7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 1/61

BHARAT HEAVY ELECTRICALS

LIMITED

TRAINING&

DEVELOPMENT

SUMMER INTERNSHIP PROJECT REPORT2008-2010

Corporate Guide:-

J.P.BANDUNI

H.R MANAGER

Faculty Guide:-

LIMT GREATER NOIDA

Submitted in Partial Fulfillment for the Award of Degree MASTER IN BUSSINESS ADMNISTRATION

Submitted by: -SURABHI SACHANRoll No:-0817270096

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 2/61

Prakash Chandra Dash

B.I.M.I.T, Bhubaneswar

FACULTY GUIDE CERTIFICATE

This is to certify that Rajendranath Behera, a student of Bhubaneswar Insti tute of Management and Information

Technology, Bhubaneswar pursuing his MBA (Marketing) has

worked under my guidance and supervision on his Work

entitled “Reliance Money – An Investment Avenue” . To the

best of my knowledge this is an original piece of work.

(Prakash Chandra Dash)Faculty Marketing

I Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 3/61

DECLARATION

I Sri Rajendranath Behera do hereby declare that the project report

entitled “Reliance Money – An Investment Avenue” being submitted to

Biju Patnaik University of Technology, Rourkela is my own piece of

work and it has not been submitted to any other institute or published at

any time before.

Rajendranath BeheraRegd No: - 0706275024

Bhubaneswar Institute of Management & InformationTechnology

II Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 4/61

ACKNOWLEDGEMENT

This report bears the imprint of many people. Right from the experienced

staff of Reliance Money, to the staff of Bhubaneswar Institute of

Management & Information Technology without whose support and

guidance I would have not got the unique opportunity to successfully

complete my internship in this esteemed organization.

I take this opportunity to express my deep gratitude to all the employeesof, Reliance Money, Bhubaneswar . Also I am indebted for the rich

guidance, knowledge and suggestions provided by my guide, Mr.

Prakash Das who took sincere efforts and illustrated the Marketing

Concept of Financial Products, with their vast knowledge in the field,

which helped me in carrying out my internship.

I am gratified to Prof. B.M. Das for their earnest coordination owing to

which, I had the leg-up of undertaking the internship at the prominent organization, Reliance Money Pvt ltd.

Last but not least, I also thank all those people whom I met in the

industry during my internship and helped me to accomplish my

assignments in the most efficient and effective manner.

Date: 18th Aug 2008

Place: Bhubaneswar (Rajendranath Behera)

III Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 5/61

EXECUTIVE SUMMARY

The project work is pursued as a part of MBA (Marketing)

Curriculum at BHUBANESWAR INSTITUTE OF MANAGEMENTAND INFORMATION TECHNOLOGY, Bhubaneswar. It is

undertaken as a traineeship at Reliance Money Ltd. The project is

done under expert supervision and guidance of Mr. Prakash Chandra

Das (Lecture in Marketing) and Mr. Suresh Behera (Center Sales

Manager, Reliance Money)

The Pro jec t i s abou t the s tudy o f market ing and sa les of

financial products and also the efforts done to make improvements inthe customer acquisition process for better results.

At RELIANCE MONEY, initially the trainees were imparted

process and product knowledge. They were given sufficient time to

know about the products and also about sales and dist ribution

channel . They had to work with the sales representatives of the

Distributor and think of ways of improving the sales and distribution

channel and implementing them. The main aim was to increase salesand for this different ways were tried and implemented. They were

provided with da tabase and had to make cold calls from the data.

Company activity was also one of the major sources for generating

business. Initially they even accompanied sales representatives to the

clients place. Main objective was to know the need of the customer

and how to fulfill that in the best way.

The project dealt with various fields like:

1. Trading and Demat account

2. Mutual funds

3. Life insurance

4. General insurance

Thus i t gave trainees the opportunity to learn about all the

products and with the range of products Reliance money offered it

IV Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 6/61

made the task a bit easier as we could fulfill the need of the customer

in a better way.

Our task was divided in 4 phases:

1. Product knowledge: This included the theoretical knowledge about

the field and products which needed to be marketed.

2. Pitching in retail sector: This included the implementation of the

knowledge impar ted to us and the tes t of our marketing ski ll s.

Initially we were accompanied by other sales executive so that we can

learn how to deal with the customers and understand their need. This

also enhanced our interpersonal skills and confidence level.

3. Implementation in retail sector and pitching in corporate: By

the start of this phase we were confident enough about the pitching

and fulfilling the needs of the customer in the retail sector. This also

included of the ways we should pitch the corporate.

4 . Implementat ion at corporate l eve ls : This included the

implementation of the all the knowledge and ways learnt for the

pitching and extracting busines s out of the corporate.

With the end of 6 weeks every phase was completed and it gave

us the real experience of retail as well as corporate world.

V Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 7/61

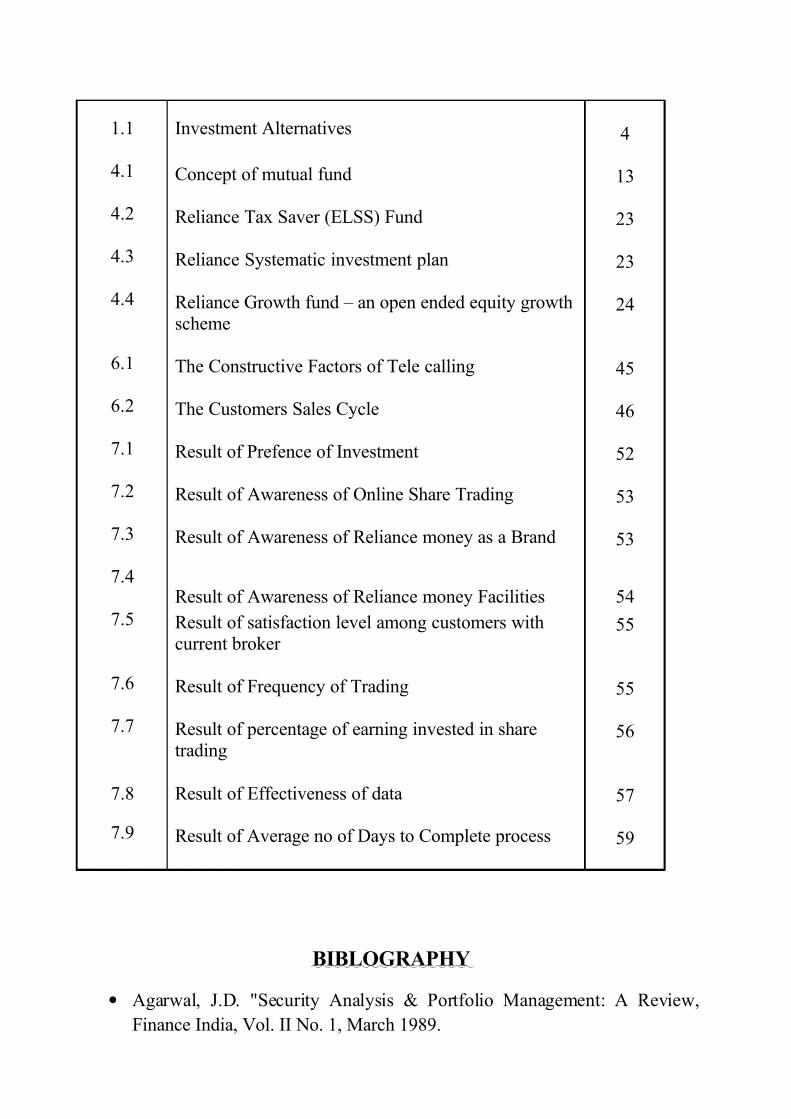

CONTENTCertificate of CompanyFaculty Guide Certificate iDeclaration iiAcknowledgement iiiExecutive Summary iv-v

CHAPTER 1 INTRODUCTION 1-8

1.1 INVESTMENT AVENUES AND ALTERNATIVES 11.1.1 Non-marketable Financial Assets 51.1.2 Equity Shares 51.1.3 Bonds 61.1.4 Money Market Instruments 61.1.5 Mutual Funds 61.1.6 Life Insurance 71.1.7 Real Estate 71.1.8 Precious Objects 7

1.1.9 Financial Derivatives 7

CHAPTER 2 LITERATURE REVIEW 9-11

2.1 Significance of Study 102.2 Objective of Study 11

CHAPTER 3 COMPANY PROFILE 12-13

3.1 PRODUCT OFFERING 133.1.1 Trading Portal 133.1.2 Financial Products 133.1.3 Value-Added Services 133.1.4 Credit Cards 133.1.5 Gold coins retailing 13

CHAPTER 4 TRADING PORTAL 14-19

4.1 DEMAT ACCOUNT 14

CHAPTER 5 FINANCIAL PRODUCTS 20-42

5.1 MUTUAL FUNDS 20

5.1.1 Open end versus Closed end Schemes 215.1.2 Constitution of a Mutual Fund 23

VI Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 8/61

5.1.3 Types of a Mutual Funds 245.1.4 How to invest in Mutual Fund 265.1.5 Nature of Income Distribution to Investors 285.1.6 Different schemes of Reliance Mutual fund 29

5.2 LIFE INSURANCE 315.2.1 Tax Benefits of Insurance 335.2.2 Claims 355.2.3 Plans 37

5.3 GENERAL INSURANCE 395.3.1 Types of General Insurance 39

5.4 BASIC FEATURES 415.5 VALUE ADDED FEATURES 415.6 POLICY FEATURES 41

CHAPTER 6 OBJECTIVE AND CONCLUSIONS 43-51

6.1 OBJECTIVE 436.2 METHODOLOGY 436.3 SWOT ANALYSIS 466.4 MY ROLE IN THE ORGANISATION 466.5 LIMITATION 486.6 LEARNINGS 48

CHAPTER 7 RESULTS AND FINDINGS 49-52

CHAPTER 8 CONCLUSION AND RECOMMENDATIONS 53-54

8.1 RECOMMENDATIONS 538.2 KEY ISSUES AND CONCLUSIONS 53

APPENDIX 55-58

A.1: QUESTIONNAIRE 55A.2: LIST OF FIGURES 57A.3: BIBLOGRAPHY 58A.4: REFERENCES 58

VII Submitted by: -Rajendranath Behera

Regd no:-0706275024

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 9/61

INTRODUCTION

Whether it’s retiring early, saving for children’s education,

paying off a loan or to live a secured and satisfied life everyone has

dreams they can achieve by investing their savings. However, the

question that arises is that, should one leave his money tucked away

in the bank or plough it into the stock market where the potential for

higher returns is greater but the chances of losing money is higher?

Deciding where to invest depends on one`s att itude towards r isk

(one`s capacity to take risk and one`s tolerance towards risk) and the

inves tment hor izon and non-availabil ity of guaranteed-re turn

investment products.

In such a scenario, investing in equity, which offers returns that

are higher than the inflation rate, help to build wealth and to improve

the standard of living. It is fine that stock market fluctuates over

time. At present as far as the world economy is concerned it is on a

boom. As soon as globalization and liberalization has come into act it

has well shaped the economy. India has turned out to be the hot

destination for the money investors and this has resulted growth in the

sensex .It was never hoped before that BSE will ever touch the mark of 16000 points. But only due to the new economic opportunities and

the confidence of people in India’s economic future i t has been

successful .Investing in equity is the way to earn money and to fulfill

the dreams. The r isk involved with invest ing in equity can be

moderated by careful stock selection and close monitoring.

INVESTMENT AVENUES AND ALTERNATIVES

Investment alternatives vary from fixed income to variableincome which includes RBI bonds, government securit ies, f ixed

deposit, equity investments, property and so on.

In recent years the 6.5 percent tax-free RBI Bonds have become

a very popular saving instrument -- especially amongst individuals.

Till 1996, these bonds gave returns of 10 per cent. This came down to

9 per cent and then 8 percent and then in 2003 it was reduced to 6.5

per cent (tax free). Nowadays, 8 percent taxable Government of India

bonds are also doing well to attract investors who want safe and

higher yield.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 10/61

However, with inflation at nearly 4.5%, the return offered by

these instruments were still attractive. However, with the scrapping of

the tax-free bonds, safe investment options for individuals have

become very limited and people are now choosing to go wi th either

post office saving schemes or equity related instruments.

