ALL EYES ON DIGITAL VIDEO

State of the Industry Video Research 2017

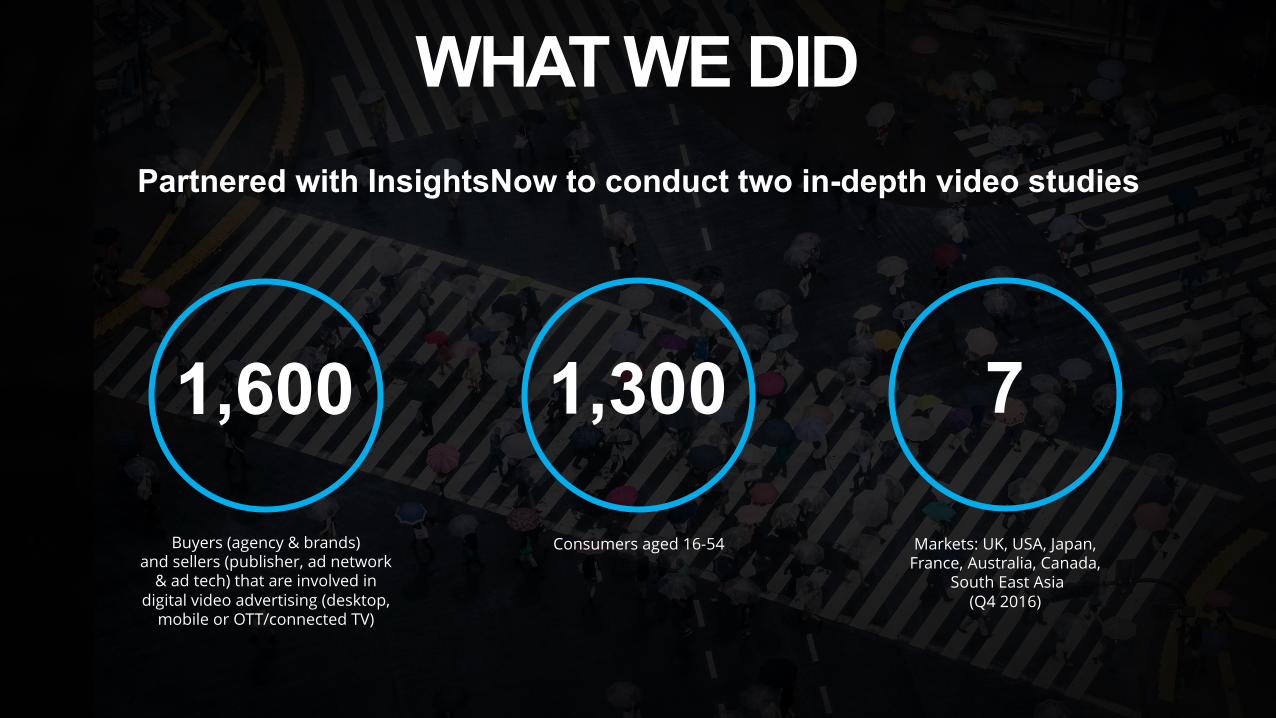

Partnered with InsightsNow to conduct two in-depth video studies

WHAT WE DID

Buyers (agency & brands) and sellers (publisher, ad network

& ad tech) that are involved in digital video advertising (desktop,

mobile or OTT/connected TV)

1,600

Consumers aged 16-54

1,300

Markets: UK, USA, Japan, France, Australia, Canada,

South East Asia (Q4 2016)

