Mr. Mark S Turowicz

Country LeaderHoneywell Performance Materials and Technologies Managing DirectorUOP India Pvt Ltd

Based in Gurgaon, Mr. Mark is responsible for local resourcemanagement and operational alignment with the unit’s overallobjectives and worldwide functional organizations.

A graduate chemical engineer, in his 30 + years with UOP, Mr. Mark hasserved in various capacities including field operating services, technicaland continuing service, technology sales support and licensing,ventures and business development and management.

In addition to the US and India, his international work experienceincludes assignments in Europe, North Africa, S. America, and theMiddle East.

Pathways to PetrochemicalsPathways to Petrochemicals

© 2013 UOP LLC. All rights reserved.

Mark Turowicz

UOP India Private Limited -- A Honeywell Company

Mark Turowicz

UOP India Private Limited -- A Honeywell Company

Indian Oil Petrochemical ConclaveMarch 18th, 2013Gurgaon, India

UOP 6012-1

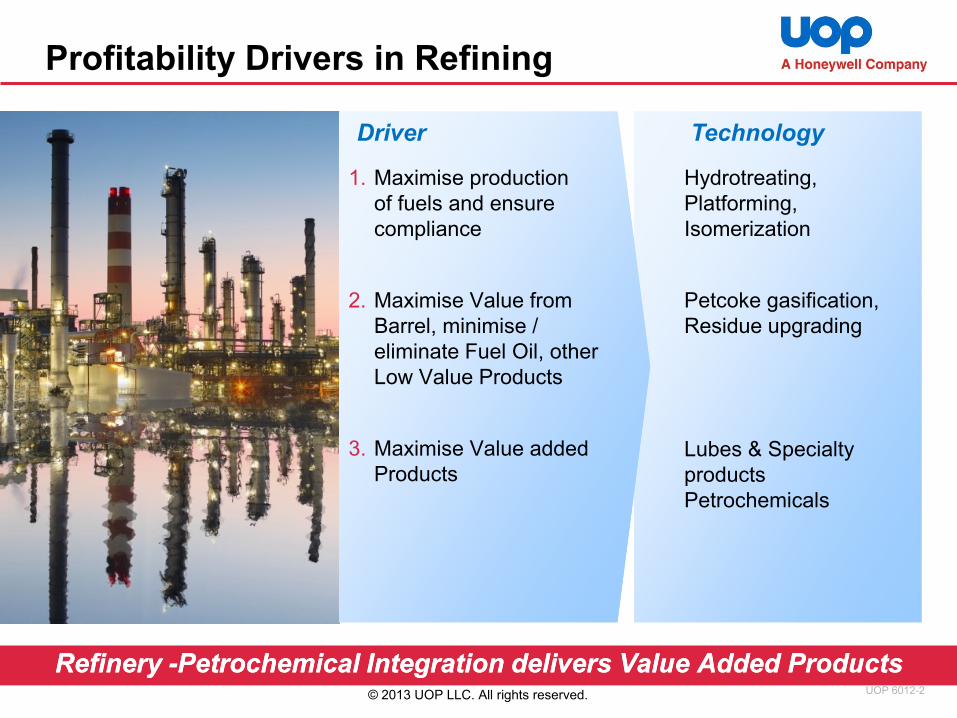

Profitability Drivers in Refining

Refinery Refinery --Petrochemical Integration delivers Value Added Products Petrochemical Integration delivers Value Added Products

1. Maximise production

of fuels and ensure

compliance

2. Maximise Value from

Barrel, minimise /

eliminate Fuel Oil, other

Low Value Products

3. Maximise Value added

Products

Driver Technology

Hydrotreating,

Platforming,

Isomerization

Petcoke gasification,

Residue upgrading

Lubes & Specialty

products

Petrochemicals

UOP 6012-2© 2013 UOP LLC. All rights reserved.

