1

Brazil Beyond the

International Crisis

October 2009

Henrique de Campos Meirelles

2

Economic Fundamentals and

Anti-Crisis Measures

3

Inflation

Source: Central Bank of Brazil

Jan 04

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

Jan 10

Sep 09

4,34% 2009

4,30%

% a

.a.

0

2

4

6

8

10 IPCA (12-month cumulative) market

expectation

4

Real Interest Rate

Sources: BM&F Bovespa and Central Bank of Brazil (Focus)

4

6

8

10

12

14

16

18

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

%

Aug 08

8.9%

5Sources: Central Bank of Brazil

% o

f G

DP

Net Public Debt

02 03 04 05 06 07 08

22

27

32

37

42

47

5251,3

53,5

48,2 48,045,9

43,9

38,8

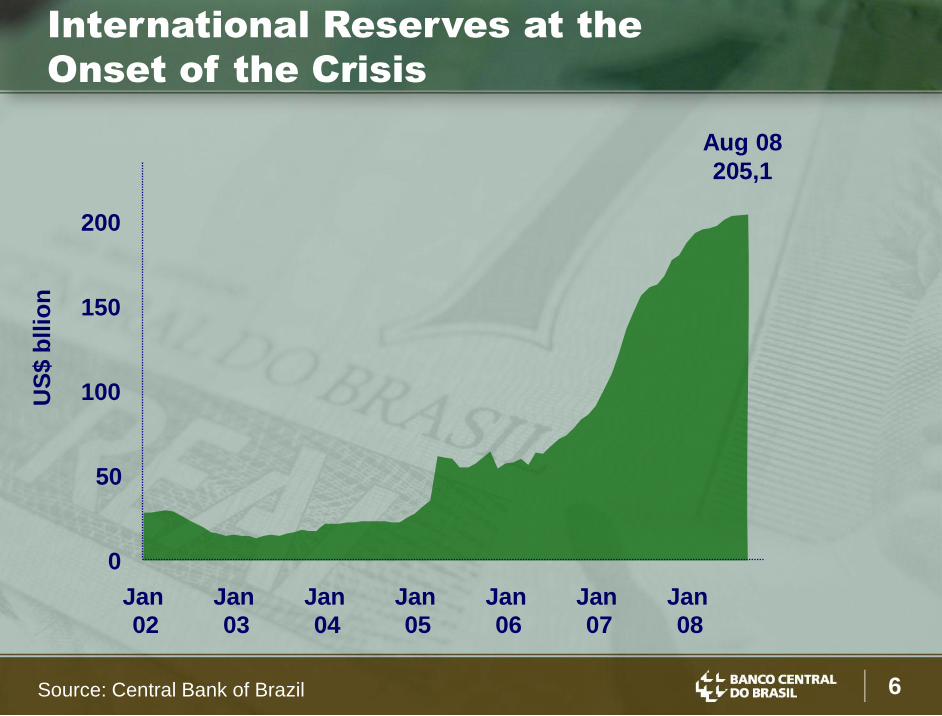

6Source: Central Bank of Brazil

50

100

150

200

US

$ b

llio

n

Aug 08

205,1

0

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

International Reserves at the

Onset of the Crisis

7

0

1

2

3

4

5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

% p

.a.

avg. 90’s avg. 2004-2008

GDP growth Current Account Balance

avg. 90’s avg. 2004-2008

% o

f G

DP

Brazil

Brazil at the Onset of the Crisis:

Better Prepared than in the Past

Source: Central Bank of Brazil

0

5

10

15

20

25

% o

f G

DP

Net External Debt

avg. 90’s avg. 2004-2008

(-1.8% in 2008)