7

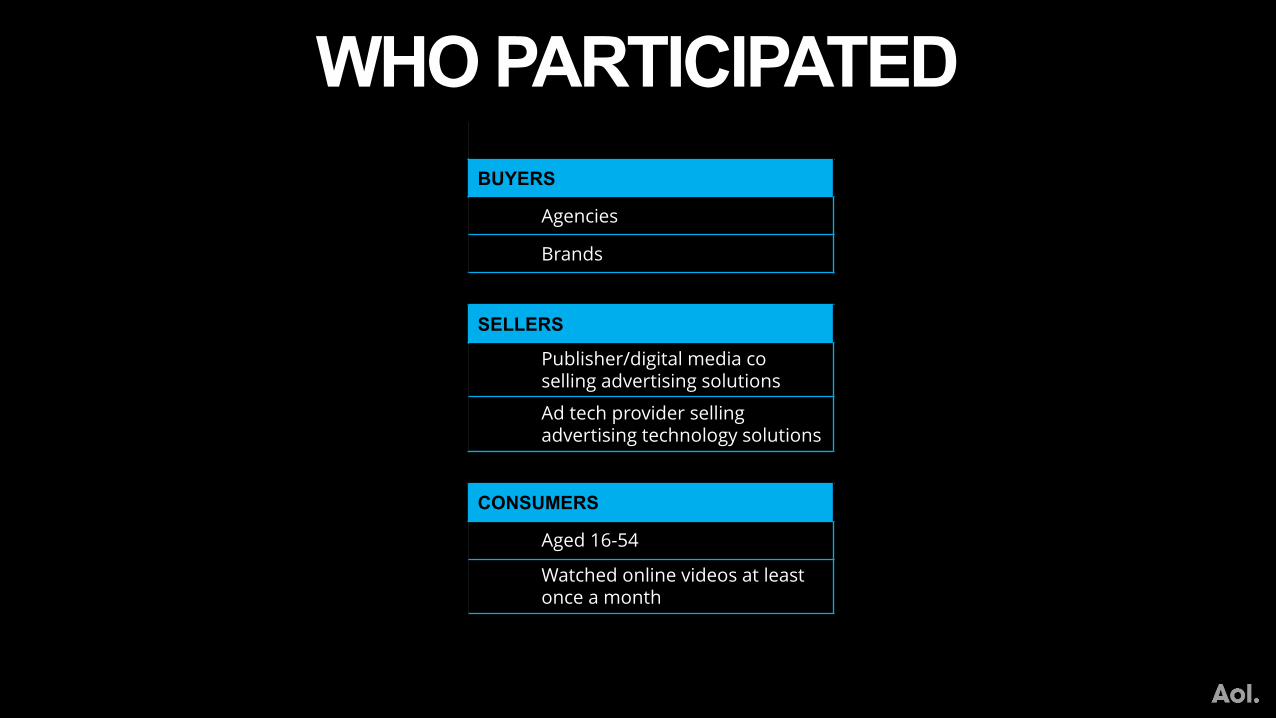

WHO PARTICIPATEDBUYERS

Agencies

Brands

SELLERS

Publisher/digital media co selling advertising solutions

Ad tech provider selling advertising technology solutions

CONSUMERS

Aged 16-54

Watched online videos at least once a month

WHAT WE LEARNED

MACRO TRENDS MOBILE VIDEO PROGRAMMATIC EMERGING VIDEO TRENDS

AD FORMATS ORIGINAL VIDEO CONTENT MEASUREMENT THE FUTURE OF DIGITAL VIDEO

ONLINE VIDEO IS A DAILY HABIT FOR CONSUMERS

of consumers watch online videos daily

71%of consumers say they watch more than a year ago

54%of consumers are watching more than 4hrs of online video a week

42%4+hrs

Source: AOL State of Video Industry 2017, UK

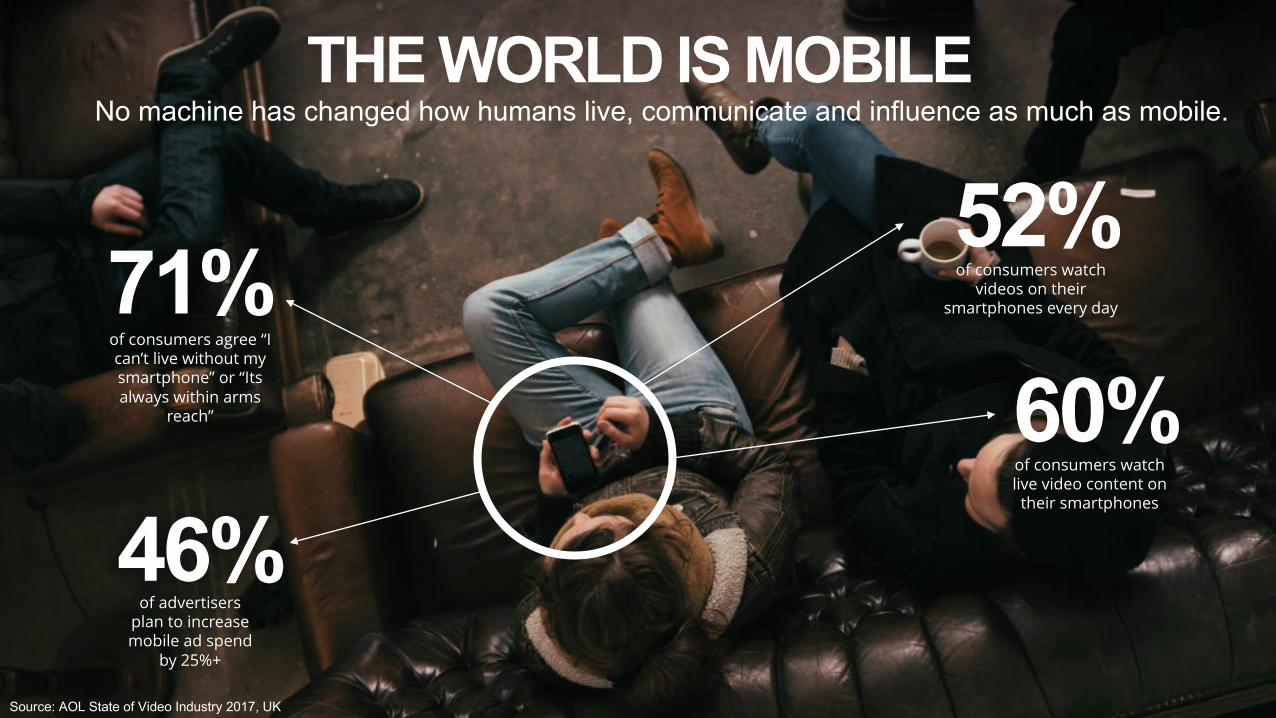

THE WORLD IS MOBILENo machine has changed how humans live, communicate and influence as much as mobile.

71%of consumers agree “I can’t live without my smartphone” or “Its always within arms

reach”

46%of advertisers

plan to increase mobile ad spend

by 25%+

52%of consumers watch

videos on their smartphones every day

60%of consumers watch live video content on their smartphones

Source: AOL State of Video Industry 2017, UK

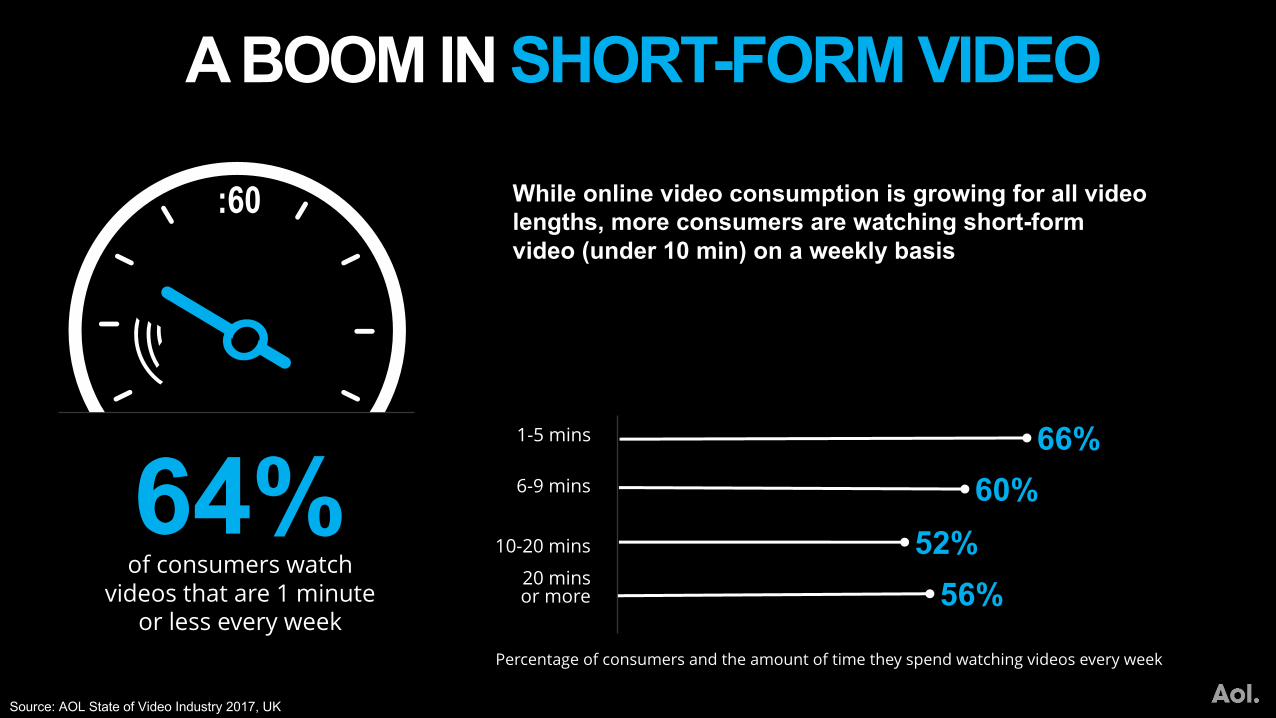

While online video consumption is growing for all video lengths, more consumers are watching short-form video (under 10 min) on a weekly basis

A BOOM IN SHORT-FORM VIDEO

64%

:60

of consumers watchvideos that are 1 minute

or less every weekPercentage of consumers and the amount of time they spend watching videos every week

