Copyright © 2005 Thomson Business & Professional Publishing.All rights reserved.

ROBERT L. MATHIS

JOHN H. JACKSON

PowerPoint Presentation by Charlie CookThe University of West Alabama

Compensation StrategiesCompensation Strategiesand Practicesand PracticesCompensation StrategiesCompensation Strategiesand Practicesand Practices

Chapter 12Chapter 12

SECTION 4SECTION 4Compensating Compensating

Human ResourcesHuman Resources

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–2

Learning ObjectivesLearning ObjectivesLearning ObjectivesLearning Objectives

• After you have read this chapter, you should be able to: Identify the two general types of compensation and

the components of each.Discuss four issues of strategic compensation design.List the basic provisions of the Fair Labor Standards

Act (FLSA).Describe the two means of valuing jobs.Outline the process of building a base pay system.Explain two ways individual pay increases are

determined.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–3

Nature of CompensationNature of CompensationNature of CompensationNature of Compensation

• Types of Rewards Intrinsic

Intangible, psychological and social effects of compensation

Extrinsic Tangible, monetary and nonmonetary effects of

compensation

• Types of CompensationDirect compensation

The employer exchanges monetary rewards for work done.

Indirect compensation Employer-provided benefits—like health insurance—that are

provide employees for being a member of the organization.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–4

Components of a Compensation SystemComponents of a Compensation SystemComponents of a Compensation SystemComponents of a Compensation System

Figure 12–1

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–5

Direct CompensationDirect CompensationDirect CompensationDirect Compensation

Base PayBase PayBase PayBase Pay

SalarySalarySalarySalary

WagesWagesWagesWages

The basic monetary compensation that an employee The basic monetary compensation that an employee receives, usually as a wage or salary.receives, usually as a wage or salary.

The basic monetary compensation that an employee The basic monetary compensation that an employee receives, usually as a wage or salary.receives, usually as a wage or salary.

Payments calculated on the amount of time worked.Payments calculated on the amount of time worked.Payments calculated on the amount of time worked.Payments calculated on the amount of time worked.

Consistent payments made each period regardless Consistent payments made each period regardless of the number of hours worked in the period.of the number of hours worked in the period.

Consistent payments made each period regardless Consistent payments made each period regardless of the number of hours worked in the period.of the number of hours worked in the period.

Variable Variable PayPay

Variable Variable PayPay

Compensation linked to individual, team, or Compensation linked to individual, team, or organizational performance.organizational performance.

Compensation linked to individual, team, or Compensation linked to individual, team, or organizational performance.organizational performance.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–6

Typical Division of HR Responsibilities: CompensationTypical Division of HR Responsibilities: CompensationTypical Division of HR Responsibilities: CompensationTypical Division of HR Responsibilities: Compensation

Figure 12–2

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–7

Strategic CompensationStrategic CompensationStrategic CompensationStrategic Compensation

• Objectives of a Strategically Supportive Compensation System:

Legal compliance with all appropriate laws and regulations

Cost effectiveness for the organization

Internal, external, and individual equity for employees

Performance enhancement for the organization

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–8

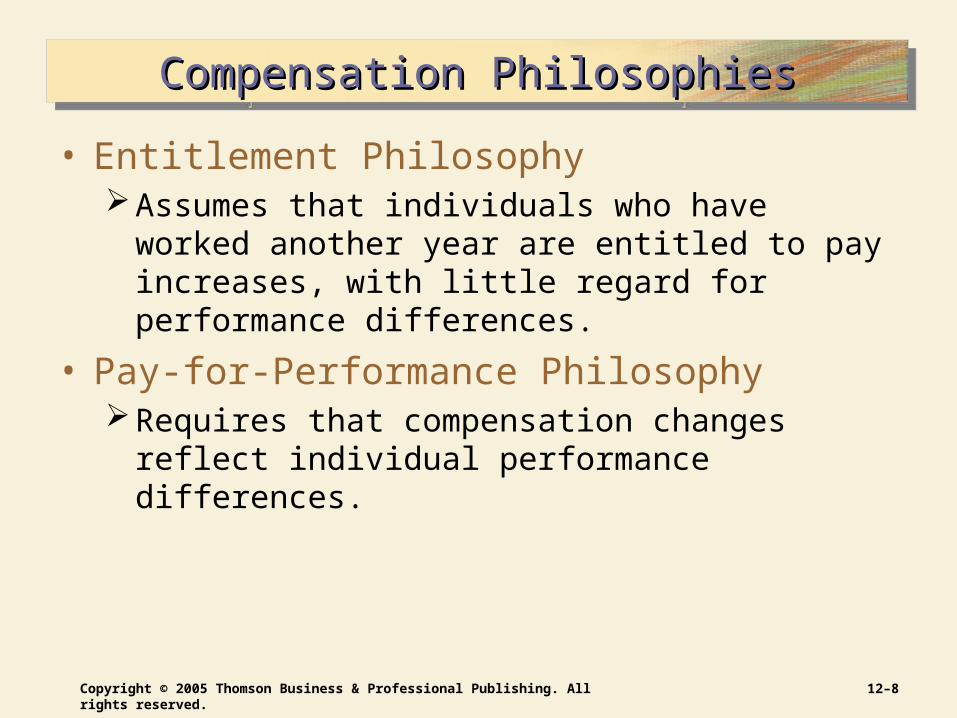

Compensation PhilosophiesCompensation PhilosophiesCompensation PhilosophiesCompensation Philosophies

• Entitlement PhilosophyAssumes that individuals who have worked another

year are entitled to pay increases, with little regard for performance differences.

