255 Chapter 8 ROLE OF PAYMENT AND SETTLEMENT SYSTEMS IN MONETARY POLICY AND FINANCIAL STABILITY FOR THE PHILIPPINES By Rolando U. Bermas 1 and Geralyn M. Zafra 2 1. Introduction Payment systems are essential to the effective functioning of financial systems worldwide. They provide the channels through which funds are transferred among banks and other institutions to discharge payment obligations arising from economic and financial transactions across the entire economy. An efficient, secure and reliable payment system reduces the cost of exchanging goods and services. It is an essential tool for the effective implementation of monetary policy and the smooth functioning of money and capital markets. In contrast, a payment system that is not efficient, secure and reliable can adversely affect the financial system and the efficient transmission of monetary policy, and that it can, in turn, contribute to a systemic crisis. It is this key role played by payment and settlement systems (PSS) in the smooth functioning of an economy in general and its financial and monetary system in particular that gives the central bank (CB) a strong incentive for ensuring that an effective, reliable and secure payment and settlement system is in place. Central banks have a strong interest in promoting and improving safety and efficiency in payments systems as part of their overall concern with financial and monetary stability. For one, the payments system is important for the smooth functioning and integration of financial markets. It can affect the speed, financial risk, reliability, and cost of domestic and international transactions. As Guitián (1998) observed, the payment system can act as a conduit through which financial and non-financial firms and other agents affect overall financial system stability. The payments system also affects the transmission process in monetary ________________ 1. Mr. Rolando U. Bermas is Bank Officer V at the Payments and Settlements Office (PSO) of the Bangko Sentral ng Pilipinas. 2. Ms. Geralyn M. Zafra is Bank Officer V at the Department of Economic Research (DER) of the Bangko Sentral ng Pilipinas.

Transcript

255

Chapter 8

ROLE OF PAYMENT AND SETTLEMENT SYSTEMS

IN MONETARY POLICY AND FINANCIAL STABILITY

FOR THE PHILIPPINES

By

Rolando U. Bermas 1

and Geralyn M. Zafra2

1. Introduction

Payment systems are essential to the effective functioning of financial

systems worldwide. They provide the channels through which funds are

transferred among banks and other institutions to discharge payment obligations

arising from economic and financial transactions across the entire economy. An

efficient, secure and reliable payment system reduces the cost of exchanging

goods and services. It is an essential tool for the effective implementation of

monetary policy and the smooth functioning of money and capital markets. In

contrast, a payment system that is not efficient, secure and reliable can adversely

affect the financial system and the efficient transmission of monetary policy,

and that it can, in turn, contribute to a systemic crisis. It is this key role played

by payment and settlement systems (PSS) in the smooth functioning of an

economy in general and its financial and monetary system in particular that

gives the central bank (CB) a strong incentive for ensuring that an effective,

reliable and secure payment and settlement system is in place.

Central banks have a strong interest in promoting and improving safety and

efficiency in payments systems as part of their overall concern with financial

and monetary stability. For one, the payments system is important for the smooth

functioning and integration of financial markets. It can affect the speed, financial

risk, reliability, and cost of domestic and international transactions. As Guitián

(1998) observed, the payment system can act as a conduit through which financial

and non-financial firms and other agents affect overall financial system stability.

The payments system also affects the transmission process in monetary

________________

1. Mr. Rolando U. Bermas is Bank Officer V at the Payments and Settlements Office (PSO)

of the Bangko Sentral ng Pilipinas.

2. Ms. Geralyn M. Zafra is Bank Officer V at the Department of Economic Research (DER)

of the Bangko Sentral ng Pilipinas.

256

management, the pace of financial deepening, and the efficiency of financial

intermediation. Consequently, monetary authorities have typically been active in

promoting sound and efficient payments systems and in seeking the means to

reduce related systemic risks.

In the Philippines, the settlement infrastructure has evolved and transformed

from a purely physical settlement structure to a more modern electronic process.

The Bangko Sentral ng Pilipinas (BSP), fully cognizant of its role in establishing

facilities for payment services as mandated under Section 102 of the New Central

Bank Act, 1993, or the BSP Charter (Republic Act No. 7653) and the importance

of a safe and efficient payments system to financial stability, developed a real

time gross settlement system (RTGS) known as the Philippine Payments and

Settlements System (PhilPaSS) on 12 December 2002. The PhilPaSS is an

automated facility that provides online, real time uninterruptible settlement of

high-value payment transactions between banks through the Demand Deposit

Accounts (DDA) of banks maintained with the BSP. As a gross settlement

system, the PhilPaSS processes and settles fund transfer instructions individually,

without netting debits against credits. As a real time settlement system, it effects

final settlement continuously rather than periodically at pre-specified times

provided that a sending bank has a sufficient balance in its DDA.

Since its implementation, the PhilPaSS has evidently minimised the settlement,

operational and other risks related to high-value and critical interbank payments

by providing a safer and cost-efficient channel for the delivery of funds to

intended counterparty-accounts maintained with the BSP. However, the changing

contours of the global financial environment have important implications for the

payment system and financial stability because they provide new sources of risk

and challenges for regulators like the BSP. In particular, developments in technology

and the financial innovation they allow, the increasing size and complexity of

financial systems, and the globalisation of financial markets are reshaping the

landscape in which the payment and settlement system operates.

This paper is generally aimed at identifying the key challenges and issues

affecting the efficiency of the payment and settlement system in the Philippines

and assessing its implications or influence on domestic monetary and financial

stability, and economic performance. The paper starts with this introduction,

followed by a section discussing the BSP policy framework in relation to monetary

stability, financial stability and an efficient payment system. The third section

gives a description of the payment system infrastructure in the Philippines and

talks about the system’s influence on domestic monetary and financial stability,

and economic performance. The paper then also briefly identifies the key issues

257

and challenges affecting the efficiency and reliability of the country’s PSS. The

next section provides an assessment of the efficiency and reliability of the

country’s current PSS infrastructure. Lastly, the paper takes stock of the policy

implications of the developments facing the Philippine payments system today.

2. BSP Policy Framework

Jenkinson (2007) noted that the central banks’ two core functions – monetary,

or more specifically, price stability, and financial stability – emerged from their

earlier role in providing the ultimate settlement asset in the payment system.

From being the provider of the ultimate settlement asset, it became critical for

the central bank to maintain monetary stability. This is because it is the central

bank’s liquid liabilities that are the instruments in which the bulk of domestic

payment obligations are legally finally settled. For central bank money to be

considered safe so that all participants remain confident about its acceptability

as a settlement asset, the promotion of monetary stability became critical.

Central banks also have a natural interest in promoting financial stability.

Specifically, it is the central bank’s role to ensure that the banking sector is able

to meet the public’s demand for liquidity. Allowing a bank run to occur when

a bank is inherently solvent is not in the interest of financial stability as this can

lead to a system-wide crisis that can weaken all banks, and possibly even the

central bank itself. Subsequently, the central bank has an integral role in

guaranteeing the safety, soundness, efficiency and fairness of the payment

system. As former US Federal Reserve Chairman Alan Greenspan observed in

his book, “The Age of Turbulence,” that if someone wanted to cripple the US

economy then they would only have to “…take out the payment system. Banks

would then be forced to fall back on inefficient physical transfers of money…the

level of economic activity across the country could drop like a rock.”

On account of the central banks’ strong interest in financial stability as well

as the maintenance of the public’s confidence in the domestic currency and the

smooth functioning of markets for the implementation of monetary policy, the

central bank needs to take an active interest in the design, development and

smooth functioning of the payment system. As Listfield and Negret (1994) noted,

CBs have “a legitimate and important role in guaranteeing the safety, soundness,

efficiency and fairness of the payment system.”

In accordance with the interrelated role of a CB in monetary and financial

stability and maintenance of a stable payment system, the BSP’s policy

framework revolves around these three main pillars. As prescribed in the BSP

258

charter, the BSP pursues the following primary activities: maintaining price stability

through the conduct of prudent monetary policy; promoting financial stability

through effective banking supervisions and regulation; and ensuring the safety,

soundness and efficiency of the payment and settlement system. These three

pillars serve as guidepost to ensure that the BSP appropriately and quickly

responds to emerging challenges to price and financial stability.

