CHICAGOLAND IASA 2014 NAIC ACCOUNTING AND REPORTING UPDATE

APRIL 17, 2014

www.mcs-nc.com

An insurance regulatory services firm dedicated to providing

statutory training and consulting services to insurance companies and regulators

Millennium Consulting Services, LLC 14460 New Falls Of Neuse Rd., Suite 149-294 • Raleigh, NC • 27614

Phone: (919) 569-6762 • www.mcs-nc.com

3

Who We Are

Bruce A. Cromartie – President & CEO • Over 30 years of insurance, regulatory,

lobbying, training, and consulting experience – SunGard Insurance Systems – 3 Years VP of

Seminars and Regulatory Consulting – BCBSA – 10 years Financial Regulatory Affairs – NAIC – 2 Years Financial Analyst – N. C. DOI – 6 Years Assistant Deputy

Commissioner – N. C. Farm Bureau – 4 Years Internal Auditor

4

Who We Are

Colleen Gingrich – Sr. Vice President • Over 20 years of insurance, regulatory,

training, and consulting experience – Family Health Partners HMO - Statutory & GAAP

Accounting/Reporting Manager – Coventry Health Plan – Accounting Manager – SunGard – Director of Seminars & Regulatory

Consulting – NAIC – P&C Financial Analyst Manager – Pinnacle Rehabilitation Company – Supervisor – Federated Rural Electric Insurance Company –

Staff Accountant

5

Who We Are

− Karen Foster – Director, Consulting Services − Brian Neader, CPA, FLMI – Director, Consulting Services − Katrina Gunn – Associate Director, Consulting Services − Kim Campbell – Consultant − Teresa Daveline – Consultant − Virginia Jett – Consultant −Nadia Nahvi – Consultant − Lori Oertli – Consultant − Jenny Sloane – Consultant −Nancy White – Consultant

6

Scope of Services

Specializing in providing comprehensive educational training and regulatory consulting for the insurance industry • Seminar Services

– Public Seminars – Private Seminars – Webinars

• Consulting Services – Outsourcing Services – Insurance Regulatory Advisory Services – Quality Control Review (QCR) Services

7

2014 NAIC ACCOUNTING and REPORTING UPDATE Agenda Topics

− Overview of Statutory Accounting Principles − Changes to Accounting Practices and Procedures Manual;

Version March 2014 – Substantive Revisions

– Nonsubstantive Revisions

– Emerging Accounting Issues

− Changes to Accounting Practices and Procedures Manual; Version March 2015

– Emerging Accounting Issues

– Substantive Revisions

– Nonsubstantive Revisions

− Outstanding Statutory Accounting Issues

CODIFICATION OF STATUTORY ACCOUNTING PRINCIPLES

9

Codification of Statutory Accounting Principles

− Guide referred to as – NAIC Accounting Practices and Procedures Manual

• Encompasses statutory accounting principles for statutory accounting and reporting

10

Codification of Statutory Accounting Principles

− Accounting Practices and Procedures Manual composed of – Preamble – Statements of Statutory Accounting Principles – Appendices – Interpretations of Emerging Accounting Issues Working Group – Collectively these items are referred to as the “Accounting Practices

and Procedures Manual (APPM)” – Adopted by NAIC in 1998 – Became effective on state-by-state basis on January 1, 2001 – Updated on an annual basis

11

Codification of Statutory Accounting Principles

− APPM applies to all types of insurers – Health Entities

• Health Maintenance Organizations (HMOs) • Limited Health Service Organization (LHSOs) • Hospital, Medical and Dental Service or Indemnity (HMDI)

Corporations – Life, Accident and Health Insurers – Mortgage Guaranty Insurers – Property and Casualty Insurers – Title Insurers

12

Maintenance of Statutory Accounting Principles

−Maintenance Process – Formal maintenance process designed to:

• Address accounting rules for new transactions that occur in the business environment of insurers and modifications

• Provide clarifications to existing accounting practices – APPM is continuously under review and periodically updated with

new: • Issue Papers • Interpretations • Statements of Statutory Accounting Principles

– Changes are done in accordance with NAIC Policy Statement on the “Maintenance of Statutory Accounting Principles”

– Updated annually to reflect the adoption of new guidance

13

Maintenance of Statutory Accounting Principles

−Accounting Practices and Procedures Task – Task Force employs two working groups with distinctly different

functions to carry out charge of maintaining SAP – Groups are made up of insurance department regulators – Staffed by NAIC personnel

• Statutory Accounting Principles Working Group • Emerging Accounting Issues Working Group

CHANGES TO THE ACCOUNTING PRACTICES AND PROCEDURES MANUAL; VERSION

MARCH 2014

15

Changes to AP&P Manual; Version March 2014

− Changes to AP&P Manual – This section addresses changes to Accounting Practices and

Procedures Manual as of March 2014 • Adopted at 2013 NAIC Fall National Meeting with 2014 effective

dates – Substantive Revisions - New Statements of Statutory Accounting

Principles

– Nonsubstantive Revisions - Amendments to current SSAPs

SUBSTANTIVE REVISIONS EFFECTIVE JANUARY 2014

17

Substantive Revisions

• At NAIC 2013 Fall National Meeting Working Group adopted the following Substantive Revisions with January 1, 2014 effective date

