IN PAS T T WO Y E ARS , PE-BACKED E X I T VAL UE T O TAL S $ 1 .0 7 TPAGE 4»

CORP OR AT E ACQUISI T IONS SURGE IN T O TAL VAL UE , HI T T ING $ 360B IN 20 15PAGE 7»

PE-BACKED IP O VAL UAT ION SL IDE S F OR SECOND Y E AR IN A ROWPAGE 9»

AND COMPANY INVENTORY2015 Annual

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

ContentNIZAR TARHUNI Senior Analyst

BRIAN LEE Data Analyst

JENNIFER SAM Senior Graphic Designer

JESS CHAIDEZ Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2016 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Introduction 3

Overview 4–5

Exits by Type & Industry 6

Corporate Acquisitions 7

Secondary Buyouts 8

IPOs 9

Company Inventory 10

Contents

2 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

A disequilibrium between sellers and buyersIntroduction

2015 remained a strong year for private equity sellers as the quantity of

acquisitive buyers in the market outpaced that of sellers, contributing to

sustained high valuations for those looking to exit. While seller expectations

remained high, and many were certainly able to negotiate attractive terms in

sales processes, those same sellers faced issues finding attractive deals to put

capital to work, continuing a bifurcation between success in buying and selling

for PE.

Trends around popular exit ramps remained similar to what we’ve observed

recently, with strategic acquisitions accounting for the bulk of PE-backed sales,

followed by PE-to-PE buyouts. Strategic and PE buyers have found themselves

in the same processes bidding for deals, increasing competition and helping pad

exit values for sellers—again a double-edged sword for PE as they look to close

deals on both sides of the table. With a wave of new fund managers spinning out

vehicles focused on utilizing operational expertise and a deeper understanding

of certain sectors, these general partners have been able to help underpin

growth in secondary buyouts, deeming their expertise a strategic advantage

over other bidders and subsequently bidding much more aggressively.

PE-backed inventory levels remain inflated, and with managers scouring for

opportunities after years of overly successful fundraising efforts, we don’t

expect this to change in a meaningful way. The rate of investments in the past,

such as those made in 2007, has contributed to a rise in zombie vehicles, as fund

managers face substantial challenges exiting various companies. Consequently,

when you consider these aging assets in conjunction with the dire need of

dealmakers to capitalize on any market stutters that could open up a window for

investors to become more aggressive, that inventory will remain at least flat in

the coming future.

This report spans PE-backed exits in North America and Europe. We hope

you find the enclosed data and insights helpful as you assess the macro PE

landscape. As always, feel free to contact us with any questions.

MAKE WAY FOR

SMARTER, ON-THE-FLY MEETING PREP

US +1 206.623.1986

UK +44 (0)207.190.9809

pitchbook.com

Introducing PitchBook

Mobile. The same

excellent data, technology

and service from the

PitchBook Platform, now

available on a mobile

device.

Search:

“PitchBook”

