Budapest, 28 November 2002

1

2Budapest, 28 November 2002

Developments in euro payment systemsChallenges for accession countries

Tom Kokkola,

Senior Policy Expert

European Central Bank

Budapest, 28 November 2002

Budapest, 28 November 2002

3

Introduction: The role of the ECB/Eurosystem

• Article 3.1 (Basic tasks of the ESCB):– definition and implementation of monetary policy

– conduct of foreign exchange operations

– holding and management of official foreign reserves of the Member States

– promotion of smooth operation of payment systems

• Article 22 (Clearing and payment systems):

“The ECB and national central banks may provide facilities, and the

ECB may make regulations, to ensure efficient and sound clearing and

payment systems within the Community and with other countries.”

Budapest, 28 November 2002

4

The role of the ECB/Eurosystem

• Maintaining systemic stability

• Ensuring efficiency of payment systems

• Maintaining public confidence in payment systems, instruments and currency

• Protecting the transmission channel for monetary policy

The objectives

Budapest, 28 November 2002

5

Introduction

Different roles to perform the same task of “promoting the smooth operation of payment systems” • Operational role

– for example, TARGET and provision of settlement facilities

• Catalyst role– for example, cross-border retail payment services

• Regulation

• Oversight

The Eurosystem’s role in payment systems

Budapest, 28 November 2002

6

Introduction

Contents:

1. Implications of the move to a common currency

2. Large-value payment systems, including future developments in TARGET

3. Retail payments issues

4. Securities settlement and collateral

5. The utmost importance of co-operation

Budapest, 28 November 2002

7

1. Implications of the move to a common currency

- Several currencies One single currency

- Autonomous national monetary policies

- Segmented money markets

- NCBs + European Monetary Institute

- National payment systems

One monetary policy

One money market

Eurosystem

An integrated payment system

Before Monetary Union (-> 1998) In Monetary Union (1999 ->)

-

-

-

-

-

The needs of the single currency

Budapest, 28 November 2002

8

• New borders: geographical borders no longer matter, but those of the single currency.

• Part of what was foreign activities becomes domestic (= euro area).

• Single European passport.

• Remote access.

• Strong foreign participation.

1. Implications of the move to a common currency

Budapest, 28 November 2002

9

1. Implications of the move to a common currency

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%B

ulga

ria

Cy

pru

s

Cze

ch

Rep

ublic

Est

onia

Hu

ngar

y

Latv

ia

Lith

uani

a

Mal

ta

Pol

and

Rom

ania

Slo

vak

ia

Slo

veni

a

Euro Area

Foreign ownership (expressed as a % of total bank assets, end 2001)

Budapest, 28 November 2002

10

2. Implications of the move to a common currency

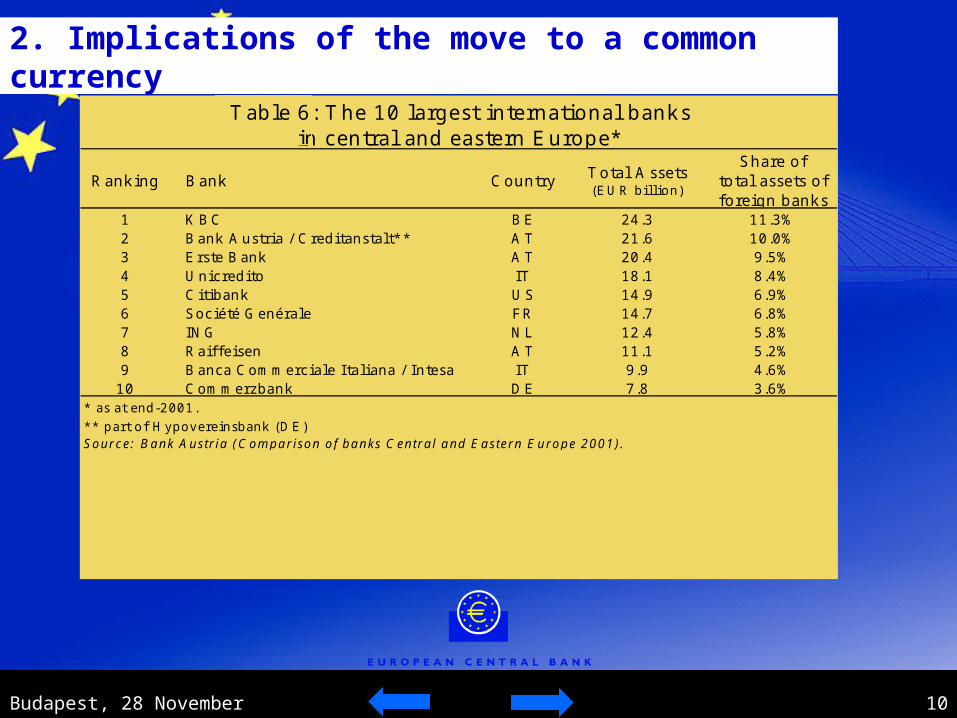

R a n k in g B a n k C o u n try T o ta l A s s e ts( E U R b i l l io n )

