AgricultureTransformationinAfricaandProspectsfortheGrainSector:

AcaseforTanzaniaDavidNyange,MiluMuyanga,DavidTschirley,ThomasSJayneDepartmentofAgricultural,FoodandResourceEconomics

MichiganStateUniversity

PresentationattheEasternAfricaGrainCouncilSecretariat7thAfricanGrainTradeSummit3-7October,2017

Dares Salaam,UnitedRepublicofTanzania

Acknowledgements:TheworkhighlightedhereisjointlyfundedthroughthegeneroussupportoftheAmericanpeoplethroughtheUnitedStatesAgencyforInternationalDevelopment(USAID)undertheFoodSecurityPolicyInnovationLabandbytheBillandMelindaGatesFoundationundertheGuidingInvestmentsinSustainableAgriculturalIntensificationGranttoMSU.

AgricultureTransformationinAfricaandProspectsfortheGrainSectorinTanzania

• Whyisagricultureandruraltransformationreceivingmuchattentioninrecentyears?

• Whatisagriculturetransformation?• IstransformationreallyhappeninginAfrica?

– Driversoftransformation

• Evidenceoftransformation– upstreamanddownstreamvaluechains

• Theprospectsforgrainsectorduringtransformation• Policyimplicationsforinclusivegrowth

WhyAgricultureandRuralTransformationinAfricaAreReceivingMuchAttentionRecently

• ReportsbyIFAD(2016),IFPRI,MSU,etc.• Rapideconomicgrowthduringthelasttwodecadesbut

povertylevelhasremainedhighinsomecountries• EvidenceconfirmsthatmostoftheAfricancountriesthat

registeredhighlevelofstructuralandeconomictransformationoverthelasttwodecadesmanagedtocutpovertyfasterthanslowtransformingcountries(IFAD,2016)

WhatisAgricultureTransformation• Istheprocessbywhichindividualfarmsshiftfromhighly

diversified,subsistence-orientedproduction,towardshighly

specialized,market-orientedsystem.

• Increasedintegrationofagriculturewithothersectorsinthe

domesticandinternationalmarkets.

• Ispartofabroaderprocessofstructuraltransformation,in

whichincreasingproportionofoutputandemploymentare

generatedbysectorsotherthanagriculture.

IsAgricultureTransformationReallyHappeninginAfrica?• Thereisacompellingevidencethatstructuralandagriculture

transformationisbeginningtotakerootinAfrica• Caveat– thereispaucityofdataandfragmentedinformation.• However,casestudiesindicatethat“Africa’sruralis

transformingdeeplyandquickly”(IFAD)• Macro-level:Evidenceofdecliningshareofagriculturelabor

force• Shiftinconsumptionpatternfrombasicstaplestowardshigh

value/processedfoodssuchashorticulturalandlivestockproducts

WhatisDrivingTransformation• Risingfooddemandandprices

– Populationexplosion

– Changingdemographics

– Risingincomes– emergingmiddleincomeclass

• Rapidurbanization

• Otherfactors– Availabilityofproductivityenhancingtechnologies

– Climatechange

– Regionalandinternationalmarketintegration

The Theory of Ag Sector Transformation

Agriculture Manufacturing Service IInformationTechnology

AgTransformationUpstreamtheValuechain

EastandSouthernAfrica(Jayne,TS,Muyanga,M,etal)

