Additional Insured Coverage: Reconciling Business Contract Obligations and Policy Terms

Maximizing Existing Coverage and Resolving Disputes Betweenpresents Maximizing Existing Coverage and Resolving Disputes Between Additional and Named Insureds

presents

A Live 90-Minute Teleconference/Webinar with Interactive Q&AToday's panel features:

Joann M. Lytle, Partner, McCarter English, PhiladelphiaJustin L. Weisberg, Partner, Arnstein & Lehr, Chicago

Robert M. Fineman, Partner, Duane Morris, San Francisco

Tuesday, March 23, 2010

The conference begins at:1 pm Easternp12 pm Central

11 am Mountain10 am Pacific

CLICK ON EACH FILE IN THE LEFT HAND COLUMN TO SEE INDIVIDUAL PRESENTATIONS.

You can access the audio portion of the conference on the telephone or by using your computer's speakers.Please refer to the dial in/ log in instructions emailed to registrations.

If no column is present: click Bookmarks or Pages on the left side of the window.

If no icons are present: Click View, select Navigational Panels, and chose either Bookmarks or Pages.

If you need assistance or to register for the audio portion, please call Strafford customer service at 800-926-7926 ext. 10

For CLE purposes, please let us know how many people are listening at your location by

• closing the notification box • and typing in the chat box your

company name and the number of attendees.

• Then click the blue icon beside the box to send.

MONEY FOR NOTHING:Additional Insured Coverage

BByJoann M. Lytle, Esq.

McCarter & English, LLP

March 23, 2010

g ,BNY Mellon Center1735 Market Street, Suite 700Philadelphia, PA [email protected]

Information which is copyrighted by and proprietary to Insurance Services Office, Inc. ("ISO Material") is included in this publication. Use of the ISO Material is limited to ISO Participating Insurers and their Authorized Representatives. Use by ISO Participating Insurers is limited to use in those jurisdictions for which the insurer has an appropriate participation with ISO. Use of the ISO Material by Authorized Representatives is limited to use solely on behalf of one or more ISO Participating Insurers.

Wh t i Additi l I dWhat is Additional Insured Coverage?

Risk transfer method that allows one party Risk transfer method that allows one party to a business relationship to obtain coverage under another party’s policy

2

Who Are The Players?

Additional Insured – the party seeking to take advantage of another party’s coverage

Named Insured – the party whose policy is providing coverage to the Additional Insured

3

Additi l I d Additi lAdditional Insured vs. Additional “Named Insured”

Not the same thing Not the same thing “Additional Named Insured” has no generally

accepted meaningp g

4

Additional Named Insured

“A person or organization, other than the first p g ,named insured, identified as an insured in the policy declarations or an addendum to the policy declarations ”declarations.

“A person or organization added to a policy after the policy is written with the status of named yinsured. This entity would have the same rights and responsibilities as an entity named as an insured in the policy declarations ”

5

insured in the policy declarations….

Irmi Online - Glossary of Insurance and Risk Management Terms

Additional Insured

“A person or organization notA person or organization not automatically included as an insured under an insurance policy, but for whom p y,insured status is arranged, usually by endorsement. …”

Irmi Online - Glossary of Insurance and Risk Management Terms

6

Benefits for Additional Insured

Coverage without premium Doesn’t erode additional insured’s own limits

of liabilityof liability No responsibility for deductibles Particularly important for companies who are y p p

self-insured or who have retentions on their own policies

7

B fit f Additi l I dBenefits for Additional Insured (cont.)

Supports indemnity obligation, which only has value if the indemnitor has assets to fulfill it

Defense coverage without having to wait for a Defense coverage, without having to wait for a resolution of the indemnity obligation

Can be independent of, and provide broader p pprotection than, the indemnity obligation, i.e., for the additional insured’s negligence

Important where applicable state’s law prohibits

8

– Important where applicable state s law prohibits indemnification for one’s own negligence

Di d t f Additi lDisadvantages for Additional Insured:

No control over the defense No control over the defense– Significant where both the Named Insured and Additional

Insured are sued Limits must be shared among all insureds Limits must be shared among all insureds Often no business relationship with carrier

9

Implications for Named Insured

ProsAllows transfer of the obligation to defend and– Allows transfer of the obligation to defend and indemnify the indemnitee to the insurer

Cons– Erosion of limits– Limits shared by all insureds

Limits used to pay claims for which the Additional– Limits used to pay claims for which the Additional Insured may be partly or entirely at fault

– Responsibility for deductible

10– Higher premiums down the road based on loss

experience

R l ti hi Gi i Ri tRelationships Giving Rise to Additional Insured Coverage

Construction Construction– General contractor requires additional insured status on

subcontractors’ policies Vendor/VendeeVendor/Vendee

– Vendor requires additional insured coverage on manufacturer’s policy

Service AgreementService Agreement– Customer requires additional insured status on service

provider’s policy Building maintenance

11 Cafeteria operation

Relationships Giving Rise to Additional Insured Coverage (cont.)

Equipment Lease

– Lessor requires additional insured status on lessee’s insurance

12

R l Lif E lReal Life Example

Manufacturer leases equipment to Customer Customer installs equipment in its plant and uses equipment to q p p q p

manufacture insulation Explosion on one of the lines Very serious injuries to Customer’s employees, including

multiple deathsmultiple deaths Customer’s employees sue Manufacturer Manufacturer has multi-million dollar retention for products

claims on its own policy, and Manufacturer’s policy does not fimpose a duty to defend

Manufacturer makes claim as an Additional Insured against Customer’s policy for both defense and indemnification

13

H D O B AHow Does One Become An Additional Insured?

Generally requires both contract between the parties and an additional insured provision in anparties and an additional insured provision in an insurance policy

14

The Contract

An obligation to indemnify does not confer additional insured statusadditional insured status

Does the contract contain an insurance provision?p

– Does it require that the other party name your client as an additional insured?

– Does it specify the type and amount of insuranceDoes it specify the type and amount of insurance coverage to be provided? CGL, Umbrella? Primary or Excess?

15

Primary or Excess? Limits?

The Insurance Policy

A contractual obligation to provide insurance is ineffective unless the Named Insured’s policy contains an Additional Insured Clause

Usually in an endorsement Usually in an endorsement

16

T f Additi l I dTypes of Additional Insured Endorsements

Both ISO endorsements and manuscript endorsementsTwo varieties– Two varieties Blanket additional insured endorsements – grant

additional insured status to categories of Additional Insureds or to those whom the NamedAdditional Insureds or to those whom the Named Insured has a contractual obligation to insure– Sometimes called automatic additional

insuredsinsureds – If the contract does not specifically require

insurance, the endorsement is ineffectiveSched led additional ins red endorsements lists

17

Scheduled additional insured endorsements – lists the name of the additional insured

Verifying Additional InsuredVerifying Additional Insured Coverage

A certificate of insurance is not proof of iinsurance

The Acord form specifically states that dditi l i d iadditional insured coverage requires an

endorsement

18

19

Verifying Additional InsuredVerifying Additional Insured Coverage (cont.)

Ideally, request a full copy of the Named I d’ liInsured’s policy

May not be that simple– For some large companies, the extent of their

insurance program, including limits and deductibles, is a closely-guarded secret, y g

– In that situation, review the additional insured endorsement(s), at a minimum

20– Review the Other Insurance Clause, if possible

Whose Coverage is Primary?

Formerly a hotly-disputed issue ISO attempted to resolve the dispute in the CGL

policy itselfTh 2001 d l t i f th ISO CGL The 2001 and later versions of the ISO CGL Policy (CG 00 01 10 01) contain an amended Other Insurance Clause (Section IV)( )

21

ISO Other Insurance Clause

• States that the Named Insured’s policy is excess over any other policy on which “You” have beenover any other policy on which “You” have been added as an additional insured by way of endorsement

• Issues still arise when the other party’s insurance purports to provide only excess coveragecoverage

• Issues also arise concerning whose policy pays after the limits of the policy providing additional insured coverage are exhausted

23

insured coverage are exhausted

S Of Additi l I dScope Of Additional Insured Coverage

How broad is it? Does it essentially back-stop the Named Insured’s

contractual indemnity obligation?– Which clause appears first in the contract – indemnity or pp y

insurance? Does it cover more than the Additional Insured would be

able to recover under the Indemnity Agreement?– What if the indemnity agreement contains a monetary cap?– What if the insurance provision states that the Additional

Insured will receive coverage in the minimum amount of $ ?

24$________?

Scope of Additional InsuredScope of Additional Insured Coverage (cont.)

What if the indemnity agreement is f bl ?unenforceable?

– For example, an agreement that purports to indemnify the indemnitee for its own negligence?indemnify the indemnitee for its own negligence?

– In a state where such an agreement is void as against public policy?

25

Gilbrane Building Co. v. Empire Steel Erectors, L.P., No. H-08-

1707, 2010 U.S. Dist. Lexis 16512 (S.D.Tex. Feb. 23, 2010)

Parr, an employee of Empire Steel, a , p y p ,Subcontractor, fell off a ladder at a construction site and sued Gilbane Building Co., the General Contractor

– Admiral Ins. Co. argued that because the indemnity agreement in the Trade Contractor Agreement was unenforceable under TX law, Gilbane was not covered as an additional insured

– Court rejected this argument and noted that the indemnity and insurance provisions were separate clauses that do not reference each other are not intertwined or interrelated and on their face

26

each other, are not intertwined or interrelated, and on their face stand independently as separate obligations

Typical Additional Insured Claim

Contract requiring that general contractor

Subcontractor’sInsuranceCompany

Contract requiring that general contractorbe added as additional insured. Subcontractor

(Named Insured)General Contractor(Additional Insured)

Does additional insured’s liability to named insured’sInjured Employee

27

Does additional insured s liability to named insured semployee “arise out of” named insured’s ongoingoperations?

C f Additi l I d’Coverage for Additional Insured’s Own Negligence

Prior to 2004, a number of ISO additional insured endorsements provided coverage for liabilityendorsements provided coverage for liability “arising out of” the Named Insured’s operations for the Additional Insured

A number of courts construed “arising out of” to be the same as “but for” causationIf the liability would not have arisen “but for” the If the liability would not have arisen “but for” the named insured’s involvement, the additional insured has coverage

28

C f Additi l I d’Coverage for Additional Insured’s Own Negligence (cont.)

Township of Springfield v. Ersek, 660 A.2d 672 (Pa. Commw. 1995) (to nship as added to pro shop’s polic as additional1995) (township was added to pro shop’s policy as additional insured “with respect to liability arising out of operations performed by” pro shop; policy covered damages for injuries to pro shop’s employee, caused by township’s negligence, because p p p y y p g g“arising out of” means causally connected with, not proximately caused by)

Aetna Cas. & Surety Guar. Corp. v. Ocean Acc. & Guarantee C 386 F 2d 413 (3d Ci 1967) ( id d f i j iCorp., 386 F.2d 413 (3d Cir. 1967) (coverage provided for injuries to named insured’s employee, caused by additional insured’s sole negligence, where the additional insured’s liability would not have arisen “but for” its engagement by or association with the

29

g g ynamed insured)

Coverage for Additional Insured’sCoverage for Additional Insured’s Own Negligence (cont.)

