QUESTIONS

“Unlike riba, profit is recognized in Islam because of its characteristic as a justified form of

reward for capital and enterprise.”

(a) Discuss the above statement

(b) List in a table the differences between profit and riba

INTRODUCTION

“Allah forbids riba and permit trades.”

Surah 2:275

Although riba is forbidden in Islam, profit generated from trade is a justifiable source of

income in Islam. This article discusses the differences between riba and profit and from there

deduces the rationale of the above injunction.

For some people, the religious commitment will be good enough to guide them to reject the

practice of riba and deem profit as the only justifiable source of income. However, for the

other group, they deserve a more convincing explanation and clarification from economical

and social point of view. Since the author is not a Muslim herself, it will not be persuasive to

advocate that riba is unjustifiable on religious ground alone. Therefore, with fair amount of

religious elements, this article examines riba and profit largely from economical aspect.

DEFINITIONS

The Prohibited Riba

In a gradual process, little by little Al-Quran prepares the ground and social environment for

final prohibition. Riba in Islamic terminology is increase or excess over principal or more

precisely, it is called a stipulated/forced/obligatory surplus on a debt.1 Or it can be defined as

an increase or excess value (fadf) which in an exchange or sale of a commodity, accrues to

the owner (lender) without giving in return any equivalent counter value or iwad. 1 In 1992,

the Pakistan Federal Shariah Court ruled that: “Any excess which is pre-determined over the

principal sum in a loan transaction will constitute Riba in all circumstances.”2 By and large,

as a general principal, riba exist as long as the exchange/transaction involves ribawi items

and gives rise to inequality of counter values (al-fadl) and determent in time of exchange (al-

nasiah).3 Terminologically the equivalence of riba in economic tradition is usury, something

that was prohibited in Jewish and Christianity also. But modern banking gets around the

prohibition of usury little by little and eventually replaces the word usury with interest.4

Usury was also prohibited in ancient China. 5 Since it is not only Islam that prohibits riba, it

is reasonable to infer that the practice of riba is somewhat harmful to the society.

The Permitted Profit

Profit is the return on trade, which is the result of difference between revenue and cost,

encompassing the effort and risk undertaken by the entrepreneur. Existence of risks either

before-sale or after-sale inadvertently results in uncertainty in profit (or loss). This is based

on the legal maxim (Qawaid Fiqiah) that states al-ghunm bil al-ghurm which can be

translated as “gain is the result of risk-taking”.6 Thus Muhammad Ayub (2007) described

profit as ex-post, which is only known after the business venture. He also insists that profit

generated from trade should be associated with real asset. 7 Islam places a great importance

in trade and encourages it because it is the major vehicle of increasing real income. Muslims

believe that God wants his people to be prosperous and to avail themselves of the bounties of

his creation.

RIBA VS PROFIT

Riba vs Profit on Counter-value

According to Fiqh scholars profit is a justified increase which is usually generated by

exchange of two goods while riba occurs in unjust inequitable exchange of one commodity

against another.1 Hanafi, Shafii and Maliki schools all agree on the term “unequal counter-

value” when it comes to defining riba albeit the differences in the exact definitions.

Therefore, this remaining of this section dedicates to explain graphically the differences of

riba and profit in term of counter-value.

Figure 1(a) Equal Exchange1 Figure 2 (b) Exchange involved

Riba1

Figure 2 (a) shows the equal exchange between A and B for Y product, in which ya + yb = Y.

MN is the opportunity space or the maximum available endowment of Y. At point E

(intersection between MN and 45o straight line from the origin), A and B is in equal

proportions - A is getting OYaE while B is getting OYb

E. The 45o straight line is the equal

counter value line, in which Y=X. Figure 1(a) shows that, it is a zero sum game activity

where the gain of one party is directly the loss of the other one.1 Any point fall out of point E

will not result in equal counter value. Additional value that accrues to either party in this

kind of transaction amounts to excess without counter value or prohibited riba in Islam.

In the case of Figure 2(b), A has endowment of good OQAe and certain amount of money

OMAe and B has endowment of good OQB

e and money amount of OMBe. A requires to have

more money and sell some of his plenty of good. While B would like to purchase some of

good Q from A in exchange for money, in which the exchange normally takes place at a

prevailing market price. However, in this transaction, A sells (QAe-QA

E) of the good for (MBe

– MBI) which B will pay by instalment. The extra price paid than that of the market value

(MBe – MB

E) is a result of interest imposed on B. This additional amount money that accrues

to A is absolutely the loss to individual B, where the stock of individual B decreases from

MBE to MB

I . Since ΔMA = ΔMB is in absolute terms, so in exchange rationale, this is one side

flow which has no any corresponding value in repayment, resulting in riba which is shaded in

yellow in Figure 2(b). In Islam, an alternative to prevent riba in deferred payment mode is

Murabaha-Mu’ajjal.

