Joan Driggs

Vice President,

Content and Thought Leadership

March 2021

CONSUMER CONNECT:LOYALTY SNAPSHOT

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 2

Executive Summary

As seen throughout 2020, consumers report they prefer to shop fewer stores and are

less inclined to clip coupons. Their desire to shop deals remains strong.

Consumers are interested in personalizing their loyalty experience.

Among subscription service vendors, Amazon Prime holds the strongest lead, followed

by Chewy for pet products, and Walmart+.

Drug and grocery channels lead in loyalty/reward adoption, with high-income households

most likely to hold reward memberships across the most channels.

Despite the turmoil of 2020 due to COVID-19, consumers’ attitudes toward their

household financial health remains similar in 2021.

Consumer sentiment took a tumble among the dual health and financial crises of 2020

but is showing strong signs of recovery in early 2021.

Consumers want to see new benefits and experiences as a reward for loyalty.

Benefits influence membership and membership influences which stores to shop.

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 3

Consumer Sentiment Index

February 2021

Consumer Sentiment Is Trending Back Up From Dismal 2020

92.991.8

96.8

98.4

96.0

87.3

80

85

90

95

100

105

20212015 2016 2017 2018 2019 2020

81.5

Source: IRI, based on University of Michigan; Moody’s Analytics Forecasted 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 4

Despite Higher Unemployment and Economic Challenges

Consumers’ Financial Health Remains

Fairly Consistent to Year-Ago Levels

Agree With Statement Much More/Somewhat More

Source: IRI Consumer Connect™, Q1 2021

Household's Financial Situation

43%

40%

25%

46%

41%

24%

My household's financial

health is strained

My household is making sacrifices

to make ends meet

My household is having difficulty

affording needed groceries

Q1 2020Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 5

Consumer Grocery Shopping Behavior

Total Population

Consumers Shopping Fewer Stores to Seek Deals

and Show Less Interest in Clipping Coupons

86%

82%

81%

72%

57%

52%

31%

27%

87%

83%

82%

71%

60%

60%

27%

26%

Order online and pick up in store

Visit multiple retailers to keep my grocery bill lower

Make an effort to purchase my needed groceries

when they are “on sale” or on deal

Buy store brand products to save money

Make additional or unplanned purchases

if in-store deals are good

Try new, lower priced brands to save money

Order online for home delivery

Clip coupons from circulars/newspapers

Q1 2020Q1 2021

Frequently/Occasionally Summary

Source: IRI Consumer Connect™, Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 6

Consumer Grocery Shopping Behavior

Total Population

Good Value, Convenient Store Location and Strong Loyalty Card

Discount Programs Are Key Drivers in Choosing Where to Shop

95%

94%

94%

92%

91%

87%

74%

94%

94%

95%

92%

90%

86%

76%

Allows me to fill my basic needs

at the lowest possible cost

Good sale prices

Quick and easy in-and-out

Lowest everyday prices

Convenient store location

Assortment that allows for one-stop shopping

Strong loyalty card discount program

Q1 2020Q1 2021

Very/Somewhat Important Summary

Source: IRI Consumer Connect™, Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 7

Dollar Shave Club

Subscription Services

Total Population

Amazon Prime, Chewy and Walmart+ Are the

Top Subscription Services Among Consumers

Source: IRI_SubscriptionServices_January'21_Omnibus

51%

7%

4%

3%

2%

2%

2%

1%

1%

1%

43%

Dollar Shave Club

Chewy

Amazon Prime

Walmart+

Instacart Express

HelloFresh

Shipt

Grove Collaborative

BarkBox

Thrive Market

None of these

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 8

Shopper Loyalty Card/Rewards Membership

Total Population

Drug, Grocery and Online Paid Programs Are

Top Shopper Loyalty/Rewards Membership Choices

74%

69%

56%

51%

43%

35%

27%

26%

16%

Convenience (such as 7-Eleven, Circle K)

Specialty Beauty (such as Ulta, Sephora)

Grocery (such as Kroger, Safeway)

Food/Beverage Restaurant

(such as Starbucks, Dunkinʼ)

Drug (such as CVS, Walgreens)

Online with annual fee (such as

Amazon Prime, Walmart+, Shipt, Instacart)

Club (such as BJ’s, Costco)

Mass/Supercenter (such as Walmart, Target)

Dollar (such as Dollar General, Family Dollar)

