Chapter 5

Accounting Entries in Special Journal and Subsidiary Ledger

1

Topics

1. Purchase Journal and A/P Subsidiary Ledger

2. Sales Journal and A/R Subsidiary Ledger

3. Cash Book

4. Cash Receipts Journal

5. Cash Payment Journal

Objectives

• Understand usefulness of special journals and subsidiary ledgers

• Record business transaction in the proper special journals and subsidiary ledgers

Accounting Record Process

2

General Journal General Ledger Trial Balance

General Journal

Special Journal

General Ledger (Control A/C)

Subsidiary Ledger (AP/AR)

Purchase Journal Sales Journal Cash Receipt Journal Cash Payment Journal

Chp 5

Why do we need special journal and subsidiary ledgers?

3

Usefulness of Special Journals and Subsidiary Ledgers

• Large entities usually have numbers of repeating transactions (e.g. sales,

purchases, payment, cash receipt)

• These transactions cause excessive accounting records in General Journal

• Free the general ledger of excessive details

• Show in a single account transactions affecting one customer or one creditor

• Help locate errors in individual accounts

• Make possible a division of labor in posting

Expanding the Special Journals

4

Special Journal is used to record similar types of transactions.

If a transaction cannot be recorded in a special journal, the company records it in the general journal.

Types of Ledgers

5

1. General Ledgers (GL)

o Recording business transaction from general journal (GJ)

o Summarizing the remaining amount of each account

o Posting each of general ledger to trial balance (TB)

o E.g. Accounts receivable, Accounts Payable

2. Subsidiary Ledgers

o Contains the details to support a general ledger control account

o Provide details of individual customers or individual creditors

Types of Ledgers

6

7

AC No.102

ACCOUNT NAME ACCOUNT NAME

25X9 25X9

Jun 1 B/F 500,000 - Jun 13 Sales Return and Allowance 50,000 -

26 Sales Journals 200,000 - 20 Cash Receipt Journal 350,000 -

31 Carry forward 300,000 -

Accounts Receivable (A/R)

Y/M/D DEBIT Y/M/D CREDIT

GENERAL LEDGER

R01Transactions Ref.

25X9

Jun 1 B/F 300,000 - 300,000 -

13 Sales Return and Allowance GJ1 - 50,000 - 250,000 -

20 Cash Receipt Journal CR1 150,000 - 100,000 -

R02

Transactions Ref.

25X9

Jun 1 B/F 200,000 - 200,000 -

26 Sales Journal S1 200,000 - 400,000 -

20 Cash Receipt Journal CR1 100,000 - 300,000 -

Company B

Y/M/D Debit Credit Balance

SUBSIDIARY LEDGER - Accounts Receivable

Y/M/D Debit Credit Balance

Company A

Special Journals

8

1. Purchase Journal

2. Sales Journal

3. Cash Book

4. Cash Receipt Journal

5. Cash Payment Journal

1. Purchase Journal

9

o Reference: “P”

o Used for “Credit Purchase of Goods or Inventories” ONLY

o Cash purchase will be recorded in Cash Payment Journal

o Not used to record purchase of non-current assets or other assets

o Supporting evidence: Invoice, Delivery Note, Purchase order

Example 1

10

ABC Company uses special journals and subsidiary journals to record business

transactions of the company. The following transactions occurs in June 25X9.

Jun 1 Purchase inventory 5,000 Baht on credit from Company X. Cash discount condition is 2/10, n/30. Attached invoice no. P2661

5 Purchase computer 15,000 Baht on credit from IT Company

9 Purchase inventory 7,000 Baht on credit from Company Y. Cash discount condition is 5/10, n/60. Attached invoice no. 4X910

14 Purchase inventory 15,000 Baht on credit from Company X. Cash discount condition is 2/10, n/30. Attached invoice no. T245

Y/M/D ACCOUNT NAME AC No. DEBIT CREDIT

25X9

Jun 5 Dr. Office equipment 111 15,000 -

Cr. Accounts Payable 201 15,000 -

Buy Computer on credit

GENERAL JOURNAL PAGE 1

11

Page_1_

Invoice

No.Creditor Name

Credit

TermRef.

25X9

Jun 1 P2661 Company X 2/10, n/30 P 5,000 -

9 4X910 Company Y 5/10, n/60 P 7,000 -

14 T245 Company Z 2/10, n/30 P 15,000 -

30 Dr. Purchase/ Cr. Accounts Payable 501/201 27,000 -

PURCHASE JOURNAL

BalanceY/M/D

AC No.501

ACCOUNT NAME ACCOUNT NAME

25X9

Jun 30 Purchase Journal 27,000 -

AC No.201

ACCOUNT NAME ACCOUNT NAME

25X9

Jun 30 Purchase Journal 27,000 -

Accounts Payable (A/P)

Y/M/D DEBIT Y/M/D CREDIT

GENERAL LEDGER

Purchase

Y/M/D DEBIT Y/M/D CREDIT

P01

Transactions Ref.