60%52%

56%

6-9 mins

10-20 mins

20 minsor more

66%1-5 mins

Source: AOL State of Video Industry 2017, UK

Source: AOL State of Video Industry 2017, UK

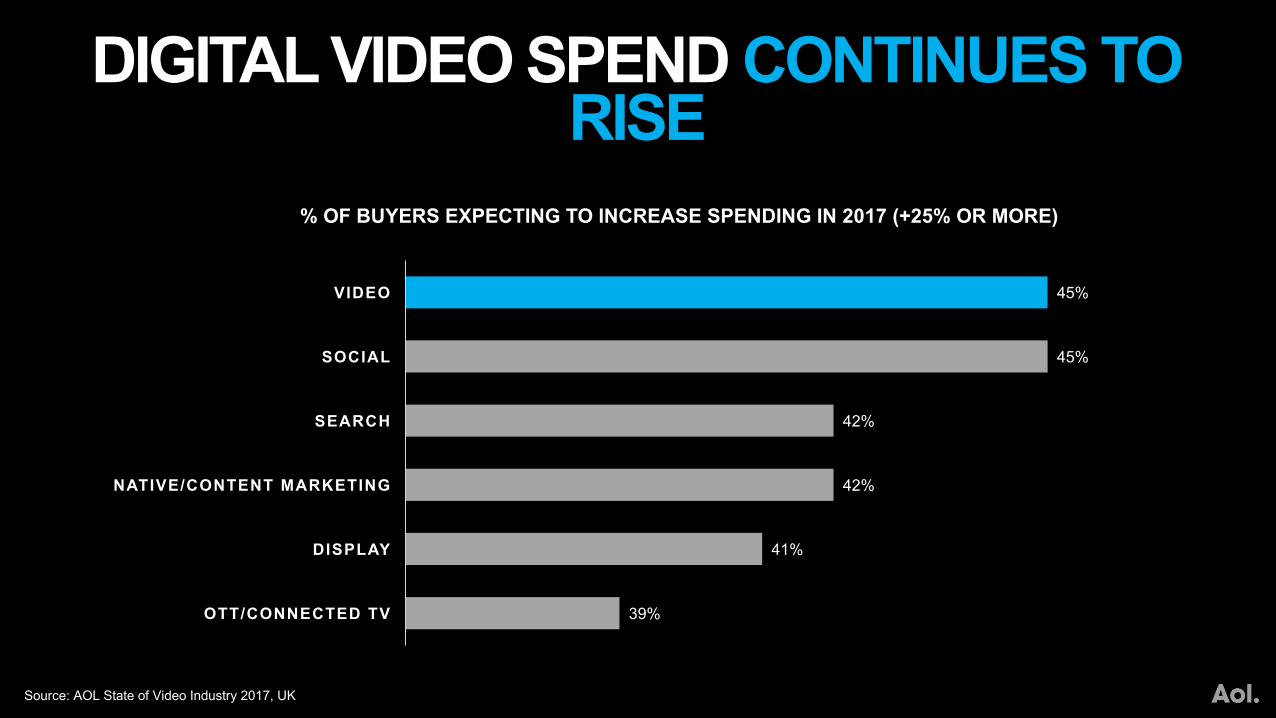

DIGITAL VIDEO SPEND CONTINUES TO RISE

39%

41%

42%

42%

45%

45%

OTT/CONNECTED TV

DISPLAY

NATIVE/CONTENT MARKETING

SEARCH

SOCIAL

VIDEO

% OF BUYERS EXPECTING TO INCREASE SPENDING IN 2017 (+25% OR MORE)

49%

49%

44%

41%

35%

33%

7%

Television

Display

Search

Out of Home

Direct Response

Other Media Type

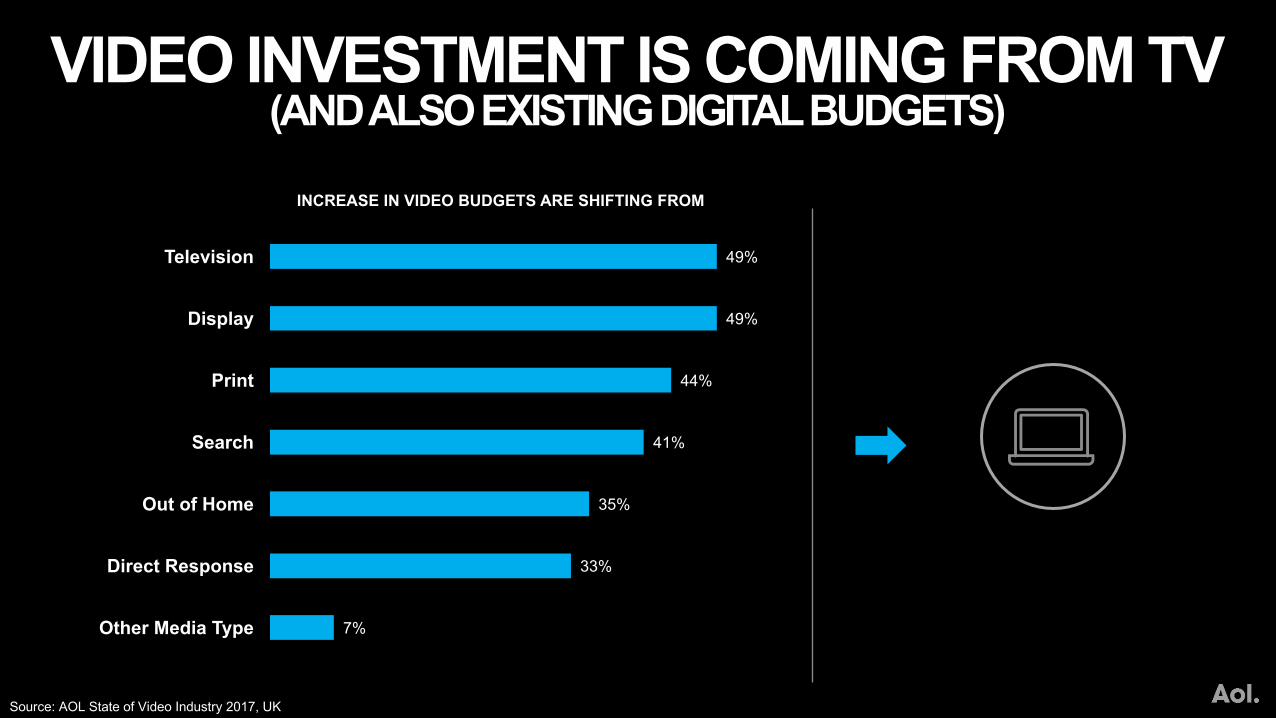

VIDEO INVESTMENT IS COMING FROM TV (AND ALSO EXISTING DIGITAL BUDGETS)