Mid-Continent Cas. Co. v. Swift Energy Co., 206 F.3d 487 (5th Cir. 2000) (finding that injuries to named insured’s employee “arose out2000) (finding that injuries to named insured’s employee “arose out of” named insured’s operations, even if the cause of the injuries was the sole negligence of the additional insured)

McIntosh v. Scottsdale Ins. Co., 992 F.2d 251 (10th Cir. 1993) (festival patron injured on fairgrounds brought suit against township/additional insured. Festival operator’s insurer obligated to cover township, even though township stipulated that it was 100% negligent, since injuries “arose out of” Festival’s operations)eg ge t, s ce ju es a ose out o est a s ope at o s)

Dayton Beach Park No. 1 Corp. v. National Union Fire Ins. Co., 573 N.Y.S.2d 700 (N.Y. App. Div. 1991) (insurer was obligated to indemnify additional insured for its own negligence where policy provided coverage for liability “arising out of” operations performed by named

30

coverage for liability “arising out of” operations performed by named insured)

Th 2004 A d t t ISO’The 2004 Amendments to ISO’s Endorsements

In response to these cases, in 2004, ISO amended some of its most commonly-used additional insured endorsements to make clear that the additional insured’s sole negligence isthat the additional insured s sole negligence is not covered

Additional Insured only has coverage with respect to liability for BI or PD caused, in whole or in part, by the Named Insured’s conduct

31

Comparison Of Pre And PostComparison Of Pre- And Post-2004 Versions Of ISO CG 20 10

32

Did ISO’s Amendment ResolveDid ISO’s Amendment Resolve The Issue?

Maybe not In the Gilbane Building Co. case, Admiral

argued that since the complaint contained no ll ti f li th t fallegations of negligence on the part of

Empire (the Subcontractor/Named Insured) or anyone acting on its behalf the Generalor anyone acting on its behalf, the General Contractor was not covered

33

Did ISO’s Amendment Resolve theDid ISO’s Amendment Resolve the Issue? (cont.)

Court rejected Admiral’s argument and sided ith th G l C t twith the General Contractor:

– Parr (the employee) was statutorily barred from naming his employer the Subcontractor as anaming his employer, the Subcontractor, as a liable party because of the Workers’ Compensation bar

– Under Texas’s comparative responsibility statute, Parr’s own negligence is at issue, even if not pled Parr while acting in the scope of his employment for

34

Parr, while acting in the scope of his employment for Empire (and thus acting on behalf of Empire) was potentially responsible for his own injuries

Revised CG 20 10 Does Not LimitRevised CG 20 10 Does Not Limit Coverage To Vicarious Liability

American Empire Surplus Lines Ins. Co. v. C & F t S i lt I C N H 06Crum & Forster Specialty Ins. Co., No. H-06-004, 2006 U.S. Dist. LEXIS 33556 (S.D. Tex. May 23 2006) (language of endorsementMay 23, 2006) (language of endorsement requiring that Additional Insured’s liability arise, in whole or in part, out of Named , p ,Insured’s conduct, does not limit coverage to vicarious liability, but provides coverage

35where both Named Insured and Additional Insured are negligent)

Final Thoughts

Additional insured coverage may provide more – or less coverage than the parties anticipatedless – coverage than the parties anticipated

Review the actual insurance policy or the additional insured endorsements

Review indemnity and insurance provisions before contracts are signed

Caution the business units about signing contracts containing indemnity and/or additional insured clauses

36

Stafford Webinar Stafford Webinar Additional Insured CoverageAdditional Insured Coverage

March 23, 2010March 23, 2010

[email protected]@arnstein.comj g@j g@

© Justin Weisberg All Rights reserved© Justin Weisberg All Rights reserved

1

Indemnification versus additional insurance• Contractual Indemnification• Contractual Insured Requirements• Additional Insured Status

2

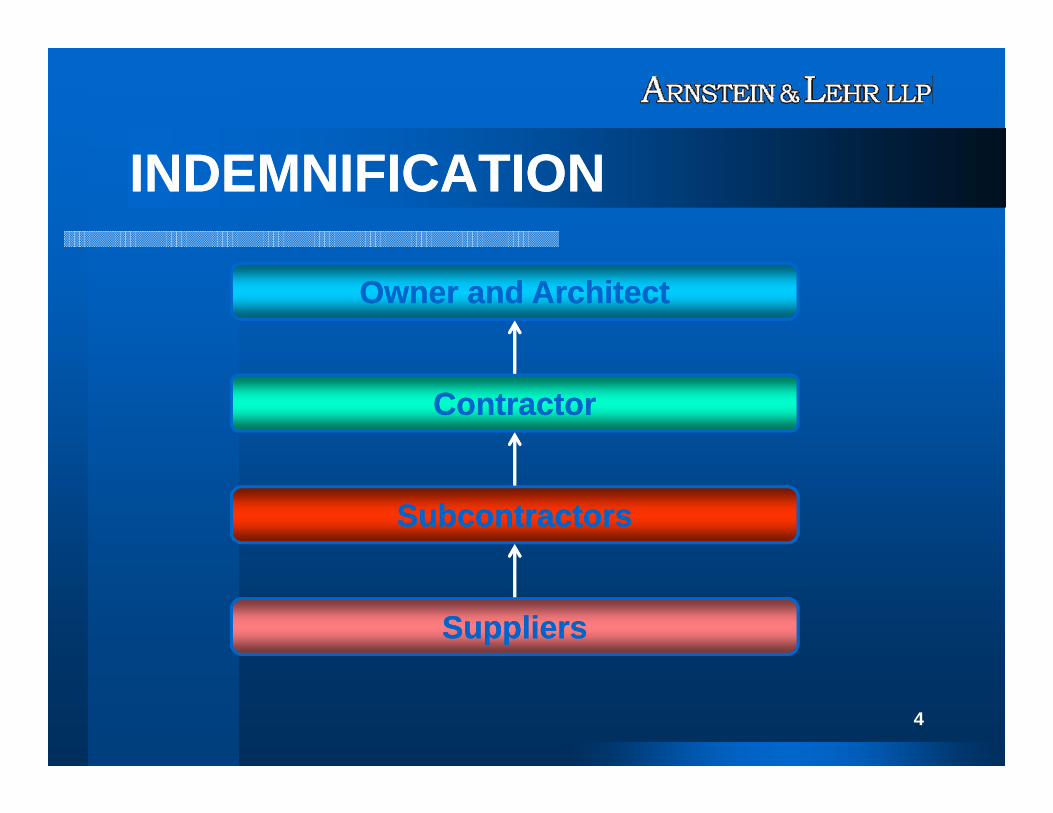

IndemnificationIndemnification

A duty to make good any loss, damage, or liability incurred by another and to the right of an injured party to claim reimbursement for its loss, damage or liability from a person who has such aliability from a person who has such a duty.

Black’s Law Dictionary 772 7th Ed. 1999

3

INDEMNIFICATIONINDEMNIFICATION

Owner and ArchitectOwner and Architect

ContractorContractor

SubcontractorsSubcontractors

SuppliersSuppliers

4

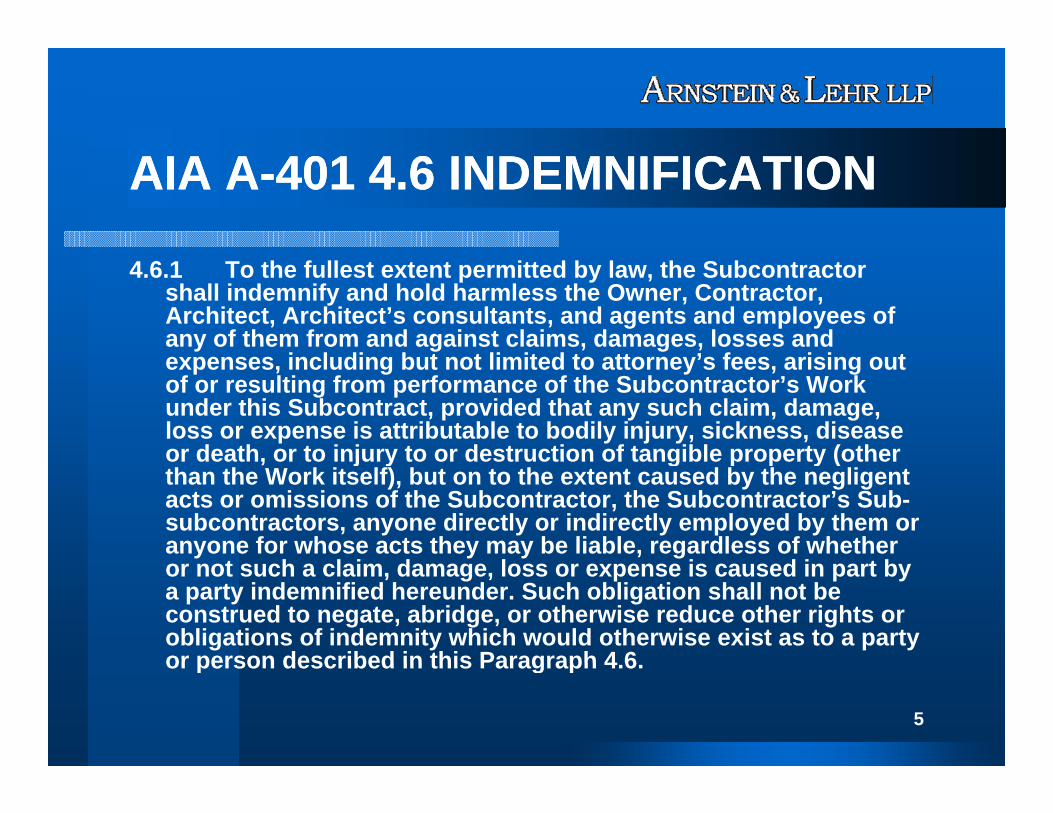

AIA AAIA A--401 4.6 INDEMNIFICATION401 4.6 INDEMNIFICATION

4.6.1 To the fullest extent permitted by law, the Subcontractor shall indemnify and hold harmless the Owner, Contractor, Architect, Architect’s consultants, and agents and employees of any of them from and against claims, damages, losses and

i l di b t t li it d t tt ’ f i i texpenses, including but not limited to attorney’s fees, arising out of or resulting from performance of the Subcontractor’s Work under this Subcontract, provided that any such claim, damage, loss or expense is attributable to bodily injury, sickness, disease or death or to injury to or destruction of tangible property (otheror death, or to injury to or destruction of tangible property (other than the Work itself), but on to the extent caused by the negligent acts or omissions of the Subcontractor, the Subcontractor’s Sub-subcontractors, anyone directly or indirectly employed by them or anyone for whose acts they may be liable, regardless of whether

t h l i d l i d i t bor not such a claim, damage, loss or expense is caused in part by a party indemnified hereunder. Such obligation shall not be construed to negate, abridge, or otherwise reduce other rights or obligations of indemnity which would otherwise exist as to a party or person described in this Paragraph 4 6or person described in this Paragraph 4.6.

