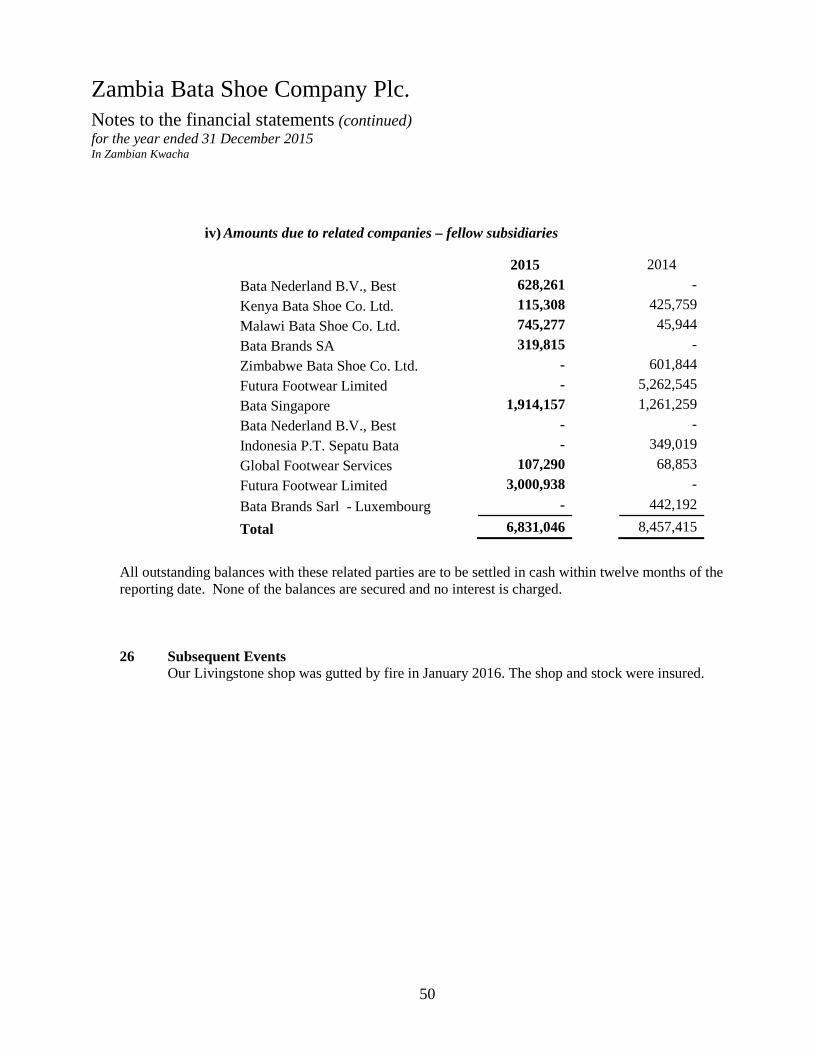

53

Zambia Bata Shoe Company Plc. Annual financial statements for the year ended 31 December 2015

Zambia Bata Shoe Company Plc. Annual financial statements for the year ended 31 December 2015

Zambia Bata Shoe Company Plc. Annual financial statements Contents Page Chairman’s report 1 - 3 Report of the Directors 4 - 5 Directors’ responsibilities in respect of the preparation of financial statements 6 Independent auditor’s report 7-8 Statement of financial position 9 Statement of profit or loss and other comprehensive income 10 Statement of changes in equity 11 Statement of cash flows 12 Notes to the financial statements 13 – 50 Appendix I 51

Zambia Bata Shoe Company Plc.

Chairman’s report

Ladies and Gentlemen,

1 Introduction

I am once again delighted to present my report to the 54th Annual General Meeting of our Company. Below are the highlights of the company’s performance for the year 2015.

HIGHLIGHTS 2015 2014 GROWTH Revenue 137,203,719 123,305,193 11% Gross profit 61,589,643 58,285,662 6% Profit before tax(PBT) 9,287,273 21,694,591 -57% Proposed dividend per share 0.06 0.09 -33% Earnings per share 0.07 0.17 -59%

2. Operating Environment

The Board would like to once again commend the Government of the Republic of Zambia for embracing viable economic policies and for creating an enabling and peaceful environment in which to do business. We take cognisance of the fact that there have been numerous challenges to both global and regional economies and Zambia was not spared. Our Government so far has managed to put in place measures that we believe will assist businesses to sustain operations and eventually begin to see improvements though this will also depend on major global players. Your company managed to avoid a loss situation through prudent management decisions even though the results were not as we are used to seeing.

3. Performance

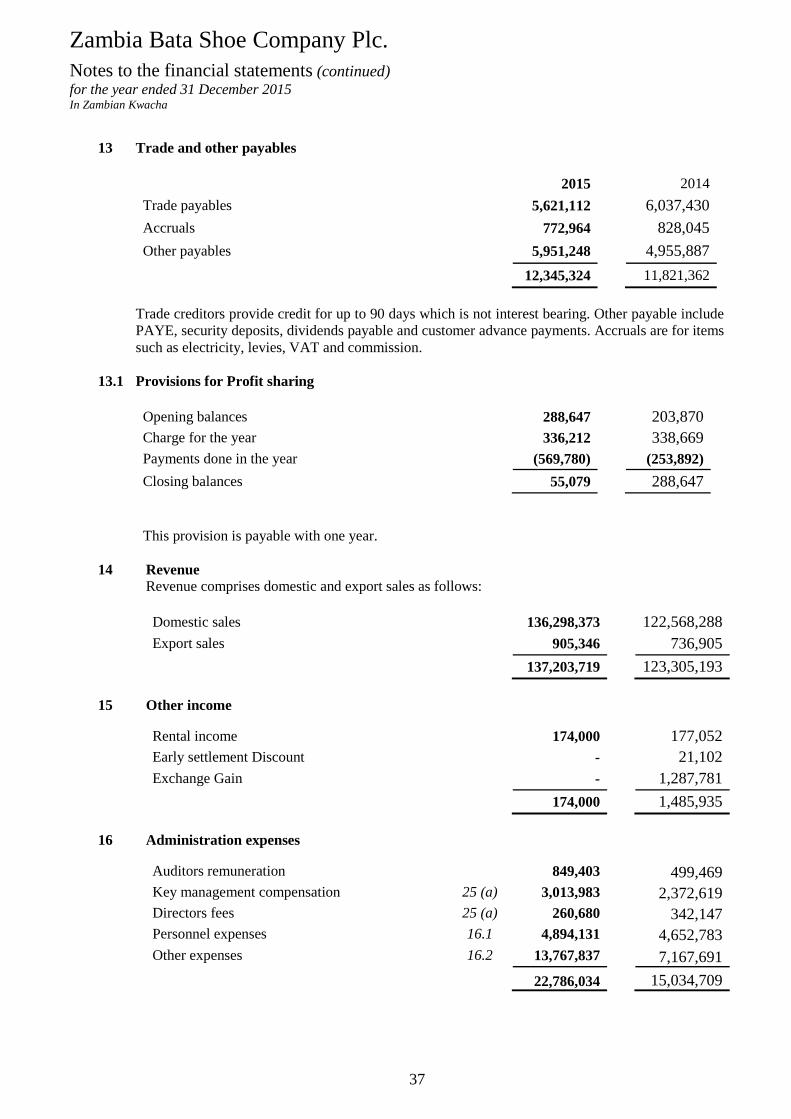

2015 was indeed very difficult and as we were unable to meet sale targets for the year. Sales in all provinces were down although the situation was worse in all our Copper belt stores. I am sure we are all aware of the problems that we continue to face in this area as there have been problems with most of the mines which employ the majority of people in this region. We are looking forward to improvement as this region is an important contributor to our sales. Central and Northern stores performed better than all other provinces and we intend to consolidate this position. This year, the first half of the year performed better than the last half and this was mainly due to good back to school business in both January and May. In the second half of the year, the situation was very dire for the Company as the seasonal sales for our gumboots was affected by the lack of rains which normally starts in October. Even our Christmas trade was also poor and not according to expectations. We however continue to dominate the Back to School business and we are taking all measures to consolidate and ensure all Primary and Secondary school going students wear Bata products. We are also ensuring that the needs of high school boys and girls are catered for as their needs are slightly different from the Junior and Primary Schools Due to these economic problems and the shrinking disposable income on the part of consumers and to achieve the results that we did despite all the mentioned problems, our merchandising team had to come up with a new template in providing our customers with good value products. We also continue to “Make Great Shoes Accessible” to everyone by making sure that we cater for different tastes and also that we cover the entire country with our distribution network. We have also started introducing in our top stores some international

1

Zambia Bata Shoe Company Plc

Chairman’s report (continued)

brands to satisfy the tastes of the upper end of our customers who demand these brands even though our core business remains firmly anchored in the middle to low segment of the market. These brands will include Clarks, Skechers for the time being. The response so far has been good and we will continue with this trend depending on the customer needs.

