Hoover Insti tution Working Group on Intellectual Property, Innovation, and Prosper ity

Stanford University

www.hooverip2.org

WORKING PAPER SERIES NO. 16011

“A NEW DATASET ON MOBILE PHONE PATENT LICENSE ROYALTIES”

ALEXANDER GALETOVIC

UNIVERSIDAD DE LOS ANDES

STEPHEN H. HABER DEPARTMENT OF POLITICAL SCIENCE AND HOOVER INSTITUTION, STANFORD UNIVERSITY

LEW ZARETZKI HAMILTON IPV

REVISED: AUGUST 2017

ORIGINAL: SEPTEMBER 25, 2016

ANewDatasetonMobilePhonePatentLicenseRoyal6es 1

August2017Update 2

AlexanderGaletovic,StephenHaber,andLewZaretzki 3

Thisversion:August22,2017

WethankJonathanBarneH,AnneLayne-Farrar,TimLong,KeithMallinson,JorgePadillaandotherswhowishedto1

remainanonymousbutprovidedimportantperspecPveandhelpfulcomments.JordanHorrilloprovidedexcellentresearchassistance.

ThisnoteupdatestheSeptember2016releaseofourdatabase,whichnowincorporatesthefullcalendaryear2016.2

WehavealsowidenedcoveragewheneverfeasibleandimprovedandcompletedsomeesPmatesofpreviousyears.AdetaileddescripPonofthechangesisintab2017ImprovementsintheExcelworkbookthataccompaniesthisnote.

AlexanderGaletovicisProfessorofEconomics,UniversidaddelosAndes,SanPago,Chile.3

HiscurrentresearchfocusesonstandardessenPalpatents,compePPonpolicyandanPtrust.GaletovichasbeenaResearchScholarattheInternaPonalMonetaryFund,aTinkerVisiPngProfessoratStanfordandaRita-RicardoNaPonalFellowattheHooverInsPtuPon.StephenHaberisA.A.andJeanneWelchMilliganProfessorintheSchoolofHumaniPesandSciences,ProfessorofPoliPcalScience,ProfessorofHistory,Professor(bycourtesy)ofEconomics,SeniorFellowoftheStanfordInsPtuteforEconomicPolicyResearch,andPeterandHelenBingSeniorFellowattheHooverInsPtuPon,atStanfordUniversity.HaberdirectstheHooverInsPtuPonWorkingGrouponIntellectualProperty,InnovaPon,andProsperity(HooverIP2).HooverIP2succeededtheHooverProjectonCommercializingInnovaPon(PCI).Toensureacademicfreedomandindependence,bothPCIandIP2,alongwithallworkassociatedwiththem,haveonlybeensupportedbyunrestrictedgi^s.SomemajordonorshaveincludedMicroso^,Pfizer,andQualcomm.LewZaretzkiisManagingDirector,HamiltonIPVaSiliconValleyIPstrategyconsulPngfirmservingmanyoftheworld’sfinesttechnologycompaniesandleadingtechnologyinvestorsinmaHersofcorporatestrategy,IPstrategy,M&A,andIPtransacPons.

� 1

1.IntroducPon

Mobilephonesintegrateawidearrayoftechnologies,fromcompuPngtoconsumer

electronicstocommunicaPons,andfromsemiconductorstohardware,so^wareand

services.Thismakesthemforalargeandbroadarrayofpatentsandlicensors.InaddiPon,

mobilephonesrelyontechnologicalstandardstomaketheminteroperable.Astandard-

compliantphoneuseshundreds,ifnotthousandsofstandardessenPalpatents(SEPs),

whichareownedbymanydifferentpatentholders. 4

WhilesomehaveclaimedthatdispersedownershipofSEPsleadstohighcumulaPve

royaltyrates,theesPmatesthatunderpintheseclaimsarebasedonthesimpleaddiPonof

publishedhandsetroyaltyrates.Thereareavarietyofreasonstobedubiousofthis

method,nottheleastofwhichisthatitconflates“rackrates”whichmightnotbepaidby

anybody,withactualmarkettransacPonrates.Indeed,justasfirmshaveincenPvesto

declareallpossiblepatentsasessenPal,theyalsohaveincenPvestoposthighroyaltyrates

tolicensetheirporjolio,eveniftheyneveractuallyearnanylicensingrevenuefromthat

porjolio. 5

ThisnotedescribesthedatasetweusedtoesPmatetheAverageCumulaPve

RoyaltyYieldpaidinthemobilephonevaluechain—thesumtotalofpatentroyalty

ItisesPmatedthatthereareabout150.000declaredmobileSEPsworldwide(issuedandappliedfor)intheso-called4

“4Gstack,”whichincludesLTE,WCDMAandGSM/GPRS/EDGE.Ofthese,about20,000areUSpatents.GaletovicandGuptareportthatin2013therewere128SEPholders.“RoyaltyStackingandStandardEssenPalPatents:TheoryandEvidencefromtheMobileWirelessIndustry,“HooverIP2WorkingPaper15012,2017.Oneshouldnotethatitmayhavebeenintheinterestsofpatentholderstodeclareallpossiblepatentsas“essenPal.”OnereasonisthatpatenteesrisklegalpenalPesfornotdeclaringapatentessenPal.Also,somefirmsmayhaveactedonthepercepPonthatalargeSEPporjoliobolsteredtheirreputaPonandincreasedtheirleveragewhennegoPaPngroyalPes.Moreover,theETSIIPRdatabasejustlistsdeclaredessenPalpatents,butneitherETSInoranybodyelseauditsthosedeclaraPons.Forthesereasons,itisnotclearhowmanyofthesepatentsaretrulyessenPal.IndustryparPcipantso^enesPmatetherateofover-declaraPonat50%ormore.OthersthinkthatfewSEPswouldpassalegaltestofessenPality.