– SSAP No. 35R – Guaranty Fund and Other Assessments – SSAP No. 104R – Share-Based Payments – SSAP No. 105 - Working Capital Finance Investments

18

Substantive Revisions

• Adopted accounting guidance for ACA Section 9010 – Insurer Fee – Statutory accounting guidance found in SSAP No. 35R,

paragraphs 16-21 – Effective January 1, 2014

SSAP No. 35R – Guaranty Fund and Other Assessments

19

Substantive Revisions

• For initial application of 2013 Data Year Insurer Fee in 2014 Reporting Entity must: – Accrue liability and expense for Insurer Fee in Fee Year (year

fee is due and paid) – Pay 2013 Data Year Insurer Fee as of September 30, 2014 (Fee

Year) • Report Insurer Fee in operating expenses in Fee Year in expense

category of “Taxes, Licenses and Fees”

SSAP No. 35R – Guaranty Fund and Other Assessments

20

Substantive Revisions

Date Data Year Fee Year

Account Debit Credit

1/1/14 N/A ACA Section 9010 Expense 120.00

Insurer Fee Liability - 2013 120.00

Recognize liability and expense for Prior Year “Data Year” ACA Section 9010 Insurer Fee in Current “Fee Year”

SSAP No. 35R – Guaranty Fund and Other Assessments

21

Substantive Revisions

• Recognize payment of 2013 Data Year Insurer Fee no later than September 30, 2014 (Fee Year)

Date Data Year Fee Year

Account Debit Credit

9/30/14 N/A Insurer Fee Liability- 2013 120.00

Cash 120.00

Payment of Prior Year “Data Year” ACA Section 9010 Insurer Fee

SSAP No. 35R – Guaranty Fund and Other Assessments

22

Substantive Revisions

Accrue monthly estimated Insurer Fee in Special Surplus for current Fee Year (2015 Fee Year/2014 Data Year) assessment

Date Current Data Year Account Debit Credit

1/31/14 Unassigned Funds 12.50 Special Surplus 12.50

Reserve for 2014 Data Year ACA Section 9010 Fee

2/28/14 Unassigned Funds 12.50 Special Surplus 12.50

Reserve for 2014 Data Year ACA Section 9010 Fee

9/30/14 Unassigned Funds 12.50 Special Surplus 12.50

Reserve for 2014 Data Year ACA Section 9010 Fee 12/31/14 Unassigned Funds 12.50

Special Surplus 12.50 Reserve 2014 Data Year ACA Section 9010 Fee (Total reclassification in the amount of $150)

SSAP No. 35R – Guaranty Fund and Other Assessments

23

Substantive Revisions

Date Data Year

Account Debit Credit

1/1/2015 Special Surplus 150.00

Unassigned Funds 150.00

Reverse 2014 reserve reclassification for 2014 Data Year ACA Section 9010 Fee

SSAP No. 35R – Guaranty Fund and Other Assessments

24

−Ref. No. 2013-03 - ASC 505-50 – Equity Payments to Non-Employees

– Adopted with modifications ASC 505-50 – Addresses equity payments to non-employees – Requires recognition in financial statements of most reliable

measurable FV of such transactions – Effective December 31, 2014

Substantive Revisions

5

SSAP No. 104R - Share-Based Payments

25

Substantive Revisions

• Adopted SSAP to provide accounting guidance for Working Capital Finance Investments – Aka vendor finance note – Created when supplier sells goods to buyer then delivers

invoice for payment – Investments typically held by commercial banks – Insurance entities have begun investing in securities – Accounted for as admitted asset pursuant to SSAP No. 105 – Reported in Schedule BA – Effective January 1, 2014

SSAP No. 105 – Working Capital Finance Investments

NONSUBSTANTIVE REVISIONS

27

Nonsubstantive Revisions

− Ref No. 2013-11 - Accounting Disclosures for Restricted Assets − Revises paragraph 17.b

− Revises disclosure requirement for investments not under exclusive control of reported entity to be included in Notes to Financial Statement

− Information currently reported in General Interrogatories. − Intent to accumulate all relevant disclosures regarding

restricted assets in one place in statutory statement

SSAP No. 1 – Disclosure of Accounting Policies

28

Nonsubstantive Revisions

• Ref No. 2013-01 - Mandatory Convertible Securities – Revises paragraph 7, adds new paragraph 9 – Revises definition of mandatory convertible securities – Revises accounting and reporting guidance to report these

securities at lower of amortized cost or fair value – Effective January 1, 2014

SSAP No. 26 – Bonds, Excluding Loan-Backed and Structured Securities

29

Nonsubstantive Revisions

− Ref No. 2012-30 – Adding Preferred Stock Class for ETFs − New paragraph 3.c − Adds classification of exchange traded funds (ETFs) to

definition of preferred stocks

SSAP No. 32 – Preferred Stock

30

Nonsubstantive Revisions

• Ref No. 2012-26 - Measurement and Classification of Real Estate Investments – Revises paragraph 4.c – Moves guidance related to measurement and classification of

real estate investments from SSAP No. 90 to SSAP No. 40

• Ref No. 2013-08 – Real Estate Encumbrances – Revises paragraph 6 – Clarifies definition of encumbrances

