Bank Reconciliation Bank Reconciliation StatementsStatements

Chapter 8Chapter 8

© © LubyLuby & & O’DonoghueO’Donoghue (2005)(2005)

TerminologyTerminology

Current accountCheque clearingBank overdraftDirect debitStanding orderCredit transferDishonoured chequeBank statement

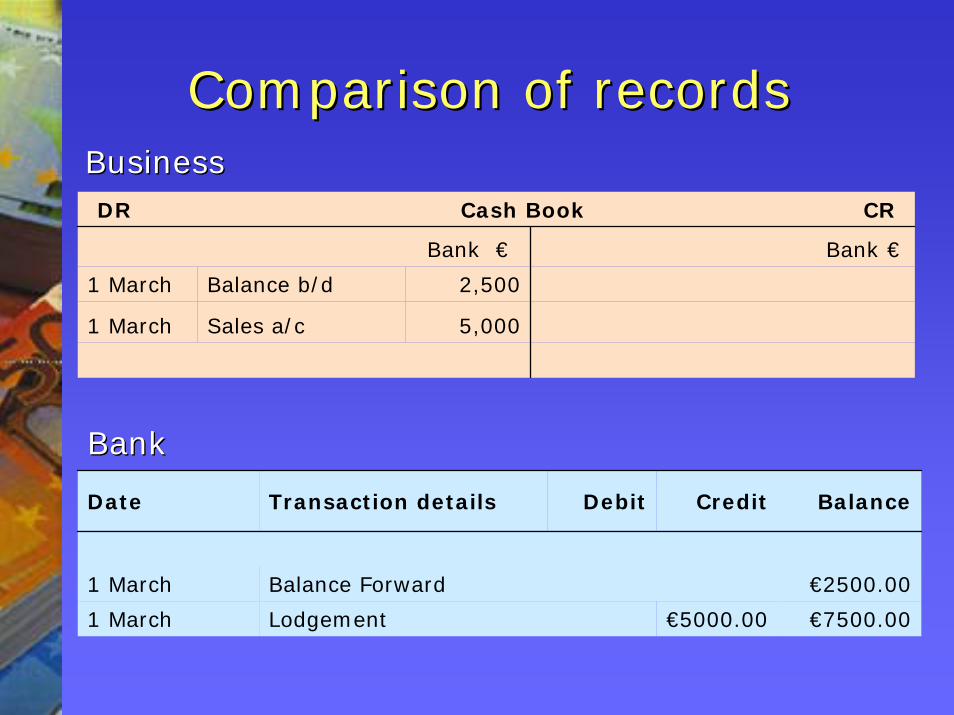

Comparison of recordsComparison of records

DR Cash Book CR

Bank € Bank €

1 March Balance b/d 2,500

1 March Sales a/c 5,000

€7500.00€5000.00Lodgement1 March

€2500.00Balance Forward1 March

BalanceCreditDebitTransaction detailsDate

BusinessBusiness

BankBank

The need for a bank The need for a bank reconciliationreconciliation

A bank statement will be received from the bank.The balance on the bank statement should be compared with the balance on the bank account in the ledger.The two balances are not likely to be the same:

Timing differencesItems on the statement not in the ledger accountsErrors

A reconciliation is carried out to verify that the balances are correct.

Reasons for differencesReasons for differences

Items that are in the bank statement but are not in the cash book

Automatic payments through the banking systemBank chargesDishonoured cheques

Items that are recorded in the cash book but not appearing in the bank statement

Un-presented chequesUn-cleared lodgements

ApproachApproach

Step 1Step 1 Each item in the bank statement needs to be traced to

the cash book in order to identify all items that appear in the bank statement but are not in the cash book. All such items should then be entered in the cash book and a new updated balance calculated.

Step 2Step 2 Each item in the cash book should be traced to the bank

statement so as to identify bank deposits and cheques drawn that are not appearing on the bank’s statement because the former are awaiting clearance and the latter are yet to be presented to the bank for payment. The bank reconciliation would look as follows.

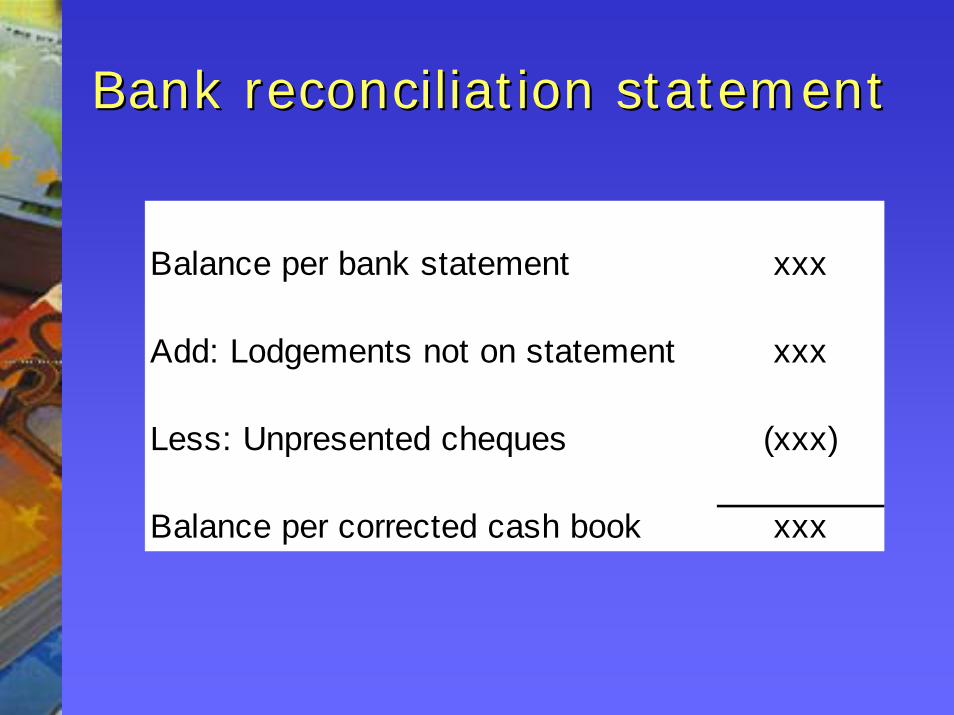

Bank reconciliation statementBank reconciliation statement

Bank Reconciliation StatementBalance per bank statement xxx

Add: Lodgements not on statement xxx

Less: Unpresented cheques (xxx)