Take a look at what is happening. Debt funds, which were said

to be relat ively r isk-free, are giving very less returns. Monthly

Income Plans offered by mutual funds are also not attractive as their

portfolio is made up of 80 percent debt and 20 percent equity. Wi th

debt giving very less returns and returns from equity becoming

stagnant, the returns from MIPs are also very attractive. The returns

offered by MIPs are totally dependant upon the type of security anddebt instruments held by the fund But with recent rally in the stock

market , very few people are now going for MIPs and have a very

positive sentiment about the market and wou ld like to stay with the

market for long. But continuously we still have a single question in

mind:

So where should individuals park their money now?

"The 8 per cent taxable RBI Bonds seem to be one of the best options

right now looking for a safe avenues."

The person in the 30 percent tax bracket, the 8 per cent RBI

bonds wi ll give returns of approximately 5.6 per cent. Though this is

much lower than the previous 6.5 percent, it is still a better than most

other options. If you are a senior citizen, the Senior Citizens Savings

scheme offering a 9 Percent yearly interest is a good investment

option. The scheme was announced in the Budget 2006-2007 and wasmeant for people above the age of 60. However, this scheme has a

maximum deposit limit of Rs. 15 lacs while RBI Bonds do not have

any l imit . In this case, the term for deposit i s f ive years with a

facility for premature withdrawal. The 9 percent returns are subject to

tax, so if you are in the 30 percent tax bracket, you will effectively

get returns of 6.3 per cent.

Another option can be Floating Rate Bond Fund offered by

mutua l fu nds. Basica lly, these funds inves t in floa ting rat einstruments and therefore have a direct correlation to interest rates. If

interest rates go up the returns from these funds rise and returns fall

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 11/61

with a fall in interest rates. This is unlike debt funds, where there is a

reverse relat ionship between interest rates and returns. A r ise in

interest rates results in a fall in returns. In the current scenario, these

funds are likely to give retu rns of 5 per cent to 5.5 per cent.

The dividends are tax-free in the hands of the investor and most

importantly, there is complete liquidity. Again, there is no limit on

the amount that can be deposited. Also, there is hardly any volatility

making it a safe option. If you are willing to take a bit of risk, you

can divide your portfolio in such a way that 60 percent is invested in

float ing rate bond funds and the remaining 40 percent in equity.

That 's l ike having an MIP except that instead of 80 percent in debt

and 20 percent in equity, here the 60 percent is in floating rate bond

funds. Such a portfolio can give you returns of aprox. 8.5 % to 9.5 %.

The NSCs and the Kisan Vikas Patras give returns of 8 percent

so for those in the 30 percent tax bracket, it works out to 5.6 percent.

Here too there is no limit on the amount of deposit. However, here the

interest is posted only at the t ime of maturi ty . So i t is not a good

option if you want regular returns. On the other hand, RBI Bonds

give returns every six months or half yearly. So, depending upon

their risk profile and need for liquidity, one will have to decide ontheir portfolio. For anyone below 35 years, it is recommend that one

should invest some part of there portfolio in RBI Bonds and in NSCs,

KVPs as a long term investments and the remaining in combination of

f loat ing rate bond funds and equity But for those above 35, i t is

advocate that one should look at nearly 40 percent in RBI Bonds,

30 percent in NSCs, KVPs, hence giving safe and regular income.

And the remaining 30 per cent in floating rate bond funds and equity.

For those above the age of 60, 40 percent must be put in the Senior Citizens Scheme (of course, this is up to a maximum limit of Rs 15

lakh), another 40 percent in RBI Bonds and the remaining 20 percent

in f loat ing rate bond funds, so that one has some l iquidi ty.As an

investor one has a wide array of investment avenues available to one

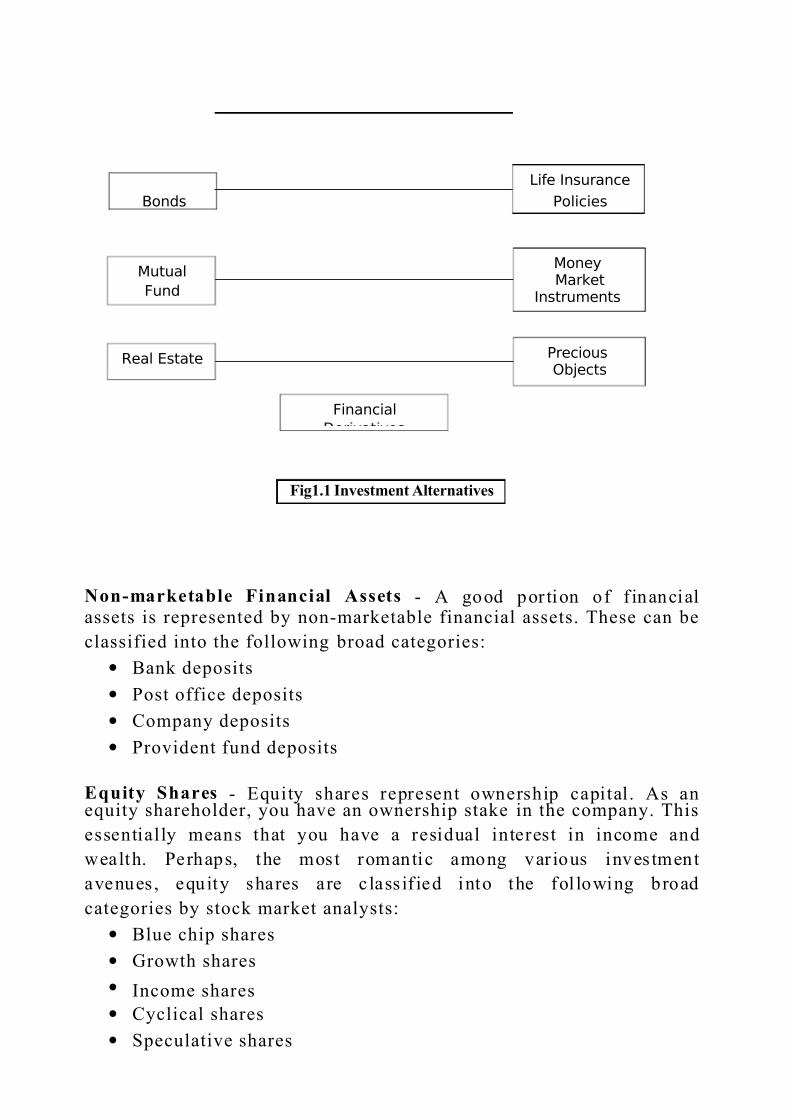

InvestmentAvenues

Equity SharesNon-

Marketable

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 12/61

Non-marketable Financial Assets - A good por tion of f inancialassets is represented by non-marketable financial assets. These can be

classified into the following broad categories:

• Bank deposits

• Post office deposits

• Company deposits

• Provident fund deposits

Equity Shares - Equity shares represent ownership capital. As anequity shareholder, you have an ownership stake in the company. This

essentially means that you have a residual interest in income and

wealth. Perhaps, the most romantic among var ious inves tment

avenues , equity shares are c lass if ied into the fol lowing broad

categories by stock market analysts:

• Blue chip shares

• Growth shares

• Income shares

• Cyclical shares

• Speculative shares

Fig1.1 Investment Alternatives

Bonds

MoneyMarket

Instruments

Mutual

Fund

Life Insurance

Policies

Real Estate PreciousObjects

Financial

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 13/61

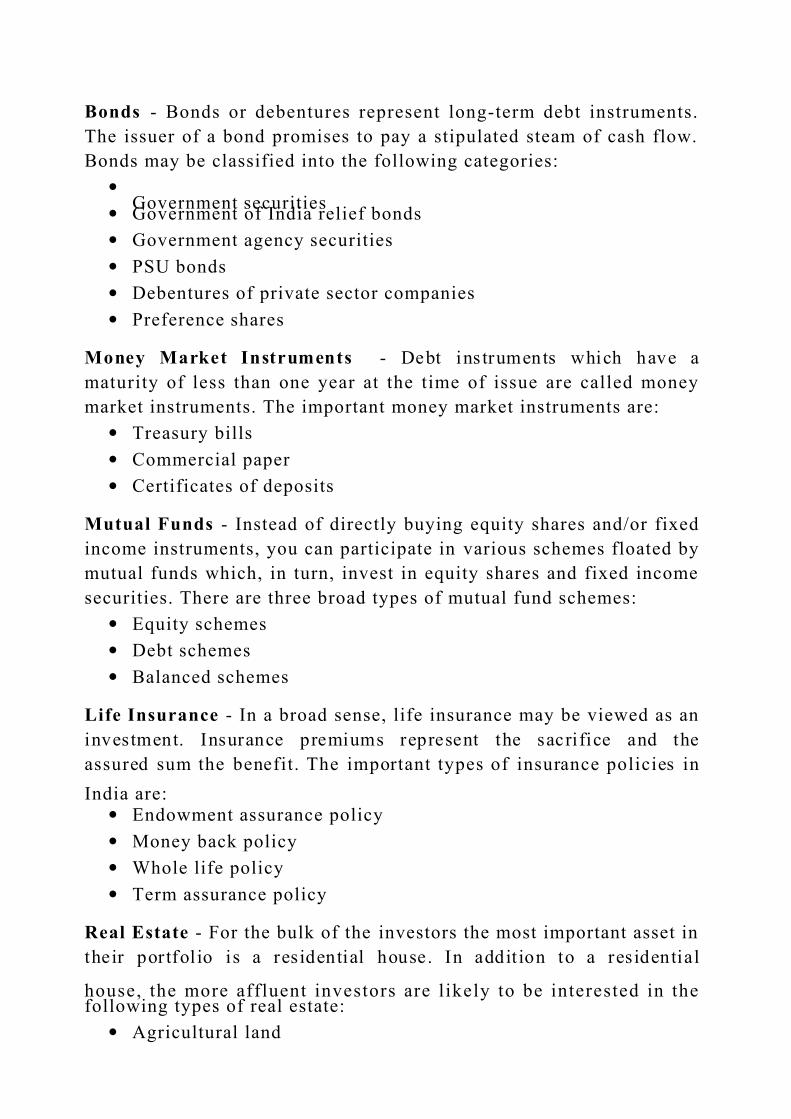

Bonds - Bonds or debentures represent long-term debt instruments.

The issuer of a bond promises to pay a stipulated steam of cash flow.

Bonds may be classified into the following categories:

•

Government securities• Government of India relief bonds

• Government agency securities

• PSU bonds

• Debentures of private sector companies

• Preference shares

Money Market Instruments - Debt ins truments which have a

maturity of less than one year at the time of issue are called money

market instruments. The important money market instruments are:

• Treasury bills

• Commercial paper

• Certificates of deposits

Mutual Funds - Instead of directly buying equity shares and/or fixed

income instruments, you can participate in various schemes floated by

mutual funds which, in turn, invest in equity shares and fixed income

securities. There are three broad types of mutual fund schemes:

• Equity schemes

• Debt schemes

• Balanced schemes

Life Insurance - In a broad sense, life insurance may be viewed as an

investment. Insurance premiums represent the sacrifice and the

assured sum the benefit. The important types of insurance policies in

India are:• Endowment assurance policy

• Money back policy

• Whole life policy

• Term assurance policy

Real Estate - For the bulk of the investors the most important asset in

their portfol io is a residential house. In addit ion to a residential

house, the more affluent investors are likely to be interested in thefollowing types of real estate:

• Agricultural land

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 14/61

• Semi-urban land

• Time share in a holiday resort

Precious Objects - Precious objects are items that are generally small

in s ize but h ighly valuable in monetary terms. Some impor tant

precious objects are:

• Gold and silver

• Precious stones

• Art objects

Financial Derivatives - A financial derivative is an instrument whose

value is derived from the value of an underlying asset . I t may be

viewed as a s ide bet on the asset . The most impor tant financialderivatives from the point of view of investors are:

• Options

• Futures

Since every indiv idual would l ike to earn return on the ir

investment but where to invest has always been a problem. There has

always been a confusion as to which instrument to invest, which

ins trument wil l give me higher returns , e tc . Even now nuclear f amil ies a re in and so are longer li fe spans . Even inflat ion is

increasing and so do the standard of life, medical costs, and other

things. In such a scenario, one need to think as to how he will take

care of all his future needs and build up a corpus that will not only

take care of routine expenses but a lso provide for ext ra cos ts ,

especially of health care. One need to have a corpus of funds, post-

ret irement, which wil l give h im close to 100% of the salary to

preserve the lifestyle he has grown to enjoy.