I have a shopper loyalty card/rewards membership Summary

Source: IRI Consumer Connect™, Q1 2021

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 9

High-Income Group More Likely to Have Shopper

Loyalty/Rewards Membership Across Most Channels

19%

30%

23%

74%

71%

55%

39%

37%

28%

30%

28%

14%

81%

80%

70%

64%

55%

44%

35%

Club

29%

49%

Grocery69%

Drug

35%

Online with annual fee

Mass/Supercenter

22%

Food/Beverage Restaurant

Specialty Beauty

Convenience

Dollar

66%

78%

62%

59%

37%

31%43%

60%

44%

21%

18%

9%

< $35K $55K-$99.9K$35K-$54.9K > $100K

80%

64%

60%

53%

35%

68%

52%

61%

36%

79%

71%

52%

32%

16%

70%

51%

51%

28%

10%

3%

19%

32%

55%

Specialty Beauty

47%

Drug

Grocery

Club

Online with annual fee 60%

Convenience

Dollar

70%

76%

63%

15%

66%

41%

67%

46%

Mass/Supercenter

29%

5%

17%

50%32%

15%

51%36%

Food/Beverage Restaurant

20%

34%

25%

11%

Millennials SeniorsGen Z Gen X Boomers

Agree With Statement

Source: IRI Consumer Connect™, Q1 2021

Shopper Loyalty Card/Rewards Membership

By Income

Shopper Loyalty Card/Rewards Membership

By Generation

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 10

Reasons For Obtaining Shopper Loyalty Card/Rewards Membership

Total Population

Free Membership, Gas Discount and Ability to Spend Points Are

Main Reasons Consumers Subscribe to Shopper Loyalty Programs

74%

56%

55%

39%

38%

38%

35%

25%

13%

12%

Membership benefits made it

worth the annual fee

Personalized or special offers

It was free

Gas/fuel discount

Ability to accrue points to spend

Access to special members-only events

Cash reward

Free beverage/food item

Access to new product(s)

Option for mobile checkout

Base=Those Respondents Who Have Shopper Loyalty Card/Rewards Membership

Source: IRI Consumer Connect™, Q1 2021

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 11

Free Membership Is the Top Reason Among Income Groups

While Ability to Spend Points Is Important to Mid-Income Groups

75%

36%

38%

37%

25%

16%

14%

76%

56%

57%

35%

25%

74%

61%

57%

44%

41%

40%

35%

26%

13%

11%

77%

55%

43%

41%

47%

34%

11%

14%

Gas / fuel discount

32%

Ability to accrue points to spend)

13%

It was free

Free beverage/food item

Cash reward

Access to special

members-only events

Personalized or special offers

Membership benefits made

it worth the annual fee

Access to new product(s)

Option for mobile checkout

54%

36%

33%

12%

51%

58%

27%

23%

< $35K $35K-$54.9K $55K-$99.9K > $100K

Base=Those Respondents Who Have Shopper Loyalty Card/Rewards Membership

Source: IRI Consumer Connect™, Q1 2021

77%

41%

71%

28%

50%

28%

22%

6%

77%

60%

44%

42%

44%

28%

19%

16%

76%

56%

39%

41%

27%

16%

57%

38%

39%

28%

10%

66%

42%

46%

36%

24%

13%

16%

9%

3%

Free beverage/food item

It was free

Membership benefits made

it worth the annual fee

Cash reward

Gas / fuel discount

Ability to accrue points to spend)

Personalized or special offers

Access to special

members-only events

Option for mobile checkout

Access to new product(s)

35%

34%

55%

22%

28%

18%

72%

61%

51%

44%

35%

40%

13%

9%

Millennials Gen XGen Z Boomers Seniors

Reasons for Obtaining Shopper Loyalty

Card/Rewards Membership

By Income

Reasons for Obtaining Shopper Loyalty

Card/Rewards Membership

By Generation

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 12

Expected Services/Benefits With a Paid Membership

Total Population

Free and Same-Day Delivery and Access to Wider

Assortment Are Top Paid Membership Expectations

58%

39%

31%

28%

27%

23%

21%

19%

16%

Access to wider assortment

than what's found in-store

Prescription delivery

Pickup

Same-day delivery

Ability to communicate with personal shopper

No minimum order for free shipping

1-day delivery

2-day delivery

Checkout from phone if I shop in the store

Base=Those Respondents Who Consider/ Not Interested In Having Shopper Loyalty Card/Rewards Membership For Online With Annual Fee