Balance per corrected cash book xxx

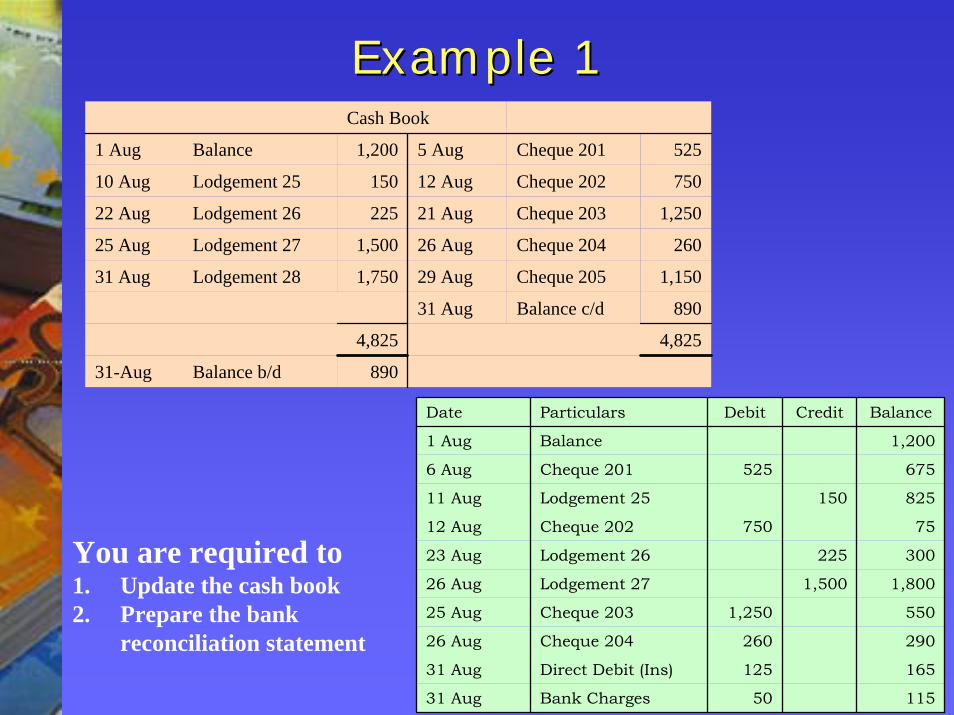

You are required to 1. Update the cash book 2. Prepare the bank

reconciliation statement

Example 1Example 1Cash Book

1 Aug Balance 1,200 5 Aug Cheque 201 525

10 Aug Lodgement 25 150 12 Aug Cheque 202 750

22 Aug Lodgement 26 225 21 Aug Cheque 203 1,250

25 Aug Lodgement 27 1,500 26 Aug Cheque 204 260

31 Aug Lodgement 28 1,750 29 Aug Cheque 205 1,150

31 Aug Balance c/d 890

4,825 4,825

31-Aug Balance b/d 890

11550Bank Charges31 Aug

165125Direct Debit (Ins)31 Aug

290260Cheque 20426 Aug

5501,250Cheque 20325 Aug

1,8001,500Lodgement 2726 Aug

300225Lodgement 2623 Aug

75750Cheque 20212 Aug

825150Lodgement 2511 Aug

675525Cheque 2016 Aug

1,200Balance1 Aug

BalanceCreditDebitParticularsDate

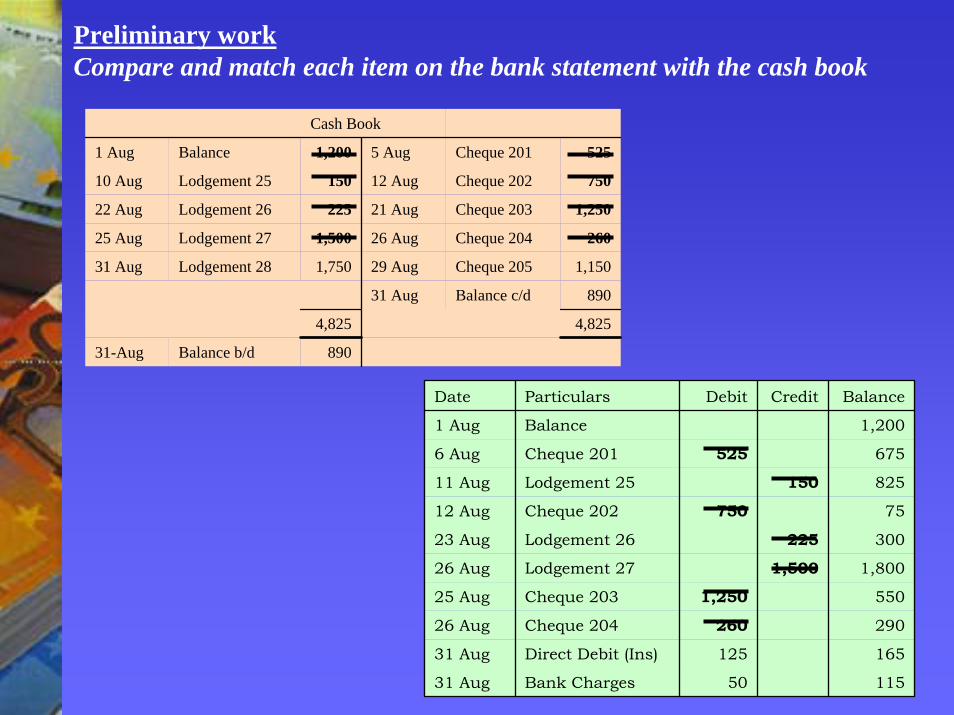

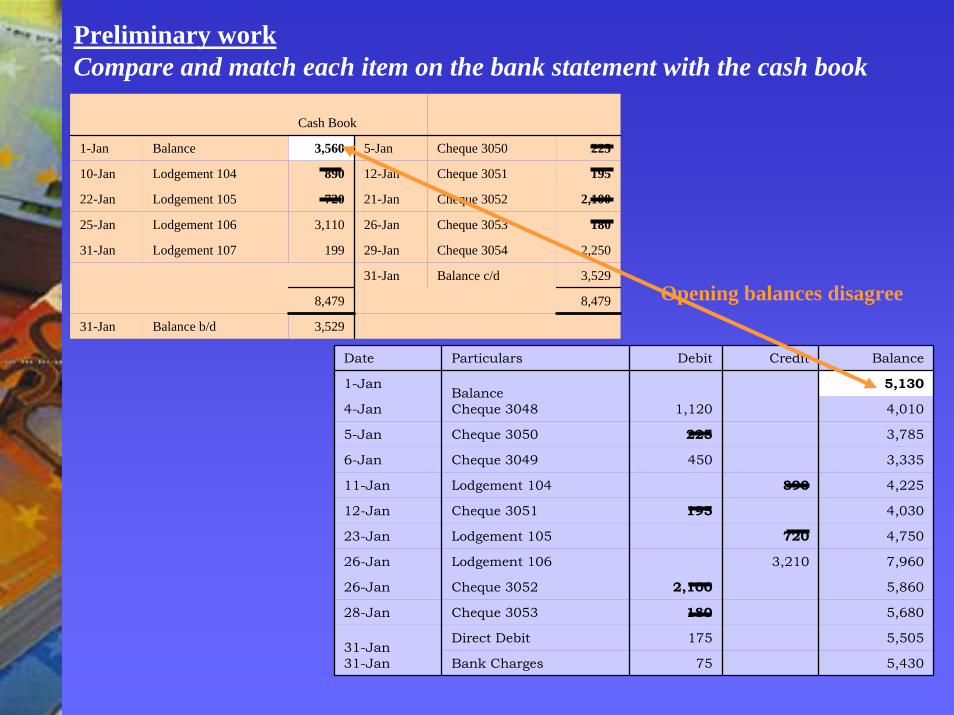

Preliminary workCompare and match each item on the bank statement with the cash book

