SPECIAL EDITION

LENDERGUIDE

CO-BRANDINGWhite labels add value for brokers

COMMERCIALCo-broker the deal With a speCialist

BUSINESS-FOR-SELFlending landsCapeshifts for bfs Clients

RENtALS offering investors expert adviCe

LENDER PRODUCt

GUIDEPAGE 24

LOOKING FOR A BANK THAT SHARES YOURCREATIVE VISION.GOOD LUCKWITH THAT.

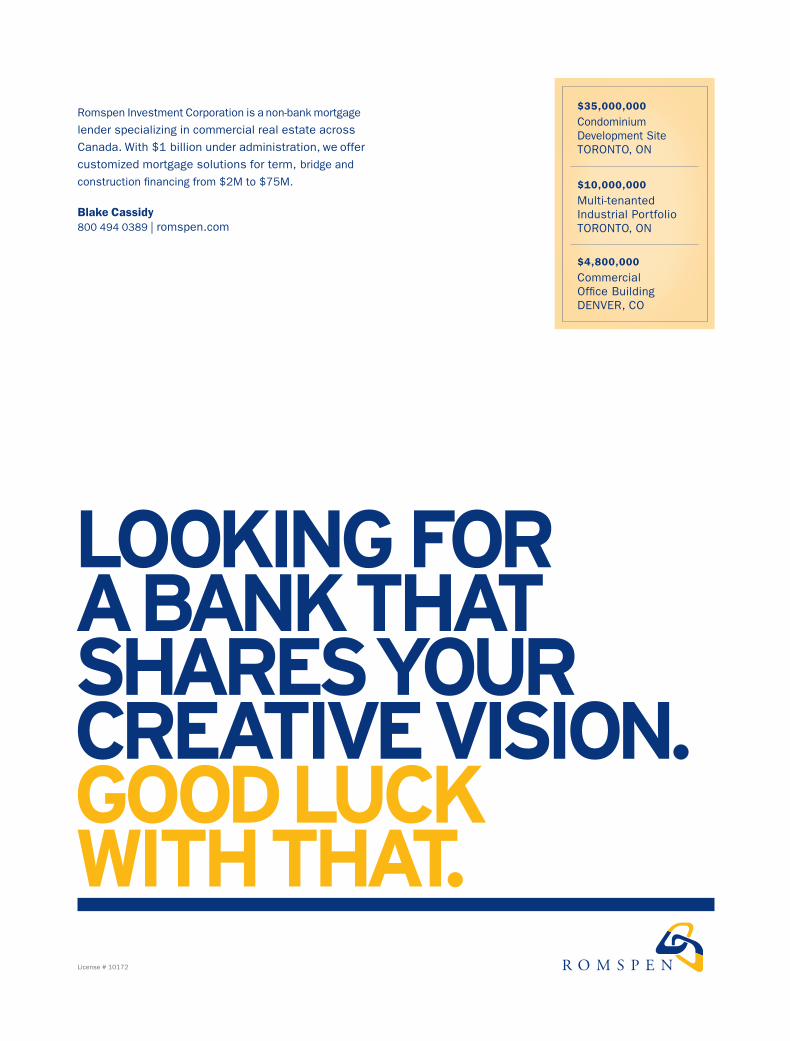

Romspen Investment Corporation is a non-bank mortgage

lender specializing in commercial real estate across Canada. With $1 billion under administration, we offer customized mortgage solutions for term, bridge and

construction � nancing from $2M to $75M.

Blake Cassidy800 494 0389 | romspen.com

SPELL CHECK

B E N S I M O N PA R T N E R S 4 4 6 S PA D I N A R O A D , S U I T E 2 0 7, T O R O N T O , O N TA R I O , M 5 P 3 M 2 , C A N A DA T E L . 4 1 6 5 9 7 9 7 0 0 FA X . 4 1 6 5 9 7 9 7 0 7

DATE:

AD NUMBER:

AD / JOB TITLE:

PUBLICATION / RUN DATE:

LIVE:

COLOUR:

CLIENT:

CREATIVE TEAM:

TRIM: BLEED:MAY 1, 2012_4:40 PM

ROM CMP 12 05 FP

BANK

CDN. MORTGAGE PRO. / MAY 2012

8.25” x 10.875”

CMYK

ROMPSEN

BENSIMON/PARKER

7.5” x 10.125” 8.75” x 11.375”

✓

License # 10172

$11,000,000

Condominium Development SiteTORONTO, ON

$7,500,000

19 ServicedIndustrial LotsEDMONTON, AB

$35,000,000

Condominium Construction FacilityVICTORIA, BC

$10,000,000

Multi-tenanted Industrial PortfolioTORONTO, ON

$4,800,000

CommercialOf� ce BuildingDENVER, CO

$35,000,000

Condominium Development SiteTORONTO, ON

MORTGAGES | CREDIT | VISA | DEPOSITS | www.hometrust.ca

Our common sense approach opens the doors to

home ownership even wider.

As Canada’s leading alternative mortgage lender, Home Trust Company has

been opening our doors to brokers for over 25 years. Our dedicated underwriting

team always uses a common sense approach, allowing you to close more deals.

It’s as simple as that. Yet another way Home Trust helps you open more doors

when opportunity knocks.

contents / lender guide

mAy 2012 lender guide | 1

Lender Product GuideA round-up of products available from broker channel lenders

8!4 | Vintage productsWhite label products, co-branding partnerships between brokerages and lenders, continue to grow in popularity. CMP explores what they are why these products are key value-adds for brokerages to use as exclusive tools by their brokers

8 | The big shiftrecent concerns about mortgage insurance funding by CMHC has caused lenders to either pull back or exit completely from the business-for-self mortgage market. While there is cause for concern, brokers and lenders say homes can still be found for these mortgages

26

contents / lender guide

2 | lender guide mAy 2012

13 | Business-for-self Canadians present big opportunitiesBrokers often turn away from this type of business because they aren’t sure how to evaluate or even put together a solution for this type of customer. But all it really takes, says Home Trust’s Pino Decina, is a more flexible type of approach

14 | Stepping up to commercialif you’re a residential agent who wants to handle your commercial referrals, it’s essential to seek out a commercial specialist willing to co-broker the deal says industry veteran Dale Bilton

20 | Rental re-think Brokers have built whole businesses around this niche area, helping real estate investors bolster their portfolios. But with a lender pullback adding to government rule changes introduced over the last couple years, they’re re-evaluating that strategy. Still, for investors, the need for broker expertise has never been greater, and that presents a whole new set of opportunities for mortgage professionals educated on today’s rental programs

26 | Lender Product GuideCMP invited broker channel lenders to provide a basic outline of their lending products and we’ve collected the results and present them here as a handy reference guide for brokers

14

20

contents / editor’s letter

mAy 2012 lender guide | 3

COPY & FEATURESeditor John Tenpennyassociate online editor Vernon Clement JonessUB-editor rachel naudstaff writer Caitlin nobescontriBUtors doren Aldana Peter Kinch nick Kyprianou

ART & PRODUCTIONdesign prodUction manager Angie gilliesgrapHic designer Alicia Chin

SALES & MARKETINGnational sales manager Trevor Biggssales manager, mortgageBrokernews Scott Clarkemarketing and commUnications Julia ComitaleproJect coordinator Jessica duce

CORPORATEpresident & ceo Tim duceoffice/traffic manager Marni Parkerevents and conference manager Chris davis

Editorial [email protected]

Advertising [email protected]

Subscriptionstel: 416 644 8740 • fax: 413 203 [email protected]

KmI Publishing 312 Adelaide Street West, Suite 800 Toronto, Ontario M5V 1R2mortgagebrokernews.ca

Copyright is reserved throughout. no part of this publication can be reproduced in whole or part without the express permission of the editor. Contributions are invited, but copies of work should be kept, as CMP magazine can accept no responsibility for loss.

SPECIAL EDITION

LENDERGUIDE

CO-BRANDINGWHITE LABELS ADD VALUE FOR BROKERS

COMMERCIALCO-BROKER THE DEAL WITH A SPECIALIST

BUSINESS-FOR-SELFLENDING LANDSCAPESHIFTS FOR BFS CLIENTS

RENTALS OFFERING INVESTORS EXPERT ADVICE

LENDER PRODUCT

GUIDEPAGE 24

the lending landscape for brokers has changed in recent months and bigger changes may be on the way soon.

The B-20 guidelines issued by the Office of the Superintendent of Financial Institutions, which were put out for comment until May 1, are designed to ensure that banks are collecting detailed information about a

borrower’s identity, background, and willingness and ability to pay their debts on time. The rules also deal with due diligence the banks should conduct on the value of properties.

There are several areas that are of particular concern for brokers.OFSI is proposing that loan documentation and underwriting occur “as

applicable for each subsequent renewal or refinancing of the mortgage.” This suggests that borrowers on renewal would have to be requalified. This is not the current practice in Canada and would represent a significant change.

The guidelines also propose “the borrower’s likely income and repayment capacity in retirement” be taken into account when qualifying. This would be additional assessment criteria that underwriters and lenders would have to consider in addition to income, including past income, credit score and other important factors such as location of the property and its value.

The elimination of “cash back” down payments is also addressed where “incentive and rebate payments should not be considered as part of the down payment.”

HELOCs are also on the table, with OSFI proposing that HELOCs be structured more like mortgages and be amortized. While some HELOCs usage might be deemed unwise, many Canadians use the financing to invest in capital markets or even for their own business purposes. Determining how people intend HELOCs could be difficult and hopefully some flexibility will be allowed beyond the proposed 65 per cent threshold.

So, as always, I encourage you to contact us with any news related to the broker and mortgage industry or just to share your opinions on how we’re doing. It is exciting times for our industry and we look forward to helping you and your business navigate them.

Cheers.

