work hours.

IR – 20 April 2018 2

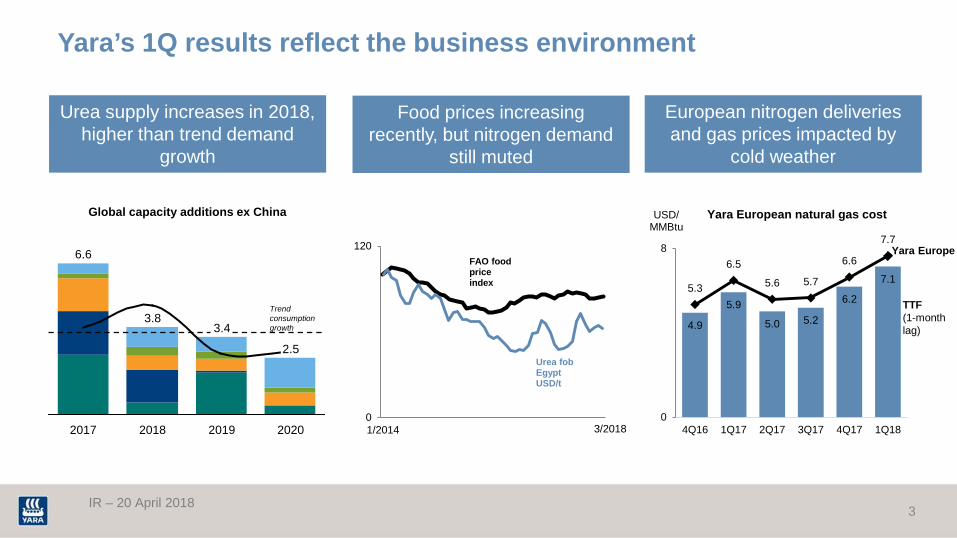

Yara’s 1Q results reflect the business environment

Food prices increasing recently, but nitrogen demand

still muted

Urea supply increases in 2018, higher than trend demand

growth

European nitrogen deliveries and gas prices impacted by

cold weather

0

120

1/2014 10/2014 7/2015 4/2016 1/2017 10/2017

Urea fob Egypt USD/t

FAO food price index

Global capacity additions ex China

4.9

5.9

5.0 5.2

6.2

7.1 5.3

6.5

5.6 5.7

6.6

7.7

0

8

4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

USD/ MMBtu

Yara European natural gas cost

3/2018

2.5

2020 2019

6.6

3.8

2017

3.4

2018

Trend consumption growth

IR – 20 April 2018 3

Yara Europe

TTF (1-month lag)

0

600

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18

USD/t

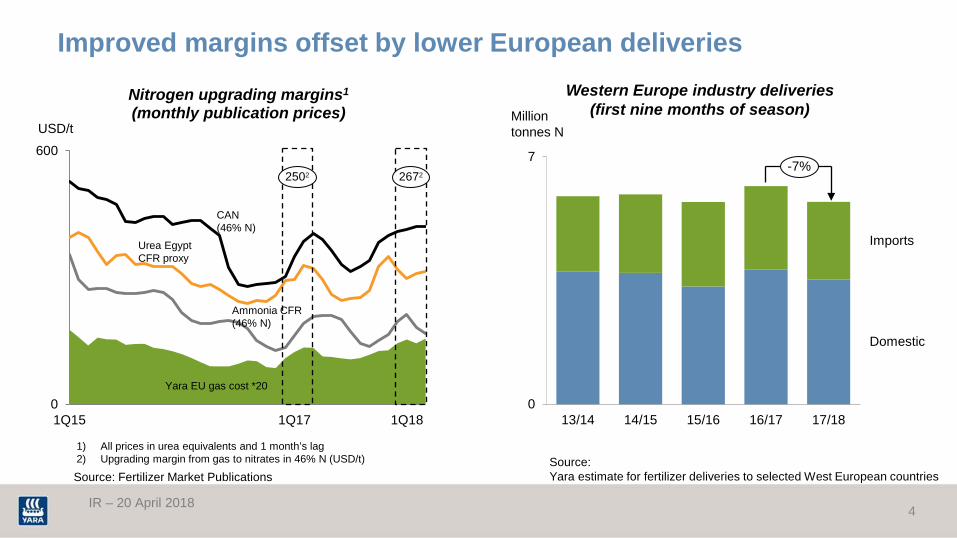

Nitrogen upgrading margins1 (monthly publication prices)

Yara EU gas cost *20

Urea Egypt CFR proxy

Improved margins offset by lower European deliveries

1) All prices in urea equivalents and 1 month’s lag 2) Upgrading margin from gas to nitrates in 46% N (USD/t)

Source: Fertilizer Market Publications

0

7

13/14 14/15 15/16 16/17 17/18

Western Europe industry deliveries (first nine months of season)

-7%

Source: Yara estimate for fertilizer deliveries to selected West European countries

Million tonnes N

Ammonia CFR (46% N)

CAN (46% N)

Domestic

Imports

2672 2502

IR – 20 April 2018 4

0

500

14 15 16 17 18

0

8,000

2014 2015 2016 2017 2018

Kilotons Kilotons

0

2,000

2014 2015 2016 2017 2018

Kilotons

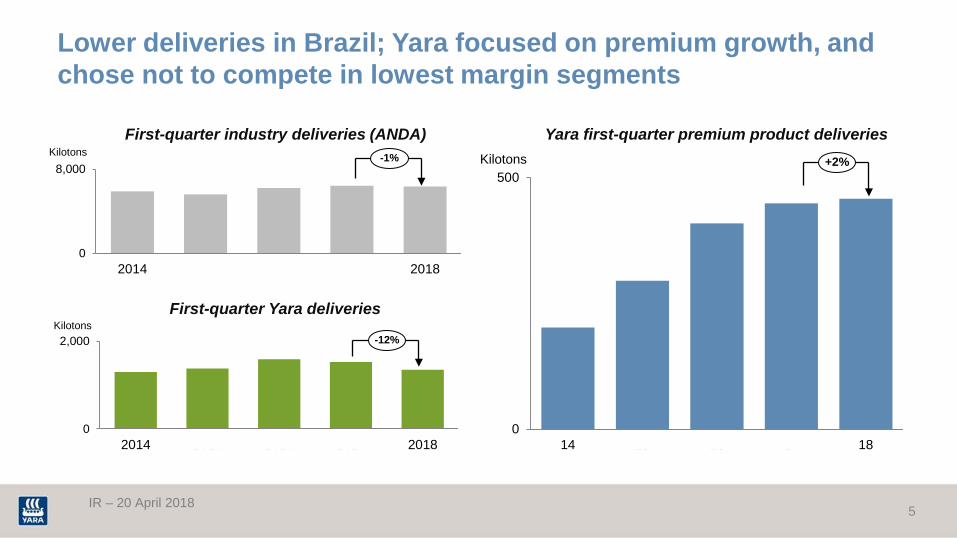

Yara first-quarter premium product deliveries First-quarter industry deliveries (ANDA)

Lower deliveries in Brazil; Yara focused on premium growth, and chose not to compete in lowest margin segments

