CYPRUS UNIVERSITY OF TECHNOLOGY

FACULTY OF MANAGEMENT AND ECONOMICS

Bachelor thesis

THE MACROECONOMIC FACTORS THAT

AFFECT IN THE SHORT-TERM THE CYPRUS

SOVEREIGN BOND YIELDS

XENIA EFTHYMIOU

Limassol 2016

i

CYPRUS UNIVERSITY OF TECHNOLOGY

FACULTY OF MANAGEMENT AND ECONOMICS

DEPARTMENT OF COMMERCE, FINANCE AND SHIPPING

Bachelor thesis

THE MACROECONOMIC FACTORS THAT

AFFECT IN THE SHORT-TERM THE CYPRUS

SOVEREIGN BOND YIELDS

XENIA EFTHYMIOU

Professor Supervisor

Dr. Christos Savva

Limassol 2016

ii

Copyrights

Copyright © Xenia Efthymiou, 2016

All rights reserved.

The thesis approval by the Department of Commerce, Finance and Shipping of the Cyprus

University of Technology does not necessarily implies acceptance of the author's views on

behalf of the Department.

iii

It is with sincerest gratitude that I would like to acknowledge the support and help of my

Supervisor, Professor of Econometrics Dr. Christos Savva for supporting me throughout my

thesis with patience and encouragement. I deeply appreciate his continuous guidance,

constructive criticisms and valuable time. In addition, I would like to thank Nektarios

Michael, Doctoral Student of Econometrics for his eagerness and assistance. This thesis is

dedicated to my family. It is with heart-felt gratitude that I would like to thank them for their

love, support and strength all of these years.

iv

ABSTRACT

This report analyses the macroeconomic determinants that affect Cyprus Sovereign Bond

Yields short-term changes over the first quarter of 2001 to the third quarter of 2015 using an

Autoregressive Model of one latent factor with Cochrane–Orcutt procedure. Remarkable that

when Cyprus Economic Profile is considered different factors appeared to be influential. The

main findings support that changes in the conventional 3-Month Money Market Rate and

Unemployment Rate yield to an increase in Cyprus Sovereign Bond Yields. Additionally,

liquidity risk premium is supported as an additional determinant. In a nutshell, if Cyprus is

rated by Credit Rating Agencies as Moderate risk of high or low level (investment grade) or

substantial risk of low level (speculative grade) additional liquidity risk premium is required.

Whilst, a percentage change in Financial Soundness of Cyprus from 2012 onwards

deteriorates Cyprus Sovereign Bond Yields revealing liquidity risk premiums adjustments.

Finally, Policy Implications are discussed by primarily pointing the importance of minimising

unemployment rate and illiquid assets, especially non-performing loans.

Keywords: Sovereign Bond Yields, Cyprus Sovereign Bond Yields, Unemployment, Money

Market Rate, Credit Ratings, Financial Soundness Indicators, Cyprus Economy, Dynamic

Model, Cyprus, Macroeconomic Analysis

v

ΠΕΡΙΛΗΨΗ

Η μελέτη αυτή αναλύει τους μακροοικονομικούς παράγοντες που επηρεάζουν βραχυχρόνια

την απόδοση των Κυπριακών Κρατικών Ομολόγων για την περίοδο του πρώτου τρίμηνου το

2001 μέχρι και το τρίτο τρίμηνο του 2015 με την χρήση ενός Μοντέλου Αυτοπαλινδρόμησης

μίας χρονικής υστέρησης με την διαδικασία του Cochrane–Orcutt. Πρέπει να σημειωθεί ότι

όταν λαμβάνεται υπόψιν το Οικονομικό Προφίλ της Κύπρου, διαφορετικοί παράγοντες

παρουσιάζονται να επηρεάζουν την απόδοση των ομολόγων. Τα κύρια αποτελέσματα

υποδεικνύουν ότι ποσοστιαίες αλλαγές στα Τριμηνιαία Διατραπεζικά Επιτόκια και στα

Ποσοστά Ανεργίας οδηγούν σε βραχυχρόνια αύξηση στην απόδοση των Κυπριακών

Κρατικών Ομολόγων. Επιπρόσθετα ο παράγοντας ασφάλιστρο κινδύνου λόγω ρευστότητάς

παρουσιάζεται εξίσου να επηρεάζει την απόδοση των ομολόγων. Συνοπτικά εάν η Κύπρος

αξιολογείτε από τους Οίκους Αξιολόγησης ως μεσαίου ρίσκου επένδυση υψηλού ή χαμηλού

επιπέδου (επενδυτική βαθμίδα) ή ως σημαντικού ρίσκου χαμηλής βαθμίδας (κερδοσκοπική

βαθμίδα) οι επενδυτές απαιτούν ασφάλιστρο κινδύνου λόγω ρευστότητας. Αυτό το επιπλέον

ασφάλιστρο από το 2012 και μετέπειτα αναπροσαρμόζεται αρνητικά αναλόγως της

Οικονομικής Ευρωστίας της Κύπρου. Τέλος, γίνεται συζήτηση για τις Πολιτικές Επιπτώσεις

που έχουν τα αποτελέσματα της έρευνας με κυριότερο σημείο την ανάγκη για περιορισμό

των Ποσοστών Ανεργίας και των Μη-Ρευστοποιήσιμων Περιουσιακών Στοιχείων, ιδίως των

μη εξυπηρετούμενων δανείων.

Λέξεις κλειδιά: Αποδώσεις Κρατικών Ομολόγων, Αποδώσεις Κυπριακών Κρατικών

Ομολόγων, Ανεργία, Διατραπεζικό Επιτόκιο, Αξιολογήσεις Πιστοληπτικής Ικανότητας,

Δείκτες Οικονομικής Ευρωστίας, Κυπριακή Οικονομία, Δυναμικό Μοντέλο, Κύπρος,

Μακροοικονομική Ανάλυση

vi

TABLE OF CONTENTS

ABSTRACT ............................................................................................................................. iv

ΠΕΡΙΛΗΨΗ ............................................................................................................................... v

TABLE OF CONTENTS ......................................................................................................... vi

LIST OF TABLES ................................................................................................................. viii

LIST OF FIGURES .................................................................................................................. ix

ABBREVIATIONS ................................................................................................................... x

INTRODUCTION ..................................................................................................................... 1

1 Literature review ................................................................................................................ 3

2 Cyprus Profile .................................................................................................................. 11

2.1 Cyprus Economic Profile ........................................................................................ 11

3 Methodology .................................................................................................................... 14

3.1 Potential Determinants ............................................................................................ 14

3.1.1 GDP Growth Rate .............................................................................................. 15

3.1.2 Fiscal Conditions Class ..................................................................................... 17

3.1.3 Inflation Class .................................................................................................... 19

3.1.4 Competitiveness Class ....................................................................................... 20

3.2 Data description ....................................................................................................... 21

3.2.1 Cyprus Special Indicators .................................................................................. 22

4 Empirical analysis ............................................................................................................ 24

4.1 Core empirical sound macroeconomic variables ..................................................... 24

4.1.1 Baseline Specification ....................................................................................... 24

4.2 Adjusted Regression Model to Cyprus Economic Profile ....................................... 26

CONCLUSION ....................................................................................................................... 31

POLICY IMPLICATIONS ..................................................................................................... 33

vii

REFERENCES ........................................................................................................................ 35

APPENDICES ......................................................................................................................... 39

Appendix 1: Cyprus Sovereign Credit Ratings .................................................................... 39

Appendix 2: Moody’s Credit Ratings Guide ....................................................................... 40