3-4

SSAP No. 40/90 – Real Estate Investments

31

Nonsubstantive Revisions

− Ref No. 2013-16 – Disclosure Requirements for Loan-Backed and Structured Securities − New paragraph 26

− Limits disclosure for bifurcated other-than-temporary credit impairments to current reporting period

− Revises guidance for interim financial statements for RMBS and CMBS securities acquired subsequent to year-end

SSAP No. 43R - Loan-Backed and Structured Securities

32

Nonsubstantive Revisions

• Ref No. 2012-23 - Seed Money Disclosure – New paragraph 35.b – Revises disclosure requirement to capture information on:

• Separate account seed money • Other fees and expenses • Additional required surplus amounts

SSAP No. 56 – Separate Accounts

33

Nonsubstantive Revisions

• Ref No. 2011-45 - Impact of Transfer on Provision for Reinsurance – New paragraphs 66-67

• Impacts asbestos and pollution reinsurance contracts • Changes Schedule F reporting and provision for reinsurance

calculation • Effective January 1, 2014

SSAP No. 62R – Property & Casualty Reinsurance

34

Nonsubstantive Revisions

– Ref No. 2013-07 -ASU 2013-01, Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities – SSAP No. 64, new paragraph 6-7 – SSAP No. 86, new paragraph 53.h – SSAP No. 86, new paragraph 28.m

• Revisions clarify that: – Derivatives, repurchase and reverse repurchase agreements, and

securities borrowing and securities lending transactions reported

» Net on Balance Sheet

» Gross on Schedule DB

– Adds disclosures to illustrate netting impact

SSAP Nos. 64, SSAP No. 86, SSAP No. 103

35

Nonsubstantive Revisions

• Ref No. 2012-24 - Hedge Accounting Requirements – Revises paragraph 15 – Allow transactions that meet criteria of highly effective hedge

transactions to follow fair value hedge accounting if elected by reporting entity

SSAP No. 86 – Accounting for Derivative Instruments

36

Nonsubstantive Revisions

• Ref No. 2013-02 - EITF 06-04, Accounting for Deferred Compensation and Postretirement Benefit Aspects of Endorsement Split-Dollar Life Insurance Arrangements – Revises paragraphs 58, 84, and 99

• Revisions adopt with modification EITF 06-04 • Specifies that endorsement split-dollar life insurance contracts

do not settle liability for postretirement benefit obligations

SSAP No. 92 – Accounting for Postretirement Benefits Other Than Pensions

37

Nonsubstantive Revisions

• Ref No. 2012-31 - Inconsistency Regarding Tax Planning Strategies

– Revises paragraphs 14 – Clarifies that tax planning strategies:

• Must be utilized in statutory valuation allowance calculation • Not required in admittance calculation • If used for admittance calculation

– Should be consistent with tax-planning strategies used in computing statutory valuation allowance

SSAP No. 101 – Income Taxes

38

Nonsubstantive Revisions

− Ref No. 2013-12 - DTA Admissibility Test for Financial and Mortgage Guaranty Insurers − Revises paragraph 11b and “Realization Threshold Limitation

Table” − Clarifies threshold limitations for calculation of RBC for

mortgage guaranty insurers

3-5

SSAP No. 101 – Income Taxes

CHANGES TO THE ACCOUNTING PRACTICES AND PROCEDURES MANUAL; VERSION

MARCH 2015

40

Changes to AP&P Manual; Version March 2015

− Changes to AP&P Manual – This section addresses changes to Accounting Practices and

Procedures Manual as of March 2015 • New Consensus Interpretations • Statements of Statutory Accounting Principles

– Substantive Revisions

– Nonsubstantive Revisions

• Outstanding Substantive and Nonsubstantive Revisions

EMERGING ACCOUNTING ISSUES

42

Consensus Interpretations

−Emerging Accounting Issues – Responds to questions of

• Application • Interpretation • Clarification of existing SSAPs

– Final consensus opinions (Consensus Interpretation) are published annually in Appendix B of APPM

– Effective upon adoption by Accounting Practices and Procedures Task Force

CONSENSUS INTERPRETATIONS (AS OF MARCH 31, 2014)

44

Consensus Interpretations

• Adopted interpretative accounting guidance for ACA’s Risk Sharing Programs – Risk Adjustment, Reinsurance, and Risk Corridors – Commonly referred as to the 3Rs

• Accounting guidance effective immediately • Applicable for 2014 1st Quarter reporting period

INT 2013-04 – Accounting for the Risk Sharing Provisions of the Affordable Care Act (ACA)

45

Consensus Interpretations

• ACA Risk Sharing Programs – Programs take effect in 2014 – Imposes both fees and premium and claim stabilization programs

on insurance companies offering commercial insurance – Accounting guidance in INT 13-04 similar to guidance in INT 05-

