139

Year End Close Workshop June 4, 2020 via ZOOM

Year End Close WorkshopJune 4, 2020 via ZOOM

Zoom Meeting InformationKeeping the WiFi//Internet presentation stable

• The chat box will be available for questions.

• We will monitor the chat box and answer questions throughout the presentation

We will have time for open discussion, participants can unmute and start video at end of workshop.

FYI: AP and AR Workshops: June 18 at 9am and 11am via Zoom More details regarding AR and AP accrual set ups.Mark your calendars now!

Workshop PurposeTopics:This workshop will prepare both District and Charter CBOs and Business Managers for completing the tasks (in a step by step manner) of closing the books for the 2019-20 fiscal year. A clean close of the books will get each LEA ready to prepare the Unaudited Actuals and have a successful audit.

● Year End Closing Timelines● Step by Step procedures/instructions● Manual provided for later use

Table of ContentsTimeline and Steps

• Table of Contents• Table of Contents - by Subject• Timeline helps you organize!

– Remember to allow yourself enough time to complete all steps.

– Work backward from recommended or due dates to schedule your work

– Calendars provided at the back of the manual

District Cutoff DatesSee June and July Calendars

• Review current open items for closed or closing resources - NOW• Vendor Warrant Cancellations• Fiscal Year Start-Up form for 2020-21 to IT• Final Cash Transfers• Final Cash Deposits• Final AP Run for 2019-20

• First AP Run for 2020-21• eFile Use Tax and mail payment

6/19/2020 6/15/2020 6/23/2020 6/23/2020 6/24/2020

7/08/2020 7/31/2020

• Last day to post 2019-20 Journals in ESCAPE 8/05/2020• Year End Close checklist due to SCOE 8/05/2020

SCOE Important Dates

• Preliminary Cash Roll 7/01/2020• SCOE: all internal entries prepared 7/24/2020• Year End Close checklist due to SCOE 8/05/2020• SCOE reviews of Adopted Budgets July - August 2020• SCOE reviews LEAs final balances August - Sept 2020

– After review completion LEAs can perform the final SACSextract for Unaudited Actual preparation

• Asset and Liability Roll August - Sept 2020• Unaudited Actuals due to SCOE 9/15/2020

Important Notes:

1. All backup for the final 2019-20 AP warrant run is due to SCOEby NOON on Wednesday, June 24, 2020.

2. DO NOT CREATE any NEW 2019-20 AP batches between June 24and June 30.

3. The last June deposit is June 23, 2020: due to SCOE by 4:30 PM.

4. DO NOT CREATE any NEW 2019-20 AR batches between June 24and June 30.

5. Payment screens for the 2020-21 fiscal year should be available Wednesday, July 1, 2020

6. All 2020-21 AP & AR batches must have a July 1st or later date.

Closing Check - Off List

Questions?

STEPS• Our presenting team will share information and

guidance for each of the closing steps next.

Step 1 Tracy Lehman

Step 1 – 2020-21 Fiscal Year End Close in EscapeClear All Prior Year Payables (9510) and Receivables (9210)

PY AP and ARs should be cleared prior to start of FY20 Close• Run the Fiscal02 Account Summary Detail OR Fiscal03 Account

Transaction Detail by Object-Balance

Go to Finance – Reports – Fiscal – Fiscal02 or Fiscal03

• Closing Year = 2020 {2019/2020}• Unposted JE? = Yes – Include unposted JE• Assets and Liabilities =Yes – Include – change Object filtering• Object = 9210,9510 (use comma no space)• Click Go to generate the report

Step 1 - Page 1

Step 1 – Fiscal02 Account Summary by Object-Balance

Enter the Search Criteria

Create Report

Favorites to save time!

Not sure of a report, use the Report Sample

link for more details and

example

Step 1 - Page 1

Step 1 – Example Fiscal02

• If there are NO Balances, skip to next step!• If there are Balances, then need to research

• Run the Ledger02 Receivable/Liabilities for more detail

Step 1 - Page 1

Step 1 – Ledger02 Receivables/Liabilities Activity

Run the Ledger02 for prior year for more detail on pending items. Determine if need to manually completed or reprocessed through year end in Steps 10 and 11.

Go to Finance – Reports – Ledger – Ledger02• Closing Year = 2019 {2018/2019}• A/R or AP ? = Both is default or change to A/R or A/P• Cleared Items? = No – Do NOT Show Cleared Items• JE Source? = Yes – Include all JE Sources• Unposted JE? = Yes – Select unposted JEs• Click Go to generate the report

Step 1 - Page 2

Step 1 – Ledger 02 Receivable/Liabilities Activity

Enter the Search Criteria

Step 1 - Page 2

Step 1 – Example Ledger02

• You now have a list of pending items that need to be reviewed• Determine if need to be cleared or reprocessed

• To clear a Requisition or Invoice, you would manually complete • To reprocess see Steps 10 and 11

Step 1 - Page 2

Step 1 – Clear Outstanding Journal EntriesThe Fiscal Year cannot be closed with outstanding JEs. They must be addressed by posting or deleting.

Go to Finance – Fiscal – Journal Entries• Search by Status:

Open SubmittedDenied Audit

Open to review Post or Delete

Step 1 - Page 3

Step 1 – Clear Outstanding Budget TransfersThe Fiscal Year cannot be closed with outstanding BTs. They must be addressed by posting or deleting.

Go to Finance – Budget – Budget TransfersOpen SubmittedDenied Audit

Open to review Post or Delete

Step 1 - Page 3

Step 1 – Fixed AssetsVerify that all assets acquired in FY20 have been entered and reviewed

Go to Finance – Assets – Fixed Assets

Search Criteria • Status = P {Pending}• Click Go to create the list

Step 1 - Page 4

Step 1 – Fixed Assets• From the list Highlight the record or double click to open• Use the Quick Link to review the Requisition detail

• If Item Received in Escape– Change Pending Status to Active

NOTE: If your District is not using Fixed Assets in Escape, now is not the time to implement, wait until after fiscal year is closed. Step 1 - Page 4

Step 1 – Fixed Assets Receive PO ItemsGo to Finance – Purchasing – Receive PO Items

Review Fixed Assets in Pending Status if items received or not• Enter Reference Number using the Requisition or PO Number• Ability to enter more that one to create a list to view• Click Go to create the list to review

Step 1 - Page 5

Step 1 – Fixed Assets Receive PO Items

• If Items received, return to Fixed Assets to update to Active Status• Date Rcvd is populated• Enter Rvc Now with number of items received • Go to Task to Post• Received Column will change to the number received

Step 1 - Page 5

Step 2 - Review Prior Year Receivables

A pre-closing step should be performed to determine the status of prior year receivables, other than object 9210. These are receivables set up in the prior year, as of June 30, 2019. The balances came over to the 2019-20 fiscal year as a starting balance, as of July 1, 2019. It is necessary to review the receivables to ascertain if a prior year balance remains. This should be done for ALL funds and resources.