Cash Book

1 Aug Balance 1,200 5 Aug Cheque 201 525

10 Aug Lodgement 25 150 12 Aug Cheque 202 750

22 Aug Lodgement 26 225 21 Aug Cheque 203 1,250

25 Aug Lodgement 27 1,500 26 Aug Cheque 204 260

31 Aug Lodgement 28 1,750 29 Aug Cheque 205 1,150

31 Aug Balance c/d 890

4,825 4,825

31-Aug Balance b/d 890

11550Bank Charges31 Aug

165125Direct Debit (Ins)31 Aug

290260Cheque 20426 Aug

5501,250Cheque 20325 Aug

1,8001,500Lodgement 2726 Aug

300225Lodgement 2623 Aug

75750Cheque 20212 Aug

825150Lodgement 2511 Aug

675525Cheque 2016 Aug

1,200Balance1 Aug

BalanceCreditDebitParticularsDate

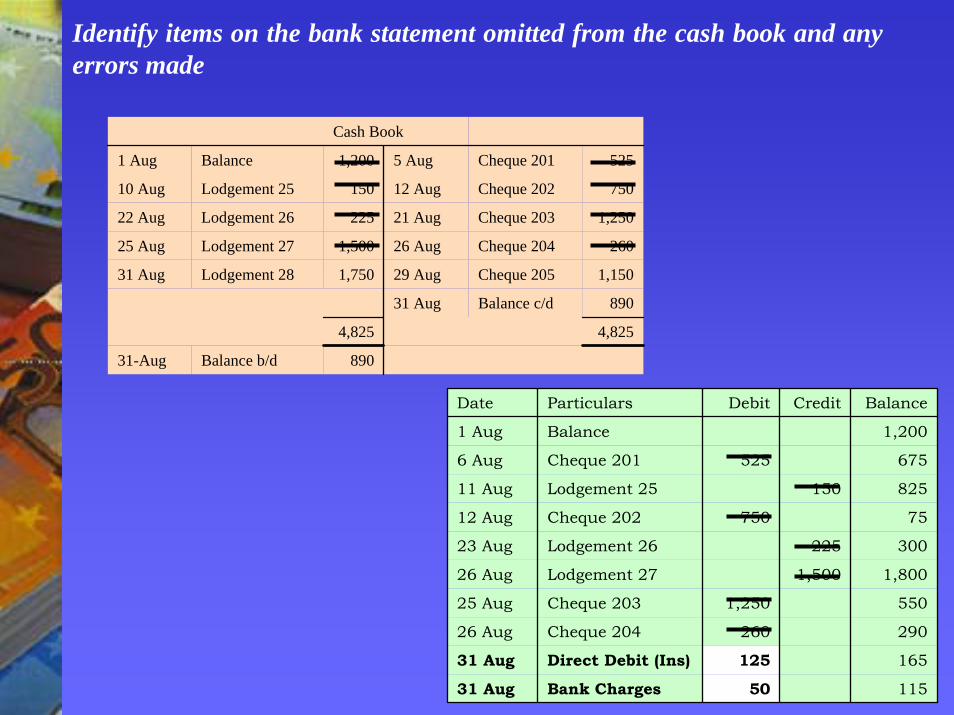

Identify items on the bank statement omitted from the cash book and any errors made