S h a re o f to ta l a s s e ts o f fo re ig n b a n k s

1 K B C B E 2 4 .3 1 1 .3 %2 B a n k A u s t r ia / C r e d i ta n s ta l t* * A T 2 1 .6 1 0 .0 %3 E r s te B a n k A T 2 0 .4 9 .5 %4 U n ic r e d i to IT 1 8 .1 8 .4 %5 C i t ib a n k U S 1 4 .9 6 .9 %6 S o c ié té G e n é r a le F R 1 4 .7 6 .8 %7 IN G N L 1 2 .4 5 .8 %8 R a if f e i s e n A T 1 1 .1 5 .2 %9 B a n c a C o m m e r c ia le I ta l ia n a / In te s a IT 9 .9 4 .6 %

1 0 C o m m e r z b a n k D E 7 .8 3 .6 %* a s a t e n d -2 0 0 1 .

* * p a r t o f H y p o v e r e in s b a n k ( D E )S o u r c e : B a n k A u s tr ia (C o m p a r is o n o f b a n k s C e n tr a l a n d E a s te r n E u r o p e 2 0 0 1 ) .

T a b le 6 : T h e 1 0 la rg e s t in te rn a t io n a l b a n k s in c e n tr a l a n d e a s te rn E u ro p e *

11Budapest, 28 November 2002

2. Large-value payment systems, including future developments in TARGET

Budapest, 28 November 2002

12

Trans-European

Automated

Real-time

Gross-settlement

Express

Transfer

2. Large-value payment systems

Budapest, 28 November 2002

13

2. Large-value payment systems

Objectives

• To contribute to the smooth conduct of monetary policy and the singleness of the money market

• To improve the soundness of payment systems (risk reduction)

• To increase the efficiency of cross-border payments in euro

Budapest, 28 November 2002

14

2. Large-value payment systems

Guiding principles

• Market principle

• Decentralisation principle

• Minimum approach with regard to harmonisation of national RTGS systems

Budapest, 28 November 2002

15

2. Large-value payment systems

Market principle

• Use of TARGET not mandatory

• Only payments directly connected with central bank operations (in which the Eurosystem involved either on the receiving or the sending side) and settlement of large-value net settlement systems have to go through TARGET

• Other payment arrangements (Euro 1, PNS, correspondent banking) can operate in parallel to TARGET

Budapest, 28 November 2002

16

2. Large-value payment systems

Decentralisation principle

• Use of RTGS infrastructures in EU countries

• Banks settlement accounts at NCBs

• Direct exchange of payments between NCBs

• Some centralised functions undertaken by ECB (TARGET co-ordinator, end-of-day functions, helpdesk, test centre, settlement accounts for Euro 1 and CLS)

Budapest, 28 November 2002

17

2. Large-value payment systems

The decentralised structure

“The central bank correspondent banking model”

NCB

ECB

Bank

NCB NCB

NCB

NCB

Bank

Bank

Bank

Bank

Bank

InterlinkingInterlinking

Budapest, 28 November 2002

18

2. Large-value payment systems

Minimum approach

• Not entirely identical services offered by the different national RTGS systems

• Rationale: minimising time and cost for the establishment of TARGET

• Harmonisation only if necessary to ensure

- singleness of monetary policy or

- level playing field for banks

Budapest, 28 November 2002

19

2. Large-value payment systems

National RTGS National RTGSInterlinking systemTARGET

Cre

dit

inst

itu

tion

s

Cred

it institu

tions

100NCB (S)

100

R

DOMESTIC MESSAGE FORMAT

INTERLINKING MESSAGEFORMAT

DOMESTIC MESSAGE FORMAT

1

2

3

100

NCB (R)

100

S

Que

uing

+ c

ash

man

agem

ent f

acil

itie

s

Communication

NETWORK

Budapest, 28 November 2002

20

2. Large-value payment systems

Operating hours and days• Common operating hours, ECB time:

Customer payments from 7.00 am to 17.00Interbank payments from 7.00 am to 18.00

• Operating days calendar: in addition to Saturdays and Sundays TARGET closed on New Year’s Day, Good Friday, Easter Monday, 1 May, Christmas Day and 26 December

• On closing days: no standing facilities, no settlement of euro money market or FX transactions involving the euro, EONIA not published

Budapest, 28 November 2002

21

2. Large-value payment systems

• Capability of processing a high number of payments

• End-to end completion of payment execution within minutes in normal operating conditions

• No liquidity shortages• TARGET is de facto standard for large-value

payments in euro• Three objectives have been met

Practical experiences

Budapest, 28 November 2002

22

2. Large-value payment systems

• Better meet customers’ needs, inter-alia, by providing an extensive harmonised service level

