Reverse Mortgages & Your Practice

Provide More Value to Your Clients

Joe ConradReverse Mortgage Planning Specialist

NMLS# 348676(818) [email protected] Conrad is our Reverse Mortgage specialist. He brings over 25 years to the mortgage industry with an emphasis on Reverse Mortgages during the last 8 years.

He approaches each transaction from the perspective of a mortgage planner. The client’s cash flow, equity position and other assets are carefully scrutinized and accounted for when providing a detailed proposal.

He will take great care of anyone that you refer to him and keep you in the loop to the extent you want to be involved.

He also has an extensive marketing background and gets greats satisfaction from leveraging his expertise for others to use

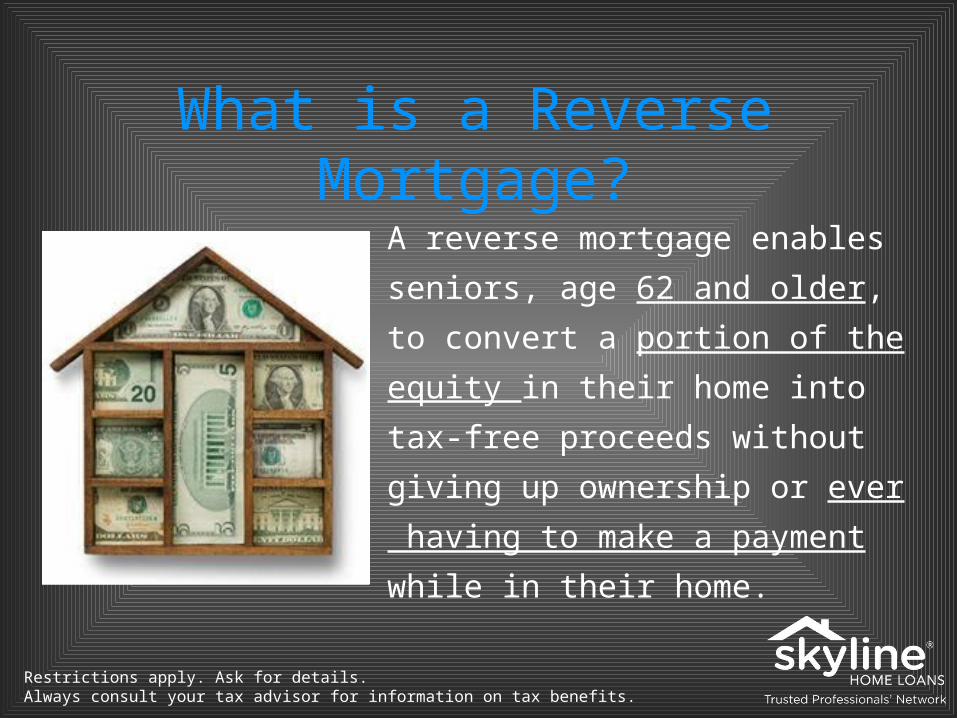

What is a Reverse Mortgage?

A reverse mortgage enables seniors, age 62 and older, to convert a portion of the equity in their home into tax-free proceeds without giving up ownership or ever having to make a payment while in their home.

Restrictions apply. Ask for details. Always consult your tax advisor for information on tax benefits.

Qualification Factors:• Age of the Youngest

Borrower • Appraised Value of the

Home • Financial Assessment (new)

FHA And HOME SAFE Loan Limits FHA $50-625K Loan LimitsHOMESAFE (Jumbo and non FHA Condos) $500K - 3 Million Loan Amounts

To Determine if You are Eligible…

All that is required is:

DOB(s) Address Lien(s)

To Determine the Benefit…All that is required is:

IncomeSSI, Pension, Other

ExpensesReal Estate, Household, Loans

AssetsLiquid, Retirement, Insurance

You can choose to receive your funds as:

• Lump Sum

• Monthly Payments

(tenure)

• Line of Credit

• Hybrid (all the

above)