Cash Book

1 Aug Balance 1,200 5 Aug Cheque 201 525

10 Aug Lodgement 25 150 12 Aug Cheque 202 750

22 Aug Lodgement 26 225 21 Aug Cheque 203 1,250

25 Aug Lodgement 27 1,500 26 Aug Cheque 204 260

31 Aug Lodgement 28 1,750 29 Aug Cheque 205 1,150

31 Aug Balance c/d 890

4,825 4,825

31-Aug Balance b/d 890

Date Particulars Debit Credit Balance

1 Aug Balance 1,200

6 Aug Cheque 201 525 675

11 Aug Lodgement 25 150 825

12 Aug Cheque 202 750 75

23 Aug Lodgement 26 225 300

26 Aug Lodgement 27 1,500 1,800

25 Aug Cheque 203 1,250 550

26 Aug Cheque 204 260 290

31 Aug Direct Debit (Ins) 125 165

31 Aug Bank Charges 50 115

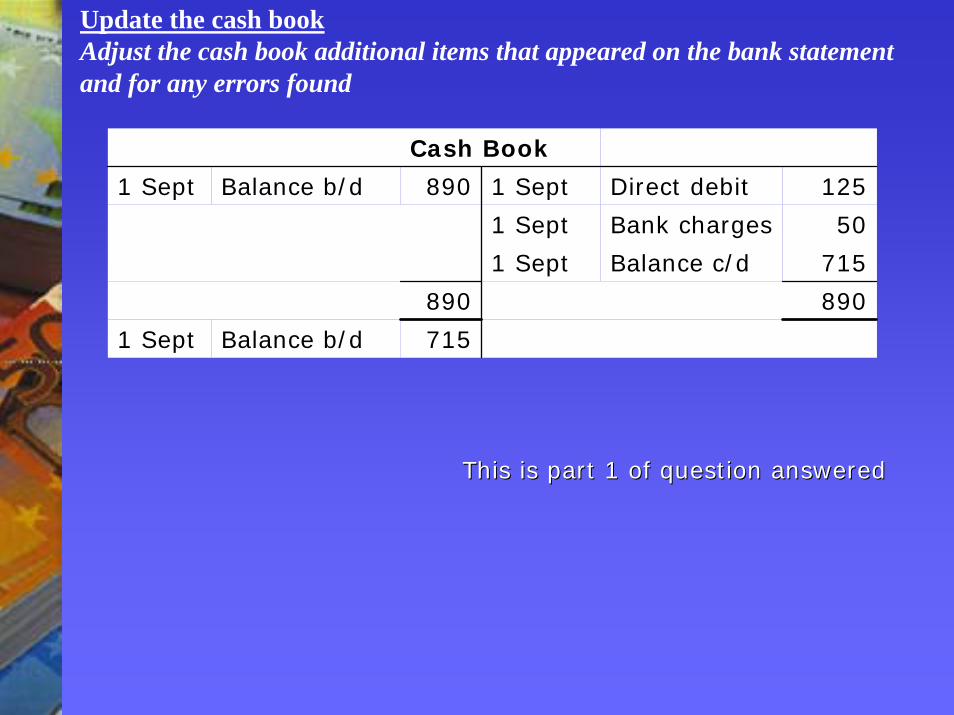

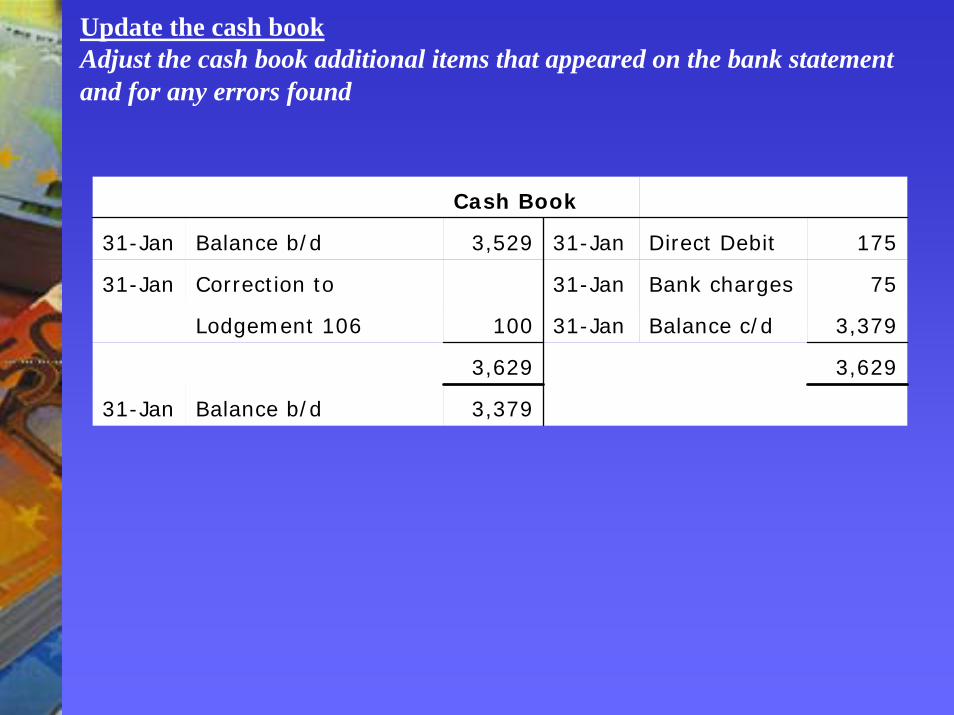

Update the cash bookAdjust the cash book additional items that appeared on the bank statement and for any errors found

Cash Book

1 Sept Balance b/d 890 1 Sept Direct debit 125

1 Sept Bank charges 50

1 Sept Balance c/d 715

890 890

1 Sept Balance b/d 715

This is part 1 of question answeredThis is part 1 of question answered

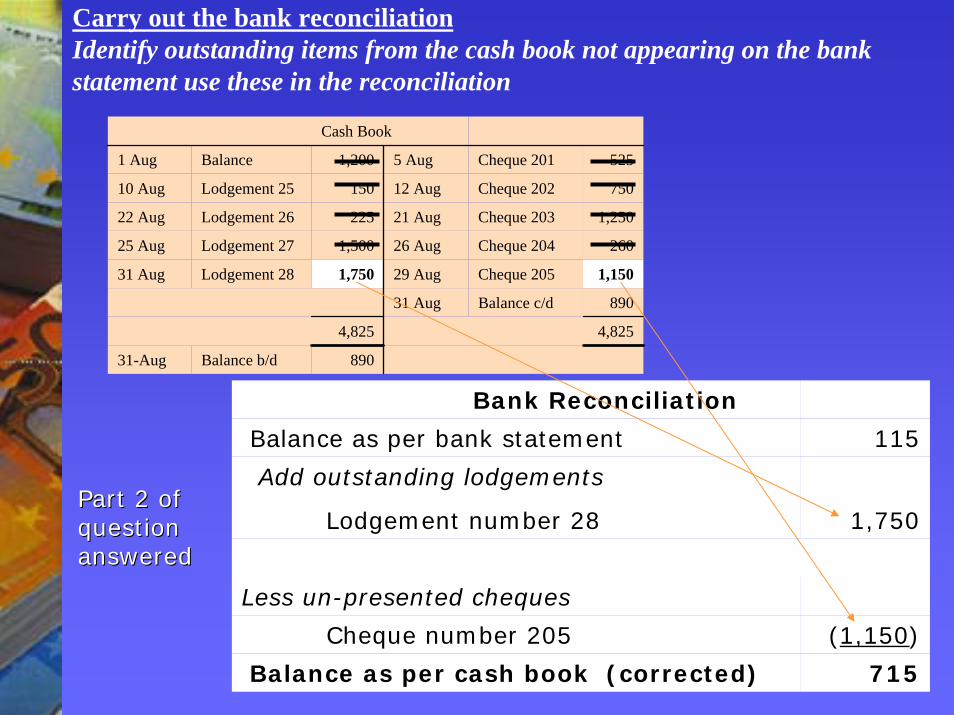

Carry out the bank reconciliationIdentify outstanding items from the cash book not appearing on the bank statement use these in the reconciliation

Cash Book

1 Aug Balance 1,200 5 Aug Cheque 201 525

10 Aug Lodgement 25 150 12 Aug Cheque 202 750

22 Aug Lodgement 26 225 21 Aug Cheque 203 1,250

25 Aug Lodgement 27 1,500 26 Aug Cheque 204 260

31 Aug Lodgement 28 1,750 29 Aug Cheque 205 1,150

31 Aug Balance c/d 890

4,825 4,825

31-Aug Balance b/d 890

Bank Reconciliation

Balance as per bank statement 115

Add outstanding lodgements

Lodgement number 28 1,750

Less un-presented cheques

Cheque number 205 (1,150)

Balance as per cash book (corrected) 715

Part 2 of Part 2 of question question answeredanswered

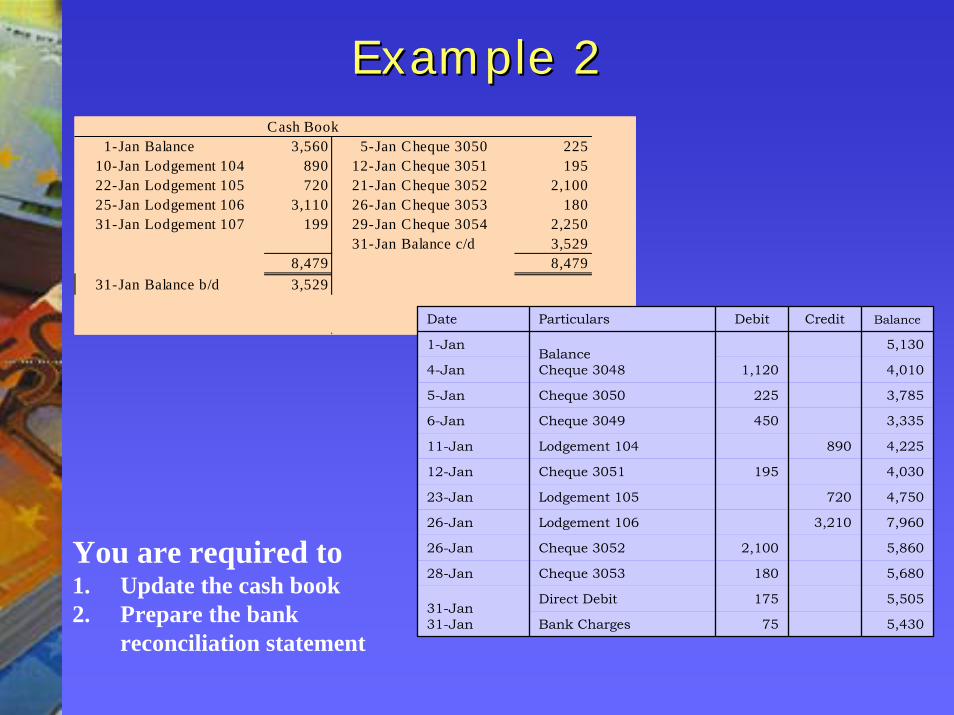

Cash Book1-Jan Balance 3,560 5-Jan Cheque 3050 225

10-Jan Lodgement 104 890 12-Jan Cheque 3051 19522-Jan Lodgement 105 720 21-Jan Cheque 3052 2,10025-Jan Lodgement 106 3,110 26-Jan Cheque 3053 18031-Jan Lodgement 107 199 29-Jan Cheque 3054 2,250