Step 2 - Review Prior Year Receivables

How to review these receivables? • Review account balances for object codes 9211,9212,9218,9219,9290,9299,

and 9310 (or object codes particular to your own district)

Best Escape reports to use for reviewing:• Fiscal 02 report (summary)• Fiscal 03 report (detail)

Example:

Step 2 - Review Prior Year Receivables

Review account balance(s) to determine if it is still a valid receivable or if the balance(s) should be cleared or adjusted.

Example below: It’s determined the account balance of $5,379.89 is 2018-19’s quarter 4 lottery receivable, which was received in the fall of 2019. Therefore, the receivable should be cleared by the completing following entry:

Debit Credit01-1100-0-0000-0000-8560-xxx-xxxx 5,379.8901-1100-0- -9290- - 5,379.89

Step 2 - Review Prior Year Receivables

Example: During 2018-19’s close, the contribution to cafeteria was reduced and therefore, a due to/due from was set up. It’s determined the due to/due from should be cleared and the cash should be moved. Therefore, by June 23rd the following entry will need to be completed:

Debit Credit13-5310-0- -9610- - 26,933.7101-0000-0- -9310- - 26,933.71

Please note: Account balances in object 9310 (Due From other fund) and object 9610 (Due To other fund) will affect cash, once cleared. Therefore, these account balances must be cleared by June’s cash cut-off deadline of June 23rd.

Step 3 - Review Prior Year Payables

A pre-closing step should be performed to determine the status of prior year payables and liabilities, other than object 9510. These are payables set up in the prior year, as of June 30, 2019. The balances came over to the 2019-20 fiscal year as a starting balance, as of July 1, 2019. It is necessary to review the payables and liabilities to ascertain if a prior year balance remains. This should be done for ALL funds and resources.

Step 3 - Review Prior Year Payables

How to review these payables? • Review account balances for object codes 9518,9519,9590,9599,9610,

and 9650 (or object codes particular to your own district)

Best Escape reports to use for reviewing:• Fiscal 02 report (summary)• Fiscal 03 report (detail)

Example:

Step 3 - Review Prior Year Payables

Review account balance(s) to determine if the balance(s) is still a valid payable/liability or if the balance(s) should be cleared or adjusted.

Example below: During 2018-19’s close, unearned revenue was set up for Title I. Based on review of the account balance it’s determined the balance should be cleared. Therefore, the following entry should be completed:

Debit Credit01-3010-0- - -9650- - 4,150.0001-3010-0-0000-0000-8290-xxx-xxxx 4,150.00

Step 2 and 3 - Reminders

• These steps are pre-closing steps to determine the status of prior year balances in payable and receivables, other than object 9210 and 9510 – See Step 1, 10 and 11 for review and analysis of objects 9210/9229 and

9510/9529– See Step 9 for payroll receivables review and analysis

• Reminder: If the entry necessary to clear the account balance(s) for the payable/liability or receivable will affect cash then the entry must be completed by June 23th

– If cash transfer deadline is missed, but there was an intent to pay, leave the account balance as is and do the entry in July.

– Clearing object 9610/9310 account balances:• If it’s determined that the payable can’t be paid at this time, see Step

12

Let’s chat

Questions?

Next Section: Step 4 Blank Resource-Payroll Cleanup

Step 4 – Payroll Related 9XXX Account ‘String’ Cleanup

Cash Must Balance by Fund, Resource and Year

• “Blank” Resource transactions are generated from Payroll activity• Accounts Payable or Manual Journal Entries can be created with the

corresponding 0000 Resource or Components

Description FD-RSRC-Y-GOAL-FUNC-OBJT-SCH-MGMT

Payroll Generated XX - - - - -9XXX- -Accounts Payable or Manual Journal Entry Generated XX - 0000 -0- - -9XXX- -Accounts Payable or Manual Journal Entry Generated XX - 0000 -0- 0000 - 0000-9XXX- 000 - 0000

Example of Account Structure:

Step 4 - Page 1

Step 4 – Review Fiscal AccountsReview Transactions in 0000 Resource, 9XXX Objects

Go to Finance – Fiscal – Accounts

• Search Criteria:

• Resource = 0000 {Unrestricted}

• Object: 9213,9511,954-957

• Click Go to generate the list

Step 4 - Page 1

• Example List: 9213, 9555 and 9557 Object Codes have activity in 0000 Resource

• Balances will need to be transferred to Blank Resource by manual Journal Entry

Step 4 – Review Fiscal Accounts

Step 4 - Page 2

Step 4 – Manual Journal Entry to Clear Payroll Account Balances

Go to Finance – Fiscal – Journal Entries• Click New to start the Journal Entry

• Must enter a Comment This is “Searchable” field

• Click New to enter accounts

• Use Tasks to Submit or Approval Override to Post

Step 4 - Page 2-3

Step 4 – Review Fiscal AccountsReturn to Account Search to Review that JE posted as expected and cleared 0000 Resource, 9XXX Objects

Go to Finance – Fiscal – Accounts• Search Criteria:• Resource = 0000 {Unrestricted}• Object: 9213,9511,954-957• Click Go to generate the list

Step 4 - Page 3

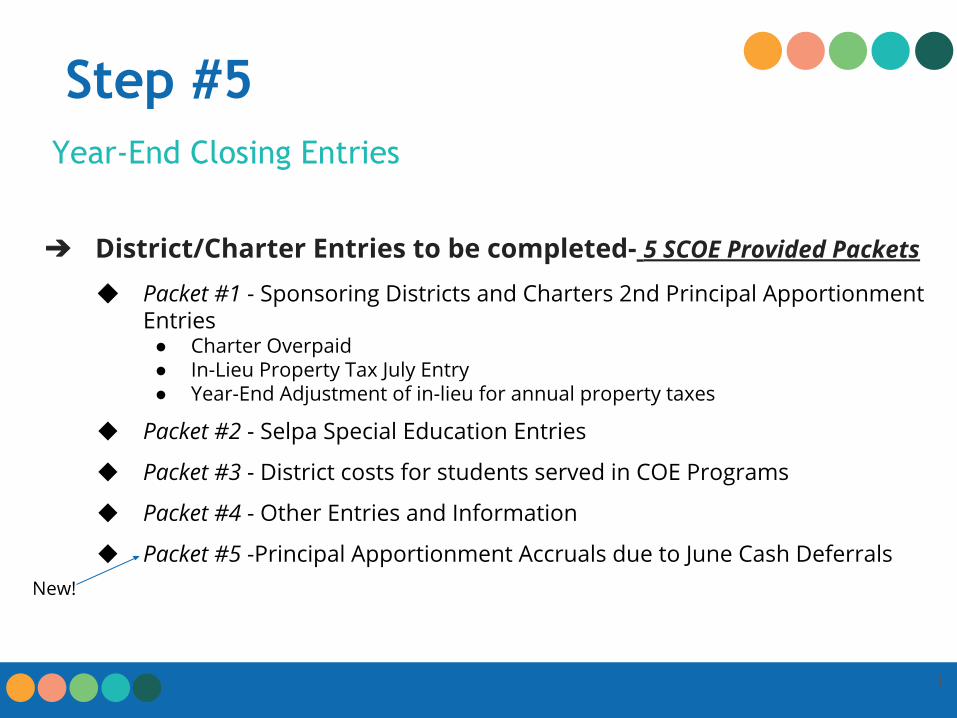

Year-End Closing Entries

➔ District/Charter Entries to be completed- 5 SCOE Provided Packets

◆ Packet #1 - Sponsoring Districts and Charters 2nd Principal ApportionmentEntries

● Charter Overpaid● In-Lieu Property Tax July Entry● Year-End Adjustment of in-lieu for annual property taxes

◆ Packet #2 - Selpa Special Education Entries

◆ Packet #3 - District costs for students served in COE Programs

◆ Packet #4 - Other Entries and Information

◆ Packet #5 -Principal Apportionment Accruals due to June Cash Deferrals

1

Step #5

New!

