Agriculture in BrazilOverview | April 2010

Los Grobo Overview

Section 1

3

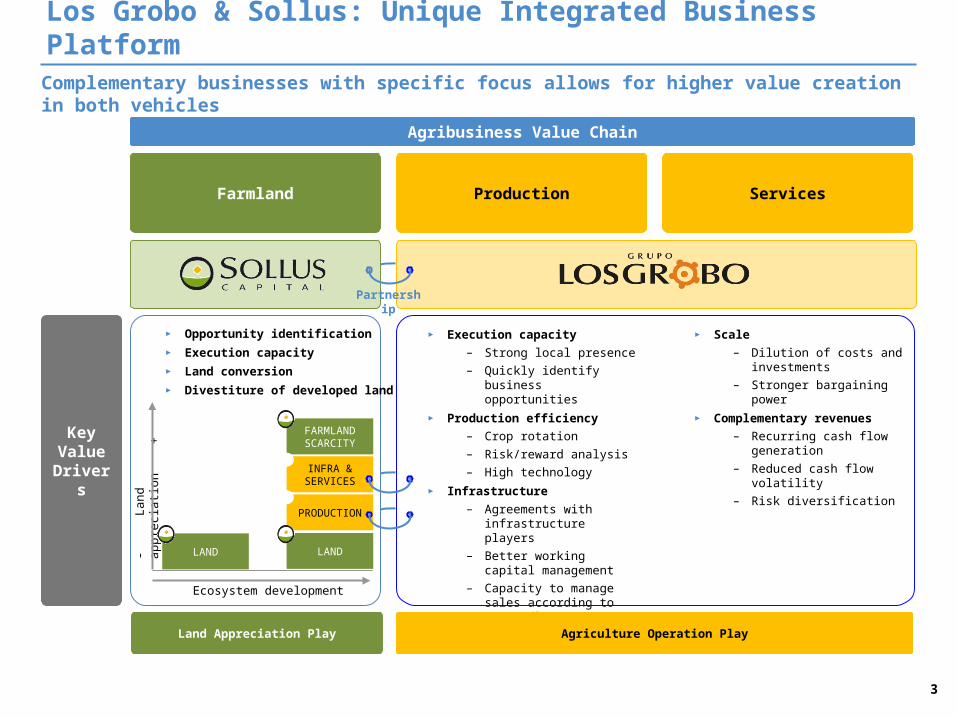

► Execution capacity

– Strong local presence

– Quickly identify business opportunities

► Production efficiency

– Crop rotation

– Risk/reward analysis

– High technology► Infrastructure

– Agreements with infrastructure players

– Better working capital management

– Capacity to manage sales according to price fluctuation

– Lower logistic costs

Los Grobo & Sollus: Unique Integrated Business Platform

ProductionFarmland Services

Agribusiness Value Chain

Key Value

Drivers

► Scale

– Dilution of costs and investments

– Stronger bargaining power ► Complementary revenues

– Recurring cash flow generation

– Reduced cash flow volatility

– Risk diversification

Complementary businesses with specific focus allows for higher value creation in both vehicles

Land Appreciation Play Agriculture Operation Play

Partnership

LAND

PRODUCTION

INFRA & SERVICES

FARMLAND SCARCITY

-

La

nd

ap

pre

cia

tion

+

LAND

Ecosystem development

► Opportunity identification► Execution capacity ► Land conversion► Divestiture of developed land