2.1 Monetary Stability

The BSP, as the Philippine’s central monetary authority, has the primary

objective to “maintain price stability conducive to a balanced and sustainable

growth of the economy.” This is spelled out in Section 3 of the New Central

Bank Act of 1993.

Achieving price stability is a universal goal shared by CBs and monetary

authorities all over the world. Price stability, or its equivalent, stability in the

domestic purchasing power of the currency, appears as the dominant or one of

the dominant legal objectives in 33 of 45 CBs (Ortiz, 2009). This does not mean,

however, that the BSP pursues price stability to the exclusion of other objectives.

Although the price stability objective is the BSP’s main priority, other economic

goals—such as achieving broadbased, sustainable economic growth—are given

consideration in policy decision-making. Thus, the BSP coordinates with other

government agencies to ensure that its policies are part of a consistent and

coherent overall policy framework.

Price stability refers to the condition of low and stable inflation. By keeping

price stable, the BSP helps ensure strong and sustainable economic growth and

better living standards. Monetary policy refers to the actions or measures taken

by the BSP to regulate the supply of money in the economy to achieve price

stability.

The BSP has a number of monetary policy instruments at its disposal to

influence the timing, cost and availability of money and credit, as well as other

financial factors, for the purpose of stabilising the price level. Of the monetary

policy tools at its disposal, the main policy levers are the policy interest rates,

which are the overnight repurchase (lending) rate (RP) and the overnight reverse

repurchase (borrowing) rate (RRP). In addition, to increase or reduce liquidity

in the financial system, the BSP also uses open market operations, accepts fixed-

term deposits, offers standing facilities such as the rediscounting facility, and

requires banking institutions to hold reserves on deposits and deposit substitutes.

259

In terms of its approach to monetary policy, the BSP followed the monetary

aggregate targeting approach in the past. This approach is based on the

assumption that there is a stable and predictable relationship between money on

the one hand, and output and inflation on the other hand. In effect, under the

monetary targeting framework, the BSP controls inflation indirectly by targeting

money supply. This approach was modified beginning in the second semester of

1995 under the modified form of monetary targeting to put greater emphasis on

price stability instead of rigidly observing the targets set for monetary aggregates.

On 24 January 2000, the BSP’s policy-making body, the Monetary Board (MB),

approved in principle the shift to inflation targeting as a framework for conducting

monetary policy. This was formally adopted in January 2002.

Inflation targeting focuses mainly on achieving price stability as the ultimate

objective of monetary policy. Under this approach, the BSP commits to keeping

inflation at a pre-announced average rate that the BSP promises to achieve

over a given time period. The BSP then compares the actual headline inflation

against its inflation forecasts. It uses the various monetary policy instruments

at its disposal to achieve the inflation target. This involves mainly adjustments

in the key policy interest rates of the BSP and the use of other instruments,

including rediscounting and reserve requirement. The CB also provides regular

reports explaining its policy decisions and containing its assessment of the inflation

environment and outlook. If the CB fails to meet the inflation target, it is required

to explain to the public why the target was not achieved and to come up with

measures on how to steer inflation towards the target level.

The inflation targets have been set at 4.5% with a tolerance interval of +1.0

percentage point for 2010 and 4.0% with a tolerance interval of +1.0 percentage

point for 2011. In July 2010, the MB announced the BSP’s shift to a fixed

inflation target for the medium term of 4 ± 1% for 2012-2014. The shift to a

fixed medium-term inflation target from a variable annual inflation target was

approved by the Development Budget Coordination Committee (DBCC) on 9

July 2010, under DBCC Resolution No. 2010-3.

During the recent global financial crisis, the BSP maintained a prudent

monetary policy stance to keep inflation in check and allow market interest

rates to decline, hence providing a conducive environment for businesses to

expand. As the impact of the global financial crisis began to be felt and the

Philippine economic growth began to slow down, the sustained decline in the

inflation rate gave the BSP scope to adopt an appropriately accommodative

monetary policy stance. Among the measures implemented accordingly include:

260

• Liquidity-easing measures in 2008 and 2009, including the reduction in bank

reserve requirements by two percentage points, opening of the US dollar

repurchase window, increase in the peso rediscounting budget to P60 billion,

and provision of greater accessibility to these facilities to banking institutions.

• Reduction in the BSP’s policy rates by a total of 200 basis points from

December 2008 to July 2009 to provide liquidity for the orderly functioning

of the financial markets and help support the economy against possible

fragilities in the operating environment.

In 2010, the relatively benign inflation environment afforded the BSP the

flexibility to keep policy rates steady during the year. At the same time, with

economic recovery underway and financial markets starting to normalise, the

BSP gradually unwound the liquidity enhancing measures it implemented in 2008-

2009 to ensure that ample liquidity was available during the global financial crisis.

The peso rediscount rate was aligned with the overnight RRP rate while the

peso rediscounting budget was lowered from P60 billion to the pre-crisis level

of P20 billion. Requirements for the availment of the rediscounting facility were

likewise brought back to their pre-crisis terms.

In early 2011, the BSP continued to unwind from liquidity enhancing

measures in the preceding years to help forestall inflation pressures as

unfavourable weather conditions and protracted tensions in the Middle East and

North Africa (MENA) contributed to mounting pressures on food and oil prices.

In particular, the policy rates were raised by total of 50 basis points from March

– June 2011. The BSP also raised the reserve requirements by two percentage

points as a preemptive move to help manage liquidity given the prospects of

sustained foreign exchange inflows. Subsequently, the BSP found scope to

maintain monetary policy settings, especially as downside risks to global growth

intensified, dampening global growth.

Starting in 2012, the MB decided to hold eight monetary policy meetings a

year to discuss and decide on the appropriate monetary policy stance of the

BSP in order to keep inflation within the target. Based on the assessment of the

macroeconomic environment and the price situation of commodities, the MB

takes the necessary actions consistent with the chosen monetary policy stance.

The MB receives recommendations from the Advisory Committee (AC), a

technical body which meets regularly a few days prior to each MB monetary

policy meeting. The meetings of the AC are intended to serve as a forum for

in-depth, comprehensive, broad-ranging and balanced assessment of monetary

conditions, economic outlook, inflationary expectations, and the forecast inflation

261

path. The AC members agree by majority vote on a set of recommendations

that are then submitted to the MB.

In the first seven months of 2012, amid continued benign inflation and the

modest pace of growth of domestic demand, reflecting mainly the impact of

weaker external demand, the MB cut policy rates by a total of 75 basis points.

Moreover, the MB decided to approve three operational adjustments in the BSP’s

reserve requirement policy during its meeting on 2 February 2012 to increase

the effectiveness of reserve requirement as a monetary policy tool, simplify its

implementation, and improve the monitoring of banks’ compliance. These

adjustments, that were made effective April 2012, include:

• The unification of the existing statutory reserve requirement and liquidity

reserve requirement into a single set of reserve requirement;

• The non-remuneration of the unified reserve requirement;

• The exclusion of vault cash (for banks) and demand deposits (for non-bank

financial institutions with quasi-banking functions) as eligible forms of reserve

requirement compliance;

• The reduction in the reserve requirement ratio by three (3) percentage points

to 18% from 21% to offset the impact on the intermediation costs of banks.

See Table 1 for changes in the BSP policy rates3 and the reserve requirement

ratio from 2001 to 2012.

2.2 Financial Stability

Alongside its mandate to support price stability, the BSP has also been tasked

with maintaining financial stability. While the BSP charter is not explicit on its

financial stability objective, the BSP has pursued the promotion of financial stability

through its mandate to supervise banks and quasi-banks, their subsidiaries and

affiliates, and the non-bank financial institutions that the BSP is mandated to

supervise under special laws. It should be noted, however, that the BSP shares

oversight responsibility over the Philippine financial systems with other domestic

financial regulators such as the Securities and Exchange Commission (SEC) for

the non-bank sector and capital market, the Insurance Commission (IC) for the

insurance industry, and the Cooperative Development Authority (CDA) for the________________

3. Specifically, the overnight RRP rate.

262

cooperative industry. However, since the Philippine financial system is largely

bank-based rather than market-based, the onus for the promotion of financial

system stability rests largely with the BSP.

