1 1

Banking

For updated information, please visit www.ibef.org

MARCH

2013

2 2

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: HDFC, Axis Bank

Opportunities

Useful information

For updated information, please visit www.ibef.org

Banking MARCH

2013

3 3

Banking

For updated information, please visit www.ibef.org ADVANTAGE INDIA

Advantage India

Advantage India

• Increase in working population and growing disposable incomes will continue to propel demand for banking and related services

• Rural banking is expected to witness strong growth in the future

• Mobile and internet banking to improve operational efficiency

• Vast un-banked population highlights scope for innovation in delivery

• Rising fee incomes improving the revenue mix of banks

• High net interest margins, along with low NPA levels, ensure healthy business fundamentals.

• Wide policy support in the form of private sector participation and liquidity infusion

• Healthy regulatory oversight and credible Monetary Policy by the Reserve Bank of India (RBI) have lent strength and stability to the country’s banking sector

Total asset size:

USD28.5 trillion

FY25F

Total asset size:

USD1.5 trillion

FY12

Source: IBA report titled “Being five-star in productivity - Roadmap for excellence in Indian banking”, Aranca Research, Notes: NPA - Non Performing Assets

Growing demand Innovation in services

Business fundamentals Policy support

MARCH

2013

4 4

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: HDFC, Axis Bank

Opportunities

Useful information

For updated information, please visit www.ibef.org

Banking MARCH

2013

5 5 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Evolution of the Indian banking sector

Source: IBA, Aranca Research, BMI Notes: RBI - Reserve Bank of India, FDI - Foreign Direct Investment

Banking

• Closed market

• State-owned Imperial Bank of India was the only bank existing

• RBI was established as the central bank of country

• Quasi central banking role of Imperial Bank came to an end

• Imperial Bank expanded its network to 480 branches

• In order to increase penetration in rural areas, Imperial Bank was converted into State Bank of India

• Nationalisation of 14 large commercial banks in 1969 and 6 more banks in 1980

• Entry of private players such as ICICI intensifying the competition

• Gradual technology upgradation in PSU banks

1921

1935

1936 -1955

1956-2000 • Number of banks increased to-27 public sector banks, 22 private sector banks and 36 foreign banks

• Advent of mobile and internet banking

• Growing FDI in the Indian banking sector

Post 2000

MARCH

2013

6 6 For updated information, please visit www.ibef.org

The structure of Indian banking sector

Source: RBI, Aranca Research Note: The data on number of banks belongs to FY11

MARKET OVERVIEW AND TRENDS

Banking

Reserve Bank of India

Banks

Scheduled Commercial Banks (SCBs)

Public sector banks (27)

Private sector banks (22)

Foreign banks (36)

Regional Rural Banks (RRB) (82)

Urban cooperative banks (1,674)

Rural cooperative credit institutions (96,751)

Cooperative credit institutions

Financial institutions

All-India financial institutions

State-level institutions

Other institutions

MARCH

2013

7 7

328

418

510 596

695

846

990 1,015

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13*

For updated information, please visit www.ibef.org

Indian banking sector has grown at a healthy and steady pace … (1/2)

MARKET OVERVIEW AND TRENDS

→ Credit off-take has been surging ahead over the past decade, aided by strong economic growth, rising disposable incomes, increasing consumerism and easier access to credit

→ Over FY07-12, credit off-take expanded at a CAGR of 18.8 per cent (to USD990.5 billion)

→ Credit off take has grown at 16.7 per cent to USD1,015 billion in August 2012 as compared to USD870 billion in August 2011.

→ Demand has grown for both corporate and retail loans.

Growth in credit off-take over past few years (USD billion)

Source: Reserve Bank of India (RBI), Aranca Research; Note: CAGR: Compounded Annual Growth Rate.

Note: FY13* - Figure mentioned is up to August 2012

Banking MARCH

2013

8 8

561.39 686.89

823.46

965.67 1,115.66

1,265.10

1,349.02

FY07 FY08 FY09 FY10 FY11 FY12 FY13*

For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

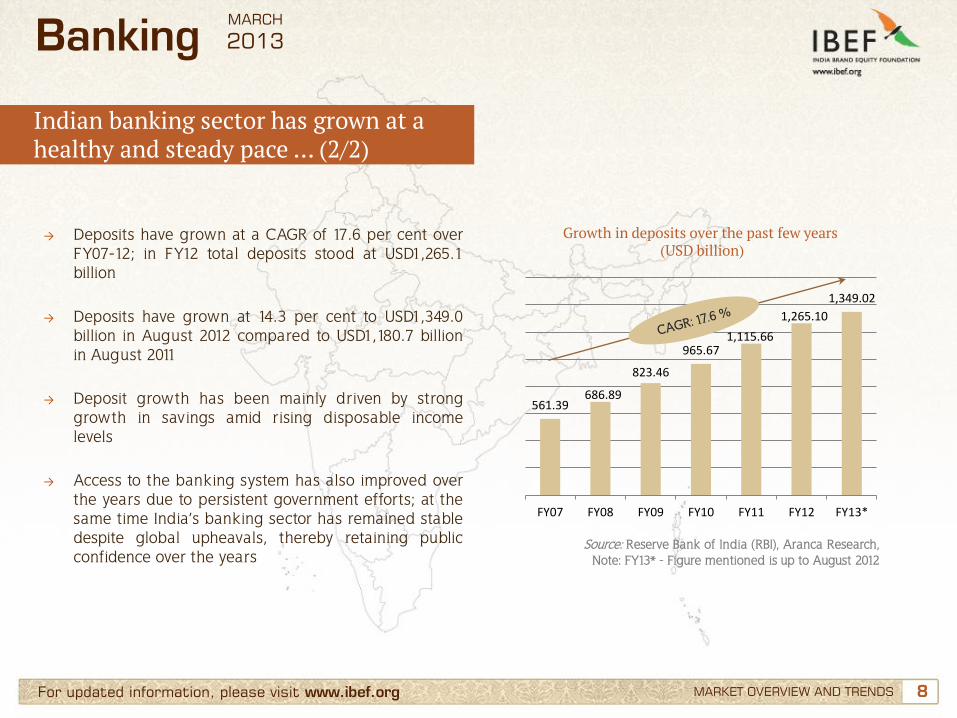

→ Deposits have grown at a CAGR of 17.6 per cent over FY07-12; in FY12 total deposits stood at USD1,265.1 billion

→ Deposits have grown at 14.3 per cent to USD1,349.0 billion in August 2012 compared to USD1,180.7 billion in August 2011

→ Deposit growth has been mainly driven by strong growth in savings amid rising disposable income levels

→ Access to the banking system has also improved over the years due to persistent government efforts; at the same time India’s banking sector has remained stable despite global upheavals, thereby retaining public confidence over the years