AtonepointinPmeitbecamecommonforthemajorequipmentvendorstopublishadeclaredLTEroyaltyrate,usually5

withcaveatsthatitcouldbeadjustedinlightofgrantbacksorforotherreasons.Forexample,Norteldeclareda1%rate,butitappearstohaveneveractuallyreceivedanyLTElicensingrevenue.

� 2

paymentsearnedbylicensors,dividedbythetotalvalueofmobilephonesshipped. We6

publishedthefirstversionofthisdatasetinSeptember2016.Thisversionimprovesour

esPmateinseveraldimensions. 7

Asinthefirstversion,webuilduponearlierworkbyMallinsonthatfocusedon

mobileSEPs. Butwegobeyondthatworkby:(i)analyzingpatentroyalPesintheenPre8

mobilephonevaluechain(i.,e,royalPesonmobileSEPs,butalsoaudioandvideocodecs,

imaging,operaPngsystems,semiconductors,andothercomponents);(ii)comparingour

resultsonpatentroyalPestoothercostsofmobilephonemanufactureandtoOEM

profits;(iii)generaPngPmeseriesthatpermitresearcherstoanalyzethestabilityofthe

AverageCumulaPveRoyaltyYieldbackto2007.Forsomefirms,ourcoveragegoesbackto

2000.

Ourpurposeistoprovideascomprehensiveandtransparentadatasourceasis

pracPcallypossibleforusebyotherresearchers,industrypracPPoners,andgovernment

officials.Thus,thisnoteshouldbereadasanadjuncttotheExcelworkbookthatwehave

postedtotheweb.Thatworkbookshowstheunderlyingdataandsources.Italsoexplains

thedecisionswemadewhenesPmaPngorapproximaPngvalues.

FollowingMallinson,weusethetermroyalty“yield”ratherthanroyalty“rate.”“Rate”referstotheactualroyaltypaid6

byalicensee,typicallyanOEMorEMs,toalicensorasapercentageofthelicensee’ssales.Yieldisthesumtotalofpatentroyaltypaymentsdividedbythetotalvalueofmobilephonesshipped,thelaHerofwhichmightincludetheproducPonofOEMsthatevadepatentlicenses.Someresearchersrefertoroyaltyyieldasthe"royaltystack,"atermweeschewbecauseitistheory-ladenandanoxymoron.

WedescribethemainchangesandimprovementsinTab2017ImprovementsintheExcelworkbook.7

SeeKeithMallinson,“CumulaPveMobile-SEPRoyaltyPaymentsNoMorethanAround5percentofMobileHandset8

Revenues,”IPFinance,August19,2015.J.GregorySidakbuildsuponMallinsonaswell,buttakesasomewhatdifferenttheorePcalapproach,includingpaymentsinkindandesPmatesofthevalueofcross-licenses.Thus,itisastudyofpotenPalIPvalue,ratherthanthecumulaPveroyaltyyield.SeeJ.GregorySidak,“WhatAggregateRoyaltyDoManufacturersofMobilePhonesPaytoLicenseStandard-EssenPalPatents?”CriterionJournalonInnova8on1(701). AnearlyesPmateofroyalPespaidbylicensorsis EricStasik,“RoyaltyRatesandLicensingStrategiesforEssenPalPatentsonLTE(4G)TelecommunicaPonsStandards,”LesNouvelles,September2010,pp.114-119.

� 3

InthisnotewedonottakeaposiPononwhethertheesPmatesoftheroyaltyyield

wepresentinthisstudyare“toohigh,”“toolow,”or“justright.”Thatisanimportant

debate,butitcanonlybejoinedonthebasisofevidence.

2.Methods—“FollowtheMoney”

Allmethodsofanalysisdependonanunderlyingtheory,andunderlyingtheoriesare

createdinordertoanswerparPcularquesPonsofinterest.ThebasicquesPonresearchers

areaskinginthiscaseishowdoroyalPespaidbyfirmsinthemobilephonevaluechain

affectproducPonanddecisionsatthemargin?Thatis,ifroyaltyrateswereXpercent

pointshigher,byhowmuchwouldoutputfallandpricesincrease?IftheywereX’percent

pointslower,byhowmuchwouldoutputriseandpricesfall?Microeconomictheory

providesaguidetotherelevantfactsnecessarytoanswerthisquesPon;ittellsusthatwe

needtoapproximatepaidper-unitroyalPes. 9

Inanidealworldforresearchers,mobilephoneOriginalEquipmentManufacturers

(OEMs),ElectronicsManufacturerServices(EMSs),OriginalDesignManufacturers(ODMs)

andcomponentmanufacturersinthemobilephonevaluechainwouldreportthe

idenPPesoftheIPholdersfromwhomtheylicenseandthevalueofthepaymentstoeach

ofthoselicensors.Itwouldthenbepossibletodeterminethe“IPBillofMaterials(BoM)”

paidbyeachfirmintheinthemobilephonevaluechain.Fromthere,onecouldcalculate

aweightedaverageBoMforeveryfirminthevaluechain,withtheweightsdeterminedby

theirrelaPvecontribuPontototalmobilephonesales.

