ALM. BRAND BANK A/S INTERIM REPORT - FIRST HALF OF YEAR 2009

ALM. BRAND BANK A/S • MIDTERMOLEN 7 • 2100 COPENHAGEN Ø · REGISTRATION (CVR) NO. 81 75 35 12

ALM. SUND FORNUFTWWW.ALMBRAND.DK

Alm. Brand Bank A/S – H1 2009

Page 1 of 33

CONTENTS

COMPANY INFORMATION2 Company information

2 Group structure

MANAGEMENT’S REVIEW3 Financial highlights and key ratios

4 Report

8 Lending portfolio and credit losses

SIGNATURES12 Statement by the Board of Directors and the Management Board

FINANCIAL STATEMENTS Group13 Accounting policies

14 Income statement

15 Balance sheet

17 Statement of changes in equity

18 Cash flow statement

19 Notes to the financial statements

Parent company24 Accounting policies

25 Income statement

26 Balance sheet

28 Statement of changes in equity

29 Notes to the financial statements

Alm. Brand Bank A/S – H1 2009

Page 2 of 33

COMPANY INFORMATION BOARD OF DIRECTORS Jørgen H. Mikkelsen, Chairman Boris Nørgaard Kjeldsen, Deputy Chairman Arne Nielsen Søren Boe Mortensen Ole Bach, elected by the employees Jesper Christiansen, elected by the employees MANAGEMENT BOARD Ole Joachim Jensen, Interim Chief Executive Bo Chr. Alberg, Managing Director REGISTRATION Alm. Brand Bank A/S Company registration (CVR) no. 81 75 35 12

AUDITORS Deloitte, Statsautoriseret Revisionsaktieselskab INTERNAL AUDITOR Poul-Erik Winther, Group Chief Auditor ADDRESS Midtermolen 7 DK-2100 Copenhagen Ø Phone: + 45 35 47 48 49 Fax: + 45 35 47 47 35 Internet: www.almbrand.dk E-mail: [email protected]

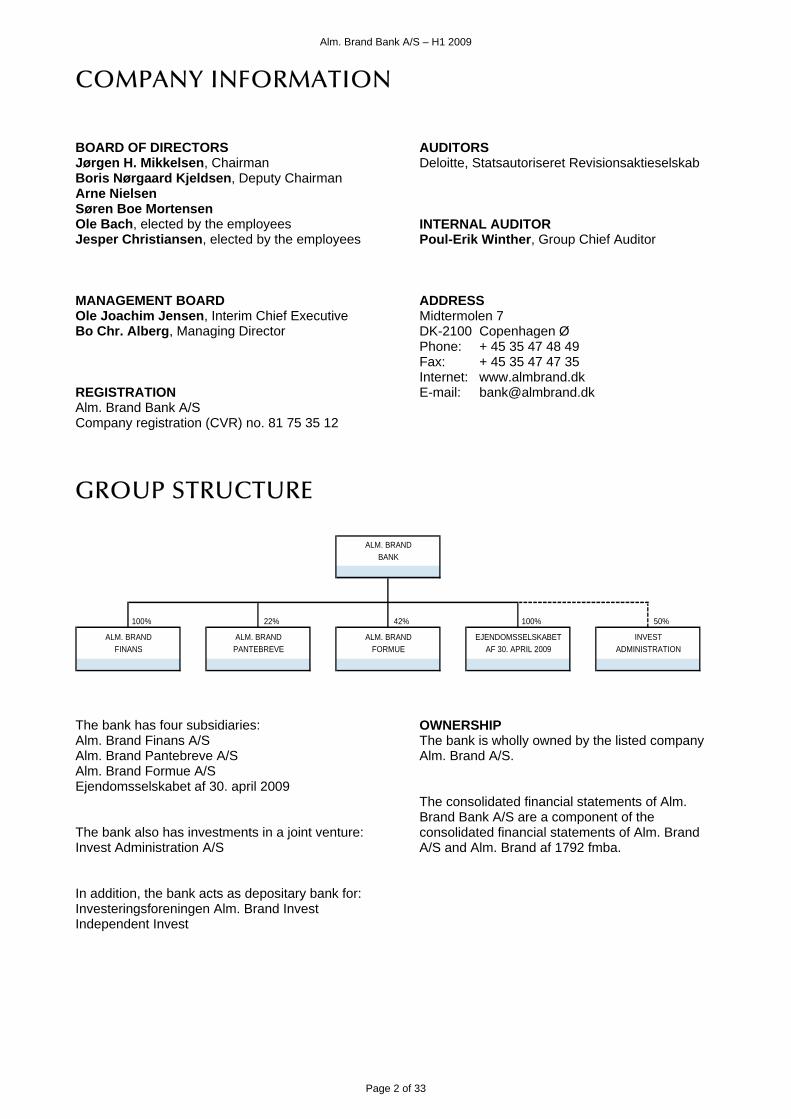

GROUP STRUCTURE

100% 22% 42% 100% 50%

INVESTFORMUE AF 30. APRIL 2009 ADMINISTRATION

ALM. BRANDFINANS

ALM. BRANDPANTEBREVE

ALM. BRANDBANK

ALM. BRAND EJENDOMSSELSKABET

The bank has four subsidiaries: Alm. Brand Finans A/S Alm. Brand Pantebreve A/S Alm. Brand Formue A/S Ejendomsselskabet af 30. april 2009 The bank also has investments in a joint venture: Invest Administration A/S In addition, the bank acts as depositary bank for: Investeringsforeningen Alm. Brand Invest Independent Invest

OWNERSHIP The bank is wholly owned by the listed company Alm. Brand A/S. The consolidated financial statements of Alm. Brand Bank A/S are a component of the consolidated financial statements of Alm. Brand A/S and Alm. Brand af 1792 fmba.

Alm. Brand Bank A/S – H1 2009

Page 3 of 33

FINANCIAL HIGHLIGHTS AND KEY RATIOS

DKKmQ2

2009Q2

2008H1

2009H1

2008Year2008

Q22009

Q22008

H12009

H12008

Year2008

INCOME STATEMENT

Interest receivable 275 395 596 745 1,498 284 406 613 762 1,523

Interest payable 161 274 377 533 1,066 163 281 383 538 1,077

Net interest income 114 121 219 212 432 121 125 230 224 446

Net fee and commission income and dividends etc. 39 54 80 111 197 38 54 78 112 195

Net interest and fee income 153 175 299 323 629 159 179 308 336 641Value adjustments -19 -143 -2 -153 -290 -9 -216 -2 -284 -535

Other operating income 7 4 10 8 14 8 4 11 8 14

Profit on ordinary activities before expenses 141 36 307 178 353 158 -33 317 60 120Operating expenses and depreciation 130 146 263 278 525 134 149 269 282 532

Other operating expenses 21 0 38 0 24 20 0 38 0 25

Write-downs of loans, advances and receivables etc. 938 13 1,003 4 340 938 13 1,003 4 340

Profit/loss on participating interests 0 5 0 6 4 0 5 0 6 4

Profit on activities before tax -948 -118 -997 -98 -532 -934 -190 -993 -220 -773Tax -228 -31 -247 -20 -104 -228 -49 -247 -41 -127

Profit for the period -720 -87 -750 -78 -428 -706 -141 -746 -179 -646Profit attributable to minority interests - - - - - 14 -54 4 -101 -218

Profit after tax exclusive minorities - - - - - -720 -87 -750 -78 -428

Profit before tax exclusive minorities - - - - - -948 -118 -997 -98 -532

BALANCE SHEET

Loans and advances 15,689 18,114 15,689 18,114 17,209 15,768 17,608 15,768 17,608 17,292

Deposits 12,392 11,791 12,392 11,791 11,143 12,391 11,791 12,391 11,791 11,141

Shareholders' equity 487 1,287 487 1,287 937 789 1,717 789 1,717 1,237

Of which attributable to minority interests - - - - - 303 431 303 431 300

Total assets 26,057 25,291 26,057 25,291 24,228 26,543 25,900 26,543 25,900 24,708KEY RATIOS ETC.

Average number of employees, full-time equivalents 361 384 365 382 380 362 385 366 383 381

Net interest margin p.a. - - - - - 1.9% 2.0% 1.9% 1.8% 1.8%

Income/cost ratio 0.13 0.26 0.24 0.65 0.40 0.14 -0.17 0.24 0.23 0.14

Impairment ratio 4.9% 0.1% 5.3% 0.0% 1.8% 4.9% 0.1% 5.2% 0.0% 1.7%

Solvency ratio - - - - - 6.9% 11.3% 6.9% 11.3% 12.6%

Return on equity before tax p.a. - -35.7% - -14.8% -45.4% - -35.7% - -14.8% -45.4%

Return on equity after tax p.a. - -26.2% - -11.8% -37.2% - -26.2% - -11.8% -37.2%

Return in excess of the money market rate - -40.9% - -19.8% -50.8% - -40.9% - -19.8% -50.8%

PRO RATA GROUP

Financial highlights and key ratios have been prepared in accordance with IFRS.

Alm. Brand Bank A/S – H1 2009

Page 4 of 33

REPORT

Financial review The bank posted a profit before writedowns and losses of DKK 66 million, thereby exceeding the forecast of an overall full-year profit for the bank of DKK 50 million before losses and writedowns. However, when including losses and writedowns, the bank incurred a highly unsatisfactory loss of DKK 997 million. In the same period of last year, the bank recorded a loss of DKK 98 million. The highly unsatisfactory performance was primarily driven by credit losses and writedowns. Total writedowns amounted to DKK 1,063 million in H1 2009, of which DKK 984 million was written down in the second quarter. The substantial writedowns in the second quarter are the result of the bank’s assessment that the market outlook within investment and development properties has become significantly more negative over the past few months. Return requirements for property investments are thus increasing while rental income is being squeezed. Moreover, it is becoming increasingly difficult to fund the necessary development and completion of ongoing projects. Net interest and fee income Net interest and fee income was DKK 299 million, against DKK 323 million in H1 2008. Interest income The bank recorded net interest income of DKK 219 million in H1 2009, which was on a par with the year-earlier period. In Q2 2009, net interest income amounted to DKK 114 million, equivalent to an increase of DKK 9 million relative to Q1 2009. Accordingly, the bank’s net interest income for the year to date was on a par with the first half year of 2008, despite a lower lending level. The bank has regularly adjusted the customer interest margin, which has been raised on several occasions since the second half of 2008. Nevertheless, the bank’s total interest margin was not increased correspondingly. There are a number of reasons for this: The most important reason was the fall in 3M CIBOR, which on a daily basis adjusts part of the bank’s loans and advances. The rate of interest on external funding, on the other hand, is fixed for three

months at a time, and declining interest rates therefore have a negative impact on the bank’s net interest income. Interest increases have the opposite effect. Secondly, the bank increased the excess cover during the reporting period, which, when seen in isolation, weakened the net interest margin. In the third quarter, a small part of the bank’s external funding will be settled, thereby correspondingly reducing the excess cover as planned. The banking group’s interest margin rose from 1.8% in H1 2008 to 1.9% in the same period of 2009. Fee income Fee income for H1 2009 amounted to DKK 80 million, against DKK 111 million for the same period of last year. The decline in fee income was mainly attributable to a fall in the volume of loans and advances. Value adjustments Value adjustments in H1 2009 amounted to a loss of DKK 2 million, against a loss of DKK 153 million in H1 2008. Mortgage deeds Value adjustments in H1 2009 were adversely affected by credit-related value adjustments of mortgage deeds in the amount of DKK 60 million. Other value adjustments on mortgage deeds totalled a loss of DKK 24 million, thereby bringing overall value adjustments on mortgage deeds to a loss of DKK 84 million. Other value adjustments Interest-related value adjustments, notably government and mortgage bonds, generated a profit of DKK 31 million in H1 2009. Of this amount, an unrealised capital gain of around DKK 26 million was attributable to a portfolio of short-term bonds maturing on 1 January 2010. Benchmarking the bank’s interest-driven value adjustments against the general trend in mortgage bonds, the bank’s portfolios outperformed the market by a significant margin. Equity-related value adjustments totalled a profit of DKK 21 million in H1 2009, against a loss of DKK 6 million in the year-earlier period.

