Annual report

2016

Mercury Processing Services International d.o.o. (former Intesa Sanpaolo Card d.o.o.) and subsidiaries

This version of the Annual report is a translation from the original, which was prepared in Croatian language. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version takes precedence over this translation.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 5

01 Introduction 7

Supervisory Board report on business operations of the Company for the year 2016 8

Management report 9

Responsibilities of the Management and Supervisory Boards for the preparation and approval of the annual report 12

02 Independent Auditors’ report 15

03 Statement of comprehensive income 21

04 Statement of financial position 25

05 Statement of changes in equity 29

06 Statement of cash flows 33

07 Notes to the financial statements 37

Contents

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 7

Introduction01

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 8

Supervisory Board report on business operations of the Company for the year 2016

Until December 15th 2016 the composition of Supervisory Board was as follows:

��Adriana Saitta as the President of the Supervisory Board�� Ivan Ivičić as the Vice-President of the Supervisory Board��Giancarlo Miranda as the Member of the Supervisory Board��Božo Prka as the Member of the Supervisory Board�� Ivica Rukavina as the Member of the Supervisory Board

After Latino Italy S.r.l. purchased all three shares of the Company on December 15th 2016, the composition of Supervisory Board changed, and was as follows:

�� Stuart James Ashley Gent as the President of the Supervisory Board��Bernardo Mingrone as the Vice-President of the Supervisory Board�� Simone Cucchetti as the Member of the Supervisory Board��Matthias Siekmann as the Member of the Supervisory Board�� Jeffrey David Paduch as the Member of the Supervisory Board��Alexander John Bowman as the Member of the Supervisory Board�� Ivica Rukavina as the Member of the Supervisory Board

The Supervisory Board held 12 (twelve) sessions until the end of the year. Amongst many decisions made in year 2016, the following are pointed out:

�� February 19th 2016 – acceptance of Annual report and financial statements for 2015, together with proposal for allocation of net profit ��March 21st 2016 – approval of the Budget for the year 2016�� June 28th 2016 – approval for the process of closing the Company’s subsidiary and branches outside of Croatia and Slovenia��December 15th 2016 – approval to the Management Board for entering into the amended Processing Services Agreement with the banks belonging to Intesa Sanpaolo Group, with respect to the Company’s change of ownership

The Supervisory Board has determined that the decisions and actions of the Management Board in year 2016 have been in accordance with the relevant laws as well as the acts of the Company and the Shareholders. The financial statements were made in accordance with the data contained in Company books, and they correctly show the assets and the business status of the Company. The Supervisory Board supports the Management Board proposal on the net profit allocation for the year 2016, and proposes to the Shareholders the acceptance of Management Board State of the Company Report for 2016, together with financial statements and proposal for net profit allocation.

Report submitted by:

Stuart James Ashley Gent President of the Supervisory Board

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 9

Management report

In 2016 the major change for the Group and the Company occured at the end of the year. In December 2016, Mercury UK Holdco Limited, the majority shareholder of Istituto Centrale delle Banche Popolari Italiane S.p.A. (“ICBPI”), and itself owned by a consortium of funds managed by Advent International, Bain Capital Private Equity and Clessidra, has completed the acquisition of Setefi Services S.p.A., and Intesa Sanpaolo Card d.o.o. (together “ISP Processing”) from Intesa Sanpaolo S.p.A for an equity value of €1,035 million. Following the change of the ownership and leaving the Intesa Sanpaolo Group, the Company and the subsidiary in Slovenia changed its name to Mercury Processing Services International d.o.o. and initiated its rebranding process.

The Group and the Company have made significant efforts in order to ensure that business relationship with ISP Group banks remains on adequate level. In that sense, on 15 December 2016, Addendum to Processing Service Agreement has been signed with all banks, ensuring continuity of the services, and guaranteeing service levels and commercial conditions for forthcoming period.

In the course of the year, the Group and the Company continued with the trends and projects started in previous periods. Its first and foremost priority was to maintain a high-level of security and regulatory compliance, while continuing with development of innovative practices, products and services and their implementation on the new markets. The Group and the Company also put emphasis on improving the quality of services provided to its customers, and as a preparation for the upcoming change of the ownership, undergone through necessary organizational changes, simplifying its structure.

High availability / disaster recovery During 2016 the Group and the Company have dedicated itself to bringing the Operational Excellence to the highest level. Therefore, High Availability / Disaster Recovery was a project of the utmost priority, aiming to deliver following results:

�� Implement High Availability solutions (cluster, load balancing) for critical applications and services between primary and secondary system room in each Data Center;�� Implement Disaster Recovery solution for critical applications in active / passive mode, between Zagreb and Koper Data Center.

Building and maintaing customer relationshipMaintaining a successful card business story is more challenging today than ever. It has never been more important to build and maintain a strong relationship with both main parties in the card business chain: the cardholders and the merchants. Taken this into account, during 2016 the Group and the Company started two initiatives with an aim to improve the quality of services and customer relations:

��Card Lifecycle managementThe project, undertaken in cooperation with MasterCard Advisors, was oriented to charge and credit cards, with the goal to initiate, build and sustain profitable cardholder behavior by gaining insight into the cardholder journey, analyzing the existent customer portfolio and identifying the most effective tactics and channels for implementing the best strategies to drive profitability. It served to obtain more insight into the performance of each bank that participated in the project, and into how these activities perform compared to each other and to local benchmarks.

Three Intesa Sanpaolo Banks, VUB Banka from Slovakia, CIB Bank from Hungary and Banca Intesa Beograd from Serbia successfully participated in the Card Lifecycle Management project.

�� Impact analysis of new Interchange Fee regulation on acquiring business

In order to help banks to be efficiently prepared for new Interchange Fee regulation implementation, we have analyzed merchant acquiring processes, particularly contracting, pricing and merchant profitability. The initiative, undertaken in cooperation with MasterCard Advisers, assessed potential impact as well as opportunities that may arise from the upcoming change in pricing, but also identified any needs to induce changes in merchant acquiring processes on banks’ side.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 10

Mobile wallet implementationIn the year 2016, the Group and the Company successfully continued with the enforcement of its strategy towards mobile payments. With further enhancements to its innovative HCE mobile wallet solution, and its implementation on the new markets, the Company is continually keeping up with the rapid pace of change in the area of mobile payments:

��With the official launch in May of 2016, Banka Koper became the third bank in Intesa Sanpaolo Group that went live with the Wave2Pay application, the first to implement the HCE with MasterCard, and also the first Slovenian bank that enabled mobile payments for its customers. �� In October of 2016, Banca Intesa Beograd from Serbia launched its mobile wallet service with VISA, again being the first bank to offer such service on its respective market.

China UnionPayBased on the agreement on mutual business cooperation between UnionPay International, a subsidiary of China UnionPay, and Banka Koper, the latter from January 2016 started accepting UnionPay cards on its ATM network, counting more than 100 ATMs in all major Slovenian cities. This has made Banka Koper the first bank in Slovenia to enable cash withdrawal with UnionPay cards via ATM network. Gradually, the option of using UnionPay cards will spread to 7,000 points of sale on which Banka Koper is acquirer.

Additionally, in October of 2016, Privredna banka Zagreb from Croatia became the second bank in Intesa Sanpaolo Group to accept UnionPay cards on their ATM network, counting over 700 ATMs.

Interchange fee regulationIn December 2015 capping of Interchange fees has come in force for EU region. This represents one of the biggest changes in card business, with substantial implications on revenue split between Issuing and Acquiring, as well as on overall card business profitability.

Parallel to Capping of Interchange Fees, the acquirers became obliged towards the merchant to reveal the fee structure, indicating also interchange fee amount per transaction, if not agreed otherwise. The Group and the Company have successfully implemented both requirements on all relevant systems and for all processed brands (MasterCard, Visa, American Express and Diners).

Group structure and reorganization The Company is the parent of the Mercury Processing Services International Group (“the Group”) which had operations in eight countries (Croatia, Slovenia, Bosnia and Herzegovina, Albania, Hungary, Romania, Serbia and Slovakia). The Company had branches in Albania, Romania, Serbia and Slovakia and has subsidiaries in Bosnia and Herzegovina and Slovenia. The subsidiary in Slovenia had a branch in Hungary. According to the organizational changes, the Group started in 2016 the project of closing and liquidation of all of its branches and its subsidiary in Bosnia and Herzegovina. Branches in Serbia, Romania, Slovakia and Hungary have been closed during the 2016, branch in Albania has been closed in January 2017 while a subsidiary in Bosnia and Herzegovina will be closed in 2017.

