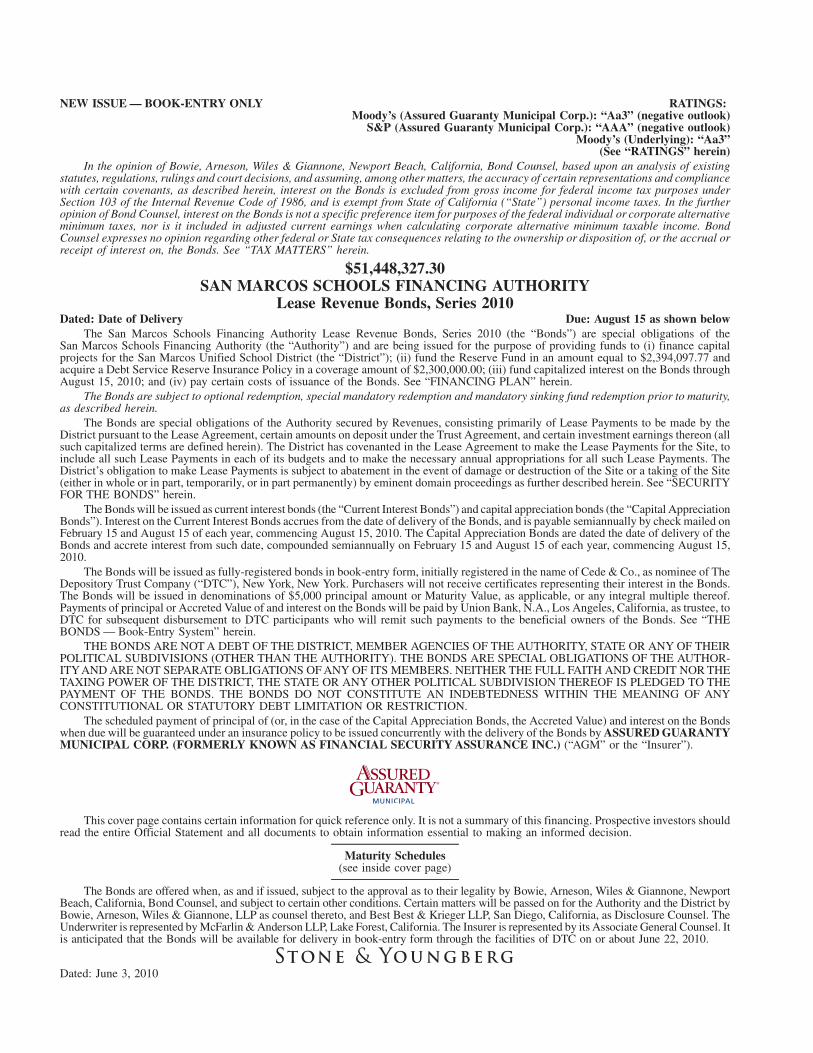

NEW ISSUE — BOOK-ENTRY ONLY RATINGS: Moody’s (Assured Guaranty Municipal Corp.): “Aa3” (negative outlook) S&P (Assured Guaranty Municipal Corp.): “AAA” (negative outlook) Moody’s (Underlying): “Aa3” (See “RATINGS” herein) In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel, based upon an analysis of existing statutes, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, as described herein, interest on the Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, and is exempt from State of California (“State”) personal income taxes. In the further opinion of Bond Counsel, interest on the Bonds is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, nor is it included in adjusted current earnings when calculating corporate alternative minimum taxable income. Bond Counsel expresses no opinion regarding other federal or State tax consequences relating to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See “TAX MATTERS” herein. $51,448,327.30 SAN MARCOS SCHOOLS FINANCING AUTHORITY Lease Revenue Bonds, Series 2010 Dated: Date of Delivery Due: August 15 as shown below The San Marcos Schools Financing Authority Lease Revenue Bonds, Series 2010 (the “Bonds”) are special obligations of the San Marcos Schools Financing Authority (the “Authority”) and are being issued for the purpose of providing funds to (i) finance capital projects for the San Marcos Unified School District (the “District”); (ii) fund the Reserve Fund in an amount equal to $2,394,097.77 and acquire a Debt Service Reserve Insurance Policy in a coverage amount of $2,300,000.00; (iii) fund capitalized interest on the Bonds through August 15, 2010; and (iv) pay certain costs of issuance of the Bonds. See “FINANCING PLAN” herein. The Bonds are subject to optional redemption, special mandatory redemption and mandatory sinking fund redemption prior to maturity, as described herein. The Bonds are special obligations of the Authority secured by Revenues, consisting primarily of Lease Payments to be made by the District pursuant to the Lease Agreement, certain amounts on deposit under the Trust Agreement, and certain investment earnings thereon (all such capitalized terms are defined herein). The District has covenanted in the Lease Agreement to make the Lease Payments for the Site, to include all such Lease Payments in each of its budgets and to make the necessary annual appropriations for all such Lease Payments. The District’s obligation to make Lease Payments is subject to abatement in the event of damage or destruction of the Site or a taking of the Site (either in whole or in part, temporarily, or in part permanently) by eminent domain proceedings as further described herein. See “SECURITY FOR THE BONDS” herein. The Bonds will be issued as current interest bonds (the “Current Interest Bonds”) and capital appreciation bonds (the “Capital Appreciation Bonds”). Interest on the Current Interest Bonds accrues from the date of delivery of the Bonds, and is payable semiannually by check mailed on February 15 and August 15 of each year, commencing August 15, 2010. The Capital Appreciation Bonds are dated the date of delivery of the Bonds and accrete interest from such date, compounded semiannually on February 15 and August 15 of each year, commencing August 15, 2010. The Bonds will be issued as fully-registered bonds in book-entry form, initially registered in the name of Cede & Co., as nominee of The Depository Trust Company (“DTC”), NewYork, New York. Purchasers will not receive certificates representing their interest in the Bonds. The Bonds will be issued in denominations of $5,000 principal amount or Maturity Value, as applicable, or any integral multiple thereof. Payments of principal or Accreted Value of and interest on the Bonds will be paid by Union Bank, N.A., Los Angeles, California, as trustee, to DTC for subsequent disbursement to DTC participants who will remit such payments to the beneficial owners of the Bonds. See “THE BONDS — Book-Entry System” herein. THE BONDS ARE NOTA DEBT OF THE DISTRICT, MEMBER AGENCIES OF THE AUTHORITY, STATE OR ANYOF THEIR POLITICAL SUBDIVISIONS (OTHERTHAN THE AUTHORITY). THE BONDS ARE SPECIAL OBLIGATIONS OF THE AUTHOR- ITYAND ARE NOT SEPARATE OBLIGATIONS OF ANY OF ITS MEMBERS. NEITHER THE FULL FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT, THE STATE OR ANY OTHER POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE BONDS. THE BONDS DO NOT CONSTITUTE AN INDEBTEDNESS WITHIN THE MEANING OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION. The scheduled payment of principal of (or, in the case of the Capital Appreciation Bonds, the Accreted Value) and interest on the Bonds when due will be guaranteed under an insurance policy to be issued concurrently with the delivery of the Bonds by ASSURED GUARANTY MUNICIPAL CORP. (FORMERLY KNOWN AS FINANCIAL SECURITYASSURANCE INC.) (“AGM” or the “Insurer”). This cover page contains certain information for quick reference only. It is not a summary of this financing. Prospective investors should read the entire Official Statement and all documents to obtain information essential to making an informed decision. Maturity Schedules (see inside cover page) The Bonds are offered when, as and if issued, subject to the approval as to their legality by Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel, and subject to certain other conditions. Certain matters will be passed on for the Authority and the District by Bowie, Arneson, Wiles & Giannone, LLP as counsel thereto, and Best Best & Krieger LLP, San Diego, California, as Disclosure Counsel. The Underwriter is represented by McFarlin & Anderson LLP, Lake Forest, California. The Insurer is represented by its Associate General Counsel. It is anticipated that the Bonds will be available for delivery in book-entry form through the facilities of DTC on or about June 22, 2010. Dated: June 3, 2010

Transcript

NEW ISSUE — BOOK-ENTRY ONLY RATINGS:Moody’s (Assured Guaranty Municipal Corp.): “Aa3” (negative outlook)

S&P (Assured Guaranty Municipal Corp.): “AAA” (negative outlook)Moody’s (Underlying): “Aa3”

(See “RATINGS” herein)In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel, based upon an analysis of existing

statutes, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliancewith certain covenants, as described herein, interest on the Bonds is excluded from gross income for federal income tax purposes underSection 103 of the Internal Revenue Code of 1986, and is exempt from State of California (“State”) personal income taxes. In the furtheropinion of Bond Counsel, interest on the Bonds is not a specific preference item for purposes of the federal individual or corporate alternativeminimum taxes, nor is it included in adjusted current earnings when calculating corporate alternative minimum taxable income. BondCounsel expresses no opinion regarding other federal or State tax consequences relating to the ownership or disposition of, or the accrual orreceipt of interest on, the Bonds. See “TAX MATTERS” herein.

Lease Revenue Bonds, Series 2010Dated: Date of Delivery Due: August 15 as shown below

The San Marcos Schools Financing Authority Lease Revenue Bonds, Series 2010 (the “Bonds”) are special obligations of theSan Marcos Schools Financing Authority (the “Authority”) and are being issued for the purpose of providing funds to (i) finance capitalprojects for the San Marcos Unified School District (the “District”); (ii) fund the Reserve Fund in an amount equal to $2,394,097.77 andacquire a Debt Service Reserve Insurance Policy in a coverage amount of $2,300,000.00; (iii) fund capitalized interest on the Bonds throughAugust 15, 2010; and (iv) pay certain costs of issuance of the Bonds. See “FINANCING PLAN” herein.

The Bonds are subject to optional redemption, special mandatory redemption and mandatory sinking fund redemption prior to maturity,as described herein.

The Bonds are special obligations of the Authority secured by Revenues, consisting primarily of Lease Payments to be made by theDistrict pursuant to the Lease Agreement, certain amounts on deposit under the Trust Agreement, and certain investment earnings thereon (allsuch capitalized terms are defined herein). The District has covenanted in the Lease Agreement to make the Lease Payments for the Site, toinclude all such Lease Payments in each of its budgets and to make the necessary annual appropriations for all such Lease Payments. TheDistrict’s obligation to make Lease Payments is subject to abatement in the event of damage or destruction of the Site or a taking of the Site(either in whole or in part, temporarily, or in part permanently) by eminent domain proceedings as further described herein. See “SECURITYFOR THE BONDS” herein.

The Bonds will be issued as current interest bonds (the “Current Interest Bonds”) and capital appreciation bonds (the “Capital AppreciationBonds”). Interest on the Current Interest Bonds accrues from the date of delivery of the Bonds, and is payable semiannually by check mailed onFebruary 15 and August 15 of each year, commencing August 15, 2010. The Capital Appreciation Bonds are dated the date of delivery of theBonds and accrete interest from such date, compounded semiannually on February 15 and August 15 of each year, commencing August 15,2010.

The Bonds will be issued as fully-registered bonds in book-entry form, initially registered in the name of Cede & Co., as nominee of TheDepository Trust Company (“DTC”), New York, New York. Purchasers will not receive certificates representing their interest in the Bonds.The Bonds will be issued in denominations of $5,000 principal amount or Maturity Value, as applicable, or any integral multiple thereof.Payments of principal or Accreted Value of and interest on the Bonds will be paid by Union Bank, N.A., Los Angeles, California, as trustee, toDTC for subsequent disbursement to DTC participants who will remit such payments to the beneficial owners of the Bonds. See “THEBONDS — Book-Entry System” herein.

THE BONDS ARE NOT A DEBT OF THE DISTRICT, MEMBER AGENCIES OF THE AUTHORITY, STATE OR ANY OF THEIRPOLITICAL SUBDIVISIONS (OTHER THAN THE AUTHORITY). THE BONDS ARE SPECIAL OBLIGATIONS OF THE AUTHOR-ITYAND ARE NOT SEPARATE OBLIGATIONS OF ANY OF ITS MEMBERS. NEITHER THE FULL FAITH AND CREDIT NOR THETAXING POWER OF THE DISTRICT, THE STATE OR ANY OTHER POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THEPAYMENT OF THE BONDS. THE BONDS DO NOT CONSTITUTE AN INDEBTEDNESS WITHIN THE MEANING OF ANYCONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION.

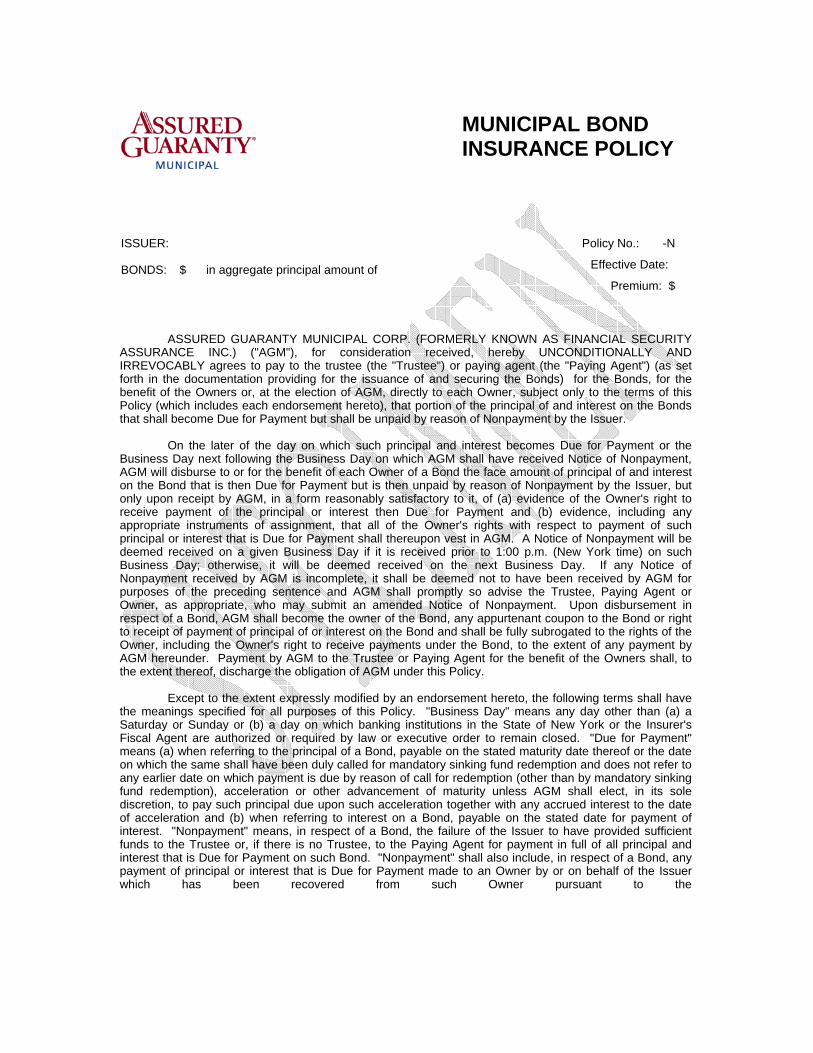

The scheduled payment of principal of (or, in the case of the Capital Appreciation Bonds, the Accreted Value) and interest on the Bondswhen due will be guaranteed under an insurance policy to be issued concurrently with the delivery of the Bonds by ASSURED GUARANTYMUNICIPAL CORP. (FORMERLY KNOWN AS FINANCIAL SECURITY ASSURANCE INC.) (“AGM” or the “Insurer”).