-1%

-12%

First-quarter Yara deliveries

IR – 20 April 2018 5

+2%

Strong ammonia production performance

1) Including share of equity-accounted investees

0

2,200 +13%

Ammonia1

Kilotons

5,500

0

+2%

Finished fertilizer & industrial products1

Kilotons

Urea

Nitrates

NPK

CN UAN SSP

2015 2016 2017 2015 2016 2017

IR – 20 April 2018 6

Ammonia1

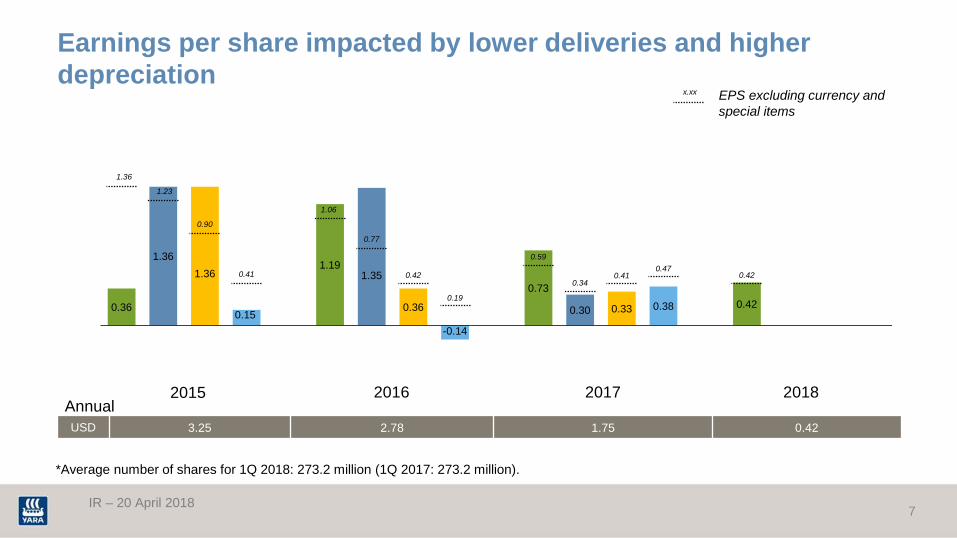

Earnings per share impacted by lower deliveries and higher depreciation

0.36

1.36 1.36

0.15

1.19 1.35

0.36

-0.14

0.73

0.30 0.33 0.38 0.42

1.36

1.23

0.90

0.41

1.06

0.77

0.42

0.19

0.59

0.34 0.41

0.47 0.42

USD 3.25 2.78 1.75 0.42

Annual 2015 2016 2017 2018

*Average number of shares for 1Q 2018: 273.2 million (1Q 2017: 273.2 million).

EPS excluding currency and special items

IR – 20 April 2018 7

x.xx

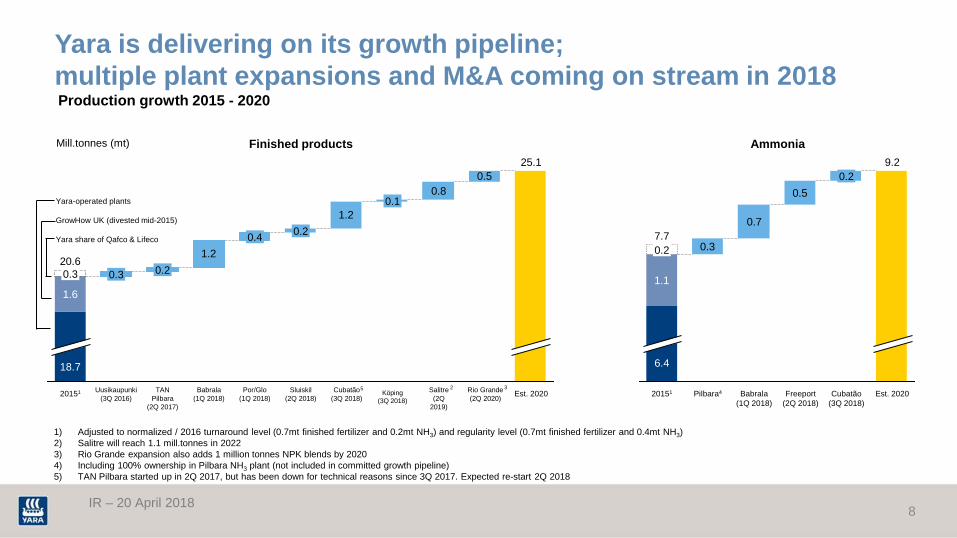

Yara is delivering on its growth pipeline; multiple plant expansions and M&A coming on stream in 2018

1) Adjusted to normalized / 2016 turnaround level (0.7mt finished fertilizer and 0.2mt NH3) and regularity level (0.7mt finished fertilizer and 0.4mt NH3) 2) Salitre will reach 1.1 mill.tonnes in 2022 3) Rio Grande expansion also adds 1 million tonnes NPK blends by 2020 4) Including 100% ownership in Pilbara NH3 plant (not included in committed growth pipeline) 5) TAN Pilbara started up in 2Q 2017, but has been down for technical reasons since 3Q 2017. Expected re-start 2Q 2018

Production growth 2015 - 2020

Finished products Ammonia Mill.tonnes (mt)

0.50.8

1.2

1.2

1.6

Est. 2020

25.1

Rio Grande (2Q 2020)

Salitre (2Q

2019)

Köping (3Q 2018)

0.1

Cubatão (3Q 2018)

Sluiskil (2Q 2018)

0.2

Por/Glo (1Q 2018)

0.4

Babrala (1Q 2018)

TAN Pilbara

(2Q 2017)

0.2

Uusikaupunki (3Q 2016)

0.3

20151

20.6

18.7

0.3

0.3

0.7

0.5

1.1

Est. 2020

9.2

Cubatão (3Q 2018)

0.2

Freeport (2Q 2018)

Babrala (1Q 2018)

Pilbara4 20151

7.7

6.4

0.2

Yara-operated plants GrowHow UK (divested mid-2015) Yara share of Qafco & Lifeco

IR – 20 April 2018 8

5 2 3

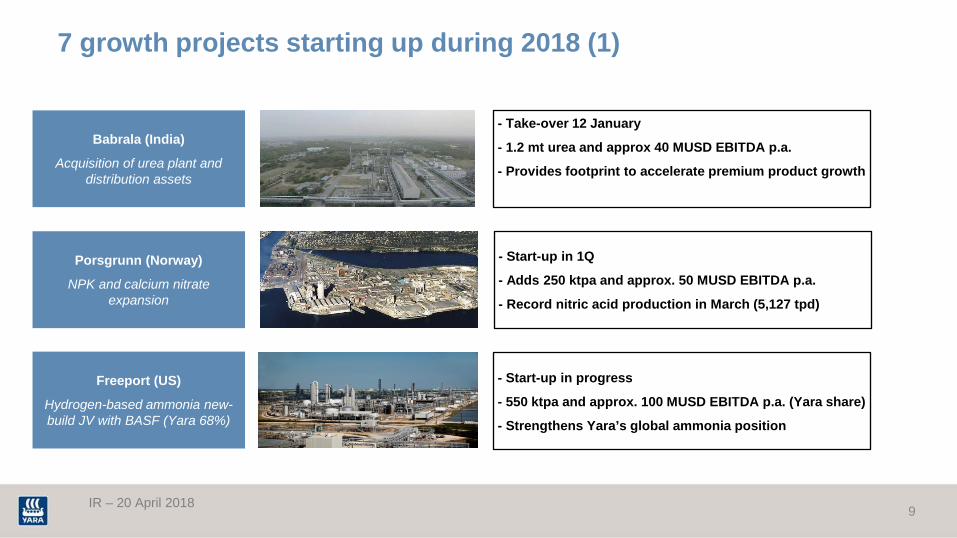

7 growth projects starting up during 2018 (1)

Babrala (India)

Acquisition of urea plant and distribution assets

Porsgrunn (Norway)

NPK and calcium nitrate expansion

Freeport (US)

Hydrogen-based ammonia new-build JV with BASF (Yara 68%)

- Start-up in progress

- 550 ktpa and approx. 100 MUSD EBITDA p.a. (Yara share)

- Strengthens Yara’s global ammonia position

- Start-up in 1Q

- Adds 250 ktpa and approx. 50 MUSD EBITDA p.a.

- Record nitric acid production in March (5,127 tpd)

- Take-over 12 January

- 1.2 mt urea and approx 40 MUSD EBITDA p.a.

- Provides footprint to accelerate premium product growth

IR – 20 April 2018 9

7 growth projects starting up during 2018 (2)

Sluiskil (NL)

Revamp and urea+S expansion

Salitre (Brazil)

Phosphate mine

Cubatao (Brazil)

N and P production facility acquisition

- Closing expected mid-2018

- 1.4 mtpa and approx. 60 MUSD EBITDA p.a.

- Strengthens production and industrial footprint in Brazil

- Start-up in 2Q (rock production only)

- Adds approx. 1.1 mtpa SSP equivalents by 2020

- Limited earnings until chemical production starts mid-2019

- Start-up in 2Q

- Adds approx. 210 ktpa and 30 MUSD EBITDA p.a.

- Improved product mix - from urea prills to nitrates and urea+S

IR – 20 April 2018

Köping (Sweden)

Nitric acid revamp and TAN expansion

- Start-up in 3Q

- 90 ktpa and approx. 50 MUSD EBITDA p.a.