Additionally due to the Company sales, which was finalized in December 2016, 8 employees from the Company Business Division were transferred to Card and Payment Office in Intesa Sanpaolo Group, continuing working on strategic Intesa Sanpaolo Group projects.

In conclusion, in the year 2016 the Group and the Company put its focus on performance enhancements and quality improvements of services provided to its customers. Furthermore, the Group and the Company successfully adapted to the new demands arising from technological changes and new banking regulations, growing its business and implementing its innovative products and services on the new markets.

Financial information of the Group and Company for the year ended 31 December 2016 are as followsSTATEMENT OF FINANCIAL POSITION

HRK’000

Group Company

2016 2016Total assets 316,356 299,290Total liabilities 29,168 20,950Total equity and reserves 287,188 278,340Total equity and reserves and liabilities 316,356 299,290

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 11

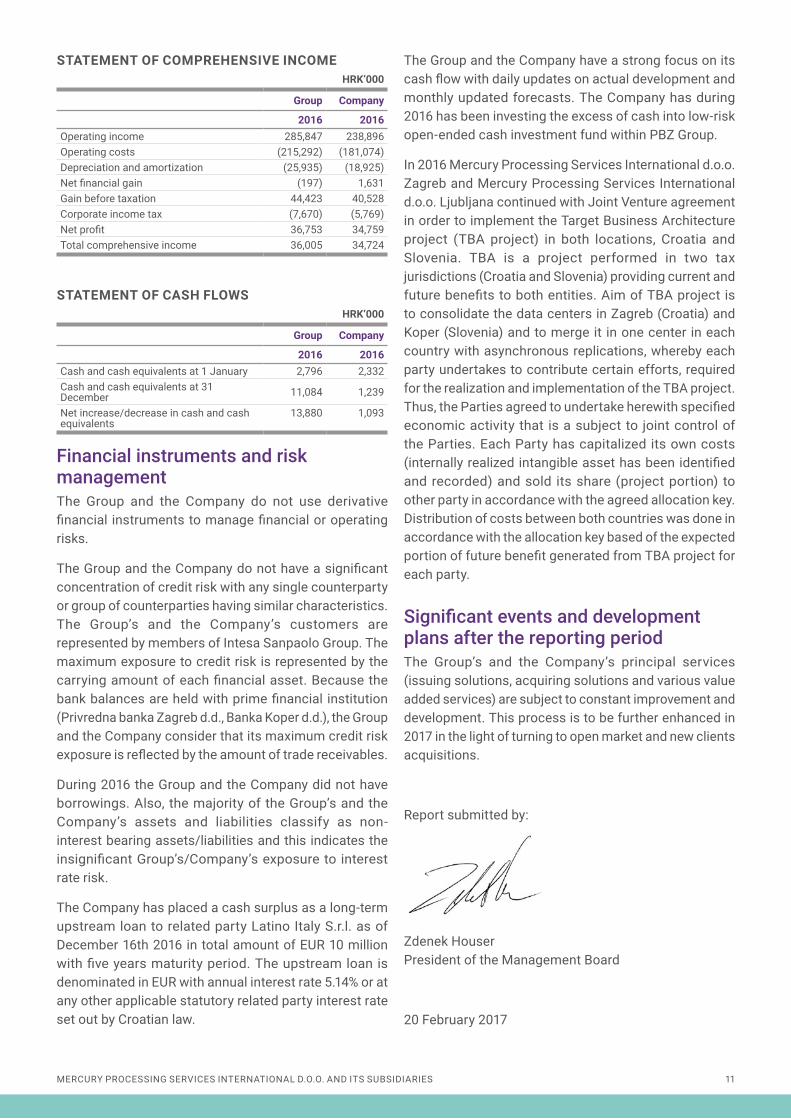

STATEMENT OF COMPREHENSIVE INCOMEHRK’000

Group Company

2016 2016Operating income 285,847 238,896Operating costs (215,292) (181,074)Depreciation and amortization (25,935) (18,925)Net financial gain (197) 1,631Gain before taxation 44,423 40,528Corporate income tax (7,670) (5,769)Net profit 36,753 34,759Total comprehensive income 36,005 34,724

STATEMENT OF CASH FLOWSHRK’000

Group Company

2016 2016Cash and cash equivalents at 1 January 2,796 2,332Cash and cash equivalents at 31 December 11,084 1,239

Net increase/decrease in cash and cash equivalents

13,880 1,093

Financial instruments and risk managementThe Group and the Company do not use derivative financial instruments to manage financial or operating risks.

The Group and the Company do not have a significant concentration of credit risk with any single counterparty or group of counterparties having similar characteristics. The Group’s and the Company’s customers are represented by members of Intesa Sanpaolo Group. The maximum exposure to credit risk is represented by the carrying amount of each financial asset. Because the bank balances are held with prime financial institution (Privredna banka Zagreb d.d., Banka Koper d.d.), the Group and the Company consider that its maximum credit risk exposure is reflected by the amount of trade receivables.

During 2016 the Group and the Company did not have borrowings. Also, the majority of the Group’s and the Company’s assets and liabilities classify as non-interest bearing assets/liabilities and this indicates the insignificant Group’s/Company’s exposure to interest rate risk.

The Company has placed a cash surplus as a long-term upstream loan to related party Latino Italy S.r.l. as of December 16th 2016 in total amount of EUR 10 million with five years maturity period. The upstream loan is denominated in EUR with annual interest rate 5.14% or at any other applicable statutory related party interest rate set out by Croatian law.

The Group and the Company have a strong focus on its cash flow with daily updates on actual development and monthly updated forecasts. The Company has during 2016 has been investing the excess of cash into low-risk open-ended cash investment fund within PBZ Group.

In 2016 Mercury Processing Services International d.o.o. Zagreb and Mercury Processing Services International d.o.o. Ljubljana continued with Joint Venture agreement in order to implement the Target Business Architecture project (TBA project) in both locations, Croatia and Slovenia. TBA is a project performed in two tax jurisdictions (Croatia and Slovenia) providing current and future benefits to both entities. Aim of TBA project is to consolidate the data centers in Zagreb (Croatia) and Koper (Slovenia) and to merge it in one center in each country with asynchronous replications, whereby each party undertakes to contribute certain efforts, required for the realization and implementation of the TBA project. Thus, the Parties agreed to undertake herewith specified economic activity that is a subject to joint control of the Parties. Each Party has capitalized its own costs (internally realized intangible asset has been identified and recorded) and sold its share (project portion) to other party in accordance with the agreed allocation key. Distribution of costs between both countries was done in accordance with the allocation key based of the expected portion of future benefit generated from TBA project for each party.

Significant events and development plans after the reporting periodThe Group’s and the Company’s principal services (issuing solutions, acquiring solutions and various value added services) are subject to constant improvement and development. This process is to be further enhanced in 2017 in the light of turning to open market and new clients acquisitions.

Report submitted by:

Zdenek HouserPresident of the Management Board

20 February 2017

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 12

Responsibilities of the Management and Supervisory Boards for the preparation and approval of the annual report

The Management Board of the Company is required to prepare separate financial statements of Mercury Processing Services International doo. (“The Company”) and consolidated financial statements of Mercury Processing Services International Group (“Group”) which give a true and fair view of the financial position of the Group and the Company and of the results of their operations and cash flows, in accordance with International Financial Reporting Standards adopted by the European Union (“IFRS”). The Management Board is responsible for implementing and maintaining internal controls relevant to the preparation and fair and true representation of financial statements that are free from material misstatement, whether due to fraud or error.

The Management Board has a general responsibility for taking such steps as are reasonably available to it to safeguard the assets of the Group and the Company and to prevent and detect fraud and other irregularities.

The Management Board is responsible for selecting suitable accounting policies to conform with applicable accounting standards and then apply them consistently,

making judgements and estimates that are reasonable and prudent, and preparing the financial statements on a going concern basis unless it is inappropriate to presume that the Group and the Company will continue in business.

The Management Board is also responsible for the preparation and content of the Management report in accordance with the Croatian Accounting Act and the rest of other information.

The Management Board is responsible for the submission of the Annual report to the Supervisory Board together with the separate and consolidated financial statements, following which the Supervisory Board is required to consider, and if appropriate approve the separate and consolidated financial statements for submission to the General Assembly for adoption.

Separate and consolidated financial statements shown on pages 21 to 73 and other information, set out on pages 7 to 12, are approved by the Management Board on 20 February 2017 and are signed and verified for the Supervisory Board.