• Store Renovations

In the first half of the year, we carried out major store renovations in 13 of our stores across the country and opened 2 new shops. This was mainly done to keep us abreast of trends in other countries and to ensure that our customers enjoy shopping in all Bata stores. This also contributed to better trading conditions which we achieved in the first half of the year. This year we expect to gain full benefit of this investment as customers will find shopping in Bata stores very convenient. We also managed to launch in the last quarter the e-commerce shop which is dedicated to those who may find it difficult to travel and make a purchase in the Bata store, to make a purchase in the comfort of their homes and offices. This trend is gaining momentum in Africa and as everyone knows, this is the norm now in all developed countries. This e-commerce business may be small today, but is going to be the way to grow in the future and your company has already taken the lead.

• Staff Training

Training remains a very strong part of our business. For us to remain in our pole position in the market place, we have to equip our people with the required skills so that they can contribute meaningfully to the business. The organisation has fully equipped training academies both regionally and internationally and Bata Zambia participates fully in these training academies. In 2015 we sent a total of 14 employees to our training institutes in China and Kenya. These employees came from various disciplines in our sales, merchandising, operational and finance division. The skills they acquire will continue to help us in our operations and this exercise will be intensified in the following year.

4. Dividends

I am pleased to inform you that your Board of Directors has recommended a dividend of K0.06 on each ordinary share (K0.09 in 2014) held as at close of business on 20th April 2015 being the record date.

5. Outlook for 2016 As this trend of down turn in the world economy persists, and especially as the commodity prices remain depressed, our own economy which mainly depends on Copper will also remain subdued. We will have to put in place strong measures in managing our business so that we can come out of this even stronger than before. Like everyone else we have to strengthen our management team and look at our expenses. We will have to rationalise our cost structure and to ensure that we live within our means. All unnecessary costs will have to be shaded off so that we can come out with a lean structure. This together with other survival strategies will have to be seriously implemented for us to survive this period. We will also be Launching the Bata Loyalty Program in the first quarter of 2016. This is a customer reward program where we will be giving points to all customers who do purchases in any of our outlets. These loyal and regular customers will then be rewarded by giving them special discounts and will also be the first to come to our clearance centres where huge discounts will be given. This program will be massively advertised and we hope this will give everyone a reason to come to Bata store.

2

Zambia Bata Shoe Company Plc

Chairman’s report (continued)

We must point out however, that in spite of all these problems, Bata Zambia remains very much optimistic about good business prospects both in the short and long term. Our brand remains very popular in the market, all our stores are now world class and we have a distribution network second to none in this country. Above all we have well-trained and experienced personnel and we remain the best footwear chain in the country. Our merchandising team are building a collection which is second to none and we continue to witness excellent customer counts into our stores on a daily basis. We are now fully prepared for 2016 as we now have the experience of last year and we should do much better this coming year. We are gearing ourselves to this competition and we will be able to sustain our growth as we continue to make improvement in our people, product, store development and above all offering our customers excellent service. These are areas where we will continue to improve and to stay ahead. During this year 2016, we intend to open six new shops in the upcoming shopping malls and in other areas where there is potential to open street stores. We have also targeted to remodel 12 stores and furniture for this purpose is already in the country. All these measures will help us to maintain our pole position and move ahead in this market. We will also intensify training of our staff in all aspects of business. Our advertising has been re-engineered as we would once again want Bata to be a truly household name. We want all Zambians to think Bata whenever they want to purchase a pair of shoes and to be at the top of their mind for school shoes.

6. Conclusion

In conclusion, I would like to pay tribute to all employees of the Company for putting in such hard work and sacrifice especially considering the difficulty conditions we had to face this year and to achieve these results. I would also like to thank fellow members of the Board and the Bata International Group for their technical support. Hernan Vizcaya Chairman

3

Zambia Bata Shoe Company Plc. Report of the Directors for the year ended 31 December 2015 Share Capital During the year 2015, the authorised and issued share capital of the company remained at K 78, 000,000 and 76,107,600 respectively at K0.01 each.

Activities The principal business of Zambia Bata Shoe Company Plc. is the manufacture and trading in footwear and other leather and plastic products.

Results Due to the tough economic conditions we experienced in the year under review, business was very difficult but we still managed to avoid the worst. The company managed to achieve a growth of 11% in sales value compared to the previous year. Sales grew in 2015 to K 137,203,719 from K 123,305,193 in 2014. Profit before tax was less than the previous year due to the various factors, but mainly due to higher costs. We achieved profit before tax of K 9,287,273 compared to K 21,694,591achieved the previous year. The source of this information is the statement of profit and loss and other comprehensive income in the audited financial statements for 2015 Directors The Directors for the year 2015 were Messer’s Hernan Vizcaya, George Sokota, Charles Mate, Prosper Bachi, Hugo Vargas and Prashant Sharma. Messrs Hugo Vargas, Prashant Sharma and Hernan Vizcaya have resigned as board members. In place of Prashant Sharma who had replaced Hugo Vargas, the board is proposing John Murathe as proposed by the main Shareholder. All the Directors, having retired in accordance with the Company`s Articles of Association have offered themselves for re-election. Directors’ Interest in Ordinary Shares There are two directors out of five who have an interest in the shares of the Company. Mr C. Mate is associated with Hilda’s Hens Family Trust that holds 6,126,000 shares and G. Sokota through D.G. Partners hold 628,434 ordinary shares of the Company through D. G. Partners. There is no right to subscribe for equity or debt securities which has been granted to any Director. Employees The average number of employees employed by the Company during the year 2015 was 95 against 94 for the year 2014. The total amount paid to the employees during the period under review (in the form of salaries, wages, housing, allowances and provision for benefits) was K8 million against K7 million paid in 2014. Health, Safety and Welfare Our Company has strict rules with regards to Environmental Health and Safety (EH&S). The Company is a member of the Bata Shoe Organisation which has very elaborate and clear guidelines when it comes to looking after our environment and the safety of all our employees. The company conducts a comprehensive risk assessment of all environment issues including safety incidents that may occur on our site. We also have a Health and Safety Committee. Our safety committee works very closely with the Zambia Environmental Management Agency to ensure that we fully comply with all environmental regulations as amended from time to time. We also hold fire drills conducted by experts from the City`s Fire Department to ensure that in the event of fire every employee is aware of their duties and are also taught how to handle fire equipment. Basic first aid lessons are also conducted by our partners who are experts in the field and they also provide us with the basic first aid kits which are kept in our premises.

4

Zambia Bata Shoe Company Plc.