4

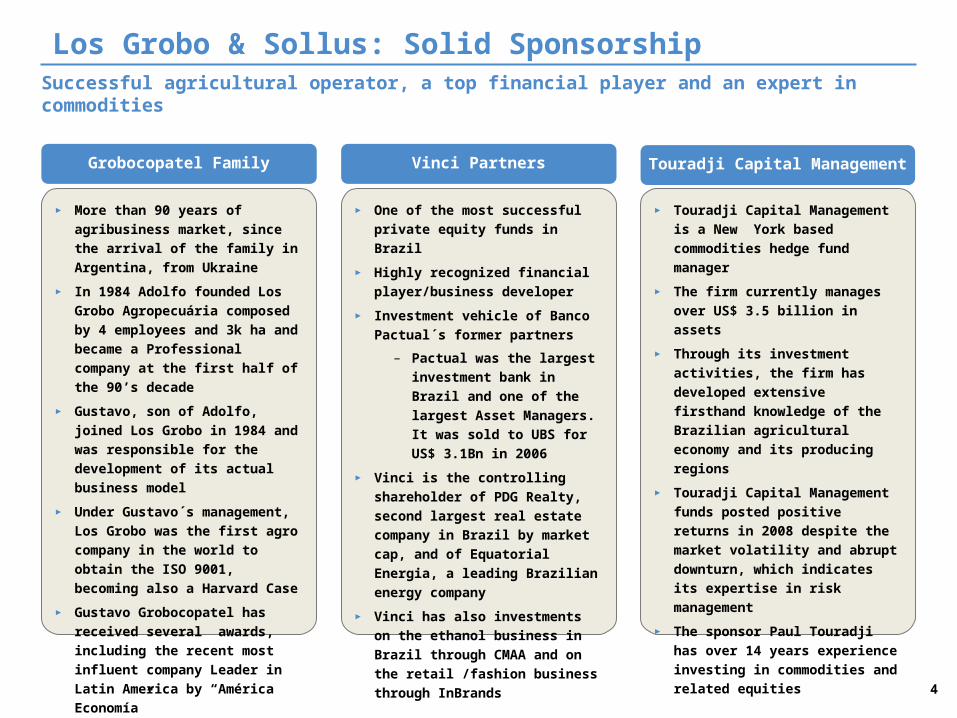

Los Grobo & Sollus: Solid SponsorshipSuccessful agricultural operator, a top financial player and an expert in commodities

► One of the most successful private

equity funds in Brazil

► Highly recognized financial

player/business developer

► Investment vehicle of Banco

Pactual´s former partners

– Pactual was the largest

investment bank in Brazil and

one of the largest Asset

Managers. It was sold to UBS

for US$ 3.1Bn in 2006

► Vinci is the controlling shareholder

of PDG Realty, second largest real

estate company in Brazil by market

cap, and of Equatorial Energia, a

leading Brazilian energy company

► Vinci has also investments on the

ethanol business in Brazil through

CMAA and on the retail /fashion

business through InBrands

Vinci Partners

► Touradji Capital Management is a

New York based commodities

hedge fund manager

► The firm currently manages over

US$ 3.5 billion in assets

► Through its investment activities,

the firm has developed extensive

firsthand knowledge of the

Brazilian agricultural economy and

its producing regions

► Touradji Capital Management funds

posted positive returns in 2008

despite the market volatility and

abrupt downturn, which indicates

its expertise in risk management

► The sponsor Paul Touradji has over

14 years experience investing in

commodities and related equities

Touradji Capital ManagementGrobocopatel Family

► More than 90 years of agribusiness

market, since the arrival of the

family in Argentina, from Ukraine

► In 1984 Adolfo founded Los Grobo

Agropecuária composed by 4

employees and 3k ha and became a

Professional company at the first

half of the 90’s decade

► Gustavo, son of Adolfo, joined Los

Grobo in 1984 and was responsible

for the development of its actual

business model

► Under Gustavo´s management, Los

Grobo was the first agro company

in the world to obtain the ISO 9001,

becoming also a Harvard Case

► Gustavo Grobocopatel has received

several awards, including the

recent most influent company

Leader in Latin America by

“América Economía”

5

Uruguay

Argentina

Chile

Brazil

Venezuela

Peru

Bolivia

Paraguay

MA

PITO

MT

GO

MS

PR

MG

Colombia

Geographically Diversified Production – 2009/2010

Los Grobo: Sizeable and Diversified LatAm Player

Planted Area (k ha)¹

Los Grobo is the 2nd largest LatAm grain producer, with more than 250k ha of productive land throughout Brazil, Argentina, Uruguay and Paraguay…

Brazil:

Production Area: 55k haInput Sales: US$ 50 mmGrain Origination: 800 tonCrushing: 90 ton

Argentina:

Production Area: 90k haInput Sales: US$ 25 mmGrain Origination: 1,000k tonCrushing: 266 ton

Uruguay:

Production Area: 90k haInput Sales: US$ 15 mmGrain Origination: 440k ton

Paraguay:

Production Area: 16k haGrain Origination: 35k ton

Total:

Production Area: 251k haInput Sales: US$ 99 mmGrain Origination: 2,255k tonCrushing: 170k ton

CAGR 02 / 03 – 09 / 10 E: 21%

Grain Origination (k tons)¹

CAGR 02 / 03 – 09 / 10 E: 20%

BA

… also servicing over 500k Ha of production through its services business

486594

8331,030

1,389

1,7631,868

2,255

02 / 03 03 / 04 04 / 05 05 / 06 06 / 07 07 / 08 08 / 09 09 / 10E

Clients Own

Soybean Wheat Corn Others

64

02 / 03

43%

31%

13%

81

03 / 04

53%

27%

10%

105

04 / 05

49%

29%

12%

118

05 / 06

54%

24%

14%

154

06 / 07

53%

27%

13%

173

07 / 08

47%

26%

18%

247

08 / 09

51%

23%

21%

251

09 / 10E

62%

24%

9%

Global Agribusiness Outlook

Section 2

7

0

40

80

120

160

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ethanol

Biodiesel

Per Capita Meat Consumption (2009=100)2

Population Growth

► Global population will rise by 1.5

billion people over the next 20

years

► Migration to urban areas, specially

in the developing countries

Global Agribusiness Outlook: Increasing and Sustainable Demand

Economic and Income Growth

► Consistent personal income

growth in developing countries

► Income growth increases meat

consumption and food demand

Development of Global Biofuels

► Development of viable and

environmental friendly fuels

globally

► Increase in blending of biofuels

with gasoline

► Fuel crops are crowding out food

crops, constraining food supply

Increasing demand for food and biofuels are the main pillars for bullish commodities outlook…

World Biofuels Production (Liters – billions)3

Urbanization (Million of people)1

Source:1. OECD2. FAPRI3. MB Agro

90

100

110

120

130

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Brazil China EU Russia

-

1,000

2,000

3,000

4,000

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

Developing urban population

Developed urban population

8

17% 5%

10%

22%

16%

22%

47%

47%

55%

8%

25% 22%

Series1 Series2

0

200

400

600

800

South andCentralAmerica

Sub-Saaharan

Africa

NorthAmerica

Europe Asia andP acific

North Asia,East Urals

NorthAfrica andNear East

Potential Arable Land

Actual Arable Land

► All-year-round crops

Long Term Competitive Advantages

Land Availability (k ha)2

Leading Producer of Major Products (% of Global Production)1

South America: The Natural Supplier… and South America is likely to consolidate its position as the global preeminent farming region…

Coffee

Soybean

Sugar

Poultry

Beef

Corn

Orange Juice

Source: 1. USDA 2008/2009 Estimates2. FAO

Source: 1. USDA 2008/2009 Estimates2. FAO

1st

1st

2nd

1st

3rd

► Highly favorable geographic and climate conditions

► Competitive production costs

► Favorable regulatory environment

3rd

2nd 5th

3rd 6th

... due to its competitive advantages and abundant resources

20%

9

South America: Upside PotentialDespite the bullish scenario for agribusiness, land prices are still lower when compared to other main productive areas…

… and are likely to appreciate as farmland becomes more scarce

Farmland Price Dynamics and Appreciation Estimates

( -

)

Dev

elo

pm

en

t S

tag

es

(+)

Raw Land

Production

Infra &Services

Scarce Land

► Agriculture potential

► No agricultural utilization

► Lack of services /

infrastructure

► Crop is implemented

► Lack of services /

infrastructure

► Developed crops

► Availability of services /

infrastructure

► Successful prior crops

► Well developed region

► Lack of available

properties nearby

STAGE CONDITIONSAPPRECIATION

ESTIMATES¹

► Balsas – MA

► US$ 1.1k / ha

► Luis Eduardo – BA

► US$ 3.0k / ha

► Rio Verde – GO

► US$ 4.0k / ha

► Ribeirão Preto – SP

► US$ 7.5k / ha

► Traditional producing area► Arbitrage opportunities rising

► Highly developed infrastructure for exports and logistics

► Concentration of high yield products

► Significant soybeans and sugarcane crops expansion

► Limited infrastructural integration

► Several infrastructure developments expected

► Further development of exports and logistics facilities

Average Agricultural Farmland Price (US$ / ha)