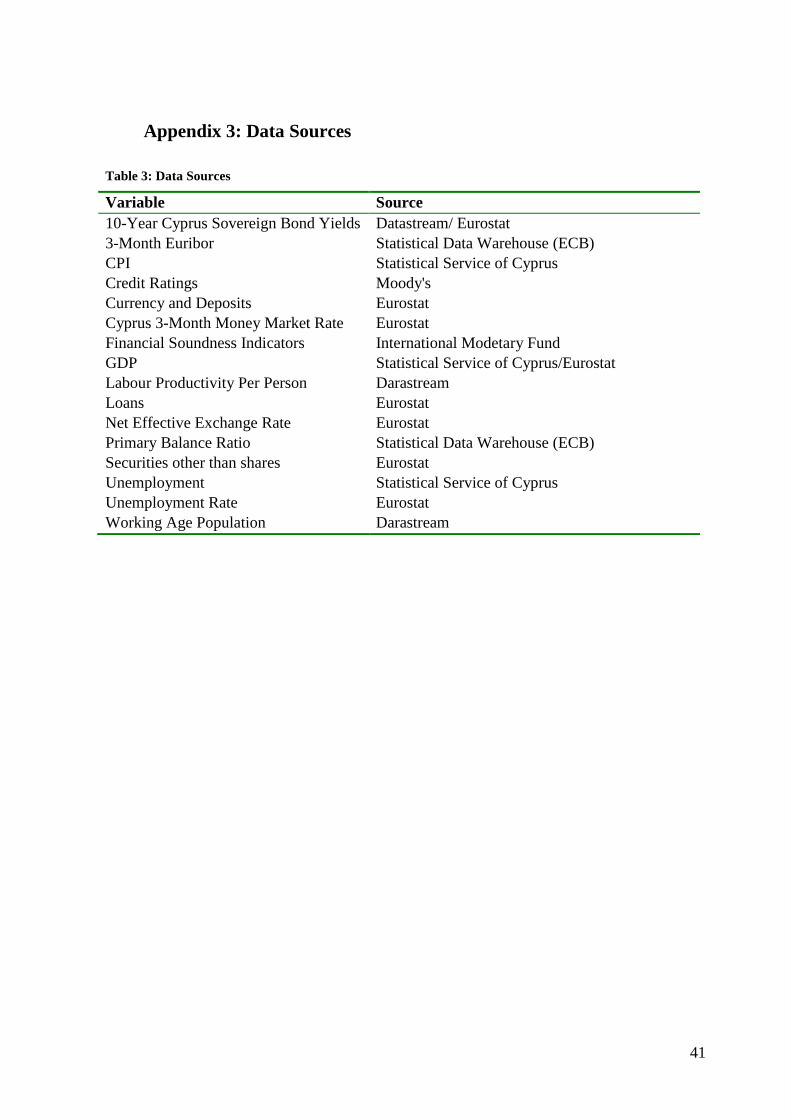

Appendix 3: Data Sources ................................................................................................... 41

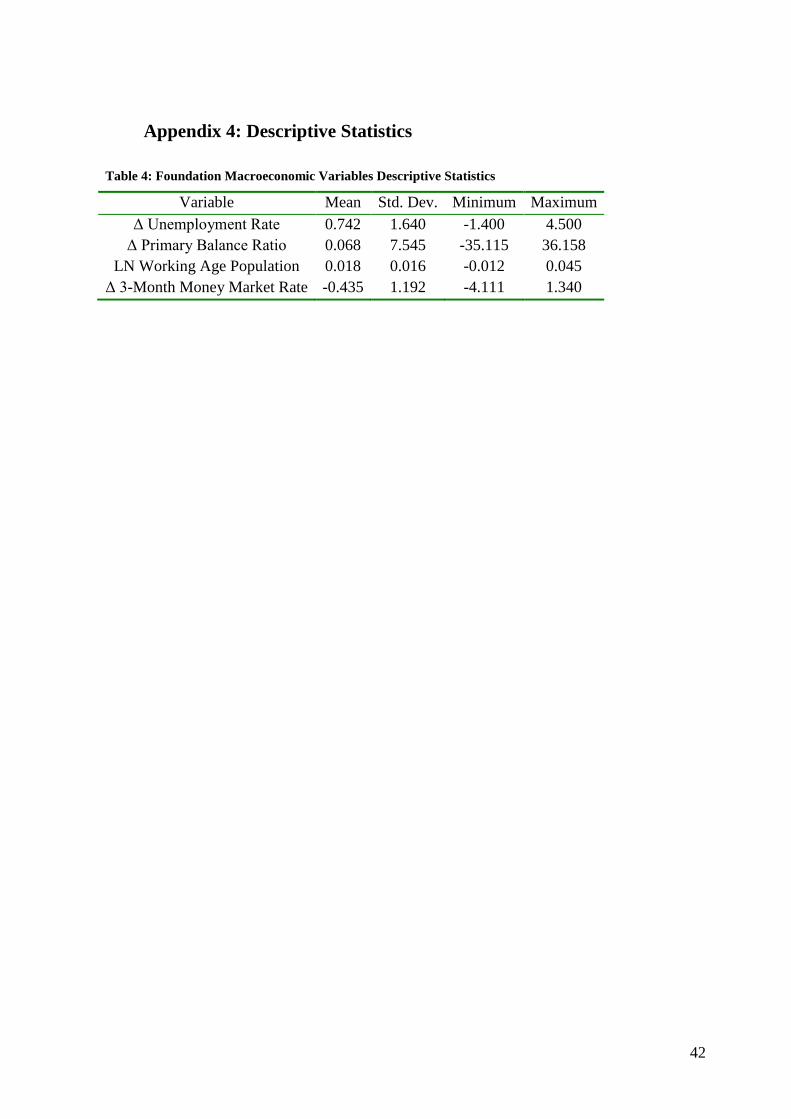

Appendix 4: Descriptive Statistics ....................................................................................... 42

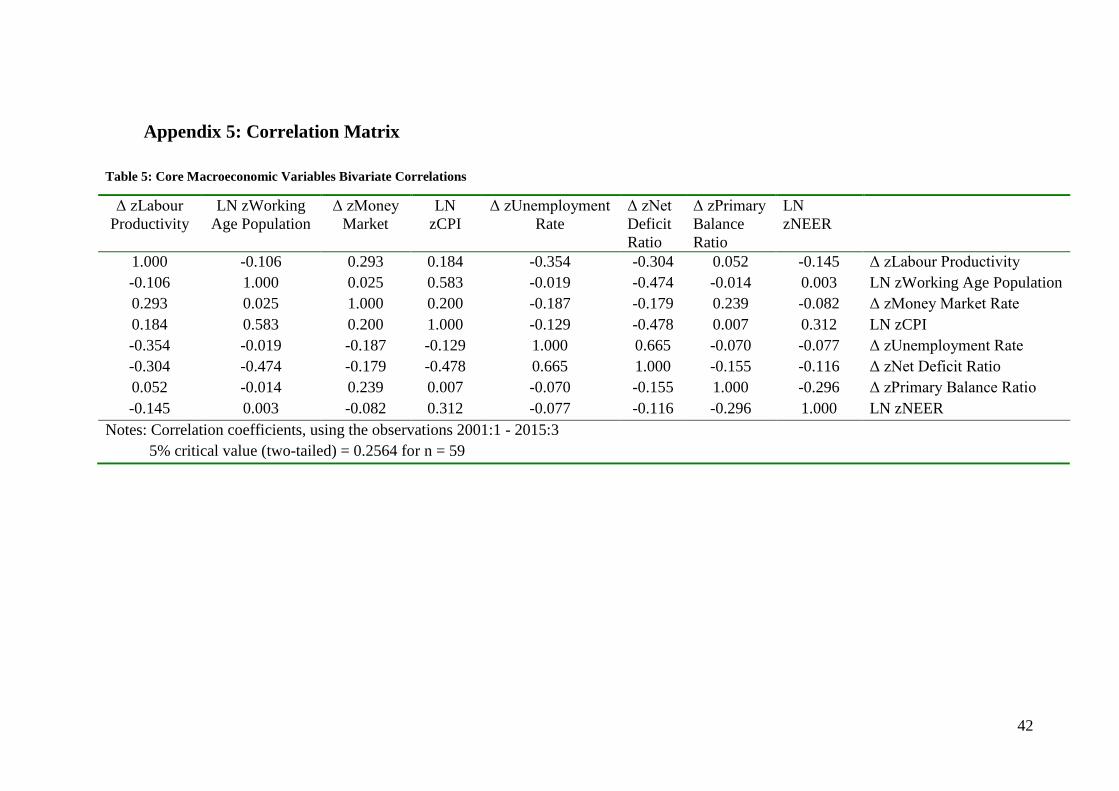

Appendix 5: Correlation Matrix .......................................................................................... 42

Appendix 6: Foundation Baseline ........................................................................................ 43

Appendix 7: Foundation Model Residuals Cyclicality ........................................................ 44

Appendix 8: Final Model Baseline ...................................................................................... 45

viii

LIST OF TABLES

Table 1: Moody’s Historical Sovereign Credit Ratings .......................................................... 39

Table 2: Moody’s Sovereign Credit Ratings Guide ................................................................ 40

Table 3: Data Sources .............................................................................................................. 41

Table 4: Foundation Macroeconomic Variables Descriptive Statistics .................................. 42

Table 5: Core Macroeconomic Variables Bivariate Correlations ........................................... 42

Table 6: Initial Model Baseline ............................................................................................... 43

Table 7: Final Model Baseline ................................................................................................ 45

ix

LIST OF FIGURES

Figure 1: Foundation Model Residuals Cyclicality (Autocorrelation Graph) ......................... 44

Figure 2: Foundation Regression Equation ............................................................................ 25

Figure 3: Suggested Regression Equation .............................................................................. 27

x

ABBREVIATIONS

CPI: Consumer Price Index

ECB: European Central Bank

GDP: Gross Domestic Product

1

INTRODUCTION

What are the macroeconomic determinants that affect the Cyprus government borrowing

costs is the short term? Overall, Cyprus it is a small country with openness to the global

financial markets which faced severe economic problems during the last years. Even though

Cyprus is a small country it is highly exposed to its banking system. The resent financial

crisis Cyprus faced was associated with high levels of unemployment, leverage and non-

performing loans as well as gradual downgrades by the credit rating agencies. Taking into

consideration the above as well that Cyprus left the assistance program earlier and enter the

capital markets, raised remarkable concerns to which extent these macroeconomic

determinants affected the Cyprus Sovereign Bond Yields.