Report of the Directors (continued) for the year ended 31 December 2015 Company Social Responsibility The Company continues to play a positive role in alleviating some desperate cases of those in need in our society. To this effect, 2015 was no exception. The Company made donations to the following Organisations: The company organised a refurbishment of an entire block at the Kalingalinga clinic. We also donated school kits to the First Lady at State House. This was in aid of her projects with the disadvantaged children especially in the rural areas. During the year we were approached again by Bwafano School in Chezanga for some assistance for the children from the very poor backgrounds and we donated some school shoes and school bags. The amount covered by these activities totalled ZMK 31,000 Your Company will continue to give assistance whenever possible. Registration The Company commenced its operations in the country in 1937. Zambia Bata Shoe Company Plc. is a public company, which was incorporated in the then Northern Rhodesia originally as a private company on 14 August 1963. In 1973, Zambia Bata Shoe Company became a public company with Zambians holding 15.5% of the share capital. The company was quoted on the LuSE in 1994 and finally moved to the listed tier on March 30, 2009. Presently more than 400 Zambians hold 26% of the company’s share capital which translates to 19,235,598 shares Corporate Governance The Board of Directors hereby confirms that the Company has complied with all the internal control aspects of the principles of good governance. The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and comply with the Companies Act 1994. The Company has no service contracts with any of the Directors, except for the Managing Director and the Finance Director. There have been no contracts of significance subsisting during or at the end of the financial year in which any Director has been materially interested. Proposed Dividend Your Board of Directors is pleased to recommend a final dividend of K0.06 ( 6 Ngwee) per share, which represent 67% of the previous year, for the record date of 15th April 2016 and payable on 18th April 2016. . By order of the Board Company Secretary

5

Zambia Bata Shoe Company Plc. Directors' responsibilities in respect of the preparation of financial statements The Company’s directors are responsible for the preparation and fair presentation of the financial statements of Zambia Bata Shoe Company Plc., comprising the statement of financial position as at 31 December 2015, and the statements of profit or loss and other comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements which include a summary of significant accounting policies and other explanatory notes in accordance with International Financial Reporting Standards, and the requirements of the Companies Act of Zambia. In addition, the directors are responsible for preparing the director’s report. The directors are also responsible for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error, and for maintaining adequate accounting records and an effective system of risk management as well as the preparation of the supplementary schedules included in these financial statements. The directors have made an assessment of the Company’s ability to continue as a going concern and have no reason to believe the Company will not be a going concern in the year ahead. The auditor is responsible for reporting on whether the annual financial statements are fairly presented in all material respects in accordance with International Financial Reporting Standards, and the requirements of the Companies Act of Zambia. Approval of the financial statements The annual financial statements, of the Company as identified in the first paragraph were approved by the Directors on 18th February 2016 and were signed on their behalf by: ................................................... …………………………………. Director Director

6

Independent Auditors' Report To the members of Zambia Bata Shoe Company Limited Plc. Report on the Financial Statements We have audited the financial statements of Zambia Bata Shoe Company Limited Plc., which comprise the statement of financial position as at 31 December 2015, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes, as set out on pages 8 to 50. Directors' Responsibility for the Financial Statements The company’s directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and requirements of the Companies Act, 1994 of Zambia, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatements, whether due to fraud or error. Auditors' Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of Zambia Bata Shoe Company Plc. as at 31 December 2015, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards, and the requirements of the Companies Act of Zambia.

7

Report on Other Legal and Regulatory Requirements As required by the Companies Act of Zambia we report to you, based on our audit, that: (a) we have obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit; (b) in our opinion proper books of accounts, other records and registers have been kept by the company, so far as appears from our examination of those books and registers; and (c) the company's statement of financial position and profit and loss account are in agreement with the books of account. Ernst & Young Chartered Accountants Henry C Nondo Partner Lusaka

8

Zambia Bata Shoe Company Plc.

Statement of financial position as at 31 December 2015

In Zambian Kwacha

Note 2015

2013 Assets

Property, plant and equipment 7 67,642,001 68,134,612 Intangible assets 7.1 194,406 37,732 Total non – current assets 67,836,407 68,172,344

Inventories 8 41,347,752 48,018,401 Amounts due from related companies 25 1,591,730 1,682,526 Trade and other receivables 9 5,471,431 4,826,887 Cash and cash equivalents 10 1,869,299 3,234,430 Total current assets 50,280,212 57,762,244

Total assets 118,116,619 125,934,588

Equity Share capital 11 761,076 761,076

Revaluation reserve

31,005,920

32,009,649 Retained earnings 50,388,237 50,626,214 Total equity 82,155,233 83,396,939

Liabilities Deferred tax liability 12 16,030,911 18,545,491 Total non-current liabilities 16,030,911 18,545,491

Current tax payable 19 699,026 3,424,734 Trade and other payables 13 12,345,324 11,821,362 Provisions 13.1 55,079 288,647 Amounts due to related companies 25 6,831,046 8,457,415 Total current liabilities 19,930,475 23,992,158

Total liabilities 35,961,386 42,537,649

Total equity and liabilities 118,116,619 125,934,588

These financial statements were approved by the board of directors on 31st March 2015 and were signed by: ................................... ................................. Director Director The notes on pages 12 to 50 form an integral part of these financial statements.

9

Zambia Bata Shoe Company Plc.

Statement of profit or loss and other comprehensive income for the year ended 31 December 2015

In Zambian Kwacha

Note 2015

2014

Revenue 14 137,203,719

123,305,193 Cost of sales

(75,614,076)

(65,019,531)

Gross profit

61,589,643

58,285,662

Other income 15 174,000

1,485,935

61,763,643

59,771,597

Administration expenses 16 (22,786,034)

(15,034,709)

Operating expenses 17 (28,299,336)

(22,948,392) Total expenses

(51,085,370)

(37,983,101)

Operating profit

10,678,273

21,788,496

Finance expense 18 (1,391,000)

(93,905)

Profit before tax

9,287,273

21,694,591

Income tax expense 19 (3,679,235)

(8,879,551)

Profit for the year

5,608,038

12,815,040

Other comprehensive income

Items that will never be reclassified to profit or loss

Revaluation surplus

-

31,496,569 Deferred Tax

-

(11,023,799)

Total other comprehensive income net of Deferred tax

-

20,472,770

Total comprehensive income for the year

5,608,038

33,287,810

Earnings per share

Basic / diluted

0.07 0.17 The notes on pages 13 to 49 form an integral part of these financial statements

10

Zambia Bata Shoe Company Plc.

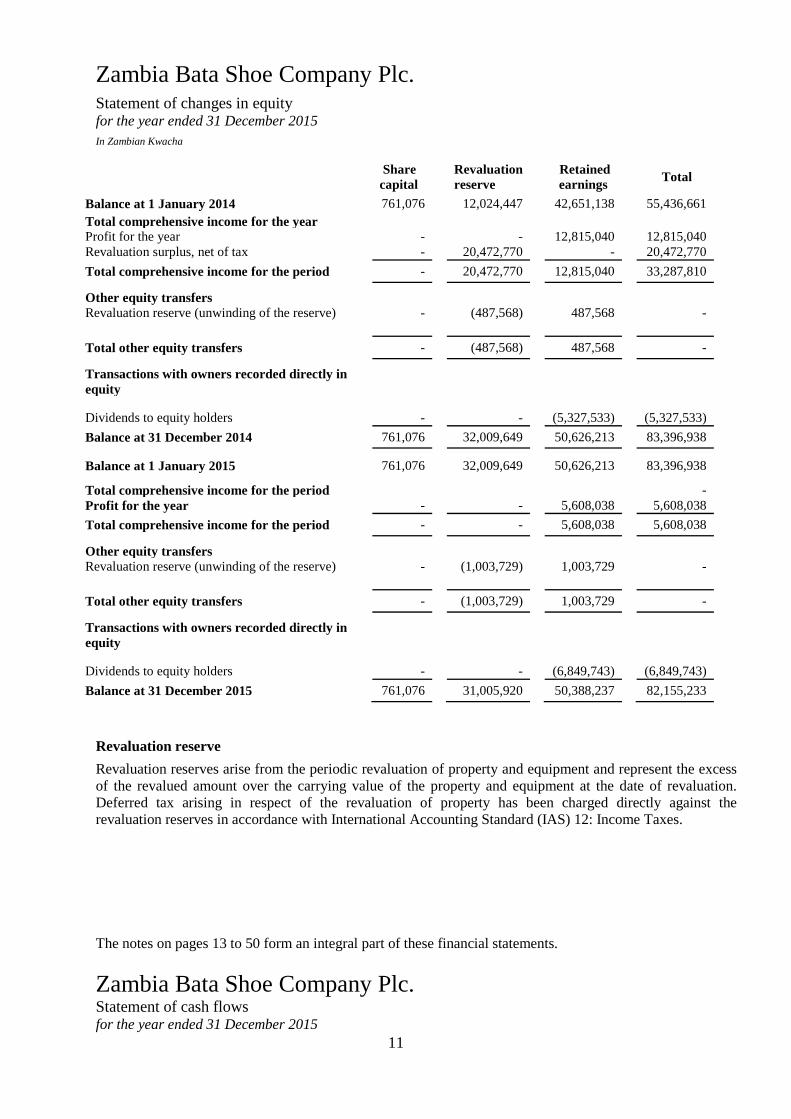

Statement of changes in equity for the year ended 31 December 2015

In Zambian Kwacha

Share capital

Revaluation reserve

Retained earnings Total

Balance at 1 January 2014 761,076 12,024,447 42,651,138 55,436,661 Total comprehensive income for the year Profit for the year - - 12,815,040 12,815,040 Revaluation surplus, net of tax - 20,472,770 - 20,472,770 Total comprehensive income for the period - 20,472,770 12,815,040 33,287,810