Source: IRI Consumer Connect™, Q1 2021

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 13

Among Generations, Gen Xers and Boomers Expect

Free Shipping Without Order Limit From Paid Membership

39%

31%

30%

21%

22%

17%

28%

65%

41%

19%

21%

18%

45%

33%

26%

35%

19%

19%

21%

65%

29%

18%

24%

19%

Checkout from phone if

I shop in the store

No minimum order

for free shipping

Access to wider assortment

than what's found in-store

Same-day delivery

26%

Pickup

Prescription delivery

1-day delivery

2-day delivery

Ability to communicate

with personal shopper

55%

58%

38%

20%

35%

20%

25%

22%

31%

17%

24%

< $35K $35K-$54.9K $55K-$99.9K > $100K

Base=Those Respondents Who Consider/Not Interested In Having Shopper Loyalty Card/Rewards Membership For Online With Annual Fee

Source: IRI Consumer Connect™, Q1 2021

41%

15%

41%

36%

34%

35%

15%

24%

25%

54%

41%

28%

32%

26%

24%

31%

18%

24%

61%

48%

36%

32%

34%

21%

26%

20%

24%

60%

38%

23%

52%

24%

30%

24%

18%

12%

7%

14%

17%

No minimum order

for free shipping

Same-day delivery

Ability to communicate

with personal shopper

Pickup

Access to wider assortment

than what's found in-store

1-day delivery

23%

2-day delivery

Checkout from phone if

I shop in the store 17%

Prescription delivery

29%

28%

17%

14%

MillennialsGen Z Boomers SeniorsGen X

Expected Services/Benefits

With a Paid Membership

By Income

Expected Services/Benefits

With a Paid Membership

By Generation

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 14

Loyalty Across the Generations

Gen Xers Lead in Loyalty Program

Adoption and Use, Followed by Millennials

Source: The truth about customer loyalty, KPMG international, 2019

Source: https://home.kpmg/xx/en/home/insights/2019/11/customer-loyalty-survey.html

Loyalty Program Adoption Writing Positive Reviews

Loyalty Program Use

Enrolled in one of five loyalty

rewards programs

Likely to write positive review

About a brand they are loyal to

Make purchases that earn rewards/benefits

several times a week

54%

57%

60% 71%

66%

59%

40%

44%

40%

Millennials

(born 1982-1999)

Generation X

(born 1965-1981)

Baby Boomers

(born 1946-1964)

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 15

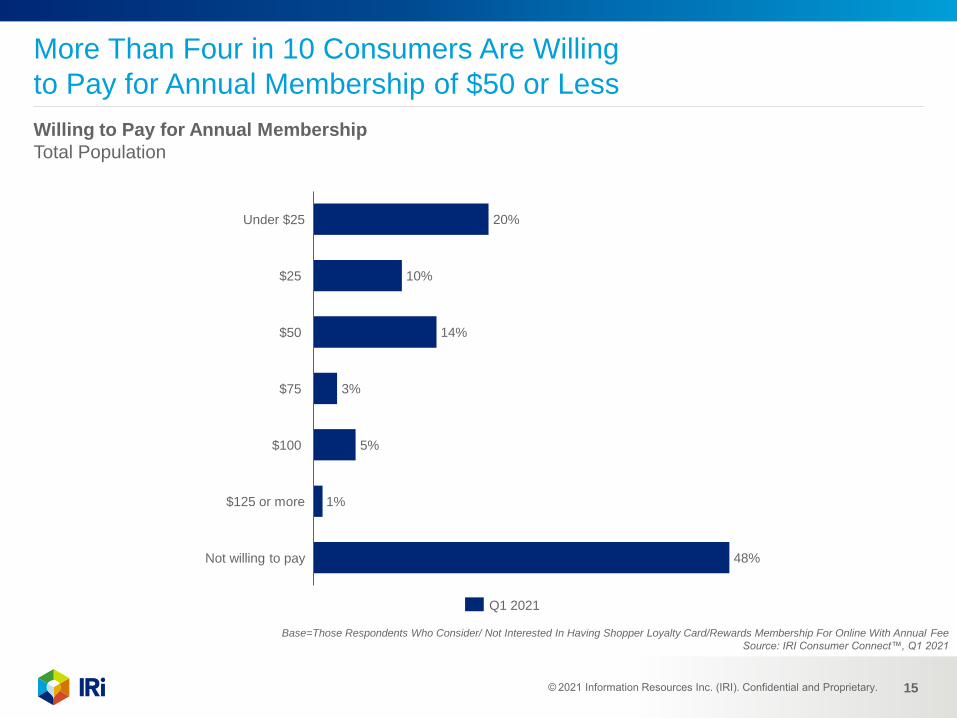

Willing to Pay for Annual Membership

Total Population

More Than Four in 10 Consumers Are Willing

to Pay for Annual Membership of $50 or Less

20%

10%

14%

3%

5%

1%

48%

$50

$100

Under $25

$25

$75

Not willing to pay

$125 or more

Base=Those Respondents Who Consider/ Not Interested In Having Shopper Loyalty Card/Rewards Membership For Online With Annual Fee