Banking

Indian banking sector has grown at a healthy and steady pace … (2/2)

MARCH

2013

Growth in deposits over the past few years (USD billion)

Source: Reserve Bank of India (RBI), Aranca Research, Note: FY13* - Figure mentioned is up to August 2012

9 9 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

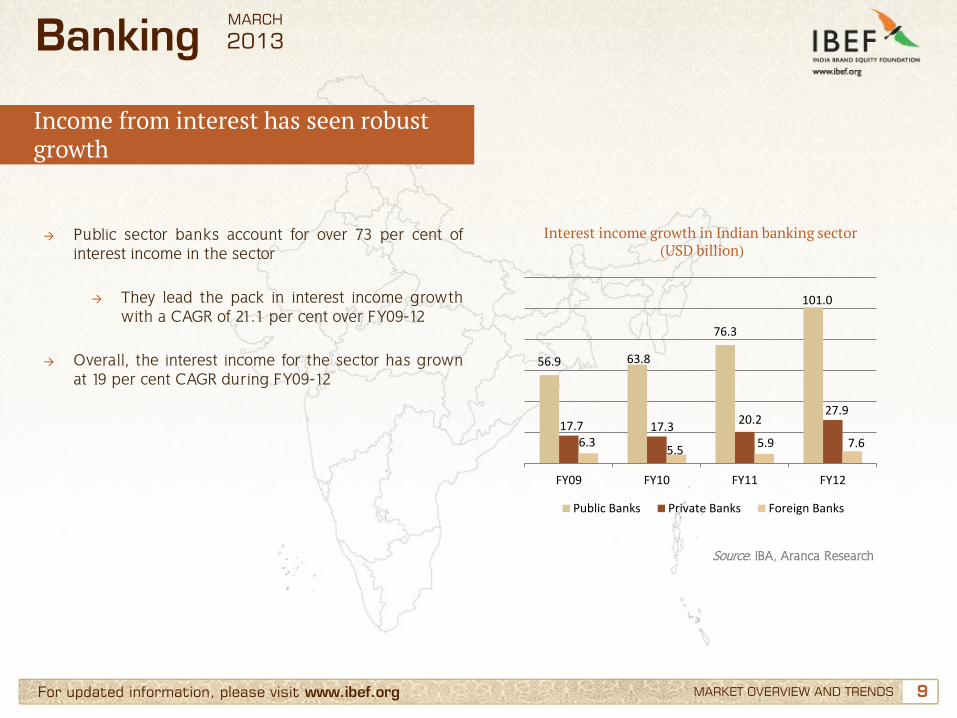

→ Public sector banks account for over 73 per cent of interest income in the sector

→ They lead the pack in interest income growth with a CAGR of 21.1 per cent over FY09-12

→ Overall, the interest income for the sector has grown

at 19 per cent CAGR during FY09-12

Source: IBA, Aranca Research

Banking

56.9 63.8

76.3

101.0

17.7 17.3 20.2

27.9

6.3 5.5

5.9 7.6

FY09 FY10 FY11 FY12

Public Banks Private Banks Foreign Banks

MARCH

2013

Income from interest has seen robust growth

Interest income growth in Indian banking sector (USD billion)

10 10 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

→ Public sector banks account for about 59 per cent of income other than from interest (‘other income’)

→ ‘Other income’ for public sector banks has risen at a CAGR of 5.7 per cent during FY09-12

→ Overall, ‘other income’ for the sector has risen at 4.5

per cent CAGR during FY09-12

Source: IBA, Aranca Research

Banking

Growth in ‘other income’ also on a positive trend

8.9

10.2 10.0 10.5

3.7 4.3 4.3 5.1

3.1 2.1 2.3 2.3

FY09 FY10 FY11 FY12

Public Banks Private Banks Foreign Banks

MARCH

2013

‘Other income’ growth in Indian banking sector (USD billion)

11 11 For updated information, please visit www.ibef.org

High NIM, Low NPA place Indian banking among the world’s best … (1/2)

MARKET OVERVIEW AND TRENDS

→ Indian banking sector enjoys healthy net interest margins (NIM) compared with global peers

→ HDFC leads the large banks with a NIM of over 4 per cent

→ Prominent Chinese banks have NIM’s between 2-3 per cent, significantly lower than Indian peers

→ Despite virtually zero cost funds, the banks in the US have NIM’s comparable to Indian peers

Healthy net interest margins (FY12)

Source: Company reports, Aranca Research Note: HDFC - Housing Development Finance Corporation,

ICICI - Industrial Credit and Investment Corporation of India, SBI - State Bank of India

Banking

4.22%

2.73%

3.85% 3.59%

HDFC ICICI SBI Axis

MARCH

2013

12 12 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

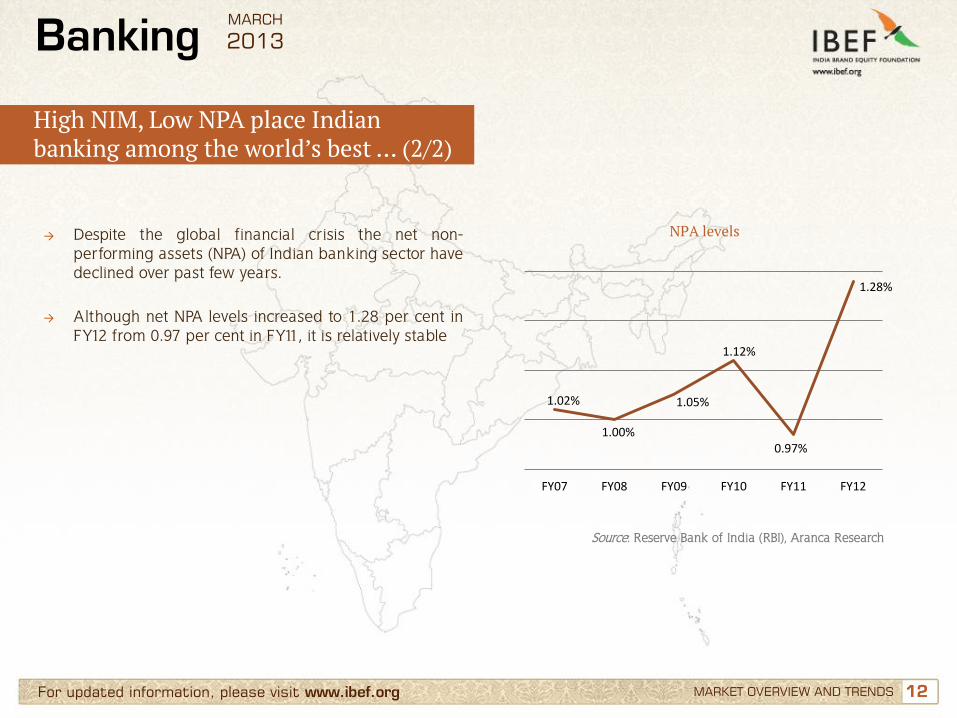

→ Despite the global financial crisis the net non-performing assets (NPA) of Indian banking sector have declined over past few years.