Mercury Processing Services International doo.Radnička cesta 50, 10 000 Zagreb, Republic of Croatia20 February 2017

Zdenek Houser, President of the Management Board

Irina Bručić,Member of the Management Board

Alberto Barroero,Member of the Management Board

Giovanni Cetrangolo,Member of the Management Board

Tatjana Novak,Member of the Management Board

This version of the Annual report is a translation from the original, which was prepared in Croatian language. All possible care has been taken to ensure that the translation is an accurate representation of the original. However, in all matters of interpretation of information, views or opinions, the original language version takes precedence over this translation.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 13

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 15

Independent Auditors’ report

02

Statement of comprehensive income

03

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 21

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 22

Statement of comprehensive income For the year ended 31 December

HRK’000

Note Group Company

2016 2015 2016 2015Sales revenue 3 282,057 294,297 197,269 211,747Other income 4 3,790 4,073 41,627 37,275Total operating income 285,847 298,370 238,896 249,022Material expenses 5 (93,251) (94,105) (72,376) (72,851)Personnel expenses 6 (103,441) (111,513) (78,786) (82,740)Depreciation and amortization 7 (25,935) (32,538) (18,925) (24,209)Other expenses 8 (18,600) (19,284) (29,912) (32,744)Operating profit 44,620 40,930 38,897 36,478Financial income 9 488 585 2,230 582Financial expenses 9 (685) (390) (599) (365)Net financial income/(loss) (197) 195 1,631 217Profit before tax 44,423 41,125 40,528 36,695Income tax expense 10 (7,670) (7,452) (5,769) (7,241)Profit for the period 36,753 33,673 34,759 29,454Other comprehensive incomeItems that are or may be reclassified subsequently to profit or lossFair value reserve (available-for-sale financial assets): - Net change in fair value - (30) - (23) - Net amount transferred to profit or loss 30 - 23 -Foreign exchange differences on translation of foreign operations (516) (141) (58) (4)

Items that will not be reclassified to profit or lossActuarial losses on defined benefit plans 21 (262) (323) - -Total comprehensive income for the period 36,005 33,179 34,724 29,427

The accompanying accounting policies and notes are an integral part of these consolidated and unconsolidated financial statements.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 23

Statement of financial position

04

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 25

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 26

Statement of financial position For the year ended 31 December

HRK’000

Group Company

Assets Note 31 Dec 2016 31 Dec 2015 31 Dec 2016 31 Dec 2015

Non-current assets

Intangible assets 11 83,131 80,741 58,474 57,918

Property, plant and equipment 12 50,950 59,499 29,292 35,035

Investments in subsidiaries 13 - - 41,933 41,933

Deferred tax assets 10 1,026 1,194 2,668 932

Loans and receivables 16 75,578 - 75,578 -

Total non-current assets 210,685 141,434 207,945 135,818

Current assets

Inventories 780 763 774 753

Trade and other receivables 14 28,674 36,699 32,587 52,300

Income tax receivable 128 359 128 359

Financial investments 15 32,901 92,447 32,719 92,211

Loans and receivables 16 104 4,909 104 104

Prepaid expenses and accrued income 18 26,392 33,183 23,794 29,184

Cash and cash equivalents 17 15,847 2,796 1,239 2,332

104,826 171,156 91,345 177,243

Disposal group held for distribution 24 845 - - -

Total current assets 105,671 171,156 91,345 177,243

Total assets 316,356 312,590 299,290 313,061

Equity and reserves

Issued capital 19 30,863 30,863 30,863 30,863

Reserves 20 185,394 187,898 195,290 195,325

Retained earnings 70,931 61,601 52,187 46,607

Total equity and reserves 287,188 280,362 278,340 272,795

Non-current liabilities

Employee benefits 21 4,260 3,971 297 255

Total non-current liabilities 4,260 3,971 297 255

Current liabilities

Income tax payable - 51 - 36

Trade and other payables 22 19,551 22,805 16,117 35,915

Employee benefits 21 649 443 560 366

Accrued expenses 23 4,645 4,958 3,976 3,694

24,845 28,257 20,653 40,011

Disposal group held for distribution 24 63 - - -

Total current liabilities 24,908 28,257 20,653 40,011

Total equity and liabilities 316,356 312,590 299,290 313,061

The accompanying accounting policies and notes are an integral part of these consolidated and unconsolidated financial statements.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 27

Statement of changes in equity

05

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 29

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 30

Statement of changes in equity For the year ended 31 December

Group HRK’000

Issued capital Legal reserves Other reserves Retained earnings Total

As at 1 January 2015 30,863 4,291 184,101 51,923 271,178

Fair value reserve (available-for-sale financial assets):

- Net change in fair value - - (30) - (30)Foreign exchange differences on translation of foreign operations - - (141) - (141)

Actuarial losses on defined benefit plans - - (323) - (323)

Other comprehensive income - - (494) - (494)

Profit for the year - - - 33,673 33,673

Total comprehensive income for the period - - (494) 33,673 33,179

Dividends paid - - - (23,995) (23,995)

Transactions with shareholders recognized directly in equity - - - (23,995) (23,995)

As at 31 December 2015 30,863 4,291 183,607 61,601 280,362

As at 1 January 2016 30,863 4,291 183,607 61,601 280,362

Fair value reserve (available-for-sale financial assets):

- Net amount transferred to profit or loss - - 30 - 30Foreign exchange differences on translation of foreign operations - - (516) - (516)

Actuarial losses on defined benefit plans - - (262) - (262)

Other comprehensive income - - (748) - (748)

Profit for the year - - - 36,753 36,753

Total comprehensive income for the period - - (748) 36,753 36,005

Transfer to retained earnings - - (1,756) 1,756 -

Dividends paid - - - (29,179) (29,179)

Transactions with shareholders recognized directly in equity - - (1,756) (27,423) (29,179)

As at 31 December 2016 30,863 4,291 181,103 70,931 287,188

The accompanying accounting policies and notes are an integral part of these consolidated and unconsolidated financial statements.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 31

Company HRK’000

Issued capital Other reserves Retained earnings Total

As at 1 January 2015 30,863 195,352 41,148 267,363

Fair value reserve (available-for-sale financial assets):

- Net change in fair value - (23) - (23)

Foreign exchange differences on translation of foreign operations - (4) - (4)

Other comprehensive income - (27) - (27)

Profit for the year - - 29,454 29,454

Total comprehensive income for the period - (27) 29,454 29,427

Dividends paid - - (23,995) (23,995)

Transactions with shareholders recognized directly in equity - - (23,995) (23,995)

As at 31 December 2015 30,863 195,325 46,607 272,795

As at 1 January 2016 30,863 195,325 46,607 272,795

Fair value reserve (available-for-sale financial assets):

- Net change in fair value - - - -

- Net amount transferred to profit or loss - 23 - 23

Foreign exchange differences on translation of foreign operations - (58) - (58)

Other comprehensive income - (35) - (35)

Profit for the year - - 34,759 34,759

Total comprehensive income for the period - (35) 34,759 34,724

Dividends paid - - (29,179) (29,179)

Transactions with shareholders recognized directly in equity - - (29,179) (29,179)

As at 31 December 2016 30,863 195,290 52,187 278,340

The accompanying accounting policies and notes are an integral part of these consolidated and unconsolidated financial statements.

