Chaos, Solitons and Fractals 102 (2017) 245–253

Contents lists available at ScienceDirect

Chaos, Solitons and Fractals

Nonlinear Science, and Nonequilibrium and Complex Phenomena

journal homepage: www.elsevier.com/locate/chaos

Pricing of basket options in subdiffusive fractional Black–Scholes

model

Gulnur Karipova, Marcin Magdziarz

∗

Faculty of Pure and Applied Mathematics, Hugo Steinhaus Center, Wroclaw University of Science and Technology, Wyspianskiego 27, 50-370 Wroclaw,

Poland

a r t i c l e i n f o

Article history:

Received 26 January 2017

Revised 4 May 2017

Accepted 5 May 2017

Available online 10 May 2017

Keywords:

Black–Scholes model

Subdiffusion

Basket options

Stable process

a b s t r a c t

In this paper we generalize the classical multidimensional Black-Scholes model to the subdiffusive case.

In the studied model the prices of the underlying assets follow subdiffusive multidimensional geometric

Brownian motion. We derive the corresponding fractional Fokker–Plank equation, which describes the

probability density function of the asset price. We show that the considered market is arbitrage-free and

incomplete. Using the criterion of minimal relative entropy we choose the optimal martingale measure

which extends the martingale measure from used in the standard Black–Scholes model. Finally, we derive

the subdiffusive Black–Scholes formula for the fair price of basket options and use the approximation

methods to compare the classical and subdiffusive prices.

© 2017 Elsevier Ltd. All rights reserved.

1

t

t

h

M

t

t

m

t

o

s

t

p

T

a

S

u

p

a

w

e

m

d

[

t

F

t

B

t

i

m

p

o

m

W

t

b

o

s

p

fi

u

t

h

0

. Introduction

During the last few decades the scientists have had a keen in-

erest to the problem of financial markets’ modelling and deriva-

ion of prices of different financial derivatives. The breakthrough

appened when in 1973 the papers of Black and Scholes [1] and

erton [14] were published. These papers had a great impact to

he financial market and arouse huge academic interest, setting up

he key principles of arbitrage option pricing. However, the original

odel has its disadvantages as it sets a number of restrictions on

he real state of life [19] . Many of assumptions were relaxed in the

ngoing researches. In this work the subdiffusive phenomena is of

pecific interest.

The fact is that in some financial markets the number of par-

icipants and, therefore, performed transactions, is so low that the

rice of the asset may remain constant during the period of time.

his phenomenon is the most inherent for the emerging markets

nd it breaks the assumption on liquidity set in the original Black–

choles (B-S) model. The idea to model the price of such assets

sing subdiffusive Geometric Brownian Motion (GBM) comes from

hysics: the so-called stagnation periods in the market are associ-

ted with the trapping events of the subdiffusive test particle [4] ,

hich is manifested by the fractional derivatives in Fokker–Planck

quations [15,16] .

∗ Corresponding author.

E-mail addresses: [email protected] (G. Karipova),

[email protected] (M. Magdziarz).

a

B

o

B

ttp://dx.doi.org/10.1016/j.chaos.2017.05.013

960-0779/© 2017 Elsevier Ltd. All rights reserved.

The generalized to the subdiffusive regime B-S model for one

imensional case was already introduced in details in the literature

9] . However, such model cannot define the price of such impor-

ant financial derivatives as, for instance, European basket options.

or these reasons the multidimensional B-S model was applied in

he standard approach. Here we generalize the multidimensional

-S model by adding the periods of stagnation, which are charac-

eristic for subdiffusion and can be modelled by equations involv-

ng fractional derivatives. We underline the extension from one- to

ultidimensional setting of the subdiffusive B-S model is at some

oints not straightforward. Property of lack of arbitrage depends

n the parameters of the volatility matrix. Also, the martingale

easure is not unique, its choice has crucial influence on the price.

e use the relative entropy criterion to solve this problem. Addi-

ionally, there is no closed-form formula for the fair price of the

asket option. It has to be approximated using Monte Carlo meth-

ds or applying deterministic approach.

Let us remind that the celebrated B-S formula was derived by

olving certain heat equation, so the motivation came clearly from

hysics. We expect that the similar process will be observed in

nancial engineering. Fractional operators, which are successfully

sed in statistical physics in the description of anomalous frac-

ional dynamics will find important applications also in finance.

The first chapter of this work includes the basic knowledge

bout the options, classical one-dimensional and multidimensional

-S models and such characteristics of the financial market as lack

f arbitrage and market completeness.

The second chapter introduces the concept of multidimensional

-S model, generalized to the subdiffusive case. At the beginning

246 G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253

2

p

e

i

t

T

t

a

s

f

d

o

Z

H

i

C

w

d

H

m

d

h

o

P

T

a

d

p

i

s

2

s

Z

d

o

Z

w

w

a

k

f

s

p

C

the inverse stable subordinator is defined and its basic character-

istics are given. The subdiffusive multidimensional GBM is intro-

duced, i.e. the subordinated process used to model the prices of

the underlying assets with specific periods of stagnation. The frac-

tional multidimensional Fokker–Planck equation is derived, which

gives the information about the dynamics of the probability den-

sity function (PDF) of the studied process [13,15,16] . In the follow-

ing it is proved that the considered market is arbitrage-free and

incomplete. It should be added that the lack of arbitrage for sub-

diffusive B-S model was also analyzed in [7] . The B-S formula of

option pricing is derived, the price of basket call option depending

on the stability parameter α, maturity time and the strike price is

approximated by the methods of numerical integration and Monte-

Carlo simulations. The obtained price functions are compared with

the classical case. We end the paper with concluding chapter.

For the sake of clarity we moved the most technical proofs to

the Appendix .

2. B-S: classical approach

2.1. Options

Let us recall the definition of an option. Option is a financial

instrument such that its buyer (owner) has the right to buy (call

option) or to sell (put option) an asset Z ( t ) at some prespecified

maturity time T for a prespecified strike price K . The underlying

asset is usually a stock but some other assets are also possible. A

European option, in contrary to the American option, can be exer-

cised at the maturity time only, whereas it is possible to exercise

American option at any time up to expiration [1,17] .

The payoffs of the European call option and the European put

option are equal to (Z(T ) − K) + and (K − Z(T )) + , respectively.