25X9

Jun 1 Purchase Journal P.1 5,000 - 5,000 -

P02Transactions Ref.

25X9

Jun 9 Purchase Journal P.1 7,000 - 7,000 -

P03Transactions Ref.

25X9

Jun 14 Purchase Journal P.1 15,000 - 15,000 -

Company ZY/M/D Debit Credit Balance

Balance

Company YY/M/D Debit Credit Balance

SUBSIDIARY LEDGER - Accounts Payable

Company X

Y/M/D Debit Credit

2. Sales Journal

12

o Reference: “S”

o Used for “Credit Sales of Goods or Products” ONLY

o Cash receipt will be recorded in Cash Receipt Journal

o Not used to record sales of non-current assets or other assets

o Supporting evidence: Invoice, Delivery Note, Billing Note

13

Page_1_

Invoice

No.Creditor Name

Credit

TermRef.

25X9

Jun 3 S7745 Company M 2/15, n/45 P 7,000 -

5 S7746 Company O 2/15, n/45 P 17,000 -

22 S7747 Company P 2/15, n/45 P 25,000 -

30 Dr. Accounts Receivable/ Cr. Sales 102/401 49,000 -

SALES JOURNAL

Y/M/D Balance

AC No.102

ACCOUNT NAME ACCOUNT NAME

25X9

Jun 30 Sales Journal 49,000 -

AC No. 401

ACCOUNT NAME ACCOUNT NAME

25X9

Jun 30 Sales Journal 49,000 -

Sales

Y/M/D DEBIT Y/M/D CREDIT

CREDIT

GENERAL LEDGER

Accounts Receivable

Y/M/D DEBIT Y/M/D

S01

Transactions Ref.

25X9

Jun 3 Sales Journal P.1 7,000 - 7,000 -

S02Transactions Ref.

25X9

Jun 5 Sales Journal P.1 17,000 - 17,000 -

S03Transactions Ref.

25X9

Jun 22 Sales Journal P.1 25,000 - 25,000 -

Company PY/M/D Debit Credit Balance

Y/M/D Debit Credit Balance

Y/M/D Debit Credit Balance

Company O

SUBSIDIARY LEDGER - Accounts Receivable

Company M

3. Cash Book

14

o Reference: “C”

o Contain all cash receipts and cash payment

o Similar with “General Ledger – Cash”

o Used in small entities with not many cash transaction

o Large entities need 2 cash books; cash receipt and cash payment

o At the end of month, net amount from cash book is posted to general

journal

Transaction A/C No.Transaction A/C No.

Y/M/DCash on

handDiscount

Y/M/D

Cash on

handDiscount

Cash at

Bank

Cash at

Bank

Transaction A/C No.Transaction A/C No.

Y/M/DCash at

Bank Y/M/D

Cash at

Bank

Cash on

hand

Cash on

hand

Transaction A/C No. Transaction A/C No. AmountY/M/D Amount Y/M/D

15

One-Column Cash Book

Two-Column Cash Book

Three-Column Cash Book

Payment

Cash outCash in

Receipt

Receipt Payment

4. Cash Receipt Journal

16

o Reference: “CR”

o Contain only cash receipt

o Used in Large entities with many cash receipt transaction

o At the end of month, net amount from cash receipt journal is posted

to general journal

17

Example: Cash receipt transactions of Acc-BA Company are as follows;

Jun 15 Receive 20,000 Baht check from sales to HH Company

Jun 21 Receive 5,000 Baht cash from sales to JJ Company

Jun 24 Receive cash from sales to PP Company on Jun 20th under cash discount condition 2/10, n/30.

Acc-BA Company receives cash 6,860 Baht and gives sales discount 140 Baht

Jun 25 Receive cash 3,000 Baht from office rental income

A/C NameA/C

No.

25X9

Jun 15 Receive check from sales AB457 20,000 20,000 -

Jun 21 Receive cash from sales AB449 5,000 - 5,000

Jun 24 Receive A/R - PP Company AB258 6,860 - 140 - 7,000 -

Jun 25 Receive cash from rental income AB445 3,000 Rental income 402 3,000 -

Jun 30 Total 14,860 - 20,000 - 140 - 7,000 - 25,000 - 3,000 -

Sales

Other accounts

Amount

Cash Receipt Journal

Y/M/D Transaction Ref.