• Pay-for-Performance PhilosophyRequires that compensation changes reflect individual

performance differences.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–9

Continuum of Compensation PhilosophiesContinuum of Compensation PhilosophiesContinuum of Compensation PhilosophiesContinuum of Compensation Philosophies

Figure 12–3

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–10

Compensation ApproachesCompensation ApproachesCompensation ApproachesCompensation Approaches

Figure 12–4

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–11

HR Metrics for CompensationHR Metrics for CompensationHR Metrics for CompensationHR Metrics for Compensation

Figure 12–5

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–12

Compensation System Design IssuesCompensation System Design IssuesCompensation System Design IssuesCompensation System Design Issues

ExpatriatesExpatriatesExpatriatesExpatriates

Host-Country Host-Country NationalsNationals

Host-Country Host-Country NationalsNationals

Third-Country Third-Country NationalsNationals

Third-Country Third-Country NationalsNationals

Global Global Compensation Compensation

IssuesIssues

Global Global Compensation Compensation

IssuesIssues

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–13

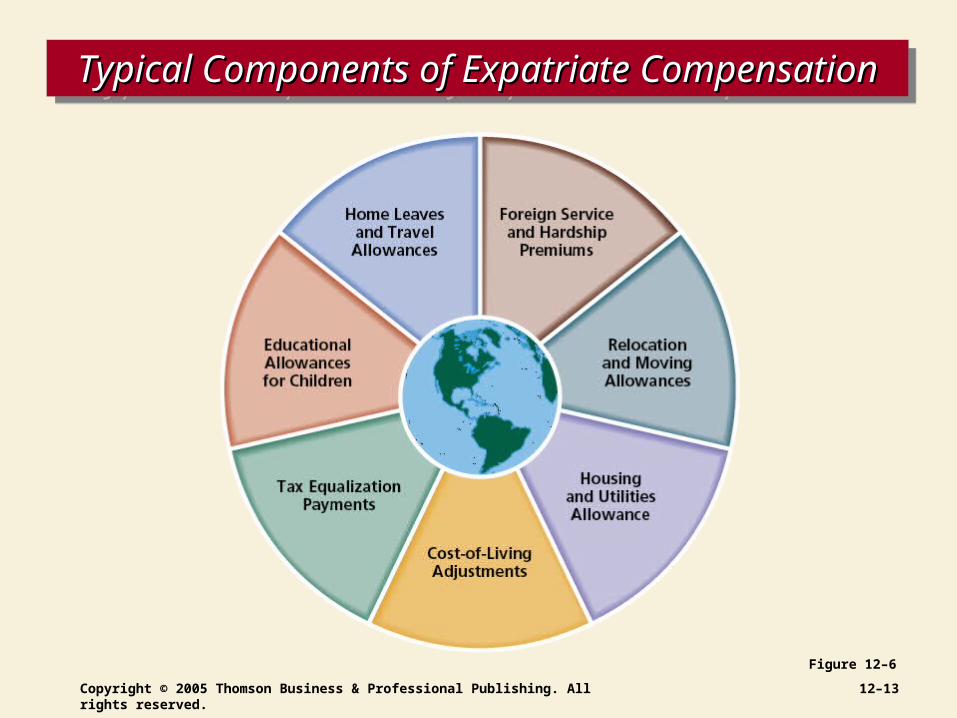

Typical Components of Expatriate CompensationTypical Components of Expatriate CompensationTypical Components of Expatriate CompensationTypical Components of Expatriate Compensation

Figure 12–6

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–14

Global Compensation ApproachesGlobal Compensation ApproachesGlobal Compensation ApproachesGlobal Compensation Approaches

• Balance Sheet Approach Compensation plan that equalizes cost differences between

identical international and home-country assignments.

• Global Market Approach Compensation plan that attempts to be more comprehensive in

providing base pay, incentives, benefits, and relocation expenses regardless of the country to which the employee is assigned.

• Tax Equalization Plan Compensation plan used to protect expatriates from negative tax

consequences.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–15

Compensation Quartile StrategiesCompensation Quartile StrategiesCompensation Quartile StrategiesCompensation Quartile Strategies

Figure 12–7

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–16

Market Competitiveness and Compensation Market Competitiveness and Compensation Market Competitiveness and Compensation Market Competitiveness and Compensation

Lead the Lead the MarketMarket

Lead the Lead the MarketMarket

Lag the Lag the MarketMarket

Lag the Lag the MarketMarket

Meet the Meet the MarketMarket

Meet the Meet the MarketMarket

Paying for higher qualified, more productive workers.Paying for higher qualified, more productive workers.Paying for higher qualified, more productive workers.Paying for higher qualified, more productive workers.

Attempting to balance employer costs and the need Attempting to balance employer costs and the need to attract and retain employees.to attract and retain employees.

Attempting to balance employer costs and the need Attempting to balance employer costs and the need to attract and retain employees.to attract and retain employees.

Paying all that the firm can afford. Taking advantage Paying all that the firm can afford. Taking advantage of the abundant supply of potential employees in a of the abundant supply of potential employees in a loose labor market.loose labor market.