5

EJCDC CEJCDC C--700700 To the fullest extent permitted by Laws and Regulations,

Contractor shall indemnify and hold harmless Owner and Engineer, and the officers, directors, members, partners, employees, agents, consultants and subcontractors of each and

f th f d i t ll l i t l dany of them from and against all claims, costs, losses, and damages (including but not limited to all fees and charges of engineers, architects, attorneys, and other professionals and all court or arbitration or other dispute resolution costs) arising out of or relating to the performance of the Work provided that anyof or relating to the performance of the Work, provided that any such claim, cost, loss, or damage is attributable to bodily injury, sickness, disease, or death, or to injury to or destruction of tangible property (other than the Work itself), including the loss of use resulting therefrom but only to the extent caused by any

li t t i i f C t t S b t tnegligent act or omission of Contractor, any Subcontractor, any Supplier, or any individual or entity directly or indirectly employed by any of them to perform any of the Work or anyone for whose acts any of them may be liable .

6

EJCDC CEJCDC C--700700 In any and all claims against Owner or Engineer or any of

their officers, directors, members, partners, employees, agents, consultants, or subcontractors by any employee (or the survivor or personal representative of such employee)the survivor or personal representative of such employee) of Contractor, any Subcontractor, any Supplier, or any individual or entity directly or indirectly employed by any of them to perform any of the Work, or anyone for whose acts p y , yany of them may be liable, the indemnification obligation under Paragraph 6.20.A shall not be limited in any way by any limitation on the amount or type of damages, compensation or benefits payable by or for Contractor orcompensation, or benefits payable by or for Contractor or any such Subcontractor, Supplier, or other individual or entity under workers’ compensation acts, disability benefit acts, or other employee benefit acts.

7

EJCDC CEJCDC C--700700 The indemnification obligations of Contractor

under Paragraph 6.20.A shall not extend to the liability of Engineer and Engineer’s officers, directors members partners employees agentsdirectors, members, partners, employees, agents, consultants and subcontractors arising out of:• the preparation or approval of, or the failure to

prepare or approve maps, Drawings, opinions,prepare or approve maps, Drawings, opinions, reports, surveys, Change Orders, designs, or Specifications; or

• giving directions or instructions, or failing to give them, if that is the primary cause of the injury or damage.

8

INDEMNIFICATIONINDEMNIFICATION

Intended beneficiary

Architect/owner

Agreement to assume the contractors Agreement to assume the contractors obligations

9

INDEMNIFICATIONINDEMNIFICATION

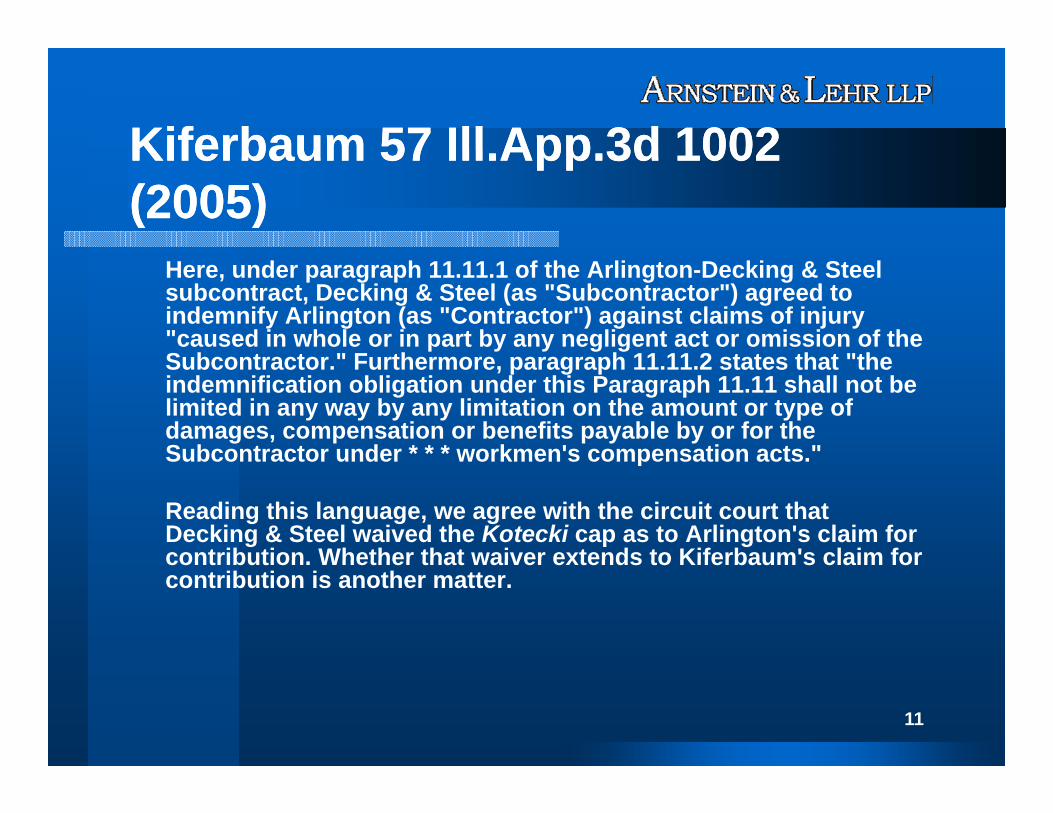

Kiferbaum 57 Ill.App.3d 1002 (2005)

General

Subcontractor

Subcontractor (Kotecki waiver)

10

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005)

Here, under paragraph 11.11.1 of the Arlington-Decking & Steel subcontract, Decking & Steel (as "Subcontractor") agreed to indemnify Arlington (as "Contractor") against claims of injury "caused in whole or in part by any negligent act or omission of the S b t t " F th h 11 11 2 t t th t "thSubcontractor." Furthermore, paragraph 11.11.2 states that "the indemnification obligation under this Paragraph 11.11 shall not be limited in any way by any limitation on the amount or type of damages, compensation or benefits payable by or for the Subcontractor under * * * workmen's compensation acts "Subcontractor under workmen s compensation acts.

Reading this language, we agree with the circuit court that Decking & Steel waived the Kotecki cap as to Arlington's claim for contribution Whether that waiver extends to Kiferbaum's claim forcontribution. Whether that waiver extends to Kiferbaum s claim for contribution is another matter.

11

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005) We also cannot agree with Kiferbaum's argument that the

Kotecki waiver in the Arlington-Decking & Steel subcontract extended to its own claim for contribution. Article I of the contract between Arlington and Decking &Article I of the contract between Arlington and Decking & Steel specifically incorporates the contract between Kiferbaum and Arlington, making it a part of the subcontract by reference. See Bransky v. Schmidt Motor y ySales, Inc., 222 Ill. App. 3d 1056, 1062 (1991) (where a contract incorporates another document by reference, its terms become part of the contract). Accordingly, we examine both contracts in determining whether Kiferbaumexamine both contracts in determining whether Kiferbaum was an intended third-party beneficiary of the Arlington-Decking & Steel subcontract.

12

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005) A third party has no rights to damages

from a breach of a contract entered into by others unless the agreed-to provision was intentionally included for the direct benefit of the third party It is not necessary thatof the third party. It is not necessary that the contract specifically name the third-party beneficiary if it adequately defines aparty beneficiary if it adequately defines a class of individual beneficiaries. Altevogt v. Brinkoetter, 85 Ill. 2d 44 (1981).

13

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005) With respect to construction contracts, it is not enough to

confer direct third-party-beneficiary status where the parties to the contract know, expect, or intend that a third party will benefit from the construction of a building in thatparty will benefit from the construction of a building in that they will be the users of it. The contract must be undertaken for the third party's direct benefit and the contract must affirmatively make such an intention clear. 155 Harbor Drive yCondominium Ass'n v. Harbor Point, Inc., 209 Ill. App. 3d 631 (1991). However, if the terms of a promise for which the promisee bargained with the promisor are to render a performance directly to the third party in nearly every caseperformance directly to the third party, in nearly every case the third party who is to receive performance will be the party intended to be benefited. Village of Fox Lake v. Aetna Casualty & Surety Co., 178 Ill. App. 3d 887, 911-12 (1989).

14

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005) Liability to a third party must appear affirmatively

in the contract language and the circumstances of the parties at the time of execution; it cannot b d d i l b th i tbe expanded simply because the circumstances justify or demand further liability. Ball Corp. v. Bohlin Building Corp., 187 Ill. App. 3d 175, 177(1989) Illinois courts require an express(1989). Illinois courts require an express provision indicating third-party-beneficiary status because of the strong presumption against construing it, and the presumption can only be g , p p yovercome by an implication so strong as to be practically an express declaration. Ball Corp., 187 Ill. App. 3d at 177.

15

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005) The Kiferbaum-Arlington contract contains no

provisions granting Kiferbaum any rights to enforce subcontracts between Arlington and

th b t t d it t iother subcontractors nor does it contain any provisions directing that any subcontracts undertaken by Arlington contain language designating Kiferbaum as an intended third-partydesignating Kiferbaum as an intended third-party beneficiary. Moreover, the Arlington-Decking & Steel subcontract contains no direct reference to Kiferbaum or any obligations by Decking & Steel y g y gtoward Kiferbaum. Therefore, we find that Kiferbaum has no rights to enforce the terms of the Arlington-Decking & Steel subcontract.

16

Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill App 3d 1002Kiferbaum 57 Ill.App.3d 1002 Kiferbaum 57 Ill.App.3d 1002 (2005)(2005) While we realize it may be of little solace to

Kiferbaum in this instance, we feel it incumbent upon us to advise general contractors to insert l i t f t t d d t t i ilanguage into future standard contracts requiring that their subcontractors designate the general contractor as an explicit third-party beneficiary of all subcontracts entered into in furtherance of theall subcontracts entered into in furtherance of the general contract. We believe such alterations would protect general contractors by providing them explicit rights of recovery in their p g yappurtenant subcontracts, and would prevent the future recurrence of the result we have just reached.

17

INDEMNIFICATIONINDEMNIFICATION

Kiferbaum

Incorporation clauseIncorporation clause

Sub-subcontractor’s Kotecki waiver did not flow to General Contractorto General Contractor

No requirement for sub-subcontractor to indemnify general contractor.indemnify general contractor.

But what about subcontractor’s indemnity obligation?obligation?