05: Accounting for Revenues under Medicare Part D Coverage • Interpretation references existing statutory accounting guidance

from various SSAPs, including SSAPs No. 6, 35R, 47, 54, 61R, 63, 66 and 84

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

46

Consensus Interpretations

• With adoption of INT 13-04 Working Group submitted referral to SAPWG to: – Address issues pertaining to admissibility of certain items within

three programs – Develop stand-alone SSAP to codify 3R guidance

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

47

Consensus Interpretations

• Accounting Issues – How to account for various components of three risk sharing

programs – Which existing SSAPs should be utilized for various program

provisions

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

48

Consensus Interpretations

• Consensus Position: Risk Adjustment Program – Permanent program designed to transfer premiums between

health insurers in individual and small-group markets, including grandfathered plans

– In/Out of Marketplace – Transfer of premiums based on relative risk scores of insurers in

program • Function of diagnosis codes without regard to actual claims

experience

– Administered by HHS or optionally a state

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

49

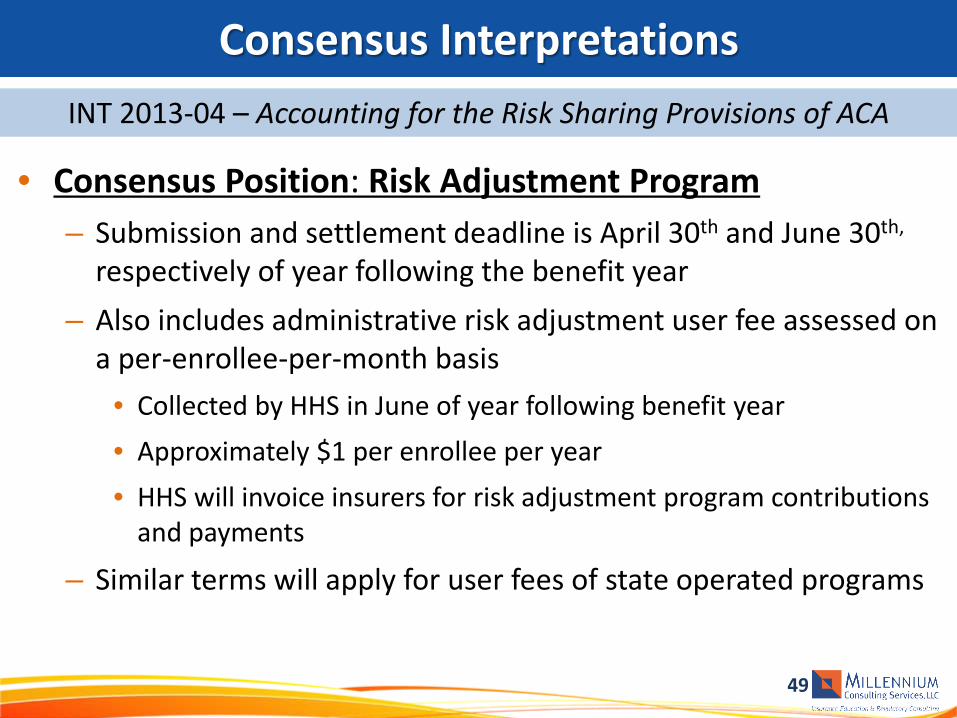

Consensus Interpretations

• Consensus Position: Risk Adjustment Program – Submission and settlement deadline is April 30th and June 30th,

respectively of year following the benefit year – Also includes administrative risk adjustment user fee assessed on

a per-enrollee-per-month basis • Collected by HHS in June of year following benefit year • Approximately $1 per enrollee per year • HHS will invoice insurers for risk adjustment program contributions

and payments

– Similar terms will apply for user fees of state operated programs

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

50

Consensus Interpretations

• Consensus Position: Risk Adjustment Program – INT 13-04 addresses two accounting issues for the Risk

Adjustment Program: • Risk adjustment contributions (premium reduction) into Program

and payments or recoveries from Program (additional premiums) • Risk adjustment user fee

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

51

Consensus Interpretations

• Consensus Position: Risk Adjustment Program – INT 13-04 clarifies two accounting issues in paragraphs 12 – 16:

• Paragraph 12 - Premium adjustments (contributions and recoveries) accounted for as “premiums subject to redetermination” per SSAP No. 54

• Paragraph 15 - Record adjustments to premium in period in which changes in risk scores of enrollees result in premium adjustment

– To extent adjustments are reasonably estimable • Paragraph 16 - Receivables or recoveries subject to 90-day rule

nonadmission rule per SSAP No. 6 – Beginning when payment is due to be disbursed by HHS or state - not

from date of initial accrual – Receivable also subject to impairment analysis

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

52

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

53

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

54

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

55

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

56

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

57

Consensus Interpretations

• Consensus Position: Risk Adjustment Program – Paragraph 13 - User fees treated as government assessments