INCREASE IN VIDEO BUDGETS ARE SHIFTING FROM

Source: AOL State of Video Industry 2017, UK

49%47%

44%41%

35%33%

7%

Display Television Print Search Out of Home Direct Response

Other Media Type

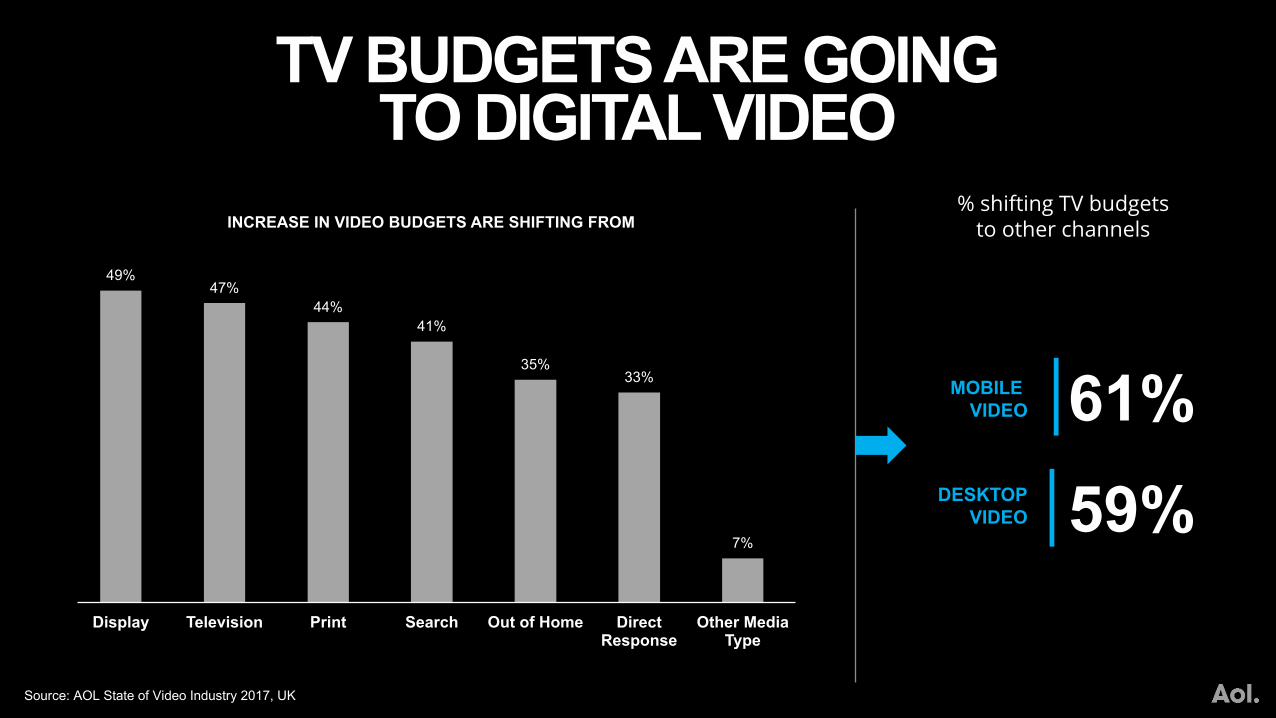

TV BUDGETS ARE GOING TO DIGITAL VIDEO

INCREASE IN VIDEO BUDGETS ARE SHIFTING FROM% shifting TV budgets

to other channels

DESKTOPVIDEO

61%MOBILE VIDEO

59%

Source: AOL State of Video Industry 2017, UK

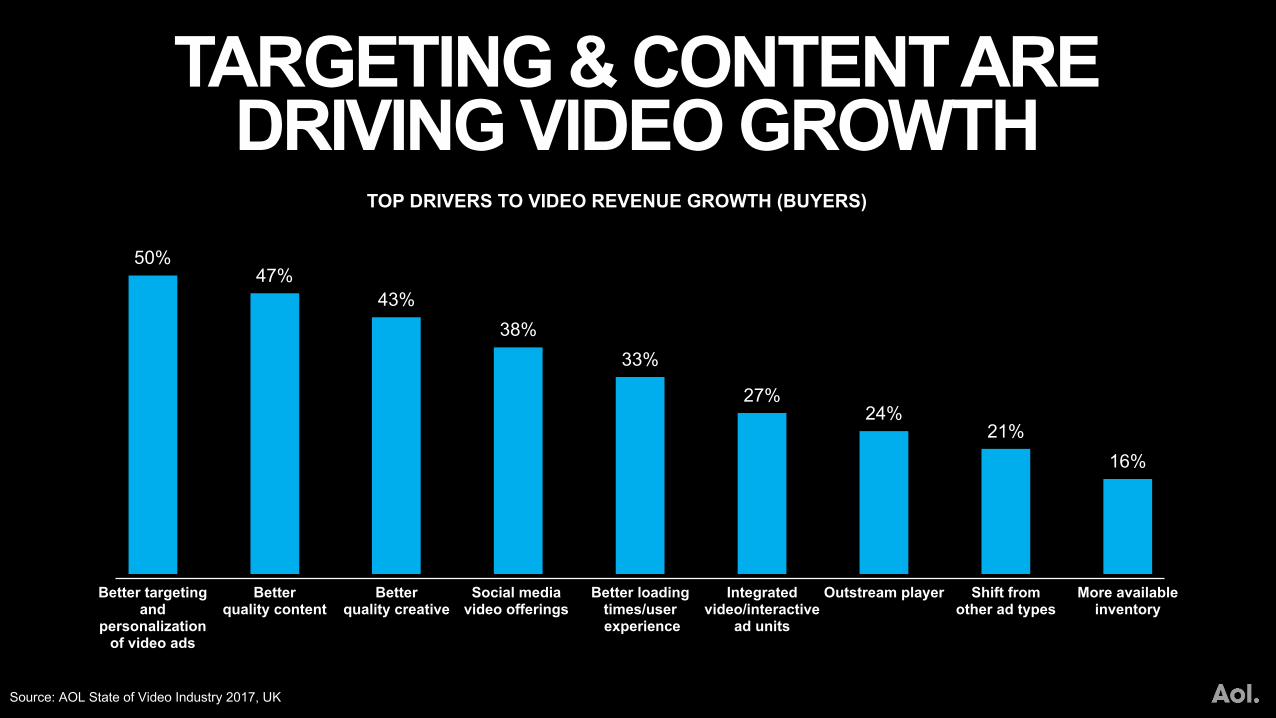

TARGETING & CONTENT ARE DRIVING VIDEO GROWTH

Social media & quality creative are50%

47%43%

38%33%

27%24%

21%16%

Better targetingand

personalization of video ads

Betterquality content

Better quality creative

Social media video offerings

Better loading times/userexperience

Integrated video/interactive

ad units

Outstream player Shift from other ad types

More available inventory

TOP DRIVERS TO VIDEO REVENUE GROWTH (BUYERS)