- Strong long-term fundamentals for civil explosives industry

10

Kilotons

> 2million tonnes delivered last 12 months

1.000

2.000

0 2018 2014

AdBlue: record deliveries and expansion in Brunsbüttel

Facility comprising storage tank, truck-loading station and harbor facilities to increase sales and exports of AdBlue

Annual AdBlue production capacity of 1.1 million tonnes

This is enough AdBlue to remove around half a million tonnes of NOX emissions a year; enough to abate all road transport-related NOX emissions of Germany, Austria and Switzerland combined

Brunsbüttel AdBlue facility opened in February

IR – 20 April 2018 11

+19% CAGR

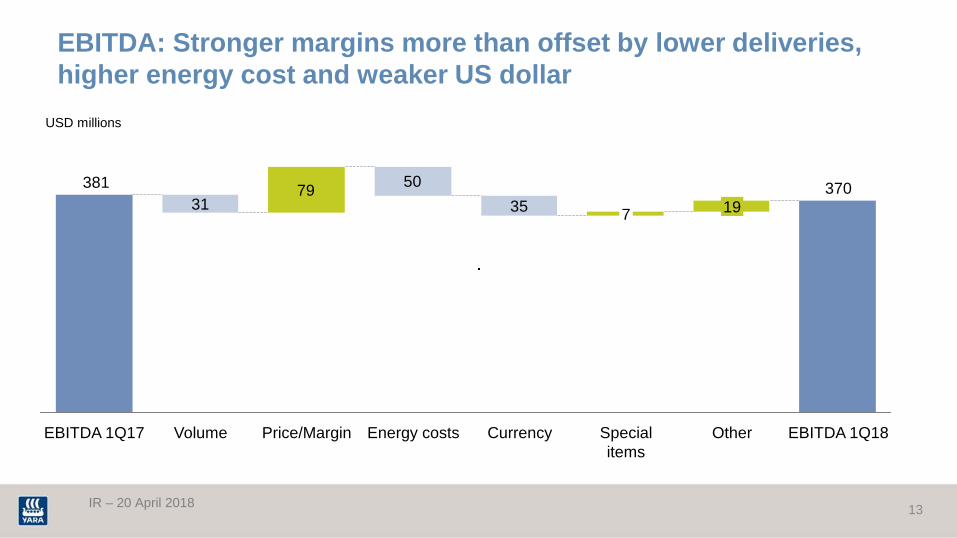

Underlying EBITDA down 5%

622 667

845

411

585 664

363 242

381 352 303 312 370

741

652

559

411

585

480

359 296

395 338 347 350 377

2015 2017 2016 2018

USD millions

EBITDA excluding special items

USD millions 2,545 1,854 1,348 370

Annual

xxx

12 IR – 20 April 2018

IR – 20 April 2018

EBITDA: Stronger margins more than offset by lower deliveries, higher energy cost and weaker US dollar

3179 50

35370381

EBITDA 1Q18 Other

19

Special items

7

Currency Energy costs Price/Margin Volume EBITDA 1Q17

USD millions

13

IR – 20 April 2018

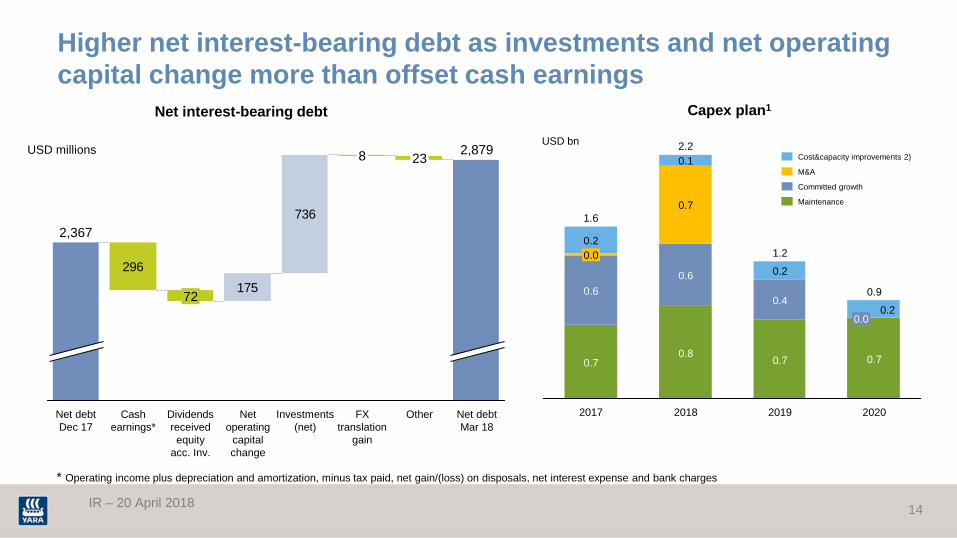

Higher net interest-bearing debt as investments and net operating capital change more than offset cash earnings

736

175296

2,879

Other

23

FX translation

gain

8

Net debt Mar 18

Investments (net)

Net operating

capital change

Dividends received equity

acc. Inv.

72

Cash earnings*

Net debt Dec 17

2,367

* Operating income plus depreciation and amortization, minus tax paid, net gain/(loss) on disposals, net interest expense and bank charges

USD millions

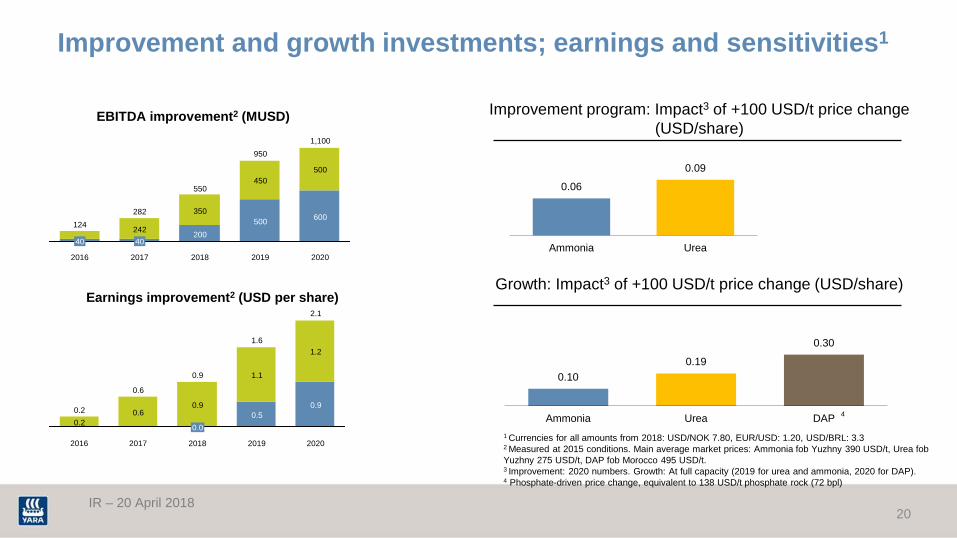

2019

1.2

0.7

0.4

0.2

2020

0.9

0.7

0.0 0.2

2018

2.2

0.8

0.6

0.7

0.0 0.2

0.1

2017

1.6

0.7

0.6

Maintenance

Cost&capacity improvements 2)

M&A

Committed growth

USD bn

Capex plan1 Net interest-bearing debt

14

IR – 20 April 2018

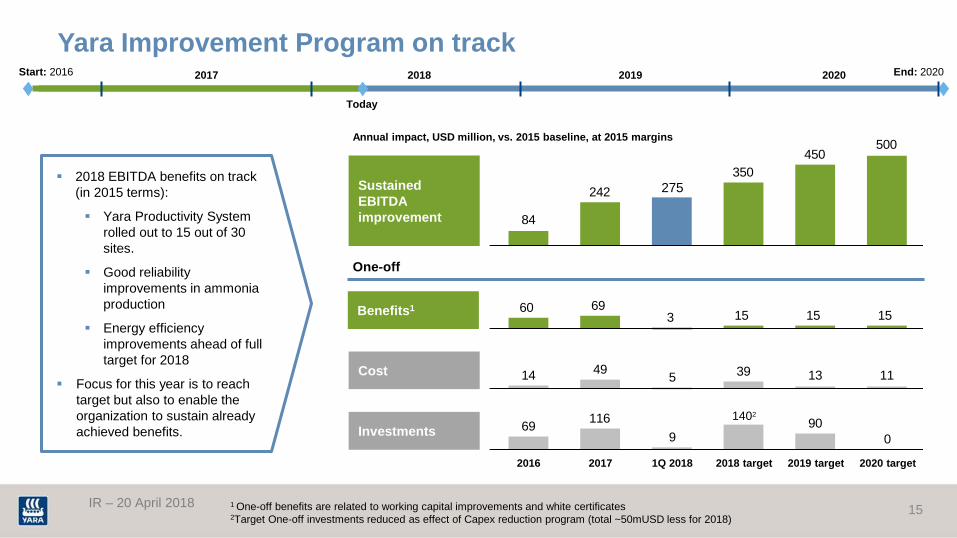

Yara Improvement Program on track

2018 EBITDA benefits on track (in 2015 terms):

Yara Productivity System rolled out to 15 out of 30 sites.