In order to increase the transparency of Alm. Brand Bank’s financial statements, the bank publishes pro rata consolidated figures. The numbers are set out in the financial highlights and key ratios and, unless otherwise indicated, the comments provided in the financial review below are for pro-rata numbers. Banking group figures are commented on only when found relevant. To the extent it is deemed relevant, the first half year of 2008 and the first quarter of 2009, respectively, are used as benchmarks for the first half year of 2009 and the second quarter of 2009, respectively.

Alm. Brand Bank A/S – H1 2009

Page 5 af 33

REPORT Overall, value adjustments of the bank’s portfolios were satisfactory with the exception of the mortgage deed portfolio. Expenses Costs for H1 2009 amounted to DKK 263 million, against DKK 278 million for the same period of last year. Accordingly, the cost level was not higher in spite of collectively agreed salary increases in the banking industry. This was due to a number of cost-saving measures implemented in 2008 and 2009. Stability package (the First Bank Package) and the Private Contingency Association The bank’s overall costs relating to the First Bank Package and the Private Contingency Association were DKK 40 million in H1 2009. Total costs in the amount of DKK 36 million were recognised under other operating expenses and DKK 4 million under writedowns on loans, advances and receivables etc. Costs are expected to total around DKK 80 million for the full year 2009. However, this figure could increase significantly if more banks become distressed. Credit package (the Second Bank Package) The bank has applied for injection of almost DKK 900 million in the form of hybrid capital under the credit package. Income/cost ratio The income/cost ratio was 0.24 in H1, against 0.65 in the first half year of 2008. Impairment of loans, etc. In the first six months of 2009, the bank took substantial writedowns on loans, advances and other receivables etc. equivalent to DKK 1,003 million, against DKK 4 million in H1 2008. Writedowns amounted to DKK 938 million in Q2 2009, against DKK 65 million in Q1 2009. In addition, the bank’s mortgage deed portfolio recorded credit-related value adjustments and losses in the amount of DKK 46 million in Q2 2009, as compared with DKK 14 million in Q1 2009. These credit losses were recognised under value adjustments. Of the total writedowns of DKK 1,063 million in H1 2009, DKK 55 million was recognised as lost. Of this amount DKK 18 million had previously been written down. Accordingly, DKK 1,026 million was written down in provision for future losses.

The bank’s accumulated writedowns were increased from 2.2% of the bank’s loans, advances and guarantees at 31 December 2008 to 7.5% at 30 June 2009. The bank’s lending portfolio and losses and writedowns are reviewed below. Balance sheet Loans and advances The bank’s loans and advances amounted to DKK 15.7 billion at 30 June 2009, which was DKK 1.5 billion lower than at 31 December 2008. Loans and advances were DKK 2.4 billion lower relative to 30 June 2008. However, DKK 1.4 billion of this amount was attributable to writedowns on loans and advances. In 2008, the bank refocused on lowering its credit exposure in particularly cyclical areas with a view to reducing its exposure to a further deterioration of economic conditions. The bank expects to continue to reduce its total loans and advances throughout 2009. The bank pursues a policy of lowering the volume of loans and advances for security financing, commercial and rental property and property development. Among other things, the bank has decided not to include funding of large investment and project properties and certain forms of security financing in its future business strategy. Moreover, the bank no longer has any activities in the market for commercial property mortgage deeds. On the other hand, the bank expects to increase loans and advances in the Alm. Brand Group’s key areas of focus, i.e. the private customer segment, small and medium-sized businesses and agricultural customers. The agricultural segment will grow as economic conditions in this industry improve. Overall, the portfolio of loans and advances is expected to decline in the years ahead. Deposits The bank’s deposits totalled DKK 12.4 billion at 30 June 2009, against DKK 11.8 billion at the year-earlier date. Debt to credit institutions The bank’s debt to credit institutions amounted to DKK 9.1 billion at 30 June 2009, which was on a par with 30 June 2008.

Alm. Brand Bank A/S – H1 2009

Page 6 of 33

REPORT Capital The banking group’s equity stood at DKK 0.8 billion at 30 June 2009, whereas the capital base totalled DKK 1.2 billion. An amount of DKK 300 million was converted from subordinated loan capital into share capital in the second quarter of 2009. No costs were incurred in connection with the transaction. Risk-weighted items in the banking group totalled DKK 16.9 billion at 30 June 2009. The solvency ratio was thus 6.9, and the tier 1 capital ratio was 3.5. Capital injection from Alm. Brand A/S The Board of Directors of Alm. Brand A/S has resolved to inject share capital in the amount of DKK 900 million into Alm. Brand Bank A/S with a view to restoring the bank’s capital base. The capital will be injected following a resolution to complete a capital increase at an extraordinary general meeting to be held in Alm. Brand Bank on 7 September 2009. The meeting will be convened on 27 August 2009. After receipt of the capital injection, the Alm. Brand Bank Group will have a solvency ratio of 13.2 and a tier 1 capital ratio of 8.8. In addition, Alm. Brand Bank expects to receive an injection of hybrid capital under the Second Bank Package of almost DKK 900 million. Major events Strengthened organisation in relation to property commitments The economic downturn has contributed to placing the property market under substantial pressure. Traditionally, Alm. Brand Bank has secured its lending commitments through a mortgage against the debtor’s assets, typically real property. As a result of the change in economic trends and the resulting plunge in real property prices, the value of such mortgages may have declined. Accordingly, the handling of property-related commitments is even more important and more resource-intensive than was previously the case. As a result, we have generally strengthened our credit department by taking on more employees.

Winding-up of business areas The bank has decided not to include funding of large investment and project properties and certain forms of security financing in its future business strategy. In this connection, the bank has consolidated the handling of these activities into a single unit under the management of the credit secretariat. These commitments and the bank’s portfolio of commercial mortgage deeds have thus been moved to a winding-up unit. The strategy for the unit is to handle the individual commitments so as to inflict as few losses as possible on the group and to sell or wind up the assets in the best possible manner. The winding-up unit is staffed by employees who possess specific knowledge within funding and handling and managing these types of assets, including the handling, development, management and sale of property. Establishment of Ejendomsselskabet af 30. april 2009 A/S The bank has established Ejendomsselskabet af 30. april 2009 A/S, which is a wholly-owned subsidiary. The company was established with the object of owning and managing a property taken over in connection with a non-performing commitment. The property taken over is called Mønten and is located at Amagerbrogade in Copenhagen. After completion of the project, the plan is to lease or sell the individual flats or the entire complex as a whole. New Senior Vice President of Alm. Brand Markets The bank has appointed Martin Rasmussen new Senior Vice President of Alm. Brand Markets. Martin Rasmussen comes from a position as Deputy Chief Executive of HSH Nordbank. New management It has been agreed with Henrik Nordam that he is retiring from his position as Chief Executive in the bank. Chief Financial Officer, Ole Joachim Jensen, has been appointed as new Interim Chief Executive in Alm. Brand Bank. The management of Alm. Brand Bank will consequently consist of Ole Joachim Jensen and Bo Christian Alberg.

Alm. Brand Bank A/S – H1 2009

Page 7 of 33

REPORT Outlook The bank retains its forecast of a full-year profit of around DKK 50 million before tax and impairment writedowns. The bank revalued a number of commitments in connection with the significant writedowns taken during the quarter. This served to align the value of the commitments to the adverse market conditions with massive value reductions in the property market in particular.

The bank thus expects its writedowns to be more consistent with market standards in the future. Nevertheless, the highly volatile economic setting entails a high degree of uncertainty with respect to the amount of future writedowns, and the bank’s financial guidance is therefore provided excluding impairment writedowns.

Disclaimer The forecasts are based on the level of interest rates prevailing at mid-August 2009. All forward-looking statements are based exclusively on the information available when this interim report was released. The actual performance of the group overall and of the individual business areas may be affected by major changes in a number of factors. Such impacts include changes in conditions in the financial market, legislative changes, changes in the competitive environment, loans and advances, etc. and guarantees, etc. The above-mentioned risk factors are not exhaustive. Investors and others who base their decisions on the information contained in this report should independently consider any uncertainties of significance to their decision. This interim report has been translated from Danish into English. In the event of any discrepancy between the Danish text and the English-language translation, the Danish text shall prevail.

Alm. Brand Bank A/S – H1 2009

Page 8 of 33

LENDING PORTFOLIO, CREDIT LOSSES AND WRITEDOWNS The bank’s total writedowns and losses on the lending and guarantee portfolio amounted to an expense of DKK 1,063 million in H1 2009. Of this amount, credit losses and writedowns on mortgage deeds accounted for DKK 60 million recognised under value adjustments. In H1 2008, writedowns and losses charged to the income statement represented a total loss of DKK 36 million. Of the total writedowns of DKK 1,063 million in H1 2009, DKK 55 million was recognised as lost. Of

this amount DKK 18 million had previously been written down. Accordingly, DKK 1,026 million was written down in provision for future losses. Losses and writedowns totalled DKK 984 million in Q2 2009, against DKK 79 million in Q1 2009. Total losses and writedowns represented 6.5% of the average portfolio of loans and advances in the first half year.