18

INDEMNIFICATIONINDEMNIFICATION

Loss must be attributable to bodily, injury, sickness, disease or death or damage to tangible property

19

INDEMNIFICATIONINDEMNIFICATION

Provisions generally exclude professional Provisions generally exclude professional actsacts

20

INDEMNIFICATIONINDEMNIFICATION

Does not include “the work itself” Does not include “the work itself” ((i ei e construction defects)construction defects)((i.e.i.e., construction defects), construction defects)

21

INDEMNIFICATIONINDEMNIFICATION

Only to the extent caused by the negligent acts or omissions of the contractor and its subcontractors

22

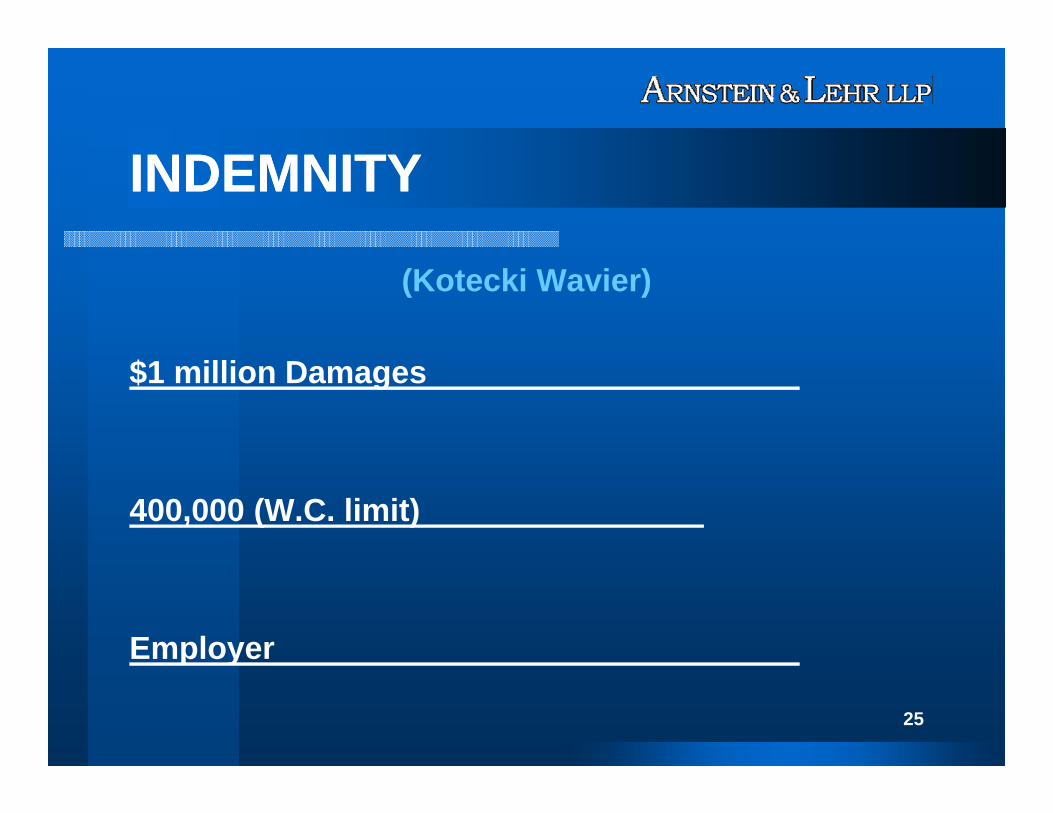

Braye v. ArcherBraye v. Archer--Daniels Midland Co.Daniels Midland Co.,,175 Ill.2d 201 (1997)175 Ill.2d 201 (1997)( )( )

Indemnitor can waive Kotecki Limits to Indemnitee

23

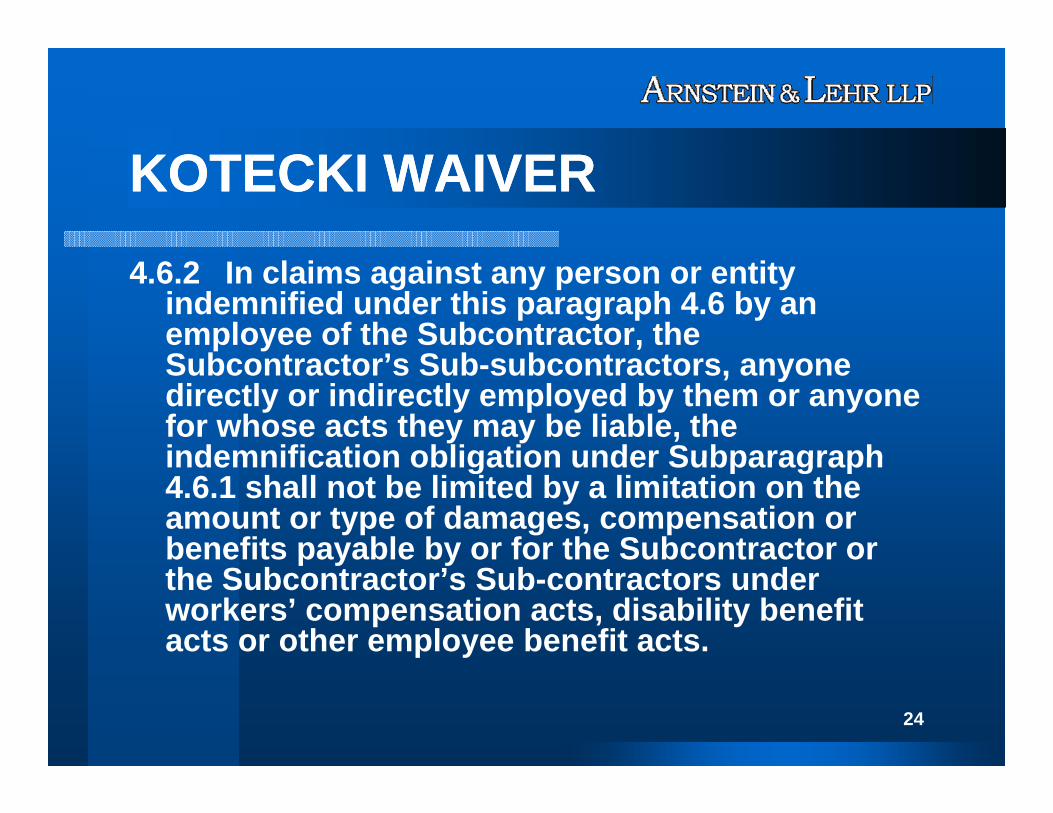

KOTECKI WAIVERKOTECKI WAIVER4.6.2 In claims against any person or entity

indemnified under this paragraph 4.6 by an employee of the Subcontractor, the S b t t ’ S b b t tSubcontractor’s Sub-subcontractors, anyone directly or indirectly employed by them or anyone for whose acts they may be liable, the indemnification obligation under Subparagraphindemnification obligation under Subparagraph 4.6.1 shall not be limited by a limitation on the amount or type of damages, compensation or benefits payable by or for the Subcontractor or p y ythe Subcontractor’s Sub-contractors under workers’ compensation acts, disability benefit acts or other employee benefit acts.

24

INDEMNITYINDEMNITY

(Kotecki Wavier)

$1 million Damages

400,000 (W.C. limit)

Employerp y

25

INDEMNIFICATIONINDEMNIFICATION

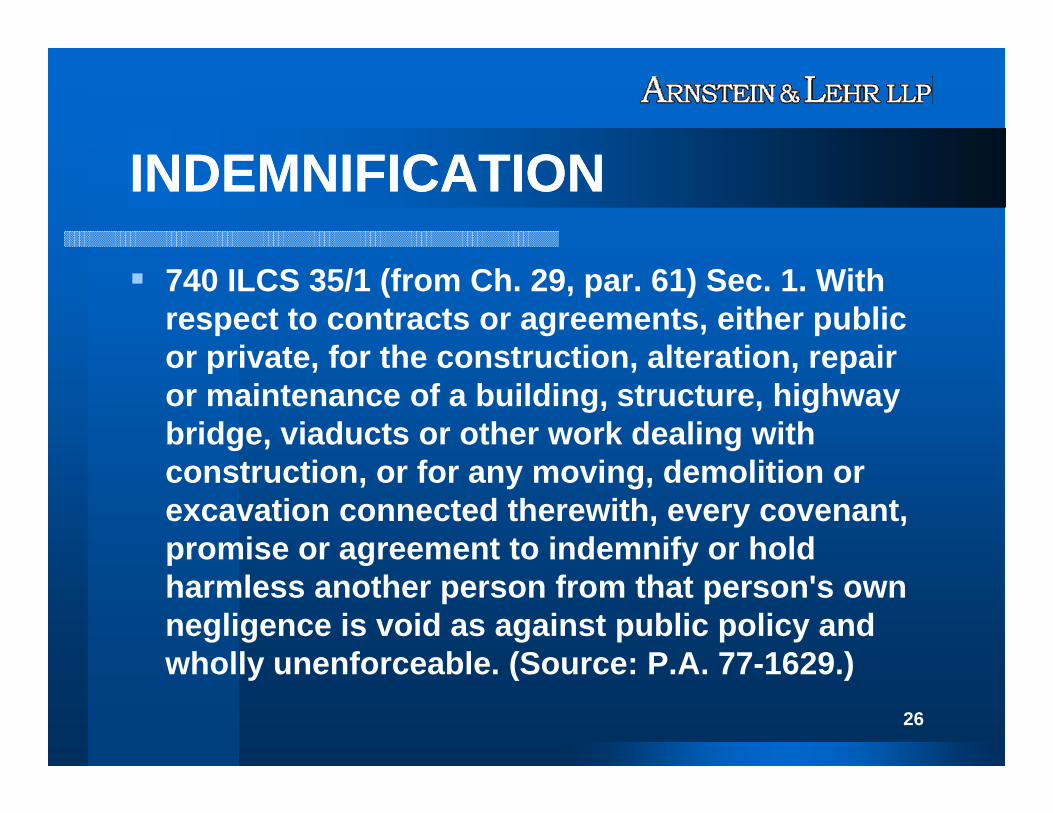

740 ILCS 35/1 (from Ch. 29, par. 61) Sec. 1. With respect to contracts or agreements, either public or private for the construction alteration repairor private, for the construction, alteration, repair or maintenance of a building, structure, highway bridge, viaducts or other work dealing with construction, or for any moving, demolition or excavation connected therewith, every covenant, promise or agreement to indemnify or hold p g yharmless another person from that person's own negligence is void as against public policy and wholly unenforceable (Source: P A 77 1629 )wholly unenforceable. (Source: P.A. 77-1629.)

26

INDEMNIFICATIONINDEMNIFICATION Can an exculpatory clause violate a Construction Contract

Indemnification For Negligence Act?

we find that the trial court correctly excluded paragraphs 9 02(B)we find that the trial court correctly excluded paragraphs 9.02(B), 9.W(A) and 9.W(C). As noted above, paragraph 9.W(A) stated that the terms of the contract did not "create, impose, or give rise to any duty in contract, tort or otherwise" owed by Baxter & Woodman to any other individual or entity. Paragraph 9.10(C) stated that Baxter & Woodman " ill t b ibl f th t i i f [th l"will not be responsible for the acts or omissions of [the general contractor] or of any [s]ubcontractor or any other individual or entity performing any of the Work." Paragraph 9.02(B) specifically incorporated all of the limitations set forth in paragraph 9.10, including the disclaimer of any duty in tort Paragraphs 9 10(A) and 9 02(B)the disclaimer of any duty in tort. Paragraphs 9.10(A) and 9.02(B) violate the Construction Contract Indemnification for Negligence Act, which precludes a party from contractually exempting itself from liability for its own negligence. See 740 ILCS 35/1 (West 2002). Dorris v. Baxter & Woodman (2008) Unpublished

27

INSURANCE COVERAGEINSURANCE COVERAGEINSURANCE COVERAGE INSURANCE COVERAGE IMPLICATIONSIMPLICATIONS Christy Foltz v. Safety Mutual Casualty

Corporation, 309 Ill.App.3d 686 (4th Dist. 2000)

• Additional liability not covered under• Additional liability not covered under workers compensation policy

• But see, Virginia Surety, 2007

28

INSURANCE COVERAGEINSURANCE COVERAGEINSURANCE COVERAGE INSURANCE COVERAGE IMPLICATIONSIMPLICATIONS Hankins v. Pekin, 305 Ill.App.3d 1088 (5th Dist.