Available for

NIZAR TARHUNI

Senior Analyst

3 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

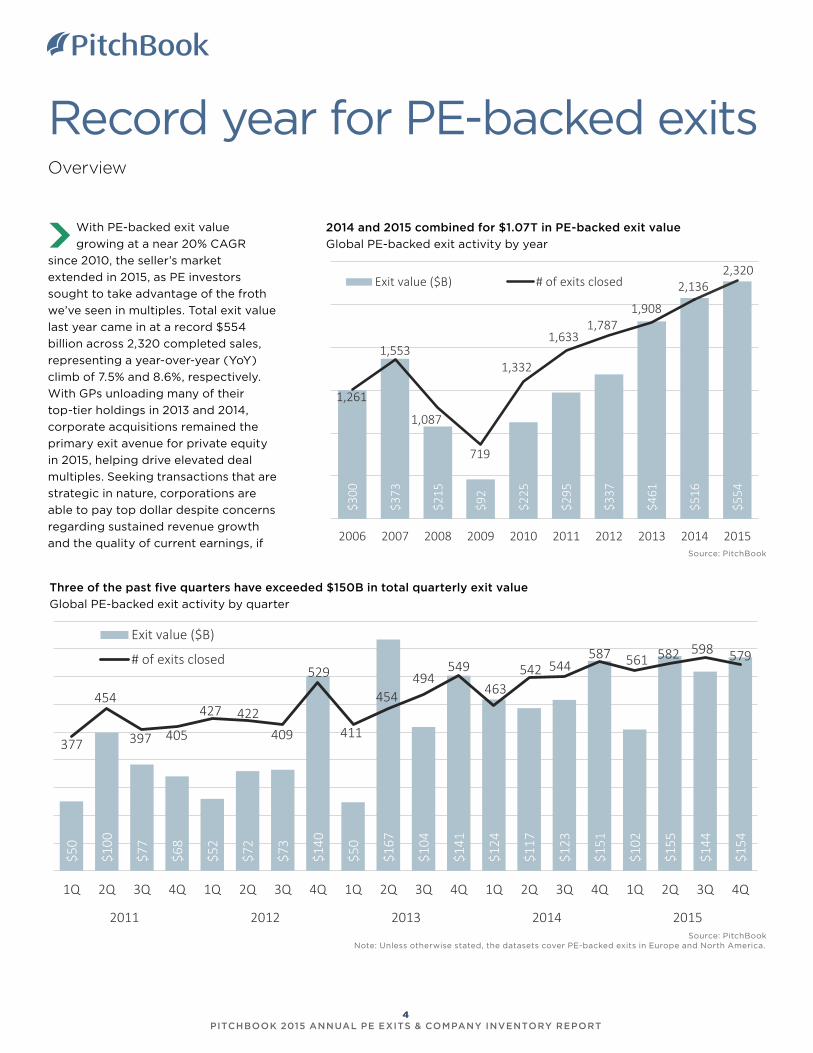

Record year for PE-backed exitsOverview

With PE-backed exit value

growing at a near 20% CAGR

since 2010, the seller’s market

extended in 2015, as PE investors

sought to take advantage of the froth

we’ve seen in multiples. Total exit value

last year came in at a record $554

billion across 2,320 completed sales,

representing a year-over-year (YoY)

climb of 7.5% and 8.6%, respectively.

With GPs unloading many of their

top-tier holdings in 2013 and 2014,

corporate acquisitions remained the

primary exit avenue for private equity

in 2015, helping drive elevated deal

multiples. Seeking transactions that are

strategic in nature, corporations are

able to pay top dollar despite concerns

regarding sustained revenue growth

and the quality of current earnings, if

Three of the past five quarters have exceeded $150B in total quarterly exit value

Global PE-backed exit activity by quarter

2014 and 2015 combined for $1.07T in PE-backed exit value

Global PE-backed exit activity by year

Source: PitchBook

$300

$373

$215

$92

$225

$295

$337

$461

$516

$554

1,261

1,553

1,087

719

1,332

1,6331,787

1,908

2,1362,320

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exit value ($B) # of exits closed

$50

$100

$77

$68

$52

$72

$73

$140

$50

$167

$104

$141

$124

$117

$123

$151

$102

$155

$144

$154

377

454

397 405

427 422409

529

411

454494

549

463542 544

587 561 582 598 579

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2011 2012 2013 2014 2015

Exit value ($B)

# of exits closed

Source: PitchBookNote: Unless otherwise stated, the datasets cover PE-backed exits in Europe and North America.