ProrataH1 2009

Loans Total loss and writedown

DKKm 31.12.2008 30.06.2009 H1 2008 H1 2009

SegmentsRetail lending 3,524 3,316 21.1% 6 14 0.4%Car finance 1,276 1,149 7.3% -9 17 1.4%Agriculture 1,081 1,110 7.1% -8 63 5.8%Other commercial lending 1,234 1,278 8.1% 4 23 1.8%Security financing 4,570 4,197 26.8% 1 204 4.6%Lending to Alm. Brand Formue and Alm. Brand Pantebreve 1,287 1,213 7.7% 0 0 0.0%Investment property 2,291 1,700 10.8% -2 382 19.1%Residential mortgage deeds 1,028 958 6.1% 6 24 2.4%Commercial mortgage deeds 309 377 2.4% 26 36 10.6%Property developments projects 609 391 2.5% 12 296 59.2%The Danish Contingency Committee - - - 0 4 -Total 17,209 15,689 100% 36 1,063 6.5%

The items Value adjustments, Writedowns of loans, advances and recievables, etc in the Income Statement includes total loss and writedown.*) Losses and writedowns as a percentage of the average portfolio in H1 2009. The percentage is not comparable with the impairmentratio in the bank's financial highlights and key ratios.

Share of portefolio

(%)Loss ratio H1 2009 *)

The table shows a segment-by-segment breakdown of the bank’s lending portfolio. The statement is made on a pro rata consolidated basis. The performance of the individual lending segments is discussed in the following sections. Retail lending Retail lending includes lending to the bank’s private customers. The portfolio has almost 17,000 private customers and is well diversified geographically across Denmark. Slightly more than three quarters of the portfolio is made up of loans secured against real property.

Half of these properties have a loan-to-value ratio of less than 80% of the most recently assessed public property value and, overall, three quarters of loans and advances are within the most recently assessed public property value. During the reporting period, the bank experienced a small run-off of the lending portfolio. This run-off was primarily attributable to conversions of existing home credits into mortgage loans. Moreover, a not insignificant part of the new loans raised by customers were facilitated through the group’s mortgage credit business partner. The bank aims to increase the volume of loans and

Alm. Brand Bank A/S – H1 2009

Page 9 of 33

LENDING PORTFOLIO, CREDIT LOSSES AND WRITEDOWNS advances to private customers and to facilitate a certain part of the home loans through its business partner. The bank achieved growth at the rate of 4% p.a. in number of accounts, while the mortgage credit portfolio rose by around DKK 700 million in H1 2009.The bank recorded a small increase in delinquencies but is generally experiencing good payment ability among its private customers. The impairment ratio was 0.4 in the first half of 2009. Car finance The car finance portfolio is managed by Alm. Brand Finans A/S, which offers car financing through car dealers. Due to a substantial decline in business activity in the car market, the bank recorded a falling trend in new loans during the reporting period. In addition, an increasing customer interest margin and tighter acceptance requirements deliberately reduced the company’s competitive strength in a highly price sensitive market. The number of customers in arrears has been slightly increasing but showed a falling trend at the end of H1 2009. The decline reflects the fact that a number of critical commitments are in the process of being wound up, while the financial strength of the remaining part of the portfolio is unchanged. The impairment ratio was 1.4 in H1 2009. The writedowns were attributable to the winding up of defaulting agreements combined with a significant fall in used car prices. Agriculture The bank has built up its agricultural portfolio over the past seven years using the substantial market position and industry know-how available to the Alm. Brand Group in the agricultural sector. The bank pursues a selective credit policy and only approves loans to farms with good efficiency ratios. The bank regularly conducts stress tests on the portfolio. This is done to identify any customer relationships requiring special attention. The commitments thus identified are closely monitored. During the period, the bank wrote down 5.8% of the portfolio. The writedowns were attributable partly to higher construction costs on property

investments and partly to a reduced earnings capacity. Other commercial lending The bank is currently building its commercial lending portfolio, having been an active player in this market for only a few years. The portfolio consists of loans to small businesses typically anchored in Alm. Brand Bank’s branches and large syndicated loans to medium-sized Danish businesses. In addition, the portfolio consists of car and equipment leases established with Alm. Brand Finans. The bank recorded an impairment ratio of 1.8 in H1 2009. The writedowns primarily included lease commitments. Security financing This portfolio consists of investment commitments secured against mortgage deeds as well as shares and bonds. Mortgage deed facilities account for almost 90% of this portfolio, and commercial mortgage deeds total around 30% of the mortgage deeds. All mortgage deeds in arrears are measured individually, and mortgaged shares listed on recognised stock exchanges are measured at their fair value. Both the bank’s own mortgage deeds and mortgage deeds against which loans are secured saw stable delinquency rates in the first half of 2009. In light of the economic crisis, the bank has chosen to write down a number of investment commitments whose excess cover was not up to the bank’s usual level. This led to substantial impairment writedowns of DKK 204 million, equivalent to an impairment ratio of 4.6. The bank has decided not to include certain forms of security financing in its future strategy. Lending to Alm. Brand Formue A/S and Alm. Brand Pantebreve A/S These loans are granted to the bank’s two partly-owned listed subsidiaries. The loans reflect the share of the bank’s lending attributable to minority interests. At 30 June 2009, minority interests had 58% ownership of Alm. Brand Formue and 78% ownership of Alm. Brand Pantebreve. Alm. Brand Pantebreve A/S was affected by the negative developments in the property market, whereas

Alm. Brand Bank A/S – H1 2009

Page 10 of 33

LENDING PORTFOLIO, CREDIT LOSSES AND WRITEDOWNS Alm. Brand Formue A/S recorded a highly satisfactory performance in the first six months of 2009. No losses were incurred in this segment. Investment properties The portfolio consists of loans for prime-location investment properties with reliable tenants, primarily within retail trade and rental housing. Danish properties make up some 75% of the portfolio, while the remaining 25% is made up of German properties with Danish debtors. During the period, the bank wrote down DKK 382 million on the portfolio, corresponding to an impairment ratio of 19.1%. The writedowns were attributable to a stagnant property market with significantly reduced commercial property prices. The bank therefore found it necessary to take very substantial writedowns on a number of commitments. The writedowns included both Danish and German properties. No losses were incurred on the bank’s loans for investment properties during the period. The bank has decided not to include investment property funding in its future strategy. Residential mortgage deeds This segment represents the bank’s portfolio of marketable mortgage deeds secured against single-family houses, freehold flats and summer houses. The bank has tightened its acceptance rules and increased the interest margin. The portfolio covers some 3,200 residential mortgage deeds and is marked to market on a current basis using a cash flow-based pricing model, which considers factors such as estimated early redemptions and credit losses. Individual writedowns are taken on all mortgages in arrears or showing well-known signs of weakness. Around 70% of the mortgage deeds have an outstanding debt of less than DKK 400,000. Loans secured against single-family houses, terraced houses or rural zone houses make up almost three quarters of the portfolio, while loans for free-hold flats and summer houses total 16% and 12%, respectively. Writedowns and credit losses totalled 2.4% of the portfolio. The losses were primarily attributable to declining debtor payment ability as a result of unemployment and the more difficult credit

situation facing the mortgage deed customers’ current banks. Commercial mortgage deeds This portfolio is being wound up, as the bank will not in future be participating in the market for large commercial mortgage deeds. A total of 60% of the portfolio consists of mortgage deeds secured against residential rental property, while the remaining part is mainly comprised of genuine commercial properties for office, trade and industrial use. The impairment ratio was 10.6. As part of the winding up of a large, non-performing security financing facility, the bank took over a number of commercial mortgage deeds at a substantially impaired value in the first quarter of 2009. In the case at hand, the bank assessed that the best way of securing the bank’s and the customer’s values would be to carry out the winding up process itself. The writedowns from this commitment were largely recognised under security financing. Property development projects The portfolio consists of a limited number of projects that will not be initiated until a significant part of the overall project has been sold. As a result of the economic downturn in the market for property projects, the bank will not participate in the financing of new property projects but will finance the completion of ongoing projects pursuant to agreements already made. Against this backdrop, the bank expects an increase in loans and advances in this area in 2009 and 2010, after which the volume of loans and advances in the area is expected to be reduced and wound up. During the first half year, the bank wrote down DKK 296 million, of which DKK 273 million was written down in the second quarter. This corresponds to an impairment ratio of 59.2 of the average lending portfolio. The revised – and individual – valuation of the properties is based on the discounted value of the cash flow which the properties are expected to be able to generate and on a valuation made by an estate agent.

Alm. Brand Bank A/S – H1 2009

Page 11 of 33

LENDING PORTFOLIO, CREDIT LOSSES AND WRITEDOWNS The bank made substantial writedowns on several large commitments. The writedowns were attributable to the general and substantial fall in real property values. Of the total amount of writedowns in H1 2009 of DKK 296 million, DKK 221 million was attributable to one single commitment in which the bank has taken over the mortgaged property due to poor project management and other factors. The bank will complete the construction of the property in order to ensure that it can be brought into use shortly. The property has been transferred to a property company established by the bank.

The bank has decided not to include property development projects in its future strategy. The Private Contingency Association In the first quarter of 2009, the bank reversed impairment writedowns relating to 2008, as the bank’s share of the costs have been lowered retroactively. In the second quarter of 2009, an amount of DKK 6 million was provided for losses on the guarantee provided.

Alm. Brand Bank A/S – H1 2009

Page 12 of 33

STATEMENT BY THE BOARD OF DIRECTORS AND THE MANAGEMENT BOARD The Board of Directors and the Management Board have today reviewed and adopted the interim report for the six months ended 30 June 2009 of Alm. Brand Bank A/S. The consolidated financial statements have been prepared in accordance with IAS 34, Interim Financial Reporting as adopted by the EU, and the interim financial statements of the parent company have been prepared in accordance with the Danish Financial Business Act and Danish accounting standards. In addition, the interim report has been presented in accordance with additional Danish disclosure requirements for listed financial enterprises.

In our opinion, the accounting policies applied are appropriate, and the interim report gives a true and fair view of the group's and the parent company's assets, liabilities and financial position at 30 June 2009 and of the results of the group's and the parent company's operations and the cash flow of the group for the financial period ended 30 June 2009. The management's review also gives a true and fair view of developments in the activities and financial position of the group.

MANAGEMENT BOARD Copenhagen, 27 August 2009 Ole Joachim Jensen Bo Chr. Alberg Interim Chief Executive Managing Director BOARD OF DIRECTORS Copenhagen, 27 August 2009 Jørgen H. Mikkelsen Boris Nørgaard Kjeldsen Chairman Deputy Chairman Arne Nielsen Søren Boe Mortensen Ole Bach Jesper Christiansen

Alm. Brand Bank A/S – H1 2009

Page 13 of 33

ACCOUNTING POLICIES GROUP The interim report has been prepared in accordance with IAS 34, Interim Financial Reporting as approved by the EU. The parent company financial statements have been prepared in accordance with the provisions of the Danish Financial Business Act, including the Executive Order on financial reports presented by credit institutions and investment companies and Danish accounting standards. In addition, the interim report has been prepared in accordance with additional Danish disclosure requirements for listed financial companies.

The accounting policies applied for the consolidated financial statements are unchanged from the policies applied for the Annual Report 2008, except that: The presentation has been adapted to reflect the amendments to IAS 1, Presentation of Financial Statements, implying presentation of comprehen-sive income in the income statement. The interim report for the first six months of 2009 is unaudited.