LITERATURE SURVEY

According to the Webster’s dictionary, literature is “the writings

that pertain to a particular branch of learning, and printed matter”.And review means “to examine again, to study carefully”.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 15/61

Therefore literature review is the printed matter which we study

very carefully during our work. This project is also a collection of

insight into the different printed material.

As this pro jec t i s speci fically related to sales of f inancial products hence books on investments is one of the study materials.

The insurance institute of India has published books which give

an insight into the l ife insurance products and general insurance

products.

The main source of data through which this project has taken its

shape is the c irculars of SEBI and IRDA. These c irculars give

description of existing market.

The knowledge about the marketing principles is gained from

the book “principles of marketing” written by Philip Kotler.

Chapter “positioning and marketing of services” of the “service

management and operations” published by prentice hall international

editions gives us the outline of marketing of services.

Chapter “Building Customer Satisfaction, Value and Retention”of “Marketing Management” written by Philip Kotler. Purpose of this

book is to provide background needed to understand the basics of

forming strong customer bonds and customer relationship

management.

Chapter on d is tr ibut ion channels in the book “marketing

channels” written by Louis W.stern & add I.E.I Ansary. Purpose of

thi s book i s to provide the de ta il ed knowledge about what is

distribution channel, its importance & role in marketing.

Chapter “The concept and role of mutual funds” of the AMFI

mutual fund testing programme by association of mutual funds in

India. This book provide concept of mutual funds.

The article “managing your Demat account” published in the

MINT dated June 18, 2007 page 12 give knowledge about Demat

account.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 16/61

Last but not the least , the pract ical experiences of rel iance

money has given the best ever exposure on the actually market works

in financial products and services.

SIGNIFICANCE OF STUDY

The need of the study arises because of the reason that a trainee

must understand the company, its achievements and tasks, products

and services and also to collect information about its competitors, its products and services offered. So that, aft er understanding and

collecting information about the organization and its competitors, a

trainee will be able to work well for the organization.

COMPANY PROFILE

Reliance Money is promoted by Reliance Capital; one of India's

l eading and fastes t growing priva te sec to r financial services

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 17/61

companies, ranking among the top 3 private sector financial services

and banking companies, in terms of net worth. Reliance Capital is a

part of the Reliance Anil Dhirubhai Ambani Group.

Thus, Reliance Money provides a comprehensive platform,offering an investment avenue for a wide range of asset classes. Its

endeavor is to change the way India transacts in financial market and

avails financial services. Reliance Money offers a single window

facility, enabling you to access amongst others, Equities, Equity and

Commodity derivatives, Offshore Investments, IPO’s, Mutual Funds,

Life Insurance and General Insurance products.

Advantages offered by Reliance money over other companies:

• Cost Effective

• Convenience

• Security

• Single Window for Multiple Products

• 3 in 1 Integrated Access

• Demat Account with Reliance Capital

•

Other Services like research, live news from Reuter and DowJones, etc.

PRODUCT OFFERING

1. Trading Portal (with almost negligible brokerage )

• Equity Broking

• Commodity Broking

• Derivatives ( Futures & Options )

• Offshore Investments (Contract For Differences)• D-Mat Account.

2. Financial Products

• Mutual Funds

• Life Insurance

o ULIP plan

o Term Plan

o Money Back Plan

• General Insurance

o Vehicle/Motor Insurance

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 18/61

o Health Insurance

o House insurance

• IPO’s

• NFOs3. Value-Added Services

• Retirement Planning

• Financial Planning

• Tax Saving

• Children Future Planning

4. Credit Cards

5. Gold coins retail ing

TRADING PORTAL

Online trading refers to buying and selling of the

shares/stocks/contracts/bonds with the use of internet. In this shares

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 19/61

are not issued in physical form rather they are t ransferred in the

dematerialized form in the Demat account directly.

DEMAT ACCOUNT

In India, a Demat account , the abbreviation for dematerialized

account, is a type of banking account which dematerializes paper-

based physical stock shares. The dematerialized account is used to

avoid holding physical shares: the shares are bought and sold through

a broker . This account i s popular in India . The Securities and

Exchange Board of India (SEBI) mandates a Demat account for

share tr ad ing above 500 shares. As o f Apr il 2006, i t became

mandatory that any person holding a Demat account should posses a

Permanent Account Number (PAN), and the deadline for submissionof PAN details to the depository lapsed on January 2007.

What are the benefits of opening a Demat account?

Demat account has become a necessity for all categories of investors

for the following reasons/ benefits:

• SEBI has made it compulsory for trades in almost all scrip’s

to be set tled in Demat mode. Although, t rades up to 500shares can be settled in physical form, physical settlement is

virtually not taking place for the apprehension of bad delivery

on account of mismatch of signatures, forgery of signatures,

fake certificates, etc.

• It is a safe and convenient way to hold securities compared to

holding securities in physical form..

• No stamp du ty is levi ed on transfer of securities held in

Demat form.

• Instantaneous transfer of securities enhances liquidity.

• I t e liminates delays, thefts, interceptions and subsequent

misuse of certificates.

• Change of name, address, registration of power of attorney,

delet ion of deceased 's name, etc . - can be effected across

companies by one single instruction to the DP.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 20/61

• Each share is a market lot for the purpose of transactions - so

no odd lot problem.

Any number of securities can be transferred/delivered with one

delivery order. Therefore, paperwork and signing of multiple transfer

forms is done away wi th . I t fac il itates tak ing advances against

securities on low margin/low interest.

DEMAT ACCOUNT

There are many broking houses doing business in

India and they charge a brokerage on every transactionmade online or offline. (Buying and Selling are treated as

separate transaction). Reliance Money’s advantage over

others is that it’s charging the lowest brokerage in the

market which is just 1 paisa on every executive trade

irrespective of the volume traded. Reliance Money, the

brokerage and distribution arm of Reliance ADA Group,

aims to tap investors in the smaller towns and cit ies

through a flat fee structure. The current leaders in theretail broking segment like ICICI Direct, India Infoline and

Indiabulls offer a ‘pay per use’ model where the customer

pays a percentage of the amount transacted by him.

Reliance Money’s brokerage rates are quite competitive.

The new wonder is Reliance Money's pre-paid card for stock

market brokerage. Reliance Money, the financial services division of

Anil Dhirubhai Ambani Group-promoted Reliance Capital, is bringingto the market pre-paid cards in denominations of Rs500, Rs1,350 and

Rs2,500 with validity period of two months, six months and twelve

months respectively.

These cards would offer brokerage at one-third of the rate being

charged by institutional and individual brokerage houses. Sample this.

For a pre-paid card worth Rs500, an investor can trade up to Rs90

lakh in futures and option segment or can undertake intra-day trade of similar amount. Besides, an investor can undertake a delivery-based

activity of Rs10 lakh.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 21/61

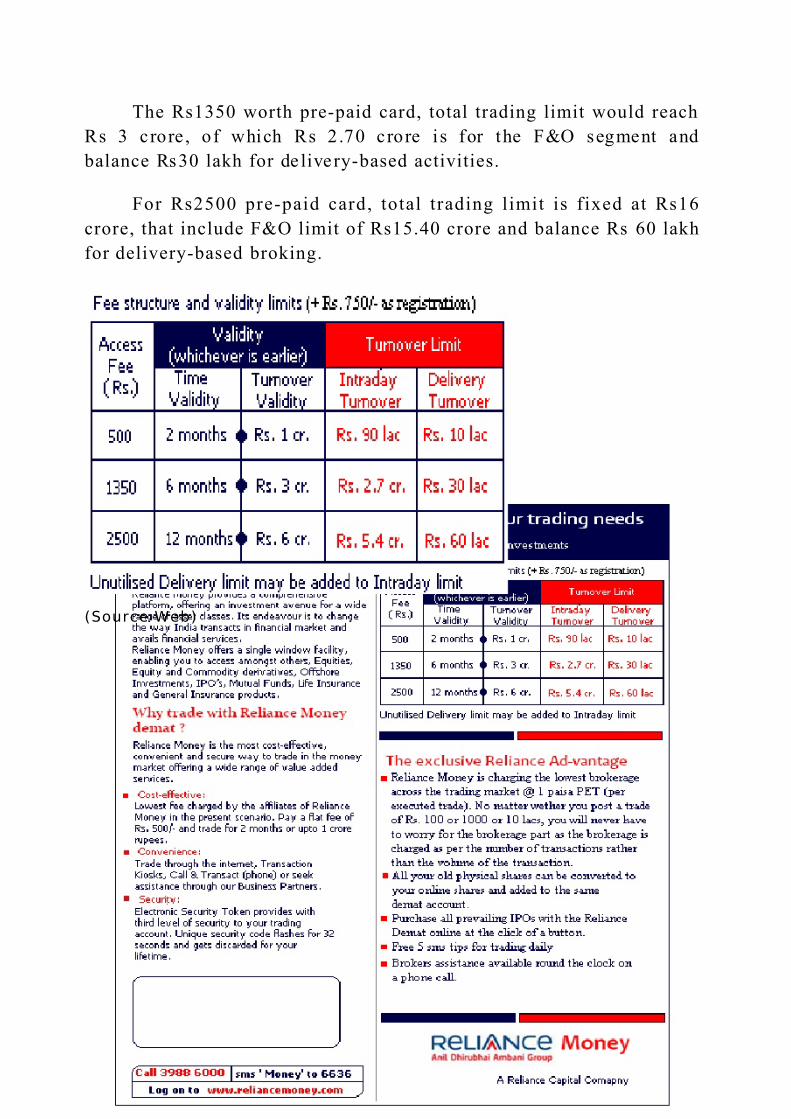

The Rs1350 worth pre-paid card, total trading limit would reach

Rs 3 crore , of which Rs 2 .70 crore i s for the F&O segment and

balance Rs30 lakh for de live ry-based activities.

For Rs2500 pre-paid card, total trading limit is fixed at Rs16

crore, that include F&O limit of Rs15.40 crore and balance Rs 60 lakh

for delivery-based broking.

(Source Web)

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 22/61

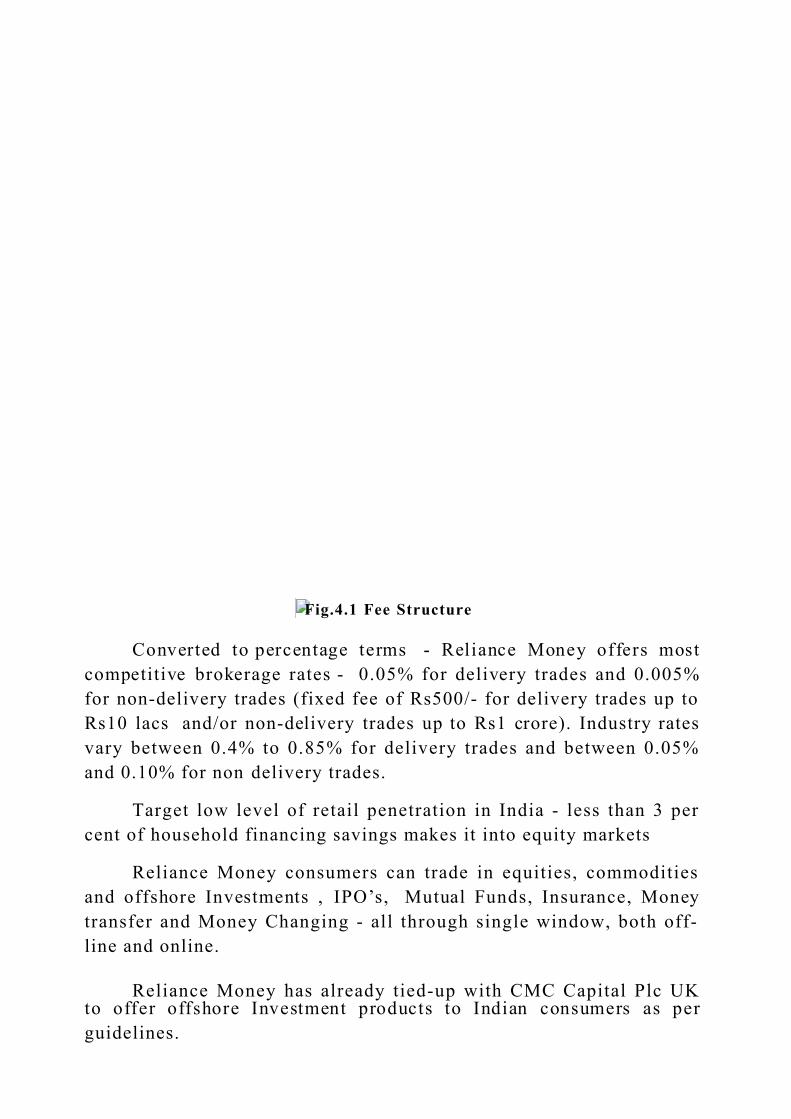

Fig.4.1 Fee Structure

Converted to percentage terms - Reliance Money offers most

competitive brokerage rates - 0.05% for delivery trades and 0.005%

for non-delivery trades (fixed fee of Rs500/- for delivery trades up to

Rs10 lacs and/or non-delivery trades up to Rs1 crore). Industry rates

vary between 0.4% to 0.85% for delivery trades and between 0.05%

and 0.10% for non delivery trades.