The BSP defines financial stability as pertaining to the financial system’s

efficiency to redistribute and manage risks and carry out payments settlement,

while remaining responsive to the demands and challenges faced by the economy.

This has been pursued through the issuance of prudential rules and adoption of

applicable internationally accepted standards and best practices cognizant of the

domestic conditions. The BSP also appropriately monitors and assesses the

operational soundness of all banks and other financial institutions under its

supervision.

Since the 1997 Asian financial crisis, the BSP has initiatives to expedite the

clearing out of non-performing assets and strengthening of bank balance sheets.

Furthermore, the BSP pursued broad-based reforms geared toward maintaining

a strong banking system, including: (a) aligning domestic prudential standards

with international benchmarks and best practices, such as Basel Committee

recommendations on supervisory practices and capital adequacy, International

Accounting Standards (IAS) and International Financial Standards (IFRS) for

the proper accounting and disclosure of financial transactions, and the Organisation

for Economic Cooperation and Development (OECD) principles on good corporate

governance; (b) implementing a consolidated and risk-based approach to

examination, a shift from the traditional checklist approach; and (c) complementing

the on-site examinations of banks with off-site surveillance functions4 through

the introduction of new supervisory reports (Financial Reporting Package and

Capital Adequacy Ratio Report) and the review of other reports periodically

submitted to the BSP. Hence, the BSP has issued rules and guidance aimed at

improving risk management and corporate governance of banks and strengthened

its own capacity to monitor and intervene.5 The BSP issued new capital adequacy

guidelines in line with BASEL II and plans to adopt BASEL III in 2014.

The BSP has also put in place macro-prudential measures that can help

guard against a credit boom and excessive leveraging. These include, among

others:

• A ceiling on the ratio of UKbs’ and Kbs’ loans to the real estate sector set

at 20% of the total loan portfolio;

________________

4. Central Point of Contact

5. IMF Report on the Philippine Financial Sector Assessment Programme, April 2010

263

• A loan-to-value (LTV) ratio ceiling for real estate loans at 70% of the

appraised value of the real estate collateral for commercial banks;

• A minimum leverage ratio of 5% as a trigger for Prompt Corrective Action

(PCA) if not complied; and

• A 100% asset cover for their foreign exchange liabilities and 30% liquidity

cover to limit the build-up in system-wide financial risk.

Supervisory coordination has also been strengthened by the creation in July

2004 of the Financial Sector Forum (FSF), composed of the BSP, the SEC, the

IC and the Philippine Deposit Insurance Corporation (PDIC). This resulted in

the improved exchange of information among the different regulatory agencies

and coordinated the supervision and regulation of the financial system, particularly

with the establishment of formal information-sharing agreements with five foreign

supervisors.

However, unlike price stability, financial stability is not easy to define or

measure given the interdependence and the complex interactions of different

elements of the financial system among themselves and with the real economy.

Cognizant of this, the BSP uses various surveillance and analytical tools to

measure the safety and soundness of banks and other institutions under the BSP

supervision.

• To assess bank’s individual performance and supplement its risk-based

approach to examination, the BSP has adopted the use of the following: the

Capital Adequacy, Asset Quality, Management, Earnings, Liquidity and

Sensitivity to Market Risks (CAMELS) ratings system; the Risk Assessment

System (RAS); the Risk Management, Operational Control, Compliance and

Asset Quality (ROCA) rating system; the Strength of Support Assessment

(SOSA) rating system; and, the Trust Rating System (TRS).

• To address both systemic and idiosyncratic risks confronting the financial

system, the BSP has developed early warning systems (EWS) for the

macroeconomy, which focuses on currency crisis contagion effects, and an

EWS for bank solvency.

• The BSP also performs periodic stress tests on the absorptive capacity of

bank capital using a modified IMF stress tester 2.0.

264

Also in relation to its financial stability role, the BSP began to draft a financial

stability report (FSR) in 2006. Initially, the exercise rested solely with the

Department of Economic Research (DER). However, over time, as interest in

financial stability continued to gain ground, the exercise has been formalised

with the establishment of the BSP Financial Stability Committee (FSC) in

September 2010. The high-level FSC is tasked to take stock of potential system-

wide risks in the Philippine financial system. Technical work is underway on the

measures and metrics needed to monitor and mitigate system-wide risks. It has

also been placed in charge of the FSR which, to date, remains distributed only

internally.

2.3 Efficient PSS

Systemically important payment systems can transmit economic shocks

across markets and international borders. Hence, poorly designed or operated

payment systems can create economic disturbances, while well-managed systems

help minimise these disturbances.

The BSP, fully cognizant of its role in establishing facilities for payment

services as mandated under Section 102 of R.A. No. 7653 and the importance

of a safe and efficient payment system to financial stability, also takes the lead

in maintaining a safe, sound and efficient payments and settlements system for

the country. As the country’s central monetary authority that has the exclusive

authority to issue the currency, the BSP performs a pivotal role in the payments

and settlements system in the Philippines by: (a) providing/operating the payment

facility for final settlement to financial institutions – i.e. through the real time

gross settlement system known as the PhilPaSS; (b) issuing policy related to

payments and settlements; (c) providing credit facilities for banks as a lender

of last resort; (d) overseeing the payments and settlements system; and (e)

initiating studies/systems reform for the improvement and maturity of payment

systems in accordance with the global standards. Moreover, the BSP constantly

strives to ensure that the payment infrastructure meets the highest standards for

safety soundness and operational resilience.

The BSP’s Payments and Settlements Office (PSO), under the direct

supervision of the Deputy Governor of the BSP’s Resource Management Sector,

performs the operator function as it is responsible for the operation and

maintenance of the PhilPaSS and its critical components. The BSP’s Payments

and Settlements Steering Committee (PSSC) recommends policy directions and

formulates strategy, standards, rules and regulations. Meanwhile, the Core

Information Technology Supervision Group (CITSG) of the BSP’s Supervision

265

and Examination Sector has oversight on all payments and settlements system

of banks and industry consortia.

As operator of the payment systems, the PSO ensures that the payment

systems remain safe and efficient and exerts all efforts so that time-critical

payments are completed as expected in order to facilitate and enhance economic

processes, manage risks, and absorb shocks in order to promote financial stability.

The BSP also provides for, maintains and upgrades the system hardware and

software to ensure uninterrupted operations, that adequate Continuity of Business

(COB) plans are in place, and that adequate back-up files are available for the

continuous and efficient operation of the system.

To ensure that the PhilPaSS efficiently processes large-value transactions,

facilitates the flow of payments among banks, and reduces losses that could

arise associated with the payments and settlements process, the following

refinements were put in place:

• Implemented the delivery-versus-payment (DvP) system for transactions

on secondary trading of government securities in 2004 and the Enhanced

Delivery-versus-Payment (e-DvP) system through the Philippine Dealing

System (PDS) Settlement Highway in 2008;

• Enhanced the Intraday Liquidity Facility (ILF) system;

• Interconnected the PDS Settlement Highway and the BSP PhilPaSS;

• Exerted continuous effort to automate other transactions affecting the demand

deposit accounts;

• Connected BancNet and MegaLink to the PhilPaSS; and

• Rationalised transaction fees charged to participants to make the fees more

reasonable and equitable from P100 per transaction to an amount ranging

between P5.00 to P400.00 depending on the value of transaction. However,

transactions valued at P100.00 and below are free of charge.