Paying all that the firm can afford. Taking advantage Paying all that the firm can afford. Taking advantage of the abundant supply of potential employees in a of the abundant supply of potential employees in a loose labor market.loose labor market.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–17

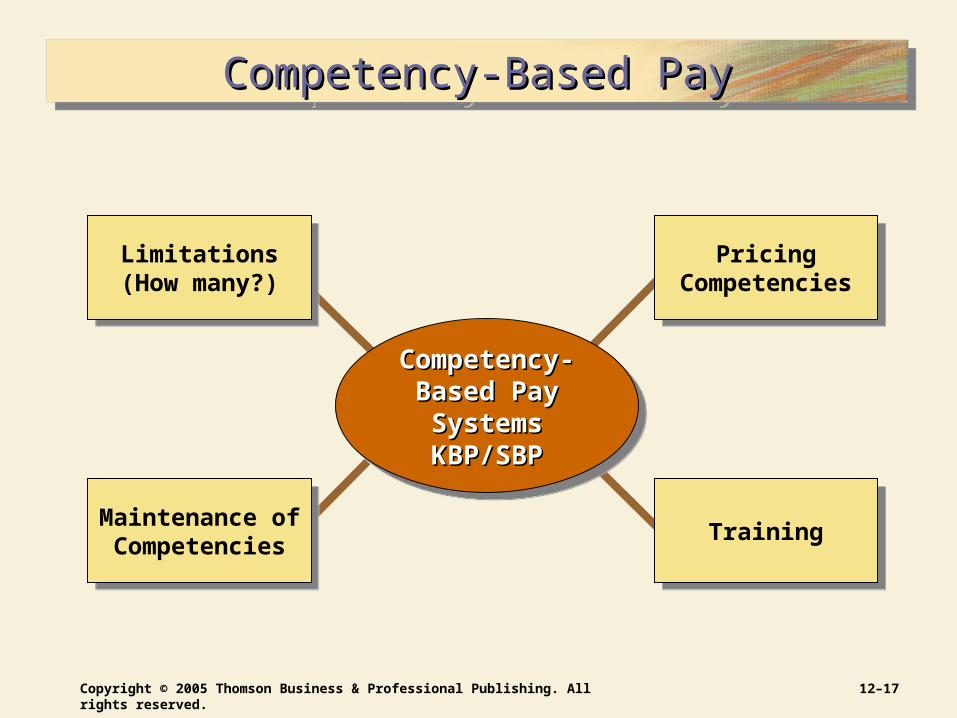

Competency-Based PayCompetency-Based PayCompetency-Based PayCompetency-Based Pay

Maintenance ofCompetencies

Maintenance ofCompetencies

Limitations(How many?)

Limitations(How many?)

PricingCompetencies

PricingCompetencies

TrainingTraining

Competency-Competency-Based Pay Based Pay SystemsSystemsKBP/SBPKBP/SBP

Competency-Competency-Based Pay Based Pay SystemsSystemsKBP/SBPKBP/SBP

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–18

Individual vs. Team RewardsIndividual vs. Team RewardsIndividual vs. Team RewardsIndividual vs. Team Rewards

Distribute variable rewards at the team levelDistribute variable rewards at the team levelDistribute variable rewards at the team levelDistribute variable rewards at the team level

Make system simple and understandable.Make system simple and understandable.Make system simple and understandable.Make system simple and understandable.

Using Team-Based Reward SystemsUsing Team-Based Reward SystemsUsing Team-Based Reward SystemsUsing Team-Based Reward Systems

Use skill-based pay for the base.Use skill-based pay for the base.Use skill-based pay for the base.Use skill-based pay for the base.

Use variable pay based on business entity performanceUse variable pay based on business entity performanceUse variable pay based on business entity performanceUse variable pay based on business entity performance

Maintain a high degree of employee involvementMaintain a high degree of employee involvementMaintain a high degree of employee involvementMaintain a high degree of employee involvement

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–19

Perceptions of Pay FairnessPerceptions of Pay FairnessPerceptions of Pay FairnessPerceptions of Pay Fairness

EquityEquityEquityEquity

InternalInternalEquityEquity

InternalInternalEquityEquity

ExternalExternalEquityEquity

ExternalExternalEquityEquity

The perceived fairness between what a person does The perceived fairness between what a person does (inputs) and what the person receives (outcomes).(inputs) and what the person receives (outcomes).

The perceived fairness between what a person does The perceived fairness between what a person does (inputs) and what the person receives (outcomes).(inputs) and what the person receives (outcomes).

Employee compensation viewed as equitable in relation to the Employee compensation viewed as equitable in relation to the compensation of employees performing similar jobs in other compensation of employees performing similar jobs in other organizations.organizations.

Employee compensation viewed as equitable in relation to the Employee compensation viewed as equitable in relation to the compensation of employees performing similar jobs in other compensation of employees performing similar jobs in other organizations.organizations.

Employees receive compensation in relation to the knowledge, Employees receive compensation in relation to the knowledge, skills, and abilities they use in their jobs as well as their skills, and abilities they use in their jobs as well as their responsibilities and accomplishments.responsibilities and accomplishments.

Employees receive compensation in relation to the knowledge, Employees receive compensation in relation to the knowledge, skills, and abilities they use in their jobs as well as their skills, and abilities they use in their jobs as well as their responsibilities and accomplishments.responsibilities and accomplishments.