Target low level of retail penetration in India - less than 3 per

cent of household financing savings makes it into equity markets

Reliance Money consumers can trade in equities, commodities

and offshore Investments , IPO’s, Mutual Funds, Insurance, Money

transfer and Money Changing - all through single window, both off-

line and online.

Reliance Money has already tied-up with CMC Capital Plc UK to offer offshore Investment products to Indian consumers as per

guidelines.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 23/61

How reliance money scored over others?

1. Two way authentication: Reliance offers its customers with

a token (an electronic gadget) that generates a password, which

are a third level of security in addition to the customer log in and

a password provided. The password generated by the token is

valid only for a period of 20 seconds. If the web page expires,

for the fresh login, a new password generated by the token has to

be keyed in by the customer.

2. Lowest brokerage: Reliance offers the lowest brokerage of

1 paisa which is very less with respect to the other DPs in the

market.

3. User friendly software: The portal offered is very easy to

understand and use.

4. Forex and offshore investment : Reliance provides the

offshore facility which no other AMC is providing in the market.

5. Better research and news: Reliance offers news from the

DOW JONES and REUTERS.

Seeking to bring share trading closer to consumers just l ike

ATMs, Reliance Capital's stock brokerage arm Reliance

Money launched Internet trading services through web-enabled retail

kiosks.

Monday, April 16, 2007

Reliance Money launches Internet trading through kiosks

NEW DELHI: Seeking to bring share trading closer to consumers just like ATMs,Rel i ance Cap i ta l 's s tock b rokerage a rm Rel i ance Money on Monday l aunchedInternet trading services through Web-enabled retail kiosks.

Becoming the f irs t Indian company to provide share trading through Web-enabledre ta i l k iosks , Ani l Dhirubhai Ambani Group f i rm sa id i t p lans to deploy 10 ,000such kiosks across the country, for which it is also talking to various retail chains.

"These Internet enabled kiosks wil l provide the users anytime-anywhere access toReliance Money 's f inancia l t ransaction por ta l th rough which they can inves t invarious f inancial ins truments in a secure environment", Mr. Sudip Bandyopadhyay,CEO, Reliance Money said.

In i ts f irs t phase, the kiosks would be operational at the retai l outlets of RelianceMoney, which had commenced operations last week across 700 cities. The kiosks atvarious retail chains would be launched in the subsequent phases.

The company has t ied up with Wincor Nixdorf , a leading global provider of retai l banking IT solution with net revenues of $1.4 bi llion and presence in 90 countries,

for these kiosks.

Winco r-Nixdorf ' s APAC Re ta i l Head , Mr . Andrew Phay s aid , "We s ee g rea t potential for our products in the country owing to the retai l boom and will continueto introduce latest products for our customers here."

The company said this would be biggest ever deployment of Internet enabled retai lkiosks by any company across the world. - PTI

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 24/61

(Source: Web)

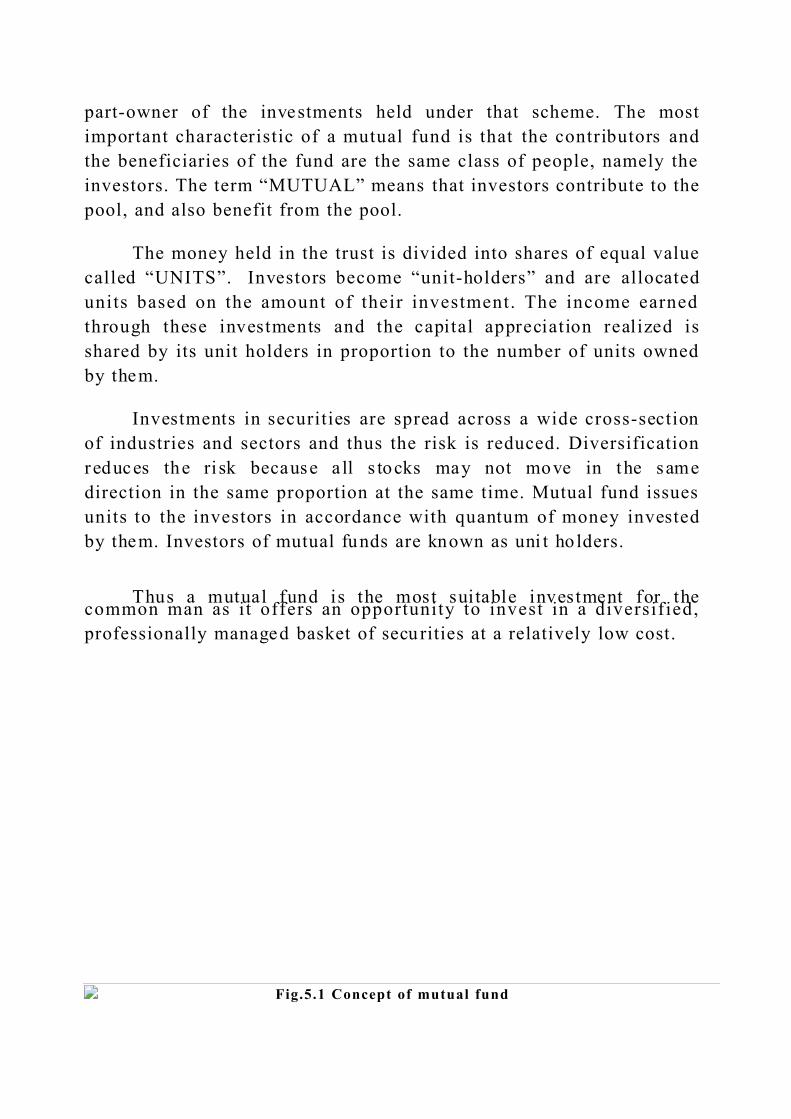

FINANCIAL PRODUCTS

A mutual fund represents a vehicle for collective investment.

When you participate in a scheme of a mutual fund, you become a

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 25/61

part-owner of the investments held under that scheme. The most

important characteristic of a mutual fund is that the contributors and

the beneficiaries of the fund are the same class of people, namely the

investors. The term “MUTUAL” means that investors contribute to the

pool, and also benefit from the pool.

The money held in the trust is divided into shares of equal value

called “UNITS”. Investors become “unit-holders” and are allocated

units based on the amount of their investment. The income earned

through these investments and the capital appreciation realized is

shared by its unit holders in proportion to the number of units owned

by them.

Investments in securities are spread across a wide cross-section

of industries and sectors and thus the risk is reduced. Diversification

reduces the ri sk because a ll s tocks may not move in the same

direction in the same proportion at the same time. Mutual fund issues

units to the investors in accordance with quantum of money invested

by them. Investors of mutual funds are known as uni t ho lders.

Thus a mutual fund is the most sui table investment for thecommon man as it offers an opportunity to invest in a diversified,

professionally managed basket of secu rities at a relatively low cost.

Fig.5.1 Concept of mutual fund

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 26/61

The shift in investor preference towards mutual funds has been

facilitated by:

• Fiscal incentives

• Increasing returns from debt mutual fund investments in the last

few years due to the secular decline in interest rates

• The growing number of choices available to investors

• The gradual change in the investors’ risks profile and returns.

Open end versus Closed end Schemes

There are two different types of funds.

• Open-ended Fund/ Scheme

• Closed-ended fund/ Scheme

The key differences between the closed-end and open-end schemes

area as follows:-

The subscription to a closed-end scheme is kept open only for a

limited period (usually one month to three months). Where an open-end scheme accepts funds from investors by offer ing i ts units or

shares on a continuing basis.

A closed-end scheme does not allow investors to withdraw funds

as and when they like, whereas an open-end scheme permits investors

to wi thdraw funds on a con tinu ing basi s under a re -purchase

arrangement.

A closed-end scheme has a fixed maturity period (usually five tofifteen years) whereas an open-end scheme has no maturity period.

The closed-end schemes are listed on the secondary market,

whereas the open-end schemes are ordinarily not list.

In India, three entities are central to a mutual fund operation:

• The sponsor,

•

The mutual fund• The asset management company.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 27/61

The sponsor is the key who establishes the mutual fund and the

asset Management Company. For example, Templeton International

( sponsor ) set up the Temple ton Mutual Fund which has been

constituted as a trust under the Indian Trusts Act, 1882 and registered

with SEBI. The mutual fund is, in a way, an umbrella organization

that floats various schemes in which investors participate. The asset

management company, organized as a separate joint Stock company,

manages the funds of mutual fund under its various schemes. For

example, Templeton Asset Management (India) Pvt. Ltd., the asset

management company set up by Templeton International, manages the

various schemes of Templeton Mutual Fund.

Why one should invest in mutual funds?

Mutual funds are preferable mode of investment due to the following

reasons:

• Reduction of risk

• Professional Management

• Tax benefits

• Low transaction costs

• Highly regulated

• Liquidity

• Easy to administer

Why one should not invest in mutual funds?

The following are the reasons, which are deterrent to mutual fund

investment:

• No control over costs

• No tailor made portfolios

• Managing a portfolio of funds

Constitution of a Mutual Fund

There are a number of bodies that form a part of the mutual fund, they

are as follows:

• Sponsors

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 28/61

The sponsor is the company which sets up the mutual fund. It means

anybody corporate acting alone or in combination with another body

corporate established a mutual fund after initiating and completing

the formalities.

• Trustees

The management of the mutual fund is subject to the control of the

board of trustees of the fund. They guide the operations of the fund

and carry the crucial responsibility to see that AMC always act in the

best interest of the inves tors .

• Asset Management Company

The mutual fund is operated by a separately established assetmanagement company (AMC).It manages the funds of the various

schemes. It is entrusted with the specific task of mobilizing funds

under the scheme.

• Custodian

A custodian is a person carrying on the activities of the safekeeping

of the securities or participating in any clearing system on behalf of

the clients to effect deliveries of the securities.

Types of Mutual Funds

There are different ways of classifying mutual funds:

• An EQUITY FUND invests mainly in s tocks and shares of

companies. EQUITY FUNDS typically aim to generate long term

growth in the unit capital. There are a variety of ways in which

an equity portfolio can be created for investors. There are thusthe following choices in equity funds:

o Simple equity funds

o Industry Specific funds

o Index funds

o ELSS

Target market:

They are idea l for inves tor s having a long term perspec tive ,

Speculative outlook- the equity cult, who would like to make gains in

the shortest period of time and investors in their prime earning years-

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 29/61

specifically the young who have a decent earning and can take some

kind of risk.

• A DEBT FUND invests mainly in debt instruments like bondsand debentures, with high and consistent dividend payout. These

funds give decent returns but the capital appreciation is not

much. There are a variety of ways in which a debt portfolio can

be created for inves tors. There are thus the fol lowing cho ices in

debt funds:

o Liquid and Money market funds

o Gilt Funds

o Monthly Income Plano Floating rate funds

Target market:

o Retired people and others with a need for stability and regular

income.

o Investors who need some income to supplement their earnings.

• A BALANCED FUND invests in both equity and debt

instruments. It aims to generate growth and income by

per iodically distributing its assets over both types of secu rities .

Target market:

These ideal for investors looking for a combination of income and

moderate growth.

