A

SUMMERE TRAINING PROJECT

ON

PUNJAB NATIONAL BANK

“HOME LOAN”

SUBMITTED TO:-

JIWAJI UNIVERSITY GWALIOR

FOR THE PARTIAL FULFILLMENT OF

BACHELOR OF BUSINESS ADMINISTRATION

2011-14

SUBMITTED TO: - SUBMITTED BY:-

MR.HARI KRISHNA SHARMA ARBIND KUMAR

(Faculty guide) BBA V Semester

Boston College For Professional Studies

Gwalior

1

DECLARATION

This is to declare that the Summer Training Report has been accomplished

by me and being submitted in partial fulfillment of requirement for the

award of the Degree of Bachelor of Business Administration Boston

College For Professional Studies Gwalior from Jiwaji University,

Gwalior The work has not been submitted by me anywhere else for the

award of any degree or diploma. All source of information are based on my

on training experience and learning.

Date: ARBIND KUMAR Place: BBA V SEMESTER

CERTIFICATE

2

This is to certify that MR. ARBIND KUMAR student

of BBA V Semester of Boston College For Professional

Studies Gwalior has successfully completed his

Summer Training dated from 45 days and this report

is submitted by Her for the completion of the

training requirement under my guidance and

supervision.

Date : MR.HARI KRISHNA SHARMA

Place: (Faculty guide)

3

ACKNOWLEDGEMENT

It is great pleasure for me to put on record my appreciation and

gratitude towards Placement and Training Coordinator of Boston

College For Professional Studies Gwalior. My special thanks to

my respected faculty MR.HARI KRISHNA SHARMA for him

valuable support and suggestions for the execution of Summer

Training. I thank her for the right direction and providing inputs

for the completion of my summer training project.

Date: ARBIND KUMAR Place: BBA V SEMESTER

4

PREFACE

Modern organizations are highly complex ad dynamics systems. They

operate under very turbulent social economic and political environment.

They are required to reconcile several incompatible goals. Conflicting roles

and divergent interest they are also fraught with the use risk and

uncertainties, hence tactful management of such organization to plan to

execute guide, coordination and control the performance of people to

achieve predetermined goals. Management has to keep the organization

vibrant moving and in equilibrium. It has to achieve goal which themselves

are changing it is therefore a problem highly complex and ticklish.

This informat ion wil l be asset to market ing manager in

making effect ive decisions. The researches are used to

acquire and analyse informat ion and to make suggest ions to

management as to how market ing problems should be solved.

The market ing research is the process which l inks to

manufacturer , dealers and individuals through informat ion in

important par t of curr iculum of M.B.A. programme is project

taken by the students to inst i tute under which he or she is

s tudying, af ter complet ion of thi rd semester of the

programme.

The object ive of this project is to enable the s tudents to

understand the appl icat ion of the academics in the real

business l ife . I am ful ly conf ident that this project repor t

wi l l be extremely useful to the management .

5

TABLE OF CONTENTS

Acknowledgement

Preface

CHAPTER 1: Overview of banking industry in India

CHAPTER 2: A Saga of Banking Excellence in Banking

(PUNJAB NATIONAL BANK)

CHAPTER 3: Performance of the PNB

CHAPTER 4: Organisational Structure

CHAPTER 5: Home Loan

CHAPTER 6: PNB Home Loan

CHAPTER 7: Suggestions & Troubleshooting Tips

CHAPTER 8: Bibliography

6

• TYPES OF BANKS• BANKS IN INDIA

7

OVERVIEW OF BANKING INDUSTRY IN

INDIA

The major participants of the Indian financial system are the

commercial banks, the financial institutions (FIs), encompassing term-

lending institutions, investment institutions, specialized financial

institutions and the state-level development banks, Non-Bank Financial

Companies (NBFCs) and other market intermediaries such as the stock

brokers and money-lenders. The commercial banks and certain variants of

NBFCs are among the oldest of the market participants. The FIs, on the

other hand, are relatively new entities in the financial market place.

Bank of Hindustan, set up in 1870, was the earliest Indian Bank .

Banking in India on modern lines started with the establishment of three

presidency banks under Presidency Bank's act 1876 i.e. Bank of Calcutta,

Bank of Bombay and Bank of Madras. In 1921, all presidency banks were

amalgamated to form the Imperial Bank of India. Imperial bank carried out

limited central banking functions also prior to establishment of RBI. It

engaged in all types of commercial banking business except dealing in

foreign exchange.

Reserve Bank of India Act was passed in 1934 & Reserve Bank of

India (RBI) was constituted as an apex bank without major government

ownership. Banking Regulations Act was passed in 1949. This regulation

brought Reserve Bank of India under government control. Under the act,

8

RBI got wide ranging powers for supervision & control of banks. The Act

also vested licensing powers & the authority to conduct inspections in RBI

In 1955, RBI acquired control of the Imperial Bank of India, which was renamed as State Bank of India. In 1959, SBI took over control of eight private banks floated in the erstwhile princely states, making them as its 100% subsidiaries.

RBI was empowered in 1960, to force compulsory merger of weak banks with the strong ones. The total number of banks was thus reduced from 566 in 1951 to 85 in 1969. In July 1969, government nationalised 14 banks having deposits of Rs.50 crores & above. In 1980, government acquired 6 more banks with deposits of more than Rs.200 crores. Nationalisation of banks was to make them play the role of catalytic agents for economic growth. The Narsimham Committee report suggested wide ranging reforms for the banking sector in 1992 to introduce internationally accepted banking practices.

The amendment of Banking Regulation Act in 1993 saw the entry of new private sector banks.

Banking Segment in India functions under the umbrella of Reserve Bank of India - the regulatory, central bank. This segment broadly consists of:

Commercial; Banks

Co-operative Banks

Commercial Banks

The commercial banking structure in India consists of:

• Scheduled Commercial Banks

• Unscheduled Banks

Scheduled commercial Banks constitute those banks which have been

included in the Second Schedule of Reserve Bank of India(RBI) Act, 1934.

RBI in turn includes only those banks in this schedule which satisfy the

criteria laid down vide section 42 (60 of the Act. Some co-operative banks

are scheduled commercial banks albeit not all co-operative banks are. Being

9

a part of the second schedule confers some benefits to the bank in terms of

access to accomodation by RBI during the times of liquidity constraints. At

the same time, however, this status also subjects the bank certain conditions

and obligation towards the reserve regulations of RBI. This sub sector can

broadly be classified into:

1. Public sector

2. Private sector

3. Foreign banks.

CO-OPERATIVE BANKS

There are two main categories of the co-operative banks.

(a) Short term lending oriented co-operative Banks - within this

category there are three sub categories of banks viz state co-operative

banks, District co-operative banks and Primary Agricultural co-

operative societies.

(b) Long term lending oriented co-operative Banks - within the

second category there are land development banks at three levels state

level, district level and village level.

The co-operative banking structure in India is divided into following

main 5 categories: (Visit us again for details of each category)

1. Primary Urban Co-op Banks:

2. Primary Agricultural Credit Societies:

3. District Central Co-op Banks:

4, State Co-operative Banks:

5. Land Development Banks:

10

BANKS IN INDIA

s S. N. Public Sector Banks Private Sector

Banks

Foreign Banks

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

Allahabad Bank

Andhra Bank

Bank of Baroda

Bank of India

Bank of Maharashtra

Canara Bank

Central Bank of India

Corporation Bank

Dena Bank

Indian Bank

Indian Overseas Bank

Oriental Bank of Commerce

Punjab and Sind Bank

Punjab National Bank

Syndicate Bank

UCO Bank

Union Bank of India

United Bank of India

Vijaya Bank

IDBI Bank

Bank of Punjab Ltd.

Centurion Bank Ltd.

Development Credit Bank Ltd.

HDFC Bank Ltd.

ICICI Bank Ltd.

IndusInd Bank Ltd.

Kotak Mahindra Bank Ltd.

UTI Bank Ltd.

Yes Bank Ltd

Bank of Rajasthan Ltd.

Dhanalakshmi Bank Ltd.

