DAnSKe BAnK A/S

HolmenS KAnAl 2-12

DK-1092 KøBenHAvn K

tel. +45 33 44 00 00

Cvr-nr. 611262 28-KøBenHAvn

www.DAnSKeBAnK.Com

An

nu

Al

re

po

rt

20

11 DANSKE BANK PLC

ANNUAL REPORT 2012

Danske Bank Plc

BoarD of Directors´ rePort ............................................. 3

ifrs financial statements ........................................................... 10

consolidated statement of comprehensive income ... 10

consolidated Balance sheet ........................................................ 11

statement of changes in equity ................................................ 11

cash flow statement ......................................................................... 12

notes to the financial statements .................. 13

summary of significant accounting Policies ................. 13

income statement ................................................................................23

corporate Governance .....................................................................25

risk management ................................................................................29

segment information .........................................................................38

other notes: .....................................................................................40

1 net interest income ................................................................40

2 fee and commission income and expenses .........40

3 net trading income .................................................................40

4 other operating income ...................................................... 41

5 net income from investments ........................................ 41

6 staff costs .....................................................................................41

7 share-based payment ..........................................................41

8 other operating expenses,

depreciations and impairments....................................43

9 audit fees ......................................................................................43

10 loan impairment charges .................................................44

11 taxes ................................................................................................44

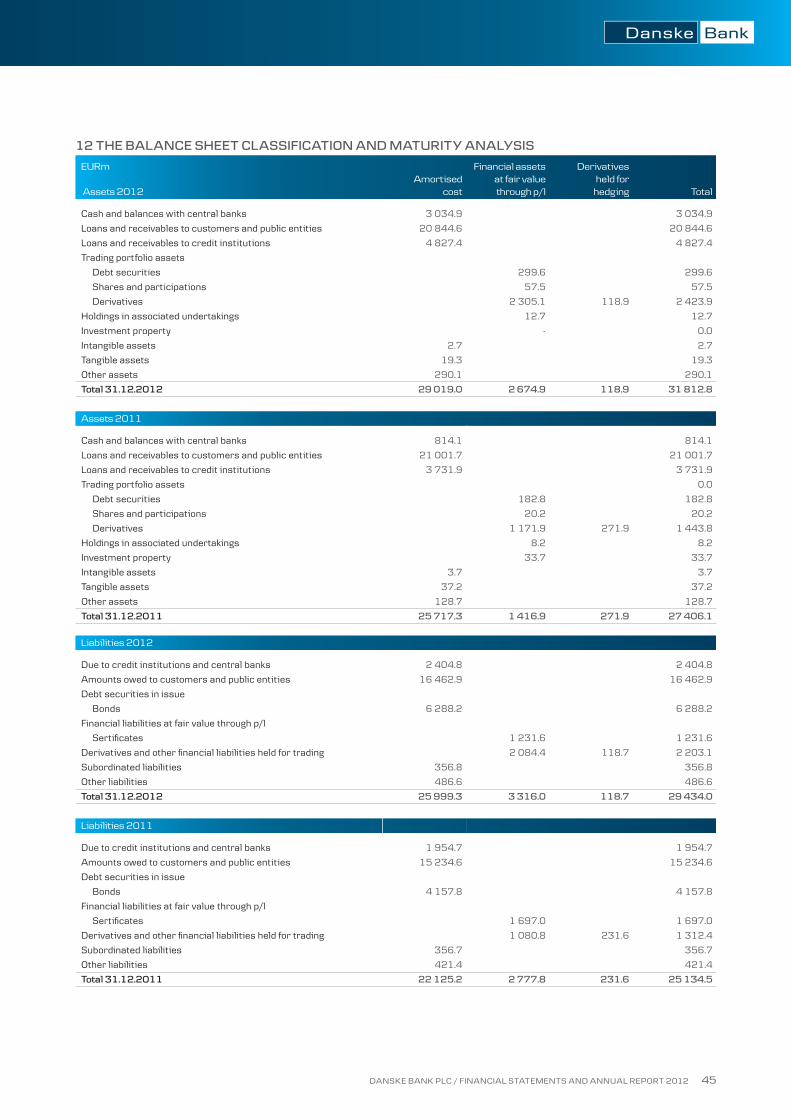

12 Balance sheet classification

and maturity analysis ..........................................................45

13 fair value .......................................................................................47

14 cash and balances at central banks .........................48

15 loans and receivables .........................................................49

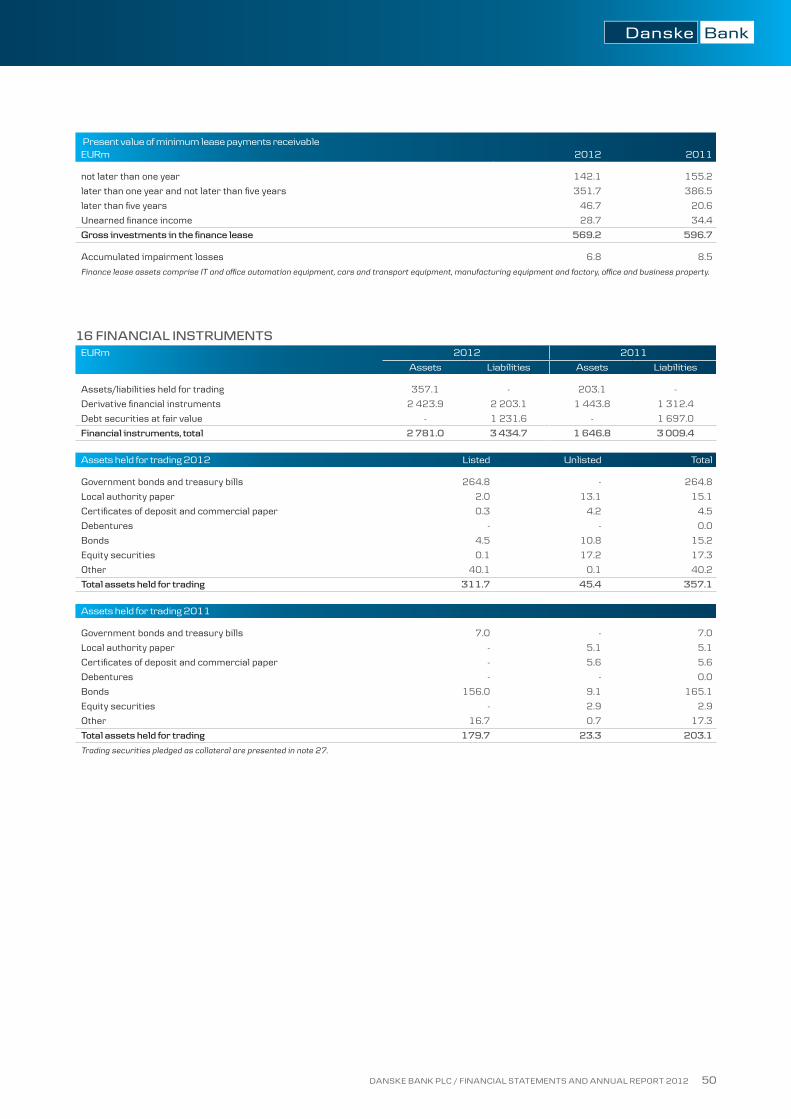

16 financial instruments .........................................................50

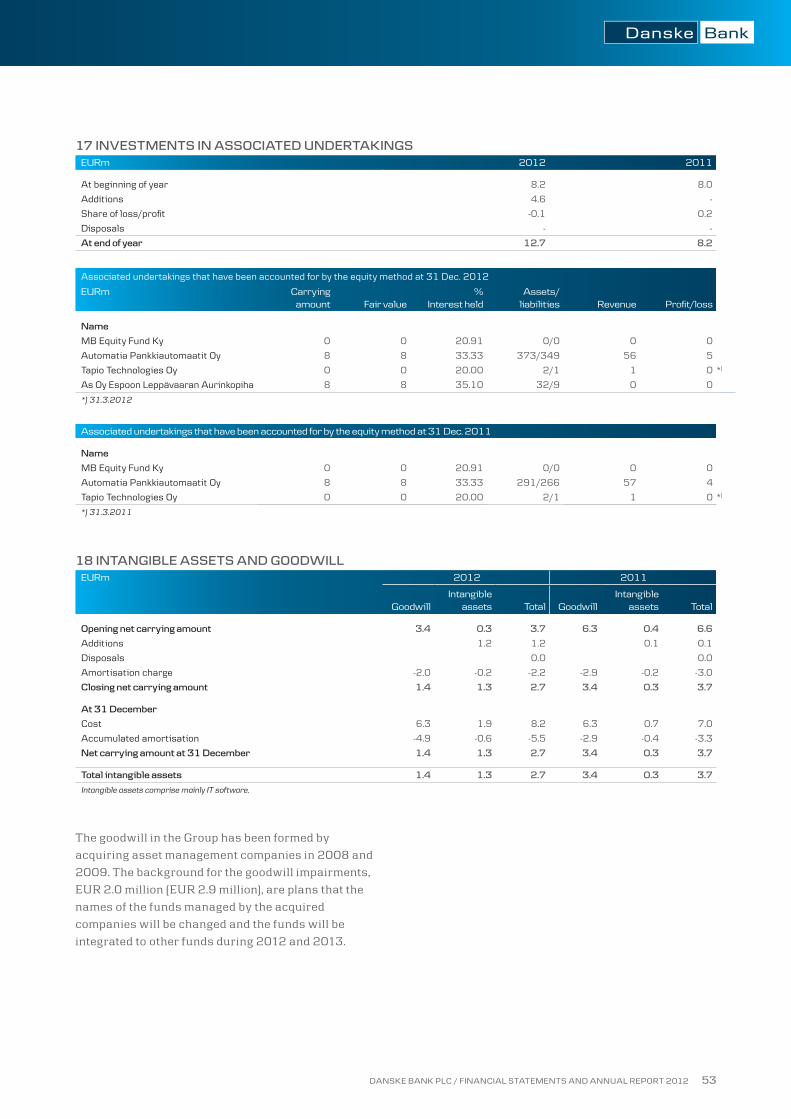

17 investments in associates ................................................53

18 intangible assets and goodwill .....................................53

19 investment property .............................................................54

20 Property, plant and equipment ......................................54

21 other assets ................................................................................55

22 tax assets and liabilities ...................................................55

23 amounts owed to credit institutions

and customers ...........................................................................55

24 Debt securities in issue.......................................................56

25 other liabilities .........................................................................57