8

Domestic Demand and Supply

Source: IBGE

%

9.3

domestic demand GDP

change year-over-year

-4.5

-3.0

-1.5

0.0

1.5

3.0

4.5

6.0

7.5

9.0

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

6.8

9

Correct Diagnosis

1) credit became scarce

About 20% of the total credit had external funding

2) crowding out of credit

Domestic companies which were funded in the foreign market

started to be funded by domestic banks

3) Companies in derivative markets helped to deteriorate credit

conditions

4) Lack of liquidity in the interbank market

10

Correct Diagnosis: Consequences

1) Liquidity squeeze in local and foreign currencies

2) Contraction of credit to exporters

3) Slowdown of economic activity in industries dependent on

credit

4) Severe stress of small and medium banks

5) Large banks’ exposure with companies exposed to

exchange rates derivates

11

Initiatives in the foreign currency market

Liquidity injection in foreign currency

Auctions directed at exporters: US$ 24.4 billion

Spot market sale of dollars: US$ 14.5 billion

Exchange rate swaps auctions: US$ 33 billion

Clearing of the Central Bank swap position

Anti-crisis Measures

Source: Central Bank of Brazil

12

Compulsory reserves placed at the Central Bank at

August 2008: R$259,4 billion

Compulsory Reserves

Source: Central Bank of Brazil

13

Liquidity injection in local currency

Compulsory reserves reduction: R$ 99.8 billion

Liquidity for smaller institutions: R$ 42.2 billion

Authorization of Bank Deposit Receipt with up to a

R$20 million guarantee by FGC, the national private

deposit insurance institution

Anti-crisis Measures

Source: Central Bank of Brazil

14

Credit Granting (Daily Average)R

$ b

illi

on

average Jan-Sep 08

7.1 7,3

5.5

5.9

6.3

6.7

7.1

7.5

Jan08

Mar08

May08

Jul08

Sep08

Nov08

Jan09

Mar09

May09

Jul*09

Sep09

average Mar-Sep 09