John tenpenny, Editor

contact the editor:[email protected]

CONNECT

Times, They are a’changing

FEATURE / whiTE lAbEls

4 | lender guide mAy 2012

White-label products, co-branding partnerships between brokerages and lenders, continue to grow in popularity. CMP explores what they are why these products are key value-adds for brokerages to use as exclusive tools by their brokers

In the mortgage industry, white label is the name given to a product that a lender creates but allows brokerages to rebrand with their own names. In the client’s eyes, this co-branding closely associates the brokerage and the loan, creating an almost bank-like experience.

In Canada, one of the earliest white labels in the industry came from Mortgage Alliance, whose Right Mortgage product was serviced by Macquarie Financial (following Macquarie’s exit, the product has been serviced by Paradigm Quest).

“We started Right Mortgage for a number of reasons,” says Tony Bartolomeo, product manager. “We wanted something to allow Mortgage Alliance agents differentiation in the marketplace, plus we wanted something designed around educating the client about the features of the mortgage.”

Right Mortgage allowed agents and their clients to focus on certain features of the mortgage that were most important to them — anything from pre-approval to LTV — and input those numbers into a calculator, rather than just focusing on the best rate. “If it starts the conversation about different aspects of a mortgage that clients didn’t think about at first, it creates a value-add,” says Bartolomeo. “For the agent, it was something unique they couldn’t get anywhere else — added

value instead of just a different name,” he says.Even though Mortgage Alliance’s Right Mortgage

isn’t technically a white label (for one, it doesn’t share a name with the brokerage, but more on that later), they were an early adopter in working on exclusive relationships with a lender in order to provide their brokers something unique. It’s a trend that has grown since, with many brokerages now offering either a white label or at least having some sort of exclusive relationship deal.

“I think the trend is we’re all trying to figure out how we can create lasting relationships with our customers,” says Ron Swift, CEO of Radius/Mortgage Architects. “As we continue to evolve this industry, those are strategies the superbrokers are looking at. It’s just whether can they do it efficiently, effectively and, because it’s a large expense and a large risk, whether your agents will support a branded company product.”

But Swift also recognizes the merit in such a relationship, as it’s a “great way to create branding,” he says. “Plus, it really helps create a long-term relationship with those clients where you don’t have to worry about cross-selling.”

It’s something Verico understands well — It has had an exclusive relationship with AGF since February of last year.

PRODUCtS

Powerful earning potential? Undeniably.The power to earn is what drives business. And unlike the big banks, we drive business by serving brokers. In fact, our Power Compensation Program™ gives member brokers powerful opportunities to increase their earnings. To us, compensation is more than just a commission. It’s about empowering our brokers with the tools to succeed.

1-888-837-2326 • bwballstarportal.ca

“We had a white label with Macquarie called Verico Mortgage, but we wanted to have another balance sheet lender, which gives more flexibility,” says Sean Widdess, national sales manager. “Plus, working with a trust company that has a balance sheet presents new opportunities that may not have been available with other lenders.”

Widdess says that AGF, which operated in the subprime sector in 2008, approached Verico to re-enter the mortgage industry in the A sector, and “the timing was just right,” he says.

“I guess it comes to all of us wanting to have some kind of differentiator in the marketplace. If we have something in our brand that agents can’t get elsewhere, it attracts them to our business — the more we give them, the more likely they are to stay, and the more likely we will attract the most talented brokers.”

As for having an actual white label like Verico Mortgage again, Widdess points out that there are pros and cons. “We’d have it again if it was extremely unique, and not just to put the name on it. Right now, it’s not a huge necessity to have our brand on the loan.”

thE PROS Edmonton Broker Vaughn Leroux has been “pretty committed” to using Dominion Lending Centre’s white label, Dominion Mortgage, for about two-and-a-half years, he says, and the company points him out as one of its top producers (Leroux says he currently does 25 per cent of his business through the white label).

Dominion Mortgage works in that it notifies the agent every time there is an action, such as a request from the client to pay out the mortgage. The intent is that since 84 per cent of clients renew with the original lender, the mortgage stays with the Dominion agent for as long as possible.

Leroux appreciates that it’s all part of a larger identity. “It’s our internal product so our reputation is aligned with that,” he says. “Clients see us and if we put them in a Dominion Mortgage, it’s similar to calling a bank.”

But like many white labels, the ultimate advantage comes in having a lender that is committed to the client and the broker come renewal time.

“Dominion isn’t the highest paying lender in the market, but I’m more concerned at what happens at renewal,” says Leroux. “We’re going into a situation that

FEATURE / whITE LAbELS

mAy 2012 lenderS guide | 5

if we have

something

in our brand

that agents

can’t get

elsewhere,

it attracts

them to our

business

FEATURE / whiTE lAbEls

6 | lender guide mAy 2012

we haven’t seen in 10 years. It’s going to be difficult to move a product and I want to make sure my clients are going to be with a lender that are competitive on renewal. It’s also a credibility factor. When you’re dealing with a white label mortgage provider you want to be sure they’re committed to the business.”

Another advantage comes with the built-in familiarity between lender and brokerage, which can help with the day-to day, as well as when an otherwise good client happens to not fit in the box.

“The process with other lenders can be a little more convoluted and take a little bit more time. This way, it’s usually same day, which is key for a first-time homebuyer. For them, a two-to-three-day turnaround process is nerve-wracking,” says Leroux, adding that “as [Dominion] gets very comfortable with the quality of clients I send them, which comes with trust and volume, I get a bit of a break, maybe some benefit of the doubt when they see my other clients are quality.”

Swift agrees: “I would expect that there would be potentially greater influence with those arranging the loan to make an exception,” he says, adding that even though Mortgage Architects don’t currently have a white label, “I officially would not say no to that concept if it was adding value and keeping this industry stronger.”

thE CONSDespite the advantages to white labels, there are

always concerns with not only having such a close relationship between a lender and a brokerage, but one that shares a name.

That was something Mortgage Alliance had in mind when it developed Right Mortgage.

“Right Mortgage wasn’t specifically associated to a company, even though clients understood where it was coming from,” says Bartolomeo, adding that they also thought having their name attached to it would limit their ability to offer more than one product.

“If you only created one and it was your name, you would only be committed to one.

How would the second one be different?” he says. “With Mortgage Alliance, the vision is to create additional product names all under one banner. It’s just a matter of having the ability. Right Mortgage is a Right Mortgage product.”

Another advantage to Right Mortgage being a Right Mortgage product, rather than a traditional white label, says Bartolomeo, was proven when Macquarie left the market.

“We had notice when Macquarie left and we were able to partner up quickly so that the service level didn’t drop and the mortgage didn’t change for the customer,” he says. “If you lose a lending partner, you can replace the lender.”

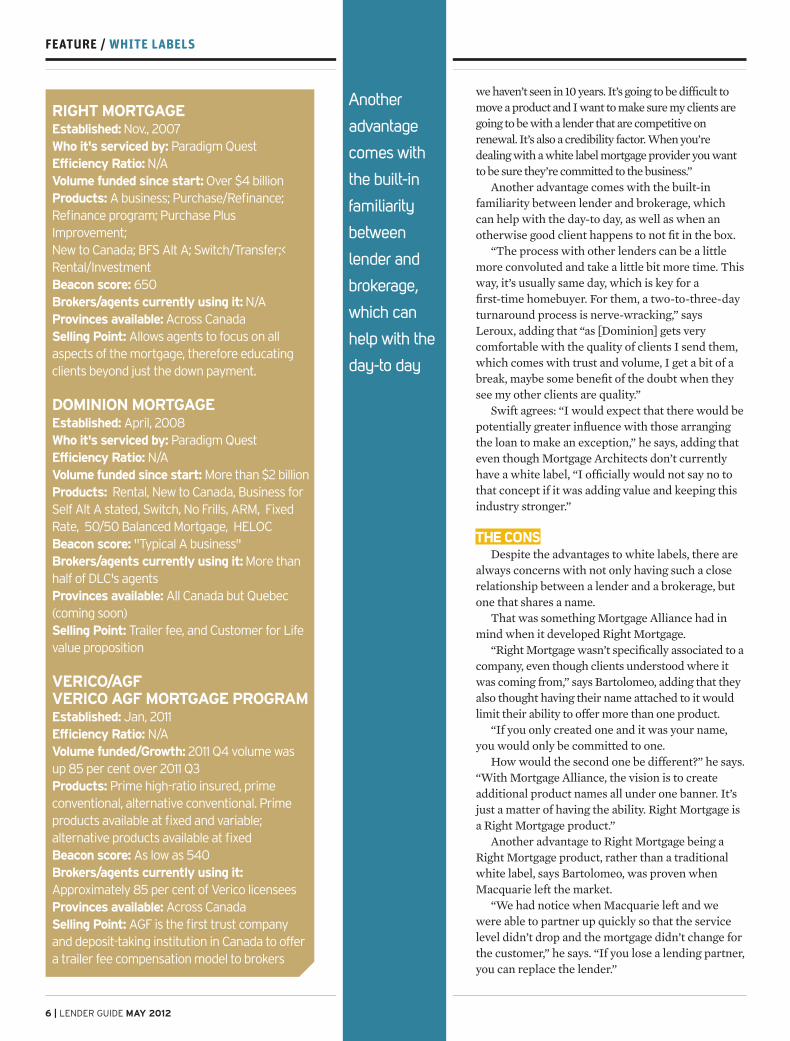

RIGhT mORTGAGEEstablished: Nov., 2007Who it's serviced by: Paradigm Quest Efficiency Ratio: n/AVolume funded since start: Over $4 billionProducts: A business; Purchase/Refinance;Refinance program; Purchase Plusimprovement;new to Canada; BFS Alt A; Switch/Transfer;<rental/investmentBeacon score: 650Brokers/agents currently using it: n/AProvinces available: Across CanadaSelling Point: Allows agents to focus on allaspects of the mortgage, therefore educatingclients beyond just the down payment.

