1FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Fin2802: Investments

Spring, 2010Dragon Tang

Fin2802: Investments

Spring, 2010Dragon Tang

Lecture 15Financial Statement Analysis

March 18, 2010

Readings: Chapter 19Practice CFA Problem Sets: 6-

9,13,14,16

2FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Everyone gets sick sometime!Everyone gets sick sometime!

• Take your stocks to a doctor!

• Regular checkups will prevent big problems

3FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Financial Statement AnalysisFinancial Statement Analysis

Objectives:

• Use a firm’s income statement, balance sheet, and statement of cash flows to calculate standard financial ratios.

• Calculate the impact of taxes and leverage on a firm’s return on equity using ratio decomposition analysis.

• Measure a firm’s operating efficiency

• Identify likely sources of biases in accounting data.

4FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Fundamental AnalysisFundamental Analysis

• Economics

• Finance

• Accounting

– How to interpret reported data?

5FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Financial StatementsFinancial Statements

• The Balance Sheet: Snapshot of Financial Condition

– Assets – Liabilities = Shareholders’ Equity

– Current vs long-term

• Income Statement: Summary of Profitability

– Revenue – Expenses = Net Income

– Expenses: raw material; salary; interest; tax

– EBIT=Earnings – Raw Material – Salary

• The Statement of Cash Flows: “Actual” Cash

– More reliable

– Activities: Operating; Investing; Financing

– Depreciation is not smoothed

6FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Accounting vs Economic EarningsAccounting vs Economic Earnings

• Economic earnings: Sustainable cash flow that can be paid out without impairing the productive capacity

• Accounting earnings: “Models” are used

• Accounting earnings are still useful

7FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

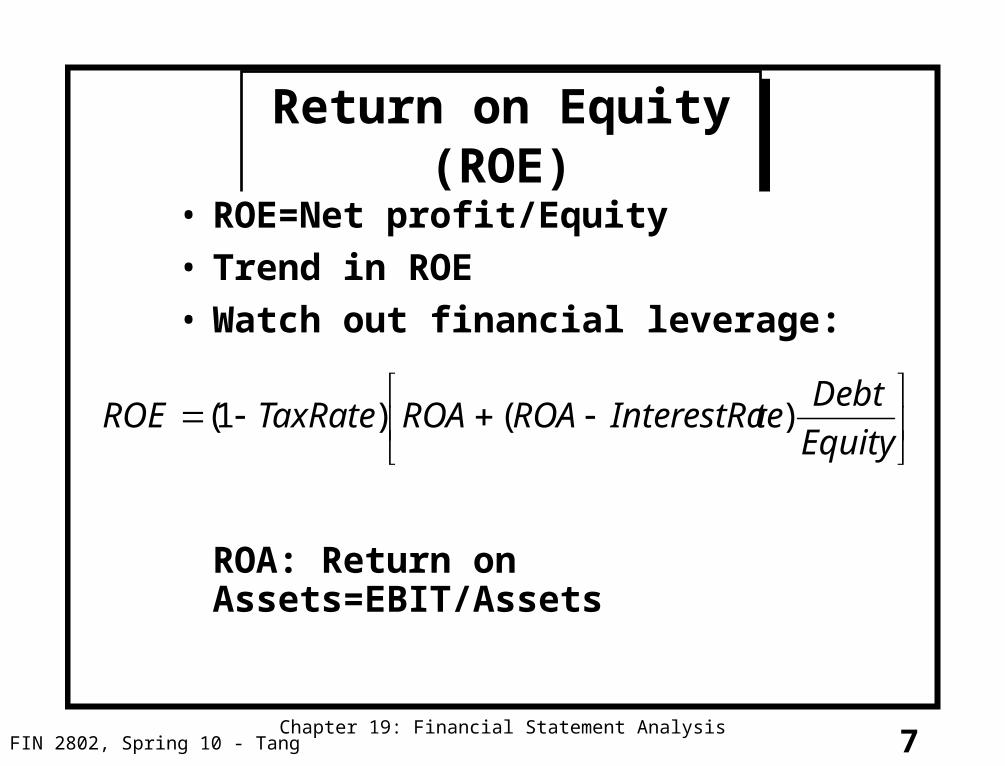

Return on Equity (ROE)Return on Equity (ROE)