Step #5 (cont.)

➔ SCOE Entries - To be Completed by Fiscal Advisors

1. True up of LCFF (object 8011) based on annual property taxesa. If you prefer to make this entry yourself, contact your Fiscal Advisor

2. Fiscal Advisor will then reverse this entry in the next fiscal year (object 8019)

2

Year-End Closing Entries

Step #5 (cont)Year-End Closing Entries

➔ SCOE/District Entries - To be completed by Districts

◆ For Basic Aid Supplemental Districts Only

◆ Fiscal Advisors will only calculate the true-up of BAS based on

annual property taxes

◆ Districts must review and concur with entry

◆ Districts to complete entry (object 8011) and reverse in the

next fiscal year (object 8019)

◆ SCOE recommends districts receive auditor concurrence

3

As a general rule, if you complete the entry, you must clear in the next fiscal year. If SCOE makes the entry, SCOE will clear in the next fiscal year

Step # 6: Nancy Linder

Step 7: Federal & State Resources Closing

For each resource w/SACS matrix end-date of 7/1/20:

Checklist provided to make sure you’ve expended & cleared any remaining balances

Run a Fiscal 13 by resource to see balances, & again once cleared, to check ending balance is zero

See example

Page 2: CDE latest list of Expiring Resource Codes

Step 7: Federal & State Resources Closing

Page 3:

CDE List of resources (not exhaustive) subject to unearned revenue

Full listing, go to webpage at

https://www.cde.ca.gov/fg/ac/ac/resource.asp

Pages 4 & 5: Fund 25: Effective 2019-20 CDE closed

Resource 0000 to object 8681. Most created a restricted res & moved activity in 2018-19.

Move interest & any 19-20 activity to Res. 9xxx

Step 7: Federal & State Resources Closing

Step 8Erin Graves

Step 8-Use Tax Liability • Sonoma County City and County Sales Tax Rates have remained the

same since effective April 1, 2019. • Payment due to CDTFA (California Department of Tax and Fee

Administration) by July 31, 2020• Steps to gather data needed for filing Use Tax for districts with Only

One Tax Rate and with Multiple Tax Rates• There are sample reports to run for reconciling• If you transfer the 9580 liability from special funds to the general

fund/resource 0000, code pay payment to the the general fund/resource 0000, object 9580 to clear 9580

• If you do not make a transfer, be certain the expenditure is coded to the appropriate funds

• Template for MultipleTax Rates posted in SCOE’s Resources/Forms/Accounts Payable

Step 9a-WARRANT CANCELLATIONS

• Review and clear prior year warrant cancellations posted to the General Fund/8966/ZERR

• All Commercial Warrant Cancellations are due to Scott Greenwood ([email protected]) by end of day on Friday, June 19th

• Cancellations received after June 19th, SCOE will:– Process the stop payment at the bank– Cancel the check at the County Treasury– Post cancellation in Escape after the district’s prior year is closed

• If there is a prior fiscal year warrant cancellation that is material, work with your Fiscal Advisor to determine the best course of action

Step 9b - HOLDING/CLEARING ACCOUNTSAdjust to actual the 9XXX Objects Holding/Clearing Accounts in ALL FUNDS

When clearing accounts from Other Funds to the General Fund, begin with Other Funds and end with the General Fund. Use journals between funds through June 23rd. For entries after this date, it will be necessary to set up Due To and Due From (see Step 12).

To review and analyze balances in Object 9XXX, run a Fiscal03 report with “Y” in the assets and liabilities filter.

Payroll Accounts Receivable (REPAY)Object Code 9213

• Occurrence:– An employee has been overpaid salary– Prior Calendar Year payroll taxes were either refunded or

collected from the employee(OASDI or Medicare)• Examples of Possible Entries on page 2

Stale Dated WarrantsObject Code 9515 Run the Fiscal03, search on the journal and open the attachment for the details (instructions on pages 3-4)• Options:

– Reissue• Process payment through AP in either the current or next

fiscal year– Journal to Original Expense Account

• Except when prior year, journal to Revenue Account

Payroll ClearingObject Codes 9530 & 9531 Amounts in object 9530 should be refunded to the employee and amounts in 9531 should be refunded to the vendor.

In no case should amounts in 9530 or 9531 be credited back to the district expenditure codes as these are Employee-Paid benefits held in trust.

Reconcile the Fiscal03 and send it to Erin Graves at SCOE.

Payroll Withholding Liabilities Object Code 9555 • SUI:

– There will be an SUI balance to carry over to FY20-21 – The FY20-21 beginning balance should include the 2nd quarter

tax amount (April - June) and the July 10th tax amount for 3rd quarter

– Run the Pay05 for Ending Pay Date 7/10/2020 to assist in reconciling (see page 7 for sample report)

– DO NOT setup a PCL for the 2nd quarter payment

Step 9c - CESAP• If there is NO Balance in 9530, SKIP To Next Step!• If there is a Balance in 9530, Research needed

Example Fiscal03: Review that June Payroll(s) have been posted

• If there is a Balance in 9530, run the Pay34 Payroll Deduction and Contribution Detail Report to review the employee Deductions and Refunds were processed

Page 3

Step 9c – CESAPIf there is a Balance in 9530 Object, run the Pay34

Go to HR/Payroll – Reports – Payroll – Pay34

Enter the Request Criteria:• Starting Pay Date: 7/1/2019• Ending Pay Date:

6/30/2020 or 7/10/2020• Deduction Ids: CLSAP,CLSAP%• Exclude Contributions Group(s): All

Page 3

Create a Report

Favorite to save time!

Steps 10 & 11 – Establish Account Receivables and Accounts Payables as of June 30, 2020

Establish AR & AP transactions in Closing Year Manual Journal Entries Year End Closing Activity

Steps 10 & 11Page 1

Submit Signed Reports to SCOE Fiscal Advisor Fiscal15 – Year End Checklist Ledger02 – Receivables/Liabilities Activity

Detailed Year End procedures and processes workshops

June 18, 2020 AP - 9:00am – 10:30 am AR - 11:00am 12:30 pm

Steps 10 & 11 – Manual Accruals of Due To/From Government Entities

Must use 9290/9590 object codes Year End Processing activity does not allow object

codes other than 9210/9510 Must create Manual Journal Entries for any accruals

associated with state or federal programs Manual Journal Entries created with 9290/9590

balances will remain in these object codes during the Asset/Liability roll and will need to be manually reversed in FY21.