Yb

Ya

M

ON

EYaE

YbE

45o

Q

OA M

O

B

e E IQ

AE

QA

e

MA

MA

MA

I

MB

IMB

e MB

QB

e

QB

E

Conclusively, riba results from an exchange without equal counter value whereas profit

results from an exchange with equal counter value. Therefore, the former is forbidden but

the latter is permitted in Islam.

Riba vs Profit on Wealth Creation

Islamic commercial law aims at promoting the actual wealth creation instead of artificial and

‘bubble’ creation of wealth.1 Profit generated in the process of trade is a result of:

i. Additional value of goods - due to physical transformation of an object from one

form to another; usually quantifiable in monetary term (price difference final

products between raw materials as well as other operational costs) and

ii. Exchange of goods with others - exchanging goods with lower marginal utility

with the higher ones results in higher utilities for both trading parties. This

concept will be illustrated below.

Exchange of goods take place because differences in endowments and abilities of producing

goods and services and differences in preferences or tastes.4 Most importantly, exchange is

needed to maximize utility because of diminishing marginal utility and different marginal rate

of substitution. Intuitively, well-balanced, diversified bundles of commodities are preferred

to bundles that are heavily weighted toward one commodity, leading to the convex nature of

most of the indifferent utility curves.8 It is noteworthy to refer this principle to the context of

the story of Bani Israel when they tired of eating the heavenly food manna and salwa and

they said that they could not keep satisfied with one type of food only.1 It implies that even

the heavenly food is less of a choice to the Israelites than variety of foods. Figure below

shows how trade can increase the real wealth between two trading parties and thus justify the

return on trade – profit.