DOmINION mORTGAGEEstablished: April, 2008 Who it's serviced by: Paradigm QuestEfficiency Ratio: n/AVolume funded since start: More than $2 billionProducts: rental, new to Canada, Business forSelf Alt A stated, Switch, no Frills, ArM, Fixedrate, 50/50 Balanced Mortgage, HelOCBeacon score: "Typical A business" Brokers/agents currently using it: More thanhalf of dlC's agentsProvinces available: All Canada but Quebec(coming soon) Selling Point: Trailer fee, and Customer for lifevalue proposition

VERICO/AGFVERICO AGF mORTGAGE PROGRAmEstablished: Jan, 2011Efficiency Ratio: n/A Volume funded/Growth: 2011 Q4 volume wasup 85 per cent over 2011 Q3 Products: Prime high-ratio insured, primeconventional, alternative conventional. Primeproducts available at fixed and variable;alternative products available at fixedBeacon score: As low as 540 Brokers/agents currently using it:Approximately 85 per cent of Verico licensees Provinces available: Across Canada Selling Point: AGF is the first trust companyand deposit-taking institution in Canada to offera trailer fee compensation model to brokers

another

advantage

comes with

the built-in

familiarity

between

lender and

brokerage,

which can

help with the

day-to day

FEATURE / whiTE lAbEls

mAy 2012 lender guide | 7

ONTARIO/QUÉBECT: 1.866.407.0004F: 1.866.407.5859

WESTERN CANADAT: 1.866.940.1201F: 1.888.440.1201

Everyone talks about service.Equitable delivers.It’s a team approach to lending.Open conversation.Partnership success.Unique, in an otherwise compartmentalized world, means Equitable can see & hear what others often miss... ...Client Circumstance.

We specialize in business-for-self, newcomers and credit challenged clients who want to be heard. Let’s talk today.

www.equitabletrust.com

CMPAd_HalfPg_SE_CLG_2012.indd 1 12-04-24 11:02 AM

Which brings up another concern — what happens when the lender your brokerage is so closely associated with either does something wrong, or in the worst-case scenario, exits the market?

“You sometimes could wear any issues that a lender may have,” says Widdess. “If you put your name on something, good or bad, the clients are going to want to come back and talk to you about it. If it’s not positive, the first thing they do is call you.”

On top of that, as a brokerage, says Widdess, “you have a responsibility to ensure your brokers feel that it’s working. You’ve licensed your name to a lender, but you’re not that lending company. There’s risk and opportunity, but when the mistake is out of your control there is an inherent risk there.”

“Because you’re relying on third parties,” adds Swift, “you have to make sure they’re doing a good job. If they do a poor job it reflects back on you. It’s a mortgage like any other mortgage, so is it a good product and are service levels high?”

And, of course, there’s the conflict of interest issue for brokers when it comes to selling a product so closely associated with your own brand.

“As brokers we always pride ourselves on

offering unbiased choice to consumers,” says Swift. “When you start offering your own products, you have to make sure you’re disclosing it properly, that the client understands the relationship and that they know how it’s working.”

Nothing less than your reputation is on the line, he adds.

“The product needs to be competitive and truly adding value to consumers, hopefully not something that is taking away from the consumer but adding to the agent.”

With even more brokerages adding white labels or establishing other types of exclusive relationships with lenders, it’s clear that the trend is moving toward lenders cozying up with brokerages that treat them right, whether or not that brokerage’s name is actually on the product being sold.

“We’re definitely seeing more preferred relationships” says Widdess. “White label or not, I wouldn’t be surprised if every national brokerage had a private relationship with a lender. And if that benefits the customer and benefits the broker, then I don’t see that as a bad thing.”

FEATURE / BFS LEnding

8 | lender guide mAy 2012

Recent concerns about mortgage insurance funding by CMHC has caused lenders to either pull back or exit completely from the business-for-self mortgage market. While there is cause for concern, brokers and lenders say homes can still be found for these mortgages

thE BIG ShIFt

In recent months some lenders in the broker channel have made a hasty retreat from the NIQ space, limiting funding options for brokers and their BFS and stated-income clients.

Their departure, kicked off by FirstLine’s decision to axe BFS lending, came after CMHC signalled it would ration access to bulk insurance for their conventional loans as the Crown corporation neared its $600-billion funding cap. Monolines are most likely to be affected because they rely on that insurance to facilitate the securitization and sale of those mortgages – a way of taking them off their books and freeing up cash for more lending.

TD, the country’s second-largest lender, stopped originating non-prime residential mortgages as of March 31. The loans, offered through TD Financing Services Home Inc., represented about 0.2 per cent of the bank’s mortgage portfolio, according to spokesman Mohammed Nakhooda.

Although the bank said it would continue to accept business-for-self business, it now requires brokers have to input all stated gross income, complete asset and liability details for equity clients regardless of loan-to-value thresholds. It has also capped loan-to-value at 75 per cent.

Calls for federally regulated lenders to better vet

their underwriting, specifically BFS, have also had a chilling effect across much of the broker channel.

But it shouldn’t lead to a spike in borrowing costs, says Lester Shore, VP of Optimum. “It’s not an oligopoly here,” he says, referring to the broker channel’s handful of Alt A institutions. “Yes, we are seeing A lenders retrench and move out of the Alt A space, but their departure won’t drive up rates, because we have enough alternative lenders in the space to ensure competition.”

Still, all of those factors are poised to grow business for Optimum and other alternative lenders as an increasing number of Canadians seek that type of mortgage funding and A lenders are unable or unwilling to service them.

“It does represent a good opportunity for us in that the big guys have stepped back,” said Shore.

Home Trust is backing up that assessment and views the channel’s retreat from business-for-self lending as a potential boon for its own book.

“We have also made tweaks in our underwriting,” said CEO Gerald Soloway. But “we see incrementally more business coming to us as those (BFS deals) are shut down by the various lenders. We feel that is a very positive trend for Home.

“We see opportunities with people that are really high-calibre borrowers with good proof of income,

Think reverse mortgages are expensive?

Think again!

CHIP Home Income Plan is provided by HomEquity Bank, a Schedule I Canadian Bank. HomEquity Bank is a wholly-owned subsidiary of HOMEQ Corporation, a TSX-listed company. TM Trademark of HomEquity Bank.

With CHIP Home Income Plan’s new low rates, homeowners 55+ can now access up to 50% of their home equity at rates comparable to other home equity lending products.

But unlike these other products, with the CHIP solution:

• no payments are required, until homeowners choose to move or sell

• no income, credit or medical qualifications are needed

• funds can be received as a lump sum or over time, giving your clients the flexibility they need

In addition, clients maintain ownership and control of their home.

Why not tap into the potential of the growing seniors market and recommend CHIP? You’ll receive a referral fee, and we’ll look after all the paperwork for you.

To find out more, or to partner with CHIP, contact us:

1-866-536-2447www.chipadvisor.ca

7.1_ThisTime.indd 31 12-01-18 10:46 PM

FEATURE / BFS LEnding

10 | lender guide mAy 2012

kim luxton lester shore Martin reid

this month’s guests

but their circumstances are a little different. We haven’t had to go down the credit scale; we’ve been able to go up the credit scale, which is an unusual phenomenon.”

Home Trust said it’s capturing mortgage business from Canadian lenders that are retreating from the non-prime market amid signs of a housing downturn.

“The big banks are sort of juggling around their mortgage strategy and as part of that, they’re tightening up in certain areas,” said Home Trust President Martin Reid. “We’re seeing some of the fallout.”

“It may be slow and gradual, but I think we’re seeing a return to the 1980s when there was a greater distinction between A and B lending,” says James Robinson, an agent with The Mortgage Centre Mortgage Watch Inc. in Toronto. “Home Trust is likely to be the winner in all this.”

With so much information surrounding the Canadian debt-to-income ratios on top of interest rates bottoming out, there is increased pressure on financial institutions to be proactive about putting measures in place now to prepare for a rise in rates, says Kim Luxton, director, broker sales with ING DIRECT.

“Equity-type products can have potential to increase risk for both consumers as well as lending institutions,” she says. “Equity is valuable for net worth but we all know that equity doesn’t pay the bills and should not be the only qualifier for a mortgage. Canadians that are business-for-self will still have the ability to borrow through the insurers “Alt A” programs that are available after reasonability of income has been established.”

While Luxton says there is no doubt that there are less specialty products today for brokers to offer, they are still out there. The challenge brokers, coming out of an environment of low rates, she says, will be to prepare applicants who are looking for an equity-based product for higher rates.

“Knowledge is power and educating clients on affordability, in particular if interest rates rise by as much as three per cent, can further heighten the

value of dealing with an experienced mortgage broker in the clients’ eyes,” she says. If ING’s volume with its stated-income products are any indication, there is still plenty of business for brokers.

Monoline lender Merix Financial recently made some changes to its business-for-self lending, while at the same time assuring brokers it will continue to offer the product.

“It was important to Merix to continue to offer those products – BFS and Rental – so originators can continue to offer them to their clients,” said Jason Kay, the lender’s VP of corporate development and sales. “We don’t want to be known just for BFS and rental product, but want all of an originator’s business.”

For LTVs greater than 65 per cent but less than 80 per cent, customers will now pay the insurance premium, according to Merix. The BFS interest rate premium will be reduced to 5 bps from 20 bps. BFS clients with LTVs less than 65 per cent won’t need to insure, although will also benefit from that slash to the interest premium. For its clients that will have to buy insurance, Merix is also allowing them to tab the default insurance premium onto the mortgage amount.

“While some clients will have to pay more, from a cash flow perspective, it is relatively neutral compared to costs before the changes,” says Kay.

Some brokers say they are turning to second mortgages to service BFS clients left stranded by retreating A players.

“I think fears about the end of that business have been exaggerated,” says Rick Caron, an agent with Verico The Mortgage Professionals in Gananoque, Ont. “Self-employed are always going to find money, but what’s happening is that brokers are having to get more creative with those deals.”

