Brazilian textile and clothing from the perspective of the

global value chain - present and future possibilities

March 20th, 2017

Fernando Pimentel President

Page 2 October 2016, Zürich

Brazilian textile and clothing

from the perspective of the

global value chain - present

and future possibilities

2017

The specific objectives of this study have been listed in the Terms of

References published by SENAI-CETIQT:

1 Describe and characterize the textile and clothing industry - processes, products and consumption - in

Brazil and worldwide, emphasizing their performance in global, regional and local value networks

2 Mapping the Global Value Chain of the textiles and clothing industry as its main concepts, actors, forms of

governance and production strategies, distribution and new markets

3 Identify the main trends of leadership, governance and business models styles of the main local and

regional firms that coordinate global value chains in the industry

4 Identify opportunities and assess the skills of the Brazilian industry in the different links and segments for

integration into the Global Value Chain

6 Provide SENAI-CETIQT with vocational training dynamic guidelines, service and investment delivery in

research and technological innovation - that meet the international standards set by global value chains -

to support the sector in its dynamic integration planned in the world production and consumption

7 Produce a SWOT analysis (strengths, weaknesses, opportunities and threats) that shows the impacts of

entry of the sector in that Global Value Chain

5 Propose public and / or private policies and outline strategic actions to Brazil be integrated into the Global

Value Chain in the textiles and clothing industry

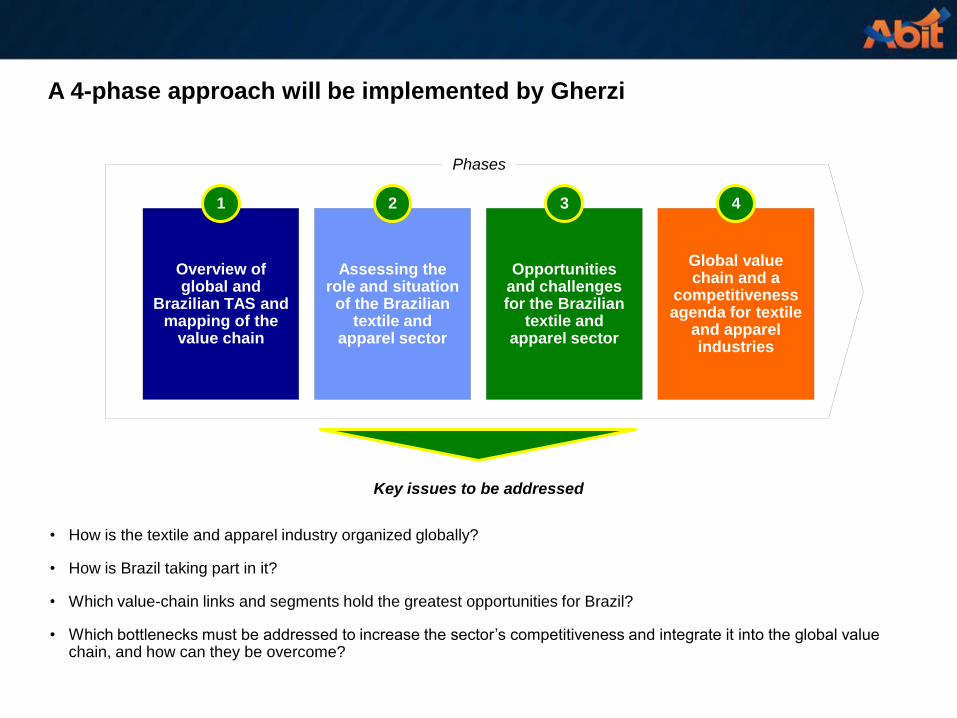

A 4-phase approach will be implemented by Gherzi

Overview of global and

Brazilian TAS and mapping of the

value chain

Assessing the role and situation

of the Brazilian textile and

apparel sector

Opportunities and challenges for the Brazilian

textile and apparel sector

Global value chain and a

competitiveness agenda for textile

and apparel industries

4 3 2 1

Key issues to be addressed

Phases

• How is the textile and apparel industry organized globally?