26 Provisions ....................................................................................57

27 contingent liabilities and commitments ................57

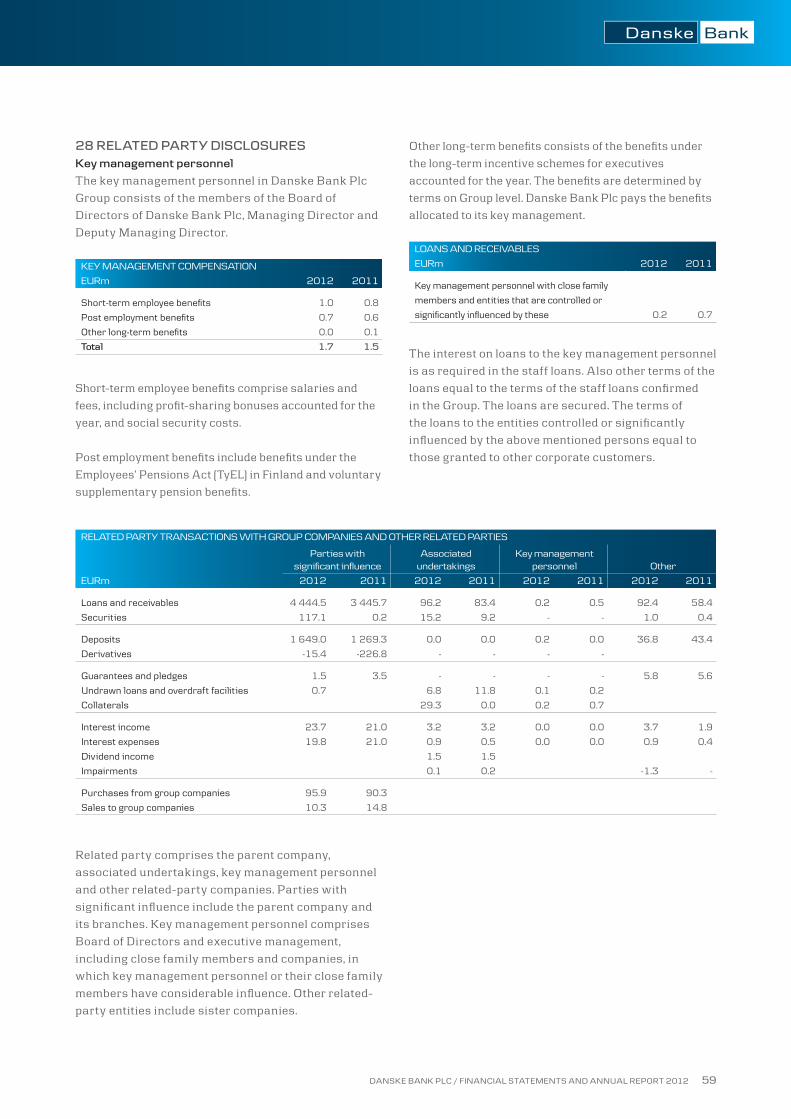

28 related party disclosures .................................................59

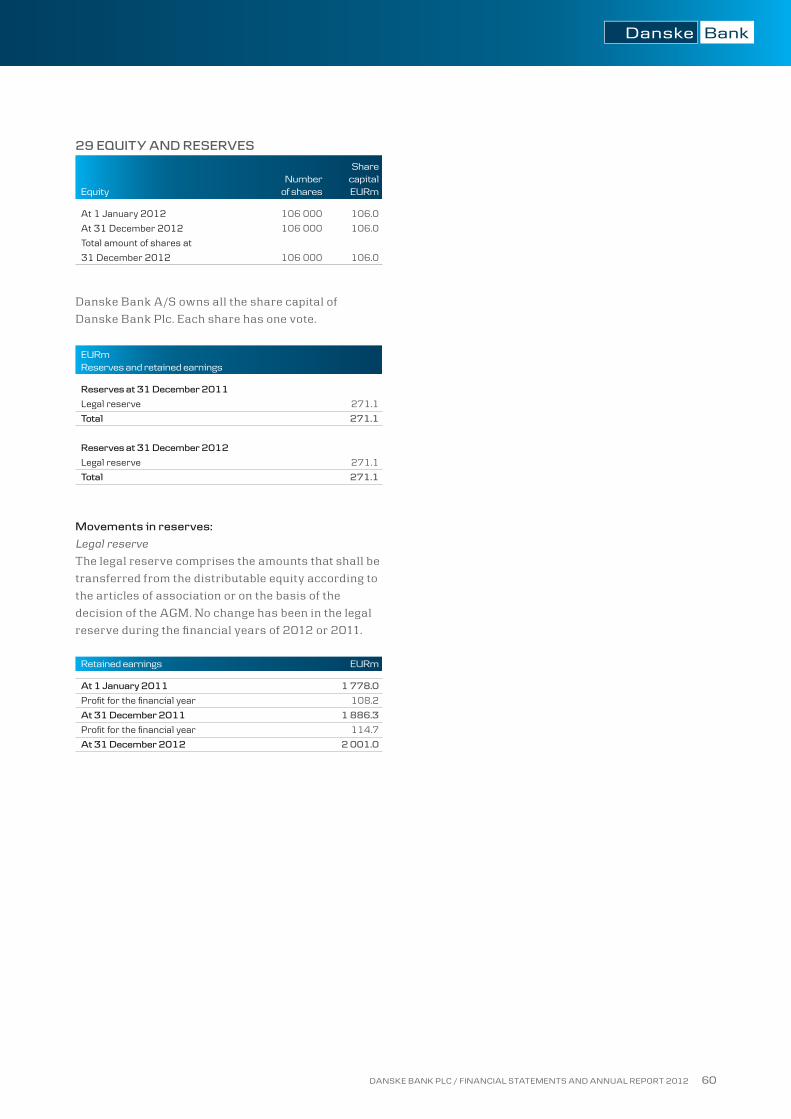

29 equity and reserves ...............................................................60

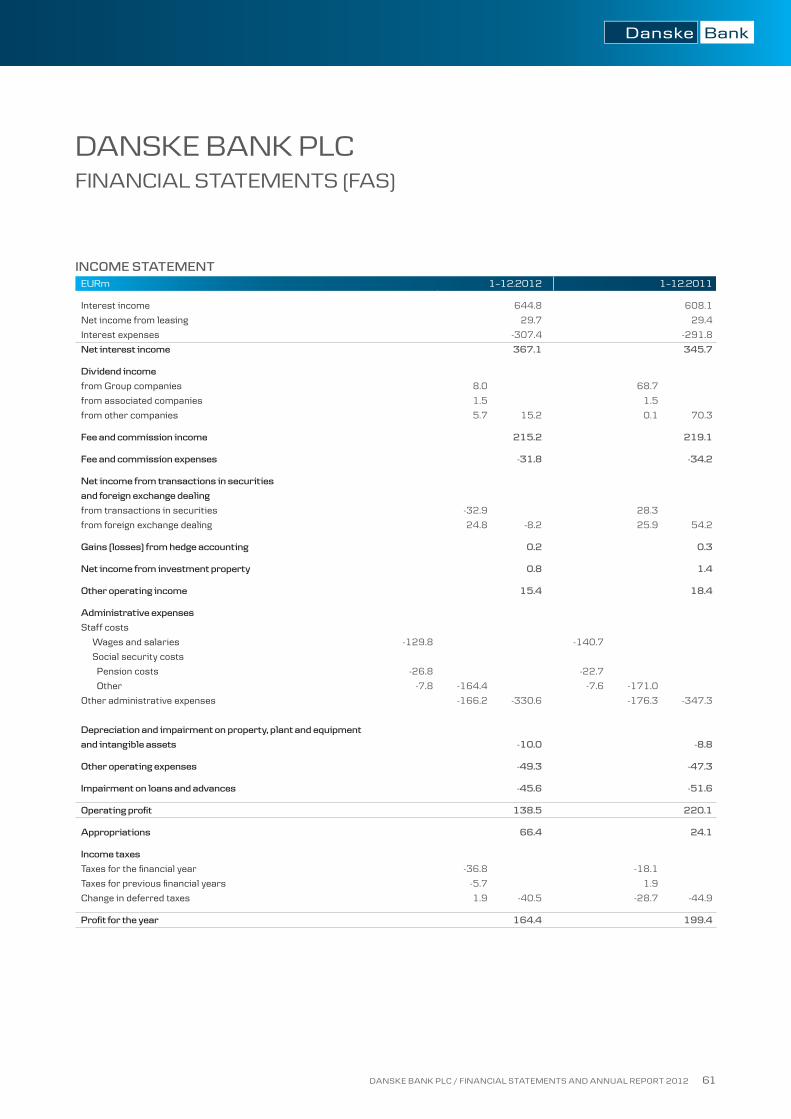

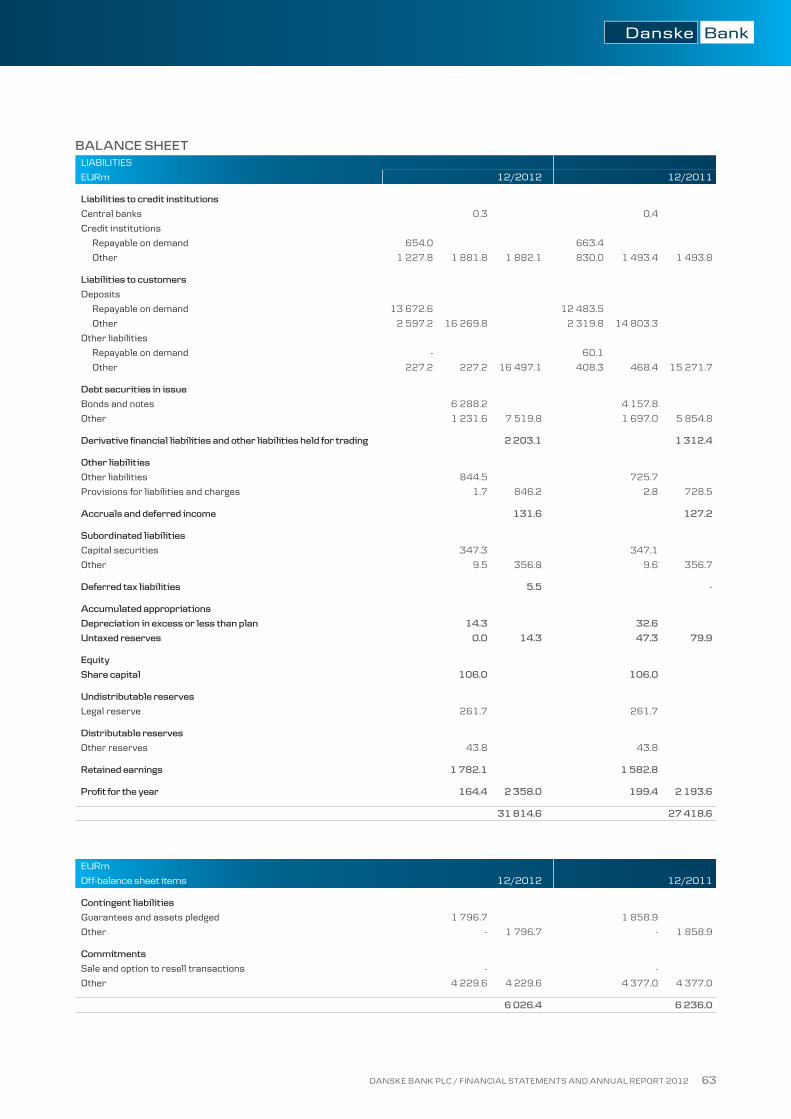

Danske Bank Plc financial statements

(fas)...............................................................................................................61

income statement ................................................................................61

Balance sheet .........................................................................................62

notes to the financial statements ..................64

accounting policies ............................................................................64

other notes to the financial

statements ........................................................................................65

Danske Bank Plc BoarD of Directors´

ProPosal to the annual General meetinG

for the DistriBution of the Profits of the

Parent comPany .........................................................................82

Danske Bank Plc is a Finnish bank which is part of the Danske Bank Group. Danske Bank Group is one of the largest

financial enterprises in the Nordic region. This Annual Report includes Danske Bank Plc and its subsidiaries.