Alm. Brand Bank A/S – H1 2009

Page 14 of 33

INCOME STATEMENT

Group

DKK '000 Note

H1

2009

H1

2008

Year2008

Interest receivable 1 612,868 761,944 1,523,152

Interest payable 2 382,799 538,302 1,076,876

Net interest income 230,069 223,642 446,276Dividend on participating interests 6,285 12,619 14,296

Fees and commissions receivable 90,834 118,498 221,743

Fees and commissions payable 19,000 19,034 41,607

Net interest and fee income 308,188 335,725 640,708Value adjustments 3 -1,766 -283,609 -534,754

Other operating income 10,367 8,236 14,470

Profit before expenses 316,789 60,352 120,424Staff costs and administrative expenses 4 263,286 281,256 530,042

Depreciation, amortisation and impairment of intangible assets and property, plant and equipment 5,170 1,097 2,455

Other ordinary expenses 37,960 - 24,961

Impairment of loans, advances and receivables, etc. 5 1,002,614 3,823 339,918

Profit from participating interests in associated and group undertakings -295 5,838 3,684

Profit before tax -992,536 -219,986 -773,268Tax -246,254 -41,409 -126,946

Profit for the period -746,282 -178,577 -646,322

Comprehensive income - - -

Total comprehensive income for the period -746,282 -178,577 -646,322

The profit for the period will be allocated as follows:Share attributable to Alm. Brand Bank -750,058 -78,086 -427,931

Share attributable to minority interests 3,776 -100,491 -218,391

Total -746,282 -178,577 -646,322

Alm. Brand Bank A/S – H1 2009

Page 15 of 33

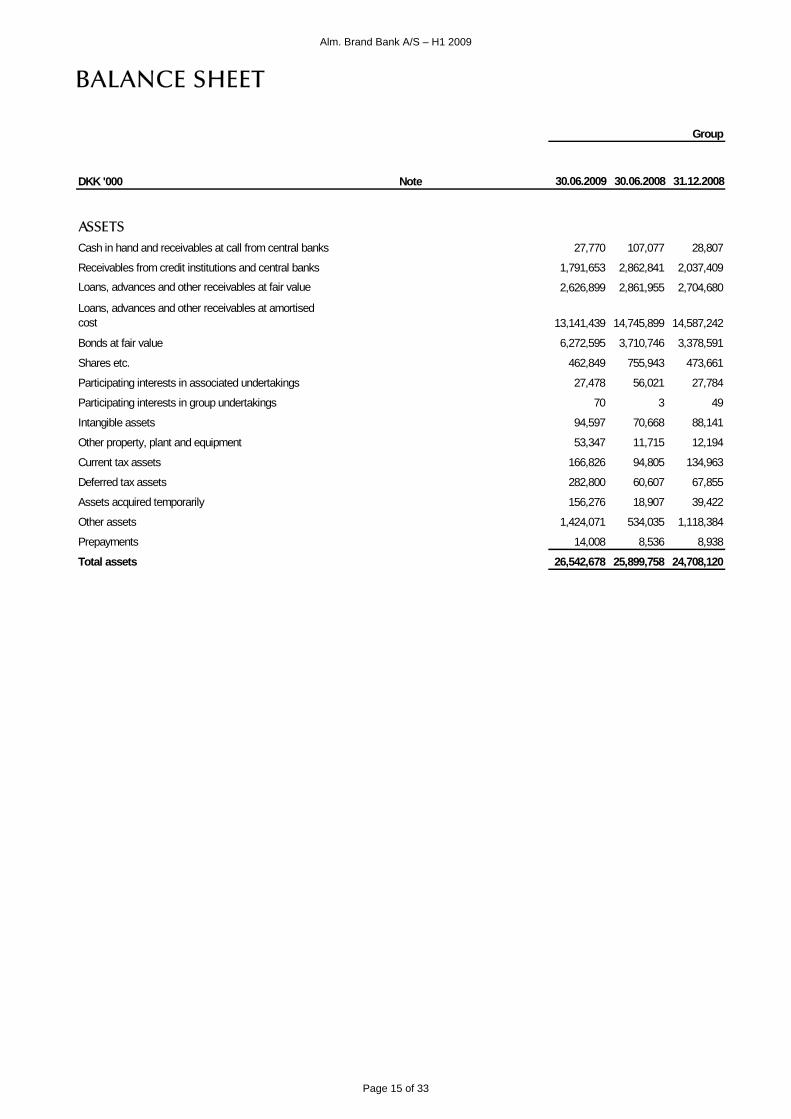

BALANCE SHEET

Group

DKK '000 Note 30.06.2009 30.06.2008 31.12.2008

ASSETSCash in hand and receivables at call from central banks 27,770 107,077 28,807

Receivables from credit institutions and central banks 1,791,653 2,862,841 2,037,409

Loans, advances and other receivables at fair value 2,626,899 2,861,955 2,704,680

Loans, advances and other receivables at amortised cost 13,141,439 14,745,899 14,587,242

Bonds at fair value 6,272,595 3,710,746 3,378,591

Shares etc. 462,849 755,943 473,661

Participating interests in associated undertakings 27,478 56,021 27,784

Participating interests in group undertakings 70 3 49

Intangible assets 94,597 70,668 88,141

Other property, plant and equipment 53,347 11,715 12,194

Current tax assets 166,826 94,805 134,963

Deferred tax assets 282,800 60,607 67,855

Assets acquired temporarily 156,276 18,907 39,422

Other assets 1,424,071 534,035 1,118,384

Prepayments 14,008 8,536 8,938

Total assets 26,542,678 25,899,758 24,708,120

Alm. Brand Bank A/S – H1 2009

Page 16 of 33

BALANCE SHEET

Group

DKK '000 Note 30.06.2009 30.06.2008 31.12.2008

LI ABI LI TI ES AND EQUI TYPayablesPayables to credit institutions and central banks 9,297,821 9,148,361 8,585,758

Deposits and other payables 12,390,923 11,790,918 11,141,332

Issued bonds 1,239,517 1,396,180 1,135,483

Current tax liabilities 125,919 2,460 6,027

Other liabilities 1,640,649 1,156,429 1,327,941

Deferred income 3,430 18,815 27,620

Total payables 24,698,259 23,513,163 22,224,161

ProvisionsProvisions for pensions and similar liabilities 4,111 5,736 4,111

Provisions for losses on guarantees 120,392 - 13,975

Total provisions 124,503 5,736 18,086

Subordinated debt 6

Supplementary capital 750,000 500,000 1,050,000

Hybrid tier 1 capital 180,678 163,442 179,305

Total subordinated debt 930,678 663,442 1,229,305

Shareholders' equityShare capital 651,000 351,000 351,000Retained earnings -164,332 935,571 585,726Minority interests 302,570 430,846 299,842

Total shareholders' equity 789,238 1,717,417 1,236,568

Total liabilities and equity 26,542,678 25,899,758 24,708,120

Alm. Brand Bank A/S – H1 2009

Page 17 of 33

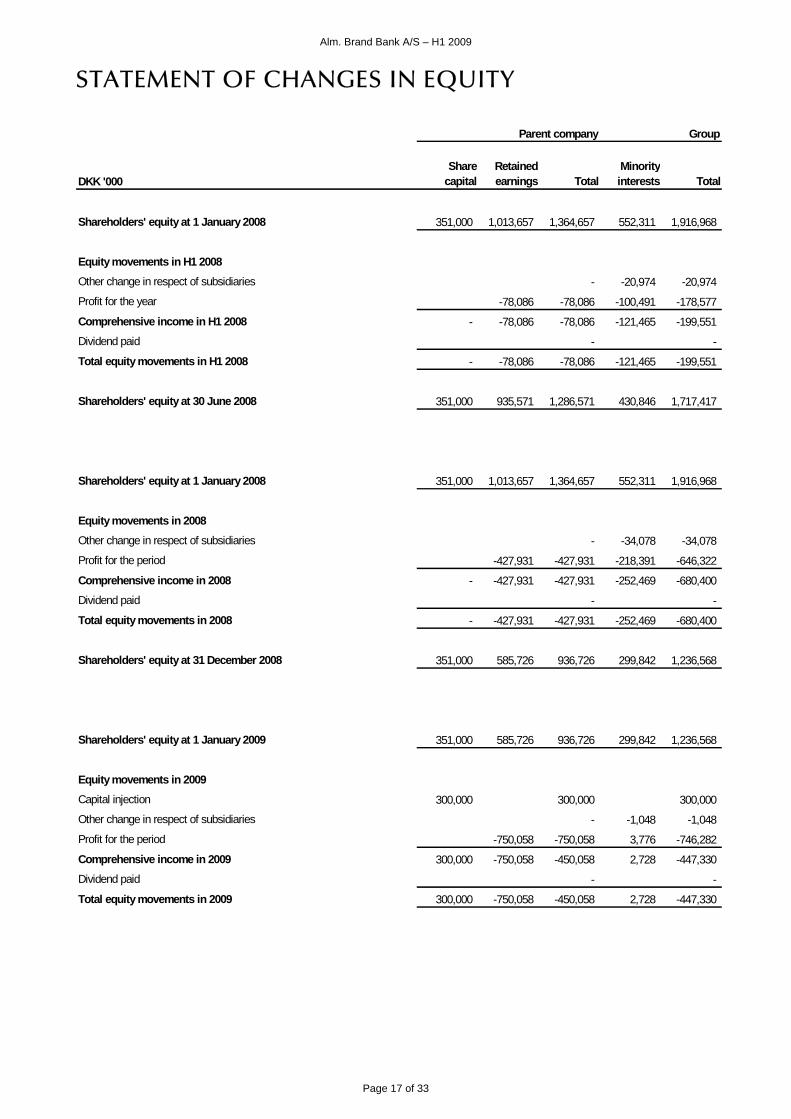

STATEMENT OF CHANGES IN EQUITY

Parent company Group

DKK '000Share

capitalRetained earnings Total

Minority interests Total

Shareholders' equity at 1 January 2008 351,000 1,013,657 1,364,657 552,311 1,916,968

Equity movements in H1 2008Other change in respect of subsidiaries - -20,974 -20,974

Profit for the year -78,086 -78,086 -100,491 -178,577

Comprehensive income in H1 2008 - -78,086 -78,086 -121,465 -199,551

Dividend paid - -

Total equity movements in H1 2008 - -78,086 -78,086 -121,465 -199,551

Shareholders' equity at 30 June 2008 351,000 935,571 1,286,571 430,846 1,717,417

Shareholders' equity at 1 January 2008 351,000 1,013,657 1,364,657 552,311 1,916,968

Equity movements in 2008Other change in respect of subsidiaries - -34,078 -34,078