• ROE=Net profit/Equity

• Trend in ROE

• Watch out financial leverage:

ROA: Return on Assets=EBIT/Assets

Equity

DebtteInterestRaROAROATaxRateROE )()1(

8FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

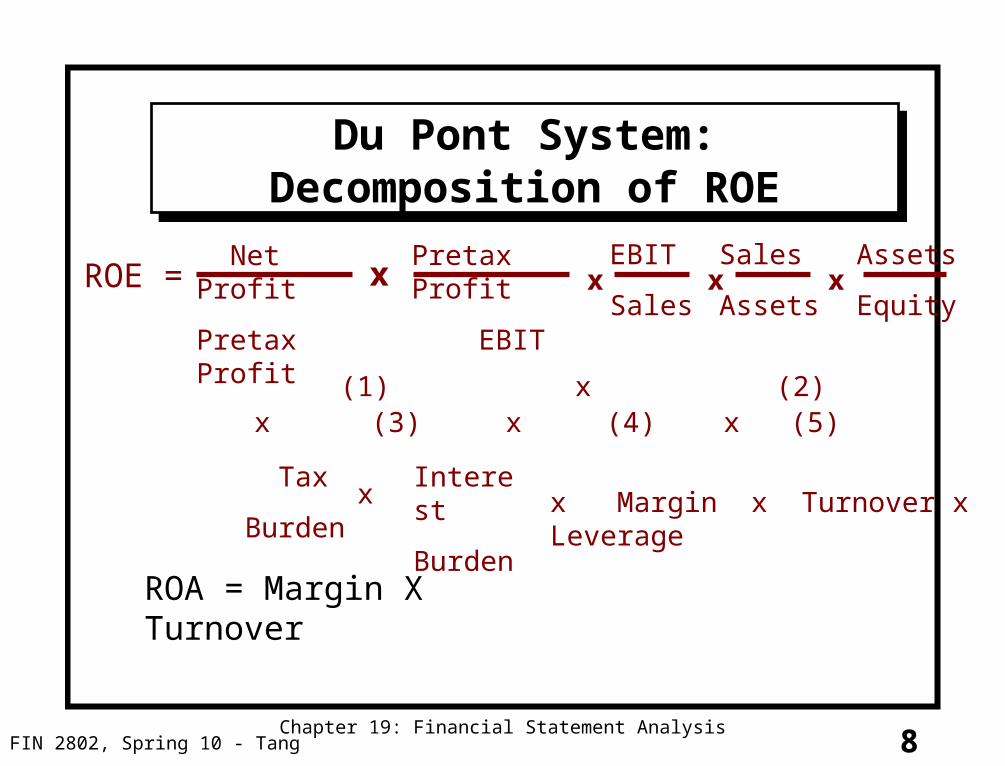

ROE = Net Profit

Pretax Profit

x

Pretax Profit

EBITx

EBIT

Sales

Sales

Assetsx x

Assets

Equity

(1) x (2) x (3) x (4) x (5)

