WORKSHOP ON DIRECT TAXES

Capital Gains – Part IJune 2016

Capital Gains - Part I 1

Concept of Capital gainsBasic principles

• General principle of taxationü Revenue receipts are

taxable unless specifically exempt

ü Capital receipts are not taxable unless specifically covered

• Capital gains – covered within the scope of the term ‘income’ under section 2(24)(vi)

Capital Gains - Part I 2

Concept of Capital gainsArrangement of sections• Section 45 - Charging section

• Section 46 – Capital gains on distribution of assets by companies in liquidation

• Section 46A - Capital gains on buyback of shares

• Section 47 – Transactions not regarded as transfer (exceptions)

• Section 47A - Withdrawal of exemption in certain cases

• Section 48 - Mode of computation

• Section 49 - Cost with reference to certain modes of acquisition

• Section 50 - Special provision for computation of capital gains in case of depreciable assets

• Section 50B - Slump Sale

• Section 50C - Defines full value of consideration in certain cases

• Section 51 - Advance money received

• Section 54 to 54GA - Exemptions of capital gains in certain cases

• Section 55 - Cost of Acquisition/ Cost of improvement

Capital Gains - Part I 3

Concept of Capital gainsBasis of charge – Section 45• Profits or gains on transfer of capital assets – 45(1)

• Compensation for damage or destruction of asset from insurer – 45(1A)

• Conversion of capital asset into stock in trade – 45(2)

• Transfer of beneficial interest in securities by depositories taxable in the hands of registered owner – section 45(2A)

• Contribution of asset to a partnership firm/ AOP/ BOI as capital – 45(3)

• Distribution of capital assets to partners on dissolution of firm – 45(4)

• Compensation received for compulsory acquisition of capital asset – 45(5)

• Difference between repurchase price and capital value of units of Mutual Funds under Equity Linked Savings Scheme – 45(6)

Capital Gains - Part I 4

Concept of Capital gainsBasis of charge – Section 45(1)

Any profits and gains arising from the transfer of a capital asset effected in the previous year, shall save as otherwise provided in sections 54, 54B, 54D, 54EC, 54ED, 54F, 54G or 54GA be chargeable to income-tax under the head ‘Capital Gains’ and shall be deemed to be the income of the previous year in which the transfer took place

Components to constitute ‘Capital gains’• Gains• Transfer• Capital asset• Availability of exemptions

Capital Gains - Part I 5

Concept of Capital gainsBasis of charge – Definitions

Section 2(14) Capital asset

Section 2(29A) Long term capital asset

Section 2(42A) Short term capital asset

Section 2(47) Transfer in relation to a capital asset

Section 47 Transactions not regarded as transfer – exceptions to section 2(47)

Capital Gains - Part I 6

Concept of Capital gainsBasis of charge – Definition of capital asset• Property* of any kind held by an assessee (whether or not connected

with his business or profession)• Securities held by Foreign Institutional Investors (‘FII’)

EXCLUSIONS• Stock-in-trade (other than those held by FIIs), raw materials,

consumable stores held for the purpose of business or profession• Personal effects excluding jewellery, archaeological collections,

drawings, paintings, sculpture, or any works of art• Agricultural land situated in India (not within municipality or

cantonment board or within the specified distance)• Gold bonds• Special bearer bonds• Gold deposit bonds

* Property includes rights in relation to Indian company including rights of management and control or any other rights

Capital Gains - Part I 7

Concept of Capital gainsBasis of charge – Concept of indirect transfer

Capital Gains - Part I 8

Concept of Capital gainsBasis of charge – Short term v. long term

* Including unit of UTI/ equity oriented fund, zero coupon bond

Capital Gains - Part I 9

Concept of Capital gainsBasis of charge – Long term v. Short termInclusions• Period of holding by previous owner• Period of holding by amalgamating company/ de-merged

company in the hands of amalgamated/ resulting company• Bonus shares or debenture – date of allotment of bonus share –

NOT the date of allotment of original share or debenture• Rights shares – date of allotment of shares – NOT date of

allotment of rights

Exclusions• Period subsequent to the date on which the company goes into

liquidation

Capital Gains - Part I 10

• Sale, exchange or relinquishment of the asset• Extinguishment of any rights in the asset• Compulsory acquisition of asset under any law• Conversion of the asset into stock-in-trade• Maturity or redemption of a zero coupon bond• Any transaction involving the allowing of the possession of any

immovable property to be taken or retained in part performance of a contract – referred to in section 53A of Transfer of Property Act, 1882