Steps 10 & 11Page 1

Steps 10 & 11 – Manual Accruals of Due To/From Government Entities

Manual Journal Entries to Setup Due To/FromGo to Finance-Fiscal-Journal Entries• Click to New to Create a Journal Entry• Must add Comment• Click New in Items to add account strings

Steps 10 & 11Page 1

Steps 10 & 11 – Manual Accruals of Due To/From Government Entities

Example: Manual JE to setup Receivable 9290 Object Code for Estimated Lottery Revenue

Steps 10 & 11Page 2

Manual set-up in 2019-2020

Steps 10 & 11 – Manual Accruals of Due To/From Government Entities

Manual Journal Entries to Reverse Due To/FromGo to Finance-Fiscal-Journal Entries

Steps 10 & 11Page 2

Enter FY 2021

Steps 10 & 11 – Manual Accruals of Due To/From Government Entities

Example: Reverse Manual JE to setup Receivable 9290 Object Code for Estimated Lottery Revenue

Steps 10 & 11Page 2

Manual reverse in 2020-2021

Steps 10 & 11 – Review Potential AR’s and AP’sRun a Fiscal15 - Fiscal Year End Checklist Report

Steps 10 & 11Page 4

Go to Finance – Reports – Fiscal – Fiscal 15• Fiscal Year: 2020 {2019/2020}• Reqs?: Yes – Include Requisitions having zero encumbrance balance• Payments?: Yes – Include Payments• Click Go to generate the report

Steps 10 & 11 – Review Potential AR’s and AP’s

Steps 10 & 11Page 3

Fiscal 15 - Year End ChecklistFiscal 15

Report must be

clear before

close of year

Steps 10 & 11 – Review AR’s & AP’s

Steps 10 & 11 Page 4

Carryover

Release

Accrual

1) Fiscal Year changed to FY212) Add accounts to FY213) Reverse outstanding encumbrance in FY204) Encumber in FY215) Write history record

1) Create JE in FY20 to set up liability2) Add liability accounts to FY213) Write history record

1) Change Accrual & Carryover to Zero2) Requisition status changed to Completed3) Reverse outstanding encumbrance in FY204) Write history record

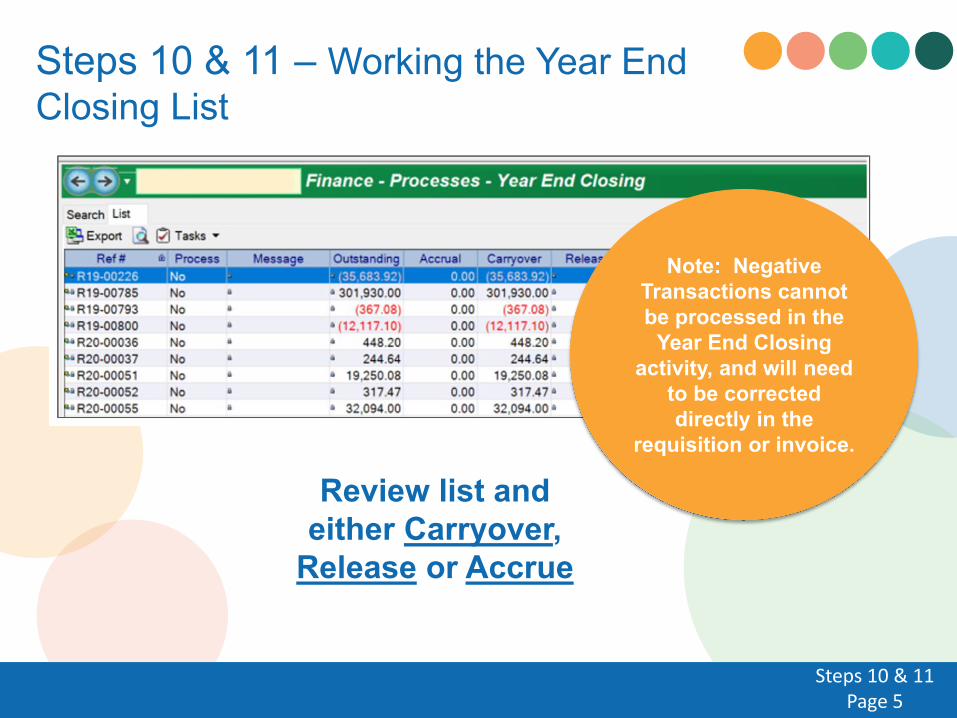

Steps 10 & 11 – Working the Year End Closing List

Steps 10 & 11Page 3

• Fiscal Year: 2020 {2019/2020}• Process Default: NO (Sets the

flag for ALL Documents on the list) If changed to YES, than ALL documents on the list defaults to be processed

• Department: Sort by Dept if desired

• Document Type: Default is All, or choose AR invoice, Dept, Stores/Vendor Req

• Reference Number: Can be AR or R

• Accounts: Specify by Accounts if desired

Go to Finance – Processes – Year End Closing

Steps 10 & 11 – Working the Year End Closing List

Steps 10 & 11Page 5

Note: Negative Transactions cannot be processed in the

Year End Closing activity, and will need

to be corrected directly in the

requisition or invoice.

Review list and either Carryover,

Release or Accrue

Steps 10 & 11 – Reports for Review

Steps 10 & 11 Page 6

Year End Processing Report

Reflects all detail for remaining options on the Process List

Option 1

Steps 10 & 11 – Reports for Review

Steps 10 & 11 Page 6

Magnifying Glass Icon

Reflects all detail for highlighted entry on the Process List

Option2

Steps 10 & 11 – Review of Additional Payables Information

Steps 10 & 11 Page 7

There are two methods to review Payables setup, activity and journal information

Go to Finance – Fiscal – Journal Entry

• Enter the R20-xxxxxx that you are

interested in

• Zero out the Fiscal Year field so you will

get a list of all journals

• Select Go

• All journals associated with that Payable

will be listed in order of entry

• Open and review the adjustment entry

Method 1 Method 2

• Blank out the Fiscal Year

• Enter and open the R20-xxxxxx you are

interested in

• Select the History Tab

• All activity will display in order of entry

• Open and review the adjustment entry

Go to Finance – Requisitions – Vendor Requisitions

Until the Asset/Liability Roll is done for your district later in August/September, you will be viewing

9529 in FY20 and 9510 in FY21 for all Payables

Steps 10 & 11 – Review of Additional Accounts Receivable Information

Steps 10 & 11 Page 7

There are two methods to review AR setup, activity and journal information

Go to Finance – Fiscal – Journal Entry

• Enter the AR20-xxxxxx that you are

interested in

• Zero out the Fiscal Year field so you will

get a list of all journals

• Select Go

• All journals associated with that AR will be

listed in order of entry

• Open and review the adjustment entry

Method 1 Method 2

• Blank out the Fiscal Year

• Enter and open the AR20-xxxxxx you are

interested in

• Select the History Tab

• All activity will display in order of entry

• Open and review the adjustment entry

Go to Finance – AR – Invoice

Until the Asset/Liability Roll is done for your district later in August/September, you will be viewing