USA 11,000

6,000 4,000

3,000

5,900

5,300

3,500

2,300

1,400

3,500

► Long cattle tradition► Northern provinces: best promises in

acreage increase

5

1

2

► Paraguay is growing its agricultural acreage steadily

3

4

6

5

1

23

4

6

Source: FNP, Iowa State University and Sollus

The Soybean in the World

EUA32%

Brasil28%

Argentina21%

China7%

Outros12%

EUA25%

Brasil15%

China19%

Argentina18%

UE 7%

Outros16%

EUA40%

Brasil35%

Argentina15%

Outros10%

Soybeans

EUA14%

Brasil22%

Índia7%

Argentina49%

Outros8%

Soymeal

UE 20%

Japão6%

Méximo5%

China45%

Outros24%

Soybeans

Soybean Production

Soybeans Crushing

Exports

Imports

Índia10%

China28%

Outros62%

SoyOil

11

Historical Soybeans Yield

Historical Soybeans Yield (tons/ha) vs. Modeled (LS)

Linear trend grow in Soybeans Yield

Argentina Uruguay

Paraguay Brazil

Production Cost BreakdownProduction Cost Breakdown

SOYBEANS BRAZIL ARGENTINA URUGUAY PARAGUAY

Cost per Ha Seeds 7% 10% 11% 9%

Chemicals 15% 9% 10% 12%

Fertilizer 22% 5% 17% 16%

Land Lease 19% 45% 32% 28%

