2018 U.S. and Rochester Area

Economic Outlook

Gary Keith – Vice President, Regional Economist

Commercial Banking Division

January 26, 2018

Solid Economic Momentum Heading Into 2018

©2018 M&T Bank, Member FDIC

2013 2014 2015 2016 2017

U.S. Leading Indicators

Point to Further Expansion

“The Index…suggests that solid

economic growth will continue

into the first half of 2018”70

75

80

85

90

95

100

105

110

00 02 04 06 08 10 12 14 16 17

107R

E

C

E

S

S

I

O

N

The Conference Board

U.S. Leading Economic Index

Sources: U.S. Bureau of Labor Statistics, The Conference Board

3.5

4.0

4.5

5.0

5.5

6.0

6.5 Number of Non-farm Job Openings

Millions

5.9

Hiring Demand

Remains Robust

Strong hiring plans set the stage

for faster income and spending

growth in the coming year

R

E

C

E

S

S

I

O

N

Index:

2016=100

M&TBank 2

Upbeat Consumer Outlook Bodes Well For Spending

“After hitting a 17-year high in

November, expectations remain

at historically strong levels,

suggesting growth will continue

well into 2018”

Sentiment Has Moved Sharply Higher Over Past Year

©2018 M&T Bank, Member FDIC

National Federation of Independent Business

U.S. Small Business Optimism Index

90

92

94

96

98

100

102

104

106

108

110

112

114

116

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

The Conference Board

U.S. Consumer Confidence Index

85

90

95

100

105

110

115

120

125

130

135

140

145

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

97.6 average

since January 1990

122.1

104.9

2015 2016 2017

2015 2016 2017

Index:

1986=100

91.5 average

since January 1990

Index:

1985=100

Small Business Optimism Is At An All-Time High

“We haven’t seen this kind of

optimism in 34 years, and we’ve

seen it only once in the 44 years

that NFIB has been conducting

this research”

M&TBank 3

$52,000

$54,000

$56,000

$58,000

$60,000

$62,000

Constant 2016 Dollars

U.S. Real Median Household Income

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Household Income Has (Finally) Crossed an Important Threshold

Adjusted for inflation, household income is up 10.7%

since 2012 and is now 0.6% above the 1999 peak

$57,214 average

from 2000-07

$59,039

©2018 M&T Bank, Member FDIC

R

E

C

E

S

S

I

O

N

R

E

C

E

S

S

I

O

N

$53,331

$58,149

M&TBank 4Source: U.S. Census Bureau, “Income & Poverty in the United States: 2016,” September 2017

2.7%2.3%

1.6%

2.4%

3.3%

2.7%

1.8%

-0.3%

-2.8%

2.5%

1.6%

2.2% 2.4%

1.5%

2.4%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Sources: U.S. Bureau of Economic Analysis, Consensus Forecast

FORECAST

5

3.0% annual average

from 1990-2007

©2018 M&T Bank, Member FDIC

2018 Growth Should Improve…With Plenty of Wildcards!

The economy is expected to grow at a solid pace in 2018, with continued support

from consumer spending, improving global trade and bump from federal tax cuts

M&TBank

U.S. Real Gross Domestic Product Growth

How’s the

Rochester Area

Performing?

$62

$63

$64

$65

$66

$67

$65.6

Net Change in Output Since 2014

+$1.3 Billion

$64.3

Still Climbing Out of a Deep Hole

Although Rochester area real GDP

reached a post-recession high in 2017,

it rose by just 0.2% from 2016 levels—

well below the 1.6% U.S. average gain

Recession

Billions of Constant 2017 Dollars

Rochester Metro Area Real Gross Domestic Product

$66.3

E

S

T

I

M

A

T

E

D

M&TBank©2018 M&T Bank, Member FDIC 7Sources: U.S. Bureau of Economic Analysis, Moody’s Analytics, M&T Bank estimates