• Cost-efficiency• Is prepared for swift adaptation to future

developments including the enlargement of the euro area and the Eurosystem

• But leave the responsibility for the business relations with the credit institutions with the NCBs

Challenges

Budapest, 28 November 2002

23

2. Large-value payment systems

1. Market principle

2. Decentralisation principle: business level,but less platforms than central banks

3. Broadly defined core service

4. Single price structure

5. Cost effectiveness

Principles for TARGET2

Budapest, 28 November 2002

24

1. Have an own platform that has to be cost recovery capable at the single price structure and compliant with all agreed TARGET2 features:• outside interface,• common services,• ...

2. Join the single shareable platform

2. Large-value payment systems

Budapest, 28 November 2002

25

2. Large-value payment systems

85.0%

68.5%

68.8% 68.8%69.4%

69.6% 69.6%70.3% 70.2%

72.0%

73.2%73.5%

81.1%

84.8%

66%

69%

72%

75%

78%

81%

84%

87%

1Q' 99 2Q' 99 3Q' 99 4Q' 99 1Q' 00 2Q' 00 3Q' 00 4Q' 00 1Q' 01 2Q' 01 3Q' 01 4Q' 01 1Q' 02 2Q' 02

TARGET market share in value (cross-border + domestic)

Budapest, 28 November 2002

26

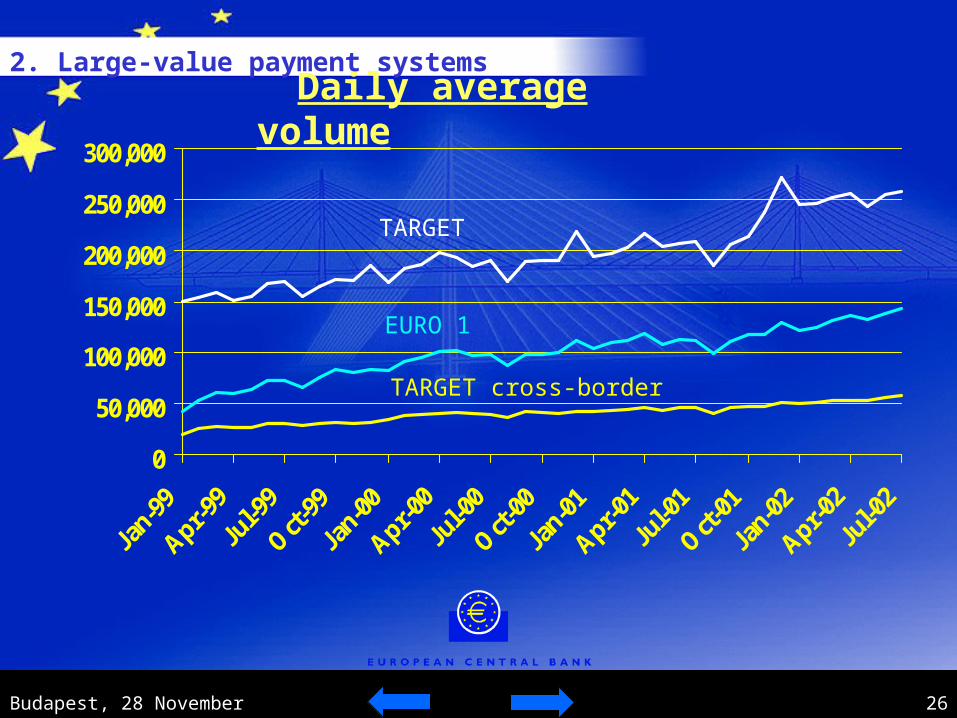

Daily average volume

0

50,000

100,000

150,000

200,000

250,000

300,000

EURO 1

TARGET

TARGET cross-border

2. Large-value payment systems

Budapest, 28 November 2002

27

Daily average value

•

0200400600800

1,0001,2001,4001,6001,800

Jan-9

9

Apr-99

Jul-9

9

Oct-

99

Jan-0

0

Apr-00

Jul-0

0

Oct-

00

Jan-0

1

Apr-01

Jul-0

1

Oct-

01

Jan-0

2

Apr-02

Jul-0

2

EU

R b

illi

ons

TARGET

TARGET cross-border

EURO 1

2. Large-value payment systems

Budapest, 28 November 2002

28

Average size of transactions

02468

101214161820

Jan-9

9

Apr-99

Jul-9

9

Oct-

99

Jan-0

0

Apr-00

Jul-0

0

Oct-

00

Jan-0

1

Apr-01

Jul-0

1

Oct-

01

Jan-0

2

Apr-02

Jul-0

2

EU

R m

illi

ons

TARGET cross-border

TARGET

EURO 1

2. Large-value payment systems

Budapest, 28 November 2002

29

2. Large-value payment systems

TARGET EURO 1 PNS SPI POPS

Participants 3830 73 24 37 9

Daily Øvolume

248,541 132,408 28,103 7,096 2,546

Daily Øvalue (bn

EUR)