G&A 6% 11% 5% 9%

Labor/Machinery 22% 10% 14% 15%

Harvest 9% 10% 11% 11%

Production Costs - SOYBEAN

Grain Production in Brazil

Section 3

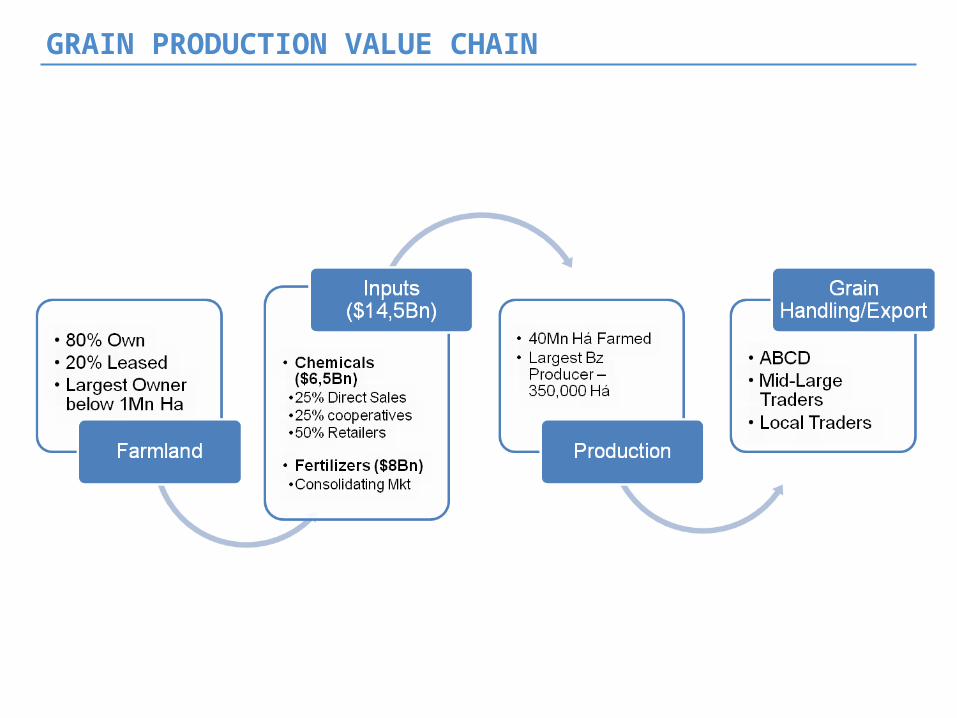

GRAIN PRODUCTION VALUE CHAIN

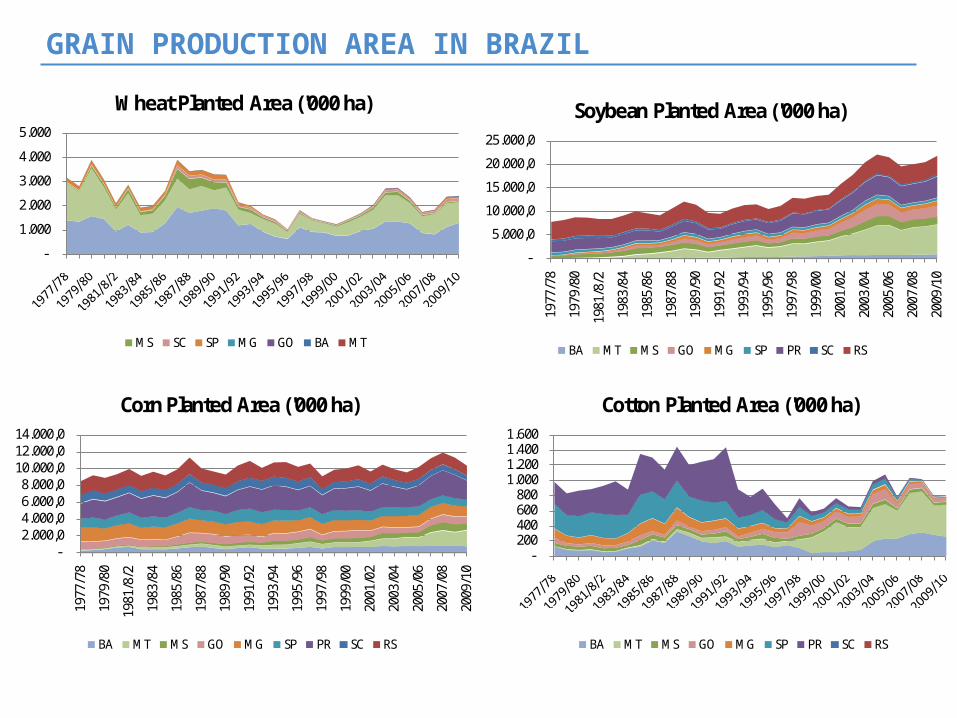

GRAIN PRODUCTION AREA IN BRAZIL

-2.000,0 4.000,0 6.000,0 8.000,0

10.000,0 12.000,0 14.000,0

1977

/78

1979

/80

1981

/8/2

1983

/84

1985

/86

1987

/88

1989

/90

1991

/92

1993

/94

1995

/96

1997

/98

1999

/00

2001

/02

2003

/04

2005

/06

2007

/08

2009

/10

Corn Planted Area ('000 ha)

BA MT MS GO MG SP PR SC RS

-

5.000,0

10.000,0

15.000,0

20.000,0

25.000,0

1977

/78

1979

/80

1981

/8/2

1983

/84

1985

/86

1987

/88

1989

/90

1991

/92

1993

/94

1995

/96

1997

/98

1999

/00

2001

/02

2003

/04

2005

/06

2007

/08

2009

/10

Soybean Planted Area ('000 ha)

BA MT MS GO MG SP PR SC RS

-200 400 600 800

1.000 1.200 1.400 1.600

Cotton Planted Area ('000 ha)

BA MT MS GO MG SP PR SC RS

-

1.000

2.000

3.000

4.000

5.000

Wheat Planted Area ('000 ha)