This cover page contains certain information for quick reference only. It is not a summary of this financing. Prospective investors shouldread the entire Official Statement and all documents to obtain information essential to making an informed decision.

Maturity Schedules(see inside cover page)

The Bonds are offered when, as and if issued, subject to the approval as to their legality by Bowie, Arneson, Wiles & Giannone, NewportBeach, California, Bond Counsel, and subject to certain other conditions. Certain matters will be passed on for the Authority and the District byBowie, Arneson, Wiles & Giannone, LLP as counsel thereto, and Best Best & Krieger LLP, San Diego, California, as Disclosure Counsel. TheUnderwriter is represented by McFarlin & Anderson LLP, Lake Forest, California. The Insurer is represented by its Associate General Counsel. Itis anticipated that the Bonds will be available for delivery in book-entry form through the facilities of DTC on or about June 22, 2010.

Dated: June 3, 2010

pbrubake

Text Box

2010-0078

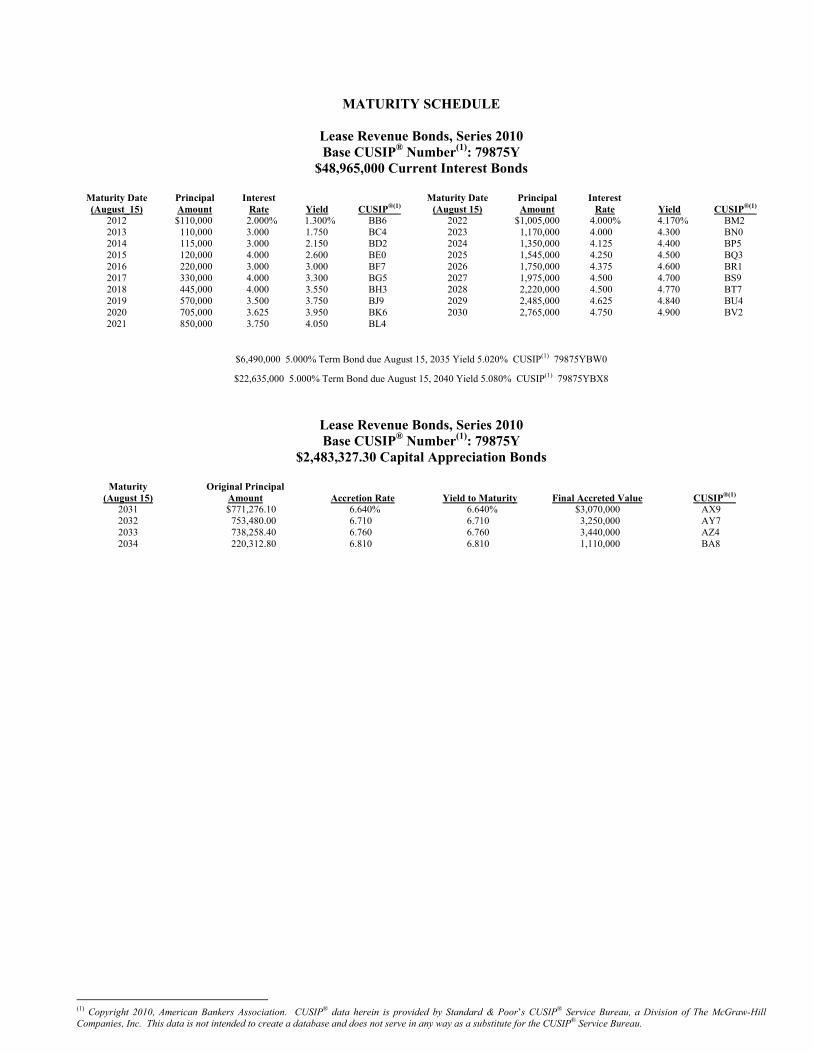

MATURITY SCHEDULE

Lease Revenue Bonds, Series 2010 Base CUSIP® Number(1): 79875Y

(1) Copyright 2010, American Bankers Association. CUSIP® data herein is provided by Standard & Poor’s CUSIP® Service Bureau, a Division of The McGraw-Hill Companies, Inc. This data is not intended to create a database and does not serve in any way as a substitute for the CUSIP® Service Bureau.

i

Table of Contents Page Page

INTRODUCTION ........................................... 1 The Bonds .................................................. 1 The Authority............................................. 2 The District ................................................ 2 Risk Factors ............................................... 2 Municipal Bond Insurance......................... 2 Tax Matters ................................................ 2 Continuing Disclosure ............................... 3 Professionals Involved in the Offering ...... 3 Forward Looking Statements..................... 3 General....................................................... 4

ESTIMATED SOURCES AND USES OF FUNDS ............................................................ 5 FINANCING PLAN ........................................ 5

The Project ................................................. 5 The Site ...................................................... 5 Substitution or Release of Site................... 6

THE BONDS ................................................... 6 Payment of Principal and Interest .............. 6 Registration of the Bonds........................... 7 Redemption ................................................ 7 The Trustee .............................................. 10 Debt Service Schedule ............................. 10 Book-Entry System.................................. 12

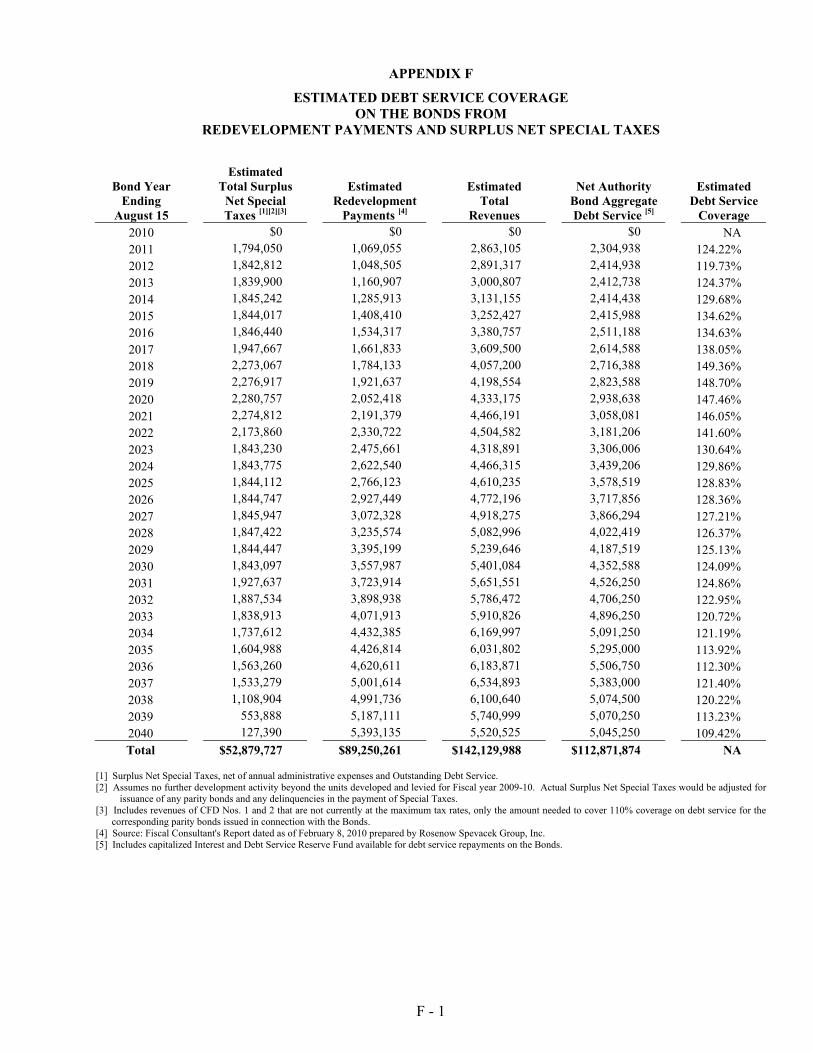

SECURITY FOR THE BONDS.................... 12 General..................................................... 12 Pledge of Revenues.................................. 12 Lease Payment Fund................................ 13 Bond Fund................................................ 13 Reserve Fund ........................................... 13 Lease Payments........................................ 15 Covenant to Budget and Appropriate ...... 16 Covenant Regarding Application of Redevelopment Payments........................ 16 Pledge Agreement.................................... 18 Estimated Debt Service Coverage on the Bonds from Redevelopment Payments and Surplus Net Special Taxes ................ 21 Limited Obligation................................... 21 Abatement ................................................ 21 Action on Default..................................... 22 Insurance .................................................. 22 Additional Bonds ..................................... 23

BOND INSURANCE .................................... 24 The Insurance Policy................................ 24 Assured Guaranty Municipal Corp. (formerly known as Financial Security Assurance Inc.) ........................................ 25

THE AUTHORITY ....................................... 26

THE DISTRICT ............................................ 27 Introduction ............................................. 27 General Information ................................ 27 Administration......................................... 27 Key Personnel.......................................... 27 Employee Relations................................. 28 Retirement Systems ................................. 28 Other Post Employment Benefits (“OPEB”)................................................. 28 Insurance.................................................. 29