1999)

• Contractual liability Exclusion

• Liability assumed in contract or agreement

• Not an “insured contract” and therefore not covered under CGL Policy

• Didn’t assume the tort liability of another• Didn t assume the tort liability of another29

INSURANCE COVERAGEINSURANCE COVERAGEINSURANCE COVERAGE INSURANCE COVERAGE IMPLICATIONSIMPLICATIONS“Insured Contract”

That part of any other contract or agreement pertaining to your Business under which you assume the tort liabilityunder which you assume the tort liability of another

30

INSURANCE COVERAGEINSURANCE COVERAGEINSURANCE COVERAGE INSURANCE COVERAGE IMPLICATIONSIMPLICATIONS Hankins v. Pekin, 305 Ill.App.3d 1088 (5th

Dist. 1999) Not “Insured Contract”

Michael Nicholas v. Royal Insurance Company, 321 Ill.App.3d 909 (2nd Dist. p y, pp (2001) “Insured Contract”

W t B d M t l I C West Bend Mutual Insurance Company v. Mulligan Masonry Company, 337 Ill.App.3d 698 (2nd Dist. 2003) “Insured Contract”698 ( st 003) su ed Co t act

31

INSURANCE COVERAGEINSURANCE COVERAGEINSURANCE COVERAGE INSURANCE COVERAGE IMPLICATIONSIMPLICATIONS Virginia Surety – Illinois Supreme Court, January

19, 2007

Typical Indemnity Provision which is limited to the negligence of the indemnitor does not indemnify assume the tort liability of another and therefore the obligation under such a provision is not covered under a standard CGL Policy Christy y yFoltz, Michael Nicholas, and West Bend are overruled.

32

Defense Obligation UnderDefense Obligation UnderDefense Obligation Under Defense Obligation Under Indemnification AgreementIndemnification Agreement Claims against indemnitee arise out of or are in

any way connected with" a negligent act or omission by indemnitor. UDC – Universal D l t CH2M Hill H033610 (C l A 1Development v. CH2M Hill, H033610 (Cal.App. 1-15-2010)

The person indemnifying is bound, on request of the person indemnified, to defend actions or proceedings brought against the latter in respect to the matters embraced by the indemnity but theto the matters embraced by the indemnity, but the person indemnified has the right to conduct such defenses, if he chooses to do so. California Civil Code § 2778Code § 2778

33

Contractual InsuranceContractual InsuranceContractual Insurance Contractual Insurance RequirementsRequirements § 11.1.1 The Contractor shall purchase from and maintain in a company or companies lawfully

authorized to do business in the jurisdiction in which the Project is located such insurance as will protect the Contractor from claims set forth below which may arise out of or result from the Contractor’s operations and completed operations under the Contract and for which the Contractor may be legally liable, whether such operations be by the Contractor or by a Subcontractor or by anyone directly or indirectly employed by any of them, or by anyone for whose acts any of them may be liable:may be liable:

.1 Claims under workers’ compensation, disability benefit and other similar employee benefit acts that are applicable to the Work to be performed;

.2 Claims for damages because of bodily injury, occupational sickness or disease, or death of the Contractor’s employees;

.3 Claims for damages because of bodily injury, sickness or disease, or death of any person th th th C t t ’ lother than the Contractor’s employees;

.4 Claims for damages insured by usual personal injury liability coverage; .5 Claims for damages, other than to the Work itself, because of injury to or destruction of

tangible property, including loss of use resulting therefrom; .6 Claims for damages because of bodily injury, death of a person or property damage arising

out of ownership, maintenance or use of a motor vehicle; .7 Claims for bodily injury or property damage arising out of completed operations; and .8 Claims involving contractual liability insurance applicable to the Contractor’s obligations

under Section 3.18.

AIA A-201 2007

34

Contractual InsuranceContractual InsuranceContractual Insurance Contractual Insurance RequirementsRequirements § 11.1.2 The insurance required by Section 11.1.1 shall be

written for not less than limits of liability specified in the Contract Documents or required by law, whichever coverage is greater. Coverages, whether written on ancoverage is greater. Coverages, whether written on an occurrence or claims-made basis, shall be maintained without interruption from the date of commencement of the Work until the date of final payment and termination of any coverage required to be maintained after final payment,coverage required to be maintained after final payment, and, with respect to the Contractor’s completed operations coverage, until the expiration of the period for correction of Work or for such other period for maintenance of completed operations coverage as specified in the Contract co p eted ope at o s co e age as spec ed t e Co t actDocuments.

AIA A-201 2007

35

Contractual InsuranceContractual InsuranceContractual Insurance Contractual Insurance RequirementsRequirements § 11.1.3 Certificates of insurance acceptable to the Owner shall be filed

with the Owner prior to commencement of the Work and thereafter upon renewal or replacement of each required policy of insurance. These certificates and the insurance policies required by this Section 11.1 shall contain a provision that coverages afforded under the policies will not becontain a provision that coverages afforded under the policies will not be canceled or allowed to expire until at least 30 days’ prior written notice has been given to the Owner. An additional certificate evidencing continuation of liability coverage, including coverage for completed operations, shall be submitted with the final Application for Payment as required by Section 9.10.2 and thereafter upon renewal or replacement ofrequired by Section 9.10.2 and thereafter upon renewal or replacement of such coverage until the expiration of the time required by Section 11.1.2. Information concerning reduction of coverage on account of revised limits or claims paid under the General Aggregate, or both, shall be furnished by the Contractor with reasonable promptness.

AIA A-201 2007

36

Contractual InsuranceContractual InsuranceContractual Insurance Contractual Insurance RequirementsRequirements § 11.1.4 The Contractor shall cause the

commercial liability coverage required by the Contract Documents to include (1) the Owner, the A hit t d th A hit t’ C lt tArchitect and the Architect’s Consultants as additional insureds for claims caused in whole or in part by the Contractor’s negligent acts or omissions during the Contractor’s operations;omissions during the Contractor s operations; and (2) the Owner as an additional insured for claims caused in whole or in part by the Contractor’s negligent acts or omissions during g g gthe Contractor’s completed operations.

AIA A-201 2007AIA A 201 2007

37

Contractual InsuranceContractual InsuranceContractual Insurance Contractual Insurance RequirementsRequirements Generally the obligation to name a party as an

additional insured has been determined to be a duty to procure insurance rather than a duty to i d ifindemnify.

Accordingly, in Illinois for example the duty to procure insurance has been determined not to be i i l ti f th Illi i A ti I d ifi ti A tin violation of the Illinois Anti-Indemnification Act even if the Subcontractor must provide insurance to cover the contractor for its own negligence. St John v City of Naperville 155 Ill App 3d 919St. John v. City of Naperville, 155 Ill.App.3d 919, 508 N.E.2d 1128, 1131-1132 (2nd Dist. 1987); Lehman v. IBP, 265 Ill.App.3d 117, 639 N.E.2d 152, 156 (3rd Dist. 1994) ( )

38

ADDITIONAL INSUREDADDITIONAL INSURED

WHO IS AN INSURED (Section II) is amended to include as an insured the person or organization shown in the Schedule, but only with respect to liability arising out of “your work” for that insuredarising out of “your work” for that insured by or for you.

CG 20 10 11 85

39

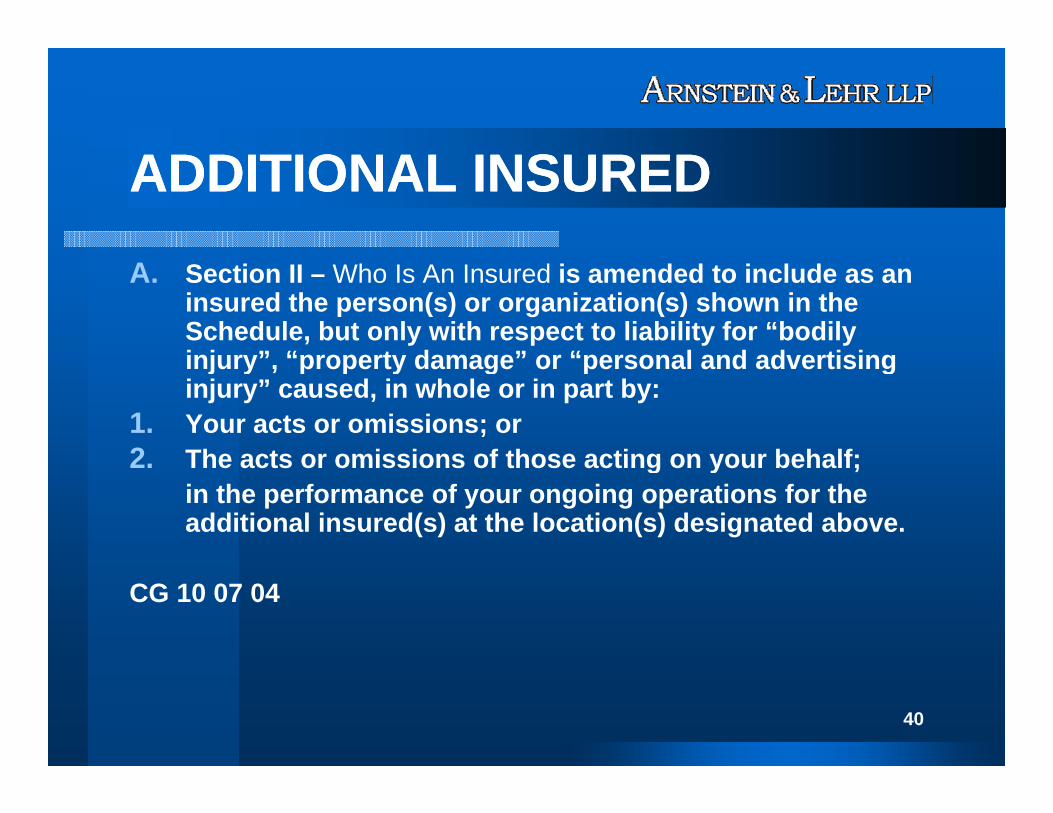

ADDITIONAL INSUREDADDITIONAL INSUREDA. Section II – Who Is An Insured is amended to include as an

insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for “bodily injury” “property damage” or “personal and advertisinginjury”, “property damage” or “personal and advertising injury” caused, in whole or in part by:

1. Your acts or omissions; or2 The acts or omissions of those acting on your behalf;2. The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

CG 10 07 04

40

ADDITIONAL INSUREDADDITIONAL INSUREDB. With respect to the insurance afforded to these additional

insureds, the following additional exclusions apply:This insurance does not apply to “bodily injury” or “property

damage” occurring after:g g1. All work, including materials, parts or equipment furnished in

connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations h b l t dhas been completed; or

2. That portion of “your work” out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as part of theengaged in performing operations for a principal as part of the same project.