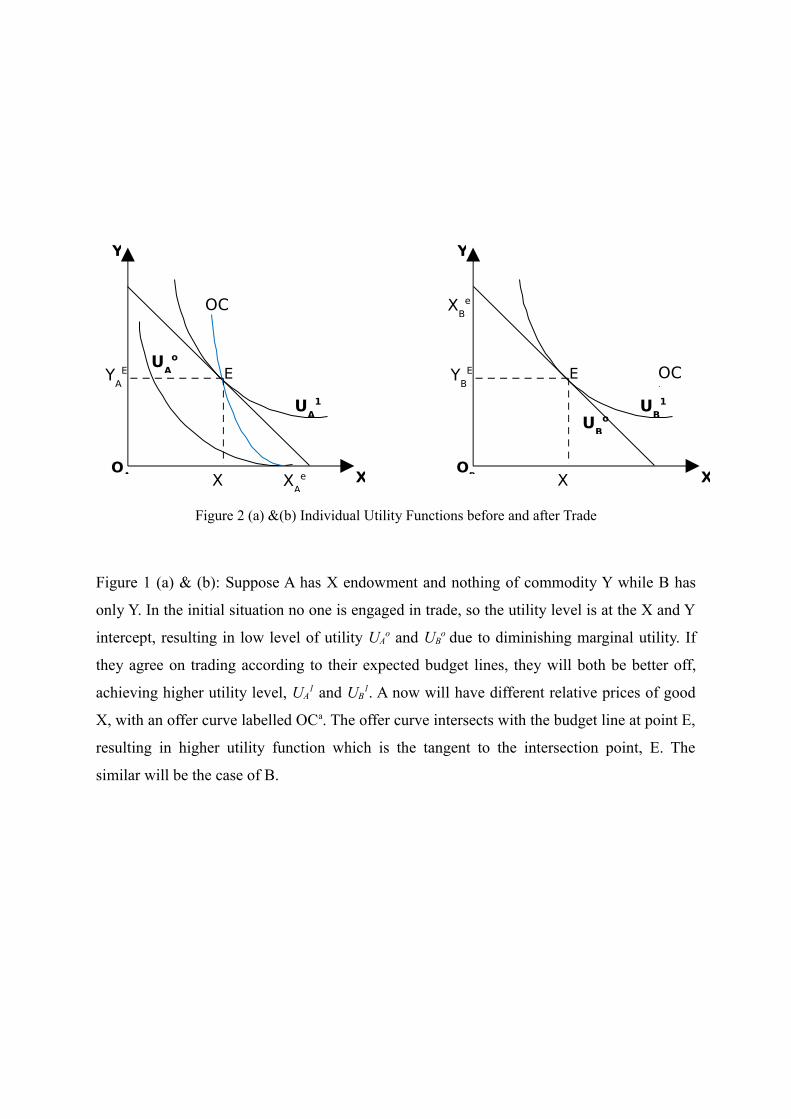

Figure 2 (a) &(b) Individual Utility Functions before and after Trade

Figure 1 (a) & (b): Suppose A has X endowment and nothing of commodity Y while B has

only Y. In the initial situation no one is engaged in trade, so the utility level is at the X and Y

intercept, resulting in low level of utility UAo and UB

o due to diminishing marginal utility. If

they agree on trading according to their expected budget lines, they will both be better off,

achieving higher utility level, UA1 and UB

1. A now will have different relative prices of good

X, with an offer curve labelled OCa. The offer curve intersects with the budget line at point E,

resulting in higher utility function which is the tangent to the intersection point, E. The

similar will be the case of B.

XA

eX

AE

Y

XO

A

E

OCa

YA

EU

Ao

UA

1

XB

e

X

BE

Y

XO

B

E OCb

YB

E

UB

oU

B1

Figure 2 (c) Superimposed Utility Functions of Two Parties of Exchange 1

Figure 1 (c): Imposing the two diagrams (a) & (b), we can find the efficiency of exchange

process by raising the welfare of both individuals. Before the exchange A and B would ends

Y

E

XA

OA

OB

M

N

UA

o

UB

o

X

UB

1

UA

1

OC

OC

XA

YB

E

XB

YA

E

YB

o

up at M and N respectively. However through exchange they will arrive at anywhere

between M and N with the highest point, E.

In contrast with trade, Riba activities do not create new stock of wealth. It is a zero sum

phenomenon arises from exchange of two identical goods, which there is no way to increase

the utility of one party without reducing the other. For an example, in many countries

government raise fund from the public by issuing interest-based notes and bonds with a fixed

return.9 If the fund raised does not result in return higher than the promised interest rate,

these interests will have to be paid by the next generation in the form of tax as suggested by

Ramsey-Cass-Coopman infinite horizon model (which is indifferent between tax and bond).

In this case wealth is merely transferred from the future generation to the current one. The

government may even find itself caught in the vicious cycle of debt, which eventually leads

to debt crisis that further deepen the hole of debt. On the other hand, if the government is to

raise shariah-compliant bond (sukuk) based on real assets by sharing the real profit or loss,

then it will be free from the problem above. It should be noted that the above example is only

one of the examples of the detrimental effect of riba to the real economy.

Conclusively, trade takes place only when situation shows a surplus of satisfaction thus

resulting in real wealth creation – profit; whereas riba activities involve only wealth transfer,

any return from these activities will result in loss of the others thus not resulting in any real

wealth creation.

ARGUMENT IN DEFENDING RIBA

In this section, two of the most common arguments defending the justifications of riba will

be discussed and the validity of these arguments will be examined.

Riba as Commodity

The practice of riba will be permissible by considering money as commodity. However,

Islam never recognized money as commodity. Money as well as fungible items have been

viewed in Islam as ribawi item, which if exchanged, have to be in equal amount as well as on

the spot interpreted from the passage as below:-

“Gold for gold, silver for silver, wheat for wheat, barley for barley, dates for dates and salt

for salt, like for like, equal for equal and hand to hand. If the commodities differ, then you

may sell as you wish provided the exchange is hand to hand.”

Narrated by Sahih Muslim

Islamic banking and finance cannot deal with money directly to generate income or profit

because money is ribawi item.7 In Islamic law, benefit or profit accruing to one party out of

bilateral contracts must be always justified on the basis on one’s exposure to some degree of

risk and liability. 9 In the case of lending with a stipulated rate of interest, the lender is not

exposed to uncertainty since the interest rate is pre-determined. Additionally, in Islam giving

a loan or extending credit (debt) comes under the contract of tabarru’ (benevolence). One

asks a loan or debt because he is in need. Such need should not be exploited by charging riba

on the loan, 3 thus prevent inflicting injustice in the society.