→ Although net NPA levels increased to 1.28 per cent in FY12 from 0.97 per cent in FY11, it is relatively stable

Source: Reserve Bank of India (RBI), Aranca Research

Banking

High NIM, Low NPA place Indian banking among the world’s best … (2/2)

1.02%

1.00%

1.05%

1.12%

0.97%

1.28%

FY07 FY08 FY09 FY10 FY11 FY12

MARCH

2013

NPA levels

13 13 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

→ Although public sector banks continue to control majority of the banking assets, their share is gradually declining

→ Share of public sector banks in total assets have declined from 76 per cent in FY05 to 72.8 per cent in FY12

Source: IBA statistics, Aranca Research

Banking

Private/foreign banks are aggressively increasing their presence … (1/2)

76.0% 72.8%

17.0% 20.2%

7.0% 7.0%

FY05 FY12

Public sector Private sector Foreign

MARCH

2013

Market share of bank groups by assets

14 14 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

→ Share of public sector banks in total deposits have also declined from 78.2 per cent in FY05 to 77.5 per cent in FY12

→ This is largely due to the fact that foreign and private sector banks are rapidly capturing share in savings deposit

Source: IBA statistics, Aranca Research

Banking

Private/foreign banks are aggressively increasing their presence … (2/2)

78.2% 77.5%

17.1% 18.2%

4.7% 4.3%

0%

20%

40%

60%

80%

100%

FY05 FY12

Public sector Private sector Foreign

MARCH

2013

Market share of bank groups by deposits

15 15 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Notable trends in the Indian banking sector … (1/2)

Improved risk management practices

• Indian banks are increasingly focusing on adopting integrated approach to risk management

• Banks have already embraced the international banking supervision accord of Basel II; interestingly, according to RBI, majority of the banks already meet capital requirements of Basel III

• Most of the banks have put in place the framework for asset-liability match, credit and derivatives risk management.

Diversification of revenue stream

• Banks are laying emphasis on diversifying the source of revenue stream to protect themselves from interest rate cycle and its impact on interest income

• Focusing on increasing fee and fund based income by launching plethora of new asset management, wealth management and treasury products

Technological innovations

• Indian banks, including public sector banks are aggressively improving their technology infrastructure to enhance customer experience and gain competitive advantage

• Internet and mobile banking is gaining rapid foothold

• Customer Relationship Management (CRM) and data warehousing will drive the next wave of technology in banks

Banking

Source: BCG-FICCI-IBA, Indian Banking sector 2020

MARCH

2013

16 16 For updated information, please visit www.ibef.org MARKET OVERVIEW AND TRENDS

Notable trends in the Indian banking sector … (2/2)

Focus on financial inclusion

• RBI has emphasised the need to focus on spreading the reach of banking services to the un-banked population of India

• Indian banks are expanding their branch network in the rural areas to capture the new business opportunity

Derivatives and risk management products

• The increasingly dynamic business scenario and financial sophistication has increased the need for customised exotic financial products

• Banks are developing Innovative financial products and advanced risk management methods to capture the market share

Consolidation

• With entry of foreign banks competition in the Indian banking sector has intensified.

• Banks are increasingly looking at consolidation to derive greater benefits such as enhanced synergy, cost take-outs from economies of scale, organisational efficiency, and diversification of risks

Banking MARCH

2013

17 17 For updated information, please visit www.ibef.org

Banks reaping benefits from increased usage of technology

Banking

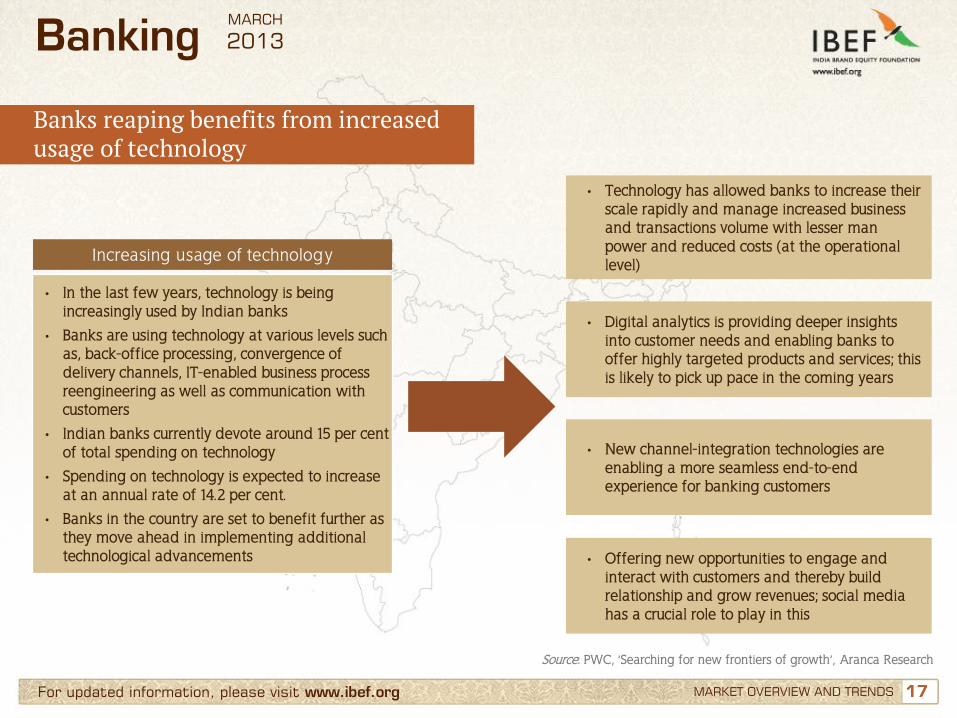

• In the last few years, technology is being increasingly used by Indian banks

• Banks are using technology at various levels such as, back-office processing, convergence of delivery channels, IT-enabled business process reengineering as well as communication with customers

• Indian banks currently devote around 15 per cent of total spending on technology

• Spending on technology is expected to increase at an annual rate of 14.2 per cent.