Procedural JusticeProcedural JusticeProcedural JusticeProcedural Justice Perceived fairness of the process and proceduresPerceived fairness of the process and proceduresused to make decisions about employees.used to make decisions about employees.

Perceived fairness of the process and proceduresPerceived fairness of the process and proceduresused to make decisions about employees.used to make decisions about employees.

Distributive JusticeDistributive JusticeDistributive JusticeDistributive Justice Perceived fairness in the distribution of outcomes.Perceived fairness in the distribution of outcomes.Perceived fairness in the distribution of outcomes.Perceived fairness in the distribution of outcomes.

Pay Openness/Pay Openness/SecrecySecrecy

Pay Openness/Pay Openness/SecrecySecrecy

The degree of openness or secrecy that an organization The degree of openness or secrecy that an organization allows regarding its pay system.allows regarding its pay system.

The degree of openness or secrecy that an organization The degree of openness or secrecy that an organization allows regarding its pay system.allows regarding its pay system.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–20

Equity Considerations in CompensationEquity Considerations in CompensationEquity Considerations in CompensationEquity Considerations in Compensation

Figure 12–8

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–21

Fair Labor Standards Act (FSLA) of 1938Fair Labor Standards Act (FSLA) of 1938Fair Labor Standards Act (FSLA) of 1938Fair Labor Standards Act (FSLA) of 1938

Provisions of the Act Provisions of the Act Provisions of the Act Provisions of the Act

Minimum wage requirement sets wage floorMinimum wage requirement sets wage floorMinimum wage requirement sets wage floorMinimum wage requirement sets wage floor

Child labor (under 14 years old) is prohibitedChild labor (under 14 years old) is prohibitedChild labor (under 14 years old) is prohibitedChild labor (under 14 years old) is prohibited

Requires overtime payments for non-exempt employeesRequires overtime payments for non-exempt employeesRequires overtime payments for non-exempt employeesRequires overtime payments for non-exempt employees

Exempts highly-paid computer workersExempts highly-paid computer workersExempts highly-paid computer workersExempts highly-paid computer workers

Requires overtime (1Requires overtime (1½) pay for hours over 40 hours½) pay for hours over 40 hoursRequires overtime (1Requires overtime (1½) pay for hours over 40 hours½) pay for hours over 40 hours

Requires compensatory time at overtime (1Requires compensatory time at overtime (1½) pay rates½) pay rates Requires compensatory time at overtime (1Requires compensatory time at overtime (1½) pay rates½) pay rates

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–22

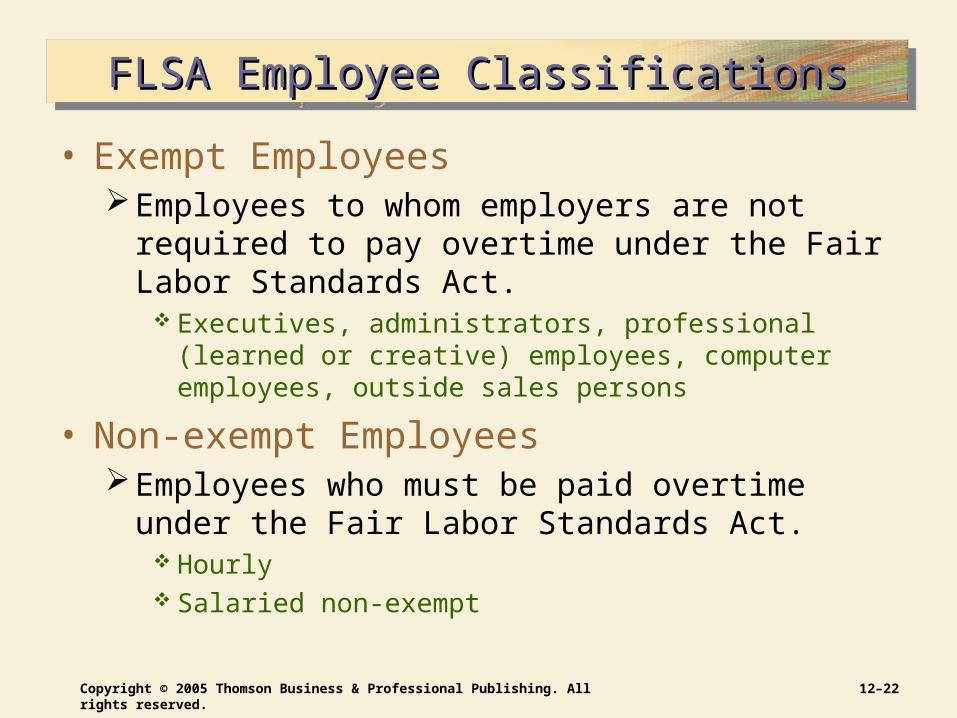

FLSA Employee ClassificationsFLSA Employee ClassificationsFLSA Employee ClassificationsFLSA Employee Classifications

• Exempt EmployeesEmployees to whom employers are not required to

pay overtime under the Fair Labor Standards Act. Executives, administrators, professional (learned or creative)

employees, computer employees, outside sales persons

• Non-exempt EmployeesEmployees who must be paid overtime under the Fair

Labor Standards Act. Hourly Salaried non-exempt

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–23

FLSA Wage ProvisionsFLSA Wage ProvisionsFLSA Wage ProvisionsFLSA Wage Provisions

• OvertimeNon-exempt employees must be paid overtime pay

(one and one-half the regular pay rate) for all hours worked over 40 regular hours in a workweek (168 hours—7days x 24 hours).