Federal Bank Ltd

ING Vysya Bank Ltd.

Jammu and Kashmir Bank Ltd.

Karnataka Bank Ltd

Karur Vysya Bank Ltd

Ratnakar Bank Ltd

SBI Commercial and

International Bank Ltd

South Indian Bank Ltd

United Western Bank Ltd

ABN-AMRO Bank N.V

Abu Dhabi Commercial Bank Ltd

American Express Bank Ltd.

BNP Paribas

Citibank N.A

DBS Bank Ltd

HSBC Ltd.

Standard Chartered Bank

11

• ABOUT PUNJAB NATIONAL BANK• HISTORY OF PNB• VISION & MISSION

12

A SAGA OF EXCELLENCE IN BANKING

Established in 1895 at Lahore, undivided India, Punjab National Bank

(PNB) has the distinction of being the first Indian bank to have been started

solely with Indian capital. The bank was nationalized in July 1969 along

with 13 other banks. From its modest beginning, the bank has grown in size

and stature to become a front-line banking institution in India at present

A professionally managed bank with a successful track record of over 110

years.

Largest branch network in India - 4668 Offices including 238 Extension

Counters spread throughout the country.

Strategic business area covers the large Indo-Genetic belt and the

metropolitan centres.

Ranked as 248th biggest bank in the world by Bankers Almanac, London.

Strong correspondent banking relationships with more than 217

international banks of the world.

More than 50 renowned international banks maintain their Rupee Accounts

with PNB.

13

Well equipped dealing rooms; 20 different foreign currency accounts are

maintained at major centres all over the globe.

Rupee drawing arrangements with M/s UAE Exchange Centre, UAE, M/s

Al Fardan Exchange Co. Doha, Qatar, M/s Bahrain Exchange Co, Kuwait,

M/s Bahrain Finance Co, Bahrain, M/s Thomas Cook Al Rostamani

Exchange Co. Dubai, UAE, and M/s Musandam Exchange, Ruwi,

Sultanate of Oman.

14

ABOUT PUNJAB NATIONAL BANK

With over 38 million satisfied customers and 4668 offices, PNB has

continued to retain its leadership position among the nationalized banks.

The bank enjoys strong fundamentals, large franchise value and good brand

image. Besides being ranked as one of India's top service brands, PNB has

remained fully committed to its guiding principles of sound and prudent

banking. Apart from offering banking products, the bank has also entered

the credit card & debit card business; bullion business; life and non-life

insurance business; Gold coins & asset management business, etc.

Since its humble beginning in 1895 with the distinction of being the first

Indian bank to have been started with Indian capital, PNB has achieved

significant growth in business which at the end of March 2009 amounted to

Rs 3, 64,463 crore. Today, with assets of more than Rs 2, 46,900 crore,

PNB is ranked as the 3rd largest bank in the country (after SBI and ICICI

Bank) and has the 2nd largest network of branches (4668 including 238

extension counters and 3 overseas offices).During the FY 2008-09, with

39% share of low cost deposits, the bank achieved a net profit of Rs 3,091

crore, maintaining its number ONE position amongst nationalized banks.

Bank has a strong capital base with capital adequacy ratio as per Basel II at

14.03% with Tier I and Tier II capital ratio at 8.98% and 5.05% respectively

as on March’09. As on March’09, the Bank has the Gross and Net NPA

ratio of only 1.77% and 0.17% respectively. During the FY 2008-09, its’

ratio of priority sector credit to adjusted net bank credit at 41.53% &

15

agriculture credit to adjusted net bank credit at 19.72% was also higher than

the respective national goals of 40% & 18%.

PNB has always looked at technology as a key facilitator to provide better

customer service and ensured that its ‘IT strategy’ follows the ‘Business

strategy’ so as to arrive at “Best Fit”. The bank has made rapid strides in

this direction. Along with the achievement of 100% branch

computerization, one of the major achievements of the Bank is covering all

the branches of the Bank under Core Banking Solution (CBS), thus

covering 100% of it’s business and providing ‘Anytime Anywhere’ banking

facility to all customers including customers of more than 2000 rural

branches. The bank has also been offering Internet banking services to the

customers of CBS branches like booking of tickets, payment of bills of

utilities, purchase of airline tickets etc. Towards developing a cost effective

alternative channels of delivery, the bank with more than 2150 ATMs has

the largest ATM network amongst Nationalised Banks.

With the help of advanced technology, the Bank has been a frontrunner in

the industry so far as the initiatives for Financial Inclusion is concerned.

With it’s policy of inclusive growth in the Indo-Gangetic belt, the Bank’s

mission is “Banking for card based technology enabled Financial Inclusion

with the help of Business Correspondents/Business Facilitators (BC/BF) so

as to reach out to the last mile customer. The BC/BF will address the

outreach issue while technology will provide cost effective and transparent

services. The Bank has started several innovative initiatives for marginal

groups like rickshaw pullers, vegetable vendors, diary farmers, construction

workers, etc. The Bank has already achieved 100% financial inclusion in

21,408 villages.

16

Backed by strong domestic performance, the bank is planning to realize its

global aspirations. In order to increase its international presence, the Bank

continues its selective foray in international markets with presence in Hong

Kong, Dubai, Kazakhstan, UK, Shanghai, Singapore, Kabul and Norway. A

second branch in Hong Kong at Kowloon was opened in the first week of

April’09. Bank is also in the process of establishing its presence in China,

Bhutan, DIFC Dubai, Canada and Singapore. The bank also has a joint

venture with Everest Bank Ltd. (EBL), Nepal. Under the long term vision,

Bank proposes to start its operation in Fiji Island, Australia and Indonesia.

Bank continues with its goal to become a household brand with global

expertise.

Amongst Top 1000 Banks in the World, ‘The Banker’ listed PNB at 250th

place. Further, PNB is at the 1166th position among 48 Indian firms making

it to a list of the world’s biggest companies compiled by the US magazine

‘Forbes’.

17

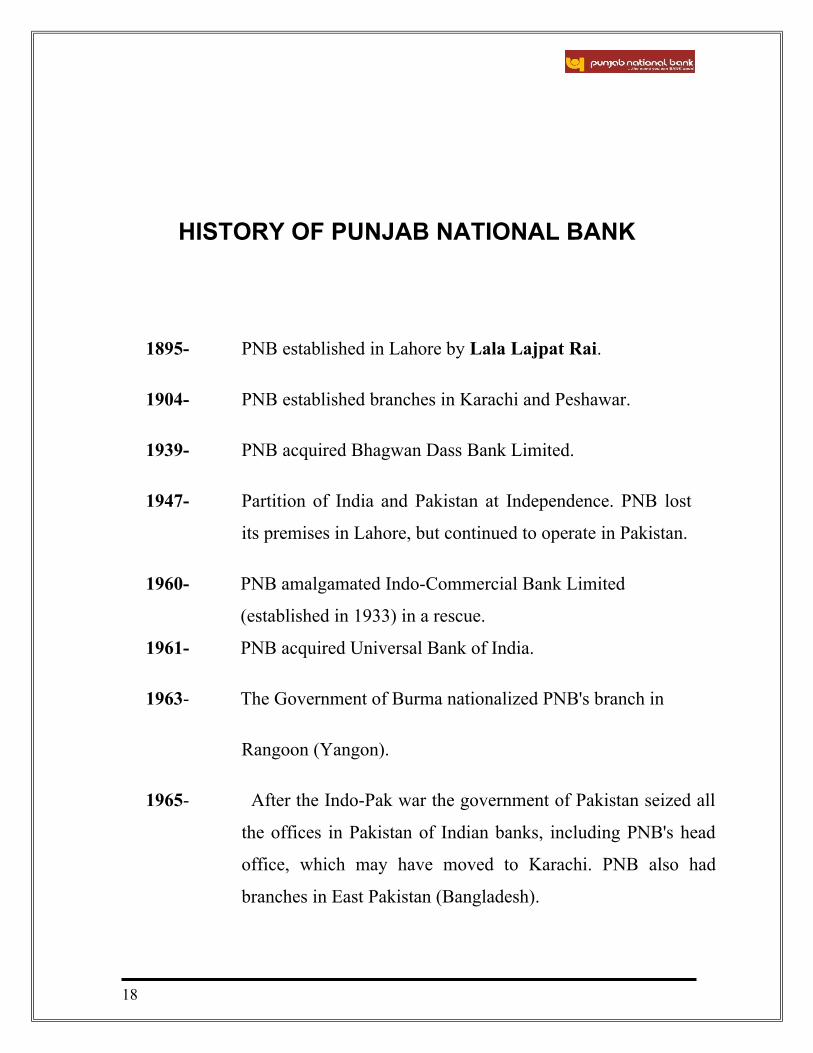

HISTORY OF PUNJAB NATIONAL BANK

1895- PNB established in Lahore by Lala Lajpat Rai.

