1

2

Chapter 9:

Long-Lived Assets and Cost

Allocation

3

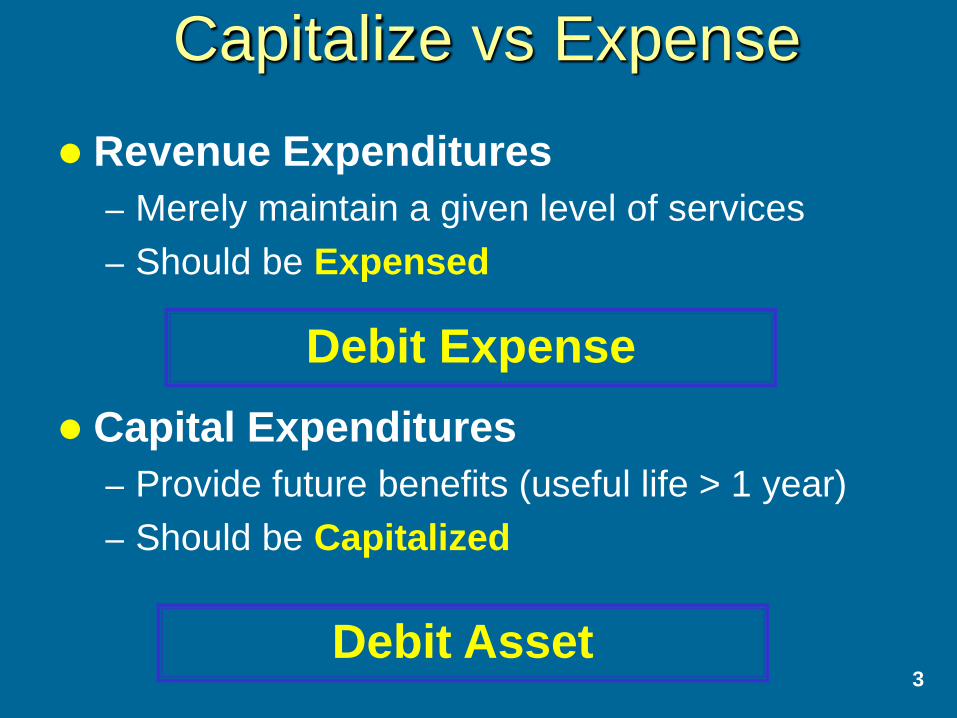

Capitalize vs Expense

Revenue Expenditures

– Merely maintain a given level of services

– Should be Expensed

Capital Expenditures

– Provide future benefits (useful life > 1 year)

– Should be Capitalized

Debit Expense

Debit Asset

4

Overview of Accounting for

Property, Plant, and

Equipment

5

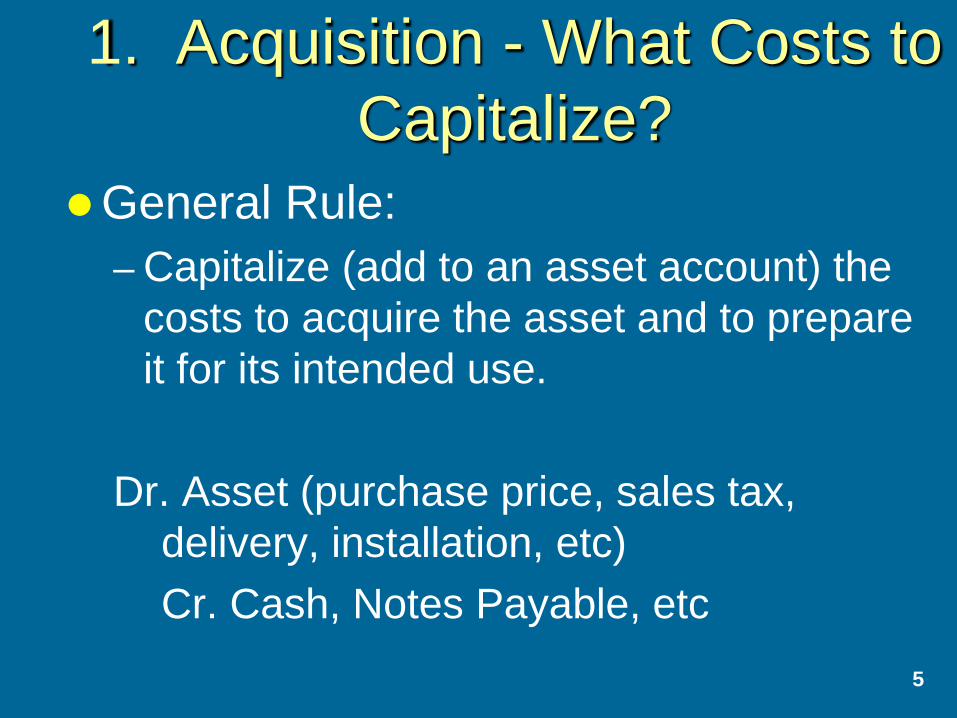

1. Acquisition - What Costs to

Capitalize?