Statement of cash flows

06

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 33

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 34

Statement of cash flows For the year ended 31 December 2016

HRK’000

Note Group Company

2016 2015 2016 2015

Profit for the year 36,753 33,673 34,759 29,454Amortisation and depreciation 7 25,935 32,538 18,925 24,209Gain on sale of property, plant and equipment (115) (3) (59) (3)Impairment and write off of property, plant, equipment and intangibles 8 6 6 1 4Net financial income 9 197 (195) (1,631) (217)Income tax expense 10 7,670 7,452 5,769 7,311

33,693 39,798 23,005 31,304

Changes in

Inventories (17) (24) (21) (27)

Trade and other receivables 7,837 2,565 19,507 (15,516)

Prepaid expenses and accrued income 6,791 545 5,390 2,182

Trade and other payables (3,199) 3,314 (19,798) 21,843

Accrued expenses and deferred income (305) (1,106) 282 (453)

Employee benefits 233 304 236 28

Cash generated from operations 81,786 79,069 63,360 68,815

Interest paid (16) (48) (5) (23)

Income tax paid (7,322) (16,432) (7,310) (16,480)

Net cash generated from operating activities 74,448 62,589 56,045 52,312

Cash flows from investing activities

Interest received 166 9 163 6

Proceeds from sale of other financial investments 191,322 80,651 191,327 80,651

Acquisition of other financial investments (131,970) (91,894) (131,977) (91,651)

Payments of loans and receivables 4,805 - - -

Proceeds from loans and receivables (75,578) (1,030) (75,578) -

Acquisition of intangible assets (15,257) (22,814) (10,124) (15,495)

Proceeds from sale of intangible assets 298 929 - 852

Acquisition of property, plant and equipment (5,408) (4,290) (3,657) (2,464)

Proceeds from sale of property, plant and equipment 153 252 62 158

Proceeds from dividends 80 7 1,825 7

Net cash from investing activities (31,389) (38,180) (27,959) (27,936)

Cash flows from financing activities

Dividends paid (29,179) (23,995) (29,179) (23,995)

Net cash from financing activities (29,179) (23,995) (29,179) (23,995)

Net (decrease)/increase in cash and cash equivalents 13,880 414 (1,093) 381

Cash and cash equivalents at the beginning of year 2,796 2,382 2,332 1,951

Cash and cash equivalents at the end of year 25 16,676 2,796 1,239 2,332

The accompanying accounting policies and notes are an integral part of these consolidated and unconsolidated financial statements.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 35

Notes to the financial statements

07

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 37

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 38

1. Reporting entity

Mercury Processing Services International d.o.o. (the ‘Company’) is a company domiciled in Republic of Croatia. The Company previously operated under the name Intesa Sanpaolo Card d.o.o. Zagreb, but had changed its name on 30 December 2016 followed by a change in ownership. Effective from 15 December 2016 the Company is owned by Latino Italy S.r.l., affiliated with Mercury UK Holdco Limited, a holding company based in London and owned by a consortium of funds managed by Advent International, Bain Capital Private Equity and Clessidra.

The Company is the parent of the Mercury Processing Services International Group (“the Group”) which had operations in eight countries (Croatia, Slovenia, Bosnia and Herzegovina, Albania, Hungary, Romania, Serbia and Slovakia). The Company had branches in Albania, Romania, Serbia and Slovakia and has subsidiaries in Bosnia and Herzegovina and Slovenia. The subsidiary in Slovenia had a branch in Hungary. According to the organizational changes, the Group started in 2016 the project of closing and liquidation of all of its branches and its subsidiary in Bosnia and Herzegovina. Branches in Serbia, Romania, Slovakia and Hungary have been closed during the 2016, branch in Albania has been closed in January 2017, while a subsidiary in Bosnia and Herzegovina will be closed in 2017.

These financial statements comprise both the separate and the consolidated financial statements of the Company as defined in International Accounting Standard 27 Consolidated and Separate Financial Statements.

The Group is a provider of payment processing services including issuing solutions, acquiring solutions and other related services.

General AssemblyThe General Assembly was represented by Intesa Sanpaolo Holding International S.A., Privredna banka Zagreb d.d. and Banka Koper d.d. until 15 December 2016. Following the change of ownership from 15 December 2016 General assembly is represented solely by Latino Italy S.r.l.

Supervisory BoardSupervisory Board members are:Stuart James Ashley Gent President of the Supervisory BoardBernardo Mingrone Vice-President of the Supervisory Board Simone Cucchetti Member of the Supervisory BoardMatthias Siekmann Member of the Supervisory BoardJeffrey David Paduch Member of the Supervisory BoardAlexander John Bowman Member of the Supervisory BoardIvica Rukavina Member of the Supervisory Board

Management BoardManagement Board members are:Zdenek Houser President of the Management BoardIrina Bručić Member of the Management BoardTatjana Novak Member of the Management BoardGiovanni Cetrangolo Member of the Management BoardAlberto Barroero Member of the Management Board

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 39

2. Summary of accounting policies

2.1 Basis of preparationStatement of complianceThese financial statements comprise both the consolidated and separate (unconsolidated) financial statements of the Company and they are prepared in accordance with International Financial Reporting Standards as adopted by European Union (“EU IFRS”).

The financial statements were authorised for issue by the Management Board on the 20 February 2017 for approval by the Supervisory Board, following which the Supervisory Board is required to approve the statements for submission to the General Assembly for adoption.

Basis of measurementThe financial statements have been prepared under the historical cost convention, except for financial assets at fair value through profit or loss and available-for-sale financial assets, which are carried at fair value.

Key accounting estimates and judgments The preparation of the financial statements requires Company’s and Group’s management to make estimates, judgements and assumptions that affect application of policies and reported amounts of assets and liabilities and the disclosure of contingent liabilities at the reporting date and reported revenues and expenses for the period then ended. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both the current and future periods. Key accounting estimates and adjustments are described in Note 2.3.

Basis of consolidationThe financial statements of the Group include the consolidated financial statements of the Company and entities controlled by the Company (its subsidiaries). The Group structure is described in Note 13. Consolidated financial statements are prepared using uniform accounting policies for similar transactions and other business events in similar situations.

SUBSIDIARIESSubsidiaries are entities controlled by the Company. Control exists when the Company has the power, directly or indirectly, to govern the financial and operating policies of an entity so as to obtain benefits from its activities. The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases.

TRANSACTIONS ELIMINATED ON CONSOLIDATIONAll intra-group transactions, balances, unrealized gains, income and expenses are eliminated on consolidation.

ACCOUNTING FOR INVESTMENTS IN SUBSIDIARIES IN THE SEPARATE FINANCIAL STATEMENTS OF THE COMPANYIn the separate financial statements of the Company, investments in subsidiaries are carried at cost less impairment losses.

Functional currencyThe Group’s and the Company’s financial statements are presented in Croatian Kuna (HRK) which is the Company’s functional currency. All amounts disclosed in the financial statements are stated in HRK, rounded to the nearest thousand, unless stated otherwise.

For the purpose of consolidation, the financial statements of foreign consolidated subsidiaries and foreign branches are translated at the year-end exchange rates with respect to the balance sheet and at the exchange rate at the date of transaction with respect to the income statement. The exchange rate differences arising on the translation are recognized in other comprehensive income and accumulated in the translation reserve, except to the extent that the translation difference is allocated to non-controlling interest.

When a foreign operation is disposed of in its entirety or partially such that control, significant influence or joint control is lost, the cumulative amount in the translation reserve related to that foreign operation is reclassified to profit or loss as part of the gain or loss on disposal.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 40

Foreign currenciesTransactions in foreign currencies are translated to the functional currency at exchange rates at the dates of the transactions.

Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated to the functional currency at the exchange rate at that date.

The effective exchange rate of the Croatian Kuna at 31 December 2016 was 7.5578 Kuna per 1 Euro, 7.1685 Kuna per 1 United States Dollar and 8.8158 Kuna per 1 British Pound (at 31 December 2015 was 7.6351 Kuna per 1 Euro, 6.9918 Kuna per 1 United States Dollar and 10.3610 Kuna per 1 British Pound).

Changes in presentation of financial statements for 2016 Certain comparative information has been reclassified in order to achieve comparability with the presentation of the current year, as follows:

�� personnel training costs in the amount of HRK 1,411 thousand in the 2015 consolidated financial statements and HRK 1,110 thousand in the 2015 separate financial statements have been reclassified from material expenses to personnel expenses;�� other employee related costs in the amount of HRK 5,561 thousand in the 2015 consolidated financial statements and HRK 2,848 thousand in the 2015 separate financial statements have been reclassified from other expenses to personnel expenses.

Reclassifications are only of a presentational nature and do not affect the result for the year.

2.2 Significant accounting policiesIntangible assetsIntangible assets are stated at cost and consist of software designed specifically for credit card operations. Software is amortised on a straight line basis over a period of four years and internally developed software on a straight line basis over a period of ten years, according to estimated useful life. Costs incurred in order to restore or maintain the future economic benefits that the Company can expect from the originally assessed standard of performance of existing software systems are recognized as an expense in the period when the restoration or maintenance work is carried out.

Software that is no longer used is eliminated from the statement of financial position together with its related accumulated amortisation. Losses arising from such disposal or retirement are recognised in the income statement in the period in which they occur.

RESEARCH AND DEVELOPMENTExpenditure on research activities, undertaken with the prospect of gaining new scientific or technical knowledge and understanding, is recognised in profit or loss when incurred.