Onemightclaimthatthisapproachtodataignoresothereconomiccostsbornebymanufacturers.Forexample,wedo9

notincludetheopportunitycostbornebyamanufacturerthatbuyspatentstopreventclaimsofinfringement,ortheopportunitycostbornebymanufacturerswhocrosslicensetheirpatents(inacrosslicensingagreementfirmsmayforegosomeoranyroyaltypaymentinexchangeforaccesstoanotherfirm’sporjolio),orthemembershipsubscripPonspaidtodefensiveaggregatorsofpatents.Suchexpenditureswillincreaseafirm’sfixedcosts.Theywillnot,however,affectmarginalcostsofproducPon,andthusdonotaffectproducPonandpricingdecisionsatthemargin.

� 4

Nevertheless,researcherscanneverworkwiththeidealdata,andthedataon

mobilephonepatentlicensesarenotanexcepPontothisrule.Thefundamentalproblem

isthatlicenseeshaveveryweakincenPvestodisclosetheirpatentlicenseroyalty

paymentssomostofthemdonotdisclosethem.

AsamaHerofaccounPng,however,paymentsbylicenseesmustshowupas

revenuesforlicensors,andlicensorshavestrongincenPvestodisclosetheirpatent

licensingrevenues.Forpublicly-tradedfirmswithlicensingrevenuesthatareanon-trivial

componentoftheirtotalrevenues,thoseincenPvesarelegalandregulatory;thesources

ofrevenuemustbedisclosedtoinvestors.Evenlicensorswithoutlegalandregulatory

incenPvestodisclosetheirrevenues,however,suchaspatentpoolsadministeredbyfirms

thatspecializeinpooladministraPon,havemarket-basedincenPvestodisclose,andthis

allowstheesPmaPonofapproximateroyaltyrevenues.

ItisthereforepossibletoesPmatethetotalcostofpatentlicensesinthemobile

phonevaluechainbyidenPfyingthemajorlicensorsandretrievingtheinformaPon

necessarytoesPmatetheirlicensingrevenues.Onecanthendividethesumofthese

revenuesacrossalllicensorsbythetotalvalueofmobilephonessoldtoobtainanaverage

cumulaPveroyaltyyield.

Therefore,therearethreenumbersthatoneneedstoknowinordertoesPmate

theAverageCumulaPveRoyaltyYield:(i)themobilephonepatentlicensingrevenue

earnedbyeachlicensor;(ii)thetotalnumberofmobilephonessold;(iii)theaverage

selling(wholesale)priceofamobilephone(ASP).

2A.EsPmaPngtheSizeoftheMarket

ThenumberofphonessoldandtheASPareeasytocomeby:anumberofdata

analyPcsfirmsesPmatethem,andissuepressreleasesthattheyposttotheweb.Firms

suchasICInsights,IDC,Gartner,andGFKproducetheseesPmates.TheesPmatestendto

� 5

bewithinafewpercentagepointsofoneanothersuchthatresultswouldnotbesensiPve

towhichsourceisused. ThesesamefirmsalsoproduceesPmatesofthequanPtyand10

valueoftablets.WedonotincludetheseinthesecalculaPons.Ifwewouldinclude

tablets,itwouldincreasethevalueofdevicesales,andthusdrivedowntheAverage

CumulaPveRoyaltyYield.

ThesesameenPPesalsoesPmatedevicesalesandpricesbymajorOEMs,and

providethisdatainpressreleases,whichtheyposttotheweb.TheseesPmatesalsotend

tobewithinafewpercentagepointsofoneanother. Weusethisdatainorderto11

esPmatetherevenuesearnedbypatentpools,whichtendtohavePeredroyalty

schedules.

2B.EsPmaPngPatentLicensingRevenue

EsPmaPngpatentlicensingrevenueisstraighjorwardinprinciple,thoughitcanbe

difficultinpracPce.Firmsthatearnsignificantrevenuesfrompatentlicensingreportthose

figuresinfinancialreports(e.g.SECforms10kand20-f).Privatefirmsarenotobligatedto

disclosesuchinformaPonabouttheiroperaPons.InthesecasesweesPmaterevenues

basedoninformaPonthatfirmsmakepubliclyavailable.Forexample,successfulpatent

poolstypicallydisclosetheidenPPesoftheirlicensorsandlicensees,thepatentscovered

bythepool,andthefeescheduleforlicensees.EsPmaPngroyaltyrevenuewiththis

informaPonispracPcal,althoughito^entendstooveresPmateroyalPes.However,thatis

consistentwithourchosenbias,andsoweexpectit. 12

Therearesomepublicfirmsthatearnpatentlicensingrevenueinthemobile

phonevaluechainbutinamountsthataremodestrelaPvetotheirotherrevenuesources.