TYPES AND USES OF REVERSE MORTGAGES

FixedAdjustable Purchase Home Safe

HECM HECM REFI

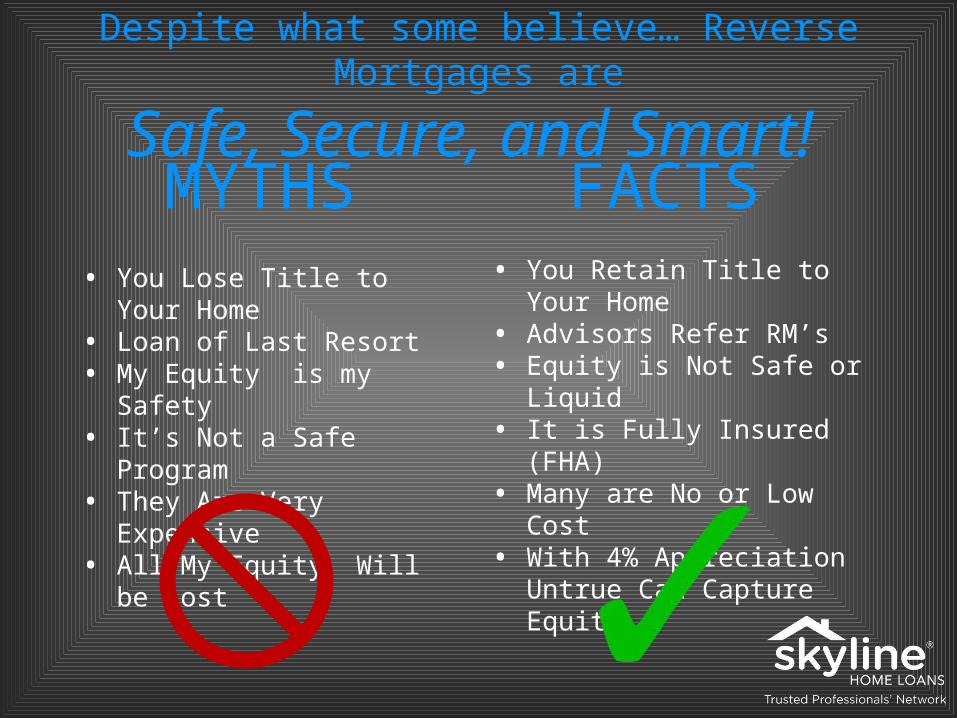

• You Lose Title to Your Home

• Loan of Last Resort• My Equity is my

Safety• It’s Not a Safe Program• They Are Very

Expensive• All My Equity Will be

Lost

MYTHS• You Retain Title to Your

Home• Advisors Refer RM’s• Equity is Not Safe or

Liquid• It is Fully Insured (FHA)• Many are No or Low Cost• With 4% Appreciation

Untrue Can Capture Equity

FACTS

Despite what some believe… Reverse Mortgages are

Safe, Secure, and Smart!

What’s New?

• Income Requirements• Costs Have Been

Lowered• Safer Access to Equity• Lower Loan to Values• “Cooling Off” Periods

SAFE• Backed by FHA• Non Recourse• Credit Line Preserves

Equity• Limits on Equity Access• 3rd Party Counseling

SECURE• No Monthly Payments• Provides Additional Cash

Flow• Access to More Equity• Ability for Youngest Living

Spouse to Stay in Home

SMART• More Trusted Advisors

Refer• Proceeds Are Not Taxed• Protect & Manage Your

Equity• Diversify Your Portfolio• Activate Dead Asset• Preserve Income Earning

Assets

Where are the Gaps?• Eliminate Mortgage Payment• Stop or Mitigate Asset

Depletion• Minimize Income Tax• Pay for Health Care• Defer SSI• Downsize and Use for Purchase• Alternative if denied for a