Source: IRI Consumer Connect™, Q1 2021

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 16

Influence of Shopper Loyalty Card/Rewards Membership Program on Shopping at Store

Total Population

Shopper Loyalty Programs Influence Choice of Stores to Shop

Agree With Statement

Source: IRI Consumer Connect™, Q1 2021

22%

51%

17%

10%

Extremely influential

Not very influential

Somewhat influential

Not at all influential

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 17

Reasons for Canceling Shopper Loyalty Card/Rewards Membership

Total Population

About a Third of Consumers Cite Membership Fees

as the Main Reason for Canceling a Loyalty Program

Agree With Statement

Source: IRI Consumer Connect™, Q1 2021

32%

30%

28%

16%

12%

6%

6%

3%Did not know I was signing up for a shopper

loyalty card/rewards membership

I no longer shop at the retailer

Due to privacy concerns/do not want

to share my personal information

Do not need the products the retailer sells

I don’t want to pay for membership

Didn’t want to pay an annual fee for membership

Not worth the hassle

I have too many loyalty cards

Q1 2021

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 18

Across Generations, Gen Z Cites the Most

Reasons for Canceling a Loyalty Membership

34%

31%

26%

17%

11%

6%

5%

4%

32%

29%

25%

18%

13%

8%

7%

3%

32%

34%

33%

14%

13%

6%

6%

3%

33%

28%

31%

17%

13%

9%

6%

1%

I no longer shop at the retailer

I don't want to pay

for membership

Did not know I was signing up for a

shopper loyalty card/

rewards membership

Didn't want to pay an annual

fee for a membership

Do not need the products

the retailer sells

Not worth the hassle

Due to privacy concerns/do not want

to share my personal information

I have too many loyalty cards

< $35K $35K-$54.9K $55K-$99.9K > $100K

Agree With Statement

Source: IRI Consumer Connect™, Q1 2021

55%

45%

34%

17%

17%

5%

9%

19%

10%

7%

34%

30%

32%

12%

5%

2%

30%

15%

12%

4%

6%

2%

22%

19%

13%

11%

3%

7%

2%

Didn't want to pay an annual

fee for a membership

Do not need the products

the retailer sells

I don't want to pay

for membership

14%

I no longer shop at the retailer

I have too many loyalty cards

Not worth the hassle

Due to privacy concerns/do not want

to share my personal information

Did not know I was signing up for a

shopper loyalty card/

rewards membership

37%

5%

30%

0%

33%

23%

30%

27%

16%

7%

Gen Z BoomersMillennials SeniorsGen X

Reasons for Canceling Shopper

Loyalty Card/Rewards Membership

By Income

Reasons for Canceling Shopper

Loyalty Card/Rewards Membership

By Generation

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 19

Survey Question

Indicate if You Agree With the Following Statements About Loyalty Programs

Consumers Are Interested in Personalizing Every Element

of Their Loyalty Experience, From Earning to Redeeming

Source: https://www.merkleinc.com/thought-leadership/white-papers/2020-loyalty-barometer-report

85%

76%

74%

73%

72%

67%

64%

Recognize me as a member

Personalize the way I earn based on my purchases

Allow me to select benefits and rewards I receive

Personalize the way I earn based on my preferences

Show me products/services based on preferences

Offer personalized rewards

Show me products/services based on purchases

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 20

Source: https://home.kpmg/xx/en/home/insights/2019/11/customer-loyalty-survey.html