How to invest in mutual funds?

The fol lowing are the essential s teps which one must take into

account while investing in Mutual funds:-

Step 1- Identify the investment needs

Financial goals of an individual wil l vary, based on his/her age,

l ifestyle , f inancial independence, family commitments , level of

income and expenses among many other factors. Therefore the first

step is to assess one’s needs, which can be done by asking oneself

these questions:

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 30/61

Q1.What is my investment objectives and needs?

Q2.How much risk I am willing to take?

Q3.What is my cash flow requirements?

By going through such an exercise, one will know what one wants out

of his investment and can set the foundation for a sound mutual

fund investment strategy.

Step 2-Choose the right mutual fund

Once an individual has a clear strategy in mind, he now has to choose

which mutual fund and scheme he wants to invest in. The offer

document of the scheme tells its objectives and provides

supplementary detail like the track record of other schemes managed by the same fund manager. Some factors to eva luate before choosing a

particular mutual fu nd are:

• The track record of the performance over the past few years

in relation to appropriate yardstick and similar funds in the same

category.

• How well the fund is organized to provide efficient, prompt and

per sonalized service.

• Degree of transparency as reflected in frequency and quality of

their communications.

Step 3-Select the ideal mix of schemes.

Investing in one mutual fund may not meet all the investment needs.

One may consider investing in a combination of schemes to achieve

the specific goals.

Step 4- Invest regularly

For most of us, the approach that works best is to invest a f ixed

amount at specific intervals, say every month. By investing a fixed

sum each month one buys fewer units when the price is higher and

more units when the price is low, thus bringing down the average cost

per unit. This is called Rupee cost aver aging and is a disciplined

investment strategy followed by investors all over the world.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 31/61

Step 5-Keep the taxes in mind

If an individual comes under the high tax bracket and has util ized

ful ly the exemptions under Section 80L of the income tax act ,

investing in mutual funds will improve his return.

Step 6-Start early

It is desirable to sta rt i nvesting early and stick to a regul ar

investment plan. If one starts now .he will make more than if he waits

and invests later. The power of compounding lets one earn income on

income and one’s money multiplies at a compounded rate of return.

Step 7-The final Step

All one needs to do now is to get in touch with a mutual fund or one’sagent and start investing. Reap the benefits in the years to come.

Mutual funds are suitable for ever kind of investor-whether starting a

career or retiring, conservative or risk taking, growth oriented or

income seeking.

Nature of Income Distribution to Investors

At a broad level, the investors have three options:

• DIVIDEND PAY OUT OPTION

In this option investors receive dividends from the mutual fund, as

and when such dividends are declared. Dividends are paid in the form

of warrants, or are directly credited to the investor’s bank accounts.

• GROWTH OPTION

Investors who do not require periodic income distributions can choose

the growth option, where the incomes earned are retained in theinvestment por tfo lio, and a llowed to grow, rathe r than being

distributed to the investors.

• RE-INVESTMENT OPTION

In this option investors re invest the dividends that are declared by

the mutual fund, back into the fund itself, at NAV that is prevalent at

the time of reinvestment .In this option, the number of units held by

the investor will change with every reinvestment. The value of the

units will be similar to that under the dividend option.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 32/61

Different schemes of Reliance Mutual fund

The different schemes offered to various kinds of investors by

Reliance mutual fund can be broadly classified into three categories –

Equity, Debt and sec tor speci fic. Each of these categor ies has

different investment objectives and therefore has different portfolio.

Equity Schemes

• Reliance Growth Fund

• Reliance Vision Fund

• Reliance NRI Equity Fund

• Reliance Equity Opportunities Fund

• Reliance Index Fund• Reliance Tax Saver Fund

• Reliance Equity Fund

Debt Schemes

• Reliance Income Fund

• Reliance Medium Term Fund

• Reliance Short Term Fund

•

Reliance Liquid Fund• Reliance Monthly Income Plan

• Reliance Gilt Securities Fund

• Reliance Floating Rate Fund

• Reliance NRI Income Fund

Sector Specific Schemes

• Reliance Banking Fund

• Reliance Pharma Fund

• Reliance Media and Entertainment Fund

• Reliance Diversified Power Sector Fund

As I was more involved in the understanding and promotion of the

NFO of Reliance Equity Fund during the initial part of my training. I

would like to summarize it in brief.

Reliance Equity Fund

The Reliance Equity Fund is an open ended diversified equity

fund that seeks to provide long term capital appreciation by investing

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 33/61

in a portfolio constituted of equity and equity related securities of top

100 companies by market capitalization and of companies that are

available in derivatives segment, belonging to diverse sectors.

The investment strategy being that even if the markets go down,

the fund has a part of its portfolio hedged, which aims at minimizing

the downside risk. The fund will not only use hedging techniques to

limit the downside risk but will also try & capitalize on short selling

opportunities to generate additional returns for the investors. The

fund will invest 75-100% in equity and equity related instruments and

0-25% in debt and money market securities. In a nut shell what this

fund tries to do:

• Generate long term returns by invest ing in a dive rs ifi ed

portfolio of stocks .

• Minimize the downside risk by being in a hedged position

• Capitalize on generating additional returns by selective shorting.

"Insurance is a contract between two parties whereby one party called insurer undertakes in exchange for a f ixed sum called premiums, to

pay the other party called insured a fixed amount of money on the

happening of a certain event."

Reliance Life Insurance is an associate company of Reliance

Capital Ltd., which along with i ts associates has acquired 100%

shares in AMP Sanmar Life Insurance Co Ltd. Rel iance Life

Insurance, has a pan presence and a range of products catering to

individual as well as corporate needs. A total of 16 products covering

savings, protection & investment requirements.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 34/61

Vision : Empowering everyone live their dreams

Mission: Create unmatched value for everyone through dependable,

effective, transparent and profitable life insurance and pension plans

• Guiding Principles

• Customer Care and Satisfaction

• Corporate Governance

• Creativity and Innovation

• Competitiveness

NEED FOR LIFE INSURANCE

• Protection of the interest of the faculty of the loss of income due

to death of the breadwinner.

• Provision for the education & marriage of children.

• Post retirement income for self & dependents.

• Special needs like loss of income due to disabilities, accidents,

treatment of diseases, sickness etc.

• To protect against inflation.

Who Can Buy A Policy?

Any person who has attained majority and is eligible to enter

into a valid contract can insure himself/herself and those in whom

he/she has insurable interest. Policies can also be taken, subject to

certain conditions, on the l ife of one 's spouse or children. While

underwriting proposals, certain factors such as the policyholder’s

state of health, the proponent's income and other relevant factors are

considered by the Corporation.

Insurance for Women

Prior to na tional izat ion (1956), many pr iva te insurance

companies would offer insurance to female lives with some extra

premium or on restrictive conditions. However, after nationalization

of life insurance, the terms under which life insurance is granted to

female l ives have been reviewed from t ime-to-time. At present ,

women who work and earn an income are treated at par with men. Inother cases, a restrictive clause is imposed, only if the age of the

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 35/61

female is up to 30 years and if she does not have an income attracting

Income Tax.

Medical and Non-Medical Schemes

Life insurance is normally offered after a medical examination

of the l ife to be assured. However, to facil itate greater spread of

insurance and also to avoid inconvenience, Companies has been

extending insurance cover without any medical examination, subject

to certain conditions.

With Profit and Without Profit Plans

An insurance policy can be 'with' or 'without' profi t . In theformer, bonuses disclosed, i f any, after periodical valuat ions are

allot ted to the policy and are payable along with the contracted

amount. In 'without' profit plan the contracted amount is paid without

any addition. The premium rate charged for a 'with' profit policy is

therefore higher than for a 'without' profit policy.

Keyman Insurance

Keyman insurance is taken by a business firm on the life of keyemployee(s) to protect the firm against financial losses, which may

occur due to the premature demise of the Keyman.

Tax Benefits of Insurance

The tax breaks that are available under our various insurance and

pension po lici es are described below:

• Life insurance plans are eligible for deduction under Sec. 80C.

• Pension plans are eligible for a deduction under Sec. 80CCC.

• Health insurance plans/riders are eligible for deduction under

Sec. 80D.

• The proceeds or withdrawals of our life insurance policies are

exempt under Sec 10(10D), subject to norms prescribed in that

section.

Unit Linked Insurance Plan

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 36/61

ULIPs have been selling like proverbial ‘hot cakes’ in the recent

past and they are likely to cont inue to ou tsell thei r plain vanilla

counterparts going ahead. Earlier there were a gamut of traditional

products, for instance Endowment Plans ; Money back plans etc, then

came the concept of Unit Link Insurance Plans, which today has

caught the fancy of many people.

Unit Link plans work like a combination of Mutual Funds and

Life Insurance, just like in Mutual Funds the Investment here is also

broken up into units based on the current NAV, these products are

termed as Unit Linked plans because the Investment is broken up into

units.

For instance if you were to invest Rs10000, it would be broken into 3

components:

• Charges- These are charges that the Insurance Company deducts

from your premium, a major chunk of charges goes into paying

commission to the Agent for sourcing the business.

• Mortality- Expense- Mortality expenses are not as high as agent

commission; they approximately tend to be around Rs100/Lakh

for a 30 yr o ld man. In case of a death c laim of 1 lakh, the

insurance company can make this claim with a mere Rs100

deducted from you, now this is made possible because mortality

charge is deducted from every customer who has invested in the

plan. In this manner the Insurance Company collects a

substantial portion and not every person dies at the same time

leading to only a few claims in a single year.

• Investment – After the above 2 deductions , the ba lance isinvested on behalf of the customers, so in reality if the current

NAV is 10, and a customer has paid a premium of 10 ,000, then

allotment of uni ts would be 10,000 – (charges + Mortali ty

expense) current NAV . The same process is repeated in the

fol lowing years when premiums are pa id however in the

following years the charges tend to be lower as insurance charge

lesser after the 1 s t year. Mortality Cost however goes up with

age but does not increase substantially for a younger person inhis 20’s or 30’s as a result of which the money allotted towards

Investment goes up.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 37/61

Unit Link plans give the flexibility to withdraw your investments

earlier than Traditional Plans, but withdrawals can decrease the

Insurance cover you have opted for. The other thing to keep in mind

is the tax implication of making early withdrawals, from the returns

point of view Unit link plans give you a chance of choosing you r own

Investment Opt ions , which could be Debt , Equity or Balanced

(combination or both) whereas tradit ional plans have primarily

invested in debt instruments like Govt. Bonds where the security is

ensured but returns may not be very high.

Unit link plans also give a greater amount of flexibility in terms of

your policy not lapsing if premium in a year or two is not paid. The

other interesting option that these plans offer is the choice to decideyour own Insurance cover in the beginning. Flexibility wise Unit Link

plans definitely score over traditional plans ; even they tend to be

more transparent.

Claims

In case of Critical i l lness, Total and permanent disability or

Death claim please log the claim and submit listed documents either

directly to the Claims department, Chennai or at any of the nearest branch.

Register the Claim under:

• Death

• Critical Illness

• Disability

Survival or Maturity Benefits

Survival Benefits: Survival benefits are those payments which

are paid during the term of the policy. The frequency of payment may

vary from product to product.

Maturity Benefits: Payment made at end of the policy term as

shown in policy documents .

Documents required for death claim

• Claim form A: This form need to be fil led by the nominee or

claimant

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 38/61

• Claim form B - Certificate of last illness to be filled, signed and

stamped by the doctor in attendance during the last illness of the

deceased life assured.

•

Original Policy Documents• Original death certificate by Death and Birth Registrar

• Death certificate by the doctor confirming cause of death

• Nominees photo identification card copy attested by Insurance

company official.

• All hospital reports, if hospitalized during the last sickness

• Post Mortem Report and Viscera report, if performed

In case of accident or suicide

• First Information Report and final Police Investigation Report

• Panchnama /Inquest report

• News paper report on the acc ident wi th pho tographs, if available

Documents required for Total & permanent disability claim

• Claim forms (A & B)

• All hospital reports (certificate of diagnosis, attended physician

report, discharge summary, first consultation notes etc)

• Original policy document

• FIR and Police Investigation Report

• News paper report on the acc ident

• Panchanama or Inquest Report

PLANS

Individual Plans Product Name Description

Reliance

Automatic

Investment

Plan

A s ma rt p la n w hi ch a da pt s t o y ou r c ha ng in g r is k p ro fi le w it h

increasing age.