regular home loan due to credit or income

The Process1. Awareness

2. Education

3. Consultation & Proposal

4. HUD Counseling

5. Application

6. Appraisal

7. Loan processing

8. Underwriting

9. Closing documents

10. Funding

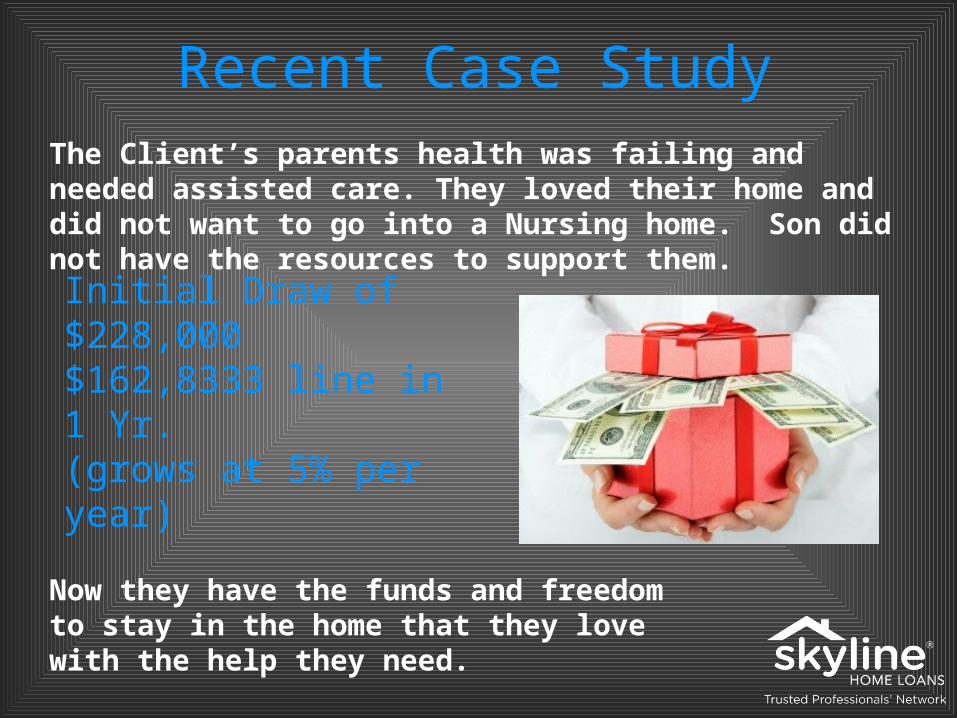

Initial Draw of $228,000 $162,8333 line in 1 Yr.(grows at 5% per year)

Recent Case StudyThe Client’s parents health was failing and needed assisted care. They loved their home and did not want to go into a Nursing home. Son did not have the resources to support them.

Now they have the funds and freedom to stay in the home that they love with the help they need.

Lump sum of $157,000LESA of $34,000 (pays taxes and Insurance)$86,000 Line 1 Yr. Later (grows at 5% per year)

Recent Case StudyClient was disabled and in a trust that and had sporadic income. The home was owned free and clear. The executor was always having to sell other assets for the trust fund to pay living and household expenses.

The Reverse Mortgage Provided funding for all living and housing expenses. This took the stress of liquidating assets for the executor and our 67 year old client can stay in the house as long as she is alive.

750K Proceeds from Sale750K Purchase Price-400K to Builder$350K Reverse Mort$350K Left to invest

Recent Case StudyThe client wanted to downsize their home and not have a mortgage payment. They sold their home for $950,000 and netted $750,000.

They were able to eliminate mortgage payments and mitigate the depletion of income earning assets. They also reinvested most of the proceeds in income generating assets.

Saved payments of $3,500 mo

Received $685,000 in cash

Recent Case StudyClient’s 80 year old parents liked to take the family on trips all over the world and they were eating into their reserves. They had $125,000 liquid left in retirement funds. We paid off a 1st and 2nd mortgage totaling 585,000

They’ve stopped depleting income earning assets and invested some of their proceeds allowing them to continue to live their lifestyle.

FAQ’s Your Borrowers May HaveDoes my home qualify? Homes eligible for a reverse mortgage include single-family homes, detached homes, townhouses, and two-to-four unit properties that are owner-occupied. Condominiums must be FHA-approved. Some manufactured homes are eligible but must meet FHA guidelines. Home Safe program allows for Non FHA approved condos with value of $500K+.

How much money can I receive from a reverse mortgage? The money a borrower can potentially get is calculated by using the age of the youngest borrower, the current expected interest rate, the mortgage option selected, amount of home equity, and the appraised value of the home.

What happens if I outlive the loan? Will I have to repay the lender? No. As long as one of the borrowers on the loan note lives in the home and continues to pay the taxes and insurance and the home remains in good condition, you will not need to repay the loan. Once the last surviving borrower passes away, the home is sold or the obligations of the loan are not met, the loan must be repaid. It is a non-recourse loan.

Does my house need to be paid off for me to qualify? No.

Do I have to pay taxes on the cash payments I receive? No, but you hold the title to your home, you are still responsible for property taxes, insurance, utilities, fuel, maintenance, and other home-related expenses. You should consult with your tax advisor to provide guidance for your particular situation.

How will this loan affect my estate and how much will be left to my heirs? Once the last surviving borrower passes away, if you sell your home, or no longer reside there as the primary residence, you or your estate is responsible for repayment of the money you received from the reverse mortgage, plus interest and other fees. Any remaining equity belongs to either you or your heirs.

Reverse Mortgages & Your Practice

Provide More Value to Your Clients

Joe ConradReverse Mortgage Planning Specialist

NMLS# 348676(818) [email protected]

Joe Conrad is our Reverse Mortgage specialist. He brings over 25 years to the mortgage industry with an emphasis on Reverse Mortgages during the last 8 years. He approaches each transaction from the perspective of a mortgage planner. The client’s cash flow, equity position and other assets are carefully scrutinized and accounted for when providing a detailed proposal. He also has an extensive marketing background and gets greats satisfaction from leveraging his expertise for others to use.

Thank You!