General Rule:

– Capitalize (add to an asset account) the

costs to acquire the asset and to prepare

it for its intended use.

Dr. Asset (purchase price, sales tax,

delivery, installation, etc)

Cr. Cash, Notes Payable, etc

Land – Has indefinite life and therefore is not depreciated

– Historical Cost includes: Purchase price, Closing costs, Cost to get ready for intended

use (Note: Sale of salvaged materials reduces cost)

Land Improvements – Have definite life and therefore are depreciated

– Fences, walls, parking lots, driveways

Buildings – Have definite life and therefore are depreciated

– Proportionate share of purchase price, or construction cost, Closing Cost, Architect & Attorney fees

Machinery, Equipment, Furniture & Fixtures – Purchase price (net of cash discounts), Freight & handling,

Insurance while in transit, Installation

Self Constructed

Assets

What to Capitalize?

Direct Materials & Labor

Variable Overhead

Apply Fixed Overhead

Interest During Construction, if constructed

–for company’s own use

–by someone else and progress payments &/or

deposit are required

8

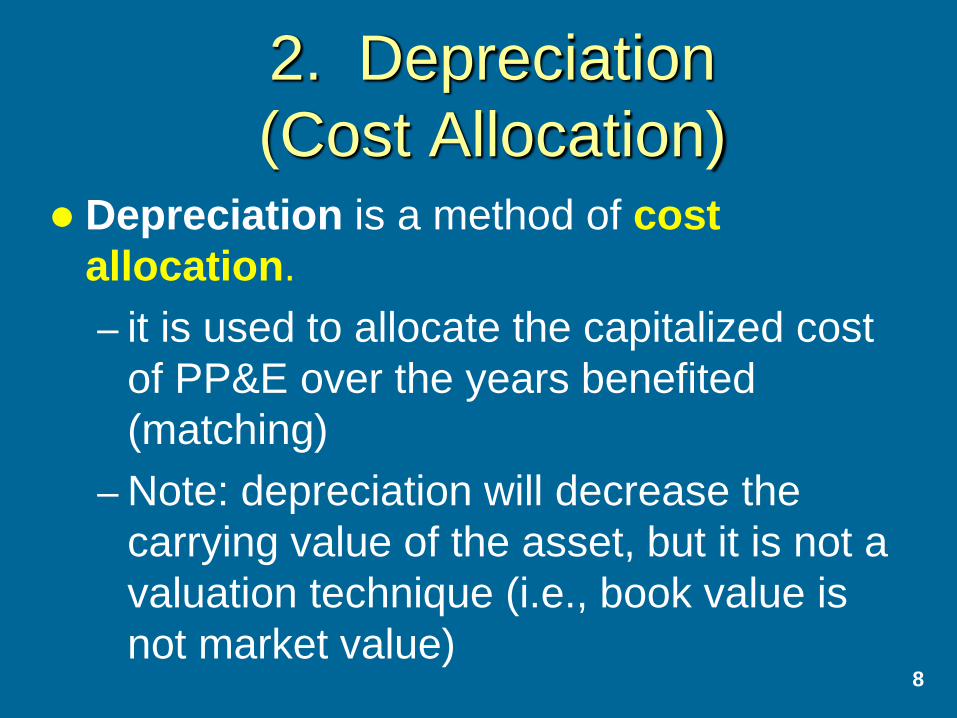

2. Depreciation

(Cost Allocation) Depreciation is a method of cost

allocation.

– it is used to allocate the capitalized cost

of PP&E over the years benefited

(matching)

– Note: depreciation will decrease the

carrying value of the asset, but it is not a

valuation technique (i.e., book value is

not market value)

9

2. Depreciation

(Cost Allocation)

Useful Life

Salvage Value

Depreciation methods

– (1) Activity (units-of-production)

– (2) Straight-line

– (3) Double-declining balance

– (4) 150 percent declining balance

– (5) Sum-of-the-years digits

– (6) MACRS (income tax depreciation)

– Under IFRS, depreciation accounting is very similar to US GAAP.

10

Class Example

Given the following information regarding an automobile purchased by the company on January 2, 2008:

Cost to acquire = $10,000

Estimated life = 4 years

Estimated miles = 100,000 miles

Salvage value = $2,000

Calculate depreciation expense for the first two years under each of the following methods.