• Accounted for under SSAP No. 35R • Treated the same as other non-income-based governmental taxes

and fees

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

58

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

59

Consensus Interpretations

• Consensus Position: Transitional Reinsurance Program – Three-year program designed to stabilize premiums for coverage

in individual market from 2014 through 2016 – Requires all health insurance issuers and TPAs on behalf of self-

insured group health plans to pay into fund via “reinsurance” – Applies to individual market covering high-cost individuals – Impacts fully insured individual, non-individual products and self

insured products but utilizes different accounting methodologies – Funding scheduled to decrease systematically from 2014 through

2016 and eliminated in 2017 – Administered by HHS or each state

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

60

Consensus Interpretations

• Consensus Position: Transitional Reinsurance Program – Funded over three-year period through:

• Transitional reinsurance assessment on health plan sponsors ($20 billion) defined as “contributions for reinsurance”

• Contributions to U.S. Treasury ($5 billion) defined as “additional U.S. Treasury contributions”

• Additional assessments of $20.3 million defined as “program administrative costs contributions”

– National per capita contribution rate of approximately $0.11 annually

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

61

Consensus Interpretations

• Consensus Position: Transitional Reinsurance Program – Accounting guidance outlined in paragraphs 20, 25-50

• Paragraph 20 clarifies that ‘reinsurance’ as used by TRP does not represent reinsurance between licensed insurers per SSAP No. 61R

• Similar to “involuntary pool” per SSAP No. 63 – “Mechanism employed by states to provide insurance coverage to those

with higher than average probability of loss who otherwise would be excluded from obtaining coverage”

• Paragraph 28, et al, clarify that contributions for reinsurance and recoveries accounted for as “traditional reinsurance” in accordance with SSAP No. 61R for fully insured individual products

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

62

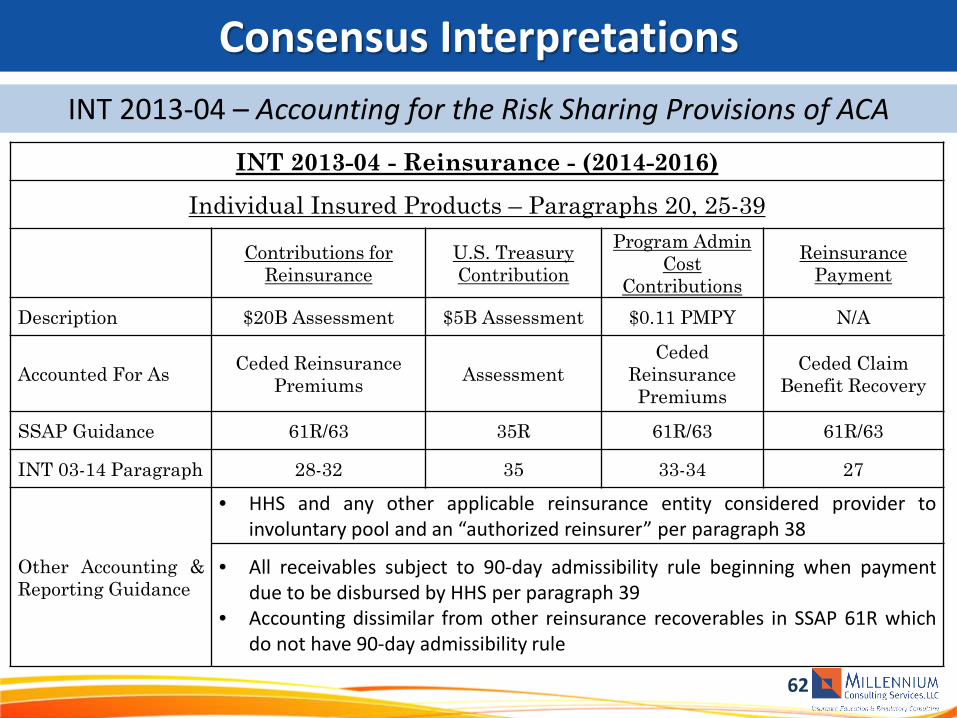

Consensus Interpretations

INT 2013-04 - Reinsurance - (2014-2016)

Individual Insured Products – Paragraphs 20, 25-39

Contributions for Reinsurance

U.S. Treasury Contribution

Program Admin Cost

Contributions Reinsurance

Payment

Description $20B Assessment $5B Assessment $0.11 PMPY N/A

Accounted For As Ceded Reinsurance Premiums Assessment

Ceded Reinsurance Premiums

Ceded Claim Benefit Recovery

SSAP Guidance 61R/63 35R 61R/63 61R/63

INT 03-14 Paragraph 28-32 35 33-34 27

Other Accounting & Reporting Guidance

• HHS and any other applicable reinsurance entity considered provider to involuntary pool and an “authorized reinsurer” per paragraph 38

• All receivables subject to 90-day admissibility rule beginning when payment due to be disbursed by HHS per paragraph 39

• Accounting dissimilar from other reinsurance recoverables in SSAP 61R which do not have 90-day admissibility rule

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

63

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

64

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

65

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

66

Consensus Interpretations

INT 2013-04 - Reinsurance - (2014-2016)