Here (x ) + = max (x, 0) . There is a relationship between price of the

put option P and the price of a call option C . This relationship is

called put-call parity [17] :

Z(0) − Ke −rT = C − P. (1)

Here r ≥ is the interest rate. Further on, we will assume for sim-

plicity that r = 0 .

Let us now introduce the concept of a basket option, which is

defined as financial instrument, where the underlying asset is a

portfolio of various assets Z ( i ) ( t ), i = 1 , . . . , m, for instance, single

stocks. Basket option among others belongs to the class of exotic

options. The basket option implies higher cost-effectiveness than a

simple collection of single options, as it is a diversification instru-

ment which also takes into account the interdependences between

diverse risk factors. As an example, there might be a negative cor-

relation between stocks in the “basket”, strong enough to signifi-

cantly reduce the total risk or even make it disappear [17] . Basket

option, exercised in European call style, has the following payoff(

m ∑

i =1

ω i Z (i ) (T ) − K

)

+ , (2)

where { ω i } m

i =1 are constant weights, such that

∑ m

i =1 ω i = 1 . Here

the constant K > 0 is the strike price.

Trading of option contracts has had a long historical life. How-

ever, the prevalence of the option market increased rapidly in 1973

when options regulations became standardized and transactions

on the stock options were performed on the Chicago Board Op-

tions Exchange. Simultaneously in 1973 Black and Scholes [1] and

Merton [14] published their celebrated papers. These papers had

a great impact to the financial market and arouse huge academic

interest, setting up the key principles of arbitrage option pricing.

While the fair prices of European options can be found using

the classical B-S formula, to find the price of a basket option one

needs to use the multidimensional models.

.2. Classical B-S model

Over the last forty years the B-S [2,14,17,19] model is being a

owerful tool for pricing derivatives. One may define it as a math-

matical model that allows us to simulate the prices of financial

nstruments, such as stocks, as well as derive the fair prices of cer-

ain financial derivatives such as European call options.

Let us consider such a market, that its development up to time

is defined on the probability space ( �, F, P ), where � is called

he sample space, F is a set of all events and possible statements

bout the prices on the market and P is the usual probability mea-

ure. The price of an asset Z t in classical B-S model is assumed to

ollow GBM given by

Z t =

(μ +

1

2

σ 2 )

Z t dt + Z t σdW t , Z 0 = z 0 (3)

r equivalently

t = Z 0 exp { μt + σW t } . (4)

ere, W t is the standard Brownian motion with respect to P, σ > 0

s the diffusion (volatility) parameter and μ ∈ R is the drift.

The celebrated B-S price of European call option equals [1] :

B −S (Z 0 , K, T , σ ) = Z 0 �(d + ) − K�(d −) , (5)

ith

± =

log Z 0 K

± 1 2 σ 2 T

σ√

T ,

ere � is the distribution function of Gaussian distribution with

ean zero and variance equal to one. This fair price was originally

erived by Black and Scholes by solving the well-known in physics

eat equation.

By the mentioned put-call parity we have for the price of put

ption

B −S (Z 0 , K, T , σ ) = C B −S (Z 0 , K, T , σ ) + K − Z 0 . (6)

he B-S model was certainly a break-through in the option pricing

pparatus. However, it has number of limiting assumptions that

o not reflect the real market conditions and behavior of assets’

rices. This gives a fruitful area for academic purposes: already ex-

sting and ongoing researches are aimed to possibly relax these as-

umptions.

.3. Multidimensional B-S model

The classical B-S model can be generalized to the multidimen-

ional case, i.e. the number of assets m > 1 and the asset prices

(t) = (Z (1) t , . . . , Z (m )

t ) follow multidimensional GBM as

Z (i ) t =

(

μi +

1

2

n ∑

j=1

σ 2 i j

)

Z (i ) t d t + Z (i )

t

n ∑

j=1

σi j d W

( j) t , Z (i )

0 = z 0 i (7)

r equivalently

(i ) t = Z (i )

0 exp

{

μi t +

n ∑

j=1

σi j W

( j) t

}

, i = 1 , . . . m,

here W (t) = (W

(1) t , . . . , W

(n ) t ) is n -dimensional Brownian motion

ith respect to P , { σ ij } m ×n , σ ij ≥ 0, is non-singular volatility matrix

nd (μ1 , . . . , μm

) is a drift vector.

Multidimensional B-S model allows to find the fair price of bas-

et options defined in (2) . Unfortunately, there is no explicit B-S

ormula for such purpose. The price of a basket option in the clas-

ical multidimensional B-S model can be found using Gentle’s ap-

roximation by geometric average [6,17] . It is given by

B −S =

(

m ∑

i =1

ω i Z (i ) 0

)

(c�(l 1 (T )) − ( K + c − 1)�(l 2 (T ))) , (8)

G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253 247

w

c

v

ρ

ω

w

l

2

m

p

[

Z

P

Q

a

i

t

r

p

fi

P

t

s

i

g

i

Q

e

l

r

I

Q

s

t

t

3

d

[

t

F

t

s

o

t

i

m

o

P

h

t

t

t

i

b

t

c

3

S

0

L

E

i

h

s

E

w

o

E

w

f

S

o

o

3

d

Z

w

c

d

c

o

r

F

t

here

= exp

{ (

1

2

v 2 − 1

2

m ∑

j=1

ˆ ω j σ2 j

)

T

}

,

2 =

m ∑

i, j=1

ρi, j ω i ω j σi σ j ,

i, j =

∑ n k =1 σik σ jk

σi σ j

, σi =

√

n ∑

k =1

σ 2 ik ,

ˆ i =

ω i Z (i ) 0 ∑ m

j=1 ω j Z ( j) 0

, K =

K ∑ m

j=1 ω j Z ( j) 0

,

here { ρ ij } m ×n are the instantaneous correlation coefficients and

1 , 2 (t) =

ln c − ln ( K + c − 1) ± 1 2 v 2 t

v √

t .