11

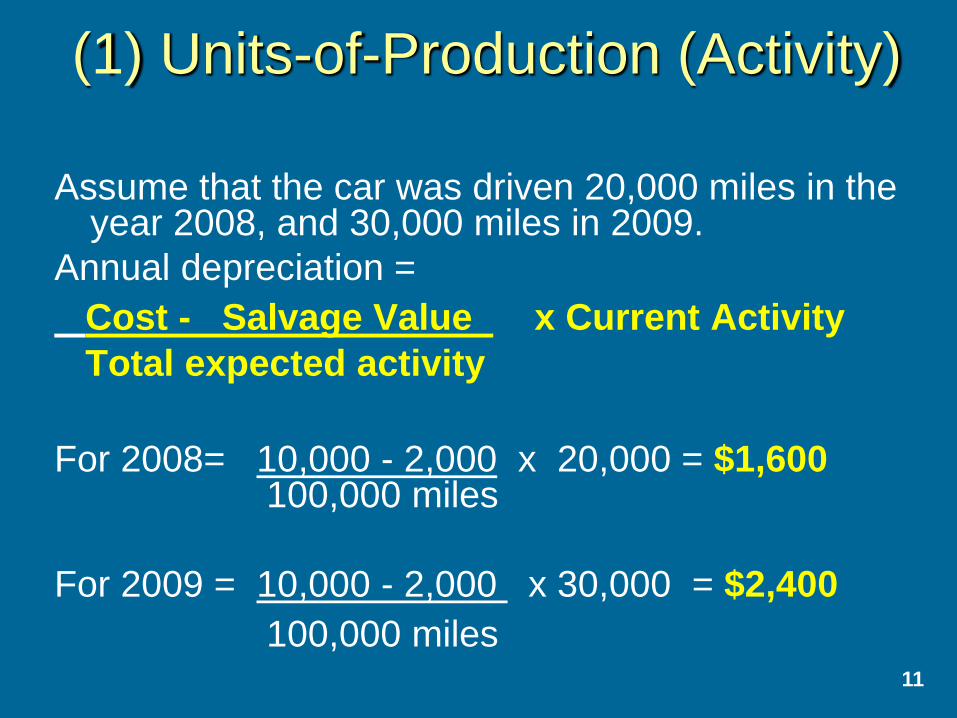

(1) Units-of-Production (Activity)

Assume that the car was driven 20,000 miles in the year 2008, and 30,000 miles in 2009.