Good reliability improvements in ammonia production

Energy efficiency improvements ahead of full target for 2018

Focus for this year is to reach target but also to enable the organization to sustain already achieved benefits.

500450

350242

84

275

Annual impact, USD million, vs. 2015 baseline, at 2015 margins

Today

Start: 2016 End: 2020 2017 2018 2019 2020

151536960 15

090

911669

500

2016

1402

1Q 2018 2017 2019 target 2018 target 2020 target

11133954914

1 One-off benefits are related to working capital improvements and white certificates

2Target One-off investments reduced as effect of Capex reduction program (total ~50mUSD less for 2018)

One-off

Sustained EBITDA improvement

Benefits1

Cost

Investments

15

IR – 20 April 2018

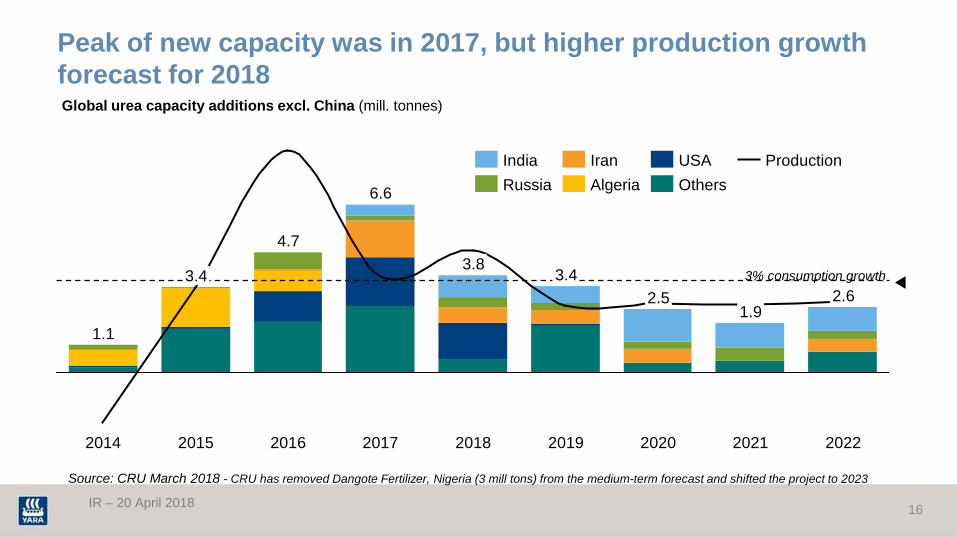

Peak of new capacity was in 2017, but higher production growth forecast for 2018

2.6

2022 2021

2.5

2020

1.9

2019

3.4

2018

3.8

2017

6.6

2016

4.7

2015

3.4

2014

1.1

Production Others

India USA Iran Algeria Russia

3% consumption growth

Global urea capacity additions excl. China (mill. tonnes)

Source: CRU March 2018 - CRU has removed Dangote Fertilizer, Nigeria (3 mill tons) from the medium-term forecast and shifted the project to 2023

16

IR – 20 April 2018 17

2020 2019

0.5

0.4

0.1

2018

1.4

1.3

0.1

2017

0.8

0.6

0.1

2016

0.9

0.9

0.1

Committed expansions + M&A

Improvement program

2020

1,100

600

500

2019

950

500

450

2018

550

200

350

2017

282

40 242

2016

104

40

2020

2.1

0.9

1.2

2019

1.6

0.5

1.1

2018

0.9

0.0

0.9

2017

0.6

0.6

2016

0.2 0.2

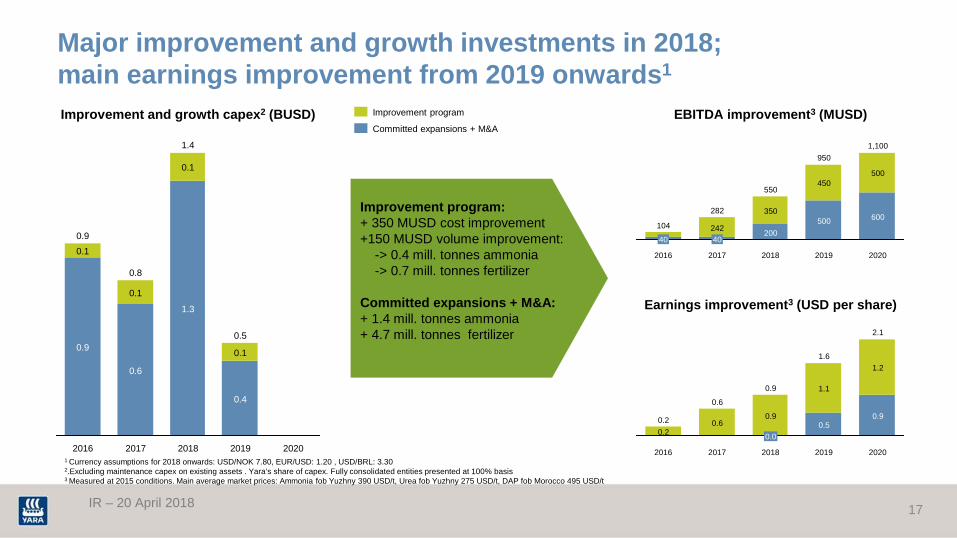

1 Currency assumptions for 2018 onwards: USD/NOK 7.80, EUR/USD: 1.20 , USD/BRL: 3.30 2.Excluding maintenance capex on existing assets . Yara’s share of capex. Fully consolidated entities presented at 100% basis 3 Measured at 2015 conditions. Main average market prices: Ammonia fob Yuzhny 390 USD/t, Urea fob Yuzhny 275 USD/t, DAP fob Morocco 495 USD/t

Improvement program: + 350 MUSD cost improvement +150 MUSD volume improvement: -> 0.4 mill. tonnes ammonia -> 0.7 mill. tonnes fertilizer Committed expansions + M&A: + 1.4 mill. tonnes ammonia + 4.7 mill. tonnes fertilizer

Major improvement and growth investments in 2018; main earnings improvement from 2019 onwards1

EBITDA improvement3 (MUSD)

Earnings improvement3 (USD per share)

Improvement and growth capex2 (BUSD)

IR – 20 April 2018

Backup / additional information

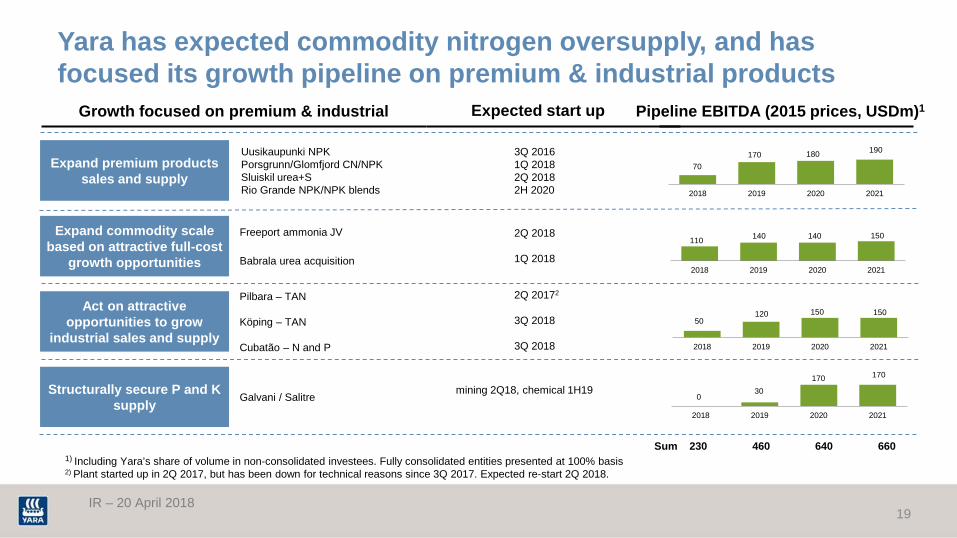

Yara has expected commodity nitrogen oversupply, and has focused its growth pipeline on premium & industrial products

Uusikaupunki NPK Porsgrunn/Glomfjord CN/NPK Sluiskil urea+S Rio Grande NPK/NPK blends

Expand premium products sales and supply

Freeport ammonia JV

Babrala urea acquisition

Expand commodity scale based on attractive full-cost

growth opportunities

Act on attractive opportunities to grow

industrial sales and supply

Galvani / Salitre Structurally secure P and K supply

Pilbara – TAN Köping – TAN Cubatão – N and P

Growth focused on premium & industrial

1) Including Yara’s share of volume in non-consolidated investees. Fully consolidated entities presented at 100% basis 2) Plant started up in 2Q 2017, but has been down for technical reasons since 3Q 2017. Expected re-start 2Q 2018.

