Advanced Financial Accounting: Chapter 11

Earnings per Share

Tan & Lee Chapter 11 © 2009 1

Learning Objectives

1. Significance of earnings per share

2. Difference between basic and diluted earnings per share

3. How new issues affect earnings per share through the weighted average number of shares

4. Concept of dilution

5. Concept of control number in diluted earnings per share

6. Apply methods for calculating diluted earnings per share:

• If-converted method• Treasury method

Tan & Lee Chapter 11 © 2009 2

Tan & Lee Chapter 11 © 2009 3

Content

1. Introduction

2. Computation of a Weighted-Average Number

of Shares

3. Diluted Earnings per Share

1. Introduction

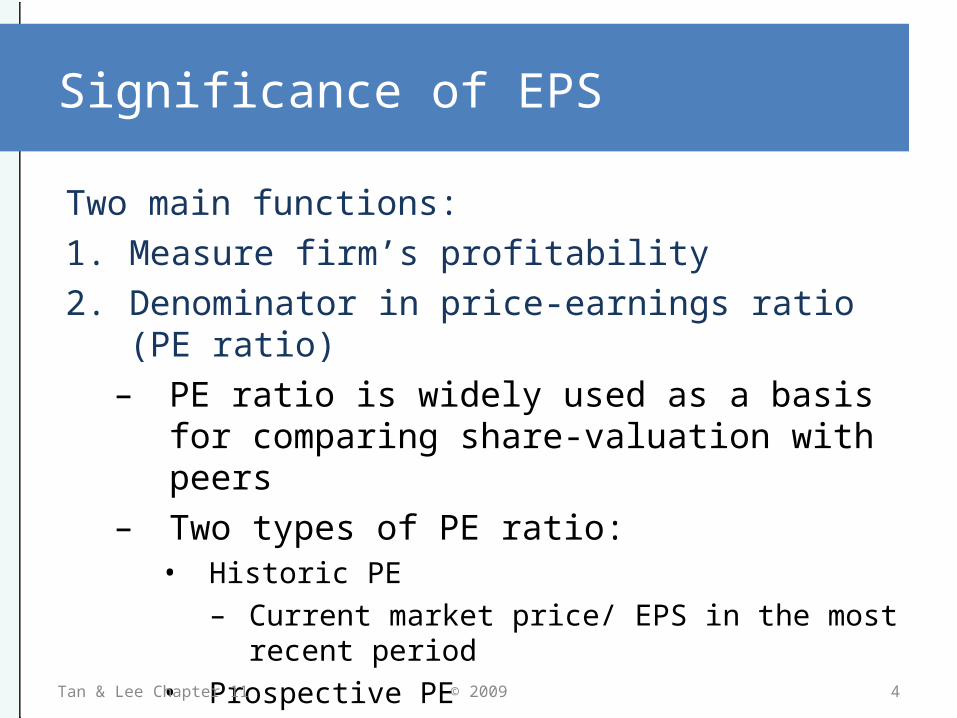

Significance of EPS

Two main functions:

1. Measure firm’s profitability

2. Denominator in price-earnings ratio (PE ratio)– PE ratio is widely used as a basis for comparing

share-valuation with peers– Two types of PE ratio:

• Historic PE

– Current market price/ EPS in the most recent period

• Prospective PE

– Current market price/ projected EPS for the upcoming period

Tan & Lee Chapter 11 4© 2009

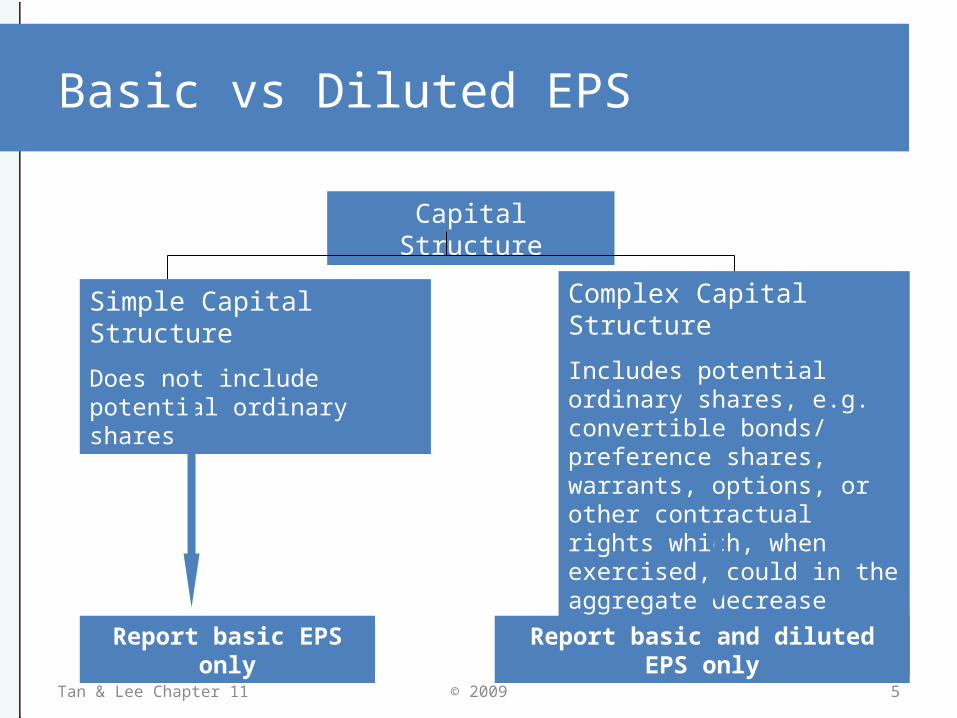

Basic vs Diluted EPS

Capital Structure

Simple Capital Structure

Does not include potential ordinary shares

Complex Capital Structure

Includes potential ordinary shares, e.g. convertible bonds/ preference shares, warrants, options, or other contractual rights which, when exercised, could in the aggregate decrease earnings per ordinary share

Report basic EPS only Report basic and diluted EPS only

Tan & Lee Chapter 11 5© 2009

Content

1. Introduction

2. Computation of a Weighted-Average Number

of Shares

3. Diluted Earnings per Share

2. Computation of a Weighted-Average Number of Shares

Tan & Lee Chapter 11 6© 2009

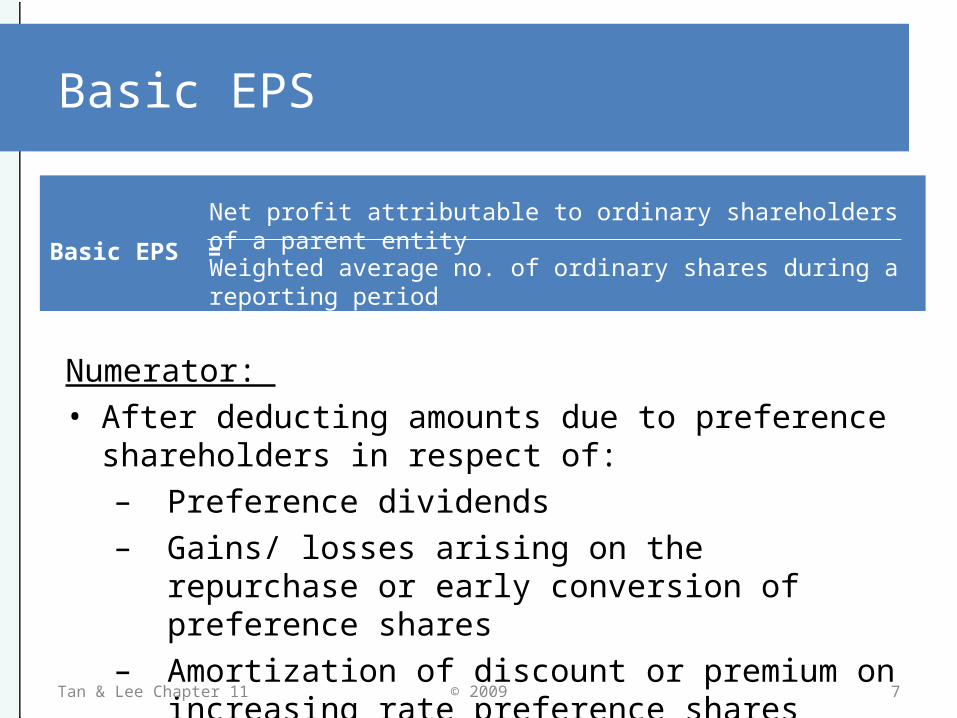

Basic EPS

Numerator: • After deducting amounts due to preference shareholders

in respect of: – Preference dividends– Gains/ losses arising on the repurchase or early

conversion of preference shares – Amortization of discount or premium on increasing

rate preference shares

Basic EPS =

Net profit attributable to ordinary shareholders of a parent entity

Weighted average no. of ordinary shares during a reporting period

Tan & Lee Chapter 11 7© 2009

Definition of Different Types of Preference Shares

• Cumulative preference shares require the issuer to pay dividends, even if in arrears.