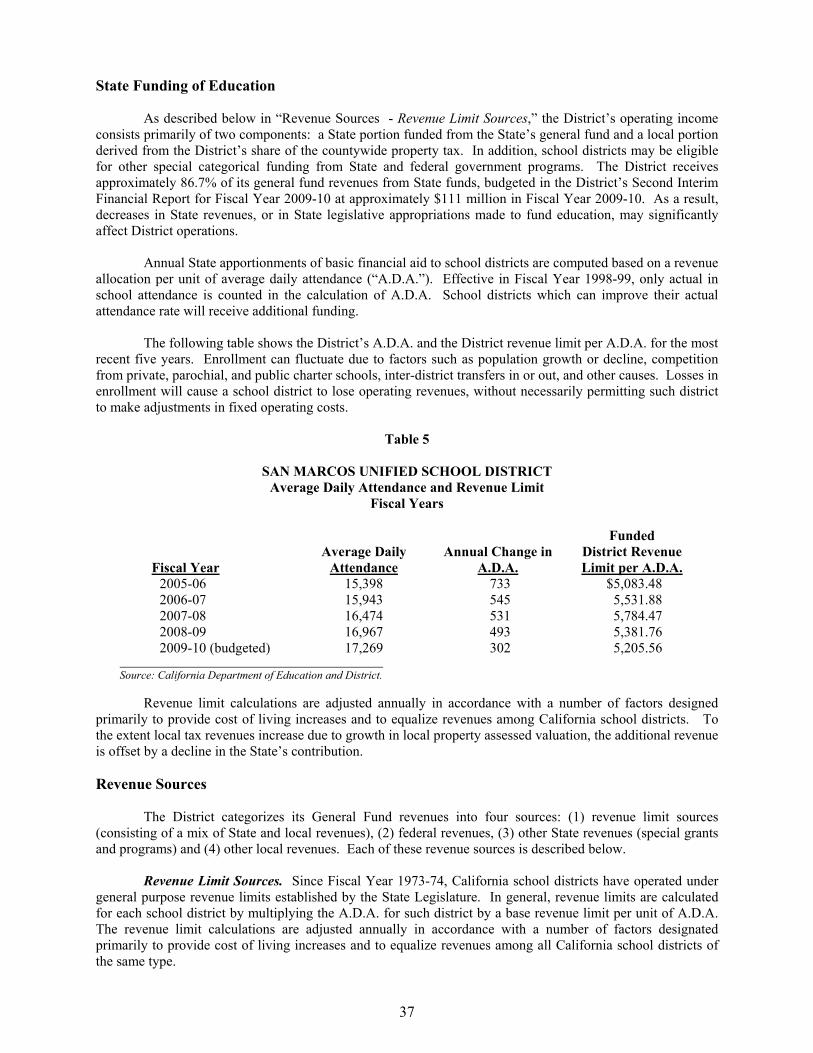

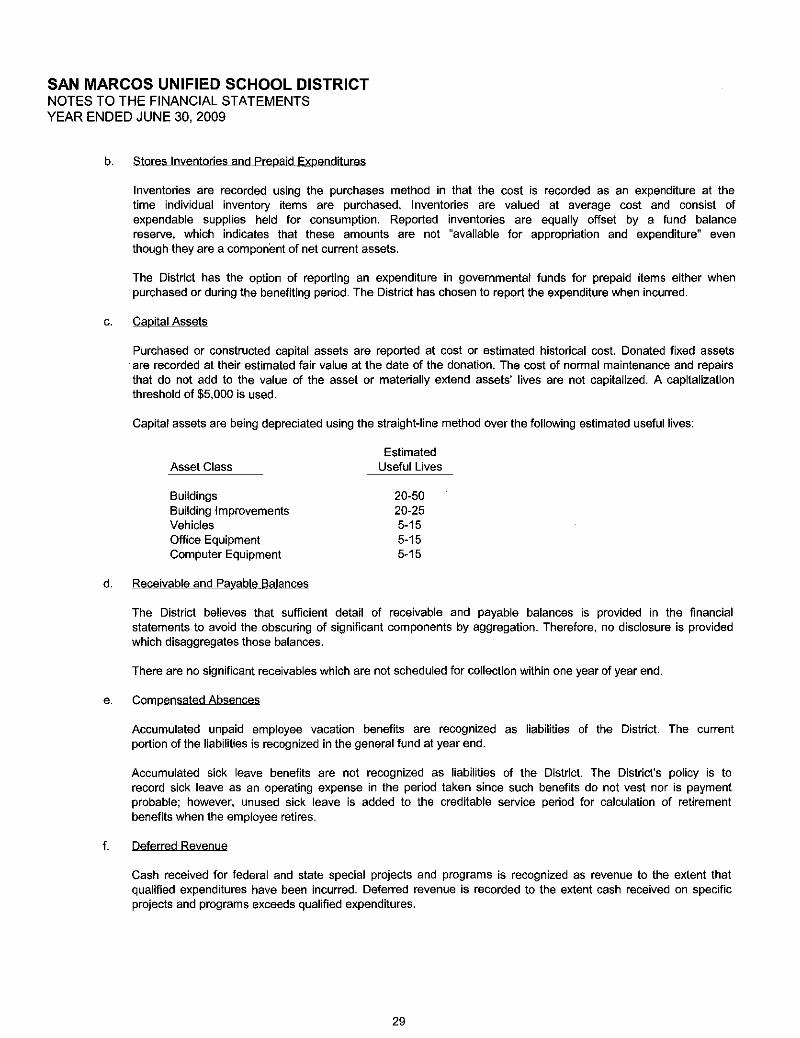

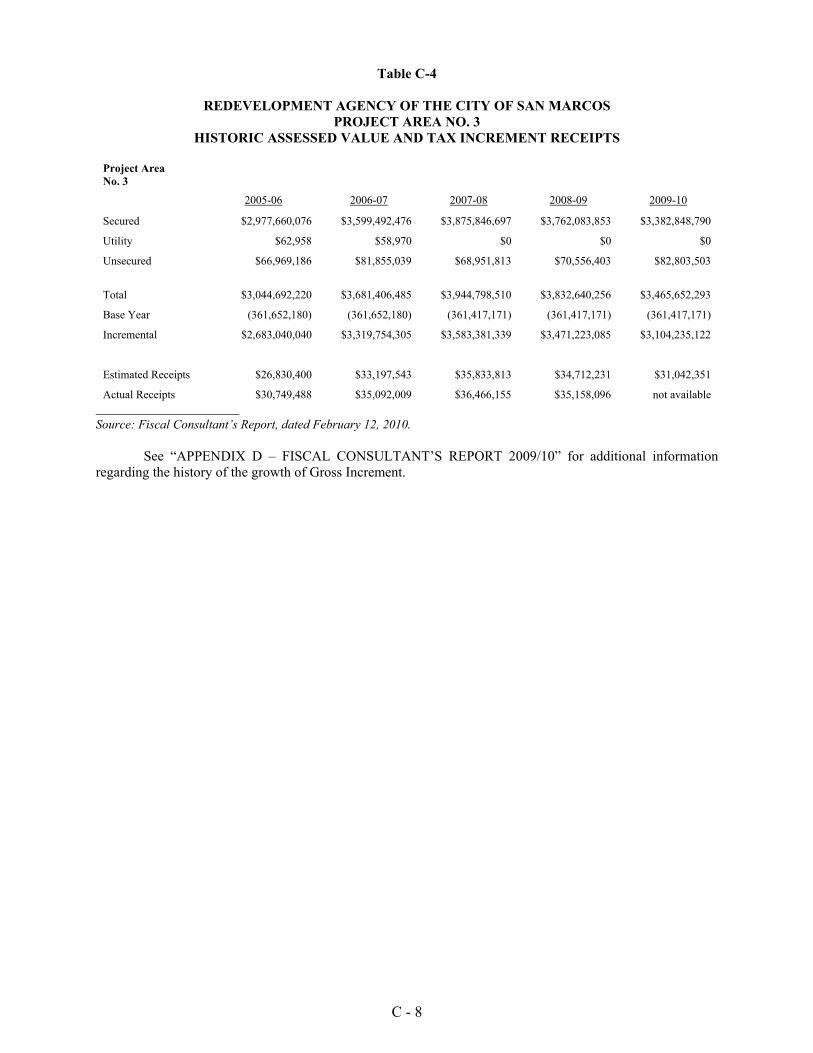

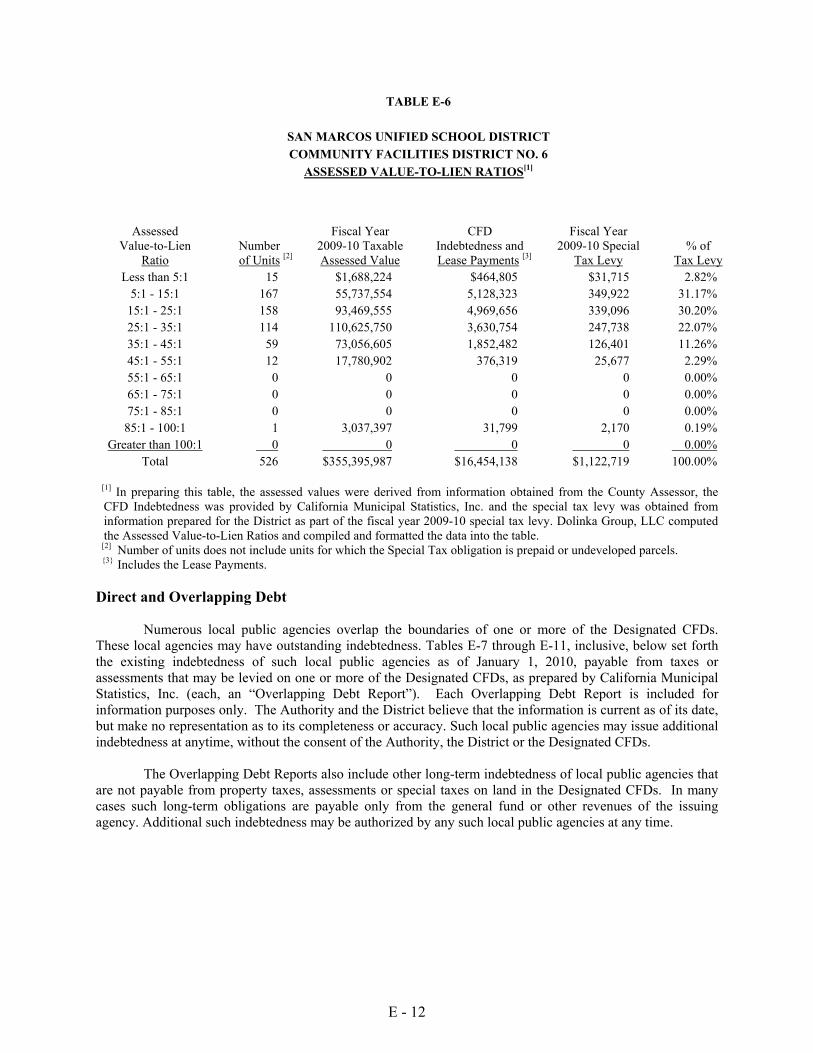

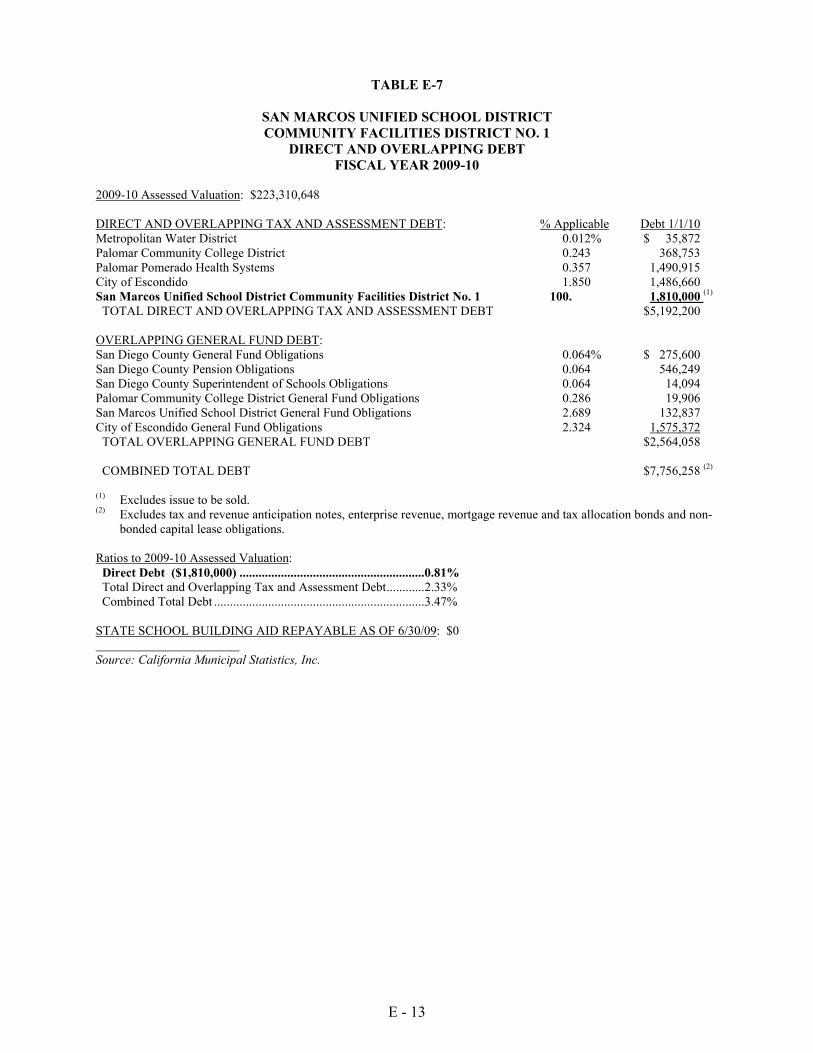

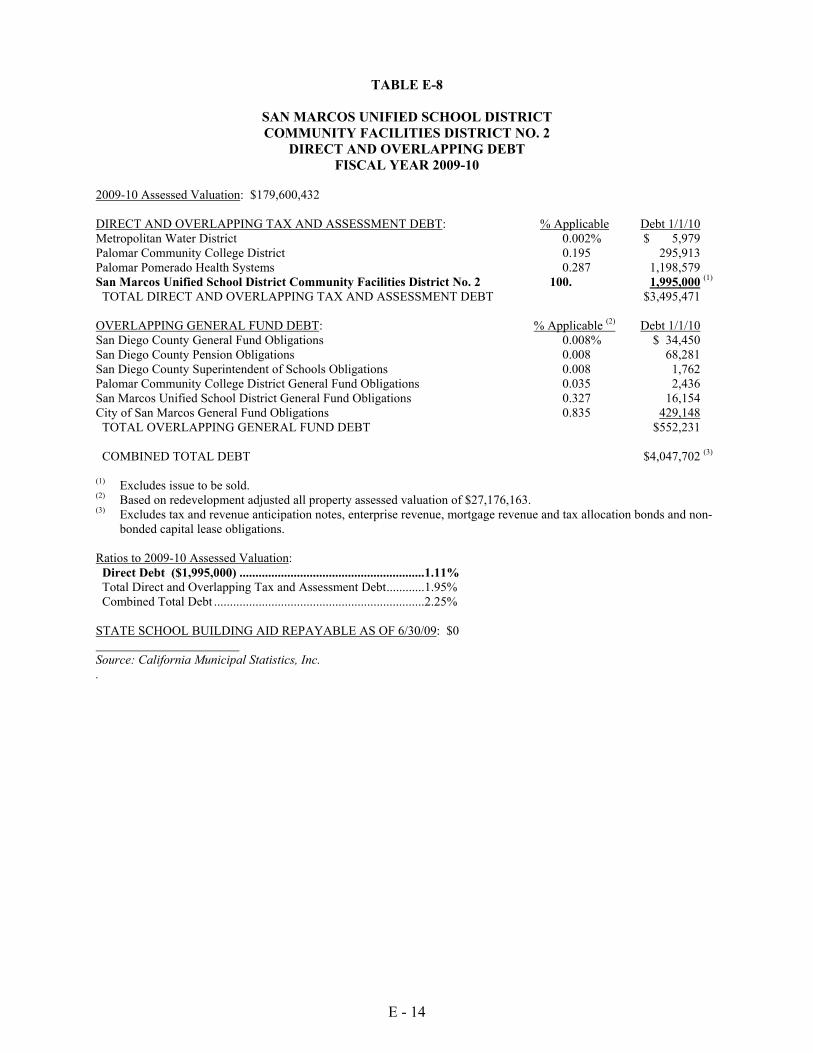

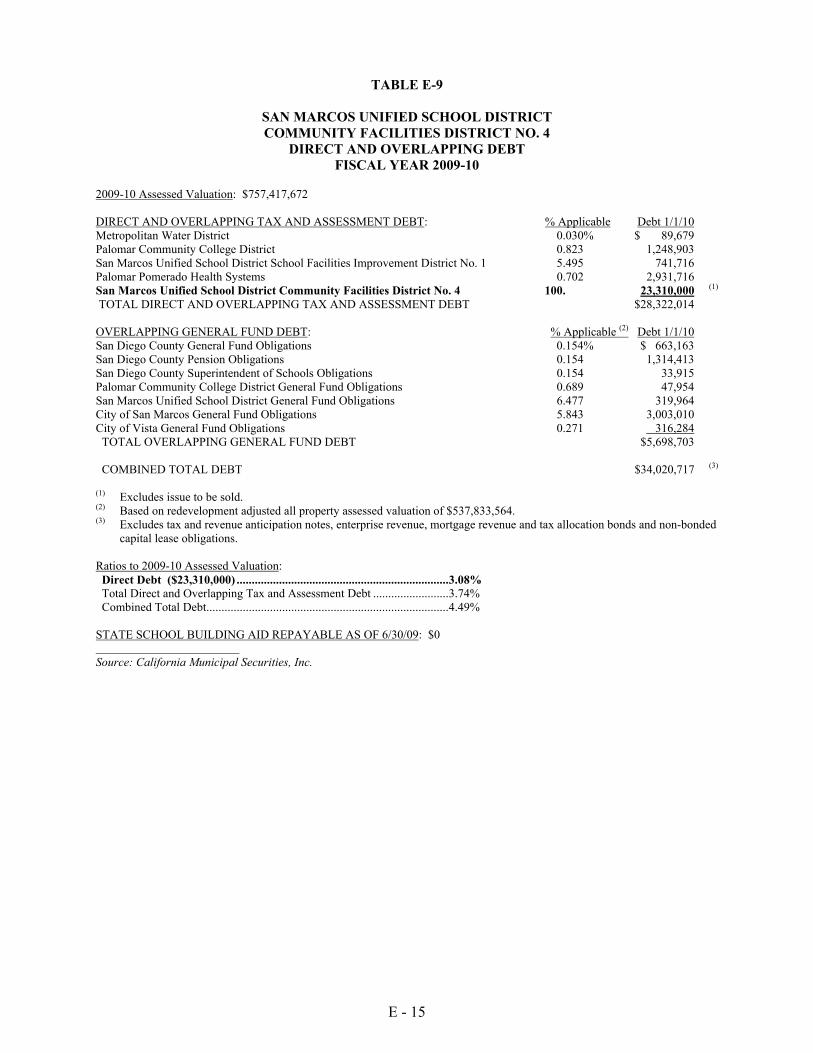

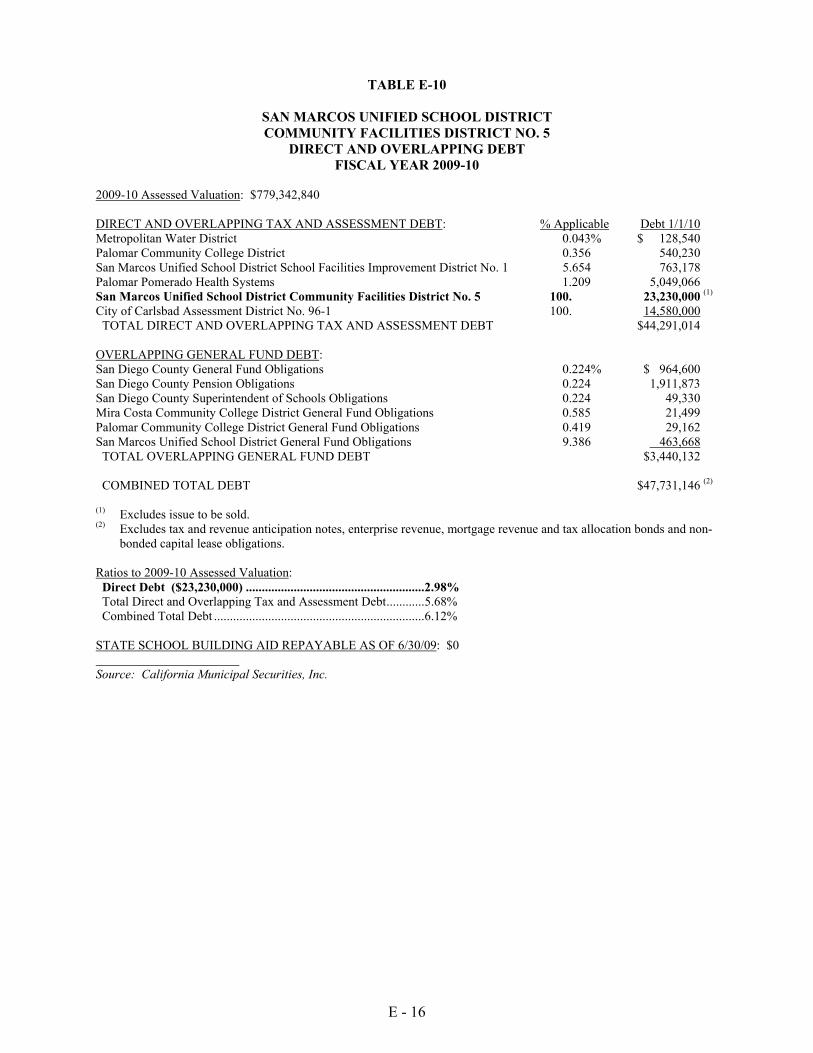

DISTRICT FINANCIAL INFORMATION.. 29 Significant Accounting Policies and Audited Financial Reports ....................... 29 Budget Process ........................................ 33 State Funding of Education ..................... 37 Revenue Sources ..................................... 37 Developer Fees ........................................ 39 Outstanding Debt; Other Financial Obligations .............................................. 40 Lease Purchase Agreement...................... 41 Assessed Valuations ................................ 42 Largest Taxpayers ................................... 43 Direct and Overlapping Debt................... 43

IMPACT OF STATE BUDGET ON DISTRICT REVENUES ............................... 46

State Funding of Education; State Budget Process..................................................... 46 Governor’s Proposed 2010-2011 State Budget; May 2010 Revision.................... 55 Future Budgets and Actions .................... 58

CONSTITUTIONAL AND STATUTORY LIMITATIONS ON DISTRICT REVENUES AND EXPENDITURES................................ 58

Article XIIIA of the California Constitution ............................................. 58 Article XIIIB of the State Constitution ... 59 Articles XIIIC and XIIID of the State Constitution ............................................. 60 Propositions 98 and 111 .......................... 60 Jarvis v. Connell ...................................... 61 Proposition 1A......................................... 61 Future Initiatives and Legislation............ 62

RISK FACTORS........................................... 62 No Tax Pledge ......................................... 62 Appropriation .......................................... 62 Abatement................................................ 63 Limitation on Enforcement of Remedies; No Acceleration....................................... 63 Constitutional School Funding Guarantee; State of California Finances .................... 64

ii

Application of Constitutional and Statutory Provisions ................................. 64 Geologic, Topographic and Climatic Conditions ................................................ 64 Economic Conditions in California ......... 65 Future State Budgets ................................ 65 Investment of District’s General Fund..... 65 No Liability by the Authority to the Owners ..................................................... 65 Hazardous Substances.............................. 66 Limitations on Remedies Available; Bankruptcy............................................... 66 State Law Limitations on Appropriations 66 Change in Law ......................................... 67 Loss of Tax Exemption............................ 67 Seismic Considerations............................ 67 Substitution of Property ........................... 67 Special Risk Factors Related to the Redevelopment Payments........................ 67 Special Risk Factors Related to Surplus Net Special Taxes .................................... 69

Opinion of Bond Counsel ........................ 77 Original Issue Discount............................ 77 Original Issue Premium ........................... 78 Impact of Legislative Proposals, Clarifications of the Code and Court Decisions on Tax Exemption ................... 78 Internal Revenue Service Audit of Tax-Exempt Bond Issues................................. 78

CERTAIN LEGAL MATTERS .................... 79

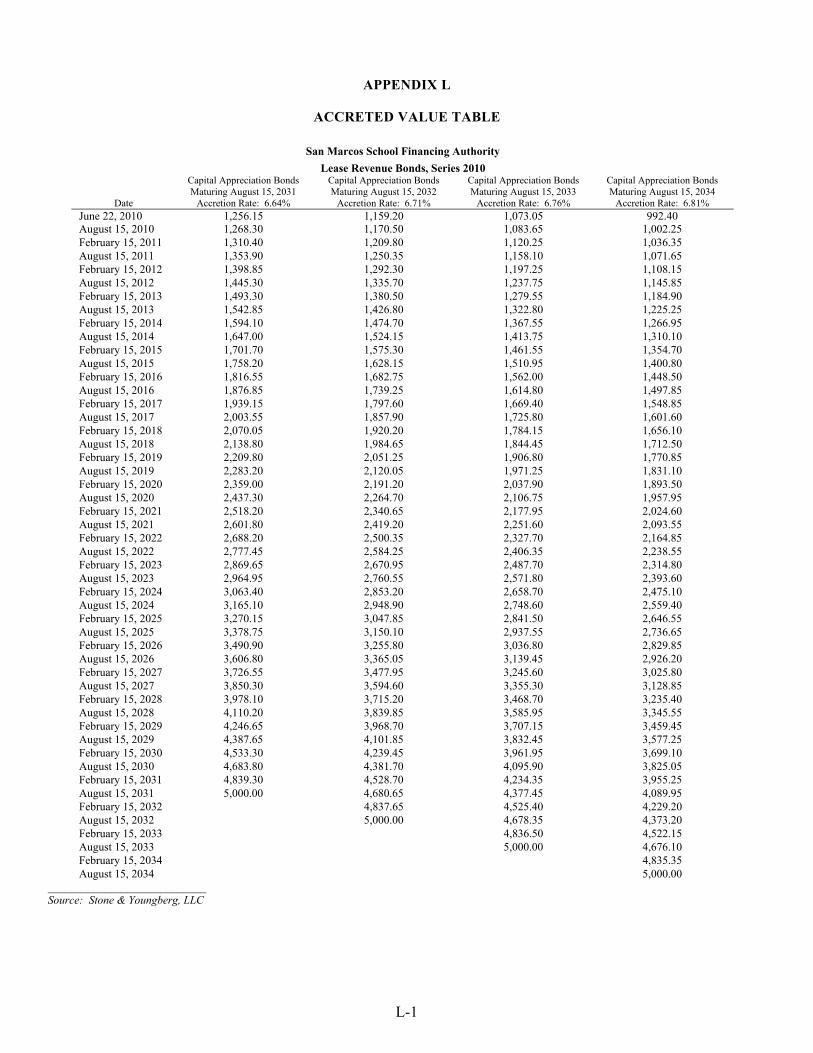