7.1

Source: Central Bank of Brazil

15

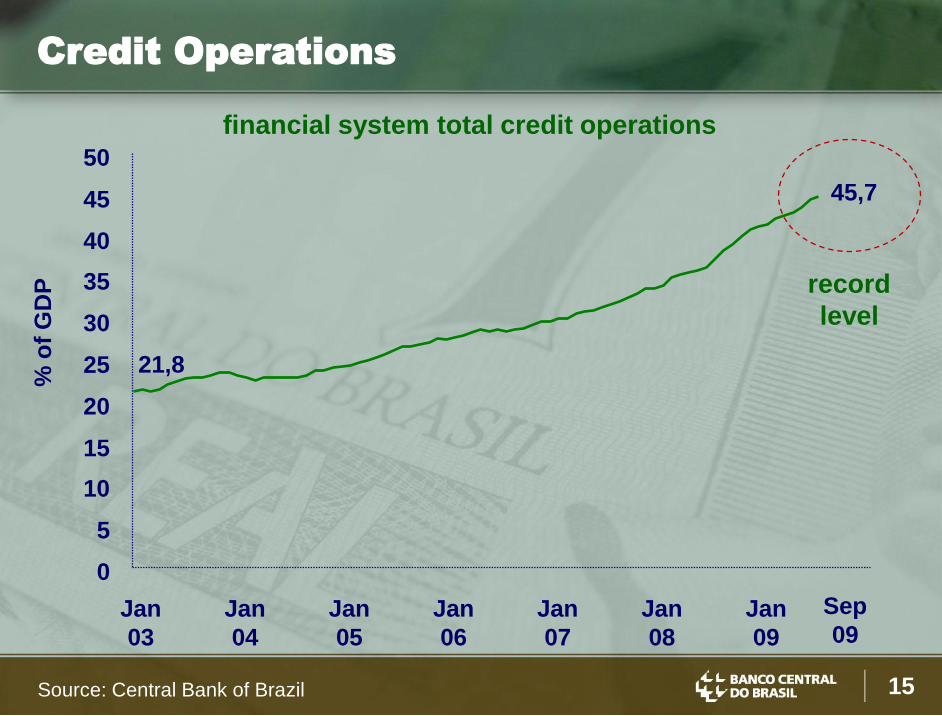

financial system total credit operations

21,8

0

5

10

15

20

25

30

35

40

45

50

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Sep

09

% o

f G

DP

Jan

09

Credit Operations

45,7

record

level

Source: Central Bank of Brazil

16

0

50

100

150

200

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

US

$ b

illi

on

Nov 4th 09

233.2Aug 08

205.1highest

level

International Reserves

Source: Central Bank of Brazil

17

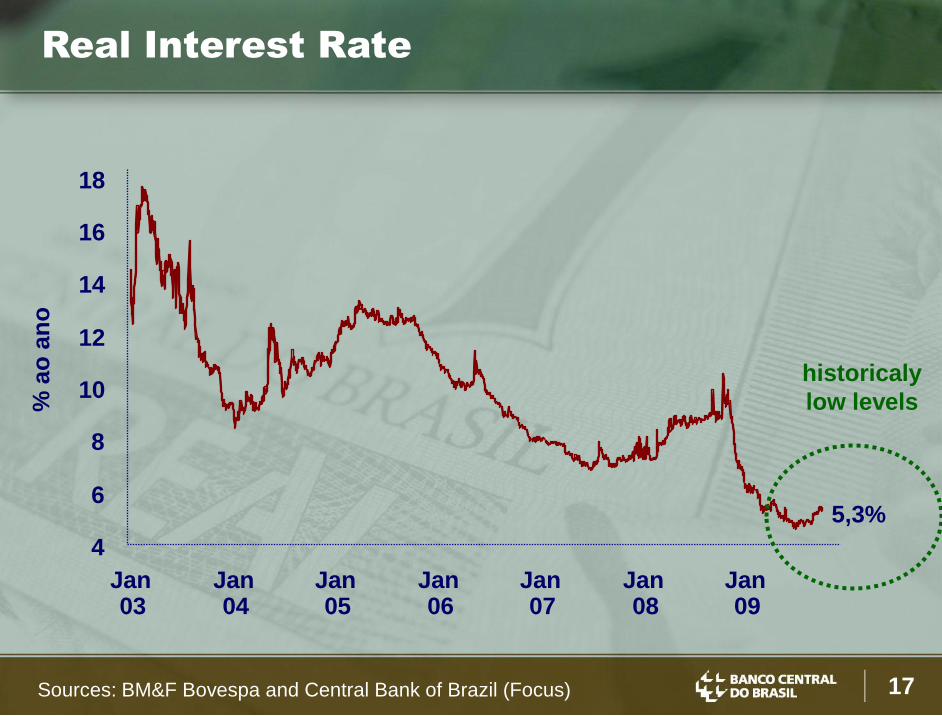

Real Interest Rate

4

6

8

10

12

14

16

18

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

% a

o a

no

5,3%

historicaly

low levels

Sources: BM&F Bovespa and Central Bank of Brazil (Focus)

18Sources: Central Bank of Brazil

22

27

32

37

42

47

52

02 03 04 05 06 07 08 09 10 11 12 13

% o

f G

DP

forecast

Net Public Debt

51,3

53,5

48,2 48,045,9

43,9

38,8

44,042,0

39,438,0

36,0

19

Banking System Soundness and

Capital Markets

20

18.5 17.4 17.8 17.3

16.4 17.2

0

4

8

12

16

20

2004 2005 2006 2007 2008 Jul 09

international

standard (8%)

regulatory

minimum (11%)

%Bank-Capital Adequacy: Basel Index

relation between capital and risk weighted assets

Source: Central Bank of Brazil

21

Central Bank of Brazil Comprehensive

Approach

Source: Central Bank of Brazil

financial

regulation

monetary

policy

financial

supervision

Comprehensive approach strengthens financial stability

22

Broad regulation: 21 modalities of financial institutions supervised by

the Central Bank of Brazil

11. Security Distribution Companies;

12. Real Estate Credit Companies;

13. Savings and Loan Associations;

14. Mortgage Companies;

15. Cooperative Companies;

16. Caixa Econômica Federal;

17. Savings Banks;

18. National Social and Economic Development

Bank (BNDES);