All Other In Insured Products – Fully Insured Non-Individual Plans – Paragraphs 40-44

Contributions for Reinsurance

U.S. Treasury Contribution

Program Admin Cost Contributions

Reinsurance Payment

Description $20B Assessment $5B Assessment $0.11 PMPY N/A

Accounted For As Assessment Federal Assessment Assessment N/A

SSAP Guidance 61R/63 35R 61R/63 N/A

INT 03-14 Paragraph 40/42 43 40/42 44

Charged To Taxes, Licenses & Fees

Taxes, Licenses & Fees

Taxes, Licenses & Fees N/A

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

67

Consensus Interpretations

INT 2013-04 - Reinsurance - (2014-2016)

Self-Insured Products – Paragraphs 45-50

Contributions for Reinsurance

U.S. Treasury Contribution

Program Admin Cost Contributions

Reinsurance Payment

Description $20B Assessment $5B Assessment $0.11 PMPY N/A

Accounted For As Uninsured Plans Federal Assessment Assessment N/A

Pass-through/Deposit Account

Pass-through/Deposit Account

Pass-through/Deposit Account

SSAP Guidance 47 47 47 N/A

INT 03-14 Paragraph 45/48 45/48/49 40/48/49 50

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

68

Consensus Interpretations

• Consensus Position: Risk Corridors Program – Provides for sharing between QHPs and Federal Government of

profits and losses resulting from inaccurate rate-setting for individual and small group markets in and out of the Marketplace

– Provides government subsidy if insurer losses exceed certain threshold and recoups funds from insurers if gains exceed certain threshold

• Unlike risk adjustment and reinsurance programs, RCP not required to be budget neutral

• Three year program (2014-2016)

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

69

• Consensus Position: Risk Corridors Program – If actual plan allowable costs (net of risk adjustment and

reinsurance payments) come within ± 3% of target • Plan bears loss or keeps gains

– If actual costs fall outside 3% corridor • Government shares in gains or losses with Plan

– In other words • Government pays Plan if costs are more than expected • Plan pays government if costs are lower than expected

– Government bears • 50% of spending between 3% and 8% of target • 80% of spending beyond 8% of the target

Consensus Interpretations INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

70

Consensus Interpretations

• Consensus Position: Risk Corridors Program – INT 13-04 outlines accounting guidance in paragraphs 56-59 – Predicated on INT 05-05 paragraph 4.b., which is accounted for

under SSAP No. 66 • Per paragraph 57 receipts and payments pursuant treated as

premium adjustments for retrospectively rated contracts pursuant to SSAP No. 66

• Per paragraph 59 all receivables considered admitted assets per SSAP No. 84

– Inasmuch as they are receivables from government or a government-sponsored entity and funding is mandated by law

– Receivable subject to impairment analysis

INT 2013-04 – Accounting for the Risk Sharing Provisions of ACA

NONSUBSTANTIVE REVISIONS EFFECTIVE JANUARY 2014

72

Nonsubstantive Revisions

• Ref. No. 2013-28 - Guaranty Fund and Other Assessments – Adopted quarterly and annual disclosures applicable to “3Rs” – Included in Notes 24, 24E and 24F of Health, Life and Property

Statements, respectively, for Retrospectively Rated Contracts and Contracts Subject to Redetermination

– Report “balances” that reside in certain Balance Sheet and Income Statement accounts for each 3R Program

• Asset balances reported on “admitted” asset basis

– Disclosure requirement currently resides in SSAP No. 35R but may be moved to stand-alone SSAP

– Effective 1st Quarter 2014 filing and data captured

SSAP No. 35R - Guaranty Fund and Other Assessments

73

Nonsubstantive Revisions

• Ref. No. 2013-28 - Guaranty Fund and Other Assessments – 24. The financial statements shall disclose the assets, liabilities

and revenue elements by program regarding the risk sharing provisions of the Affordable Care Act for the reporting periods, which are impacted by programs including the listing in sections a-c below. Asset balances shall reflect admitted assets. In addition, material re-estimations and or impairments for the reporting period should also be disclosed.

SSAP No. 35R - Guaranty Fund and Other Assessments

74

Nonsubstantive Revisions

• Ref. No. 2013-28 - Guaranty Fund and Other Assessments – ACA Permanent Risk Adjustment Program:

• Premium adjustments receivable due to ACA Risk Adjustment $__________

• Risk adjustment user fees payable for ACA Risk Adjustment $__________

• Premium adjustments payable due to ACA Risk Adjustment $__________

• Reported as revenue in premium for accident and health contracts $__________

• (written/collected) due to ACA Risk Adjustment $__________ • Reported in expenses as ACA risk adjustment user fees