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

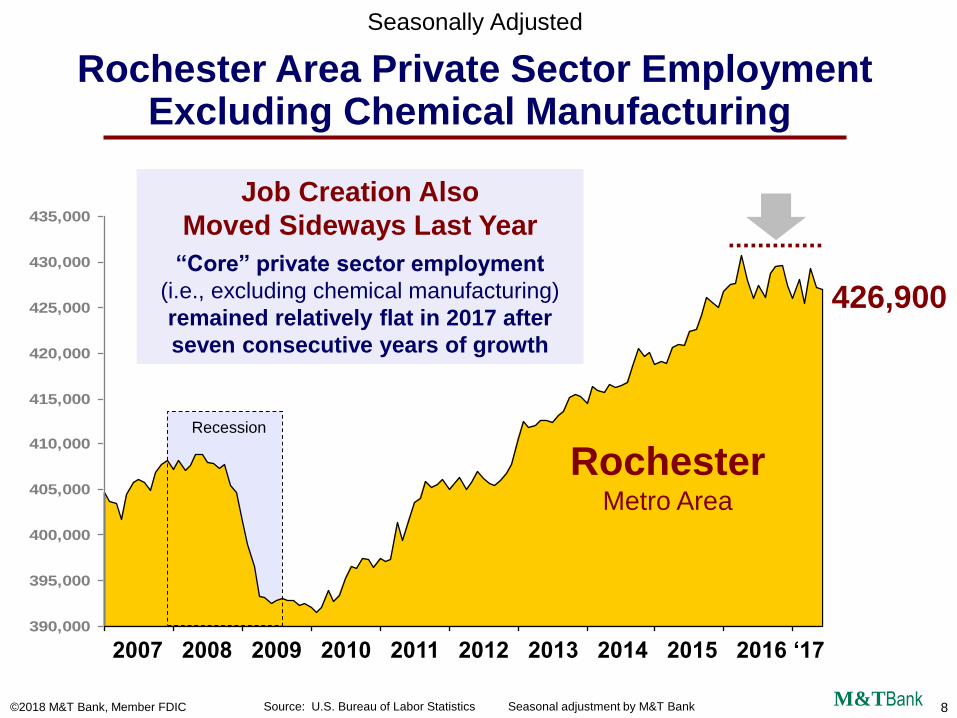

8

390,000

395,000

400,000

405,000

410,000

415,000

420,000

425,000

430,000

435,000

Seasonally Adjusted

Rochester Area Private Sector EmploymentExcluding Chemical Manufacturing

426,900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 ‘17

M&TBank©2018 M&T Bank, Member FDIC Source: U.S. Bureau of Labor Statistics Seasonal adjustment by M&T Bank 8

Recession

Job Creation Also

Moved Sideways Last Year

“Core” private sector employment

(i.e., excluding chemical manufacturing)

remained relatively flat in 2017 after

seven consecutive years of growth

RochesterMetro Area

M&TBank

3%

4%

5%

6%

7%

8%

9%

10%

Seasonally Adjusted

Rochester Area and U.S. Unemployment Rate

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

5.3%

4.1%Rochester data seasonally adjusted by M&T

9

July 2012

8.3%

UnitedStates

Nov. 2016

4.8%

“But Isn’t Labor Stress Continuing to Ease?”

While down three points since 2012, the Rochester area

jobless rate edged up slightly during the past year

RochesterMetro Area

©2018 M&T Bank, Member FDIC Sources: U.S. Bureau of Labor Statistics, New York State Department of Labor

So…Not Much

Good News to Get

Excited About?