1904- PNB established branches in Karachi and Peshawar.

1939- PNB acquired Bhagwan Dass Bank Limited.

1947- Partition of India and Pakistan at Independence. PNB lost

its premises in Lahore, but continued to operate in Pakistan.

1960- PNB amalgamated Indo-Commercial Bank Limited

(established in 1933) in a rescue.

1961- PNB acquired Universal Bank of India.

1963- The Government of Burma nationalized PNB's branch in

Rangoon (Yangon).

1965- After the Indo-Pak war the government of Pakistan seized all

the offices in Pakistan of Indian banks, including PNB's head

office, which may have moved to Karachi. PNB also had

branches in East Pakistan (Bangladesh).

18

1969- The Government of India nationalized PNB and 13 other

major banks on 19th July, 1969.

1978- PNB opened a branch in London.

1988- PNB acquired Hindustan Commercial Bank Limited in a

rescue.

1993- PNB acquired New Bank of India, which the Government of

India had nationalized in 1980.

1998- PNB set up a representative office in Almaty, Kazakhstan.

2003- PNB took over Nedungadi Bank (established the bank in

1899), the oldest private sector bank in Kerala. It was

incorporated in 1913 and in 1965 had acquired selected

assets and deposits of the Coimbatore National Bank. At the

time of the merger with PNB, Nedungadi Bank's shares had

zero value, with the result that its shareholders received no

payment for their shares.

19

VISION

"To be a Leading Global Bank with Pan India footprints and become a

household brand in the Indo-Gangetic Plains providing entire range of

financial products and services under one roof"

MISSION

"Banking for the unbanked

20

• FINANCIAL PERFORMANCE OF PNB

• AWARDS & RECOGNITION

• PEST ANALYSIS

• SWOT ANALYSIS

21

Financial Performance of the Bank

Punjab National Bank continues to maintain its frontline position retained

its NUMBER ONE position among the nationalized banks in terms of

number of branches, Deposit, Advances, total Business, operating and net

profit in the year 2008-09. The impressive operational and financial

performance has been brought about by Bank’s focus on customer based

business with thrust on SME, Agriculture, more inclusive approach to

banking; better asset liability management; improved margin management,

thrust on recovery and increased efficiency in core operations of the Bank.

The performance highlights of the bank in terms of business and profit are

shown below:

Parameters Mar'07 Mar'08 Mar'09 CRAR

Operating Profit* 3617 4006 5744 26.02

Net Profit* 1540 2049 3091 41.67

Deposit 139860 166457 209760 22.47

Advance 96597 119502 154703 26.55

Total Business 236456 285959 364463 24.15

(Rs.Crores)

• Respective figure for the corresponding financial year

22

AWARDS & RECOGNITIONS

"Best IT Team of the Year Award"- At the IDRBT Banking Technology awards for the year 2005-06.

SKOTCH Challenger Award-For Change Management for the year 2005-06

Best IT User in Banking & Financial Services Industry – 2004

By NASSCOM in partnership with Economic Times.

Golden Peacock Award-

For Excellence in Corporate Governance - 2005 by Institute of Directors.

FICCI's Rural Development Award-

For Excellence in Rural Development – 2005

Skotch Challenger Award for Exemplary use of Technology

For becoming a pioneer in Public Banks – 2005

Golden Peacock National Training - 2004 & 2005

23

By Institute of Directors

National Award for Excellence in SSI Lending

Ranked 2nd for 4 consecutive years - 2002, 2003, 2004 & 2005

Banking Technology Awards 2004 Runner up in 'Best IT Team of the Year Award 2005'

Jointly Adjudged by IBA, Finacle & TFCI

Money Outlook Award - 2004

Runner up in 'Best Bank (public Sector) of the year Award' –2005

Niryat Bandhu Gold Trophy

For excellence in export performance for 3 consecutive years 2001, 2002 & 2003 by Federation of Indian Exporters Organization (FIEO)

21st Amongst Top 500 Companies

By the leading Financial Daily the Economic Times, June 2005

9th amongst India's Top 50 Most Trusted

A.C Nielson Survey, The Economic Times Dec 2004

Service Brands 3rd Rank amongst Banking Sector in India 323rd Rank in the World

The Bankers' Almanac, January 2006

24

368 amongst Top 1000 Global Banks

The Banker, London July 2005

PEST ANALYSIS

25

SWOT ANALYSIS

Objective

Analysis of PNB

Strengths

• Wide network• Large no. of

customers• Fast adaptability to technology• Brand recognition• Excellent Training

Weaknesses

Opportunities

• Fast growing Indian

economy• High growth in

bankingsector• Liberal markets• Micro financing

• Home to home banking services

• Diversification towards other field

• Globalization

• Decentralized decision making

• Awards & Incentives

Threats

• Large no. of market players

• Providing betterservices• Building long termcustomer relationships

• Fast Decision making• Competitive edge• Changing culture

26

• STRUCTURE OF THE ORGANISATION

• HIERARCHY

• MANAGEMENT OF PNB

• ABOUT M.D. & CHAIRMAN SINCE INCEPTION

27

ORGANISATIONAL STRUCTURE

Bank has its Corporate Office at New Delhi and supervises 58 Circle

Offices under which the branches function. The delegation of powers is

decentralised upto the branch level to facilitate quick decision making.

28

HEAD OFFICE7, Bhikhaji Cama Place, New Delhi-110026

CGM OFFICES

CIRCLE OFFICES

BRANCHES

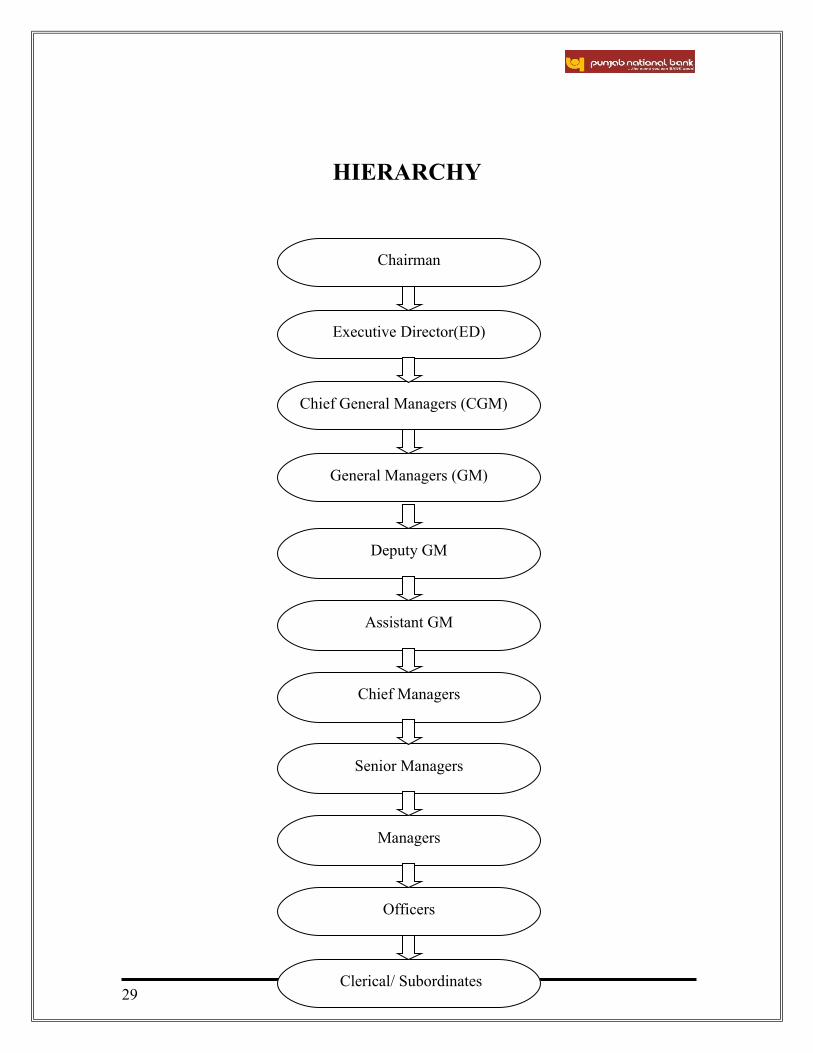

HIERARCHY

29

Executive Director(ED)

