Computational Economics

Prof. Dr. Maik Wolters

Friedrich-Schiller-University Jena

Overview

Objective:

Learn doing empirical and applied theoretical work in monetarymacroeconomics

Implementing macroeconomic models on the computer

Doing policy simulations, estimating models, forecasting with models

Model Class:

Vector Autoregressions (VAR)

Dynamic Stochastic General Equilibrium (DSGE) Models

Methods and Tools:

VARs: OLS, Bayesian estimation, structural identification

DSGE: Derivation, stochastic simulation, deterministic simulation, Bayesianestimation

2

Lecturers

Lectures:

Prof. Dr. Maik Wolters, [email protected]

Exercise sessions / Research Project

Lars Other, Office 4.162, [email protected]

Josefine Quast, Office 4.148, [email protected]

Office Hours

By appointment (send an Email)

3

Outline

Part 1: Vector Autoregressions

Part 2: The baseline New Keynesian model – Derivation and stochastic simulations

Part 3: Medium-scale DSGE models – Stochastic simulations

Part 4: Deterministic simulations – Fiscal policy applications

Part 5: Estimation of DSGE models, Forecasting

4

Literature

Macroeconomic Theory:

Walsh, Carl (2010). Monetary Theory and Policy, The MIT Press, Third Edition.

Galí, Jordi (2015). Monetary Policy, Inflation, and the Business Cycle: An Introduction to the New Keynesian Framework and Its Applications, Princeton Press, Second Edition.

Romer, David, (2012). Advanced Macroeconomics, McGraw-Hill, Fourth Edition.

Wickens, Michael (2011). Macroeconomic Theory. A Dynamic General Equilibrium Approach, Princeton University Press, Second Edition.

Heijdra, Ben j. (2017). Foundations of Modern Macroeconomics, Oxford University Press, Third Edition.

Methodology:

Canova, F. (2007). Methods for Applied Macroeconomic Research, Princeton University Press.

DeJong, David N., and Chentan Dave (2011). Structural Macroeconometrics, Princeton University Press, Second Edition.

Lütkepohl, H. (2007). New Introduction to Multiple Time Series Analysis, Springer.

Kilian, L. and H. Lütkepohl (2017). Structural Vector Autoregressive Analysis, Cambridge University Press, http://www-personal.umich.edu/~lkilian/book.html

Dynare User Guide, Dynare Manual.

Academic papers:

Will be announced during the course.

5

6

Part 1

Vector Autoregressions

Data in monetary macroeconomics

Time series of aggregate data

Examples: GDP, CPI inflation, short- and long-term interest rates, exchange rates, …

Frequency: typically quarterly and sometimes monthly

Data availability: only data for few recent decades available

Many structural breaks (different policy regimes, structural change in the economy, etc.)

Typical time series: 80-120 observations in quarterly frequency

7

8

0

2

4

6

8

10

12

14

16

18

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

3

4

5

6

7

8

9

10

11

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

-4

-2

0

2

4

6

8

10

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

-2

0

2

4

6

8

10

12

14

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Real GDP growth (year-on-year) Unemployment Rate

CPI Inflation (year-on-year) Fed Funds Rate

Core Macro Time Series (US Data)

Trends and persistence

Some time series show trends and keep growing: GDP, CPI, …

9

2000

4000

6000

8000

10000

12000

14000

16000

18000

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

20

70

120

170

220

270

Real GDP (level) CPI (level)

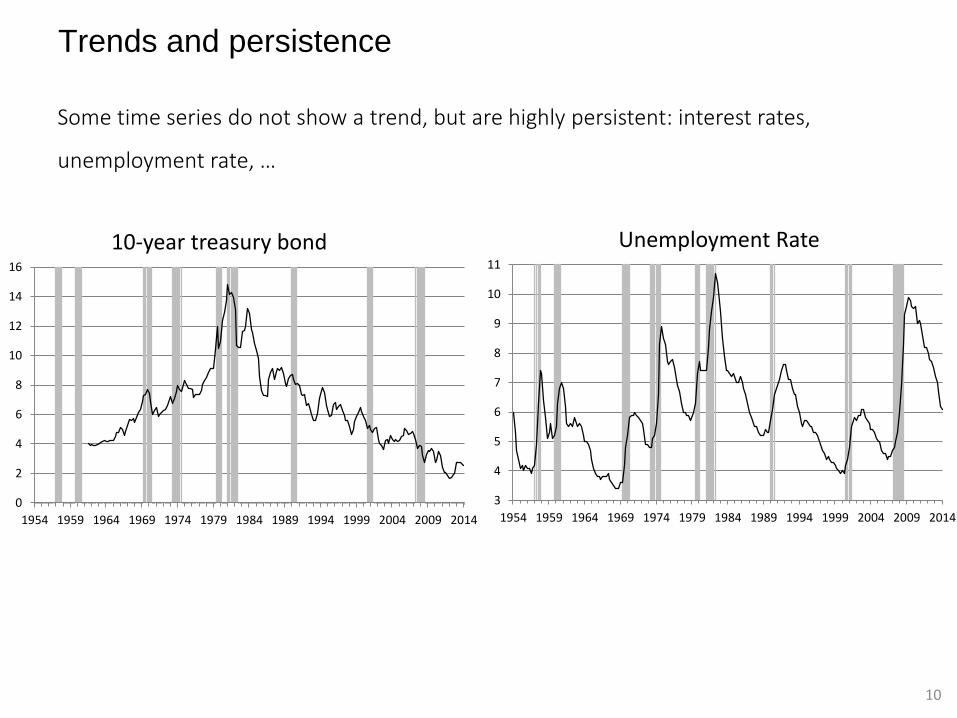

Trends and persistence

Some time series do not show a trend, but are highly persistent: interest rates,

unemployment rate, …

10

3

4

5

6

7

8

9

10

11

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

Unemployment Rate

0

2

4

6

8

10

12

14

16

1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

10-year treasury bond

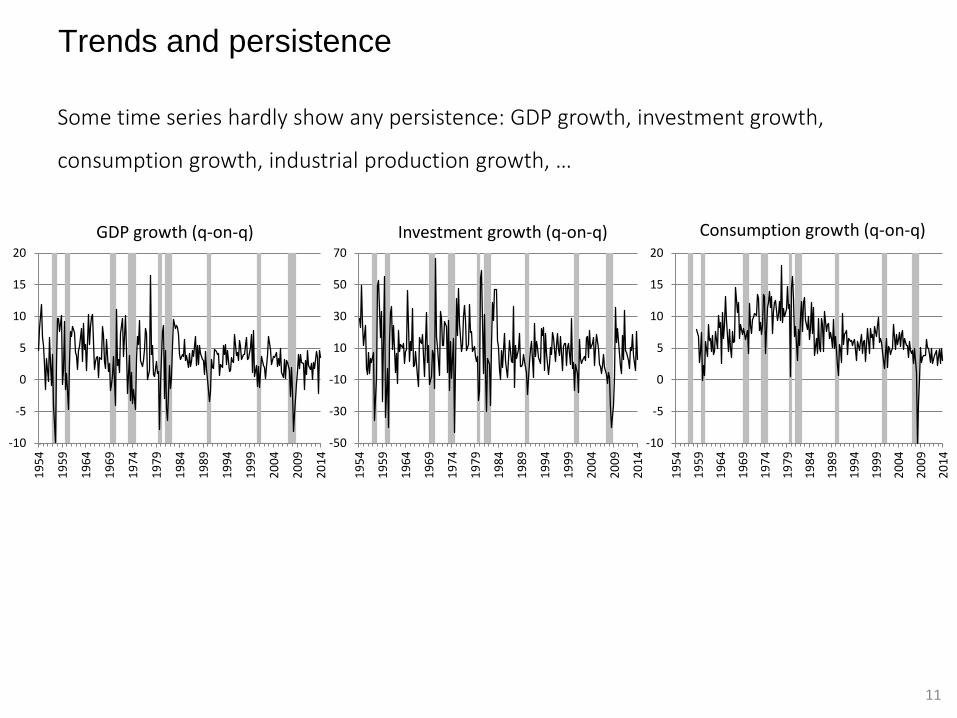

Trends and persistence

Some time series hardly show any persistence: GDP growth, investment growth,

consumption growth, industrial production growth, …

11

-10

-5

0

5

10

15

20

19

54

19

59

19

64

19

69

19

74

19

79

19

84

19

89

19

94

19

99

20

04

20

09

20

14

-50

-30

-10

10

30

50

70

19

54

19

59

19

64

19

69

19

74

19

79

19

84

19

89

19

94

19

99

20

04

20

09

20

14

-10

-5

0

5

10

15

20

19

54

19

59

19

64

19

69

19

74

19

79

19

84

19

89

19

94

19

99

20

04

20

09

20

14

GDP growth (q-on-q) Investment growth (q-on-q) Consumption growth (q-on-q)

Collinearity and dynamic correlation

Macroeconomic datasets are characterized by collinearity

GDP, consumption, investment, industrial production, …

Inflation, interest rates, …

Dynamic interaction of macroeconomic variables

Phillips curve: unemployment rate and inflation

IS-curve: real interest rate and output

Taylor rule: output gap, inflation and interest rate

We do not study univariate time series models (AR, ARMA, ARIMA, ARCH,

GARCH, …), but focus on multivariate models (VAR)