Forthedata,seeTab1.8,DeviceSales,intheExcelworkbook.10

Forthedata,seeTab1.9,OEMSales,intheExcelworkbook.11

Forthedata,seeTab1.7,RevenuesbyLicensor,intheExcelworkbook.12

� 6

Theythereforedonotbreakoutthisrevenueasareportablesegmentintheirpublic

filings.Therearealsoprivatefirms,andthesearenotobligatedtodisclosetheirrevenue

sources.WhenitispracPcable,weesPmatetherevenuesofbothtypesoffirmsonthe

basisofinformaPonontheirwebsites,reportsinthetradeandfinancialpress,and

interviewswithindustrypracPPoners. WhennotpracPcable,weenumeratethosefirms13

thatmayhavegeneratedroyaltyrevenue,butforwhichwehaveneitherdatanora

plausibleesPmate. WethendoasensiPvityanalysisinwhichweassignaseriesof14

plausibletotalrevenuesforthesefirmsasagroupinordertoseerobustnessofour

results. ThatsensiPvityanalysisshowsthatevenanupperboundesPmateofthe15

cumulaPvemobilephonepatentlicensingrevenuesofthesefirmswouldnothavea

significanteffectontheresults:ifthemobilephonepatentlicensingrevenuesforthese

firmsasagroupwere$2billion,theAverageCumulaPveRoyaltyYieldwouldincreaseby

roughly0.5percentagepoints.

Thecoreofourmethod,then,isto“followthemoney.”Infollowingthemoney,

wemakenodisPncPonsastowherealicensorisearningrevenuesinthemobilephone

valuechain,nordowemakedisPncPonsamongthedifferentpatentedtechnologiesina

mobilephone.Wecapture,forexample,revenuesearnedfromlicensestakenby

semiconductorandbasebandchipproducers,aswellastheOEMsandEMSsthat

assemblephones.Wealsocapturerevenuesearnedfromlicensesonpatentsthatenable

video,imaging,audio,andotherfuncPons,aswellastheSEPsthatenablemobility.We

capture,aswell,therevenuesofamajorso^warecompanythatearnsrevenuefromits

patentsthatreadonthemostpopularmobilephoneoperaPngsystem.

Forthedata,seeTab1.7,RevenuesbyLicensor,intheExcelworkbook.13

Forthelistoffirms,seeTab6.0,OtherFirms,intheExcelworkbook.14

See,Tab1.6Sensi8vity,tableformobilephones,intheExcelworkbook.15

� 7

2C.BasicPrinciplesofDataCollecPon

Infollowingthemoneyweareguidedbyfourprinciples.First,totheextentthatit

ispossible,theesPmatesshouldusepublicly-availablesourcessothatourresultscanbe

replicatedandimproveduponbyotherresearchers.Indeed,weinviteusersofthedatain

theExcelworkbookthataccompaniesthisdocumenttoshareinformaPonwithussothat

wecanimproveouresPmates.Second,ouraimistohaveaslongaPmeseriesforeach

licensorasispracPcallypossible.Third,decisionsabouthowtotreatdatashouldbiasin

favorofobtainingalargerroyaltyyield.Thisimpliesthatweerronthesideof:(i)including

licensorsthatlicensetoavarietyofindustries,notjustmobilephones,whichmeansthat

wemaybecounPngtheirrevenuesfromotherproductsasroyalPesonmobilephones;(ii)

aHribuPngroyalPestomobilephonesthatmayhavebeenpaidonothermobileproducts,

suchastablets;(iii)doublecounPng,whichmeansthatwemaybeincludingboththe

royaltyrevenuesdeclaredbyalicensorandtheroyaltyrevenuesearnedbyapoolwhere

thelicensorisamember;(iv)biasingesPmatesupwards. 16

3.DataQuality

Thequalityofdatavariesacrosslicensors.Weclassifylicensorsinfourcategories

accordingtheaccuracyoftheirlicensingdata:Confirmed,Documented,Approximated,

andResearched.Table1showsthelicensorsclassifiedineachcategory. 17

Asasageneralrule,thelargestlicensorsarealsothosewhichreportlicensing

revenuesseparatelyfromotherrevenues,andforwhichwehaveaprimarysource

Forexample,inthecaseofHuawei,whichisarelaPvelynewlicensorwhoselegalstatusasaprivatelyownedcollecPve16

meansthatitisnotsubjecttothesamereporPngrequirementsasU.S.orEuropeanfirms,weliberallyassumethatitsmobilephoneroyaltyrevenuesarethesameasawell-established,U.S.-basedtechnologycompany,Interdigital.Indoingso,weassumethatHuaweiisearning,onitsmobilephonepatentsalone,roughly30percentofallpatentrevenuesearnedbyallChinesecompaniesinanylineofeconomicacPvity.SeethediscussioninTab5.6,Huaweiintheworkbook.

AlsoseeTab6.0,Others,intheExcelworkbook.17

� 8

documentthatwasgeneratedasalegalrequirement.Qualcomm,Interdigital,Nokia,and

Ericsson,areexamplesoftheselicensors.Giventhehighqualityandaccountability,their

knowledgeoftheiroperaPonsandtheirreporPngunderSECauspices,weconsiderthese

figures"Confirmed.”In2016thiscategoryaccountedfor75.2percentoftotalrevenues.