Chief General Managers (CGM)

General Managers (GM)

Deputy GM

Assistant GM

Chief Managers

Senior Managers

Managers

Officers

Clerical/ Subordinates

Chairman

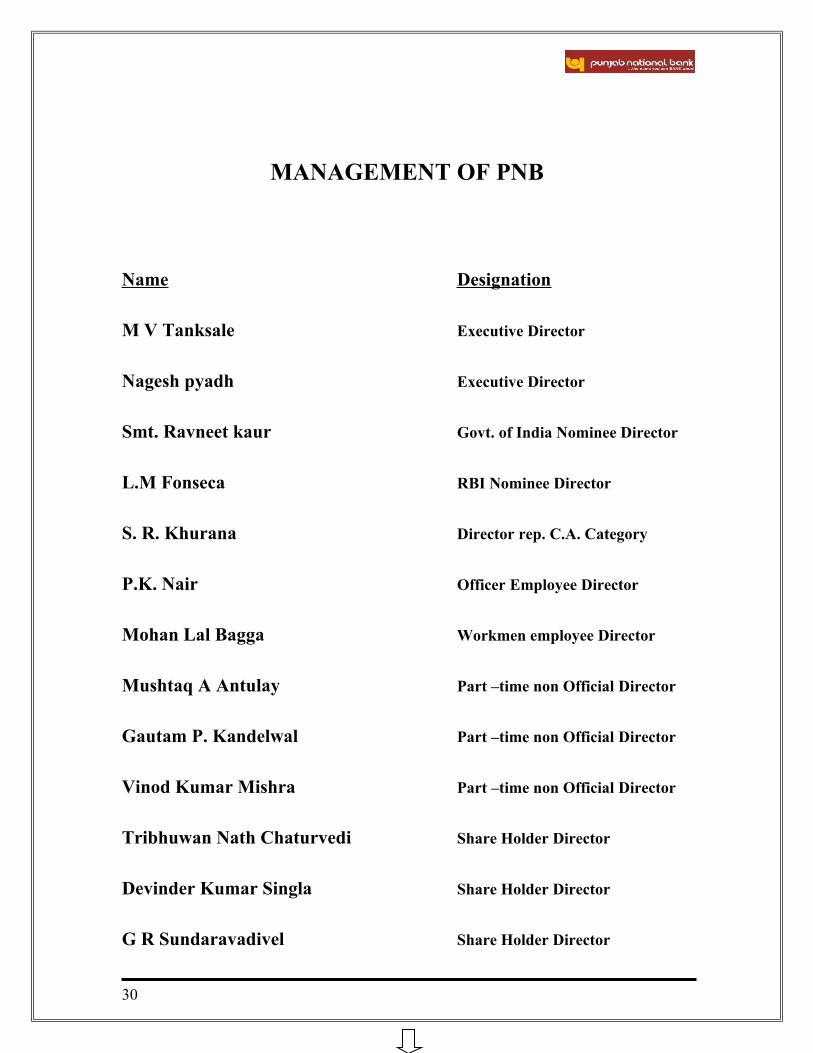

MANAGEMENT OF PNB

Name Designation

M V Tanksale Executive Director

Nagesh pyadh Executive Director

Smt. Ravneet kaur Govt. of India Nominee Director

L.M Fonseca RBI Nominee Director

S. R. Khurana Director rep. C.A. Category

P.K. Nair Officer Employee Director

Mohan Lal Bagga Workmen employee Director

Mushtaq A Antulay Part –time non Official Director

Gautam P. Kandelwal Part –time non Official Director

Vinod Kumar Mishra Part –time non Official Director

Tribhuwan Nath Chaturvedi Share Holder Director

Devinder Kumar Singla Share Holder Director

G R Sundaravadivel Share Holder Director

30

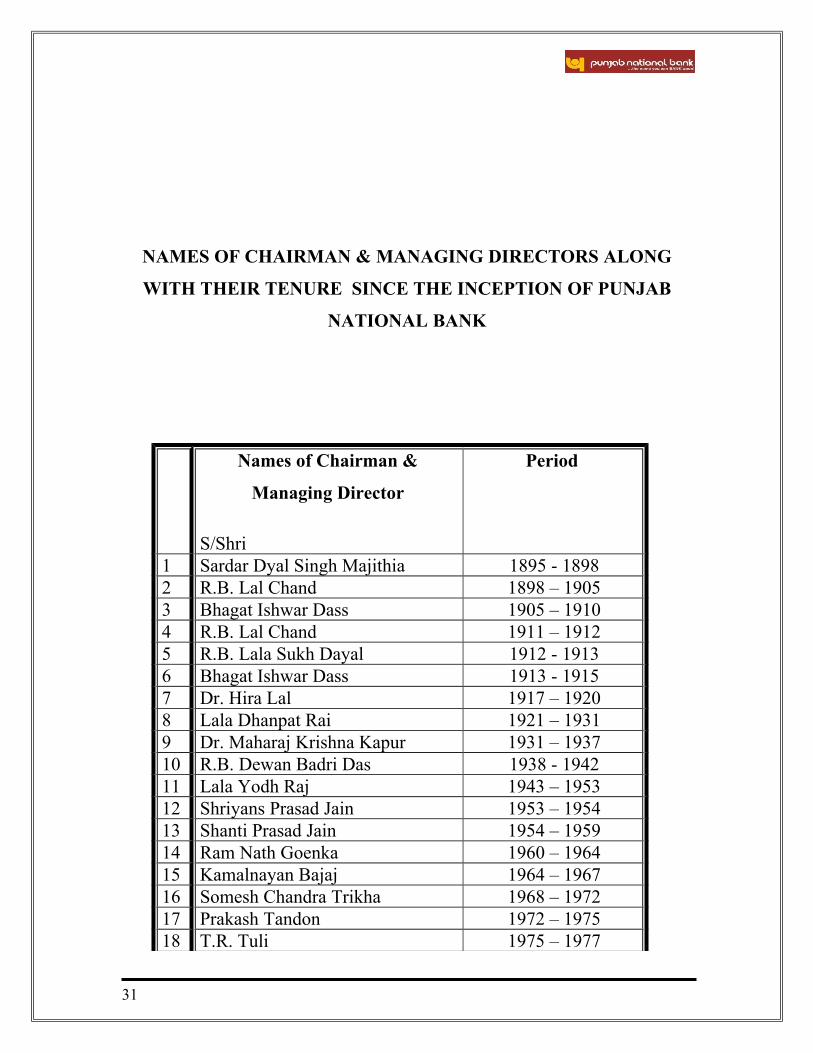

NAMES OF CHAIRMAN & MANAGING DIRECTORS ALONG

WITH THEIR TENURE SINCE THE INCEPTION OF PUNJAB

NATIONAL BANK

Names of Chairman &

Managing Director

S/Shri

Period

1 Sardar Dyal Singh Majithia 1895 - 18982 R.B. Lal Chand 1898 – 19053 Bhagat Ishwar Dass 1905 – 19104 R.B. Lal Chand 1911 – 19125 R.B. Lala Sukh Dayal 1912 - 19136 Bhagat Ishwar Dass 1913 - 19157 Dr. Hira Lal 1917 – 19208 Lala Dhanpat Rai 1921 – 19319 Dr. Maharaj Krishna Kapur 1931 – 193710 R.B. Dewan Badri Das 1938 - 194211 Lala Yodh Raj 1943 – 195312 Shriyans Prasad Jain 1953 – 195413 Shanti Prasad Jain 1954 – 195914 Ram Nath Goenka 1960 – 196415 Kamalnayan Bajaj 1964 – 196716 Somesh Chandra Trikha 1968 – 197217 Prakash Tandon 1972 – 197518 T.R. Tuli 1975 – 1977