12

Data transformation

Seasonal adjustment

13

Source: Leamer, 2009, Chapter 2

Data transformation

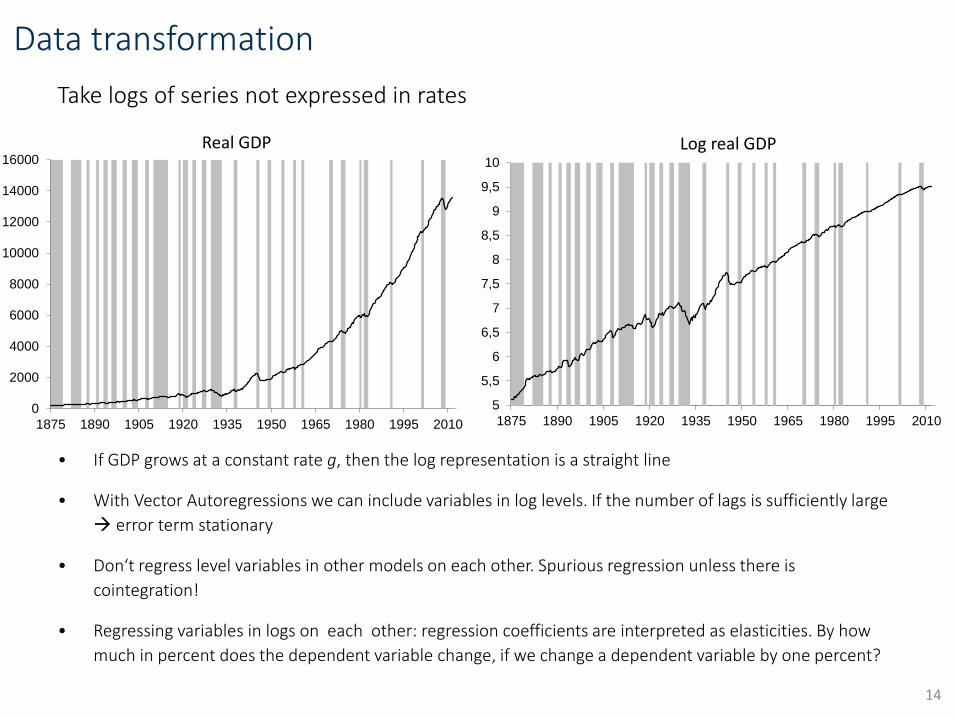

Take logs of series not expressed in rates

• If GDP grows at a constant rate g, then the log representation is a straight line

• With Vector Autoregressions we can include variables in log levels. If the number of lags is sufficiently large

error term stationary

• Don‘t regress level variables in other models on each other. Spurious regression unless there is

cointegration!

• Regressing variables in logs on each other: regression coefficients are interpreted as elasticities. By how

much in percent does the dependent variable change, if we change a dependent variable by one percent?

14

5

5,5

6

6,5

7

7,5

8

8,5

9

9,5

10

1875 1890 1905 1920 1935 1950 1965 1980 1995 20100

2000

4000

6000

8000

10000

12000

14000

16000

1875 1890 1905 1920 1935 1950 1965 1980 1995 2010

Real GDP Log real GDP

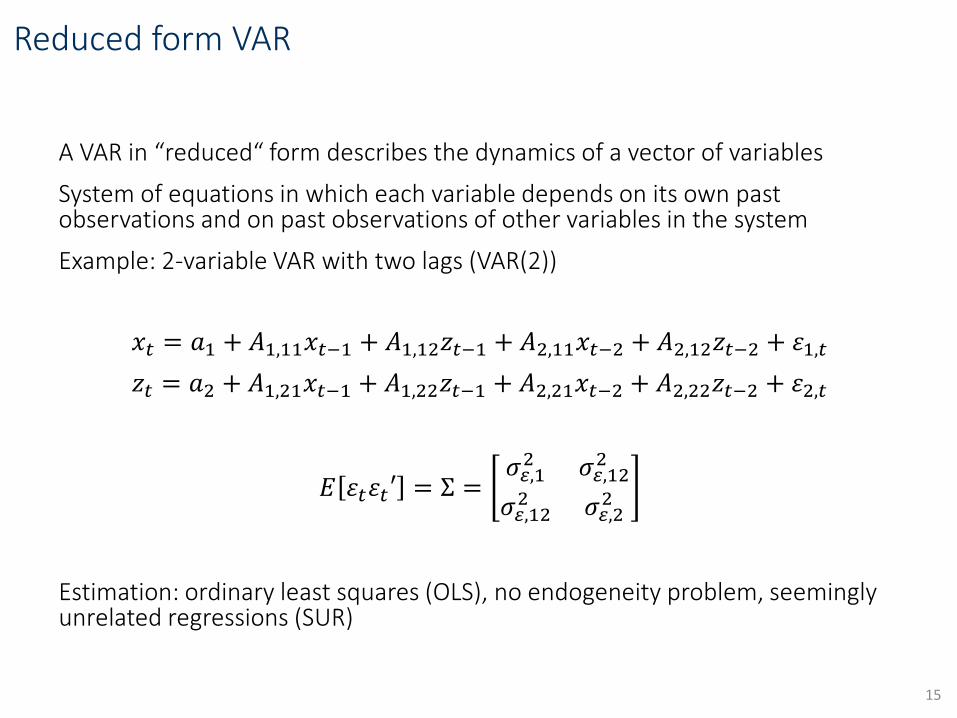

Reduced form VAR

A VAR in “reduced“ form describes the dynamics of a vector of variables

System of equations in which each variable depends on its own pastobservations and on past observations of other variables in the system

Example: 2-variable VAR with two lags (VAR(2))

𝑥𝑡 = 𝑎1 + 𝐴1,11𝑥𝑡−1 + 𝐴1,12𝑧𝑡−1 + 𝐴2,11𝑥𝑡−2 + 𝐴2,12𝑧𝑡−2 + 𝜀1,𝑡

𝑧𝑡 = 𝑎2 + 𝐴1,21𝑥𝑡−1 + 𝐴1,22𝑧𝑡−1 + 𝐴2,21𝑥𝑡−2 + 𝐴2,22𝑧𝑡−2 + 𝜀2,𝑡

𝐸 𝜀𝑡𝜀𝑡′ = Σ =𝜎𝜀,12 𝜎𝜀,12

2

𝜎𝜀,122 𝜎𝜀,2

2

Estimation: ordinary least squares (OLS), no endogeneity problem, seeminglyunrelated regressions (SUR)

15

VAR notation

VAR(2)

𝑥𝑡 = 𝑎1 + 𝐴1,11𝑥𝑡−1 + 𝐴1,12𝑧𝑡−1 + 𝐴2,11𝑥𝑡−2 + 𝐴2,12𝑧𝑡−2 + 𝜀1,𝑡

𝑧𝑡 = 𝑎2 + 𝐴1,21𝑥𝑡−1 + 𝐴1,22𝑧𝑡−1 + 𝐴2,21𝑥𝑡−2 + 𝐴2,22𝑧𝑡−2 + 𝜀2,𝑡

𝐸 𝜀𝑡𝜀𝑡′ = Σ =𝜎𝜀,12 𝜎𝜀,12

2

𝜎𝜀,122 𝜎𝜀,2

2

Write the VAR(2) in Matrix notation

𝑥𝑡𝑧𝑡

=𝑎1𝑎2

+𝐴1,11 𝐴1,12

𝐴1,21 𝐴1,22

𝑥𝑡−1𝑧𝑡−1

+𝐴2,11 𝐴2,12

𝐴2,21 𝐴2,22

𝑥𝑡−2𝑧𝑡−2

+𝜀1,𝑡𝜀2,𝑡

𝐸 𝜀𝑡𝜀𝑡′ = Σ =𝜎𝜀,12 𝜎𝜀,12

2

𝜎𝜀,122 𝜎𝜀,2

2

16

VAR notation

VAR(2) in Matrix notation

𝑥𝑡𝑧𝑡

=𝑎1𝑎2

+𝐴1,11 𝐴1,12

𝐴1,21 𝐴1,22

𝑥𝑡−1𝑧𝑡−1

+𝐴2,11 𝐴2,12

𝐴2,21 𝐴2,22

𝑥𝑡−2𝑧𝑡−2

+𝜀1,𝑡𝜀2,𝑡

𝐸 𝜀𝑡𝜀𝑡′ = Σ =𝜎𝜀,12 𝜎𝜀,12

2

𝜎𝜀,122 𝜎𝜀,2

2

Define: Yt =𝑥𝑡𝑧𝑡

VAR(p) in Matrix notation:

𝑌𝑡 = 𝐴(1)𝑌𝑡−1 + 𝐴(2)𝑌𝑡−1 +⋯+ 𝐴 𝑝 𝑌𝑡−𝑝 + 𝜀𝑡

Short notation with lag operator:

𝑌𝑡 = 𝐴 𝐿 𝑌𝑡−1 + 𝜀𝑡, 𝐸 𝜀𝑡𝜀𝑡′ = Σ

𝑌𝑡 can include of course more than 2 variables

17

Origin of VARs in Economics

VARs were popularized by Sims (1980) in his classic paper, “Macroeconomics and Reality“, Econometrica, 48, 1-48.