Since payment systems affect the daily demand for liquidity of banks/financial

institutions and may therefore affect the level of money market interest rates,

the BSP, as a lender of last resort, provides liquidity tools to the PhilPaSS

participants. Aside from the overnight repos that banks may avail with the BSP

in case of liquidity problems, the BSP also established liquidity facilities intended

266

for banks experiencing unexpected temporary liquidity shortages so as to ensure

continuous settlement of banks financial transaction, prevent chain defaults and

achieve financial stability. The liquidity support facilities provided by the BSP

include:

• ILF – a fully collateralised facility established to maintain the smooth and

efficient operation of the payments system in order to avoid interbank

payments gridlock in the settlement process.

• Overdraft Credit Line (OCL) – a short term credit facility intended to assist

bank experiencing unexpected or higher than usual volume of inward cheque

transactions. The governing policies and procedures are provided under BSP

Circular 681 in order to provide additional liquidity for banks encountering

liquidity problems due to cheque clearing losses as well as protect the BSP

against settlement exposures.

As overseer of the payment systems, the BSP also relies on policies, circulars,

rules and regulations, as well as moral suasion to conduct review and evaluation

of systematically important payment systems operating outside of the BSP.

Pending the enactment of the Payments Act, the oversight of payment system

outside of the BSP is currently confined only to the following:

• The PDS Group due to its quasi-banking licence to provide electronic

depository, registry and custody services and the linkage of the PDS

Settlement Highway to the PhilPaSS;

• BancNet, Inc. and MegaLink Inc., since both are affiliates of banks and

outsourse service providers for ATM switch networks;

• Smart Money by Smart Telco, since this is an outsourcing service provided

by Smart to its partner banks (i.e. BDO, Chinabank and Landbank), it allows

the BSP to have access to the operations of Smart Money; and

• Globe G-Cash operation under Circular 649 dated 9 March 2009.

Lastly, through the role it plays in the PSS, the BSP promotes financial

stability by exerting all efforts to ensure that time-critical payments are completed

as expected especially of financial/interbank market transactions in order to

facilitate and enhance economic processes, manage risks, and absorb shocks.

Likewise, the payments system plays a critical role in the implementation of the

BSP’s monetary policy through the settlement of domestic money market

267

transactions, e.g. siphoning off excess liquidity in the system and ensuring that

monetary policy changes get transmitted to the markets faster. The BSP, through

the payments system, is also able to monitor the behaviour of the interbank

money market and is able to effectively forecast liquidity conditions in the

economy. Given a reliable and efficient payment system with real time or same-

day settlement, the BSP is able to enhance the effectiveness of monetary policy

tools used.

3. Philippine Payment and Settlement Infrastructure

A payment system is defined as an arrangement that allows users to transfer

“money”. In simple terms, “money” is regarded as cash (i.e., notes and coins

issued by the government or central bank) and claims against credit institutions

in the form of deposits. The use of bank deposits to make payments has become

an important medium in most developed countries and to make a payment, the

payer must issue an instruction in the form of a paper-based instrument (e.g.

a cheque) or an electronic instruction (e.g. using a credit or plastic card).

The effectiveness of payment activities is fully dependent on the arrangements

that facilitate fund transfers between members and it is these arrangements that

constitute a “payment system”. Payment systems consist therefore of networks

that link the members with existing rules and procedures for the of use of this

infrastructure. A payment system normally requires the following:

• Standard methods of transmitting payment messages between members;

• Agreed means of settling claims within the members/participants (normally

through the deposits of the members/participants with the central bank);

and

• Common operating procedures and rules (admission, fees, operating hours).

3.1 PSS Participants

3.1.1 Bangko Sentral ng Pilipinas

The BSP’s role in the PSS is already discussed above.

268

3.1.2 Banks, Non-banks with Quasi Banking Function, and Other

Financial Institutions

In the Philippines, the majority of payment service providers are banks.

Though there are few non-bank payment service providers, they are not

independent from the banks. Under the BSP charter, all banks and non-banks

with quasi banking function (NBQBs), including their subsidiaries and affiliates

engaged in related activities are supervised and regulated by the BSP.

As of end-June 2012, there were 37 universal and commercial banks, with

4,928 branches. Among such commercial banks, 18 were privately domestic

banks, 3 were government-owned banks, and 16 were foreign banks and their

subsidiaries. Almost all commercial banks issue their own Automated Teller

Machines (ATM) cards.

There are four types of thrift banks operating in the Philippines. These are

the Savings and Mortgage Banks (SMBs), Private Development Banks (PDBs)

and Stock Savings and Loan Associations (SSLAs) and microfinance-thrift banks.

As of end-June 2012, there were 69 thrift banks, with 1,453 branch offices.

For rural banks, as of end-June 2012, there are 606 rural and cooperative

banks with 2,114 branches.

The existing specialised government banks are the Development Bank of

the Philippines (DBP), the Land Bank of the Philippines (LBP), and Al-Amanah

Islamic Investment Bank of the Philippines (AAIIB).

In addition to the foregoing banking institutions, as of end-June 2012, there

were 15 non-banks financial intermediaries performing quasi-banking functions

with 62 branches. Those non-banks without quasi-banking functions consist of

71 non-stock savings and loan associations with 124 branches, 6,463 pawnshops

with 10,665 branches – all under the regulation/supervision of the BSP.

3.1.3 Other Bodies (PCHC, ATM Consortiums, PDS, Credit Card

Companies, Other Self-Regulating Organisations (SROs) and

Government Agencies)

3.1.3.1 Philippine Clearing House Corporation (PCHC)

The PCHC, incorporated in July 1977, is a private corporation co-owned by

all commercial banks enlisted as members of the Bankers Association of the

269

Philippines (BAP). With the Clearing House Rules and Regulations approved

and subsequently the arbitration mechanisms in place, the PCHC commenced

its live operations on 06 June 1980 and stood proud being the first automated

Magnetic Ink Character Recognition (MICR) Cheque Clearing House in

Southeast Asia. Its main purpose was to automate the cheque clearing system

through the medium of MICR-encoded cheques.

The PCHC provides cheque clearing services covering sixty nine (69)

geographical regions – thirty (35) Greater Manila/Integrated Regions and thirty

nine (34) Regional “local” exchange centres, processing a daily average of about

700,000 clearing items from more than 6,000 participating bank branches

nationwide. The clearing period for Inter-Regional cheques is 4 days while Greater

Manila cheques is 3 days.

3.1.3.2 ATM Consortiums

There are 5 Automated Teller Machine (ATM) switch operators in the

Philippines, namely: BancNet, ENCASH, ExpressNet, MegaLink and

NATIONLINK. BancNet, ExpressNet and MegaLink are considered major

players in the payment systems because of their customer reach. BancNet,

ExpressNet and MegaLink are co-owned by the big commercial banks. Their

services go beyond the traditional transactions that coursed through the ATM.

Meanwhile, ENCASH and NATIONLINK are more geared towards reaching

out to people in the rural areas who are not normally reached by the major ATM

consortiums.

a) BancNet connects the ATM Consortium networks of more than 49 local

banks. As a multi-channel payment gateway, BancNet enables its customers

to transact at any ATM terminals anywhere, anytime, at point-of-sale (POS),

the Internet or through mobile phones. BancNet is also the exclusive gateway

of China UnionPay. BancNet has also forged an alliance with the global

payment brand JCB International. BancNet serves 8 million members with

over 4,000 ATMs and more than 10,000 POS terminals.

b) ExpressNet connects the ATM networks of seven major banks in the

Philippines. At present, ExpressNet has 3.5 million customers and has 2,213

ATMs operating nationwide.

270

c) MegaLink connects the ATM networks of 15 member banks in the

Philippines with a more than 2,921 ATMs nationwide and 32,4396 POS

terminals.

To this date, this three major ATM networks are already interconnected

with each other to enhance the services they provide to their clients.

d) Electronic Network Cash Tellers, Inc. (ENCASH) is an independent

switch network that also provides ATM service to the Philippine countryside

and a close competitor of ENCASH. As the first Independent ATM deployer,

ENCASH provides privately-owned ATMs to areas not deemed viable by

commercial banks, allowing users in remote locations to conveniently access

to their finances. Initially connecting the ATMs of five (5) rural banks in

the Philippines, the ENCASH network eventually expanded to more than

101 member- rural banks and cooperatives with 220 ATMs deployed, and

operations implemented Luzon, Visayas and Mindanao. ENCASH is a

member of MegaLink which is interconnected with the other Philippine

interbank networks, i.e., BancNet and ExpressNet. It is also the first network

in the Philippines to fully adopt EMV technology on all its ATM cards,

although the regular magnetic stripe cards remain an option for the network.