• Banks in the country are set to benefit further as they move ahead in implementing additional technological advancements

• Technology has allowed banks to increase their scale rapidly and manage increased business and transactions volume with lesser man power and reduced costs (at the operational level)

• Digital analytics is providing deeper insights into customer needs and enabling banks to offer highly targeted products and services; this is likely to pick up pace in the coming years

• New channel-integration technologies are enabling a more seamless end-to-end experience for banking customers

• Offering new opportunities to engage and interact with customers and thereby build relationship and grow revenues; social media has a crucial role to play in this

Increasing usage of technology

Source: PWC, ‘Searching for new frontiers of growth’, Aranca Research

MARCH

2013

MARKET OVERVIEW AND TRENDS

18 18

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: HDFC, Axis Bank

Opportunities

Useful information

For updated information, please visit www.ibef.org

Banking MARCH

2013

19 19 For updated information, please visit www.ibef.org GROWTH DRIVERS

Growth drivers of Indian banking sector

Banking

Notes: GDP - Gross Domestic Product, KYC - Know Your Customer, RBI - Reserve Bank of India, ATM - Automated Teller Machine

• Favourable demographics and rising income levels

• Strong GDP growth (CAGR of 7.7 per cent expected over 2012-17) to facilitate banking sector expansion

• The sector will benefit from structural economic stability and continued credibility of Monetary Policy

• Extension of interest subsidy to low cost home buyers

• Simplification of KYC norms, introduction of no-frills accounts and Kisan Credit Cards to increase rural banking penetration

• RBI is considering giving more licenses to private sector players to increase banking penetration

• India currently spends 6 per cent of GDP on infrastructure; Planning Commission expects this fraction to grow going ahead

• Banking sector is expected to finance part of the USD1 trillion infrastructure investments in the 12th Five Year Plan, opening a huge opportunity for the sector

Economic and demographic drivers Policy support Infrastructure financing

• Technological innovation will not only help to improve products and services but also to reach out to the masses in cost effective way

• Use of alternate channels like ATM, internet and mobile hold significant potential in India

Technological innovation

MARCH

2013

20 20

54.2 58.2 62.7

72.1

80.8

FY08 FY09 FY10 FY11 FY12

For updated information, please visit www.ibef.org

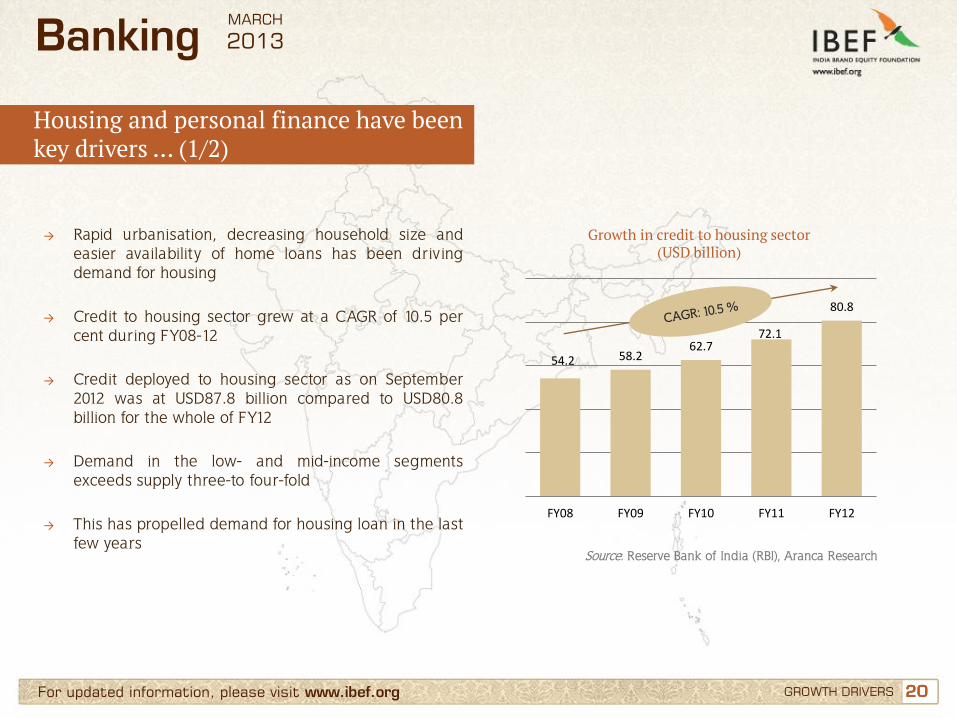

→ Rapid urbanisation, decreasing household size and easier availability of home loans has been driving demand for housing

→ Credit to housing sector grew at a CAGR of 10.5 per cent during FY08-12

→ Credit deployed to housing sector as on September 2012 was at USD87.8 billion compared to USD80.8 billion for the whole of FY12

→ Demand in the low- and mid-income segments exceeds supply three-to four-fold

→ This has propelled demand for housing loan in the last

few years

Growth in credit to housing sector (USD billion)

Source: Reserve Bank of India (RBI), Aranca Research

Banking

Housing and personal finance have been key drivers … (1/2)

GROWTH DRIVERS

MARCH

2013

21 21 For updated information, please visit www.ibef.org

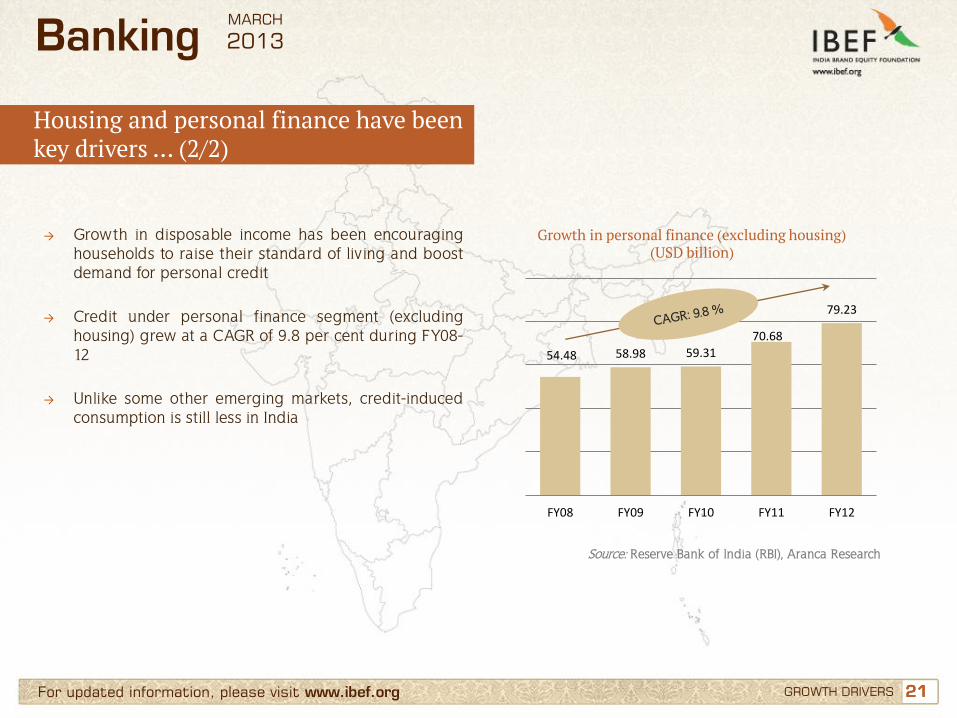

→ Growth in disposable income has been encouraging households to raise their standard of living and boost demand for personal credit