• Increasing rate preference shares are shares that are issued at a discount and that provide a low initial dividend to compensate the issuer for selling at a discount.

Tan & Lee Chapter 11 8© 2009

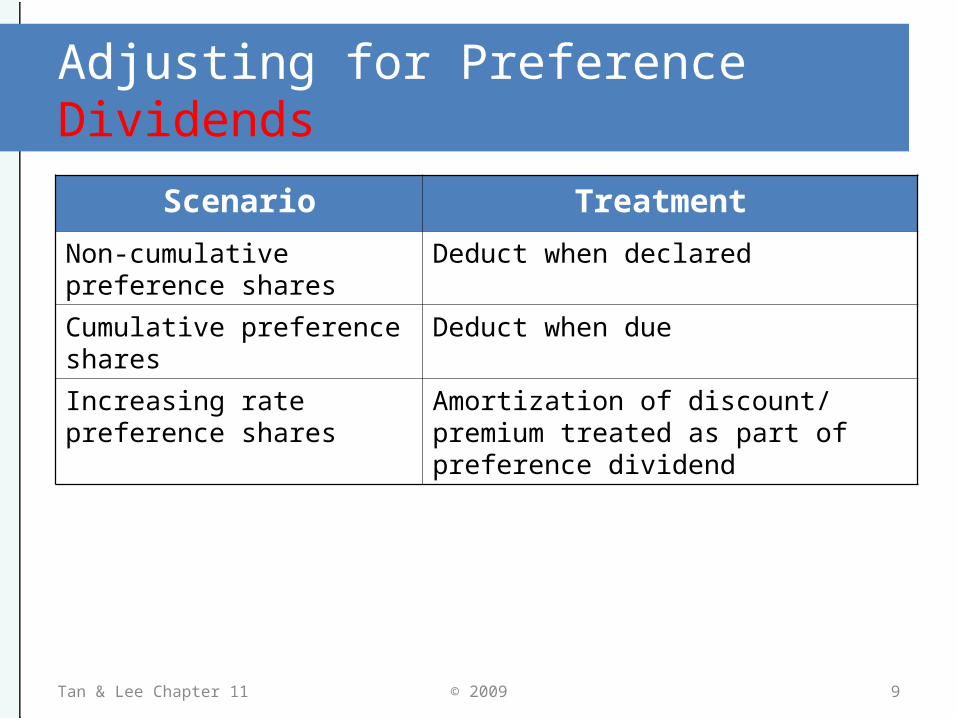

Adjusting for Preference Dividends

Scenario Treatment

Non-cumulative preference shares

Deduct when declared

Cumulative preference shares

Deduct when due

Increasing rate preference shares

Amortization of discount/ premium treated as part of preference dividend

Tan & Lee Chapter 11 9© 2009

Adjusting for Preference Dividends

Scenario Treatment

Non-cumulative preference shares

Deduct when declared

Cumulative preference shares

Deduct when due

Increasing rate preference shares

Amortization of discount/ premium treated as part of preference dividend

Tan & Lee Chapter 11 10© 2009