.4. Arbitrage free market and market completeness

The lack of arbitrage for a market model is crucial require-

ent for pricing regulations, i.e. it should not be possible to get a

rofit without any risk. The Fundamental Theorem of Asset Pricing

3] states that the market model is arbitrage-free if the asset price

( t ) is a martingale with respect to some measure Q equivalent to

. In other words, Z ( t ) is a fair-game process w.r.t. Q . The measure

is such a measure under which the expected rate of return on

ll assets existing in arbitrage-free market is equal for all financial

nstruments despite the variability of assets’ price, whereas under

he real-life measure P the higher is the risk, the larger is expected

ate of return [9] .

Another vital characteristic of the market model is market com-

leteness which assures the uniqueness of the fair price for each

nancial instrument. The Second Fundamental Theorem of Asset

ricing [3] states that if there is only one martingale measure Q

hen the market is complete.

One can show that the classical one-dimensional B-S model re-

ponds to both arbitrage-free and completeness criteria, therefore,

ts B-S formula for option pricing defines a unique fair price of sin-

le European option. The martingale measure Q for the B-S model

s given by

(A ) =

∫ A

exp

{

−(μ + σ 2 / 2

σ

)2 T

2

− μ + σ 2 / 2

σW T

}

dP, A ∈ F .

(9)

In the multidimensional B-S model the case looks a bit differ-

nt. Let us introduce constants { γ j } n j=1 as the solution of the fol-

owing system

− μi −1

2

n ∑

j=1

σ 2 i j =

n ∑

j=1

σi j γ j , i = 1 , . . . m, (10)

f the solution of such system exists, then there exists Q defined as

(A ) =

∫ A

exp

{

−n ∑

i =1

γi W

(i ) T

− 1

2

n ∑

i =1

γ 2 i T

}

dP, A ∈ F , (11)

uch that Z ( t ) is a martingale w.r.t. Q . This implies the lack of arbi-

rage. One can show that the considered market model is complete,

herefore, all financial derivatives have unique fair prices.

. Subdiffusive multidimensional B-S model

The generalized to the subdiffusive regime B-S model for one

imensional case was already introduced in details in the literature

9] . However, such model cannot define the price of such impor-

ant financial derivatives as, for instance, European basket options.

or these reasons the multidimensional B-S model was applied in

he classical approach.

The following chapter introduces the concept of multidimen-

ional B-S model, generalized to the subdiffusive case. It consists

f three sections. The first defines the inverse α-stable subordina-

or and gives its basic characteristics. The second introduces subd-

ffusive multidimensional GBM, i.e. subordinated process used to

odel the prices of the underlying assets with specific periods

f stagnation. There is also a fractional multidimensional Fokker–

lank equation derived, which gives the information about the be-

avior of the PDF of the studied process [13,15,16] . The third sec-

ion shows that the introduced subdiffusive market has no arbi-

rage and is not complete. The subdiffusive B-S formula of op-

ion pricing is derived here, the price of basket options depend-

ng on the α, maturity time and the strike price is approximated

y the methods of numerical integration and Monte-Carlo simula-

ions. The obtained price functions are compared with the classical

ase.

.1. Inverse alpha-stable subordinator

The inverse α-stable subordinator is defined as

α(t) = inf { τ > 0 : U α(τ ) > t} , (12)

< α < 1. Here { U α( τ )} τ > 0 is the strictly increasing α-stable

évy process (subordinator). It has the following Laplace transform

(e −uU α (t) ) = e −tu α [8,22,23] . Here E denotes the expectation. Us-

ng the fact that U α( t ) is 1/ α-self-similar process, we get that S α( t )

as the same distribution as [ t / U α(1)] α . The moments of the con-

idered process can be found in [12]

[ S n α(t )] =

t nαn !

(nα + 1) , (13)

here ( ·) is the gamma function. Moreover, the Laplace transform

f S α( t ) equals

(e −uS α (t) ) = E α(−ut α) , (14)

here the function E α(z) =

∑ ∞

n =0 z n

(nα+1) is the Mittag-Leffler

unction [11,21] .

Simulated trajectories of the processes U α( t ) and corresponding

α( t ) are presented in Fig. 1 . As it can be seen, consecutive jumps

f U α( t ) are reflected by the flat periods (the periods of stagnation)

f S α( t ), which is characteristic for subdiffusion.

.2. Subdiffusive geometric Brownian motion

Let us consider such a market model in which the price of m

ifferent assets is given by the following subdiffusive process

α(t) = Z(S α(t)) , (15)

here S α( t ) is inverse α-stable subordinator and Z(t) =(Z (1)

t , . . . , Z (m ) t ) is the GBM given in (15) . Such defined pro-

ess Z α(t) = (Z (1) α (t ) , . . . , Z (m )

α (t )) will describe the prices of m

ifferent assets. We will call it subdiffusive GBM. Contrary to the

lassical one, it will capture the property of subdiffusion (periods

f stagnation), characteristic for emerging markets or interest

ates.

The next theorem determines the multidimensional fractional

okker–Plank equation (fFPE), which gives the information about

he behavior of the PDF of Z α( t ).

248 G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253

Fig. 1. Trajectories of the α-stable and inverse α-stable subordinators, α = 0 . 9 .

a

I

k

L

t

a

d

o

3

s

T

m

s

e

Y

i

A

i

r

Theorem 1. Let Z α( t ) be given by (15) . Then its PDF is the solution

of the fFPE

∂ω(x, t)

∂t = 0 D

1 −αt

[−

m ∑

i =1

∂

∂x i

(μi +

1

2

n ∑

j=1

σ 2 i j

)x i ω(x, t)

+

m ∑

i =1

m ∑

j=1

∂ 2

∂ x i ∂ x j (K i j (x ) ω(x, t))

], (16)

ω(x, 0) = δZ 0 (x ) , K i j (x ) =

1 2

∑ n k =1 σik σ jk x i x j . Here, the operator

0 D

1 −αt g(t) =

1

(α)

d

dt

∫ t

0

(t − s ) α−1 g(s ) ds,

0 < α < 1, is the Riemann–Liouville fractional derivative [21] .