31

19 O.P. Gupta 1977 – 198020 S.L. Chopra 1980 – 198121 S.L. Baluja 1981 – 198522 J.S. Varshneya 1985 – 198923 Rashid Jilani 1990 - 200024 S.S. Kohli 2000 – 200525 S.C. Gupta 2005 - 200726 Dr. K.C. Chakrabarty 2007 – 2009

32

• FEATURES OF HOME LOAN

• HOME LOAN INDIA

• TYPES OF HOME LOAN

• WHY TAKE A HOME LOAN

• CHECK LIST FOR HOME LOAN

• RBI DIRECTIVES FOR HOME LOAN

HOME LOAN

Home loans are provided based on the market value, mainly estimation

given by banks or the registration value of the property. Availing various

types of house loans to suit your individual needs at the lowest rates & easy

financing can now fulfill the need for a house of your own.

Home loan is not a one-time decision; do review the market periodically

33

before availing them. Today there are unlimited numbers of banks in the

country wanting to give out Home loans. Given this scenario, it may seem

easy getting yourself a loan. But is it really??

Buyers tend to make mistakes while entering into deals, which may not be

beneficial for them, so better compare all the variables before signing a loan

agreement by different banks. However the loan agreement should be

finalized only after reading the terms and conditions carefully.

You can apply for a Home loan even before you select your property. The

loan amount would be sanctioned or approved for you, based on your

repayment capability.

Features of house loan:

• Purpose: For purchase of house from builder / resale and construction /

extension of existing house.

• Loan amount: You can avail for Home loans need based depending on

your eligibility, income and repayment capacity.

34

• Security: Home loan is a secured loan wherein collateral are required.

• Loan tenor: The maximum loan tenure is 25 years.

Planning to avail a home loan, you must adhere underneath points:

Firstly, take your own time and evaluate your expenses and do a market

survey about the property buying process. Buying a house, which is way

beyond your range, could affect you financially; banks help in financing

your dream home via home loans.

1. Eligibility

Banks determine your eligibility based on your repayment capacity and

discuss about the loan amount up front. The eligibility for acquiring a home

loan is augmented by clubbing income of your father/spouse/mother/son, by

clearing your outstanding debts, by stretching your loan tenure, Salaried

individuals can increase their eligibility by showing their performance

linked income or bonus earned.

Secondly, Do your own analysis and check the impact of your repayment of

home loan on your monthly expenditure, as a thumb rule, it’s recommended

to make sure the EMI of your home loan do not exceed more than 50% of

your gross monthly income.

2. Interest rates

35

An important factor that goes into your EMI calculations is the interest

rates, which may vary from bank to bank, so do compare them. Also do a

complete and detailed analysis of the various options like the interest rates

i.e. fixed and floating rate of interest.

Thirdly, if two banks give you the same amount of loan but at different

interest rates do your math and work out what's best for you.

a) Fixed interest loans

Charge an interest, which remains the same through out the tenure of the

loan. This means that the consumer is immune to market risk or the possible

upward movement in the interest rates.

Hence, fixed rate is a good option when the interest rates are expected to

move up in the future.

b) Floating rate loans

A consumer is exposed to market risk and his gain or loss depends on the

interest rate condition prevailing in the market. Floating rate is beneficial if

the interest rate falls in the future. A floating rate is considered non-

transparent and is also known as 'adjustable rate'.

Fourthly, if you decide to opt for a fixed rate loan, you can still switch to a

floating rate loan in the future and vice versa as and when rates go in your

favour and if you do decide to switch, you should take into account the cost

of doing so and the interest rate benefits of switching.

36

For a given interest rate, loan with a daily or monthly reducing balance is

better than an annual reducing balance loan. Interest rates vary depending

on the tenure of the loan, the amount of the loan and your personal profile.

3. Insurance covers (an added cost)

Also, many banks may insist on getting your home insured to safeguard

their interest. There are various kinds of insurance covers available for you.

Apart from getting the mandatory ones you should try to get insurance as

per your circumstances. You also have a choice of getting insured from

another company without any objection from your bank.

4. Other costs

The interest rates and EMIs are not the only cost factor. Rs. 1350/

documentation charges and 0.90% + service tax. Processing fees,

administration fees, valuation fee, legal fee, is to be paid when you apply for a

loan and other fees paid at closing.

Make sure you work out as to how much these other costs add up to. So even

though the interest rate may be lower, it usually adds up to being expensive. If

the EMIs may come out a lot more than what you can afford on a monthly

basis; try to redo the math with changes in the tenure and loan amount (if

possible).

5. Advance EMI

37

Advanced EMI is the number of equated monthly installments in the form

of post dated cheques, paid out in advance at the time of disbursement of

loan.

6. Document required

Most importantly, all deals and offers agreed upon are supported by relevant

papers. Self employed and salaried require different documents to support

the deal.

So make sure you always ask for a letter on the banks letterhead mentioning

the likes of, exact rate of interest, processing fees, pre-payment charges

along with interest-schedule.

Before signing the documents, make sure you recheck all terms and

conditions.

Do make sure you understand and agree with each of the clauses in the

documents. Do not sign any blank documents. Even if it takes you a few

hours to fill-up the form, please do so.

Do not leave anything for the executive to fill-up. It's always better to get a

legal opinion from someone on your loan papers. Do not under any

circumstance give any false information. This may amount to fraud and

could land you in trouble.

38

7. Penalties Once you have received the loan do your best to pay it back as

quickly as possible. But this early payment might invite a pre-payment

clause.

Banks make their money off the interest they charge and the sooner you pay

back a loan the less money you will have to pay in interest. When it comes

to Home loans, penalties are binding, like if you chose to pay up your entire

money before the tenure, a Pre-payment penalty is charged. So you should

know about such penalties beforehand to avoid future misunderstanding

between you and the bank.

8. Home loan glossary Confused in the Home Loan jargon? Our glossary

will help you in understanding the basic home loan related terms. Browse

through the glossary or search for a term through the menu to resolve any

doubts.

Glossary of Home Loan terms

A B C D E F G H I J K L M

N O P Q R S T U V W X Y Z

9. Acceptance Letter

Acceptance letter is the letter that a borrower or applicant provides on

reading the terms of the issue; and communicate his willingness to accept

the loan by way of an acceptance letter within a particular time frame which

39

varies between 1-3 months from the date of the sanction letter and also pay

the requisite administrative fee.

HOME LOAN IN INDIA

It is definitely one of the major things that you can board on in your

lifetime. The bad news is: however is that not everyone in this globe is like

40

you, loaded enough (financially, of course) to be able to build a house as

soon as he wants to.

Whether you are Non Resident Indian or Resident of India, and you are

thinking to start your journey of buying a new house, looking to move to a

new house, investing in property or are looking forward to refinance,

Consider answering these questions to yourself:

• Which type of home loan should I prefer?

• Will it be the best scheme that will be fitting my budget?

• Can any insurance plan cover for an unpaid monthly due?

• Is there a fine or penalty or even some reward as well if the whole

amount of loan is paid ahead of the due date?

These are just a dash of the questions to be answered when considering

taking the plunge…into the loan journey. The different home loan types are

hereby presented to you to make your journey that more smoother or step by

step, safer and comfortable. Yet, Got a fix on fixed rate or variable rates,

offset accounts, lines of credit or bridging loans!!