• Any transaction which has the effect of transferring or enabling the enjoyment of any immovable property

Concept of Capital gainsBasis of charge – Definition of transfer

Transfer shall be deemed to include disposing off or parting with any asset irrespective of whether it has taken place on account of transfer of shares of a foreign company

Capital Gains - Part I 11

Concept of Capital gainsComputation mechanism - Basics

Step 1 Determine full value of consideration

Step 2 Deduct:i) Expenditure incurred wholly and exclusively in

connection with the transferii) Cost/ Indexed cost of acquisitioniii) Cost/ Indexed cost of improvement

Step 3 Deduct – Exemptions, if any

Step 4 Capital gain/ loss

Capital Gains - Part I 12

Concept of Capital gainsBasis of charge – Section 45(2)

Section 45(2)• Overrides provisions of section 45(1)• Gains arising from transfer by way of conversion by the owner of a

capital asset into stock-in-trade - chargeable to tax as capital gains in the year in which the stock-in-trade is sold or otherwise transferred

• Consideration - Fair market value on the date of conversion

Example [assuming section 45(2) is not in existence]• Cost of acquisition – INR 1,000• Fair market value as on date – INR 1,000,000• The assessee can convert the capital asset into stock trade and

record the same at fair market value as on date• Net gain on transfer as per Profit & Loss account would be Nil

Capital Gains - Part I 13

Concept of Capital gainsBasis of charge – Section 45(3) and (4)

Section 45(3)• Profits or gains arising from transfer of capital asset• By way of contribution to the firm by way of capital or otherwise• Consideration – Value recorded in the books• Cost of acquisition in the hands of the firm – amount recorded in the

books

Section 45(4)• Profits or gains arising on distribution of assets by a firm on

dissolution• Consideration – Fair value of the asset as on the date of distribution• Whether dissolution includes retirement? – both views are possible

depending on the facts - prone to litigation

Capital Gains - Part I 14

Concept of Capital gainsBasis of charge – Section 45(5)

Section 45(5)• Overrides section 45(1)• Transfer of capital asset by way of compulsory acquisition or where

consideration is determined by Central Govt• Consideration/ Additional consideration - taxable in the year of

receipt

Capital Gains - Part I 15

Concept of Capital gainsExemptions – section 47

• Distribution of capital assets on the total or partial partition of a HUF

• Transfer of a capital asset under a gift, will or an irrevocable trust (excluding ESOPs)

• Transfer of a capital asset by a holding company to its wholly-owned Indian subsidiary and vice versa (subject to certain conditions)

• Transfer of capital assets, shares in a scheme of amalgamation/ demerger if the amalgamated/ resulting company is an Indian company

• Transfer of bonds or GDRs made outside India by a non-resident to another non-resident

Capital Gains - Part I 16

Concept of Capital gainsExemptions – section 47

• Transfer of agricultural land in India before 1 March 1970

• Transfer of capital asset, being any work of art, archaeological, scientific or art collection, etc to Government, University, etc

• Conversion of bonds/ debentures, etc into shares/ debentures

• Transfer of land of a sick industrial company under a scheme prepared and sanctioned by SICA, 1985 subject to certain conditions

• Transfer of any capital/ intangible assets by a firm to the company which succeeds the concern

• Transfer by a sole proprietary concern of any capital/ intangible assets to a company which succeeds the concern

Capital Gains - Part I 17

Concept of Capital gainsExemptions – section 47• Transfer by a recognized stock exchange of any capital asset to the

company in the course of corporatization of the exchange

• Any transfer of a capital/ intangible asset by a private company/ public unlisted company to a LLP or transfer of a share or shares held in the company by a shareholder as a result of conversion of the company into a LLP (subject to conditions)

• Transfer in a scheme for lending of any securities under a stock lending scheme which is subject to the guidelines of SEBI/ RBI

• Transfer of a capital asset in a transaction of reverse mortgage under a scheme made and notified by the Central Government

• Transfer of shares of SPV to a trust under scheme of REIT

• Transfer of units of mutual fund under consolidation

Capital Gains - Part I 18

Computation of Capital gainsMode of computation - Section 48

Step 1 Determine full value of consideration

Step 2 Deduct:i) Expenditure incurred wholly and exclusively in

connection with the transferii) Cost/ Indexed cost of acquisitioniii) Cost/ Indexed cost of improvement