4 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

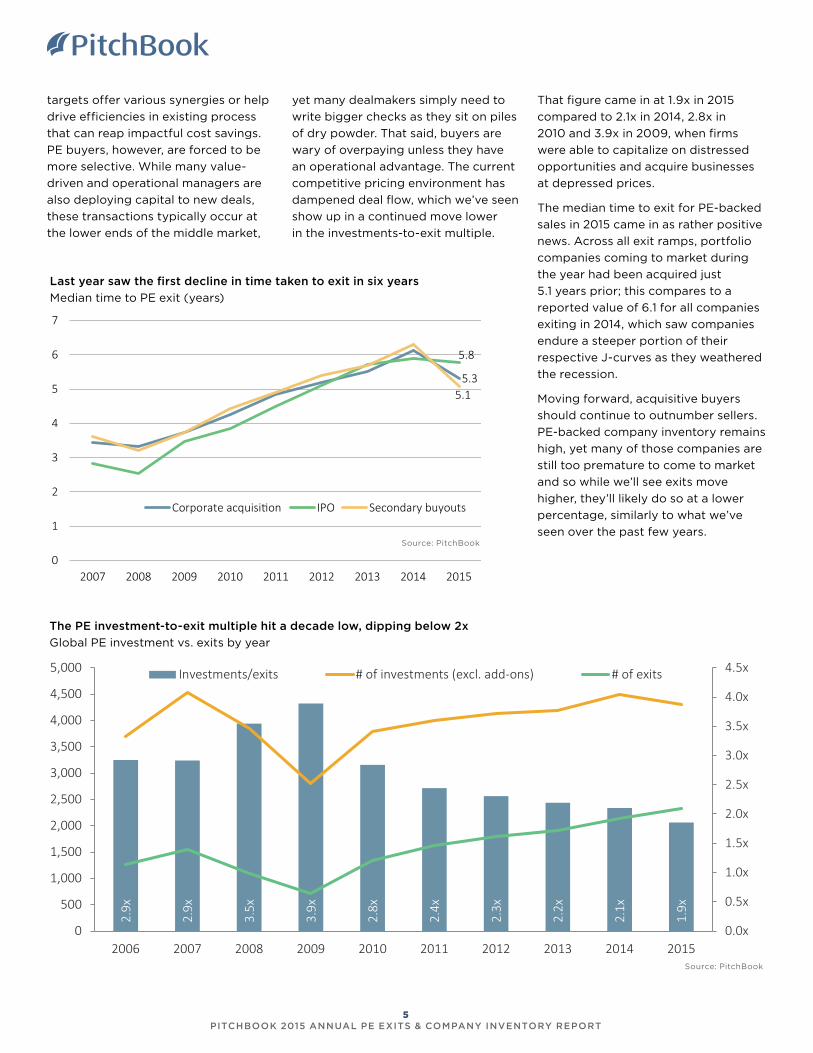

The PE investment-to-exit multiple hit a decade low, dipping below 2x

Global PE investment vs. exits by year

Last year saw the first decline in time taken to exit in six years

Median time to PE exit (years)

0

1

2

3

4

5

6

7

2007 2008 2009 2010 2011 2012 2013 2014 2015

Corporate acquisition IPO Secondary buyouts

5.8

5.35.1

Source: PitchBook

2.9x

2.9x

3.5x

3.9x

2.8x

2.4x

2.3x

2.2x

2.1x

1.9x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Investments/exits # of investments (excl. add-ons) # of exits

Source: PitchBook

targets offer various synergies or help

drive efficiencies in existing process

that can reap impactful cost savings.

PE buyers, however, are forced to be

more selective. While many value-

driven and operational managers are

also deploying capital to new deals,

these transactions typically occur at

the lower ends of the middle market,

yet many dealmakers simply need to

write bigger checks as they sit on piles

of dry powder. That said, buyers are

wary of overpaying unless they have

an operational advantage. The current

competitive pricing environment has

dampened deal flow, which we’ve seen

show up in a continued move lower

in the investments-to-exit multiple.

That figure came in at 1.9x in 2015

compared to 2.1x in 2014, 2.8x in

2010 and 3.9x in 2009, when firms

were able to capitalize on distressed

opportunities and acquire businesses

at depressed prices.

The median time to exit for PE-backed

sales in 2015 came in as rather positive

news. Across all exit ramps, portfolio

companies coming to market during

the year had been acquired just

5.1 years prior; this compares to a

reported value of 6.1 for all companies

exiting in 2014, which saw companies

endure a steeper portion of their

respective J-curves as they weathered

the recession.

Moving forward, acquisitive buyers

should continue to outnumber sellers.

PE-backed company inventory remains

high, yet many of those companies are

still too premature to come to market

and so while we’ll see exits move

higher, they’ll likely do so at a lower

percentage, similarly to what we’ve

seen over the past few years.

5 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

IT saw a whopping $98.8B in total exit value last year,

an increase of 50% over 2014

Global PE-backed exits ($B) by industry

Strategics dominate, but 2015 saw $153B in value

exited through SBOs

Global PE-backed exits ($B) by type

B2B and B2C combined accounted for nearly 60% of

all PE-backed exits last year

Global PE-backed exits (#) by industry

The number of secondary buyouts eclipsed 950 to

reach a high for the decade

Global PE-backed exits (#) by type

Exits by type & industry

0

500

1,000

1,500

2,000

2,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Corporate acquisition IPO

Secondary buyout $0

$100

$200

$300

$400

$500

$600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Corporate acquisition IPO

Secondary buyout

Source: PitchBook

Source: PitchBook

0

500

1,000

1,500

2,000

2,500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

B2B B2C

Energy Financial services

Healthcare IT

Materials & resources

$0

$100

$200

$300

$400

$500

$600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

B2B B2C

Energy Financial services

Healthcare IT

Materials & resources

Source: PitchBook

Source: PitchBook

Strategic M&A has been the primary driver of exit value for PE sellers, although SBOs played a considerable role.