Source: AOL State of Video Industry 2017, UK

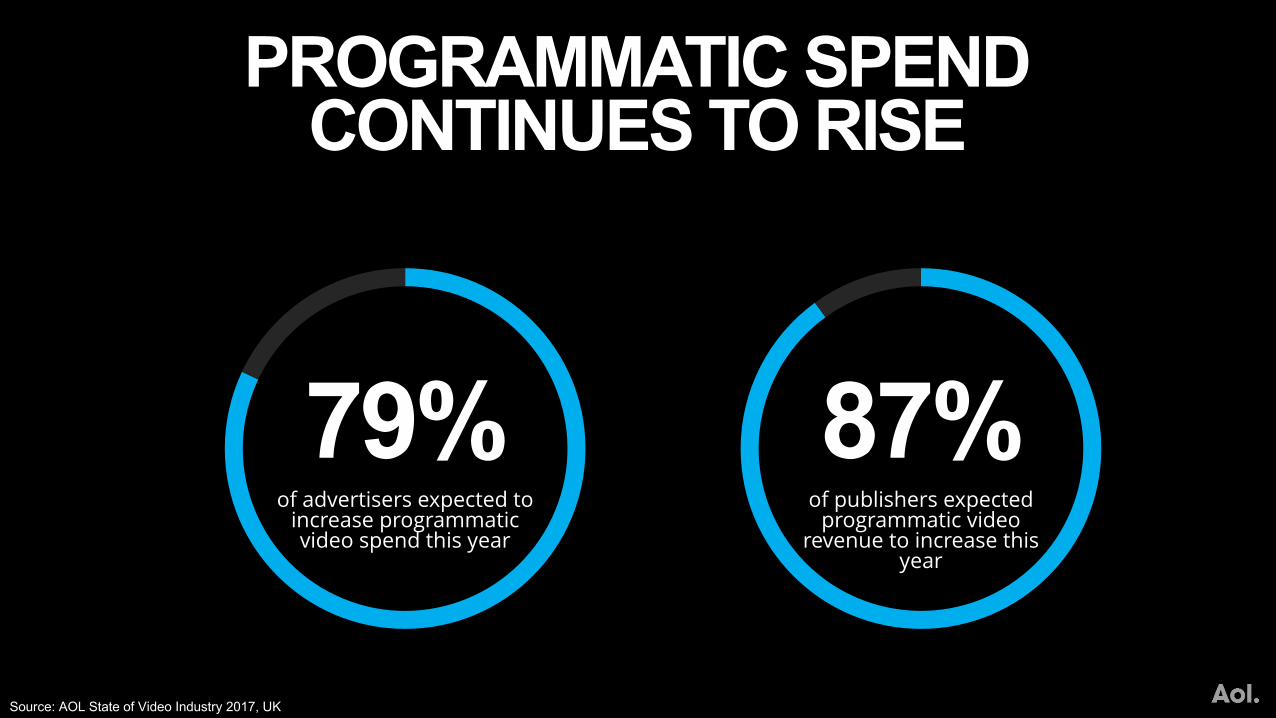

PROGRAMMATIC SPEND CONTINUES TO RISE

of advertisers expected to increase programmatic video spend this year

79%of publishers expected

programmatic video revenue to increase this

year

87%

Source: AOL State of Video Industry 2017, UK

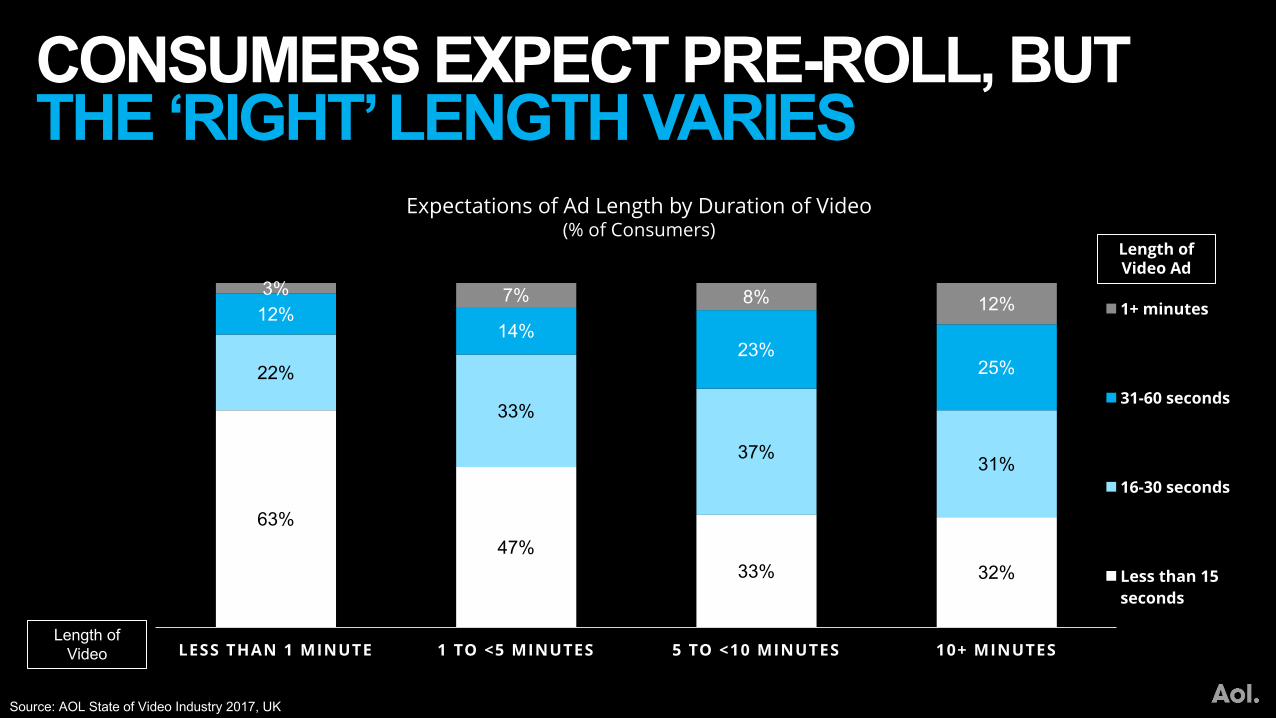

CONSUMERS EXPECT PRE-ROLL, BUT THE ‘RIGHT’ LENGTH VARIES

63%47%

33% 32%

22%

33%

37% 31%

12%14%

23%25%

3% 7% 8% 12%

LESS THAN 1 MINUTE 1 TO <5 MINUTES 5 TO <10 MINUTES 10+ MINUTES

1+ minutes

31-60 seconds

16-30 seconds

Less than 15 seconds

Length of Video

Expectations of Ad Length by Duration of Video(% of Consumers)

Length of Video Ad

Source: AOL State of Video Industry 2017, UK

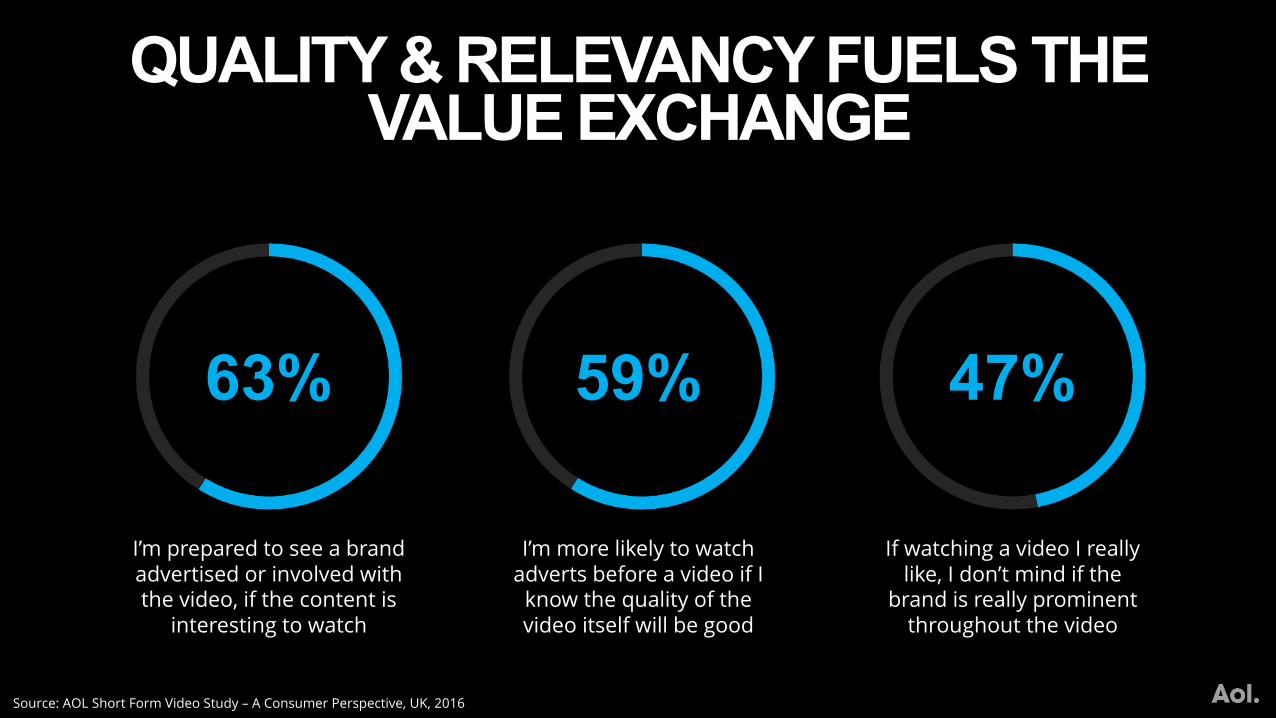

QUALITY & RELEVANCY FUELS THE VALUE EXCHANGE

Source: AOL Short Form Video Study – A Consumer Perspective, UK, 2016

I’m prepared to see a brand advertised or involved with the video, if the content is