31-Jan Balance c/d 3,5298,479 8,479

31-Jan Balance b/d 3,529

Date Particulars Debit Credit Balance

1-Jan 5,130

4-Jan 1,120 4,010

5-Jan Cheque 3050 225 3,785

6-Jan Cheque 3049 450 3,335

11-Jan Lodgement 104 890 4,225

12-Jan Cheque 3051 195 4,030

23-Jan Lodgement 105 720 4,750

26-Jan Lodgement 106 3,210 7,960

26-Jan Cheque 3052 2,100 5,860

28-Jan Cheque 3053 180 5,680

Direct Debit 175 5,505

Bank Charges 75 5,43031-Jan31-Jan

BalanceCheque 3048

Example 2Example 2

You are required to 1. Update the cash book 2. Prepare the bank

reconciliation statement

Opening balances disagree

Preliminary workCompare and match each item on the bank statement with the cash book

Cash Book

1-Jan Balance 3,560 5-Jan Cheque 3050 225

10-Jan Lodgement 104 890 12-Jan Cheque 3051 195

22-Jan Lodgement 105 720 21-Jan Cheque 3052 2,100

25-Jan Lodgement 106 3,110 26-Jan Cheque 3053 180

31-Jan Lodgement 107 199 29-Jan Cheque 3054 2,250

31-Jan Balance c/d 3,529

8,479 8,479

31-Jan Balance b/d 3,529

Date Particulars Debit Credit Balance

1-Jan 5,130

4-Jan 1,120 4,010

5-Jan Cheque 3050 225 3,785

6-Jan Cheque 3049 450 3,335

11-Jan Lodgement 104 890 4,225

12-Jan Cheque 3051 195 4,030

23-Jan Lodgement 105 720 4,750

26-Jan Lodgement 106 3,210 7,960

26-Jan Cheque 3052 2,100 5,860

28-Jan Cheque 3053 180 5,680

Direct Debit 175 5,505

Bank Charges 75 5,43031-Jan31-Jan

BalanceCheque 3048

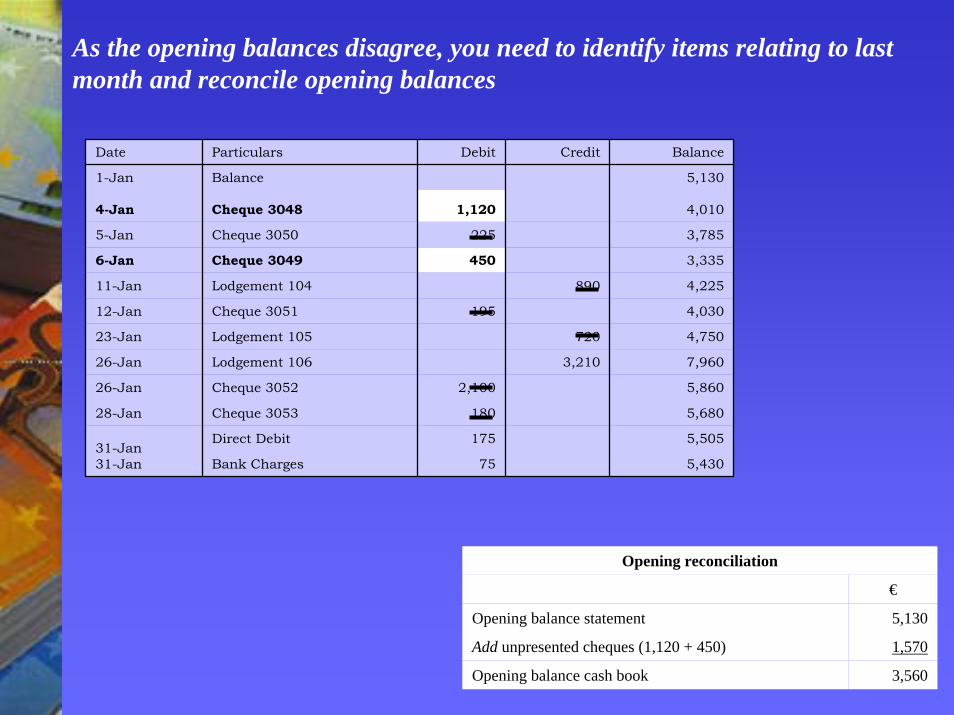

As the opening balances disagree, you need to identify items relating to last month and reconcile opening balances

Date Particulars Debit Credit Balance

1-Jan 5,130

4-Jan 1,120 4,010

5-Jan Cheque 3050 225 3,785

6-Jan Cheque 3049 450 3,335

11-Jan Lodgement 104 890 4,225

12-Jan Cheque 3051 195 4,030

23-Jan Lodgement 105 720 4,750

26-Jan Lodgement 106 3,210 7,960

26-Jan Cheque 3052 2,100 5,860

28-Jan Cheque 3053 180 5,680

Direct Debit 175 5,505

Bank Charges 75 5,43031-Jan31-Jan

Balance

Cheque 3048

3,560Opening balance cash book

1,570Add unpresented cheques (1,120 + 450)

5,130Opening balance statement

€

Opening reconciliation

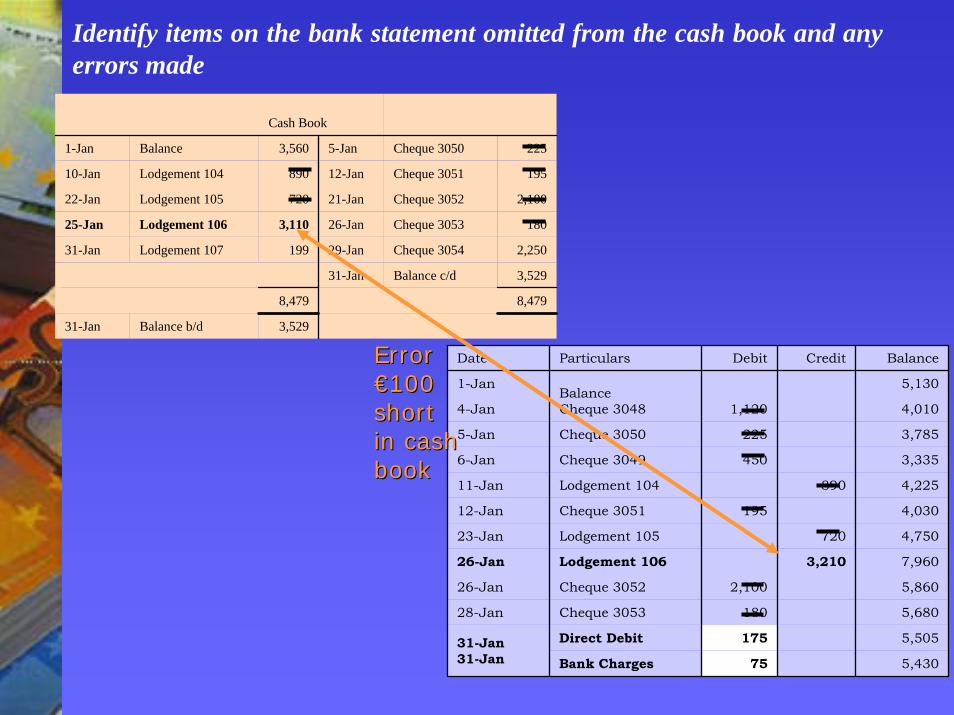

Identify items on the bank statement omitted from the cash book and any errors made