Proof. We will apply the technique from the one-dimensional

case. Let p ( x, t ) be the PDF of Z α( t ). The total probability formula

implies that

ˆ p (x, k ) =

∫ ∞

0

e −kt p(x, t) dt =

∫ ∞

0

f (x, τ ) g (τ, k ) dτ. (17)

The above functions f ( x, τ ) and g ( τ , t ) are the respective PDFs of

the processes Z ( τ ) and S α( t ). We use the convention that ˆ h is the

Laplace transform of a function h w.r.t. the time variable. Recall

that Z ( τ ) is defined in (15) , therefore its PDF solves the Fokker–

Plank equation

∂ f (x, t)

∂t = −

m ∑

i =1

∂

∂x i

(μi +

1

2

n ∑

j=1

σ 2 i j

)x i f (x, t)

+

m ∑

i =1

m ∑

j=1

∂ 2

∂ x i ∂ x j (K i j (x ) f (x, t)) ,

Putting the Laplace transform on both sides of the above we arrive

at

k f (x, k ) − f (x, 0) = −m ∑

i =1

∂

∂x i

(μi +

1

2

n ∑

j=1

σ 2 i j

)x i f (x, t)

+

m ∑

i =1

m ∑

j=1

∂ 2

∂ x i ∂ x j (K i j (x ) f (x, t)) . (18)

Using selfsimilarity of S α( t ) and U α( t ) we obtain

g(τ, t) = − ∂

∂τ

∫ t

0

u (y, τ ) dy =

t

ατu (t, τ ) ,

where by u ( t, τ ) we denote the PDF of U α( τ ). This implies that

ˆ g (τ, k ) = k α−1 e −τk α

nd consequently

ˆ p (x, k ) =

∫ ∞

0

f (x, τ ) k α−1 e −τk α dτ = k α−1 ˆ f (x, k α) .

f we change the variables k → k α , we arrive at.

p (x, k ) − p(x, 0) = k α−1

[−

m ∑

i =1

∂

∂x i

(μi +

1

2

n ∑

j=1

σ 2 i j

)x i p (x, t)

+

m ∑

i =1

m ∑

j=1

∂ 2

∂ x i ∂ x j (K i j (x ) p (x, t))

].

astly, if we invert the Laplace transform, we arrive at the equa-

ion

∂ p(x, t)

∂t = 0 D

1 −αt

[−

m ∑

i =1

∂

∂x i

(μi +

1

2

n ∑

j=1

σ 2 i j

)x i p(x, t)

+

m ∑

i =1

m ∑

j=1

∂ 2

∂ x i ∂ x j (K i j (x ) p(x, t))

],

nd the proof is completed. �

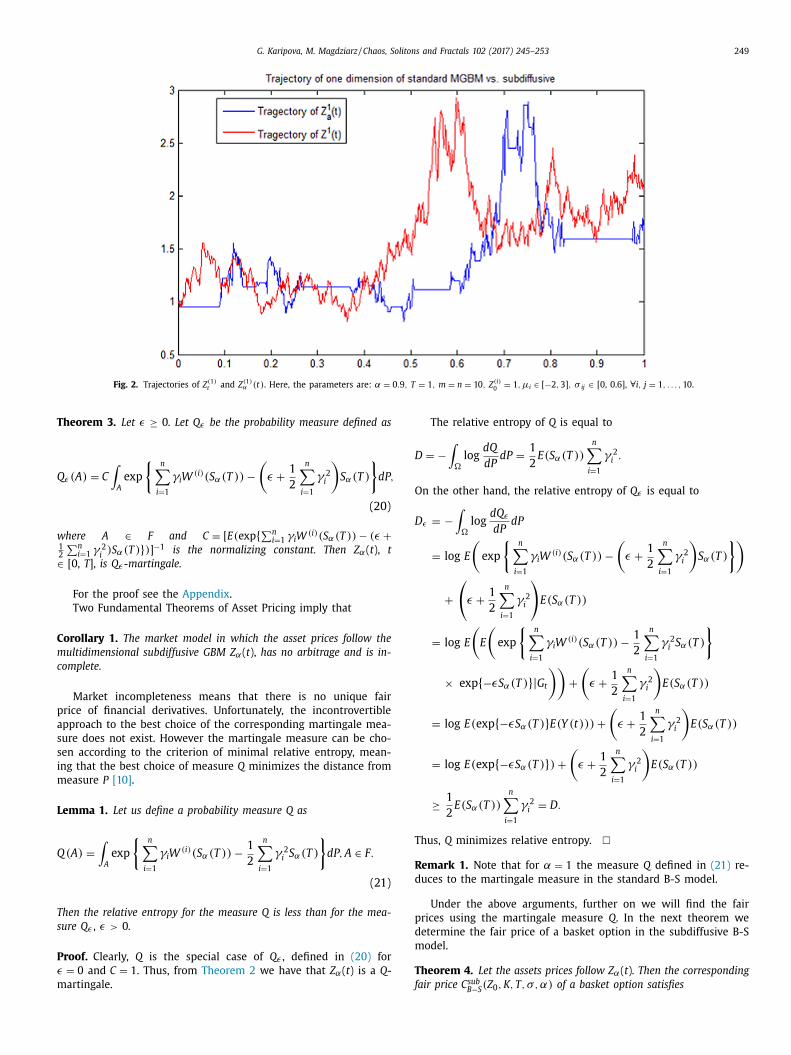

In Fig. 2 we compare trajectory of the first coordinate of stan-

ard multidimensional GBM and trajectory of the first coordinate

f the corresponding subdiffusive multidimensional GBM.

.3. Subdiffusive B-S formula

The following theorems verify the existence of martingale mea-

ures for Z α( t ).

heorem 2. If C ( t ) is a linear combination of independent Brownian

otions, i.e. C(t) =

∑ n i =1 γi W

(i ) (t) , γi = const, ∀ i, then the subdiffu-

ion process A (t) = C(S α(t)) is a martingale. Moreover, the stochastic

xponential of A ( t ) defined as

(t) = exp

{λA (t ) − λ2

2

〈 A (t ) , A (t ) 〉 }

, λ � = 0

s also a martingale. Here < A ( t ), A ( t ) > is the quadratic variation of

( t ) .

For the proof see the Appendix .

Let us introduce constants { γ j } n j=1 as the solution of the follow-

ng system

− μi −1

2

n ∑

j=1

σ 2 i j =

n ∑

j=1

σi j γ j , i = 1 , . . . , m. (19)

G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253 249

Fig. 2. Trajectories of Z (1) t and Z (1)

α (t) . Here, the parameters are: α = 0 . 9 , T = 1 , m = n = 10 , Z (i ) 0

= 1 , μi ∈ [ −2 , 3] , σ ij ∈ [0, 0.6], ∀ i, j = 1 , . . . , 10 .