Pipeline EBITDA (2015 prices, USDm)1

70 170 180 190

2018 2019 2020 2021

110 140 140 150

2018 2019 2020 2021

0 30

170 170

2018 2019 2020 2021

Expected start up

3Q 2016 1Q 2018 2Q 2018 2H 2020

2Q 2018 1Q 2018

mining 2Q18, chemical 1H19

2Q 20172 3Q 2018 3Q 2018

Sum 230 460 640 660

50 120 150 150

2018 2019 2020 2021

IR – 20 April 2018 19

2020

1,100

600

500

2019

950

500

450

2018

550

200

350

2017

282

40 242

2016

124

40

Improvement and growth investments; earnings and sensitivities1

EBITDA improvement2 (MUSD)

Earnings improvement2 (USD per share)

0.10 0.19

0.30

Ammonia Urea DAP

Growth: Impact3 of +100 USD/t price change (USD/share)

1 Currencies for all amounts from 2018: USD/NOK 7.80, EUR/USD: 1.20, USD/BRL: 3.3

2 Measured at 2015 conditions. Main average market prices: Ammonia fob Yuzhny 390 USD/t, Urea fob Yuzhny 275 USD/t, DAP fob Morocco 495 USD/t. 3 Improvement: 2020 numbers. Growth: At full capacity (2019 for urea and ammonia, 2020 for DAP). 4 Phosphate-driven price change, equivalent to 138 USD/t phosphate rock (72 bpl)

Improvement program: Impact3 of +100 USD/t price change (USD/share)

0.06

0.09

Ammonia Urea

4

2020

2.1

0.9

1.2

2019

1.6

0.5

1.1

2018

0.9

0.0

0.9

2017

0.6

0.6

2016

0.2 0.2

IR – 20 April 2018 20

IR – 20 April 2018

Higher margins in Crop Nutrition and Industrial segment

124 141

45 53

237

157 149

223

158

1Q17 1Q18

EBITDA (USD millions)

EBITDA excluding special items

Crop Nutrition Industrial Production

21

IR – 20 April 2018

Debt/equity ratio

-0.04

0.05

0.13 0.11

0.18

0.30

0.01

0.06

0.15 0.13

0.22

0.06 0.08

0.06

0.14

0.22

0.06

0.17 0.16 0.17

0.25

2013 2014 2015 2016 2017 2018

Net interest-bearing debt / equity ratio (end of period)

22

IR – 20 April 2018

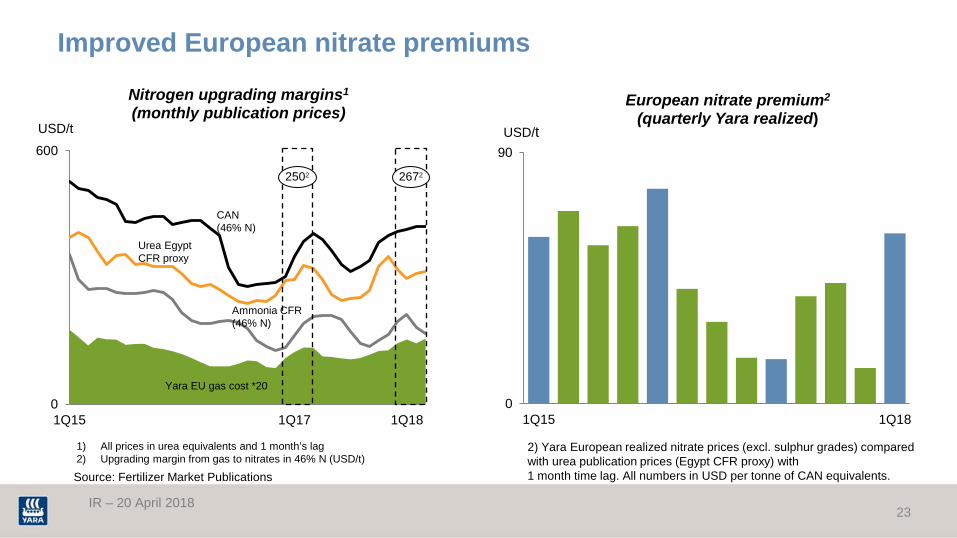

Improved European nitrate premiums

23

2) Yara European realized nitrate prices (excl. sulphur grades) compared with urea publication prices (Egypt CFR proxy) with 1 month time lag. All numbers in USD per tonne of CAN equivalents. Source: Fertilizer Market Publications

0

90

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18

European nitrate premium2 (quarterly Yara realized)

USD/t

0

600

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18

USD/t

Nitrogen upgrading margins1 (monthly publication prices)

Yara EU gas cost *20

Urea Egypt CFR proxy

Ammonia CFR (46% N)

CAN (46% N)

2672 2502

1) All prices in urea equivalents and 1 month’s lag 2) Upgrading margin from gas to nitrates in 46% N (USD/t)

IR – 20 April 2018

Weighted average global premium above blend cost

0

700

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18

USD/t NPK premium over blend1

Value above raw material

0

600

1Q15 3Q15 1Q16 3Q16 1Q17 3Q17 1Q18

USD/t Phosphate upgrading margins

DAP FOB US Gulf

Solid commodity phosphate margins and compound NPK premiums

24

1) Export NPK plants, average grade 19-10-13, net of transport and handling cost.

Rock, fob North Africa *1.4

NH3, fob Black Sea *0.22

Source: Fertilizer Market Publications

DAP, CIF inland Germany

MOP, CIF inland Germany

Urea, CIF inland Germany

Nitrate premium, CIF inland Germany

IR – 20 April 2018

64

45 27

42 46

90

70

18

20

20

12

0102030405060708090

100

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

USD millions

EU/US estimate* EU/US actual

Higher natural gas cost expected for the next two quarters

25

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

USD/ MMBtu

TTF (1-month lag) Yara Europe

Yara European natural gas cost Change in global natural gas cost

Source: Yara, World Bank, Argus/ICIS Heren *Dotted lines denote forward prices as of 30 January 2018 Pilbara actual

IR – 20 April 2018

Energy cost

26

4.0 4.4 4.0

2.8 3.7

4.4

2.6 2.0 2.1

2.8 3.0 3.0 3.0 2.9 2.9 3.2 3.2 2.7 2.8

4.8 5.7

8.2 8.0 8.0 6.9

5.5

4.1 3.8 4.0 4.3 5.3 4.7

5.9 6.0 5.7 4.7

6.6

9.2 9.4 10.5

8.1

6.4

4.2 4.4 4.2

5.4 5.8 5.0 5.5

6.6 6.8 6.9 6.9 6.6

7.6

10.7 11.0 11.4

9.1

7.1

5.0 4.6 4.9 5.3

6.5 5.6 5.7

6.6 7.7 8.0

7.4

2009 2010 2011 2012 2013 2014 2015 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

US gas price (Henry Hub) Yara Global TTF day ahead (Zeebrugge 2009-2012) Yara Europe

Yearly averages 2009 – 2015, quarterly averages for 2016-18 with forward prices* for 1Q18 and 2Q18.