Healthcare exits grew in count by 19% YoY, accounting for a massive $67.7B in 2015, 12% of total annual exit value.

6 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

Strategics predominateCorporate acquisitions

Accounting for more than 54% of

all PE-backed exits in 2015, the

corporate acquisition ramp remains

the most sought-after exit avenue for

In the past three years, strategic M&A value has totaled $963B

Global corporate acquisitions by year

A slight decline year-over-year

Median corporate acquisition valuation/EBITDA

multiples

Despite sliding from 2014, last year sustained a high

level of median deal size

Median corporate acquisition size ($M)

$150

$151

$140

$72

$134

$201

$193

$296

$307

$360

606

759646

441

761

9161,023 1,038

1,1251,263

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exit value ($B)

# of exits closed

Source: PitchBook

$180

$172

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

9.7x9.0x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Source: PitchBook Source: PitchBook

PE. Since the $133.6 billion in total exit

value generated via sales to strategics

in 2010, the ramp has seen total exit

value grow at a CAGR of 22%, with

$360 billion being exited across 1,263

corporate buys last year. The record

amount of PE-backed inventory

continues to contribute to the asset

class serving as a playground for

corporate acquirers unable to show

appealing growth to shareholders

amid a changing business landscape

and an ostensibly slowing global

economy. Further, as competitors

continue to seek acquisitive growth,

companies are at times being forced

to shift their strategies away from

traditional organic growth in fear of

losing market share. The healthcare

and technology sectors accounted for

the largest percentage growth in total

capital exited to strategics. PE-backed

tech sector sales in 2015 amounted

to over $64 billion while healthcare

represented $55.5 billion, representing

respective yearly growth rates of 63%

and near 80%.