interesting to watch

63%

I’m more likely to watch adverts before a video if I

know the quality of the video itself will be good

59%

If watching a video I really like, I don’t mind if the

brand is really prominent throughout the video

47%

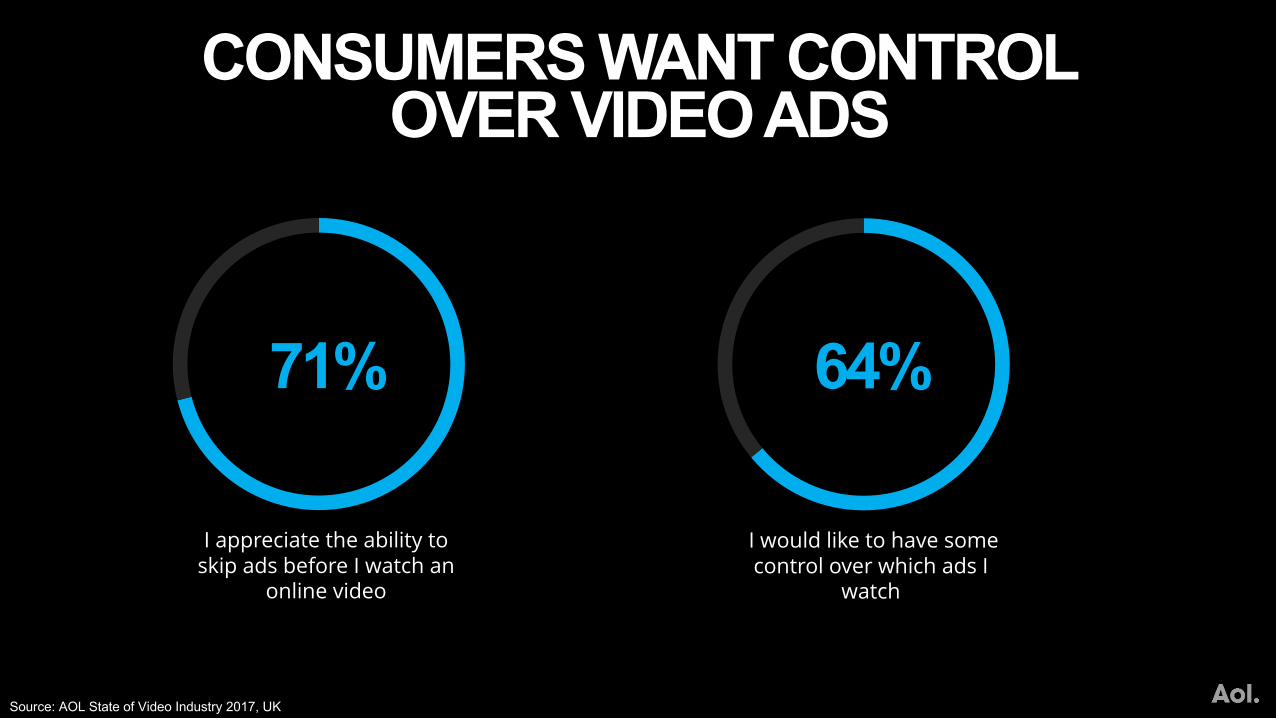

CONSUMERS WANT CONTROL OVER VIDEO ADS

I appreciate the ability to skip ads before I watch an

online video

71%

I would like to have some control over which ads I

watch

64%

Source: AOL State of Video Industry 2017, UK

57% of Advertisers identified branded content as the biggest revenue opportunity over the next 12 months.

BRANDED VIDEO IS STILL A TOP REVENUE DRIVER

48%

57%

55%

User generated content

Branded video content (content that is co-created between an advertiser and a publisher/content creator)

New Formats like 360 Video, Vertical Video, Virtual Reality, Augmented Reality, Outstream

2017 TOP 3 REVENUE OPPORTUNITIES – VIDEO CONTENT FORMATS

Source: AOL State of Video Industry 2017, UK

ADVERTISERS SEE QUALITY & PROOF POINTS AS TOP CHALLENGES

13%

17%

21%

21%

21%

29%

29%

29%

38%

38%

46%

Scale

Lack of understanding of the space

Lack of promotion of the video content to audiences

Lack of custom integration

Audience and campaign measurement

Lack of transparency in the buying process

Video ad unit lengths

Price/cost

Lack of standard success metrics

Proof of ROI for video vs. other media

Quality of content

MARKETERS TOP 3 CHALLENGES WITH BUYING BRANDED VIDEO CONTENT

Source: AOL State of Video Industry 2017, UK

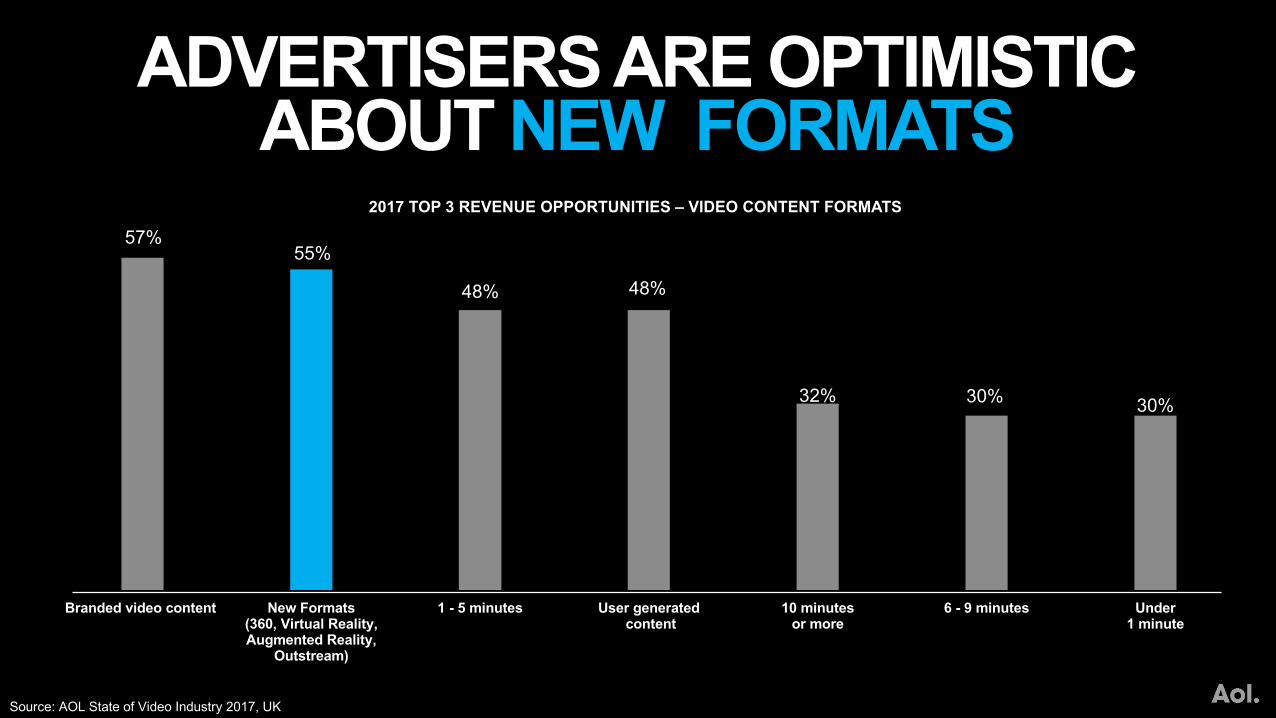

ADVERTISERS ARE OPTIMISTIC ABOUT NEW FORMATS

57%55%

48% 48%

32% 30% 30%

Branded video content New Formats(360, Virtual Reality, Augmented Reality,

Outstream)