• How is Brazil taking part in it?

• Which value-chain links and segments hold the greatest opportunities for Brazil?

• Which bottlenecks must be addressed to increase the sector’s competitiveness and integrate it into the global value chain, and how can they be overcome?

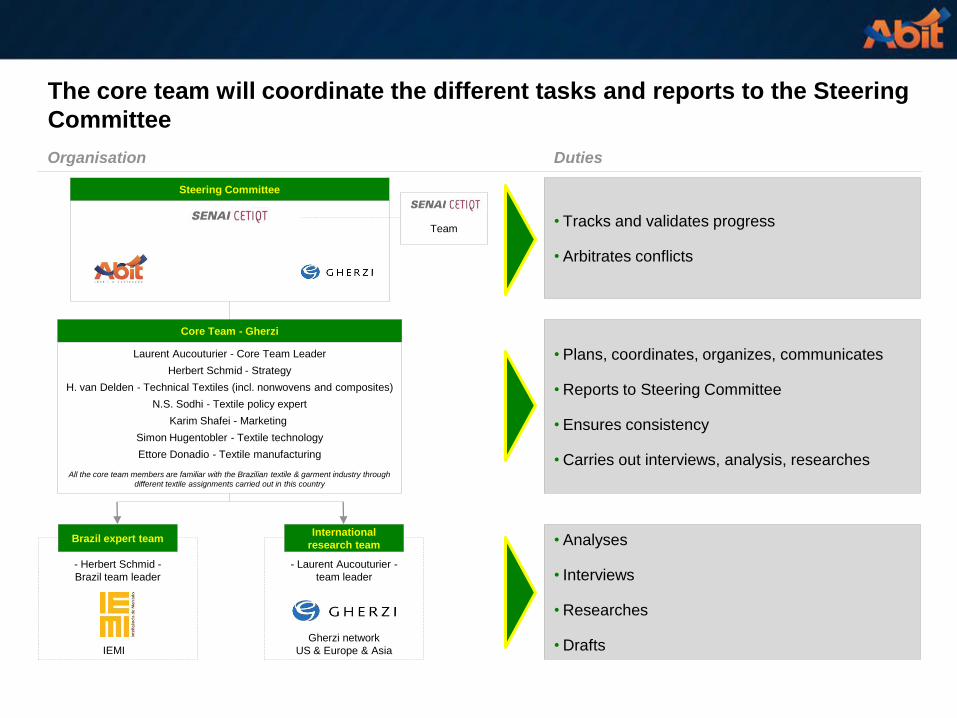

The core team will coordinate the different tasks and reports to the Steering

Committee

Brazil expert team

- Herbert Schmid -

Brazil team leader

IEMI

- Laurent Aucouturier -

team leader

Gherzi network

US & Europe & Asia

International

research team

Core Team - Gherzi

Laurent Aucouturier - Core Team Leader

Herbert Schmid - Strategy

H. van Delden - Technical Textiles (incl. nonwovens and composites)

N.S. Sodhi - Textile policy expert

Karim Shafei - Marketing

Simon Hugentobler - Textile technology

Ettore Donadio - Textile manufacturing

All the core team members are familiar with the Brazilian textile & garment industry through

different textile assignments carried out in this country

Steering Committee

Team • Tracks and validates progress

• Arbitrates conflicts

• Analyses

• Interviews

• Researches

• Drafts

• Plans, coordinates, organizes, communicates

• Reports to Steering Committee

• Ensures consistency

• Carries out interviews, analysis, researches

Organisation Duties

The mission will last 7 months starting in October 2016

1.1

1.2

1.3

2.1

2.2

2.3

2.4

2.5

2.6

2.7

3.1

3.2

3.3

3.4

3.5

3.6

3.7

4.1

4.2

1

2

3

4

Overview of global and Brazilian TAS and mapping of

the value chain

Assessing the role and influence of the Brazilian textile

and apparel sector

Opportunities and challenges for the Brazilian textile and

apparel sector

Global value chain and a competitiveness agenda for textile and apparel industries