Profit for the period -427,931 -427,931 -218,391 -646,322

Comprehensive income in 2008 - -427,931 -427,931 -252,469 -680,400

Dividend paid - -

Total equity movements in 2008 - -427,931 -427,931 -252,469 -680,400

Shareholders' equity at 31 December 2008 351,000 585,726 936,726 299,842 1,236,568

Shareholders' equity at 1 January 2009 351,000 585,726 936,726 299,842 1,236,568

Equity movements in 2009Capital injection 300,000 300,000 300,000

Other change in respect of subsidiaries - -1,048 -1,048

Profit for the period -750,058 -750,058 3,776 -746,282

Comprehensive income in 2009 300,000 -750,058 -450,058 2,728 -447,330

Dividend paid - -

Total equity movements in 2009 300,000 -750,058 -450,058 2,728 -447,330

Alm. Brand Bank A/S – H1 2009

Page 18 of 33

CASH FLOW STATEMENT

Group

DKK '000

H1

2009

H1

2008Year2008

Operating activitiesProfit for the period before tax -992,537 -219,986 -773,268

Tax paid during the period -494 - 36,449

Adjustment for amounts with no cash flow impact:

Other adjustments to cash flows from operating activities 998,386 219,920 722,837

Total, operating activities 5,355 -66 -13,982

Working capitalLoans and advances, etc. 551,412 -540,009 -620,478

Deposits 1,249,590 32,751 -615,735

Bonds -2,767,964 1,103,896 797,705

Shares 56,842 -35,672 106,531

Total, working capital -910,120 560,966 -331,977

Investing activitiesInvestments in associates - -25,412 1,151

Investments in group enterprises -1,005 6,313 5,786

Intangible assets -6,455 -8,095 -25,569

Property, plant and equipment -46,322 -3,647 -5,483

Total, investing activities -53,782 -30,841 -24,115

Financing activitiesPayables to credit institutions 711,754 286,193 -266,276

Hybrid tier 1 capital - - 548,900

Total, financing activities 711,754 286,193 282,624

Change in cash and cash equivalents -246,793 816,252 -87,450

Cash and cash equivalents, beginning of period 2,066,216 2,153,666 2,153,666

Change in cash and cash equivalents -246,793 816,252 -87,450

Cash and cash equivalents, end of period 1,819,423 2,969,918 2,066,216

Cash and cash equivalents, end of periodCash and balances due from central banks 27,770 107,077 28,807

Balances due from credit institutions less than 3 months 1,791,653 2,862,841 2,037,409

Cash and cash equivalents, end of period 1,819,423 2,969,918 2,066,216

Alm. Brand Bank A/S – H1 2009

Page 19 of 33

NOTES TO THE FINANCIAL STATEMENTS

Group

DKK '000H1

2009H1

2008Year2008

NOTE 1 Interest receivableReceivables from credit institutions and central banks 24,973 31,194 74,436

Loans, advances and other receivables 516,840 589,805 1,218,863

Bonds 98,657 112,667 189,935

Total derivatives -32,133 28,278 39,897

Of which:

Currency contracts 26,305 25,919 52,067

Interest rate contracts -58,438 2,359 -12,170

Other interest receivable 4,531 0 21

Total interest receivable 612,868 761,944 1,523,152

Interest receivable from genuine purchase and resale transactions:

Balances due from credit institutions and central banks 347 4,012 4,929

Loans, advances and other receivables 3,668 6,203 25,776

NOTE 2 Interest payableCredit institutions and central banks 106,812 204,243 416,001

Deposits and other payables 216,426 269,179 522,093

Issued bonds 22,863 44,001 88,639

Subordinated debt 36,179 20,220 49,058

Other interest payable 519 659 1,085

Total interest payable 382,799 538,302 1,076,876

Interest payable from genuine sale and repurchase transactions:

Payables to credit institutions and central banks 3,751 8,219 10,607

Deposits and other payables 14 847 847

NOTE 3 Value adjustmentsLoans, advances and other receivables at fair value -116,299 -55,256 -123,701

Bonds 75,187 -129,512 -132,094

Shares etc. 51,760 -67,625 -289,643

Foreign exchange 5,073 -33,704 -80,328

Derivatives -17,487 2,014 88,913

Other commitments - 474 2,099

Total value adjustments -1,766 -283,609 -534,754

Alm. Brand Bank A/S – H1 2009

Page 20 of 33

NOTES TO THE FINANCIAL STATEMENTS

Group

DKK '000H1

2009H1

2008Year2008

NOTE 4 Staff costs and administrative expenses Remuneration to the Executive Board and Board of Directors:

Remuneration to the Executive Board

Salaries and wages 1,943 3,861 3,935

Pensions 357 427 841

Total 2,300 4,288 4,776

Remuneration to the Board of Directors:

Fees 212 213 450

Total remuneration to the Executive Board and Board of Directors 2,512 4,501 5,226

Staff costs:

Salaries and wages 104,449 105,113 213,747

Pensions 10,675 10,199 21,101

Social security costs 10,731 11,148 19,840

Total 125,855 126,460 254,688

Other administrative expenses 134,919 150,295 270,128

Total staff costs and administrative expenses 263,286 281,256 530,042

Number of employees

Average number of employees during the period, full-time equivalents 366 383 381

NOTE 5 Impairment of loans, advances and receivables, etc.Individual assessment:

Impairment and value adjustments, respectively, during the year 1,011,404 47,064 380,049

Reversal of impairment in previous years 31,918 33,013 56,955

Total individual assessment 979,486 14,051 323,094

Group assessment:

Impairment and value adjustments, respectively, during the year 33,757 3,131 13,078

Reversal of impairment in previous years 13,850 15,135 6,689

Total group assessment 19,907 -12,004 6,389

Losses not previously provided for 14,148 6,560 21,132

Bad debts recovered 10,927 4,784 10,697

Total impairment of loans, advances and receivables, etc. 1,002,614 3,823 339,918

Alm. Brand Bank A/S – H1 2009

Page 21 of 33

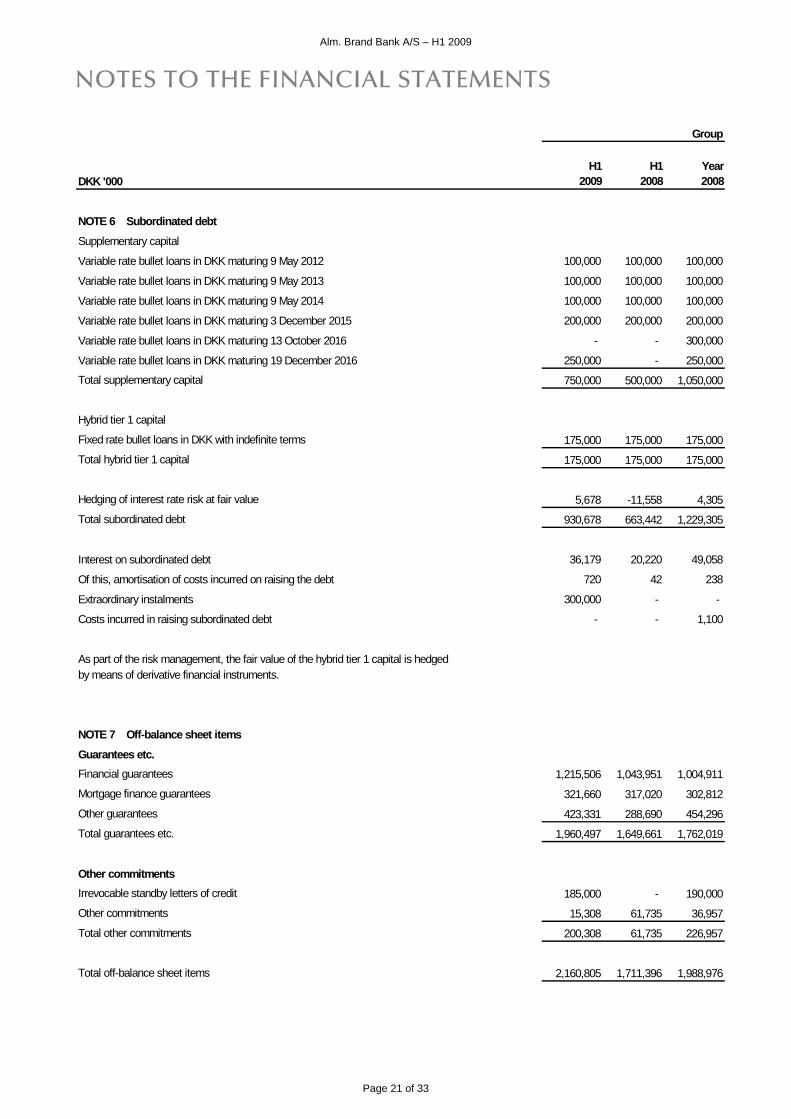

NOTES TO THE FINANCIAL STATEMENTS

Group

DKK '000H1

2009H1

2008Year2008

NOTE 6 Subordinated debtSupplementary capital

Variable rate bullet loans in DKK maturing 9 May 2012 100,000 100,000 100,000

Variable rate bullet loans in DKK maturing 9 May 2013 100,000 100,000 100,000

Variable rate bullet loans in DKK maturing 9 May 2014 100,000 100,000 100,000

Variable rate bullet loans in DKK maturing 3 December 2015 200,000 200,000 200,000

Variable rate bullet loans in DKK maturing 13 October 2016 - - 300,000

Variable rate bullet loans in DKK maturing 19 December 2016 250,000 - 250,000

Total supplementary capital 750,000 500,000 1,050,000

Hybrid tier 1 capital

Fixed rate bullet loans in DKK with indefinite terms 175,000 175,000 175,000

Total hybrid tier 1 capital 175,000 175,000 175,000

Hedging of interest rate risk at fair value 5,678 -11,558 4,305

Total subordinated debt 930,678 663,442 1,229,305

Interest on subordinated debt 36,179 20,220 49,058

Of this, amortisation of costs incurred on raising the debt 720 42 238

Extraordinary instalments 300,000 - -

Costs incurred in raising subordinated debt - - 1,100

As part of the risk management, the fair value of the hybrid tier 1 capital is hedged by means of derivative financial instruments.