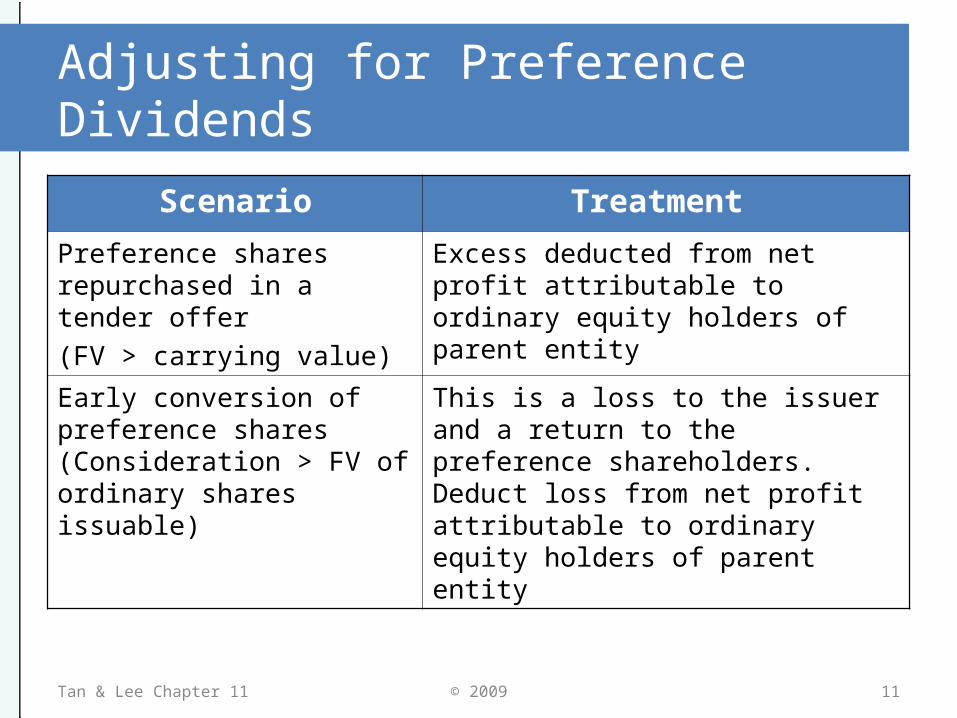

Adjusting for Preference Dividends

Scenario Treatment

Preference shares repurchased in a tender offer

(FV > carrying value)

Excess deducted from net profit attributable to ordinary equity holders of parent entity

Early conversion of preference shares (Consideration > FV of ordinary shares issuable)

This is a loss to the issuer and a return to the preference shareholders. Deduct loss from net profit attributable to ordinary equity holders of parent entity

Tan & Lee Chapter 11 11© 2009

Basic EPS

Denominator (examples):

The term “weighted average” refers to time-weighting, when there are changes in the number of ordinary shares during the financial year.

General rule: • Shares are time-weighted from the date consideration is

receivable (usually the date of share issue)