9229 in FY20 and 9210 in FY21 for all Receivables

Steps 10 & 11 – Final Reports for Submission

Fiscal 15 – Fiscal Year End ChecklistGo to Finance – Reports – Fiscal – Fiscal15 Fiscal Year End ChecklistFiscal Year: 2020 {2019/2020} Click Go to generate report

Steps 10 & 11 Page 8

Steps 10 & 11 – Final Reports for Submission

Ledger02 – Receivables/Liabilities ActivityGo to Finance – Reports – Ledger – Ledger02 Receivables/Liabilities Activity

Steps 10 & 11 Page 8

Review Final Report

Must be signed by LEA Authorized

Signature

Step 12 - Due To/From and LOANS (INTERFUND AND TRANS)

● Temporary Loans typically occur when one fund is short of cash and needs to borrow money from another fund. Due From/Due To typically occurs when one fund pays an expense or liability on behalf of another fund.

● TRANS is Tax and Revenue Anticipation Notes (Object 9641). TRANS loans (other than cross year TRANS) must be repaid in full by May 1st of each year. Review the account balance (Object 9641) to determine if a balance remains after May 1. If a balance remains, an adjustment will be necessary. For more detailed information pertaining to TRANS, please refer to CSAM Procedure 715.

Step 12 - Due To/Due From and LOANS

Temporary Loans between funds (Object 9315/9615) and Due From/Due To between funds (Object 9310/9610) need to be reviewed for proper classification and repayment terms. Entries to set up transactions between these objects are presented in this section.

No matter which type of transaction occurs, the rule is the same: No more than 75%* of money held in any fund may be transferred and the amount shall be repaid in the same year or the following year if borrowing takes place within 120 days of the current fiscal year end. In other words, if a transfer takes place between March 1 and June 30 of the current year, repayment of the funds must occur by June 30 of the next year. If the transfer took place before March 1, the funds must be repaid by June 30 of the current year.

*Note that Governor Gavin Newsom has proposed, in his May Revision, to increase the percentage from 75% to 85%. This is not a done deal yet, but may be in the enacted State Budget.

Step 12 - Due To/Due From and LOANS

9315/9615 – Temporary Loan Due From/Due To Other Funds

Note: 9315 (asset) is Temporary Loan Due From Other Funds and is a receivable. 9615 (liability) is Temporary Loan Due To Other Funds and is a payable. The total of 9315 in all funds must equal the total of 9615 in all funds.

Review the above account balances and history behind them in order to determine if an account balance needs to be repaid within the parameters mentioned above.

To assist with this review, run a Fiscal 02 (summary) or Fiscal 03 (detail) report.

Step 12 - Due To/Due From and LOANS

9315/9615 – Temporary Loan Due From/Due To Other Funds

entry examples:

Original Set-Up: If the cafeteria fund is short of cash and needs to borrow from the general fund, an Inter Fund Cash JE (IFC) will need to be done (Note: if this occurs in June, it must be done no later than June 23.) Sample Entry:

Debit Credit

01-XXXX-0- - -9315- - 15,000.00

13-XXXX-0- - -9615- - 15,000.00

2) If it is determined that the loan was set-up prior to March 1 of the current year, and funds are available to pay the loan before the year ends, an Inter Fund Cash JE (IFC) will need to be done no later than June 23. Sample Entry:

Debit Credit

01-XXXX-0- - -9315- - 15,000.00

13-XXXX-0- - -9615- - 15,000.00

Step 12 - Due To/Due From and LOANS

If there was intent to pay the loan but the cash transfer deadline of June 23 is missed, do the above entry in July. If it’s determined that the loan can not be paid at this time, re-evaluate the circumstances and consider if the original cash transfer should be permanent in nature. If this conclusion is drawn, restate the loan as Transfer In/Out (891X/761X) via a Journal Entry (GJ) (may need Board approval). Sample Entries:

First Entry to be done: Debit Credit

01-XXXX-0- - -9315- - 15,000.00

01-XXXX-0-0000-9300-7616-000-0000 15,000.00

Second Entry to be done:

13-XXXX-0- - -9615- - 15,000.00

13-XXXX-0-0000-0000-8916-000-0000 15,000.00

If it is determined that the loan was set-up between March 1 and June 30 of the current year, leave the account balance as is. (Then, in the next fiscal year either #2 or #3 above will be performed.) Alternatively, if the district chooses to pay the loan before June 30 of the current year, follow #2 above.

Step 12 - Due To/Due From and LOANS

9310/9610 – Due From/Due To Other Funds

Entry examples:

Note: 9310 (asset) is Due From Other Funds and is a receivable. 9610 (liability) is Due To Other Funds and is a payable. The total of 9310 in all funds must equal the total of 9610 in all funds.

Original Set-Up: If the general fund bought supplies (expense) on behalf of the child development fund and Fund 12 can not pay it back immediately, or this event occurs June 24-30, a Journal Entry (GJ) is necessary to set-up the Due From/Due To. Sample Entries:

First Entry to be done: Debit Credit

01-XXXX-0- - -9310- - 3,000.00

01-XXXX-0-0000-0000-4XXX-000-0000 3,000.00

Second Entry to be done:

12-XXXX-0- - -9610- - 3,000.00

12-XXXX-0-0000-0000-4XXX-000-0000 3,000.00

Step 12 - Due To/Due From and LOANS

If there was intent to pay the amount but the cash transfer deadline of June 23 is missed, do the above entry in July. If it’s determined that the amount can not be paid at this time, re-evaluate the circumstances and consider if the original transaction should be permanent in nature. If this conclusion is drawn, restate the amount as Transfer In/Out (891X/761X) via Journal Entry (GJ) (may need Board approval). Sample Entries:

First Entry to be done: Debit Credit

01-XXXX-0- - -9310- - 3,000.00

01-XXXX-0-0000-9300-7611-000-0000 3,000.00

Second Entry to be done:

12-XXXX-0- - -9610- - 3,000.00

12-XXXX-0-0000-0000-8911-000-0000 3,000.00

5) If it is determined that the amount was set-up between March 1 and June 30 of the current year, leave the account balance as is. (Then, in the next fiscal year either #3 or #4 above will be performed.) Alternatively, if the district chooses to pay the amount before June 30 of the current year, follow #3 above.

Step 12 - Due To/Due From and LOANS

9641 – TRANS (CSAM Procedure 715)

1) Ascertain that TRANS has been paid in full by June 30 (this does not apply to a cross year TRANS). If an amount remains in the account balance determine if a payment was miscoded. If not miscoded, pay the amount due.