Development activities involve a plan or design for the production of new or substantially improved products and processes. Development expenditure is capitalised only if development costs can be measured reliably, the product or process is technically and commercially feasible, future economic benefits are probable, and the Group intends to and has sufficient resources to complete the development and to use or sell the asset. The expenditure capitalised

includes the cost of materials, direct labour and overhead costs that are directly attributable to preparing the asset for its intended use. Other development expenditure is recognised in profit or loss when incurred.

Capitalised development expenditure is measured at cost less accumulated amortisation and accumulated impairment losses, if any.

SUBSEQUENT CAPITALISATIONSubsequent expenditure is capitalised only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is recognised in profit or loss when incurred.

PROPERTY, PLANT AND EQUIPMENTItems of property, plant and equipment are stated at cost less accumulated depreciation. This cost includes all costs attributable to bringing an asset into its intended use.

Depreciation is recognised on a straight-line basis over the estimated useful lives of each item of property, plant and equipment as follows:

2016 2015

Equipment 4 – 10 years 4 – 10 years

Furniture 5 years 5 years

Leasehold improvements 10 years 10 years

Items of property and equipment that were disposed of or retired have been eliminated from the balance sheet together with the accompanying depreciation. Any gains or losses arising from disposal or retirement are included in the income statement for the period.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 41

SUBSEQUENT COSTSThe cost of replacing part of an item of property and equipment is recognised in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Group and its cost can be measured reliably. The costs of the day-to-day servicing of property and equipment are recognised in profit or loss as incurred.

ImpairmentA) FINANCIAL ASSETSA financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset.

An impairment loss in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount, and the present value of the estimated future cash flows discounted at the original effective interest rate.

Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed collectively in companies that share similar credit risk characteristics.

All impairment losses are recognised in the income statement. Any cumulative loss in respect of an available-for-sale financial asset recognised previously in equity is transferred to profit or loss.

An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognised. For financial assets measured at amortised cost and available-for-sale financial assets that are debt securities, the reversal is recognised in profit or loss. For available-for-sale financial assets that are equity securities, the reversal is recognised in equity.

B) NON-FINANCIAL ASSETSThe carrying amounts of the Company’s and Group’s non-financial assets, other than inventories and deferred tax assets are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists then the asset’s recoverable amount is estimated. For goodwill and intangible assets that have indefinite lives or that are not yet available for use, recoverable amount is estimated at each reporting date.

An impairment loss is recognised if the carrying amount of an asset or its cash-generating unit exceeds its recoverable amount. A cash-generating unit is the

smallest identifiable group of assets that generates cash flows that largely are independent from other assets and groups of assets.

Impairment losses are recognised in profit or loss. Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill allocated to the units and then to reduce the carrying amount of the other assets in the unit (group of units) on a pro rata basis.

The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

An impairment loss in respect of goodwill is not reversed. In respect of other assets, impairment losses recognised in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

InventoriesInventories of materials and spare parts are stated at lower of cost and net realisable value and weighted average price method is used on their consumption.

Cash at bank and in handCash at bank and in hand includes cash in hand and in banks.

Financial instrumentsFinancial assets of the Group and the Company are categorised into portfolios depending on Group’s and Company’s intentions in the moment of purchase and according to Group’s investment strategy. Financial assets are classified into the following categories: financial assets at fair value through profit or loss, loans and receivables and financial assets available-for-sale.

FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS Financial assets at fair value through profit or loss are financial assets which are classified as held for trading

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 42

or on initial recognition designated by the Group as at fair value through profit or loss. The Group does not apply hedge accounting. As stated above, this category has two sub-categories: financial instruments held for trading, and those designated by management as at fair value through profit or loss at inception. Trading assets and liabilities are those assets and liabilities that the Group acquires or incurs principally for the purpose of selling or repurchasing in the near term, or holds as a part of a portfolio that is managed together for short-term profit or position taking.

The Group designates financial assets and liabilities at fair value through profit or loss when either:

�� the assets or liabilities are managed, evaluated and reported internally on a fair value basis; or�� the designation eliminates or significantly reduces an accounting mismatch which would otherwise arise; or�� the asset or liability contains an embedded derivative that significantly modifies the cash flows that would otherwise be required under the contract.

LOANS AND RECEIVABLESLoans and receivables are non-derivative financial assets with fixed or otherwise identified repayments, unquoted in an active market. All loans and receivables are recognized in the moment of allocation of the funds to the debtor. After the initial recognition, the loans and receivables are carried at amortised cost, using the effective interest method, reduced by impairment losses.

Loans and receivables are reduced by impairment losses. The write-down of loans for impairment is recorded in case there is objective evidence that the Group and the Company will not succeed to collect all receivables at maturity date. Amount of impairment represents the difference between the book value and the recoverable amount that represents the net present value of the estimated cash flows. If the Group and the Company determine that there is no objective evidence of impairment of financial asset, whether it is significant or not, this financial asset is categorized into group of financial assets with similar credit risk characteristics and collectively assessed for impairment. Individually impaired assets are not included in collectively assessed impairment test.

Impairment losses are estimated based on the debtors’ creditworthiness and business results considering the value of the collaterals or third party guarantee.

When it is obvious that there is no possibility of collecting the loan, and that all legal options had been used, and the total loss is identified, the loan is written off. If the

amount of impairment is subsequently decreased as a result of event occurring after initial impairment, impairment or provision is adjusted through income statement.

Penalty interests are charged to the customers when a portion of the loan falls overdue. Penalty interest is accounted for on a cash received basis as ‘Interest income’.

FINANCIAL ASSETS AVAILABLE FOR SALEFinancial instruments available for sale are those non-derivative financial assets that are designated as available for sale or are not classified in any other financial instruments category.

At the initial recognition the financial instruments available for sale are recorded at fair value, including transaction costs and revenues directly attributable to the instrument, and afterwards they are carried at fair value based on quoted market prices or cash flow model amounts. The instruments for which the fair value is not reliably measurable are carried at cost.

The gains and losses arising from the change in fair value are recognized directly in equity until the asset is removed from the balance sheet or until there is impairment in the instrument. At the time of the removal from the balance sheet or when impairment is identified, the accumulated gain or loss is recognized in the income statement.

Foreign exchange differences for equity securities denominated in foreign currencies classified as available for sale are recognized within the equity, together with gains and losses from fair value changes until the asset is sold. Foreign exchange differences for debt securities denominated in foreign currencies classified as available for sale are recognized through the income statement.

Provisions Provisions are recognized when the Group has a present obligation (legal or constructive) as a result of a past event, it is probable that the Group will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation at the reporting date, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 43

Employee benefitsCONTRIBUTIONS TO DEFINED CONTRIBUTIONS PENSION PLANSContributions to defined contribution pension plans are recognised as an expense in profit or loss as incurred.

BONUS PLANSA liability for employee bonuses is recognised in provisions based on the Group and Company’s formal plan and when past practice has created a valid expectation by the Management Board that they will receive a bonus and the amount can be determined before the time of issuing the financial statements.

Liabilities for bonus plans are expected to be settled within 12 months of the balance sheet date and are measured at the amounts expected to be paid when they are settled.

RETIREMENT ALLOWANCESThe obligation and costs of retirement benefits are determined using a projected unit credit method which considers each period of service as giving rise to an additional unit of benefit entitlement and measures each unit separately to build up the final obligation. Certain actuarial assumptions were made by the Management in this assessment.

Leases Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases. Rentals payable under operating leases are charged to the income statement on a straight-line basis over the term of the relevant lease.

Revenue recognitionRevenue from provision of services is recognised when services have been rendered.

Interest income and expenses are recognized in the income statement using the effective interest method.

The effective interest method is a method of calculating the amortized cost of a financial asset and of allocating interest income over the relevant period. The effective interest rate is the rate used for discounting estimated future cash flows (including all paid or received fees that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the financial asset, or, where appropriate, a shorter period.

Borrowing costsBorrowing costs are expensed as incurred. Borrowing costs include interest charges and other costs incurred in connection with the borrowing of funds, including exchange differences arising from foreign currency borrowings used.

Financial income and expensesFinancial income comprises interest income on funds invested, changes in the fair value of financial assets at fair value through profit or loss and foreign currency gains.

Interest income is recognised as it accrues, using the effective interest method.

Financial expenses comprise interest expense on borrowings, foreign currency losses, changes in the fair value of financial assets at fair value through profit or loss and impairment losses recognised on financial assets.

TaxationThe income tax liability is based on taxable profit for the year and considering deferred taxes.

Deferred taxes are calculated using the liability method. Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. Deferred tax assets and liabilities are measured using the tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled based on tax rates enacted or substantially enacted at the reporting date.