• Time-weighting is only performed when there is an inflow of resources

Tan & Lee Chapter 11 12© 2009

Basic EPS

Denominator: - examples

Scenario Date to use for time-weighting

Shares issued for acquisition/ Business combination

Date of acquisition

Conversion of mandatory convertible instrument

Date of contract

Contingently issuable shares are issued

Date when all necessary conditions are satisfied

Tan & Lee Chapter 11 13© 2009

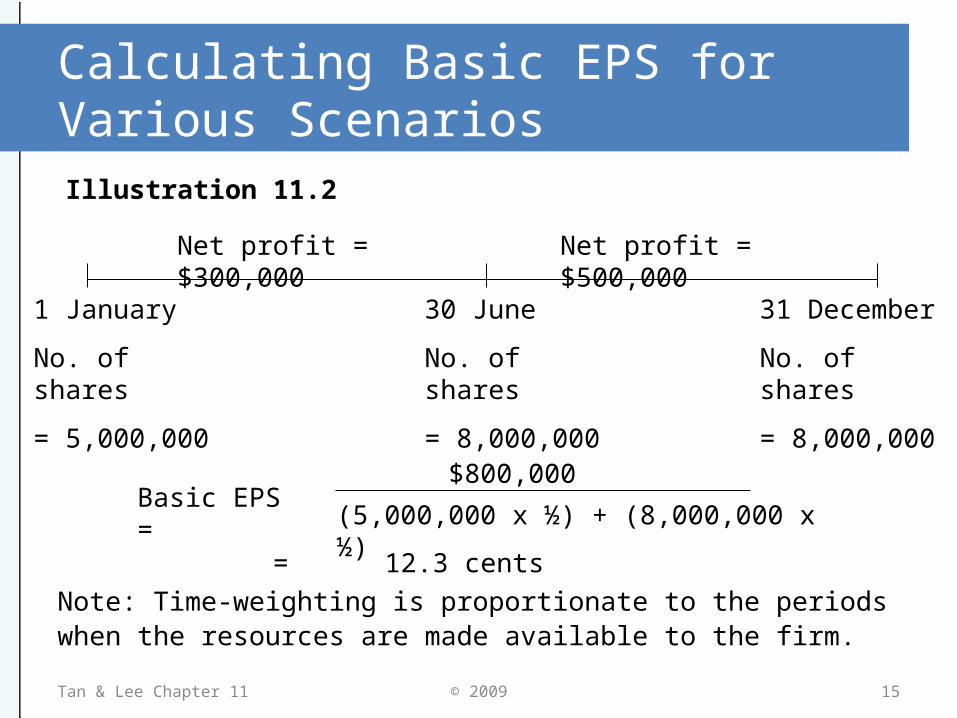

Calculating Basic EPS for Various Scenarios

Scenario 1: New shares are issued for cash/ other assets

Illustration 11.2

Company A had issued share capital of 5,000,000 ordinary shares at the beginning of the year. On 30 June, it issued 3,000,000 shares at fair market value for cash. Net profit attributable to ordinary shares was $300,000 for the first 6 months and $800,000 for the full year.

Tan & Lee Chapter 11 14© 2009

Calculating Basic EPS for Various ScenariosIllustration 11.2

Note: Time-weighting is proportionate to the periods when the resources are made available to the firm.

1 January

No. of shares

= 5,000,000

30 June

No. of shares

= 8,000,000

31 December

No. of shares

= 8,000,000

Net profit = $300,000 Net profit = $500,000

Basic EPS =$800,000

(5,000,000 x ½) + (8,000,000 x ½)

= 12.3 cents

Tan & Lee Chapter 11 15© 2009

Calculating Basic EPS for Various Scenarios

Scenario 2: Issue of bonus shares (stock dividends)

Reserves (Retained earnings + Capital reserves) Total

Equity

Reserves

Bonus issue

Share capital

shareholders

Total

Equity

Share capital

Tan & Lee Chapter 11 16© 2009

Calculating Basic EPS for Various Scenarios

• Bonus shares are issued out of reserves, such as capital reserves or retained earnings.

• Share capital increases, total number of shares increase, reserves decrease, total shareholders’ equity remains unchanged

No inflow of resources not time-weighted• Treatment:

– Any bonus issues taking place in a period are assumed to be issued at the beginning of the period. (no time-weighting)

– Retroactively restate previous year’s EPS comparatives based on new number of shares.

Tan & Lee Chapter 11 17© 2009

Calculating Basic EPS for Various Scenarios

Scenario 3: Share splits• An existing share is split into 2 or more shares• No inflow of resources not time-weighted• Retroactive restatement of comparative EPS

Scenario 4: Consolidation of existing shares through reverse splits• 2 or more shares are consolidated into one share• No inflow of resources not time-weighted.• Retroactive restatement of comparative EPS