Kerosene

Benzene

N-Paraffin

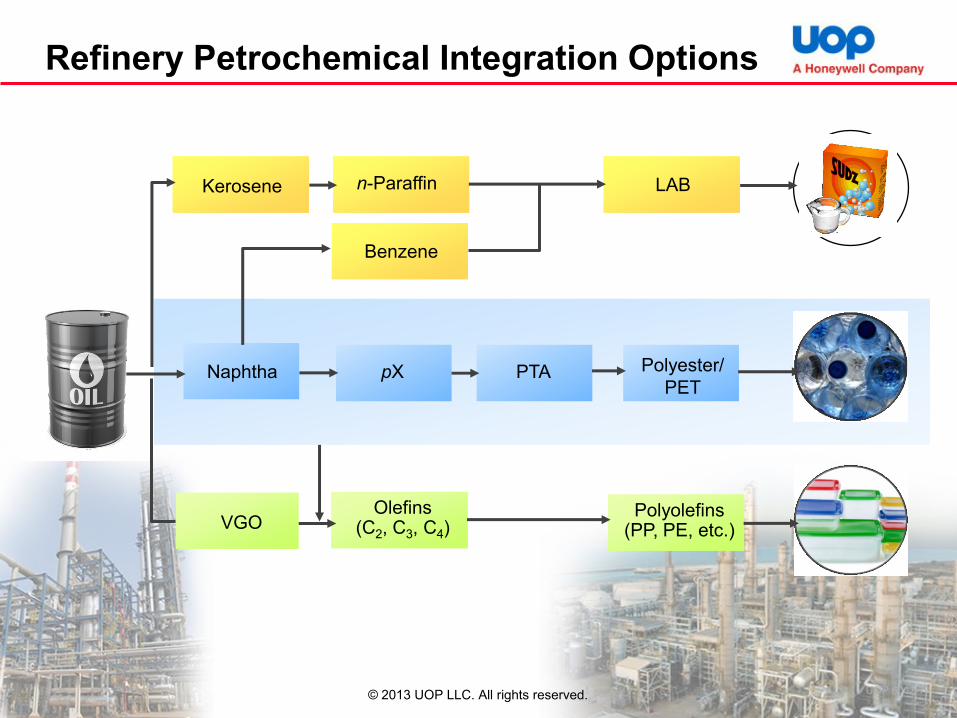

Refinery Petrochemical Integration Options

Kerosene n-Paraffin LAB

Benzene

Naphtha pX PTA Polyester/

PET

Olefins(C2, C3, C4)

Polyolefins(PP, PE, etc.)VGO

UOP 6012-3© 2013 UOP LLC. All rights reserved.

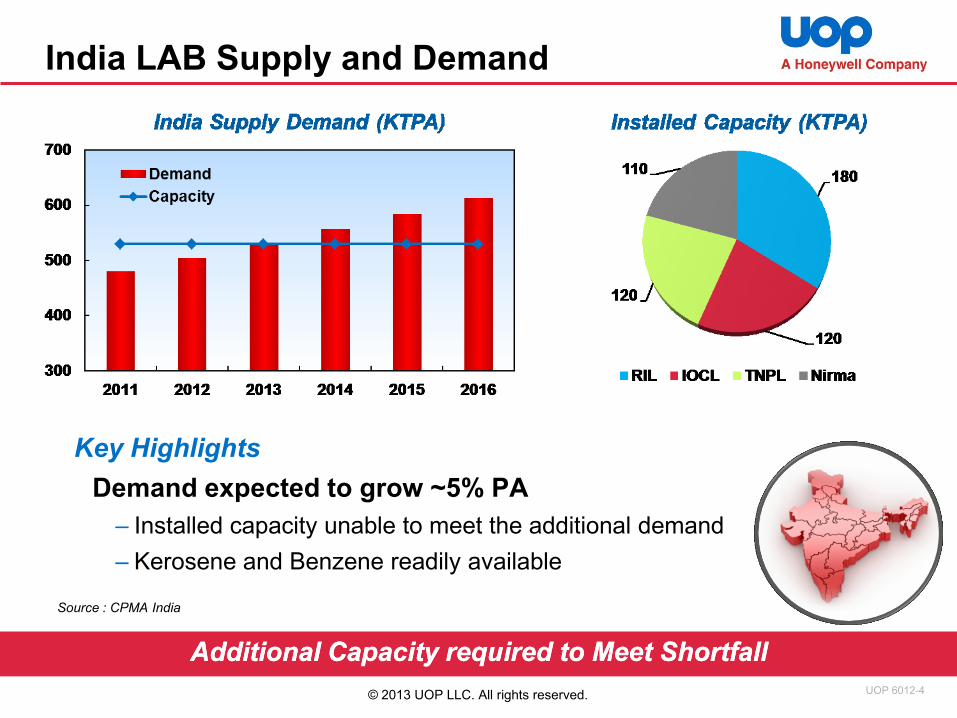

India LAB Supply and Demand

Key Highlights

Demand expected to grow ~5% PA

– Installed capacity unable to meet the additional demand

– Kerosene and Benzene readily available

Source : CPMA India

Additional Capacity required to Meet ShortfallAdditional Capacity required to Meet Shortfall

UOP 6012-4© 2013 UOP LLC. All rights reserved.