Other equity transfers Revaluation reserve (unwinding of the reserve) - (487,568) 487,568 -

Total other equity transfers - (487,568) 487,568 -

Transactions with owners recorded directly in equity

Dividends to equity holders - - (5,327,533) (5,327,533) Balance at 31 December 2014 761,076 32,009,649 50,626,213 83,396,938

Balance at 1 January 2015 761,076 32,009,649 50,626,213 83,396,938

Total comprehensive income for the period - Profit for the year - - 5,608,038 5,608,038 Total comprehensive income for the period - - 5,608,038 5,608,038

Other equity transfers Revaluation reserve (unwinding of the reserve) - (1,003,729) 1,003,729 - Total other equity transfers - (1,003,729) 1,003,729 -

Transactions with owners recorded directly in equity

Dividends to equity holders - - (6,849,743) (6,849,743) Balance at 31 December 2015 761,076 31,005,920 50,388,237 82,155,233

Revaluation reserve

Revaluation reserves arise from the periodic revaluation of property and equipment and represent the excess of the revalued amount over the carrying value of the property and equipment at the date of revaluation. Deferred tax arising in respect of the revaluation of property has been charged directly against the revaluation reserves in accordance with International Accounting Standard (IAS) 12: Income Taxes.

The notes on pages 13 to 50 form an integral part of these financial statements. Zambia Bata Shoe Company Plc. Statement of cash flows for the year ended 31 December 2015

11

In Zambian Kwacha

Note 2015

2014

Cash flows from operating activities Profit before tax

9,287,274

21,694,591

Adjustment for:

Depreciation 7 6,324,326

4,166,562

Unrealised exchange differences 3,054,903 (1,287,779)

Equipment & Spare parts expensed - 106,942

Reversal of impairment of inventory 8 (733,178)

392,103

Provisions for Profit sharing 13.1 336,212 338,669

Impairment of receivables 22 (12,250)

574,961

Amortisation of intangible assets 7.1 20,742

14,954

Loss on disposal of equipment

164,378

-

Finance expense 18 1,391,000

93,905

19,833,407

26,094,908

Changes in:

- inventories

7,403,827

(19,146,521)

- trade and other receivables

(632,294)

(2,477,512)

- balances due from related companies

658,413

14,995

- balances due to related companies

(4,082,086)

4,027,010

- Provisions (569,780) (253,892)

- trade and other payables

(496,270)

7,743,240

Cash generated from operating activities

22,115,217

16,002,226 Income tax paid 19 (8,919,524)

(5,738,074)

Interest received 18 -

-

Interest expense paid 18 (1,391,000)

(93,905)

Net cash from operating activities

11,804,693

10,170,247

Cash flows from investing activities

Purchase of property plant and equipment 7 (6,333,408)

(5,934,578)

Acquisition of intangible assets 7.1 (177,416)

(21,429)

Proceeds from disposal of equipment 337,315 -

Net cash used in investing activities

(6,173,509)

(5,956,007)

Cash flows from financing activities

Dividends paid

(6,849,743)

(5,327,533)

Net cash used in financing activities

(6,849,743)

(5,327,533)

Net increase/(decrease) in cash and cash equivalents

(1,218,559)

(1,113,291)

Cash and cash equivalents at 1 January

3,234,430

4,342,474

Effect of exchange rate fluctuations on cash held

(146,572)

5,247

Cash and cash equivalents at 31 December 10 1,869,299

3,234,430

The notes on pages 13 to 50 form an integral part of these financial statements.

12

Zambia Bata Shoe Company Plc.

Notes to the financial statements for the year ended 31 December 2015

1 Principal business activity

Zambia Bata Shoe Company Plc. (“the Company”) is domiciled in Zambia. The address of the Company’s registered office is plot 6437, Mukwa Road, Lusaka. The Company is engaged in the business of manufacturing and trading in shoes, other leather and plastic products.

2 Basis of preparation

(a) Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs) and the requirements of the Companies Act of Zambia.

Details of the Company’s accounting policies, including changes during the year, are included in Notes 3 to 6.

(b) Functional and presentation currency

These financial statements are presented in Zambian Kwacha (“Kwacha”), which is the Company’s functional and presentation currency.

3 Use of estimates and judgements

The preparation of the Company’s financial statements requires management to make judgements, estimates and assumptions that affect the reported amounts of revenues, expenses, assets and liabilities, and the accompanying disclosures, and the disclosure of contingent liabilities. Uncertainty about these assumptions and estimates could result in outcomes that require a material adjustment to the carrying amount of assets or liabilities affected in future periods. In the process of applying the Company’s accounting policies, management has made various judgements. Those which management has assessed to have the most significant effect on the amounts recognised in the financial statements have been discussed in the individual notes of the related financial statement line items. The Company based its assumptions and estimates on parameters available when the financial statements were prepared. Existing circumstances and assumptions about future developments, however, may change due to market changes or circumstances arising that are beyond the control of the Company. Such changes are reflected in the assumptions when they occur. The company made estimates in making provisions for bad debts on trade receivables and in assessing residual values, provision for inventory write offs and useful lives of property, plant and equipment. The aging of trade receivables was used in making a determination of amounts to be provided for while managements experience was used in determining residual values and useful lives.

13

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

3 Use of estimates and judgements (continued)

Measurement of fair values The Company measures land, building and equipment at fair value.

The Company has an established control framework with respect to the measurement of fair values.

When measuring the fair value of an asset or a liability, the Company uses market observable data as far as possible. Fair values are categorised into different levels in a fair value hierarchy based on the inputs used in the valuation techniques as follows:

Level 1: quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2: inputs other than quoted prices included in Level 1 that are observable for the

asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices). Level 3: inputs for the asset or liability that are not based on observable market data

(unobservable inputs).

If the inputs used to measure the fair value of an asset or a liability might be categorised in different levels of the fair value hierarchy, then the fair value measurement is categorised in its entirety in the same level of the fair value hierarchy as the lowest level input that is significant to the entire measurement.

Further information about the assumptions made in measuring fair values is included in the following notes: Note 7 – Property, plant and equipment (revaluation of property).

4A Changes in accounting policies The accounting policies adopted by the Company are consistent with those of the prior year.

Amendments and improvements to standards that became effective for the Company in the current year did not have a material impact on the company’s financial results.

14

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

4B Standards issued but not yet effective

Below is the listing of standards issued but not yet effective which are reasonably expected to impact the Company in the future. Amendments to IAS 16 and IAS 38: Clarification of Acceptable Methods of Depreciation and Amortisation The amendments clarify the principle in IAS 16 and IAS 38 that revenue reflects a pattern of economic benefits that are generated from operating a business (of which the asset is part) rather than the economic benefits that are consumed through use of the asset. As a result, a revenue-based method cannot be used to depreciate property, plant and equipment and may only be used in very limited circumstances to amortise intangible assets. The amendments are effective prospectively for annual periods beginning on or after 1 January 2016, with early adoption permitted. These amendments are not expected to have any impact to the Company given that the Company has not used a revenue-based method to depreciate its non-current assets. Annual Improvements 2012-2014 Cycle These improvements are effective for annual periods beginning on or after 1 January 2016. They include: IFRS 5 Non-current Assets Held for Sale and Discontinued Operations Assets (or disposal Companies) are generally disposed of either through sale or distribution to owners. The amendment clarifies that changing from one of these disposal methods to the other would not be considered a new plan of disposal, rather it is a continuation of the original plan. There is, therefore, no interruption of the application of the requirements in IFRS 5. This amendment must be applied prospectively. IFRS 7 Financial Instruments: Disclosures (i) Servicing contracts The amendment clarifies that a servicing contract that includes a fee can constitute continuing involvement in a financial asset. An entity must assess the nature of the fee and the arrangement against the guidance for continuing involvement in IFRS 7 in order to assess whether the disclosures are required. The assessment of which servicing contracts constitute continuing involvement must be done retrospectively. However, the required disclosures would not need to be provided for any period beginning before the annual period in which the entity first applies the amendments. (ii) Applicability of the amendments to IFRS 7 to condensed interim financial statements The amendment clarifies that the offsetting disclosure requirements do not apply to condensed interim financial statements, unless such disclosures provide a significant update to the information reported in the most recent annual report. This amendment must be applied retrospectively.