OtherlicensorsprovidesufficientinformaPoninpubliclyavailabledocumentsto

esPmatetheirlicensingrevenues.Insomecaseswehavetoseparatelicensingrevenues

frommobilephonesfromotherlicensingrevenues,basedoninformaPoninfootnotesto

SEC10k’s.Inothercases,wehavelicensingfeeschedulesandtheidenPPesofthe

licensees,andcanesPmatethelicensingrevenuesofeachlicensee.Wedenotetheseas

"Documented."EnPPesinthiscategoryincludethemajorpatentpoolssuchasMPEGLA

MPEG4;MPEGLAAVC/H.264,andViaLicensing’sAACpool.ItalsoincludesMicroso^,

whichlicensesitspatentsthatreadontheAndroidOperaPngSystemtoOEMs.In2016

thiscategoryaccountedfor8.5percentoftotalrevenues.

TherearesomeenPPesthatarenon-trivialmobilephonevaluechainlicensorsfor

whichwehaveinformaPonabouttheirtotallicensingrevenues.Wehavetomake

assumpPons,however,basedonotherdataorinterviews,aboutthepercentageoftheir

totallicensingrevenuesthatcomefromthemobilephonevaluechain.Wedenotethese

as"Approximated."TheyincludeXperi(formerlyTessera),Quarterhill(formerlyWiLAN)

andRambus.In2016thiscategoryaccountedfor11.9percentoftotalrevenues.

Finally,therearesomeenPPeswithliHleornodisclosurebutuponexaminaPonit

seemsthattheyhaveverymodest,somePmeszero,revenues. Wedenotetheseas18

“Researched.”In2016thiscategoryaccountedfor4.3percentoftotalroyaltyrevenue.

TheoneexcepPontothegeneralizaPonaboutsizeanddataqualityisIntellectualVentures.Inthiscase,wehave18

esPmateditstotalrevenuesfrominformaPononitsownwebsiteoverPme(usingtheweb-toolsthatallowresearcherstolookatarchivedwebpages)andfrominformaPoninthetradepressaboutitsfinancialperformance.WehavetoapproximatethepercentageofthisrevenuefromthemobilephonevaluechainbasedoninformaPononthefirm’swebsiteaboutitspatentporjolio,aswellasinterviewswithindustrypracPPoners.

� 9

InaddiPon,therearefirmsthatappeartoearnsomepatentlicensingroyalPesfrom

themobilephonevaluechain,butthereislimitedinformaPoninthepublicdomainabout

themagnitudes.Somelarge,publiccompanies(someofwhicharemobilephoneOEMs)

earnsomepatentlicensingrevenues,buttheirlicensingacPviPesarenotsignificant

enoughtobeareportablesegmentintheirfinancialstatements.Someofthesefirms,or

EMSsthatproduceforthem,arealsomajorsourcesoflicensingrevenueforotherfirms

coveredinthisstudy.Therearealsosmallprivatecompaniesthatappeartoearnsome

patentlicensingroyalPesfromthemobilephonevaluechain,butthepubliclyavailable

informaPonabouttheirrevenuesandoperaPonsisfragmentary.Wecallthose“Other

idenPfiedfirms.”Theavailableevidencedoesnotsuggestanyoneofthesefirms—public

orprivate—individuallyhaslicensingrevenuessignificantenoughthatitsaddiPonwould

haveamaterialeffectontheoverallmagnitudeofthecumulaPveroyaltyyield.

4.Results

4.AThe2016Update

WeareabletoesPmate,withvaryingdegreesofaccuracy,themobilephone

patentlicensingrevenuesof39licensorsinthemobilephonevaluechain.WeesPmate

thatthe39licensorsasagrouphadcumulaPveroyalPesin2016ofalmost$14.2billion

(seeTable2). Ofthese39,10havelicensingrevenuesofeffecPvelyzero.In2016Royalty19

revenuesoftheremaining29firmsvarybetween$1.6millionand$7.7billion.