• Compensatory Time Off (Comp Time)Hours off regular work time given to an employee in

lieu of payment for extra time worked. Compensatory hours off must be awarded at rate of one and

one-half times hours worked over 40 hours.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–24

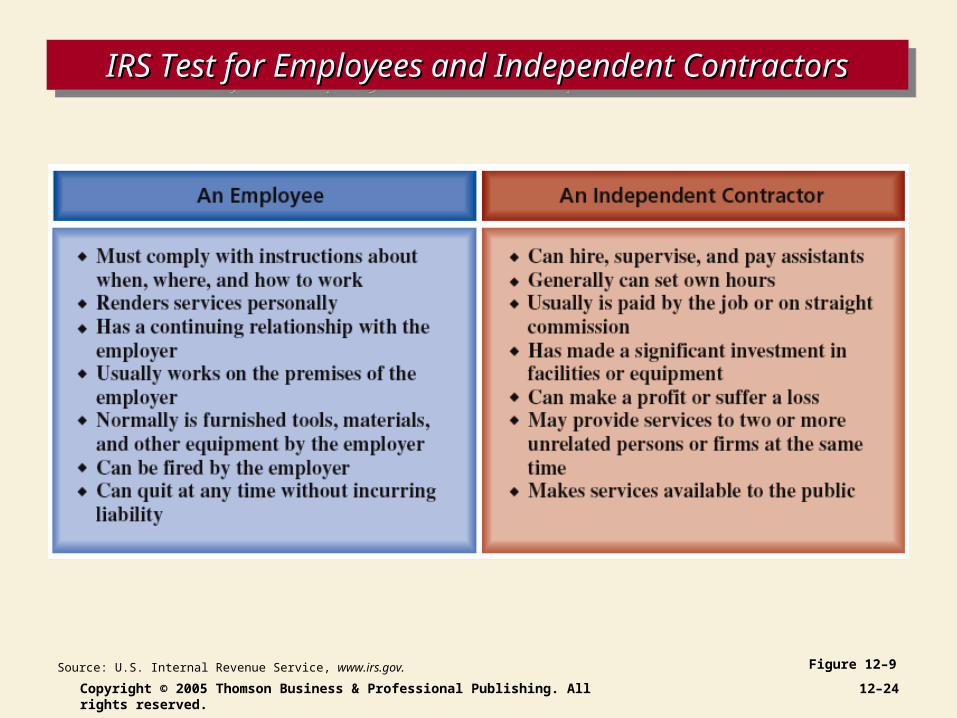

IRS Test for Employees and Independent ContractorsIRS Test for Employees and Independent ContractorsIRS Test for Employees and Independent ContractorsIRS Test for Employees and Independent Contractors

Figure 12–9Source: U.S. Internal Revenue Service, www.irs.gov.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–25

Other Laws Affecting CompensationOther Laws Affecting CompensationOther Laws Affecting CompensationOther Laws Affecting Compensation

• Davis-Bacon Act of 1931Required payment of “prevailing wage” by firms

engaged in federal construction projects.

• Walsh-Healy Public Contracts Act and the McNamara-O’Hara Service Contract ActExtended the payment of “prevailing wage” to service

contracts

Required overtime payment for any employee hours worked over eight hours in one day; applies only to to federal contracts, not the private sector.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–26

Legislation on Equal Pay and Pay EquityLegislation on Equal Pay and Pay EquityLegislation on Equal Pay and Pay EquityLegislation on Equal Pay and Pay Equity

• Equal Pay Act of 1963Requires that men and women be paid the same for

performing substantially similar jobs with limited non-gender exceptions (e.g., merit and seniority).

• Pay Equity (or Comparable Worth)Similarity in pay for all jobs requiring comparable level

of knowledge, skills, and abilities, even if actual duties and market rates differ significantly.

• GarnishmentA court action in which a portion of an employee’s

wages is set aside to pay a debt owed a creditor.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–27

Compensation Compensation Administration Administration

ProcessProcess

Compensation Compensation Administration Administration

ProcessProcess

Figure 12–10

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–28

Development of a Base Pay SystemDevelopment of a Base Pay SystemDevelopment of a Base Pay SystemDevelopment of a Base Pay System

• Job EvaluationFormal, systematic means to identify the relative

worth of jobs within an organization. Evaluating every job in the organization on:

Knowledge, skills, and abilities required Nature of job tasks, duties, responsibilities, and

competencies Difficulty of the job, including the physical and mental

demands

• Compensable factorFactor that identifies a job value commonly present

throughout a group of jobs.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–29

Examples of Compensable Factors Examples of Compensable Factors for Different Job Familiesfor Different Job Families

Examples of Compensable Factors Examples of Compensable Factors for Different Job Familiesfor Different Job Families

Figure 12–11

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–30

Job EvaluationJob EvaluationJob EvaluationJob Evaluation

FactorFactorComparisonComparison

FactorFactorComparisonComparison

RankingRankingRankingRanking ClassificationClassificationClassificationClassification