T

Q

w

∈

C

m

c

p

a

s

s

i

m

L

Q

T

s

P

ε

m

D

O

D

T

R

d

p

d

m

T

f

heorem 3. Let ε ≥ 0 . Let Q ε be the probability measure defined as

ε (A ) = C

∫ A

exp

{n ∑

i =1

γi W

(i ) (S α(T )) −(

ε +

1

2

n ∑

i =1

γ 2 i

)S α(T )

}dP,

(20)

here A ∈ F and C = [ E( exp { ∑ n i =1 γi W

(i ) (S α(T )) − (ε +1 2

∑ n i =1 γ

2 i ) S α(T ) } )] −1 is the normalizing constant. Then Z α( t ), t

[0, T ], is Q ε-martingale.

For the proof see the Appendix .

Two Fundamental Theorems of Asset Pricing imply that

orollary 1. The market model in which the asset prices follow the

ultidimensional subdiffusive GBM Z α( t ), has no arbitrage and is in-

omplete.

Market incompleteness means that there is no unique fair

rice of financial derivatives. Unfortunately, the incontrovertible

pproach to the best choice of the corresponding martingale mea-

ure does not exist. However the martingale measure can be cho-

en according to the criterion of minimal relative entropy, mean-

ng that the best choice of measure Q minimizes the distance from

easure P [10] .

emma 1. Let us define a probability measure Q as

(A ) =

∫ A

exp

{n ∑

i =1

γi W

(i ) (S α(T )) − 1

2

n ∑

i =1

γ 2 i S α(T )

}dP, A ∈ F .

(21)

hen the relative entropy for the measure Q is less than for the mea-

ure Q ε , ε > 0 .

roof. Clearly, Q is the special case of Q ε , defined in (20) for

= 0 and C = 1 . Thus, from Theorem 2 we have that Z α( t ) is a Q -

artingale.

The relative entropy of Q is equal to

= −∫ �

log dQ

dP dP =

1

2

E(S α(T )) n ∑

i =1

γ 2 i .

n the other hand, the relative entropy of Q ε is equal to

ε = −∫ �

log dQ ε

dP dP

= log E

(exp

{n ∑

i =1

γi W

(i ) (S α(T )) −(

ε +

1

2

n ∑

i =1

γ 2 i

)S α(T )

})

+

(

ε +

1

2

n ∑

i =1

γ 2 i

)

E(S α(T ))

= log E

(E

(exp

{n ∑

i =1

γi W

(i ) (S α(T )) − 1

2

n ∑

i =1

γ 2 i S α(T )

}

× exp {−εS α(T ) }| G t

))+

(ε +

1

2

n ∑

i =1

γ 2 i

)E(S α(T ))

= log E ( exp {−εS α(T ) } E (Y (t))) +

(ε +

1

2

n ∑

i =1

γ 2 i

)E(S α(T ))

= log E( exp {−εS α(T ) } ) +

(ε +

1

2

n ∑

i =1

γ 2 i

)E(S α(T ))

≥ 1

2

E(S α(T )) n ∑

i =1

γ 2 i = D.

hus, Q minimizes relative entropy. �

emark 1. Note that for α = 1 the measure Q defined in (21) re-

uces to the martingale measure in the standard B-S model.

Under the above arguments, further on we will find the fair

rices using the martingale measure Q . In the next theorem we

etermine the fair price of a basket option in the subdiffusive B-S

odel.

heorem 4. Let the assets prices follow Z α( t ) . Then the corresponding

air price C sub B −S

(Z 0 , K, T , σ, α) of a basket option satisfies

250 G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253

Fig. 3. Prices of the basket option, exercised in European call style, depending on the maturity time for different α. The parameters for the figure above are as follows:

m = n = 10 , σ ij ∈ [0, 1], Z (i ) 0

= 1 , ∀ i, j, K = 40 . The results were obtained using (22) from 10 0 0 simulated independent realizations of the random variable S α ( T ).

C

C

t

t

n

u

t

m

B

C

T

P

R

t

a

m

t

g

T

S

a

t

t

(

b

s

o

w

t

a

m

c

sub B −S (Z 0 , K, T , σ, α) = E(C B −S (Z 0 , K, S α(T ) , σ ))

=

∫ ∞

0

C B −S (Z 0 , K, x, σ ) T −αg α(x/T α) dx, (22)

where C B −S (Z 0 , K, T , σ ) is price of the basket option in the standard

multidimensional B-S model, g α( z ) stands for the PDF of S α(1) and

can be expressed using Fox function

g α(z) = H

10 11

(z| (1 −α,α)

(0 , 1)

).

Proof. The arbitrage-free rule of pricing requires that

sub B −S (Z 0 , K, T , σ, α) = E Q

((m ∑

i =1

ω i Z (i ) α (T ) − K

)+

)

= E

(exp

{n ∑

i =1

γi W

(i ) (S α(T ))

− 1

2

n ∑

i =1

γ 2 i S α(T )

}(m ∑

i =1

ω i Z (i ) α (T ) − K

)+

)

= E

(E

(exp

{n ∑

i =1

γi W

(i ) (S α(T ))

− 1

2

n ∑

i =1

γ 2 i S α(T )

}

×(

m ∑

i =1

ω i Z (i ) α (T ) − K

)+

)| S α(T )

)= E(C B −S (Z 0 , K, S α(T ) , σ ))

=

∫ ∞

0

C B −S (Z 0 , K, x, σ ) g α(x, T ) dx.

Here by g α( x, T ) we denote the PDF of S α( T ). since S α( T ) is α-

selfsimilar, we obtain g α(x, T ) = T −αg α(x/T α) . Thus, the statement

follows. �

Remark 2. There is no explicit formula for C B −S (Z 0 , K, T , σ ) , there-

fore, in order to find the basket option price in the subdiffusive

case, it is necessary to use the approximation methods. One needs

o approximate first the classical price C B −S (Z 0 , K, x, σ ) using Gen-

le’s approximation (already given in (8) , see [6,17] ). Next, one

eeds to approximate the integral ∫ ∞

0 C B −S (Z 0 , K, x, σ ) g α(x, T ) dx

sing some standard method. Another possibility is to use the fact

hat C sub B −S

(Z 0 , K, T , σ, α) = E(C B −S (Z 0 , K, S α(T ) , σ )) and to approxi-

ate C sub B −S

(Z 0 , K, T , σ, α) using Monte Carlo methods.