Annual depreciation =

Cost - Salvage Value x Current Activity Total expected activity

For 2008= 10,000 - 2,000 x 20,000 = $1,600

100,000 miles

For 2009 = 10,000 - 2,000 x 30,000 = $2,400

100,000 miles

12

(2) Straight-Line

= $10,000 - $2,000 = $2,000 per year

4 years

Cost - Salvage

Estimated Life Annual depreciation =

13

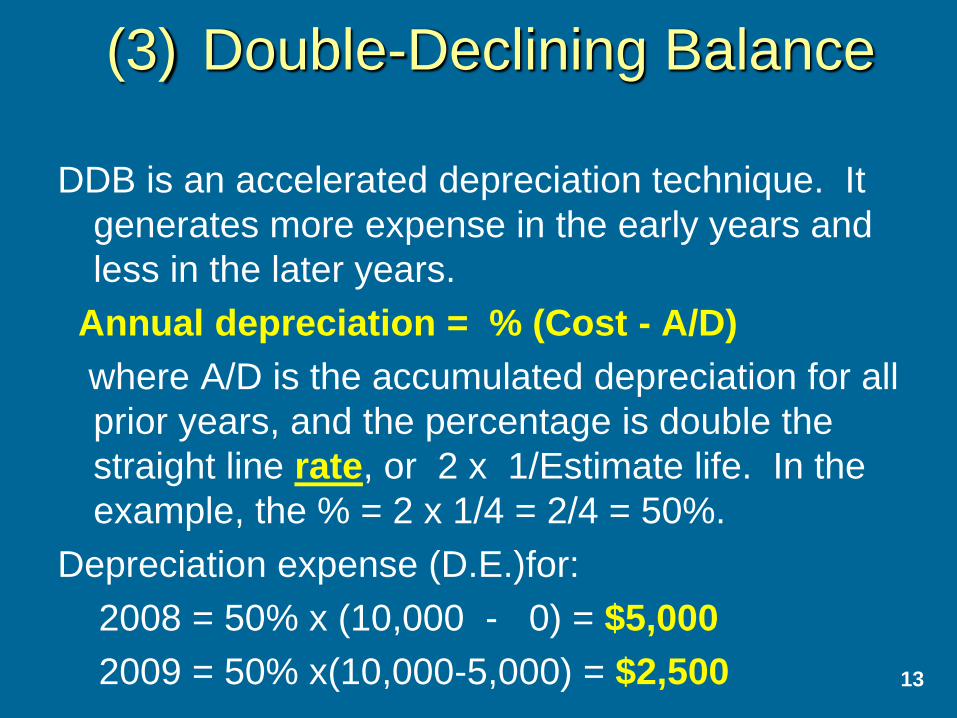

(3) Double-Declining Balance

DDB is an accelerated depreciation technique. It

generates more expense in the early years and

less in the later years.

Annual depreciation = % (Cost - A/D)

where A/D is the accumulated depreciation for all

prior years, and the percentage is double the

straight line rate, or 2 x 1/Estimate life. In the

example, the % = 2 x 1/4 = 2/4 = 50%.

Depreciation expense (D.E.)for:

2008 = 50% x (10,000 - 0) = $5,000

2009 = 50% x(10,000-5,000) = $2,500

14

(4) 150% Declining Balance

150%DB is another accelerated depreciation technique. It also generates more expense in the early years and less in the later years.

Annual depreciation = % (Cost - A/D)

where A/D is the accumulated depreciation for all prior years, and the percentage is 1.5 times the straight line rate, or

1.5 x 1/Estimate life. In the example, the % =

1.5 x 1/4 = 37.5%.

Depreciation expense (D.E.)for:

2008 = 37.5% x (10,000 - 0) = $3,750

2009 = 37.5% x(10,000-3,750) = $2,344

15

(5) Sum-of-the-years Digits SYD is another accelerated technique that calculates

more expense in early years and less in later years.

Annual depreciation = Fraction x (Cost-Salvage)

where the fraction is calculated as follows:

Numerator = declining years (highest first)

Denominator = sum of the years digits

In the class example, the denominator is

4+3+2+1 = 10

D.E. for 2008 =4/10(10,000-2,000) = $3,200

D.E. for 2009 = 3/10(10,000-2,000) = $2,400

16

(6) MACRS

MACRS (modified accelerated cost recovery system) is a technique developed by the IRS for tax reporting. It utilizes combinations of DDB, 150%DB, and SL to calculate a table of percentages that can be applied to any depreciable asset.

Additionally, the IRS assumes no salvage value, and a half year in the first and last year of depreciation (some limitations on fourth quarter purchases).

17

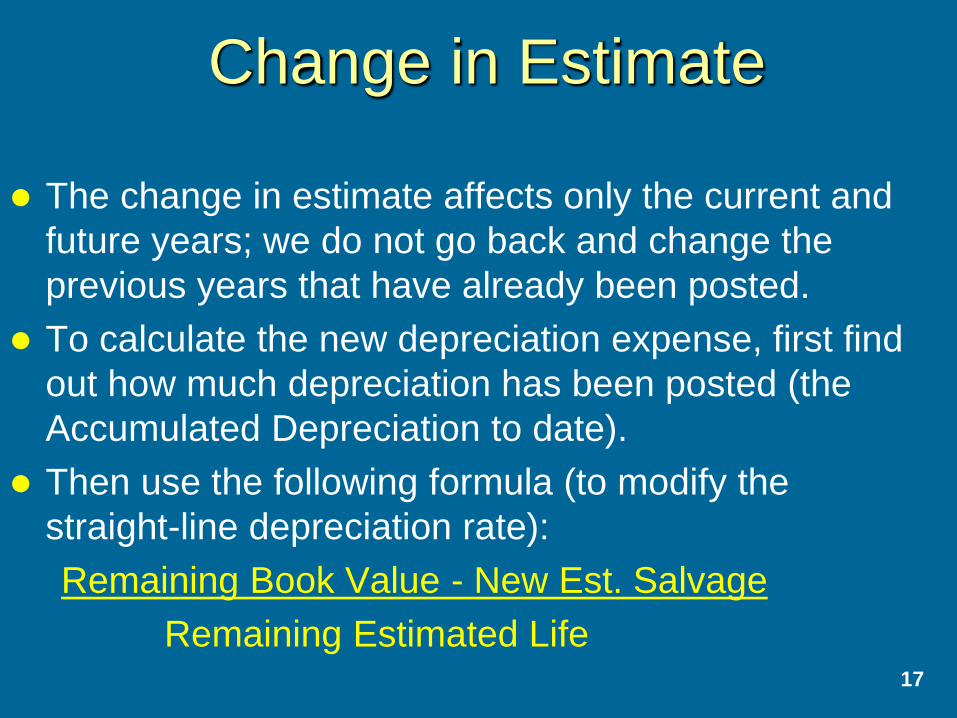

Change in Estimate

The change in estimate affects only the current and

future years; we do not go back and change the

previous years that have already been posted.