19. Consórcio Management and their groups;

20. Foreign Exchange Bank;

21. Financial institutions in liquidation process.

1. Multiple Banks;

2. Commercial Banks;

3. Development Banks;

4. Development Agencies;

5. Investment Banks;

6. Credit, Finance and Investment

Companies;

7. Microcredit Companies;

8. Leasing Companies;

9. Stock and Bond Brokerage

Companies;

10. Exchange Brokerage Companies;

Financial System Supervision

Source: Central Bank of Brazil

23

Bad-debt provisions take into consideration expected

losses, and not only the possible payment in arrears;

Capital requirements are applied in consolidated terms,

including off-balance sheet exposures;

Daily monitoring of both liquidity and market risk.

Financial System Supervision

24

The Central Bank monitors over-the-counter operations

performed by financial institutions;

The Central Bank receives information from all Clearing

Houses.

Financial System Supervision:

OTC Operations

25

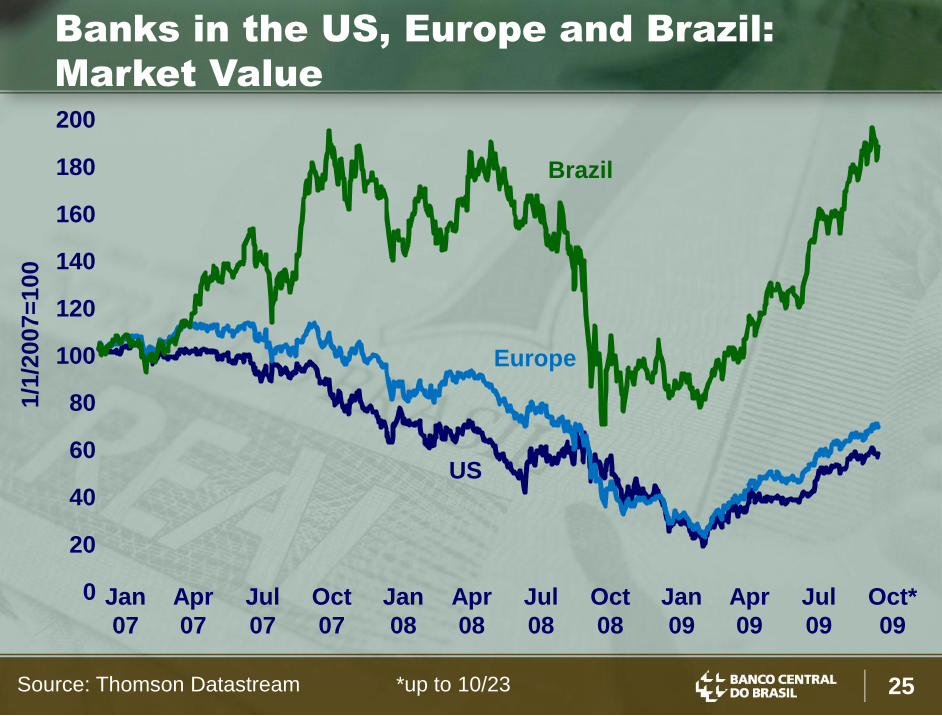

Banks in the US, Europe and Brazil:

Market Value

Source: Thomson Datastream *up to 10/23

1/1

/2007=

100

0

20

40

60

80

100

120

140

160

180

200

Jan

07

Apr

07

Jul

07

Oct

07

Jan

08

Apr

08

Jul

08

Oct

08

Jan

09

Apr

09

Jul

09

Oct*

09

Brazil

Europe

US

26

Capital Markets

Source: CVM *in the year through September

**in the year through Oct 23

R$ b

illi

on

primary issues of securities

equities** debentures others

0

20

40

60

80

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009*

secondary market

2009 through Oct 23:

Redecard R$2.2 bi

Visanet R$8.4 bi

MRV R$0.1 bi

BR Malls Part. R$0.4 bi

Light R$0.8 bi

Hypermarcas R$0.2 bi

Natura R$1.5 bi

Tivit R$0.7 bi

PDG Realty R$0.3 bi

Gol R$0.4 bi

Brookfield Inc. R$0.1 bi

Total R$15.1 bi

27

Stock of Foreign InvestmentU

S$ b

illi

on

Sources: BCB and CVM

international

reserves

equities

(Bovespa)0

30

60

90

120

150

180

210

240

270

Jan

07

Apr

07

Jul

07

Oct

07

Jan

08

Apr

08

Jul

08

Oct

08

Jan

09

Apr

09

Aug

09

fixed income

investment

28

The New Macroprudential Approach

The Basel Committee for Bank Supervision established a five

key points strategy:

o Strengthening the regulatory capital framework

o Increasing banks’ liquidity buffers

o Enhancing bank governance, risk management and

supervision

o Improving market transparency

o Cross-border supervisory cooperation for internationally

active banks

The objective is to promote a banking sector that is more

resilient to future periods of economic and financial stress and

help reduce systemic risk

29

Industrial Production, Sales and

Employment

30

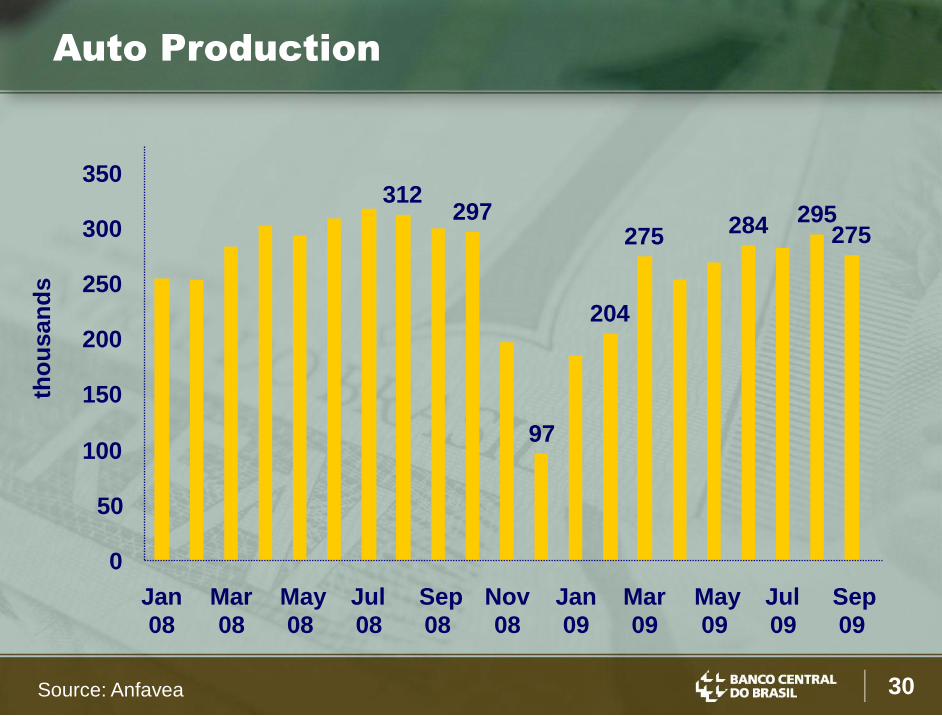

312297

97

204

275 284 295275

0

50

100

150

200

250

300

350

Jan

08

Mar

08

May

08

Jul

08

Sep

08

Nov

08

Jan

09

Mar

09

May

09

Jul

09

Sep

09

Auto Production

Source: Anfavea

tho

usan

ds

31

Jan

07 =

100

50

60

70

80

90

100

110

120

130

Jan 08

Mar 08

Mai 08

Jul 08

Set 08

Nov 08

Jan 09

Mar 09

Mai 09

Jul 09

Set 09

Sources: IBGE and Central Bank of Brazil (Focus)