-1%

0%

1%

2%

3%

4%

5%

6%

7%

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J

+6.1%

+6.5%

2015 2016 2017

Source: U.S. Bureau of Labor Statistics Seasonal adjustment by M&T Bank

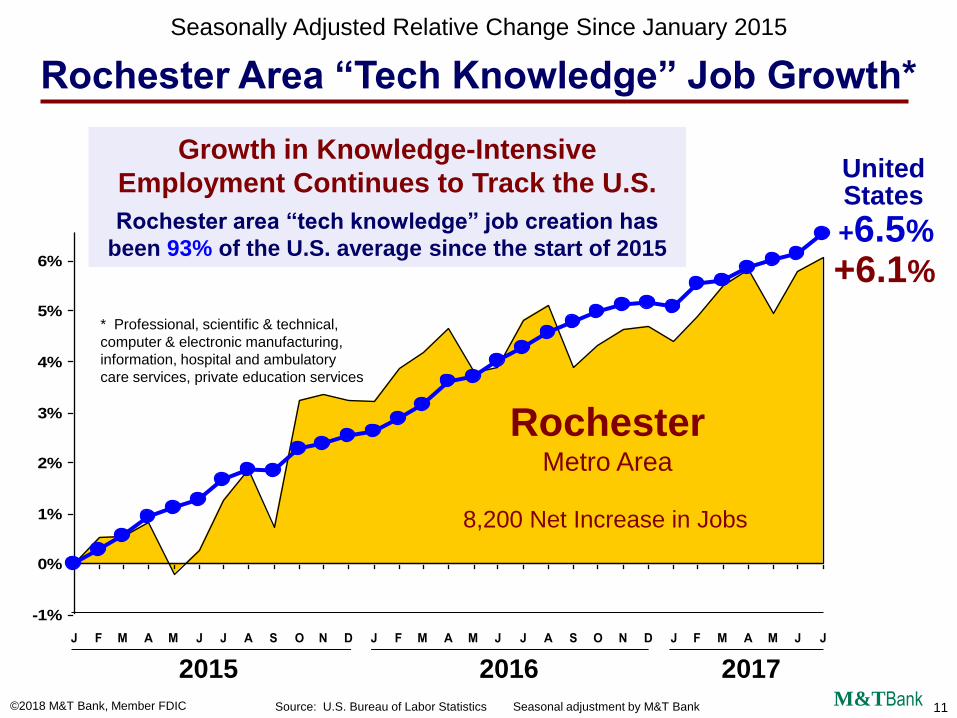

Seasonally Adjusted Relative Change Since January 2015

Rochester Area “Tech Knowledge” Job Growth*

Growth in Knowledge-Intensive

Employment Continues to Track the U.S.