Increasingly, that means arranging a prime-rate mortgage with an A lender willing to go as high as 65 per cent LTV for a stated-income client. Caron and others are then arranging a second mortgage for as much as 15 per cent of the value of the mortgage

FEATURE / BFS LEnding

mAy 2012 lender guide | 11

$600billion - CmhC mortgage insurance cap, up $250 billion since 2007

STATS

TrusT. Leadership. performance.

© 2012 equity financial Trust company

A new spirit in mortgage lendingDedicated to mortgage brokers

at equity financial mortgage services we deliver a new level of responsiveness and common sense lending to the ontario mortgage broker community.

EquityFinancialTrust.com/Mortgage Toll Free: 1.866.393.4891

with alternative lender offering B rates, or, if push comes to shove, a private lender demanding slightly higher rates.

Those second loans are for terms of one or two years, according to Caron, but are essential for brokers looking to fill the funding gap left by the industry’s move away from BFS lending.

However, his more creative solution may not be for every self-employed. The interest rates attached to those second mortgages means clients need to have strong exit strategies that will allow them to retire that debt. “They’re a short-term thing,” said Caron.

Credit unions are also hoping the retreat of some lenders from the BFS arena will be their gain, as Ontario’s largest player actively reaching out to brokers seeking a new home for BFS clients.

“This really is an opportunity for brokers to take a look at other lenders,” says Robert Leaker, VP of emerging markets for Meridian Credit Union. “And quite frankly we are that other lender, with the products, the services and the common-sense lending guidelines to accommodate that business.”

If Leaker gets his way some of that growth will

come directly from self-employed borrower deals brokers would otherwise have taken to lenders who have now left the space or scaled back their offerings.

Meridian’s self-employed terms are increasingly hard to come by: no automatic interest rate premium for clients with beacon scores above 600 and there’s no mortgage insurance requirement.

“We don’t do high ratio,” Chris Fontana, manager of Meridian’s broker Unit, “and we may or may not bulk insure a loan ourselves, but the member doesn’t pay it.”

Still, some brokers worry the loss of high-ratio mortgages for self-employeds might limit both the professional and personal ambitions of mortgage professionals.

“We had already seen Scotia move to limit those mortgages to five-year terms, and recently one of the few monolines offering those mortgages told me that they were no longer considering them for the rest of the year and next year only on a case-by-case basis,” says Michael Marini, a mortgage agent with Dominion Lending Centres Funds in Toronto. “Even then, the application would have to be with them for

FEATURE / BFS LEnding

12 | lender guide mAy 2012

Being asked to work magic? n Seeing more customers with challenging income and credit situations?n Having difficulty with “out-of-the-box” applications?n Frustrated with restrictive lending criteria?n Ready to expand your client base beyond the traditional borrower?

We are the home of Sensible Lending® and have mortgage options suitable for most borrowers. (TSX:CWB)

Questions? Comments? Deals? Contact your regional business development manager or our underwriting centre at 866.441.3775

Serving brokers in Alberta, British Columbia, Manitoba, Ontario, and Saskatchewan. 866.441.3775 www.OptimumMortgage.ca

a minimum of five days.”Marini and others are pointing the finger at

default insurers suggesting their appetite for high-ratio BFS deals has effectively disappeared, something possibly owing to concerns around exposure to fraud and a possible market correction and economic downturn.

That explains the higher down payment requirements and insurance costs, but even with those buffers, fewer and fewer lenders appear willing or able to offer prime rates to BFS – including mortgage brokers themselves.

Marini is among those concerned that lenders are simply finding it hard to get those loans insured. The reluctance has everything to do with more conservative underwriting by the sole default insurer now serving that niche market, argue some brokers.

The loss of that type of loan would effectively leave BFS clients with little choice but to go conventional. It’s something few have wanted to do in order to capitalize on low interest rates and invest their money into growing their businesses.

Marini’s concerns mirror those of other brokers from across the country who are now seeing the pendulum swing back from the dark days of 2007/8 when broker channel lenders had all but closed their doors to non-income qualifying mortgages. But while banks and monolines are increasingly willing to fund those deals at prime rates, they are still demanding default insurer backing.

That’s where brokers are hitting a snag, said broker Vittorio Oliverio with Centum Professional Mortgage Group. He works the entrepreneurial-rich Alberta market where the business-for-self market is viewed as a key growth area for brokers looking to grow originations in a slowing market. The statistics back them up with more than 22 per cent of Canadians now self-employed, among them mortgage brokers.

“The change means that many of us will be challenged to get a mortgage as well,” said Marini, fearful 2012 will see it become nearly impossible for self-employeds to win high-ratio mortgages at the rates of their salaried counterparts.

fewer and fewer lenders appear willing or able to offer prime rates to bfs

profile / home trust

mAy 2012 lender guide | 13

BUSINESS-FOR-SELF CANADIANS PRESENt BIG OPPORtUNItIESBrokers often turn away from this type of business because they aren’t sure how to evaluate or even put together a solution for this type of customer. But all it really takes is a more flexible type of approach

Think Business-for-Self (BFS) Canadians aren’t worth your time (particularly those who are ‘stated income’ BFS)? Think again. Fact is, the potential customers in this steadily increasing sector have a proven track record of solid performance and are no different than a salaried customer. They just happen to be in business for themselves.

Being in business-for-self is a decision that more and more Canadians are making every year. The numbers say it all: this market has shown a steady two per cent in growth/year since 1983 and is showing no signs of slowing down. In 2011, there were 2,670,000 self-employed Canadians, representing 14 per cent of the labour force. This growing group is wildly underserved by the major banks when it comes to meeting their financial needs with lending products. And that can add up to a lot of business opportunity for those brokers willing to think a little outside of the box while providing lending solutions.

This is where a trusted lending partner like Home Trust can help.

“As a niche lender, Home Trust has been providing alternative lending solutions for these customers for 25 years,” explains Pino Decina, SVP, Mortgage Lending at Home Trust. “Brokers often turn away from this type of business because they aren’t sure how to evaluate or

even put together a solution for this type of customer. But all it really takes is a more flexible type of approach.”

StARt By GEttING tO kNOw yOUR CUStOMER. Do your due diligence by getting to know your customer’s business. Take a proactive interest in their business, the market, their short- and long-term goals. Understanding this will help you know what to ask and how to assess the risk associated with taking this customer on.

kNOw thAt LENDING CRItERIA wILL vARy. Every deal in the BFS space can be different, and the requirements to satisfy a lender’s criteria may vary. But the payoffs for this bit of extra effort are huge: you are providing a solution for your customer and in the process, building a relationship. And that relationship can lead to future business on other investment or lending products down the road.

RECOGNIzE thAt POtENtIAL RISk CAN BE MItIGAtED. When adjudicated under a proprietary lending model, the possibility of risk is mitigated. An overwhelming majority of BFS customers will actually be found to perform at the same level as a salaried client.

SEE yOUR BFS CUStOMER AS A wAy tO tAP INtO thE BFS NEtwORk. People socialize and do business with like-minded individuals. So there’s a very good chance that your BFS customer is connected to a network of other BFS individuals. People are likely to recommend those who provide them with great products and services. And that can translate into a lot of potential new business leads, with minimum effort on your part.

Still not sure whether you want to take on a BFS customer?

Consider these 3 possible outcomes when faced with the potential:

1. turning away from the opportunity= $0 revenue for you2. co-broker with someone who has experience = $ You enjoy shared revenue3. take it on yourself by engaging the services of a lender like Home trust= $$ You capture all the revenue

In closing, think about this: approximately 15,000 active brokers across Canada could provide an alternative financing solution for BFS customers. If you don’t take an active interest in providing one, somebody else will.

Pino Decina

FEATURE / COMMERCIAL LENDING

StEPPING

14 | lender guide mAy 2012

If you’re a residential agent who wants to handle your commercial referrals, it’s essential to seek out a commercial specialist willing to co-broker the deal says industry veteran Dale Bilton

StEPPING

mAy 2012 lender guide | 15

FEATURE / commERciAl lEnding

16 | lender guide mAy 2012

There are many critical steps residential agents can follow in order to become more successful in, and proficient at, getting involved with commercial brokering.

The most important step is to ensure residential agents don’t

try to pass themselves off as commercial specialists if they lack the required commercial lending background, experience and knowledge to put the deal together. A commercial Realtor or commercial buyer will quickly see through this lack of knowledge and the residential agent’s credibility will immediately be lost and the Realtor or client will move on. After all, you only have one shot at making the right first impression.

When a residential agent receives an inquiry to arrange financing for a commercial purchase of a business owner occupied property or an investment property such as an apartment building, plaza or industrial building, for instance, the basic requirements to start the deal are similar to the residential realm, but the lenders in most cases will be completely different.

The majority of brokerage firms want their residential agents to work 100 per cent on the type of brokering they’ve been trained in – residential – and recommend co-brokering the deal with a commercial agent they know and trust. That said, it’s still important to know the multiple steps involved in putting together a commercial deal.

9.2%8.3%7.6% - overall canadian office vacancy rate in 2009, 2010 2011. Source:Avison Young

STATS

the majority of brokerage firms want their residential agents to work 100 per cent on the type of brokering they’ve been trained in – residential – and recommend co-brokering the deal with a commercial agent they know and trust

Dale Bilton

LEARNING thE COMMERCIAL StEPS It’s important to carefully listen to the commercial request and ask if there is an MLS listing or an old appraisal available for the property. This listing will often offer a good description of the property and its buildings.

Hopefully there is also an income/expense recap of the operation and a current rent roll. Find out what the buyer is prepared to pay and ask how much they actually have or can raise in cash to invest into it, just to get a general overview of what they can afford to inject.

At this point, it’s important to never estimate how much you think you can arrange or what the interest rate will be, as this approach is sure to backfire on you.