CONTENTS

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 2

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 3

DANSKE BANK PLC BOARD OF DIRECTORS´ REPORT 2012

Changes in the operating environment

World economic growth slowed in 2012. the

international monetary fund estimates that world

growth in 2012 will remain at 3.3 per cent, down from

3.8 per cent in the previous year. europe’s weak

economic situ ation and worries about the endurance

of the euro area were particular causes of uncertainty

for the global economy. Growth was stronger in the

usa than in europe, but the economic outlook became

more cautious also on the other side of the atlantic.

the presidential and congressional elections in

november and the economic tightening measures in

late 2012 caused uncertainty in the us economy. on

the emerging markets, growth was generally clearly

faster than in the western countries, but the growth

rate declined from the previous level. in china, annual

growth fell below the 8 per cent level in the second

and third quarters. in uncertain conditions, price

pressures on raw materials eased, and inflation

remained low in various parts of the world. on the

other hand, unemployment was higher than its natural

level, and the employment trend was downward at the

end of the year.

the poor state of the economy and low inflation led

to exceptional support measures by the european

central Bank (ecB). at the end of December 2011 and

february 2012, the ecB lent nearly eur 1,000 billion

to the european banking sector on favourable terms.

the ecB also lowered its refinancing rate to a record

low level of 0.75 per cent in July. these measures

contributed to the decline of market interest rates, and

the 12-month euribor was at 0.54 per cent at the end

of the year. housing loan interest rates fell to record-

low levels in finland, although credit margins were

raised during the year. housing loan interest rates in

finland were the lowest of the euro states, with the

average interest rate at 1.68 per cent in november.

the interest rates of the most creditworthy states,

such as Germany and finland, remained at historically

low levels. the outcome of Greece’s debt arrangement

was that investors and banks had to record losses in

march. the interest rates of spain and italy rose at the

beginning of the year as investors doubted the

countries’ debt sustainability. it was only after the

ecB President mario Draghi promised in July that the

central bank would do whatever it takes to save the

euro and would, if necessary, buy large quantities of

euro area crisis states’ government bonds that the

markets calmed down, and the interest rates of the

crisis countries fell to a clearly lower level. the crisis

and the lack of confidence raised banks’ refinancing

costs, and in order to secure profitability they sought

to transfer these to customer financing margins.

Banks also tightened credit policy in the euro area.

economic integration in the euro area was deepened,

and in late June, the first steps towards a euro area

bank union were taken when the establishment of a

european bank supervisor and the possibility of direct

assistance to banks from shared european assets

were agreed upon at the eu summit.

finland’s gross domestic product remained near the

previous year’s level in 2012. household consumer

demand partially protected finland against the euro

crisis. Private consumption grew by 2 per cent in

January-september, while exports and imports

contracted by around 1 per cent. however, the outlook

deteriorated towards the end of the year, as the private

consumption peak was not reached, the value of new

industrial orders declined virtually throughout the

year, and the number of granted building permits and

housing starts declined. early in the year, consumer

demand was supported by pay rises in line with a

framework decision and an amendment to vehicle tax

in april, which encouraged households and companies

to focus their consumption on the early part of the

year. the uncertain economic situation was reflected

in the postponement of investments. the economy was

steadied by the moderate house price rise and the low

number of bankruptcies, causing banks’ credit losses

to remain reasonable. the number of corporate

bankruptcies in January-november 2012 remained

on the same level as previous year.

the seasonally adjusted unemployment rate remained

at 7.5 per cent in the early part of the year. in the latter

part of the year, the unemployment rate rose to 8 per

cent. the financial situation of households was

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 4

improved by historically low interest rates. early in the

year, consumer prices were still rising at an annual

rate of over 3 per cent, but in november inflation fell

to 2.2 per cent. the amendments to indirect taxes

carried out during the year raised inflation by nearly

a percentage point. consumer confidence rose early in

the year, but in June, outlooks fell to exceptionally low

levels again. consumers had cautious expectations

regarding their own finances, and their outlooks on

the finnish economy were gloomy.

Revenue performance

total income for the full financial year was near the

2011 level and amounted to eur 637.5 million

(649.8 million). net interest income for the financial

year increased to eur 358.1 million (345.7 million),

an increase of 4 per cent on the previous year. the

performance of market interest rates was visible in both

credit and lending. the Group’s funding costs continued

to grow during the financial year, as expected.

the Group’s net commission income declined by 3 per

cent compared with the same period a year earlier,

and was eur 196.4 million (202.2 million). the net

commission income performance was affected by

one-off commissions from lending recognised in the

corresponding period in 2011, for which there were no

corresponding items in this review period. net income

from transactions in securities and foreign exchange

dealing increased by 4 per cent on the previous year,

to eur 41.6 million (40.1 million). net trading income

also include a positive change in value in the units of

suomen luotto-osuuskunta held by the bank, as the

cooperative sold the entire stock of luottokunta oy

in august 2012. the Group’s other income decreased

by 34 per cent year on year to eur 39.1 million (58.9

million). in the financial statements for 2011, non-

recurring items were recognised in the Group’s other

income for which there were no corresponding items

in this review period.

Banking activities

net revenue from banking decreased by 8.3 per cent

on the previous year to eur 518.1 million (565.3

million). revenue was positively affected by the

increase in net interest income, which was due to

market interest rate movements and their effect on

credit and lending. net commission income from

banking also increased by 2.3%. income performance

was negatively influenced by the development of other

income, where there were a number of non-recurring

income items in the previous financial year but there

were no corresponding income items in the 2012

financial year. the increase in funding costs continued

during the financial year, and as a result, loan pricing

has been tightened. the organisational structure and

business practices of banking were renewed during

the financial year to respond to the market challenges

imposed on banks by low interest rates, lacklustre

economic growth, the increased cost of refinancing,

regulatory changes in the business, and the change in

customer behaviour in the internet and mobile age.

a key aspect of the renewal of business practices is

that the bank will be able to harness all available

channels (branches, financial centres, private bank

units, telephone services and electronic channels) into

a single entity for serving the customer.

When customers are given a chance to choose their

method of banking, they increasingly choose a remote

banking method. this has allowed us to reassess the

bank’s branch network, and we have consequently

been able to reduce the number of branches.

improving the features of the eBank, together with

other efficient channels, has been one of the most

important development areas for a long time, and

Danske Bank currently has 534,000 active eBank

users. Demand for mobile banking services also

continued to grow significantly during the financial

year. investment functions were added to the tablet

Bank. Danske Bank Plc currently has 155,000 mobile

and tablet bank customers.

at the beginning of the year, an iPad version of

investment-themed magazine was launched, and the

navigator asset management strategy was included in

the asset management service package. a total of 26

new investment bonds were also launched on the

market during the financial year. over 6,300 new long-

term savings agreements were made during the year.

Markets

Despite the prolonged uncertainty in the capital

markets, the income of the Danske markets business

was positive and amounted to eur 61.6 million (51.6

million). income and customer activity remained at the

high level attained in the previous year both in fixed

income and foreign currency products. the business

area received positive feedback in a number of

customer satisfaction surveys conducted during the

year and has solidified its market share position

among the top two in several product areas.

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 5

During the financial year, the Danske markets

business area arranged bonds for the finnish

government and for major finnish corporations,

including elisa corporation, metso corporation,

kesko corporation and stockmann plc.

Capital

Despite the cost pressures created by nervy markets

and increasing regulations, the business area’s income

was reasonably good at eur 29.1 million (36.3 million).

Danske capital continued its strong performance in

institutional asset management. according to a

survey by scandinavian financial research, Danske

capital became finland’s preferred institutional asset

manager in 2012 measured in terms of customer

relationships. the ratings for quality of operations

also continued to rise. Danske capital received

excellent marks especially in customer service. the

number of institutional customer relationships rose

substantially in 2012.

Danske invest fund management ltd is the third-

largest fund management company in finland with

a market share of 13.7 per cent. assets under

management were eur 9.1 billion at the end of

December (7.8 billion on 31 December 2011). net

subscriptions by fund management companies

registered in finland were eur 4,635 million in

January-December. in the same period, net

subscriptions by Danske invest fund management

were eur 327 million.

according to a comparison by the global fund analysis

company morningstar, Danske invest had the most

top-rated five-star funds in finland. a total of 19 of

Danske invest’s funds had either the highest (five-star)

or second-highest ranking in the comparison survey

that included 52 of the company’s funds. the average

overall star rating was 3.4.

the Danske invest european small cap fund was

ranked number one in european equity funds

registered in finland, with a return of 30.5 per cent in

2012. Danske invest excelled in emerging market

equity funds, taking first place with the Danske invest

Black sea fund, which returned 61.3% in 2012.

measured in terms of the number of unit holders, the

Danske invest compass 25 fund remained finland’s

most popular balanced fund, with nearly 63,000 unit

holders.

Result and cost structure

the Danske Bank Plc Group’s profit before taxes for

the full financial year was eur 156.8 million (147.3

million). the result was eur 115.3 million (109.8

million). net interest income and the Group’s costs

throughout the year, in particular, had a positive

impact on the result. correspondingly, the increase in

impairment charges and one-off costs had a negative

impact on the result. net impairment on loans and

receivables was eur 63.9 million (53.4 million).

individually assessed impairment charges and final

write-offs totalled eur 63.6 million (68.0 million).

eur 18.9 million (0.3 million) was recorded in

collective impairments, and recoveries came to eur

18.5 million (15.0 million). During the review period

the Group modified the parameters used in the

impairment charge models, following which an

additional one-off entry was made in receivables.

impairment charges and write-offs were mainly from

a few corporate customers.

the Danske Bank Plc Group’s operating expenses

totalled eur 416.7 million (eur 449.0 million),

a decrease of 7.2 per cent (eur 32.4 million) on the

previous year. the consolidated result for the year

was burdened by a number of one-off expenses

– over eur 14 million - from projects associated

with the reorganising of operations and expenses

associated with the Group’s name change. the Group’s

fixed costs in the financial year decreased by 8.1 per

cent year on year.

Balance sheet and funding

the Danske Bank Plc Group’s balance sheet total for

2012 was eur 31,812.8 million (27,406.1 million).

loans and receivables from customers grew by eur

938.4 million to a total of eur 25,672.0 million

(24,733.6 million). Demand for housing loans

continued to be good, and the housing loan portfolio

grew 2.8 per cent on the previous year. Deposits

increased by eur 1,228.4 million to a total of eur

16,462.9 million (15,234.6 million).

the financial and liquidity situation remained good,

and short-term funding performed well during the

year. the continuation of the exceptional market

situation was reflected in the fact that long-term

funding prices remained at a high level. Danske Bank

Plc issued eur 2 billion worth of covered bonds and

eur 47.3 million in other bonds during the year.

capital securities and terms are described in note 24.