And we have covered the basics of your journey here. Going back to you

future house owner, have you got the answers to your questions? Start

answering them now and take the plunge!

With so many real estates sites coming up in Indian market, finding an ideal

house isn't that big a issue nowadays, when you can virtually see all across

the home you need to purchase by the various real estate simulation

programs and videos available, but you still need to purchase it, right? - To

really say "own" it. A home loan, also popularly identified as a mortgage, is

41

an easier financial option to own a house. Once you've decided to endeavor

on a home loan, there are so many things that you need to be informed with.

Not only is it going to be an emotional experience, it is also going to be a

very informative monetary journey, as you will be dealing with the whole

caboodle of the mortgage process along the way.

There are thousands of home loan companies waiting to provide you with

your financial needs. Part of the success of this whole financial move is

partly in your hands, the greater part relies on the efficiency of your chosen

mortgage company.

TYPES OF HOME LOAN

42

Owning a piece of land or property is a lifetime dream for every

individual. There are many home loans provider in the market to make your

dream come true. But before you opt for any home loan provider, you need

to consider certain factors related to property that you are interested in

buying and also about the salient features offered by a home loan provider

and also study some Home Loans and Home Insurance FAQs which helps

in applying a Home Loan in India.

And the most important thing is you should know about each and every

term related with Home Loans before applying for a Loan. It is always

advisable to consult a home loan expert or consultant before applying for a

home loan or purchasing a property.

You can take different types of home loans like Bridge Loans, Home

construction Loans, Home Equity Loans, Home Extension Loans, Home

Improvement Loans, Land Purchase Loans etc for different schemes

available in the market. There are different types of home loans tailored to

meet your needs.

• Home Purchase Loans: These are the basic forms of home loans

used for purchasing of a new home.

• Home Improvement Loans: These loans are given for implementing

repair works, healing and renovations in a home that has already been

purchased.

• Home Construction Loans: These loans are available for the

construction of a new home.

43

• Home Extension Loans: These loans are given for expanding or

extending an existing home. For e.g.: addition of an extra room etc.

• Home Conversion Loans: These loans are available for those who

have financed the present home with a home loan and wish to

purchase and move to another home for which some extra funds are

required. Through home conversion loan, the existing loan is

transferred to the new home including the extra amount required,

eliminating the need of pre-payment of the previous loan.

• Land Purchase Loans: These loans are available for purchasing land

for both construction and investment purposes.

• Bridge Loans: Bridge loans are designed for people who wish to sell

the existing home and purchase another one. The bridge loans help

finance the new home, until a buyer is found for the home.

Why take a Home Loan?

What's an average middle class Indian's most cherished dream? A date in

world trips in islands with Aishwarya Rai in complete solitude. This would

44

seem to be the answer from the maximum number of episodes of Kaun

Banega Crorepati (KBC), despite recently of course, when she has decided

to change her fortunes first with Abhishek!

Jokes apart, purchasing and moving into a dream house would generally

rank among the top three things on the wish list of most people. After all it’s

what been proved by Maslow’s Law of Hierarchy as well. That entire house

hunting every few years, grumpy landlords, killing rents would be a thing of

the past. Hey, you even get to use nails to hang your favorite paintings and

pictures. Don’t you???

Taking a home loan nowadays has become very simpler. The RBI has been

regularly slashing interest rates, with the result that housing finance loans

that came at an interest rate of 16.5% to 18% four years ago are now

available at 11.5% to 13% or lower. Each year the Finance Minister's

generosity during the Budget seems to be solely concentrated for the

housing sector and construction sector. The Budget 2000's allowed interest

payment up to Rs 1 lakh and principal payment of Rs 20,000 to be

exempted from income tax. To top it all, the Housing Finance Companies

(HFCs) are aggressively wooing customers. Now, when the sun shines, it’s

the best time to make hay. Isn’t it?

Check list for Home Loans

45

If you have arrived here by the help of search engine, we pre assume that

you are seeking some home loans to purchase a home or on the look out for

some information related to Home loans or Home Loan Types or you must

read some Home Loan Articles. Hereby, we present to you the home loan

documents checklist that you need to ensure is with you, before you apply

for a home loan. A basic checklist for home buyers like proper and clear

title and correct proposition will help you make a safe and informed

purchase. There are other home loan tools like calculators suitably devised

to assist you.

Confirmation of Income

• If you are a salaried person, please provide two recent consecutive

pay slips or a copy of your employment contract or a letter from your

employer.

• If you are self-employed, please provide copies of your last two

Financial Accounts as prepared by your accountant.

• Appointment Letter

• Salary Certificate

• Retainer ship Agreement, if appointed as a consultant

• FORM 16 issued by the employer in your name.

• Last three years income tax returns duly filed and certified by the

Income Tax Authorities

• Similar Document -separately for each co-applicant.

Employment Proof

46

• Identity card issued by your employer

• Visiting card

Age Proof

• Passport

• Voter's ID card

• PAN card

• Ration card

• Employer's Identity card

• School leaving certificate

• Birth certificate

Residence Proof

• Ration card

• Passport

• PAN card

• Rent agreement, if you are staying currently on rent

• Bank Pass book

• Allotment letter from your company if you are residing in company

quarters.

Name Change Proof (If Applicable)

A copy of the official gazette b. A copy of a newspaper advertisement

publicizing the name change c. Marriage certificate

47

Investment Proof (If Applicable)

• Bank statement for the last six months of all operating and salary

accounts

• Bank statements for the last six months of all current accounts, if self-

employed.

• Any other photocopies of investments held, if required by the Bank

Property Title Proof

• Original Sale agreement with Builder/Developer duly registered,

Registration receipt

• Tripartite agreement from builder/developer

• Land documents indicating ownership, e.g.- Photocopies of title

deeds, if applicable

• A certificate by the legal advisor of the builder to the effect that the

builder has a good reputation and it is free from encumbrance and

other charges.

• A certificate from builder's Chartered Accountant certifying that the

builder has not mortgaged the property anywhere else.

• Certified true copy of approved plan.

• Copies of receipts of payments made to builder/developer.

• Allotment letter

• Possession letter

• Lease agreement, if applicable (Property bought from a development

authority)

• Mortgage deed if the Bank opts for a registered mortgage.

48

• No Objection Certificate from the developer, society or development

authority as applicable

• Personal Guarantees, if applicable.

• In case of alternate or additional security, documents for the same

depending upon the security details.

• For self-construction: Approved plans and clearance certificates

along with estimates

• Post dated cheques for the EMIs.

Confirmation of Rental Income

Copy of the existing tenancy agreement, or a rental appraisal, from a local

real estate agent signed by branch manager, or rental manager.

Deposit or Investments

• Evidence of your deposit or investment funds, i.e. a bank statement or

term deposit receipt.

• For low equity loans (5-19% deposit), copy of your savings account

statements over the last six months.

Sale and Purchase Agreement

• If you are planning to buy a property, please provide a copy of the

successful sale and purchase agreement signed by both you and the

vendor.

• If you are planning to sell or have already sold your existing property,

please provide a copy of that property's sales and purchase

agreement.

49

New Customer to the banks of India

• If you are refinancing from another bank please provide copies of

your loan statements covering the last six months.

• Please provide copies of your account statements covering the last six

months from your current bank.

• Please provide copies of your identification and if you have arrived in

the country within the last 5 years, please provide a copy of your

passport.

Government Valuation and rating System

A copy of the latest Government or Ratings Valuation is to be provided.

Depending on the age and value indicated in conjunction with the amount

required to borrow, the Bank may require a Registered Valuation and your

Banker will advise you

New RBI Directive for Home Loans

50

The Reserve Bank of India (RBI) has in the latest directive asked the Indian

banks to be more "fair and transparent" while signing their agreements with

the consumers. This has come following complaints from various consumer

sections regarding home loans.

• It has emphasized on the fact that while giving a home loan, the

banks should not tie their loans with their own prime lending rates

(PLR) which often results in pro-bank and against consumer interest.