1,533 190 78 1 1

Ø size oftransactions(mn EUR)

6.20 1.43 2.78 0.14 0.39

Figures as of May 2002

Budapest, 28 November 2002

30

EURO1 - Institutional set-up=> EURO 1 is a real cross-border system:• The EBA Clearing Company S.A., which is in

charge of the daily management and operation of EURO 1, is located in Paris,

• the legal basis and the clearing rules of EURO 1 are under German law,

• the netting centre (SWIFT) is incorporated in Belgium and

• the participants come from 20 different countries.

2. Large-value payment systems

Budapest, 28 November 2002

31

EURO1 - Type of system

• EURO 1 is a net system, but not a netting system:

• “Netting” is a legal concept• “Net system” is an economic concept

2. Large-value payment systems

Budapest, 28 November 2002

32

EURO1 - Legal structure

• SOS (Single Obligation Structure)

=> Economically the SOS is equal to multilateral netting, but legally it is different!

=> The SOS foresees that a participant has always only one single claim or obligation towards the system (i.e. the community of other participants), payment orders become part of the single claim/obligation upon processing; no bilateral obligations exist at any time.

=> Due to the SOS an unwinding is not possible.

2. Large-value payment systems

Budapest, 28 November 2002

33

EBA Clearing System: Euro 1Features:1. Single obligation structure (SOS)

2. Bilateral credit lines (min EUR 5 million; max EUR 30 million) multilateral credit and debit limits (max. EUR 1 billion)

3. Cash liquidity pool

4. If failure > liquidity pool, surviving banks provide additional liquidity

5. Settlement at the ECB via TARGET at the end of business day

6. Role of the ECB: Settlement agent, holder of the liquidity pool and overseer

2. Large-value payment systems

Budapest, 28 November 2002

34

EURO1 - Types of transactions

• EURO 1 processes credit transfers (customer and interbank payments)

• At present: Division between interbank and customer payments: 35% interbank payments and 65% customer payments

• Processing of direct debits planned

2. Large-value payment systems

Budapest, 28 November 2002

35

EURO1 - Access criteria• Own funds of at least EUR 1.25 billion• Short-term credit rating of at least

P2 (Moody’s) or A2 (Standard & Poor)• Direct access to an EU RTGS system connected to

TARGET• Adequate technical and operational facilities

• =>Since 17 September 2001: 73 participants from all 15 EU countries and from Australia, Japan, Norway, Switzerland, USA (EU branches of the latter five countries)

2. Large-value payment systems

Budapest, 28 November 2002

36

Continuous Linked SettlementCLS is a project for establishing a multi-currency system for the

settlement of foreign exchange transactions on a PVP basis in the books of a private bank acting as settlement agent where all members will open multi-currency accounts.

Start of operations: September 2002

Eligible currencies from the start:euro, pound sterling, US dollar, Swiss franc, Canadian dollar, Japanese yen and Australian dollar.

Later on also: Norwegian krone, Hong Kong dollar, Danish krone, Swedish krona and New Zealand dollar.

2. Large-value payment systems

Budapest, 28 November 2002

37

You deliver the currency being sold

butbut

you do not receive the currency you bought

the full amount of each trade is at risk

= principal risk= principal risk

What is FX settlement risk ?

2. Large-value payment systems

Budapest, 28 November 2002

38

Settlement of one leg occurs if, if,

and only if,and only if,

the other leg settles

If you pay,

you will eithereither get paid

oror get a refund

No risk of losing principal amount of fx transactions

PvP mechanism

2. Large-value payment systems

Budapest, 28 November 2002

39

C LS Bank In te rnational(N ew York)

- Edge C orporation under U S law- chartered by Fed in 1999

C LS Services L td.(London)

- lim ited com pany under U K law- operational and back office support

C LS U K H old ings L td.(London)

C LS G roup H o ld ings AG(Zurich)

Shareho lders o f C LS:67 financia l institu tions (22 euro area)

loca ted in 17 countries

General Overview of CLSCorporate structure:

2. Large-value payment systems

Budapest, 28 November 2002

40

USD

EUR

JPY

GBP

CHF

CAD

AUS

CLSBank

Bank ofJapan

Bank of England

SwissNational Bank

Bank of Canada

Reserve Bankof Australia

NY Fed

ECB

Fedwire

TARGET

FEYCS/BoJ

NewChaps

SIC

LVTS

RITS

The CLS Bank... ...has settlement accounts with

…to receive andpay fundsthrough

2. Large-value payment systems

41Budapest, 28 November 2002

3. Retail payments issues

Budapest, 28 November 2002

42

Trends within the European Union:

Payment instruments

‘93 ‘99

Cheques 29 % 18 %

Card payments 12 % 18 %

Credit transfers 35 % 36 %

Direct debit 22 % 27 %

3. Retail payment issues

Budapest, 28 November 2002

43

Banknotes and coins in circulation outside credit institutions, as a percentage of GDP

1993 2000

European Union 5,6 % About 4 %

Highest (ES) 8.9 %Lowest (FI) 2.2 %

Accession countries Highest (LV) 9.9 %Lowest (SI) 3.0 %

3. Retail payment issues

Budapest, 28 November 2002

44

3. Retail payment issues

Budapest, 28 November 2002

45

The current situation

• Relatively poor service level for cross-border retail payments

– in terms of pricing

– in terms of speed of payment execution

• Low volumes, but not necessarily low demand

3. Retail payment issues

Budapest, 28 November 2002

46

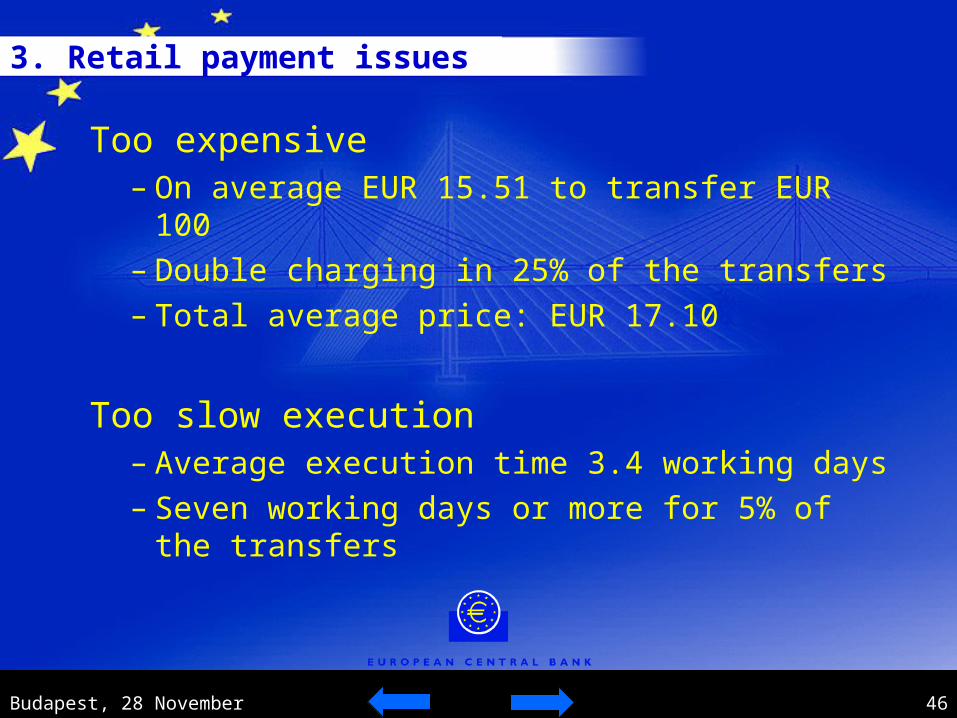

Too expensive– On average EUR 15.51 to transfer EUR 100– Double charging in 25% of the transfers– Total average price: EUR 17.10

Too slow execution– Average execution time 3.4 working days– Seven working days or more for 5% of the

transfers

3. Retail payment issues

Budapest, 28 November 2002

47

Standardisation some attempts...

BE

FR

DE

IT

UK

..have clearly failed...

3. Retail payment issues

Budapest, 28 November 2002

48

Future prospects

What is needed

IPISWIFT MT102+/103+

• Straight-through-processing– consistent routing mechanism --> IBAN/BIC––

• Common default interbank exchange fee

• Reduced balance of payments reportingrequirements

3. Retail payments issues

Budapest, 28 November 2002

49

How to achieve the single payment area?– Integrate national and cross-border activity– Clubs– ACH network– Single ACH– Technology jump a possibility?

3. Retail payments issues

Budapest, 28 November 2002

50

EURO1 - STEP 1

STEP 1:• EBA developed STEP 1 in order to offer cross-border retail

payment services• STEP 1 is operating since November 2000• It uses the technical platform of EURO 1• STEP 1 participants settle their balances via a EURO 1 participant

3. Retail payments issues

Budapest, 28 November 2002

51

3. Retail payments issues

Participants

• 5 rounds since 20th November 2000

• 81 Institutions • from 10 different EU countries

• 23 different Settlement Banks designated

• (to be opened to EEA based banks)

STEP 1:

Budapest, 28 November 2002

52

Regulation (EC) No 2560/2001:• establishes the principle of equal charges for domestic payments

and cross-border payments in euros

• requires banks to inform their customers in advance on the charges they apply for all payment services

• lays down standards to facilitate automation of payment systems (such as the International Bank Account Number and the Bank Identifier Code). Banks must indicate them on account statements and companies on their invoices

• national rules, such as statistical reporting obligations, which make practical distinctions between domestic and cross-border payments will be either eliminated or harmonised

• threshold to be increased from € 12,500 to € 50,000 on 1.1.2006.