Farm size

Numberoffarms(%oftotal) %growthinnumberoffarmsbetweeninitialandlatestyear

%oftotaloperatedlandonfarmsbetween

0-100ha

2008 2012 2008 2012

0– 5ha 5,454,961(92.8) 6,151,035(91.4) 12.8 62.4 56.3

5– 10ha 300,511(5.1) 406,947(6.0) 35.4 15.9 18.0

10– 20ha 77,668(1.3) 109,960(1.6) 41.6 7.9 9.7

20– 100ha 45,700(0.7) 64,588(0.9) 41.3 13.8 16.0

Total 5,878,840(100%) 6,732,530(100%) 14.5 100.0 100.0

Changes in farm structure in Tanzania (2008-2012), LSMS/National Panel Surveys

43.7%

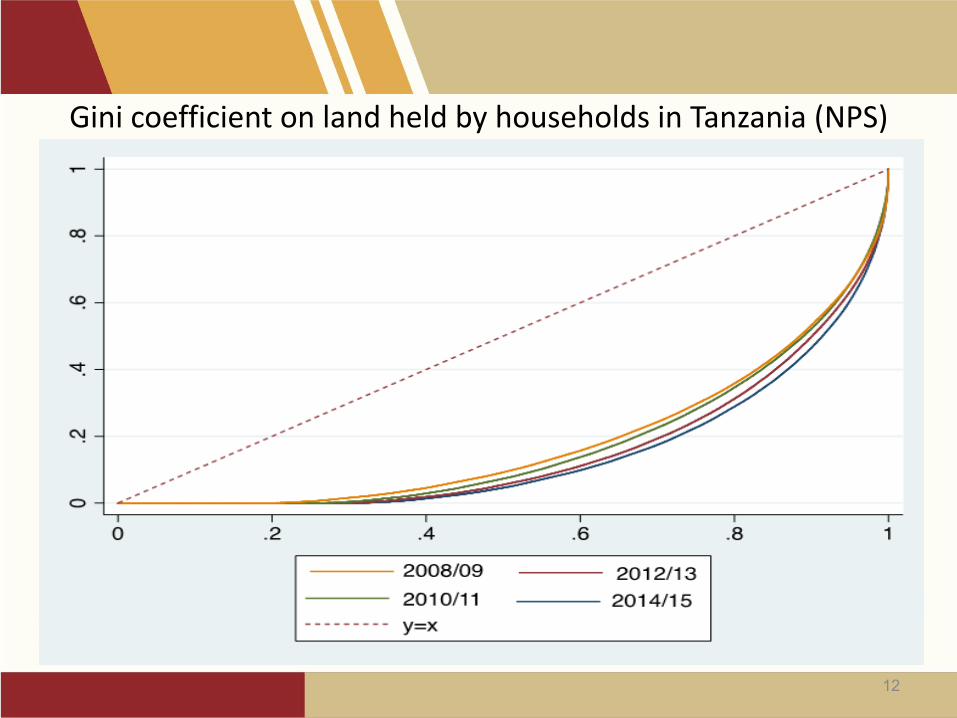

GinicoefficientonlandheldbyhouseholdsinTanzania(NPS)

12

Changesinfarmsizedistributions:Summary

1. Numberofsmallfarmsgrowingslowly

2. Numberofmedium-scalefarmsgrowingrapidly

3. Shareofareaundersmallfarmsdeclining

4. Shareofareaundermedium-scalegrowing,andcurrentlyover40%offarmholdings(>30%ofcultivatedarea)

13

Whoarethese

medium-scalefarmers?

14

% of National Landholdings held by Urban Households

26.8%

22.0%

11.2%

18.3%

10.9% 11.8%

32.7%

16.8%

22.0%

0%

5%

10%

15%

20%

25%

30%

35%

2008 2009 2004 2010 2010 2004/2005 2010 2007 2013/2014

Ghana Kenya Malawi Rwanda Tanzania Zambia

Source: Demographic and Health Surveys, various years between 2004-2014.