Instead, start your work with a commercial financing partner who specializes in commercial mortgages and (who will give you a percentage of the fees earned). You want to get him or her involved at the onset of the deal. Jointly you can call the buyer so you can introduce the commercial specialist and explain he/she is your commercial financing resource and will be handling the deal moving forward.

At this stage, once the initial information has been reviewed (the real estate listing and any other info that has been provided), the commercial specialist will determine the buyer’s knowledge of the commercial industry in which they’re looking to invest to ensure there’s a good fit.

If an offer has not yet been completed, this needs to be coordinated to ensure an acceptable purchase can be worked out. The offer needs to allow adequate time for due diligence to be carried out. In most cases, at least a full month is required. But if the deal is for an apartment building and the mortgage is going to be CMHC insured, a minimum of 35-40 days is required to meet conditions.

One of the next priorities involves finding out if the property has any environmental issues. Has there ever been a gas station in the immediate area or any business that may have created concerns? The commercial expert will explain to the client that a Phase One environmental report will be needed in most cases for any commercial lenders, and this is also a good requirement for any investor to be sure the property is clean of contamination. If there are any concerns raised with the Phase One, a Phase Two report will be required. This involves holes being drilled to confirm if the property has issues. A Phase 2 will take an additional month to complete and is also fairly expensive.

It’s important to note that you don’t want the buyer to order an environmental report until a

FEATURE / commERciAl lEnding

mAy 2012 lender guide | 17

lender has been secured, as it’s important to ensure the environmental firm is approved by the actual lender. So, at this stage, the commercial specialist will request and review the buyer’s financial statements, while also presenting the deal to a number of suitable commercial lenders that lend on this type of property, to see who has the most suitable offer for the buyer.

As it takes a while to establish a solid list of and working relationship with commercial lenders, this is where it becomes extremely difficult for a residential expert to complete the deal alone.

An experienced commercial broker will have an extensive list of, and relationship with, suitable commercial lenders and will know precisely what type of deals fit with each lender.

Once a commitment is obtained, the environmental report and the AACI appraisal can commence, as the lender will offer a list of approved consultants..

Once all conditions are met and the offer is firmed up, the commercial specialist’s job is still not complete. The specialist then needs to ensure the lawyer has received all required information from

the lender. The lawyer will typically need two weeks to complete the file. A brokerage agreement must be in place so the lawyer will pay your commission from the closing proceeds.

Because of the above extensive list of steps, it’s not uncommon for a commercial deal to take six to 12 months to complete, and sometimes longer.

The commercial brokering world has a lot of room for growth, but only the experienced seem to survive. So, if you’re a residential agent who wants to control who handles your commercial referrals, it’s essential to seek out a commercial specialist willing to co-broker the deal with someone trustworthy that has a stellar reputation in the commercial brokering industry.

dale Bilton is a veteran commercial mortgage agent,

president of dominion lending centres commercial and

residential mortgages ltd., and handles all eastern

commercial referrals on behalf of the dominion lending

centres inc. commercial division. He has successfully

funded more than half a billion dollars in commercial

mortgages throughout his well-established career.

In today’s market,you need a partnernot a competitor.

Canadians need choices when it comes tohome ownership and Street Capital knowsthat every deal is unique. That’s why we offer brokers a full range of flexible mortgageproducts to close more deals.

The new Street Options Program is an alter-native lending program assisting borrowerswho don’t meet traditional prime businesslending guidelines.

• Self-employed

• New to Canada

• Applicants with imperfect credit history or bankruptcy

More than ever, Canadians are shopping forthe ideal mortgage. Our job is to help yougrow your market share. To provide brokerswith a significant competitive advantage, we offer:

• Competitive rates

• More compensation choices with Street and Street Loyalty Programs

• Superior customer service

• A broad range of prime and near-primemortgage products

• Status programs with unique advantages

Tel: 647.259.7873 • Toll Free: 1.877.416.7873 • www.streetcapital.ca™ Trademark of Street Capital Financial Corporation. FSCO Licence No. 11428

Street Capital’s broader lending programs will give you the advantage.

To learn more about how Street Capital programs can work for you, contact your local RVP today.

“I often work withclients who are self-employed. Now I have a mortgage solution that will suit them.”

– Sandra Taylor, Broker

“I need a lending partnerthat can offer mortgagesolutions to all myclients, no matter whattheir situation.”

– Tom Rindler, Broker

BROKER FOCUSED. BROKER LOYAL.

SC_Options_2pg_ad_CMP_FNL 5/8/12 2:24 PM Page 1

In today’s market,you need a partnernot a competitor.

Canadians need choices when it comes tohome ownership and Street Capital knowsthat every deal is unique. That’s why we offer brokers a full range of flexible mortgageproducts to close more deals.

The new Street Options Program is an alter-native lending program assisting borrowerswho don’t meet traditional prime businesslending guidelines.

• Self-employed

• New to Canada

• Applicants with imperfect credit history or bankruptcy

More than ever, Canadians are shopping forthe ideal mortgage. Our job is to help yougrow your market share. To provide brokerswith a significant competitive advantage, we offer:

• Competitive rates

• More compensation choices with Street and Street Loyalty Programs

• Superior customer service

• A broad range of prime and near-primemortgage products

• Status programs with unique advantages

Tel: 647.259.7873 • Toll Free: 1.877.416.7873 • www.streetcapital.ca™ Trademark of Street Capital Financial Corporation. FSCO Licence No. 11428

Street Capital’s broader lending programs will give you the advantage.

To learn more about how Street Capital programs can work for you, contact your local RVP today.

“I often work withclients who are self-employed. Now I have a mortgage solution that will suit them.”

– Sandra Taylor, Broker

“I need a lending partnerthat can offer mortgagesolutions to all myclients, no matter whattheir situation.”

– Tom Rindler, Broker

BROKER FOCUSED. BROKER LOYAL.

SC_Options_2pg_ad_CMP_FNL 5/8/12 2:24 PM Page 1

FEATURE / REnTAl PRogRAms

20 | lender guide mAy 2012

Rental R

FEATURE / REnTAl PRogRAms

mAy 2012 lender guide | 21

For real estate investors, the need for broker expertise has never been greater, and that presents a whole new set of opportunities for mortgage professionals educated on today’s rental programs

As the axe fell on stated-income programs this year, it also sliced through another bread-and-butter segment for brokers.

“Investor clients, or those relying on rental programs, used to be 20 per cent to 25 per cent of my book,” Vancouver broker Jeff Trounsell, with Centum Pacific Mortgages, tells CMP. “It now represents about 15 per cent of it.”

That’s a relatively modest chop compared to those suffered by some of the channel’s biggest monolines. Those would have, in most cases, been self-inflicted – an effort by lenders to tighten up guidelines before federal regulators did it for them.

In February, CMHC warned that their access to its $600-billion insurance fund would be rationed as the Crown corp. approaches the limits of that funding. Government hasn’t yet agreed to raise the ceiling.

The decision was world-changing for monolines

who used that fund to bulk insure their conventional loans in order to pass them on as mortgage securities to investors. That avenue to getting those loans off their books and freeing up space to write new ones had virtually disappeared.

Adding to the decision by some lenders to cut the rental and BFS lending they’d now have difficulty insuring they were warnings coming from the federal regulator of Canada’s banking industry.

That same month, documents from The Office of the Superintendent of Financial Services revealed its concerns about liberal lending practices at lenders across the sector. Proposed guideline changes, now before brokers for comment, threaten to tighten up those standards, giving some lenders another reason to shy away from the rental programs that property investors rely on.

But the death of rental programs at some monolines wasn’t quite the straw that broke the

E-th Nk

channel’s back, says one broker working with investor clients. The premium many of those mortgage lenders attach to rental properties has been a much bigger factor in deciding which of the remaining lenders get those deals.

“In general, if you have a client that can be approved by both a major bank and a monoline lender for an investment property, it certainly doesn’t make sense to have the client pay a premium on the rate or pay an insurance premium with the monoline lender,” Dave Butler of Verico Butler Mortgages, tells CMP. “I use monoline lenders all the time – they are very important to our industry.

“But if I am comparing apples to apples for a client that can be approved by both types of lenders, it is a no-brainer to get your client a better overall package and that is present with a major bank such as National Bank or Scotia.”

That’s increasingly the case after several monolines signalled their intentions earlier this year to back away from the rental market. The move, made in tandem with their retreat from BFS programs, has actually benefited banks, which continue to take those deals and keep them on their books.

The monolines’ move to severely curtail their own rental product is the direct result of that CMHC decision to ration bulk insurance.

Make no mistake, suggests Butler, banks have

been the most obvious beneficiaries even as they too apply more conservative guidelines to that lending, especially around condo investments.

“Even with the latest changes to Scotia’s pricing on rental properties, adding 0.20 per cent to their fixed rate and variable rate,” says Butler. “The rate still ends up being better than those offered by monoline lenders who incorporate the insurance premium into the rate.

“For those monoline lenders that give their lowest rate on rentals but charge an insurance premium to the client instead of pricing it in the rate, the premium paid by the client ends up adding to more than the savings that was had in the lower rate compared to the major bank.”

Still, the monolines haven’t entirely left the game, even as other broker lenders become stronger players because of rental offsets.

The recent changes have had an effect, certainly,” says Trounsell, “but rental offsets have been much more important in determining where I take clients. Credit unions, at least in Vancouver, are doing 80 per cent rental offsets where the banks and the monolines are ranging between 50 and 70.”

“The 80 per cent rental offset is favoured by brokers because it allowed their client easier qualifying and greater purchasing power,” Sebastien Ballin, an agent with Mortgage Alliance - Mortgagelinx Financial Corp., says. “What we

FEATURE / RENTAL PROGRAMS

22 | lenderS guide mAy 2012

Dave ButlerJeff Trounsell

the 80 per

cent rental

offset is

favoured

by brokers

because it

allowed their

client easier

qualifying

and greater

purchasing

power

FEATURE / REnTAl PRogRAms

mAy 2012 lender guide | 23

started to see post-April 2010, when CMHC introduced the changes to the rental program, was that it became more challenging to find lenders willing to use the offset, with most of them instead opting for a 50 per cent add-back onto the client’s total income.”