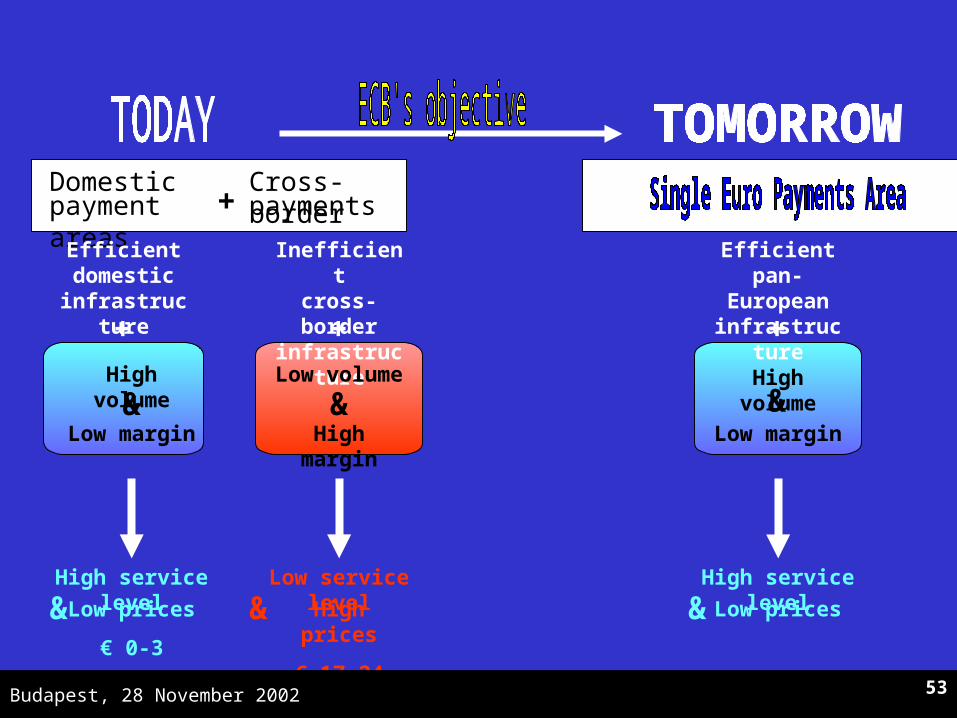

3. Retail payments issues

Domestic payment areas

Cross-border

payments

+

Efficientdomestic

infrastructure

Inefficientcross-border

infrastructure

Efficientpan-Europeaninfrastructure

High volume

Low margin

+

&

High service level

Low prices

€ 0-3

&

High volume

Low margin

+

&

High service level

Low prices&

Low volume

High margin

+

&

Low service level

High prices

€ 17-24

&

5353Budapest, 28 November 2002

Domestic payments

Efficientpan-Europeaninfrastructure

payments

Cross-border

Profit margin

Processingcosts

Profit margin

Processingcosts

Cross-border

Loss

Processingcosts

Pan-European

payments

Profit margin

Processingcosts

payments

•Co-operation bodies

•Business practises

•STP standards

•Clearing&settlement

infrastructure

Transparency &

Competition

Price € 17-24

€ 0.1- 0.4

•“OUR”charging

•“Eurocred”

•MIF (cost based)