ENCASH provides both rural and commercial bank ATM cardholders with

the convenience of having access to ATMs in more locations all over the

country.

e) NATIONLINK’s members consist mostly of savings banks, credit unions,

rural banks, cooperatives and non-governmental organisations, and is largely

concentrated in rural areas, where the reach of ATMs are more limited

than in the cities. The network focuses heavily on the overseas Filipino

worker (OFW) market.

The use of ATM networks enable their customers to transact at any ATM

terminal anywhere, anytime, at point of sale, the internet or through mobile

phones the following transactions: cash withdrawal, cash advance, account

balance inquiry, bills payments, funds transfer, load fulfillment and purchases.

3.1.3.3 Philippine Dealing System

The Philippine Dealing System Holdings Corp (“PDS Group”) is a private

corporation tasked to reshape the architecture of the Philippine financial markets

________________

6. Source: MegaLink, figures as of end-December 2011.

271

to meet the needs of public investors while abiding with best international

standards. The PDS Group has three operating subsidiaries: Philippine Dealing

& Exchange Corp. (PDEx) - an entity that operates electronic trading platforms

for securities; Philippine Depository & Trust Corp. (PDTC) - one that provides

securities depository, registry and custody services, and Philippine Securities

Settlement Corp. (PSSC) - the company that provides electronic settlement

facilities with straight through process and delivery vs. payment capabilities.

The PDS Group manages or operates electronic trading and settlement platforms

in the Philippine’s Debt Securities and Foreign Exchange markets, and performs

key post-settlement functions for the Debt and Equity markets through its

electronic Depository, Registry and Custody services. The large value of financial

transactions coursing through the Group’s collective platforms make these

important to the Philippine financial system. The Group’s shareholders are all

institutions that are established leaders across the sectors of finance,

manufacturing and technology. The Group actively interacts with financial market

regulators and participants in its effort to build the venue where investors may

have a wider array of financial instruments and issuers have an efficient medium

to raise capital for their company’s requirements.

3.1.3.4 Bureau of Treasury

With the transfer of the fiscal agency functions from the BSP to the

Department of Finance (DoF), the Bureau of Treasury (BTr) has taken the

function of booking government securities through the Registry of Scripless

Securities (RoSS) effective November 4, 1996. RoSS is the official registry of

government securities maintained and administered by the BTr.

3.1.3.5 Philippine Postal Corporation

Under the Republic Act No. 7354, the Philippine Postal Corporation (PPC)

is authorised to issue domestic and international money orders. Any mailing

patron can buy money order cheques from their local post office; this may be

drawn payable to another person or to the person making such application, if

he desires so. Money order cheques are then transmitted to the beneficiary

either through registered letter or speedy airmail. Upon receipt, domestic money

orders may be presented for payment at the designated paying office, issuing

office or commercial bank within 90 days from date of issue. For services

provided, fees are collected by the issuing post office based on the aggregate

or total amount applied for.

272

3.1.3.6 Securities and Exchange Commission

The SEC, established on 26 Oct 1936 by virtue of the Commonwealth Act

No. 83 or the Securities Act, was prompted by the need to safeguard public

interest in view of the local stock market boom at that time. Its major functions

included registration of securities, analysis of every registered security, evaluation

of the financial condition and operations of applicants for security issuance,

screening of applications for broker’s or dealer’s licence and supervision of

stock and bond brokers as well as the stock exchanges.

3.1.3.7 Privately-owned Payment Service Providers

Since all large-value payments are finally settled in the DDAs of banks in

the BSP and this type of payment is normally used by banks, there is no existing

large-value payment system (LVPS) other than the PhilPaSS. Retail payment

systems (RPS), on the other hand, are owned by private payment service

providers, which are incidentally owned by the banks themselves through a

separate corporation. Though the majority of the RPS in the Philippines are co-

owned by the banks, there are few systems which are owned by non-banking

institutions. These retail payment services are registered and supervised under

the jurisdiction of the SEC.

3.2 Payment Instruments

Payment instruments in the Philippines may be classified into cash or non-

cash. Non-cash payment instruments may be sub-classified generically into cheque

payments, direct fund transfers and card payments.

3.2.1 Cash

By law, the BSP has the sole right and authority to issue currency in the

Philippines. At present, currency notes are issued in denominations of 1000,

500, 100, 50 and 20 pesos; and, coins in 25, 10, 5 and 1 cent(s). Although in

recent years there has been an increasing tendency to use alternative payment

methods, a large portion of payments to individuals is still made in the form of

cash, especially in the areas of retail trade, land transportation and personal

services. This explains the wide increase of cash in circulation from P194.7

billion in 2001 to P484.0 billion as of end-2011 or 148.6% in 10 years.

273

3.2.2 Non-cash

There are six main non-cash payment instruments/media that are currently

used in the Philippines, as follows:

3.2.2.1 Cheques

Cheques are commonly used by consumers for bills and small value payments.

For businesses, cheques are utilised as payment for purchases of goods and

services. In the Philippines, banks exchange cheques through Electronic Cheque

Clearing System (ECCS) operated by the PCHC for processing and consolidation.

The cheque clearing results are then electronically transmitted to the BSP for

the corresponding settlement in the banks’ respective DDAs.

The volume of cheques cleared in the PCHC increased by 2.15% from

169.952 million in 2005 to 178.60 million in 2011. The increase in volume indicates

that cheque is still the preferred mode of payment indicative of consumers’

confidence and trust in such payment medium in spite of the availability of

electronic payment instruments.

3.2.2.2 Direct Debit and Credit Transfers

The direct debit and credit transfers are used mainly for the settlement of

large value payments for small volume transactions such as Interbank Call Loan

(IBCL) lending/borrowing, P/USD trades/purchases as well as Government

Securities trades and purchases. These direct debit and credit transactions

covering large value payments settle through the country’s real time gross

settlement system called the PhilPaSS.

3.2.2.3 Credit and Debit Cards

There are at least 12 major credit cards issued in the Philippines. All credit

cards in the Philippines have affiliations with major international credit cards,

such as Visa, MasterCard, Diners and JCB. Some domestic and international

cards have access to the banks’ ATM network in the Philippines. Several stores/

retailers issue cards for use in their own chains.

Credit cards in the Philippines are usually issued by the banks which have

formed part of their marketing strategy to increase the number of their customer

base and improve income that can be generated from retail consumer business.

Credit card use is no longer limited to the ordinary purchase of goods and services

274

by the cardholders. Banks have expanded its usage for other purposes such

as cash advance, easy installment plan for purchases, link-up to savings and

chequeing accounts of cardholders, etc., to attract more customers. On the other

hand, most commercial banks and some thrift banks issue debit cards. Debit

cards enable the holder to have his purchases directly charged to funds on his

account at a deposit-taking institution (may sometimes be combined with another

function, e.g. that of a cash card or cheque guarantee card).

3.2.2.4 ATM Cards

The ATM card is a commonly used card issued normally by banks and can

be used for account inquiry/information, deposits, withdrawals, bills payment,

and interbank funds transfer coursed through the network switches, i.e., BancNet,

MegaLink, ExpressNet, NATIONLINK and ENCASH. Some of these switches

have developed their own POS systems to allow their cardholders to pay for

their purchases electronically through their accounts for credit to the retailer’s

account.

3.2.2.5 E-money or Stored Value Cards

E-money is a kind of value stored electronically in a device such as a chip

card or a hard drive in a personal computer. The BSP classifies e-money further

as monetary value stored electronically in an instrument or device, which can

be withdrawn in cash and, if issued by a bank, shall not be considered as deposit.

The most popular forms of e-money in the Philippines are SMART Money and

Globe’s G-Cash.