Cash Book

1-Jan Balance 3,560 5-Jan Cheque 3050 225

10-Jan Lodgement 104 890 12-Jan Cheque 3051 195

22-Jan Lodgement 105 720 21-Jan Cheque 3052 2,100

25-Jan Lodgement 106 3,110 26-Jan Cheque 3053 180

31-Jan Lodgement 107 199 29-Jan Cheque 3054 2,250

31-Jan Balance c/d 3,529

8,479 8,479

31-Jan Balance b/d 3,529

Date Particulars Debit Credit Balance

1-Jan 5,130

4-Jan 1,120 4,010

5-Jan Cheque 3050 225 3,785

6-Jan Cheque 3049 450 3,335

11-Jan Lodgement 104 890 4,225

12-Jan Cheque 3051 195 4,030

23-Jan Lodgement 105 720 4,750

26-Jan Lodgement 106 3,210 7,960

26-Jan Cheque 3052 2,100 5,860

28-Jan Cheque 3053 180 5,680

Direct Debit 175 5,505

Bank Charges 75 5,43031-Jan31-Jan

BalanceCheque 3048

ErrorError€100 €100 short short in cash in cash bookbook

Update the cash bookAdjust the cash book additional items that appeared on the bank statement and for any errors found

Cash Book

31-Jan Balance b/d 3,529 31-Jan Direct Debit 175

31-Jan Correction to 31-Jan Bank charges 75

Lodgement 106 100 31-Jan Balance c/d 3,379

3,629 3,629

31-Jan Balance b/d 3,379

Carry out the bank reconciliationIdentify outstanding items from the cash book not appearing on the bank statement use these in the reconciliation

Cash Book

1-Jan Balance 3,560 5-Jan Cheque 3050 225

10-Jan Lodgement 104 890 12-Jan Cheque 3051 195

22-Jan Lodgement 105 720 21-Jan Cheque 3052 2,100

25-Jan Lodgement 106 3,110 26-Jan Cheque 3053 180

31-Jan Lodgement 107 199 29-Jan Cheque 3054 2,250

31-Jan Balance c/d 3,529

8,479 8,479

31-Jan Balance b/d 3,529

3,379Balance as per cash book (corrected)

(2,250)Cheque 3054

Less un-presented cheques

199Lodgement 107

Add outstanding lodgements

5,430Balance as per bank statement

€

Bank Reconciliation Statement

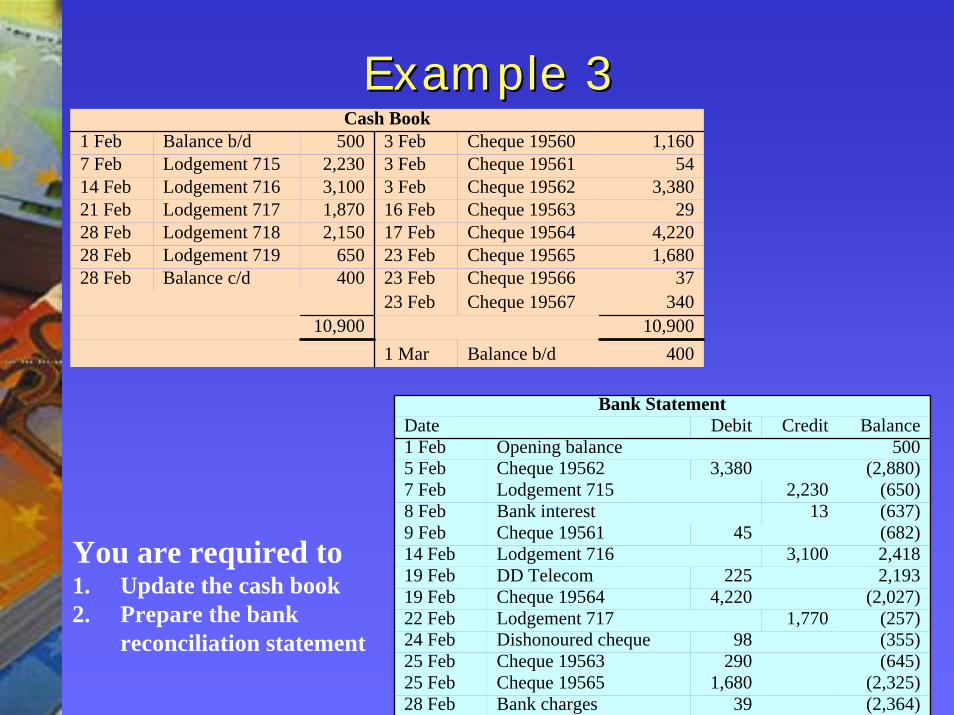

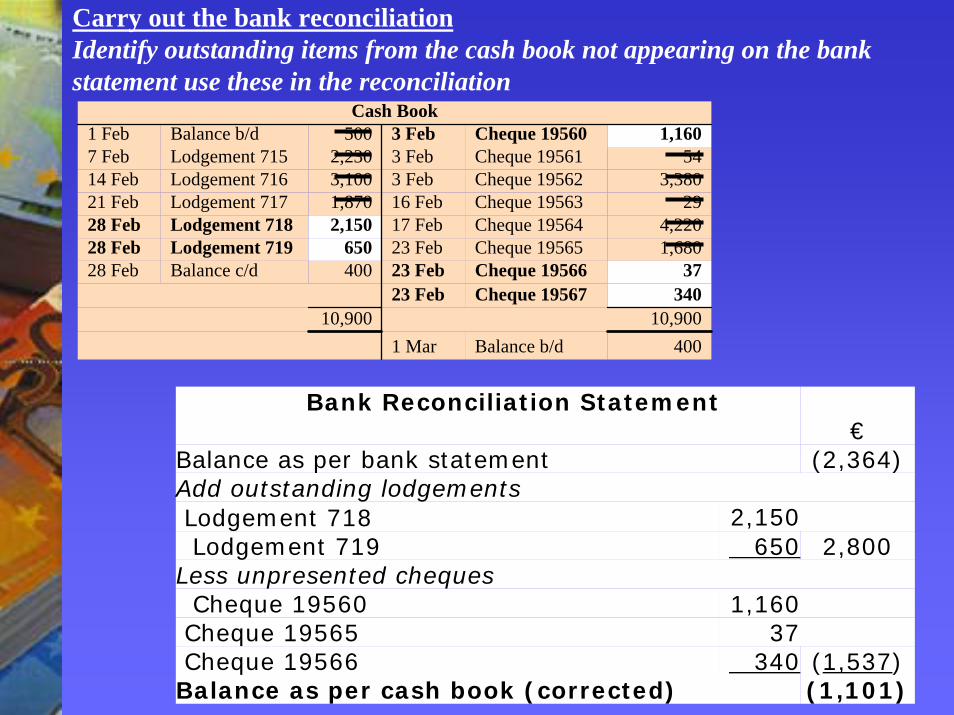

Example 3Example 3Cash Book

1 Feb Balance b/d 500 3 Feb Cheque 19560 1,1607 Feb Lodgement 715 2,230 3 Feb Cheque 19561 5414 Feb Lodgement 716 3,100 3 Feb Cheque 19562 3,38021 Feb Lodgement 717 1,870 16 Feb Cheque 19563 2928 Feb Lodgement 718 2,150 17 Feb Cheque 19564 4,22028 Feb Lodgement 719 650 23 Feb Cheque 19565 1,68028 Feb Balance c/d 400 23 Feb Cheque 19566 37