CG 10 07 04

41

ADDITIONAL INSUREDADDITIONAL INSURED

Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for “bodily injury” or “ t d ” d i h l i t b“property damage” caused, in whole or in part, by “your work” at the location designated and described in the schedule of this endorsement performed for the additional insured and includedperformed for the additional insured and included in the “products-completed operations hazard.”

CG 20 37 07 04CG 20 37 07 04

42

ADDITIONAL INSUREDADDITIONAL INSURED

Section II – Who Is An Insured is amended to include as an insured the person or organization shown in the Schedule g(hereinafter referred to as “additional insured”), but only with respect to its vicarious liability for damages because of y g“bodily injury” or “property damage” directly caused by the Named Insured’s acts or omissions at the location designated and d ib d i th S h d l f thidescribed in the Schedule of this endorsement and included in the “products –completed operations hazard”

43

THE HISTORY OF TARGETEDTHE HISTORY OF TARGETEDTHE HISTORY OF TARGETED THE HISTORY OF TARGETED TENDER IN ILLINOISTENDER IN ILLINOIS The right of a contractor or owner to

demand that a subcontractor’s insurer provide primary non-contributory coverage when the contractor has been named as an additional insured on thenamed as an additional insured on the subcontractor’s policy.

44

THE HISTORY OF TARGETEDTHE HISTORY OF TARGETEDTHE HISTORY OF TARGETED THE HISTORY OF TARGETED TENDER IN ILLINOISTENDER IN ILLINOIS Institute of London Underwriters v.

Hartford Fire Insurance Co., 240 Ill.App.3d 70 (1992)

Contractor may select additionalContractor may select additional insurance policy and instruct its own policy not to contribute.policy not to contribute.

45

THE HISTORY OF TARGETEDTHE HISTORY OF TARGETEDTHE HISTORY OF TARGETED THE HISTORY OF TARGETED TENDER IN ILLINOISTENDER IN ILLINOIS Bituminous Casualty Corp. v. Royal

Insurance Co. of America, 301 Ill.App.3d 720 (1998)

If an insured does not select its ownIf an insured does not select its own insurer, the targeted insurer cannot demand contribution from additionaldemand contribution from additional insured’s own insurance policy pursuant to other insurance clase.

46

THE HISTORY OF TARGETEDTHE HISTORY OF TARGETEDTHE HISTORY OF TARGETED THE HISTORY OF TARGETED TENDER IN ILLINOISTENDER IN ILLINOIS Alcan United Inc. v West Bend Mutual

Insurance Co., 303 Ill.App.3d.72 (1999)

An “other insurance” clause in a policy will not automatically reach intowill not automatically reach into coverages provided under other policies merely because such other policies are inmerely because such other policies are in existence.

47

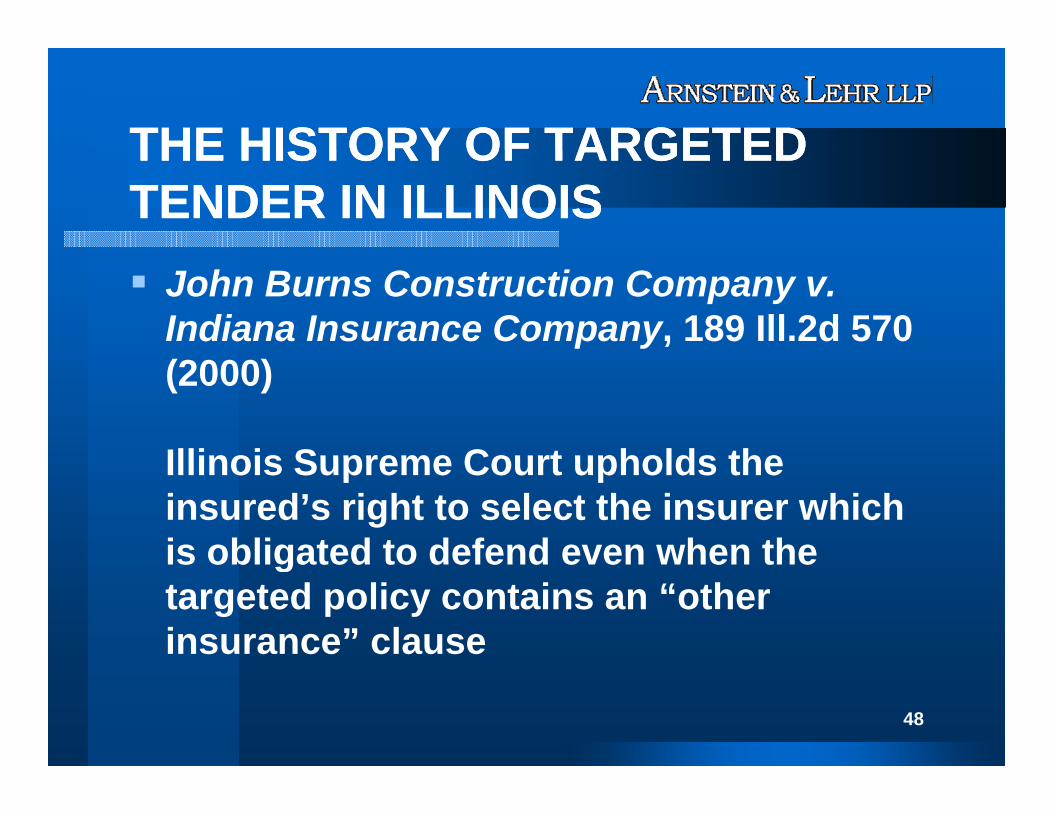

THE HISTORY OF TARGETEDTHE HISTORY OF TARGETEDTHE HISTORY OF TARGETED THE HISTORY OF TARGETED TENDER IN ILLINOISTENDER IN ILLINOIS John Burns Construction Company v.

Indiana Insurance Company, 189 Ill.2d 570 (2000)

Illinois Supreme Court upholds theIllinois Supreme Court upholds the insured’s right to select the insurer which is obligated to defend even when theis obligated to defend even when the targeted policy contains an “other insurance” clause

48

Targeted TenderTargeted Tender

However, under Illinois law an excess policy has no obligation to provide defense or indemnity until all primary policies are exhausted. Kajimauntil all primary policies are exhausted. Kajima Const. v. St. Paul, 227 Ill.2d 102, 114 (2007).

In addition, a contract that requires a contractor to name a party as an additional insured butto name a party as an additional insured, but does not specify whether the policy is primary does not require that contractor to provide primary noncontributory coverage to theprimary noncontributory coverage to the additional insured. River Village v. Central Insurance, Co. 1-08-3529 (5th Dist. 2009).

49

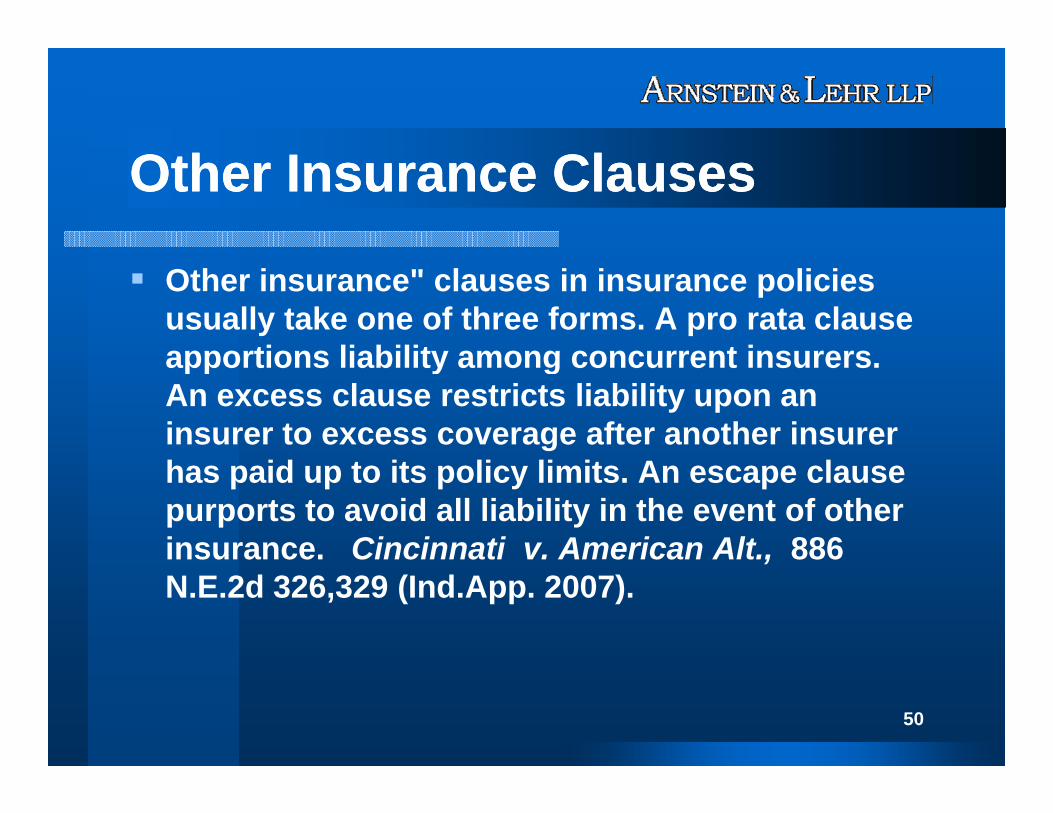

Other Insurance ClausesOther Insurance Clauses

Other insurance" clauses in insurance policies usually take one of three forms. A pro rata clause apportions liability among concurrent insurersapportions liability among concurrent insurers. An excess clause restricts liability upon an insurer to excess coverage after another insurer has paid up to its policy limits. An escape clause purports to avoid all liability in the event of other insurance. Cincinnati v. American Alt., 886 ,N.E.2d 326,329 (Ind.App. 2007).

50

Other Insurance ClausesOther Insurance Clauses

Cincinnati Policy Pro rata allocation

A. If there is other applicable liability insurance, "we" will pay only "our" share of the loss "Our" share is the proportionof the loss. Our share is the proportion that "our" limit of liability bears to the total of all applicable limits. Any insurance "we" provide for a vehicle "you" do not own shall be excess over any other collectible insurancecollectible insurance. . . .

51

Other Insurance ClausesOther Insurance Clauses

AAIC Policy Excess

For any covered "auto" you own, this Coverage Form provides primary insurance. For any covered "auto" you don't own, the insurance provided by this C F i thCoverage Form is excess over any other collectible insurance. . . .