Industrial Production

seasonally adjustedforecast

32Source: IBGE

índ

ice d

e 0

a 1

00

58,5

54,4

60,159,4 60,462,0

58,1

52,5

47,4

58,2

65,9

25

30

35

40

45

50

55

60

65

1T

06

2T

06

3T

06

4T

06

1T

07

2T

07

3T

07

4T

07

1T

08

2T

08

3T

08

4T

08

1T

09

2T

09

3T

09

4T

09

49,4

Oct 08: all

sectors with

indexes

above 50

seasonally adjusted

Industrial Confidence

33Source: IBGE

95

100

105

110

115

120

125

130

135

Jan

04

Jul

04

Jan

05

Jul

05

Jan

06

Jul

06

Jan

07

Jul

07

Jan

08

Jul

08

Jan

09

Jul

09

200

4 =

100

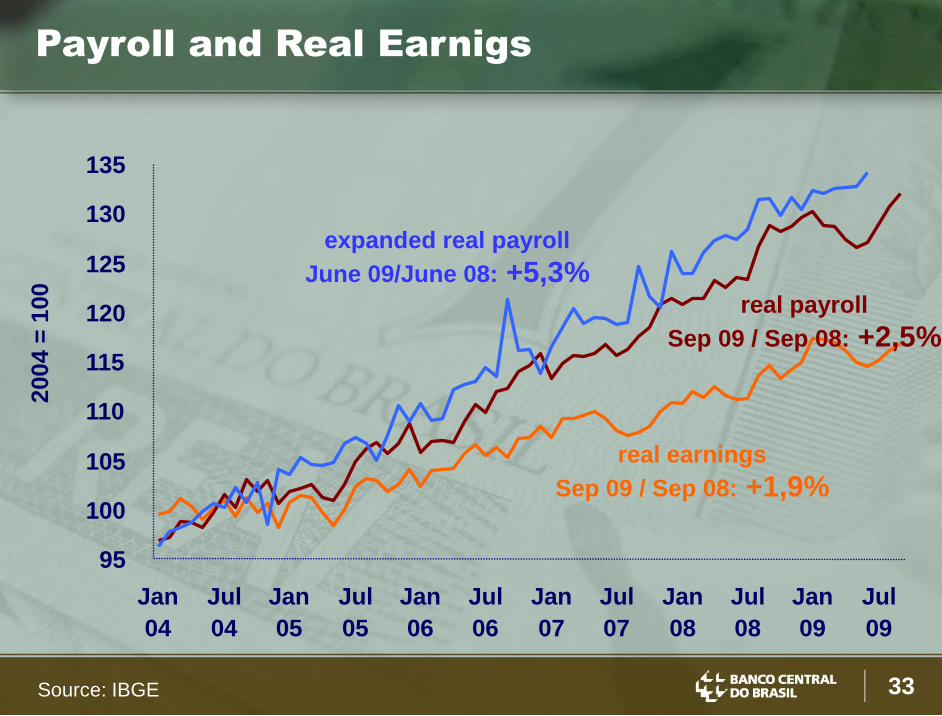

real earnings

Sep 09 / Sep 08: +1,9%

real payroll

Sep 09 / Sep 08: +2,5%

Payroll and Real Earnigs

expanded real payroll

June 09/June 08: +5,3%

34

95

100

105

110

115

120

Jan

06

Jul

06

Jan

07

Jul

07

Jan

08

Jul

08

Jan

09

Jul

09

200

6 =

100

Expanded Real Payroll and

Supermarket Sales

expanded real

payroll

supermarket

sales

Sources: ABRAS and IBGE (seasoonally adjusted)