23 Feb Cheque 19567 34010,900 10,900

1 Mar Balance b/d 400

(2,364)39Bank charges28 Feb(2,325)1,680Cheque 1956525 Feb

(645)290Cheque 1956325 Feb(355)98Dishonoured cheque24 Feb(257)1,770Lodgement 71722 Feb

(2,027)4,220Cheque 1956419 Feb2,193 225DD Telecom19 Feb2,418 3,100Lodgement 71614 Feb(682)45Cheque 195619 Feb(637)13Bank interest8 Feb(650)2,230Lodgement 7157 Feb

(2,880)3,380Cheque 195625 Feb500 Opening balance1 Feb

BalanceCreditDebitDateBank Statement

You are required to 1. Update the cash book 2. Prepare the bank

reconciliation statement

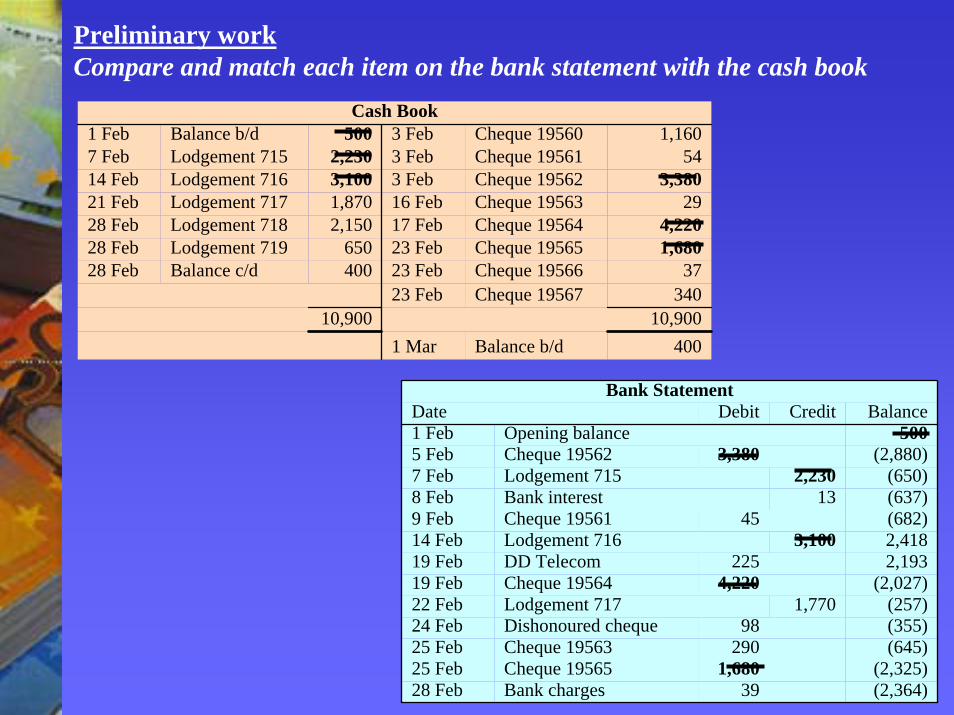

Preliminary workCompare and match each item on the bank statement with the cash book

Cash Book1 Feb Balance b/d 500 3 Feb Cheque 19560 1,1607 Feb Lodgement 715 2,230 3 Feb Cheque 19561 5414 Feb Lodgement 716 3,100 3 Feb Cheque 19562 3,38021 Feb Lodgement 717 1,870 16 Feb Cheque 19563 2928 Feb Lodgement 718 2,150 17 Feb Cheque 19564 4,22028 Feb Lodgement 719 650 23 Feb Cheque 19565 1,68028 Feb Balance c/d 400 23 Feb Cheque 19566 37

23 Feb Cheque 19567 34010,900 10,900

1 Mar Balance b/d 400

(2,364)39Bank charges28 Feb(2,325)1,680Cheque 1956525 Feb

(645)290Cheque 1956325 Feb(355)98Dishonoured cheque24 Feb(257)1,770Lodgement 71722 Feb

(2,027)4,220Cheque 1956419 Feb2,193 225DD Telecom19 Feb2,418 3,100Lodgement 71614 Feb(682)45Cheque 195619 Feb(637)13Bank interest8 Feb(650)2,230Lodgement 7157 Feb

(2,880)3,380Cheque 195625 Feb500Opening balance1 Feb

BalanceCreditDebitDateBank Statement

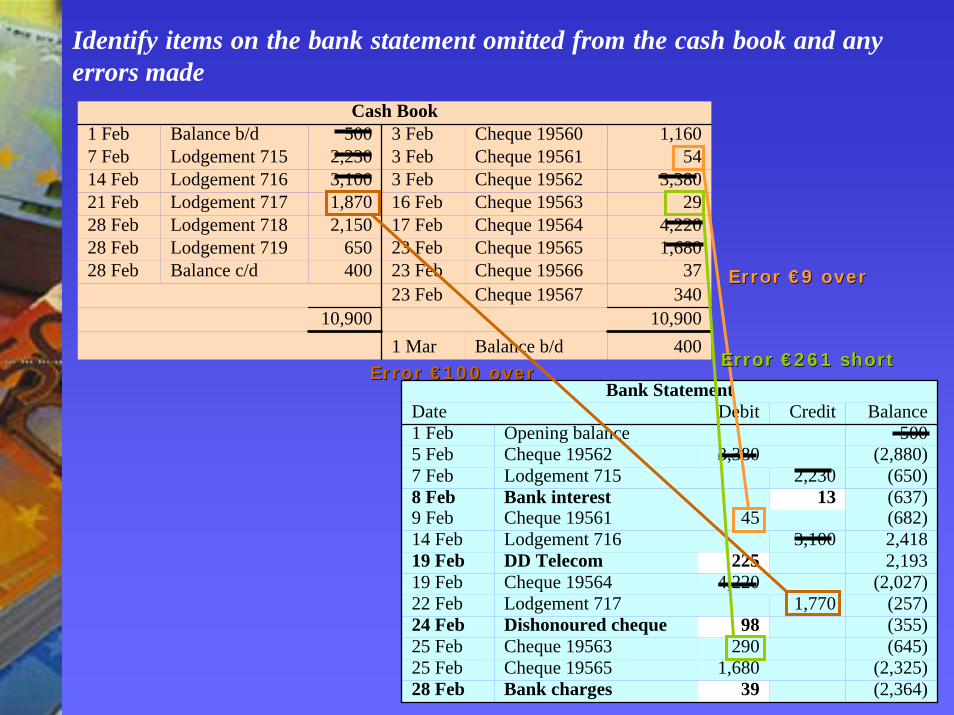

Identify items on the bank statement omitted from the cash book and any errors made

Cash Book1 Feb Balance b/d 500 3 Feb Cheque 19560 1,1607 Feb Lodgement 715 2,230 3 Feb Cheque 19561 5414 Feb Lodgement 716 3,100 3 Feb Cheque 19562 3,38021 Feb Lodgement 717 1,870 16 Feb Cheque 19563 2928 Feb Lodgement 718 2,150 17 Feb Cheque 19564 4,22028 Feb Lodgement 719 650 23 Feb Cheque 19565 1,68028 Feb Balance c/d 400 23 Feb Cheque 19566 37