Step 3 Deduct – Exemptions, if any

Step 4 Capital gain/ loss

Capital Gains - Part I 19

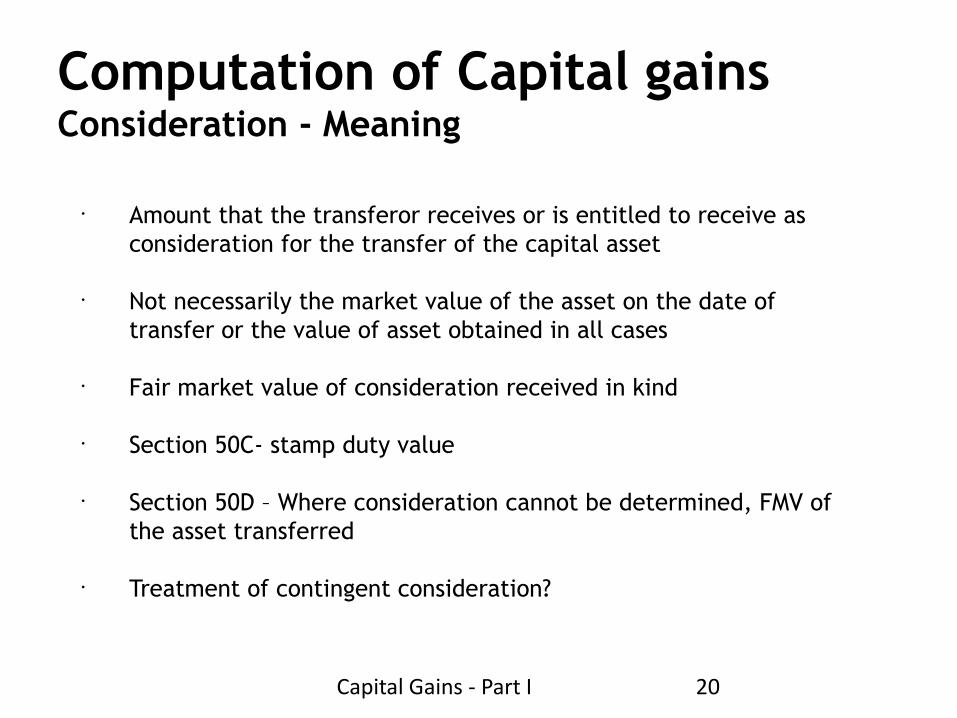

Computation of Capital gainsConsideration - Meaning

• Amount that the transferor receives or is entitled to receive as consideration for the transfer of the capital asset

• Not necessarily the market value of the asset on the date of transfer or the value of asset obtained in all cases

• Fair market value of consideration received in kind

• Section 50C- stamp duty value

• Section 50D – Where consideration cannot be determined, FMV of the asset transferred

• Treatment of contingent consideration?

Capital Gains - Part I 20

S.No. Mode of transfer Deemed full value of consideration Section

1 Asset received from insurer on account of damage or destruction of capital asset

FMV on the date of receipt 45(1A)

2 Conversion of capital asset into stock-in-trade

FMV on the date of conversion 45(2)

3 Introduction of capital into Firm/AOP/BOI

Amount recorded in the books of accounts 45(3)

4 Distribution of assets on dissolution of Firm/ AOP/ BOI

FMV on the date of distribution 45(4)

5 Shareholders receiving assets on liquidation of company

Market value on date of distribution (-) deemed dividend under section 2(22)(c)

46(2)

6 Gift, etc of shares or debentures allotted under ESOP

Market value on the date of gift etc Proviso 4 to section 48

7 Transfer of land or building or both

Value adopted by stamp valuation authority if consideration declared by assessee is less

50C

Computation of Capital gainsDeemed consideration

Capital Gains - Part I 21

Computation of Capital gainsTransfer of shares/ debentures by a non-resident

Applicability • Where the transferor is a non-resident;• Capital asset transferred - shares or debentures of an Indian company;• Purchased in foreign currency;• No indexation even if long-term capital gains

Computation• Capital gain shall be computed by converting the cost of acquisition, expenses on transfer

and full value of consideration into the same foreign currency as was initially utilized for purchase of asset

• Reconverting the capital gains in such foreign currency into the Indian currency