2) If it is determined that TRANS has been paid in full but a debit amount appears in the account balance, it should be cleared to zero via a Journal Entry (GJ). Sample Entry:

Debit Credit

01-XXXX-0-0000-9100-5880-000-0000 6,732.58

01-XXXX-0- - -9641- - 6,732.58

Step 13 - Revolving Cash and Stores Inven tory

Revolving Cash Reserve (object 9711) must equal its corresponding asset, Revolving Cash (object 9130). Stores Reserve (object 9712) must equal its corresponding asset, Stores -Inventory (object 9320). Review the account balance for all four accounts (if applicable). If the reserve account balance is zero, or an amount different from the asset account balance, an adjustment is necessary to the reserve account so that it’s properly reported in SACS. This can be done by a budget transfer in Escape or by direct entry into SACS.

Note: This section does not apply to Charters with fund 62.

Step 13 - Revolving Cash and Stores Inventory

● Do a Budget Transfer. The amount in 9711 and 9712 will download into SACS. For unaudited actuals period only, the system will check the related asset amounts (in 9130 and 9320) and automatically change 9711 and 9712 to equal the respective asset amount. Therefore, during the closing process be sure to verify that the amount in 9130 and 9320 is accurate. See Sample Entries below for set up and adjustment.

Option 1:

9711 – Revolving Cash Reserve

The revolving cash account (9130) has a $5,000 balance. But the reserve (9711) account balance is zero. Do a Budget Transfer to set up the reserve amount:

Increase Decrease

01-XXXX-0- - -9711- - 5,000.00

01-XXXX-0- - -9790- - 5,000.00

9712 – Stores Reserve

The stores-inventory account (9320) has a $7,000 balance. But the reserve (9712) account balance is $3,000. Do a Budget Transfer to adjust the reserve amount:

Increase Decrease

01-XXXX-0- - -9712- - 4,000.00

01-XXXX-0- - -9790- - 4,000.00

Step 13 - Revolving Cash and Stores Inventory

● Do an entry in SACS. For budget and interim reporting periods, manually enter the reserve amount in Components of Ending Fund Balance under the Forms tab. See below for Sample Form. For unaudited actuals period a manual entry is not allowed. The system will check the related asset amounts (in 9130 and 9320) and automatically change 9711 and 9712 to equal the asset amount. Therefore, during the closing process be sure to verify that the amount in 9130 and 9320 is accurate.

Option 2:

Enter the total reserve balance directly into SACS. Sample Form:

Let’s chat

Questions?

Next Section: Step 14 Special Education: IDEA

Federal Revenue

STEP 14: Special Education-IDEA Federal Revenue All Federal Special Education Revenue must be expended by June 30th each year.2019-20 Federal Resources & Revenue::• Resource #3310 - Local Assistance Entitlement• Resource #3315 Federal Preschool Grant• Resource #3327 - ERMHS

Expenditures should equal the entitlement

Do not make a contribution to a Federal Grant Award, as this will impact your Maintenance of Effort (MOE)

Step #15Time Accounting for Federal Programs

LEA administrative use of Title funds in response to COVID-19 continues as does the time accounting

❖ General Rule: For each employee whose salary and wages are supported with Federal funds, time accounting is required. ➢ Employees who work on a single cost objective must do at least a semi-annual

certification

➢ Employees who work on multiple cost objectives must do a monthly Personal

Activity Report (PAR), or use a substitute system.

4

Step #15 (cont)Time Accounting for Federal Programs

❖ Approved Substitute System based on Sampling Method:➢ Uses sampling methods that meet statistical sampling standards (see

CSAM Procedure 905)

➢ Designed to simplify recordkeeping for LEA’s

➢ Use is optional. LEA does not need CDE approval to implement

➢ 1st year on system – PARS are required every 4th month (3 times a

year)

➢ 2nd year and forward – PARS are prepared twice a year

➢ If you choose to use the substitute system, all multi-funded employees

must be included

5

Step #15 (cont)Time Accounting for Federal Programs

❖ Newer Approved Substitute System based on Employee’s Predetermined Schedule:➢ For employees who work in multiple cost objectives on a predetermined

schedule. Instead of a monthly PAR, employee could do semi-annual certification using predetermined written schedule as support. (see pages 6-13 of the manual for samples)

➢ Signed by employee and supervisor.➢ Written schedule must indicate specific activity or cost objective for each

segment of the schedule; account for total hours employee is paid.➢ If there are significant deviations from established schedule then employee

should use PAR for that period.➢ Must have CDE approval. To get authorization to use the new substitute

system:■ CARS (Consolidated Application Reporting System) has the

management certification. Yearly certification is required. CARSexpected to open July 6.

6

Step #15 (cont)Time Accounting for Federal Programs

➔ The new substitute system does not apply to employees working on a single cost objective.

➔ The new substitute system may only be used by employees with a set schedule.

➔ Only one substitute system may be used. An LEA may not choose to use the new system for employees working a set schedule and the existing system for all other employees who are only eligible to use the existing system.

For additional information:★ See CSAM Procedure 905★ Review CDE Guidance letter (pages 2-5 step #15 of manual)★ See examples of semi-annual certification using predetermined schedule

(pages 6-13 of manual)★ Escape Pos11 report information with samples (pages 8-13 of manual)

7

Step #16: Shelley Stiles

STEP 16: Interest Calculation Specific resources or capital projects may require interest income to be postedTreasury Quarterly Rates 2019-20:• Quarter 1: 2.213%• Quarter 2: 2.060%• Quarter 3: 2.023%• Quarter 4: recommend an average of 3 known quarters

Federal Programs - reporting and remitting:• Must be done quarterly• Interest calculation - daily cash basis: use ESCAPE Fiscal 24

– Sample screen included in manual Step 17:Linda Daugherty

Step 17: Sub-Agreements & Multi-District Agreements

Page 1:

Both are monitored closely by CDE to insure that expenditures for program delivery are not double counted, & do not incorrectly affect the Indirect Cost Rate calculation.

Sub-Agreements: Sub-Agreement examples: Contracts for special

education, transportation, nonpublic schools, & between Charter schools and mangement companies.

Federal coding rules apply in the use of objects 5100 and 5800.

Step 17: Sub-Agreements & Multi-District Agreements

Page 2:

Feds require that sub-agreements (object 5800) be excluded from the indirect cost rate calculation and from program costs on which indirect costs are charged.

Allows only the first $25k to be charged to object 5800, and the remaining balance must be charged to object 5100.

LEAs can classify these expenditures as part of the year-end closing process, or on purchase orders throughout the year.

Step 17: Sub-Agreements & Multi-District Agreements

Page 2:

CDE provided clarification that a single contract and not per pupil constitutes a sub-agreement for the $25k.

Page 3:

Example of Escape vendor report to capture vendors over $25k that may be a Sub-Agreement.

Step 17: Sub-Agreements & Multi-District Agreements

Page 3:

Multi-District Agreements: Typically one LEA serves as the lead and

opperates the project for other participants(consortium/shared services services).

Most common are those formed for special education, transportation, food services, or shared staff such as PE Teachers, Nurses, Psychologists, or Speech Therapists.

Step 17: Sub-Agreements & Multi-District Agreements

Page 3 & 4: Again, from a statewide persepective,

expenditures for program delivery should not be double counted.