Debit Credit

Cash on

hand

Cash at

Bank

Sales

Discount

Accounts

receivable

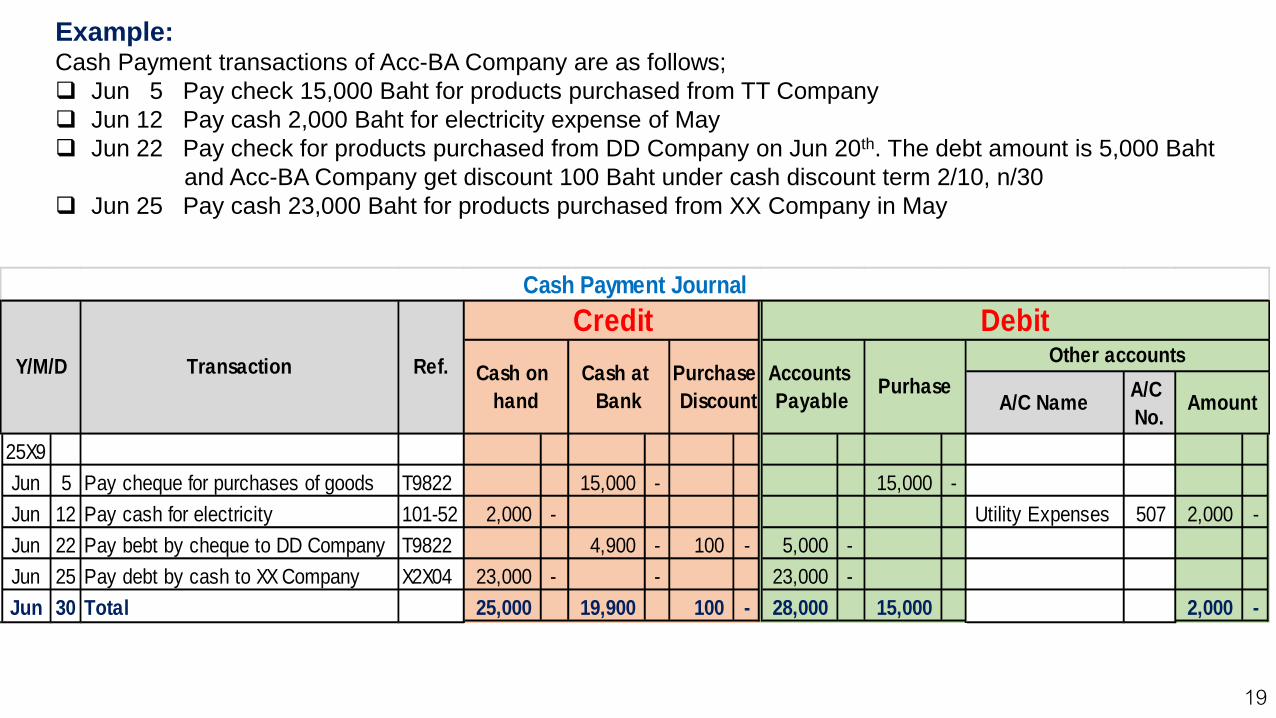

5. Cash Payment Journal

18

o Reference: “CP”

o Contain only cash payment

o Used in Large entities with many payment transaction

o At the end of month, net amount from cash payment journal is posted

to general journal

19

Example: Cash Payment transactions of Acc-BA Company are as follows;

Jun 5 Pay check 15,000 Baht for products purchased from TT Company

Jun 12 Pay cash 2,000 Baht for electricity expense of May

Jun 22 Pay check for products purchased from DD Company on Jun 20th. The debt amount is 5,000 Baht

and Acc-BA Company get discount 100 Baht under cash discount term 2/10, n/30

Jun 25 Pay cash 23,000 Baht for products purchased from XX Company in May

A/C NameA/C

No.

25X9

Jun 5 Pay cheque for purchases of goods T9822 15,000 - 15,000 -

Jun 12 Pay cash for electricity 101-52 2,000 - Utility Expenses 507 2,000 -

Jun 22 Pay bebt by cheque to DD Company T9822 4,900 - 100 - 5,000 -

Jun 25 Pay debt by cash to XX Company X2X04 23,000 - - 23,000 -

Jun 30 Total 25,000 19,900 100 - 28,000 15,000 2,000 -

Purchase

Discount

Ref.TransactionY/M/D

Credit Debit

Amount

Other accountsAccounts

PayablePurhase

Cash on

hand

Cash at

Bank

Cash Payment Journal