OnewaytoputthesenumbersintoperspecPveiscomparethemwiththevalueof

mobilephoneshipments.In2016originalequipmentmanufacturers(OEMs)sold1.97

billionmobilephonesfor$425.1billion. ItfollowsthattheASPwas$215.5,andthatthe20

Forthedatabylicensor,seeTab1.7,RevenuesbyLicensor,intheExcelworkbook.19

AccordingtoIDC.Forthedata,seeTab1.8,DeviceSales,intheExcelworkbook.20

� 10

AverageCumulaPveRoyaltyperphonewas$7.2.TheAverageCumulaPveRoyaltyYieldis

totalpatentroyalPesdividedbythevalueoftotalphoneshipments,or3.3percent. 21

YetanotherwaytoputthesenumbersintoperspecPveistoaskhowtheycompare

withthosefromearlieryears.BecausewetakeaPme-seriesapproach,someofourfirm-

levelrevenueesPmatesgobackto2000.By2007,wehavedatafor17licensors,which

accountedfor78.2percentofallroyaltyrevenuesin2016.By2009,wehavedataon22

firms,andtheseaccountedfor92.5percentofallroyaltyrevenuesin2016 .AsFigure122

shows,bothofthoseseriesareremarkablystable.The2009-2016series,forexample,

hoversataround3percent,fallingonlymarginallyduringthelastthreeyears. 23

YetanotherwaytoputthesedataintoperspecPveistoaskhowtheycompareto

esPmatesthatotherresearchershavemadeabouttherestofthecostsincurredto

manufacturephones,suchassemiconductorsandbasebandprocessors,aswellasOEM

operaPngmarginsonmobilephones.Figure2presentsthatdata.Theresultsindicate

thatpatentlicensingisthesmallestofthecategories:somewhatlowerthanthecostof

basebandprocessors,slightlylessthanone-seventhofthecostofsemiconductors,and

aboutone-fourthofOEMoperaPngmargins. 24

4.B.2016and2015Compared

AscanbeseencomparingFigures2and3,theAverageCumulaPveRoyaltyYielditissPll

3.3percent---itdidnotvarybetween2015and2016.Nevertheless,theshareof

manufacturers’profitsintheaveragesellingpriceofaphonefellfrom14.9percentto11.8

percent,andsemiconductorcosts(basebandprocessorsandothersemiconductors)rose

ForthecalculaPons,seeTab1.3,RoyaltyYieldSummary,intheExcelworkbook.21

Someofthesefirmsdonotreportanyrevenues.22

Forthedata,seeTab1.4,RoyaltyYieldSeries,intheExcelworkbook.23

Forthedataandsources,seeTab1.5,EconomicAnalysis,intheExcelworkbook.24

� 11

from19.1percentto25.1percent.Last,theshareofothercostsfellfrom62.6percentto

59.8percent.

Tables2and3decomposethecumulaPveroyaltyyieldbyqualityofdataandtype

oflicensorin2015and2016.WhilethetotalcumulaPveyieldfellfrom$14.5billionin

2015to$14.2billionin2016,thecomposiPonbarelychanged. AtthesamePme,the25

royaltyyieldsofsomeindividuallicensorsvariedalotfrom2015to2016.Forexample,

Ericson’sroyaltyyieldfellby$536million,from$1,701millionin2015to$1,165millionin

2016.Interdigital’sroyaltyyield,bycontrast,roseby$223million,from$432millionin

2015to$655millionin2016.

5.SensiPvityAnalysis

OurresultsdonotseemtobesensiPvetohowonetreatsthedata.Forexample,

whatwouldhappenifweassumethatonlysmartphonespaidroyalPesandallfeature

phonespaidnoroyalPesatall?ThenallthecumulaPveroyalPesof$14.2billionin2016

wouldbespreadacross1,474millionsmartphoneswithatotalvalueof$415.2billion

(insteadof1.97billionsmartandfeaturephoneswithavalueof$425.1billion).The

AverageCumulaPveRoyaltypersmartphonewouldrisefrom$7.20perphoneto$9.60

andtheAverageCumulaPveRoyaltyYieldwouldrisefrom3.3percentto3.4percent. 26

WhatwouldhappenifweimputedtheroyalPesoffirmsthatweknowearnsome

licensingrevenues,butthatdonotprovideenoughinformaPonforustoesPmatethose

revenuesonafirm-by-firmbasis?AsTable4shows,theresultswouldbeamodest

ThenumbersreportedinTable3areslightlydifferentofwhatwereportedabout2015inourSeptember2016release25

ofthedatabase.ThereasonisthatinthisupdatewehavecorrectedsomeofouriniPalesPmatesfor2015andaddedpatentholdersintothedatabase.

SeeTab1.3RoyaltyYieldSummary,intheExcelworkbook.26

� 12

increaseintheAverageCumulaPveRoyaltyYieldofsmartphones. Forexample,ifwe27

assumethatthesefirmsasagroupearned$1billioninlicensingrevenuesin2016,which

wouldbeagenerousassumpPon,thentheroyaltyyieldonasmartphonewouldincrease

from3.4percentto3.7percent(seethefirstrowinTable4).Ifwemaketheextremely

generousassumpPonthatthecombinedroyalPesofthesefirmscameto$2billion,then

thecumulaPveaverageroyaltyyieldwouldsPllonlybe3.9percent.

WhathappensifwerelaxtheassumpPonthateverysmartphoneshippedin2016

paidlicensingroyalPes?WhatifitwasthecasethatsomeOEMsevadedlicenses,such

thatthe$14.2billionisactuallyspreadacrossfewerthan1,473millionsmartphones?Asa

firststep,wefinddetermineanupper-boundevasionrate,whichweputat30percent. 28

WethencalculatetheAverageCumulaPveRoyaltyYieldassumingthatonly70percentof

smartphonespaidlicensingroyalPes.ThelastrowinTable4showstheresults.Underthe

assumpPonsthat:(i)allroyalPesarechargedonsmartphones(noneonfeaturephones);

and(ii)that30percentofsmartphoneproducPonevadesroyalPes,theaverage

cumulaPveroyaltyrateonasmartphonewouldincreasefrom3.4percentto4.9percent.

WhatifwepushedhardersPll,andmadethreestrongassumpPons:allroyalPes

areearnedonsmartphones;theevasionrateis30percent;andtheroyalPesfirmsinthe

“Other”un-enumeratedcategoryin2016equaled$2billion?Howhighcouldwepushthe

esPmateoftheAverageCumulaPveRoyaltyYield?AsTable4shows,theansweris5.6

percent.