The measurement of deferred tax liabilities and deferred tax assets reflects the tax consequences that would follow from the manner in which the enterprise expects, at the reporting date, to recover or settle the carrying amount of its assets and liabilities. Deferred tax assets and liabilities are not discounted and are classified as non-current assets (liabilities) in the balance sheet.

Deferred tax assets are recognized when it is probable that sufficient taxable profits will be available against which the deferred tax assets can be utilized. At each reporting date, the Company re-assesses unrecognized deferred tax assets and the carrying amount of deferred tax assets.

Tax returns are subject to subsequent tax audits by tax authorities. As various interpretations of numerous tax laws exist, the amounts stated in these financial statements could be subject to change depending on the decision of the relevant tax authority.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 44

Contingent liabilitiesContingent liabilities are not recognised in the financial statements. They are disclosed unless the possibility of an outflow of resources embodying economic benefits is remote.

A contingent asset is not recognised in the financial statements but is disclosed when an inflow of economic benefits is probable.

Subsequent eventsSubsequent events that provide additional information about the Group’s and the Company’s position at the balance sheet date (adjusting events) are reflected in the financial statements. Subsequent events that are not adjusting events are disclosed in the notes when material (Note 29).

2.3 Significant accounting estimates and judgementsAccounting judgementsIn applying the Group’s and Company’s accounting policies, the Management Board has made the following judgments, apart from those involving estimates, which have the greatest effect on the amounts recognised in the financial statements:

INTERNALLY DEVELOPED SOFTWARE-DETERMINATION OF CAPITALISATION CRITERIA AND ESTIMATED USEFUL LIFEIn 2012 the Group initiated the Target Business Architecture project (TBA) in order to merge the two data centres, one in Zagreb (MPSI Croatia) and one in Koper (MPSI Slovenia) to act as a back-up to one another. Every transaction or change which occurs for a client of primary data centre (MPSI Croatia or MPSI Slovenia according to the client’s location) will automatically be transferred to the system of the other (secondary) data centre, so in case of a disaster and data loss the secondary centre could take over data processing service of the primary data centre. The Group and the Company assessed which costs are eligible for capitalisation and have established a process to record and monitor these costs separately.

Expenditure related to the development of TBA is capitalised when it meets the criteria outlined in IAS 38 Intangible Assets. Such assets are then systematically amortised over their useful economic life of 10 years.

There is judgement involved in determining an appropriate framework to consider which expenditure requires capitalisation and which should be expensed. Note 11 of the financial statements provides details of the amounts capitalised.

The major sources of estimation uncertaintiesThe estimates and assumptions with significant risk of material adjustments to the carrying amounts of assets and liabilities within the next financial year are discussed below.

TAXIncome tax calculation is made on the basis of interpretation of current laws and regulations. The basis for tax return calculation may be subject of examination by tax authorities.

IMPAIRMENT OF INVESTMENTS IN SUBSIDIARIESImpairment of investments in subsidiaries is based on the Management’s best judgement of the recoverable amount of the investments. The recoverable amount is the higher of the fair value of the investment less cost of sales or value in use. Information about assumptions is disclosed in Note 13.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 45

2.4 Standards, interpretations and amendments to published standards that are not yet effective and were not used in preparation of these financial statementsA number of new standards and amendments to standards are effective for annual periods beginning after 1 January 2016 and earlier application is permitted. However, the Group has not early adopted the following new or amended standards in preparing these consolidated financial statements.

Disclosure Initiative (Amendments to IAS 7) The amendments require disclosures that enable users of financial statements to evaluate changes in liabilities arising from financing activities, including both changes arising from cash flow and non-cash changes. The amendments are effective for annual periods beginning on or after 1 January 2017, with early adoption permitted. To satisfy the new disclosure requirements, the Group intends to present a reconciliation between the opening and closing balances for liabilities with changes arising from financing activities.

Recognition of Deferred Tax Assets for Unrealised Losses (Amendments to IAS 12) The amendments clarify the accounting for deferred tax assets for unrealised losses on debt instruments measured at fair value. The amendments are effective for annual periods beginning on or after 1 January 2017, with early adoption permitted. The Group is assessing the potential impact on its consolidated

financial statements resulting from the amendments. So far, the Group does not expect any significant impact.

IFRS 15 Revenue from Contracts with Customers IFRS 15 establishes a comprehensive framework for determining whether, how much and when revenue is recognised. It replaces existing revenue recognition guidance, including IAS 18 Revenue, IAS 11 Construction Contracts and IFRIC 13 Customer Loyalty Programmes. IFRS 15 is effective for annual periods beginning on or after 1 January 2018, with early adoption permitted. The Group is assessing the potential impact on its consolidated financial statements resulting from the amendments. So far, the Group does not expect any significant impact.

The Group plans to adopt IFRS 15 in its consolidated financial statements for the year ending 31 December 2018, using the retrospective approach. As a result, the Group will apply all of the requirements of IFRS 15 to each comparative period presented and adjust its consolidated financial statements.

The Group plans to use the practical expedients for completed contracts. This means that completed contracts that began and ended in the same comparative reporting period, as well as the contracts that are completed contracts at the beginning of the earliest period presented, are not restated.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 46

3. Sales revenue

a) Analysis by nature of services provided

HRK’000

Group Company

2016 2015 2016 2015

Transaction processing services 171,344 175,534 117,789 128,929

Account maintenance services 29,749 25,983 22,868 18,961

POS terminal maintenance services 15,076 15,417 10,839 10,315

Basic fraud management services 14,949 16,183 9,536 9,914

Card personalisation services 13,084 15,984 13,084 15,439

ATM account maintenance services 7,809 7,475 4,683 4,250

PINs generation and production services 3,197 3,209 3,197 3,006

Statement generation and production services 2,406 1,825 2,179 1,595

Account set up services 139 3,876 7 2,631

Other services 24,304 28,811 13,087 16,707

282,057 294,297 197,269 211,747

Transaction processing services fee is charged based on the number of transactions.

Account maintenance services fee is charged based on the active accounts on the system.

POS terminal maintenance services fee is charged based on the active and pending POS terminals on the system.

Basic fraud management services fee is charged based on the number of active issuing accounts, POS TIDs and ATM TIDs.

Card personalisation services fee is charged based on the number of generated and personalized cards (chip and non-chip).

ATM account maintenance services fee is charged based on the active ATM terminals on the system.

PINs generation and production services fee is charged based on the number of generated PINs and printed PINs.

Statement generation and production services fee is charged based on the number of generated cardholder and merchant statements.

Account set up services is charged based on number of new POS, ATM TIDs and issuing accounts.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 47

b) Analysis by counterpartyHRK’000

Group Company

Processing services income 2016 2015 2016 2015

PBZ Card d.o.o., Zagreb 73,492 72,516 73,492 72,516

PBZ d.d., Zagreb 38,939 41,918 38,896 41,918

Všeobecna Uverova Banka a.s., Bratislava 57,911 58,503 57,020 58,077

Intesa Sanpaolo Banka d.d. BIH, Sarajevo 7,291 7,201 6,490 5,925

Banka Koper d.d., Koper 47,454 56,756 6,829 7,185

Banca Intesa ad Beograd, Novi Beograd 45,763 43,430 6,562 17,064

CIB Bank Zrt, Budapest 4,707 6,162 3,412 3,837

Intesa Sanpaolo Bank Albania SH.A., Tirana 2,675 3,180 1,986 2,355

Bank of Alexandria S.A.E., Cairo 652 596 99 28

Intesa Sanpaolo Bank Romania S.A., Arad 2,062 3,067 1,507 1,925

Pravex-Bank PJSCCB, Kiev 6 6 6 6

Banca Intesa Russia, Moscow 6 6 6 6

Others 1,099 956 964 905

282,057 294,297 197,269 211,747

4. Other income

HRK’000

Group Company

2016 2015 2016 2015

Intergroup IT system and support services - - 39,013 34,572Refund of materials, postage, IT costs and telecommunications links 2,668 2,675 2,321 2,309

Collection of receivables previously written-off 20 46 - -

Other income 1,102 1,352 293 394

3,790 4,073 41,627 37,275

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 48

5. Material expenses

HRK’000

Group Company

2016 2015 2016 2015

Materials used 1,141 1,056 1,105 929

Data processing services 57,800 57,749 45,461 45,657

Business premises lease 14,082 14,479 10,365 10,578

Advisory services 6,001 6,205 4,843 4,991

Post, telecommunication and transportation costs 7,473 7,619 5,034 4,812

Vehicles lease, maintenance and other related costs 5,168 5,308 4,018 4,243

Other services 1,586 1,689 1,550 1,641

93,251 94,105 72,376 72,851

The Auditor’s fee for the statutory audit of the unconsolidated and consolidated statutory financial statements of the Company as of and for the year ended 31 December 2016 amounts HRK 314 thousand (2015: HRK 287 thousand), and for the Group amounts HRK 421 thousand (2015: HRK 375 thousand). During 2016 and 2015 Auditors did not provide any other advisory services to the Group nor to the Company.