Method of Conversion into foreign currency (Rule 115A)• Cost of acquisition (in foreign currency) = (COAQ in INR/ Average SBI TT rate) on date of

acquisition (A)• Expenses on transfer = (Expenditure in INR/ Average TT rate) on date of transfer (B)• Full value of consideration = (Consideration in INR/ Average TT rate) on date of transfer

(C)• Capital Gains in foreign currency = A – B – C• Capital gains in INR = Capital gains in foreign currency x SBI TT buying rate

Capital Gains - Part I 22

Computation of Capital gainsTransfer of capital asset – other cases

Particulars Short term Long term

Consideration

Deduct:i) Expenditure incurred wholly and exclusively in

connection with the transfer *ii) Cost/ Indexed cost of acquisitioniii) Cost/ Indexed cost of improvement

No indexation Indexation benefit

available**

Deduct – Exemptions, if any N A Available

Capital gain/ loss

* No deduction in respect of Securities Transaction Tax** Other than asset in the nature of bond/ debenture other than capital indexed bonds

Indexed cost of acquisition to be computed using Cost Inflation Index

Capital Gains - Part I 23

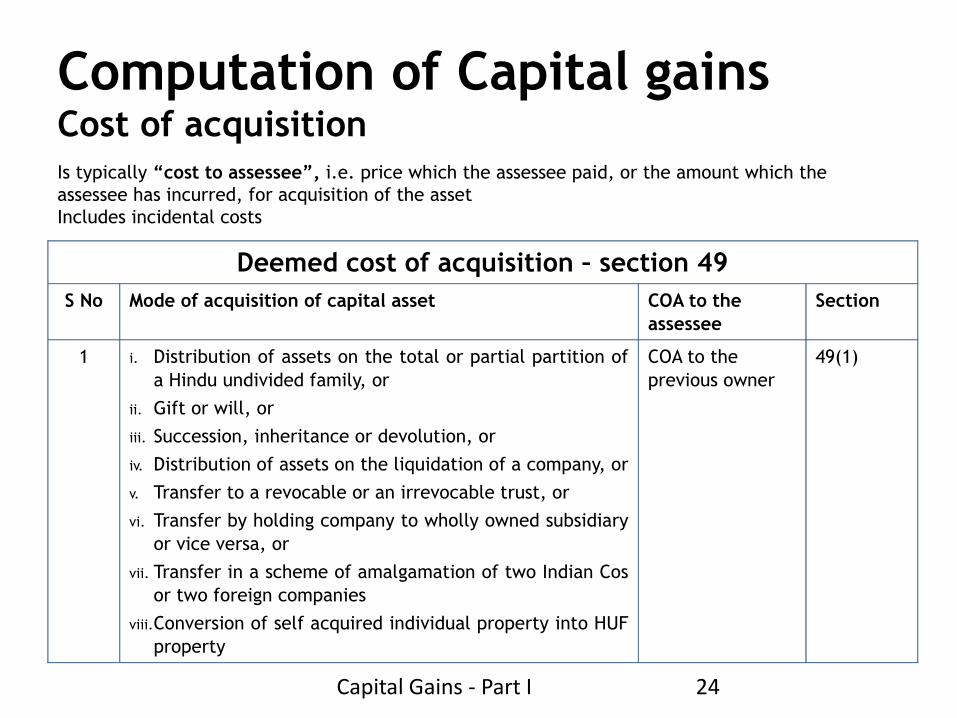

Is typically “cost to assessee”, i.e. price which the assessee paid, or the amount which the assessee has incurred, for acquisition of the assetIncludes incidental costs

Computation of Capital gainsCost of acquisition

Capital Gains - Part I 24

Deemed cost of acquisition – section 49S No Mode of acquisition of capital asset COA to the

assesseeSection

1 i. Distribution of assets on the total or partial partition of a Hindu undivided family, or

ii. Gift or will, or

iii. Succession, inheritance or devolution, or

iv. Distribution of assets on the liquidation of a company, or

v. Transfer to a revocable or an irrevocable trust, or

vi. Transfer by holding company to wholly owned subsidiary or vice versa, or

vii. Transfer in a scheme of amalgamation of two Indian Cos or two foreign companies

viii.Conversion of self acquired individual property into HUF property

COA to the previous owner

49(1)