52

Other Insurance ClausesOther Insurance Clauses

Lamb-Weston, Inc. v. Oregon Auto. Ins. Co., 219 Or. 110, 341 P.2d 110 (1959). As adopted by our supreme court this ruleadopted by our supreme court, this rule provides, "where `other insurance' clauses conflict, . . . they are to be ignored , y gand each insurer is liable for a prorated amount of the resultant damage not to exceed his policy limits In such a caseexceed his policy limits. In such a case, there exists dual primary liability." Id. at 407

53

Other Insurance ClausesOther Insurance Clauses If the language of a policy is clear and unambiguous, we

give the language its plain and ordinary meaning. The power to interpret contracts does not extend to changing their terms and we will not give insurance policies antheir terms, and we will not give insurance policies an unreasonable construction. If, in fact, it is impossible to reconcile competing "other insurance" clauses by reference to the ordinary rules of contract interpretation, y p ,then there might be room to invoke the Lamb-Weston rule. Such cases should be relatively rare. First and foremost, we should make every attempt to discern the intent of the parties who drafted "other insurance" clauses by referenceparties who drafted other insurance clauses by reference to the language of the policies. Cincinnati v. American Alt., at 886 N.E.2d 332.

54

Other Insurance ClausesOther Insurance Clauses

Here, we readily conclude that the "other insurance" clauses are reconcilable and provide that Cincinnati's policy provides sole primary coverage for this accident, with AAIC's policy only providing excesswith AAIC s policy only providing excess coverage upon exhaustion of the limits of the Cincinnati policy. Cincinnati v.the Cincinnati policy. Cincinnati v. American Alt., at 886 N.E.2d 332.

55

Equitable SubrogationEquitable Subrogation An insurer's cause of action for equitable subrogation

contains six elements: (1) the insured has suffered a loss for which the party to be charged is liable; (2) the insurer has compensated for the loss; (3) the insured has existing,has compensated for the loss; (3) the insured has existing, assignable causes of action against the party to be charged, which the insured could have pursued had the insurer not compensated the loss; (4) the insurer has suffered damages caused by the act or omission whichsuffered damages caused by the act or omission which triggers the liability of the party to be charged; (5) justice requires that the loss be shifted entirely from the insurer to the party to be charged; and (6) the insurer's damages are in a stated sum, which is usually the amount paid to the a stated su , c s usua y t e a ou t pa d to t einsured, assuming the payment was not voluntary and was reasonable. Gulf Insurance Company v. TIG Insurance Co.,86 Cal.App.4th 422, 432 (2nd Dist 2001)

56

ADDITIONAL INSURED STATUSADDITIONAL INSURED STATUSADDITIONAL INSURED STATUS ADDITIONAL INSURED STATUS VERSUS INDEMNIFICATIONVERSUS INDEMNIFICATION Comparative Fault

Impact of Anti-Indemnity Act

Direct Obligation by Insurers Direct Obligation by Insurers

Employee ExclusionEmployee Exclusion

Insured Contract

57

For More Information:For More Information:

Justin L. WeisbergArnstein & Lehr LLP120 South Riverside Plaza Suite 1200Chicago, IL 60606Ph: 312-876-6688Ph: 312 876 6688Email: [email protected]

58

Additional Insured Coverage: Reconciling Business g gContract Obligations and Policy Terms

Maximizing Existing Coverage and Resolving Disputes Between Additional and Named Insureds

Strafford Publications Webinar

Robert M. Fineman, Esq.

March 23, 2010

, qDuane Morris LLP

One Market, Spear Tower, Suite 2200 San Francisco, CA 94105

www.duanemorris.com

©2009 Duane Morris LLP. All Rights Reserved. Duane Morris is a registered service mark of Duane Morris LLP. Duane Morris – Firm and Affiliate Offices | New York | London | Singapore | Los Angeles | Chicago | Houston | Hanoi | Philadelphia | San Diego | San Francisco | Baltimore | Boston | Washington, D.C.

Las Vegas | Atlanta | Miami | Pittsburgh | Newark | Boca Raton | Wilmington | Cherry Hill | Princeton | Lake Tahoe | Ho Chi Minh City | Duane Morris LLP – A Delaware limited liability partnership

Typical Scenario

• A general contractor and subcontractor enter into an agreement by which the subcontractor g yagrees to indemnify the general contractor and name the general contractor as an additional insuredinsured.

• A third party sues the general contractor. What is the general contractor’s response?– The general contractor-additional insured submits a claim

to the subcontractor’s insurer. – The general contractor-indemnitee also seeks

i d ifi ti f th b t t i d it Th

www.duanemorris.com

indemnification from the subcontractor-indemnitor. The subcontractor then submits the indemnity claim to its insurer.

2

THE BASICSThe General Contractor

– Make written indemnity demand upon Sub

The General Contractor

Contractor.– Obtain copies of Contract, any Additional

Insured endorsements and certificates ofInsured endorsements and certificates of insurance, and copies of Contractor’s insurance policy. p y

– Place Sub Contractor’s insurer on notice. – Consider placing own insurer on notice.

www.duanemorris.com3

THE BASICS (cont.)Th G l C t t ’ I

– Acknowledge tender, under a reservation of

The General Contractor’s Insurer (if tendered)

rights, within statutory time period. – Investigate facts of claim.

D t i d t t d f d d l t– Determine duty to defend and evaluate whether to reserve rights. Request copies of contract and all Sub– Request copies of contract and all Sub Contractors’ insurance policies.

– Direct insured to tender to all Sub Contractors’

www.duanemorris.com

Direct insured to tender to all Sub Contractors insurers.

4

THE BASICS (cont.)Th S b C t t

– Place insurer on notice of indemnity demand.

The Sub Contractor

– Review indemnity and insurance procurement i iprovisions.

www.duanemorris.com5

THE BASICS (cont.)A k l d Additi l I d t d bThe Sub Contractor's Insurer– Acknowledge Additional Insured tender by General Contractor, under a reservation of rights (if appropriate), within statutory time period.

The Sub Contractor s Insurer

( ) y– Investigate facts of claim. – Obtain copies of Contract, any Additional Insured

d t d tifi t f i dendorsements and certificates of insurance, and copies of Sub Contractor’s insurance policy.

– Determine additional insured status.– Determine duty to defend within statutory time

period.

www.duanemorris.com

– Ask General Contractor to place own insurer on notice.

6

KEY ISSUES• Does Injury “Arise Out Of” Contractor’s Work?

– Vitton Const. Co. v. Pacific Ins. Co., 110 Cal.App.4th 762 (2003) The fact that an accident is not attributable to the named

i d' li i i l t h th dditi l i dinsured's negligence is irrelevant when the additional insured endorsement does not purport to allocate or restrict coverage to fault.

– Acceptance Ins. Co. v. Syufy Enterprises, 69 Cal.App.4th 321p y y p pp(1999) Courts have held that the following provisions effectively limit

coverage to only vicarious liability: “liability connected to named insured's work excepting any loss caused bynamed insured s work excepting any loss caused by additional insured's sole negligence”; “liability with respect to acts or omissions by named insured”; and “only to the extent additional insured is held liable for named insured's acts or omissions ”

www.duanemorris.com

omissions.

7

KEY ISSUESD I j “A i O Of” C ’ W k?• Does Injury “Arise Out Of” Contractor’s Work?– St. Paul Mercury Ins. Co. v. Frontier Pac. Ins. Co., 111

Cal.App.4th 1234 (2003) Liability “arising out of” or “based on” the named insured’s Liability arising out of or based on the named insured s

work for the additional insured broadly cover an additional insured for claims caused by its own negligence

– St. Paul Fire & Marine Ins. Co. v. American Dynasty Surplus Lines Ins. Co. 101 Cal.App.4th 1038 (2002) pp ( ) Court found that phrase “arising out of ... your ongoing

operations” was ambiguous, but looking at the contract as a whole to resolve ambiguity, held additional insured coverage was intended to cover only such liability as might arise from

b t t ' t l f f th k ll d fsubcontractor's actual performance of the work called for. This was consistent with the parties' contract under which Subcontractor's duty to indemnify Contractor was limited to liability for Subcontractor's “acts or omissions.”

www.duanemorris.com8

KEY ISSUES

• Who Controls the Defense?– Retaining separate counsel for the AI Considerations with respect to use of

separate counsel for AI or joint defense of AIseparate counsel for AI or joint defense of AI– Different considerations when subcontractor

is a party versus situation where b t t i tsubcontractor is a non-party

– Controlling the defense of AI

www.duanemorris.com9

KEY ISSUES• Defense cost issues• Defense cost issues

– Potential methods of allocating defense costs Equal shares among all insurers, unless GC primary/non-

contributory Other allocation methods

– Ensure that all AI insurers are pursued to participate in defense Burden on AI to identify and demand defense from other AI insurersy

– Recalculation of allocated shares Re-allocate each time an additional AI insurer is added? Retroactive versus prospective re-allocation?Problems when not all AI insurers agree to defend– Problems when not all AI insurers agree to defend Potential bad faith exposure? Attorney’s fees?

www.duanemorris.com10

KEY ISSUES• Defense cost issues (cont.)

– Limitations imposed by construction subcontract Issues when subcontract with general contractor

i AI i t b i d t ib trequires AI insurer to be primary and noncontributory to the Developer/GC insurance

Issues when subcontract states amount of limits available to AI

– Shared defense by multiple AI carriers Specify law firm obligations Establish billing rates Detail requirements to submit budgets and plans Explain reporting requirements

www.duanemorris.com11

KEY ISSUES• Defense cost issues (cont.)

– Policies excess of SIR Depending on language of SIR endorsement, payment of

other valid and collectible will generally satisfy the SIR (Theother valid and collectible will generally satisfy the SIR (The Vons Cos. v. United States Fire Ins. Co., 78 Cal.App.4th 52 (2000)). Exception where SIR endorsement states that insured “will be

responsible for full Retention Amount before the limits of Insurance under this policy apply”

Negotiations with insured for payment of SIR if insured itself is required to satisfy SIR

– Other defense cost issues Scope of duty to defend – in California, each insurer

obligated to defend 100% (Presley Homes v. American States, 90 Cal.App.4th 571 (2001))

No AI endorsement, but Type I indemnity

www.duanemorris.com12

KEY ISSUES• Other defense cost issues (cont.)

– Seeking reimbursement of defense costs from other insurers and/or from the insured R i b f id i d f f l i h Reimbursement for amounts paid in defense of claims that

were not even potentially covered (Buss and Scottsdale) Must include right to seek reimbursement in ROR

– Sharing of limits between both insureds if defense is within limitsSharing of limits between both insureds, if defense is within limits Implied covenant of good faith and fair dealing prohibits the

favoring of one insured over another in splitting payments made from a policy’s limits. See, e.g., Schwartz v. State Farm Fire and Cas Co 88 Cal App 4th 1329 (2001) (holdingFarm Fire and Cas. Co., 88 Cal.App.4th 1329 (2001) (holding that settlements must be split evenly between insureds unless the co-insureds mutually agree to an unequal division)

www.duanemorris.com13

KEY ISSUES• Other defense cost issues (cont.)