Tan & Lee Chapter 11 18© 2009

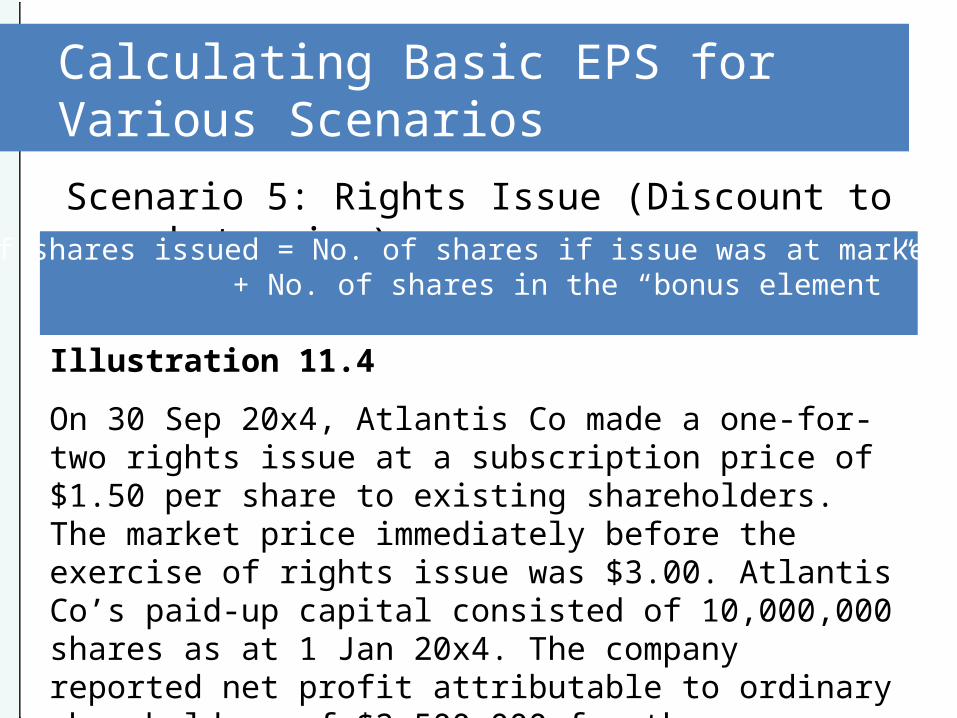

Calculating Basic EPS for Various Scenarios

Scenario 5: Rights Issue (Discount to market price)No. of shares issued = No. of shares if issue was at market price

+ No. of shares in the “bonus element”

Illustration 11.4

On 30 Sep 20x4, Atlantis Co made a one-for-two rights issue at a subscription price of $1.50 per share to existing shareholders. The market price immediately before the exercise of rights issue was $3.00. Atlantis Co’s paid-up capital consisted of 10,000,000 shares as at 1 Jan 20x4. The company reported net profit attributable to ordinary shareholders of $2,500,000 for the year ended 31 Dec 20x4.

Calculating Basic EPS for Various Scenarios

Illustration 11.4

On 30 Sep 20x4, Atlantis Co made a one-for-two rights issue at a subscription price of $1.50 per share to existing shareholders. The market price immediately before the exercise of rights issue was $3.00. Atlantis Co’s paid-up capital consisted of 10,000,000 shares as at 1 Jan 20x4. The company reported net profit attributable to ordinary shareholders of $2,500,000 for the year ended 31 Dec 20x4.

Calculating Basic EPS for Various Scenarios

This solution applies the treasury method.

• 5,000,000 new shares.

• 5,000,000 x $1.50 = $7,500,000 total proceeds

inflow of new resources time-weighting involved

• If the issue was made at full market price, only 2,500,000 new shares needed to be issued ($7,500,000 / $3). Therefore no. of shares in bonus element = 2,500,000

Tan & Lee Chapter 11 21© 2009

Reasoning – the treasury method: • Company B needs to buy back 2,500,000 shares

from the open market to issue to shareholders, with the proceeds it collected from the rights issue of $7,500,000.

• An additional 2,500,000 are issued as bonus shares. 10M +2.5M+2.5M

• Actual number of shares issued = 15,000,000• Number of shares issued for cash = 12,500,000

Calculating Basic EPS for Various Scenarios

Tan & Lee Chapter 11 22© 2009 10M +2.5M

Calculating Basic EPS for Various Scenarios

• The bonus issue factor is 1.2 (15,000,000/ 12,500,000) shares for every 1 existing share held.

• The bonus factor should be applied retrospectively to outstanding shares before the rights issue.

Tan & Lee Chapter 11 23© 2009

Calculating Basic EPS for Various Scenarios

From 1 January 20x4 to 30 September 20x4

10,000,000 x 1.2 x 9/12 = 9,000,000

From 1 October 20x4 to 31 December 20x4

15,000,000 x 3/12 = 3,750,000

Weighted average number of shares 12,750,00

Net profit attributable to ordinary shareholders $2,500,000

Basic earnings per share = 19.6 cents

Tan & Lee Chapter 11 24© 2009

Calculating Basic EPS for Various Scenarios

Scenario 6: New issue of shares from the conversion of debt

• No inflow of cash, but reduction of debt which increases net assets of issuer.

• Interest expense on debt is saved Earnings increase • Therefore, time-weighting should be applied.

Tan & Lee Chapter 11 25© 2009

Calculating Basic EPS for Various Scenarios

Scenario 7: Contingently issuable shares• IAS 33:5: These are ordinary shares issuable for little/ no

cash or other consideration upon the satisfaction of specified conditions in a contingent share agreement

• When contingent events have occurred, such shares are time-weighted, even if the shares have yet to be issued.

Tan & Lee Chapter 11 26© 2009