Although, there is a considerable number of existing studies that explore the relationship

among macroeconomic determinants and sovereign bond yields in the long-term and some of

them pointed out the different impact of them in the short-term, however, there are no

existing studies that revealed solely the short-term determinants of nominal sovereign bond

yields. Therefore, there is a need to address a model which reveals the short-term

determinants of Sovereign Bond Yields; especially, a model that captures the special Cyprus

Economic Profile.

The main scope of this study is to examine the macroeconomic determinants that affect in the

short-term the Cyprus Sovereign Bond Yields in order to investigate how policy makers can

influence Cyprus borrowing costs. In order to shed light on this issue a Dynamic

Autoregressive Model (AR(1)) with Cochrane–Orcutt procedure for the yearly changes of the

Bond Yields from the first quarter of 2001 and the third quarter of 2015 was used. By using

this Dynamic model, the autocorrelation indications that appeared were taken into account.

Consequently, this study enhances the existing literature since it focuses non only in short

term drivers but explores the Country Specific Drivers according to the Cyprus Profile.

A foundation model as a first stage was conducted with Ordinary Least Squares with

Heteroscedasticity Consistent Standard Errors. Then this model was used as a foundation

model where other macroeconomic determinants that capture Cyprus Economic Profile were

employed to a Dynamic Autoregressive Model with one latent factor. The conventional

macroeconomics determinants that appear to impact the short-term changes of the Cyprus

2

Sovereign Bond Yields were differently than those when Cyprus Special Economic Profile

was taken into consideration.

The suggested model that considers Cyprus Economic Profile supports the following

findings. A percentage change in 3-Month Money Market Rate will lead to a 0.345 increase

in Cyprus Sovereign Bond Yields. A percentage change in Unemployment Rate would

increase Cyprus Sovereign Bond Yields by 0.399. The percentage change in the Financial

Soundness of Cyprus lowers bond yields by about 0.099. Whilst, if Cyprus is rated as Baa1

then Short Term Yields would increase. If Cyprus is rated as Baa3 then it the rates would

surge to a higher extent. Quite puzzling, if Cyprus is rated as Ba1 then it will lead to a

positive increase in yields but to a lesser extent than Baa3. However, taking into account that

Financial Soundness of Cyprus during the same period also adjust the liquidity risk premium

that Investors required it is reasonable. Precisely, when Cyprus is Rated as Baa1 then

Sovereign Bond Yields change by 1.179 percentage points. When Cyprus is Rated as Baa3

then Sovereign Bond Yields change by 1.348 percentage points and when is rated as Ba1

Sovereign Bond Yields change by 1.331 percentage points.

The rest of the study is structured as follows. Section 1 reviews the literature of the last

couple of decades. Section 2 illustrates Cyprus Profile and more precisely the Economic

Profile of Cyprus. Section 3 reveals the empirical analysis technique that would be employed,

the potential determinants that may affect Sovereign Bond Yields as well as the Cyprus

unconventional special determinants. Section 4 discuss the empirical analysis and points the

empirical findings. Then the next section concludes with the reveal for the Policy

Implications of the Empirical Analysis.

3

1 Literature review

The literature review of the macroeconomic determinants of sovereign bond yields it is

primarily concentrated in investigating the long term factors of sovereign bond yields on

panel data of advanced economies rather than single country studies. Remarkable that there is

a big part of the literature that concentrates on explaining the yields spreads1 among different

economies but this is not the scope of this particular research. Furthermore, the empirical

literature on investigating the macroeconomic factors that influence sovereign bond yields

can be divided into real-term analysis2 and nominal-term analysis. The current study will

focus on presenting the nominal-term empirical analyses for the last couple of decades and

will highlight couple key real-term studies.

To begin with, Cantor and Packer (1996) among others, revealed that Sovereign Credit

Ratings implying risks are in line with macroeconomic fundamentals. Overall, they depicted

six determinants that seem to play crucial role in determining Sovereign Ratings as follows:

per capita income; GDP growth; inflation; external debt; level of economic development and

default history. All in all, sovereign credit ratings strongly correlated with market-determined

spreads because they effectively summarize the information contained in macroeconomic

determinants. Despite the fact that most of the correlation seems to reflect comparable

1 For example, Attinasi, Checherita and Nickel (2009) used a dynamic panel model in order to explain the

factors that expand sovereign bond yield spreads vis-à-vis Germany in selected euro area countries between

the end of July 2007 and the end of March 2009. They concluded that higher expected budget deficits and/or

greater government debt ratios relative to Germany contributed to greater extent to government bond yield

spreads in the euro area. Additionally, announcements of bank rescue packages led some investors to

reexamine sovereign credit risk by transferring risk from the private financial sector to the government.

Another example, Bernoth and Erdogan (2012) investigated the determinants of sovereign bond yield spreads

among 10 countries of the Economic and Monetary Union of the European Union from the first quarter of

1999 and first quarter of 2010. Generally, the point out the need of time-varying coefficient models.

2 For instance, Engen and Hubbard (2004) by using predicted values of the fiscal position from the

Congressional Budget Office for the United States they depicted that a percentage point increase in Federal

Government debt to GDP, all else being equal, is expected to increase by three basis points the long run real

interest rate.

4

interpretations of publicly available information by the rating agencies and by market

participants; the above mentioned author discovered that opinions of rating agencies affect

independently the market spreads. Remarkable that, sovereign bond yields changed in the

expected direction with a statistical significant manner in the event of Rating Agencies

announcements of modifications in their sovereign risk opinion. Nevertheless, the authors

noted puzzling results regarding that rating announcements influence spreads in a greater

manner for below-investment grade sovereigns and rating announcements are expected to

have a higher impact than those that are less expected.

Later, Balduzzi, Elton and Green (2001) examined the effects of arranged macroeconomic

announcements on prices, trading volume, and bid-ask spreads by using intraday data from

the interdealer government bond market from the first of July 1991 to 29th of September

1995. They concluded that 17 announcements as measured by the surprise in the announced

quantity, had a significant impact on the price of at least one of the following instruments: a

three-month bill, a two-year note, a 10-year note, and a 30-year bond. Not to mention that the

effects vary significantly according to maturity. Remarkable that the prices of all instruments

react considerably to eight different types of announcements: Durable Goods Orders,

Housing Starts, Initial Jobless Claims, Nonfarm Payrolls, Producers Price Index, Consumer

Confidence, The National Association Of Purchasing Managers Index, and New Home Sales.

Moving on Gale and Orszag (2002) synopsise the results of the major existed literature back

then in order to examine the effects of long-term discipline and interest rates effects. They

point out that it is important to consider future deficits when examine the linkage among

deficits and interest rates. Out of 17 papers that consider future deficits, 12 of them resulted

in a statistical significance association between deficits and interest rates; whereas, four

found diverse effects. Only one paper did not support any effect from projected deficits on

interest rates unsuccessfully. Briefly, macro-econometric models recommend that one percent

increase in the budget to GDP would lead to an increase in long term interest rates by about

50 basis points after a year and about 100 basis point after 10 years.

As regards to Ang and Piazzesi (2003), they worked on a Gaussian model of the yield curve

with observable macroeconomic variables and typical latent yields variables. The scope of

their paper was the identification of how macroeconomic variables affect bond prices and

dynamics of the yields curve. The authors used various zero coupon bond yields maturities.

They limited their study in the period of June 1952 to December 2000. They differentiated

5

their work from previous Vector Autoregressive Models studies of yields and

macroeconomic variables since they imposed no-arbitrage assumptions. The term structure

model used consisted factors of inflation (CPI, Producer Price index of finished goods and

spot market commodity prices) and economic growth - real activity (unemployment,

employment growth rate, industrial production growth rate and index of Help Wanted

Advertising in Newspapers) alongside with latent variables. In order to reduce the system

dimensions, they used Principal Components Analysis and obtain the first Principal

Components generated from inflation factors and the same for real activity factors. They

demonstrate that macroeconomic indicators explain a substantial part of short term and

middle term yields of approximately 85%. However, macroeconomic factors explanation

power shrinkages on explaining long-term yields with an explanation of about 40%.