Here again, charge some brokers, monolines have placed themselves at a disadvantage, whether intentionally or otherwise, with offsets routinely lower than some of the more aggressive credit unions.

They are generally on par with the banks, though, said Trounsell.

But property investors may be justified in feeling deserted as other restrictions impact just what they can qualify for without heading into the private lending sphere and confronting its higher interest rates.

“While we’re looking for rental income that is 10 per cent higher than the carrying cost of that property,” Harry Singh, manager of residential sales for Equitable Trust, tells CMP, “we are trying to cap the maximum number of properties a borrower can have, including the property they’re coming to us to provide financing for, at four or below.”

The leading alternative lender isn’t alone, with most monolines and, indeed, banks applying a similar ceiling of four to five properties to their own borrower applications. Equitable also puts a 0.20

Sebastien Ballin Nawar Naji

per cent premium on its rental rates.Still, the terms for condominium investors are

even steeper, if, in fact, lenders are still willing to go there.

That’s an increasingly a big if.With both the federal government and the

Central Bank predicting the condo market would be the epicentre of any housing correction to come, lenders have started to limit their exposure to those properties.

“The concern is that investors, in particular, may find that they owe more on the property that its worth if a correction happens,” says Nawar Naji, with Verico The Mortgage Wellness Group. “That means that where they may be willing to fund owner-occupieds, they may not be willing to do it for investors.”

The thinking reflects concerns Canada could see investors follow the lead of American homeowners, many of who swam away from their homes as they went “underwater.”

The market down south is still recovering from that highly publicized chop to its economy. Canada, and its lenders, is keen to escape the same axe.

FEATURE / lEndER pRodUcT gUidE

24 | lender guide mAy 2012

LENDER PRODUCt PURPOSE OF FUNDS MORtGAGE AMOUNt AMORtIzAtION tERMS PAyMENt FREQUENCy PRE-APPROvALS LOAN tO vALUE BEACON GDS/tDS PREPAyMENt PREPAyMENt PENALty PORtABILIty OthER

BRIDGEwAtER BANk

Insured fixed rate Purchase, plus improvements; refinance plus improvements; rent-als; new constrution

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year, fixed, closed

Monthly, bi-weekly, semi-monthly, weekly and accelerated

no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

Up to 20% of original principal or the new term principal, paid annually with min. payment of $500; regular mortgage payment increased up to 20% during term

the greater of either 3 months interest and the IRD ased on the difference between the mortgage interest rate and the yield on a Government of Canada Bond with a similar remaining term, plus 0.75%

straight port only; no blend and/or extend available; port and decrease - client to payout difference; port and increase - done as a second mortgage

Ri-fi express equity take out; debt consolidation; refinances with improvements

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year, fixed, closed

See above no Owner occupied refinace 1-4 units max. 85%; non-owner occupied refinance 1-4 units max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

Reno-for-more purchase plus improvements; refinance plus improvements

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

, 2, 3, 4, 5 or 10 year, fixed, closed

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

Progress advance new construction: residential builder, general contractor, acting contractor, acting as own contrac-tor; Interest rate: Prime +3% during construction

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

Construction must be com-pleted according to the draw schedule

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; rentals max. 80%

Min. 610 15% overrun must be available in ratio, liquid assets or line of credit

n/a See above n/a

Rental Property purchase; purchase plus improve-ments; refinance; new construction

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

5 year, fixed, closed

See above no non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 660; Min. personal net worth of $50,000; no worse that R2 rating over past 24 months

710 beacon score=no GDS, tDS 44%; 709<beacon score=GDS 35%, tDS 42%; 50% add on=(PItH + other debt service cost)/Gross annual income

Up to 20% of original principal or the new term principal, paid annually with min. payment of $500; regular mortgage payment increased up to 20% during term

See above straight port only; no blend and/or extend available; port and decrease - client to payout difference; port and increase - done as a second mortgage

Second / vacation home purchase; purchase plus improve-ments; refinance; new construction

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year fixed, closed

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied refinance 1-2 units max. 85%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

Welcome to Canada Purchase; purchase plus improve-ments; refinance

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year fixed, closed

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%

Min. 610 will accept reject beacons with alternate credit sources for co-borrower(s)

GDS 35%, tDS 42% See above See above See above

Second mortgage equity take out; port with increase; debt consolidation; first mortgage must be with Bridgewater

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years; must match remain-ing amortization of first mortgage

1-5 year fixed, closed; must match remaining term of first mortgage

See above no Max. 95% owner occupied; max. 80% non-owner occupied; owner occupied Port 1-2 units max. 95%; owner occu-pied Port 3-4 units max. 90%; owner occupied etO/Refinance max. 85%; non-owner occupied max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

State income (exclusive to Power Compensation Brokers)

Purchase plus improvements; refinance plus improvement; new construction; interest rate: market term rate +30bps; CMHC stated eligibility

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years; min. 16 years

1, 2, 3, 4, 5 or 10 year fixed, closed

See above no Owner occupied purchase 1-2 units max. 90%; owner occupied refinance 1-2 units max. 85%

Min. 650 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

adjustabel rate mortgage (ex-clusive to Power Compensation Brokers)

Purchase; refinance Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years; min. 16 years

3 year closed with option to convert to 3 or 5 year fixed

Monthly only available for the 1st of each month

no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 650; no worse than R2 rating over past 24 months

Bank of Canada 5 year benchmark rate used for qualify-ing; 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above 3 months interest See above

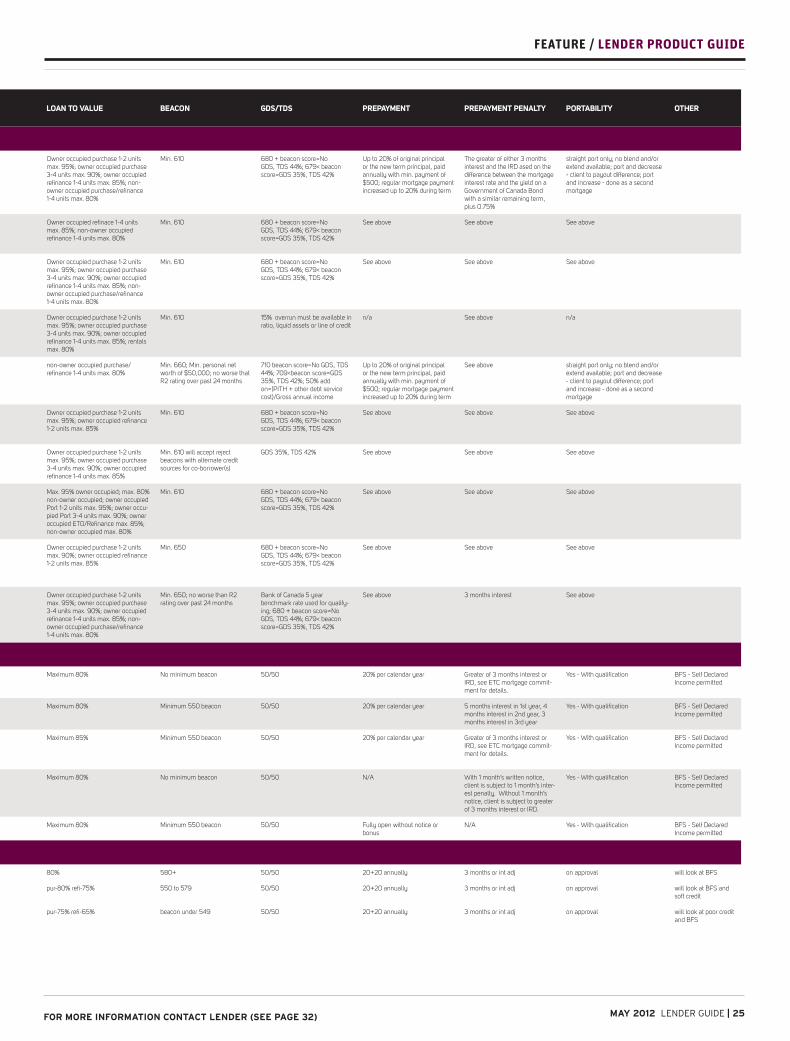

EQUItABLE tRUSt COMPANy

Fixed Rate Mortgage Purchase, Refinance & Rentals Scaled lending amounts 30 years 1 to 5 year terms Monthly, bi-weekly or semi-monthly

no Maximum 80% no minimum beacon 50/50 20% per calendar year Greater of 3 months interest or IRD, see etC mortgage commit-ment for details.

Yes - With qualification BFS - Self Declared Income permitted

aRM Purchase, Refinance & Rentals Scaled lending amounts 30 years 3 and 5 year terms only

Monthly no Maximum 80% Minimum 550 beacon 50/50 20% per calendar year 5 months interest in 1st year, 4 months interest in 2nd year, 3 months interest in 3rd year

Yes - With qualification BFS - Self Declared Income permitted

Yes You Can - High Ratio Purchase or Refinance * Rentals-On

Scaled lending amounts 30 years *Western Canada 1 & 2 year terms, Ontario 1, 2 & 3 year terms

Monthly no Maximum 85% Minimum 550 beacon 50/50 20% per calendar year Greater of 3 months interest or IRD, see etC mortgage commit-ment for details.

Yes - With qualification BFS - Self Declared Income permitted

1+1 Option Purchase, Refinance & Rentals Scaled lending amounts 30 years 1 year term Monthly, bi-weekly or semi-monthly

no Maximum 80% no minimum beacon 50/50 n/a With 1 month’s written notice, client is subject to 1 month’s inter-est penalty. Without 1 month’s notice, client is subject to greater of 3 months interest or IRD.