7 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

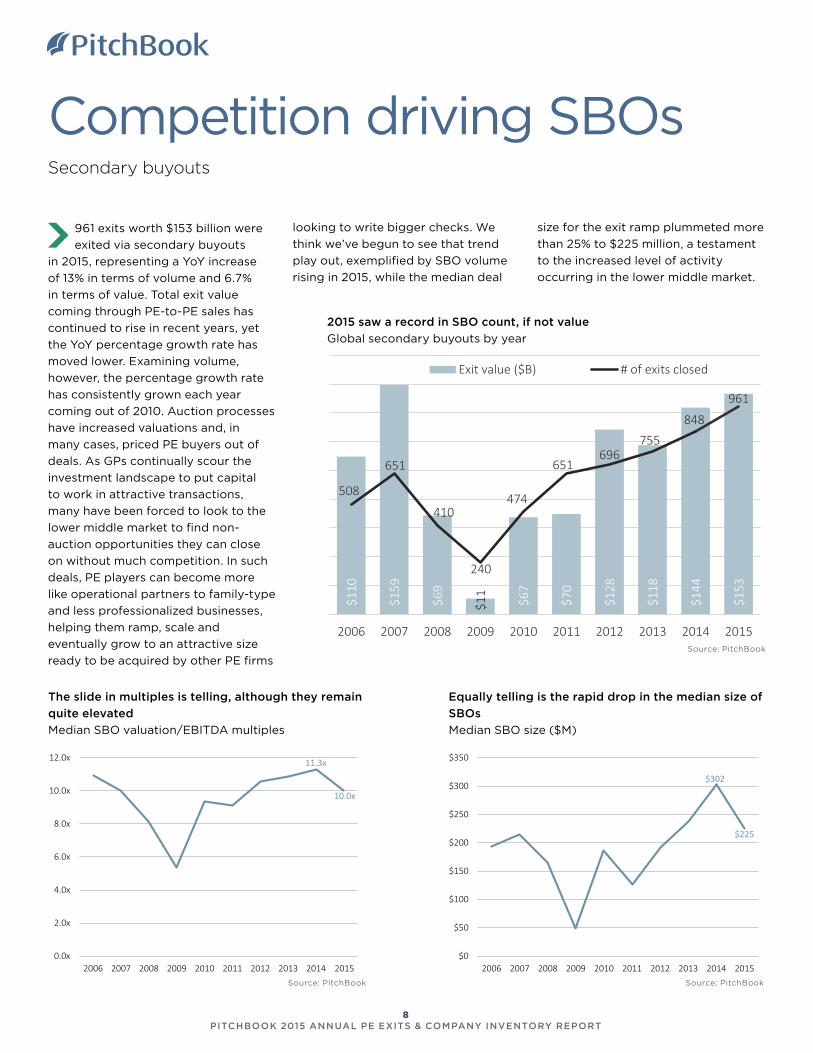

Competition driving SBOsSecondary buyouts

961 exits worth $153 billion were

exited via secondary buyouts

in 2015, representing a YoY increase

of 13% in terms of volume and 6.7%

in terms of value. Total exit value

coming through PE-to-PE sales has

continued to rise in recent years, yet

the YoY percentage growth rate has

moved lower. Examining volume,

however, the percentage growth rate

has consistently grown each year

coming out of 2010. Auction processes

have increased valuations and, in

many cases, priced PE buyers out of

deals. As GPs continually scour the

investment landscape to put capital

to work in attractive transactions,

many have been forced to look to the

lower middle market to find non-

auction opportunities they can close

on without much competition. In such

deals, PE players can become more

like operational partners to family-type

and less professionalized businesses,

helping them ramp, scale and

eventually grow to an attractive size

ready to be acquired by other PE firms

2015 saw a record in SBO count, if not value

Global secondary buyouts by year

The slide in multiples is telling, although they remain

quite elevated

Median SBO valuation/EBITDA multiples

Equally telling is the rapid drop in the median size of

SBOs

Median SBO size ($M)

Source: PitchBook

$302

$225

$0

$50

$100

$150

$200

$250

$300

$350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Source: PitchBook

11.3x

10.0x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Source: PitchBook

looking to write bigger checks. We

think we’ve begun to see that trend

play out, exemplified by SBO volume

rising in 2015, while the median deal

size for the exit ramp plummeted more

than 25% to $225 million, a testament

to the increased level of activity

occurring in the lower middle market.

$110

$159

$69

$11

$67

$70

$128

$118

$144

$153

508

651

410

240

474

651696

755848

961

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Exit value ($B) # of exits closed