15

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

Changes in accounting policies, (continued)

IAS 19 Employee Benefits The amendment clarifies that market depth of high quality corporate bonds is assessed based on the currency in which the obligation is denominated, rather than the country where the obligation is located. When there is no deep market for high quality corporate bonds in that currency, government bond rates must be used. This amendment must be applied prospectively. There is no impact on the company on this change as the company only has a defined contribution pension plan. IAS 34 Interim Financial Reporting The amendment clarifies that the required interim disclosures must either be in the interim financial statements or incorporated by cross-reference between the interim financial statements and wherever they are included within the interim financial report (e.g., in the management commentary or risk report). The other information within the interim financial report must be available to users on the same terms as the interim financial statements and at the same time. This amendment must be applied retrospectively. The company will consider the amendments, once effective, when preparing its interim financial statements. Amendments to IAS 1 Disclosure Initiative The amendments to IAS 1 Presentation of Financial Statements clarify, rather than significantly change, existing IAS 1 requirements. The amendments clarify: The materiality requirements in IAS 1

That specific line items in the statement(s) of profit or loss and OCI and the statement of financial position may be disaggregated

That entities have flexibility as to the order in which they present the notes to financial statements

That the share of OCI of associates and joint ventures accounted for using the equity method must be presented in aggregate as a single line item, and classified between those items that will or will not be subsequently reclassified to profit or loss

Furthermore, the amendments clarify the requirements that apply when additional subtotals are presented in the statement of financial position and the statement(s) of profit or loss and OCI. These amendments are effective for annual periods beginning on or after 1 January 2016, with early adoption permitted. These amendments are not expected to have any impact on the Company, but the Company will consider the flexibility offered by the amendments when preparing its financial statements

16

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

Amendments to IFRS 10, IFRS 12 and IAS 28 Investment Entities: Applying the Consolidation Exception the amendments address issues that have arisen in applying the investment entities exception under IFRS 10. The amendments to IFRS 10 clarify that the exemption from presenting consolidated financial statements applies to a parent entity that is a subsidiary of an investment entity, when the investment entity measures all of its subsidiaries at fair value. Furthermore, the amendments to IFRS 10 clarify that only a subsidiary of an investment entity that is not an investment entity itself and that provides support services to the investment entity is consolidated. All other subsidiaries of an investment entity are measured at fair value. The amendments to IAS 28 allow the investor, when applying the equity method, to retain the fair value measurement applied by the investment entity associate or joint venture to its interests in subsidiaries. These amendments must be applied retrospectively and are effective for annual periods beginning on or after 1 January 2016, with early adoption permitted. These amendments are not expected to have any impact on the Company as it is not an investment entity, is not a subsidiary of an investment entity and does not have investees that are investment entities.

IFRS 9 Financial Instruments In July 2014, the IASB issued the final version of IFRS 9 Financial Instruments that replaces IAS 39 Financial Instruments: Recognition and Measurement and all previous versions of IFRS 9. IFRS 9 brings together all three aspects of the accounting for financial instruments project: classification and measurement, impairment and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted. Except for hedge accounting, retrospective application is required but providing comparative information is not compulsory. For hedge accounting, the requirements are generally applied prospectively, with some limited exceptions. The Company plans to adopt the new standard on the required effective date. During 2015, the Company has performed a high-level impact assessment of all three aspects of IFRS 9. This preliminary assessment is based on currently available information and may be subject to changes arising from further detailed analyses or additional reasonable and supportable information being made available to the Company in the future. Overall, the Company expects no significant impact on its balance sheet and equity except for the effect of applying the impairment requirements of IFRS 9. The Company expects a higher loss allowance resulting in a negative impact on equity and will perform a detailed assessment in the future to determine the extent. (a) Classification and measurement The Company does not expect a significant impact on its balance sheet or equity on applying the classification and measurement requirements of IFRS 9. Loans as well as trade receivables are held to collect contractual cash flows and are expected to give rise to cash flows representing solely payments of principal and interest. Thus, the Company expects that these will continue to be measured at amortised cost under IFRS 9. However, the Company will analyse the contractual cash flow characteristics of those instruments in more detail before concluding whether all those instruments meet the criteria for amortised cost measurement under IFRS 9.

17

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015 (b) Impairment IFRS 9 requires the Group to record expected credit losses on all of its debt securities, loans and trade receivables, either on a 12-month or lifetime basis. The Company expects to apply the simplified approach and record lifetime expected losses on all trade receivables. The Company expects a significant impact on its equity due to unsecured nature of its loans and receivables, but it will need to perform a more detailed analysis which considers all reasonable and supportable information, including forward-looking elements to determine the extent of the impact. (c) Hedge accounting IFRS 9 does not change the general principles of how an entity accounts for effective hedges. The company has not entered into any hedge agreements. IFRS 15 Revenue from Contracts with Customers IFRS 15 was issued in May 2014 and establishes a five-step model to account for revenue arising from contracts with customers. Under IFRS 15, revenue is recognised at an amount that reflects the consideration to which an entity expects to be entitled in exchange for transferring goods or services to a customer. The new revenue standard will supersede all current revenue recognition requirements under IFRS. Either a full retrospective application or a modified retrospective application is required for annual periods beginning on or after 1 January 2018. Early adoption is permitted. The Company plans to adopt the new standard on the required effective date and will apply it prospectively as there are no contracts that will be affected by the adoption. During 2015, the Company performed a preliminary assessment of IFRS 15, which is subject to changes arising from a more detailed ongoing analysis. The company is in the business of selling shoes, bags and other shoe related products. (a) Sale of goods Contracts with customers in which shoes and other products sale is the only performance obligation are not expected to have any impact on the Company. The Company expects the revenue recognition to occur at a point in time when control of the asset is transferred to the customer, generally on delivery of the goods. In applying IFRS 15, the Group considered the following: (i) Variable consideration Some contracts with customers provide a right of return, trade discounts or volume rebates. Currently, the Company recognises revenue from the sale of goods measured at the fair value of the consideration received or receivable, net of returns and allowances, trade discounts and volume rebates. If revenue cannot be reliably measured, the Company defers revenue recognition until the uncertainty is resolved. Such provisions give rise to variable consideration under IFRS 15, and will be required to be estimated at contract inception. IFRS 15 requires the estimated variable consideration to be constrained to prevent over-recognition of revenue. However the company does not expect to have instances where the consideration cannot be determined.

18

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015 (ii) Loyalty points programme The Company has an intention to introduce loyalty programmes in the coming years and the Company determines that the loyalty programme offered will give rise to a separate performance obligation because it provides a material right to the customer. Thus, it will need to allocate a portion of the transaction price to the loyalty programme based on relative stand-alone selling price instead of the allocation methodologies allowed under IFRIC 13 Customer Loyalty Programmes. IFRS 16 - Leases The International Accounting Standards board (IASB) issued IFRS 16 in January 2016 which requires lessees to recognize assets and liabilities for most leases on their balance sheets. Under the new standard, a lease is a contract or part of a contract that conveys the right to use an asset for a period of time in exchange for consideration. To be a lease, a contract must convey the right to control the use of the identified asset, which could be a physically distinct portion of an asset. The standard will be effective for annual periods beginning on or after 1 January 2019.The Company is still assessing the impact of the standard.