Riseofthemedium-scalefarmers

Riseofthemedium-scalefarmers

Riseofthemedium-scalefarmers

Type 1: Urban-based investor farmer

Modeofentry tomedium-scalefarmingstatus:acquirefarmusingnon-farmincome

Zambia Kenya(n=164) (n=180)

%ofcases 58 60%men 91.4 80Yearofbirth 1960 1947Yearsofeducationofhead 11 12.7Haveheldajobotherthanfarmer(%) 100 83.3Formerly/currentlyemployedbythepublicsector(%) 59.6 56.7

Currentlandholdingsize(ha) 74.9 50.1%oflandcurrentlyundercultivation 24.7 46.6Decadewhenlandwasacquired1969orearlier 1.1 61970-79 5.1 181980-89 7.4 201990-99 23.8 322000orlater 63.4 25

Source: MSU, UP, and ReNAPRI Retrospective Life History Surveys, 2015

Type 2: Rural-based ‘elite’ farmer

Modeofentryintomedium-scalefarmingstatus:expansion ofruraleliteZambia Kenya(n=118) (n=120)

%ofcases 42 40%men 92.9 82.5Yearofbirth 1966 1945Yearsofeducationofhead 8.2 7.5Haveheldajobotherthanasafarmer(%) 32.9 17.5Landholding sizewhenoperatorstartedownhousehold(ha) 10.7 16.2

Currentlandholdingsize(ha) 38.2 32.7%oflandcurrentlyundercultivation 46.9 54.1Decadewhenlandwasacquired1969orearlier 3.9 291970-79 6.7 241980-89 14.8 201990-99 32.2 182000orlater 42.0 9

Source: MSU, UP, and ReNAPRI Retrospective Life History Surveys, 2015

Consequencesof

changingfarmsize

distributions

21

Consequencesofchangingfarmsizedistributions

1. Risinguseofmechanization2. Morecapitalusing/labor-savingformsofagricultural

production3. Arablelandlessfullyutilized,butbetterlandmgt4. Somedisplacement5. Risinglandpricesà strainingyouthaccesstoland6. Multipliereffectsofaggrowtharechanging7. Govts lessabletoaccuratelyestimateagproduction

22

NominalvalueoftractorimportstoSub-SaharanAfrica(excludingSouthAfrica),2001-2015

23

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

2001 2003 2005 2007 2009 2011 2013 2015

Nom

inal

val

ue o

f im

ports

in ‘0

00 U

S$

Sub-Saharan Africa Southern Africa North Eastern AfricaWestern Africa Linear (Sub-Saharan Africa)

Source: vanderWesthuisen, forthcoming

Nominal value of tractor imports in selective Sub-Saharan African countries (2001-2015)

24Source: vanderWesthuisen, forthcoming

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

2001 2003 2005 2007 2009 2011 2013 2015

Valu

e of

Impo

rts: U

S$ T

hous

and

Ghana Nigeria Kenya Tanzania Zambia

Linear (Ghana) Linear (Nigeria) Linear (Kenya) Linear (Tanzania) Linear (Zambia)