*Dotted lines denote forward prices as of 30 January 2018 Source: Yara, World Bank, Argus/ICIS Heren

IR – 20 April 2018

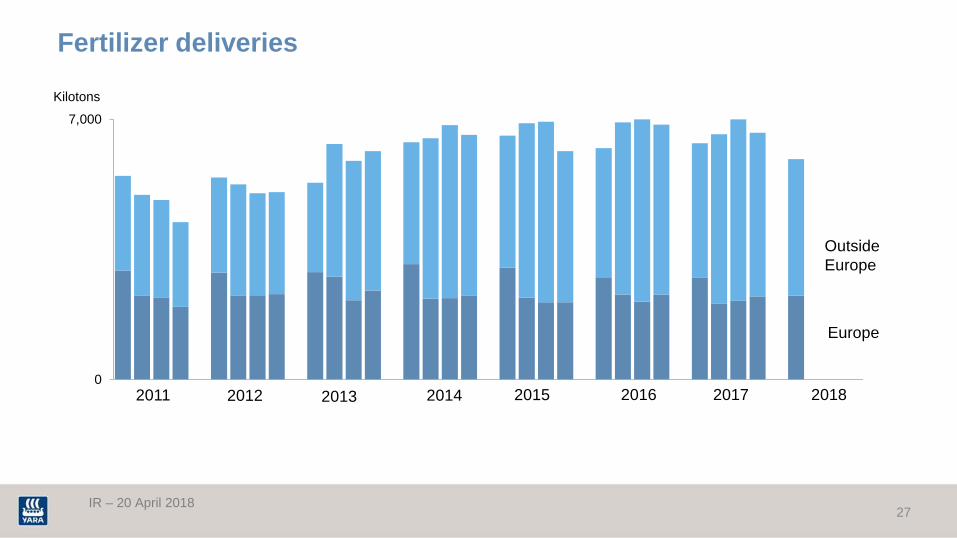

Fertilizer deliveries

27

0

7,000

Kilotons

2014 2011 2012 2013 2015 2016 2017 2018

Europe

Outside Europe

IR – 20 April 2018

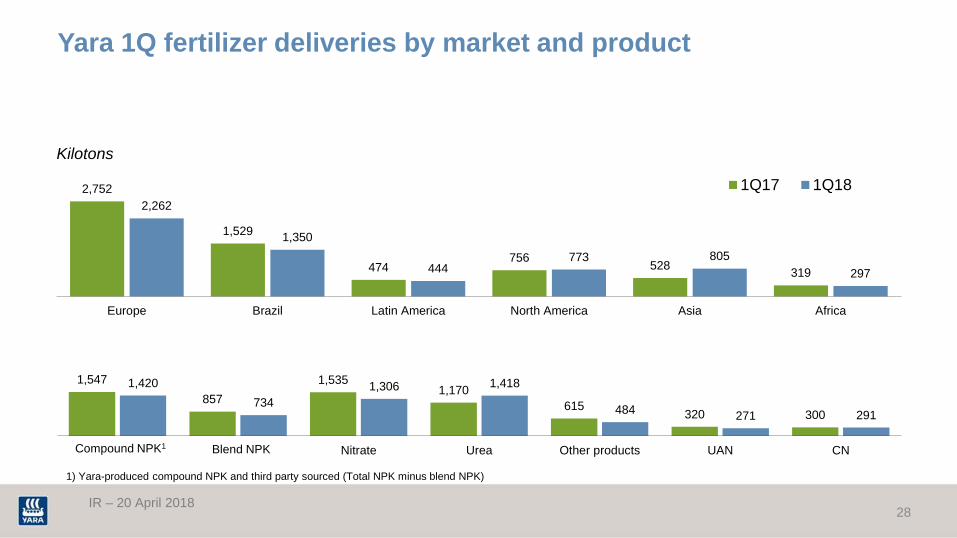

Yara 1Q fertilizer deliveries by market and product

28

2,752

1,529

474 756 528 319

2,262

1,350

444 773 805

297

Europe Brazil Latin America North America Asia Africa

1Q17 1Q18

1,547 857

1,535 1,170

615 320 300

1,420 734

1,306 1,418

484 271 291

Nitrate Urea Other products UAN CNCompound NPK1 Blend NPK

1) Yara-produced compound NPK and third party sourced (Total NPK minus blend NPK)

Kilotons

IR – 20 April 2018

Fertilizer deliveries by product and source

29

1,535 1,306

1,547 1,420

857 734

1,170

1,418

320 271

929 783

1Q17 1Q18 1Q17 1Q18 1Q17 1Q18 1Q17 1Q18 1Q17 1Q18 1Q17 1Q18

Yara-produced deliveries Joint venture & third party sourced

NPK compounds NPK blends Urea UAN Other

Kilotons

Nitrate

IR – 20 April 2018

Strong premium product deliveries

30

1) YaraBela, YaraMila and YaraLiva deliveries

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1Q14 1Q15 1Q16 1Q17 1Q18

250

409

198

43

172

317

449

237

70

180

307

458

236

100

176

Asia Brazil LatinAmerica excl.

Brazil

Africa NorthAmerica

Value-added fertilizer deliveries1 Value-added fertilizer deliveries1

CAGR 8%

Outside Europe Europe 1Q18 1Q17 1Q16

IR – 20 April 2018

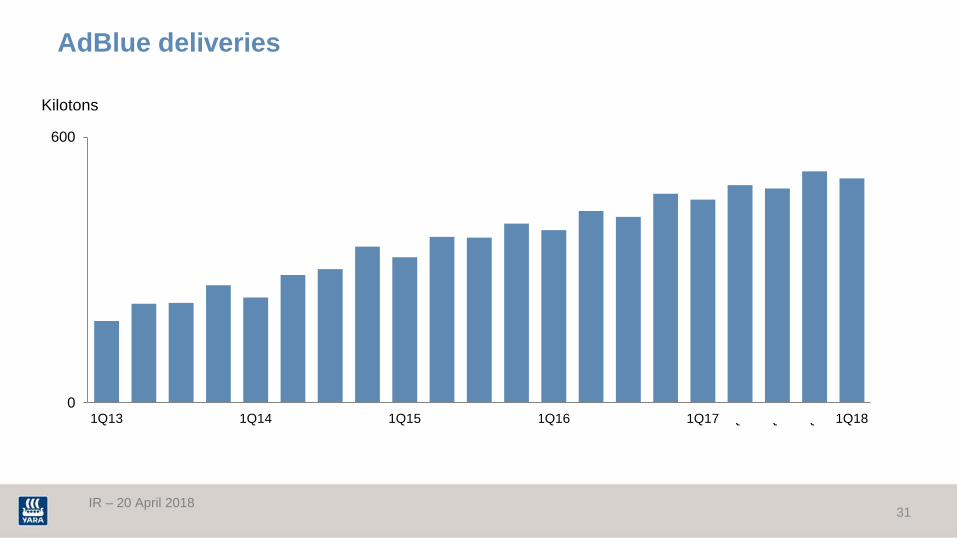

AdBlue deliveries

31

0

600

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18

Kilotons

IR – 20 April 2018

0

8,000

Yara stocks

32

Kilotons Finished fertilizer

Urea

Nitrates

Compound NPK

Other

IR – 20 April 2018

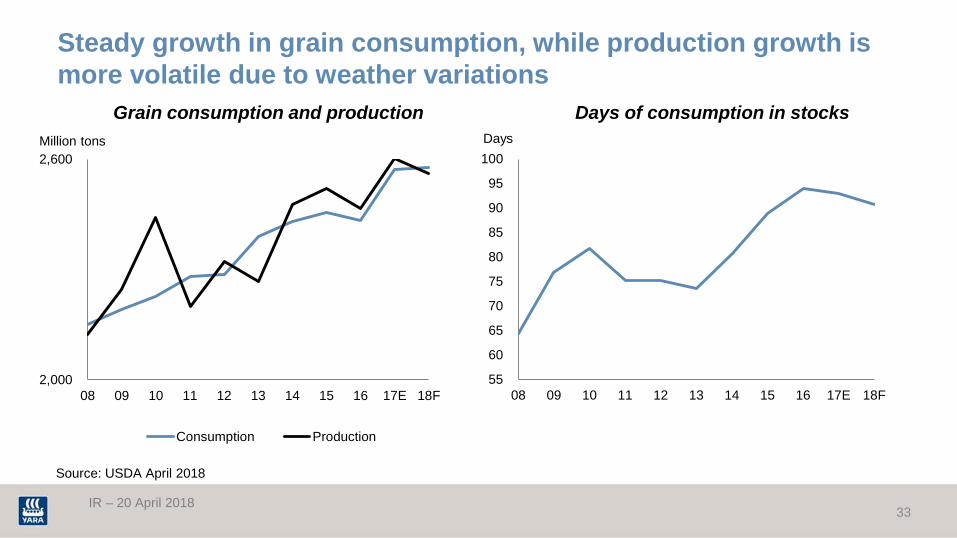

Steady growth in grain consumption, while production growth is more volatile due to weather variations