On the contrary, Goldberg and Leonard (2003) analysed the United States and German

sovereign bond markets in order to define the economic announcements that impact

sovereign bond yields. This examination has taken place on the hourly changes of the

sovereign bond yields during the third of January 2000 to the 28th of June 2002. The outcome

of the above mentioned examination was: economic announcements influence significantly

bond yields. Main findings consist of that European Markets were independent on United

States financial markets. Sovereign bond yields are expected to increase on announcements

of better economic conditions or greater inflation than expected. The greater effects that were

found to impact both markets consisted of labour market announcements on payrolls,

unemployment and initial unemployment claims as well as advance readings of real GDP.

Then Ardagna, Caselli and Lane (2004) explored the effects of fiscal policy, precisely:

government debt and deficit on long-term interest rates. They used panel data from 1960 to

2002 of 16 OECD countries. The model included the variables of primary deficit and Public

Debt to GDP as well as other relevant control variables such as 3-month the Treasury bills

rate, the inflation rate, the GDP growth rate and the global indicators of world fiscal

imbalances. The study revealed that one percentage point increase on the Primary Deficit to

GDP ratio leads to a rise of 10 basis points in 10-year government bonds nominal interest

rates. In addition, in a Dynamic Vector Autoregressive Models the same event leads to a

cumulative increase of approximately 150 basis points after 10 years. The lag length of the

model was two. Briefly, the effect of such event is greater when considering that a positive

shock to the primary deficit has on expected future fiscal policy and macroeconomic

6

variables in the long term. Debt influence interest rates on non-linear way; whereby,

exclusively countries with above average levels of debt can influence interest rates by an

increase in debt. Furthermore, the study investigated that World fiscal policy is statistically

important on influencing each country’s interest rates.

Meanwhile, Izák (2004) explored the relationship among debt, deficit, inflation, growth and

interest rates by using panel analysis with fixed effects of four transition countries: Czech

Republic, Hungary, Poland and Slovakia between 1994 and 2002. It was assumed that the

variables influencing debt dynamics would also impact the interest cost of the debt. The study

suggested that one percentage point increase in inflation will lead to a 17 basis point increase

in interest rates. As per growth, the results showed that a percentage point increase in growth

will lead to 37 basis points increase in interest rates. Furthermore, one percentage point

increase in the primary balance results will lead to 12 basis points decline in interest rates.

As regards debt variable, the author points out puzzling results.

Next, Dai and Philippon (2005) develop an empirical macro-finance model that combines a

no-arbitrage affine term structure model with a set of structural limitations that let to classify

fiscal policy shocks and identify the effects of these shocks on the prices of bonds of different

maturities. The pricing equation included: federal funds rate; government deficit; inflation;

real activity and one latent factor. The findings of the study depicted that government deficits

influence long-run interest rate. In brief, one percentage point increase of Deficit to GDP

ratio rises by 35 basis points after three years the 10-year rate. This showcase greater

expected spot rates as well as risk premium on long rum bonds. Overall, fiscal policy shocks

represent up to 13 percent of the variance of predicted errors in bond yields.

Afterwards, Aisen and Hauner (2008) analysied a large sample of 60 advanced and emerging

economies from 1970 to 2006 they re-examined the relationship between budget deficits and

interest rates. To address the association, they applied a Generalised Method of Moments

system. In short, the model consisted lagged dependent variable in order to account for

delayed adjustment and other variables to control depending on the country profile. For

perfect capital mobility, the nominal interest rate is determined exclusively by external

factors such as foreign nominal interest rate, expected depreciation and country specific risk

spread. Whilst, closed economies are determined merely by domestic factors such as

expected inflation, real money supply which affect interest rates temporarily through liquidity

and real interest rates. The first two dynamics are captured through real GDP growth while

7

the savings rate is captured by the constant and the budget deficit. The findings showed that

budget deficits are highly significant and positive affecting interest rates. In detail, one

percentage point increase in budget deficits to GDP leads to an increase of interest rates of

about 26 basis points. Moreover, they remarked that this effect depends primarily on

interaction term and is only significant under certain conditions. More precisely, the

conditions are the following: if deficits are high; major part of them is financed domestically;

or interact with domestic debt; financial openness is low; interest rates are liberalised or

financial sector is less developed.

In the meantime, Tam and Yu (2008) modelled the sovereign bond yield curves of the United

States, Japan and Germany using data from January 1992 to March 2006 by using a new

macro-finance framework. More precisely, the yield curve model used was a combination of

latent factors and macroeconomic variables: capacity utilisation; policy rate; and inflation.

The authors supported the dynamic interaction among the yield curve latent factors and

macroeconomic variables for the United States and Germany. However, the failed to proove

the same for the Japanese economy. Moreover, this finding may be biased due to years of

ineffectiveness monetary policy in Japan during persistent depression. With the help of a

DCC-GARCH model first proposed by Engle (2002) the authors supported the existence of

cross-country correlations of the bond markets of the examined countries.

Later, Ardagna (2009) studied the changes in interest rates (government and corporate bonds)

and stock market prices before and after the periods of large changes in fiscal policy. To

address this, she used panel data of OECD countries between 1960 and 2002. The paper

revealed that interest rates of 10-year government bonds plunge approximately by 124 basis

points during events of fiscal consolidations. In contrast, during years of loose fiscal policy,

interest rates surge by 162 basis points. Noteworthy that these events affect 3-month Treasury

Bills too. These findings depend on countries’ initial fiscal conditions and on the type of

fiscal consolidations. Specifically, fiscal adjustments that occur in years with high levels of

government deficit, which are applied by mitigation in government spending and generate a

permanent and remarkable decline in government debt are associated with greater reductions

in interest rates. In contrast, during years of fiscal expansions, the interest rates of 10-year

government bonds go up no matter the fiscal conditions of the country.

Whilst, Laubach (2009) examined the relationship among long-horizon forward rates and

future federal government deficits and debt in the United States between 1975 and 2005. The

8

author used three different interest rates series as dependent variables; 5-years-ahead 10-year

forward rate, 5-year-ahead 10-year forward rate and 10-year constant maturity Treasury

Yield. Projections published by the Congressional Budget Office were used as expectations

of future fiscal policy. The study points out that a percentage point increase in the projected

deficit to GDP ratio leaded to an increase of the forward rates of 5 and more years ahead by

20 to 30 basis points. Likewise, a percentage point increase in the projected debt to GDP

leaded to an increase of 3 to 4 basis points.

Regarding to Baldacci and Kumar (2010), they reviewed the influence of fiscal deficits and

public debt on long-term interest rates between 1980 and 2008 from a panel data of 31

Advance and Emerging economies. The study concluded that greater deficits and public debt

lead to substantial increase in long-run interest rates. This study differentiates from all others

due to the fact that this paper addressed that the above magnitude depends on the country

specific factors: the initial fiscal, institutional, other structural conditions, and spill-overs

from worldwide financial markets. All in all, high levels of fiscal deficits and public debts are

likely to put substantial upward pressures on sovereign bond yields in many advanced

economies over the medium term. Moreover, the Regression Analysis constituted short-term

interest rates to control for monetary policy effect of the term structure, CPI for inflation

purposes and output growth to control for the country’s cyclical conditions. The authors run

an auxiliary regression without taking into consideration countries special characteristics with

lagged dependent variable to separate short term and long-term effects with a Generalised

Method of Moments of the above discussed model. The results showed that the overall effect

were comparable to that found in the static model (fixed effects Least Squares estimates) with

the size of the short-run impact of government deficits being less than one third of the overall

effect.

At the same time, Gruber and Kamin (2010) research the relationship among long-term

sovereign bonds yields, fiscal balance and government debt in the OECD from 1988 to 2007

with a dynamic panel approach. Due to the endogeneity of fiscal positions to the business

cycle the authors used forwards projections of the fiscal positions. The control variables that

were included through the model consist of: short-term interest rates; lagged dependent

variable; two-year ahead projected rate of real GDP growth and CPI inflation; constant term;

fixed period and effects. The coefficients of short-term interest rates, inflation and GDP

growth are positive and statistical significant. On the first hand, the findings revealed that as

9

per G7 panel regression one percentage point increase in structural deficit to GDP ratio

increases by 15 basis points government bond yields in the long-term; whereas one

percentage point increase in net debt to GDP ratio increase bond yields by 2 basis points. On

the other hand, OECD panel fiscal effects are approximately the half of these estimated for

G7.

Noteworthy, Poghosyan (2012) developed cointegration techniques on explaining long-term

and short-term determinants of Sovereign Bond Yields in a panel data of 22 advanced

economies from the 1980 to 2010. Despite the fact that this paper investigated the

determinants of the real bond yields this paper is worth mentioning since it is one of the few

papers that examined short-term factors of sovereign bond yields. The results showed that, in

the long-term the yields rise approximately to two basis points in reaction to one percentage

point of the ratio of Government Debt to GDP; in reaction to one percentage point increase in

potential growth rate the yields go up to 45 basis points. In contrast, in the short-term there is

discrepancy of the sovereign bond yields from the level determined by the long-term

fundamentals. There is a positive effect on the sovereign bond yields in reaction to changes in

Debt to GDP ratio, Real Money Market Rate and negative effect on Inflation changes.