Riba actually bring some benefits

AP Dr Mohd Daud Bakar revealed that some may justify riba by suggesting that riba actually

benefitted the society, individuals and institutions, lenders and borrowers. For an example,

profit earned by financial institutions is in part used to pay salaries and thereby allow

employees to enjoy life. And surely shareholders of the banks, they will also benefit of the

income earned.9 It should be noted that however, Islamic bank in Malaysia is not less

efficient than the conventional banks according to the studies done by Mariani Abdul Majid ,

Nor Ghani Md. Nor, Fathin Faizah Said.10 This implies that Islamic banks can perform as

well as conventional banks without engaging in riba related activities. Therefore, the

arguments that riba is needed for the good of employee and shareholder have no ground.

Even if it really brings some benefits to the society, the harm that it does (which will be

discussed in next section) will be too big to be surpassed by the advantages.

IMPACT OF RIBA-BASED BANKING SYSTEM

Some of the undesirable features of riba-based banking system suggested by AP Dr. Mohd

Daud Bakar from Islamic International University Malaysia are as below: -

i. Inflexibility of riba-based banking system tends to cause loss of productivity in the

future.

a. The borrowers have to pay a pre-determined rate of interest of the sum even

though he may have incurred loss or earned less than the sum needed to pay

for the interest rate, adding into the burden of entrepreneurs and thus its

expansion.9

b. In the early stage, some businesses may achieve a smaller rate of return than

that of the interest rate imposed on them. However, these businesses may

possess high growth potential in long term point of view. A pre-determined

interest rate may jeopardize the solvency of the businesses and the worst case

scenario is folding-up before good profits can be generated. This again results

in loss of productive potential.

c. Inflexibility in the interest-based system also causes inflexibility in business

strategies. Businesses tend to draw strategies that enable them to meet the

current financial obligations instead of what is really good for long term

productivity. The less than perfect business strategies again results in loss in

future productivity.

ii. The interest-based system is security-oriented rather than growth-oriented9.

a. In their lending operations, banks are most concerned about the safe return of

the principal lent along with the stipulated interest because of their

commitment to pay a pre-determined rate of interest to depositors. To reduce

risk, banks tend to allocate resources to well established big businesses instead

of potential entrepreneurs who may not be able to satisfy the banks criteria of

creditworthiness. As a result, entrepreneurship which is the backbone of

economic growth could not reach its full potential growth.

b. Oversupply of credit to well established parties and its denial to a large

segment of population also results in increasing inequalities in income and

wealth.

c. Security-oriented economy inadvertently results in stock market boom and

bust.

iii. The interest-based system discourages innovations9.

a. This is particularly true on the part of small-scale enterprises. Small-scale

enterprises are less willing to involve in R&D activities or new method of

production with the money borrowed from banks because these activities do

not always guarantee a fixed return. On a contrary, the business is obliged to

pay for the interest in addition to the principal for the money borrowed. Big

businesses, given preference from the banks and large cash reserve, will do

most of the R&D and getting more productive, resulting in further inequality.

b. In addition, with lack of incentive to innovate, the society does not reach its

full potential of technological change given the same resources. Many modern

economists suggest that technological change is one of the most important

determinants in economic growth. Thus a less aggressive technological change

may result in a slower economic growth.

Equity or debt financing in Islamic banking does not result in any of the above mentioned

problems. The techniques of the newly emerged riba-free institutions consist of: musharaka

(partnership), murabaha (cost-plus-profit contract), ijara (lease contract), ijarawa-iqtina'

(hire-purchase contract), qard hasan (interest-free loan), takaful (mutual guarantee) and

mudaraba (commenda partnership)4, which will not be discussed here as they deserve

another article to discuss in detail.