6.ConcludingRemarks

SeeTab1.6,Sensi8vity,intheExcelworkbook.27

ForadiscussionofhowweesPmatedthatupper-boundevasionrate,seethefootnoteinTab1.6,Sensi8vity,inthe28

Excelworkbook.� 13

Acrucialinputtoanyacademicinquiry,policydebate,orindustrystudyisthefacts,

dispassionatelygathered.OurpurposeincreaPngthedatasetweoutlineinthisnoteisto

dothat.TheinformaPoninthisdatasetisthereforenotmeantasajudgmentofanysort

uponthemeritsoreffecPvenessofanyenPtyoritsoperaPons.Weinviteusersofthis

datasettosharetheirideas,suggesPons,andcorrecPonswithussothattheymaybe

includedinfutureversions.Aswehavedonewiththefirstversionofthisdataset,we

wouldliketoimproveupontheseesPmatesbymakingcorrecPonswhenwehaveerred

andtoobtainsuperiordatasourceswhentheyexist.Wewillbethefirsttoseek

improvementinourthirdediPon,andhopetobenefitfromthesupportofothers.

PerhapswithongoingcooperaPonwithinthecommunityoverPmewemayallgain

greaterclarityastothefuncPoningofindividualfirmsandtheindustry.

� 14

Table1:TypesofLicensorsClassifiedbyTypeandtheQualityofTheirData

(TabsintheWorkbookinparentheses.)LicensorsincludedintheCumula6veRoyaltyYieldes6mateinboldface.Technologyleadersinitalics.**Addedinthe2017update.Source:seetab1.7RevenuesbyLicensor,intheExcelworkbook.

Confirmed Documented Approximated Researched OtheridenPfiedfirms

PubliccorporaPon

Qualcomm(2.1)Ericsson(2.2)

Nokia(2.3)(incl.Alcatel-Lucent,

2.3.1)1

Interdigital(2.4)ParkerVision(3.9)UnwiredPlanet

(3.10)2VirnetX(3.11)

MicrosoL(2.5)

Philips(3.1)3Xperi(3.5)4

Rambus(3.6)AcaciaTechnologies

(3.7)Quarterhill(3.8)5

MarathonPatentGroup(3.12)IBM(3.13)**

Tivo(3.14)**

Technicolor(3.15)**

Blackberry(3.16)**

AT&T802.11(3.2)AT&TMPEG4(3.3)Broadcom(3.4)

Apple(6.0)Google(6.0)Infineon(6.0)

SamsungElectronics(6.0)

Siemens(6.0)TexasInstruments(6.0)

SonyCorp(6.0)LGElectronics(6.0)

PrivatecorporaPon

Huawei(5.6)

SISVELWireless(5.1)IPCom(5.2)7

PanOp6s-Op6s(5.3)2

IPBridge(5.4)IntellectualVentures

(5.5)Conversant(5.7)8

FormHoldings(6.0)11

FranceBrevets(6.0)12ETRI(6.0)13ITRI(6.0)14

LongitudeLicensing(6.0)15

MobileMediaIdeas(6.0)

Rockstar(6.0)VoiceAge(6.0)

RoundRock(6.0)

Patentpool

ViaLicensingAAC(4.1)