October November December January February March April

2016 2017

R0

R0

R0

KO

KO

KO

CC1

CC1

CC1

R1

R1

R1

CC2

CC2

CC2

CC2

CC2

M1

M1

M1

M1

M1

M1

M1

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

CC3

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

R2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

M2

CC4

CC4

CC4

CC4

CC4

CC4

CC4

CC4

CC4

FR

FR

FR

FR

FR

FR

FR

FR

FR

M3

M3

M3

M3

M3

M3

M3

M3

M3

40 41 42 43 44 45 46 47 48 49 50 51 52 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

R0 : Research Executive Project

R1 : Report #1

R2 : Report #2

FR : Report #3 (Final report)

CC1 : Conference Call #1

CC2 : Conference Call #2

CC3 : Conference Call #3

CC4 : Conference Call #4

KO : Kick-off Meeting

M1 : Meeting #1

M2 : Meeting #2

M3 : Meeting #3

Report Conference

Call

Meeting in

Brazil

19.10.2016

11.01.2017

22.02.2017

26.04.2017

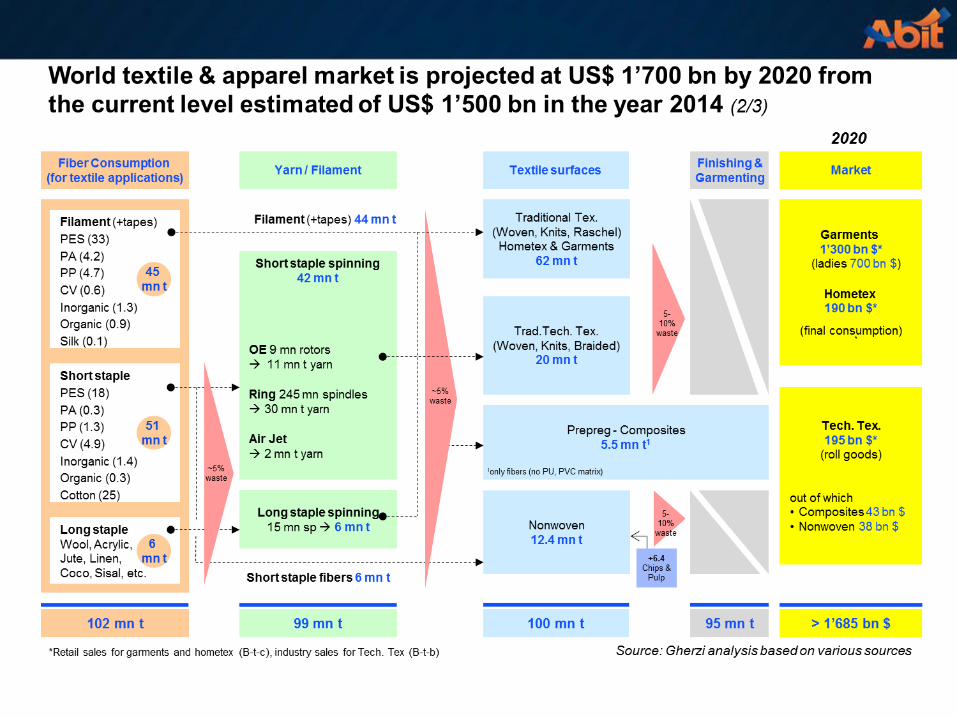

Gherzi has reviewed three main topics in order to assess the World and Brazil TAS

Product

overview

Technology World trade

Production

capacities Key success

factors

Raw

materials

World TAS

Business

models

End of life

Consumption

Retail Production

Design

Resources Systems thinking

Overview of the World TAS Overview of the TAS in Brazil Mapping the global value chain for the TAS