UNDERWRITING........................................ 79 MISCELLANEOUS...................................... 79 APPENDIX A - SUMMARY OF PRINCIPAL LEGAL DOCUMENTS ........ A-1 APPENDIX B - AUDITED FINANCIAL STATEMENTS OF THE DISTRICT FOR FISCAL YEAR ENDED JUNE 30, 2009 ... B-1 APPENDIX C - REDEVELOPMENT PAYMENTS................................................ C-1 APPENDIX D - FISCAL CONSULTANT’S REPORT 2009/10........................................ D-1 APPENDIX E - SURPLUS NET SPECIAL TAXES .........................................................E-1 APPENDIX F - ESTIMATED DEBT SERVICE COVERAGE ON THE BONDS FROM REDEVELOPMENT PAYMENTS AND SURPLUS NET SPECIAL TAXES...F-1 APPENDIX G - PROPOSED FORM OF BOND COUNSEL’S OPINION ................. G-1 APPENDIX H - FORM OF CONTINUING DISCLOSURE AGREEMENT................... H-1 APPENDIX I - BOOK-ENTRY-ONLY SYSTEM .......................................................I-1 APPENDIX J - SAN DIEGO COUNTY INVESTMENT POOL ..................................J-1 APPENDIX K – SPECIMEN MUNICIPAL BOND INSURANCE POLICY .................. K-1 APPENDIX L – ACCRETED VALUE TABLE............................................................ L-1

IN CONNECTION WITH THE OFFERING OF THE BONDS, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL THE BONDS TO CERTAIN DEALERS AND DEALER BANKS AND BANKS ACTING AS AGENTS AT PRICES LOWER THAN THE PUBLIC OFFERING PRICES STATED ON THE COVER PAGE HEREOF AND SAID PUBLIC OFFERING PRICES MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER.

THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEMPTION CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

This Official Statement speaks only as of its date, and the information contained herein is subject to change. This Official Statement and any continuing disclosure documents of the District and the Authority are intended to be made available through the District at the address indicated below. The District has undertaken to provide certain continuing disclosure pursuant to a Continuing Disclosure Agreement, as described herein. Copies of the resolutions and other documents relating to the issuance of the Bonds are available upon request, and upon payment to the District of a charge for copying, mailing and handling, from the office of the Assistant Superintendent, Business Services of the District at 255 Pico Avenue, Suite 250, San Marcos, California 92069.

No dealer, broker, salesperson or other person has been authorized to give any information or to make any representations, other than those contained in this Official Statement, and, if given or made, such other information or representations must not be relied upon as having been authorized by the Authority, the District or the Underwriter.

The information set forth herein has been obtained from the District and other sources believed to be reliable, but the accuracy or completeness of such information is not guaranteed by, and should not be construed as a representation by, the Underwriter. This information is not guaranteed as to accuracy and is not to be construed as a representation by the District, the Authority or the Underwriter.

This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by any person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as a representation of facts.

The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Authority or the District since the date hereof. All summaries contained herein of the Lease Agreement, the Trust Agreement and other documents are made subject to the provisions of such documents and do not purport to be complete statements of any or all of such provisions.

The issuance and sale of the Bonds have not been registered under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, in reliance upon exemptions for the issuance and sale of municipal securities provided under Section 3(a)(2) of the Securities Act of 1933 and Section 3(a)(12) of the Securities Exchange Act of 1934.

Assured Guaranty Municipal Corp. (formerly known as Financial Security Assurance Inc.) (“AGM”) makes no representation regarding the Bonds or the advisability of investing in the Bonds. In addition, AGM has not independently verified, makes no representation regarding, and does not accept any responsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, or omitted herefrom, other than with respect to the accuracy of the information regarding AGM supplied by AGM and presented under the heading “BOND INSURANCE” and “APPENDIX K – Specimen Municipal Bond Insurance Policy.”