MS SC SP MG GO BA MT

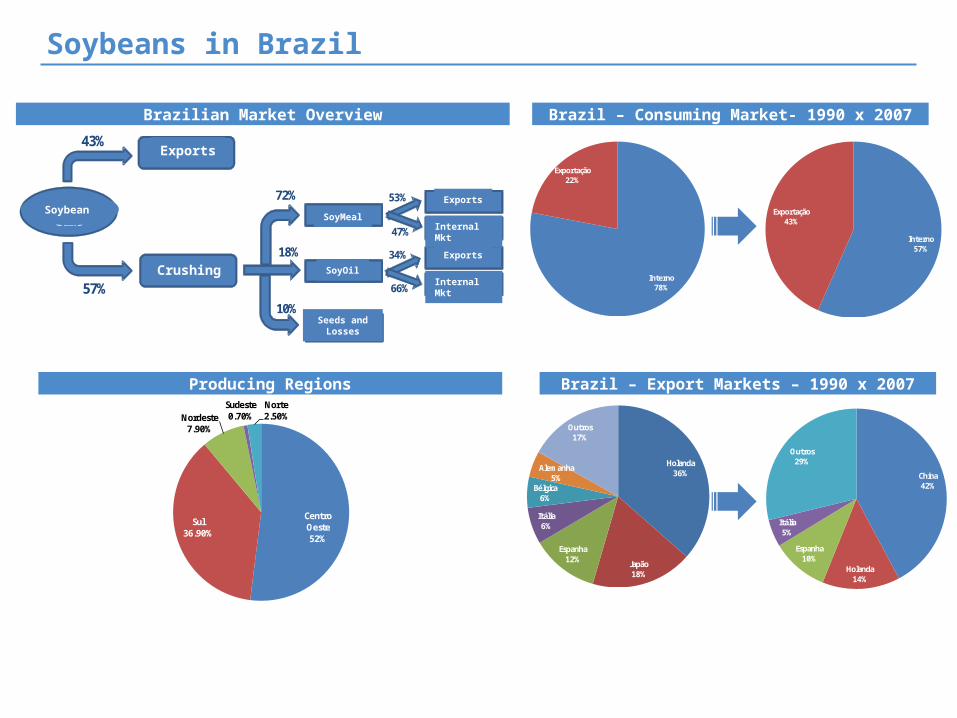

Interno57%

Exportação43%

Soybeans in Brazil

Brazilian Market Overview Brazil – Consuming Market- 1990 x 2007

Producing Regions

Soja em Grão

Exportação

Moagem

Farelo

Óleo

Perda e Sementes

Exportação

Mercado Interno

Exportação

Mercado Interno

43%

57%10%

18%

72% 53%

47%

34%

66%

Centro Oeste52%

Sul36.90%

Nordeste7.90%

Sudeste0.70%

Norte2.50%

Interno78%

Exportação22%

Holanda36%

Japão18%

Espanha12%

Itália6%

Bélgica6%

Alemanha5%

Outros17%

China42%

Holanda14%

Espanha10%

Itália5%

Outros29%

Brazil – Export Markets – 1990 x 2007

Exports

Soybean

Crushing

SoyMeal

SoyOil

Seeds and Losses

Exports

Internal Mkt

Exports

Internal Mkt

17

Brazilian States Risk Reward Analisys

Historical Data

Different Risk and Risk x Reward relationships

10

Y W

ors

t G

ross

Ma

rgin

0%

5%

10%

15%

20%

25%

30%

35%

0% 5% 10% 15% 20% 25% 30%

RS

GO

MS

MAPR

GOMT

MAPR

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

GO MS MT PR RS MA

10

Y Y

ield

Vo

latil

ity

Gross Margin

Too Risky

Best Risk x Reward

Good Risk x Reward

Hard to Scale Up

Good Risk x Reward

Lowest Risk and Margin

18

Los Grobo: LatAm Agribusiness Preeminent Agriculture Company

+

+

+

+

+

Sizeable and Diversified LatAm Player

One-Stop-Shop

Network Model

Superior Productivity and Efficiency

Proven Track Record with Strength Financials

Sponsors & Fully Aligned Management Team With Strong

Execution Capacity

Structured and scalable growth platform with secured

access to relevant grain production/origination

… leading to a highly synergistic business to maximize value creation throughout the Agribusiness Value Chain

Antonio Oliva [email protected]+55 62 3018-2700

Gustavo [email protected]+55 21 2554-1300

Contacts