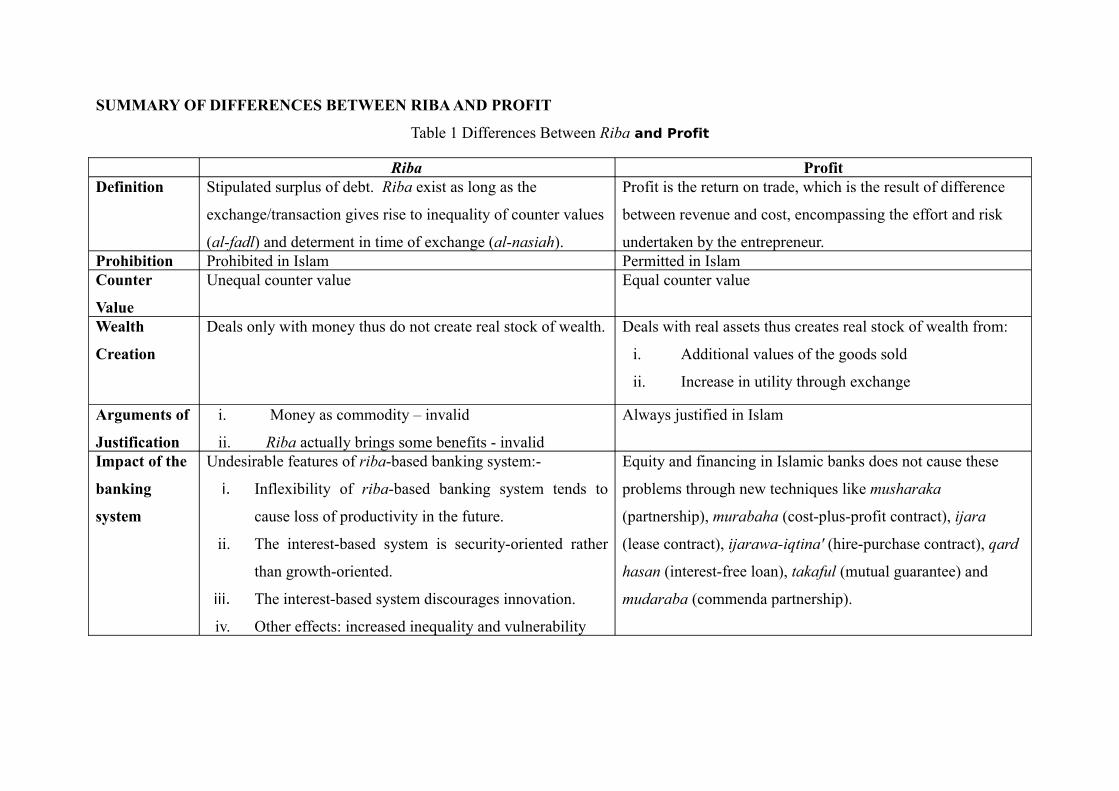

SUMMARY OF DIFFERENCES BETWEEN RIBA AND PROFIT

Table 1 Differences Between Riba and Profit

Riba ProfitDefinition Stipulated surplus of debt. Riba exist as long as the

exchange/transaction gives rise to inequality of counter values

(al-fadl) and determent in time of exchange (al-nasiah).

Profit is the return on trade, which is the result of difference

between revenue and cost, encompassing the effort and risk

undertaken by the entrepreneur.Prohibition Prohibited in Islam Permitted in IslamCounter

Value

Unequal counter value Equal counter value

Wealth

Creation

Deals only with money thus do not create real stock of wealth. Deals with real assets thus creates real stock of wealth from:

i. Additional values of the goods sold

ii. Increase in utility through exchange

Arguments of

Justification

i. Money as commodity – invalid

ii. Riba actually brings some benefits - invalid

Always justified in Islam

Impact of the

banking

system

Undesirable features of riba-based banking system:-

i. Inflexibility of riba-based banking system tends to

cause loss of productivity in the future.

ii. The interest-based system is security-oriented rather

than growth-oriented.

iii. The interest-based system discourages innovation.

iv. Other effects: increased inequality and vulnerability

Equity and financing in Islamic banks does not cause these

problems through new techniques like musharaka

(partnership), murabaha (cost-plus-profit contract), ijara

(lease contract), ijarawa-iqtina' (hire-purchase contract), qard

hasan (interest-free loan), takaful (mutual guarantee) and

mudaraba (commenda partnership).

COMMENTS

Current economic crisis has awakened the world the many loopholes of conventional banking

system. Islamic banking and finance is the most appealing alternative for the regulators and

investors as they are looking for a better way of doing things. For an example, French

Finance Minister Christine Lagarde at a recent forum in Paris said that Western financiers

could learn a thing or two from the Islamic world as global leaders try to establish “new

principles for the international financial system, based on transparency, responsibility and, I

would like to add, moderation.” 11 It neighbouring country, Britain owns the largest sharia-

compliant asset among the non-muslims countries. (See figure below).

Undoubtedly, the potential of Islamic banking and finance is vast, however fully shariah-

compliant especially in the area of interest-free is unlikely, at least for the next few decades.