23 Feb Cheque 19567 34010,900 10,900

1 Mar Balance b/d 400

(2,364)39Bank charges28 Feb(2,325)1,680Cheque 1956525 Feb

(645)290Cheque 1956325 Feb(355)98Dishonoured cheque24 Feb(257)1,770Lodgement 71722 Feb

(2,027)4,220Cheque 1956419 Feb2,193 225DD Telecom19 Feb2,418 3,100Lodgement 71614 Feb(682)45Cheque 195619 Feb(637)13Bank interest8 Feb(650)2,230Lodgement 7157 Feb

(2,880)3,380Cheque 195625 Feb500 Opening balance1 Feb

BalanceCreditDebitDateBank Statement

Error €100 overError €100 over

Error €9 overError €9 over

Error €261 shortError €261 short

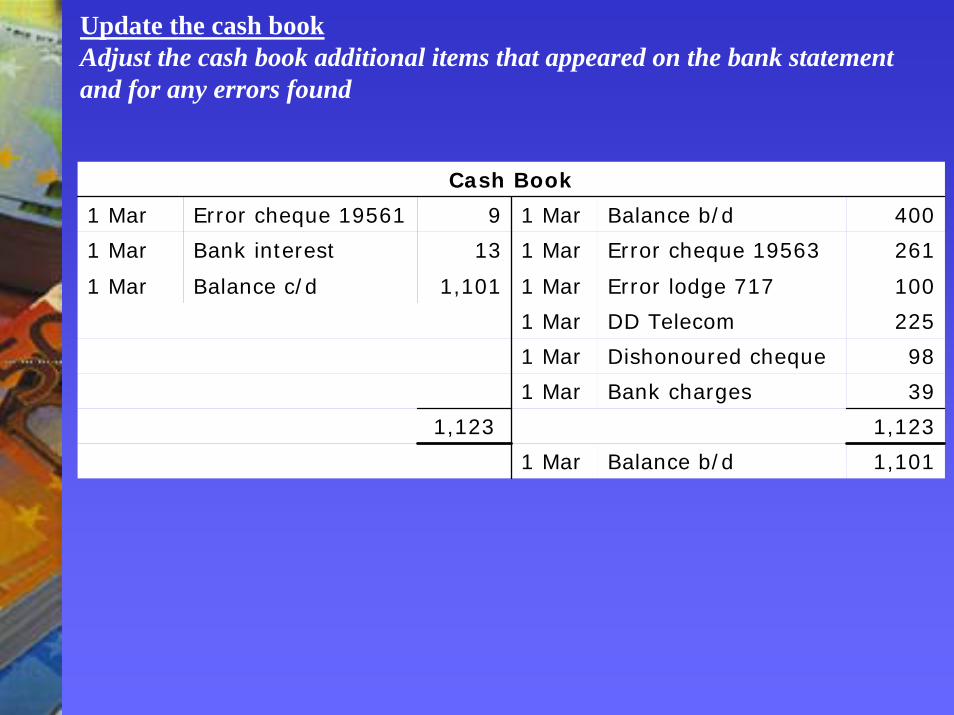

Update the cash bookAdjust the cash book additional items that appeared on the bank statement and for any errors found

Cash Book

1 Mar Error cheque 19561 9 1 Mar Balance b/d 400

1 Mar Bank interest 13 1 Mar Error cheque 19563 261

1 Mar Balance c/d 1,101 1 Mar Error lodge 717 100

1 Mar DD Telecom 225

1 Mar Dishonoured cheque 98

1 Mar Bank charges 39

1,123 1,123

1 Mar Balance b/d 1,101

Carry out the bank reconciliationIdentify outstanding items from the cash book not appearing on the bank statement use these in the reconciliation

Cash Book1 Feb Balance b/d 500 3 Feb Cheque 19560 1,1607 Feb Lodgement 715 2,230 3 Feb Cheque 19561 5414 Feb Lodgement 716 3,100 3 Feb Cheque 19562 3,38021 Feb Lodgement 717 1,870 16 Feb Cheque 19563 2928 Feb Lodgement 718 2,150 17 Feb Cheque 19564 4,22028 Feb Lodgement 719 650 23 Feb Cheque 19565 1,68028 Feb Balance c/d 400 23 Feb Cheque 19566 37

23 Feb Cheque 19567 34010,900 10,900

1 Mar Balance b/d 400

(1,101)Balance as per cash book (corrected)(1,537)340Cheque 19566

37Cheque 195651,160Cheque 19560

Less unpresented cheques2,800650Lodgement 719

2,150Lodgement 718Add outstanding lodgements

(2,364)Balance as per bank statement€

Bank Reconciliation Statement

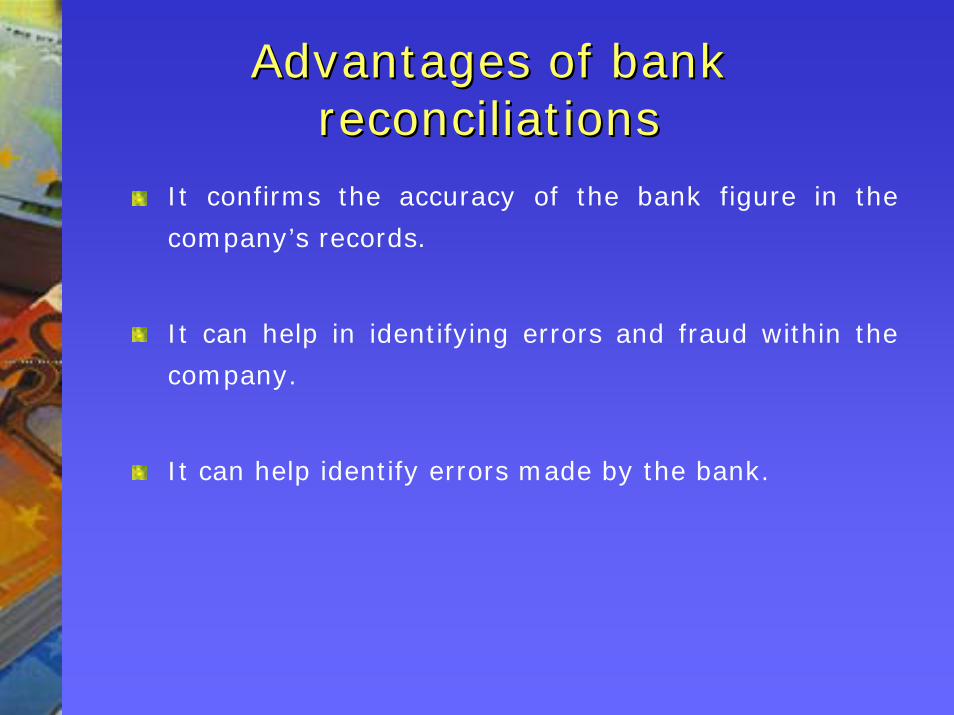

Advantages of bank Advantages of bank reconciliationsreconciliations

It confirms the accuracy of the bank figure in the

company’s records.

It can help in identifying errors and fraud within the

company.

It can help identify errors made by the bank.

Other control aspectsOther control aspects

Dealing with cash

Dealing with cheques

Dealing with debit / credit cards