Raw materials, investments and

international trade are going through

structural changes

Despite economic upheaval, the Brazilian

TAS remains robust but needs to address

its weaknesses

The World TAS and Brazil will be impacted

by 33 trends segmented in 7

categories

Overview of the World TAS

01

02

03

04

05

06

07

Focus on 12 products in

apparel and home

textiles

Product overview

Promising developments

in all process steps

Technology Growth and heavyweights

World trade

Asian domination for

textile machine

investments

Production capacities Key success factors

Raw materials

World TAS

Business models

Strengthening of MMF at the

expense of natural fibers

11 KSF for the TAS

4 major business models

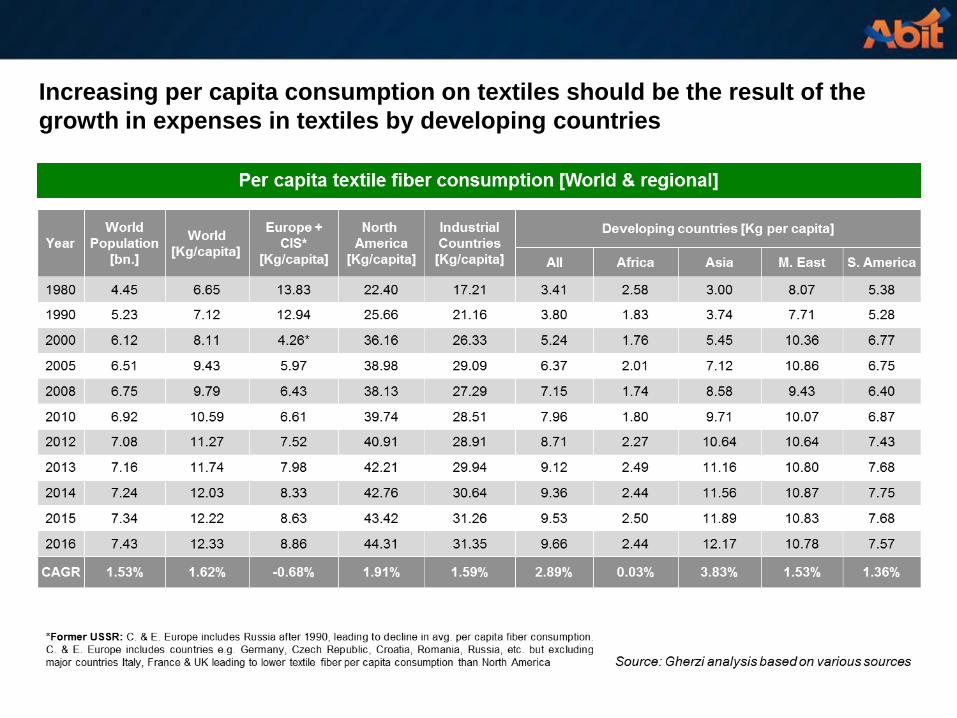

Increasing per capita consumption on textiles should be the result of the

growth in expenses in textiles by developing countries

Global retail market for apparel is forecast to grow by 2.5% annually till

2020 wherein India will be the fastest growing market positioned at 4th

The intra-Asia textile trade is gaining importance due to shifting of

garment industry and increasing sourcing options

Textile worldwide trade in 2014 (bn US$ and percent change 2013-2014 / 2004-2005)