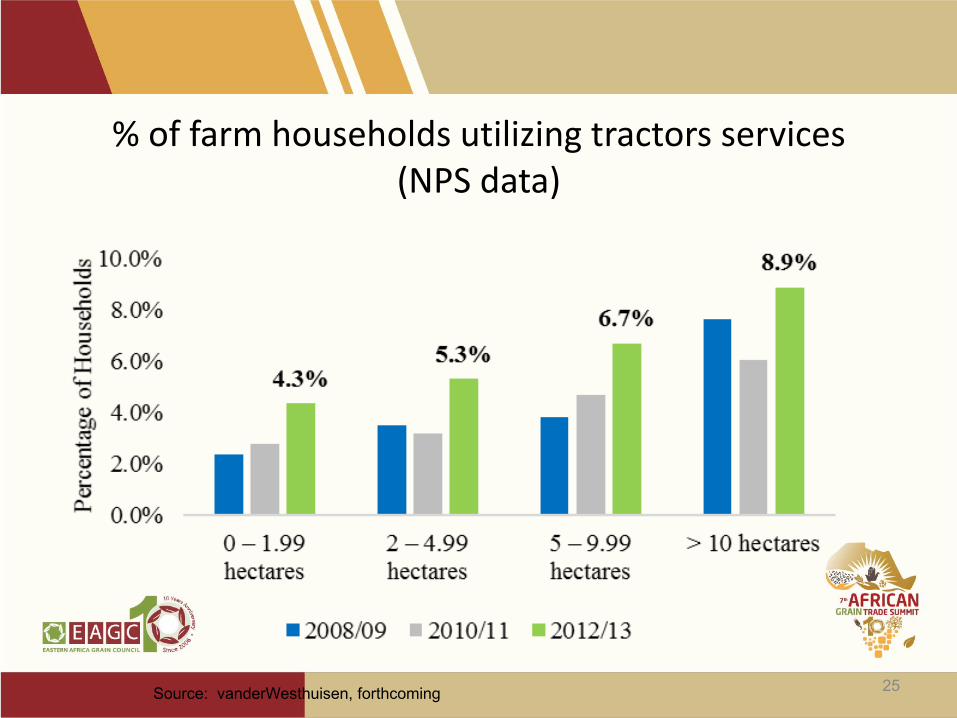

%offarmhouseholdsutilizingtractorsservices(NPSdata)

25Source: vanderWesthuisen, forthcoming

GINIcoefficientsinfarmlandholding

26

Period MovementinGinicoefficient:

Ghana(cult.area)(GLSS) 1992à 2013 0.54à 0.70

Kenya(cult.area)(KIHBS) 1994à 2006 0.51à 0.55

Tanzania(landholdings)(LSMS) 2008à 2012 0.63à 0.69

Tanzania(areacontrolled)(ASCS) 2008 0.89

Zambia(landholding)(CFS) 2001à 2012 0.42à 0.49

Source:Jayneetal.2014(JIA)

27

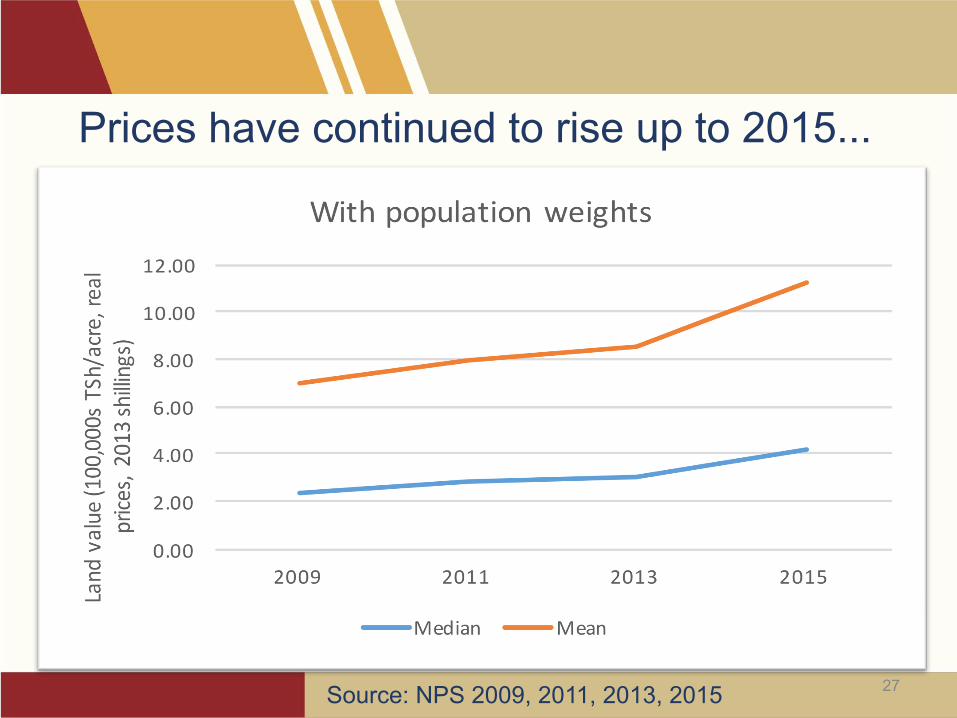

Prices have continued to rise up to 2015...