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 6

Capital adequacy

Danske Bank Plc applies the standard method (capital

requirement for credit and operational risk) and

regulatory approaches (capital requirement for market

risks) to capital adequacy calculations. the Danske

Bank Plc Group’s capital adequacy ratio was 15.8 per

cent (14.4), which clearly exceeds the regulatory

minimum requirement. the tier 1 capital ratio was

15.8 per cent (14.4). the total capital included in

capital adequacy was eur 2,586.0 million on 31

December 2012 (eur 2,617.3 million). the Group’s

risk weighted assets were eur 16,324.7 million

(18,155.0 million).

at the request of the european Banking authority

(eBa), Danske Bank Plc’s parent company, Danske

Bank a/s, published an updated test of its

SOLVENCY Danske Bank Plc Group Danske Bank Plc

Own funds EURm 31.12.2012 31.12.2011 31.12.2012 31.12.2011

Tier 11) 2 586.0 2 617.3 2 586.7 2 632.8

Share capital 106.0 106.0 106.0 106.0

Legal reserve 271.1 271.1 261.7 261.7

Capital securities 350.0 350.0 350.0 350.0

Distributable capital 2 001.0 1 886.3 2 010.4 1 919.0

Non-controlling interest 0.6 8.2 - -

Intangible assets -2.7 -3.7 -1.4 -3.4

Proposed/actual dividend -140.0 - -140.0 -

Other deductions from Tier 1 -0.1 -0.6 -0.1 -0.6

Tier 2 - - - -

Total capital 2 586.0 2 617.3 2 586.7 2 632.8

Risk-weighted assets (on-balance sheet and off-balance sheet) 16 324.7 18 155.0 16 303.3 16 911.1

Capital requirement (8% of risk-weighted assets) 1 306.0 1 452.4 1 304.3 1 352.9

Credit and counterparty risk 1 196.0 1 345.2 1 197.3 1 248.6

Market risk 22.9 17.2 22.9 17.2

Operational risk 87.1 90.0 84.1 87.1

Solvency ratio, %

- total capital/risk-weighted assets 15.8% 14.4% 15.9% 15.6%

- Tier 1 capital/risk-weighted assets 15.8% 14.4% 15.9% 15.6%

Group capital adequacy ratio has been calculated in accordance with Credit Institutions Act Sect 5:44-48§ and 54-66§. For calculation of credit, market and

operational risk’s risk-weighted assets, Danske Bank Plc Group applies standard method.1) Danske Bank Plc Group Tier 1 includes capital securities 14% (14%). Danske Bank Plc Tier 1 includes capital securities 14% (14%).

capitalisation level in october 2012 that was

calculated in accordance with the methods used in the

2011 stress test. the capital adequacy of the Danske

Bank Group exceeded the level required to pass the

stress test by a clear margin, as was the case in the

previous year.

as a result of the financial crisis, banks’ capital

adequacy requirements are being tightened. the

objective of the tighter regulations is to improve the

quality of banks’ capital, reduce the cyclical nature of

the capital requirement and banks’ indebtedness, and

impose quantitative limits on liquidity risks. the

changes, planned for entry into force during 2013–

2019, are still being drafted and their eventual effects

cannot be assessed with certainty

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 7

Employees and organization

the Group had 2,252 employees (2,501) at the end of

the financial year, which was 249 persons, or 10.0 per

cent, less than at the end of 2011. During the review

period, 16 people transferred from Danske Bank Plc

to the helsinki branch of Danske Bank a/s. of all the

employees, 94.7 per cent were employed in banking

activities, 2.8 per cent in markets and 2.5 per cent in

capital.

Credit ratings

in may 2012 both standard & Poor’s and moody’s

downgraded Danske Bank Plc’s ratings. standard &

Poor’s lowered its counterparty credit ratings to

a-/a-2 (from a/a-1) and changed outlook from

negative to stable. in the course of a major review

of 114 european financial institutions that was

announced on 15 february 2012, moody’s

downgraded Danske Bank Plc’s the long-term

deposit rating to a2 (from (a1) with stable outlook.

the Prime-1 short term rating was affirmed. the

announcements were simultaneous with downgrade

announcements for the parent company Danske Bank

a/s. in november 2012 standard & Poor’s revised its

outlook for the bank rating from stable to positive.

Danske Bank Plc’s Board of Directors and auditors

During the financial year, the members of Danske

Bank Plc’s Board of Directors were thomas f. Borgen

(chairman until 1 June 2012), tonny thierry

andersen (chairman from 1 June 2012), Per Damborg

skovhus (Vice chairman until 1 June 2012), henrik

ramlau-hansen (Vice chairman from 1 June 2012),

niels-ulrik mousten, mikael ericson (until 1 June

2012), Georg schubiger (until 1 June 2012), ilkka

hallavo (from 1 september 2012), esko mäkeläinen

and maija strandberg.

the annual General meeting of Danske Bank Plc

chose kPmG oy ab, a firm of authorised public

accountants, as its auditor, with Petri kettunen, aPa,

as the auditor with principal responsibility.

related party loans and receivables can be found in

note 28 and corporate governance from page 25.

Changes in Danske Bank Plc’s shares, ownership and

group structure

sampo Bank Plc changed its name to Danske Bank Plc

as of november 15th 2012.

the Danske Bank Plc Group is part of the Danske

Bank Group. the parent company of the Danske Bank

Group is Danske Bank a/s. the parent company of the

Danske Bank Plc Group is Danske Bank Plc.

the following were also Danske Bank Plc Group

companies on 31 December 2012: Danske invest fund

management ltd, kiinteistömaailma oy, aurinkopihan

Palvelut oy, mB equity Partners oy and mB

mezzanine funD ii ky. as Danske Bank Plc’s holding

in as. oy espoon leppävaaran aurinkopiha fell below

50 per cent at the end of may 2012, the company is

now presented under associated companies.

Danske Bank Plc’s share capital is eur 106 million,

divided into 106,000 shares. Danske Bank a/s holds

the entire stock of Danske Bank Plc.

Risk management

the main objective of risk management is to ensure

that the capital base is adequate in relation to the risks

arising from the business activities. the Board of

Directors of Danske Bank Plc establishes the

principles of risk management, risk limits and other

general guidelines according to which risk

management is organised at Danske Bank Plc. to

ensure that the bank’s risk management organisation

meets both the external and internal requirements,

the Board of Directors has set up a risk committee,

the main objective of which is to ensure Danske Bank

Plc’s compliance with the risk management guidelines

issued by the Board of Directors and that Danske

Bank Plc monitors all types of risk and provides

reports to the appropriate parties. the Board has also

established an asset and liability committee (alco),

which is responsible for monitoring and directing the

management of structural balance sheet interest rate

risk positions in accordance with Danske Bank Plc’s

policies and delegated limits. alco also determines

the operating target levels for liquidity risk

management and oversees the management of

liquidity risk. the risk management unit monitors

daily business operations together with the finance

department’s market risk team.

in addition to the capital adequacy calculation, risks

in the Danske Bank Plc Group are described and

assessed internally through economic capital

indicators, which describe the amount of capital

needed to bear different kinds of risks. the capital

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 8

requirement is adequately covered by equity, capital

securities and debenture loans. the principal risks

associated with the Danske Bank Plc Group’s

activities are credit risk, interest rate and liquidity

risks of banking book, operational risks and various

business risks.

the Group’s risk position remained at a good level. the

principal risks associated with the Group’s business

operations involve developments in the general

economic operating environment and investment

market and future changes in financial regulations.

in relation to the loan and guarantee portfolio, bad

and doubtful debts were at a low level. the majority of

net write-offs and impairment charges consisted of

customer-specific impairment charges. there was

a decrease in the volume of bad and doubtful debts

in comparison with the previous year, and these

amounted to eur 180.6 million (197.0 million) or 0.79

per cent (0.85) of the loan and guarantee portfolio.

the Danske Bank Plc Group has not invested in the

bonds of GiiPs countries.

a more detailed account of risks and risk management

can be found in the risk management note at page 31.

Events after the reporting period

the Board of Directors of Danske Bank Plc has 28th

of January 2013 decided to transfer its asset finance

business to a subsidiary. Danske finance ltd is

established for the purpose.

Outlook

the weak economic situation in europe is causing

uncertainty in the financial markets. the main risks

from the Bank’s point of view concern the trends in the

global economy and the financial markets. the

unpredictability in the financial markets and the weak

state of the economy are having a negative impact on

the economy in general and consequently on the result

for the Group.