→ Credit under personal finance segment (excluding housing) grew at a CAGR of 9.8 per cent during FY08-12

→ Unlike some other emerging markets, credit-induced consumption is still less in India

Growth in personal finance (excluding housing) (USD billion)

Source: Reserve Bank of India (RBI), Aranca Research

Banking

Housing and personal finance have been key drivers … (2/2)

GROWTH DRIVERS

54.48 58.98 59.31

70.68

79.23

FY08 FY09 FY10 FY11 FY12

MARCH

2013

22 22

0

500

1,000

1,500

2,000

2,500

0

100

200

300

400

500

600

700

2001 2006 2011E 2016F

Population GDP per capita (USD)

For updated information, please visit www.ibef.org

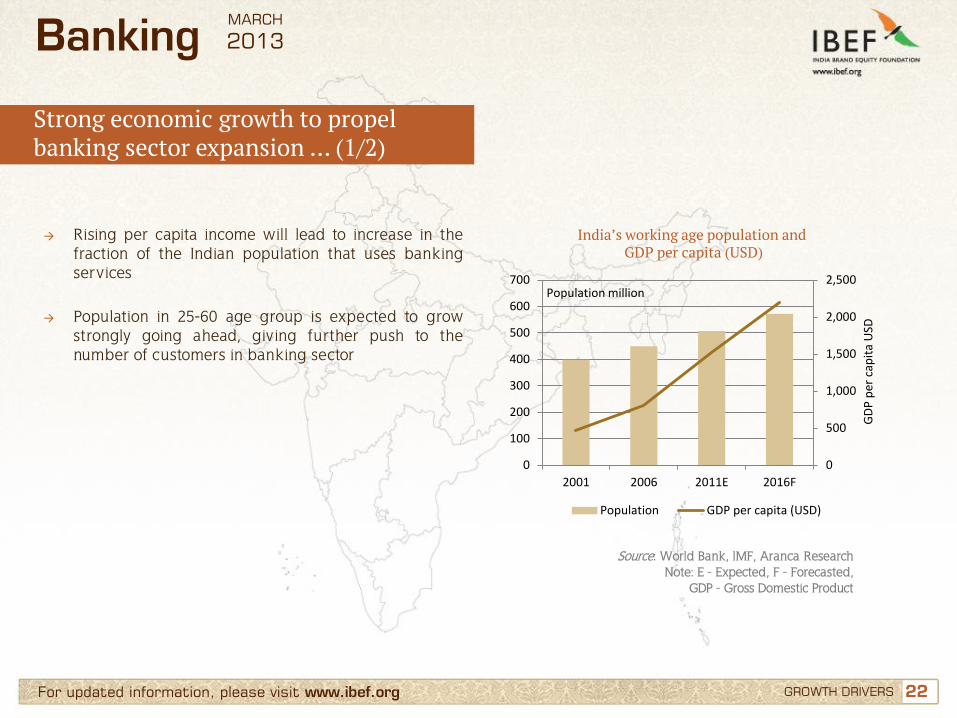

→ Rising per capita income will lead to increase in the fraction of the Indian population that uses banking services

→ Population in 25-60 age group is expected to grow strongly going ahead, giving further push to the number of customers in banking sector

India’s working age population and GDP per capita (USD)

Source: World Bank, IMF, Aranca Research Note: E - Expected, F - Forecasted,

GDP - Gross Domestic Product

Banking

Strong economic growth to propel banking sector expansion … (1/2)

GROWTH DRIVERS

Population million

MARCH

2013

GD

P p

er c

apit

a U

SD

23 23

858

978

1,173 1,431

1,775 2,218

-

500

1,000

1,500

2,000

2,500

2011E 2012F 2013F 2014F 2015F 2016F

For updated information, please visit www.ibef.org

→ India’s GDP is forecasted to grow at a healthy CAGR of 7.7 per cent during 2012-17 to USD2,218 billion

→ Strong GDP growth will facilitate banking sector expansion

→ The sector will also benefit from economic stability and credibility of Monetary Policy

Total loans: growth forecast over 2011-16

Source: Business Monitor International Ltd (BMI), Aranca Research

Banking

Strong economic growth to propel banking sector expansion … (2/2)

GROWTH DRIVERS

USD billion

MARCH

2013

24 24 For updated information, please visit www.ibef.org

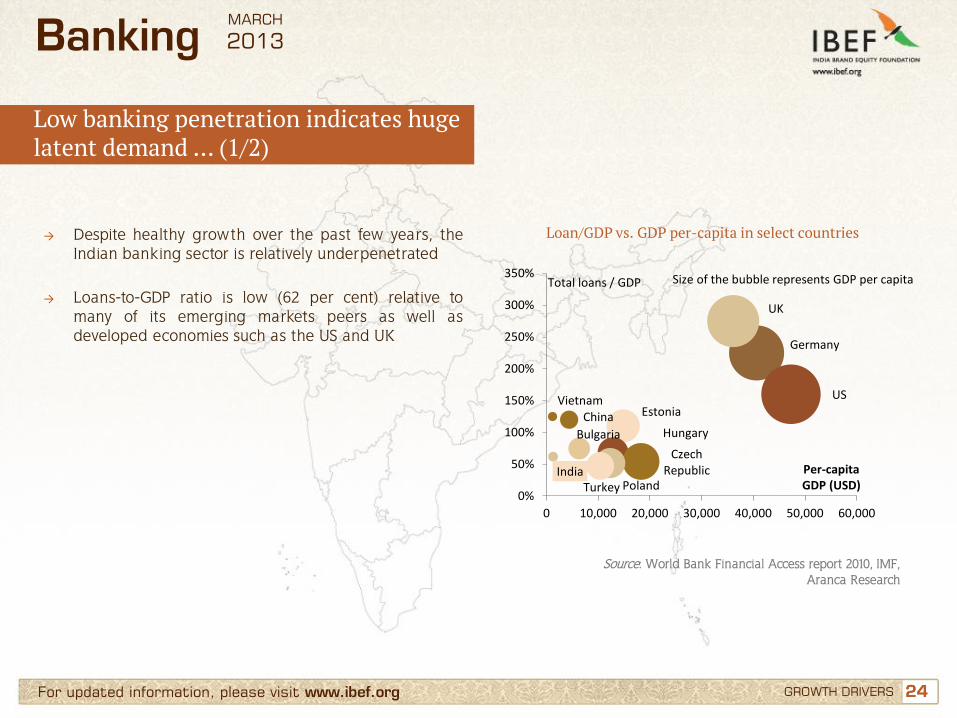

→ Despite healthy growth over the past few years, the Indian banking sector is relatively underpenetrated