He got the nobel price in 2011 for this work

Response to the failure of structural assumptions in Keynesian large scale econometric models

“The connection between ... models and reality – the style in which‘identification‘ is achieved for these models – is inappropriate, to the point at which claims for identification in these models cannot be taken seriously.“ (Sims, 1980)

So far, we have a system of equations that requires just twoassumptions

1. Which variables to include (usually based on economic theory)

2. How many lags to include (guided by practical considerations: uncorrelatedresiduals, cover dynamics of a certain time span, information criterion ...)

18

Usage of VARs

1. Describe and summarize macroeconomic data; find stylized facts in

the data that structural models should generate

No further modifications of our VAR system required

2. Make macroeconomic forecasts

Need Bayesian methods to avoid in-sample over fit and poor out-of-sample

forecasts

3. Structural analysis; example: effects of a monetary policy shock

Need additional identifying assumptions

19

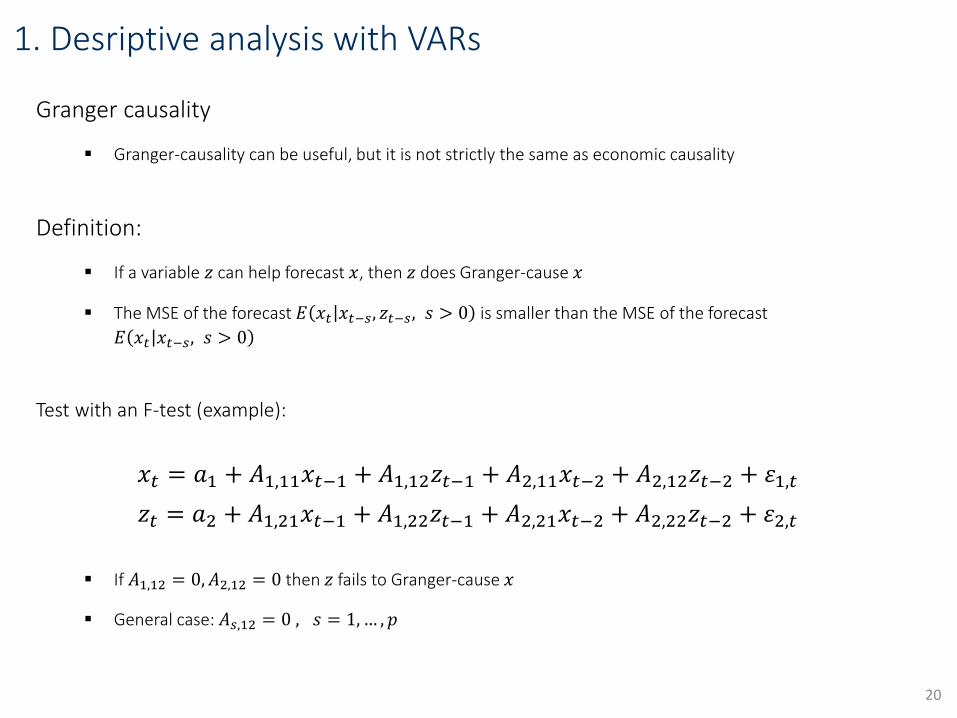

1. Desriptive analysis with VARs

Granger causality

Granger-causality can be useful, but it is not strictly the same as economic causality

Definition:

If a variable 𝑧 can help forecast 𝑥, then 𝑧 does Granger-cause 𝑥

The MSE of the forecast 𝐸 𝑥𝑡 𝑥𝑡−𝑠, 𝑧𝑡−𝑠, 𝑠 > 0 is smaller than the MSE of the forecast

𝐸 𝑥𝑡 𝑥𝑡−𝑠, 𝑠 > 0

Test with an F-test (example):

𝑥𝑡 = 𝑎1 + 𝐴1,11𝑥𝑡−1 + 𝐴1,12𝑧𝑡−1 + 𝐴2,11𝑥𝑡−2 + 𝐴2,12𝑧𝑡−2 + 𝜀1,𝑡

𝑧𝑡 = 𝑎2 + 𝐴1,21𝑥𝑡−1 + 𝐴1,22𝑧𝑡−1 + 𝐴2,21𝑥𝑡−2 + 𝐴2,22𝑧𝑡−2 + 𝜀2,𝑡

If 𝐴1,12 = 0, 𝐴2,12 = 0 then 𝑧 fails to Granger-cause 𝑥

General case: 𝐴𝑠,12 = 0 , 𝑠 = 1,… , 𝑝

20

Granger causality: example with a bivariate VAR

RBC models with nominal neutrality imply that money has no effect on the real variables

Classical dichotomy (real and nominal variables can be analyzedseparately)

We can use a VAR to check whether money in fact does not Granger-cause real variables

Sims (1972) finds that output does not Granger-cause money, but thatmoney Granger causes output

His interpretation was that money supply is exogenous (set by the Fed) and thus isnot influenced by output

On the other hand money has real effects (rejection of the classical dichotomy)

Here, a combination of two Granger causality tests has been used to make an economic interpretation

21

Granger causality: example with a 3-variable VAR

Stock and Watson (2001) use a VAR with inflation, unemployment and the federal funds rate

Table 1 shows p-values of F-tests

VAR can be roughly be interpreted as

Phillips Curve

IS equation (however, inflation not significant)

Taylor Rule

22

2. Forecasting with VARs

Univariate case

Autoregression: AR(p)

𝑥𝑡 = 𝛼 + 𝑎1𝑥𝑡−1 + 𝑎2𝑥𝑡−2 +⋯+ 𝑎𝑝𝑥𝑡−𝑝 + 𝜀𝑡

Forecast is simply obtained by iterating forward

One-step forecast: 𝐸𝑡𝑥𝑡+1 = 𝛼 + 𝑎1𝑥𝑡 + 𝑎2𝑥𝑡−1 +⋯+ 𝑎𝑝𝑥𝑡−𝑝+1 + 𝐸𝑡𝜀𝑡+1

Two-step forecast: 𝐸𝑡𝑥𝑡+2 = 𝛼 + 𝑎1𝐸𝑡𝑥𝑡+1 + 𝑎2𝑥𝑡 +⋯+ 𝑎𝑝𝑥𝑡−𝑝+2 + 𝐸𝑡𝜀𝑡+2

…

h-step in general: 𝐸𝑡𝑥𝑡+ℎ = 𝛼 + 𝑎1𝐸𝑡𝑥𝑡+ℎ−1 +⋯+ 𝑎𝑝𝐸𝑡𝑥𝑡−𝑝+ℎ + 𝐸𝑡𝜀𝑡+ℎ=0

Multivariate model

Consider the following model: 𝑥𝑡 = 𝛼 + 𝑎1𝑥𝑡−1 + 𝑏1𝑧𝑡−1 + 𝜀𝑡

One-step forecast: 𝐸𝑡𝑥𝑡+1= 𝛼 + 𝑎1𝑥𝑡 + 𝑏1𝑧𝑡

Two-step forecast: 𝐸𝑡𝑥𝑡+2 = 𝛼 + 𝑎1𝐸𝑡𝑥𝑡+1 + 𝑏1𝐸𝑡𝑧𝑡+1

VAR(p) model:

Joint forecasting model for all variables that can simply be iterated forward:

𝐸𝑡𝑥𝑡+ℎ = 𝑎1 + 𝐴1,11𝐸𝑡𝑥𝑡+ℎ−1 + 𝐴1,12𝐸𝑡𝑧𝑡+ℎ−1 + 𝐴2,11𝐸𝑡𝑥𝑡+ℎ−2 + 𝐴2,12𝐸𝑡𝑧𝑡+ℎ−2

𝐸𝑡𝑧𝑡+ℎ = 𝑎2 + 𝐴1,21𝐸𝑡𝑥𝑡+ℎ−1 + 𝐴1,22𝐸𝑡𝑧𝑡+ℎ−1 + 𝐴2,21𝐸𝑡𝑥𝑡+ℎ−2 + 𝐴2,22𝐸𝑡𝑧𝑡+ℎ−223

What to use here?