Yes - With qualification BFS - Self Declared Income permitted

Ultimate Open Purchase, Refinance & Rentals Scaled lending amounts 30 years 1 year term Monthly, bi-weekly or semi-monthly

no Maximum 80% Minimum 550 beacon 50/50 Fully open without notice or bonus

n/a Yes - With qualification BFS - Self Declared Income permitted

EQUIty FINANCIAL tRUSt

a Purchase or refi max $1 million 35 1 to 5 yrs weekly/bi-weekly/monthly no 80% 580+ 50/50 20+20 annually 3 months or int adj on approval will look at BFS

B pur-80% refi-75% max $1 million 35 1 to 5 yrs weekly/bi-weekly/monthly no pur-80% refi-75% 550 to 579 50/50 20+20 annually 3 months or int adj on approval will look at BFS and soft credit

C purchase or refi max $1 million 35 1 to 5 yrs weekly/bi-weekly/monthly no pur-75% refi-65% beacon under 549 50/50 20+20 annually 3 months or int adj on approval will look at poor credit and BFS

FEATURE / lEndER pRodUcT gUidE

For more inFormation contact lender (see page 32) mAy 2012 lender guide | 25

LENDER PRODUCt PURPOSE OF FUNDS MORtGAGE AMOUNt AMORtIzAtION tERMS PAyMENt FREQUENCy PRE-APPROvALS LOAN tO vALUE BEACON GDS/tDS PREPAyMENt PREPAyMENt PENALty PORtABILIty OthER

BRIDGEwAtER BANk

Insured fixed rate Purchase, plus improvements; refinance plus improvements; rent-als; new constrution

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year, fixed, closed

Monthly, bi-weekly, semi-monthly, weekly and accelerated

no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

Up to 20% of original principal or the new term principal, paid annually with min. payment of $500; regular mortgage payment increased up to 20% during term

the greater of either 3 months interest and the IRD ased on the difference between the mortgage interest rate and the yield on a Government of Canada Bond with a similar remaining term, plus 0.75%

straight port only; no blend and/or extend available; port and decrease - client to payout difference; port and increase - done as a second mortgage

Ri-fi express equity take out; debt consolidation; refinances with improvements

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year, fixed, closed

See above no Owner occupied refinace 1-4 units max. 85%; non-owner occupied refinance 1-4 units max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

Reno-for-more purchase plus improvements; refinance plus improvements

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

, 2, 3, 4, 5 or 10 year, fixed, closed

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

Progress advance new construction: residential builder, general contractor, acting contractor, acting as own contrac-tor; Interest rate: Prime +3% during construction

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

Construction must be com-pleted according to the draw schedule

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; rentals max. 80%

Min. 610 15% overrun must be available in ratio, liquid assets or line of credit

n/a See above n/a

Rental Property purchase; purchase plus improve-ments; refinance; new construction

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

5 year, fixed, closed

See above no non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 660; Min. personal net worth of $50,000; no worse that R2 rating over past 24 months

710 beacon score=no GDS, tDS 44%; 709<beacon score=GDS 35%, tDS 42%; 50% add on=(PItH + other debt service cost)/Gross annual income

Up to 20% of original principal or the new term principal, paid annually with min. payment of $500; regular mortgage payment increased up to 20% during term

See above straight port only; no blend and/or extend available; port and decrease - client to payout difference; port and increase - done as a second mortgage

Second / vacation home purchase; purchase plus improve-ments; refinance; new construction

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year fixed, closed

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied refinance 1-2 units max. 85%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

Welcome to Canada Purchase; purchase plus improve-ments; refinance

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years

1, 2, 3, 4, 5 or 10 year fixed, closed

See above no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%

Min. 610 will accept reject beacons with alternate credit sources for co-borrower(s)

GDS 35%, tDS 42% See above See above See above

Second mortgage equity take out; port with increase; debt consolidation; first mortgage must be with Bridgewater

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years, min. 16 years; must match remain-ing amortization of first mortgage

1-5 year fixed, closed; must match remaining term of first mortgage

See above no Max. 95% owner occupied; max. 80% non-owner occupied; owner occupied Port 1-2 units max. 95%; owner occu-pied Port 3-4 units max. 90%; owner occupied etO/Refinance max. 85%; non-owner occupied max. 80%

Min. 610 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

State income (exclusive to Power Compensation Brokers)

Purchase plus improvements; refinance plus improvement; new construction; interest rate: market term rate +30bps; CMHC stated eligibility

Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years; min. 16 years

1, 2, 3, 4, 5 or 10 year fixed, closed

See above no Owner occupied purchase 1-2 units max. 90%; owner occupied refinance 1-2 units max. 85%

Min. 650 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above See above See above

adjustabel rate mortgage (ex-clusive to Power Compensation Brokers)

Purchase; refinance Max. $750,000, min. $75,000; $50,000, atlantic Canada; $10,000 second mortgage

Max. 30 years; min. 16 years

3 year closed with option to convert to 3 or 5 year fixed

Monthly only available for the 1st of each month

no Owner occupied purchase 1-2 units max. 95%; owner occupied purchase 3-4 units max. 90%; owner occupied refinance 1-4 units max. 85%; non-owner occupied purchase/refinance 1-4 units max. 80%

Min. 650; no worse than R2 rating over past 24 months

Bank of Canada 5 year benchmark rate used for qualify-ing; 680 + beacon score=no GDS, tDS 44%; 679< beacon score=GDS 35%, tDS 42%

See above 3 months interest See above

EQUItABLE tRUSt COMPANy

Fixed Rate Mortgage Purchase, Refinance & Rentals Scaled lending amounts 30 years 1 to 5 year terms Monthly, bi-weekly or semi-monthly

no Maximum 80% no minimum beacon 50/50 20% per calendar year Greater of 3 months interest or IRD, see etC mortgage commit-ment for details.

Yes - With qualification BFS - Self Declared Income permitted

aRM Purchase, Refinance & Rentals Scaled lending amounts 30 years 3 and 5 year terms only

Monthly no Maximum 80% Minimum 550 beacon 50/50 20% per calendar year 5 months interest in 1st year, 4 months interest in 2nd year, 3 months interest in 3rd year

Yes - With qualification BFS - Self Declared Income permitted

Yes You Can - High Ratio Purchase or Refinance * Rentals-On

Scaled lending amounts 30 years *Western Canada 1 & 2 year terms, Ontario 1, 2 & 3 year terms

Monthly no Maximum 85% Minimum 550 beacon 50/50 20% per calendar year Greater of 3 months interest or IRD, see etC mortgage commit-ment for details.

Yes - With qualification BFS - Self Declared Income permitted

1+1 Option Purchase, Refinance & Rentals Scaled lending amounts 30 years 1 year term Monthly, bi-weekly or semi-monthly

no Maximum 80% no minimum beacon 50/50 n/a With 1 month’s written notice, client is subject to 1 month’s inter-est penalty. Without 1 month’s notice, client is subject to greater of 3 months interest or IRD.

Yes - With qualification BFS - Self Declared Income permitted

Ultimate Open Purchase, Refinance & Rentals Scaled lending amounts 30 years 1 year term Monthly, bi-weekly or semi-monthly

no Maximum 80% Minimum 550 beacon 50/50 Fully open without notice or bonus

n/a Yes - With qualification BFS - Self Declared Income permitted

EQUIty FINANCIAL tRUSt

a Purchase or refi max $1 million 35 1 to 5 yrs weekly/bi-weekly/monthly no 80% 580+ 50/50 20+20 annually 3 months or int adj on approval will look at BFS

B pur-80% refi-75% max $1 million 35 1 to 5 yrs weekly/bi-weekly/monthly no pur-80% refi-75% 550 to 579 50/50 20+20 annually 3 months or int adj on approval will look at BFS and soft credit

C purchase or refi max $1 million 35 1 to 5 yrs weekly/bi-weekly/monthly no pur-75% refi-65% beacon under 549 50/50 20+20 annually 3 months or int adj on approval will look at poor credit and BFS