Reliance

Money

Guarantee

Plan

Under th is p lan the inves tment r i sk in the inves tment por t fo l io i s

borne by the policyholder.

Reliance

Endowment Plan

This p lan wi ll keep you f inanc ial ly p repa red for a l l t he s pec ial

occasions in your life.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 39/61

Reliance

Special

Endowment

Plan

This insurance policy is designed for people who wish to combine

savings with extended security.

Reliance

Cash Flow

Plan

This insurance pol icy is des igned for those who have a recur r ing

need for reinvestment in business or look for short- term investment

channels.

Reliance

Child Plan

This ins u rance po li cy i s designed fo r peop le who wish to s ave

money for a future time.

Reliance

Term Plan

This insurance policy is designed for those who only want life cover

for the p ro tec tion o f thei r f ami ly , and do not wish to s ave for

themselves.

RelianceWhole Life

Plan

This insurance pol icy is des igned for people who do not wish to

avai l o f any benef i t s themselves bu t wish to crea te an immedia teestate to protect their family by avail ing of insurance cover on their

life at a very low cost.

Reliance

Market

Return Plan

Reliance Market Return Fund is the unit- l inked product that helps

you invest in the f inancial markets in a combination of investment

instruments of your choice.

Reliance

Golden Years

Plan

Rel iance Go lden Year s P lan i s a f l ex ible package tha t p rov ides

f reedom of choice in choos ing the type of inves tment , l i fe cover ,

vesting options such as commuting and annuity options.

RelianceSimple Term

Plan

Reliance Simple Term Plan is a cost-effective, pure l ife insurance plan that offers you comprehensive and affordable coverage for a

limited period of time to suit your needs.

Reliance

Special Term

Plan

Reliance Special Term Plan is a pure l ife insurance plan that offers

you comprehensive and affordable coverage for a l imited period of

time to suit your needs.

Reliance

Credit

Guardian

Plan

Rel iance Credi t Guardian P lan ens u res tha t your hous ing loans,

personal loans or even outs tanding credit card bil ls are paid in the

e ve nt o f u nt im el y d em is e. T hu s k ee pi ng y ou a nd y ou r f am il y

protected from the burden and the worry of debt in such a si tuation.Reliance

Special

Credit

Guardian

Plan

Rel iance Specia l Credi t Guard ian Plan helps you and your family

avoids such s i tua t ions by secur ing your hous ing loans , personal

loans and even credit card payments. What makes the Plan special is

the fac t tha t on surv iva l a t matur i ty , a l l p remiums paid for your

basic policy will be returned to you.

Reliance

Connect 2

Life Plan

Reliance Connect 2 Life Plan helps you build securi ty and savings

for a better tomorrow.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 40/61

Employee Benefit Plans

Product Name Description

Reliance Group

Term Assurance

Policy

R el ia nc e G ro up T er m A ss ur an ce P ol ic y i s a o ne y ea r

Renewable Term Assurance contract . The benefi t is payable

on the happening of the contingency during one year . At the

end of the year, the contract may be renewed.

Reliance EDLI

Scheme

A ll e st ab li sh me nt s w it h a t l ea st 1 0 f ul l- ti me p er ma ne nt

employees and to whom the Employee' s Provident Fund and

Miscellaneous Provis ions Act, 1952 applies , have a s tatutory

liabil i ty to subscribe to Employee's Deposit Linked Insurance

Scheme (EDLI ), to p rov ide for l i fe ins u rance fo r a l l t hei r

employees.

Reliance GroupGratuity Policy A gra tu i ty po l icy tha t ref lec ts your company 's iden t i ty andwhich highlights the value of the benefi ts you provide to your

employees.

Reliance Group

Superannuation

Policy

A superannuation policy that ref lects your company's identi ty

and which highlights the value of the benefi ts you provide to

your employees.

Fundamentals of General Insurance companies are business

houses. The product they sell is financial protection. To succeed andsurvive, they must cover their costs, which include payments to cover

the losses of policyholders , as well as sales and administrative

expenses, taxes and dividends. Insurance companies have two sources

of income for covering these costs: premium and investment income.

The premium are co llec ted on a regu lar bas is and invested in

Government Bonds, Gift stocks, mutual funds, real estates and other

conservative avenues. However, investment income depends on

market conditions, interest rates, economy etc and varies from year toyear. Because of the uncertainty associated with the investment

income, insurance companies must generate enough income form

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 41/61

premium to cover the bulk of their expenses. The pr imary function of

insurance is to provide protection against financial losses caused by

unforeseen events. This pro tect ion is available to indiv iduals ,

businessmen and large companies alike.

Types of General Insurance

Health

• Individual Mediclaim

• Group Mediclaim

• Reliance Health Wise Policy

Personal Accident• Personal Accident

• Group Personal Accident

Fire

• Standard Fire and Special Perils

• Consequential Loss (Fire)

• Industrial All Risks

Engineering

• Erection All Risks/Storage-cum-Erection

• Contractor’s All Risks

• Contractor’s Plant and Machinery

• Machinery Breakdown Insurance

• Machinery Loss of Profits Insurance

• Boiler and Pressure Plant Insurance

• Electronic Equipment Insurance

Marine

• Marine Cargo Insurance

Motor

• Private Car Comprehensive

Liability

• Directors and Officers Liability• Public Liability (Act)

• Public Liability

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 42/61

• Product Liability

• Professional Indemnity

• Workmen’s compensation

Miscellaneous

• Industry Care

• Commercial Care

• Office Package

• Fidelity Guarantee

• Burglary and Housebreaking

• Money Insurance

• Householder’s Package

• Shopkeeper’s Package

Travel

• Individual and Family

• Asia

• Student

• Corporate

BASIC FEATURES

• Hospitalization Expenses

• Daycare Treatment

• Domiciliary Hospitalization

• Pre and Post Hospitalization

• Coverage of Pre-Existing Diseases

• Critical Illness Cover

• Donor Expenses

VALUE ADDED FEATURES

• Expenses of accompanying person at the Hospital

• Local Road Ambulance Services

• Recovery Benefit

• Cost of Health Check up

• Nursing Allowance

• Hospital Daily Allowance

POLICY FEATURES

• Income Tax Benefit

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 43/61

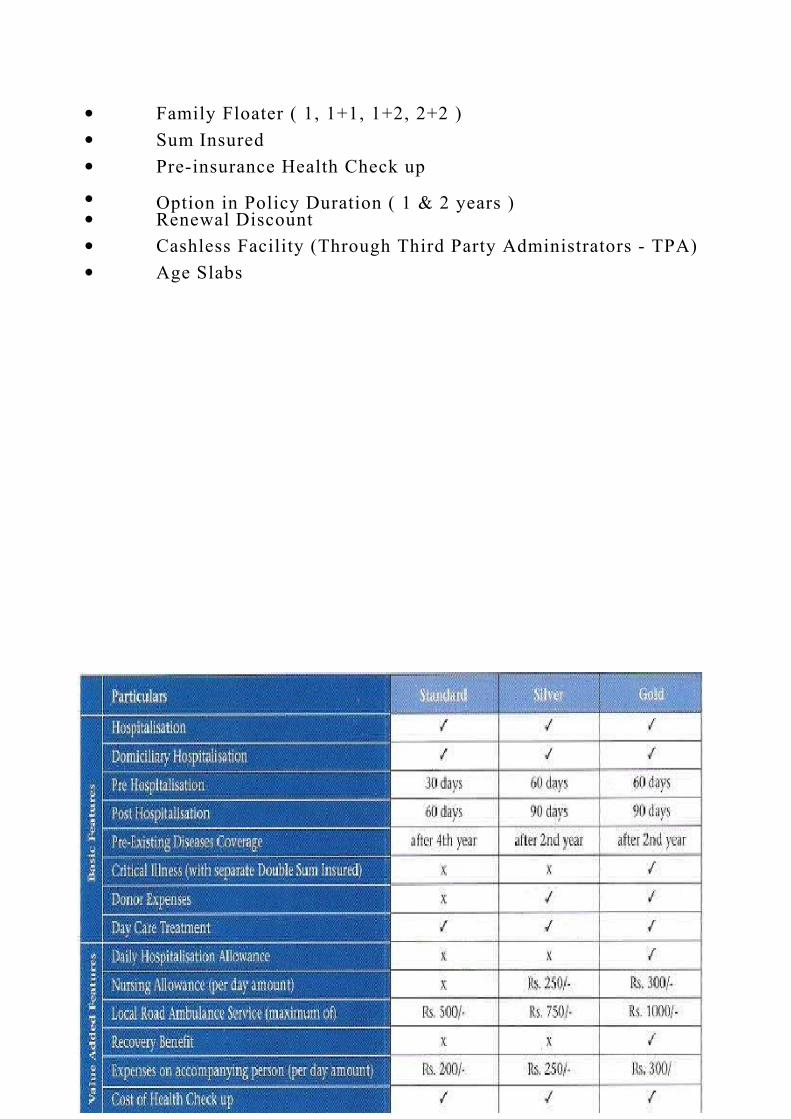

• Family Floater ( 1, 1+1, 1+2, 2+2 )

• Sum Insured

• Pre-insurance Health Check up

• Option in Policy Duration ( 1 & 2 years )• Renewal Discount

• Cashless Facility (Through Third Party Administrators - TPA)

• Age Slabs

Plan Details

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 44/61

(Source: web)

OBSERVATION & FINDINGS

To study the sales and distribution management and

improve the Customer Acquisition Process by analyzing

the consumer behavior, response and mindset towards

the product and services the company offers.

OBJECTIVE

• To find the market potential and market penetration of Reliance

Money product offerings in Bhubaneswar.

• To collect the real time information about preference level of

customers using Demat account and their inclination towards

various other brokerage f irms e.g. Indiabulls , Sharekhan,Indiainfoline, Religare, Alankit , Unicon.

• To expand the market penetration of Reliance money.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 45/61

• To provide pricing strategy of competitors to fight cut throat

competition.

• To increase the product awareness of Reliance money as single

window shop for investment solutions.

METHODOLOGY

We were supposed to operate from reliance money Nehru place

branch. We were made aware about all the products Reliance Money

was providing with a more stress on their core product i .e. Demat

account.

TARGETS

The time duration of the project is 2 months starting from 1 s t July

and ending on 30 t h August. We were given targets to be achieved

during training months. The targets of each month were:

• 3Demat Accounts

• 1SIP or Mutual Fund worth Rs10,000

• General Insurance Premium worth Rs50,000

• Life Insurance Premium worth Rs1,00,000

I was supposed to use the database provided by the company to

make cold calls or by directly meeting people to get new leads

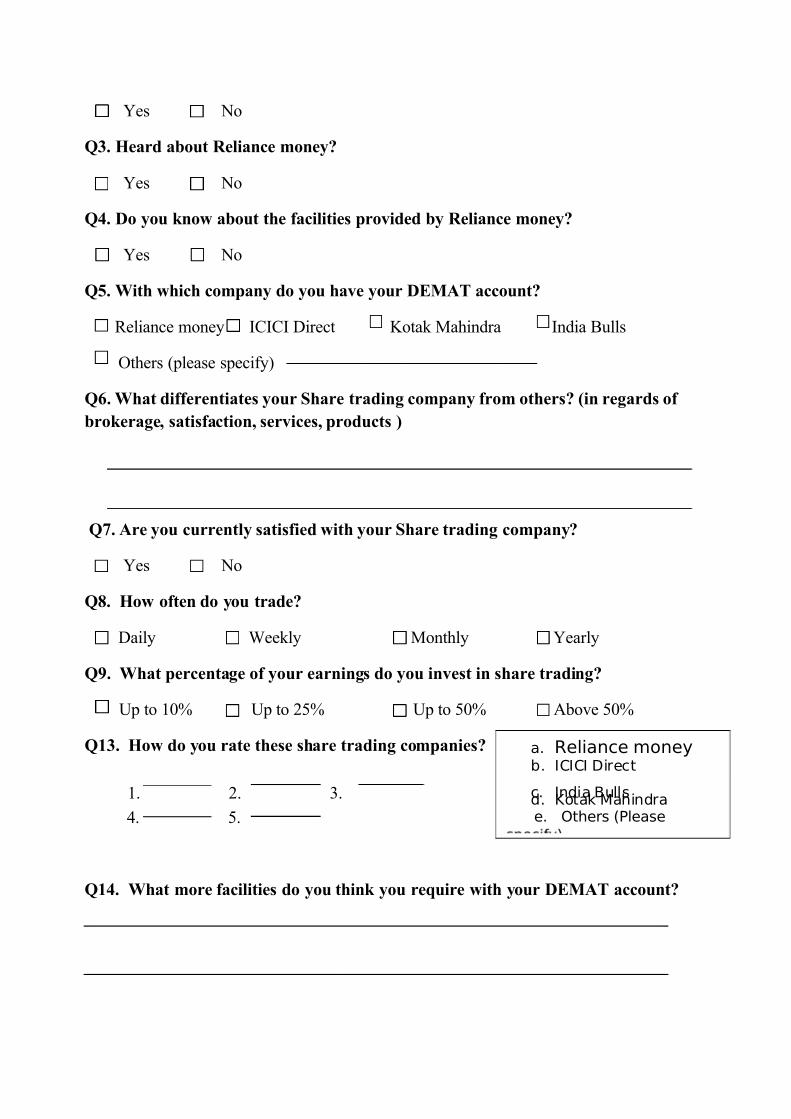

The questionnaire used is attached in appendix A.1

While making cold calls, we need to have:

• Good Communicat ion Skil ls (Voice qual ity i s clear and

articulate)

• Persistent and able to bounce back from rejection

• Good organizational skills.• Abi li ty to project a te lephone pe rsonal ity (Enthusiasm,

friendliness)

• Flexibi l ity: can adapt to different types of clients and new

situations.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 46/61

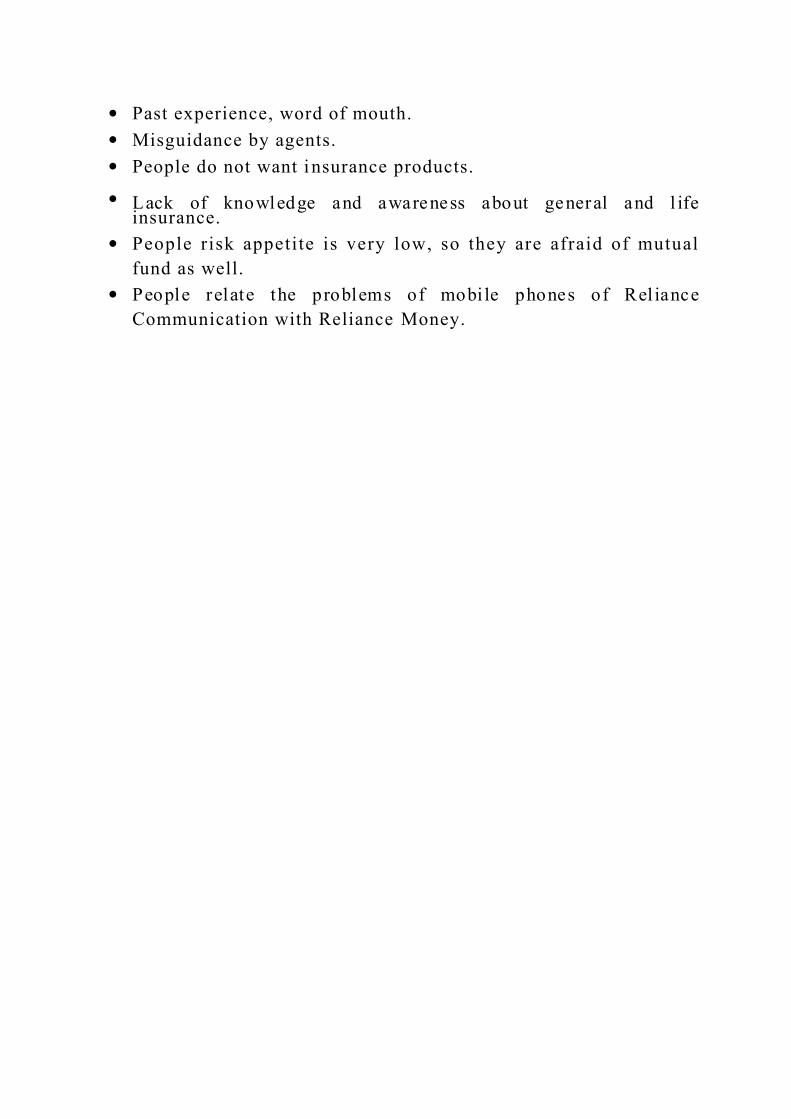

Using a good database is very essential.

“ Eighty percent of our business comes from 20 percent of our

customers" is a frequent statement at any sales convention. There's

hardly a sales executive who is not aware of the 80/20 rule”.

While talking to customers, I analyze their needs. Whether they want

to go for investment purpose or insurance or both. Suggest them the

plan that best suits them. If they agree to it then eithe r we send across

the agents to close the deal or close it themselves .

Fig6.2 The Customers Sales Cycle

Problems faced while selling products:

• Customer dissatisfied with the services.

• People fear that Reliance Money Being a Private company and a

new entrant may be able to sustain or not.

• Insurance means LIC for people.

Fig6.1 The Constructive Factors of Tele calling

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 47/61

• Past experience, word of mouth.

• Misguidance by agents.

• People do not want i nsurance products.

• Lack of knowledge and awareness about general and l ifeinsurance.

• People risk appetite is very low, so they are afraid of mutual

fund as well.

• People relate the problems of mobi le phones of Rel iance

Communication with Reliance Money.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 48/61

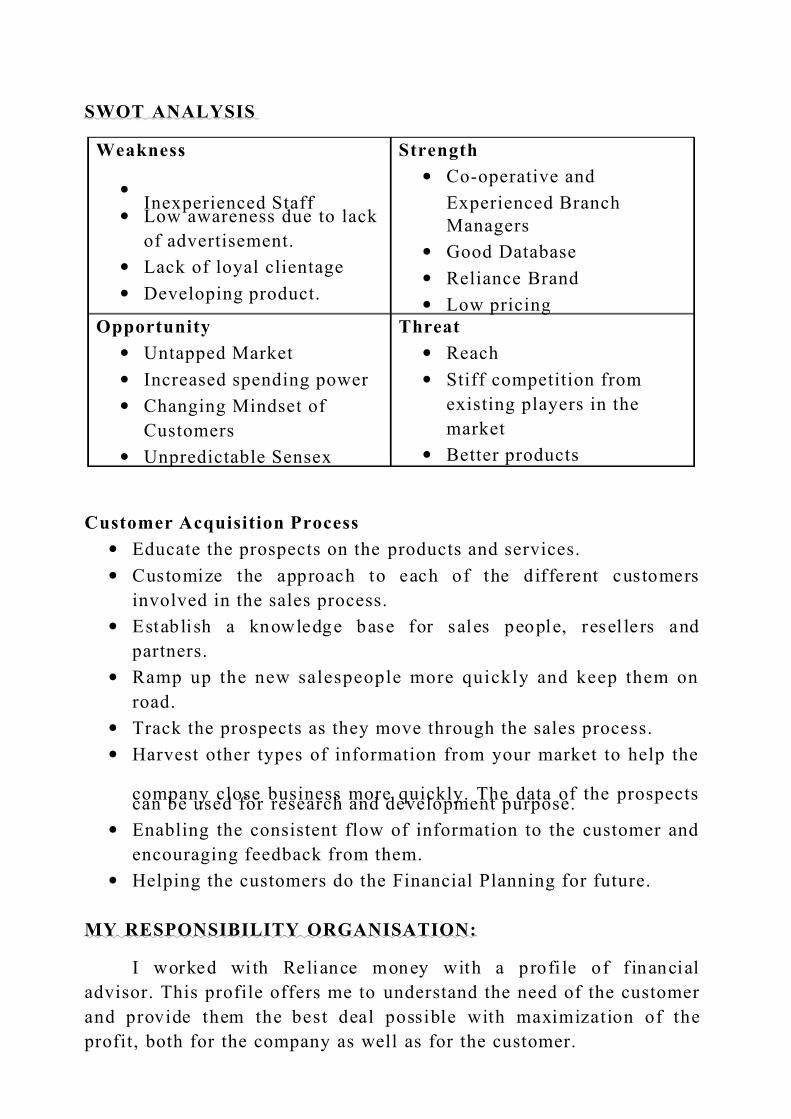

SWOT ANALYSIS

Weakness

•

Inexperienced Staff • Low awareness due to lack

of advertisement.

• Lack of loyal clientage

• Developing product.

Strength

• Co-operative and

Experienced Branch

Managers

• Good Database

• Reliance Brand

• Low pricing

Opportunity

• Untapped Market

• Increased spending power

• Changing Mindset of

Customers

• Unpredictable Sensex

Threat

• Reach

• Stiff competition from

existing players in the

market

• Better products

Customer Acquisition Process

• Educate the prospects on the products and services.

• Customize the approach to each of the different customers

involved in the sales process.

• Establish a knowledge base for sales people, resel le rs and

partners.

• Ramp up the new salespeople more quickly and keep them on

road.

• Track the prospects as they move through the sales process.

• Harvest other types of information from your market to help the

company close business more quickly. The data of the prospectscan be used for research and development purpose.

• Enabling the consistent flow of information to the customer and

encouraging feedback from them.

• Helping the customers do the Financial Planning for future.

MY RESPONSIBILITY ORGANISATION:

I worked wi th Reliance money with a profi le of f inancial

advisor. This profile offers me to understand the need of the customer

and provide them the best deal possible with maximization of the

profit, both for the company as well as for the customer.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 49/61

The most important aspect for the role of financial advisor is trust.

So for fulfillment of the targets one needs to:

• Capital ize on old and loyal clientage which can be building

slowly by advising people in the best possible way.• Generating new leads through various activities.

Generation of leads:

Since I was new in this field so I had to start from the scratch

and generate new leads to sustain in the market.

Cold calling is one of the trusted ways of getting to the customers

without meeting them. Although the rate of conversion remained very

less. For cold calling the quality and accent remains a very important

criterion. This activity gave me mixed results. I often got success and

generated many leads through it but i t also landed me in awkward

position where the customer were in different mood and made us hea r

words for which a marketer should be always prepared to hear.

Corporate calls always remained more difficult to crack with respect

to retail sector.

The corporate were the most difficult and most tempting to get the business from. It took me one day to crack Hi-tech Gears.

At Reliance money after getting the product knowledge in the first

week at the branch I was also allotted distributor to work with. In the

initial phase I was accompanied by more experienced staff. After I

became known to the market and procedure I started attending calls

alone only.

After the third week my performance also improved and I wasable to get close to the targets, though it looked difficult to achieve in

the beginning. To get awareness of the every product I attended

diversified calls. This helped me to implement cross selling to get

better results.

Since the reliance money core product is Demat account more

stress was given over this. Demat account was also the most tempting

of all the products as it was difficult to convince the customer for the

rel iance Demat as i t was new and wi th many l imi tations. I t was

always d if ficult to convince on 1 paisa, as i t wasn’ t mentioned

anywhere in ink.

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 50/61

LIMITATIONS:

1. Cold Calling

• Voice and accent plays a major role.

•

The r ight t ime to cal l a customer cannot be decided, as thecustomer may in a different mood at the time of calling.

• Time consuming

• Less success rate

2. Corporate

• Time consuming

• Contacts with higher authorities play a major role

LEARNINGS

• To get initial success in this field is very difficult. Although the

business generation becomes easier with time as we serve more

people who then get added up in the loyal clientage. Thus time

and service are two most factors to get in this field.

• Also the corporate remains a very important segment which gets

business in bulk bu t retail cannot be ignored which makes your

business ticking.• Customer remains in the pivotal position.