33

Source: USDA April 2018

2,000

2,600

08 09 10 11 12 13 14 15 16 17E 18F

Million tons

Consumption Production

Grain consumption and production Days of consumption in stocks

55

60

65

70

75

80

85

90

95

100

08 09 10 11 12 13 14 15 16 17E 18F

Days

IR – 20 April 2018

Relatively weak grain economics

34

0

50

100

150

200

250

300

1/2006 1/2007 1/2008 1/2009 1/2010 1/2011 1/2012 1/2013 1/2014 1/2015 1/2016 1/2017 1/2018

Index FAO price index

Cereals Price Index Cereals 5 year avg. Food Price Index Food 5 year avg.Source: FAO

IR – 20 April 2018

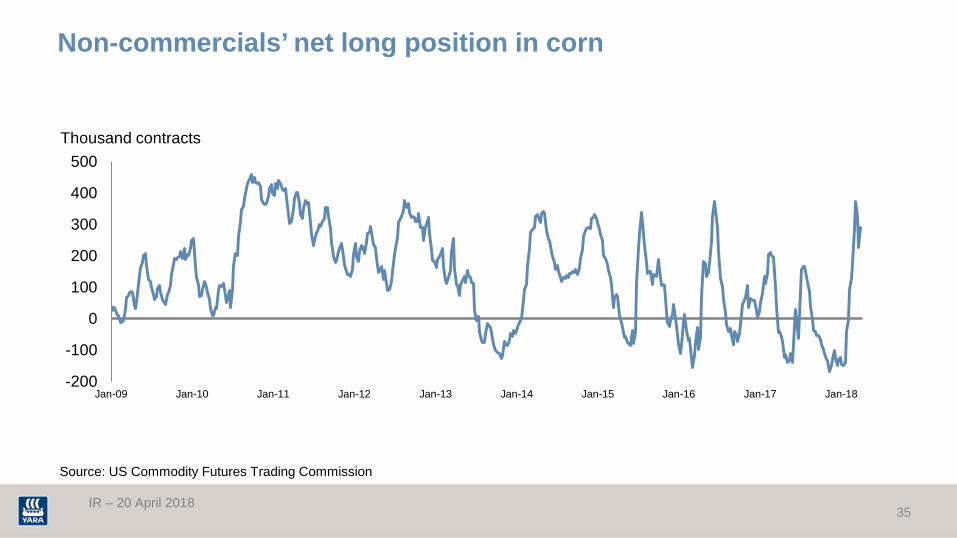

Non-commercials’ net long position in corn

35

-200

-100

0

100

200

300

400

500

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Thousand contracts

Source: US Commodity Futures Trading Commission

IR – 20 April 2018

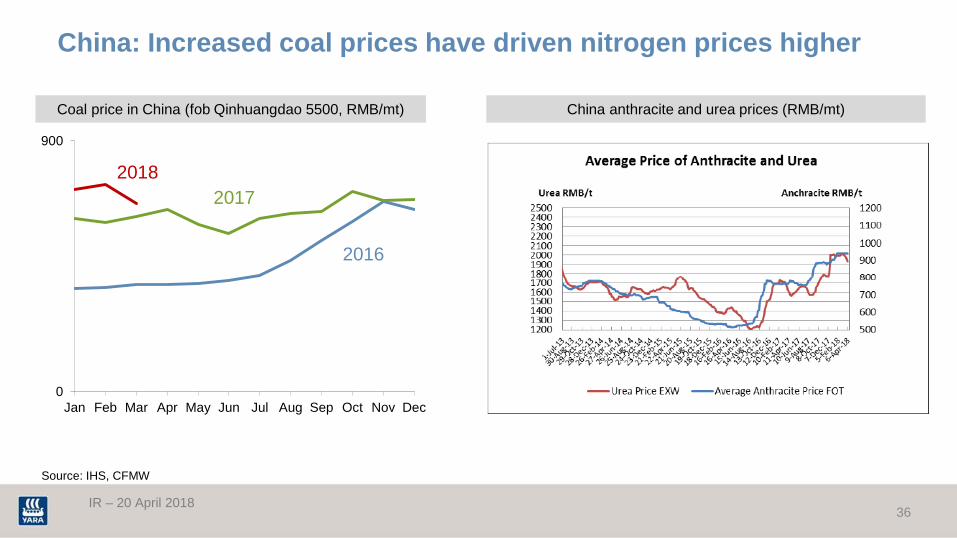

China: Increased coal prices have driven nitrogen prices higher

36

Coal price in China (fob Qinhuangdao 5500, RMB/mt) China anthracite and urea prices (RMB/mt)

Source: IHS, CFMW

0

900

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016

2018 2017

IR – 20 April 2018

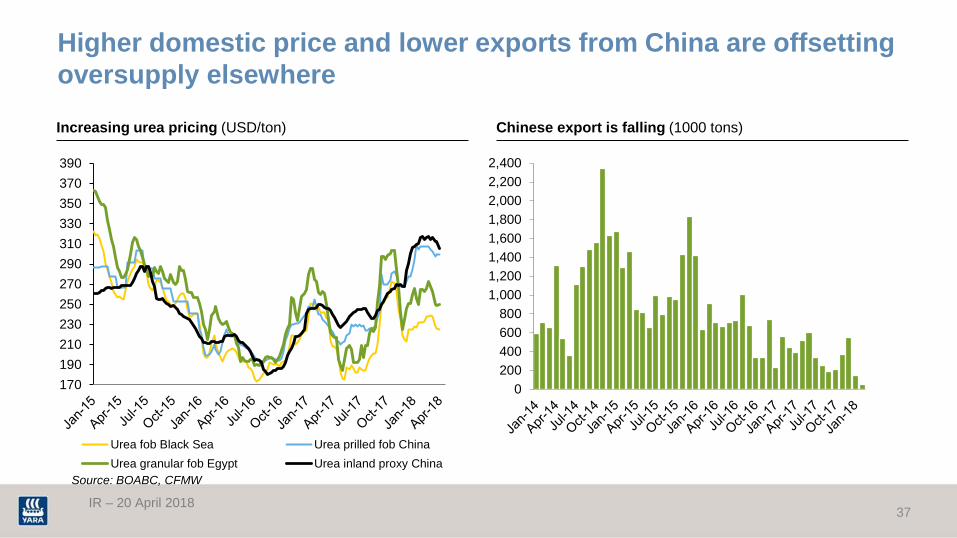

Higher domestic price and lower exports from China are offsetting oversupply elsewhere

37

170190210230250270290310330350370390

Urea fob Black Sea Urea prilled fob ChinaUrea granular fob Egypt Urea inland proxy China

Source: BOABC, CFMW

Increasing urea pricing (USD/ton) Chinese export is falling (1000 tons)

0200400600800

1,0001,2001,4001,6001,8002,0002,2002,400

IR – 20 April 2018

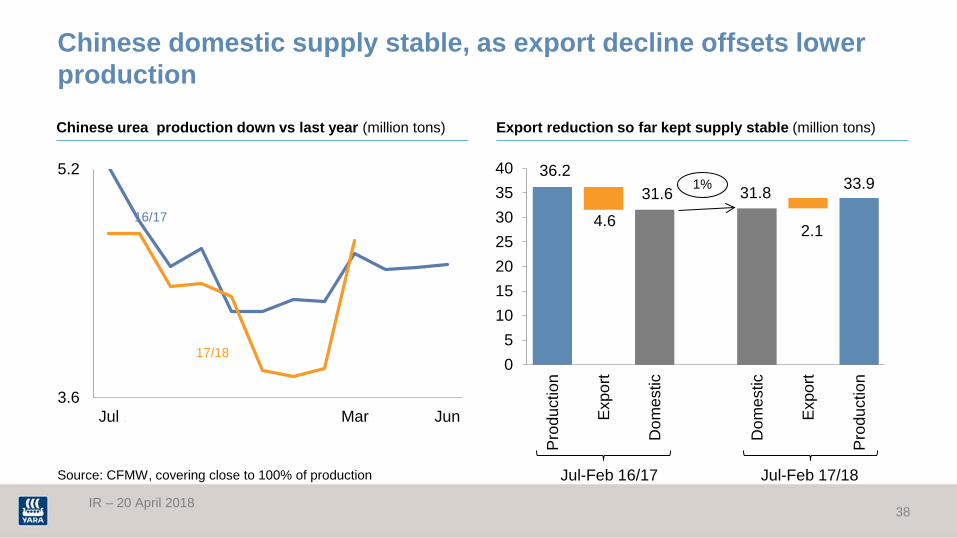

36.2

4.6

31.6 31.8

2.1

33.9

05

10152025303540

Pro

duct

ion

Exp

ort

Dom

estic

Dom

estic

Exp

ort

Pro

duct

ion

3.6

5.2

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Source: CFMW, covering close to 100% of production