The put-call parity applied to the multidimensional subdiffusive

-S model, with r = 0 is as follows

sub B −S (Z 0 , K, T , σ, α) − P sub

B −S (Z 0 , K, T , σ, α) = Z α(0) − K, .

hus the subdiffusive price of the put option yields

sub B −S (Z 0 , K, T , σ, α) = C sub

B −S (Z 0 , K, T , σ, α) + K − Z α(0) .

emark 3. The derivatives prices with payoff functions, different

han European basket option, can be calculated using analogous

pproach.

The above result allows us to find fair price of basket option in

ultidimensional subdiffusive B-S model. For instance, for α = 1 / 2

he Fox function can be evaluated as follows [18]

1 / 2 (z) =

1 √

πexp

{− z 2

4

}, z ≥ 0 .

he price of a basket option in the classical Multidimensional B-

model can be found using Gentle’s approximation by geometric

verage, mentioned in previous chapter. The approximate value of

he classical B-S formula is given by (8) . Thus, one can estimate

he value of C sub B −S

by numerical integration of expression in formula

22) . Another method of finding the price of the basket option is

y using well-known Monte Carlo methods. It is only needed to

imulate the realization of S α( T ). From the self-similarity property

f S α( t ) it is evident that S α( T ) is equal in distribution to (

T U α (1)

)α,

here U α( τ ) is α-stable subordinator. U α(1) can be generated in

he standard way, see [5] . Thus, one only needs to simulate U α(1)

nd estimate the expectations in formula (22) using Monte-Carlo

ethod.

In Fig. 3 prices of the basket option, exercised in European

all style, depending on the maturity time for different α are

G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253 251

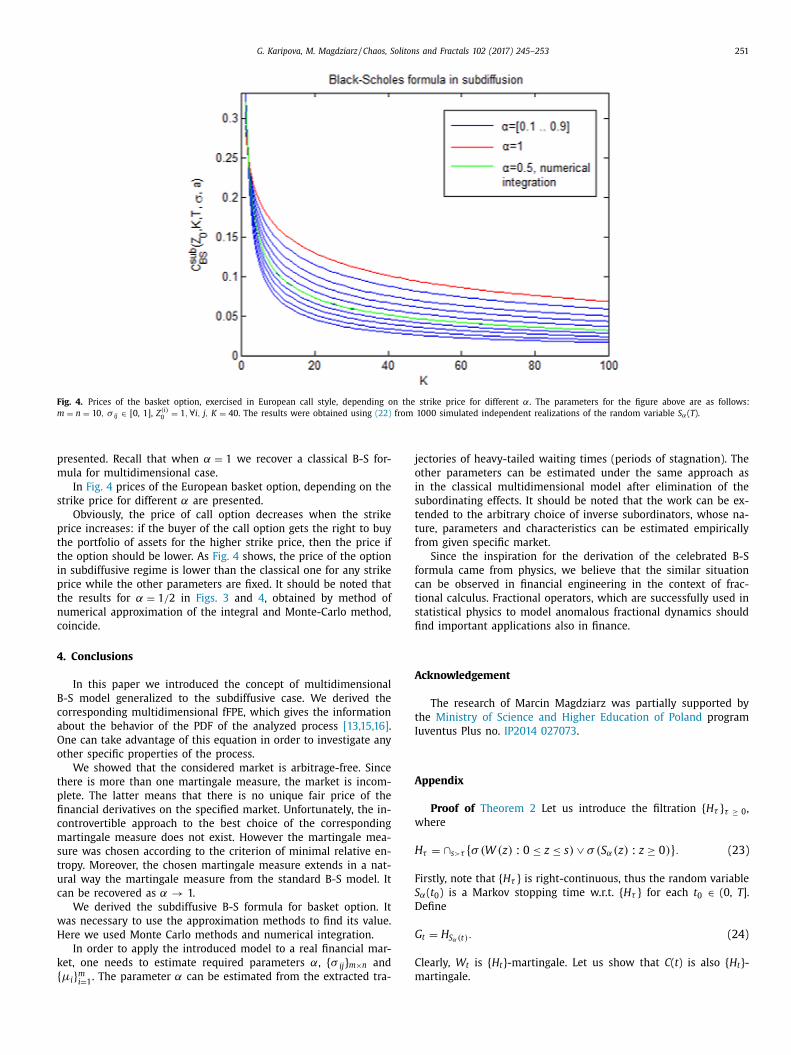

Fig. 4. Prices of the basket option, exercised in European call style, depending on the strike price for different α. The parameters for the figure above are as follows:

m = n = 10 , σ ij ∈ [0, 1], Z (i ) 0

= 1 , ∀ i, j, K = 40 . The results were obtained using (22) from 10 0 0 simulated independent realizations of the random variable S α( T ).

p

m

s

p

t

t

i

p

t

n

c

4

B

c

a

O

o

t

p

fi

c

m

s

t

u

c

w

H

k

{

j

o

i

s

t

t

f

f

c

t

s

fi

A

t

I

A

w

H

F

S

D

G

C

m

resented. Recall that when α = 1 we recover a classical B-S for-

ula for multidimensional case.

In Fig. 4 prices of the European basket option, depending on the

trike price for different α are presented.

Obviously, the price of call option decreases when the strike

rice increases: if the buyer of the call option gets the right to buy

he portfolio of assets for the higher strike price, then the price if

he option should be lower. As Fig. 4 shows, the price of the option

n subdiffusive regime is lower than the classical one for any strike

rice while the other parameters are fixed. It should be noted that

he results for α = 1 / 2 in Figs. 3 and 4 , obtained by method of

umerical approximation of the integral and Monte-Carlo method,

oincide.

. Conclusions

In this paper we introduced the concept of multidimensional

-S model generalized to the subdiffusive case. We derived the

orresponding multidimensional fFPE, which gives the information

bout the behavior of the PDF of the analyzed process [13,15,16] .

ne can take advantage of this equation in order to investigate any

ther specific properties of the process.