PointPointMethodMethod

PointPointMethodMethod

Job Job Evaluation Evaluation MethodsMethods

Job Job Evaluation Evaluation MethodsMethods

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–31

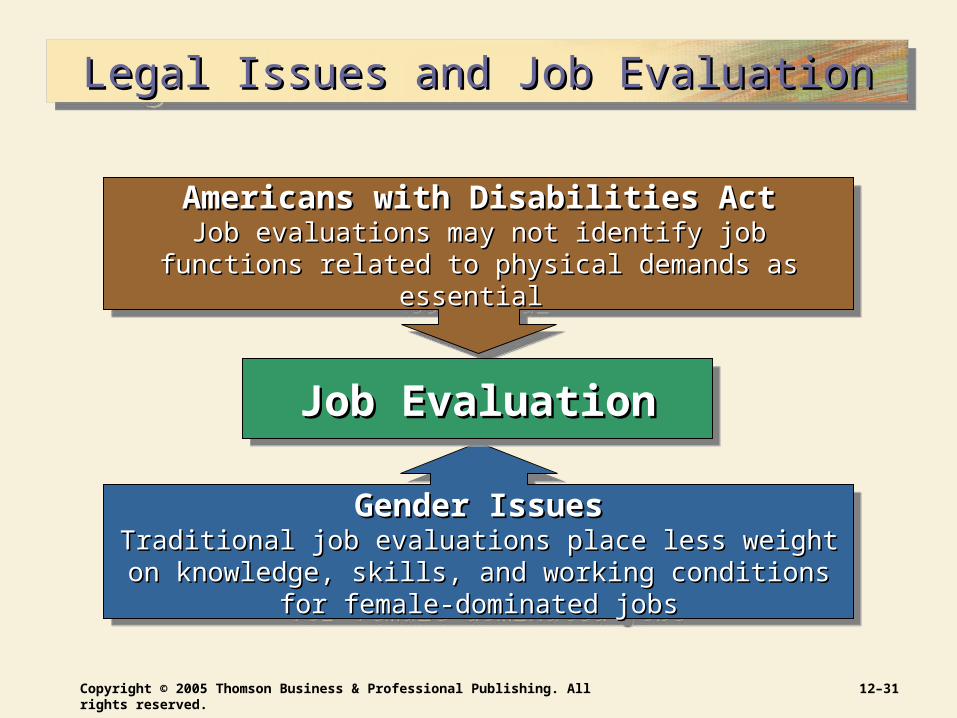

Legal Issues and Job EvaluationLegal Issues and Job EvaluationLegal Issues and Job EvaluationLegal Issues and Job Evaluation

Americans with Disabilities ActAmericans with Disabilities ActJob evaluations may not identify job functions related Job evaluations may not identify job functions related

to physical demands as essential to physical demands as essential

Americans with Disabilities ActAmericans with Disabilities ActJob evaluations may not identify job functions related Job evaluations may not identify job functions related

to physical demands as essential to physical demands as essential

Gender IssuesGender IssuesTraditional job evaluations place less weight on Traditional job evaluations place less weight on

knowledge, skills, and working conditions for female-knowledge, skills, and working conditions for female-dominated jobsdominated jobs

Gender IssuesGender IssuesTraditional job evaluations place less weight on Traditional job evaluations place less weight on

knowledge, skills, and working conditions for female-knowledge, skills, and working conditions for female-dominated jobsdominated jobs

Job EvaluationJob EvaluationJob EvaluationJob Evaluation

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–32

Valuing Jobs Using Market PricingValuing Jobs Using Market PricingValuing Jobs Using Market PricingValuing Jobs Using Market Pricing

• Market PricingUse of pay survey data to identify the relative value of

jobs based on what other employers pay for similar jobs.

• Advantages of Market PricingTies organizational pay levels to what is actually

occurring in the market, without being distorted by “internal” job evaluation.

Communicates to employees that the compensation system is “market linked,” rather than distorted by internal issues.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–33

Valuing Jobs Using Market Pricing (cont’d)Valuing Jobs Using Market Pricing (cont’d)Valuing Jobs Using Market Pricing (cont’d)Valuing Jobs Using Market Pricing (cont’d)

• Disadvantages of Market Pricing It relies on market survey data that is limited or may

have been gathered in methodologically sound ways.

The responsibilities of a specific job in a company may be somewhat different from those of the “matching” job identified in the survey.

The market data’s scope (range of sources) is another concern.

Tying pay levels to market data can lead to wide fluctuations based on market conditions.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–34