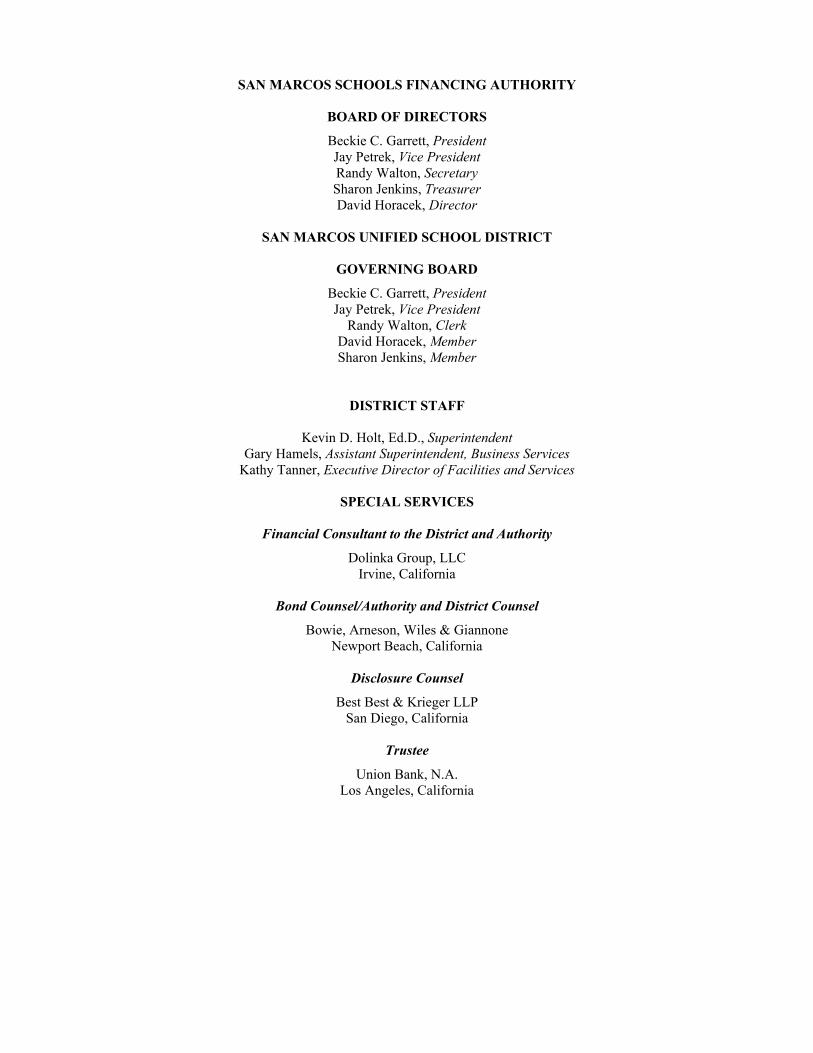

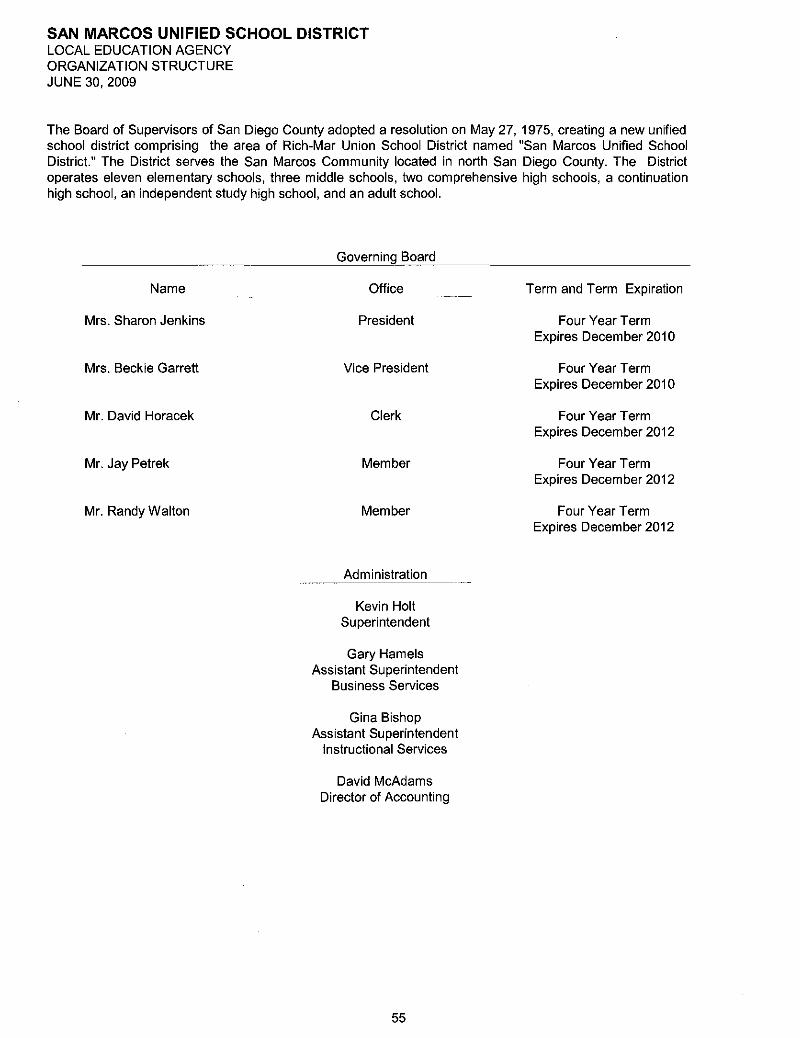

SAN MARCOS SCHOOLS FINANCING AUTHORITY

BOARD OF DIRECTORS

Beckie C. Garrett, President Jay Petrek, Vice President Randy Walton, Secretary Sharon Jenkins, Treasurer David Horacek, Director

SAN MARCOS UNIFIED SCHOOL DISTRICT

GOVERNING BOARD

Beckie C. Garrett, President Jay Petrek, Vice President

Randy Walton, Clerk David Horacek, Member Sharon Jenkins, Member

DISTRICT STAFF

Kevin D. Holt, Ed.D., Superintendent Gary Hamels, Assistant Superintendent, Business Services

Kathy Tanner, Executive Director of Facilities and Services

SPECIAL SERVICES

Financial Consultant to the District and Authority

Dolinka Group, LLC Irvine, California

Bond Counsel/Authority and District Counsel

Bowie, Arneson, Wiles & Giannone Newport Beach, California

Disclosure Counsel

Best Best & Krieger LLP San Diego, California

Trustee

Union Bank, N.A. Los Angeles, California

1

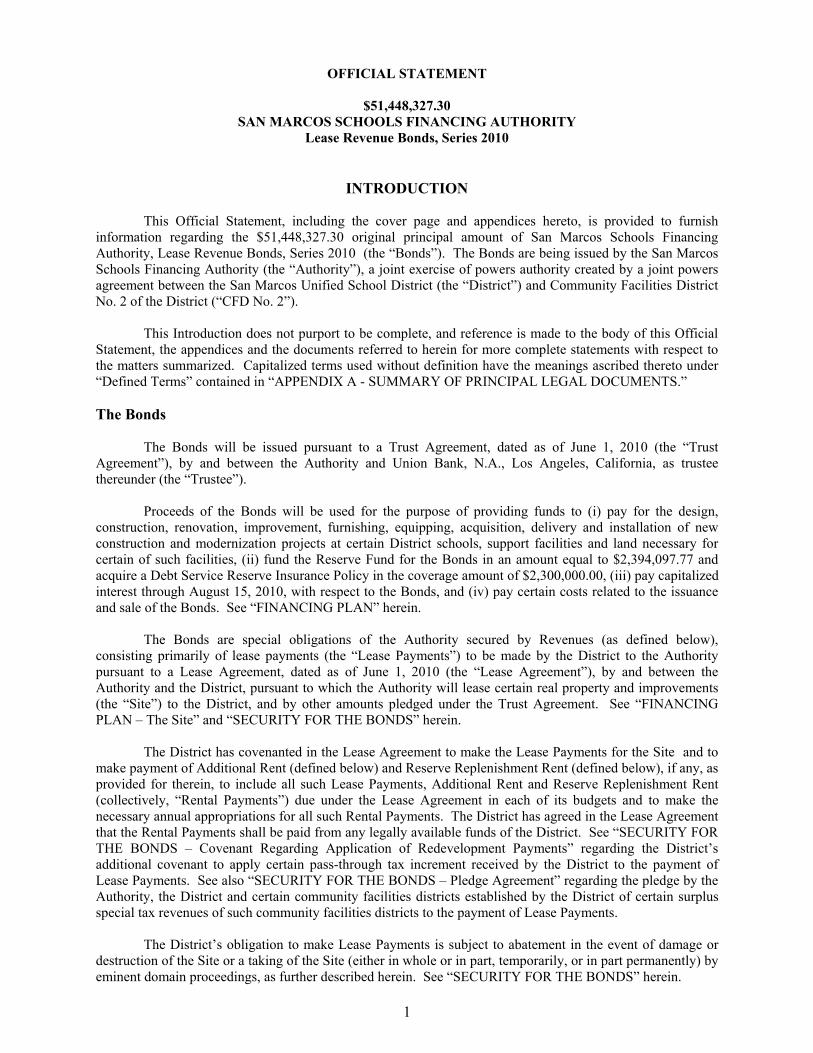

OFFICIAL STATEMENT

$51,448,327.30 SAN MARCOS SCHOOLS FINANCING AUTHORITY

Lease Revenue Bonds, Series 2010

INTRODUCTION

This Official Statement, including the cover page and appendices hereto, is provided to furnish information regarding the $51,448,327.30 original principal amount of San Marcos Schools Financing Authority, Lease Revenue Bonds, Series 2010 (the “Bonds”). The Bonds are being issued by the San Marcos Schools Financing Authority (the “Authority”), a joint exercise of powers authority created by a joint powers agreement between the San Marcos Unified School District (the “District”) and Community Facilities District No. 2 of the District (“CFD No. 2”).

This Introduction does not purport to be complete, and reference is made to the body of this Official Statement, the appendices and the documents referred to herein for more complete statements with respect to the matters summarized. Capitalized terms used without definition have the meanings ascribed thereto under “Defined Terms” contained in “APPENDIX A - SUMMARY OF PRINCIPAL LEGAL DOCUMENTS.”

The Bonds

The Bonds will be issued pursuant to a Trust Agreement, dated as of June 1, 2010 (the “Trust Agreement”), by and between the Authority and Union Bank, N.A., Los Angeles, California, as trustee thereunder (the “Trustee”).

Proceeds of the Bonds will be used for the purpose of providing funds to (i) pay for the design, construction, renovation, improvement, furnishing, equipping, acquisition, delivery and installation of new construction and modernization projects at certain District schools, support facilities and land necessary for certain of such facilities, (ii) fund the Reserve Fund for the Bonds in an amount equal to $2,394,097.77 and acquire a Debt Service Reserve Insurance Policy in the coverage amount of $2,300,000.00, (iii) pay capitalized interest through August 15, 2010, with respect to the Bonds, and (iv) pay certain costs related to the issuance and sale of the Bonds. See “FINANCING PLAN” herein.

The Bonds are special obligations of the Authority secured by Revenues (as defined below), consisting primarily of lease payments (the “Lease Payments”) to be made by the District to the Authority pursuant to a Lease Agreement, dated as of June 1, 2010 (the “Lease Agreement”), by and between the Authority and the District, pursuant to which the Authority will lease certain real property and improvements (the “Site”) to the District, and by other amounts pledged under the Trust Agreement. See “FINANCING PLAN – The Site” and “SECURITY FOR THE BONDS” herein.

The District has covenanted in the Lease Agreement to make the Lease Payments for the Site and to make payment of Additional Rent (defined below) and Reserve Replenishment Rent (defined below), if any, as provided for therein, to include all such Lease Payments, Additional Rent and Reserve Replenishment Rent (collectively, “Rental Payments”) due under the Lease Agreement in each of its budgets and to make the necessary annual appropriations for all such Rental Payments. The District has agreed in the Lease Agreement that the Rental Payments shall be paid from any legally available funds of the District. See “SECURITY FOR THE BONDS – Covenant Regarding Application of Redevelopment Payments” regarding the District’s additional covenant to apply certain pass-through tax increment received by the District to the payment of Lease Payments. See also “SECURITY FOR THE BONDS – Pledge Agreement” regarding the pledge by the Authority, the District and certain community facilities districts established by the District of certain surplus special tax revenues of such community facilities districts to the payment of Lease Payments.

The District’s obligation to make Lease Payments is subject to abatement in the event of damage or destruction of the Site or a taking of the Site (either in whole or in part, temporarily, or in part permanently) by eminent domain proceedings, as further described herein. See “SECURITY FOR THE BONDS” herein.

2

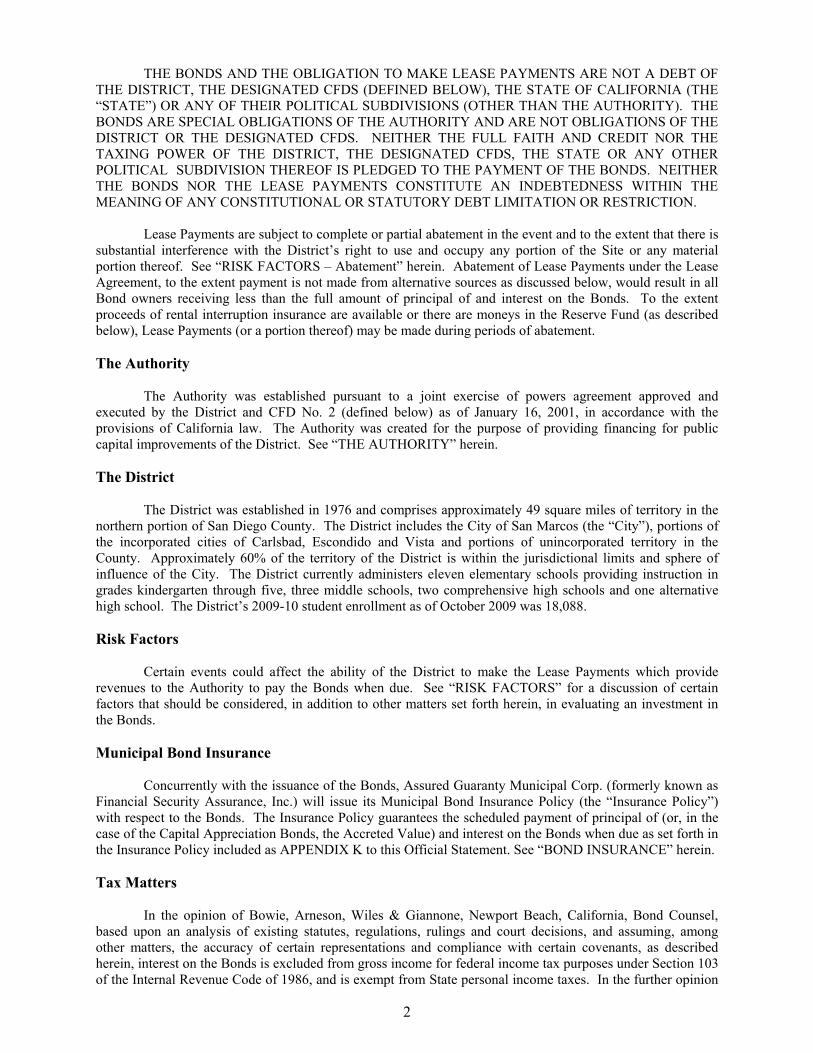

THE BONDS AND THE OBLIGATION TO MAKE LEASE PAYMENTS ARE NOT A DEBT OF THE DISTRICT, THE DESIGNATED CFDS (DEFINED BELOW), THE STATE OF CALIFORNIA (THE “STATE”) OR ANY OF THEIR POLITICAL SUBDIVISIONS (OTHER THAN THE AUTHORITY). THE BONDS ARE SPECIAL OBLIGATIONS OF THE AUTHORITY AND ARE NOT OBLIGATIONS OF THE DISTRICT OR THE DESIGNATED CFDS. NEITHER THE FULL FAITH AND CREDIT NOR THE TAXING POWER OF THE DISTRICT, THE DESIGNATED CFDS, THE STATE OR ANY OTHER POLITICAL SUBDIVISION THEREOF IS PLEDGED TO THE PAYMENT OF THE BONDS. NEITHER THE BONDS NOR THE LEASE PAYMENTS CONSTITUTE AN INDEBTEDNESS WITHIN THE MEANING OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION.