Price € 0-3

54Budapest, 28 November 2002

Budapest, 28 November 2002

55

Eurosystem/EPC co-operation

European Payments Council Co-ordination group

European Payments Council General Assembly

European Payments Council Working Groups

- customer requirements

- cash

- cards

- STP

- infrastructure

Budapest, 28 November 2002

56

STEP2 blueprinting: Objectives and principles

offering distribution of payment instructions to any bank

operating in the EU

a pan-European system with direct bank participation

highly automated, simple to use, based on broadly

accepted industry standards

open to progressive integration of domestic traffic

minimising bank internal costs related to processing

customer payments

3. Retail payments issues

Budapest, 28 November 2002

57

3. Retail payments issues

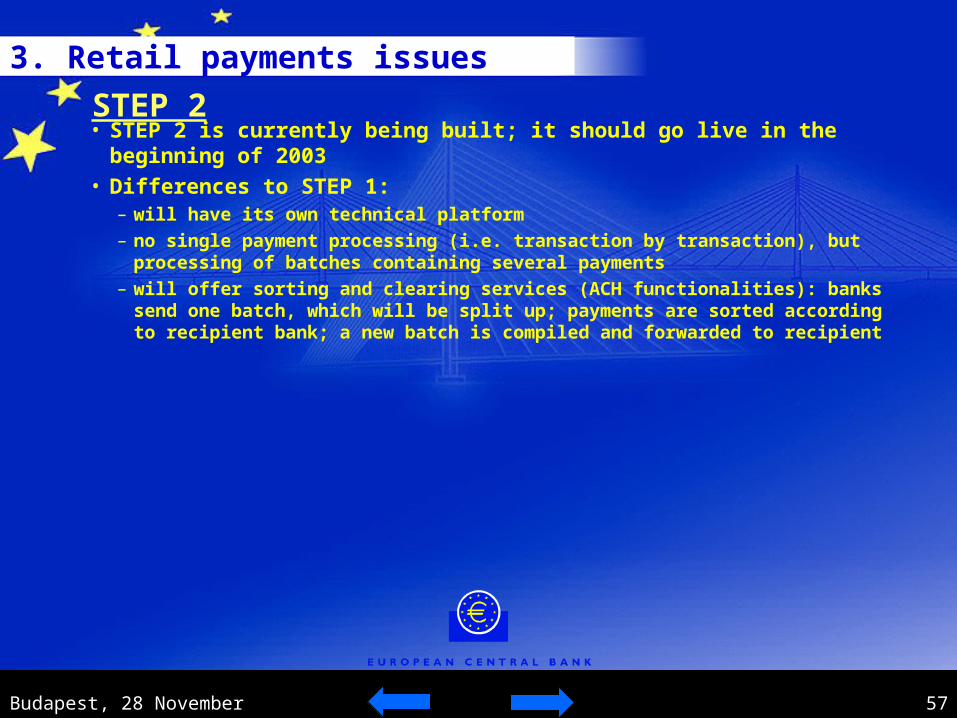

• STEP 2 is currently being built; it should go live in the beginning of 2003• Differences to STEP 1:

– will have its own technical platform– no single payment processing (i.e. transaction by transaction), but processing of

batches containing several payments – will offer sorting and clearing services (ACH functionalities): banks send one

batch, which will be split up; payments are sorted according to recipient bank; a new batch is compiled and forwarded to recipient

STEP 2

Budapest, 28 November 2002

58

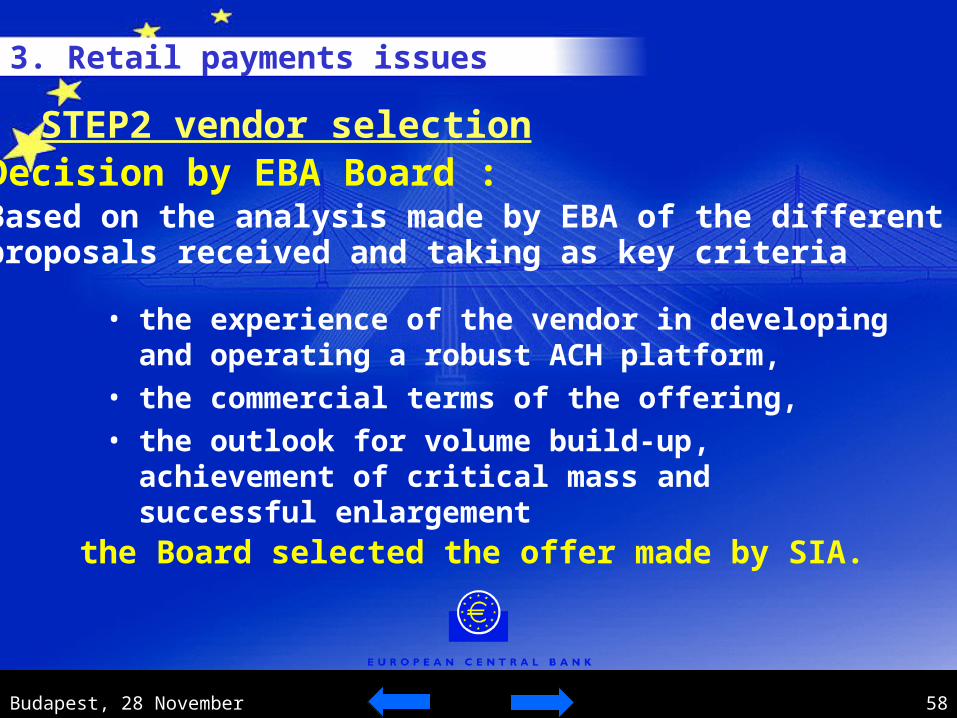

Decision by EBA Board :Based on the analysis made by EBA of the differentproposals received and taking as key criteria

• the experience of the vendor in developing and operating a robust ACH platform,

• the commercial terms of the offering,• the outlook for volume build-up, achievement of

critical mass and successful enlargement

STEP2 vendor selection

the Board selected the offer made by SIA.