NOTE 7 Off-balance sheet items

Guarantees etc.Financial guarantees 1,215,506 1,043,951 1,004,911

Mortgage finance guarantees 321,660 317,020 302,812

Other guarantees 423,331 288,690 454,296

Total guarantees etc. 1,960,497 1,649,661 1,762,019

Other commitmentsIrrevocable standby letters of credit 185,000 - 190,000

Other commitments 15,308 61,735 36,957

Total other commitments 200,308 61,735 226,957

Total off-balance sheet items 2,160,805 1,711,396 1,988,976

Alm. Brand Bank A/S – H1 2009

Page 22 of 33

NOTES TO THE FINANCIAL STATEMENTS

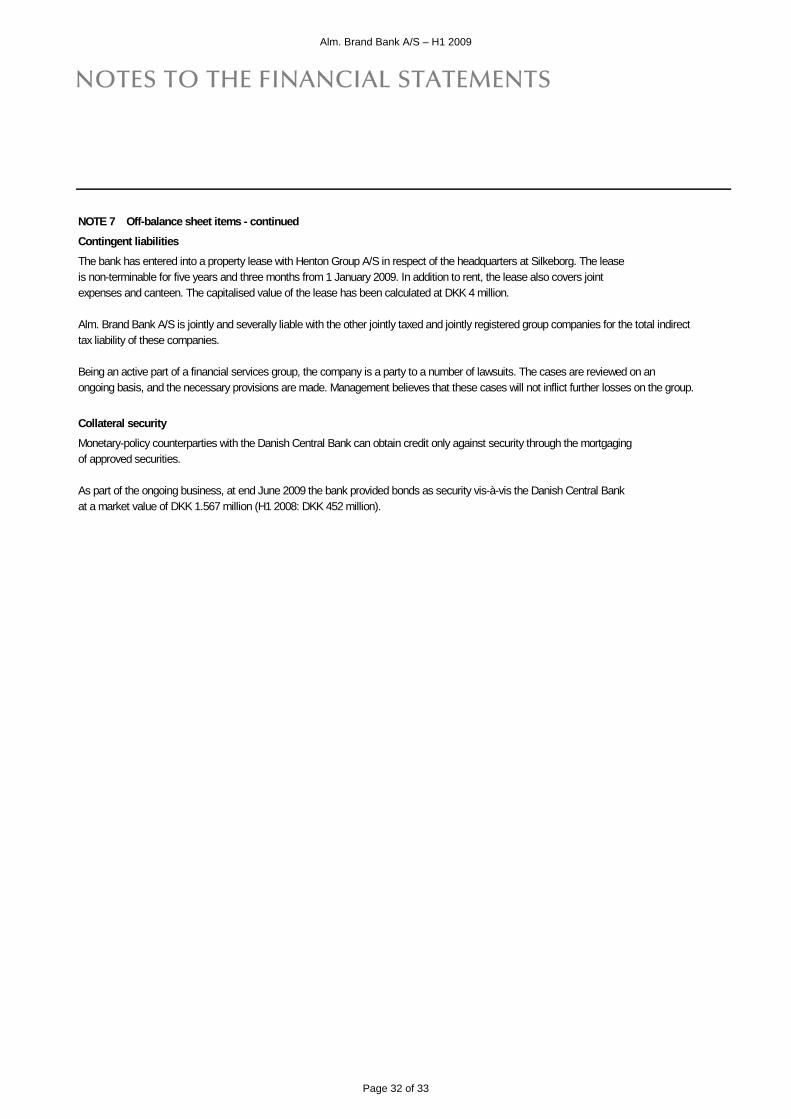

NOTE 7 Off-balance sheet items - continued

Contingent liabilitiesThe bank has entered into a property lease with Henton Group A/S in respect of the headquarters at Silkeborg. The leaseis non-terminable for five years and three months from 1 January 2009. In addition to rent, the lease also covers jointexpenses and canteen. The capitalised value of the lease has been calculated at DKK 4 million.

Being an active financial services group, the group is a party to a number of lawsuits. The cases are reviewed on an ongoingbasis, and the necessary provisions are made. Management believes that these cases will not inflict further losses on the group.

Collateral securityMonetary-policy counterparties with the Danish Central Bank can obtain credit only against security through the mortgagingof approved securities.

As part of the ongoing business, at end June 2009 the bank provided bonds as security vis-à-vis the Danish Central Bankat a market value of DKK 1.567 million (H1 2008: DKK 452 million).

Alm. Brand Bank A/S – H1 2009

Page 23 of 33

NOTES TO THE FINANCIAL STATEMENTS

Group

H1 2009

DKK '000Retail

bankingWhole-sale

bankingAlm. Brand

Finans

Alm. Brand Pante-breve

Alm. Brand Formue

Other/Elimina-

tions

Alm. Brand Bank

Group

NOTE 8 Segment information

Interest receivable 382,940 458,969 48,591 61,948 12,066 -351,646 612,868

Interest payable 268,736 318,601 28,970 46,603 13,959 -294,070 382,799

Net interest income 114,204 140,368 19,621 15,345 -1,893 -57,576 230,069

Net fee and commission income, etc. 15,779 58,253 3,726 -2,572 921 2,012 78,119

Value adjustments 324 -2,661 - -29,343 40,179 -10,265 -1,766

Other operating income - 4,204 5,789 219 - 155 10,367

Profit on ordinary activities before expenses (Net income) 130,307 200,164 29,136 -16,351 39,207 -65,674 316,789

Operating expenses 75,849 63,469 24,828 5,923 2,278 134,069 306,416

Write-downs of loans, advances and receivables, etc. 93,947 883,924 24,743 - - - 1,002,614

Profit/loss on paticipating interests - 241 - - - -536 -295

Profit on activities before tax -39,489 -746,988 -20,435 -22,274 36,929 -200,279 -992,536

H1 2008

DKK '000Retail

bankingWhole-sale

bankingAlm. Brand

Finans

Alm. Brand Pante-breve

Alm. Brand Formue

Other/Elimina-

tions

Alm. Brand Bank

Group

Interest receivable 391,460 499,888 61,515 67,329 44,035 -302,283 761,944

Interest payable 297,378 382,318 39,035 48,503 50,231 -279,163 538,302

Net interest income 94,082 117,570 22,480 18,826 -6,196 -23,120 223,642

Net fee and commission income, etc. 16,454 82,847 6,247 -2,562 5,374 3,723 112,083

Value adjustments 234 -14,310 - -29,096 -180,746 -59,691 -283,609

Other operating income 29 3,128 4,512 353 - 214 8,236

Profit on ordinary activities before expenses (Net income) 110,799 189,235 33,239 -12,479 -181,568 -78,874 60,352

Operating expenses 71,904 67,665 22,898 3,571 1,674 114,641 282,353

Write-downs of loans, advances and receivables, etc. -1,885 17,119 -11,411 - - - 3,823

Profit/loss on paticipating interests - -1,156 3,196 - - 3,798 5,838

Profit on activities before tax 40,780 103,295 24,948 -16,050 -183,242 -189,717 -219,986

Alm. Brand Bank A/S – H1 2009

Page 24 of 33

ACCOUNTING POLICIES PARENT COMPANY The parent company financial statements have been prepared in accordance with the provisions of the Danish Financial Business Act, including the executive order on financial reports presented by credit institutions and investment companies, etc. and Danish accounting standards. The consolidated financial statements have been prepared in accordance with the International Financial Reporting Standards (IFRS) as adopted by the EU. The accounting policies of the parent company on the recognition and measurement are in accordance with the accounting policies of the group, except for the following point:

Investments in group enterprises are measured according to the equity method, implying that the investments are measured at the parent company’s proportionate share of the net asset value of the associates and group enterprises at the balance sheet date. The accounting policies are unchanged as compared with the annual report for 2008. The interim report for the first six months of 2009 is unaudited.

Alm. Brand Bank A/S – H1 2009

Page 25 of 33

INCOME STATEMENT

Parent company

DKK '000 Note

H1

2009

H1

2008

Year2008

Interest receivable 1 570,612 717,248 1,444,593

Interest payable 2 373,616 528,717 1,057,412

Net interest income 196,996 188,531 387,181Dividend on participating interests 3,342 2,585 2,836

Fees and commissions receivable 90,487 119,648 223,511

Fees and commissions payable 17,785 19,208 39,452

Net interest and fee income 273,040 291,556 574,076Value adjustments 3 -12,604 -73,766 -130,520

Other operating income 4,360 3,370 7,531

Profit before expenses 264,796 221,160 451,087Staff costs and administrative expenses 4 235,259 253,114 473,093

Depreciation, amortisation and impairment of intangible assets and property, plant and equipment 993 1,097 2,455

Other ordinary expenses 37,135 - 23,453

Impairment of loans, advances and receivables, etc. 5 977,871 15,234 341,796

Profit from participating interests in associated and group undertakings -5,236 -50,051 -132,793

Profit before tax -991,698 -98,336 -522,503Tax -241,640 -20,250 -94,572

Profit for the period -750,058 -78,086 -427,931

Alm. Brand Bank A/S – H1 2009

Page 26 of 33

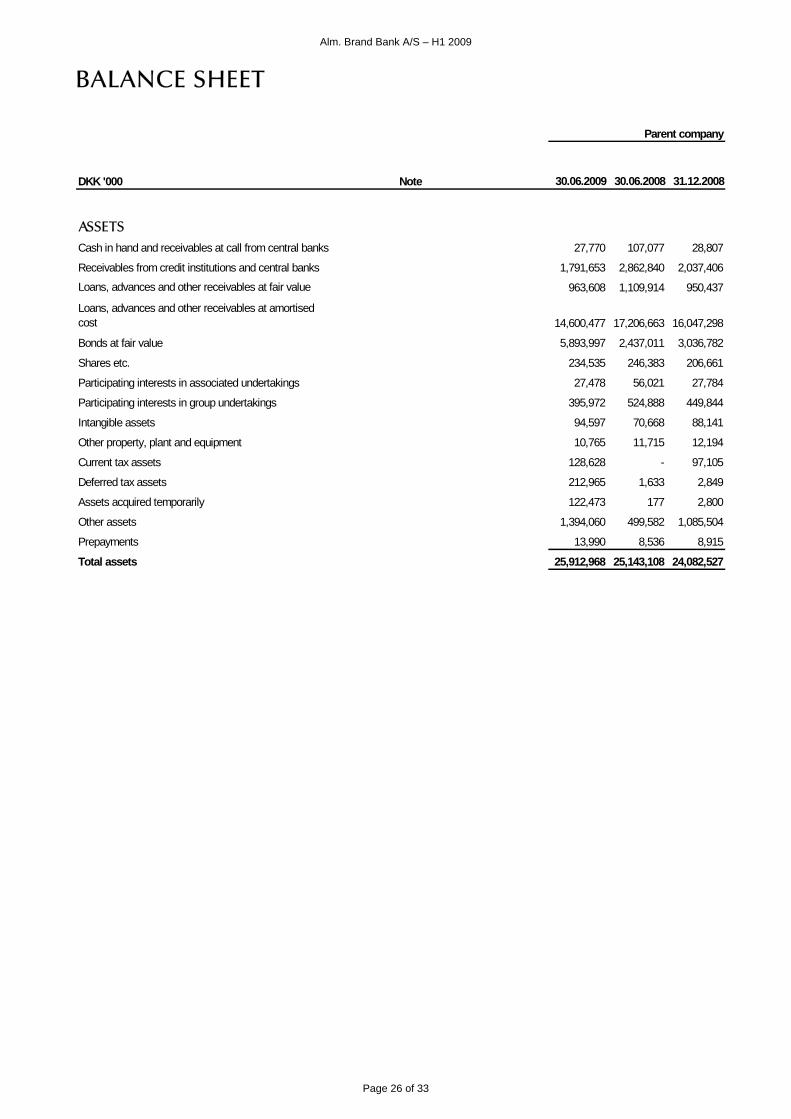

BALANCE SHEET

Parent company

DKK '000 Note 30.06.2009 30.06.2008 31.12.2008

ASSETSCash in hand and receivables at call from central banks 27,770 107,077 28,807