8 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

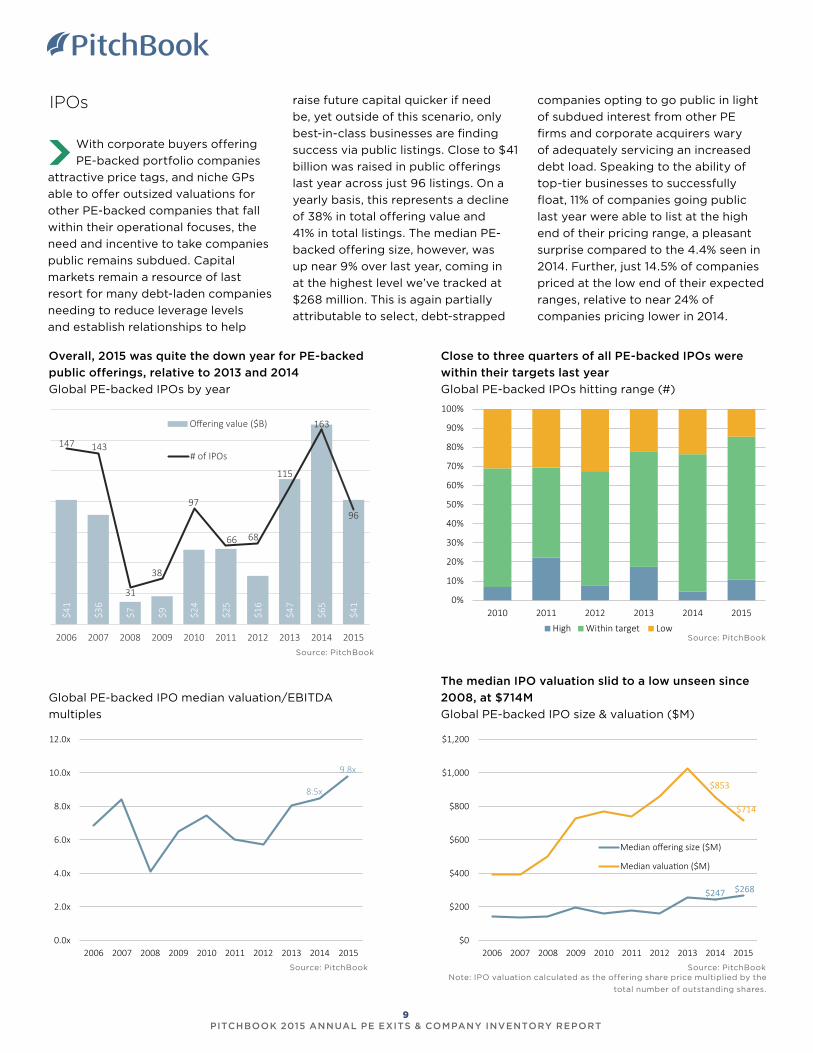

With corporate buyers offering

PE-backed portfolio companies

attractive price tags, and niche GPs

able to offer outsized valuations for

other PE-backed companies that fall

within their operational focuses, the

need and incentive to take companies

public remains subdued. Capital

markets remain a resource of last

resort for many debt-laden companies

needing to reduce leverage levels

and establish relationships to help

The median IPO valuation slid to a low unseen since

2008, at $714M

Global PE-backed IPO size & valuation ($M)

Close to three quarters of all PE-backed IPOs were

within their targets last year

Global PE-backed IPOs hitting range (#)

Global PE-backed IPO median valuation/EBITDA

multiples

Overall, 2015 was quite the down year for PE-backed

public offerings, relative to 2013 and 2014

Global PE-backed IPOs by year

raise future capital quicker if need

be, yet outside of this scenario, only

best-in-class businesses are finding

success via public listings. Close to $41

billion was raised in public offerings

last year across just 96 listings. On a

yearly basis, this represents a decline

of 38% in total offering value and

41% in total listings. The median PE-

backed offering size, however, was

up near 9% over last year, coming in

at the highest level we’ve tracked at

$268 million. This is again partially

attributable to select, debt-strapped

companies opting to go public in light

of subdued interest from other PE

firms and corporate acquirers wary

of adequately servicing an increased

debt load. Speaking to the ability of

top-tier businesses to successfully

float, 11% of companies going public

last year were able to list at the high

end of their pricing range, a pleasant

surprise compared to the 4.4% seen in

2014. Further, just 14.5% of companies

priced at the low end of their expected

ranges, relative to near 24% of

companies pricing lower in 2014.

IPOs

$41

$36

$7 $9 $24

$25

$16

$47

$65

$41

147 143

31

38

97

66 68

115

163

96

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Offering value ($B)

# of IPOs

$247 $268

$853

$714

$0

$200

$400

$600

$800

$1,000

$1,200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median offering size ($M)

Median valuation ($M)

Source: PitchBook

Source: PitchBook

8.5x

9.8x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015Source: PitchBook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

High Within target LowSource: PitchBook

Note: IPO valuation calculated as the offering share price multiplied by the

total number of outstanding shares.