5 Significant accounting policies

The accounting policies set out below have been applied consistently to all periods presented in these financial statements.

(a) Foreign currency transactions

Transactions in foreign currencies are translated to the functional currency of the Company at the foreign exchange rate ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated at the foreign exchange rate ruling at that date. Foreign exchange differences arising on translation or settlement of foreign denominated monetary assets and liabilities are recognised in profit or loss. Non-monetary assets and liabilities denominated in foreign currencies, which are stated at historical cost, are translated at the foreign exchange rate ruling at the date of the transaction.

(b) Revenue

Revenue from the sale of goods is measured at the fair value of the consideration received or receivable, net of returns and allowances, trade discounts and volume rebates. Revenue is recognised when the significant risks and rewards of ownership have been transferred to the buyer, recovery of the consideration is probable, the associated costs and possible return of goods can be estimated reliably, and there is no continuing management involvement with the goods and the amount of revenue can be measured reliably. If it is probable that discounts will be granted and the amount can be measured reliably, then the discount is recognised as a reduction of revenue as the sales are recognised. Risks and rewards pass on delivery.

(c) Inventories

Inventories are measured at the lower of cost and net realisable value. The cost of

inventories is based on the first in-first out (FIFO) method. Cost includes direct costs and production overheads incurred in bringing goods to their present location and condition. Net realisable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and selling expenses.

19

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

(d) Financial instruments

A financial instrument is any contract that gives rise to a financial asset of one entity

and a financial liability or equity instrument of another entity.

i) Financial assets Initial recognition and measurement Financial assets are classified, at initial recognition, as financial assets at fair value through profit or loss, loans and receivables, held-to-maturity investments, Availabe For Sale (AFS) financial assets, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. All financial assets are recognised initially at fair value plus, in the case of financial assets not recorded at fair value through profit or loss, transaction costs that are attributable to the acquisition of the financial asset. Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the market place (regular way trades) are recognised on the trade date, i.e., the date that the company commits to purchase or sell the asset. Subsequent measurement For purposes of subsequent measurement financial assets are classified in four categories:

► Financial assets at fair value through profit or loss ► Loans and receivables ► Held-to-maturity investments ► AFS financial assets

The Company’s financial assets, which comprise trade and other receivables, amounts due from related Companies and cash and cash equivalents, are all classified as loans and receivables. Loans and receivables This category is the most relevant to the company. Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial measurement, such financial assets are subsequently measured at amortised cost using the effective interest rate (EIR) method, less impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included in finance income in the statement of profit or loss. The losses arising from impairment are recognised in the statement of profit or loss in finance costs for loans and in cost of sales or other operating expenses for receivables. This category generally applies to trade and other receivables. For more information on receivables, refer to Note 9

20

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

Derecognition A financial asset (or, where applicable, a part of a financial asset or part of a group of similar financial assets) is primarily derecognised (i.e., removed from the Company’s statement of financial position) when:

► The rights to receive cash flows from the asset have expired Or

► The Company has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party under a ‘pass-through’ arrangement; and either (a) the company has transferred substantially all the risks and rewards of the asset, or (b) the company has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset

When the company has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, it evaluates if and to what extent it has retained the risks and rewards of ownership. When it has neither transferred nor retained substantially all of the risks and rewards of the asset, nor transferred control of the asset, the company continues to recognise the transferred asset to the extent of the company’s continuing involvement. In that case, the company also recognises an associated liability. The transferred asset and the associated liability are measured on a basis that reflects the rights and obligations that the company has retained. Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Company could be required to repay. Impairment of financial assets Further disclosures relating to impairment of financial assets are also provided in the Trade receivables Note 9. The company assesses, at each reporting date, whether there is objective evidence that a financial asset or a group of financial assets is impaired. An impairment exists if one or more events that has occurred since the initial recognition of the asset (an incurred ‘loss event’), has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the debtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganisation and observable data indicating that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults. Financial assets carried at amortised cost For financial assets carried at amortised cost, the Company first assesses whether impairment exists individually for financial assets that are individually significant, or collectively for financial assets that are not individually significant. If the Company determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial

21

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognised are not included in a collective assessment of impairment. The amount of any impairment loss identified is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future expected credit losses that have not yet been incurred). The present value of the estimated future cash flows is discounted at the financial asset’s original effective interest rate The carrying amount of the asset is reduced through the use of an allowance account and the loss is recognised in the statement of profit or loss. Interest income (recorded as finance income in the statement of profit or loss) continues to be accrued on the reduced carrying amount and is accrued using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss. Loans together with the associated allowance are written off when there is no realistic prospect of future recovery and all collateral has been realised or has been transferred to the Company. If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognised, the previously recognised impairment loss is increased or reduced by adjusting the allowance account. If a write-off is later recovered, the recovery is credited to finance costs in the statement of profit or loss. ii) Financial liabilities Initial recognition and measurement Financial liabilities are classified, at initial recognition, as financial liabilities at fair value through profit or loss, loans and borrowings, payables, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. All financial liabilities are recognised initially at fair value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs. The Company’s financial liabilities include trade and other payables and amounts due to related parties.

After initial recognition, trade and accounts payable and amounts due to group companies are subsequently measured at amortised cost using the effective interest rate method. Gains and losses are recognised in profit or loss when the liabilities are derecognised as well as through the effective interest rate method (EIR) amortisation process. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortisation is included in finance costs in the statement of comprehensive income Derecognition A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as the derecognition of the original liability and the recognition of a new liability. The difference in the respective carrying amounts is recognised in the statement of profit or loss

22

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

(iii) Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount reported in the consolidated statement of financial position if, and only if, there is a currently enforceable legal right to offset the recognised amounts and there is an intention to settle on a net basis, or to realise the assets and settle the liabilities simultaneously.

(e) Share capital

Ordinary shares Incremental costs directly attributable to the issue of ordinary shares, net of any tax effects, are recognised as a deduction from equity.

(g) Property, plant and equipment

(i) Recognition and measurement

Items of property, plant and equipment are either measured at cost or re-valued amount less accumulated depreciation and accumulated impairment losses.

Land, buildings and Equipment are measured at revalued amounts less

accumulated depreciation and accumulated impairment losses.

Fixtures, equipment and motor vehicles are measured at cost less accumulated depreciation and accumulated impairment losses.

Cost includes expenditure that is directly attributable to the acquisition of the

asset. The cost of self-constructed assets includes the cost of materials and direct labour, any other costs directly attributable to bringing the assets to working conditions for their intended use, the costs of dismantling and removing the items and restoring the site on which they are located and capitalised borrowing cost.

When parts of an item of property, plant and equipment have different useful

lives, they are accounted for as separate items (major components) of property, plant and equipment.

Gains and losses on disposal of an item of property, plant and equipment are

determined by comparing the proceeds from disposal with the carrying amount of property and equipment, and are recognised net within other income in profit or loss. When re-valued assets are sold, the amounts included in the revaluation reserve are transferred to retained earnings.

23

Zambia Bata Shoe Company Plc. Notes to the financial statements (continued) for the year ended 31 December 2015 5 Significant accounting policies (continued)

(ii) Subsequent costs

The cost of replacing a part of an item of property, plant and equipment is

recognised in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Company and its cost can be measured reliably. The carrying amount of the replaced part is derecognised in profit or loss as incurred. On-going repairs and maintenance is expensed as incurred.

(iii) Depreciation

Depreciation is calculated over the depreciable amount, which is the cost of an asset, less its residual value.

Depreciation is recognised in profit or loss on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment, since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset.

The estimated useful lives for the current and comparative periods are as follows: Buildings 20 years Computer and other Equipment 4 and 10 years Motor vehicles 4 years Furniture and fixtures 5-10 years Land is not depreciated

Depreciation methods, useful lives and residual values are reviewed at each

financial year-end and adjusted if appropriate.

(iv) Revaluation An external, independent valuation expert, having appropriate recognised professional qualifications and recent experience in the location and category of property being valued, values the Company’s land and buildings and equipment frequently. The fair values are based on market values, being the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at measurement date.