Capital Gains - Part I 25

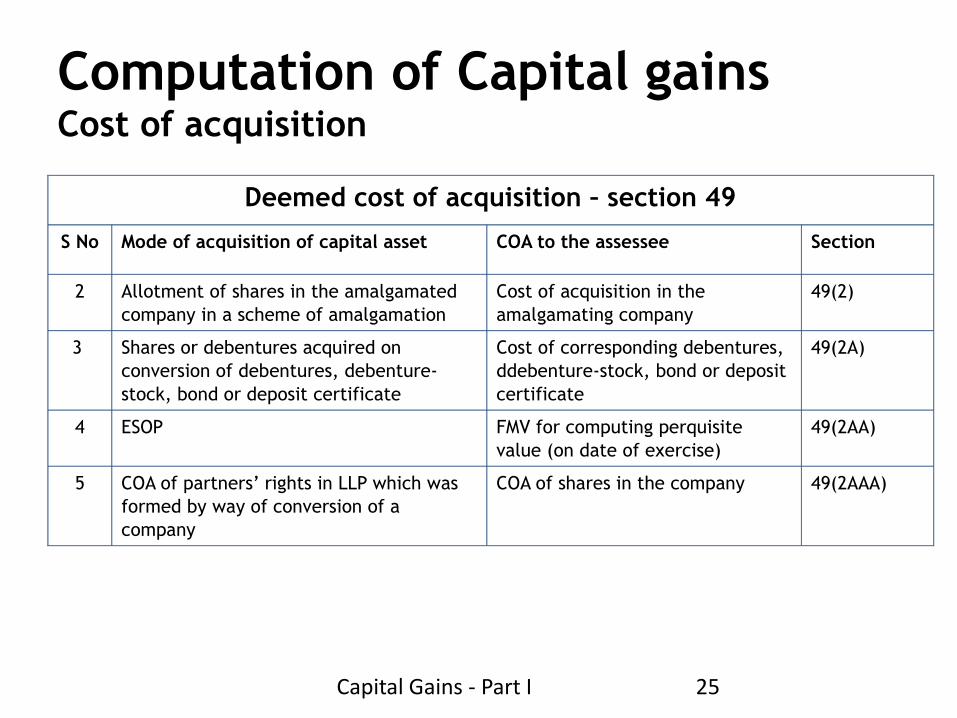

Deemed cost of acquisition – section 49

S No Mode of acquisition of capital asset COA to the assessee Section

2 Allotment of shares in the amalgamated company in a scheme of amalgamation

Cost of acquisition in the amalgamating company

49(2)

3 Shares or debentures acquired on conversion of debentures, debenture-stock, bond or deposit certificate

Cost of corresponding debentures, ddebenture-stock, bond or deposit certificate

49(2A)

4 ESOP FMV for computing perquisite value (on date of exercise)

49(2AA)

5 COA of partners’ rights in LLP which was formed by way of conversion of a company

COA of shares in the company 49(2AAA)

Computation of Capital gainsCost of acquisition

Capital Gains - Part I 26

Computation of Capital gainsCost of acquisition

Deemed cost of acquisition - section 49

S No Mode of acquisition of capital asset COA to the assessee Section

6 COA of shares in the resulting company allotted due to demerger

COA of shares in demerged Co. x Net book value of assets transferred in demerger/ Net worth of demerged company before demerger *

49(2C)

7 COA of original shares of demerged company

Original COA Minus COA of shares in the resulting Company as computed in section 49(2C)

49(2D)

8 Transfer by holding company to its subsidiary company or vice versa AND exemption is withdrawn under section 47A

Cost to the transferee company shall be the cost for which such asset was acquired by it

49(3)

Net worth = Aggregate of paid up capital and general reserves as appearing in the balance sheet of the demerged company immediately before demerger

Capital Gains - Part I 27

S.No

Mode of acquisition of capital asset COA to the assessee Section

1 i. Goodwill of a business, trademark or brand name associated with a business

ii. Right to manufacture or produce or process any article or thing

iii. Right to carry on any business or tenancy rights

iv. State carriage permits or loom hours purchased from previous owner

Amount of purchase price 55(2)(a)(i)

2 Same assets as mentioned in (1) above but self generated

NIL (FMV as on 1-4-1981 not allowed) 55(2)(a)(ii)

3 COA of right shares:

i. When assessee subscribes to right shares

ii. Right renounced in favour of any other person

iii. COA in respect of person in whose favour right is renounced

Amount actually paid for acquiring right shares

NIL

Amount paid for acquiring shares plus amount paid to person renouncing the right

55(2)(aa)(ii)

55(2)(aa)(iii)

55(2)(aa)(iv)