To calculate the new depreciation expense, first find

out how much depreciation has been posted (the

Accumulated Depreciation to date).

Then use the following formula (to modify the

straight-line depreciation rate):

Remaining Book Value - New Est. Salvage

Remaining Estimated Life

18

Class Problem: Problem 9-7

(a)Book Value at 1/1/06:

First: annual depr. expense =

(180-30)/10 = 15/yr.

Then Accumulated Depr. to 1/1/11:

15 x 5 yrs = $75,000

So BV = 180,000 - 75,000 = 105,000

19

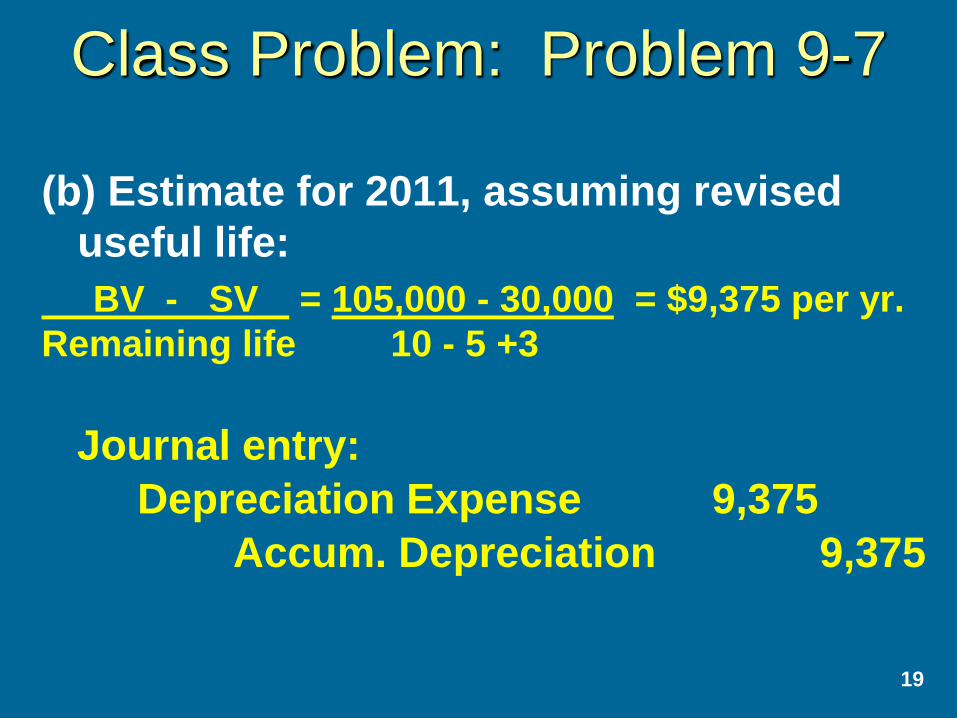

Class Problem: Problem 9-7

(b) Estimate for 2011, assuming revised

useful life:

BV - SV = 105,000 - 30,000 = $9,375 per yr.

Remaining life 10 - 5 +3

Journal entry:

Depreciation Expense 9,375

Accum. Depreciation 9,375

20

3. Postacquisition Expenditures: Betterments or

Maintenance? Betterments:

– Increase asset’s useful life

– Improve quality of asset’s output

– Increase quantity of asset’s output

– Reduce asset’s operating costs

Maintenance – maintain existing productivity or useful life

Accounting treatment – Betterments are capitalized

– Maintenance expenditures are expensed

21

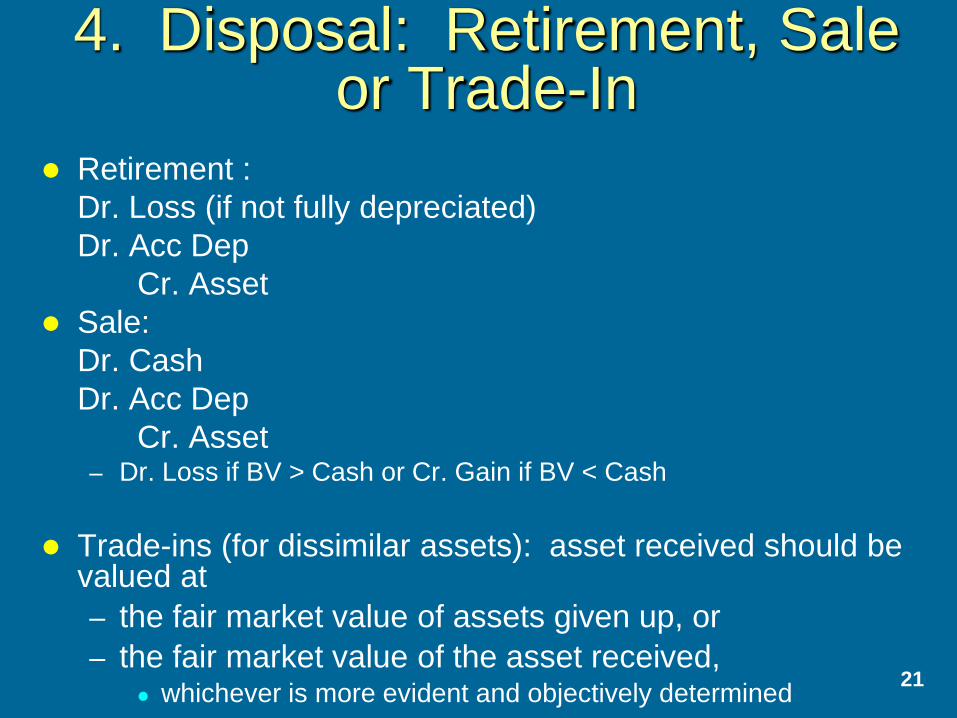

4. Disposal: Retirement, Sale or Trade-In

Retirement :

Dr. Loss (if not fully depreciated)

Dr. Acc Dep

Cr. Asset

Sale:

Dr. Cash

Dr. Acc Dep

Cr. Asset – Dr. Loss if BV > Cash or Cr. Gain if BV < Cash

Trade-ins (for dissimilar assets): asset received should be valued at

– the fair market value of assets given up, or

– the fair market value of the asset received, whichever is more evident and objectively determined

22

4. Disposal - continued

Using earlier example (cost = $10,000, salvage = $2,000). After 4 years straight-line, $8,000 would be in A/D.

1. Assume the asset is retired (no cash received)

Loss on retirement 2,000

Accumulated Depr. 8,000

Automobiles 10,000

2. Assume the asset is sold for $3,000:

Cash 3,000

Accumulated Depr. 8,000

Automobiles 10,000

Gain on sale 1,000

23

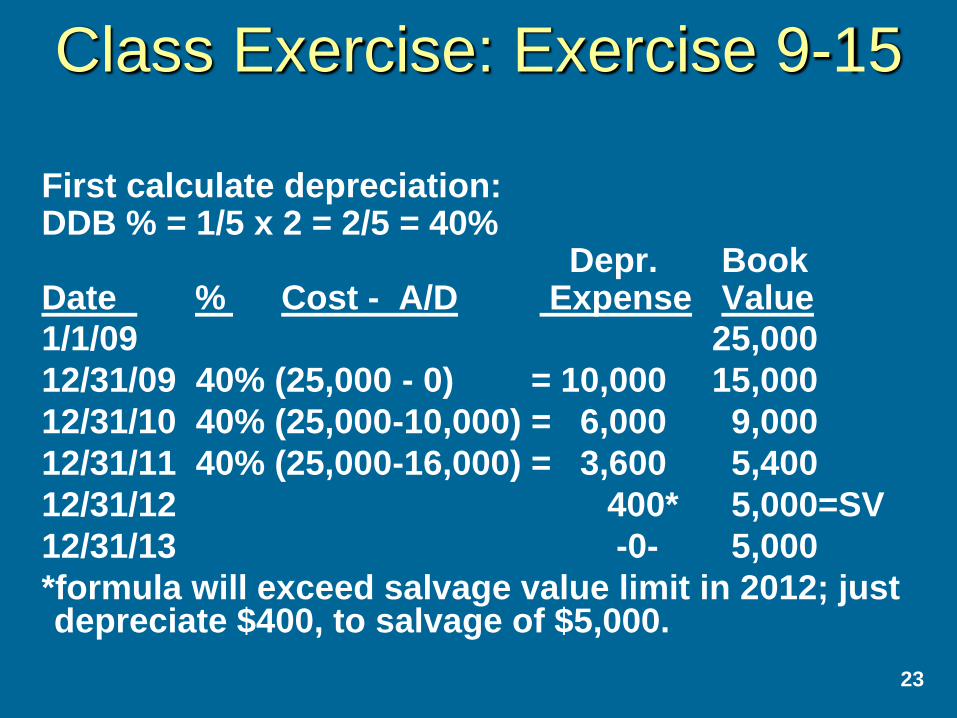

Class Exercise: Exercise 9-15

First calculate depreciation: DDB % = 1/5 x 2 = 2/5 = 40% Depr. Book Date % Cost - A/D Expense Value

1/1/09 25,000

12/31/09 40% (25,000 - 0) = 10,000 15,000

12/31/10 40% (25,000-10,000) = 6,000 9,000

12/31/11 40% (25,000-16,000) = 3,600 5,400

12/31/12 400* 5,000=SV

12/31/13 -0- 5,000

*formula will exceed salvage value limit in 2012; just depreciate $400, to salvage of $5,000.