(v) Revaluation surplus

The surplus arising on the revaluation of properties is initially credited to a revaluation surplus, which is a non-distributable reserve. A transfer is made (net of tax) from this reserve to retained earnings each year, equivalent to the difference between the actual depreciation charge for the year and the depreciation charge based on historical values, in respect of the re-valued assets.

24

Zambia Bata Shoe Company Plc. Notes to the financial statements (continued) for the year ended 31 December 2015 5 Significant accounting policies (continued)

(v) Revaluation surplus (continued)

If the asset’s carrying amount is decreased as a result of a revaluation, the decrease is recognised in other comprehensive income to the extent of any credit balance existing in the revaluation surplus in respect of that asset, thereafter the remaining decrease is recognised in profit or loss.

(vi) Derecognition

An item of property, plant and equipment is derecognised on disposal or when it is withdrawn from use and no future economic benefits are expected from its disposal. The gain or loss on disposal is recognised in profit and loss.

(h) Intangible assets

Recognition and measurement The Company’s intangible assets comprise computer software. Intangible assets acquired separately are recognised at cost less accumulated amortisation and accumulated impairment losses . Subsequent expenditure Subsequent expenditure on intangible assets is capitalised only when it increases the future economic benefits embodied in the specific asset it relates to. All other expenditure is expensed as incurred.

Amortisation

Amortisation is charged on a straight line basis over their estimated useful lives from the date that it is available for use. Amortisation methods, useful lives and residual values are reviewed at the reporting date and adjusted if appropriate. The effects of any changes in estimates are accounted for on a prospective basis. Software is amortised over three years.

Derecognition An intangible asset is derecognised on disposal or when it is withdrawn from use and no future economic benefits are expected from its disposal.

The gain/loss arising from the de-recognition of the intangible is determined as the difference between the net disposal proceeds, if any, and the carrying amount of the asset and is recognised in profit or loss

(i) Impairment of non-financial assets

At each reporting date, the Company reviews the carrying amounts of its non-financial assets to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. For impairment testing, assets are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or CGUs Goodwill arising from a business combination is allocated to CGUs or groups of CGUs that are expected to benefit from the synergies of the combination.

25

Zambia Bata Shoe Company Plc. Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

(i) Impairment of non-financial assets (continued)

The recoverable amount of an asset or CGU is the greater of its value in use and its fair value less costs of disposal. Value in use is based on the estimated future cash flows, discounted to their present value using a pre-tax discount rate that reflects current market assessment of the time value of money and the risks specific to the asset or CGU. An impairment loss is recognised if the carrying amount of an asset or CGUs exceeds its recoverable amount. Impairment losses are recognised in profit or loss except for a property or plant and equipment previously revalued where the revaluation was taken to other comprehensive income. In this case, the impairment is also recognised in other comprehensive income, up to the amount of any previous revaluation. Any excess is taken to the profit and loss.

Impairment losses are allocated first to reduce the carrying amount of any goodwill allocated to the CGU, and then to reduce the carrying amounts of the other assets in the CGU on a pro rata basis. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised. Such reversal is recognised in profit or loss unless the asset is carried at a revalued amount, in which case the reversal is treated as a revaluation increase.

(j) Segment reporting

Segment results that are reported to the Company’s Managing Director (the Chief

Operating Decision Maker) include items directly attributable to a segment as well as those that can be allocated on a reasonable basis. Head office items comprise mainly corporate assets (primarily the Company’s headquarters), head office expenses and liabilities.

(k) Dividends

Dividends are recognised as a liability in the period in which they are approved by the shareholders.

(l) Earnings per share

The Company presents basic and diluted earnings per share (EPS) data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss attributable to ordinary shareholders of the Company by the weighted average number of ordinary shares outstanding during the period. Diluted EPS is determined by adjusting the profit or loss attributable to ordinary shareholders and the weighted average number of ordinary shares outstanding for the effects of all dilutive potential ordinary shares.

26

Zambia Bata Shoe Company Plc. Notes to the financial statements (continued) for the year ended 31 December 2015 5 Significant accounting policies (continued)

(m) Employee benefits

(i) Short-term benefits

Short-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related service is provided.

A liability is recognised for the amount expected to be paid under short-term cash bonus or profit-sharing plans if the Company has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee and the obligation can be estimated reliably.

(ii) Termination benefits

Termination benefits are employee benefits provided in exchange for the termination of an employee's employment as a result of either an entity's decision to terminate an employee's employment before the normal retirement date or an employee's decision to accept an offer of benefits in exchange for the termination of employment. The Company recognises termination benefits as a liability and an expense at the earlier of when the offer of termination cannot be withdrawn or when the related restructuring costs are recognised under IAS 37 Provisions, Contingent Liabilities and Contingents Assets.

Termination benefits are measured according to the terms of the termination contract. Where termination benefits are due more than 12 months after the reporting period, the present value of the benefits shall be determined. The discount rate used to calculate the present value shall be determined by reference to market yields on high quality corporate bonds at the end of the reporting period.

(n) Income and Deferred tax and Value Added Tax (VAT)

Income tax for the year comprises current and deferred tax. Income tax is recognised in profit or loss except to the extent that it relates to items recognised directly in equity, or other comprehensive income in which case it is also recognised directly in equity or other comprehensive income. Current tax is the expected tax payable on taxable income for the year, using tax rates enacted or substantially enacted at the reporting date, and any adjustment to tax payable in respect of previous years.

Deferred tax is recognised in respect of temporary differences between the carrying

amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is not recognised on the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit. Deferred tax is measured at the tax rates that are

27

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

expected to be applied based on the laws that have enacted or substantively been enacted by the reporting date.

A deferred tax asset is recognised to the extent that it is probable that future taxable profits will be available against which temporary differences can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised. Additional income taxes that arise from the distribution of dividends are recognised at the same time as the liability to pay the related dividend is recognised. Deferred tax assets and liabilities are offset, if there is a legally enforceable right to offset current tax liabilities and assets, and they relate to taxes issued by the same tax authority on the same taxable entity

Value added tax (VAT) is charged at a rate of 16% for all the value added. The company charges output VAT for all its sales and input VAT for most of its purchases. Revenues, expenses and assets are recognised net of the amount of value added tax except: - Where the value added tax incurred on a purchase of assets or services is not recoverable from the taxation authority, in which case the value added tax is recognised as part of the cost of acquisition of the asset or as part of the expense item as applicable - Receivables and payables that are stated with the amount of value added tax included. The net amount of Value Added Tax recoverable from, or payable to, the taxation authority is included as part of receivables or payables in the statement of financial position.

(o) Leases

Assets held under other leases are classified as operating leases and are not

recognised in the Company’s statement of financial position.

Lease payments – lessee and lessor

Payments under operating leases are recognised in profit or loss on a straight-line basis over the term of the lease.

Determining whether an arrangement contains a lease

At inception of an arrangement, the Company determines whether such an arrangement is or contains a lease. This will be the case if the following two criteria are met:

28

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

5 Significant accounting policies (continued)

The fulfilment of the arrangement is dependent on the use of a specific asset or assets; and

The arrangement contains a right to use the asset(s).

At inception or on reassessment of the arrangement, the Company separates payments and other consideration required by such an arrangement into those for the lease and those for other elements on the basis of their relative fair values. If the Company concludes for a finance lease that it is impracticable to separate the payments reliably, then an asset and a liability are recognised at an amount equal to the fair value of the underlying asset. Subsequently the liability is reduced as payments are made and an imputed finance cost on the liability is recognised using the Company’s incremental borrowing rate.