Rochester area “tech knowledge” job creation has

been 93% of the U.S. average since the start of 2015

8,200 Net Increase in Jobs

United States

* Professional, scientific & technical,

computer & electronic manufacturing,

information, hospital and ambulatory

care services, private education services

11M&TBank©2018 M&T Bank, Member FDIC

RochesterMetro Area

12

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

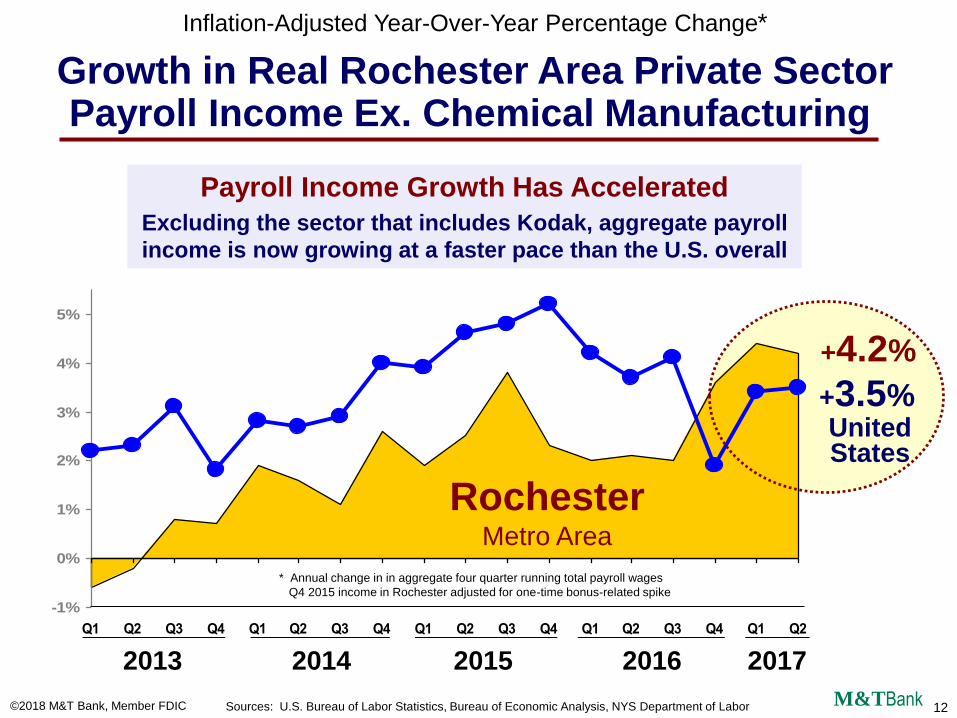

Inflation-Adjusted Year-Over-Year Percentage Change*

Growth in Real Rochester Area Private SectorPayroll Income Ex. Chemical Manufacturing

+4.2%

2013 2014 2015 2016 2017

+3.5%

* Annual change in in aggregate four quarter running total payroll wages

Q4 2015 income in Rochester adjusted for one-time bonus-related spike

M&TBank

UnitedStates

Payroll Income Growth Has Accelerated

Excluding the sector that includes Kodak, aggregate payroll

income is now growing at a faster pace than the U.S. overall

12

RochesterMetro Area

©2018 M&T Bank, Member FDIC Sources: U.S. Bureau of Labor Statistics, Bureau of Economic Analysis, NYS Department of Labor

13

$46,000

$48,000

$50,000

$52,000

$54,000

$56,000

Rochester Area Median Household Income

$56,300

Household Spending Power Climbs

For the Third Consecutive Year

Median household income has increased

by an estimated 10% since 2014—

matching the U.S. average and boosting

consumer spending and housing demand

06 07 08 09 10 11 12 13 14 15 16 17est

RochesterMetro Area

M&TBank13

Recession

$51,086

©2018 M&T Bank, Member FDIC Sources: U.S. Census Bureau, Bureau of Economic Analysis, M&T Bank estimate for 2017

0%

1%

2%

3%

4%

5%

Inflation-Adjusted Relative Change Since Q1 2014

Rochester Area Real Sales Tax Collections*

+5.2%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015 2016 2017

Consumer Spending Picked Up Steam

In the Second Half of 2017

NYS sales tax collections—a good proxy for

consumer spending trends—turned sharply higher

last year, suggesting that Rochester area

economic growth may be stronger than reported

Inflation-Adjusted

Sales Tax Collections* Four-quarter running total

M&TBank14Sources: U.S. Bureau of Economic Analysis, Bureau of Labor Statistics, NYS Dept of Taxation & Finance©2018 M&T Bank, Member FDIC

Inflation-Adjusted Year-Over-Year Percentage Change

Rochester Area Real GDP Growth Forecast

Sources: U.S. Bureau of Economic Analysis, M&T Bank forecast

Manufacturing Non-Manufacturing

Rochester U.S. Metro Area Average

-3.0%-3.4%

-12.1%

-9.9%

8.9%

-12.0%

-3.8%

-9.2%

3.3%

-6.9%

-1.4%

-15%

-10%

-5%

0%

5%

10%

06 07 08 09 10 11 12 13 14 15 16 17 18

Forecast Forecast

0.9%

1.7%

3.9%

1.1%

-0.3%

-1.2%

2.0%

2.7%2.5%

-0.1%

-2.1%

1.2%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

Two-Track Recovery Should Continue in 2018

Drag from contracting manufacturing output should diminish,

lessening downward pressure on growth in other sectors

M&TBank15

06 07 08 09 10 11 12 13 14 15 16 17 18

©2018 M&T Bank, Member FDIC

16

Impact on

Housing Demand

17

12,95113,133

13,977

15,247

14,802

2013 2014 2015 2016 2017

Rochester Regional Housing Market*

Closed & Pending Sales of Existing Homes

Total Closed Sales Pending Sales (At Year End)