→ Loans-to-GDP ratio is low (62 per cent) relative to

many of its emerging markets peers as well as developed economies such as the US and UK

Loan/GDP vs. GDP per-capita in select countries

Source: World Bank Financial Access report 2010, IMF, Aranca Research

Banking

Low banking penetration indicates huge latent demand … (1/2)

Estonia

Bulgaria Hungary

Czech Republic

Poland Turkey

Vietnam

India

China

Germany

UK

US

0%

50%

100%

150%

200%

250%

300%

350%

0 10,000 20,000 30,000 40,000 50,000 60,000

Total loans / GDP

Per-capita GDP (USD)

GROWTH DRIVERS

Size of the bubble represents GDP per capita

MARCH

2013

25 25 For updated information, please visit www.ibef.org

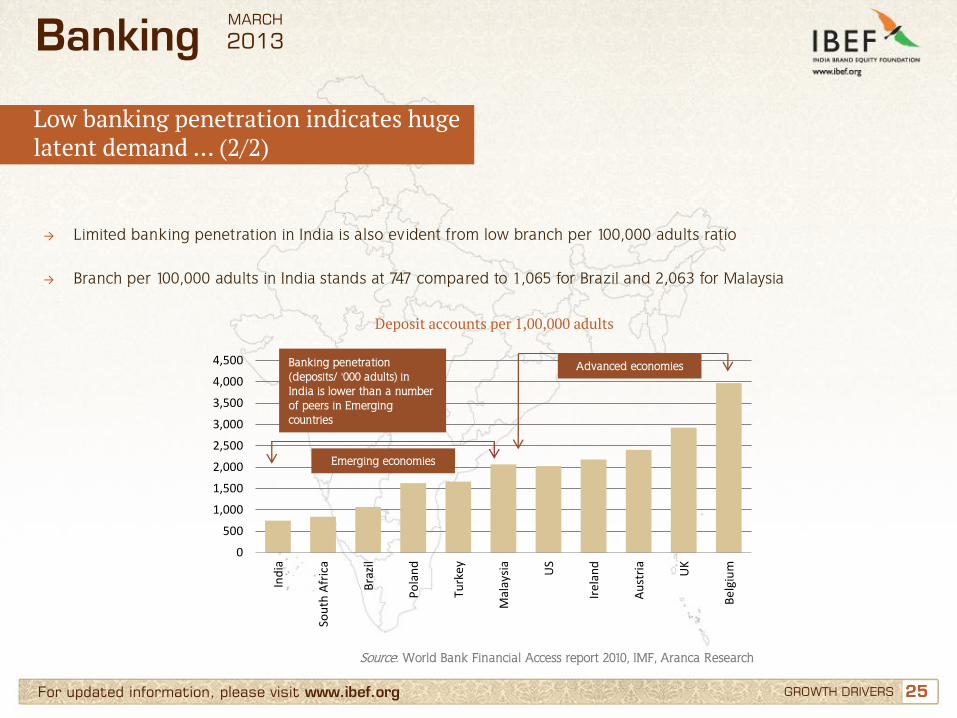

→ Limited banking penetration in India is also evident from low branch per 100,000 adults ratio

→ Branch per 100,000 adults in India stands at 747 compared to 1,065 for Brazil and 2,063 for Malaysia

Deposit accounts per 1,00,000 adults

Source: World Bank Financial Access report 2010, IMF, Aranca Research

Banking

Low banking penetration indicates huge latent demand … (2/2)

GROWTH DRIVERS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Ind

ia

Sou

th A

fric

a

Bra

zil

Po

lan

d

Turk

ey

Mal

aysi

a

US

Ire

lan

d

Au

stri

a

UK

Be

lgiu

m

Banking penetration (deposits/ '000 adults) in India is lower than a number of peers in Emerging countries

Advanced economies

Emerging economies

MARCH

2013

26 26

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: HDFC, Axis Bank

Opportunities

Useful information

For updated information, please visit www.ibef.org

Banking MARCH

2013

27 27 For updated information, please visit www.ibef.org SUCCESS STORIES: HDFC, AXIS BANK

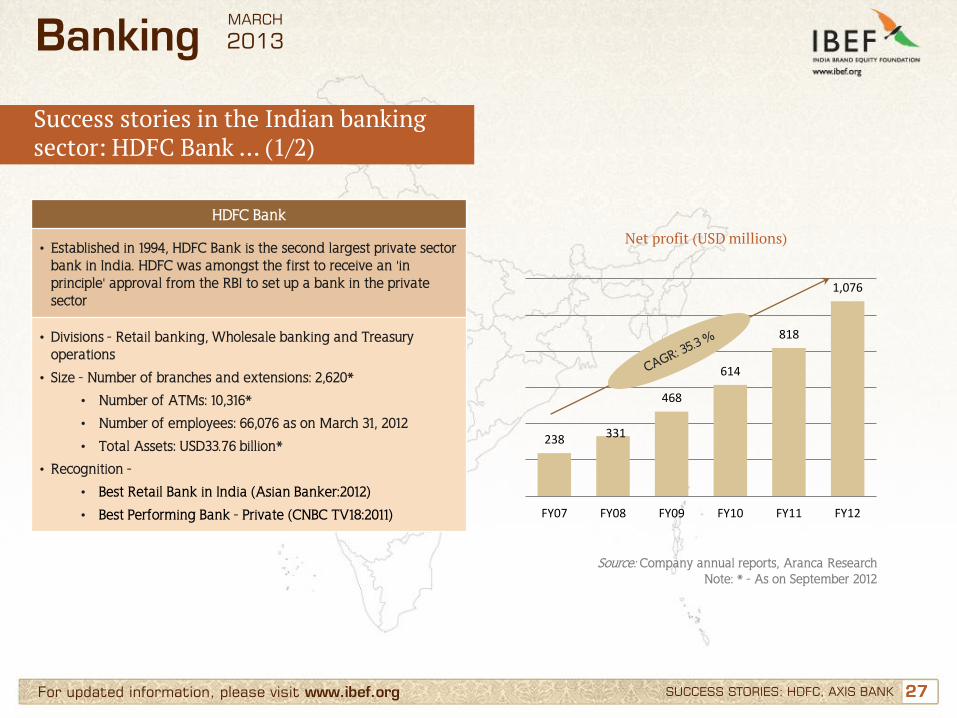

Success stories in the Indian banking sector: HDFC Bank … (1/2)