Receivables from credit institutions and central banks 1,791,653 2,862,840 2,037,406

Loans, advances and other receivables at fair value 963,608 1,109,914 950,437

Loans, advances and other receivables at amortised cost 14,600,477 17,206,663 16,047,298

Bonds at fair value 5,893,997 2,437,011 3,036,782

Shares etc. 234,535 246,383 206,661

Participating interests in associated undertakings 27,478 56,021 27,784

Participating interests in group undertakings 395,972 524,888 449,844

Intangible assets 94,597 70,668 88,141

Other property, plant and equipment 10,765 11,715 12,194

Current tax assets 128,628 - 97,105

Deferred tax assets 212,965 1,633 2,849

Assets acquired temporarily 122,473 177 2,800

Other assets 1,394,060 499,582 1,085,504

Prepayments 13,990 8,536 8,915

Total assets 25,912,968 25,143,108 24,082,527

Alm. Brand Bank A/S – H1 2009

Page 27 of 33

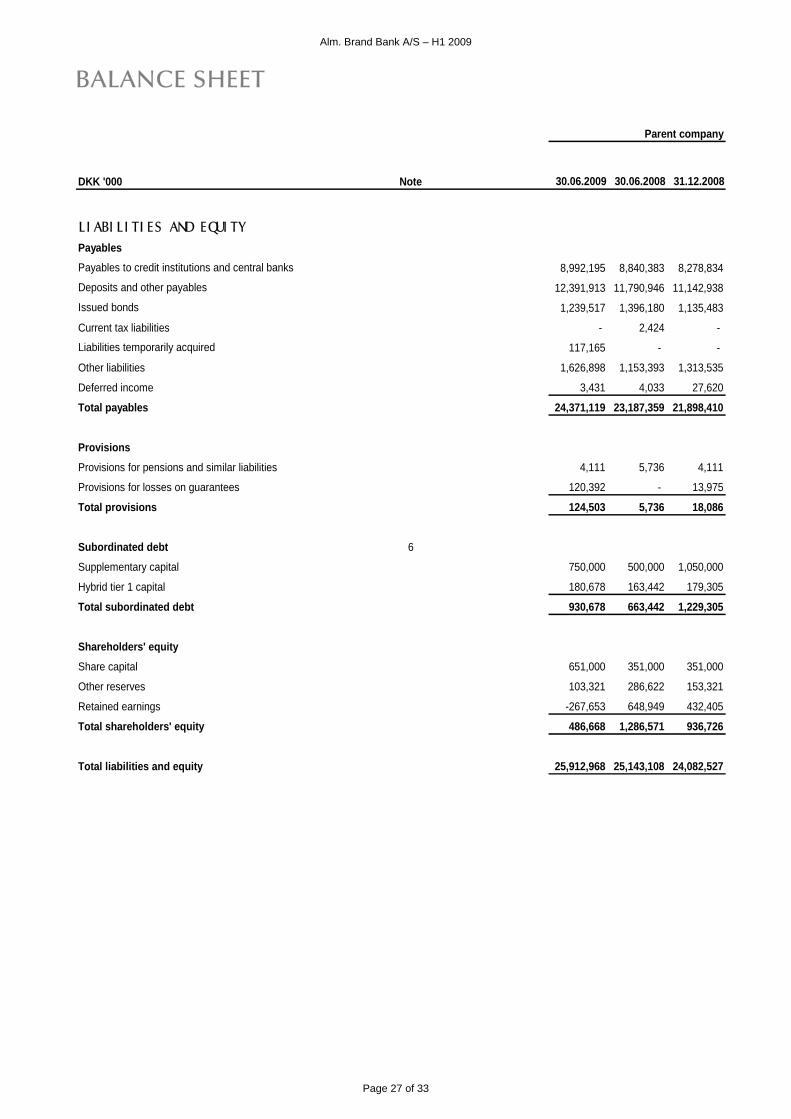

BALANCE SHEET

Parent company

DKK '000 Note 30.06.2009 30.06.2008 31.12.2008

LI ABI LI TI ES AND EQUI TYPayablesPayables to credit institutions and central banks 8,992,195 8,840,383 8,278,834

Deposits and other payables 12,391,913 11,790,946 11,142,938

Issued bonds 1,239,517 1,396,180 1,135,483

Current tax liabilities - 2,424 -

Liabilities temporarily acquired 117,165 - -

Other liabilities 1,626,898 1,153,393 1,313,535

Deferred income 3,431 4,033 27,620

Total payables 24,371,119 23,187,359 21,898,410

ProvisionsProvisions for pensions and similar liabilities 4,111 5,736 4,111

Provisions for losses on guarantees 120,392 - 13,975

Total provisions 124,503 5,736 18,086

Subordinated debt 6

Supplementary capital 750,000 500,000 1,050,000

Hybrid tier 1 capital 180,678 163,442 179,305

Total subordinated debt 930,678 663,442 1,229,305

Shareholders' equityShare capital 651,000 351,000 351,000

Other reserves 103,321 286,622 153,321

Retained earnings -267,653 648,949 432,405

Total shareholders' equity 486,668 1,286,571 936,726

Total liabilities and equity 25,912,968 25,143,108 24,082,527

Alm. Brand Bank A/S – H1 2009

Page 28 of 33

STATEMENT OF CHANGES IN EQUITY

Parent company

DKK '000Share

capitalOther

reservesRetained earnings Total

Shareholders' equity at 1 January 2008 351,000 336,622 677,035 1,364,657

Equity movements in H1 2008Dividend subsidiaries -50,000 50,000 -

Profit for the year - - -78,086 -78,086

Comprehensive income in H1 2008 - -50,000 -28,086 -78,086

Dividend paid -

Total equity movements in H1 2008 - -50,000 -28,086 -78,086

Shareholders' equity at 30 June 2008 351,000 286,622 648,949 1,286,571

Shareholders' equity at 1 January 2008 351,000 336,622 677,035 1,364,657

Equity movements in 2008Dividend subsidiaries -50,000 50,000 -

Profit for the period - -133,301 -294,630 -427,931

Comprehensive income in 2008 - -183,301 -244,630 -427,931

Dividend paid -

Total equity movements in 2008 - -183,301 -244,630 -427,931

Shareholders' equity at 31 December 2008 351,000 153,321 432,405 936,726

Shareholders' equity at 1 January 2009 351,000 153,321 432,405 936,726

Equity movements in 2009Capital injection 300,000 300,000

Dividend subsidiaries -50,000 50,000 -

Profit for the period -750,058 -750,058

Comprehensive income in 2009 300,000 -50,000 -700,058 -450,058

Dividend paid -

Total equity movements in 2009 300,000 -50,000 -700,058 -450,058

Shareholders' equity at 30 June 2009 651,000 103,321 -267,653 486,668

Alm. Brand Bank A/S – H1 2009

Page 29 of 33

NOTES TO THE FINACIAL STATEMENTS

Parent company

DKK '000H1

2009H1

2008Year2008

NOTE 1 Interest receivableReceivables from credit institutions and central banks 24,973 31,194 74,436

Loans, advances and other receivables 490,231 592,851 1,209,898

Bonds 86,418 70,519 129,631

Total derivatives -35,184 22,684 30,628

Of which:

Currency contracts 23,254 20,325 42,798

Interest rate contracts -58,438 2,359 -12,170

Other interest receivable 4,174 - -

Total interest receivable 570,612 717,248 1,444,593

Interest receivable from genuine purchase and resale transactions:

Balances due from credit institutions and central banks 347 4,012 4,929

Loans, advances and other receivables 3,668 21,020 25,776

NOTE 2 Interest payableCredit institutions and central banks 97,603 194,666 396,384

Deposits and other payables 216,453 269,187 522,246

Issued bonds 22,863 44,001 88,640

Subordinated debt 36,179 20,220 49,058

Other interest payable 518 643 1,084

Total interest payable 373,616 528,717 1,057,412

Interest payable from genuine sale and repurchase transactions:

Payables to credit institutions and central banks 3,751 8,219 10,607

Deposits and other payables 14 847 847

NOTE 3 Value adjustmentsLoans, advances and other receivables at fair value -74,778 -39,181 -114,964

Bonds 66,753 -63,241 -47,940

Shares etc. 16,045 -5,603 -29,332

Foreign exchange -3,753 -340 -12,124

Derivatives -16,871 34,125 71,741

Other commitments - 474 2,099

Total value adjustments -12,604 -73,766 -130,520

Alm. Brand Bank A/S – H1 2009

Page 30 of 33

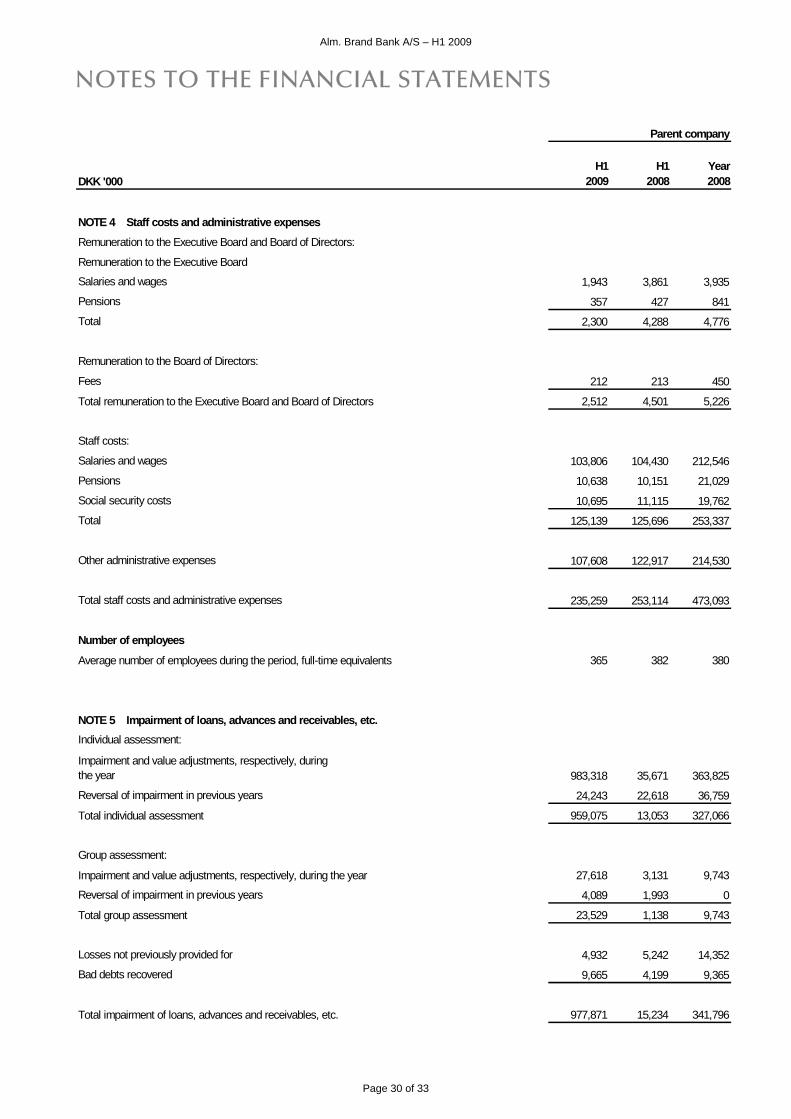

NOTES TO THE FINANCIAL STATEMENTS

Parent company

DKK '000H1

2009H1

2008Year2008

NOTE 4 Staff costs and administrative expenses Remuneration to the Executive Board and Board of Directors:

Remuneration to the Executive Board

Salaries and wages 1,943 3,861 3,935

Pensions 357 427 841

Total 2,300 4,288 4,776

Remuneration to the Board of Directors:

Fees 212 213 450

Total remuneration to the Executive Board and Board of Directors 2,512 4,501 5,226

Staff costs:

Salaries and wages 103,806 104,430 212,546

Pensions 10,638 10,151 21,029

Social security costs 10,695 11,115 19,762

Total 125,139 125,696 253,337

Other administrative expenses 107,608 122,917 214,530

Total staff costs and administrative expenses 235,259 253,114 473,093

Number of employees

Average number of employees during the period, full-time equivalents 365 382 380

NOTE 5 Impairment of loans, advances and receivables, etc.Individual assessment:

Impairment and value adjustments, respectively, during the year 983,318 35,671 363,825

Reversal of impairment in previous years 24,243 22,618 36,759

Total individual assessment 959,075 13,053 327,066

Group assessment:

Impairment and value adjustments, respectively, during the year 27,618 3,131 9,743

Reversal of impairment in previous years 4,089 1,993 0

Total group assessment 23,529 1,138 9,743

Losses not previously provided for 4,932 5,242 14,352

Bad debts recovered 9,665 4,199 9,365

Total impairment of loans, advances and receivables, etc. 977,871 15,234 341,796

Alm. Brand Bank A/S – H1 2009

Page 31 of 33

NOTES TO THE FINANCIAL STATEMENTS

Parent company

DKK '000H1

2009H1

2008Year2008

NOTE 6 Subordinated debtSupplementary capital

Variable rate bullet loans in DKK maturing 9 May 2012 100,000 100,000 100,000

Variable rate bullet loans in DKK maturing 9 May 2013 100,000 100,000 100,000

Variable rate bullet loans in DKK maturing 9 May 2014 100,000 100,000 100,000

Variable rate bullet loans in DKK maturing 3 December 2015 200,000 200,000 200,000

Variable rate bullet loans in DKK maturing 13 October 2016 - - 300,000

Variable rate bullet loans in DKK maturing 19 December 2016 250,000 - 250,000

Total supplementary capital 750,000 500,000 1,050,000

Hybrid tier 1 capital

Fixed rate bullet loans in DKK with indefinite terms 175,000 175,000 175,000

Total hybrid tier 1 capital 175,000 175,000 175,000

Hedging of interest rate risk at fair value 5,678 -11,558 4,305

Total subordinated debt 930,678 663,442 1,229,305

Interest on subordinated debt 36,179 20,220 49,058

Of this, amortisation of costs incurred on raising the debt 720 42 238

Extraordinary instalments 300,000 - -

Costs incurred in raising subordinated debt - - 1,100

As part of the risk management, the fair value of the hybrid tier 1 capital is hedged by means of derivative financial instruments.

NOTE 7 Off-balance sheet itemsGuarantees etc.Financial guarantees 1,215,506 1,043,951 1,004,911

Mortgage finance guarantees 321,660 317,020 302,812

Other guarantees 423,331 288,690 454,296

Total guarantees etc. 1,960,497 1,649,661 1,762,019

Other commitmentsIrrevocable standby letters of credit 185,000 - 190,000

Other commitments 15,308 61,735 36,957

Total other commitments 200,308 61,735 226,957

Total off-balance sheet items 2,160,805 1,711,396 1,988,976

Alm. Brand Bank A/S – H1 2009

Page 32 of 33

NOTES TO THE FINANCIAL STATEMENTS

NOTE 7 Off-balance sheet items - continuedContingent liabilitiesThe bank has entered into a property lease with Henton Group A/S in respect of the headquarters at Silkeborg. The leaseis non-terminable for five years and three months from 1 January 2009. In addition to rent, the lease also covers jointexpenses and canteen. The capitalised value of the lease has been calculated at DKK 4 million.

Alm. Brand Bank A/S is jointly and severally liable with the other jointly taxed and jointly registered group companies for the total indirecttax liability of these companies.

Being an active part of a financial services group, the company is a party to a number of lawsuits. The cases are reviewed on anongoing basis, and the necessary provisions are made. Management believes that these cases will not inflict further losses on the group.

Collateral securityMonetary-policy counterparties with the Danish Central Bank can obtain credit only against security through the mortgagingof approved securities.

As part of the ongoing business, at end June 2009 the bank provided bonds as security vis-à-vis the Danish Central Bankat a market value of DKK 1.567 million (H1 2008: DKK 452 million).

Alm. Brand Bank A/S – H1 2009

Page 33 of 33

NOTES TO THE FINANCIAL STATEMENTS

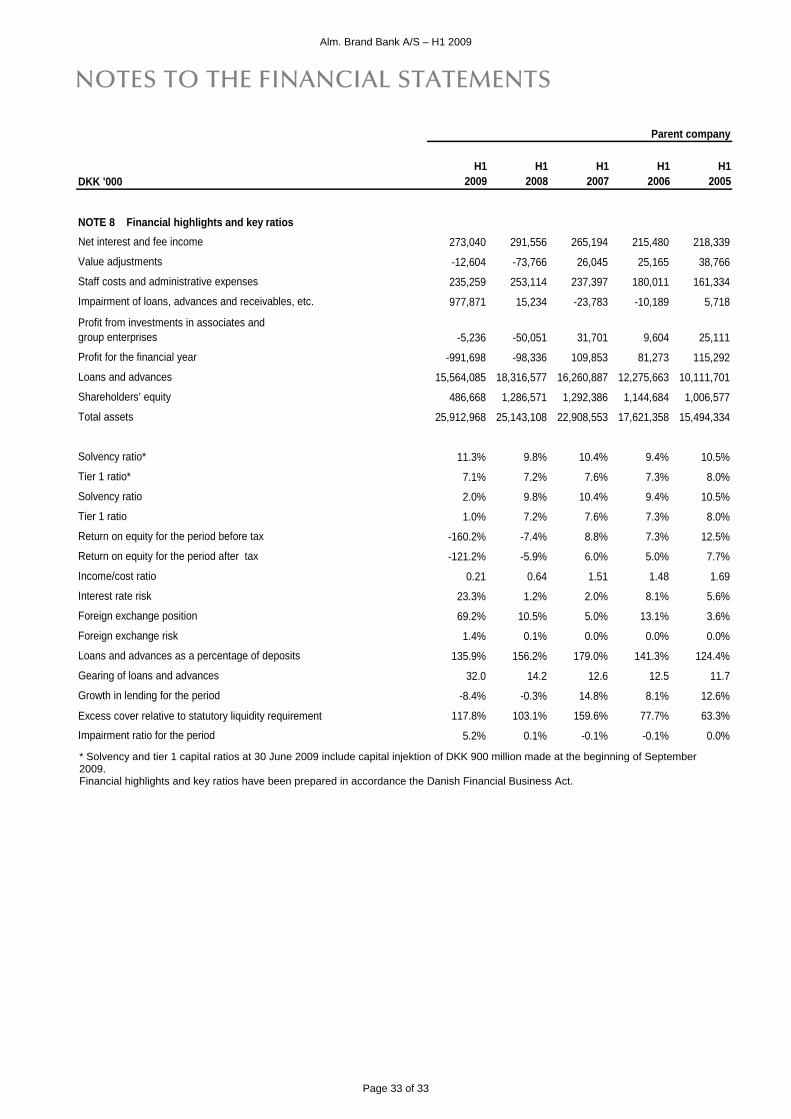

Parent company

DKK '000H1

2009H1

2008H1

2007H1

2006H1

2005

NOTE 8 Financial highlights and key ratiosNet interest and fee income 273,040 291,556 265,194 215,480 218,339

Value adjustments -12,604 -73,766 26,045 25,165 38,766

Staff costs and administrative expenses 235,259 253,114 237,397 180,011 161,334

Impairment of loans, advances and receivables, etc. 977,871 15,234 -23,783 -10,189 5,718

Profit from investments in associates andgroup enterprises -5,236 -50,051 31,701 9,604 25,111

Profit for the financial year -991,698 -98,336 109,853 81,273 115,292

Loans and advances 15,564,085 18,316,577 16,260,887 12,275,663 10,111,701

Shareholders’ equity 486,668 1,286,571 1,292,386 1,144,684 1,006,577

Total assets 25,912,968 25,143,108 22,908,553 17,621,358 15,494,334

Solvency ratio* 11.3% 9.8% 10.4% 9.4% 10.5%

Tier 1 ratio* 7.1% 7.2% 7.6% 7.3% 8.0%

Solvency ratio 2.0% 9.8% 10.4% 9.4% 10.5%

Tier 1 ratio 1.0% 7.2% 7.6% 7.3% 8.0%

Return on equity for the period before tax -160.2% -7.4% 8.8% 7.3% 12.5%

Return on equity for the period after tax -121.2% -5.9% 6.0% 5.0% 7.7%

Income/cost ratio 0.21 0.64 1.51 1.48 1.69

Interest rate risk 23.3% 1.2% 2.0% 8.1% 5.6%

Foreign exchange position 69.2% 10.5% 5.0% 13.1% 3.6%

Foreign exchange risk 1.4% 0.1% 0.0% 0.0% 0.0%

Loans and advances as a percentage of deposits 135.9% 156.2% 179.0% 141.3% 124.4%

Gearing of loans and advances 32.0 14.2 12.6 12.5 11.7

Growth in lending for the period -8.4% -0.3% 14.8% 8.1% 12.6%

Excess cover relative to statutory liquidity requirement 117.8% 103.1% 159.6% 77.7% 63.3%

Impairment ratio for the period 5.2% 0.1% -0.1% -0.1% 0.0%

* Solvency and tier 1 capital ratios at 30 June 2009 include capital injektion of DKK 900 million made at the beginning of September 2009. Financial highlights and key ratios have been prepared in accordance the Danish Financial Business Act.