x Margin x Turnover x Leverage Tax

Burden

Interest

Burden

Du Pont System: Decomposition of ROEDu Pont System: Decomposition of ROE

x

ROA = Margin X Turnover

9FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

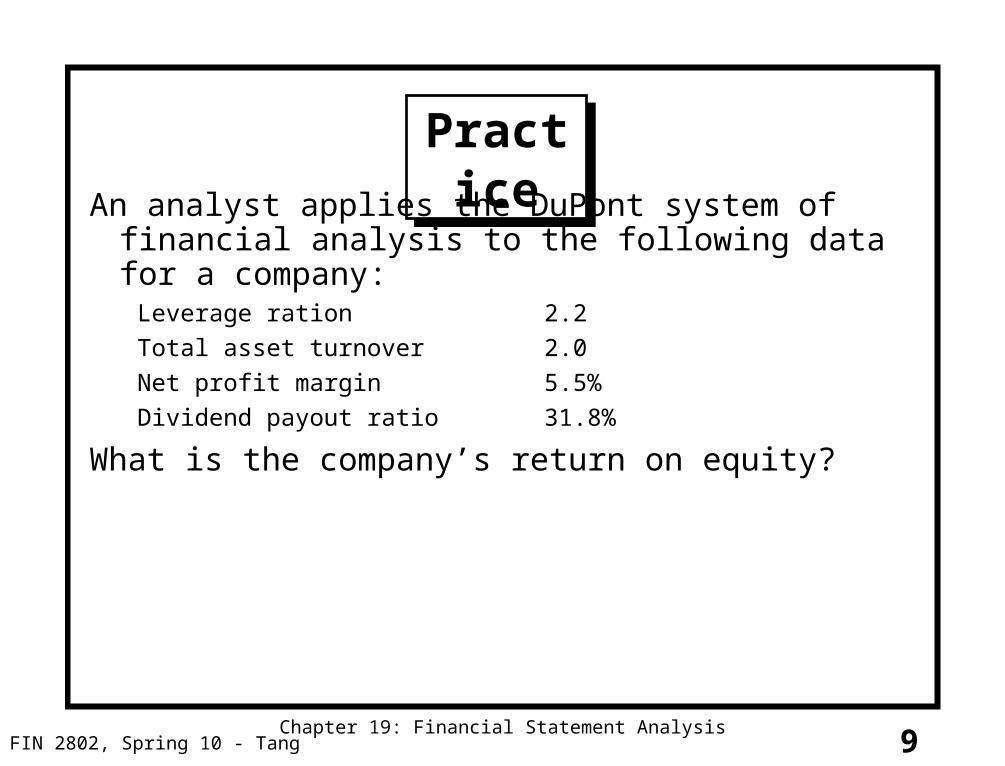

PracticePractice

An analyst applies the DuPont system of financial analysis to the following data for a company:

Leverage ration 2.2

Total asset turnover 2.0

Net profit margin 5.5%

Dividend payout ratio 31.8%

What is the company’s return on equity?

10FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Ratio AnalysisRatio Analysis• Asset utilization ratios: Efficiency

– Fixed-asset turnover=Sales/Fixed Assets

– Inventor turnover=cost of goods sold/average inventory

– Average collection period=(Account receivables/Sales)*365

• Liquidity and coverage ratios: Financial health– Current ratio=current assets/current liabilities

– Quick ratio=(cash+receivables)/current liabilities

– Interest coverage ratio=EBIT/interest expense

• Market price ratios: Relative Value– Market/Book ratio(P/B): “Safeness”

– Price-earnings ratio (P/E): No easy bargain

– E/P=ROE/(P/B)

• Choose a benchmark!

11FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Intel’s Financial Ratios Over TimeIntel’s Financial Ratios Over Time

12FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

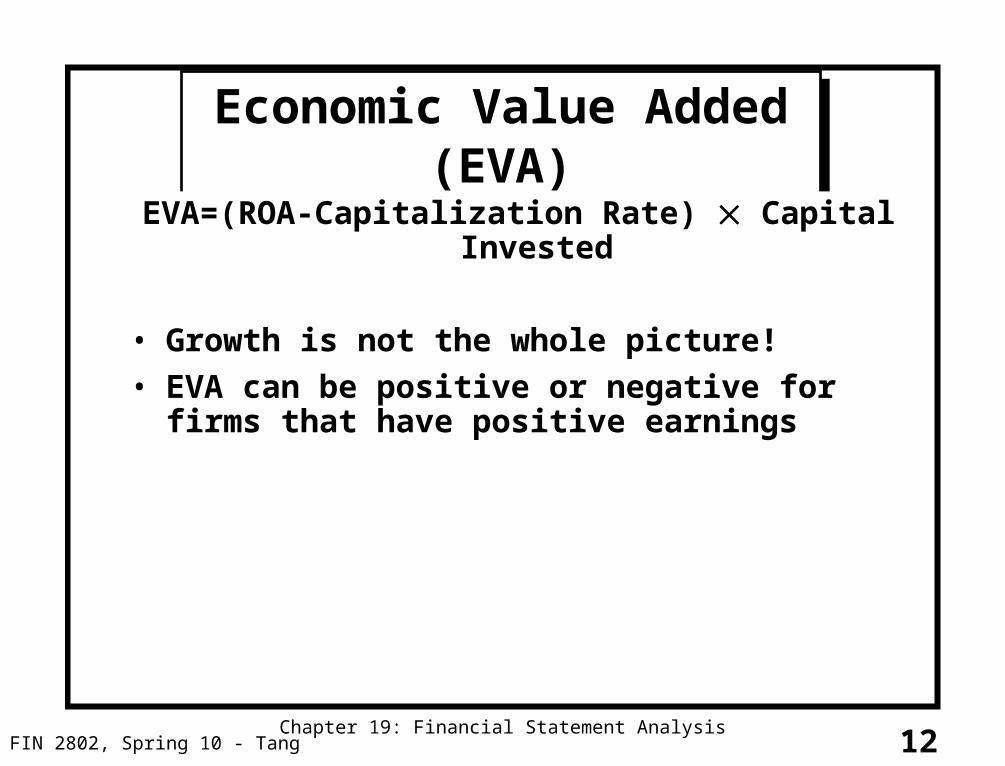

Economic Value Added (EVA)Economic Value Added (EVA)

EVA=(ROA-Capitalization Rate) Capital Invested

• Growth is not the whole picture!

• EVA can be positive or negative for firms that have positive earnings

13FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Key Financial Ratios of Growth Industries Inc.Key Financial Ratios of Growth Industries Inc.

14FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Growth Industries Statements of Cash FlowGrowth Industries Statements of Cash Flow

15FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

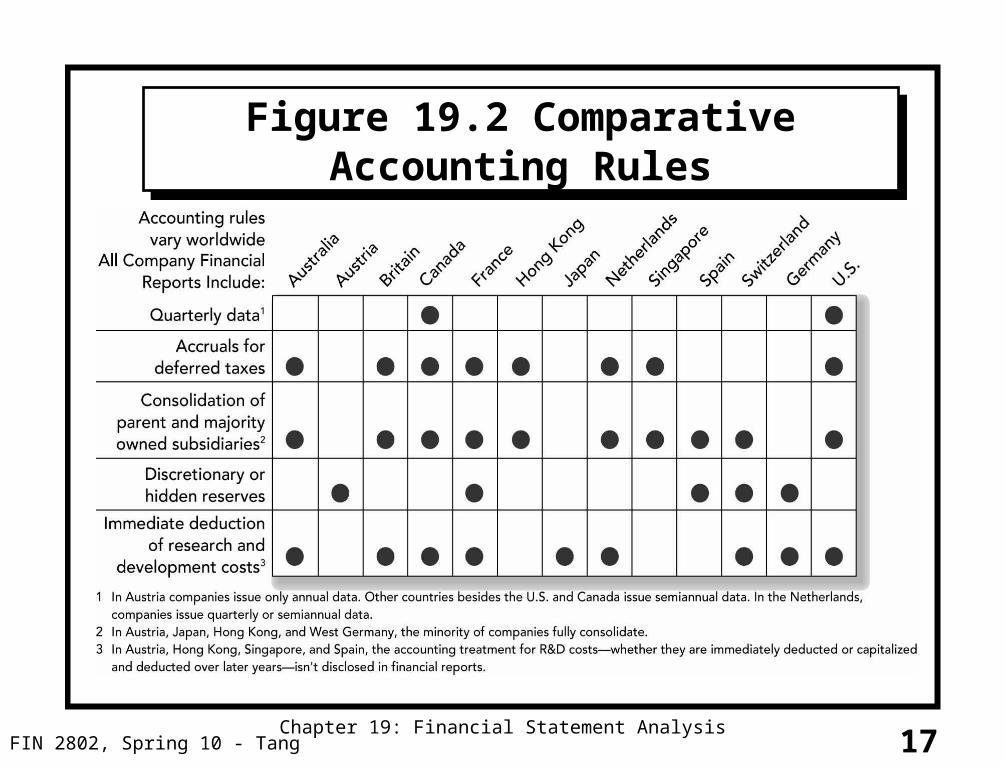

Comparability ProblemsComparability Problems

• GAAP (Generally Accepted Accounting Principles) is not unique– Inventory valuation: LIFO vs FIFO

– Depreciation: Straight line vs Accelerated

– Real interest payments

• Quality of earnings affected by:– Allowance of bad debt; nonrecurring items; stock option;

revenue recognition; off-balance-sheet assets and liabilities

• GAAP vs IAS (International Accounting Standards)

16FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Quality of Earnings:Areas of Accounting Choices

Quality of Earnings:Areas of Accounting Choices

• Allowance for bad debts

• Non-recurring items

• Reserves management

• Stock options

• Revenue recognition

• Off-balance sheet assets and liabilities

17

Figure 19.2 Comparative Accounting RulesFigure 19.2 Comparative Accounting Rules

FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

18FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

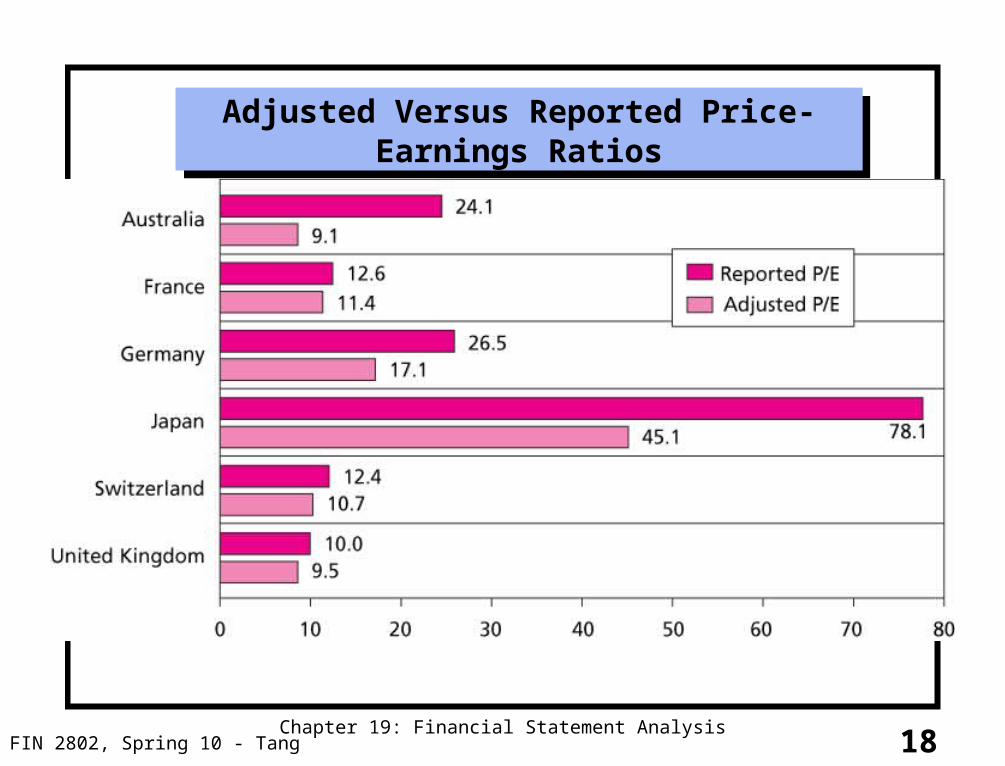

Adjusted Versus Reported Price-Earnings RatiosAdjusted Versus Reported Price-Earnings Ratios

19FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

Value InvestingValue Investing

• Benjamin Graham

• Pick value stocks (low P/B)