Lease Payments are subject to complete or partial abatement in the event and to the extent that there is substantial interference with the District’s right to use and occupy any portion of the Site or any material portion thereof. See “RISK FACTORS – Abatement” herein. Abatement of Lease Payments under the Lease Agreement, to the extent payment is not made from alternative sources as discussed below, would result in all Bond owners receiving less than the full amount of principal of and interest on the Bonds. To the extent proceeds of rental interruption insurance are available or there are moneys in the Reserve Fund (as described below), Lease Payments (or a portion thereof) may be made during periods of abatement.

The Authority

The Authority was established pursuant to a joint exercise of powers agreement approved and executed by the District and CFD No. 2 (defined below) as of January 16, 2001, in accordance with the provisions of California law. The Authority was created for the purpose of providing financing for public capital improvements of the District. See “THE AUTHORITY” herein.

The District

The District was established in 1976 and comprises approximately 49 square miles of territory in the northern portion of San Diego County. The District includes the City of San Marcos (the “City”), portions of the incorporated cities of Carlsbad, Escondido and Vista and portions of unincorporated territory in the County. Approximately 60% of the territory of the District is within the jurisdictional limits and sphere of influence of the City. The District currently administers eleven elementary schools providing instruction in grades kindergarten through five, three middle schools, two comprehensive high schools and one alternative high school. The District’s 2009-10 student enrollment as of October 2009 was 18,088.

Risk Factors

Certain events could affect the ability of the District to make the Lease Payments which provide revenues to the Authority to pay the Bonds when due. See “RISK FACTORS” for a discussion of certain factors that should be considered, in addition to other matters set forth herein, in evaluating an investment in the Bonds.

Municipal Bond Insurance

Concurrently with the issuance of the Bonds, Assured Guaranty Municipal Corp. (formerly known as Financial Security Assurance, Inc.) will issue its Municipal Bond Insurance Policy (the “Insurance Policy”) with respect to the Bonds. The Insurance Policy guarantees the scheduled payment of principal of (or, in the case of the Capital Appreciation Bonds, the Accreted Value) and interest on the Bonds when due as set forth in the Insurance Policy included as APPENDIX K to this Official Statement. See “BOND INSURANCE” herein.

Tax Matters

In the opinion of Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel, based upon an analysis of existing statutes, regulations, rulings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, as described herein, interest on the Bonds is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986, and is exempt from State personal income taxes. In the further opinion

3

of Bond Counsel, interest on the Bonds is not a specific preference item for purposes of the federal, individual or corporate alternative minimum taxes, nor is it included in adjusted current earnings when calculating corporate alternative minimum taxable income. Bond Counsel expresses no opinion regarding other federal or State consequences relating to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See “TAX MATTERS – Opinion of Bond Counsel.”

Continuing Disclosure

In order to assist the original purchaser and underwriter of the Bonds in complying with Rule 15c2-12(b)(5) of the Securities and Exchange Commission, the Authority and the District will undertake, pursuant to the Lease Agreement and a Continuing Disclosure Agreement, to provide certain annual financial information and notices of the occurrence of certain events, if material. See “CONTINUING DISCLOSURE” herein.

Except as provided in the following sentence, neither the Authority nor the District has failed to comply, in all material respects, with any annual or material event reporting requirements of any undertakings. The District unintentionally failed to timely file the annual report for Fiscal Year 2004-05 pursuant to the undertaking entered into for the School Facilities Improvement District No. 1 of the San Marcos Unified School District 2004 General Obligation Refunding Bonds. Such annual report has since been completed and was filed on April 15, 2010.

Professionals Involved in the Offering

Dolinka Group, LLC, Irvine, California, is the Authority’s and the District’s financial consultant with respect to the Bonds. The proceedings of the Authority in connection with the issuance of the Bonds are subject to the approval as to their legality of Bowie, Arneson, Wiles & Giannone, Newport Beach, California, Bond Counsel to the Authority. Bowie, Arneson, Wiles & Giannone is also serving as counsel to the Authority and the District. Best Best & Krieger LLP, San Diego, California, will serve as Disclosure Counsel to the District and the Authority. McFarlin & Anderson LLP, Lake Forest, California, is serving as counsel to the Underwriter. The Insurer is represented by its Associate General Counsel. Union Bank, N.A., Los Angeles, California, will act as the Trustee under the Trust Agreement.

Forward Looking Statements

Certain statements included or incorporated by reference in this Official Statement constitute “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995, Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. Such statements are generally identifiable by the terminology used such as “plan,” “expect,” “estimate,” “project,” “budget” or similar words. Such forward-looking statements include, but are not limited to certain statements contained in the information under the caption “APPENDIX E – SURPLUS NET SPECIAL TAXES – Estimated Assessed Value-to-Lien Ratios,” “APPENDIX E – SURPLUS NET SPECIAL TAXES – Estimated Surplus Net Special Taxes for Each Designated CFD” and “APPENDIX F - ESTIMATED DEBT SERVICE COVERAGE ON THE BONDS FROM REDEVELOPMENT PAYMENTS AND NET SURPLUS SPECIAL TAXES.”

THE ACHIEVEMENT OF CERTAIN RESULTS OR OTHER EXPECTATIONS CONTAINED IN SUCH FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER FACTORS WHICH MAY CAUSE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS DESCRIBED TO BE MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. NEITHER THE AUTHORITY NOR THE DISTRICT PLANS TO ISSUE ANY UPDATES OR REVISIONS TO THE FORWARD-LOOKING STATEMENTS SET FORTH IN THIS OFFICIAL STATEMENT.

4

General

This Official Statement speaks only as of its date, and the information contained herein is subject to change. All references herein to the Trust Agreement, the Lease Agreement and the Pledge Agreement are qualified in their entirety by reference to the Trust Agreement, the Lease Agreement and the Pledge Agreement and all references to the Bonds are further qualified by reference to the definitive Bonds and to the terms thereof which are contained in the Trust Agreement.

5

ESTIMATED SOURCES AND USES OF FUNDS

The anticipated sources and uses of funds relating to the Bonds, excluding accrued interest which will be deposited in the Interest Account of the Bond Fund, are summarized below.

Sources Principal Amount of Bonds $51,448,327.30 Less Net Original Issue Discount (719,614.45) Less Purchaser’s Discount (643,104.09) Total Sources $50,085,608.76

Uses Deposit to Construction Fund(1) $46,184,224.69 Deposit to Costs of Issuance Fund(2) 1,167,948.28 Deposit to the Reserve Fund 2,394,097.77 Deposit to Capitalized Interest Account of the Bond Fund(3) 339,338.02 Total Uses $50,085,608.76

(1) This amount will be used to finance capital projects for the District. See “FINANCING PLAN – The Project” herein. (2) This amount includes legal, financial advisory, rating agency, printing, Insurance Policy and Debt Service Reserve Policy premiums and fees and other miscellaneous Costs of Issuance. (3) This amount will be used to pay capitalized interest on the Bonds through August 15, 2010.

FINANCING PLAN

The Project

The Project will include the design, construction, renovation, installation, improvement, furnishing, equipping, acquisition, delivery and installation of new construction and modernization projects at the school sites identified below, and such costs shall include, but not be limited to, preparation, planning, engineering and architectural work, infrastructure and related expenses, site preparation, project management costs, and related geotechnical, State planning review costs, environmental review and mitigation costs, local government planning and/or environmental costs and fees for, including, but not limited to, the following District schools and the support facilities and land necessary for these school facilities: (a) Alvin Dunn Elementary School; (b) Carrillo Elementary School; (c) Discovery Elementary School; (d) Knob Hill Elementary School; (e) La Costa Meadows Elementary School; (f) Mission Hills High School; (g) Paloma Elementary School; (h) Richland Elementary School; (i) San Elijo Elementary School; (j) San Elijo Middle School; (k) San Marcos Middle School; (1) San Marcos High School; (m) Twin Oaks Elementary School; (n) Twin Oaks High School; (o) Woodland Park Middle School, (p) San Marcos Elementary School and (q) Foothills High School.

The Site

The Site consists of an approximate 44-acre site and improvements that comprise the District’s Mission Hills High School. The Mission Hills High School was constructed to accommodate 1,700 students and opened its doors in August 2004. Built as a comprehensive high school, Mission Hills High School offers the facilities necessary to serve a full range of academic programs and includes specialized spaces for the sciences, arts and career oriented programs to complement the basic classroom learning spaces. In addition, Mission Hills High School has a library, theater, gymnasium and athletic stadium. The District estimates that the current value of the Site is approximately $81 million, based upon estimated land values and existing improvements thereon.

The District is the owner of fee title to the Site. The Site will be leased by the District to the Authority pursuant to a Site Lease, dated as of June 1, 2010, by and between the District, as lessor, and the Authority, as lessee. The Site will be leased back to the District by the Authority pursuant to the Lease Agreement.

6

Substitution or Release of Site

The District shall have the right, but only upon the prior written consent of the Insurer, to substitute alternate real property for any portion of the Site or to release a portion of the Site from the Lease Agreement pursuant to the terms thereof. Any such substitution or release of any portion of the Site shall be subject to certain specific conditions set forth in the Lease Agreement, which are conditions precedent to such substitution or release. The conditions precedent to such substitution and release include, among other such conditions, the following:

• an Independent Appraiser (as defined in APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – DEFINITIONS) shall find (and shall have delivered a certificate to the District, the Trustee and the Insurer setting forth its findings) that the Site, as constituted after such substitution or release: (i) has an annual fair rental value greater than or equal to 105% of the maximum amount of Lease Payments payable by the District in any Rental Period (as defined in APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – DEFINITIONS), and (ii) has a useful life equal to or greater than the useful life of the Site as constituted prior to such substitution or release;

• the District shall provide the Trustee with an Opinion of Bond Counsel (as defined in APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – DEFINITIONS) to the effect that such substitution or release will not, in and of itself, cause the interest on the Bonds to be included in gross income for federal income tax purposes; and

• the District shall certify to the Authority that the substituted real property is of approximately the same degree of essentiality to the District as the portion of the Site for which it is being substituted.

See “APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – THE LEASE AGREEMENT – Substitution or Release of Site” for the other conditions which must be satisfied before the District may substitute alternative real property for any portion of the Site or to release a portion of the Site from the Lease Agreement.

THE BONDS

Payment of Principal and Interest

The Bonds will be issued as current interest bonds (the “Current Interest Bonds”) and capital appreciation bonds (the “Capital Appreciation Bonds”).

Current Interest Bonds. The Current Interest Bonds will be dated the date of their delivery, will bear current interest at the rates and mature on August 15 in the years indicated on the inside cover page hereof. Interest on the Current Interest Bonds will be payable semi-annually on each February 15 and August 15 (the “Payment Dates”), commencing August 15, 2010. Interest on each Current Interest Bond shall be payable on each Payment Date until maturity or earlier redemption, computed using a year of 360 days comprised of twelve 30-day months. Interest on any Current Interest Bond shall be payable from the Payment Date next preceding the date of authentication thereof, unless: (i) it is authenticated on or before a Payment Date and after the close of business on the preceding Record Date (defined below), in which event interest shall be payable from such Payment Date; or (ii) it is authenticated prior to the first Record Date, in which event interest thereon shall be payable from the Dated Date; provided, however, that if on the date of authentication of any Current Interest Bond interest thereon is in default, interest thereon shall be payable from the Payment Date to which interest has previously been paid or made available for payment or if no interest has been paid or made available for payment, from the Dated Date.

Capital Appreciation Bonds. The Capital Appreciation Bonds will be dated the date of their delivery. The Capital Appreciation Bonds are payable only at maturity and will not pay interest on a current basis. The maturity value of a Capital Appreciation Bond is equal to the Accreted Value (as defined in APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS) upon the maturity thereof (the “Maturity Value”), being composed of its original principal amount (the “Denominational Amount”) and the interest accreting thereon between the date of delivery thereof and its respective maturity date.

7

General. Interest on the Current Interest Bonds is payable in lawful money of the United States of America on each Payment Date to the persons shown as the registered Owners of the Current Interest Bonds on the registration books of the Trustee (the “Registration Books”) as of the first day of the calendar month of the Payment Date (whether or not such day is a business day) (the “Record Date”), payable by check mailed by first-class mail to such Owners on the Payment Date. Payment of such interest, at the option of any Owner of at least $1,000,000 in aggregate principal amount of Current Interest Bonds, will be transmitted by wire transfer to an account in the United States if such Owner makes a written request of the Trustee prior to the first day of the calendar month of the Payment Date specifying the account address. The notice may provide that it will remain in effect for subsequent interest payments until changed or revoked by another written notice.

The Bonds are payable as to principal or Accreted Value, as applicable, upon surrender thereof at the Office of the Trustee. The principal or Accreted Value of the Bonds, as applicable, shall be payable by check in lawful money of the United States of America.

Registration of the Bonds

The Bonds will be issued as fully-registered bonds in book-entry form and in the denomination of $5,000 principal amount or $5,000 Maturity Value, as applicable, or any integral multiple thereof. The Bonds will be dated June 22, 2010, will bear or accrete interest at the rates per annum and will mature on the dates and in the principal amounts, or Maturity Values, as applicable, as set forth on the inside cover page hereof.

Notwithstanding the foregoing, while the Bonds are held in the book-entry system of DTC, all such payments of principal, interest, Maturity Value and premium, if any, will be made to Cede & Co. as the registered owner of the Bonds, for subsequent disbursement to Participants (as defined in Appendix I) and beneficial owners. See “Book-Entry System” below.

Redemption

Optional Redemption. The Current Interest Bonds maturing on or before August 15, 2020, are not subject to optional redemption prior to maturity. Current Interest Bonds maturing on or after August 15, 2021, are subject to redemption prior to maturity from any funds legally available therefor and deposited with the Trustee and on deposit in the Optional Redemption Account of the Redemption Fund, in whole or in part on any date, on or after August 15, 2020, at the principal amount of the Current Interest Bonds to be redeemed, plus accrued but unpaid interest to the redemption date, without premium.

The Capital Appreciation Bonds are not subject to optional redemption prior to maturity.

Special Mandatory Redemption from Insurance or Condemnation Proceeds. The Current Interest Bonds are subject to mandatory redemption prior to maturity, as a whole or in part on any date, at a redemption price equal to the principal amount thereof plus accrued but unpaid interest to the redemption date, without premium, from Net Proceeds (as defined in APPENDIX A – SUMMARY OF THE PRINCIPAL LEGAL DOCUMENTS - DEFINITIONS) deposited in the Mandatory Redemption Account of the Redemption Fund pursuant to the Trust Agreement following an event of damage to, or destruction, theft or condemnation of, the Site or any portion thereof or loss of the use or possession of the Site or any portion thereof due to a title defect.