Fees for tax and regulatory consulting services of the Company in 2016 amounts HRK 353 thousand (2015: HRK 581 thousand) and for the Group amounts HRK 416 thousand (2015: HRK 683 thousand).

Legal consulting services of the Company in 2016 amounts HRK 1,769 thousand (2015: HRK 1,333 thousand) and for the Group amount HRK 1,999 thousand (2015: HRK 1,540 thousand).

6. Personnel expenses

At the 31 December 2016 the Group had 344 employees (2015: 369 employees), and the Company had 259 employees (2015: 273 employees).

HRK’000

Group Company

2016 2015 2016 2015

Net wages and salaries 48,654 52,457 38,924 40,452

Income taxes and pension contributions 31,845 34,594 24,800 26,426

Social security contributions 16,215 17,490 11,185 11,904

Personnel training costs 1,021 1,411 841 1,110

Other employee related costs 5,706 5,561 3,036 2,848

103,441 111,513 78,786 82,740

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 49

7. Depreciation and amortisation expense

HRK’000

Group Company

2016 2015 2016 2015

Depreciation 13,607 19,668 9,357 14,026

Amortisation 12,328 12,870 9,568 10,183

25,935 32,538 18,925 24,209

8. Other expenses

HRK’000

Group Company

2016 2015 2016 2015

Marketing and promotion 625 882 601 882

Payment transactions fee 23 26 - -

Bank charges 214 283 167 217

Insurance premium 974 1,213 860 1,005

Intergroup IT system and support services - - 24,545 26,654

Other taxes 9,838 9,575 - -

Damage compensation to the Clients 1,136 104 513 64

Travel expenses 935 1,214 525 698

Student services 1,264 1,368 744 805

Other operating costs 3,190 4,145 1,589 1,999

Contributions unrelated to the business performance 395 468 367 416

Tangible asset impairment and write off 6 6 1 4

18,600 19,284 29,912 32,744

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 50

9. Net financial income

HRK’000

Group Company

2016 2015 2016 2015

Interest income 166 9 163 6

Unrealised gains on financial assets at fair value through profit or loss - 118 - 118

Gains realised on sale of available-for-sale securities 242 451 242 451

Dividends income 80 7 1,825 7

Financial income 488 585 2,230 582

Interest expense (16) (48) (5) (23)

Foreign exchange losses, net (203) (342) (187) (342)Unrealised losses on financial assets at fair value through profit or loss (172) - (172) -

Impairment of available-for-sale securities (294) - (235) -

Financial expense (685) (390) (599) (365)

Net financial income/(loss) recognised in profit or loss (197) 195 1,631 217

10. Income taxes

a) Income tax recognised in the income statementHRK’000

Group Company

2016 2015 2016 2015

Current tax expense (7,508) (7,324) (7,511) (7,311)

Deferred tax expense (162) (128) 1,742 70

(7,670) (7,452) (5,769) (7,241)

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 51

b) Deferred tax assets/liabilitiesHRK’000

Group Company

1 January 2016

Additions/ Reversals

recognised in income statement

Additions recognised

in equity

31 December

2016

1 January

2016

Additions/ Reversals

recognised in income statement

Additions recognised

in equity

31 December

2016

Bonus accruals 876 (257) - 619 875 (257) - 618

Trade receivables impairment 1 - - 1 - - - -

Provision for retirement benefits 311 53 - 364 51 3 - 54Available for sale financial assets -unrealised loss recognised in equity 6 - (6) - 6 - (6) -

Available for sale financial assets - impairment - 42 - 42 - 42 - 42

Impairment of ISPC BH subsidiary - - - - - 1,954 - 1,954

Deferred tax assets 1,194 (162) (6) 1,026 932 1,742 (6) 2,668

HRK’000

Group Company

1 January 2015

Additions/ Reversals

recognised in income statement

Additions recognised

in equity

31 December

2015

1 January

2015

Additions/ Reversals

recognised in income statement

Additions recognised

in equity

31 December

2015

Bonus accruals 805 71 - 876 805 70 - 875

Trade receivables impairment 226 (225) - 1 - - - -

Provision for retirement benefits 284 27 - 311 50 1 - 51Assets written-off (evidence on disposal not available) 1 (1) - - 1 (1) - -

Available for sale financial assets -unrealised loss recognised in equity - - 6 6 - - 6 6

Deferred tax assets 1,316 (128) 6 1,194 856 70 6 932

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 52

c) Reconciliation of the effective income tax rateReconciliation of the income tax calculated at the effective income tax rate to income tax expense:

HRK’000

Group Company

2016 2015 2016 2015

Profit before tax 44,423 41,125 40,528 36,695

Income tax at 20% (8,885) (8,225) (8,106) (7,339)

Effect of different tax rates in subsidiaries 145 117 (1) (12)

Non-deductible expenses (441) (516) (326) (125)

Non-taxable income 243 229 574 72

Tax benefits 702 553 136 163

Usage of tax losses, not recognised as deferred tax asset 566 390 - -Recognition of previously unrecognised deferred tax asset on impairment of investment in subsidiary - - 1,954 -

(7,670) (7,452) (5,769) (7,241)

Effective income tax rate 17.27% 18.12% 14.23% 19.73%

As of 31 December 2016 the Group has unused tax losses of HRK 3,665 thousand (2015: HRK 6,999 thousand) for which deferred tax asset was not recognised.

As of 31 December 2016 the Company recognised in its separate financial statements deferred tax asset of HRK 1,954 thousand relating to impairment loss of investment in subsidiary in Bosnia and Herzegovina which was recognised in previous periods. In 2016 the Company made a decision to close this subsidiary and as a result recognised previously unrecognised deferred tax asset.

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 53

11. Intangible assets

Movements in the intangible assets of the Group during 2016 and 2015 were as follows:

HRK’000

Internally generated software Software Assets under construction

– internally generatedAssets under

construction – other Total

Cost

1 January 2015 11,730 118,103 33,614 6,311 169,758

Additions - - 16,456 6,358 22,814

Transfer into use 6,660 9,690 (6,660) (9,690) -

Disposals and write-offs - (1,942) - - (1,942)

Translation differences (6) (180) (35) (6) (227)

31 December 2015 18,384 125,671 43,375 2,973 190,403

1 January 2016 18,384 125,671 43,375 2,973 190,403

Additions - - 12,161 3,096 15,257

Transfer into use 3,495 4,335 (3,495) (4,335) -

Disposals and write-offs - (669) - - (669)

Translation differences (40) (533) (141) (6) (720)

31 December 2016 21,839 128,804 51,900 1,728 204,271

Accumulated amortisation

1 January 2015 1,053 96,907 - - 97,960

Charge for the year 1,596 11,274 - - 12,870

Disposals and write-offs - (1,013) - - (1,013)

Translation differences (1) (154) - - (155)

31 December 2015 2,648 107,014 - - 109,662

1 January 2016 2,648 107,014 - - 109,662

Charge for the year 2,064 10,264 - - 12,328

Disposals and write-offs - (371) - - (371)

Translation differences (2) (477) - - (479)

31 December 2016 4,710 116,430 - - 121,140

Net carrying value

1 January 2015 10,677 21,196 33,614 6,311 71,798

31 December 2015 15,736 18,657 43,375 2,973 80,741

31 December 2016 17,129 12,374 51,900 1,728 83,131

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 54

Movements in the intangible assets of the Company during 2016 and 2015 were as follows:

HRK’000

Internally generated software Software Assets under construction –

internally generatedAssets under

construction – other Total

Cost

1 January 2015 9,960 66,195 23,673 4,561 104,389

Additions - - 10,280 5,215 15,495

Transfer into use 4,538 7,453 (4,538) (7,453) -

Disposals and write-offs - (997) - - (997)