(incurred/paid) $__________

SSAP No. 35R - Guaranty Fund and Other Assessments

75

Nonsubstantive Revisions

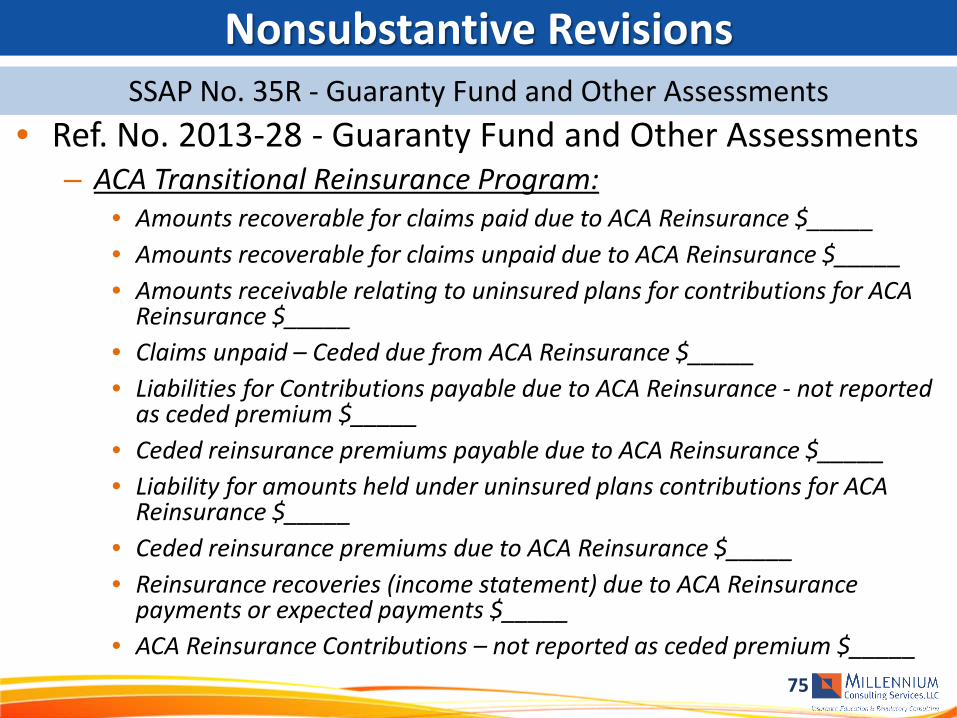

• Ref. No. 2013-28 - Guaranty Fund and Other Assessments – ACA Transitional Reinsurance Program:

• Amounts recoverable for claims paid due to ACA Reinsurance $_____ • Amounts recoverable for claims unpaid due to ACA Reinsurance $_____ • Amounts receivable relating to uninsured plans for contributions for ACA

Reinsurance $_____ • Claims unpaid – Ceded due from ACA Reinsurance $_____ • Liabilities for Contributions payable due to ACA Reinsurance - not reported

as ceded premium $_____ • Ceded reinsurance premiums payable due to ACA Reinsurance $_____ • Liability for amounts held under uninsured plans contributions for ACA

Reinsurance $_____ • Ceded reinsurance premiums due to ACA Reinsurance $_____ • Reinsurance recoveries (income statement) due to ACA Reinsurance

payments or expected payments $_____ • ACA Reinsurance Contributions – not reported as ceded premium $_____

SSAP No. 35R - Guaranty Fund and Other Assessments

76

Nonsubstantive Revisions

• Ref. No. 2013-28 - Guaranty Fund and Other Assessments – ACA Temporary Risk Corridors Program:

• Accrued retrospective premium due from ACA Risk Corridors $__________

• Reserve for rate credits or policy experience rating refunds due to ACA Risk Corridors $__________

• Effect of ACA Risk Corridors on net premium income (paid/received) $__________

• Effect of ACA Risk Corridors on change in reserves for rate credits $__________

SSAP No. 35R - Guaranty Fund and Other Assessments

77

Nonsubstantive Revisions

• Ref. No. 2013-29 – Clarification of Merger Footnote – Adopted revisions to SSAP Nos. 3 and 68 – Clarifies that disclosure exemption for shell companies does not

change January 1 date used to determine how cumulative effect in accounting principle is measured

SSAP No. 3 - Accounting Changes and Corrections of Errors and SSAP No. 68 - Business Combinations and Goodwill

78

Nonsubstantive Revisions

• Ref. No. 2013-31 – Clarification of Appendix B in SSAP No. 97 – Adopted new reference to “Appendix B – Determining the

Valuation Method Under SSAP No. 97” regarding guidance for a downstream holding company

– New reference revises flowchart in Appendix B – Clarifies that for downstream holding companies

• “Sum of all investments in the SCAs within (in accordance with the valuation methods by type of SCA) are calculated as the investment in the downstream holding company”

• As detailed in paragraph 21 of SSAP

SSAP No. 97 – Investments in SCA Entities

79

Nonsubstantive Revisions

• Ref. No. 2013-32 - ASU 2013-10: Inclusion of the Fed Funds Swap Rate as a Benchmark Interest Rate – Adopted revisions to SSAP No. 86 to adopt ASU 2013-10 – Revisions incorporate GAAP definition of benchmark interest rate – Deletes prior guidance indicating that entities should designate

same benchmark interest rate as risk being hedged for similar hedges

SSAP No. 86 - Accounting for Derivative Instruments and Hedging Income Generation and Replication Transactions