Stored Value Cards are prepaid cards in which the record of funds can be

increased as well as decreased. It is also called an electronic purse. In the

Philippines, these cards are commonly single use instruments and non-reusable.

Typical examples of single use cards are those issued by the Light Rail Transit

Authority (LRTA), Metro Rail Transit Authority (MRTA) and major

telecommunications companies. A bank also pioneered the use of multi-purpose

reloadable e-Cash that can be used for cash withdrawals through the bank’s

counter or automated teller machines or payment of bills to the accredited

establishment of the e-Cash issuer.

275

3.2.2.6 Electronic Banking

Banking institutions in the Philippines provide electronic banking services

which includes telephone banking, desktop banking and mobile banking. Desktop

banking and telephone banking are common electronic distribution channels.

Most banking institutions also offer services through their internet banking

facilities such as account balance summary, request for account statements,

funds transfer between own accounts or third-party accounts, bills payments,

cheque book request services and even mobile banking registration.

Likewise, most users of the electronic bill payment system that facilitates

customers to pay their various utility bills (e.g. electricity, telephone and water

bills, etc.) electronically are coursed through the various ATM network facilities

of banks. However, credit card and direct debit are still the preferred method

of payment.

3.3 Philippine Payment System Landscape

The Philippine PSS began when banks and other financial institutions used

the Enhanced Multi-transaction Interbank Payment System (MIPS2) for their

interbank transaction. The MIPS2 was an electronic net clearing system operated

by the BAP and the PCHC, in coordination with the BPS. Both counterparties

in an interbank transaction under the MIPS2 had to input their transactions

through the PCHC, which, in turn, verified and authenticated the transactions

prior to electronic transmission to the BSP for settlement. The details of the

transactions of banks/financial institutions were obtained by the participants

through the reports from the MIPS2, while the balances of their demand deposits

were being advised through an hourly electronic broadcast by the BSP

Comptrollership Department.

However, the MIPS2 had some problems that hampered the speed of

transactions between banks. First, the participant banks needed to wait for the

fixed hourly broadcast from the BSP through cc:mail system in order to know

the details of the transactions debited from and credited to their accounts and

the available balances of their DDA. Second, the MIPS2 had limited operating

hours between 10:00 a.m. and 4:00 p.m. daily.

Recognising the need for a system that would enable online, real-time

settlement of interbank transactions and eliminate risk in the settlement process,

the BSP, in collaboration with the BAP, the Chamber of Thrift Banks (CTB),

276

the Rural Bankers Association of the Philippines (RBAP) and the Investment

House Association of the Philippines (IHAP), formally launched on 12 December

2002 an RTGS known as the PhilPaSS.

Today, the landscape of Philippine Payment and Settlement System is

composed of the following major systems:

3.3.1 Philippine Payments and Settlements System (PhilPaSS)

The PhilPaSS is a real time gross settlement system, owned and operated

by the BSP that caters to the settlement of large value transactions of banks

through their DDA maintained with the BSP. The system was implemented in

2002. In the PhilPaSS, all transactions are processed and settled on a real time

basis through its Central Accounting System (CAS) which prompts the accounting

and recording of the settlement instructions received from SWIFT (for Swift

member banks) and Philippine Payment System – Front-End System (PPS-FES)

(for non-swift), into the participants’ DDA with the BSP. The CAS debits the

account of the paying bank and credits the account of the receiving bank.

Commercial banks use the SWIFT-based network and message formats to

transmit their financial transactions to the PhilPaSS for processing and settlement.

The thrift/savings banks, financial institutions or NBQBs and rural banks use

the PPS-FES which was developed by the BSP’s Information Technology,

Infrastructure and Operations Department (ITIOD) to enable them to transmit

their financial transactions to their counterparties through the PhilPaSS-CAS.

In February 2012, the BSP implemented the use of Participant Browser

(PB) for the PhilPaSS participants. The PB is a web-based facility that aims

to improve the banks’ mode of accessing the PhilPaSS. It is a state of the art

browser that will enable the PhilPaSS participating banks to efficiently manage

their respective DDA maintained with the BSP. The authorised users of the

system will be capable of checking and verifying the status and details of incoming

and outgoing interbank transactions. Users can also re-prioritise or cancel queued

payments as well as generate reports reflecting the DDA transaction that has

settled during the day based on the file formats available in the system. More

importantly, the PB will eliminate the connectivity problems normally encountered

when using dial-up access to establish the link with the BSP-PhilPaSS.

The PhilPaSS maintains an interface or also act as settlement system

for other major payment systems operating in the country (as shown in diagram

below).

277

3.3.1.1 Electronic Peso Clearing System (EPCS) and ECCS owned

and operated by the PCHC

The ECCS pertains to the online transmission of cheque data to the PCHC

for a faster exchange of value and the delivery of the corresponding physical

items later. Banks use the ECCS front-end application to transmit their outward

clearing demands and retrieve their inward data clearing files to debit the account

of their individual clients. The cheque items/data are processed and cleared

through the PCHC ECCS, the net clearing results of which are then electronically

transmitted in the afternoon of the same day by PCHC to the PhilPaSS for

settlement.

The EPCS, on the other hand, is an interbank account-to-account fund

transfer system that supports bulk, recurring and non-time sensitive payment

and collection transactions. Under this system, the PCHC receives payment

instructions from various participating banks. These are instructions coming from

bank’s client to pay his obligations by transferring the amount owed from his

account to the account of the creditor maintained in another bank, which are

then forwarded to the PCHC. The electronic transmissions of electronic peso

Figure 1

The Philippine Payments and Settlements System (PhilPass)

278

transfers between banks occur between 9:00AM and 4:00PM. Being an online

processing system, the participating banks/branches are permitted to gain access

to the EPCS Host Computer located at the PCHC via data communication lines.

The system enables payees to use funds on the next business day while

withdrawals of transferred funds from the payees’ accounts in the Peso Netting

require at least 48 hours following the remittance date. The fund transfer

instructions are processed and cleared through the PCHC EPCS, the net clearing

results of which are also electronically transmitted in the afternoon of the same

day by the PCHC to the PhilPaSS for settlement.

Unlike the ECCS, the payment instruction documents by the banks from

their clients are retained by the banks, and no physical document is forwarded

to the PCHC.

Any bank which incurs an overdraft in its deposit account with the BSP

shall fully cover it, including interest at a rate equivalent to one-tenth of one

percent. (1‰) per day or the prevailing 91-day T-bill rate plus three percentage

points, whichever is higher, not later than the next clearing day. The corresponding

clearing office (PCHC and the BSP Regional Clearing Office) shall officially

notify the banks with overdrawn balances.

Settlement of the clearing balances with the BSP shall not be effected for

any account which continues to be overdrawn for five consecutive banking days

until such time that the overdrawn amount is fully covered or otherwise converted

into an emergency loan or advances pursuant to the provisions of Section 84 of

R.A. No. 7653. Banks may also borrow from other banks through the interbank

facility or from the BSP through the overnight or term regular repurchase facilities

at existing rates to cover overdrafts.

3.3.1.2 Philippine Domestic Dollar Transfer System (PDDTS)

The PDDTS is a local clearing and electronic communication system operated

by the BAP, PCHC, PSSC and Citibank Manila (as the USD settlement bank).

It is a facility used by the banking industry to move US dollar funds from one

Philippine bank to another on the same day without having to go through a

correspondent bank in the US. The PDDTS allows on-line, real-time gross

settlement of domestic interbank US dollar transfer and third-party account to

account US dollar transfers.

The PDDTS participating bank maintains a US dollar interest bearing account

with the settlement/depository bank (PDDTS account) used solely for effecting

279

credits and debits and other transaction arising from the PDDTS transactions

as well as payment(s) of transactions and other charges attendant to the PDDTS

transactions. The end-of-day net positions of banks arising from OFW remittances

which are coursed through the PCHC, are also settled through the PDDTS.

If the sending bank’s PDDTS account balance is insufficient to cover the

transfer, the transfer instruction will be placed on queue. Participants who may

be temporarily short of funds during the day may then request Citibank for

daylight overdraft facility for the queued transactions.