Computation of Capital gainsCost of acquisition in relation to certain assets – 55(2)

Capital Gains - Part I 28

S No

Mode of acquisition of capital asset COA to the assessee Section

4 i. Equity shares allotted to a shareholder on corporatization of stock exchanges

ii. Trading or clearing rights, acquired by shareholder mentioned in 4(i) above

COA of the original membership of stock exchange

NIL

55(2)(ab)

Proviso to 55(2)(ab)

5 Any other asset becoming the property of the assessee before 1-4-1981

COA to the assessee or its FMV as on 1-4-1981 at the option of the assessee

55(2)(b)(i)

6 Capital asset becoming the property of the assessee in any of the modes specified in section 49(1) and it became the property of the previous owner before 1-4-1981

COA to the previous owner or its FMV as on 1-4-1981 at the option of the assessee

55(2)(b)(ii)

7 Capital asset becoming the property of the assessee on distribution by the company on liquidation provided capital gains tax has been assessed under section 46(2)

FMV of the asset on the date of distribution

55(2)(b)(iii)

8 Shares or stock of company becoming assessee’s property by consolidation, conversion etc of shares or stock

COA calculated with reference to COA of shares or stock from which asset is derived

55(2)(b)(v)

Computation of Capital gainsCost of acquisition in relation to certain assets – 55(2)

Capital Gains - Part I 29

• Applies to capital gains from transfer of long-term capital asset

• Does not applies to the following:

• Where first proviso applies i.e. Capital gains arising to a non resident from transfer of shares/ debentures of Indian company purchased in Foreign Currency

• Bonds and debentures except for capital indexed bonds

• Indexed COA shall be as under:

Mode I- Assets acquired directly by the assessee himself

a) Asset acquired on or after 1.4.1981= COA X Cost Inflation Index (CII)) of the year of transfer Cost Inflation Index of the year of acquisition

b) Asset acquired before 1.4.1981= COA or FMV as on 1.4.1981 X CII of the year of transfer

CII of PY 1981-82 (i.e. 100)

Mode II- Assets acquired from previous owner in mode given under section 49(1)

COA to the previous owner X CII of the year of transfer CII of the year in which the asset is first held by the assessee

Computation of Capital gainsIndexed cost of acquisition - Second Proviso to Sec 48

Capital Gains - Part I 30

Computation of Capital gainsCost of improvement – section 55(1)

S No

Capital asset Cost of improvement (‘COI’) to the assessee Section

1 Goodwill of a business or a right to manufacture, produce or process any article or thing or right to carry on any business

NIL 55(1)(b)(1)

2 Where the capital asset became the property of the previous owner or the assessee before 1-4-1981

Capital expenditure incurred in making any additions or alterations to the capital asset on or after 1-4-1981 by the previous owner or the assessee

55(1)(b)(2)(i)

3 Capital assets acquired after 1-4-1981

Capital expenditure incurred in making any additions or alterations to the capital asset by the assessee after it became his property and

where the capital asset became the property of the assessee by any mode specified in section 49(1), capital expenditure incurred by the previous owner also be treated as cost of improvement

55(1)(b)(2)(ii)

Capital Gains - Part I 31

Computation of Capital gainsIndexed cost of improvement – section 55(1)

Explanation (iv) to section 48

• Indexed COI for Cost of improvement incurred prior to 1.4.1981 – To be ignored

• COI incurred after 1.4.1981

I. Cost incurred by the assessee

Cost incurred X CII of the year of transfer CII of the year in which improvement made by the

assessee

II. Cost incurred by the previous owner

Cost incurred X CII of the year of transferCII of the year in which improvement made by

the Previous owner and not of the year in which the asset first held by the assessee

Capital Gains - Part I 32

Computation of Capital gainsDepreciable assets – section 50

• Concept of block of assets based on nature of asset and rate of depreciation

Nature of asset Rate of depreciation

Plant and Machinery Computers – 60%

Energy generation and saving devices – 80%

Others - 15%

Buildings Temporary fittings – 100%

Factory building – 10%

Others – 5%

Furniture 10%

Intangibles 25%

Capital Gains - Part I 33

Consideration Block cease to exist Block exists

Exceeds (WDV+ actual cost of asset acquired during the year+ expenses on transfer)

Short-term capital gain Short-term capital gain

Is less than (WDV+ actual cost of asset acquired during the year+ expenses on transfer)