Banking

HDFC Bank

• Established in 1994, HDFC Bank is the second largest private sector bank in India. HDFC was amongst the first to receive an 'in principle' approval from the RBI to set up a bank in the private sector

• Divisions - Retail banking, Wholesale banking and Treasury operations

• Size - Number of branches and extensions: 2,620*

• Number of ATMs: 10,316*

• Number of employees: 66,076 as on March 31, 2012

• Total Assets: USD33.76 billion*

• Recognition -

• Best Retail Bank in India (Asian Banker:2012)

• Best Performing Bank - Private (CNBC TV18:2011)

Net profit (USD millions)

Source: Company annual reports, Aranca Research Note: * - As on September 2012

238 331

468

614

818

1,076

FY07 FY08 FY09 FY10 FY11 FY12

MARCH

2013

28 28

13

21 26

33

41

21

30 35

43

51

FY08 FY09 FY10 FY11 FY12

Advances Deposits

USD billion

For updated information, please visit www.ibef.org SUCCESS STORIES: HDFC, AXIS BANK

Success stories in the Indian banking sector: HDFC Bank … (2/2)

Source: Company annual reports, Aranca Research

Banking

Advances and deposits Income break-up (FY12)

70%

24%

6%

Net Interest Income

Fee Income

Other Income

MARCH

2013

29 29 For updated information, please visit www.ibef.org SUCCESS STORIES: HDFC, AXIS BANK

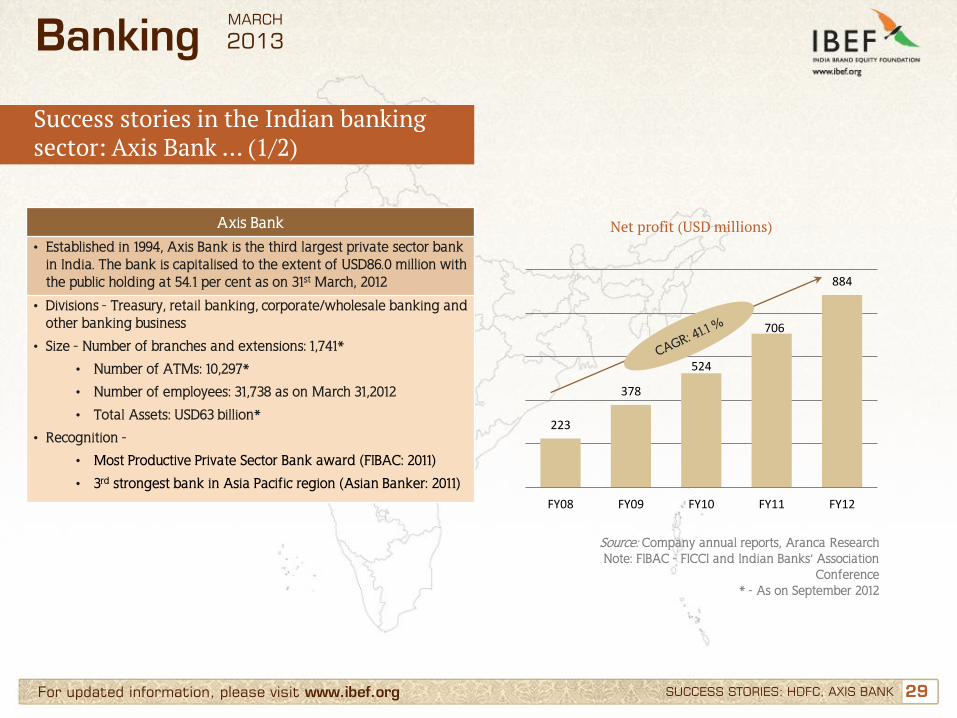

Success stories in the Indian banking sector: Axis Bank … (1/2)

Banking

Axis Bank

• Established in 1994, Axis Bank is the third largest private sector bank in India. The bank is capitalised to the extent of USD86.0 million with the public holding at 54.1 per cent as on 31st March, 2012

• Divisions - Treasury, retail banking, corporate/wholesale banking and other banking business

• Size - Number of branches and extensions: 1,741*

• Number of ATMs: 10,297*

• Number of employees: 31,738 as on March 31,2012

• Total Assets: USD63 billion*

• Recognition -

• Most Productive Private Sector Bank award (FIBAC: 2011)

• 3rd strongest bank in Asia Pacific region (Asian Banker: 2011)

Net profit (USD millions)

Source: Company annual reports, Aranca Research Note: FIBAC - FICCI and Indian Banks’ Association

Conference * - As on September 2012

223

378

524

706

884

FY08 FY09 FY10 FY11 FY12

MARCH

2013

30 30

12

17 22

30 35

18

24

29

39 46

FY08 FY09 FY10 FY11 FY12

Advances Deposits

USD billion

For updated information, please visit www.ibef.org SUCCESS STORIES: HDFC, AXIS BANK

Success stories in the Indian banking sector: Axis Bank … (2/2)