Findings

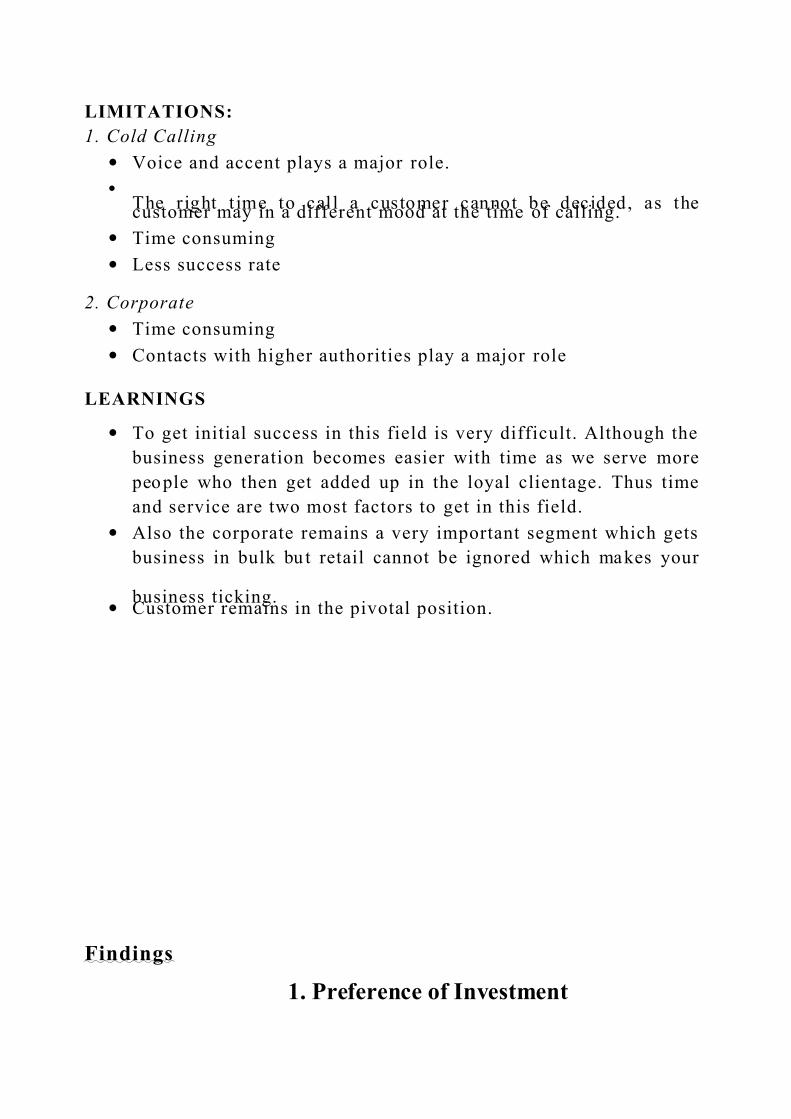

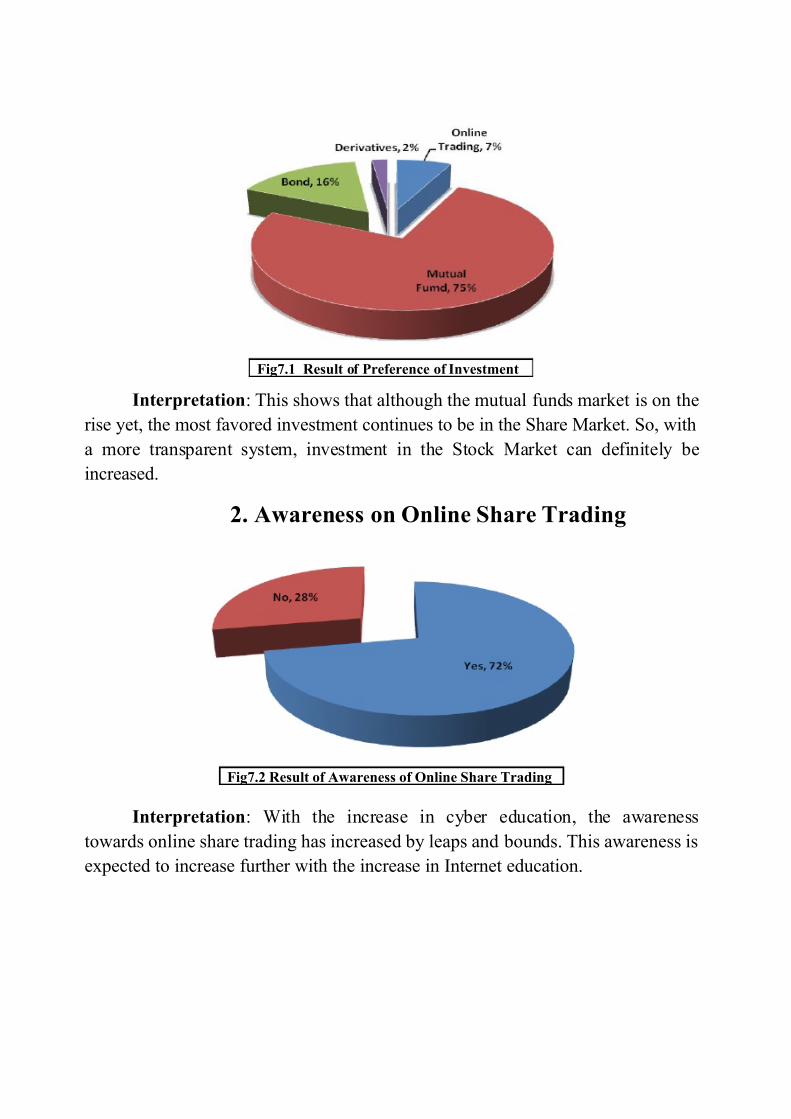

1. Preference of Investment

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 51/61

Interpretation: This shows that although the mutual funds market is on the

rise yet, the most favored investment continues to be in the Share Market. So, with

a more transparent system, investment in the Stock Market can definitely be

increased.

2. Awareness on Online Share Trading

Fig7.2 Result of Awareness of Online Share Trading

Interpretation: With the increase in cyber education, the awareness

towards online share trading has increased by leaps and bounds. This awareness is

expected to increase further with the increase in Internet education.

Fig7.1 Result of Preference of Investment

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 52/61

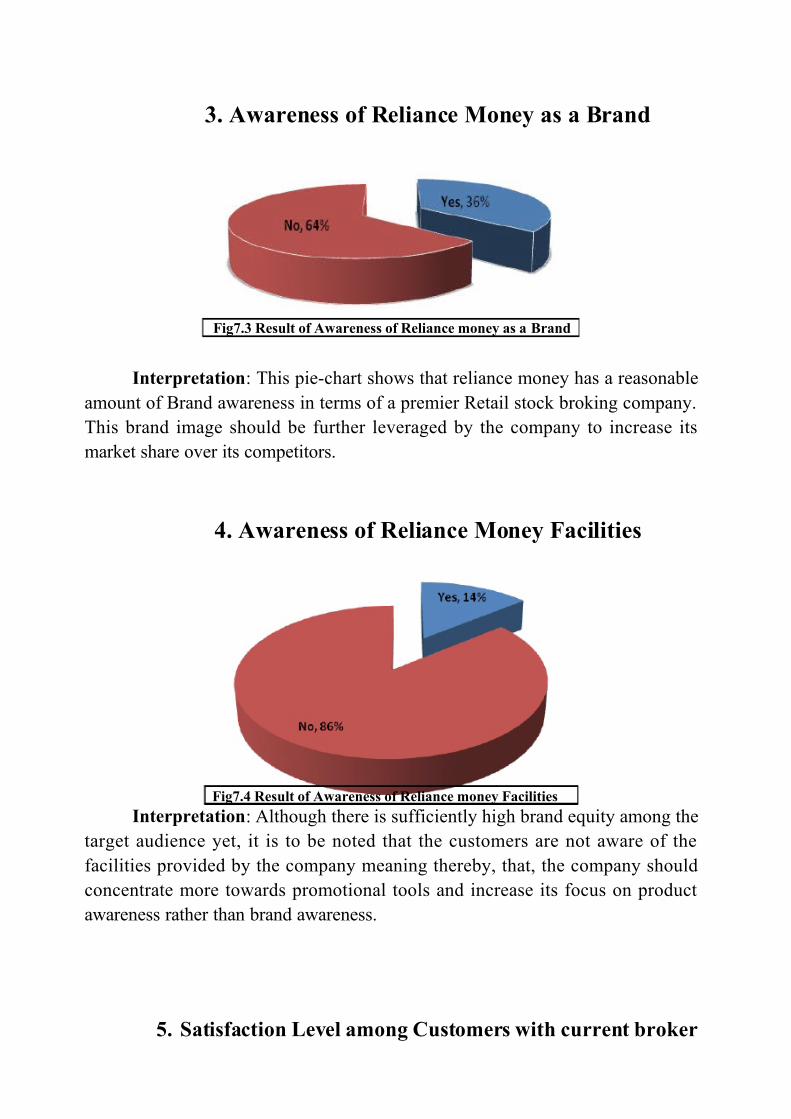

3. Awareness of Reliance Money as a Brand

Interpretation: This pie-chart shows that reliance money has a reasonable

amount of Brand awareness in terms of a premier Retail stock broking company.

This brand image should be further leveraged by the company to increase its

market share over its competitors.

4. Awareness of Reliance Money Facilities

Interpretation: Although there is sufficiently high brand equity among the

target audience yet, it is to be noted that the customers are not aware of the

facilities provided by the company meaning thereby, that, the company should

concentrate more towards promotional tools and increase its focus on product

awareness rather than brand awareness.

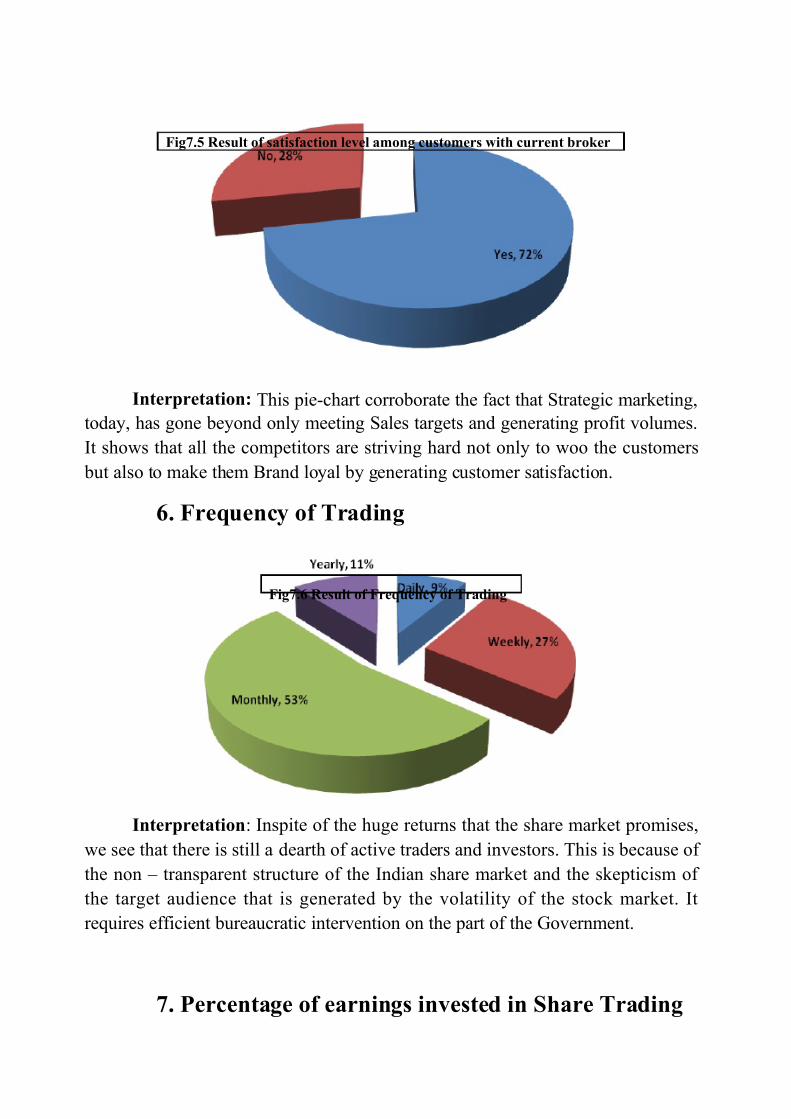

5. Satisfaction Level among Customers with current broker

Fig7.3 Result of Awareness of Reliance money as a Brand

Fig7.4 Result of Awareness of Reliance money Facilities

7/31/2019 17704886 Reliance Money Mann

http://slidepdf.com/reader/full/17704886-reliance-money-mann 53/61