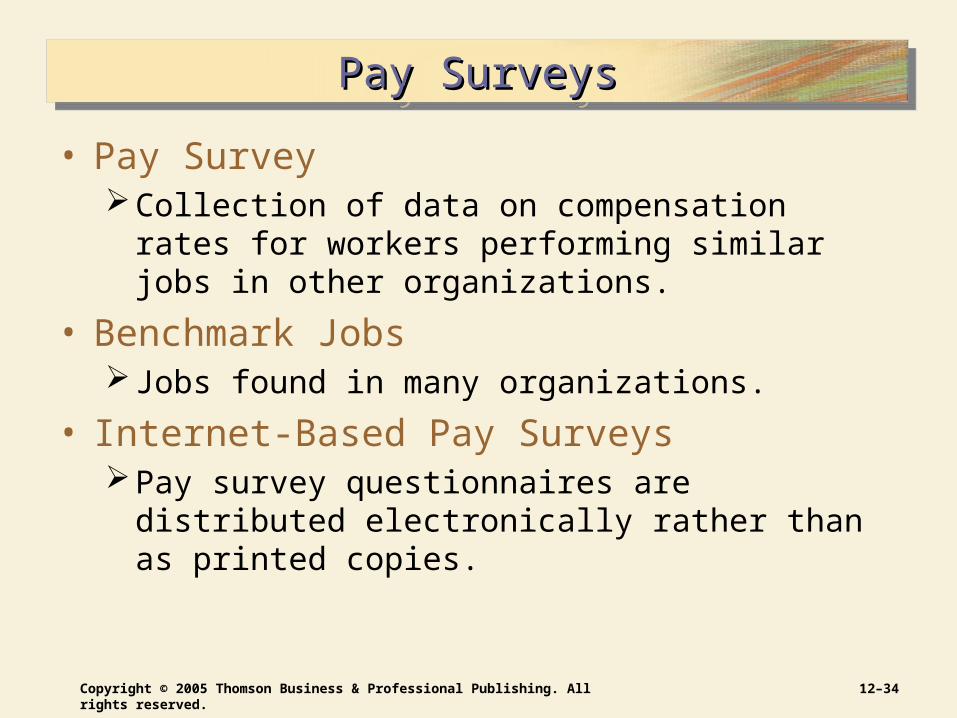

Pay SurveysPay SurveysPay SurveysPay Surveys

• Pay SurveyCollection of data on compensation rates for workers

performing similar jobs in other organizations.

• Benchmark JobsJobs found in many organizations.

• Internet-Based Pay SurveysPay survey questionnaires are distributed

electronically rather than as printed copies.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–35

Using Pay SurveysUsing Pay SurveysUsing Pay SurveysUsing Pay Surveys

MethodologyMethodologyMethodologyMethodology

ParticipantsParticipantsParticipantsParticipants Broad-basedBroad-basedBroad-basedBroad-based

TimelinessTimelinessTimelinessTimelinessSurvey Data Survey Data RelevanceRelevance

Survey Data Survey Data RelevanceRelevanceJob MatchesJob MatchesJob MatchesJob Matches

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–36

Developing Pay SurveysDeveloping Pay SurveysDeveloping Pay SurveysDeveloping Pay Surveys

Select Employers with Comparable JobsSelect Employers with Comparable JobsSelect Employers with Comparable JobsSelect Employers with Comparable Jobs

Determine Jobs to be SurveyedDetermine Jobs to be SurveyedDetermine Jobs to be SurveyedDetermine Jobs to be Surveyed

Decide What Information Is NeededDecide What Information Is NeededDecide What Information Is NeededDecide What Information Is Needed

Conduct SurveyConduct SurveyConduct SurveyConduct Survey

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–37

Pay StructuresPay StructuresPay StructuresPay Structures

• Job FamilyA group of jobs having common organizational

characteristics.

• Common Pay StructuresHourly and salariedOffice, plant, technical, professional, managerialClerical, information technology, professional,

supervisory, management, and executive

• Pay GradesGroupings of individual jobs having approximately the

same job worth.

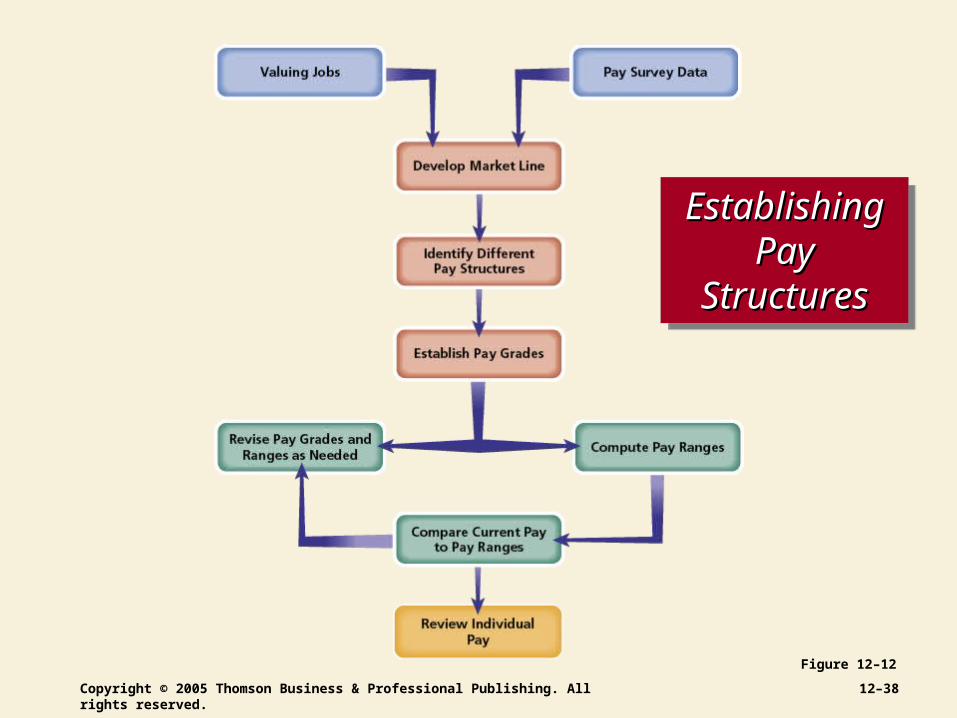

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–38

Establishing Establishing Pay Pay

StructuresStructures

Establishing Establishing Pay Pay

StructuresStructures

Figure 12–12

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–39

Market-Banded Pay Grades for Community BankMarket-Banded Pay Grades for Community BankMarket-Banded Pay Grades for Community BankMarket-Banded Pay Grades for Community Bank

Figure 12–13

*Computed by averaging the pay survey summary data for the jobs in each pay grade.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–40

Pay Structures (cont’d)Pay Structures (cont’d)Pay Structures (cont’d)Pay Structures (cont’d)

• Market BandingGrouping jobs into pay grades based on similar

market survey amounts.