1 - 5 minutes User generatedcontent

10 minutes or more

6 - 9 minutes Under 1 minute

2017 TOP 3 REVENUE OPPORTUNITIES – VIDEO CONTENT FORMATS

Source: AOL State of Video Industry 2017, UK

LIVE VIDEO GAINS GROUND

73%of consumers have

watched live video content

68%of advertisers plan

to invest in live videoin 2017

Source: AOL State of Video Industry 2017, UK

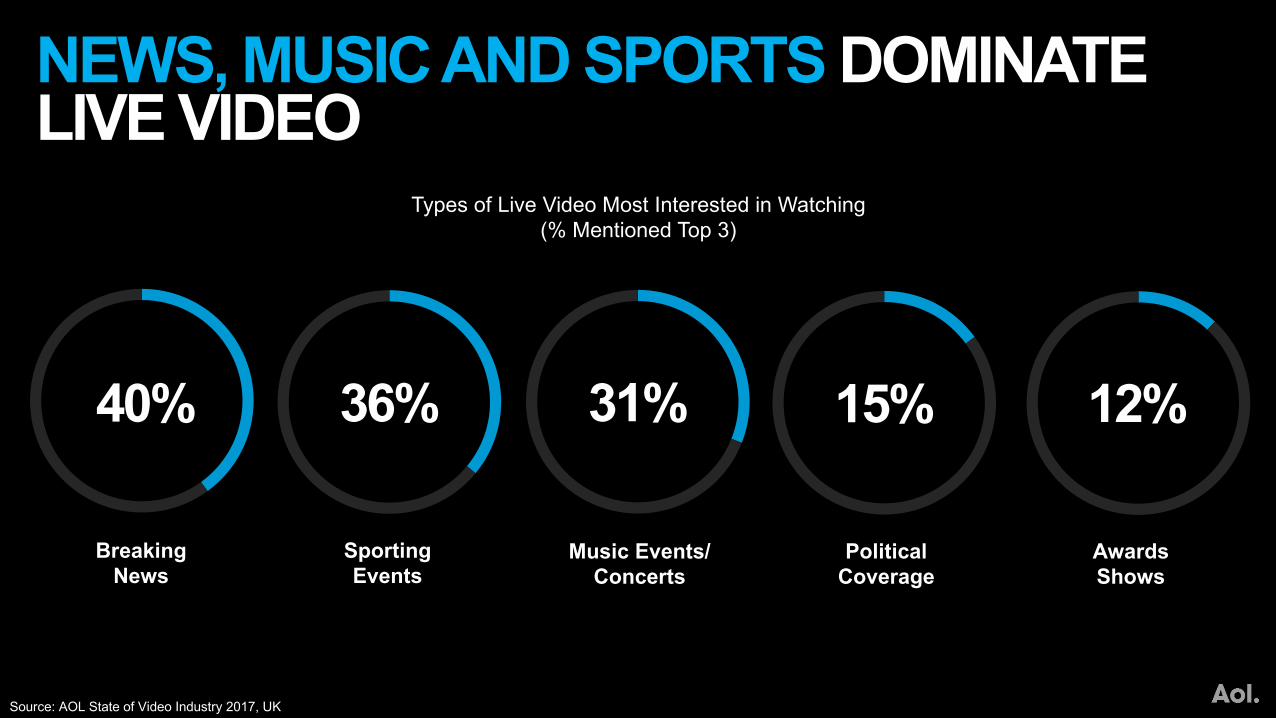

NEWS, MUSIC AND SPORTS DOMINATE LIVE VIDEO

Types of Live Video Most Interested in Watching(% Mentioned Top 3)