The PDDTS also made possible the implementation of Payment vs. Payment

(PvP) facility in 2003 for interbank USD-Peso transactions with the dollar leg

settling in the PDDTS and the peso leg settling through the BSP-PhilPaSS.

In PvP transactions, the USD leg is checked first and where sufficient, the

USD amount is earmarked. A peso payment instruction is then sent to the

PhilPaSS system, which is queued together with all other payment instructions

of the same bank. Upon successful posting of the peso payment debiting the

USD buyer’s PhilPaSS account and crediting the USD seller’s PhilPaSS, the

PhilPaSS sends a confirmation message to the PSSC PDDTS System, which

triggers the actual transfer of the earmarked USD amount in the USD seller’s

PDDTS account to the PDDTS account of the USD buyer.

In the Philippines, the peso-dollar trading among banks and between these

banks and the BSP are done through the PDS electronic platform called the

Philippine Dealing and Exchange Corporation (PDEx).

3.3.1.3 PhilPaSS REMIT System

The PhilPass REMIT is a system developed by the ITSS group of the

BSP that will allow the use of the PhilPaSS as a settlement arm for overseas

Filipino (OF) remittances in order to ensure safe and immediate transfer and

settlement of remittance funds into beneficiary accounts maintained in another

bank. Implemented in May 2010, the system interfaces with the PhilPaSS to

cover the electronic settlement of OF remittances that are received by the 11

private commercial banks, three government-owned banks, and one thrift bank

from overseas branches or correspondent banks and partner remittances agencies

abroad but for further credit to beneficiary accounts maintained with other banks

in the Philippines. Once an OF remits funds through the overseas bank branch

or remittance partners abroad, and sent via wire transfer to the participating

remitting bank in the Philippines, the remitting banks using an interface PhilPaSS

280

Remit system will prepare and transmit the batched files indicating the details

of beneficiary accounts to be credited. Upon settlement in the PhilPaSS, the

beneficiary bank will further credit the remittance to the account of the ultimate

beneficiary. The system has a feedback mechanism feature that requires the

beneficiary banks to inform the BSP and remitting bank that it has credited the

OFW’s beneficiary account within the same day (Day 1) or at the latest on Day

2 , if further validation of beneficiary accounts is needed.

3.3.1.4 BancNet and MegaLink ATM Network Systems

BancNet is the biggest interbank network connecting the ATM Consortium

networks of more than 49 local banks compared to MegaLink with just 15

member banks.

The use of ATM networks enable their customers to transact at any ATM

terminal anywhere, anytime, at point of sale, the internet or through mobile phones.

BancNet and MegaLink send electronic payment instructions/settlement report

via leased line to the PhilPaSS for the settlement of network funds against the

DDA maintained by member banks with the BSP.

3.3.1.5 Registry of Scriptless Securities (RoSS)

The RoSS is a central securities (Treasury Bills and Bonds) depository

maintained and administered by the BTr. All government securities (GS) floated/

originated by the National Government under its scripless policy is recorded in

the registry in the name of the Government securities eligible dealer (GSED) by

virtue of the auction award made by an auction committee. Subsequent transfer

of ownership on the scripless securities out of the securities account of a GSED

is recorded in the RoSS through the securities account of the counterparty GSED.

As of end-December 2011, there are 11,228 registered accounts. (Banks – 12;

Non-bank financial institutions – 11; and Others – 11,205).

In the primary market, the BTr through the bridge systems announces, two

days in advance, the details of the scheduled GS for auction. The GSED submits

their bids using the Reuters Interface, which are electronically linked to the

BTr’s Automated Debt Auction Processing System (ADAPS). Upon award of

GS to a winning GSED bidder, the securities award are electronically downloaded

to the RoSS system and cash settlement reports are generated and forwarded

to the PhilPaSS for debiting the DDA of the winning GSEDs and crediting the

DDA of the BTr.

281

In the secondary market, the GSEDs/non-GSEDs input settlement instructions

for closed deals via the PDEx of the PDS which is electronically linked to the

RoSS System. The RoSS system checks the securities in the seller’s account

and earmarks these for transfer. The system then sends an electronic settlement

file to the PhilPaSS to debit the DDA of the buyer and credit the account of

the seller. Securities and cash settlement of GS transaction to the secondary

market is done via delivery versus payment on a real time gross trade for trade

basis.

3.3.1.6 Philippine Depository and Trust Corporation System (PDTC)

The PDTC a subsidiary of PDS, that provides depository and settlement

services for listed fixed income securities traded and cleared in the PDEx (another

subsidiary of PDS). This includes government securities and corporate debt

issues. The PDTC operates a depository and electronic book-entry transfer

system for the centralised handling of all kinds of securities which supports the

settlement of securities by book entries in the records of the PDTC without

physical delivery of stock certificates. As a depository for the equities market,

the PCTC centralises the management of shareholders information through

dematerialisation. Dematerialisation eliminates the need to deliver paper

certificates for securities traded; hence it eliminates the risk associated with

maintaining physical certificates and speeds up the processing and settlement of

trade transaction.

Fixed income trades at the PDEx settle on T+1 under PDEx DvP model

1 system (i.e., gross simultaneous settlement of securities and funds transfer)

method in which the cash settlement side is linked to the PhilPaSS.

3.3.1.7 In the Pipeline

Soon to settle in the PhilPaSS are equities traded at the Philippine Stock

Exchange (PSE), the clearing of which is handled by the Securities Clearing

Corporation of the Philippines (SCCP). Trades at the PSE settle on T+3 under

SCCP-DvP model 3 system (simultaneous net settlement of securities and fund

transfer) net settlement method for broker-to-broker transactions. Meanwhile,

settlement of trades in the PSE-listed stocks between broker and investor is

typically done via cheque for local clients and direct credit to bank accounts for

foreign clients.

282

3.3.1.8 Other BSP Internal Systems

The BSP has also integrated in the PhilPaSS various BSP internal systems

affecting the the DDA accounts of the banks, such as:

a) Electronic Fund Transfer Instruction System (EFTIS) - developed and

implemented in 1997 to automate the peso funds transfer instructions coming

from authorised agent banks (AABs) of the Bureau of Internal Revenue

(BIR) and the Bureau of Customs (BOC) to the BSP. The System ensures

that such peso funds transfer instructions are transmitted and settled promptly

and efficiently without delay or with minimal manual intervention. The

system’s implementation was a joint effort between the BAP and the BSP

utilising Lotus Notes as the messaging software.

AABs accept the public’s (individual/corporate) payments of internal revenue

taxes of the BIR and customs duties of the BOC and electronically transmit

the fund transfer instructions via EFTIS their remittances of revenue

collections to the PhilPaSS - for credit to the deposit account of the BTr-

National Government maintained with the BSP.

Banks also use EFTIS to transmit transfer instructions to comply with the

reserve requirements of other intra-bank accounts with BSP, namely:

Common Trust Fund (CTF), Trust, Other Fiduciary Accounts (TOFA) and

Small- and Medium-enterprise (SME) accounts.

As identified in the BSP’s COB Plan, the EFTIS also serves as the back-

up messaging system in case SWIFT or PPS-FES Client System becomes

inoperable.

b) Electronic Cash Withdrawal System (ECWS) - implemented in February

2006 in order to improve the processing and settlement of banks’ cash

withdrawals for their daily requirements for peso notes and coins in various

denominations.

The ECWS standardised the process of ordering various currency

denominations by the introduction of a Cash Order Slip (COS), where banks

specify their desired currency denominations subject to approval based on

the availability of currency stock held at the BSP Cash Department. The

amount approved in the processed COS is indicated in the SWIFT/PPS-

FES message instruction sent to the PhilPaSS for settlement, subject to

available balances in the deposit account of the withdrawing bank. Once

283

settled, a system-generated settlement electronic notification is transmitted

to the BSP-Cash Department to trigger the release of the proceeds of

withdrawals to awaiting bank representatives.