This is because interest rate is one of the most important regulatory tools for the government

in monetary policy. Additionally, many economic theories which are used in deriving fiscal

policies have been established in which interest rate is one of the variables. A complete

overhaul of such well-established policies and theories is unlikely in a foreseeable future

albeit the recognition of the detrimental effects of interest-based banking system. The society

may deem the cost of changing the system is higher than the cost paid for the mess created

from the riba-based system and thus choose to stay in the old system. This case is especially

true for non-Muslims as religion is not a strong ground for change. Therefore, the author

suggests that while riba-free banking system is a more viable one, it will remain a

complementary to that of the conventional system in the next few decades until a set of new

and sound economic theories and policies emerge and become well-established.

Figure 3 Rank in Sharia-compliant Assets 200712

CONCLUSION

Riba which is forbidden in Islam is a stipulated surplus from debt. It exists as long as the

exchange/transaction gives rise to inequality of counter values (al-fadl) and determent in time

of exchange (al-nasiah). On the other hand, profit which is permitted in Islam is a return

from trade (revenue minus cost).

Riba activities incur unequal counter value in exchange and do not create new stock of

wealth. The opposite is true for profit. Additionally, Riba has never been able to be justified

in Islam since arguments that i. money as a form of commodity and ii. riba actually brings

some benefits could not be rightly justified.

Finally, riba-based banking results in the following adverse effects to the society: loss of

future productivity, security-oriented economics, stifled innovations and increased inequality

and vulnerability. Islamic banking system, on the other hand, avoids these problems by using

various shariah-compliant techniques.

Despite all the benefits, it is unlikely for global banking and finance to be riba-free in the

near future because the practices of interest-based activities have been deeply rooted in the

current economic system. Therefore, it is presumed that riba-free banking system will only

play a complementary role to that of the conventional one.

BIBLIOGRAPHY

1 “Chapter 5 Riba vs Profit in Exchage Context.” 20 Feb.2009. < http://72.14.235.132/

search?q=cache:5OphFX9QykJ:prr.hec.gov.pk/Chapters/1055.pdf+riba+vs+profit&hl=en&ct=clnk&cd

=1&gl=my >.

2 “Malaysia Toward an Islamic State: Islamic Banking in Malaysia.” Publication of Islamic System of

Zakat. 20 Feb. 2009. <http://www.islamic-world.net/islamicstate/malay_ islambank.htm>.

3 AP Dr Radiah Abdul Kader. “Main Prohibitions in Muamalat Transactions.” BSP-02, FEP, University

of Malaya. 22 Jan. 2009.

4M.H.Zahedi Vafa.“ Comment of M.H Zahedi Vafa on Riba Versus Profit in Exchange Economy:

Conceptual Foundations for Stable Financial System in Islamic Perspectives by Elmi Nur.” 20 Feb.

2009. <http://islamiccenter.kaau.edu.sa/7iecon/Ahdath/Con06/pdf/Vol2/ 55%20

Comment%20by%20Zahedi%20Vafa.pdf>.

5 “Usury.” Wikepedia. 22 Feb. 2009. <http://en.wikipedia.org/wiki/ Usury>.

6 AP Dr Radiah Abdul Kader. “Profit: The Islamic Alternative to Riba.” BSP-02, FEP, University of

Malaya. 13 Feb. 2009.

7 Ayub, Muhammad. Understanding Islamic Finance. John Wiley and Sons, 2007.

8 Michael E. Wetzstein. Mircoeconomic Theory. USA: Thomsan South-Western, 2005. 34.

9 AP Dr Mohd Abdul Bakar. “Riba and Islamic Banking and Finance.” 22 Feb. 2009.

<http://www.cert.com.my/cert/pdf/riba_drdaud.pdf>.

10Mariani Abdul Majid, Nor Ghani Md. Nor, Fathin Faizah Said. “Efficiency of Islamic Banks in

Malaysia.” International Islamic University Malaysia. 20 Feb. 2008.

<HTTP://ISLAMICCENTER.KAAU.EDU.SA/7IECON/AHDATH/CON05/5TH%20CONF%20

PPR%20FOR%20BAHRAIN/EFFICIENCY%20OF%20ISL.%20BANKS%20IN%20MALAYS

IA%20BY%20MARIANI%20ABDUL%20MAJID%20.DOC>.

11 “Appeal of Islamic Finance.” Malay Mail – Your Voice. 25 Dec. 2008.

12 “Faith Based Finance.” The Economist. 4 Sept. 2008.