24

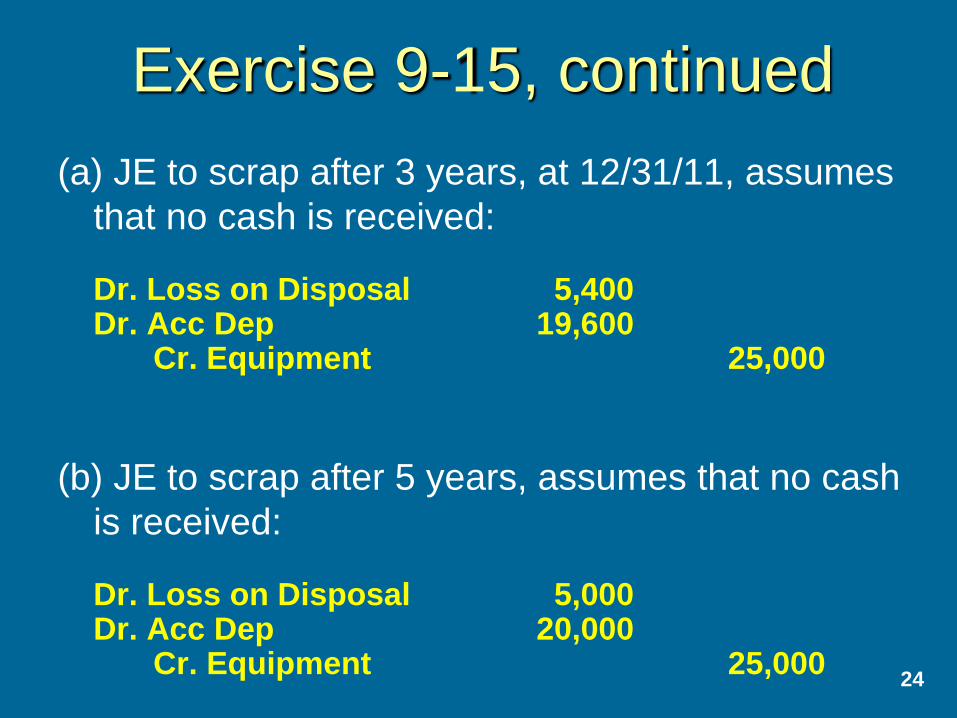

Exercise 9-15, continued

(a) JE to scrap after 3 years, at 12/31/11, assumes

that no cash is received: Dr. Loss on Disposal 5,400 Dr. Acc Dep 19,600 Cr. Equipment 25,000

(b) JE to scrap after 5 years, assumes that no cash

is received: Dr. Loss on Disposal 5,000 Dr. Acc Dep 20,000 Cr. Equipment 25,000

25

Exercise 9-15, continued

(c) JE to sell for $8,000 after 3 years: Dr. Cash 8,000

Dr. Acc Dep 19,600

Cr. Equipment 25,000 Cr. Gain 2,600

(d) JE if, after 5 years, the equipment and $28,000 traded for a dissimilar asset with a fair market value of $30,000:

Dr. Asset (new) 30,000 Dr. Acc Dep 20,000 Dr. Loss 3,000 Cr. Equipment (old) 25,000 Cr. Cash 28,000

26

B. Intangible Assets Intangible assets are characterized by (1)

lack of physical evidence, and

(2) high uncertainty about future benefits.

Cost is amortized over useful life (or legal life, if less), but not to exceed 40 years.

– Exception is Goodwill, which is no longer amortized.

Under IFRS, revaluing intangibles is an option, but not a requirement. Under US GAAP, revaluation is not an option.