Inversely, the negative influence of growth rate and the Primary Balance Ratio is weaker.

However, approximately half of the discrepancy from the long-term equilibrium adjust in one

year. The paper concluded that sovereign borrowing costs of some euro area countries deviate

from the equilibrium level defined by macroeconomic fundamentals after the crisis.

Remarkable, Ichiue and Shimizu (2012) investigated the determinants of real long-term bond

yields. This paper was discussed through the Literature Review despite the fact that the

authors examined the factors affecting real bond yields since throughout this research a lot of

techniques were adopted from the authors. The authors developed cross-country panel data of

10 developed countries during 1990 and 2010. In order to address endogeneity, they have

used forward interest rates and numerous forecasts. The independent variables employed

through the model consist of: fiscal conditions; foreign borrowings; labour productivity;

demographics and inflation uncertainty. The findings suggest that when an increase in

government debt is financed entirely by foreign borrowing the increase in the forward real

interest rate is around three times when it is finance domestically. Furthermore, aging

expectations tends to lower yields. In contrast, primary balance effects are insignificant and

current account balance provides no further information beyond net foreign debt.

10

Finally, Malešević Perović (2015), examined government debt and primary balance

influences on long-term government bond yields in 10 CEE countries from 2000 to 2013. To

address any influences, the author generated a static panel model where despite government

debt to GDP and Net Government Borrowing/Lending to GDP ratio included through the

model other control variables such as GDP growth, Inflation and Money Market Rate.

Noteworthy that those control variables were statistical significant except of Inflation at a 5

percent significance level. Short term interest rates appear to have negative impact, whereas

the other two control variables have positive. However, the scope of this study was not to

address the impact of these variables and they were not discussed further throughout the

study. The findings of this papers are tested throughout an extensive variety of specifications.

The study lead to the finding that one percentage point increase in stock of government debt

leads to an increase in government bond yields of approximately 2.7 to 4 basis points;

whereas, one percentage point increase in primary deficit to GDP ratio leads to an increase in

government bond yields of 12.9 to 24.3 basis points. The author investigates and finds

significant non-linearities on the debt and interest rate relationship. Precisely a threshold of

30% is remarked as the point that if it exceeded then it turns the relationship into positive.

11

2 Cyprus Profile

Statistical Service of Cyprus (2012) provided a short country profile revealing key aspects of

Cyprus Profile. More precisely, Cyprus is a small island on the crossroads of Africa, Asia and

Europe. The independence of Cyprus was gained in 1960 by a Britain rule; however, in

nowadays an approximately area of 40 percent is occupied from 1974. In May 2004 the

Republic of Cyprus became a full member of the European Union and in January 2008 the

country joined the Eurozone.

2.1 Cyprus Economic Profile

In brief, Statistical Service of Cyprus (2014) outlines the crucial points need to be framed in

this section in order to adapt a clear view of the Cyprus Economic Profile. Initially, Cyprus

prior to the global economic crisis experienced substantial economic growth alongside with

low levels of unemployment and generally steady macroeconomic conditions. These positive

economic conditions proved to worked as a boomerang for the forthcoming economic issues

since excessive credit and consumption was taking place. Subsequently, the accumulated

credit lead to the well-known severe macroeconomic imbalances. As economic crisis

emerged, these imbalances deteriorate and let Cyprus with an egregious economic crisis

which was worsen during spring of 2013. As characteristically Statistical Service of Cyprus

(2014) points out “Indicatively, the economy exhibited a contractionary path since 2011,

while unemployment followed a rapidly increasing trend since 2008.”

Further to the excessive debt levels Cyprus had, other catalytically events lead Cyprus outside

of the international capital markets in spring of 2011 as follows: Firstly, Insufficient

regulatory and supervisory framework. Secondly, Excessive credit expansion of the financial

sector. Not to mention, Panayi and Zenios (2015) findings that foreign depositors held the

primary part of Cyprus Banking Sector Assets. Bank assets were 8 times bigger than Cyprus

GDP. Thirdly, Cypriot banks’ exposure to Greek economy and Greek sovereign bonds.

Astonishing, Stephanou (2011) warned for the forthcomings and presented adjustments

needed to be taken in order the banking system in Cyprus to be under control. Last but not

least, extensively loose fiscal policy that led to rapid deterioration in public finances.

12

In addition, the bad economic position Cyprus held deteriorated even more and led to a

plunge in March of 2013. At that time, ex Laiki Bank collapsed and Eurogroup decided the

recapitalisation of the Bank of Cyprus through creditors participation (bailed-in of

depositors). The main factors that influence these events were the Eurogroup decision for

Private Sector Involvement including among others “haircut” on Greek Government debt

holdings in autumn of 2011, along with the substantial delay in the submission of a request

for financial support by the European Stability Mechanism and the International Monetary

Fund. Subsequently, Cyprus Banking Sector deteriorated rapidly and substantially, while real

economy faced difficulties with the disposable income of Cypriot citizens and their affluence

being decreasing.

In short, the agreement that was established with Programme Partners on a macroeconomic

adjustment Programme, the well-known Memorandum of Understanding had as a main scope

to address the challenges in key sectors of the economy. It was a decision taken under caution

since it was important at the time to regained consumer’s as well as investor’s confidence,

and among others to bounced back the economy to steadiness. Overall, the Memorandum

addresses challenges in three major extents: fiscal; financial and structural issues.

On the whole, Cyprus held investment grade levels of credit ratings with low risk before the

third quarter of 2011. However, from then onwards Cyprus credit rating incrementally

downgraded and reached the lowest point during the first quarter of 2013 to the third quarter

of 2014 with speculative rating of very high credit risk. Afterward the rating bounce back to

high credit risk. In fact, Cyprus was exposed to Credit Rating agencies announcements the

last couple of years3.

Panayi and Zenios (2015) sum-up economic crisis impact to the macro-economy between

2011 and 2014: The economic shrinkage was approximately a cumulative percentage point of

11% and the the unemployment rate peaked during this period at 17%. In addition, they

3 The Credit Ratings were obtained from the historical data of Moody's Investors Service, Inc. The particular

rating agency is one of the biggest and well-respected credit rating agencies around the world. There is a

debate for the timeliness and accuracy of the Credit Rating Agencies but this analysis would not explore and

identify any issues according to these debates. For example, see Bae, Kang and Wang (2015), Cantor and

Packer, (1996) and Bae, Kang and Wang, (2015).

13

remarked real estate bubble that emerge years before and the financial crisis and the crucial

role it had to the economy collapse.

Currently, the Memorandum was concluded on 31st of March 2016 and Cyprus no longer

receives financial assistance as European Stability Mechanism (2016) points out. The Cyprus

economy bounce back quickly and recovered before than expected. Therefore, from the 10

billion euros projected at the beginning only 7.3 billion euros were used. During the

Memorandum Period Cyprus regain economic growth and repair public finances rapidly. The

main problem of the crisis which was the financial sector was restructured, recapitalised and

downsized. In addition, the legal framework and the supervisory was updated. Also, Cyprus

returned to the bond market and regained back the investors trust. However, remaining puzzle

to the economy are the high levels of Non-Performing Loans.

14

3 Methodology

3.1 Potential Determinants

To put in a nutshell, during the last couple of years the majority of the literature focused on

investigating the long-term relationship among fiscal positions and sovereign bond yields. A

major part of these studies pointed out that there is a threshold where if it is reached the fiscal

deficits impact sovereign bond yields and that budget deficits in some cases appeared to

impact the yields too. However, there is not a consensus. Others, revealed the

macroeconomic announcements that immediately impact sovereign bond yields; whereas

some others pointed out the impact of world conditions.

In a synopsis of the previous literature and a consideration of the Cyprus Profile an analogous

model would be employed. In this study we followed the results of Ang and Piazzesi (2003)

who they find out that macroeconomic determinants can explain a substantial part of short

term and middle term sovereign bond yields. More precisely, macroeconomic factors have an

explanatory power approximately of 85%. With this in mind as well as Tam and Yu (2008)

finding that a macro-finance framework had dynamic interaction among the yield curve latent

factors and macroeconomic variables for the two examined countries among three; the model

baseline will be constructed into two different phases: The first one consists of identification

of the core empirical sound macroeconomic variables that affect most of the countries; The

second step would try to shed light in the determinants that affect short-term changes in

sovereign bond yields according to Cyprus Economic Profile since it is expected that a large

part of the dependent variable explanation would be undefined. All in all, in order to capture

the best possible macroeconomic determinants of Cyprus sovereign bond yields a dynamic

model that captures Cyprus Economic Profile along with the classic variables would be

generated.