We showed that the considered market is arbitrage-free. Since

here is more than one martingale measure, the market is incom-

lete. The latter means that there is no unique fair price of the

nancial derivatives on the specified market. Unfortunately, the in-

ontrovertible approach to the best choice of the corresponding

artingale measure does not exist. However the martingale mea-

ure was chosen according to the criterion of minimal relative en-

ropy. Moreover, the chosen martingale measure extends in a nat-

ral way the martingale measure from the standard B-S model. It

an be recovered as α → 1.

We derived the subdiffusive B-S formula for basket option. It

as necessary to use the approximation methods to find its value.

ere we used Monte Carlo methods and numerical integration.

In order to apply the introduced model to a real financial mar-

et, one needs to estimate required parameters α, { σ ij } m ×n and

μi } m

i =1 . The parameter α can be estimated from the extracted tra-

ectories of heavy-tailed waiting times (periods of stagnation). The

ther parameters can be estimated under the same approach as

n the classical multidimensional model after elimination of the

ubordinating effects. It should be noted that the work can be ex-

ended to the arbitrary choice of inverse subordinators, whose na-

ure, parameters and characteristics can be estimated empirically

rom given specific market.

Since the inspiration for the derivation of the celebrated B-S

ormula came from physics, we believe that the similar situation

an be observed in financial engineering in the context of frac-

ional calculus. Fractional operators, which are successfully used in

tatistical physics to model anomalous fractional dynamics should

nd important applications also in finance.

cknowledgement

The research of Marcin Magdziarz was partially supported by

he Ministry of Science and Higher Education of Poland program

uventus Plus no. IP2014 027073 .

ppendix

Proof of Theorem 2 Let us introduce the filtration { H τ } τ ≥ 0 ,

here

τ = ∩ s>τ { σ (W (z) : 0 ≤ z ≤ s ) ∨ σ (S α(z) : z ≥ 0) } . (23)

irstly, note that { H τ } is right-continuous, thus the random variable

α( t 0 ) is a Markov stopping time w.r.t. { H τ } for each t 0 ∈ (0, T ].

efine

t = H S α (t) . (24)

learly, W t is { H t }-martingale. Let us show that C ( t ) is also { H t }-

artingale.

252 G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253

Y

Y

Y

a

h

Q

T

o

E

U

E

f

E

A

m

i

E

T

E

T

f

t

Z

E(C(t) | H s ) = E

(n ∑

i =1

γi W

(i ) (t) | H s

)

=

n ∑

i =1

E(γi W

(i ) (t) | H s ) =

n ∑

i =1

γi W

(i ) (s ) = C(s ) .

Therefore, C ( t ) is { H t }-martingale, C(t) ∼ N(0 , t ∑ n

i =1 γ2

i ) . Define

the following { H τ }-stopping times

T n = inf { τ > 0 : | C(τ ) | = n } . Note that T n ↗∞ when n → ∞ . Additionally C ( T n ∧ τ ) is a martin-

gale, Moreover, it is bounded by n . Therefore using Doob’s theorem

we get for s < t

E{ C(T n ∧ S α(t)) | G s } = C(T n ∧ S α(s )) .

Now, we are in position to use the Lebesgue dominated conver-

gence theorem, which yields

E{ C(T n ∧ S α(t)) | G s } → E{ C(S α(t)) | G s } as n → ∞ . Finally, we obtain E{ C(S α(t)) | G s } = C(S α(s ))) , thus

A (t) = C(S α(t)) is a { G t }-martingale.

Using Prop. 3.4, Chap. 4 in [20] we obtain that the process Y ( t )

is a local martingale. Additionally, E( sup o≤u ≤t Y (u )) < ∞ . This im-

plies that Y ( t ) is also a martingale.

Proof of Theorem 3 :

Let us put

(t) = exp

{n ∑

j=1

γ j W

( j) t − 1

2

n ∑

j=1

γ 2 j t

},

Z (i ) (t) = exp

{μi t +

n ∑

j=1

σi j W

( j) t

},

Z(t) = (Z (1) (t ) , . . . , Z (m ) (t )) .

Using the fact

〈 A (t) , A (t) 〉 = 〈 C(S α(t)) , C(S α(t)) 〉 =

n ∑

i =1

γ 2 i S α(t) (25)

and setting λ = 1 , from Theorem 1 we know that Y ( S α( t )) is a ( G t ,

P )-martingale. The following holds

(t) Z (i ) (t) = exp

{(μi −

1

2

n ∑

j=1

γ 2 j

)t +

n ∑

j=1

(σi j + γ j ) W

( j) t

}.

Set μi = −( 1 2

∑ n j=1 σ

2 i j

+

∑ n j=1 σi j γ j ) , then

(t) Z (i ) (t) = exp

{−

(1

2

n ∑

j=1

σ 2 i j +

n ∑

j=1

σi j γ j +

1

2

n ∑

j=1

γ 2 j

)t

+

n ∑

j=1

(σi j + γ j ) W

( j) t

}

= exp

{n ∑

j=1

(σi j + γ j ) W

( j) t − 1

2

n ∑

j=1

(σi j + γ j ) 2 t

}.

This implies that the processes Y ( t ) Z ( i ) ( t ), ∀ i are { H t }-martingales

w.r.t. P .

Introduce the process

Z S α (T ) (t) = Z(t ∧ S α(T )) .

Then we get that the processes (e −εS α (T ) Y (t ∧ S α(T )) Z (i )

S α (T ) (t)

)t≥0

(26)

re martingales w.r.t. H t . Next, for every A ∈ H t the following

olds

ε (A ) = E

(1 A exp

{n ∑

i =1

γi W

(i ) (S α(T )) −(

ε +

1

2

n ∑

i =1

γ 2 i

)S α(T )

})

= E

(1 A e

−εS α (T ) E

(exp

{n ∑

i =1

γi W

(i ) (S α(T ))

− 1

2

n ∑

i =1

γ 2 i S α(T )

}| H t

))= E ( 1 A e

−εS α (T ) (E (Y (S α(T )) | H t ))

=

{E( 1 A e

−εS α (T ) Y (t)) , t < S α(T )

E( 1 A e −εS α (T ) Y (S α(T ))) , t ≥ S α(T )

= E( 1 A e −εS α (T ) Y (t ∧ S α(T ))) .

his implies that Z S α(T ) (t) is a martingale w.r.t. ( H t , Q ε ). More-

ver

Q ε

(sup

t≥0

Z (i ) S α (T )

(t) )

= E Q ε(

sup

t≤S α (T )

Z (i ) (t) )

= E

(exp

{n ∑

i =1

γi W

(i ) (S α(T ))

−(

ε +

1

2

n ∑

i =1

γ 2 i

)S α(T )

}sup

t≤S α (T )

Z (i ) (t)

)

≤ E

(exp

{n ∑

i =1

γi W

(i ) (S α(T ))

}e | μi | S α (T )

× sup

t≤T

n ∑

j=1

σi j W

( j) (S α(t))

). (27)

sing the already mentioned formula for moments E(S n α(T )) =T nαn !