About

Benefits

for retailers

Challenges

for retailers/

customers

Point-based loyalty

reward cards with

point accumulation

on every purchase

Access to purchase-

related data

Low customer

participation/retention

— unused points act as

liability for the retailers

Advanced loyalty

reward cards, offering

vouchers/coupons in

addition to redeemable

points

Multi-brand, tier-

based loyalty reward

cards with an option to

use across multiple

retail brands

Privilege loyalty

program with

personalized and

customized offers

Umbrella loyalty

program with

enhanced convenience

— everything under

one ecosystem —

along with rewards

Enables cross-selling,

product bundling —

using insights derived

from transactional data

Enhanced customer

engagement — one

card for a group of

retailers

Increased engagement

— offers ecosystem

of value, service and

content; additional

income as subscription

fees

Ability to offer

integrated experiences

between online and

offline channels; tracks

the entire consumer

behavior inside the

ecosystemUnable to meet

growing customer

demand of those who

seek more value than

just reward points or

vouchers

Expensive scheme for

retailers with little

customer insight

around each individual

brand

No tier-based rewards;

no single interface

to access grocery

shopping, video

or music

Available in China and

U.S., but other countries

may rely on outside

delivery, with no

home/overnight delivery

Phase

01Phase

02Phase

03Phase

04Phase

05

Examples* MasterCard Rewards

*Note Examples based on above program definitions

DSW VIP program Lancôme tiered

loyalty programRun Everything Labs

Rewards

Amazon Prime

Retailers Expand From Point-Based Loyalty Programs

Retailers Are Moving Toward Integrated and Unified Rewards

Programs to Provide Personalized Offers and Experiences

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 21

To Succeed, a Loyalty Ecosystem Should Be

Centered Around Seven Design Principles

Shared Consumer in Mind

The program must be highly personalized to the individual consumer, leveraging the full stack of consumer data across brands

to offer personalized messages, offers and experiences. Brands should mutually understand the value of the consumer.

Brand Synergy

The program must be structured to elevate brand equity. Every brand must have an important role in the given ecosystem and

provide value to that ecosystem through its products and/or services.

Diversity of Products and Services

The program must provide consumers with value through tangible goods, services or experiences in order to reinforce the

program’s underlying appeal. Brands should develop common features and benefits together.

Seamless Consumer Experience

Sign-ups, use and redemption must be intuitive and responsive, keeping the program simple for consumers.

All-In Brand Commitment

Companies must be willing to commit to the partnership, allocating adequate marketing spend and having clear agreements

about sharing consumer data in a way that adheres to all relevant regulations.

Alignment on Governance Process

Brands should enter the partnership with aligned strategies and goals, defined roles and responsibilities, and a process for

managing risk effectively.

Data and Tech Focused on Connectivity

Brands will need to ensure, within the confines of the shifting regulatory landscape, that their data can be exported or used as

needed — for example, through the use of application programming interfaces (APIs). Brands within the ecosystem need to

commit to standards and processes for tracking key performance indicators, adhering to regulations, and establishing

protocols for connecting technologies and sharing data.

Source: https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/preparing-for-loyaltys-next-frontier-ecosystems

1

2

3

4

5

6

7

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 22

About the Consumer Connect Index

The Consumer Connect Index (CCI) is intended to monitor

consumers’ financial health and their purchase behavior in terms

of brand loyalty, attitudes toward organic/natural food and

beverages, perception of national vs. store brands, and frequency

of using retailer and manufacturer coupons.

CCI uses the data collected through the Consumer Connect

Survey every quarter, which is benchmarked to Q1 2020

(indexed at 100).

Higher CCI index means that consumers have better financial

health, are more loyal to certain brands in each category, give

higher importance to organic/natural food and beverages, have

better perception toward national brands, and use retailer and

manufacturer coupons less frequently.

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 23

Measures

CCI is measured based on responses to five questions:

1. My household’s financial health is good (Agreement Scale)

2. Store brands are a better value than national brands (Agreement Scale)

3. Download coupons from a retailer/manufacturer website (Frequency Scale)

4. Good selection of natural/organic food/beverages (Importance Scale)

5. I have a few brand(s) in each category I will stay loyal to (Frequency Scale)

Calculation

Calculate weighted

proportion for each

question by 3 age

groups — (T2B for all

questions except B2B

for the 3rd question).

Get total weighted

proportion based on

each question

CCI = (current

quarter’s weighted

average of all 5

questions divided by

the average of Q1

2020)*100

Sample and Assumptions

The Consumer Connect Survey is fielded to a nationally representative Consumer Network sample of over

2,000 respondents every quarter. Sample demos are comparable over time and changes in the state of the

economy and the CPG industry are reflected in each quarter.

Methodology

© 2021 Information Resources Inc. (IRI). Confidential and Proprietary. 24© 2021 Information Resources Inc. (IRI).

Confidential and Proprietary.24

CONTACT US FOR MORE

INFORMATION

IRI Global Headquarters

203 N. LaSalle St., Suite 1500

Chicago, IL 60601

+1 312.726.1221

Follow IRI on Twitter: @IRIworldwide