The Capital Appreciation Bonds are subject to mandatory redemption prior to maturity, as a whole or in part on any date, as a redemption price equal to the Accreted Value thereof on the redemption date, without premium, from Net Proceeds deposited in the Mandatory Redemption Account of the Redemption Fund pursuant to the Trust Agreement following an event of damage to, or destruction, theft or condemnation of, the Site or any portion thereof or loss of the use or possession of the Site or any portion thereof due to a title defect.

Sinking Fund Redemption. The Current Interest Bonds maturing on August 15, 2035, are subject to sinking fund redemption, in part, by lot, on August 15, 2034, and on each August 15 thereafter prior to maturity, from Sinking Fund Payments on deposit in the Sinking Fund Redemption Account of the

8

Redemption Fund, at the principal amount of such Current Interest Bonds to be redeemed, without premium, plus accrued but unpaid interest to the redemption date as indicated on the following table:

Sinking Fund Redemption Date

(August 15)

Principal Amount

To be Redeemed 2034 $2,525,000 2035 (maturity) 3,965,000

The Current Interest Bonds maturing on August 15, 2040, are subject to sinking fund redemption, in

part, by lot, on August 15, 2036, and on each August 15 thereafter prior to maturity, from Sinking Fund Payments on deposit in the Sinking Fund Redemption Account of the Redemption Fund, at the principal amount of such Bonds to be redeemed, without premium, plus accrued but unpaid interest to the redemption date as indicated on the following table:

Sinking Fund Redemption Date

(August 15)

Principal Amount

to be Redeemed 2036 $4,375,000 2037 4,470,000 2038 4,385,000 2039 4,600,000 2040 (maturity) 4,805,000

In the event of a partial redemption of the Current Interest Bonds maturing on August 15, 2035, or on

August 15, 2040, Sinking Fund Payments for such Current Interest Bonds shall be proportionately reduced pursuant to calculations made by the Trustee.

Selection of Bonds for Redemption. Whenever provision is made in the Trust Agreement for the redemption of Bonds (other than from Sinking Fund Payments for sinking fund redemption) and less than all Outstanding Bonds are to be redeemed, an Authority Representative shall direct the principal amount of each maturity of Bonds to be redeemed. Within a maturity, the Trustee shall select Bonds for redemption by lot. Redemption by lot shall be in such manner as the Trustee shall determine; provided, however, that (a) the portion of any Current Interest Bond to be redeemed in part shall be in the principal amount of $5,000 or any integral multiple thereof and (b) the portion of any Capital Appreciation Bonds to be redeemed shall be in integral multiples of the Accreted Value per $5,000 Maturity Value of Capital Appreciation Bonds.

In the event that Bonds are to be subject to optional and sinking fund redemption or special mandatory and sinking fund redemption on the same date, the Trustee shall first select the Bonds to be redeemed by lot for sinking fund redemption. Upon the occurrence of optional redemption or special mandatory redemption, the Trustee shall immediately notify the Insurer in writing of the Bonds selected for redemption, which shall be subject to the Insurer’s approval, which approval shall not be unreasonably withheld or delayed. A failure by the Insurer to object to the Bonds selected for such redemption within five Business Days shall, for all purposes, be deemed an approval of such selection.

Notice of Redemption. When redemption is authorized or required pursuant to the provisions of the Trust Agreement, the Trustee shall give to the Owners and the Insurer notice of the redemption of the Bonds at the expense of the Authority. Such redemption notice shall specify: (a) that the whole or a designated portion of the Bonds is to be redeemed, (b) the numbers (if less than all the Bonds of a maturity are to be redeemed) and CUSIP® numbers of the Bonds to be redeemed, (c) the date of notice and the date of redemption, (d) the place or places where the redemption will be made including the name and address of any redemption agent, and (e) descriptive information regarding the Bonds, including the dated date, interest rates and stated maturity dates. Such notice shall further state that on the specified redemption date there shall become due and payable upon each Bond to be redeemed, the principal or Accreted Value, as applicable (or portion) with respect thereto, together with interest accrued or accreted, as applicable, to said redemption date and redemption premium, if any, and that from and after such redemption date interest with respect thereto shall cease to accrue or accrete, as applicable, and be payable (or in the case of a partial redemption, interest shall cease to

9

accrue or accrete, as applicable, with respect to such redeemed portion) from and after this date fixed for redemption.

Neither failure to receive any redemption notice nor any defect in such redemption notice so given shall affect the sufficiency of the proceedings for the redemption of the Bonds.

Any notice of redemption may specify that redemption of the Bonds designated for redemption on the specified redemption date will be subject to the receipt by the Authority of moneys sufficient to cause such redemption (and will specify the proposed source of such moneys), and neither the Authority, the District nor the Trustee will have any liability to the Owners of any Bonds, or any other party, as the result of the Authority’s failure to redeem the Bonds designated for redemption as a result of insufficient moneys therefor.

Partial Redemption of Bonds. Upon surrender of any Bond redeemed in part only, the Trustee shall execute, and deliver to the Owner thereof, at the expense of the Authority, a new Bond or Bonds in an amount equal in aggregate principal amount to the unredeemed portion of the Bond surrendered and of the same interest rate and the same principal Payment Date. Such partial redemption shall be valid upon payment of the amount thereby required to be paid to such Owner, and the Authority, the District and the Trustee shall be released and discharged from all liability to the extent of such payment.

Rescission of Notice of Optional Redemption. The Authority may rescind any optional redemption of the Bonds, and notice thereof, for any reason on any date prior to the date fixed for such redemption by causing written notice of the rescission to be given to the Owners of the Bonds so called for redemption. Notice of rescission of redemption shall be given in the same manner in which the Redemption Notice was originally given. The actual receipt by the Owner of any Bond of notice of such rescission shall not be a condition precedent to rescission, and failure to receive such notice or any defect in such notice shall not affect the validity of the rescission. Neither the Authority nor the Trustee shall have any liability to the Owners of any Bonds, or any other party, as a result of the Authority’s decision to rescind the redemption of any Bonds pursuant to the provisions of the Trust Agreement.

Effect of Redemption. Notice of redemption having been given, and the moneys for the redemption, including interest to the applicable redemption date, having been set aside in the Redemption Fund, the portion of Bonds to be redeemed shall become due and payable on said redemption date, and, upon presentation and surrender thereof at the office or offices specified in such notice, such Bonds shall be paid at the redemption price with respect thereto, plus any unpaid and accrued interest to said redemption date.

When any Bond or portion thereof has been duly called for redemption prior to maturity, or with respect to which irrevocable instructions to call for redemption prior to maturity at the earliest redemption date have been given to the Trustee, in form satisfactory to it, and sufficient money shall be held by the Trustee irrevocably in trust for the redemption price of such Bond or portion thereof, and accrued interest thereon to the date fixed for redemption, all as provided in the Trust Agreement, then such Bond or portion thereof shall no longer be deemed Outstanding under the provisions of the Trust Agreement.

Purchase in Lieu of Redemption. Without the prior written consent of the Insurer, no Bonds shall be purchased by the Authority, the District or any of its affiliates, in lieu of redemption, unless such Bonds are redeemed, defeased or cancelled. With the prior written consent of the Insurer, money held in the Redemption Fund and money held in the Principal Account of the Bond Fund may be used to reimburse the Authority for the purchases of Bonds that would otherwise be subject to redemption from such moneys upon the delivery of such Bonds to the Trustee for cancellation at least 10 days prior to the date on which the Trustee is required to select Bonds for redemption. The purchase price of any Bonds purchased by the Authority shall not exceed the applicable redemption price of the Bonds which would be redeemed (accrued interest to be paid from the Interest Account of the Bond Fund). Any such purchase must be completed prior to the time notice would otherwise be required to be given to redeem the related Bonds. All Bonds so purchased shall be surrendered to the Trustee for cancellation and applied as a credit against the obligation to redeem Bonds from such moneys.

Transfer of Bonds. Each Bond shall be transferable only upon the Bond Register which shall be kept for that purpose at the Principal Office of the Trustee, by the registered Owner thereof in person or by his attorney duly authorized in writing, upon surrender thereof, together with a written instrument of transfer

10

satisfactory to the Trustee, duly executed by the registered Owner or his duly authorized attorney. Upon the transfer of any such Bond, the Trustee shall provide in the name of the transferee, a new Bond, or Bonds, of the same aggregate principal amount and maturity as the surrendered Bonds (unless there has occurred a partial redemption of such Bond in which case the principal amount of the new Bond shall be equal to the unredeemed principal portion of the Bond submitted for transfer).

Exchange of Bonds. Bonds may be exchanged at the Principal Office of the Trustee for a like aggregate principal amount of bonds of other authorized denominations of the same maturity and interest rate.

The Trustee

Union Bank, N.A., Los Angeles, California, has been appointed as the initial Trustee for the Bonds under the Trust Agreement. See “APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – Trust Agreement” for a further description of the rights and obligations of the Trustee under the Trust Agreement.

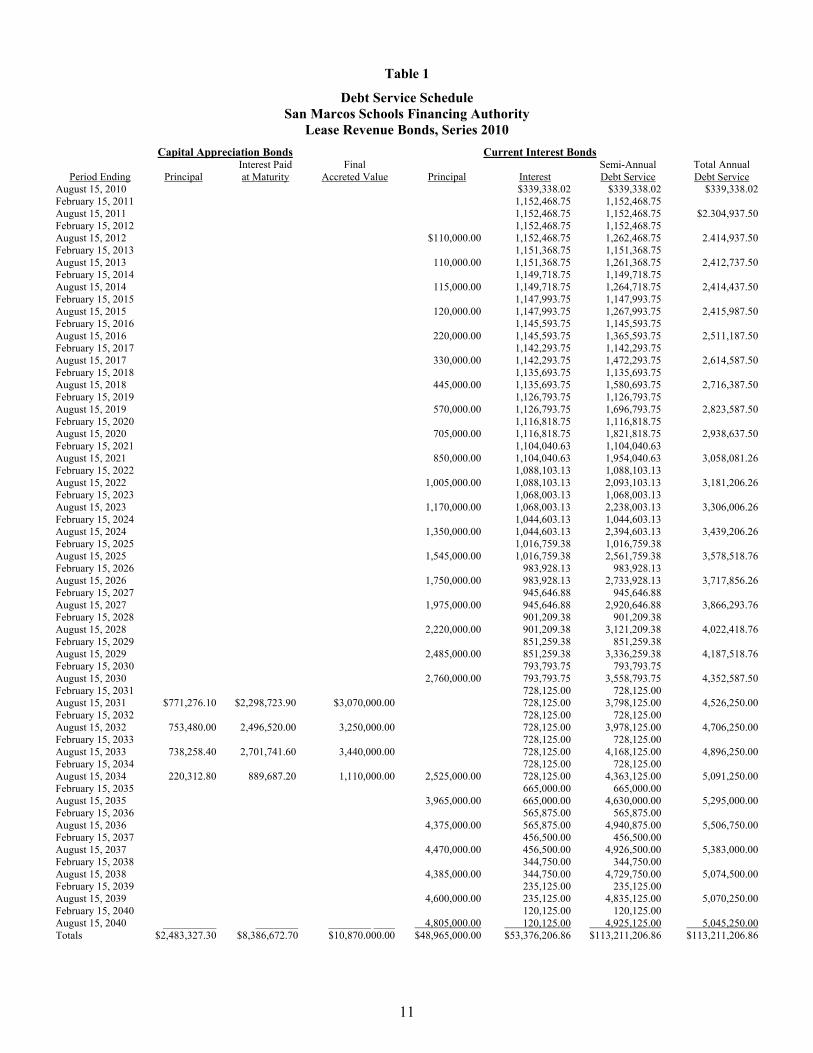

Debt Service Schedule

The table below sets forth the annual debt service for the Bonds based on the maturity schedule and interest rates set forth on the inside cover page of this Official Statement.

11

Table 1

Debt Service Schedule San Marcos Schools Financing Authority

Lease Revenue Bonds, Series 2010 Capital Appreciation Bonds Current Interest Bonds