Source: NPS 2009, 2011, 2013, 2015

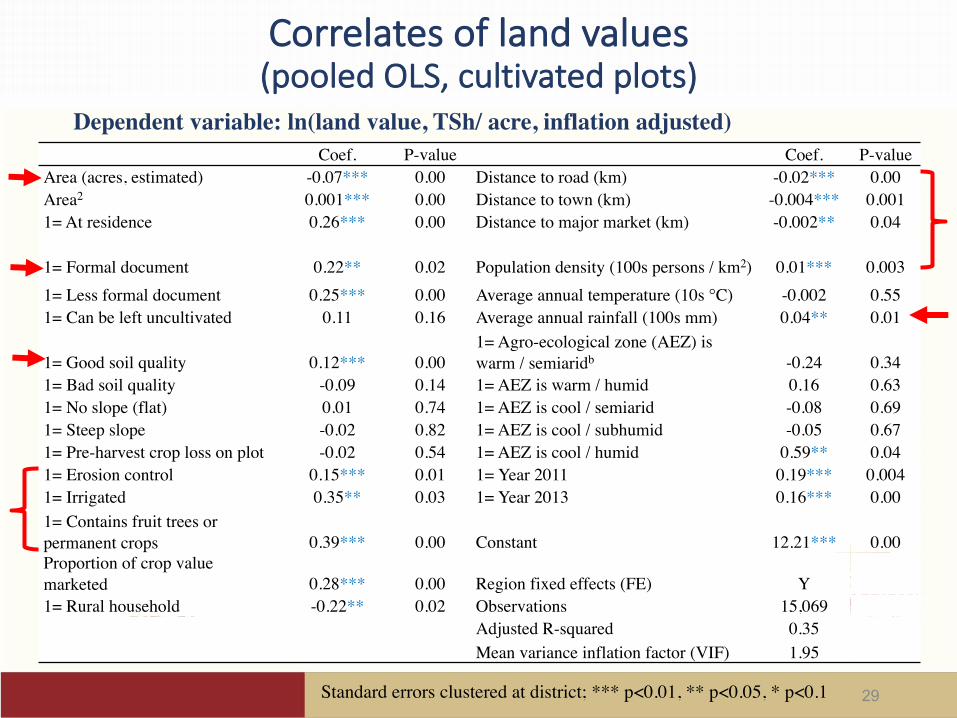

Topic FactorHypothesized relationship

Miscellaneous Plot size ConvexPopulation density +Tenure security +Forest / fallow / other use +

Agricultural potential Soil quality +Slope -Average rainfall / temperature + / -On-farm amendments +Pre-harvest crop losses -

Market access / urban pressure Rural location of homestead -Distance from road / town / market -Household's market orientation +

Hypothesized correlates of land values in Tanzania

28

Coef. P-value Coef. P-valueArea (acres, estimated) -0.07*** 0.00 Distance to road (km) -0.02*** 0.00Area2 0.001*** 0.00 Distance to town (km) -0.004*** 0.0011= At residence 0.26*** 0.00 Distance to major market (km) -0.002** 0.04

1= Formal document 0.22** 0.02 Population density (100s persons / km2) 0.01*** 0.0031= Less formal document 0.25*** 0.00 Average annual temperature (10s °C) -0.002 0.551= Can be left uncultivated 0.11 0.16 Average annual rainfall (100s mm) 0.04** 0.01

1= Good soil quality 0.12*** 0.001= Agro-ecological zone (AEZ) is warm / semiaridb -0.24 0.34