• Market LineGraph line that shows the relationship between job

value as determined by job evaluation points and job value as determined by pay survey rates.

Shows the distribution of pay for the surveyed jobs, allowing a linear trend line to be developed by the least-squares regression method.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–41

Pay RangesPay RangesPay RangesPay Ranges

• BroadbandingThe practice of using fewer pay grades having

broader pay ranges that in traditional systems.Benefits

Encourages horizontal movement of employees

Is consistent with trend towards flatter organizations

Creates a more flexible organization

Encourages competency development

Emphasizes career development

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–42

Example of Example of Pay Grades Pay Grades

and Pay and Pay RangesRanges

Example of Example of Pay Grades Pay Grades

and Pay and Pay RangesRanges

Figure 12–14

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–43

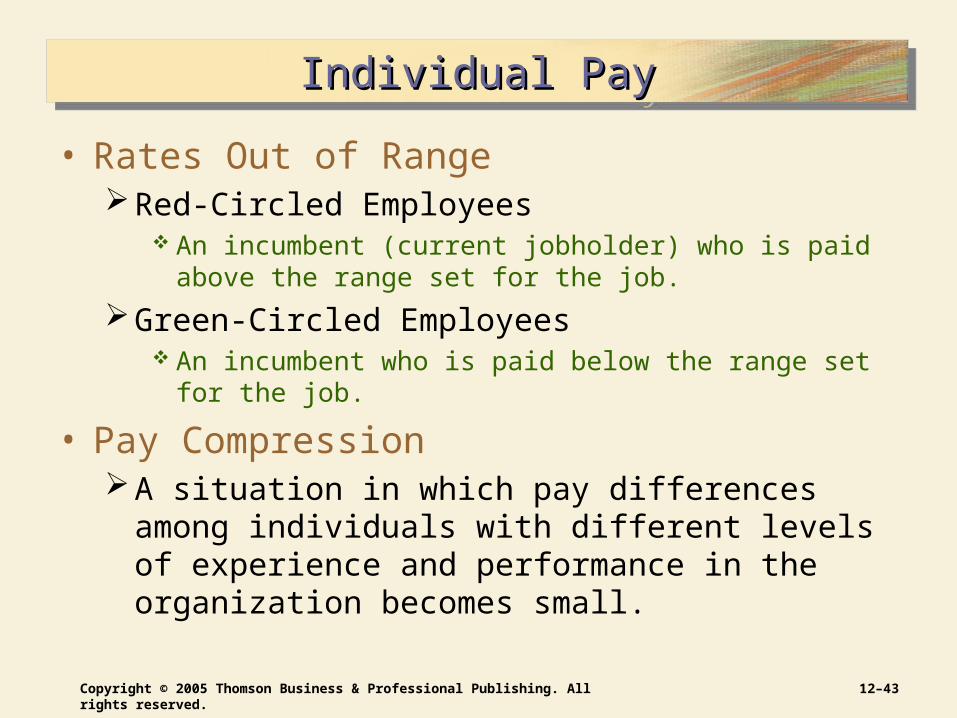

Individual PayIndividual PayIndividual PayIndividual Pay

• Rates Out of RangeRed-Circled Employees

An incumbent (current jobholder) who is paid above the range set for the job.

Green-Circled Employees An incumbent who is paid below the range set for the job.

• Pay CompressionA situation in which pay differences among individuals

with different levels of experience and performance in the organization becomes small.

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–44

Pay Adjustment MatrixPay Adjustment MatrixPay Adjustment MatrixPay Adjustment Matrix

• Compa-ratioThe pay level divided by the midpoint of the pay

range.

ratio)-(Compa 110100(midpoint) 15.00

pay)(current $16.50 Employee R

ratio)-(Compa 87 100(midpoint) 15.00

pay)(current $13.05 Employee J

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–45

Pay Adjustment MatrixPay Adjustment MatrixPay Adjustment MatrixPay Adjustment Matrix

Figure 12–15

Copyright © 2005 Thomson Business & Professional Publishing. All rights reserved. 12–46

Determining Pay IncreasesDetermining Pay IncreasesDetermining Pay IncreasesDetermining Pay Increases

• Seniority Time spent in an organization or on a particular job that is used

to determine eligibility for organizational rewards and benefits.

• Cost-of-Living Adjustments (COLA) A percentage increase in wages to maintain real wages in a

period of economic inflation.

Adjustments are tied to changes in an economic measure (e.g., the Consumer Price Index).

• Lump-Sum Increases (LSI) A one-time payment of all or part of a yearly pay increase that

does not increase base wages.