• Rule: stock price < net current-asset value

• Information sources: S&P’s Outlook and Value Line Investment Survey

20FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

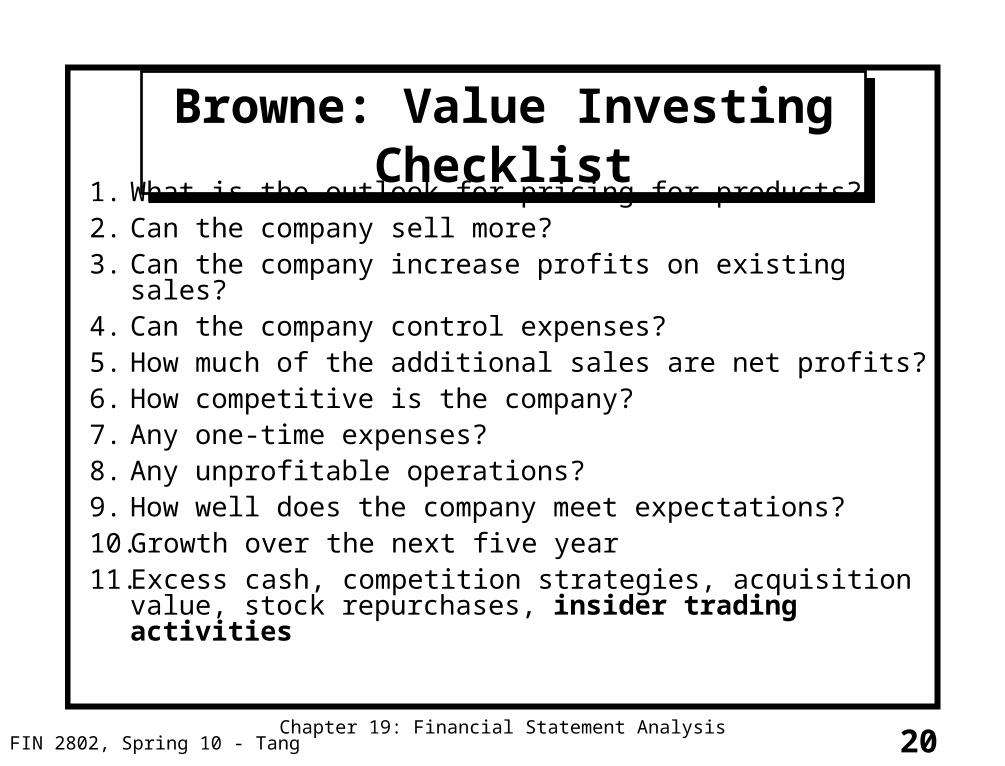

Browne: Value Investing ChecklistBrowne: Value Investing Checklist

1. What is the outlook for pricing for products?2. Can the company sell more?3. Can the company increase profits on existing sales?4. Can the company control expenses?5. How much of the additional sales are net profits?6. How competitive is the company?7. Any one-time expenses?8. Any unprofitable operations?9. How well does the company meet expectations?10. Growth over the next five year11. Excess cash, competition strategies, acquisition value, stock

repurchases, insider trading activities

21FIN 2802, Spring 10 - TangChapter 19: Financial Statement Analysis

SummarySummary

• Fundamental Analysis

• Economic earnings vs accounting earnings

• Financial Statements

• Du Pont System; ratio analysis

• Economic Value Added

• Comparability

• Next: Macroeconomy and Stock Market

![NATO phonetic alphabet - · PDF file14.06.2015 · RAH SEE-AIR-AH ERR-ah T Tango TANG go TANG GO TANGGO or TANG-GO ˈtænɡo tang go [ˈtæŋɡoʊ] /ˈtæŋɡoʊ/ TANG-goh U Uniform](https://static.documents.pub/doc/80x56/5a7a9f247f8b9abd768d9267/nato-phonetic-alphabet-see-air-ah-err-ah-t-tango-tang-go-tang-go-tanggo-or-tang-go.jpg)