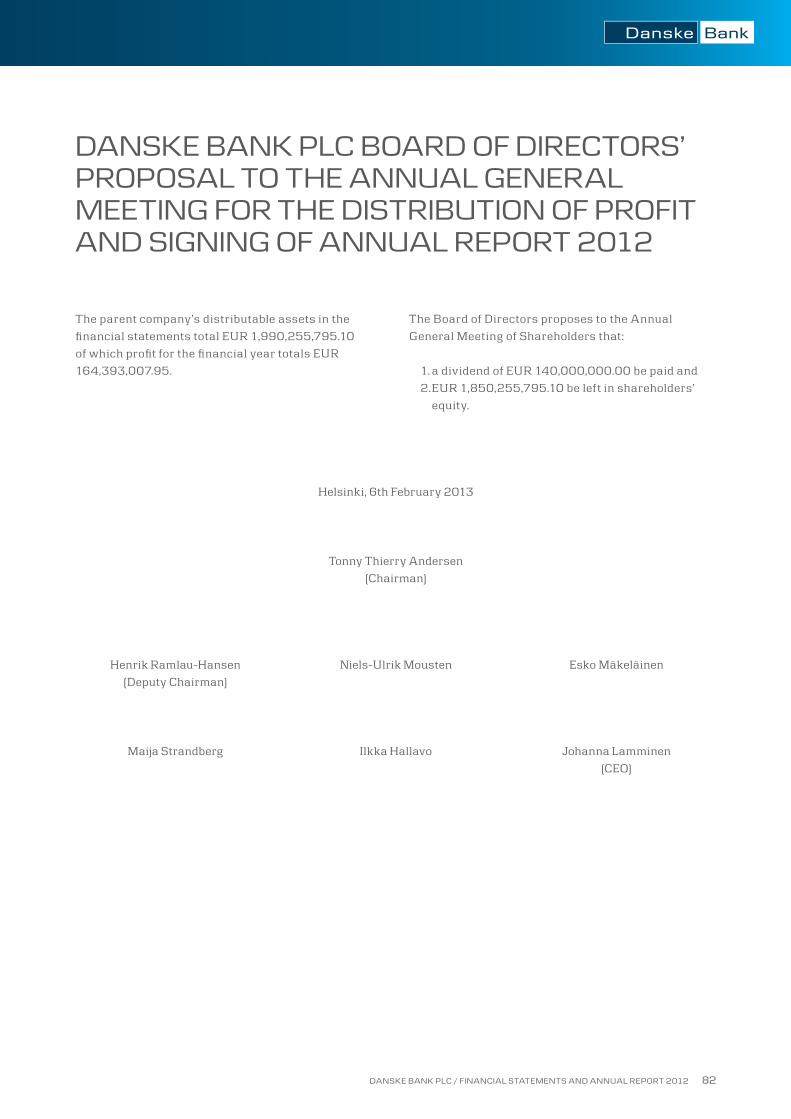

helsinki, 6 february 2013

Danske Bank Plc

Board of Directors

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 9

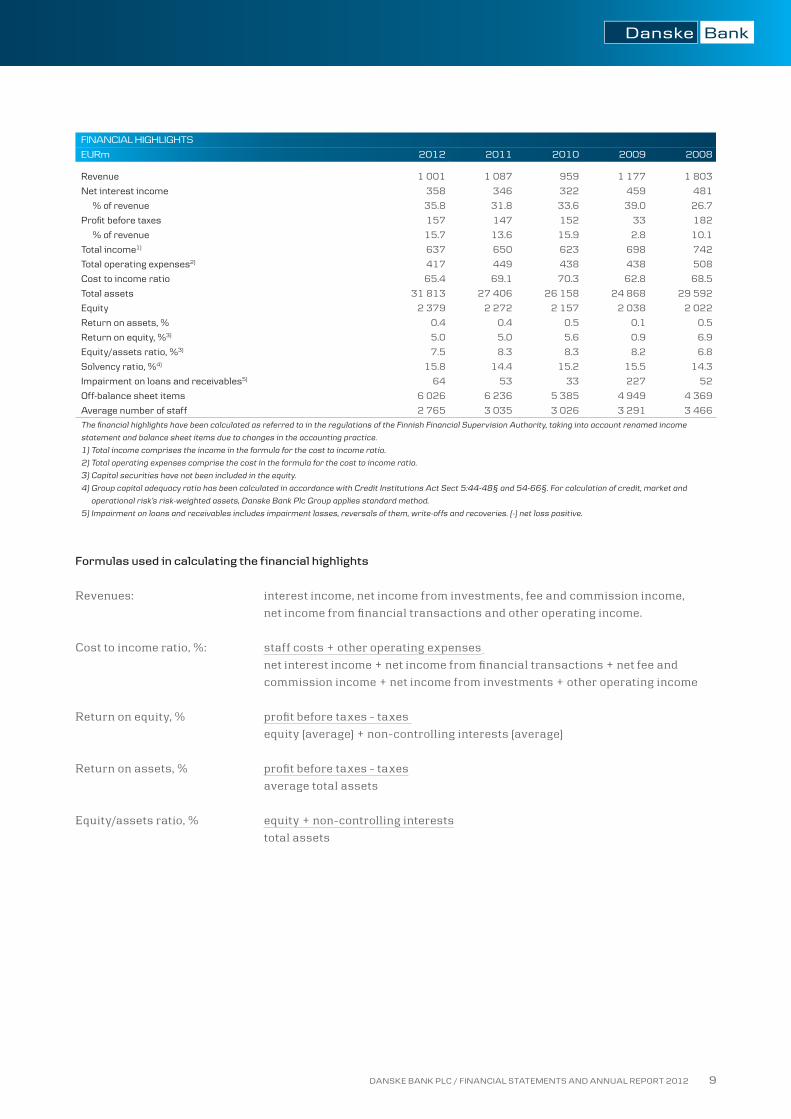

FINANCIAL HIGHLIGHTS

EURm 2012 2011 2010 2009 2008

Revenue 1 001 1 087 959 1 177 1 803

Net interest income 358 346 322 459 481

% of revenue 35.8 31.8 33.6 39.0 26.7

Profit before taxes 157 147 152 33 182

% of revenue 15.7 13.6 15.9 2.8 10.1

Total income1) 637 650 623 698 742

Total operating expenses2) 417 449 438 438 508

Cost to income ratio 65.4 69.1 70.3 62.8 68.5

Total assets 31 813 27 406 26 158 24 868 29 592

Equity 2 379 2 272 2 157 2 038 2 022

Return on assets, % 0.4 0.4 0.5 0.1 0.5

Return on equity, %3) 5.0 5.0 5.6 0.9 6.9

Equity/assets ratio, %3) 7.5 8.3 8.3 8.2 6.8

Solvency ratio, %4) 15.8 14.4 15.2 15.5 14.3

Impairment on loans and receivables5) 64 53 33 227 52

Off-balance sheet items 6 026 6 236 5 385 4 949 4 369

Average number of staff 2 765 3 035 3 026 3 291 3 466

The financial highlights have been calculated as referred to in the regulations of the Finnish Financial Supervision Authority, taking into account renamed income

statement and balance sheet items due to changes in the accounting practice.

1) Total income comprises the income in the formula for the cost to income ratio.

2) Total operating expenses comprise the cost in the formula for the cost to income ratio.

3) Capital securities have not been included in the equity.

4) Group capital adequacy ratio has been calculated in accordance with Credit Institutions Act Sect 5:44-48§ and 54-66§. For calculation of credit, market and

operational risk’s risk-weighted assets, Danske Bank Plc Group applies standard method.

5) Impairment on loans and receivables includes impairment losses, reversals of them, write-offs and recoveries. (-) net loss positive.

Formulas used in calculating the financial highlights

revenues: interest income, net income from investments, fee and commission income,

net income from financial transactions and other operating income.

cost to income ratio, %: staff costs + other operating expenses

net interest income + net income from financial transactions + net fee and

commission income + net income from investments + other operating income

return on equity, % profit before taxes - taxes

equity (average) + non-controlling interests (average)