MPEGLAMPEG4(4.3)MPEGLAAVCH.264

(4.4)MPEGLAHEVC(4.9)**

HEVCAdvance(4.10)**

ViaLicensingLTE(4.2)6SISVELLTE(4.5)SISVELWiFi(4.6)ViaLicensingWCDMA(4.7)9

Vec6sWiFi(4.8)10VelosMediaHEVC

(4.11)**

� 15

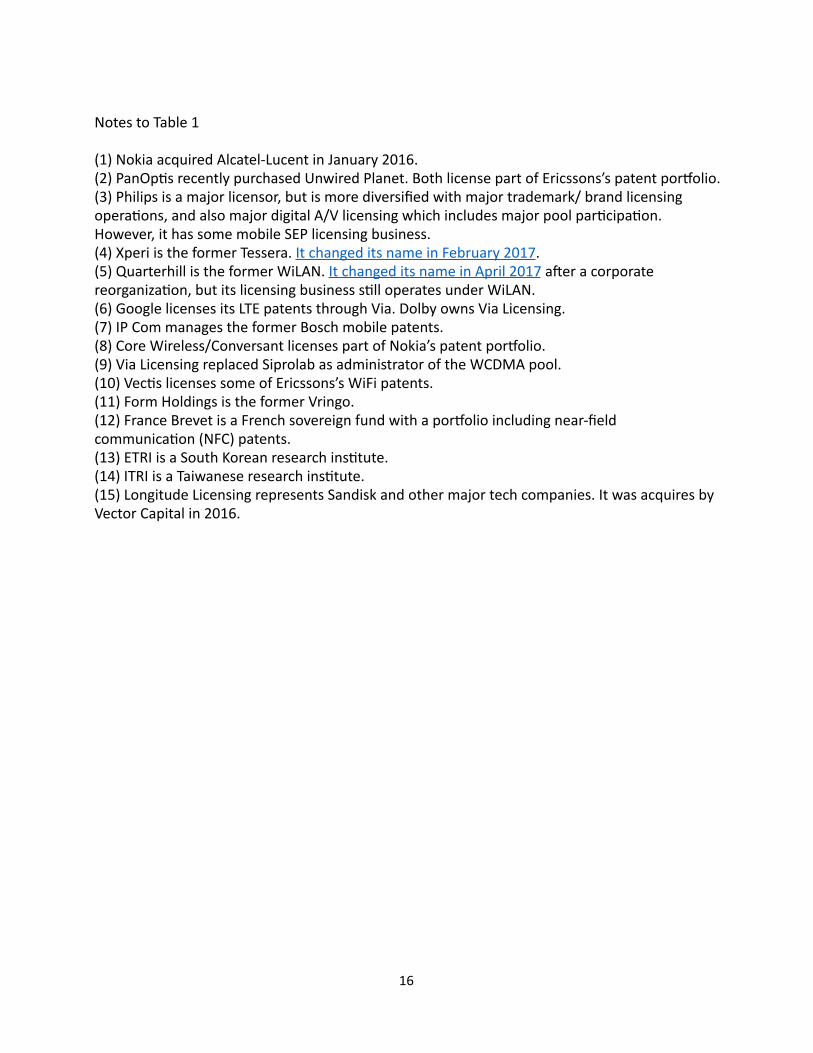

NotestoTable1

(1)NokiaacquiredAlcatel-LucentinJanuary2016.(2)PanOpPsrecentlypurchasedUnwiredPlanet.BothlicensepartofEricssons’spatentporjolio.(3)Philipsisamajorlicensor,butismorediversifiedwithmajortrademark/brandlicensingoperaPons,andalsomajordigitalA/VlicensingwhichincludesmajorpoolparPcipaPon.However,ithassomemobileSEPlicensingbusiness.(4)XperiistheformerTessera.ItchangeditsnameinFebruary2017.(5)QuarterhillistheformerWiLAN.ItchangeditsnameinApril2017a^eracorporatereorganizaPon,butitslicensingbusinesssPlloperatesunderWiLAN.(6)GooglelicensesitsLTEpatentsthroughVia.DolbyownsViaLicensing.(7)IPCommanagestheformerBoschmobilepatents.(8)CoreWireless/ConversantlicensespartofNokia’spatentporjolio.(9)ViaLicensingreplacedSiprolabasadministratoroftheWCDMApool.(10)VecPslicensessomeofEricssons’sWiFipatents.(11)FormHoldingsistheformerVringo.(12)FranceBrevetisaFrenchsovereignfundwithaporjolioincludingnear-fieldcommunicaPon(NFC)patents.(13)ETRIisaSouthKoreanresearchinsPtute.(14)ITRIisaTaiwaneseresearchinsPtute.(15)LongitudeLicensingrepresentsSandiskandothermajortechcompanies.ItwasacquiresbyVectorCapitalin2016.

� 16

Table2:Cumula6veRoyaltyYieldClassifiedbytheQualityoftheData(in2016)

Source:Seetab1.7RevenuesbyLicensor,intheExcelworkbook.

Type1Public

company

Type2Privatecompany

Type3PatentPools Total

Confirmed$10,679,127,886

(75.2%)- - $10,679,127,886

(75.2%)

Documented$828,185,000

(5.8%)- $378.780.681

(2.7%)$1.206.965.681

(8.5%)

Approximated$1,035,503,336

(7.3%)$655,360,000

(4.6%)- $1,690,863,336

(11.9%)

Researched$382,000,000

(2.7%)$145,683,346

(1.0%)$86,982,900

(0.6%)$614,666,246

(4.3%)

Total$12,924,816,222

(91.1%)$801,043,346

(5.6%)$465.763.581

(3.3%)$14.191.623.148

(100%)

� 17

Table3:Cumula6veRoyaltyYieldClassifiedbyQualityofData(in2015)

Source:Seetab1.7RevenuesbyLicensor,intheExcelworkbook.

Type1Public

company

Type2Privatecompany

Type3PatentPools Total

Confirmed$11,280,132,214

(73.6%)- - $11,280,132,214

(73.6%)

Documented$1,134,500,000

(5.7%)- $311.408.407

(2.6%)$1.445.908.407

(8.3%)

Approximated$871,263,710

(7,1%)$432,488,000

(4.5%)- $1,303,751,710

(11.7%)

Researched$245,000,000

(2.6%)$144,461,024

(1.0%)$86,982,900

(0.6%)$476,443,924

(4.2%)

Total$13,530,895,924

(89.1%)$576,949,024

(5.5%)$392,183,807

(3.2%)$14.506.236.255

(100%)

� 18

Table4:ASensi6vityAnalysisoftheAverageCumula6veRoyaltyYield(2016,smartphonesonly)

Source:seeTab1.6Sensi8vityintheworkbook.

%Unlicensed EffecPveSmartphonesRoyalPesChargedby"Other"licensorsasagroup($m)

Phones $0 $500 $1,000 $1,500 $2,000

0% 3.4% 3.5% 3.7% 3.8% 3.9%

5% 3.6% 3.7% 3.9% 4.0% 4.1%

10% 3.8% 3.9% 4.1% 4.2% 4.3%

15% 4.0% 4.2% 4.3% 4.4% 4.6%

20% 4.3% 4.4% 4.6% 4.7% 4.9%

25% 4.6% 4.7% 4.9% 5.0% 5.2%

30% 4.9% 5.1% 5.2% 5.4% 5.6%

� 19

�

� 20

!

!

� 21