Music Events/Concerts

BreakingNews

SportingEvents

AwardsShows

PoliticalCoverage

40% 31% 15% 12%36%

Source: AOL State of Video Industry 2017, UK

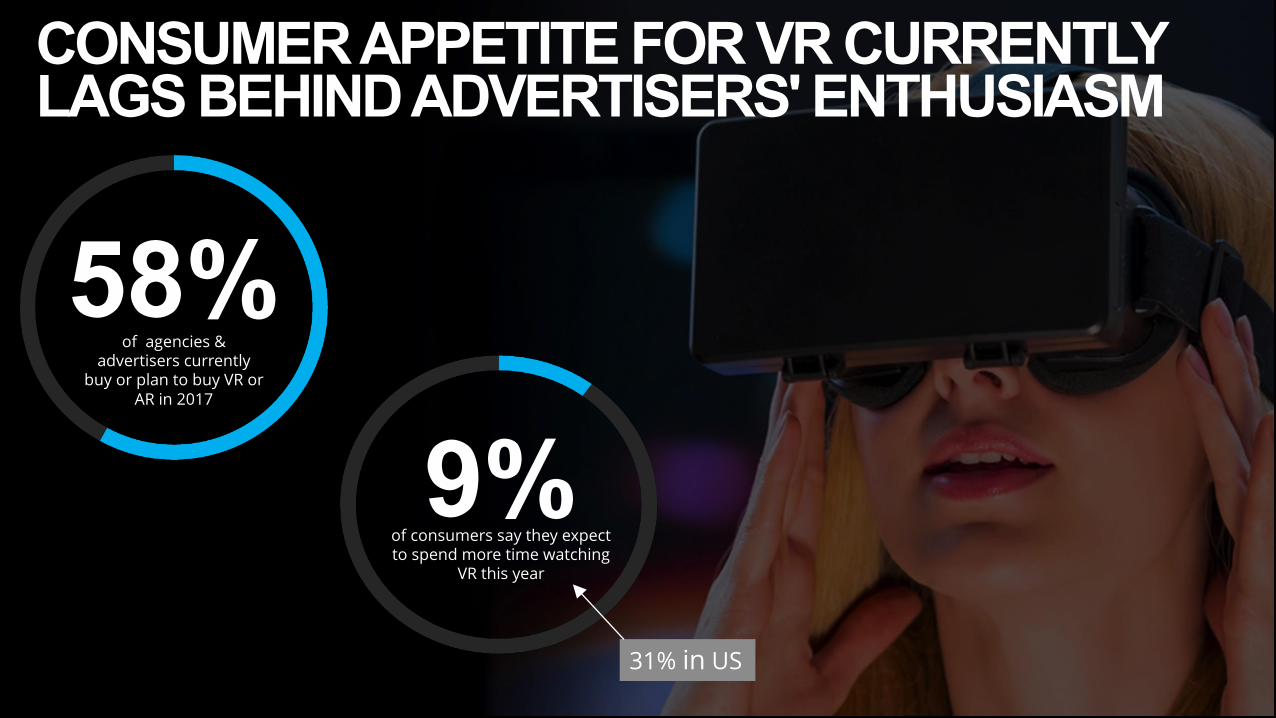

CONSUMER APPETITE FOR VR CURRENTLY LAGS BEHIND ADVERTISERS' ENTHUSIASM

of agencies & advertisers currently

buy or plan to buy VR or AR in 2017

58%

of consumers say they expect to spend more time watching

VR this year

9%31% in US

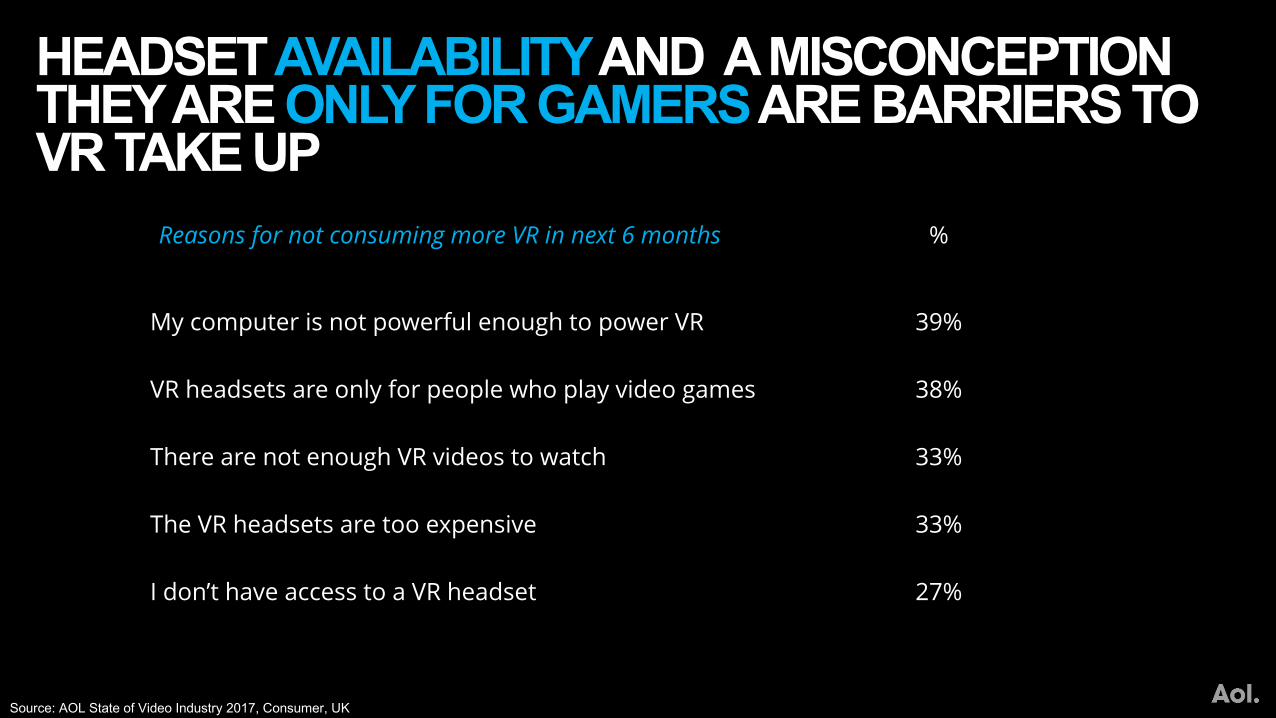

HEADSET AVAILABILITYAND A MISCONCEPTION THEY ARE ONLY FOR GAMERSARE BARRIERS TO VR TAKE UP

Reasons for not consuming more VR in next 6 months %

My computer is not powerful enough to power VR 39%

VR headsets are only for people who play video games 38%

There are not enough VR videos to watch 33%

The VR headsets are too expensive 33%

I don’t have access to a VR headset 27%

Source: AOL State of Video Industry 2017, Consumer, UK

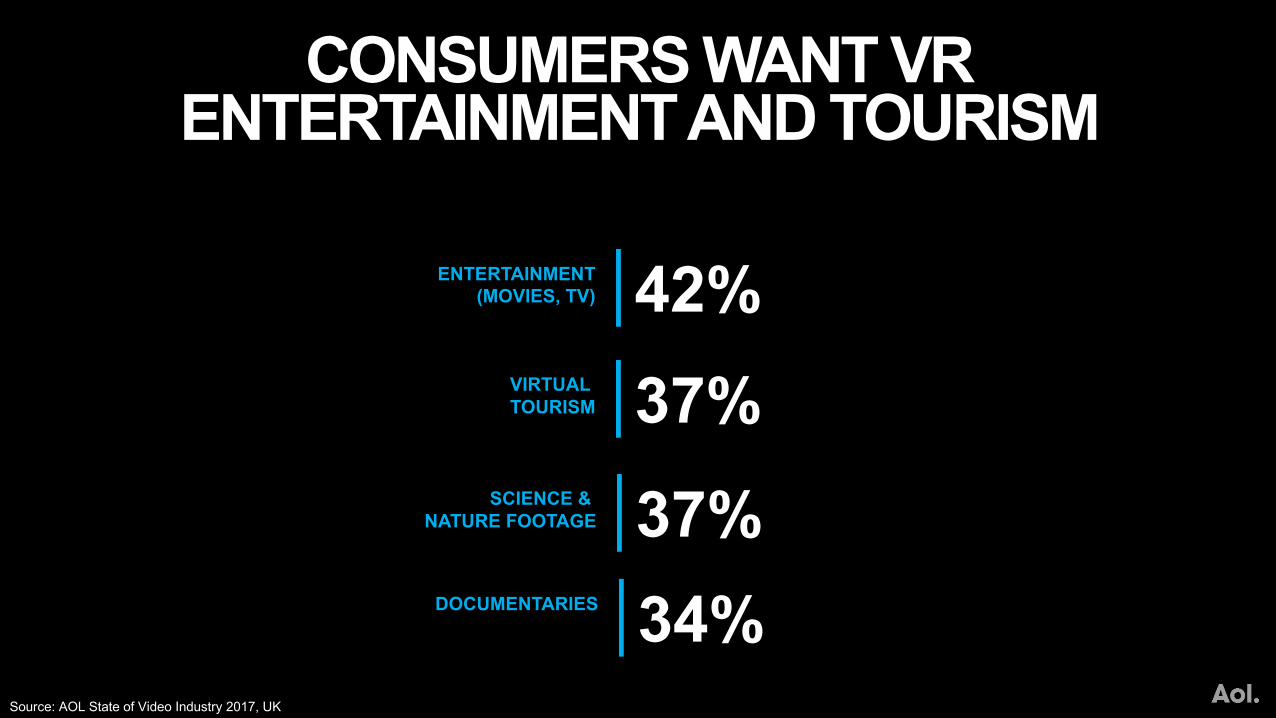

CONSUMERS WANT VR ENTERTAINMENT AND TOURISM

ENTERTAINMENT(MOVIES, TV) 42%

VIRTUAL TOURISM 37%

SCIENCE & NATURE FOOTAGE 37%

DOCUMENTARIES 34%Source: AOL State of Video Industry 2017, UK