The use of the PhilPaSS as the settlement system of the ECWS eliminated

the use and presentation of cheques before cash withdrawals can be

completed. The ECWS also facilitated the reengineering of processes

involved on previously transacted over-the-counter (OTC) cash withdrawals

from the BSP. The system has made cash more convenient and efficient

for the banks.

The implementation of the ECWS also resulted in man-hour savings for the

banks in terms of time spent in cheque preparation, authorisation of signatures

and delivery to the BSP.

c) eRediscounting System – The Electronic Rediscounting System or

eRediscounting is an online internet-based rediscounting facility that the BSP

makes available to all active and qualified banks nationwide. This facility

allows banks to conduct their rediscounting transactions and inquiries with

the BSP in on-line, real time basis at the convenience of their own bank

premises. With its simplified and end-to-end processing capability, the system

provides immediate availability and fast delivery of credit to banks, especially

those in the countryside. More importantly, it will reduce the transaction

costs of banks, which will mutually benefit the participating banks and their

clients.

d) PhilPaSS Participants

As of end-August 2012, the following institutions participated in the

PhilPaSS:

• 34 commercial banks

• 3 specialised banks

• 40 savings and thrift banks

• 30 rural banks

• 14 Non-bank with Quasi Banking Function (NBQBs)

• 2 ATM Networks

• Bureau of the Treasury (BTr)

284

• BSP-Department of Loans and Credit (DLC)7

• BSP-Provident Fund Office (PFO)8

• BSP-Supervision Departments

• BSP-Treasury Department (TD)

• Philippine Clearing House Corporation

• Philippine Dealing Exchange

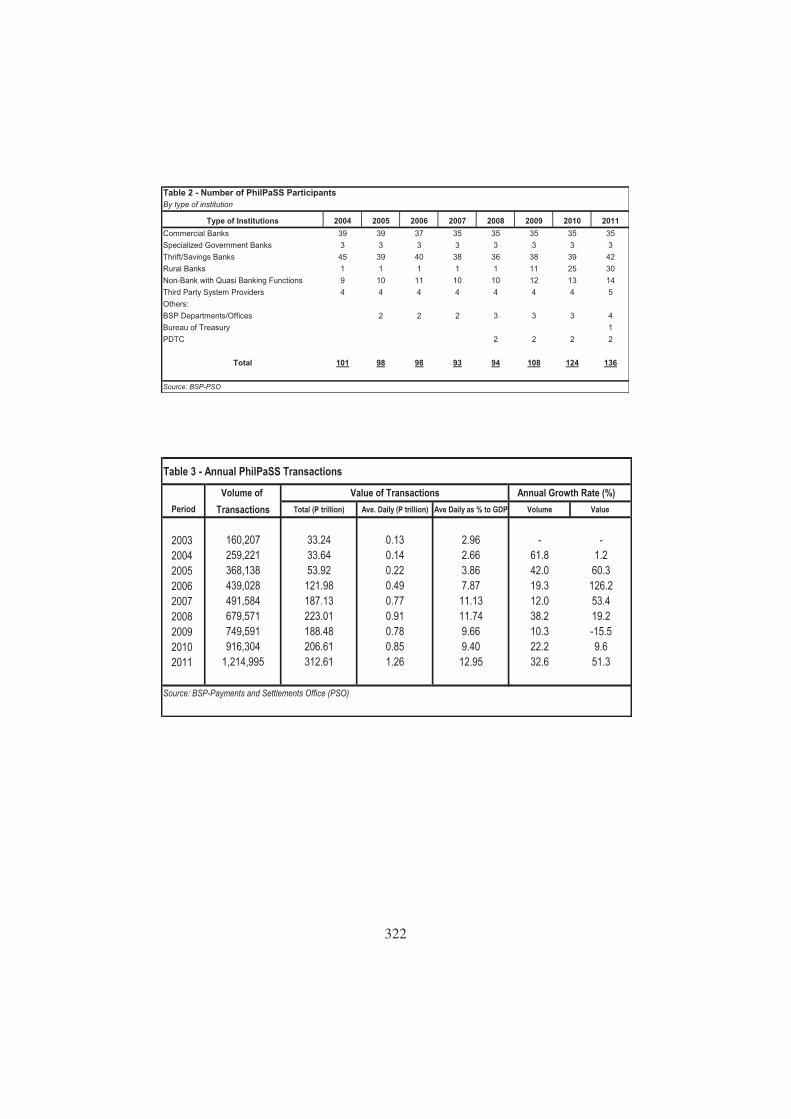

See Table 2 on the number of the PhilPaSS participants from 2004 to 2011.

3.3.1.9 Transactions Processed and Settled in PhilPaSS

To date, the following transactions (with value dates equal to the PhilPaSS

business day) are accepted for processing and settlement in the PhilPaSS:

• High-value interbank transfers

• Sale and Purchase of GS trades under outright and repurchase agreements

with the BSP in connection with the latter’s Open Market Operations

• Interbank Sale and Purchase of Primary and Secondary Market GS trades

via the DvP System

• Settlement of payments for the public (tertiary level) market trading of

government securities

• Settlement of the peso leg of foreign currency transactions via the PvP

System

• Interbank settlement of ATM transactions within the members of ATM

network provider and settlement of inter-network transactions of ATM

network providers

• Customer payment instructions

• Cash deposits/withdrawals of notes and coins – banks’ head offices

• Cash deposits/withdrawals of notes and coins – banks’ regional branches

• Results of cheque clearing

• Revenue Collections (Internal Revenue Taxes and Customs Taxes/Duties)

________________

7. DLC manages the e-rediscounting window and overdraft clearing lines of banks.

8. PFO manages the investment portfolio of BSP employees’ retirement fund.

285

• Treasury Department (domestic) trades/purchases and lending/borrowing

• E-rediscounting, emergency and special facility loans

• OF remittances

• Withdrawal of banks’ excess reserves

• Annual supervisory fees

There are no limits on the value or type of transactions that can be processed

in the PhilPaSS provided both counterparties are maintaining DDAs in the

PhilPaSS and the value dates of the transactions are equal to the current business

date of the PhilPaSS. If the transactions are future dated, the value dates

should not be more than four (4) calendar days than the current value date of

the system. The PhilPaSS Business Day opens at 9:00AM and closes at 5:45PM.

Participants may issue system enquiries and secure settlement/status reports

through the System by using the message types applicable to SWIFT-user

(commercial) banks and PPS-FES user (thrift/rural) banks.

The system has the following capabilities: real time accounting, availability

of on-line inquiries and on-demand reports; gridlock detection resolution; liquidity

management (Intraday Liquidity Facility); payment queuing/prioritisation; general

ledger interface and system security, control and audit trails.

The system rules and regulations governing the PhilPaSS are embodied in

the Agreement for the Philippine Payments System via Real Time Gross

Settlement (PPS-RTGS) and the Rules and Regulations Governing the Philippine

Payments System via RTGS that were signed and approved individually by the

PhilPaSS participants.

Because of the different types of transactions processed and settled in the

PhilPaSS and sent by other payment systems interfacing the PhilPaSS, different

settlement timelines are implemented to avoid settlement concentration and

prevent closing time bottlenecks. For instance, the cut-off time for settlement

of ATM transactions is before 11 am, while for the net results of cheque clearing

before 5:45 pm.

3.3.2 Other Retail Payment System Providers

Third party non-financial institutions also offer payment processing services

through the internet (such as Pay Pal, Western Union) and through the mobile

286

payment system. However, in the absence of a Payments Act, these are not

subject to BSP’s oversight and supervision.

3.3.2.1 Mobile Payments System

The most popular forms of e-money in the Philippines are Smart Money

and Globe’s Gcash. Gcash is an internationally acclaimed micropayment service

which transforms a mobile phone into a virtual wallet for a secure, fast and

convenient money transfers at the speed and cost of a text message. Gcash

is owned and operated by a private company, Globe Telecoms.

Smart money is a Mastercard electronic product issued by Banco De Oro

and co-branded with Smart Communications Inc. It is a reloadable payment

card that may either be accessed through a smart mobile phone or a mastercard-

powered card, similar to a debit/cash card. Smart money enables smart