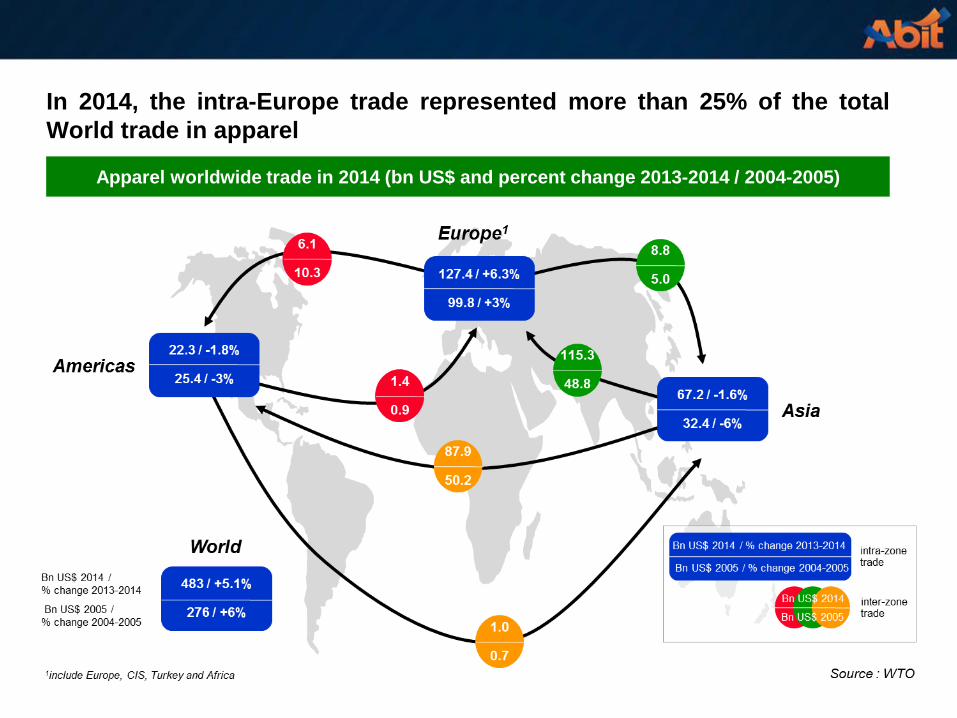

In 2014, the intra-Europe trade represented more than 25% of the total

World trade in apparel

Apparel worldwide trade in 2014 (bn US$ and percent change 2013-2014 / 2004-2005)

Future sourcing: Industry shifting from China to other cost competitive countries