Rising Income & Pent Up Demand Keep Sales Elevated…

While existing home sales dipped slightly in 2017, they remain high by

historic standards, propelled by improving household incomes, rising

consumer confidence and affordable mortgage rates

Source: Greater Rochester Realtors Association M&TBank©2018 M&T Bank, Member FDIC

* Monroe, Cayuga, Allegany, Genesee, Livingston, Ontario, Orleans, Seneca, Steuben, Wayne, Wyoming and Yates counties

17

12,772

13,257

14,372

15,22115,010

2013 2014 2015 2016 2017

18

5.1

4.5

4.0

2.82.5

Rochester Regional Housing Market*

Inventory of Existing Homes For Sale

Months Supply of Inventory

…Even as Available Supply Continues to Tighten

Inventory constraints are a major challenge, intensifying competition

for prime properties and putting upward pressure on pricing

M&TBank©2018 M&T Bank, Member FDIC 18Source: Greater Rochester Realtors Association

* Monroe, Cayuga, Allegany, Genesee, Livingston, Ontario, Orleans, Seneca, Steuben, Wayne, Wyoming and Yates counties

2013 2014 2015 2016 2017

5,446

5,0094,818

3,578

3,135

Inventory of Homes For Sale

2013 2014 2015 2016 2017

19

-0.8%

2.8%

-1.2%

4.0%

Rochester Regional Housing Market*

Median Price of Existing Homes Sold

Annual Change in Median Price

Net Result: Economics 101

Solid Demand + Less Supply = Positive Pricing Momentum

Limited inventory should continue to put upward pressure on pricing

M&TBank©2018 M&T Bank, Member FDIC 19Source: Greater Rochester Realtors Association

* Monroe, Cayuga, Allegany, Genesee, Livingston, Ontario, Orleans, Seneca, Steuben, Wayne, Wyoming and Yates counties

2014 2015 2016 2017

$124,000

$123,000

$126,500

$125,000

$130,000

Median Sales Price

2013 2014 2015 2016 2017

20

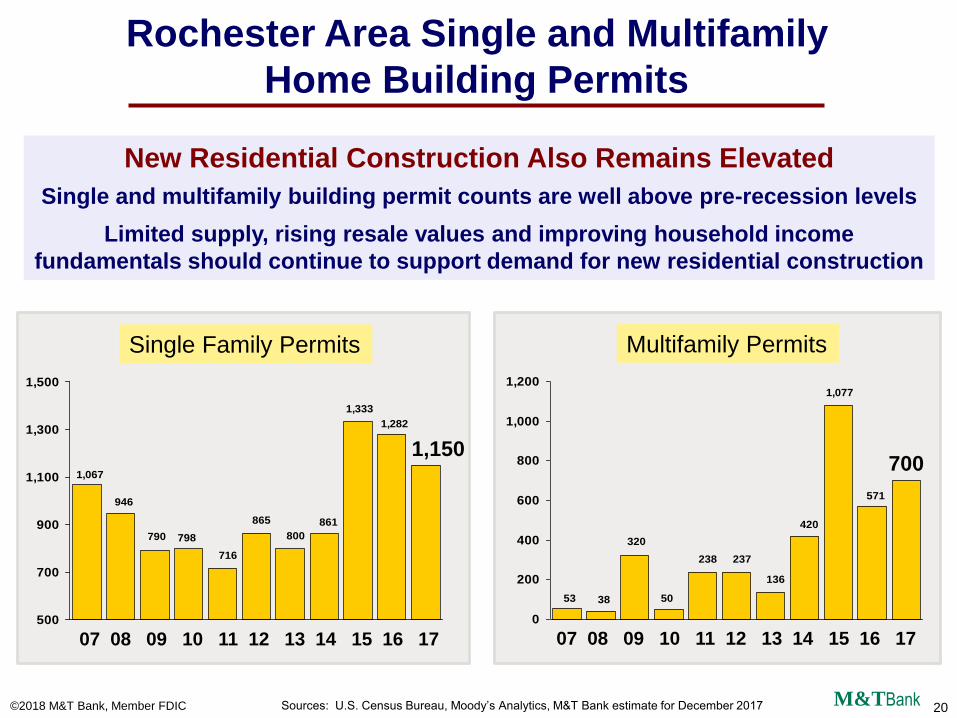

Rochester Area Single and Multifamily

Home Building Permits

Sources: U.S. Census Bureau, Moody’s Analytics, M&T Bank estimate for December 2017