Short-term capital loss Balance left shall be WDV at the end of the year

Computation of Capital gainsDepreciable assets – section 50

Capital Gains - Part I 34

Computation of Capital gainsDepreciable assets – section 50

Case study

Asset Scenario 1 Scenario 2

Amount (in INR) Amount (in INR)

Plant A 500,000 500,000

Plant B 400,000 400,000

Plant C 600,000 600,000

Total 1,500,000 1,500,000

Additions during the year 700,000 700,000

2,200,000 2,200,000

Disposal of assets (A&B) 2,500,000 2,000,000

Short term capital gain/ (loss) 300,000 Nil

WDV as at the end of the previous year Nil 200,000

Capital Gains - Part I 35

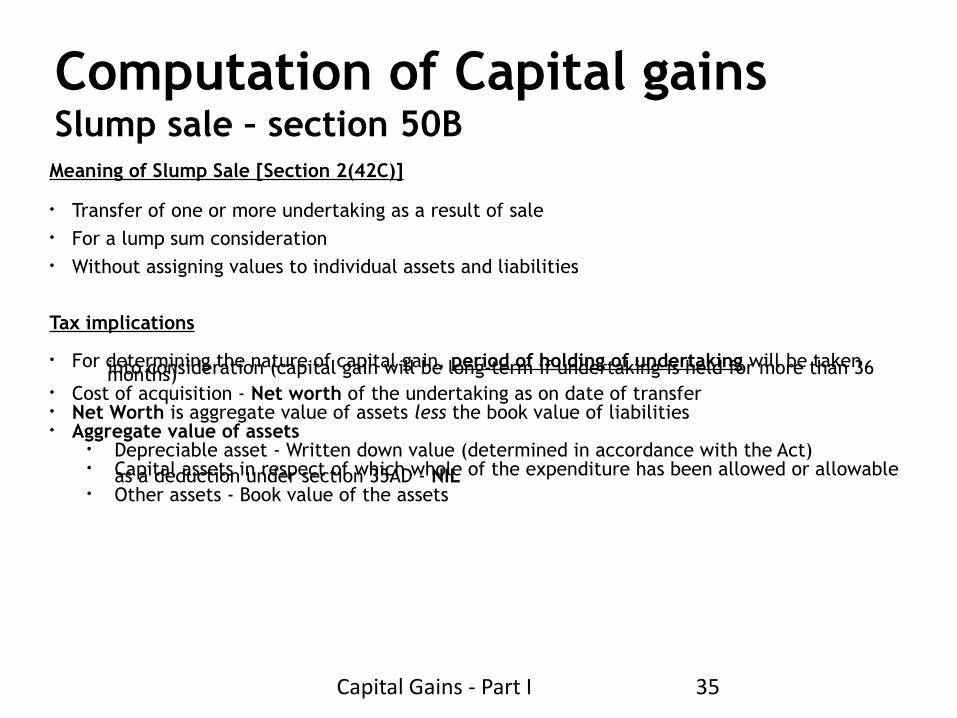

Computation of Capital gainsSlump sale – section 50BMeaning of Slump Sale [Section 2(42C)]

• Transfer of one or more undertaking as a result of sale• For a lump sum consideration• Without assigning values to individual assets and liabilities

Tax implications

• For determining the nature of capital gain, period of holding of undertaking will be taken into consideration (capital gain will be long-term if undertaking is held for more than 36 months)• Cost of acquisition - Net worth of the undertaking as on date of transfer• Net Worth is aggregate value of assets less the book value of liabilities• Aggregate value of assets

• Depreciable asset - Written down value (determined in accordance with the Act)• Capital assets in respect of which whole of the expenditure has been allowed or allowable as a deduction under section 35AD - NIL• Other assets - Book value of the assets

Capital Gains - Part I 36

Computation of Capital gainsSlump sale – section 50BOther aspects

• Determination of value for stamp duty purposed would not shall not violate this condition [Explanation 2 to section 2(42C)

• Benefit of indexation would not be available

Issues for consideration

• Where any asset of the undertaking is not transferred (say, motor cars), whether such transfer shall be regarded as slump sale?

• Where the value of asset has been computed separately and the Business Transfer Agreement captures the lumpsum amount as consideration, whether such transfer be regarded as slump sale?

• Incase of negative net worth, whether the same should be considered as deemed cost of acquisition?

• In a case where the transferor receives consideration in the form of shares, whether the provisions of section 50B would apply?