Therefore, this study will differentiate from all previous studies to the extent that it will

concentrate on revealing the macroeconomic determinants that affect a single country,

Cyprus. In short, a Dynamic Model will be employed in order to capture special country

characteristics. In spite of this research, short-term factors would be examined rather than

long-term vastly tested determinants.

15

Before moving on the econometric analysis in this section, potential determinants of short-

term changes in Cyprus Sovereign bond yields would be discussed. The empirical analysis

would be based on key determinants that Poghosyan (2012) tested among others. More

precisely, Debt to GDP ratio, Money Market Rate, Inflation (CPI changes). GDP growth rate

and Primary Balance Ratio. In accordance to Ichiue and Shimizu (2012) who separated the

potential factors in five different classes: Fiscal Conditions, Foreign Borrowing, Labor

Productivity, Demographics, and Inflation Uncertainties (Inflation), the potential

determinants would be divided into analogous type of classes. More precisely the classes

would be the following: Fiscal Conditions, Labour Productivity, Demographics and

Competiveness.

Despite the fact that these papers based their investigation on the identification of the

determinants of real yields we assumed that the factors that may affect real yields may

perhaps affect nominal yields too. Recalling Fisher’s equation that states that nominal rates

are equal to the natural rate of interest (real interest rate) and the inflation. We assumed that

nominal sovereign bond yields would be impacted by events in real activity and inflation.

3.1.1 GDP Growth Rate

Sovereign bonds are substantially impacted in the long-term from the real GDP growth rate.

With regards to Claeys, Moreno and Suriñach (2012) economic growth influence private

investment demand; which consequently, impacts positively the supply of corporate bonds.

Moreover, government bonds supply decreases since GDP growth increases the tax revenues

in the meantime and especially in extremely indebted countries doubts of unsustainable debt

positions increases. Hence, this means that government bond yields are lower.

Specifically, as Ichiue and Shimizu (2012) stated that GDP growth rate should be

decomposed into two variables, the growth rate of GDP per working age population (Labor

Productivity Class) and the growth rate of working age population ratio (Demographics

Class). These variables will need to be discussed separately. The reasons are: the complexity

of the economy and the effects of other channels rather than the physical rate of interest rates

which does not allow any investigation and consideration of their implications as a unified

variable. As a consequence, the Labor Productivity Class as well as the Demographics Class

would be employed in order to proxy the variables discussed above. The main scope for this

induction would be the examination whether these variables impact significantly Cyprus

Sovereign Bond Yields in the Short-Term.

16

3.1.1.1 Labour Productivity Class

Considering labor productivity, Ichiue and Shimizu (2012) claim that in respect to the natural

theory an improvement in labor productivity growth rate leads to an uptrend in real interest

rates and thus impacts nominal interest rates too. The extent to which it will impact nominal

yields depends on the inflation.

3.1.1.2 Demographic Class

In this section the variable of growth rate of working age population would be employed.4 As

suggested by Ichiue and Shimizu (2012), demographics are believed to have the ability to

affect real interest rates through multiple channels:

On the first channel, aging population may put descending pressure on interest rates. This is

supported as follows: aging population drops the marginal productivity of capital through a

plunge in labour supply and declines investment demand.

On the other channel, they assert that aging population is reputed to have upward pressure on

long-term interest rates. This was based on the life cycle theory which as the authors states

people tend to spend their savings after their retirement. Hence, long-term interest rates will

be impacted upside through the decrease of the savings rate. Not to mention that, aging

population has upward pressure on long-term interest rates through prospects for “fiscal

deterioration” triggered by collapse of tax revenues and rising social security spending.

Either way, in practice this is not always supported. For example, Ichiue and Shimizu (2012)

tested this in the US and Japan but they found out that elderly own a higher amount of

financial assets than other age population group. All in all, even if the life cycle theory holds,

the decrease in financial assets may be supported by the fact that the lifespan of elderly is

shorter; thus, their duration on investment is lower they tend to have lower risky assets as

they will not be benefit from them due to the high volatility of those assets in the short-run

(Poterba, 2001).

4 For the period of 2000 to 2003, the only available data for the Working Age Population were the average

annual rate. In spite of these circumstances, the Working Age Population for the missing quarters were

obtained by using an average growth model to estimate the working age population during the missing

quarters.

17

3.1.2 Fiscal Conditions Class5

3.1.2.1 Sovereign Debt and Deficit Ratio

It is reputed that fiscal debt and deficit may influence sovereign bond yields through multiple

perspectives. As per Malešević Perović (2012), in the short-term a rise in government deficit

enhances aggregate demand, which subsequently increases interest rates. Likewise, an

increase in government debt affects aggregate demand over wealth effects on aggregate

consumption. Gruber and Kamin (2010) reveal that a compensation is needed in bond yields

when an increase in debt causes doubts that the government may default. As Baldacci and

Kumar (2010) and Ardagna, Caselli and Lane (2004) reveal, uncertainties regarding the

economic activity in combination with enormous deficits and debt may well lead to credit

risk premium; therefore, higher fiscal bond yields. All in all, taking into account the above

perspectives, sovereign bond yields are expected to rise when there is an upward trend in debt

and deficit6.

Overall, in theory the relationship among fiscal conditions and interest rates may be

expressed by two variables: Debt to GDP and Deficit to GDP. Precisely, Ardagna, Caselli

and Lane (2004) mentioned that even if you believe that one of them is important it is

valuable to include the other variable for controlling reasons as well as interactions between

them.

5 Among this class, two critical variables are omitted due to data availability. Firstly, Budget Deficits are

reputed to affect sovereign bond yields. A countless part of the empirical literature was based on exploring

and proving the relationship among Budget Deficits and Sovereign Bond Yields. However, due to the lack of

available information this will not be tested throughout this research. Secondly, foreign borrowing was not

tested. Funding sources are suggested as explanatory influences on government debt effects on sovereign

bond yields. However, due to the lack of available information this determinant will not be tested.

6 Noteworthy, Baldacci and Kumar (2010) revealed that over the medium-term massive amounts of fiscal

deficits and public debts are expected to have upward pressures on sovereign bond yields of advanced

economies. Other studies explored the fiscal positions relationships with sovereign bond yields stressed out

that there is a non-linear effect. If a threshold is reached then the sovereign bond yields are affected. For

example, Ardagna, Caselli and Lane (2004). Throughout the examine period Cyprus Held high levels of Deficit.

Thus, it would not be examined any existence of non-linearities. Not to mentioned that those papers tested

long-term relationships.

18

3.1.2.2 Primary Balance and Fiscal Balance Ratio

Not to mention that, Ichiue and Shimizu (2012) explained that fiscal balance contains finance

expenses (interest payments). An increase in interest rates is expected to cause deterioration

in fiscal balance. As a consequence, using fiscal balance in the regression will end up

including a “reverse causation”; hence, fiscal balance may well be overestimated. To get rid

of this endogeneity bias Primary Balance should be used as a flow variable. Primary deficit

rather than total deficit was used by Ardagna, Caselli and Lane (2004) in order to capture in a

better way the independent changes in fiscal policy.

The model will employ General Government Deficit to GDP and Primary Balance to GDP as

independent variables.

3.1.2.3 Gross Government Deficit and Net Government Deficit Ratio

There is a controversial discussion on whether Gross Government Debt or Net Government

Debt influence substantially sovereign bond yields. The theoretical side suggest that net debt

is the variable of importance. In respect to Ichiue and Shimizu (2012) they support of the

above argument as follows; if debts can be repaid by the financial assets held by the

government, it is proper to consider that the default risk effect can be determined by net debt.

On the other side, others dispute that due to the illiquidity of financial assets held by the

government; gross government debt believe to be a better indicator.

Taking into consideration the above, Gross Government Deficit would be adjusted to Net

Deficit after deducting the most liquid and sound assets7.

3.1.2.4 Unemployment Rate

Recalling basic economics, an increase in unemployment rate leads to higher government

spending. In order to cover the unemployment needs with different unemployment benefits,

government increases its spending, while government income tax is facing a downfall. All in

7 The distinction between the appropriate assets to be deducted from Consolidated General Government Debt

was adopted from Eurostat’s (2014) suggested asset classes. In short, Cyprus Maastricht Debt was adjusted

from currency and deposits, securities other than shares (excluding financial derivatives) and loans. It should

be noted that Loans comprise of Non-Performing Loans. This part of Loans could not be excluded due to

limited data availability.