3. Retail payments issues

59Budapest, 28 November 2002

4. Securities settlement and collateral

Budapest, 28 November 2002

60

Liquidity in TARGET• Minimum reserves = liquidity available intraday

for payment activity

• Unlimited intraday credit free of interest

– Broad range of assets eligible as collateral for both

payment systems and monetary policy

operations

– Easy substitution of collateral

– Cross-border use of collateral

• 100% collateralisation of any credit

4. Securities settlement and collateral

Budapest, 28 November 2002

61

4. Securities settlement and collateral

TARGET and Securities Settlement Systems

• All ESCB lending operations (intraday andovernight) have to be fully collateralised

• “Standards for the use of EU SSSs inESCB credit operations”

• Overall objectives:– avoidance of inappropriate risks

– same safety level for all central banks’operations, regardless of settlement method

Budapest, 28 November 2002

62

4. Securities settlement and collateral

Risk aspects:minimum standards for SSSs

• Content of the standards • Scope of the standards

- domestic SSSs

- international SSSs

- links between SSSs

Eligible in Eurosystem operations:

- 20 SSSs (17 + 3)- 66 Links

- settlement risk- custodian risk- legal aspects- operational aspects

Budapest, 28 November 2002

63

Consolidation

Monte Titoli (IT)

Horizontal consolidation of SSSs at a domestic level

Monte Titoli

CAT

LDT

Iberclear (ES)CADE

SCLV

4. Securities settlement and collateral

Budapest, 28 November 2002

64

4. Securities settlement and collateral

CIK (BE)

Euroclear (ICSD)

Sicovam (FR)

Necigef (NL)

CBISSO (IE)

Euroclear

ClearstreamDBC (DE)

CEDEL (ICSD)

Crest (UK)

Horizontal consolidation of SSSs at a European level

Interbolsa (PT) ?

Budapest, 28 November 2002

65

SBF (FR)

BXS (BE)

AEX (NL)

Clearnet

BCC (FR)

Consolidation of CCPs for securities at a European level

4. Securities settlement and collateral

Budapest, 28 November 2002

66

4. Securities settlement and collateral

Trade Execution

CentralCounter -party

Settlement

DBAG

CLEARSTREAM

Eurex Clearing

Vertical consolidation at domestic level:

Stock Exchanges MEFF-AIAF-SENAF

IBERCLEAR

MEFF

Borsa Italiana

MONTE TITOLI

Italian CCP

Budapest, 28 November 2002

67

4. Securities settlement and collateral

Trade Execution

CentralCounter -party

Settlement

EURONEXT

EUROCLEAR

CLEARNET

Vertical consolidation at European level:

Budapest, 28 November 2002

68

1 2000 International, FR, IE2 2000 International, LU, DE3 2000 UK, IE4 2000 ES5 2000 IT6 2000 SE7 2000 UK8 2000 DK9 2000 BE

10 2000 GR… … …25 2001 HU… … …

Year CountryValue of transaction

(EUR billions)Euroclear 130,600Clearstream nav CREST 79,893 CADE 30,455 Monte Titoli 30,210 VPC 8,974

1,081

CMO 3,946 VP 3,028

Name of the system

KELER 84… …

… …

NBB clearing 2,372 BOGS

4. Securities settlement and collateral

69Budapest, 28 November 2002

5. The utmost importance of co-operation

Budapest, 28 November 2002

70

5. The utmost importance of co-operation

Payment and Settlement Systems Committee

Eurosystemcomposition

Extendedcomposition

Securities Settlement Working Group

Payment SystemsPolicy Working Group TARGET Management

Working Group

Among central banks

Budapest, 28 November 2002

71

Eurosystem: TARGET issues

PSSC

TMWG

NCBs

COGEPS (large value)

Ad hoc Meetings

TMWG-TWG

TARGET user groups

Ad hoc groups of

banks

TWG

National banking

communities

5. The utmost importance of co-operation

Budapest, 28 November 2002

72

Eurosystem/EPC co-operation

PSSC

ECB Observer

COGEPS (Retail)

EPC Co-ordination group

EPC General Assembly

EPC Working Groups

- customer requirements

- cash

- cards

- STP

- infrastructure

ECBS

5. The utmost importance of co-operation

Budapest, 28 November 2002

73

Securities Clearing and Settlement Systems (SCSS)

PSSC COGESI

Groups of banks

(custodians and users)

CSDs & ICSDs

5. The utmost importance of co-operation

Budapest, 28 November 2002

74

5. The utmost importance of co-operation

Constructive co-operation between

• central bank, market participants and systems operators

• EU and accession countries

- Banking associations

- Banks and system operators

Budapest, 28 November 2002

75

Summary

• Move to integrated (and consolidated) euro payment and settlement infrastructures

• Transition strategy

• Active co-operation

Budapest, 28 November 2002

76