9 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

Company inventory

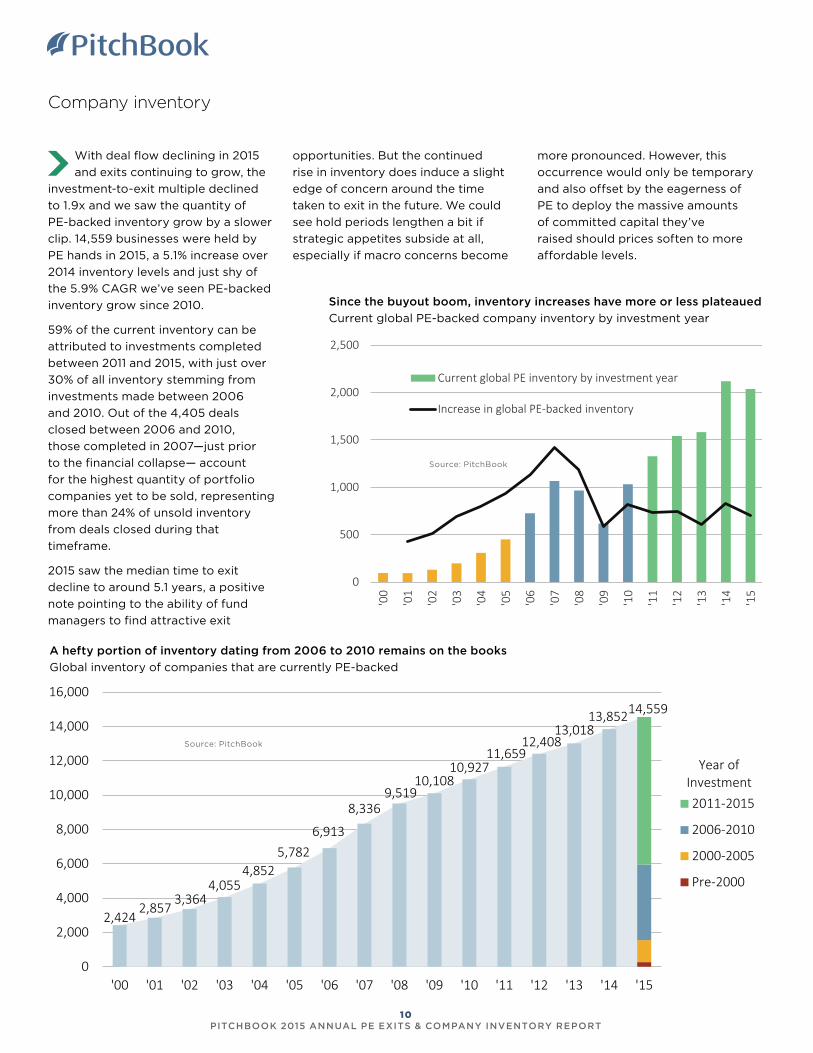

With deal flow declining in 2015

and exits continuing to grow, the

investment-to-exit multiple declined

to 1.9x and we saw the quantity of

PE-backed inventory grow by a slower

clip. 14,559 businesses were held by

PE hands in 2015, a 5.1% increase over

2014 inventory levels and just shy of

the 5.9% CAGR we’ve seen PE-backed

inventory grow since 2010.

59% of the current inventory can be

attributed to investments completed

between 2011 and 2015, with just over

30% of all inventory stemming from

investments made between 2006

and 2010. Out of the 4,405 deals

closed between 2006 and 2010,

those completed in 2007—just prior

to the financial collapse— account

for the highest quantity of portfolio

companies yet to be sold, representing

more than 24% of unsold inventory

from deals closed during that

timeframe.

2015 saw the median time to exit

decline to around 5.1 years, a positive

note pointing to the ability of fund

managers to find attractive exit

A hefty portion of inventory dating from 2006 to 2010 remains on the books

Global inventory of companies that are currently PE-backed

Since the buyout boom, inventory increases have more or less plateaued

Current global PE-backed company inventory by investment year

0

500

1,000

1,500

2,000

2,500

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

Current global PE inventory by investment year

Increase in global PE-backed inventory

Source: PitchBook

2,4242,857

3,3644,055

4,8525,782

6,913

8,3369,519

10,10810,927

11,65912,408

13,01813,85214,559

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

2011-2015

2006-2010

2000-2005

Pre-2000

Year of Investment

Source: PitchBook

opportunities. But the continued

rise in inventory does induce a slight

edge of concern around the time

taken to exit in the future. We could

see hold periods lengthen a bit if

strategic appetites subside at all,

especially if macro concerns become

more pronounced. However, this

occurrence would only be temporary

and also offset by the eagerness of

PE to deploy the massive amounts

of committed capital they’ve

raised should prices soften to more

affordable levels.

10 PITCHBOOK 2015 ANNUAL PE EXITS & COMPANY INVENTORY REPORT

Contact PitchBook

pitchbook.com

RESEARCH [email protected]

EDITORIAL [email protected]

SALES [email protected]

YOUR JOURNEY TO STRONGER RETURNS STARTS HERE

With data on:

Companies

Investors

Deals

M&A

Limited partners

Funds

Financials

Advisors

People

Request a free trial

US +1 206.623.1986

UK +44 (0)207.190.9809

pitchbook.com

The PitchBook Platform for private equity

• Strengthen your LP relationships

• Build a better portfolio

• Exit efficiently and successfully

• Elevate your firm with award-winning technology