19

all, in order to bounce back the economy, the government is most likely to choose to borrow

instead of imposing reductions upon other government spending. Under these circumstances,

private spending drops, as well as private investment and GDP diminishes. Overall, an

increase in unemployment rate increases bond yields through the channel that high levels of

unemployment rates are an indication of financial distress.

Throughout the Literature Review of the last couple of decades the relationship between this

variable and the sovereign bond yields was not empirically tested. Instead, existing literature

have tested United States and Germany’s economic announcements and their influence on the

bond yields as a whole (For example se Balduzzi, Elton and Green (2001) and Goldberg and

Leonard (2003)).

3.1.3 Inflation Class

Taking into account Gruber and Kamin (2010), inflation expectations play a significant role

too on fiscal debt relationship with sovereign bond yields. A climb in sovereign bond yields

is mandatory when possible concerns that the central banks will “monetize” sovereign debt

and deficits exists as they may perhaps lift inflation expectations.

3.1.3.1 Inflation Uncertainty

Even more, inflation uncertainty is represented within the risk premium in interest rates.

Given that Wright (2011), found a high and positive relationship among long-term inflation

uncertainty and the term premiums on nominal bonds, hereby confirm the above statement. In

a nutshell, Piazzesi and Schneider (2006) asserted that investors require compensation for the

risk of unexpected inflation. Therefore, bond risk premium may be subject to unexpected

inflation risk. In this case, it is easy to interpret that countries with high levels of inflation

uncertainty may choose to issue short-term debt (Wright, 2011). As the author reveals,

inflation uncertainty may collapse in the case that the government maintains a specific

inflation target. In addition, business cycle state it is expected to impact inflation

uncertainties. 8

8 Numerous empirical studies focused on exploring the relationship between inflation uncertainty and

inflation. Among others, Conrad and Karanasos (2005) and Caporale and Kontonikas (2009) investigate the

aforementioned relationship and support the existence of this relationship.

20

In this class, inflation rate would be employed throughout CPI. Considering Jiranyakul and

Opiela (2010) findings that rising inflation rises inflation uncertainty and that rising inflation

uncertainty increases inflation, inflation rate is a good proxy to use.

3.1.4 Competitiveness Class

3.1.4.1 Exchange Rates

As Aisen and Hauner (2008) depicts\ed an economy that is described as open it is expected to

be majorly impacted by external factors. Such factors include exchange rates. Recalling basic

economics in the short-term exchange rates may do not reflect the Purchasing Power Parity,

hence, providing information of the countries competiveness among other countries. In order

to capture such effects, Net Effective Exchange Rate would be employed through the model.9

3.1.4.2 Short-Term Interest Rates Class

One of the shortest interest rate is the Interbank Rate10. The level of this short-term rate it is

widely expected to influence the economy. Recalling basic economics and the Term Structure

of Interest Rates11 it is widely accepted that lower interest rates yield to higher consumption

and investments. This is taking place since banks would be able to borrow one from another

with lower costs and hence these lower borrowing costs will pass through the interest rates of

individuals and corporations. All in all, lower interest rates are giving a boost to the economy

and inflation to increase. Otherwise, higher interest rates are translated to higher savings rates

and borrowing rates. Thus, the consumption deteriorates as well as the investments since

individuals and business save rather spend. By the same token, the economy slowdown and

the inflation decreases. Subsequently, Central Banks by influencing the Interbank rate

through Open Market Operations, Discount Window and Reserve Requirements are able to

influence the economy as a whole.

9 More Precisely, the Nominal Effective Exchange Rate would be adopted from Eurostat’s historical data and

represents the weighted average of bilateral nominal exchange rate against the currencies of 42 selected

trading partners.

10 The Interbank Rate it is the interest rate within the interbank market. Otherwise, it is the interest rate that

the banks within a market borrow from each other.

11 (Mishkin, 2007)

21

As regards bond yields, the Interbank Rate plays a significant role in coordinating the yields

through the expectations of future interest rates. According to the level of the Short-Term

Interest rates the Inflation expectations are adjusted as already aforementioned. Hence, the

time value of money is adjusted accordingly leading to higher or lower yields. For example,

if they are high inflation expectations then bond yields will decline. In order to compensate

for the shortfall in the purchasing power of future cash flows higher yields are given.

Accordingly, different bonds would be impacted differently. As per this study, we will focus

on examining the left side of the yields curve (short-term) of the 10-year Cyprus Sovereign

Bond Yields.

Therefore, the 3-Month Money Market Rate12 would be employed as a proxy for the short-

term interest rates.

3.2 Data description

In order to address the macroeconomic determinants that affect the short-term changes of the

Cyprus Sovereign Bond Yields a Regression Analysis would be conducted with data from the

first quarter of 2000 and the third quarter of 2015. Generally, the data were generated from

the database of Statistical Service of Cyprus, Eurostat, Statistical Data Warehouse of the

European Central Bank and Datastream13. The dependent variable of Cyprus Sovereign Bond

Yields is represented by the 10-year Cyprus Sovereign Bond Yields. The changes of the

variables were obtained by taking the differences of the variables from the values that they

had the year before.

Looking at the different range of their standard deviation, all the variables were standardised.

In this way, the contribution of the independent variables to the dependent during the

Regression Analysis would be the correct one. This sacrifice is important in order to gain the

best possible estimations.

12 The interbank rate that would be employed consist of the Cyprus interbank rate before Cyprus entered the

Eurozone in 2008; frrom then onwards, Euribor rate would be used.

13 See Appendix 3

22

3.2.1 Cyprus Special Indicators

Overall, Cyprus is a small country with openness to the global financial markets. The country

faced severe economic problems during the last years. Generally, the country is high

leveraged and exposed to the banking system. However, the exposure shrinkage in a crucial

extent during the Memorandum Period. All in all, Cyprus is expected to be impacted

significantly from credit ratings announcements (Cantor and Packer, 1996) since it was

considered as a high risk investment. Additionally, as Cyprus may be considered as an

economy with remarkable openness to the global financial markets as per Aisen and Hauner

(2008) Cyprus sovereign bond yields are expected to be determine largely by external factors

and crucially from credit risk spreads. Again, supporting that Credit Ratings may contribute

to the explanation of sovereign bond yields. Generally, the economic profile of Cyprus

revealed that Cyprus sovereign bond yields may well be impacted by risk indicators among

other macroeconomic variables.

The second Regression Analysis that would be conducted includes independent variables

based on Cyprus Economic Characteristics:

A latent factor would be generated in order to capture any delayed adjustment as Cyprus is a

small economy; whilst, they are couple of studies supporting the existence of latent factors

even in bigger economies such as Tam and Yu (2008). In short, the model would be a

Dynamic Autoregressive one latent factor (AR(1)) model with the help of Cohrane-Orcutt.

Furthermore, Financial Soundness Indicators would be obtained for the period of 2012 to the

last quarter examined from the IMF database. As Financial Soundness Indicators (2006)

complication guide states Financial Soundness Indicators represent indicators of the current

financial health and soundness of the financial institutions in a country, and of their corporate

and household counterparts. They comprise both accumulated individual institution data and

indicators that are representative of the markets in which the financial institutions operate. As

the only type of information available for Cyprus was the Core Financial Soundness

Indicators for Depositors and the Encouraged it was decided to used only the Core to defend

any Small Sample Issues that may arise from adding too many variables in relation to the

Sample size.

23

Last but not least, Duymmy Variables would be generated in order to represent the credit

ratings of Cyprus as it was mentioned before Cyprus faced serious economic issues and high

risk. The data was obtained from Moody’s Investors Service Inc. Historical Database.

24

4 Empirical analysis

4.1 Core empirical sound macroeconomic variables

4.1.1 Baseline Specification

According to the literature review as well as the potential factors discussed above, the key

factors that evidently impact bond yields are seven macroeconomic variables. Firstly, as a

decomposition of the real GDP, Labour Productivity Per Person and the Working Age

Population as mentioned above, will perhaps influence Cyprus sovereign Bond Yields.

Secondly, other major macroeconomic variables that were tested widely are also believed to

have an influence on fiscal bond yields. Specifically, these six variables consist of 3-Month

Money Market Interest Rate, Unemployment Rate, Inflation Rate, Net Deficit to GDP ratio,

Primary Balance to GDP ratio and Net Effective Exchange Rate.

Noteworthy, the Ordinary Least Squares Regression Analysis was conducted with robust

standard errors in order to cure if any heteroscedasticity exists.

A Regression Analysis was generated with the core empirical sound macroeconomic

independent variables. The analysis portrayed few variables as statistical insignificant. As a

result, the most statistical insignificant variable at a confidence interval of 95% was excluded

at a time. The results showed that Inflation Rate, Net Effective Exchange Rate, Net Deficit to

GDP and Labour Productivity per Person are insignificant to explain the short term changes

of Cyprus Sovereign Bond Yields. Thus, these variables do not contribute to the explanation

of the model.