Forecasting with VARs: Example

1. Decide on variables to include in the VAR

2. Decide on number of lags

3. Estimate with OLS

4. Iterate forward to get forecasts

24Source: Stock and Watson (2001)

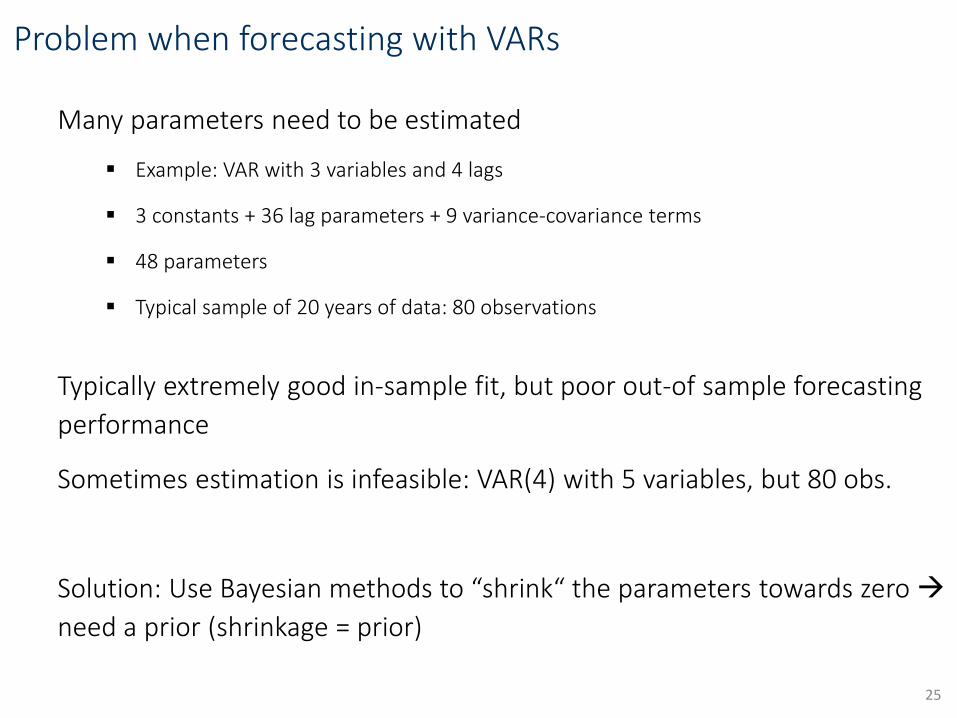

Problem when forecasting with VARs

Many parameters need to be estimated

Example: VAR with 3 variables and 4 lags

3 constants + 36 lag parameters + 9 variance-covariance terms

48 parameters

Typical sample of 20 years of data: 80 observations

Typically extremely good in-sample fit, but poor out-of sample forecasting

performance

Sometimes estimation is infeasible: VAR(4) with 5 variables, but 80 obs.

Solution: Use Bayesian methods to “shrink“ the parameters towards zero

need a prior (shrinkage = prior)

25

The Bayesian approach

Frequentist approach:

Inference by means of hypothesis testing, confidence intervals

Probability viewed as long-run frequency

Unknown „true“ parameters are constant

Bayesian approach:

Inference by means of posterior distributions

Probability viewed as subjective belief

Unknown parameters are treated as random variables with a probability distribution

For forecasting the Bayesian approach can also simply be viewed as a

pragmatic tool to increase forecasting accuracy

26

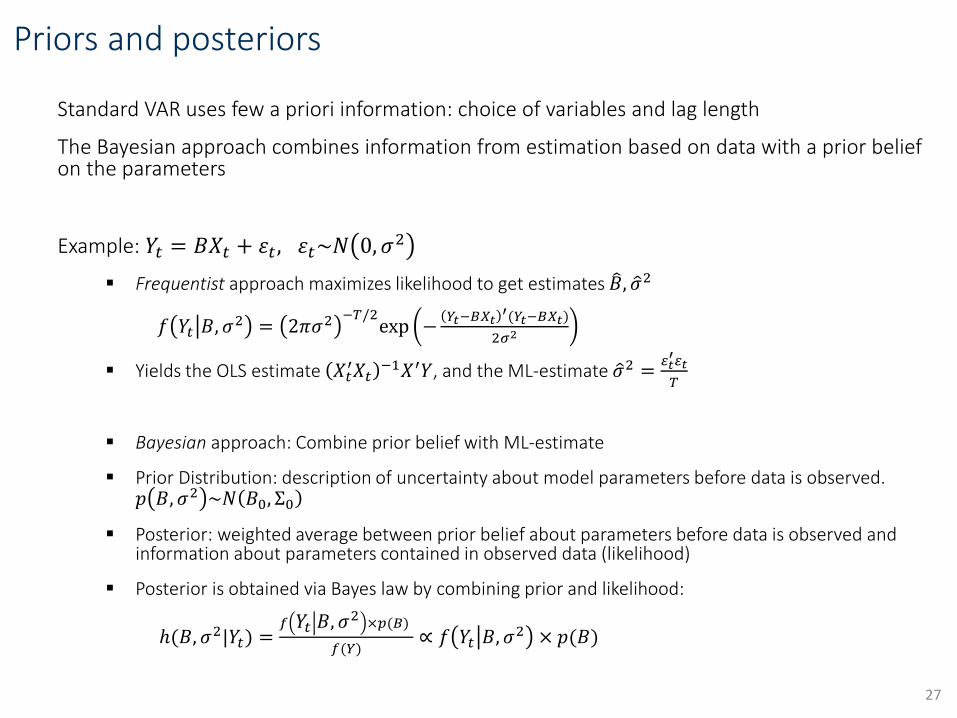

Priors and posteriors

Standard VAR uses few a priori information: choice of variables and lag length

The Bayesian approach combines information from estimation based on data with a prior belief on the parameters

Example: 𝑌𝑡 = 𝐵𝑋𝑡 + 𝜀𝑡, 𝜀𝑡~𝑁 0, 𝜎2

Frequentist approach maximizes likelihood to get estimates 𝐵, 𝜎2

𝑓 𝑌𝑡 𝐵, 𝜎2 = 2𝜋𝜎2 −𝑇/2

exp −𝑌𝑡−𝐵𝑋𝑡

′(𝑌𝑡−𝐵𝑋𝑡)

2𝜎2

Yields the OLS estimate 𝑋𝑡′𝑋𝑡

−1𝑋′𝑌, and the ML-estimate 𝜎2 =𝜀𝑡′𝜀𝑡

𝑇

Bayesian approach: Combine prior belief with ML-estimate

Prior Distribution: description of uncertainty about model parameters before data is observed. 𝑝 𝐵, 𝜎2 ~𝑁 𝐵0, Σ0

Posterior: weighted average between prior belief about parameters before data is observed andinformation about parameters contained in observed data (likelihood)

Posterior is obtained via Bayes law by combining prior and likelihood:

ℎ(𝐵, 𝜎2|𝑌𝑡) =𝑓 𝑌𝑡 𝐵, 𝜎

2×𝑝(𝐵)

𝑓(𝑌)∝ 𝑓 𝑌𝑡 𝐵, 𝜎2 × 𝑝(𝐵)

27

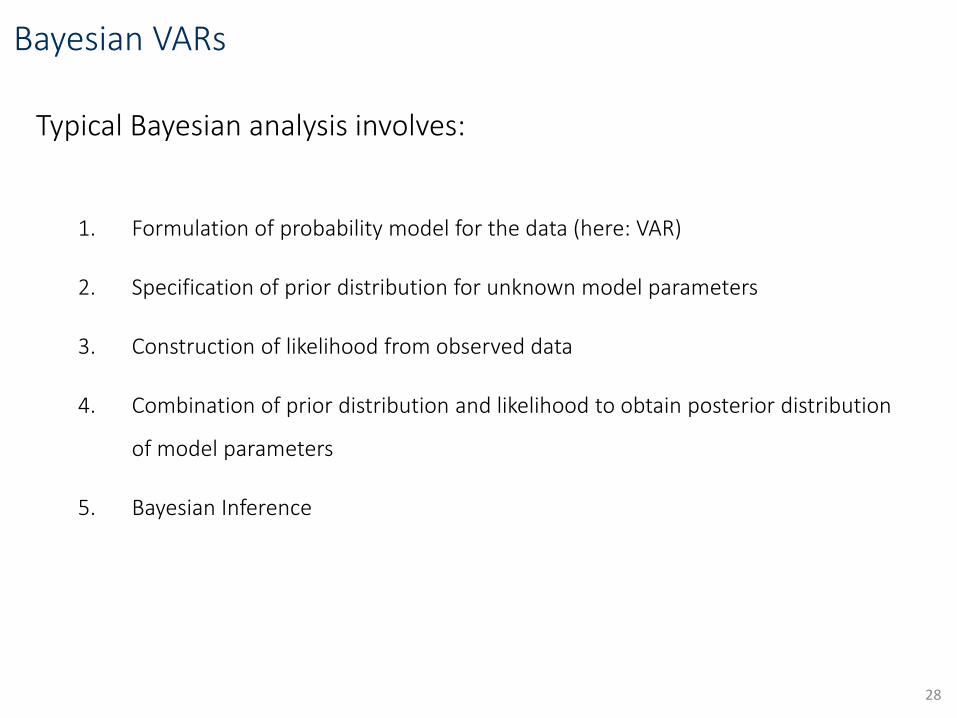

Bayesian VARs

Typical Bayesian analysis involves:

1. Formulation of probability model for the data (here: VAR)

2. Specification of prior distribution for unknown model parameters

3. Construction of likelihood from observed data

4. Combination of prior distribution and likelihood to obtain posterior distribution

of model parameters

5. Bayesian Inference

28

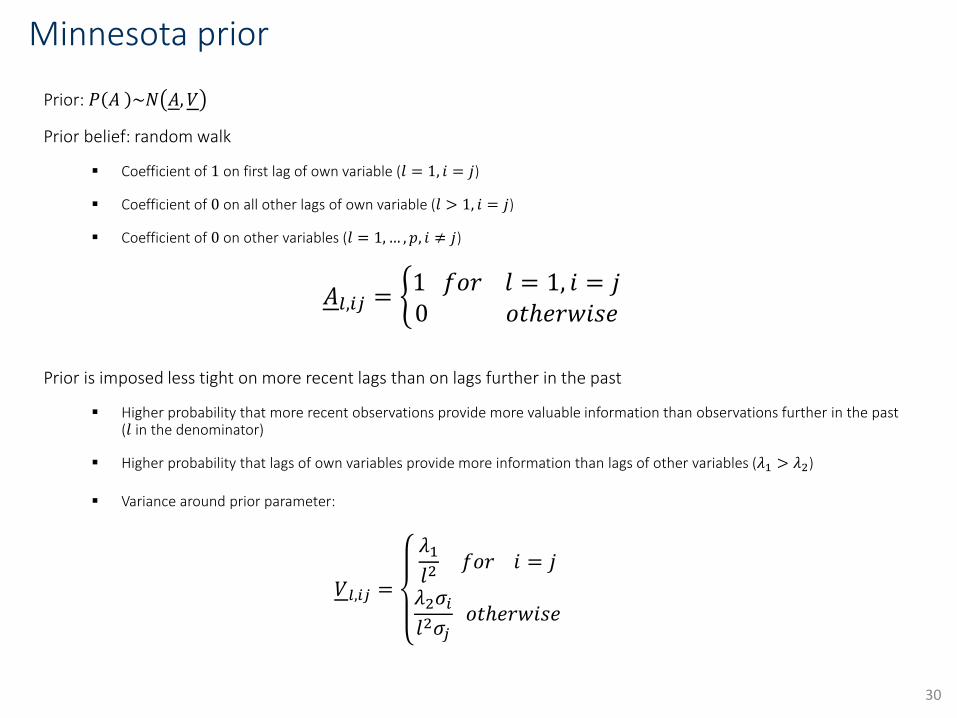

Minnesota prior

Prior developed to achieve a good forecasting model

Achieve a parsimonous model by shrinking parameters towards zero

Developed by Litterman and Sims at the University of Minnesota and the Federal Reserve Bank of

Minneapolis

VAR: 𝑥𝑡 = 𝑎1 + 𝐴1,11𝑥𝑡−1 + 𝐴1,12𝑧𝑡−1 + 𝐴2,11𝑥𝑡−2 + 𝐴2,12𝑧𝑡−2 + 𝜀1,𝑡

𝑧𝑡 = 𝑎2 + 𝐴1,21𝑥𝑡−1 + 𝐴1,22𝑧𝑡−1 + 𝐴2,21𝑥𝑡−2 + 𝐴2,22𝑧𝑡−2 + 𝜀2,𝑡

𝐸 𝜀𝑡𝜀𝑡′ = Σ

Need a prior for 𝐴1,11, … , 𝐴2,22 and Σ

Minnesota prior simplifies by replacing Σ with an estimate Σ need only priors for 𝐴1,11, … , 𝐴2,22

Minnesota prior assumes that most time series can be described as a random walk (with drift) process: 𝑥𝑡 = 𝛼 + 𝑥𝑡−1 + 𝜀𝑡

Coefficient of 1 on first lag of own variable

Coefficient of 0 on all other lags of own variable

Coefficient of 0 on other variables

29

Minnesota prior

Prior: 𝑃 𝐴 ~𝑁 𝐴, 𝑉

Prior belief: random walk

Coefficient of 1 on first lag of own variable (𝑙 = 1, 𝑖 = 𝑗)

Coefficient of 0 on all other lags of own variable (𝑙 > 1, 𝑖 = 𝑗)

Coefficient of 0 on other variables (𝑙 = 1,… , 𝑝, 𝑖 ≠ 𝑗)

𝐴𝑙,𝑖𝑗 = 1 𝑓𝑜𝑟 𝑙 = 1, 𝑖 = 𝑗0 𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒

Prior is imposed less tight on more recent lags than on lags further in the past

Higher probability that more recent observations provide more valuable information than observations further in the past(𝑙 in the denominator)

Higher probability that lags of own variables provide more information than lags of other variables (𝜆1 > 𝜆2)

Variance around prior parameter:

𝑉𝑙,𝑖𝑗 =

𝜆1𝑙2

𝑓𝑜𝑟 𝑖 = 𝑗

𝜆2𝜎𝑖𝑙2𝜎𝑗

𝑜𝑡ℎ𝑒𝑟𝑤𝑖𝑠𝑒

30

Illustration: Minnesota prior

31

Source: Canova (2007)

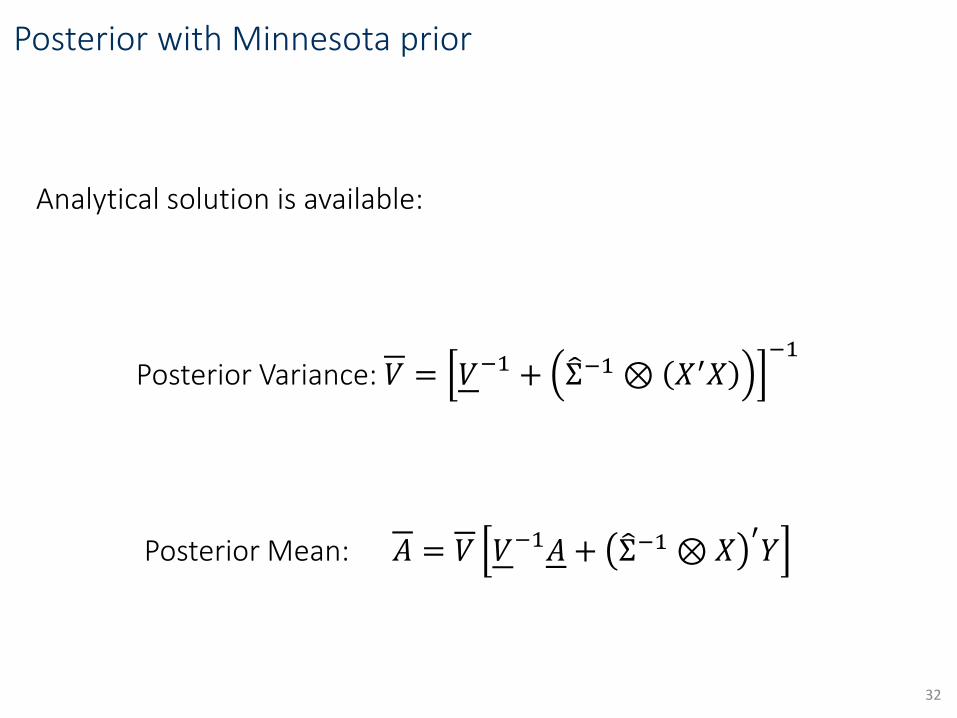

Posterior with Minnesota prior

Analytical solution is available:

Posterior Variance: 𝑉 = 𝑉−1 + Σ−1 ⊗ 𝑋′𝑋−1

Posterior Mean: 𝐴 = 𝑉 𝑉−1𝐴 + Σ−1 ⊗𝑋′𝑌

32

Example: BVAR with Minnesota prior

• Forecasting German macroeconomic variables (Pirschel and Wolters, 2017)

• Variables: GDP, CPI, short-term interest rate, unemployment rate

Bayesian VAR: 4 lags, Normal-Wishart Minnesota prior

Unrestricted VAR: number of lags chosen with Bayesian Information Criterion

Evaluation sample: 1994Q4-2013Q4

33

horizon BVAR: RMSFE VAR: RMSFE

1 (GDP) 3.29 3.72

4 (GDP) 3.44 3.95

8 (GDP) 3.51 3.55

1 (CPI) 1.33 1.43

4 (CPI) 1.29 1.52

8 (CPI) 1.35 1.65

3. Structural VARs

So far the reduced form VAR was restricted to dynamic interactions betweenvariables

This assumption is implausible for structural analysis. Variables depend on each otheralso in period 𝑡 and not only in 𝑡 − 1, 𝑡 − 2,…

Structural form 2-variable VAR with 2 lags: SVAR(2)

𝐹11𝑥𝑡 + 𝐹12𝑧𝑡 = 𝑏1 + 𝐵1,11𝑥𝑡−1 + 𝐵1,12𝑧𝑡−1 + 𝐵2,11𝑥𝑡−2 + 𝐵2,12𝑧𝑡−2 + 𝑢1,𝑡

𝐹21𝑥𝑡 + 𝐹22𝑧𝑡 = 𝑏2 + 𝐵1,21𝑥𝑡−1 + 𝐵1,22𝑧𝑡−1 + 𝐵2,21𝑥𝑡−2 + 𝐵2,22𝑧𝑡−2 + 𝑢2,𝑡

𝐸 𝑢𝑡𝑢𝑡′ = D =𝜎𝑢,12 𝜎𝑢,12

2

𝜎𝑢,122 𝜎𝑢,2

2

This could be a structural model derived from theory. Traditional Cowles commissionmodels have this structure

Structural parameters 𝐹, 𝐵, 𝐷 are different from the reduced form parameters 𝐴, Σ. In particular the structural shocks 𝑢𝑖,𝑡 are different from the reduced form shocks 𝜀𝑖,𝑡.