• Households should get credit counseling before signing any loan

agreement. In such case, banks should give credit counseling to

customer before giving a loan. Any non-governmental organization

can also give independent credit counseling to small borrowers.

• Consumers often complain of not receiving benefits of falling interest

rates as banks tie their floating rate loans with its PLR and even when

rates fall, the banks kept the PLR unchanged. But when interest rates

are hiked, the banks increase the benchmark rate, thus making

customers pay a higher rate and consequently increase the number of

EMIs too. The RBI has asked the banks to mend rules for the same.

• Individual borrowers should ask for the exact tenure and EMI while

taking a fixed rate loan. The RBI has also resolved to look into all

consumer complaints if it is bought to the regulator's notice.

51

• The IRDA (insurance regulator) has powers to take action against

banks if a customer feels cheated while buying an insurance product.

On its regulatory role, the RBI is trying to maintain a balance

between the extent of freedom granted to the banks and the objectives

of governance.

• RBI has made it mandatory for all banks - including private and

foreign banks - to offer a passbook to their customers with the

address and telephone number of the nearest branch.

• Customers have often been harassed by banks' call centers where

there is no accountability of the query made. The "do not call"

registry has also been flouted by banks as customers are bombarded

with unnecessary product offerings. The RBI has directed the Indian

Banks' Association to come out with a single "do not call" registry or

when a customer adds his name to a single bank registry it should

then stop unsolicited calls from all banks.

• On rising credit card frauds and wrong statements given by the banks,

the RBI has asked the customers to approach the ombudsman to

redress their problems. This way the RBI feels would inculcate more

consumer friendly practices among Indian banks.

52

Choosing the right home loan

If you are planning to buy home, you need to know about home loans

processes, troubleshooting and how to choose the right home loan for house

that falls within your budget. There are various types of home loans offered

53

by different financial institutions. You need to figure out which type of

home loan is beneficial for you.

Types of Home Loans Available:

• Home Equity Loans

• Home Extension Loans

• Home Improvement Loans

• Home Purchase Loans

• Land Purchase Loans

• Mortgage Loans

Many banks and financial companies offer home loans. But before choosing

any home loan option, consider few points as mentioned below.

Property Types: You should know more about type of property in lieu of

which you seek loan. There are loans offered by banks to Resident Indians

and NRIs for ready property, under construction property, self-construction

and home improvement.

Loan Tenure: The loans provided by financial institution are offered in

tenures or period of years. You should check out the tenure for loans

available in the market. There are loan tenures available for upto 25 years.

Repayment Options - You need to choose between fixed and floating rate

home loans. Many banks and financial institutions will provide you with the

option of switching from a floating rate home loan to a fixed rate home loan

once a year at no extra cost. But you need to check out the facts first with

the loan providing firm.

54

No Penalty option - There are also no penalty option offered by few

finance companies. In this mode, you can opt to pre-pay up to 25% of your

loan every year. Pre-payment is permitted after a minimum of 6 months

following loan disbursal.

Tax Benefits - You should know the right of your tax benefits on home

loans. Resident Indians are eligible for certain tax benefits on principal and

interest components of a housing loan under the Income Tax Act, 1961.##

List of Premium Banks Offering Home Loans:

• ICICI Bank - ICICI Bank Home Loan

• HDFC Bank - Adjustable Rate Home Loan

• Bank of India - Star Home Scheme

• Standard Chartered - Home Assist

• State Bank of India - SBI Unique Housing Scheme

• Bank of Baroda - Housing Offer

• Citibank- Building & Renovation of House

Always check with a financial home loan expert or financing company to

understand home loan processes and to avail the best bargain on your home

purchase.

55

• ELIGIBILITY

• DOCUMENTATION

• EXTENT OF LOAN

• RATE OF INTEREST

• REPAYMENT & SECURITY

• FEATURES & CONDITIONS OF PNB HOME

LOAN

PNB HOME LOAN

56

Punjab National Bank provides its customers with various Home loan

policies and features at highly competitive rates. They know the needs of

the Indian customers that they have to deal with, on a regular basis, and

provide the policies accordingly. The PNB Home Loan cater mainly to the

requirement of the middle class individuals of India, as Pnb itself is one of

the leading public –sector banks of the nation.

The PNB Home loans are very easily available, and have an even easier

process of repayment that is given over a prearranged time period. This

period of time is determined, when the PNB Home loans are being finalized

and along with the loans, the buyers get the opportunity of having a life

insurance covered against him. The basic grounds on which the PNB Home

loans are provided are:

• Extending, repairing, modification and even renovating of an already

existing building or flat.

• Purchase or building of a new house or flat.

The basic interest of the PNB Home loans may be around 9.5%, and the

time period may vary from a minimum of 5 years to a maximum of 25

years. However there is a certain limitation of the loan amount that an

individual may take from the bank. The maximum amount of the loan

amount sanctioned under PNB Home loans is need based. It generally

takes around 7 days to process the PNB Home loans, from the day it has

been finalized with the bank.

Apart from all these details, the PNB Home loans also enable us to choose

between fixed and floating rates that may be applicable from time to time,

and keep varying from one time period to another. As far as the eligibility is

57

concerned, a person between the age group of 18 to 60 years may be

qualified to apply for the PNB Home loans. Along with this, it has also to be

noted that the annual income of the individual, who is applying for the loan,

must be greater than or equal to 1.2 Lac INR.

Eligibility

• Age of the applicant must be less than 60 years.

• Existing home loan borrower can also apply provided their loan

account is regular and no IR irregularity persist.

Documents Needed

1. Proof of identity

2. Proof of income

3. Proof of residence

4. Bank statement or Pass Book where salary or income is credited.

5. Education Certificate

6. Photos

7. Salary slip & form 16

8. Income tax return last 3 years along with balance sheets.

9. Assets liabilities statements.

10. Documents of property.

11. Estimate of construction.

12. Guarantor

58

Freehold and Leasehold Property

1. The loan can be granted both for freehold and leasehold property.

2. In case of leasehold, loan can be granted on the basis of power of

attorney basis from original allotee where DDA/PUDA/HUDA permit

conversion of leasehold into freehold property otherwise advance is not

permitted against plot purchased on Power of Attorney basis.

Extent of loan

• For construction/purchased of house/flat 75% of the cost of

construction or purchase of house/flat.

• For carrying out repairs/renovation/additions/alternation: - 75% of the

estimated cost subject to maximum of Rs. 20 lacs.

• Loan upto Rs. 20 lacs for purchase of land/plot

• Loan is available maximum upto Rs. 2 lacs for furnishing.