31 December 2015 14,498 72,651 29,415 2,323 118,887

1 January 2016 14,498 72,651 29,415 2,323 118,887

Additions - - 7,815 2,309 10,124

Transfer into use 2,426 2,951 (2,426) (2,951) -

Disposals and write-offs - - - - -

31 December 2016 16,924 75,602 34,804 1,681 129,011

Accumulated amortisation

1 January 2015 861 50,070 - - 50,931

Charge for the year 1,343 8,840 - - 10,183

Disposals and write-offs - (145) - - (145)

31 December 2015 2,204 58,765 - - 60,969

1 January 2016 2,204 58,765 - - 60,969

Charge for the year 1,618 7,950 - - 9,568

Disposals and write-offs - - - - -

31 December 2016 3,822 66,715 - - 70,537

Net carrying value

1 January 2015 9,099 16,125 23,673 4,561 53,458

31 December 2015 12,294 13,886 29,415 2,323 57,918

31 December 2016 13,102 8,887 34,804 1,681 58,474

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 55

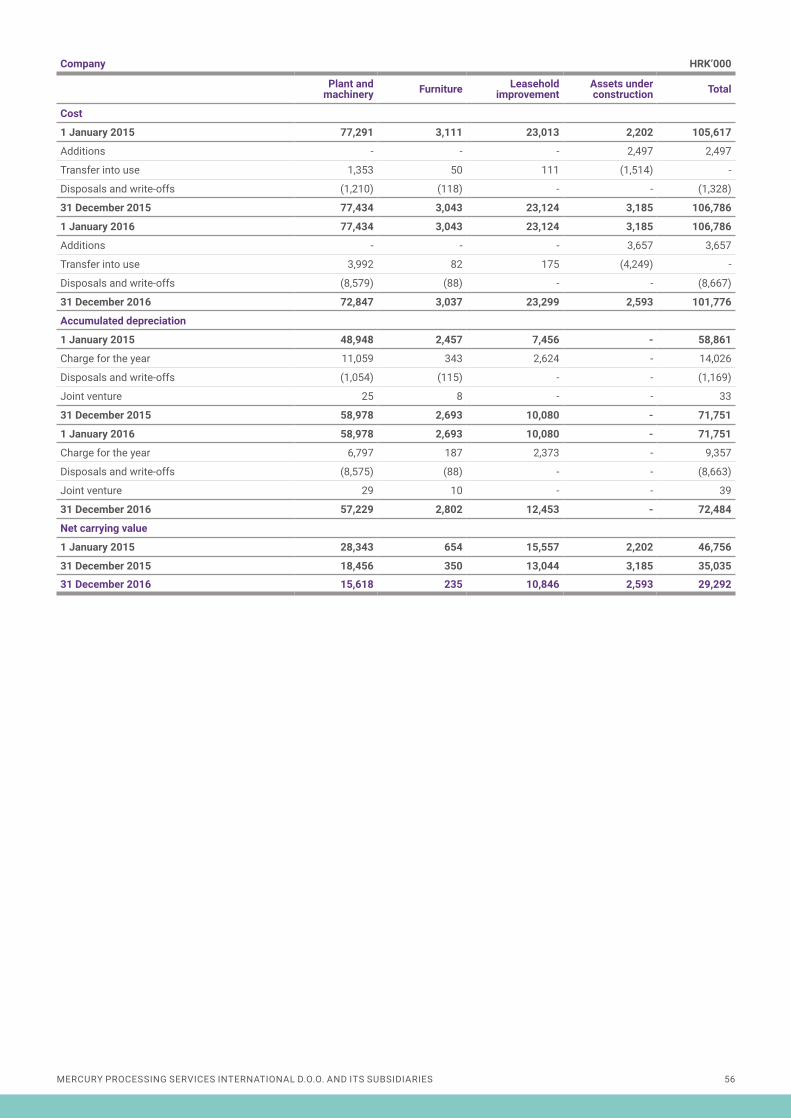

12. Property, plant and equipment

Group HRK’000

Plant and machinery Furniture Leasehold

improvementAssets under construction Total

Cost

1 January 2015 119,167 4,732 28,837 10,450 163,186Additions - - - 4,290 4,290Transfer into use 9,089 50 110 (9,249) -Disposals and write-offs (1,881) (118) - - (1,999)Translation differences (137) (5) (20) (29) (191)31 December 2015 126,238 4,659 28,927 5,462 165,286

1 January 2016 126,238 4,659 28,927 5,462 165,286Additions - - - 5,408 5,408Transfer into use 5,273 88 175 (5,536) -Disposals and write-offs (19,005) (226) - (30) (19,261)Translation differences (471) (17) (59) (23) (570)31 December 2016 112,035 4,504 29,043 5,281 150,863

Accumulated depreciation

1 January 2015 76,017 3,958 7,961 - 87,936Charge for the year 16,046 379 3,243 - 19,668Disposals and write-offs (1,666) (115) - - (1,781)Joint venture 29 8 - - 37Translation differences (69) (4) - - (73)31 December 2015 90,357 4,226 11,204 - 105,787

1 January 2016 90,357 4,226 11,204 - 105,787Charge for the year 10,428 221 2,958 - 13,607Disposals and write-offs (18,992) (225) - - (19,217)Joint venture 34 10 - - 44Translation differences (283) (16) (9) - (308)31 December 2016 81,544 4,216 14,153 - 99,913Net carrying value

1 January 2015 43,150 774 20,876 10,450 75,250

31 December 2015 35,881 433 17,723 5,462 59,499

31 December 2016 30,491 288 14,890 5,281 50,950

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 56

Company HRK’000

Plant and machinery Furniture Leasehold

improvementAssets under construction Total

Cost

1 January 2015 77,291 3,111 23,013 2,202 105,617

Additions - - - 2,497 2,497

Transfer into use 1,353 50 111 (1,514) -

Disposals and write-offs (1,210) (118) - - (1,328)

31 December 2015 77,434 3,043 23,124 3,185 106,786

1 January 2016 77,434 3,043 23,124 3,185 106,786

Additions - - - 3,657 3,657

Transfer into use 3,992 82 175 (4,249) -

Disposals and write-offs (8,579) (88) - - (8,667)

31 December 2016 72,847 3,037 23,299 2,593 101,776

Accumulated depreciation

1 January 2015 48,948 2,457 7,456 - 58,861

Charge for the year 11,059 343 2,624 - 14,026

Disposals and write-offs (1,054) (115) - - (1,169)

Joint venture 25 8 - - 33

31 December 2015 58,978 2,693 10,080 - 71,751

1 January 2016 58,978 2,693 10,080 - 71,751

Charge for the year 6,797 187 2,373 - 9,357

Disposals and write-offs (8,575) (88) - - (8,663)

Joint venture 29 10 - - 39

31 December 2016 57,229 2,802 12,453 - 72,484

Net carrying value

1 January 2015 28,343 654 15,557 2,202 46,756

31 December 2015 18,456 350 13,044 3,185 35,035

31 December 2016 15,618 235 10,846 2,593 29,292

MERCURY PROCESSING SERVICES INTERNATIONAL D.O.O. AND ITS SUBSIDIARIES 57

13. Investments in subsidiaries

Investments in subsidiaries are stated at cost less impairment allowance with net book value as follows:

31 December 2016

31 December 2016

31 December 2015

31 December 2015

Subsidiary Domicile Ownership HRK ‘000 Ownership HRK’000

Intesa Sanpaolo Card BH d.o.o. u likvidaciji Bosnia and Herzegovina 100% - 100% -

Mercury Processing Services International procesiranje plačilnih kartic in razvoj d.o.o. Slovenia 100% 41,933 100% 41,933

41,933 41,933

Impairment of investments in subsidiaries, i.e. calculation of recoverable amount is based on approved plans. Future cash flows derived from those plans are discounted using the weighted average cost of capital.

Cost of investment in subsidiary Mercury Processing Services International procesiranje plačilnih kartici in razvoj d.o.o. equals its carrying value of HRK 41,933 thousand, i.e. no impairment was identified. Future cash flows were discounted by 8.11% (2015: 9.81%)

Cost of investment in subsidiary Intesa Sanpaolo Card BH d.o.o. u likvidaciji was HRK 10,854 thousand. Methodology and assumptions used by Management Board to estimate future cash flows indicated that the investment in the subsidiary Intesa Sanpaolo Card BH d.o.o. u likvidaciji is not fully recoverable, and in 2012 the Company recognised impairment of investment in subsidiary Intesa Sanpaolo Card BH d.o.o. u likvidaciji in the amount of HRK 10,066 thousand and in 2011 in the amount of HRK 788 thousand.