Coding examples are provided using object 51xx/58xx (participating school district), vs. objects 1xxx, 2xxx, 3xxx, etc. (local operating agency).

Step 18Deborah Malone-Larson

STEP 18 - Special EducationMaintenance of Effort Report

The Special Education MOE Reports are used to determine if a Local Educational Agency (LEA) met the maintenance of effort required by the federal IDEA

• An LEA may not reduce the amount of state & local, or local only expenditures for the education of children with a disabilities below the amount it spent in the comparison year

STEP 18 - Special EducationMaintenance of Effort ReportThere are two components for the LEA MOE requirement:

• MOE - SEMB Report : eligibility standard:– To find if an LEA is eligible to receive IDEA funds– If an LEA does not meet the eligibility test, CDE will

withhold IDEA funds that the LEA is entitled to receive for the next fiscal year

• MOE - SEMA : compliance standard:– Determines if an LEA meets the federal compliance– If an LEA does not meet the requirement, CDE will

invoice the LEA for the amount not meeting the MOE

STEP 18 - Special EducationMaintenance of Effort Report

There are four methods to meet the MOE Compliance for both eligibility (SEMB) and compliance (SEMA) standards

• Combined state and local expenditures;• Combined state and local expenditures on a per capita

basis;• Local expenditures• Local expenditures one on a per capita basis

STEP 18 - Special EducationMaintenance of Effort ReportMOE Allowable Exemptions:

• Voluntary departure, departure for just cause of special education personnel

• Decrease in enrollment of children with disabilities• Termination of the obligation to provide special

education services to a child:– Left the jurisdiction of the agency;– Has reached the age at which the obligation has

terminated– No longer needs the program of special education

STEP 18 - Special EducationMaintenance of Effort ReportReduction to MOE Requirement under IDEA:

• Up to 50% of the increase in federal funds in the current year compared to the prior year may be used to reduce the required level of state and local expenditures

• This option can only be used if the LEA used the freed up funds for activities authorized under ESEA

• LEA must indicate how the freed up funds were used

STEP 18 - Subsequent Year Tracking WorksheetFederal Subsequent Year Rule:

In order to determine the required level of effort, the LEA must look back to the last fiscal year in which the LEA maintained effort using the same method by which is is currently establishing the compliance.

The Subsequent Year Tracking (SYT) Worksheet must be completed before the MOE - SEMB & SEMA Reports are finalized

STEP 18 - Subsequent Year Tracking WorksheetFederal Subsequent Year Worksheet:

● Complete one SYT Worksheet for both MOE Reports● 2011-12 Fiscal Year baseline year● Tracking the results for all four methods

- Combined state & local expenditures- Combined state & local expenditures per capita- Local expenditures only- Local expenditures only per capita

STEP 18b - Excess Cost Calculation

Excess cost are those cost for the education of an elementary school or secondary school student with a disability that are in excess of the average annual per student expenditure in an LEA

STEP 18b - Excess Cost CalculationImportant points in completing the Excess Cost Calculation

• Sections A - D are the expenditures for the prior year

• Sections E - F are the current year expenditures • Does not include expenditures for Infants or

Preschool Programs• Item #21 is not the same as Item #8:

– Item #8 is for the prior year– Item #21 is for the current year

• Item #21 should be a positive amount

STEP 19a - STRS On-BehalfAnd other Accounting and Financial Reporting for Pensions

• GASB 68: Pension Reporting– CalPERS - Government Wide reporting – Cal STRS - Government Wide reporting

• Work with your auditor for both CalPERS and Cal STRS

• Charters: may not be applicable - check with your auditor

• GASB 74 & 75: OPEB– Requires notes to financial statements– Uses Actuarial Study for valuations to report

STEP 19a - STRS On-BehalfRecording STRS On-Behalf under GASB 85

• Report in Fund Financial Statements– Entries for LEAs calculate and post into ESCAPE

BASC/ESSCO sub committees have provided the calculation for LEA use. See spreadsheet for Sonoma County on page 3 of Step 19a.

LEAs can take the amount calculated and plug into CDE on-behalf tool to get specific entries to enter. See pages 4 & 5 of Step 19a.

STRS On-Behalf Analysis Spreadsheet Application: See detailed instructions in Manual - pages Step 19a pages 4 & 5

● Click the SELECT and LOAD file button● Load the last saved UA reporting .DAT file● Enter the STRS on-behalf amount from BASC/ESSCO

calculation● Click Run Extract and Analysis● Journal entry is produced on the Journal entry tab. Use

this information to create a journal in ESCAPE.

Step 19bNancy Linder

Step #19b MaintenanceAll LEA’s are required to maintain facilities in good repair.

Restricted Maintenance resource 8150

Minimum contribution required unless exempt

3% of general fund expenditures and other financing uses

• based on 19-20 actual expenditures

Step #19b Maintenance (cont)

Deferred Maintenance Fund 14

A fund used to account separately for revenues that are restricted or committed for deferred maintenance purposes.

portion of LCFF committed for deferred maintenance

01-0000-0-0000-0000-8091-000-0000 (DEBIT)

14-0000-0-0000-0000-8091-000-0000 (CREDIT)

Step #20Review of Coding for SACS Form CEAImportant to import your budget into SACS during Year-End Close

process and review CEA Form.● If percent of current cost of education for the classroom does not meet the

minimum required percentage, district needs to look for potential coding errors and other issues that would affect the formula BEFORE closing your books.

8

Minimum Classroom Compensation Requirement:

Elementary 60%

Unified 55%

High School 50%

Step #20 (cont)Review of Coding for SACS Form CEA

Who is excluded from the CEA requirement?

➔ Districts with less than 101 units of ADA in the previous year➔ Charter Schools➔ Districts that maintain all “individual class sessions” with equal to or less than the following number

of pupils in attendance:◆ An elementary school district – 28 pupils◆ A high school district – 25 pupils◆ A unified school district:

● Grades K-8 – 28 pupils● Grades 9-12 – 25 pupils● Grades 7-9 of a junior high school shall be deemed to be high school grades for the

purposes of this section

(The number of pupils in attendance in each “individual class session” must not exceed the limit for a district to be exempt from the calculation. Ed code is not clear how the class size is calculated for this purpose. Some auditors check the daily count; others average class size by month. Check with your auditor before claiming the exemption.)

9

Step #20 (cont)Review of Coding for SACS Form CEA

Form CEA calculates the total classroom compensation percentage (Objects 1000-3999 and Functions 1000-1999) of the total actual expenditures in the general fund.

10

Classroom Compensation (Form CEA, Part II)Total Expenses (Form CEA, Part I)______________________________________

Classroom Compensation % =

The goal is to accurately reflect classroom compensation included in the formula (Part II – Minimum Classroom Compensation) and appropriately reduce or eliminate other costs from the total expenditures section (Part I – Current Expense Formula). Decreasing Total General Fund Expenditures (Part I), other than classroom salary and benefits, will increase the Classroom Compensation % and help to meet the minimum requirement.