1= Bad soil quality -0.09 0.14 1= AEZ is warm / humid 0.16 0.631= No slope (flat) 0.01 0.74 1= AEZ is cool / semiarid -0.08 0.691= Steep slope -0.02 0.82 1= AEZ is cool / subhumid -0.05 0.671= Pre-harvest crop loss on plot -0.02 0.54 1= AEZ is cool / humid 0.59** 0.041= Erosion control 0.15*** 0.01 1= Year 2011 0.19*** 0.0041= Irrigated 0.35** 0.03 1= Year 2013 0.16*** 0.001= Contains fruit trees or permanent crops 0.39*** 0.00 Constant 12.21*** 0.00Proportion of crop value marketed 0.28*** 0.00 Region fixed effects (FE) Y1= Rural household -0.22** 0.02 Observations 15,069

Adjusted R-squared 0.35Mean variance inflation factor (VIF) 1.95

Correlatesoflandvalues(pooledOLS,cultivatedplots)

29Standard errors clustered at district; *** p<0.01, ** p<0.05, * p<0.1

Dependent variable: ln(land value, TSh/ acre, inflation adjusted)

30

The Cropping Pattern is Changing –Area under legumes and oil seed increasing much faster, followed by maize and rice

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Hectares

Areasundercropcategories,summedoverbothseasonsAllhouseholds

2009 2011 2013 2015

AgTransformationDownstreamtheValuechain

ForEastandSouthernAfrica(Tschirley,D.,etal)

31

EvolutionofRealFoodMarketSizeinEast&SouthernAfrica2010-2040(USD)

$0

$50

$100

$150

$200

$250

$300

2010 2015 2020 2025 2030 2035 2040

Billio

nUSD

perY

ear

Ownproduction Unprocessed FormalLow FormalHigh

EvolutionofRealFoodMarketSizeinEast&SouthernAfrica,2010-2040(USD)

Totalvalue,processedfood

$0

$50

$100

$150

$200

$250

$300

2010 2015 2020 2025 2030 2035 2040

Billion

USD

perYear

Ownproduction Unprocessed FormalLow FormalHigh Totalprocessed

Totalprocessedup7x

Willruralareas

lookdifferent?

EvolutionofRealpercapita FoodExpendituresinRural&UrbanESA,2010-2040

Rural Urban

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2010 2015 2020 2025 2030 2035 2040

USDExpenditureperCapitaperDay

Unprocessed FormalLow FormalHigh Totalprocessed

Up>2x

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2010 2015 2020 2025 2030 2035 2040

USDExpenditureperCapitaperDay

Unprocessed FormalLow FormalHigh Totalprocessed

Up3x

Willthepoor

lookdifferent?

EvolutionofRealpercapita FoodExpendituresamongPoorest&RichestOne-ThirdofPopulationofESA,

2010-2040

Bottomone-third Topone-third

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2010 2015 2020 2025 2030 2035 2040

USDExpenditureperCapitaperDay

Unprocessed FormalLow FormalHigh Totalprocessed

Up3.5x

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2010 2015 2020 2025 2030 2035 2040

USDExpenditureperCapitaperDay

Unprocessed FormalLow FormalHigh Totalprocessed

Up3.5x

Take-home

Growthwillbestronginruralandurban

areas,andamongthepoorandnon-poor

(thoughfromdifferentstartingpoints)

Willthe“traditional”retailsectordisappear?• No!

• Sharewillfallfrom90%to65%by2040• Butsizewillincrease6.5x

– Duetogrowthinincomes,population,andurbanshare

• Butitwillneedtobeadifferent traditionalsector• Consumerincomes3x-4xhigher• Willdemandmorequality,packaging,variety,safety• Needfortraining,entrepreneurialassistance

Yes!

No!

ConclusionandPolicyImplications• Thegrainsectorwillcontinuetogrowamidthechanging

productionandconsumptionpattern• Theslowdowninproductionofmaizemayaccelerateasthe

feedindustryexpandsinresponsetoincreasedconsumptionoflivestockproducts

• Theincreaseindemandforprocessedfoodscontributetotransformationinthefoodsystems

• Failuretoinvestadequatelyinagricultureandtherestofthefoodsystemcanchokeofftheprocessofstructuraltransformationandfoodsecurity.