FEATURE / lEndER pRodUcT gUidE

26 | lender guide mAy 2012

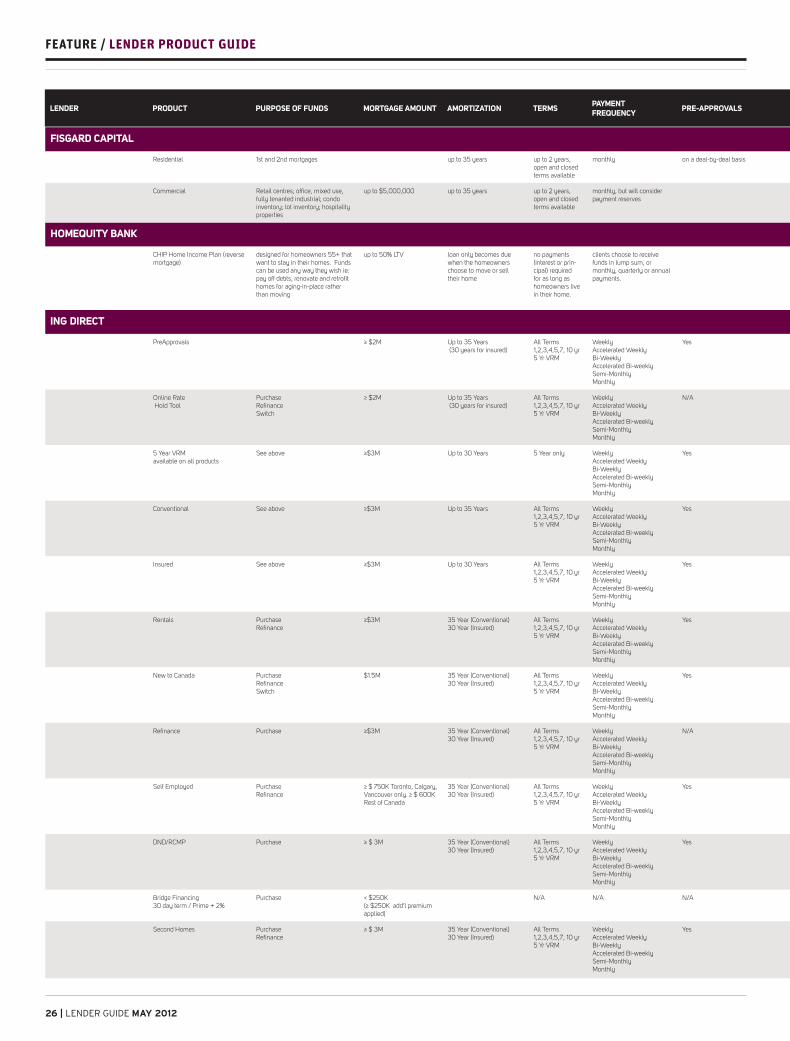

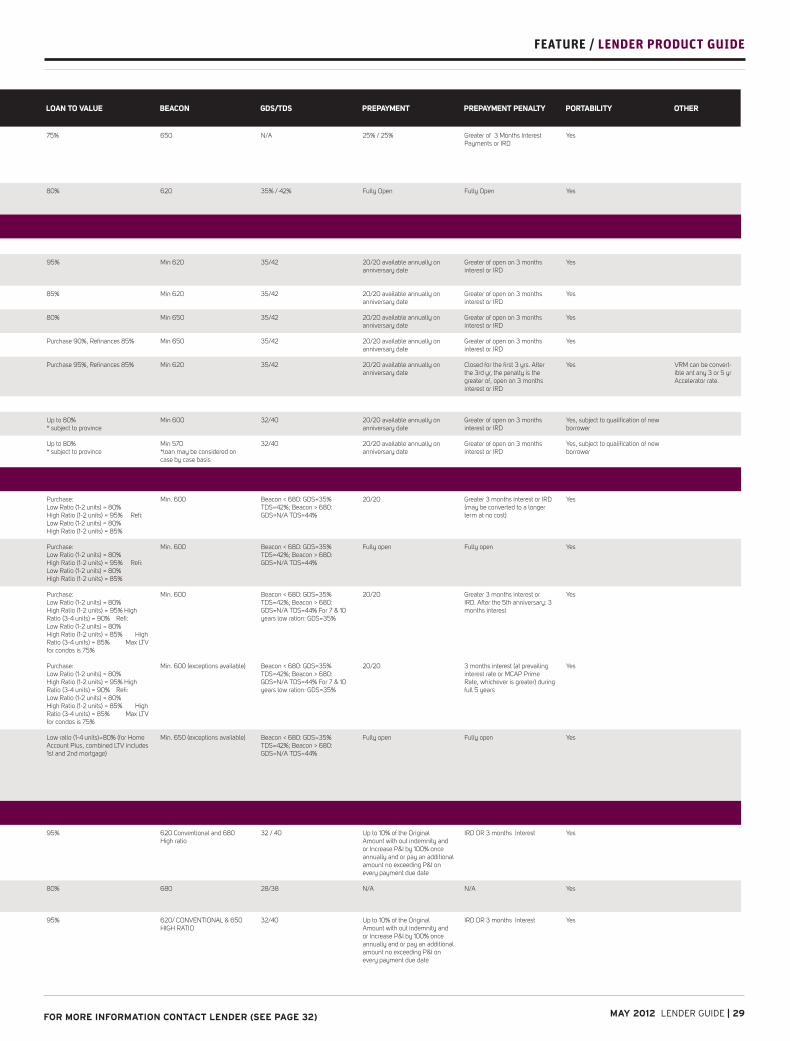

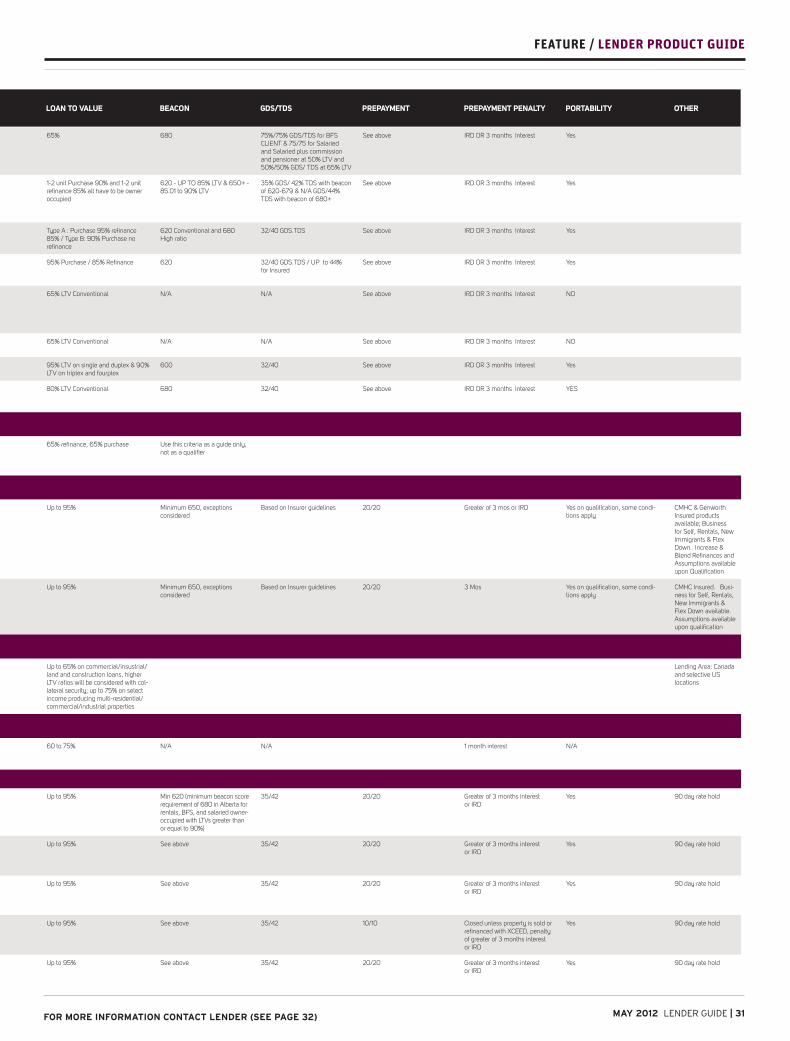

FISGARD CAPItAL

Residential 1st and 2nd mortgages up to 35 years up to 2 years, open and closed terms available

monthly on a deal-by-deal basis up to 75% no min. beacon available 3 months interest on closed term lending areas: BC and alberta only

Commercial Retail centres; office, mixed use, fully tenanted industrial; condo inventory; lot inventory; hospitality properties

up to $5,000,000 up to 35 years up to 2 years, open and closed terms available

monthly, but will consider payment reserves

up to 75% no min. beacon available 3 months interest on closed term lending areas: BC and alberta only

hOMEQUIty BANk

CHIP Home Income Plan (reverse mortgage)

designed for homeowners 55+ that want to stay in their homes. Funds can be used any way they wish ie: pay off debts, renovate and retrofit homes for aging-in-place rather than moving

up to 50% ltV loan only becomes due when the homeowners choose to move or sell their home

no payments (interest or prin-cipal) required for as long as homeowners live in their home.

clients choose to receive funds in lump sum, or monthly, quarterly or annual payments.

up to 50% ltV no credit qualifications no credit qualifications clients may choose to pay inter-est or principal at any time.

an early payment charge may apply for principal repayments depending on when repayment is made, but may be waived or reduced in the event of death or move to a long-term care facility or retirement residence.

some flexibility 50bps discount for clients that choose to pay their full annual interest

ING DIRECt

Preapprovals ≥ $2M Up to 35 Years (30 years for insured)

all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

Yes Up to 95% 620 32% / 42% n/a n/a n/a

Online Rate Hold tool

Purchase RefinanceSwitch

≥ $2M Up to 35 Years (30 years for insured)

all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

n/a Up to 95% 620 n/a n/a n/a n/a Rate Hold for 30 days, + 90 if rate hold turns to real deal within first 30 days

5 Year VRM available on all products

See above ≥$3M Up to 30 Years 5 Year only Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

Yes Up to 95% 620 35% / 45% (Conv) 32% / 42% (Insured)

25% / 25% 3 Months Interest Yes

Conventional See above ≥$3M Up to 35 Years all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

Yes 80% 620 35% / 45% 25% / 25% Greater of 3 Months Interest Payments or IRD

Yes

Insured See above ≥$3M Up to 30 Years all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

Yes 95% 620 32% / 42% (if beacon <680, Unlimited GDS / 44%

25% / 25% Greater of 3 Months Interest Payments or IRD

Yes

Rentals Purchase Refinance

≥$3M 35 Year (Conventional) 30 Year (Insured)

all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

Yes 80% (Conventional) 680 Unlimited GDS / 42% 25% / 25% Greater of 3 Months Interest Payments or IRD

Yes

new to Canada Purchase Refinance Switch

$1.5M 35 Year (Conventional) 30 Year (Insured)

all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

Yes 65% (Conventional) 95% (insured) 85% (Refinance)

620 35% / 42% 25% / 25% Greater of 3 Months Interest Payments or IRD

Yes (If permanent residence.) no (If on Worker Permit)

Refinance Purchase ≥$3M 35 Year (Conventional) 30 Year (Insured)

all terms 1,2,3,4,5,7, 10 yr 5 Yr VRM

Weekly accelerated Weekly Bi-Weekly accelerated Bi-weekly Semi-Monthly Monthly

n/a 80% (Conventional) 85% (Insured)

620 35% / 45% (Conv) 32% / 42% (Insured)

25% / 25% Greater of 3 Months Interest Payments or IRD

Yes