return on assets, % profit before taxes - taxes

average total assets

equity/assets ratio, % equity + non-controlling interests

total assets

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 10

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

EURm Note 1–12/2012 1–12/2011

Interest income 1 665.2 723.0

Interest expense 1 -307.1 -377.3

Net interest income 358.1 345.7

Fee income 2 252.9 261.7

Fee expenses 2 -56.6 -59.5

Net trading income 3 41.6 40.1

Other operating income 4 39.1 58.9

Net income from investments 5 2.2 2.9

Total operating income 637.5 649.8

Staff costs 6 -169.2 -175.8

Other operating expenses 8 -221.8 -237.2

Depreciations and impairments 8 -25.7 -36.0

Total operating expenses -416.7 -449.0

Loan impairment charges 10 -63.9 -53.4

Profit before taxes 156.8 147.3

Taxes 11 -41.6 -37.5

Total comprehensive income for the year 115.3 109.8

Attributable to

Equity holders of parent company 114.7 108.3

Non-controlling interest 0.6 1.5

IFRS FINANCIAL STATEMENTS

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 11

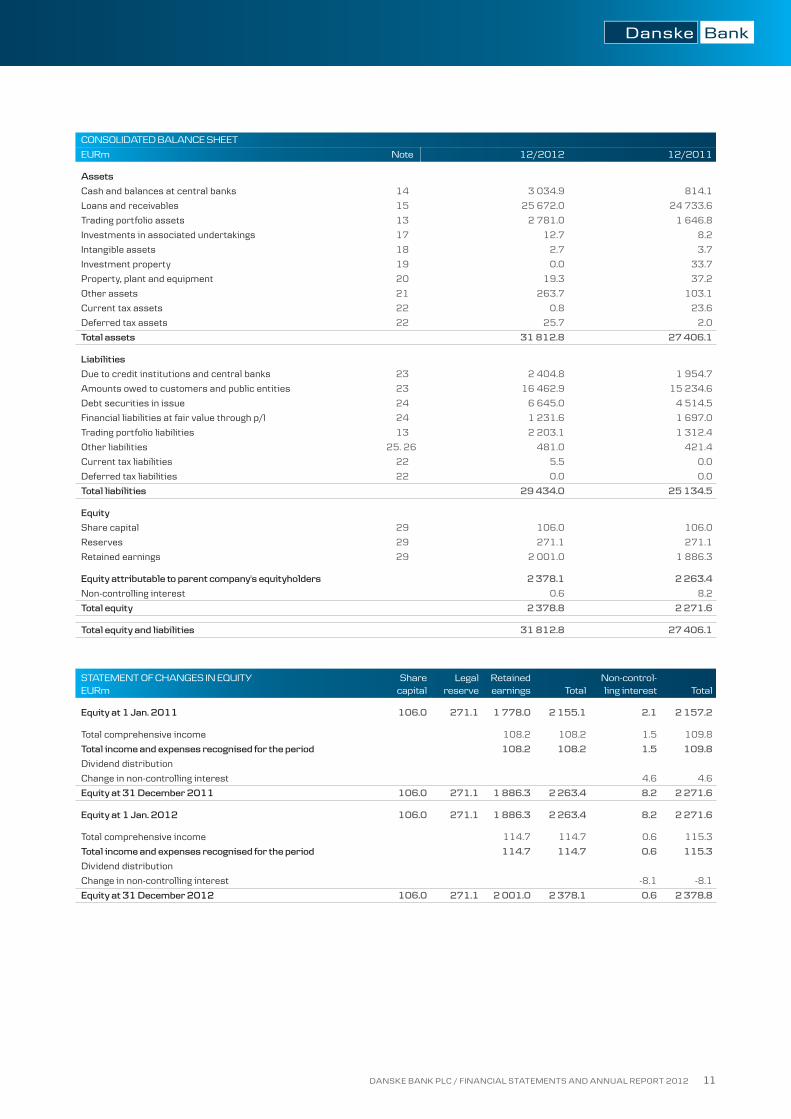

CONSOLIDATED BALANCE SHEET

EURm Note 12/2012 12/2011

Assets

Cash and balances at central banks 14 3 034.9 814.1

Loans and receivables 15 25 672.0 24 733.6

Trading portfolio assets 13 2 781.0 1 646.8

Investments in associated undertakings 17 12.7 8.2

Intangible assets 18 2.7 3.7

Investment property 19 0.0 33.7

Property, plant and equipment 20 19.3 37.2

Other assets 21 263.7 103.1

Current tax assets 22 0.8 23.6

Deferred tax assets 22 25.7 2.0

Total assets 31 812.8 27 406.1

Liabilities

Due to credit institutions and central banks 23 2 404.8 1 954.7

Amounts owed to customers and public entities 23 16 462.9 15 234.6

Debt securities in issue 24 6 645.0 4 514.5

Financial liabilities at fair value through p/l 24 1 231.6 1 697.0

Trading portfolio liabilities 13 2 203.1 1 312.4

Other liabilities 25. 26 481.0 421.4

Current tax liabilities 22 5.5 0.0

Deferred tax liabilities 22 0.0 0.0

Total liabilities 29 434.0 25 134.5

Equity

Share capital 29 106.0 106.0

Reserves 29 271.1 271.1

Retained earnings 29 2 001.0 1 886.3

Equity attributable to parent company's equityholders 2 378.1 2 263.4

Non-controlling interest 0.6 8.2

Total equity 2 378.8 2 271.6

Total equity and liabilities 31 812.8 27 406.1

STATEMENT OF CHANGES IN EQUITYEURm

Share capital

Legal reserve

Retained earnings Total

Non-control-ling interest Total

Equity at 1 Jan. 2011 106.0 271.1 1 778.0 2 155.1 2.1 2 157.2

Total comprehensive income 108.2 108.2 1.5 109.8

Total income and expenses recognised for the period 108.2 108.2 1.5 109.8

Dividend distribution

Change in non-controlling interest 4.6 4.6

Equity at 31 December 2011 106.0 271.1 1 886.3 2 263.4 8.2 2 271.6

Equity at 1 Jan. 2012 106.0 271.1 1 886.3 2 263.4 8.2 2 271.6

Total comprehensive income 114.7 114.7 0.6 115.3

Total income and expenses recognised for the period 114.7 114.7 0.6 115.3

Dividend distribution

Change in non-controlling interest -8.1 -8.1

Equity at 31 December 2012 106.0 271.1 2 001.0 2 378.1 0.6 2 378.8

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 12

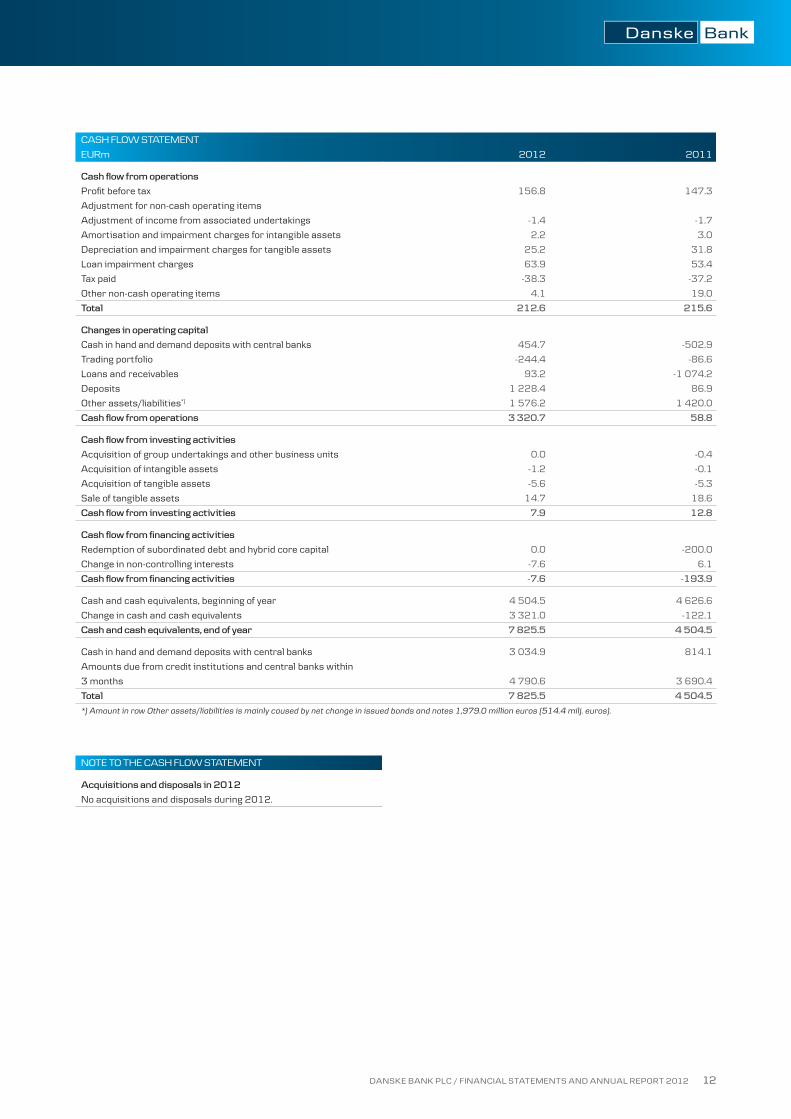

CASH FLOW STATEMENT

EURm 2012 2011

Cash flow from operations

Profit before tax 156.8 147.3

Adjustment for non-cash operating items

Adjustment of income from associated undertakings -1.4 -1.7

Amortisation and impairment charges for intangible assets 2.2 3.0

Depreciation and impairment charges for tangible assets 25.2 31.8

Loan impairment charges 63.9 53.4

Tax paid -38.3 -37.2

Other non-cash operating items 4.1 19.0

Total 212.6 215.6

Changes in operating capital

Cash in hand and demand deposits with central banks 454.7 -502.9

Trading portfolio -244.4 -86.6

Loans and receivables 93.2 -1 074.2

Deposits 1 228.4 86.9

Other assets/liabilities*) 1 576.2 1 420.0

Cash flow from operations 3 320.7 58.8

Cash flow from investing activities

Acquisition of group undertakings and other business units 0.0 -0.4

Acquisition of intangible assets -1.2 -0.1

Acquisition of tangible assets -5.6 -5.3

Sale of tangible assets 14.7 18.6

Cash flow from investing activities 7.9 12.8

Cash flow from financing activities

Redemption of subordinated debt and hybrid core capital 0.0 -200.0

Change in non-controlling interests -7.6 6.1

Cash flow from financing activities -7.6 -193.9

Cash and cash equivalents, beginning of year 4 504.5 4 626.6

Change in cash and cash equivalents 3 321.0 -122.1

Cash and cash equivalents, end of year 7 825.5 4 504.5

Cash in hand and demand deposits with central banks 3 034.9 814.1

Amounts due from credit institutions and central banks within

3 months 4 790.6 3 690.4

Total 7 825.5 4 504.5

*) Amount in row Other assets/liabilities is mainly caused by net change in issued bonds and notes 1,979.0 million euros (514.4 milj. euros).

NOTE TO THE CASH FLOW STATEMENT

Acquisitions and disposals in 2012

No acquisitions and disposals during 2012.

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 13

DANSKE BANK PLC GROUPNOTES TO THE FINANCIAL STATEMENTS

ACCOunTing PRinCiPLEsgroup in brief

Danske Bank Plc Group is part of the Danske Bank

Group, which is one of the largest financial enterprise

in the nordic region. Danske Bank Group operates in

15 countries and has more than five million private

customers. the Group is headquartered in

copenhagen and Danske Bank’s share is quoted on

the copenhagen stock exchange.

Danske Bank Plc has more than 1.1 million personal

customers and about 90,000 corporate and

institutional customers in finland. at the moment

Danske Bank Plc has 93 branches.

signiFiCAnT ACCOunTing POLiCiEsgeneral

Danske Bank Plc Group presents its consolidated

financial statements in accordance with the

international financial reporting standards (ifrss),

issued by the international accounting standards

Board (iasB) and ifric interpretations issued by

ifrs interpretations committee, as endorsed by the

eu. certain additional requirements in accordance

with finnish accounting act, finnish act on credit

institutions and finnish financial supervision

standards have also been applied. Danske Bank Plc

Group has not changed its significant accounting

policies from those followed in annual report 2011.

the consolidated financial statements are presented

in euro (eur), in million euros with one decimal,

unless otherwise stated. figures in notes are rounded

so combined individual figures might differ from the

presented total amount.

standards and interpretations not yet in force

the iasB has issued a number of amendments to

international financial reporting standards that have

not yet come into force. similarly, the ifric has issued

a new interpretation that has not yet come into force.

the paragraphs below list the standards and inter-

pretations that are likely to affect the Group’s financial

reporting.

in october 2010, the iasB amended ifrs 9, financial

instruments. this version is the first part of a standard

expected to replace the requirements of ias 39 in

2012. the amended ifrs 9 now includes principles on

classification and derecognition of financial

instruments. Principles for impairment and hedge

accounting are expected to follow in 2013 or later.

the transitional rules adopted in the amended ifrs 9

imply implementation of the standard by 2015. the eu

has decided to postpone adoption of the amended ifrs

9 until the details of the entire standard are known.

under ifrs 9, financial assets are classified on the

basis of the business model adopted for managing the

assets and on the basis of their contractual cash flow

characteristics, including any embedded derivatives

(unlike ias 39, ifrs 9 no longer requires bifurcation).

assets held with the objective of collecting contractual

cash flows that are solely payments of principal and

interest on the principal amount outstanding are

measured at amortised cost. other assets are

measured at fair value through profit or loss.

the principles applicable to financial liabilities are

largely unchanged from ias 39. Generally, financial

liabilities are still measured at amortised cost with

bifurcation of embedded derivatives not closely

related to a host contract. financial liabilities

measured at fair value comprise derivatives, the

trading portfolio and liabilities designated at fair value

through profit or loss. however, value adjustments

relating to the inherent credit risk of financial

liabilities designated at fair value are recognised

in other comprehensive income unless this leads

to an accounting mismatch.

ifrs 9 incorporates the existing derecognition

principles of ias 39.

meaningful classification of financial instruments

is not possible without information about the future

parts of ifrs 9 to clarify the overall accounting

effects of the standard.

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 14

the iasB ended its project on consolidation in

may 2011 by issuing a number of new international

financial reporting standards (ifrs 10, ifrs 11 and

ifrs 12) and revised standards (ias 27 and ias 28).

With these standards the iasB establishes a uniform

definition of control to be used for determining

whether an entity should be consolidated and

introduces enhanced disclosure requirements for

consolidated and unconsolidated entities, joint

arrangements and associated undertakings.

Danske Bank Plc Group will adopt the standard

form 1 January 2014 in accordance with the eu’s

postponement of the effective date by one year.

the Group does not expect the new requirements to

significantly change its consolidation of undertakings.

in may 2011, the iasB issued ifrs 13, fair Value

measurement. the standard introduces a new

definition of fair value and provides guidance on how

to measure and disclose fair value. ifrs 13 applies

when another standard requires fair value to be used

or *disclosed. the standard was adopted from 1

January 2013. adoption did not result any significant

effect on the Group’s financial results.

in June 2011, the iasB issued an amended ias 19,

employee Benefits. the amended standard eliminates

the option to defer the recognition of actuarial gains

and losses on defined benefit pension plans, known as

the “corridor method”. the present value of net pension

assets and obligations must be recognised in the

balance sheet instead. the Group will adopt the

standard from the beginning of 2013, but this

standard will not affect its present financial results.

in December 2011, the iasB clarified the ias 32

requirements for offsetting financial instruments.

the clarification is not expected to change the

offsetting of financial instruments to any significant

degree. the iasB also enhanced its ifrs 7 disclosure

requirements to include both gross and net amounts

when offsetting financial instruments and rights to

additional set-off in the event of counterparty default.

the changes, which have not yet been adopted by

the eu, must be implemented in 2014 and 2013,

respectively.