17/18

Chinese domestic supply stable, as export decline offsets lower production

Jul-Feb 16/17 Jul-Feb 17/18

1%

16/17

Chinese urea production down vs last year (million tons) Export reduction so far kept supply stable (million tons)

38

IR – 20 April 2018

Deliveries in USA and Europe lagging last season, partly due to late spring

0

14

13/14 14/15 15/16 16/17 17/180

7

13/14 14/15 15/16 16/17 17/18

Source: Yara estimate for fertilizer deliveries to selected West European countries. Total nitrogen deliveries based on TFI, US Trade Commission, Blue-Johnson and Yara estimates

West Europe Million tons N USA Million tons N

39

-5% -7%

Domestic

Production

Production

Net imports

IR – 20 April 2018

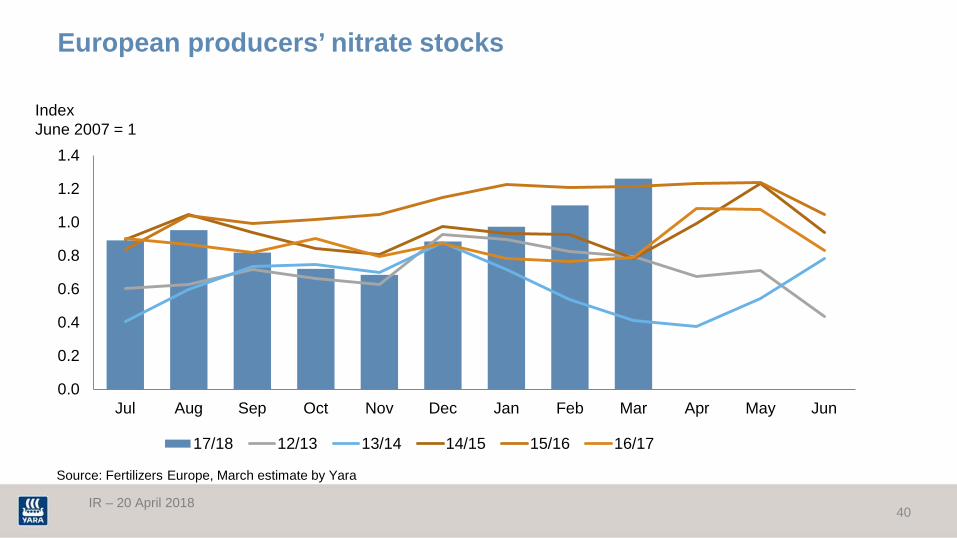

European producers’ nitrate stocks

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

17/18 12/13 13/14 14/15 15/16 16/17

Source: Fertilizers Europe, March estimate by Yara

Index June 2007 = 1

40

IR – 20 April 2018

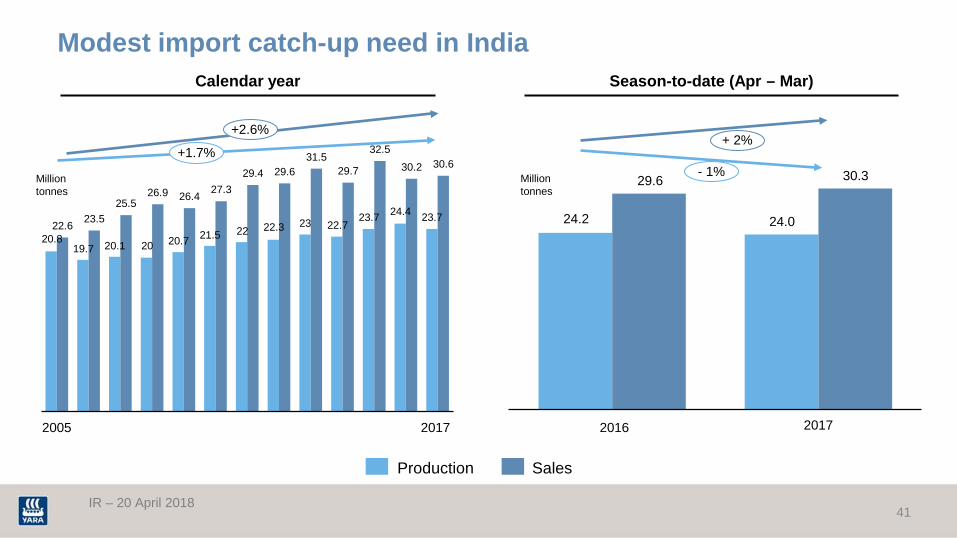

24.2 24.0

29.6 30.3

Modest import catch-up need in India

41

20.8 19.7 20.1 20 20.7 21.5 22 22.3 23 22.7

23.7 24.4 23.7 22.6 23.5

25.5 26.9 26.4 27.3

29.4 29.6 31.5

29.7

32.5 30.2 30.6

+1.7%

2017 2016 2017

+2.6%

2005

Production Sales

Million tonnes

+ 2%

- 1%

Season-to-date (Apr – Mar) Calendar year

Million tonnes

IR – 20 April 2018

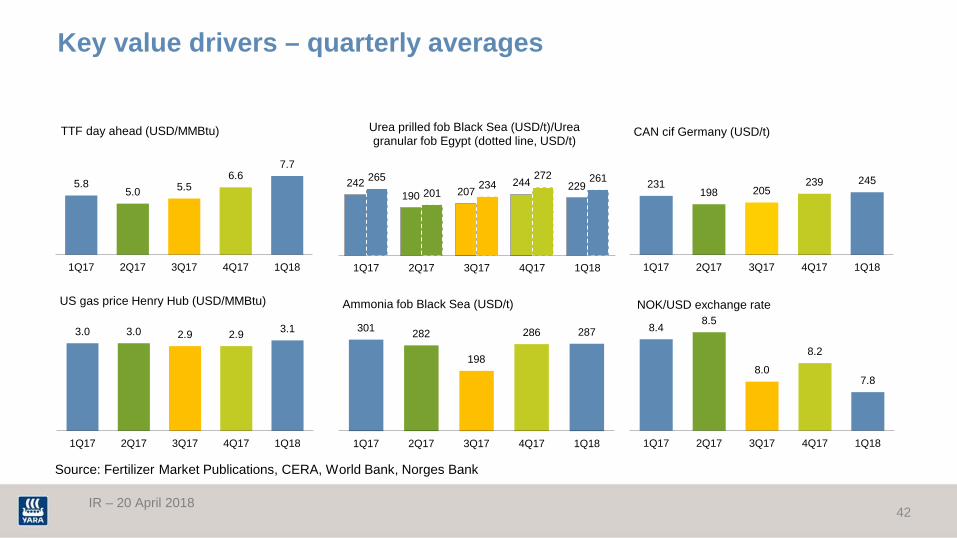

Key value drivers – quarterly averages

42

242 190 207

244 229 265

201 234

272 261

1Q17 2Q17 3Q17 4Q17 1Q18

Urea prilled fob Black Sea (USD/t)/Urea granular fob Egypt (dotted line, USD/t)

231 198 205

239 245

1Q17 2Q17 3Q17 4Q17 1Q18

CAN cif Germany (USD/t)

3.0 3.0 2.9 2.9 3.1

1Q17 2Q17 3Q17 4Q17 1Q18

US gas price Henry Hub (USD/MMBtu)

5.8 5.0 5.5

6.6 7.7

1Q17 2Q17 3Q17 4Q17 1Q18

TTF day ahead (USD/MMBtu)

8.4 8.5

8.0

8.2

7.8

1Q17 2Q17 3Q17 4Q17 1Q18

NOK/USD exchange rate

301 282

198

286 287

1Q17 2Q17 3Q17 4Q17 1Q18

Ammonia fob Black Sea (USD/t)

Source: Fertilizer Market Publications, CERA, World Bank, Norges Bank

IR – 20 April 2018

10-year fertilizer prices – monthly averages

43

0

200

400

600

800

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USD/t Urea prilled fob Black Sea/Urea granular fob Egypt

Average prices 2008 - 2017

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USD/t DAP fob US Gulf/MOP granular fob Vancouver

0

100

200

300

400

500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USD/t CAN cif Germany

0

200

400

600

800

1,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USD/t Ammonia fob Black Sea

Source: Fertilizer Market Publications

IR – 20 April 2018