Step #20Review of Coding for SACS Form CEA★ See page #2-3 of Step#20 in the manual for coding tips

★ Review expenditures that can be manually excluded from the calculation on the SACS Form. ○ It is recommended to receive auditor concurrence for any overrides.○ Even if you are exempt from the calculation or won’t make the

minimum percentage even after reviewing coding and overrides, it is still recommended to include any appropriate overrides in an effort to accurately disclose the true percentage.

★ Do NOT rely on an exemption. The circumstances under which the County Superintendent may grant an exemption from the requirements are defined very precisely (and narrowly) in the Ed Code:

○ The application of EC Section 41372 would result in a serious hardship to the district.

○ The application of EC Section 41372 would result in the district paying its classroom teachers salaries that exceed those of other districts of comparable type and functioning under comparable conditions.

11

Step #21: Linda Daugherty

Step 21: Transfers of Direct Costs Costs for services such as IT expenses, photocopying,

fieldtrips, etc. charged to goal 0000, or accumulated in a particular function.

Later, costs are distributed on the basis of a work order (ex. district grounds worker’s salary costs) by per unit or fee.

Accounting ex: object 5710 within same fund

Accounting ex: object 5750 not w/in same fund

CSAM Procedure 615, or Fiscal Advisor for help

Fund Resource Project Year Goal Function Object School Cr 01 0000 0 0000 3600 5710 000 Dr 01 0000 0 1110 1000 5710 000

Fund Resource Project Year Goal Function Object School Cr 01 0000 0 0000 7200 5750 000 Dr 25 9010 0 0000 7200 5750 000

Step 22: Indirect Cost & Function Coding

Page 1: Agency wide costs for general management such

as accounting, budgeting, purchasing, HR etc. Purpose: To charge a particular program a

portion of these support services, and thereby reflecting the program’s true costs.

Rates: Some programs have a capped rate or limited cost recovery not to exceed statewide average. Some do not allow any indirect costs.

Pages 4-6 includes the latest Charter and District Indirect Rates from the CDE

Step 22: Indirect Cost & Function Coding

Accounting: Recording Indirect Costs at budget and year-end examples provided on pages 1 & 2.

Page 2: Rate calculation: SACS Form ICR in the

Unaudited Actual software. Based on specific LEA general ledger data. Function driven.

Exclusions from calculation: Some cost categories are excluded from the rate calculation & are listed. New for 2019-20 is the exclusion of Food object 4700.

Step 22: Indirect Cost & Function Coding

Page 3: Function coding errors (TRC): Before it’s too

late to change account coding. Import into SACS2020ALL and review the 2019-20 rate as compared to prior years. Also, check for Function coding TRC errors.

Steps 23 & 24Nancy Linder

Step #23 Contributions Between Programs (object 8980 and object 8990)

From unrestricted resources

From restricted resources

Step #23 Contributions (cont)

Between Programs (object 8980 and object 8990)

Reminders:

To use Federal Transferability you must request through the consolidated application

Object 8980 must net to zero at fund level

Object 8990 must net to zero at fund level

Step #24 Determining Fund Balance vs Unearned RevenueBy resource – determine if fund balance is allowed

Refer to the CDE SACS Query Page

F subject to ending resource balance

U subject to unearned revenue

Ending resource balance must be zero

Unearned revenue may need to be posted

Step #24 Unearned Revenue (cont)

Step #24 Unearned Revenue (cont)

SACS2020ALL Form CAT

Optional toolavailable todocumentyear-endaccruals forrestrictedcategoricalprograms

Step 25: Review All Resources & Funds

All resources must have a positive or zero fund balance by June 30. Review each to dertermine none are negative, and that ending balances are allowed.

Resource Balance Review1) Run a Fiscal 13 report, sorted by resource in each fund.2) Determine that no resource has a negative ending balance. Options to clear….. Make sure all A/P and A/Rs were set up Transfer expenditures Contribution

Step 25: Review All Resources & Funds

Resource Balance Review

3) Deterimine which resources allow a positive ending balance SACS Query

4) Options to clear unallowable balance Set up Unearned Revenue Transfer expenditures Complete a contribution

Step 25: Review All Resources & Funds

Fund Balance Review1) Deterimine all funds have a positive ending balance at 6/30 Make sure all receivables, payables and

allowable costs & transfers have been recorded.

2) Options to clear a negative ending fund balance Temporary Loan – Must be completed by

6/23/20 Contribution – Must be completed by 6/23/20

Step 25: Review All Resources & Funds

Step 26Nancy Linder

Step #26 Review Expense Budget By Major Object Code

The total amount budgeted in each major expenditure classification is the maximum amount that can be expended in the school year. ref EdC 42600

Step #26 Review Expense Budget By Major Object Code

This year-end budget update is not intended to replace periodic budget updates & is not permitted for revenue updates.

After all checks are made and journals posted

Review the budget

Determine if expenditures exceed budget

Decide if a budget transfer is necessary

STEP 27 : GASB 34 and 84

• GASB 34: Fixed Asset reporting - Government Wide Financial Statements– ESCAPE has a fixed asset reporting system– If using a system outside of ESCAPE, be sure make sure the

total of the 6xxx accounts in ESCAPE agree with the current year additions to fixed assets in the system and reports used.

• GASB 84: Fiduciary Activities - ASB Reporting requirements– Implementation delayed to 2020-21 – Check in with your auditor to confirm their view of

reporting requirements– Start thinking about how you will implement during

2020-21 to be ready for the 2020-21 closing.

STEP 28 Account Coding

• Supplemental & Concentration Grant Coding– If using a locally defined unrestricted resource

• Unspent balances would appear subject to carryover, which is not the intent since dollars are unrestricted

• Object 8980 for recording contribution from RS 0000• E-Rate Reimbursements

– Record as local unrestricted revenue– Review CSAM Procedure 560

• Donated Food Commodities - Object 8221– Record value in Resource 5310 (or 5330)– 2019-20 Commodity value is $.3625– Multiply total lunches served by the commodity value– Record: debit object 4710, Credit object 8221

STEP 28 Audit RemindersBe ready for your Annual Audit!

• LCAP Audit Procedures– LCAP delay to 12/15/20 – NO CHANGES in audit process!

• Ratio of Administrative Employees to Teachers– Definitions and procedures detailed in Ed Code– Will be a finding if district cannot show it was in compliance

• Read / Review the 2019-20 Audit Guide found at http://eaap.ca.gov/audit-guide/current-audit-guide-booklet/

Wrapping up the CloseThree things that follow Steps 1 through 28:

29: After all of the above steps are completed, re-run Fiscal 15 to assure no open or pending transactions exist.

This is a double check measure!30 : Download to SACS2020ALL and Run TRC. Correct any fatal errors. Submit

w/this checklist.No detail is provided in manual.

31: Run ICR report (in SACS2020ALL) to review indirect cost rate.No detail is provided in manual.

PROVIDE the Year End Close Check-list (signed) and listed documents to SCOE staff as indicated!

Open Discussion

Open discussion time. All participants can unmute and start video.

Thank you!

Contact your SCOE Fiscal Advisor with individual questions about SACS

Contact your IT Analysts for help with ESCAPE!