Source: Company annual reports, Aranca Research

Banking

Advances and deposits Income break-up

60%

37%

3%

Net Interest income

Fee Income

Other Income

MARCH

2013

31 31

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: HDFC, Axis Bank

Opportunities

Useful information

For updated information, please visit www.ibef.org

Banking MARCH

2013

32 32

133 151

174 194

225 265

295

FY06 FY07 FY08 FY09 FY10 FY11QE

FY12RE

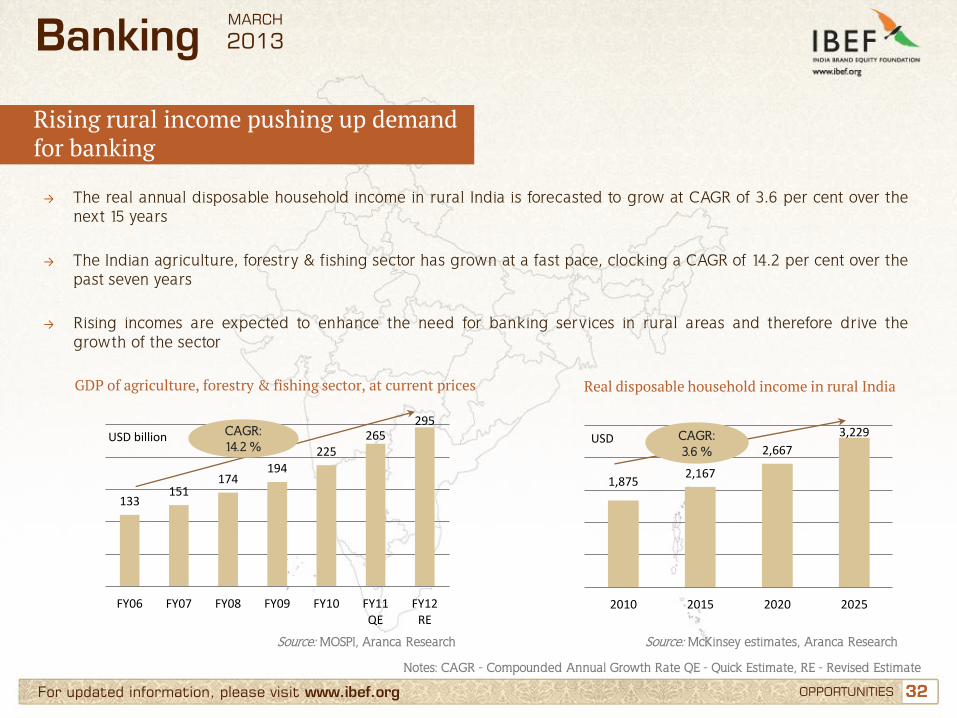

For updated information, please visit www.ibef.org OPPORTUNITIES

Rising rural income pushing up demand for banking

Notes: CAGR - Compounded Annual Growth Rate QE - Quick Estimate, RE - Revised Estimate

Banking

→ The real annual disposable household income in rural India is forecasted to grow at CAGR of 3.6 per cent over the next 15 years

→ The Indian agriculture, forestry & fishing sector has grown at a fast pace, clocking a CAGR of 14.2 per cent over the past seven years

→ Rising incomes are expected to enhance the need for banking services in rural areas and therefore drive the growth of the sector

GDP of agriculture, forestry & fishing sector, at current prices

Source: MOSPI, Aranca Research

Real disposable household income in rural India

Source: McKinsey estimates, Aranca Research

1,875 2,167

2,667

3,229

2010 2015 2020 2025

USD billion USD CAGR: 14.2 %

CAGR: 3.6 %

MARCH

2013

33 33

0.4 9.2

15.2

24.29

37.48

40.36

2007 2008 2009 2010 2011 2012*

For updated information, please visit www.ibef.org

Mobile banking to provide a cost effective solution

Source: TRAI, Aranca Research Note: * - As on September 2012

Banking

Banking penetration is low in rural India

• Of the 600,000 village habitations in India only 5 per cent have a

commercial bank branch

• Only 40 per cent of the adult population has bank accounts

• Debit card holders constitute only 13 per cent of the population and

only 2 per cent have a credit card

• 51.4 per cent of nearly 89.3 million farm households do not have

access to any credit either from institutional or non-institutional

sources

• Only 13 per cent of farm households are availing loans from the

banks in the income bracket of < USD1000

Soaring rural teledensity opens avenue of mobile banking

→ Agriculture requires timely credit to enable smooth functioning. However, only one-eighth of farm households avail bank credit

→ Local money-lending practices involve interest rates well above 30 per cent, therefore making bank credit a compelling alternative

→ Tele-density in rural India soared to nearly 40.4 per cent in 2012* from less than 1 per cent in 2007

→ Banks, telecom providers and RBI are making efforts to make inroads into the un-banked rural India through mobile banking solutions

OPPORTUNITIES

%

MARCH

2013

34 34

Mobile commerce

Payment of bills

Mobile banking (fund transfers,

etc.)

Mobile recharge

Mobile remittances

For updated information, please visit www.ibef.org

Mobile banking to transform the banking space

Banking

OPPORTUNITIES

• Mobile banking allows customers to avail banking services on the move through their mobile phones. The growth of mobile banking could impact the banking sector significantly

• Mobile banking across the world is still at a primitive stage with countries like China, India and UAE taking the lead

• Mobile banking is especially critical for countries like India, as it promises to provide an opportunity to provide banking facilities to a previously under-banked market

• RBI has taken several steps to enable mobile payments, which forms an important part of mobile banking; the central bank has recently removed the transaction limit of INR50,000 and allowed banks to set their own limits

• Mobile banking transactions in India will cross 340 million by 2015 and would result in cost savings of approximately INR11 billion (USD230 million)

Evolution of mobile banking

Key services provided through mobile banking

Source: PWC, ‘Searching for new frontiers of growth’, Aranca Research

MARCH

2013

35 35

Contents

Advantage India

Market overview and trends

Growth drivers

Success stories: HDFC, Axis Bank

Opportunities

Useful information

For updated information, please visit www.ibef.org

Banking MARCH

2013

36 36 For updated information, please visit www.ibef.org USEFUL INFORMATION

Industry Associations

Indian Banks' Association World Trade Centre, 6th Floor Centre 1 Building, World Trade Centre Complex, Cuff Parade, Mumbai - 400 005 India E-mail: [email protected]

Banking MARCH

2013

37 37 For updated information, please visit www.ibef.org

Glossary

→ ATM: Automated Teller Machines

→ CAGR: Compound Annual Growth Rate

→ FY: Indian financial year (April to March)

→ GDP: Gross Domestic Product

→ INR: Indian Rupee

→ KYC: Know Your Customer

→ NIM: Net interest margin

→ NPA: Non-performing assets

→ RBI: Reserve Bank of India

→ USD: US Dollar → Conversion rate used: USD1=INR 48

→ Wherever applicable, numbers have been rounded off to the nearest whole number

USEFUL INFORMATION

Banking MARCH

2013

38

India Brand Equity Foundation (IBEF) engaged Aranca to prepare this presentation and the same has been prepared by Aranca in consultation with IBEF. All rights reserved. All copyright in this presentation and related works is solely and exclusively owned by IBEF. The same may not be reproduced, wholly or in part in any material form (including photocopying or storing it in any medium by electronic means and whether or not transiently or incidentally to some other use of this presentation), modified or in any manner communicated to any third party except with the written approval of IBEF. This presentation is for information purposes only. While due care has been taken during the compilation of this

presentation to ensure that the information is accurate to the best of Aranca and IBEF’s knowledge and belief, the content is not to be construed in any manner whatsoever as a substitute for professional advice. Aranca and IBEF neither recommend nor endorse any specific products or services that may have been mentioned in this presentation and nor do they assume any liability or responsibility for the outcome of decisions taken as a result of any reliance placed on this presentation. Neither Aranca nor IBEF shall be liable for any direct or indirect damages that may arise due to any act or omission on the part of the user due to any reliance placed or guidance taken from any portion of this presentation.

For updated information, please visit www.ibef.org DISCLAIMER

Banking MARCH

2013

Disclaimer