(nα+1) , n ∈ N, we obtain

( exp { λS α(T ) } ) =

∞ ∑

n =0

λn E(S n α(T ))

n ! =

∞ ∑

n =0

(T αλ) n

(nα + 1) < ∞

or any λ > 0. Now, using the conditioning argument we arrive at

(exp

{n ∑

i =1

γi W

(i ) (S α(T ))

})

= E

(exp

{1

2

S α(T ) n ∑

j=1

γ 2 j

})< ∞ .

dditionally, as exp { ∑ n j=1 σi j W

( j) (S α(t)) } is a non-negative sub-

artingale, we apply the Doob’s inequality and obtain the follow-

ng

(sup

t≤T

exp

{n ∑

j=1

σi j W

( j) (S α(t))

})2

≤ 4 E

(exp

{2

n ∑

j=1

σi j W

( j) (S α(T ))

})< ∞ .

his implies

Q ε

(sup

t≥0

Z (i ) S α (T )

(t) )

< ∞ .

herefore, Z (i ) S α(T )

(t) are martingales. Additionally, they are uni-

ormly integrable. Thus there must exist a sequence { X (i ) } m

i =1 with

he following property Z (i ) S α(T )

(t) = E Q ε (X (i ) | H t ) and

(i ) α (t) = Z (i )

S α (T ) (S α(t)) = E Q ε (X

(i ) | H S α (t) ) .

G. Karipova, M. Magdziarz / Chaos, Solitons and Fractals 102 (2017) 245–253 253

L

ε

m

R

[

[

[

astly, Z α( t ) is a martingale w.r.t. (H S α(t) , Q ε ) Note that for each

≥ > 0 we obtain different measure Q ε . So, there is no unique

artingale measure for Z α( t ). �

eferences

[1] Black F , Scholes M . The pricing of options and corporate liabilities. J Pol Econ1973;81:637–54 .

[2] Company R , Jodar L . Numerical solution of Black–Scholes option pricing with

variable yield discrete dividend payment. Banach Cent Publ 2008;83:37–47 . [3] Cont R , Tankov P . Financial modeling with jump processes. Chapman &

Hall/CRC, Boca Raton; 2004 . [4] Elizar I , Klafler J . Spatial gliding, temporal trapping and anomalous transport.

Physica D 2004;187:30–50 . [5] Janicki A , Weron A . Simulation and chaotic behaviour of α-stable stochastic

processes. New York: Marcel Dekker; 1994 .

[6] Krekel M , Kock J , Korn R , Man T-K . An analysis of pricing methods for basketsoptions. Wilmott Mag 2004;3:82–9 .

[7] Li GH , Zhang H , Luo MK . A multidimensional subdiffusion model: an arbi-trage-free market. Chin Phys B 2012;21:128901 .

[8] Magdziarz M , Weron A . Anomalous diffusion and semimartingales. EPL20 09;86:60 010 .

[9] Magdziarz M . Black–Scholes formula in subdiffusive regime. J Stat Phys

2009;136:553–64 . [10] Magdziarz M , Gajda J . Anomalous dynamics of Black–Scholes model time

changed by inverse subordinators. ACTA Physica Polonica 2012;B 43:1093–110 .[11] Magdziarz M . Path properties of subdiffusion - a martingale approach. Stochas-

tic Models 2010;26:256–71 .

[12] Magdziarz M . Stochastic representation of subdiffusion processes withtime-dependent drift. Stochastic Process Appl 2009;119:3238–52 .

[13] Martens W , Wagner U . Advances in solving high dimensional Fokker–Planckequations. Rome: ENOC; 2011 .

[14] Merton RC . Theory of rational option pricing. Bell J Econ Manag Sci1973;4:141–83 .

[15] Metzler R , Barkai E , Klafter J . Anomalous diffusion and relaxation close to ther-mal equilibrium: a fractional Fokker–Planck equation approach. Phys Rev Lett

1999;82:3563–7 .

[16] Metzler R , Klafter J . The random walk’s guide to anomalous diffusion: a frac-tional dynamics approach. Phys Rep 20 0 0;339:1–77 .

[17] Musiela M , Rutkowski M . Martingale methods in financial modelling. Berlin:Springer; 1997 .

[18] Piryatinska A , Saichev AI , Woyczynski WA . Models of anomalous diffusion: thesubdiffusive case. Physica 2005;A 349:375–420 .

[19] Ray S . A close look into Black–Scholes option pricing model. J Sci (JOS)

2012;2:172–8 . 20] Revuz D , Yor M . Continuous martingales and Brownian motion. Berlin:

Springer; 1999 . [21] Samko SG , Kilbas AA , Maritchev DI . Integrals and derivatives of the fractional

order and some of their applications. Amsterdam: Gordon and Breach; 1993 . 22] Xu L . Ergodicity of the stochastic real Ginzburg–Landau equation driven by

α-stable noises. Stochastic Process Appl 2013;123:3710–36 .

23] Zhang X . Derivative formulas and gradient estimates for SDEs driven byα-stable processes. Stochastic Process Appl 2013;123:1213–28 .

本文献由“学霸图书馆-文献云下载”收集自网络,仅供学习交流使用。

学霸图书馆(www.xuebalib.com)是一个“整合众多图书馆数据库资源,

提供一站式文献检索和下载服务”的24 小时在线不限IP

图书馆。

图书馆致力于便利、促进学习与科研,提供最强文献下载服务。

图书馆导航:

图书馆首页 文献云下载 图书馆入口 外文数据库大全 疑难文献辅助工具