34

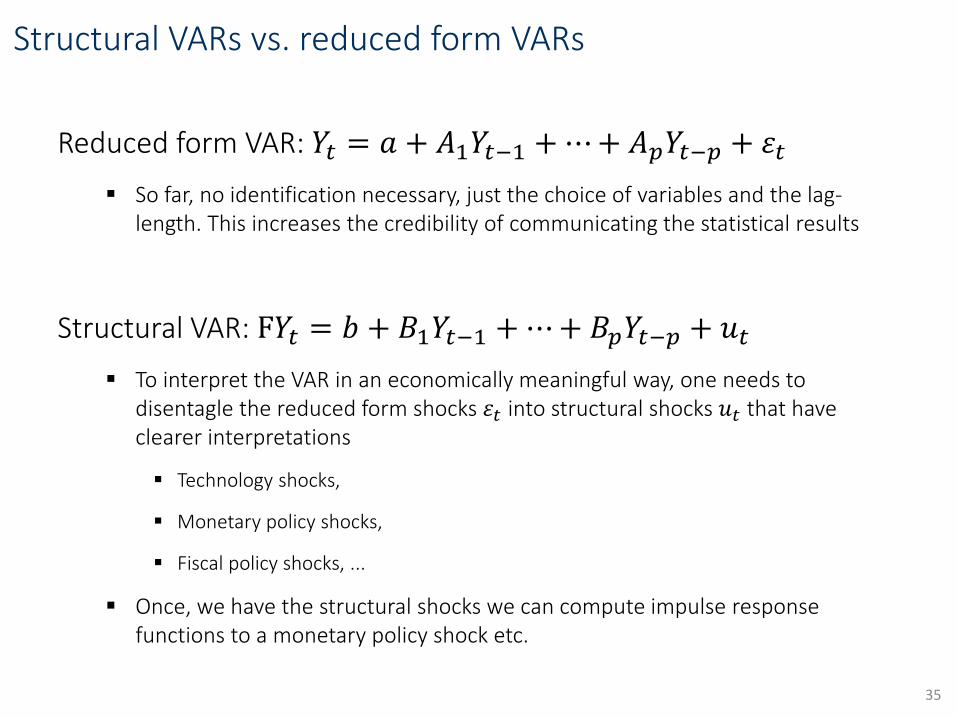

Structural VARs vs. reduced form VARs

Reduced form VAR: 𝑌𝑡 = 𝑎 + 𝐴1𝑌𝑡−1 +⋯+ 𝐴𝑝𝑌𝑡−𝑝 + 𝜀𝑡

So far, no identification necessary, just the choice of variables and the lag-length. This increases the credibility of communicating the statistical results

Structural VAR: F𝑌𝑡 = 𝑏 + 𝐵1𝑌𝑡−1 +⋯+ 𝐵𝑝𝑌𝑡−𝑝 + 𝑢𝑡

To interpret the VAR in an economically meaningful way, one needs todisentagle the reduced form shocks 𝜀𝑡 into structural shocks 𝑢𝑡 that haveclearer interpretations

Technology shocks,

Monetary policy shocks,

Fiscal policy shocks, ...

Once, we have the structural shocks we can compute impulse responsefunctions to a monetary policy shock etc.

35

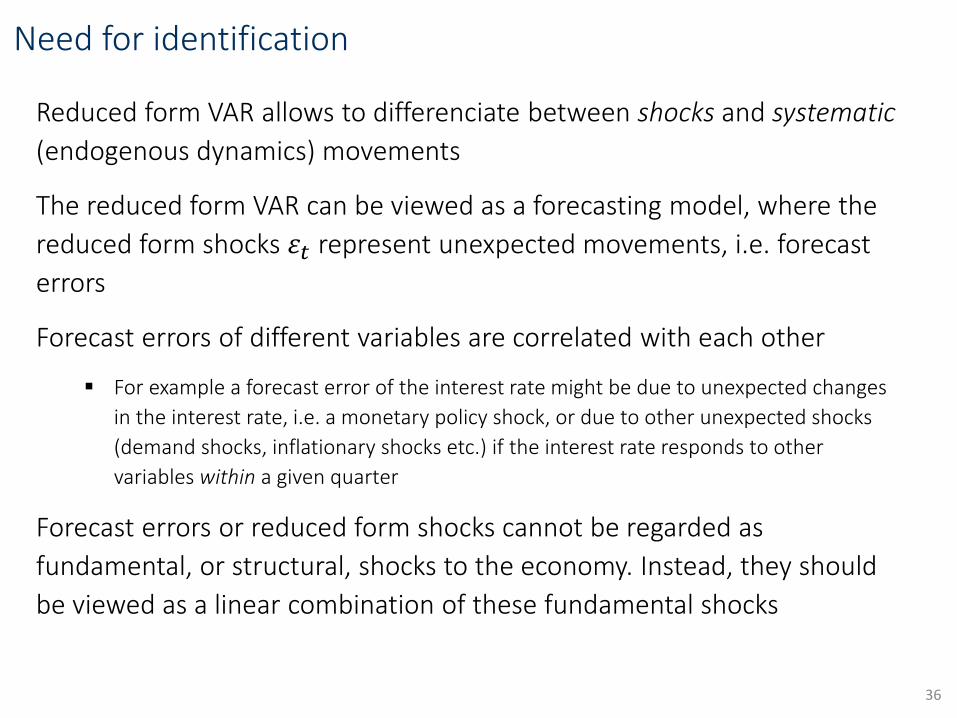

Need for identification

Reduced form VAR allows to differenciate between shocks and systematic

(endogenous dynamics) movements

The reduced form VAR can be viewed as a forecasting model, where the

reduced form shocks 𝜀𝑡 represent unexpected movements, i.e. forecast

errors

Forecast errors of different variables are correlated with each other

For example a forecast error of the interest rate might be due to unexpected changes

in the interest rate, i.e. a monetary policy shock, or due to other unexpected shocks