716

865

946

1,067

790 798 800

861

1,333

1,282

500

700

900

1,100

1,300

1,500

07 08 09 10 11 12 13 14 15 16 17

M&TBank20

238 237

3853

320

50

136

420

1,077

571

0

200

400

600

800

1,000

1,200

07 08 09 10 11 12 13 14 15 16 17

7001,150

New Residential Construction Also Remains Elevated

Single and multifamily building permit counts are well above pre-recession levels

Limited supply, rising resale values and improving household income

fundamentals should continue to support demand for new residential construction

©2018 M&T Bank, Member FDIC

Multifamily PermitsSingle Family Permits

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Interest Rate ForecastJanuary 18, 2018

Forecast

©2018 M&T Bank, Member FDIC

2.50%2.36%

2.08%

21M&TBank

10 Year LIBOR swap

2 Year LIBOR swap

Monetary Policy Will Continue to Slowly Tighten,

But Remain Accommodative by Past Recovery Standards

The next Fed rate hikes are expected in March and July 2018 with one

more increase in 2019. Meanwhile, a tame inflation outlook will keep

downward pressure on medium- and long-term rates.

1 MonthLIBOR

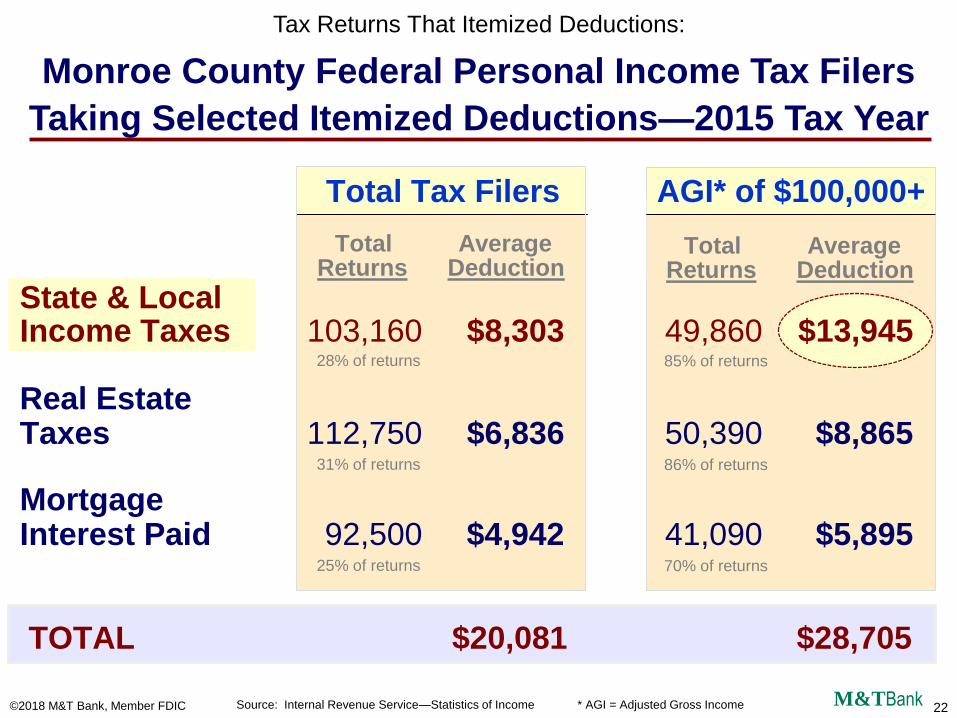

Total AverageReturns Deduction

State & LocalIncome Taxes 103,160 $8,303 49,860 $13,945

Real EstateTaxes 112,750 $6,836 50,390 $8,865

MortgageInterest Paid 92,500 $4,942 41,090 $5,895

TOTAL $20,081 $28,705

Source: Internal Revenue Service—Statistics of Income * AGI = Adjusted Gross Income