COnsOLiDATiOnsubsidiaries

the consolidated financial statements cover Danske

Bank Plc and group undertakings in which the Group

has control over financial and operating policy

decisions. control is said to exist if Danske Bank Plc

directly or indirectly holds more than half of the voting

rights in an undertaking or otherwise has power to

control management and operating policy decisions,

provided that most of the return on the undertaking

accrues to the Group and that the Group assumes most

of the risk. operating policy control may be exercised

through agreements about the undertaking’s activities.

Potential voting rights that are exercisable on the

balance sheet date are included in the assessment of

whether Danske Bank Plc controls an undertaking.

the consolidated financial statements are prepared by

consolidating items of the same nature and

eliminating intra-group transactions, balances and

trading profits and losses.

undertakings acquired are included in the accounts

at the time of acquisition. the net assets of such

undertakings (assets including identifiable intangible

assets, less liabilities and contingent liabilities) are

included in the financial statements at fair value on

the date of acquisition according to the acquisition

method.

if the cost of acquisition (including direct transaction

costs until 1 January 2010) exceeds the fair value of

the net assets acquired, the excess amount is

recognised as goodwill. Goodwill is recognised in the

functional currency of the undertaking acquired. if the

fair value of the net assets exceeds the cost of

acquisition (negative goodwill), the excess amount is

recognised as income at the date of acquisition. the

portion of the acquisition that is attributable to non-

controlling interests does not include goodwill.

Divested undertakings are included in the accounts

until the transfer date.

Associated undertakings

associated undertakings are businesses, other than

subsidiaries, in which the Group has holdings and

significant influence but not control. the Group

generally classifies undertakings as associated

undertakings if Danske Bank Plc, directly or

indirectly, holds 20-50% of the share capital and

has influence over management and operating

policy decisions.

holdings are recognised at cost at the date of

acquisition and are subsequently measured according

to the equity method. the proportionate share of the

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 15

net profit and loss of the individual undertaking is

included under net income from investments.

the proportionate share of the profit and loss on

transactions between associated undertakings and

group undertakings is eliminated.

list of subsidiaries and associated undertakings

included in the consolidated annual report can be

found from page 81.

segment reporting

the Group consists of a number of business units and

resource and support functions. the business units

are segmented according to organizational structure.

inter-segment transactions are settled on an arm’s-

length basis. expenses incurred centrally, including

expenses incurred by support, administrative and

back-office functions, are charged to the business

units according to consumption and activity at

calculated unit prices or market prices, if available.

segment assets and liabilities are assets and

liabilities that are used for maintaining the operating

activities of a segment or have come into existence as

a result of such activities and that are either directly

attributable or may be reasonably allocated to a

segment. a calculated share of shareholders’ equity is

allocated to each segment. other assets and liabilities

are recognised in the other activities segment.

liquidity expenses are allocated on the basis of a

maturity analysis of loans and deposits. Prices are

based on interbank rates and funding spreads.

Offsetting

assets and liabilities are netted when the Group has

a legally enforceable right to set off recognised

amounts and intends either to settle the balance

on a net basis or to realise the asset and settle the

liability simultaneously.

Translation of transactions in foreign currency

the presentation currency of the consolidated

financial statements is euro which is also the

functional currency. monetary assets and liabilities in

foreign currency are translated at the exchange rates

at the balance sheet date. exchange rate adjustments

of monetary assets and liabilities arising as a result of

differences in the exchange rates at the transaction

date and at the balance sheet date are recognised in

the income statement.

transactions in foreign currency are translated at the

exchange rate of the unit’s functional currency at the

transaction date. Gains and losses on exchange rate

differences between the transaction date and the

settlement date are recognised in the income

statement. non-monetary assets and liabilities in

foreign currency that are subsequently revalued at fair

value are translated at the exchange rates at the date of

revaluation. exchange rate adjustments are included in

the fair value adjustment of an asset or liability. other

non-monetary items in foreign currency are translated

at the exchange rates at the transaction date.

Critical accounting policies and estimates

management’s judgment, estimates and assumptions of

future events that will significantly affect the carrying

amounts of assets and liabilities underlie the preparation

of the Group’s consolidated financial statements.

the estimates and assumptions that are deemed

critical to the consolidated financial statements are

• t hefairvaluemeasurementoffinancial

instruments

• t hemeasurementofloansandadvances

• t hemeasurementofgoodw ill

• t herecognit ionofdeferredtaxassets

the estimates and assumptions are based on

premises that management finds reasonable but are

inherently uncertain and unpredictable. the premises

may be incomplete, unexpected future events or

situations may occur, and other parties may arrive at

other estimated values.

Fair value measurement of financial instruments

measurements of financial instruments based on

prices quoted in an active market or based on

generally accepted models employing observable

market data are not subject to critical estimates.

measurements of financial instruments that are only

to a limited extent based on observable market data,

such as unlisted shares and certain bonds for which

there is no active market, are subject to estimates.

the estimated fair value of illiquid bonds significantly

depends on the estimated current credit spread.

Measurement of loans and advances

the Group makes impairment charges to account for

any impairment of loans and advances that occurs after

initial recognition. impairment charges consist of

individual and collective charges and rely on a number

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 16

of estimates, including identification of loans or

portfolios of loans with objective evidence of

impairment, expected future cash flows and the

value of collateral. the Group determines the need for

impairment charges on the basis of customers’ expected

ability to repay their debts. their ability depends on a

number of factors, including the customers’ earnings

capacity and trends in general economic growth and

unemployment. expectations of deteriorating repayment

ability reduce credit quality and lead to downgrading of

customers. the extent of losses incurred under non-

performing loan agreements depends, among other

factors, on the value of collateral provided.

Measurement of goodwill

Goodwill on acquisition is tested for impairment once

a year or more frequently if indications of impairment

exist. impairment testing requires management to

estimate future cash flows from acquired units.

a number of factors affect the value of such cash

flows, including discount rates.

Recognition of deferred tax assets

Deferred tax assets arising from unused tax losses

are recognised to the extent that such losses can be

offset against tax on future profit. recognition of

deferred tax assets requires management to assess

the probability and amount of future taxable profit at

units with unused tax losses

Classification and recognition of financial

instruments in balance sheet

Purchases and sales of financial instruments are

measured at fair value at the settlement date.

Classification

at initial recognition, a financial asset is assigned to

one of the following two categories:

• t radingport foliomeasuredatfairvaluet hrough

profit and loss

• loansandadvancesmeasuredatamort isedcost

at initial recognition, a financial liability is assigned to

one of the following three categories:

• t radingport foliomeasuredatfairvaluet hrough

profit and loss

• financialliabilit iesdesignatedatfairvalue

through profit or loss

• ot herfinancialliabilit iesmeasuredatamort ised

cost

Recognition

the purchase and sale of financial assets and

liabilities at fair value through profit or loss are

recognised in the balance sheet on the settlement

date, or the date on which the Group agrees to buy or

sell the asset or liability in question. loans granted

are recognised as financial assets on the date on

which the customer draws the loan and other

receivables on the trans action date.

Derivative instruments, quoted securities and foreign

exchange spot transactions are recognized on and

derecognized from the balance sheet on the

settlement date.

financial assets and liabilities are offset and the

net amount reported in balance sheet only if there

is a legally enforceable right to offset the recognised

amounts and there is an intention to settle on a net

basis.

financial assets are derecognised when the

contractual right to receive cash flows from the

financial assets has expired or the Group has

transferred all risks and rewards of ownership.

financial liabilities are derecognised when they are

extinguished, i.e. when the obligation is discharged,

cancels or expires.

transaction costs are included in the initial carrying

amount, unless the item is measured at fair value

through the profit and loss.

Due from credit institutions and central banks

amounts due from credit institutions and central banks

comprise amounts due from other credit institutions

and term deposits with central banks. reverse

transactions (purchases of securities from credit

institutions and central banks that the Group agrees

to resell at a later date) are recognised as amounts

due from credit institutions and central banks.

amounts due from credit institutions and central

banks are measured at amortised cost as described

under loans and advances at amortised cost.

Trading portfolio (assets and liabilities)

the trading portfolio includes financial assets and

liabilities acquired or undertaken by the Group for sale

or repurchase in the near term. the trading portfolio

also contains collectively managed financial assets

and liabilities for which a pattern of short-term profit

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 17

taking exists. Derivatives, including bifurcated

embedded derivatives, form part of the trading

portfolio.

the trading portfolio is measured at fair value through

profit and loss. realised and unrealised capital gains

and losses and dividends are carried in the income

statement under net trading income.

Fair value option – financial liabilities designated as at

fair value through profit and loss

financial liabilities at fair value through profit and loss

includes issued certificates of deposits.

financial liabilities at fair value through profit and loss

are measured at fair value. interest income and

expenses on financial instruments carried at fair

value are presented in net interest income, realised

and unrealised capital gains and losses are included

in net trading income.

Hedge accounting

the Group uses derivatives to hedge the interest rate

risk on fixed-rate assets and fixed-rate liabilities

measured at amortised cost. hedged risks that meet

specific criteria qualify for fair value hedge accounting

and are treated accordingly. the interest rate risk on

the hedged assets and liabilities is measured at fair

value through profit or loss.

if the hedge criteria cease to be met, the accumulated

value adjustments of the hedged items are amortised

over the term to maturity.

Loans and advances at amortised cost

loans and advances consists of loans and advances

disbursed directly to borrowers and loans and

advances acquired after disbursement. loans and

advances extended or acquired by the Group for

resale in the near term are included in the trading

portfolio. loans and advances includes conventional

bank loans, finance leases and reverse transactions,

except for transactions with credit institutions and

central banks.

at initial recognition, loans and advances are

measured at fair value plus transaction costs.

subsequently, they are measured at amortised cost,

according to the effective interest method, less any

impairment charges. the difference between the value

at initial recognition and the redemption value is

amortised over the term to maturity and recognised

under interest income. if fixed-rate loans and

advances and amounts due are accounted for under

hedge accounting that is determined effective, the fair

value of the hedged interest rate risk is added to the

amortised cost of the assets.

impairment

if objective evidence of impairment of a loan, an

advance or an amount due exists, and the effect of

the impairment event or events on the expected cash

flow from the loan is reliably measurable, the Group

determines the impairment charge individually.

significant loans, advances and amounts due are

tested individually for impairment at the end of each

reporting period.

objective evidence of impairment of loans and

advances exists if at least one of the following events

has occurred:

• Theborrowerisexperiencingsignificantfinancial

difficulties

• Theborrower’sact ions,suchasdefaultor

delinquency in interest or principal payments, lead

to a breach of contract

• TheGroup,forareasonsrelat ingtot heborrower’s

financial difficulty, grants to the borrower a

concession that the Group would not otherwise

grant

• Itbecomesprobablet hatt heborrowerw illenter

bankruptcy or other financial restructuring

the impairment charge equals the difference between

the carrying amount of the loan and the present value

of the most likely future cash flows from the loan and is

assessed by credit officers. the present value of fixed-

rate loans and advances is calculated at the original

effective interest rate, whereas the present value of

loans and advances with a variable rate of interest is

calculated at the current effective interest rate.

the customer’s debt is written down to the amount

that the borrower is expected to be able to repay after

a financial restructuring. if financial restructuring is

not possible, the write-down equals the estimated

recoverable amount in the event of bankruptcy. if the

borrower’s ability to repay depends significantly on

the assets that have been provided as collateral (asset

financing), the customer’s debt is written down to the

fair value of the collateral.