(demand shocks, inflationary shocks etc.) if the interest rate responds to other

variables within a given quarter

Forecast errors or reduced form shocks cannot be regarded as

fundamental, or structural, shocks to the economy. Instead, they should

be viewed as a linear combination of these fundamental shocks

36

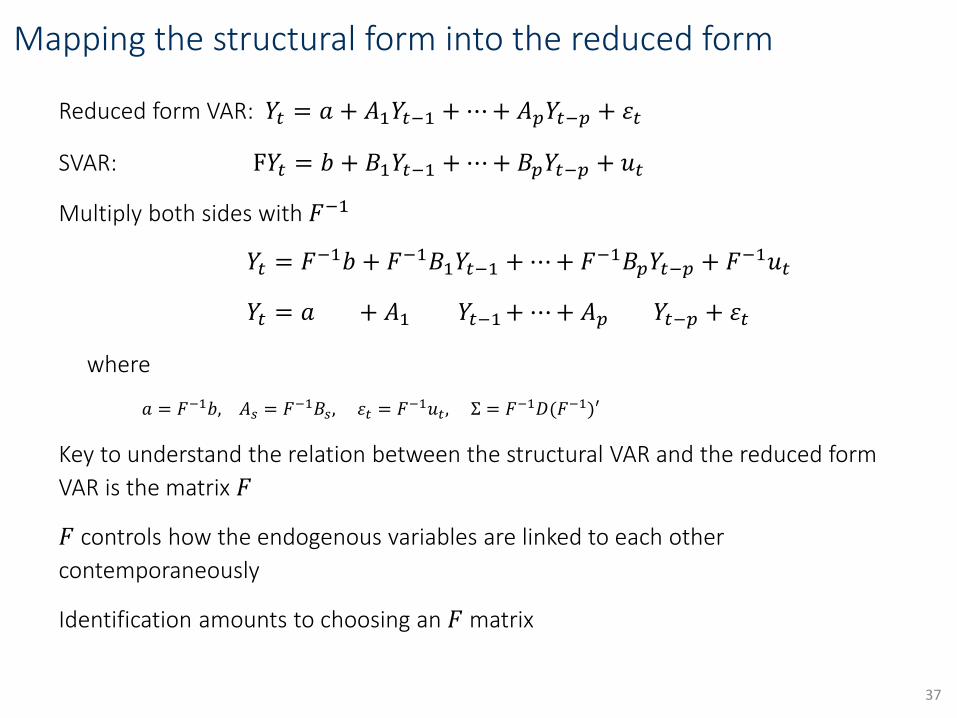

Mapping the structural form into the reduced form

Reduced form VAR: 𝑌𝑡 = 𝑎 + 𝐴1𝑌𝑡−1 +⋯+ 𝐴𝑝𝑌𝑡−𝑝 + 𝜀𝑡

SVAR: F𝑌𝑡 = 𝑏 + 𝐵1𝑌𝑡−1 +⋯+ 𝐵𝑝𝑌𝑡−𝑝 + 𝑢𝑡

Multiply both sides with 𝐹−1

𝑌𝑡 = 𝐹−1𝑏 + 𝐹−1𝐵1𝑌𝑡−1 +⋯+ 𝐹−1𝐵𝑝𝑌𝑡−𝑝 + 𝐹−1𝑢𝑡

𝑌𝑡 = 𝑎 + 𝐴1 𝑌𝑡−1+⋯+ 𝐴𝑝 𝑌𝑡−𝑝 + 𝜀𝑡

where

𝑎 = 𝐹−1𝑏, 𝐴𝑠 = 𝐹−1𝐵𝑠, 𝜀𝑡 = 𝐹−1𝑢𝑡, Σ = 𝐹−1𝐷(𝐹−1)′

Key to understand the relation between the structural VAR and the reduced form

VAR is the matrix 𝐹

𝐹 controls how the endogenous variables are linked to each other

contemporaneously

Identification amounts to choosing an 𝐹 matrix

37

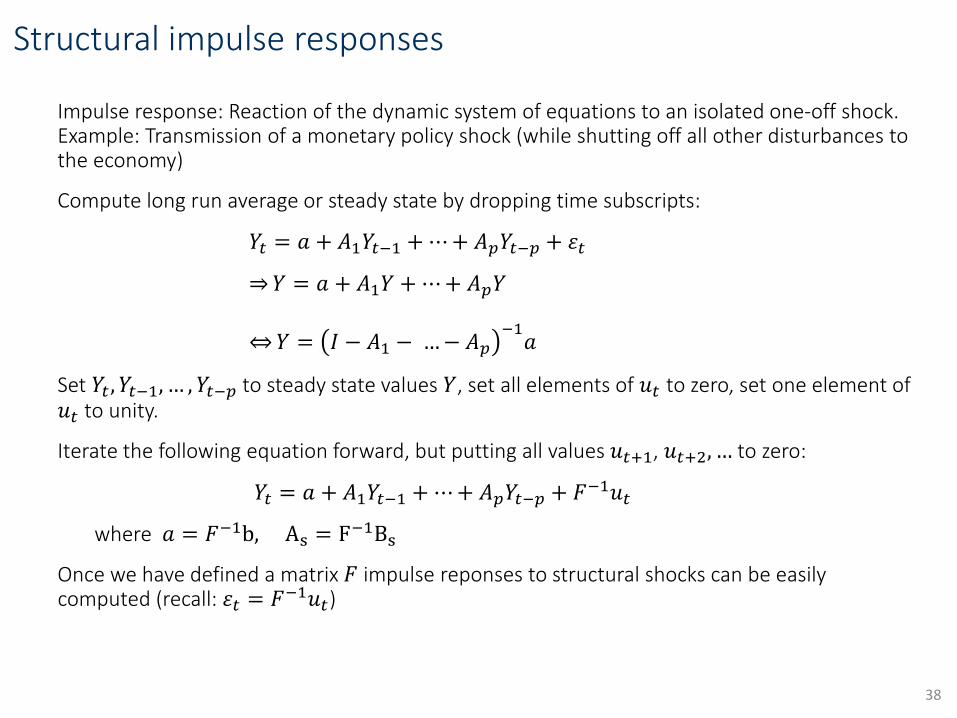

Structural impulse responses

Impulse response: Reaction of the dynamic system of equations to an isolated one-off shock. Example: Transmission of a monetary policy shock (while shutting off all other disturbances tothe economy)

Compute long run average or steady state by dropping time subscripts:

𝑌𝑡 = 𝑎 + 𝐴1𝑌𝑡−1 +⋯+ 𝐴𝑝𝑌𝑡−𝑝 + 𝜀𝑡

𝑌 = 𝑎 + 𝐴1𝑌 +⋯+ 𝐴𝑝𝑌

𝑌 = 𝐼 − 𝐴1 − …− 𝐴𝑝−1𝑎

Set 𝑌𝑡 , 𝑌𝑡−1, … , 𝑌𝑡−𝑝 to steady state values 𝑌, set all elements of 𝑢𝑡 to zero, set one element of𝑢𝑡 to unity.

Iterate the following equation forward, but putting all values 𝑢𝑡+1, 𝑢𝑡+2, … to zero:

𝑌𝑡 = 𝑎 + 𝐴1𝑌𝑡−1 +⋯+ 𝐴𝑝𝑌𝑡−𝑝 + 𝐹−1𝑢𝑡

where 𝑎 = 𝐹−1b, As = F−1Bs

Once we have defined a matrix 𝐹 impulse reponses to structural shocks can be easilycomputed (recall: 𝜀𝑡 = 𝐹−1𝑢𝑡)

38

Structural identification

Structural VAR

F𝑌𝑡 = 𝑏 + 𝐵1𝑌𝑡−1 +⋯+ 𝐵𝑝𝑌𝑡−𝑝 + 𝑢𝑡, 𝐶𝑜𝑣 𝑢𝑡 = 𝐷

Includes 𝑝 + 1 𝑛2 parameters in 𝐹, 𝐵1, … , 𝐵𝑝 , 𝑛 parameters in 𝑏 and 𝑛 + 1 𝑛/2 in 𝐷 (it is

symmetric)

Reduced form VAR

𝑌𝑡 = 𝑎 + 𝐴1𝑌𝑡−1 +⋯+ 𝐴𝑝𝑌𝑡−𝑝 + 𝜀𝑡 , 𝐶𝑜𝑣 𝜀𝑡 = Σ

Includes 𝑝𝑛2 parameters in 𝐴1, … , 𝐴𝑝 , 𝑛 parameters in 𝑎 and 𝑛 + 1 𝑛/2 in Σ

The SVAR includes more parameters than estimated in the reduced form VAR.

We have to impose restrictions on the SVAR to have a clear one-to-one

mapping between the parameters of the two VARs

We have to impose 𝑛2 restrictions on the structural parameters

𝐹, 𝐵1, … , 𝐵𝑝, 𝑏, 𝐷 to identifiy all of them

39

Recursive identification (Sims, 1980)

Impose restrictions on the contemporaneous response of the different endogenous

variables to the different structural shocks

Example: interest rate reacts contemporaneously to monetary policy shocks and to

inflationary shocks. Inflation reacts contemporaneously to inflationary shocks, but only with

a lag to monetary policy shocks

Implement this identification scheme via assuming that 𝐹 is lower triangular and 𝐷 being

diagonal (diagonal elements are the variances of shocks):

First variable can react to lags and the first shock

Second variable can react to lags and the first two shocks

Third variable can react to lags and the first three shocks...

Need to be careful how to order the variables (guided by economic theory)

Number of restrictions on 𝐹: 𝑛(𝑛 + 1)/2

Number of restrictions on 𝐷: 𝑛(𝑛 − 1)/2

Overall number of restrictions: 𝑛²

40

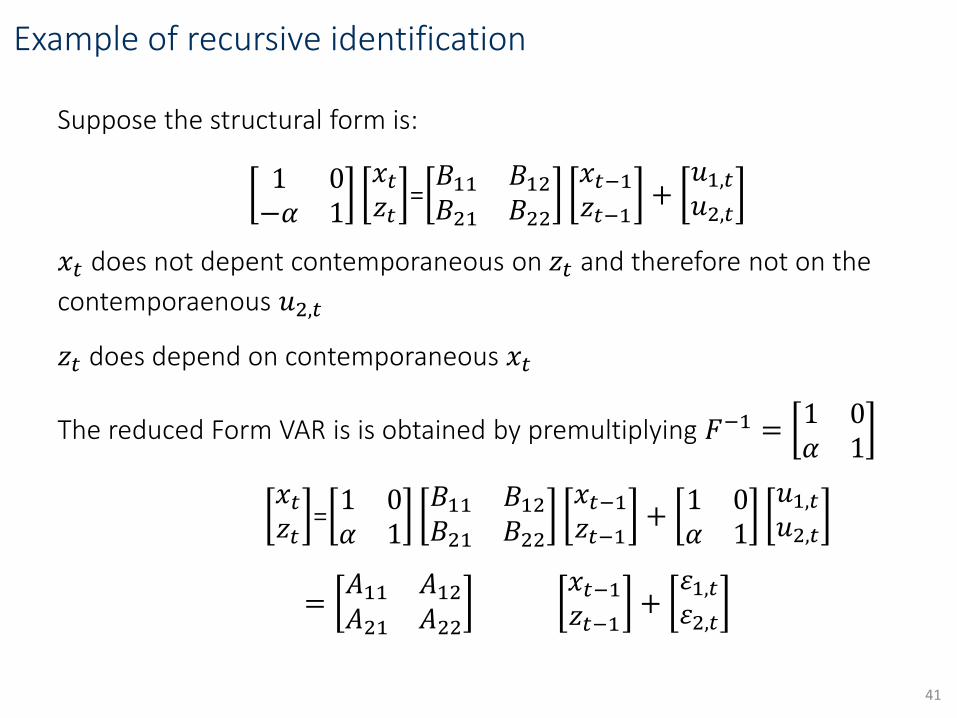

Example of recursive identification

Suppose the structural form is:

1 0−𝛼 1

𝑥𝑡𝑧𝑡

=𝐵11 𝐵12

𝐵21 𝐵22

𝑥𝑡−1𝑧𝑡−1

+𝑢1,𝑡𝑢2,𝑡

𝑥𝑡 does not depent contemporaneous on 𝑧𝑡 and therefore not on the

contemporaenous 𝑢2,𝑡

𝑧𝑡 does depend on contemporaneous 𝑥𝑡

The reduced Form VAR is is obtained by premultiplying 𝐹−1 =1 0𝛼 1

𝑥𝑡𝑧𝑡

=1 0𝛼 1

𝐵11 𝐵12

𝐵21 𝐵22

𝑥𝑡−1𝑧𝑡−1

+1 0𝛼 1

𝑢1,𝑡𝑢2,𝑡

=𝐴11 𝐴12

𝐴21 𝐴22

𝑥𝑡−1𝑧𝑡−1

+𝜀1,𝑡𝜀2,𝑡

41

Example of recursive identification

The reduced Form VAR is is obtained by premultiplying 𝐹−1 =1 0𝛼 1

𝑥𝑡𝑧𝑡

=1 0𝛼 1

𝐵11 𝐵12

𝐵21 𝐵22

𝑥𝑡−1𝑧𝑡−1

+1 0𝛼 1

𝑢1,𝑡𝑢2,𝑡

=𝐴11 𝐴12

𝐴21 𝐴22

𝑥𝑡−1𝑧𝑡−1

+𝜀1,𝑡𝜀2,𝑡

𝜀1,𝑡 = 𝑢1,𝑡

𝜀2,𝑡 = 𝛼𝑢1,𝑡 + 𝑢2,𝑡, so the second reduced form shock is a linear combination of thefirst two structural shocks

The covariance matrix is:

𝐶𝑜𝑣𝜀1,𝑡𝜀2,𝑡

= 𝐹−1𝐷 𝐹−1 ′ =𝜎𝑢,12 𝛼𝜎𝑢,1

2

𝛼𝜎𝑢,12 𝛼2𝜎𝑢,1

2 + 𝜎22 𝐶𝑜𝑣

𝑢1,𝑡𝑢2,𝑡

=𝜎𝑢,12 0

0 𝜎22

42

Bring SVAR into a form with identity covariance matrix

To recover the SVAR from the estimated reduced form VAR the Cholesky

decomposition is used

Rewrite the SVAR: instead of lower triangular with unity elements on the

diagonal of 𝐹 and the diagonal of 𝐷 representing the variances of the

structural shocks, we can write 𝐹 in general lower triangular form

Example: premultiply the structural form by1/𝜎𝑢,1 0

0 1/𝜎𝑢,2

1/𝜎𝑢,1 0

−𝛼/𝜎𝑢,1 1/𝜎𝑢,2

𝑥𝑡𝑧𝑡

=𝐵11/𝜎𝑢,1 𝐵12/𝜎𝑢,1𝐵21/𝜎𝑢,2 𝐵22/𝜎𝑢,2

𝑥𝑡−1𝑧𝑡−1

+𝑢1,𝑡/𝜎𝑢,1𝑢2,𝑡/𝜎𝑢,1

This structual form has a triangular 𝐹 matrix and a covariance matrix equal to

an identity matrix 𝐼

43

Cholesky decomposition

We estimate Σ = 𝐹−1𝐼( 𝐹−1)′ and want to find 𝐹

We know that 𝐹 is lower triangular

Let Σ be a 𝑛𝑥𝑛 symmetric positive definite matrix. The Cholesky decomposition

gives the unique lower triangular matrix 𝑃 such that Σ = 𝑃′𝑃

Step 1: From Σ = 𝐹−1𝐼( 𝐹−1)′ (recall 𝐷 = 𝐼 is assumed) the Cholesky

decomposition recovers 𝐹−1. Invert to get 𝐹, which is triangular

Step 2: Compute the structural parameters:

𝑏 = 𝐹 a, 𝐵𝑠 = 𝐹 𝐴𝑠

44

Application: Monetary policy transmission

Study the transmission of a monetary policy shock on key

macroeconomic aggregates

• Main reference: Christiano, L. J., M. Eichenbaum and C. L. Evans (1999).

“Monetary policy shocks: What have we learned and to what end?“

Handbook of Macroeconomics.

Stylized facts

Interest rates initially rise

Aggregate price level initially responds very little. Price level decreasesafter 1-2 years

Aggregate output initially falls with a zero long-run effect

45

Set up a monetary SVAR

Structural VAR with Cholesky identification to study the

transmission of a structural monetary policy shock to the economy

GDP, consumption, investment

GDP deflator, commodity price index

Fed Funds Rate, 10-year Rate, non-borrowed reserves, total

reserves

46

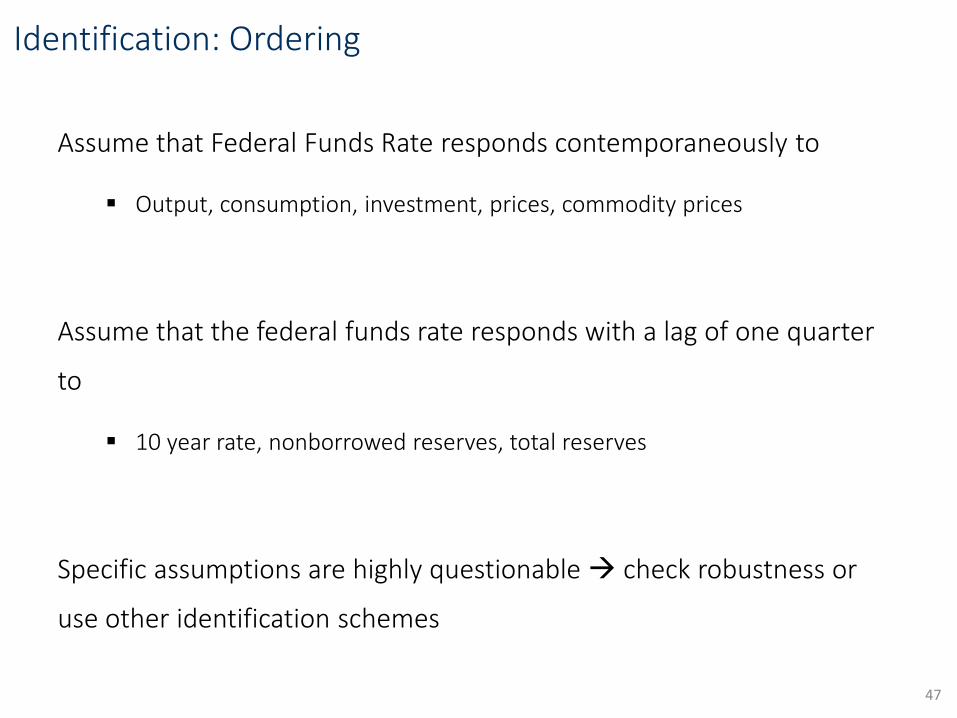

Identification: Ordering

Assume that Federal Funds Rate responds contemporaneously to

Output, consumption, investment, prices, commodity prices

Assume that the federal funds rate responds with a lag of one quarter

to

10 year rate, nonborrowed reserves, total reserves

Specific assumptions are highly questionable check robustness or

use other identification schemes

47

48

Monetary policy transmission

49

Summary

VARs are one of the most important analysis tools in monetary

macroeconomics

Account for collinearity and dynamic correlation between variables

Need a minimum number of assumptions let the data speak

Three application areas

1. Desriptive analysis: need to choose number of variables and lags

2. Forecasting: need to shrink parameters towards zero BVAR

3. Structural analysis: need additional identification assumptions.

VAR methodology is restricted to study the transmission of one

time (temporary) suprise changes in policy. To study permanent

changes in policy regimes we need structural models.

50

ReferencesOverview VARs:

Stock, James H. and Mark W. Watson (2001). “Vector Autoregressions”, Journal of Economic Perspectives, 15(4): 101-115.

Structural Identification

Söderlind, P. (2005). “Lecture Notes in Empirical Macroeconomics”, available online on Paul Söderlind’swebsite.

Kilian, L. (2013). “Structural Vectorautoregressions“, in Handbook of Research Methods and Applications, Chapter 22.

Lütkepohl, H., and M. Krätzig (2004). “Applied Time Series Econometrics“, Cambridge University Press, Chapters 3 and 4.

Enders, W. (2004). “Applied Econometric Time Series“, John Wiley & Sons, Ch. 5.

Bayesian VARs

Koop, G., and D. Korobilis (2010). “Bayesian Multivariate Time Series Methods for Empirical Macroeconomics”, available on Gary Koop’s website

Canova, F. (2007). “Methods for Applied Macroeconomic Research“, Princeton University Press, Chapter 10.

Forecasting with Bayesian VARs

Karlsson, S. (2013). “Forecasting with Bayesian Vectorautoregressions“, Handbook of EconomicForecasting, Vol. 2, Chapter 15.

Bayesian VAR: Gibbs sampler (simulating the posterior distribution)

Blake, A., and H. Mumtaz (2012). “Applied Bayesian econometrics for central bankers“, Technical Handbook No. 4, Center for Central Banking Studies, Bank of England.

51