Margin

Land/Plot 40%

Construction/repair/addition 25%

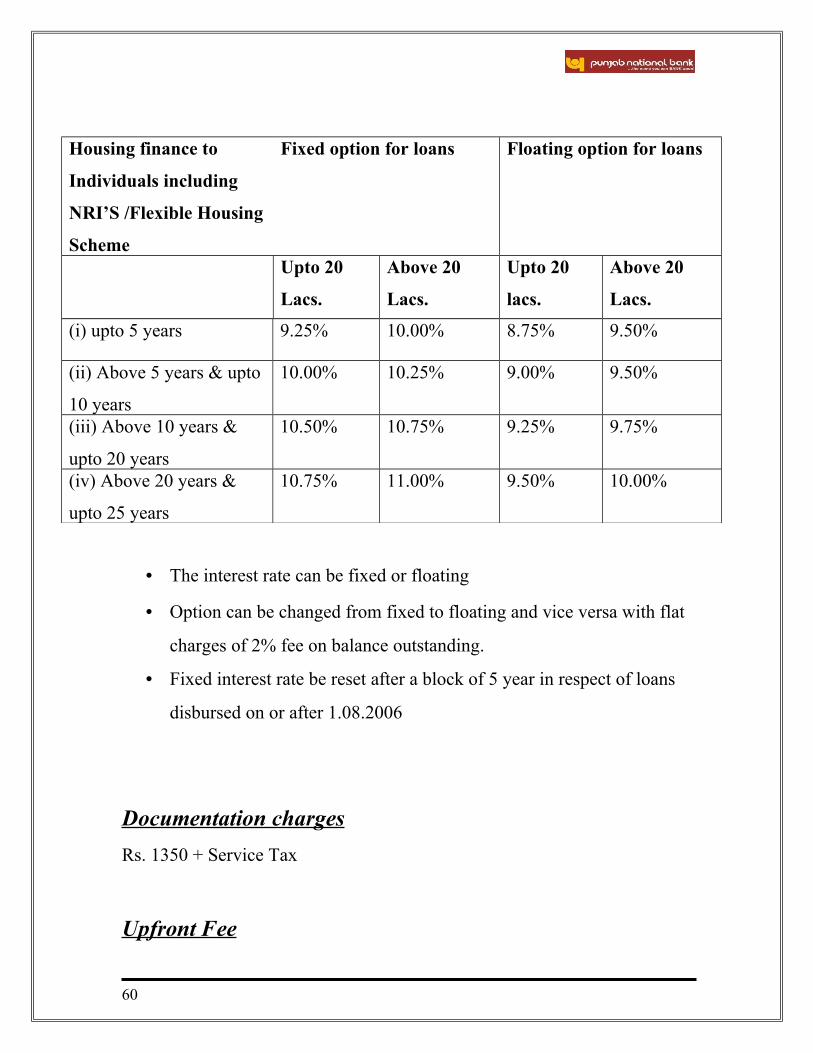

Rate of Interest

(Effective from 1st May 2009 – BPLR 11.00%)

59

Housing finance to

Individuals including

NRI’S /Flexible Housing

Scheme

Fixed option for loans Floating option for loans

Upto 20

Lacs.

Above 20

Lacs.

Upto 20

lacs.

Above 20

Lacs.

(i) upto 5 years 9.25% 10.00% 8.75% 9.50%

(ii) Above 5 years & upto

10 years

10.00% 10.25% 9.00% 9.50%

(iii) Above 10 years &

upto 20 years

10.50% 10.75% 9.25% 9.75%

(iv) Above 20 years &

upto 25 years

10.75% 11.00% 9.50% 10.00%

• The interest rate can be fixed or floating

• Option can be changed from fixed to floating and vice versa with flat

charges of 2% fee on balance outstanding.

• Fixed interest rate be reset after a block of 5 year in respect of loans

disbursed on or after 1.08.2006

Documentation charges

Rs. 1350 + Service Tax

Upfront Fee

60

0.90% of the loan amount + Service Tax& Education Cess

Repayment

• Maximum 25 years.

• Installment can be fixed upto maximum age of 65 years.

• The income of spouse and earning children can be taken into account

provided they are made co-borrower.

• Father/Mother can also be made co-borrower in cases property is in

single name of his /her son and also clubbing of their income is

permitted for determining eligibility criteria.

• Minimum 24 advance cheque should be obtained as and when, 6

cheques remain, fresh lot to be obtained out of 24, 23 cheques should

be of the amount equal to the balance.

• Loan is to be repaid in EMI within a period of 25 years or before the

borrower attains the age of 65 years.

Security

• Equitable/Registered mortgage of immovable property.

• Tripartite agreement be executed amongst Housing Board/ Dev

Authority / Coop Society / Builder the borrower and the bank where

mortgage cannot be created immediately.

• Equitable mortgage of other immovable property or pledge of NSC

etc. upto 125% of loan amount if property is being purchased from 1st

P/A holder and where there is delay in the execution of Tripartite

agreement.

61

• Verification of security is required once in 2 years.

Features

• Loan can be sanctioned by branch/hub near to the present place of

work/posting /residence of the borrower.

• Loan can be sanctioned even if property is in the name of

wife/parents provided that the owner is made co-borrower.

• Loan can be granted for 2nd house in the same city.

• Loan can be granted for purchase of house for rental purpose

• For take over, permission of higher authority is not required.

Important Conditions

Loan cannot be granted:

• For construction in Un-authorized colonies.

• If property is to be used for commercial purpose.

• Without approved Map.

62

• SUGGESTIONS & RECOMMENDATIONS• TROUBLESHOOTING TIPS FOR WOULD BE

HOME LOAN BUYERS

SUGGETIONS & RECOMMENDATIONS

63

There are some suggestions, which I would like to give the private

banks, which I noticed in my project. This are-

o Banks should improve the quality of their products (Specially Home

loan).

o Most of the private banks and public banks are much aggressive

about home loan than PNB. So, PNB should also be focus and

aggressive about its home loan products.

o In my project period I notice that many of the hidden costs are

accumulate with the services, which are not informed to the

customers at the first time, and then customers suffer many of the

problems. So, banks should disclose all the fee structure, terms &

conditions regarding the product before making sale.

o In the bank premises front office executives are not co-operative

with the customers. So, higher authority should keep control over

theses types of activities.

o Most the banks believe in large sales force than the quality sales

force, which are more competitive. So, banks should improve their

quality sales force, which include the competitive sales personnel.

Troubleshooting Tips for Would Be Home Buyers

64

Past few years have witnessed a paradigm shift in the scenario for home

loan seekers. However, things for the consumers were fairly good till mid-

2004. Property prices have been steady and the interest rates were at historic

lows.

Undoubtedly, the picture has much changed now. Real estate in India is

going through its own boom, with property prices going higher and higher

as there is no tomorrow. Also, there is no sign that this rise in underlying

property prices is going to slow down soon. This has widened the gap

between have and have not for a home loan consumer.

Though, there has been a great progress in the financial status of different

income groups but there are many other hassles along the way to add to the

woes of an interested home buyer.

With an increase in loan interest rates, it has been noticed that a consumer

gives away a major portion of his increased income as the down payment

and later as EMI. This is a story with every next typical consumer in a

metropolitan city. No wonder that the dream for owning a home is on the

verge of turning into a mirage for most middle class.

So what are the options left with a prospective home loan consumer?

• If you are planning to purchase a home for the purpose of your own

residence, then don't make your search a wild goose chase by trying

and wasting time in the market.

• If your dream house requires you to hunt a treasure to buy it, you may

consider a smaller property in the same area.

65

• But, if you are deciding to buy a house with the intention of selling it

for quick profits, then never fasten the process. Wait for the

overheated property market to cool. Meanwhile, work out your

budget and advantages before treating the property as an investment.

Let's view the top four problems faced by home loan consumers during

the pre-disbursement process as well as troubleshooting tips:

Problem I: Most times, the desired home loan amount is not available or if

available, then getting a fixed rate of interest is just like striving for

impossible. Moreover, there are a few financial institutions that provide the

home loan consumers with a promising interest rate.

- Get a promise that if you don't receive the home loan amount offered you

can press for a refund of your processing fee. Don't rely on words but take

it in writing or by mail.

Problem II: Generally, there is no guarantee that you will get your

processing fee back if the loan is not sanctioned or if the loan is sanctioned

then the individual does not want it.

-The situation seems a little complex unless promised in writing or in

advance.

Problem III: At times, loan amount gets restricted after being sanctioned

due to lower valuation of the property by the bank.

- You may ask your lender to get a valuation done before the sanction of the

loan so that this does not come as a surprise afterwards. Else, the bank will

evaluate it at one figure and you will be purchasing it at another. For that

66

reason, it is always recommend buying a property from a well known

builder.

Problem IV: Non availability of title documents and/ or NOCs in the

format desired by the bank. Or, problems with any other legal/ title

document.

- Most banks go through your legal documents with a discerning eye if they

are submitted along with a home loan application form. You are required to

check with the concerned builder/ society/ authority about the format of the

NOC that plays a critical role in the procedure. If they have a different

format, get that cleared from the bank to avoid messy disputes and

headaches later.

67

68

BIBLIOGRAPHY

BANKING LAW AND PRACTICE -- P.N. VARSHNEY

INDIAN CASES IN MARKETING -- NEELAMEGHAM , S.

WEB SITES:

www.pnbindia.com

www.guide2homeloan.com

www.google.com

69