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 18

loans and advances without objective evidence of

impairment are included in an assessment of

collective impairment at portfolio level. collective

impairment is calculated for portfolios of loans and

advances with similar credit characteristics when

impairment of expected future cash flows from a

portfolio has occurred. the collective impairment

charge reflects downgrading of customer ratings over

time (migration). the loans and advances are divided

into portfolios on the basis of current ratings.

calculation of charges also factors in loan portfolios

for customers with upgraded ratings.

the cash flows are specified by means of parameters

used for solvency calculations and historical loss

data adjusted for use in the financial statements,

for example. the adjustment reflects the loss

identification period shown by the Group’s empirical

data. this period is the period from the first evidence

of impairment to the determination of a loss at

customer level.

collective impairment is calculated as the difference

between the carrying amount of the loans and

advances of the portfolio and the present value of

expected future cash flows.

the collective impairment charge based on migration

is adjusted if the Group is aware of market conditions

at the balance sheet date that are not fully reflected in

the Group’s models. in times of favourable economic

conditions, adjustments will reduce the impairment

charge, while it may increase in an economic

downturn. examples of such market conditions are

levels of unemployment and housing prices.

impairment charges for loans, advances and

guarantees are booked in an allowance account and

set off against loans and advances or recognised as

provisions for guarantees. impairment charges for

loans and advances are recorded under loan

impairment charges in the income statement. if

subsequent events show that impairment is not

permanent, charges are reversed.

loans and advances that are considered uncollectible

are written off. Write-offs are debited to the allowance

account. loans and advances are written off once the

usual collection procedure has been completed and

the loss on the individual loan or advance can be

calculated. if the full loss is not expected to be realised

until after a number of years, for example in the event

of administration of complex estates, a partial write-

off is recognised, reflecting the Group’s claim less

collateral, estimated dividend and other cash flows.

in accordance with the effective interest method,

interest is recognised on the basis of the value of

the loans and advances less impairment charges.

consequently, part of the allowance account balance

is set aside for future interest income until the time

of write-off.

Leases

Group as a lessor

leases in which assets are leased out and

substantially all the risks and rewards of ownership

are transferred to the lessee are classified as finance

leases. finance leases are recognised as receivables

in the balance sheet at an amount equal to the net

investment in the leases. the lease payment is

allocated between the repayment of principal and

interest income. the interest income is amortised over

the lease period so as to achieve a constant periodic

rate of return on the remaining net investment for the

lease term. finance leases are included in loans and

receivables and interest in interest income.

leases in which assets are leased out and the Group

retains substantially all the risks and rewards of

ownership are classified as operating leases. these

rented assets are included in Property, plant and

equipment in the balance sheet. they are depreciated

over their expected useful lives on the basis consistent

with similar owned property, plant and equipment, and

thy impairment losses are recognised on the same

basis as for these items. rental income on assets held

as operating leases is recognised on a straight-line

basis over the lease term in profit and loss.

Group as a lessee

leases of assets in which substantially all the risks

and rewards of ownership are transferred to the

Group are classified as finance leases. finance leases

are recognised at the lease’s inception at the lower of

the fair value of the leased asset and the present value

of the minimum leases payments. the corresponding

obligation is included in other liabilities in the balance

sheet. the assets acquired under financial leases are

amortised or depreciated over the shorter of the

asset’s useful life and the lease term. each lease

payment is allocated between the liability and the

interest expense. the interest expense is amortised

over the lease period to produce a constant periodic

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 19

rate of interest on the remaining balance of the

liability for each period.

assets in which the lessor retains substantially all the

risks and rewards of ownership are classified as

operating leases and they are included in the lessor’s

balance sheet. Payment made on operating leases are

recognised on a straight-line basis over the lease term

as rental expenses in profit and loss.

inTAngiBLE AssETsgoodwill

Goodwill arises on the acquisition of an undertaking

and is calculated as the difference between the cost

of the undertaking and the fair value of its net assets,

including contingent liabilities, at the time of acquisition.

Goodwill is allocated to cash-generating units at the

level at which management monitors the investment.

Goodwill is not amortised; instead each cash-

generating unit is tested for impairment once a year or

more frequently if indications of impairment exist.

Goodwill is written down to its recoverable amount

through profit or loss if the carrying amount of the net

assets of the cash-generating unit exceeds the higher

of the assets’ fair value less costs to sell and their

value in use, which equals the present value of the

future cash flows expected from the unit.

Other intangible assets

software acquired is measured at cost, including

expenses incurred to make each software application

ready for use. software acquired is amortised over its

expected useful life, which is usually three years,

according to the straight-line method.

software developed by the Group is recognised as an

asset if the cost of development is reliably measurable

and analyses show that the future earnings from

using the individual software applications exceed

cost. cost is defined as development costs incurred to

make each software application ready for use. once a

software application has been developed, the cost is

amortised over the expected useful life, which is

usually three years, according to the straight-line

method. the cost of development consists primarily of

direct remuneration and other directly attributable

development costs. expenses incurred in the planning

phase are not included but booked when incurred.

identifiable intangible assets taken over on the

acquisition of undertakings are measured at the time

of acquisition at their fair value and amortised over

their expected useful lives, which are usually three

years, according to the straight-line method. the value

of intangible assets with indefinite useful lives is not

amortised, but the assets are tested for impairment at

least once a year according to the principles applicable

to goodwill.

other intangible assets to be amortised are tested for

impairment if indications of impairment exist, and the

assets are subsequently written down to their

recoverable amount.

costs attributable to the maintenance of intangible

assets are expensed in the year of maintenance.

investment property

investment property is real property, including real

property let under operating leases, which the Group

owns for the purpose of receiving rent and/or

obtaining capital gains. the section on domicile

property below explains the distinction between

domicile and investment property.

on acquisition, investment property is measured at cost,

including transaction costs, and subsequently measured

at fair value. fair value adjustments and rental income

are recognised under other income in the income

statement. real property taken over by the Group under

non-performing loan agreements that is expected

to be sold within 12 months of classification is valued

in accordance with principled used for investment

property but presented as assets held for sale.

the fair value is assessed at least once a year.

assessment is based on the actual selling prices,

market prices and evaluations made by external

valuators. Based on the assessment of future events

and information available management has

determined the fair value.

Tangible assets

tangible assets includes domicile property, machinery,

furniture and fixtures. machinery, furniture and

fixtures covers equipment, vehicles, furniture, fixtures,

leasehold improvement and leased assets.

Domicile property

Domicile property is real property occupied by the

Group’s administrative departments, branches and

other service units. real property with both domicile

and investment property elements is allocated

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 20

proportionally to the two categories if the elements

are separately sellable. if that is not the case, such real

property is classified as domicile property, unless the

Group occupies less than 10% of the total floorage.

Domicile property is measured at cost plus property

improvement expenditure and less depreciation and

impairment charges. the straight-line depreciation of

the property is based on the expected scrap value and

an estimated useful life of 20 to 50 years. real

property held under long-term leases is depreciated

on a progressive scale.

investment property which becomes domicile property

because the Group starts using it for its own activities

is measured at fair value at the time of reclassification.

Domicile property which becomes investment property

is measured at fair value at the time of reclassification.

Domicile property which, according to a publicly

announced plan, the Group expects to sell within 12

months is recognised as an asset held for sale under

other assets. the same principle applies to property

taken over in connection with the settlement of debt if

such property is likely to be sold within 12 months.

however, if such property is unlikely to be sold within

this period, it is classified as investment property.

Machinery, furniture and fixtures

equipment, vehicles, furniture, fixtures and property

improvement expenditure are measured at cost less

depreciation and impairment charges. assets are

depreciated over their expected useful lives, which

are usually three years, according to the straight-line

method. leasehold improvements are depreciated

over the term of the individual lease, with a maximum

of 10 years.

Lease assets

lease assets consists of assets, except real property,

let under operating leases. lease assets are measured

using the same valuation technique as that applied by

the Group to its other equipment, vehicles, furniture

and fixtures. When, at the end of the lease period,

lease assets are put up for sale, the assets are

transferred to other assets.

impairment

tangible assets are tested for impairment if indications

of impairment exist. an impaired asset is written down

to its recoverable amount, which is the higher of its fair

value less costs to sell and its value in use.

Other assets

other assets includes interest and commission due,

prepayments and lease assets put up for sale at the

expiry of lease agreements.

lease assets put up for sale are measured at the lower

of their carrying amount at the time of reclassification

(expiry of lease agreements) and their fair value less

expected costs to sell.

Amounts due to credit institutions and central banks/

Deposits

amounts due to credit institutions and central banks

and Deposits include amounts received under repo

transactions (sales of securities which the Group

agrees to repurchase at a later date).

amounts due to credit institutions and central banks

and Deposits are measured at amortised cost and

where hedge accounting applies at amortised cost

plus the fair value of the hedged interest rate risk.

Other issued bonds/subordinated debt

other issued bonds and subordinated debt comprise

bonds issued by the Group. subordinated debt is

liabilities in the form of subordinated loan capital and

other capital investments which, in case of the Group’s

voluntary or compulsory winding-up, will not be repaid

until the claims of its ordinary creditors have been met.

other issued bonds and subordinated debt are

measured at amortised cost plus the fair value of the

hedged interest rate risk.

the yield on some issued bonds depends on an index

that is not closely linked to the bonds’ financial

characteristics, for example an equity or commodity

index. such embedded derivatives are bifurcated and

measured at fair value in the trading portfolio.

Other liabilities and provisions

other liabilities includes accrued interest, fees and

commissions that do not form part of the amortised

cost of a financial instrument. other liabilities also

includes pension obligations and provisions for other

obligations, such as lawsuits and guarantees.

a provision is recognised if, as a result of a past event,

the Group has a present legal or constructive

obligation that can be estimated reliably, and it is

probable that an outflow of economic benefits will be

required to settle the obligation.

DANSKE BANK PLC / FINANCIAL STATEMENTS AND ANNUAL REPORT 2012 21

if a lawsuit is likely to result in a payment obligation, a

liability is recognised if it can be measured reliably.

the liability is recognised at the present value of

expected payments.

Fair value

the fair value of financial assets and liabilities is

measured on the basis of quoted market prices of

financial instruments traded in active markets.

if an active market exists, fair value is based on the

most recently observed market price at the balance

sheet date.

if a financial instrument is quoted in a market that is

not active, the Group bases its valuation on the most

recent transaction price. it adjusts the price for

subsequent changes in market conditions, for instance

by including transactions in similar financial

instruments that are motivated by normal business

considerations.

if an active market does not exist, the fair value of

standard and simple financial instruments, such as

interest rate and currency swaps and unlisted bonds,

is measured according to generally accepted

measurement methods. market-based parameters are

used to measure fair value. the fair value of more

complex financial instruments, such as swaptions,