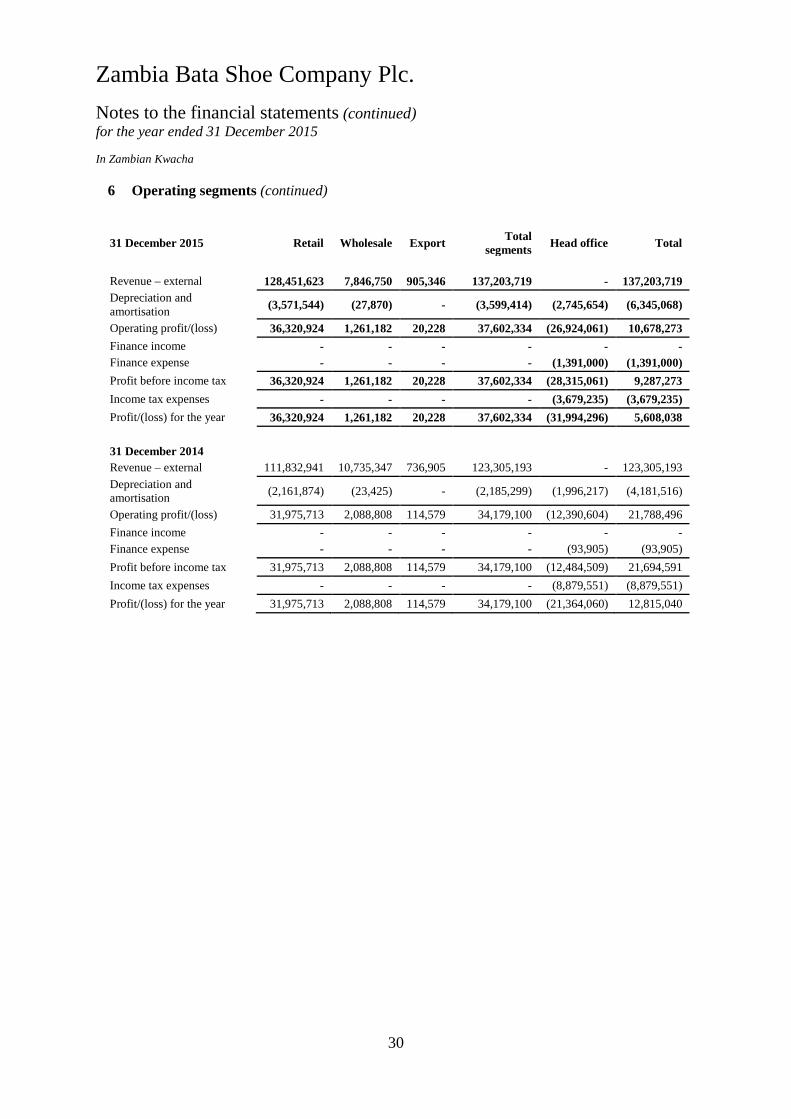

6 Operating segments

The Company has three reportable segments as detailed below, which are its strategic segments. For each of the strategic supply lines, the Company’s Managing Director (the Chief Operating Decision Maker) reviews internal management reports on a monthly basis. The reviews performed are based on the following reportable segments:

Retail Wholesale Export Information regarding the results of each reportable segment is included below. Performance is measured based on products, growth and profit before income tax, as included in the internal management reports that are reviewed by the Managing Director. Segment growth and profit are used to measure performance as management believes that such information is relevant in evaluating the results of the segment. Segment results, assets and liabilities include items directly attributable to a segment as well as those that can be allocated on a reasonable basis. Segment capital expenditure is the total cost incurred to acquire segment assets that are expected to be used for more than one period.

29

Zambia Bata Shoe Company Plc.

Notes to the financial statements (continued) for the year ended 31 December 2015

In Zambian Kwacha

6 Operating segments (continued)

31 December 2015 Retail Wholesale Export Total segments Head office Total

Revenue – external 128,451,623 7,846,750 905,346 137,203,719 - 137,203,719 Depreciation and amortisation (3,571,544) (27,870) - (3,599,414) (2,745,654) (6,345,068)

Operating profit/(loss) 36,320,924 1,261,182 20,228 37,602,334 (26,924,061) 10,678,273 Finance income - - - - - - Finance expense - - - - (1,391,000) (1,391,000) Profit before income tax 36,320,924 1,261,182 20,228 37,602,334 (28,315,061) 9,287,273 Income tax expenses - - - - (3,679,235) (3,679,235) Profit/(loss) for the year 36,320,924 1,261,182 20,228 37,602,334 (31,994,296) 5,608,038

31 December 2014 Revenue – external 111,832,941 10,735,347 736,905 123,305,193 - 123,305,193 Depreciation and amortisation (2,161,874) (23,425) - (2,185,299) (1,996,217) (4,181,516)

Operating profit/(loss) 31,975,713 2,088,808 114,579 34,179,100 (12,390,604) 21,788,496 Finance income - - - - - - Finance expense - - - - (93,905) (93,905) Profit before income tax 31,975,713 2,088,808 114,579 34,179,100 (12,484,509) 21,694,591 Income tax expenses - - - - (8,879,551) (8,879,551) Profit/(loss) for the year 31,975,713 2,088,808 114,579 34,179,100 (21,364,060) 12,815,040

30

Zambia Bata Shoe Company Plc. Notes to the financial statements (continued) for the year ended 31 December 2015 In Zambian Kwacha

6 Operating segments (continued)

Segment assets, liabilities and cash flows

The segment assets, liabilities and cash flows as at 31 December were as follows:

31 December 2015 Retail Wholesale Export Total segments

Head office Total

Segment assets 31,745,439 1,896,470 1,591,730 35,233,639 82,882,980 118,116,619

Segment liabilities - - - - 35,961,386 35,961,386

31 December 2014 Segment assets 43,475,497 1,667,953 1,682,526 46,825,976 79,108,612 125,934,588

Segment liabilities - - - - 42,537,649 42,537,649

Segment assets comprise primarily property, plant and equipment, intangible assets, inventories, receivables and operating cash.

All assets are in Zambia except for some trade receivables and balances due from related parties and these have been disclosed in notes 9 and 25.

Head office liabilities comprise operating liabilities that are managed at head office level and are not split between segments.

Revenue per product line was as follows:

2015

2014 Footwear 130,104,224 116,913,961 Non footwear 7,099,495 6,391,232

137,203,719 123,305,193

31

Zambia Bata Shoe Company Plc. Notes to the financial statements (continued) for the year ended 31 December 2015 In Zambian Kwacha

7 Property, plant and equipment

Land and

Fixtures

Motor

buildings

Equipment

&fittings

vehicles

Total Cost/revaluation Revaluation

Cost

Cost

Cost

At 1 January 2014 28,105,239

4,122,368

13,382,289

441,818

46,051,714 Additions 55,203

169,679

5,709,696

-

5,934,578

Transfer to inventory -

(75,931)

(106,942)

-

(182,873) Revaluation 25,719,558

(788,716)

-

-

24,930,842

At 31 December 2014 53,880,000

3,427,400

18,985,043

441,818

76,734,261

At 1 January 2015 53,880,000

3,427,400

18,985,043

441,818

76,734,261 Additions -

617,090

5,716,319

-

6,333,408

Disposals -

(498,122)

-

-

(498,122) Write off -

-

(6,123)

-

(6,122)

At 31 December 2015 53,880,000

3,546,368

24,695,239

441,818

82,563,425

Accumulated depreciation At 1 January 2015 2,539,459

2,440,185

5,598,856

420,314

10,998,814 Depreciation for the year 1,178,216

407,867

2,560,624

19,855

4,166,562

Revaluation (3,717,675)

(2,848,052)

-

-

(6,565,727) At 31 December 2014 -

-

8,159,480

440,169

8,599,649

At 1 January 2015 -

-

8,159,480

440,169

8,599,649 Depreciation for the year 1,974,386

333,610

4,014,681

1,649

6,324,326

Write off -

-

(2,551)

-

(2,551) At 31 December 2015 1,974,386

333,610

12,171,610

441,818

14,921,424

Carrying amounts At 31 December 2014 53,880,000

3,427,400

10,825,563

1,649

68,134,612

At 31 December 2015 51,905,614

3,212,758

12,523,629

-

67,642,001

The disposed asset was bought and sold within the same year hence no accumulated depreciation on disposal. Fair valuation of leasehold land, buildings and Equipment The fair value of property was determined by an external, independent property valuer, Anderson and Anderson International, having appropriate recognised professional qualifications and recent experience in the location and category of the property being valued. The valuation was in line with the Company’s accounting policy to recognise its leasehold land, buildings and equipment at fair value. Fair value hierarchy for property, plant and equipment as at 31 December 2015 Asset type Level 1 Level 2 Level 3 Land and Buildings - 51,905,614 - Production equipment - - 3,212,758

32

Zambia Bata Shoe Company Plc.