Period Ending Principal Interest Paid at Maturity

Final Accreted Value Principal Interest

Semi-Annual Debt Service

Total Annual Debt Service

August 15, 2010 $339,338.02 $339,338.02 $339,338.02 February 15, 2011 1,152,468.75 1,152,468.75 August 15, 2011 1,152,468.75 1,152,468.75 $2.304,937.50 February 15, 2012 1,152,468.75 1,152,468.75 August 15, 2012 $110,000.00 1,152,468.75 1,262,468.75 2.414,937.50 February 15, 2013 1,151,368.75 1,151,368.75 August 15, 2013 110,000.00 1,151,368.75 1,261,368.75 2,412,737.50 February 15, 2014 1,149,718.75 1,149,718.75 August 15, 2014 115,000.00 1,149,718.75 1,264,718.75 2,414,437.50 February 15, 2015 1,147,993.75 1,147,993.75 August 15, 2015 120,000.00 1,147,993.75 1,267,993.75 2,415,987.50 February 15, 2016 1,145,593.75 1,145,593.75 August 15, 2016 220,000.00 1,145,593.75 1,365,593.75 2,511,187.50 February 15, 2017 1,142,293.75 1,142,293.75 August 15, 2017 330,000.00 1,142,293.75 1,472,293.75 2,614,587.50 February 15, 2018 1,135,693.75 1,135,693.75 August 15, 2018 445,000.00 1,135,693.75 1,580,693.75 2,716,387.50 February 15, 2019 1,126,793.75 1,126,793.75 August 15, 2019 570,000.00 1,126,793.75 1,696,793.75 2,823,587.50 February 15, 2020 1,116,818.75 1,116,818.75 August 15, 2020 705,000.00 1,116,818.75 1,821,818.75 2,938,637.50 February 15, 2021 1,104,040.63 1,104,040.63 August 15, 2021 850,000.00 1,104,040.63 1,954,040.63 3,058,081.26 February 15, 2022 1,088,103.13 1,088,103.13 August 15, 2022 1,005,000.00 1,088,103.13 2,093,103.13 3,181,206.26 February 15, 2023 1,068,003.13 1,068,003.13 August 15, 2023 1,170,000.00 1,068,003.13 2,238,003.13 3,306,006.26 February 15, 2024 1,044,603.13 1,044,603.13 August 15, 2024 1,350,000.00 1,044,603.13 2,394,603.13 3,439,206.26 February 15, 2025 1,016,759.38 1,016,759.38 August 15, 2025 1,545,000.00 1,016,759.38 2,561,759.38 3,578,518.76 February 15, 2026 983,928.13 983,928.13 August 15, 2026 1,750,000.00 983,928.13 2,733,928.13 3,717,856.26 February 15, 2027 945,646.88 945,646.88 August 15, 2027 1,975,000.00 945,646.88 2,920,646.88 3,866,293.76 February 15, 2028 901,209.38 901,209.38 August 15, 2028 2,220,000.00 901,209.38 3,121,209.38 4,022,418.76 February 15, 2029 851,259.38 851,259.38 August 15, 2029 2,485,000.00 851,259.38 3,336,259.38 4,187,518.76 February 15, 2030 793,793.75 793,793.75 August 15, 2030 2,760,000.00 793,793.75 3,558,793.75 4,352,587.50 February 15, 2031 728,125.00 728,125.00 August 15, 2031 $771,276.10 $2,298,723.90 $3,070,000.00 728,125.00 3,798,125.00 4,526,250.00 February 15, 2032 728,125.00 728,125.00 August 15, 2032 753,480.00 2,496,520.00 3,250,000.00 728,125.00 3,978,125.00 4,706,250.00 February 15, 2033 728,125.00 728,125.00 August 15, 2033 738,258.40 2,701,741.60 3,440,000.00 728,125.00 4,168,125.00 4,896,250.00 February 15, 2034 728,125.00 728,125.00 August 15, 2034 220,312.80 889,687.20 1,110,000.00 2,525,000.00 728,125.00 4,363,125.00 5,091,250.00 February 15, 2035 665,000.00 665,000.00 August 15, 2035 3,965,000.00 665,000.00 4,630,000.00 5,295,000.00 February 15, 2036 565,875.00 565,875.00 August 15, 2036 4,375,000.00 565,875.00 4,940,875.00 5,506,750.00 February 15, 2037 456,500.00 456,500.00 August 15, 2037 4,470,000.00 456,500.00 4,926,500.00 5,383,000.00 February 15, 2038 344,750.00 344,750.00 August 15, 2038 4,385,000.00 344,750.00 4,729,750.00 5,074,500.00 February 15, 2039 235,125.00 235,125.00 August 15, 2039 4,600,000.00 235,125.00 4,835,125.00 5,070,250.00 February 15, 2040 120,125.00 120,125.00 August 15, 2040 __________ ________ ________ ____ 4,805,000.00 120,125.00 4,925,125.00 5,045,250.00 Totals $2,483,327.30 $8,386,672.70 $10,870.000.00 $48,965,000.00 $53,376,206.86 $113,211,206.86 $113,211,206.86

12

Book-Entry System

DTC will act as securities depository for the Bonds. The Bonds will be issued as fully-registered certificates registered in the name of Cede & Co. (DTC’s partnership nominee). One fully-registered Bond will be issued for each maturity of the Bonds, each in the aggregate principal amount of such maturity, and will be deposited with DTC. See “APPENDIX I – BOOK-ENTRY-ONLY SYSTEM” herein.

The Authority and the Trustee cannot and do not give any assurances that DTC, DTC Participants or any other person will distribute payments of principal, interest or premium, if any, with respect to the Bonds paid to DTC or its nominee as the registered owner, or will distribute any prepayment notices or other notices, to the Beneficial Owners, or that they will do so on a timely basis or will serve and act in the manner described in this Official Statement. The Authority and the Trustee are not responsible or liable for the failure of DTC or any DTC Participant to make any payment or give any notice to a Beneficial Owner with respect to the Bonds or an error or delay relating thereto.

SECURITY FOR THE BONDS

The principal of and interest on the Bonds are not a debt of the Authority or the District, nor a legal or equitable pledge, charge, lien or encumbrance, upon any of their respective property, or upon any of their income, receipts, or revenues except the Revenues (defined below) and other amounts pledged under the Trust Agreement.

This section provides summaries of the security for the Bonds and certain provisions of the Trust Agreement, the Lease Agreement, the Site Lease and the Pledge Agreement. See “APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS” for a more complete summary of the Trust Agreement, the Lease Agreement, the Site Lease and the Pledge Agreement.

General

The Bonds are special obligations of the Authority secured by Revenues, primarily consisting of Lease Payments to be made by the District pursuant to the Lease Agreement, certain amounts on deposit under the Trust Agreement and certain investment earnings thereon.

The Authority, pursuant to the Assignment Agreement, will sell, assign and transfer to the Trustee for the benefit of the Owners substantially all of the Authority’s right, title and interest in and to the Site Lease and the Lease Agreement, including, without limitation, its right to receive Lease Payments and other rental to be paid by the District under the Lease Agreement and the right to exercise such rights and remedies as are conferred on the Authority by the Lease Agreement as may be necessary to enforce payment of the Lease Payments and other rental when due, or otherwise protect the Authority’s interests in the event of a default by the District under the Lease Agreement. The District will pay Lease Payments directly to the Trustee, as assignee of the Authority. See “Lease Payments” below.

Pledge of Revenues

Under the Trust Agreement, the Authority and the District, as their respective interests may appear, expressly grant to the Trustee for the benefit of the Owners a first lien on and a security interest in all “Revenues” held by the Trustee under the Trust Agreement (with the exception of the Construction Fund, Costs of Issuance Fund, and the Rebate Fund and any moneys to be deposited therein or interest earnings thereon), including, without limitation, the Bond Fund, the Lease Payment Fund, the Reserve Fund (including payments of Reserve Replenishment Rent), the Redemption Fund, and the Insurance and Condemnation Fund, and all such moneys shall be held by the Trustee in trust and applied to the respective purposes specified in the Trust Agreement and in the Lease Agreement.

“Revenues” are defined in the Trust Agreement as: (a) all revenues, issues, income, rents, royalties, profits and receipts derived or to be derived by the Authority from or attributable to the lease of the Site to the

13

District, including revenues attributable to the lease of the Site or to the payment of the costs thereof received or to be received by the Authority under the Lease Agreement or any contractual arrangement with respect to the use of the Site, including the payment of the Lease Payments, Additional Rent and Reserve Replenishment Rent thereunder; (b) the proceeds of any insurance, including the proceeds of any self-insurance covering the loss relating to the Site; (c) all proceeds of rental interruption insurance policies, if any, carried with respect to the Site pursuant to the Lease Agreement; (d) all amounts on hand from time to time in the funds and accounts established under the Trust Agreement (other than the Construction Fund, Costs of Issuance Fund and the Rebate Fund); and (e) any additional property that may, from time to time, by delivery or by writing of any kind, be subjected to the lien of the Trust Agreement by the Authority or by anyone on the Authority’s behalf, subject only to the provisions of the Trust Agreement and the Lease Agreement.

THE OBLIGATION OF THE DISTRICT TO PAY THE LEASE PAYMENTS DOES NOT CONSTITUTE AN INDEBTEDNESS OF THE DISTRICT, THE AUTHORITY, ANY MEMBERS OF THE AUTHORITY, THE DESIGNATED CFDS, THE STATE OR ANY OF ITS POLITICAL SUBDIVISIONS WITHIN THE MEANING OF ANY CONSTITUTIONAL OR STATUTORY DEBT LIMITATION OR RESTRICTION. THE OBLIGATION OF THE DISTRICT TO PAY THE LEASE PAYMENTS DOES NOT CONSTITUTE AN OBLIGATION OF THE DISTRICT FOR WHICH THE DISTRICT IS OBLIGATED TO LEVY OR PLEDGE ANY FORM OF TAXATION OR FOR WHICH THE DISTRICT HAS LEVIED OR PLEDGED ANY FORM OF TAXATION.

Lease Payment Fund

All Lease Payments received by the Trustee under the Lease Agreement shall be deposited into the Lease Payment Fund established pursuant to the Trust Agreement. The Trustee shall transfer on each Payment Date from the Lease Payment Fund to the Interest Account of the Bond Fund an amount which, together with any amount on deposit therein, equals the interest then due on such Payment Date on the Bonds. The Trustee shall transfer on each maturity date for the Bonds from the Lease Payment Fund to the Sinking Fund Redemption Account of the Redemption Fund, or the Principal Account of the Bond Fund, as applicable, an amount which, together with any amount on deposit therein, equals the principal then due on such maturity date with respect to the Bonds in accordance with the terms of the Trust Agreement.

All delinquent Lease Payments received by the Trustee pursuant to the Lease Agreement and the proceeds of rental interruption insurance with respect to the Site, if any, received by the Trustee shall be deposited into the Lease Payment Fund. All proceeds of rental interruption insurance and delinquent Lease Payments so received shall be applied first to the payment of overdue installments of interest on the Bonds, then to the payment of any overdue installments of principal of the Bonds and then to make up any deficiency in the Reserve Fund. Any amounts remaining in the Lease Payment Fund on each Payment Date or maturity date which are not required for the payment of principal or interest on the next succeeding Payment Date or maturity date shall be first transferred to the Reserve Fund to the extent necessary to make the amount on deposit therein equal to the Reserve Requirement and, second, applied as a credit against the next following Lease Payment, including any remaining money representing delinquent Lease Payments and any proceeds of rental interruption insurance, which shall remain on deposit in the Lease Payment Fund.

Bond Fund

The Trustee shall establish the Bond Fund pursuant to the Trust Agreement and, within the Bond Fund, the Trustee shall establish the Interest Account, the Capitalized Interest Account and the Principal Account. Moneys transferred to the Interest Account, the Capitalized Interest Account and the Principal Account shall be applied by the Trustee to the payment of interest and principal due and payable on the Bonds. See “APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS.”

Reserve Fund

Application of Moneys in the Reserve Fund or Reserve Facility. If, on any Payment Date, the amount on deposit in the Lease Payment Fund is insufficient to pay the principal and interest accrued or

14

accreted on the Bonds on such Payment Date, the Trustee shall transfer from the Reserve Fund and deposit in the Lease Payment Fund an amount sufficient to make up such deficiency. If a Reserve Facility (defined below) is credited to the Reserve Fund to satisfy a portion of the Reserve Requirement (defined below), the Trustee shall make a claim for payment under such Reserve Facility, in accordance with the provisions thereof, in an amount which, together with other available moneys in the Reserve Fund, will be sufficient to make said deposit in the Lease Payment Fund. See “APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – Trust Agreement.”

Reserve Requirement. The “Reserve Requirement” is defined in the Trust Agreement, as of the date of calculation, as an amount equal to the least of:

(i) 125% of the average annual aggregate Lease Payments over the remaining term of the Lease Agreement;

(ii) the maximum aggregate annual Lease Payments over the remaining term of the Lease Agreement; or

(iii) ten percent (10%) of the net proceeds of the Bonds.

The Reserve Requirement on the Delivery Date of the Bonds shall be satisfied by a cash deposit from the Bond proceeds in the amount of $2,394,097.77 and the delivery to the Trustee of a Reserve Facility in the form of the Debt Service Reserve Insurance Policy to be issued by the Insurer in the coverage amount of $2,300,000.

Reserve Facility. The Authority may substitute a line of credit, letter of credit, insurance policy, surety bond or other credit source deposited with the Trustee pursuant to the provisions of the Trust Agreement (“Reserve Facility”) for all or part of the moneys on deposit in the Reserve Fund by depositing such Reserve Facility with the Trustee so long as, at the time of such substitution, the amount on deposit in the Reserve Fund, together with the amount available under such Reserve Facility and any previously substituted Reserve Facilities, shall be at least equal to the Reserve Requirement; provided, however, that prior to any such substitution, the Trustee shall have received written confirmation from the Rating Agencies (defined below) that such substitution would not cause such Rating Agencies to lower or withdraw its rating then in effect with respect to the Bonds. “Rating Agencies” is defined in the Trust Agreement to mean Moody’s (defined below), or any national rating agency then rating the Bonds at the request of the Authority. “Moody’s” is defined in the Trust Agreement to mean Moody’s Investors Service, and its successors and assigns, except that if such corporation shall be dissolved or liquidated or shall no longer perform the functions of a securities rating agency, then the term “Moody’s” shall be deemed to refer to any other nationally recognized securities rating agency selected by the Authority. “S&P” is defined in the Trust Agreement to mean Standard and Poor’s Ratings Services, and its successors and assigns, except that if such corporation shall be dissolved or liquidated or shall no longer perform the functions of a securities rating agency, then the term “S&P” shall be deemed to refer to any other nationally recognized securities rating agency selected by the Authority. The Authority shall not substitute any Reserve Facility in lieu of all or any portion of moneys on deposit in the Reserve Fund without the prior written consent of the Insurer (so long as the Insurer is not in default in its payment obligations under the Insurance Policy).

Moneys for which a Reserve Facility has been substituted as provided in the Trust Agreement shall be transferred, at the election of the Authority, to the Lease Payment Fund, or upon receipt of a written opinion of counsel of recognized standing in the field of law relating to municipal bonds, appointed and paid by the Authority, to the effect that such transfer, in and of itself, will not adversely affect the exclusion of principal and interest accrued or accreted due on the Bonds from gross income for federal income tax purposes, to a special account to be held by the Trustee and applied to the payment of capital costs of the Authority, as directed in a Written Request of the Authority (as defined in APPENDIX A – SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – DEFINITIONS).

Any amounts paid pursuant to any Reserve Facility shall be deposited in the Reserve Fund.

15

Allocation if Cash and a Reserve Facility Are on Deposit. Amounts on deposit in the Reserve Fund which were not derived from payments under any Reserve Facility credited to the Reserve Fund to satisfy a portion of the Reserve Requirement shall be used and withdrawn by the Trustee prior to using and withdrawing any amounts derived from payments under any such Reserve Facility. In order to accomplish such use and withdrawal of such amounts not derived from payments under any such Reserve Facility, the Trustee shall, as and to the extent necessary, liquidate any investments purchased with such amounts. If and to the extent that, more than one Reserve Facility is credited to the Reserve Fund to satisfy a portion of the Reserve Requirement, drawings thereunder, and repayment of expenses with respect thereto, shall be made on a pro rata basis (calculated by reference to the policy limits available thereunder).

Replenishment of the Reserve Fund. If there are no amounts currently due under any Reserve Facility and the sum of the amount on deposit in the Reserve Fund, plus the amount available under any Reserve Facilities, shall be reduced below the Reserve Requirement, the first of Lease Payments thereafter received from the District under the Lease Agreement and not needed to pay the principal and interest accrued or accreted on the Bonds on the next Payment Date, shall be used, first, to reinstate the amounts available under the Reserve Facilities that have been drawn upon and, second, to increase the amount on deposit in the Reserve Fund, so that the amount available under the Reserve Facilities, when added to the amount on deposit in the Reserve Fund, shall equal the Reserve Requirement.