Number of apparel factories in 2014

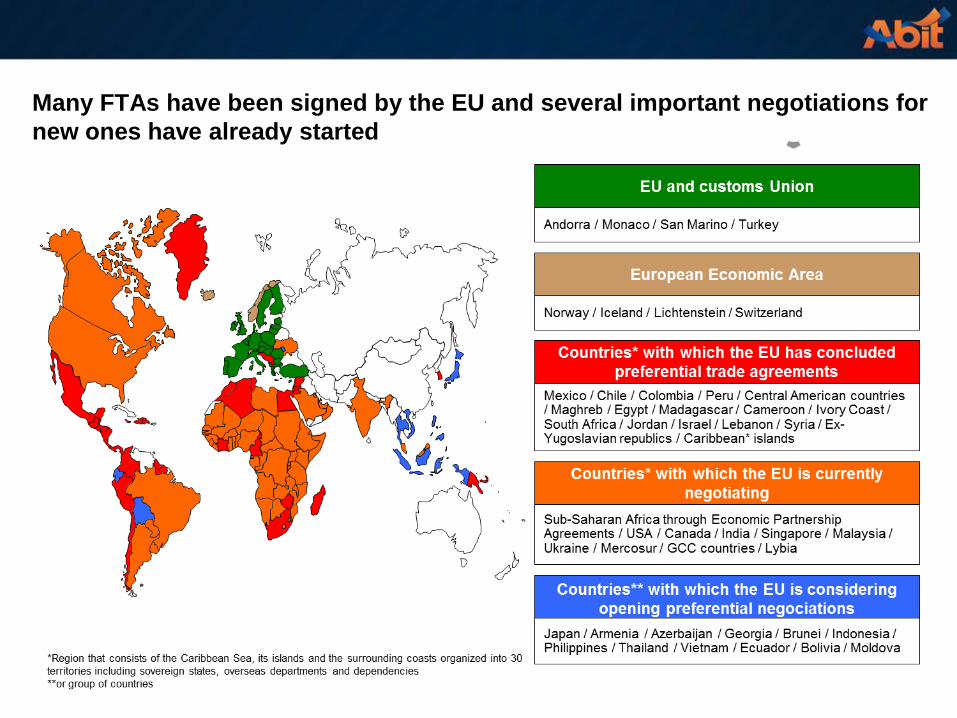

Many FTAs have been signed by the EU and several important negotiations for

new ones have already started

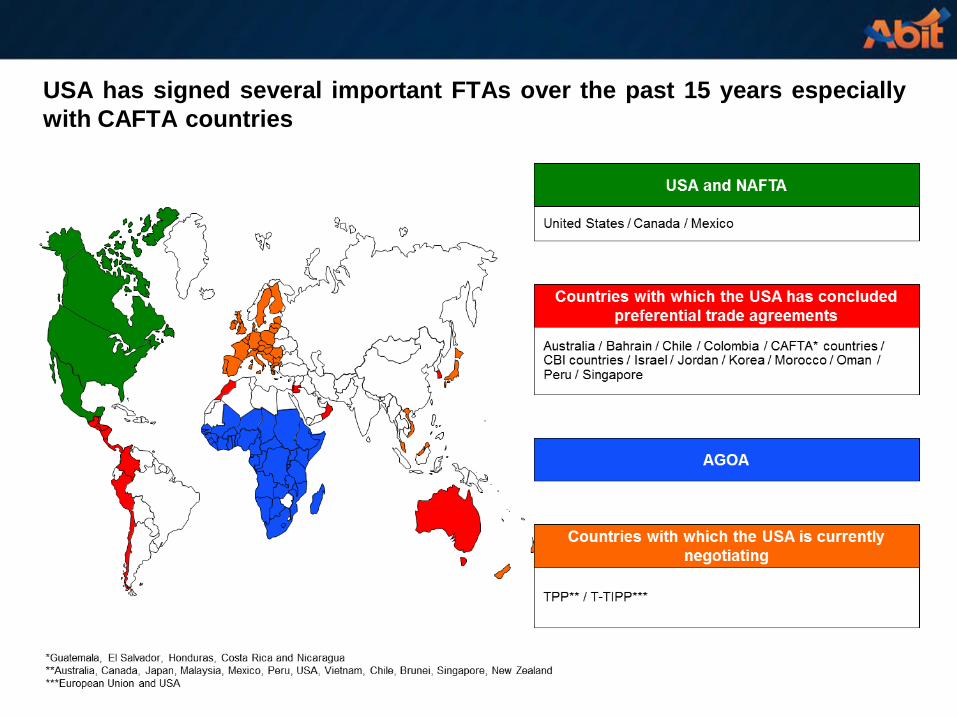

USA has signed several important FTAs over the past 15 years especially

with CAFTA countries

Vietnam is the highest ranked country for supplying garments to brands followed by Cambodia

China

Vietnam

Cambodia

Thailand

Indonesia

India

Sri Lanka

Bangladesh

Pakistan

Myanmar

[…Our sourcing priorities are determined by ranking along 6

criteria per country (like a traffic light system)…]

[…Raising costs in China are forcing us to evaluate sourcing

alternatives…]

[…At the moment Vietnam looks promising…]

Source: Adidas Good Medium Weak

21 trends to carefully monitor

33 trends and impacts

The importance of the different Key Success Factors (KSF) varies in

dependence of the process step within the TAS

23 sub-segments of the Brazil TAS have been analyzed in order to identify their respective export readiness and potential

Brazil suffers from a lack of competitiveness analyzed by a recent CNI study

Source: CNI

The regulatory framework has been assessed to determine the positive and negative impacts on the Brazil TAS and the future priorities for changes

Next Steps......

DONE

UNDER REVIEW

NEXT STEPS

THANK YOU!