Before moving on and presenting the generated model it is important to adapt a clearer view

of the variable omissions from the model with the help of bivariate correlation14 of the

variables:

Firstly, removing Inflation Rate as the most insignificant variable it is worth stating that it is

highly, positive and significantly correlated with the variable of Working Age Population.

Additionally, the variable is also negative and significantly correlated with the variable Net

Deficit to GDP. Thereby, the variable exclusion did not affect the model explanation since

14 See Appendix 5

25

the information that the variable contain can also be achieved by a high extent from the

independent variable of Working Age Population as well as form the Net Deficit to GDP

independent variable.

Taking into account the rationale behind this finding, it is no surprise that these variables are

correlated, as an increasing amount of working age population leads to higher generated

revenues boosting the economy, hence creating inflation. In a nutshell, in short-term

increasing inflation is a sign of economic upward trend which is translated into higher GDP,

consequently net deficit to GDP would diminished. Despite that it is appropriate to omit this

variable in order to avoid any multicollinearity issues that may arise due to the correlation of

the variable with other independent variables that would violate Linear Regression

Assumptions.

Secondly, the omission of Net Effective Exchange Rate it was supported by the non-

statistical significance of the variable. This was not a surprise since the generated model

investigates the macroeconomic indicators affecting the yearly changes of the Cyprus

Sovereign Bond Yields. This was not a surprise since most of the currencies are pegged to

other currencies.

Thirdly, excluding Net Deficit to GDP independent variable from the model it is remarkable

to mention that is highly, positive and significantly correlated with Unemployment Rate

Variable. A high unemployment rate means that the economy is on a recession and a sluggish

trend. Therefore, that’s why these variables are correlated since high unemployment and high

Net Deficit to GDP both are indications that the economy is facing a recession. The omission

of Net Deficit to GDP independent variable from the model did not caused dramatic changes

since the variable is highly correlated with Unemployment Rate. Again, it is appropriate to

remove such variables with high autocorrelation in order to avoid multiocolliniearity

problems.

Finally, Labour Productivity per Person variable dropped from the model as an insignificant

independent variable.15 The zero hypothesis of this variable cannot be rejected at a statistical

level of 5%. As consequence this variable would be excluded from the model. This is not a

surprise since this variable mostly indicates long-term influences on sovereign bond yields.

15 Remember that was a one proxy for the real GDP growth determinant.

26

Additionally, the constant factor of the regression was statistically insignificant. However, the

constant was not excluded from the model as removing the constant from the model would

have impacted the model inversely. The effect would be a violation of linear regression

assumption of zero mean of the disturbances.

All in all, the model suggests that short-term changes of Cyprus Sovereign Bond Yields can

be explained through: Working Age Population; 3-Month Money Market Interest Rate;

Unemployment Rate and Primary Balance to GDP ratio. Each of the variable is statistical

significant at a 1% significant level as well as the comprehensive significance of all the

variables. The suggested model baseline is the below:

Δ z10-year Cyprus Sovereign Bond Yields= 0.000 + 0.319*LN zWorking Age Population

+0.436*Δ z3-Month Money Market Rate

+0.457*Δ zUnemployment Rate

+0.130*Δ zPrimary Balance to GDP

Figure 2: Foundation Regression Equation

According to the foundation model, a percentage change in Working Age Population will

yield to 0.319 increase in Cyprus Sovereign Bond Yields. Likewise, a percentage increase in

Unemployment Rate will lead to 0.457 increase in Cyprus Sovereign Bond Yields. Whereas,

a percentage increase in 3-Month Money Market Interest Rate would lead to a 0.436 increase

in Cyprus Sovereign Bond Yields. To a lesser extent, a percentage increase in Primary

Balance Ratio will yield to an increase of 0.130 in the Cyprus Sovereign Bond

Yields.Overall, the independent variables can explain Cyprus Sovereign Bond Yields short-

term changes at 42% level (Adjusted R square). It is generally considered as a model with

some explanatory power. However, there is room of improvement to the model.

4.2 Adjusted Regression Model to Cyprus Economic Profile

Taking into consideration Cyprus Economic Profile it is important to adjust the suggested

model to Cyprus special characteristics. Subsequently, the above model was kept as a

foundation and upon it new macroeconomic and dummy variables were tested. This time the

27

Regression Analysis was conducted with a Dynamic model of Cochrane-Orcutt

Autoregressive model of one latent factor (AR(1))16.

In addition, Principal Components Analysis was conducted for the standardised Financial

Soundness Indicators during the period of 2012 were Cyprus Recession started to the last

quarter examine. All in all, as the sample size of the data is small and there was no room for

excess variables into the model that is why a Principal Components Analysis was conducted.

Overall, four Principal Components were chosen under the rule of “Greater than One”

eigenvalue17.

The aforementioned variables were added to the basic model and afterwards other Dummy

Variables were added to test the importance of Cyprus Sovereign Credit Ratings.18 Not to

mention that A2 credit Rating was omitted from the model in order to avoid multicollinearity

issues. Anyway, the dummy variable importance would be captured through the model’s

coefficient.

The Regression Analysis depicted couple of variables as statistical insignificant. As a

consequence, the most statistical insignificant variable at a confidence interval of 95% was

excluded at a time. The results showed that three Principal Components out of four, the

16 The decision-making on this was crucially based on the fact that when plotting the residuals of the basic

model a Positive Autocorrelation is obvious (see Appendix 7). The residuals are correlated violating the

assumption of the OLS assumptions that residuals are independent. Residuals are moving with a cyclical

motion throughout time. That is why a Cochrane-Orcutt model was employed.

17 Additionally, two Dummy Variables were generated in order to adjust the coefficient value to the Cyprus

Crisis Period. One of the two was a general verification of any additional liquidity premium bondholders may

require during the second quarter of 2011 were Cyprus lost access to the international markets until the last

quarter examine. The second dummy was generated in order to specify if any reduction of investors liquidity

premium taken place due to Cyprus entrance into a Memorandum Assistance Program in the second quarter

of 2013. The generated dummy variables failed to reveal in a statistical significant manner any differences in

liquidity premium investors required during the Cyprus crisis other than Financial Soundness Indicators depict

or Credit Ratings.

18 Remarkable that the Dummy Variables of the Credit Ratings tested at a second phase. Dummy Variables

were not tested with the other variables because the sample of the model was really small and the degrees of

freedom would have been affected significantly.

28

Working Age Population, the Primary Balance and the ratings of Ba3, A2, B3, Aa3, Caa319

are insignificant to explain the short term changes of Cyprus Sovereign Bond Yields. Thus,

these variables do not contribute to the explanation of the model.

Before moving on and presenting the generated model it is important to adapt a clearer view

of the variable omissions from the model:

First and foremost, Working Age Population and Primary Balance to GDP despite their

significance on the foundation model they appear as non-statistical significant indicators to

the new adjusted model. Thus, these variables omitted from the model. Subsequently, no one

of the two variables that Ichiue and Shimizu (2012) provided as key indicators of Sovereign

Bond Yields as proxies of real GDP were significant. The thing is that Cyprus Special

Characteristics give room to other type of macroeconomic variables to explained short-term

changes of the Sovereign Bond Yields that may well do not work for other Countries. In

contrast, Primary Balance to GDP ratio is not able to contribute to the explanation of the

model. This finding is not a big surprise since this variable is generally considered to be a

long-term macroeconomic factors.

The suggested final model is as follows:

Δ z10-year Cyprus Sovereign Bond Yields= -0.232 + 0.345*Δ z3-Month Money Market Rate

+0.399* Δ zUnemployment Rate

-0.099*Δ zFinancial Soundness Indicators

+1.179*Δ Credit Rating: Baa1

+1.348*Δ Credit Rating: Baa3

+1.331*Δ Credit Rating: Ba1

Figure 3: Suggested Regression Equation

Specifically, the findings were as follows. The suggested model that considers Cyprus

Economic Profile supports the following findings. A percentage change in 3-Month Money

Market Rate will lead to a 0.345 increase in Cyprus Sovereign Bond Yields. A percentage

change in Unemployment Rate would increase Cyprus Sovereign Bond Yields by 0.399. The

percentage change in the Financial Soundness of Cyprus lowers bond yields by about 0.099.

Whilst, if Cyprus is rated as Baa1 then Short Term Yields would increase. If Cyprus is rated

as Baa3 then it the rates would surge to a higher extent. Quite puzzling, if Cyprus is rated as

19 See Appendix 1 and Appendix 2 for further information

29

Ba1 then it will lead to a positive increase in yields but to a lesser extent than Baa3. However,

taking into account that Financial Soundness of Cyprus during the same period also adjust the

liquidity risk premium that Investors required it is reasonable. Precisely, when Cyprus is