80

Nonsubstantive Revisions

• Ref. No. 2013-37 - ASU 2011-09: Compensation –Retirement Benefits–Multiemployer Plans Disclosures about an Employer’s Participation in a Multiemployer Plan – Adopted revisions to SSAP No. 92 and 102 to adopt by reference

ASU 2011-09 to incorporate limited disclosures – Disclosures capture limited instances in which reporting entities

participate in multiemployer plans – Revisions ensure that GAAP and SAP differences are minimal

SSAP No. 92 - Accounting for Postretirement Benefits Other than Pensions and SSAP No. 102 - Accounting for Pensions

EXPOSED SUBSTANTIVE REVISIONS (COMMENTS DUE BY MAY 8, 2014)

82

Exposed Substantive Revisions

• Ref. No. 2014-01 – ACA Guidance in Separate Statements – Working Group exposed revisions to SSAP No. 35R to move ACA

Section 9010 accounting and reporting guidance from SSAP No. 35R to stand-alone SSAP

New SSAP and Issue Paper No. 148

EXPOSED NONSUBSTANTIVE REVISIONS (COMMENTS DUE BY MAY 8, 2014)

84

Exposed Nonsubstantive Revisions

• Ref. No. 2013-28 - ACA Risk Sharing Provisions – Exposed “roll-forward” disclosure applicable to ACA Risk Sharing

Provisions – Required to:

• Disclose roll forward of certain prior year ACA risks sharing asset and liability balances in Notes to Financial Statements

• Disclose asset balances gross of any nonadmission • Provide reasons for adjustments to prior year balances

– Requires disclosure requirement for both annual and quarterly statement beginning with 2014 year-end statement

SSAP No. 35R - Guaranty Fund and Other Assessments

85

SSAP No. 35R - Guaranty Fund and Other Assessments

Exposed Nonsubstantive Revisions

86

Exposed Nonsubstantive Revisions

• Ref. No. 2014-02 – Disclosure for Structured Notes – Exposed revisions to incorporate new structured note disclosure

for 2014 year-end statutory statements – Disclose information for structured notes as defined in SVO

P&PM including: • CUSIP number • Actual cost • Fair and book/adjusted carrying values

– Additional information required if structured note is considered “mortgage-referenced security”

– Adds clarification to SSAP No. 43R that guidance pertains to “structured securities” and not “structured notes”

– Will be data-captured for 2014

SSAP No. 26 - Bonds, Excluding Loan-backed and Structured Securities and SSAP No. 43R - Revised Loan-Backed and Structured Securities

87

Exposed Nonsubstantive Revisions

• Ref. No. 2014-04 – Inconsistent Audit Requirement in SSAP No. 16R – Exposed revisions to:

• Make disclosure related to changes in written capitalization policy threshold consistent with similar guidance in other SSAPs

• Remove restriction that disclosure to be in “annual audited financial statements only”

SSAP No. 16R - Electronic Data Processing Equipment and Accounting for Software

88

Exposed Nonsubstantive Revisions

• Ref. No. 2014-05 – ASU 2014-05, Service Concession Arrangements – Exposed revisions to SSAP No. 19 that adopt modified version of

ASU 2014-05 clarifying that: • Service concession arrangements are not within scope of SSAP No.

22 • Shall not be recognized as property, plant or equipment in SSAP No.

19

SSAP No. 19 - Furniture, Fixtures and Equipment; and SSAP No. 22 - Leases

89

Exposed Nonsubstantive Revisions

• Ref. No. 2014-05 – Title Insurance Premium Classifications – Exposed revisions that:

• Changes premium disclosure categories with five activity codes • Expands definitions of “type of rate” to coincide with previous

changes to Title Blank • Deletes categories for Gross All Inclusive Premiums and Gross Risk

Rate Premiums • Replaces them with five Activity Codes - Risk Rate, Search, Exam,

Closing, and Escrow

SSAP No. 57 – Title Insurance

90

Exposed Nonsubstantive Revisions

• Ref. No. 2014-07 – SSAP No. 11 – Clarification of Adopted GAAP – Exposed revisions to incorporate adoption of paragraphs 6A and

7 of APB 12, Omnibus Opinion – 1967 – Adds guidance to reflect previously adopted GAAP

• GAAP guidance addresses compensated absences, sick leave benefits, and sabbatical leave benefits

– For statutory accounting these types of benefits are addressed in SSAP No. 11

• Proposed revisions will update SSAP No. 11 to clearly identify adopted GAAP guidance

SSAP No. 11—Postemployment Benefits and Compensated Absences

91

Exposed Nonsubstantive Revisions

• Ref. No. 2014-08 – Reference SSAPs on Issue Papers – Exposed revisions to all IPs to add reference to SSAP that

corresponds with IP • IPs not considered authoritative and currently do not identify the

location of authoritative guidance regarding the topical issue • Proposes to incorporate information on face of IP to assist users in

quickly finding current authoritative literature with relevant SSAP

Various Issue Papers

. Questions? Comments? Thoughts?