27

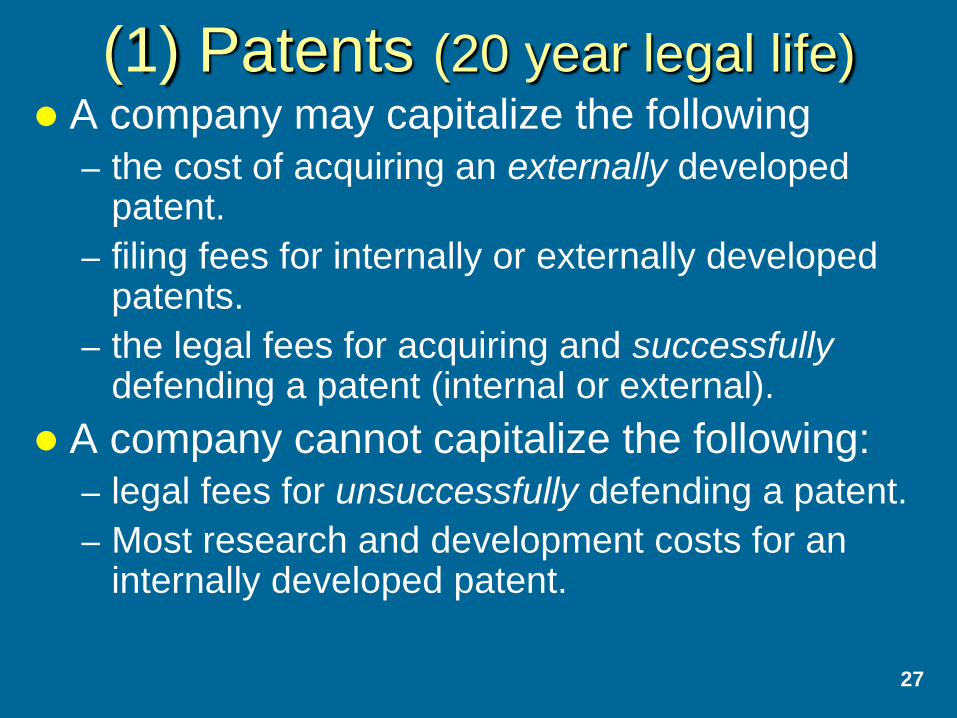

(1) Patents (20 year legal life) A company may capitalize the following

– the cost of acquiring an externally developed patent.

– filing fees for internally or externally developed patents.

– the legal fees for acquiring and successfully defending a patent (internal or external).

A company cannot capitalize the following:

– legal fees for unsuccessfully defending a patent.

– Most research and development costs for an internally developed patent.

28

Research and Development

Costs (for internally developed

patents) Prior to 1974, most companies capitalized research

and development costs, then amortized the cost to future periods.

The FASB stated in SFAS 2 that, because “future benefits” were uncertain, companies should expense all R&D costs, unless they were related to tangible assets (like buildings and equipment) that had multi-year lives.

Companies complied with the standard, but for several years many companies actually reduced their R&D activities, because of concern for excess expense on the income statement.

29

Other Intangible Assets (2) Copyrights

– granted for the life of the creator plus 70 years.

– capitalization rules similar to patents: costs of internally developed copyright material cannot be capitalized.

(3) Trademarks and Trade Names

– granted for 10 year periods, but indefinite renewals.

– some of design costs may be capitalized.

(4) Organization Costs

– costs related to the creation of a company including underwriting fees, legal and accounting, licenses, titles, etc.

– treatment similar to R&D costs; even though there may be some future benefit, costs are expensed in the period incurred.

30

Other Intangible Assets -

continued (5) Software Development Costs (SFAS 86)

– Capitalize the costs of developing software for sale or lease.

– Expense software development costs if for internal use.

(6) Goodwill (also discussed in Chapter 8)

– Recognized when one company purchases another company.

– Causes include reputation, good customer relations, superior product development, etc.

– To calculate:

Purchase price paid for the company versus the fair market value of the net assets acquired

= Goodwill (the excess amount paid)

– No longer amortized, instead subjected to an impairment test

31

IFRS vs. US GAAP: Revaluations to Fair

Market Value

One very important way in which IFRS differs from US GAAP involves the use of fair market value as a basis for valuation on the balance sheet.

– Under US GAAP, long-lived assets must be accounted for at original cost less accumulated depreciation.

– Under IFRS, companies can either follow the US GAAP method or they can periodically revalue their long-lived assets to fair market value.

In essence, US GAAP tends to follow a conservative “lower-of-cost-or-market” valuation principle, whereas IFRS allows managers the option to more closely follow a pure market valuation principle.

Copyright

32

Copyright © 2011 John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in Section

117 of the 1976 United States Copyright Act without the express written

permission of the copyright owner is unlawful. Request for further

information should be addressed to the Permissions Department, John

Wiley & Sons, Inc. The purchaser may make back-up copies for his/her

own use only and not for distribution or resale. The Publisher assumes no

responsibility for errors, omissions, or damages, caused by the use of

these programs or from the use of the information contained herein.