Tax Returns That Itemized Deductions:

Monroe County Federal Personal Income Tax Filers

Taking Selected Itemized Deductions—2015 Tax Year

Total AverageReturns Deduction

28% of returns 85% of returns

31% of returns 86% of returns

25% of returns 70% of returns

©2018 M&T Bank, Member FDIC 22M&TBank

Total Tax Filers AGI* of $100,000+

23

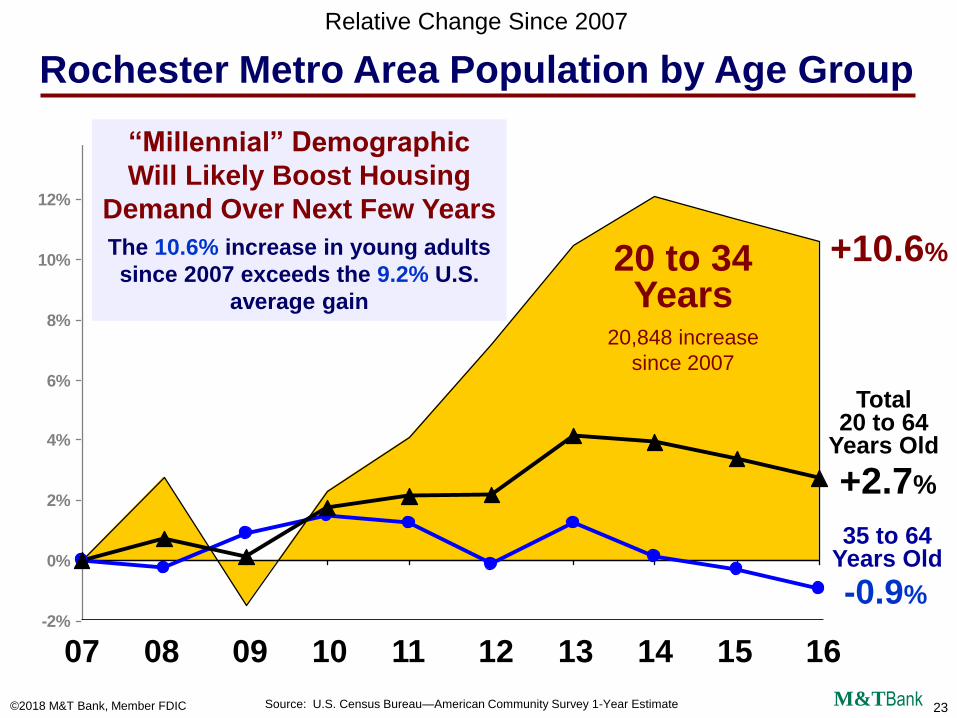

-2%

0%

2%

4%

6%

8%

10%

12%

14%

+10.6%

-0.9%

07 08 09 10 11 12 13 14 15 16

Relative Change Since 2007

Rochester Metro Area Population by Age Group

Total20 to 64

Years Old

+2.7%

35 to 64Years Old

20 to 34Years

20,848 increase

since 2007

23M&TBank

“Millennial” Demographic

Will Likely Boost Housing

Demand Over Next Few Years

The 10.6% increase in young adults

since 2007 exceeds the 9.2% U.S.

average gain

©2018 M&T Bank, Member FDIC Source: U.S. Census Bureau—American Community Survey 1-Year Estimate

24

Note: This presentation is for informational and educational purposes only. Nothing herein should be considered or relied upon as legal,

tax, accounting or financial advice. The author assumes no responsibility or liability for the specific applicability of the information

provided. Please consult your own legal counsel for any legal advice.