– Duties owed to multiple insureds Denial of coverage as to one insured does not negate Denial of coverage as to one insured does not negate

the separate obligations owed by the insurer to others that may be insured under the same policy

Application of deductible to both defense and indemnity– Application of deductible to both defense and indemnity Who pays deductible, GC or subcontractor? Splitting deductible in same manner as splitting limits?

www.duanemorris.com14

KEY ISSUES

• What Are the “Other Insurance” Implications?• Hartford Casualty Ins. Co. v. Mt. Hawley Ins. Co., 123

Cal App 4th 278 (2004)Cal.App.4th 278 (2004)– General contractor’s insurer can not be liable to a subcontractor’s

insurer for any costs of defense or indemnity where the subcontractor agreed to indemnify the general contractor for all liabilities “which arise out of or are in any way related to” theliabilities which arise out of or are in any way related to the relevant construction project.

• Reliance National Indemnity Co. v. General Star Indemnity Co., 72 Cal.App.4th 1063 (1999)

R did t t t t bli h l l th t– Rossmoor did not purport to establish a general rule that a contractual indemnification agreement between an insured and a third party takes precedence over well established general rules of primary and excess coverage in an action between insurers

www.duanemorris.com15

The Relationship Between Indemnity and Insurance• Rossmoor Sanitation Inc v. Pylon, 13 Cal. 3d 622 (1975).

T ti th l t t th th i l ld– To apportion the loss pursuant to the other insurance clause would effectively negate the indemnity agreement and impose liability on [the owner’s insurer] when [the owner] bargained with [the Contractor] to avoid that very result as part of the consideration for the construction agreement.

• McCrary Construction Co v Metal Deck Specialists Inc 133McCrary Construction Co. v. Metal Deck Specialists, Inc. 133 Cal.App.4th 1528 (2005)– An indemnity provision that does not refer to the issue of the indemnitee’s

negligence will be considered to be a general indemnity clause under which the indemnitee is not entitled to indemnity for its active negligence, unless th i t f th d th l f th t t ithe circumstances of the case and the language of the contract evince a different intent by the parties.

• American Casualty v. General Star Indemnity Co., 125 Cal.App.4th 1510 (2005)

C f dditi l i d ti if i d it t i– Coverage for additional insured continues even if indemnity agreement is unenforceable under Civil Code section 2782(a))

• JPI Westcoast Construction v. RJS Assoc., et al., 156 Cal.App.4th

1448 (2007)

www.duanemorris.com

– Subcontractor’s excess policy not triggered until subcontractor’s and general contractor’s primary policies are exhausted, notwithstanding indemnity agreement

16

Other Key Issues

• Issue: Is the subcontractor’s obligation to indemnify the general contractor covered underindemnify the general contractor covered under the subcontractor’s CGL policy?

• Coverage for the indemnity claim turns on g ywhether the indemnity agreement is an “insured contract” as defined by the subcontractor’s CGL policypolicy.

www.duanemorris.com17

Insurance Coverage for Contractual Indemnity Claims: Significant CGL Provisions

• Typical CGL Coverage Grant: “The company will pay on behalf of the insuredcompany will pay on behalf of the insured all sums which the insured shall become legally obligated to pay as damageslegally obligated to pay as damages because of bodily injury or property damage to which this insurance appliesdamage to which this insurance applies caused by an occurrence.”

www.duanemorris.com18

Insurance Coverage for Contractual Indemnity Claims: Significant CGL Provisions (cont.)

Typical CGL Contractual Liability Exclusion: “This insurance does not apply to . . . ‘bodily injury’ or ‘property damages’ for which the insured is obligated to pay as damages by reason of the assumption of liability in a contract or agreement ”liability in a contract or agreement.

This exclusion would appear to eliminate coverage forThis exclusion would appear to eliminate coverage for claims arising out of a contractual indemnification agreement. However . . .

www.duanemorris.com

g

19

Exception to the Contractual Liability Exclusion

• Typical CGL Exception to the Contractual Liability Exclusion: “This exclusion does not apply to liability for damages:damages:

(1) that the insured would have in the absence of the contract or ( )agreement; or

(2) assumed in a contract or agreement that is an ‘insured contract’, provided the bodily injury or property damage occurs subsequent to p y j y p p y g qthe execution of the contract agreement.”

What is an “insured contract”?

www.duanemorris.com

• What is an “insured contract”?

20

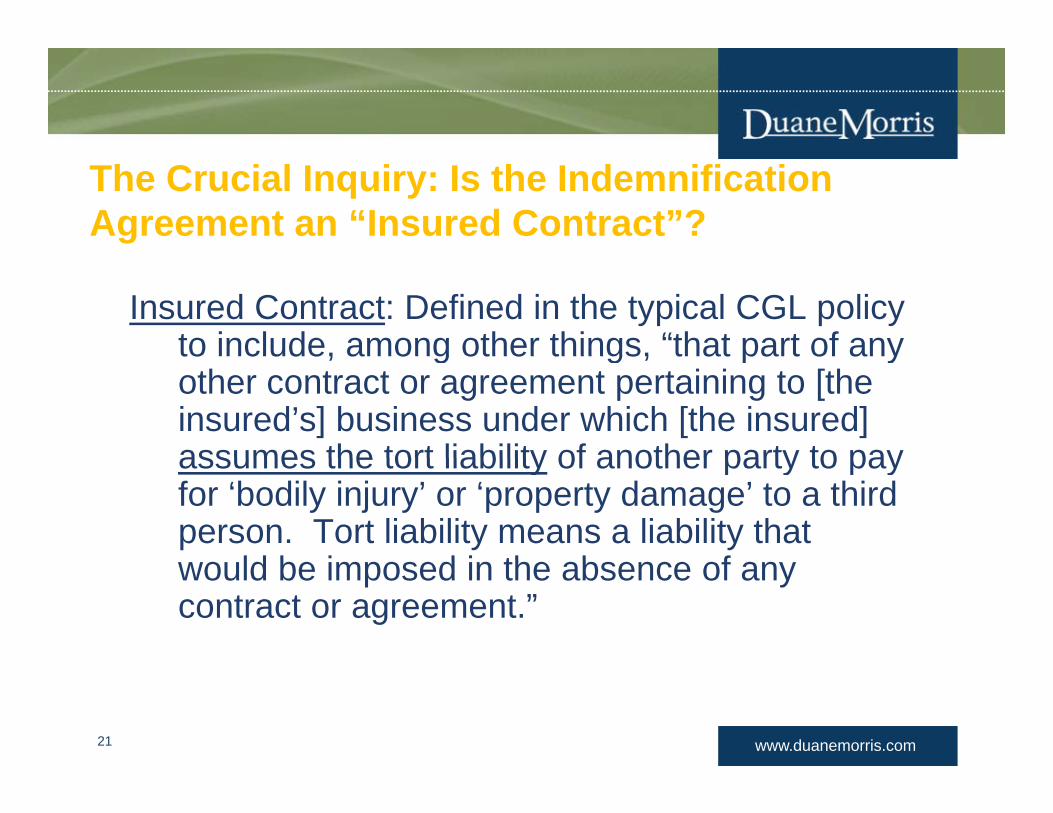

The Crucial Inquiry: Is the Indemnification Agreement an “Insured Contract”?

Insured Contract: Defined in the typical CGL policy to include, among other things, “that part of anyto include, among other things, that part of any other contract or agreement pertaining to [the insured’s] business under which [the insured] assumes the tort liability of another party to payassumes the tort liability of another party to pay for ‘bodily injury’ or ‘property damage’ to a third person. Tort liability means a liability that

ld b i d i th b fwould be imposed in the absence of any contract or agreement.”

www.duanemorris.com21

The Crucial Inquiry: Is the Indemnification Agreement an “Insured Contract”? (cont.)• Thus, to qualify as an insured contract, the

contract must:– Pertain to the insured’s business– Have been entered into before the underlying

liability (a tort liability) occurs – Assume the tort liability of another

www.duanemorris.com22

“Insured Contract” Litigation Outcomes• West Bend Mut. Ins. v. Mulligan Masonry Co., 337 Ill. App. 3d

698 (2003) (indemnity agreement was an insured contract even though indemnitor had only agreed to provide indemnification f it li d t th li f thfor its own negligence and not the negligence of the indemnitee) (Illinois)

• Hankins v. Pekin Ins. Co., 713 N.E.2d 1244 (1999) (not insured t t h i d it l d t idcontract where indemnitor only agreed to provide

indemnification for its own negligence; tort liability of the indemnitee was not assumed) (Illinois)G ld E l I C I C f th W t 99 C l A 4th• Golden Eagle Ins. Co. v. Ins. Co. of the West, 99 Cal. App. 4th 837 (2002) (“The insured must assume the other contracting party’s tort liability to third parties in order for insured contract

t tt h”) (C lif i )

www.duanemorris.com

coverage to attach”) (California)

23

The Duty to Defend and the Impact on Policy Limitsts

• Does an Insurer have a duty to defend an indemnitee? M b if th i d it i d dditi lMaybe, if the indemnitee is named as an additional insured.

• Alex Robertson Co. v. Imperial Cas. & Indem. Co., 8Alex Robertson Co. v. Imperial Cas. & Indem. Co., 8 Cal.App.4th 338 (1992) (an insurer’s duty to defend extends only to insureds; an insurer need not defend an indemnitee)indemnitee).

• CGL policy language states: “we will have the right and duty to defend the insured against any suit . . ..”

www.duanemorris.com

y g y

24

Potential Application of Cross-Suits Exclusion

• Exclusion for coverage based upon claim by any “insured” against another “insured”

T i Cit Fi I C Ohi I C I 480 F 3d 1254– Twin City Fire Ins. Co. v. Ohio cas. Ins. Co., Inc., 480 F.3d 1254 (11th Cir. 2007) Rejecting application of cross-suits exclusion in litigation between

named insured and additional insurednamed insured and additional insured– Great Western Drywall v. Interstate Fire & Cas. Co., 161 Cal. App.

4th 1033 (2008) Upholding application of cross suits exclusion in litigation between Upholding application of cross-suits exclusion in litigation between

named insured and additional insured

www.duanemorris.com25

Practical Tips

An indemnitee should examine all of its rights under:

• The indemnity contract• Any insurance policy naming it as an additional insured

D t f i d it d i bli ti• Do not confuse indemnity and insurance obligations --separate issues requiring separate analysis.

• Make indemnity demands and insurance tendersMake indemnity demands and insurance tenders promptly.

• Caution!! Don’t ignore additional insured issues.

www.duanemorris.com26

Robert M. FinemanRobert M. FinemanDirect No: (415) 957-3210

Duane Morris LLPua e o sOne Market, Spear Tower

Suite 2000San Francisco, CA 94105-1104

Office Tel: (415) 957 3210

www.duanemorris.com27

Office Tel: (415) 957-3210Office Fax: (415) 957-3001

www.duanemorris.com