35Source: IBGE

seasonally adjusted

Retail Sales

Jan07

Apr07

Jul07

Oct07

Jan08

Apr08

Jul08

Oct08

Jan09

Apr09

Jul09

Aug 09 / Aug 08: +5,3%

Aug 09 / Jul 09: +0,7%

Jan

2007 =

100

100

105

110

115

120

36Source : IBGE

%

7,7

6

7

8

9

10

11

12

13

Jan Fev Mar Abr Mai Jun Jul Ago Set Out Nov Dez

2004

2005

2006

2007

2008

2009

Unemployment Rate

37

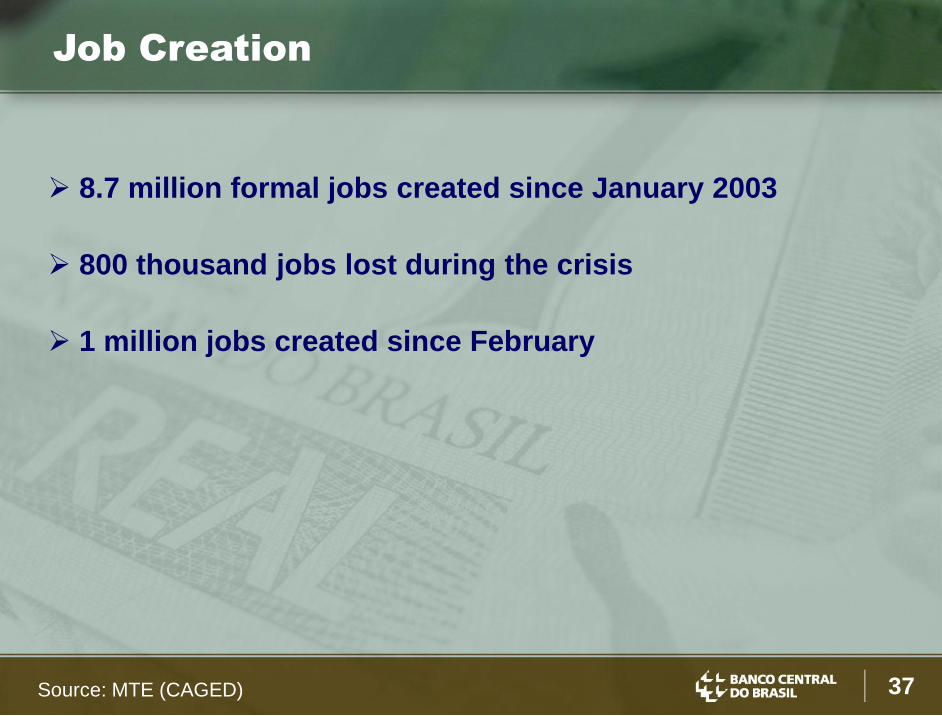

Job Creation

Source: MTE (CAGED)

8.7 million formal jobs created since January 2003

800 thousand jobs lost during the crisis

1 million jobs created since February

38Source: CNI (INEC)

Consumer Confidence

116.0

114.7

111.4 111.0111.5

109.8

115.6

109.8

106.3

110.3

115.4

100

102

104

106

108

110

112

114

116

3Q

2006

4Q 1Q

2007

2Q 3Q 4Q 1Q

2008

2Q 3Q 4Q 1Q

2009

2Q 3Q

2001 =

100

39

GDP Recovery

40

GDP Growth

85

87

89

91

93

95

97

99

101

103

105

1st Q

2008

2nd Q 3rd Q 4th Q 1st Q

2009

2nd Q

United States

Euro Area

Japan

Brazil

South Korea

quarterly GDP seasonally adjusted

4th

Qu

art

er

2008 =

100

Source: Bloomberg

41

Growth with Social Inclusion

42

Lower Income and Middle Class

Source: FGV; lower = E class, middle = C class.

42.4 41.644.1 45.5

48.250.2

52.3 53.2

29.2 30.427.9

24.4 23.020.8

18.4 18.3

0

10

20

30

40

50

60

Jun

02

Jun

03

Jun

04

Jun

05

Jun

06

Jun

07

Jun

08

Jun

09

middle income

lower level income

% o

f p

op

ula

tio

n

43Fonte: FGV-CPS

Income Inequality

0,6001

0,5937 0,5947 0,5957

0,58860,5829

0,57170,5680

0,5620

0,5546

0,50

0,52

0,54

0,56

0,58

0,60

98 99 00 01 02 03 04 05 06 07

Gini coefficient

44

November 2009

Henrique de Campos Meirelles