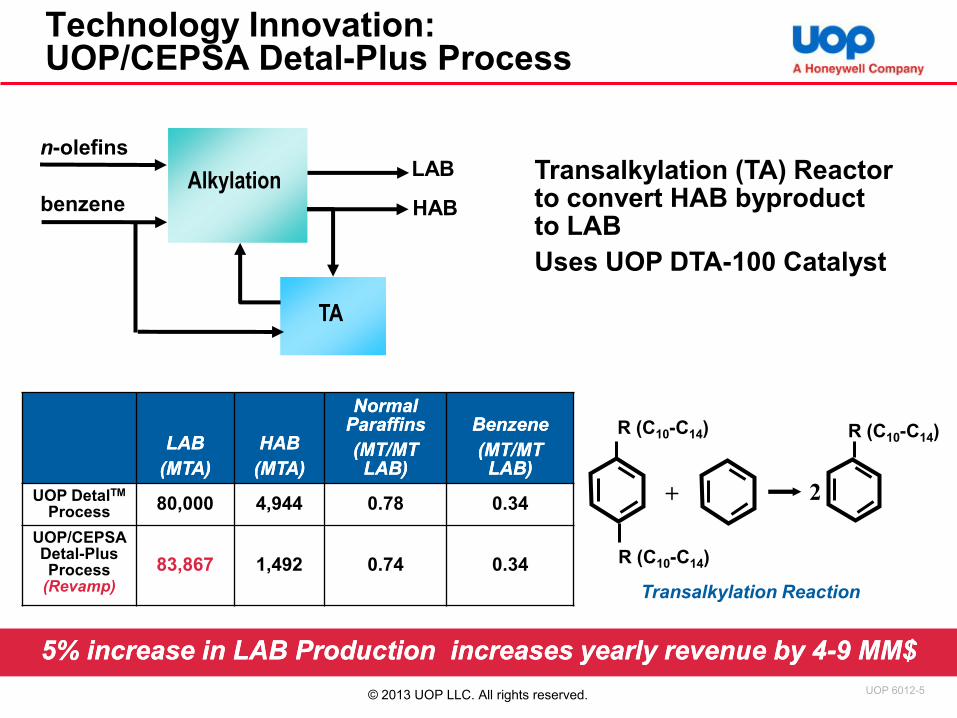

Technology Innovation: UOP/CEPSA Detal-Plus Process

5% increase in LAB Production increases yearly revenue by 45% increase in LAB Production increases yearly revenue by 4--9 MM$9 MM$

Alkylation

TA

HAB

LAB

benzene

n-olefinsTransalkylation (TA) Reactor to convert HAB byproduct to LAB

Uses UOP DTA-100 Catalyst

+

R (C10-C14)

R (C10-C14)

R (C10-C14)

2

LABLAB

(MTA)(MTA)

HABHAB

(MTA)(MTA)

Normal Normal ParaffinsParaffins

(MT/MT (MT/MT LAB)LAB)

BenzeneBenzene

(MT/MT (MT/MT LAB)LAB)

UOP DetalTM

Process 80,000 4,944 0.78 0.34

UOP/CEPSA Detal-Plus Process

(Revamp)

83,867 1,492 0.74 0.34

Transalkylation Reaction

UOP 6012-5© 2013 UOP LLC. All rights reserved.

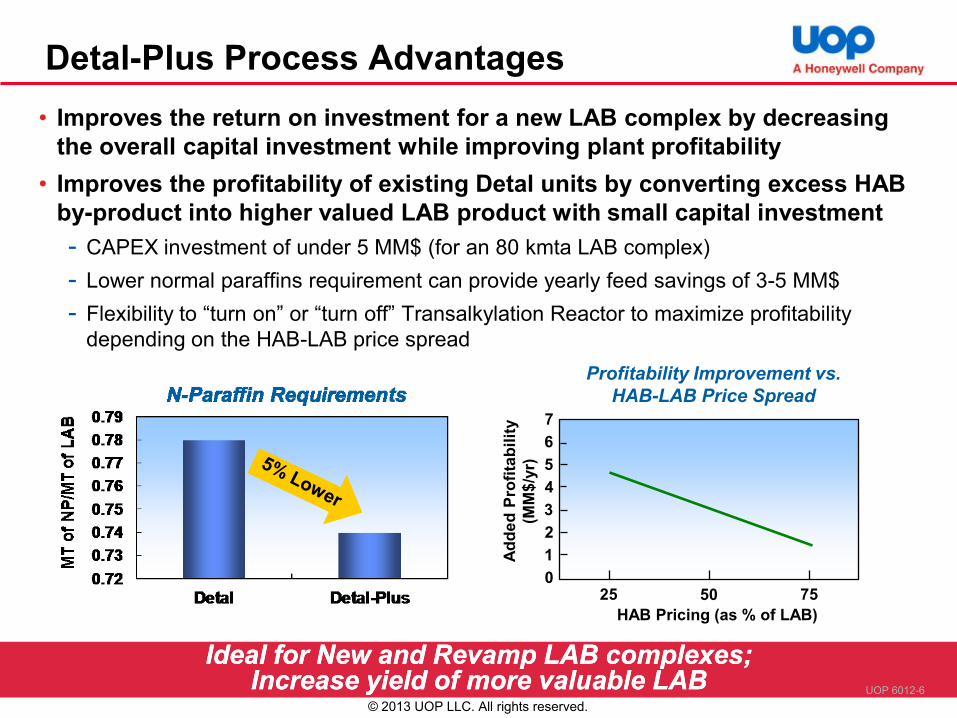

Detal-Plus Process Advantages

• Improves the return on investment for a new LAB complex by decreasing

the overall capital investment while improving plant profitability

• Improves the profitability of existing Detal units by converting excess HAB

by-product into higher valued LAB product with small capital investment

- CAPEX investment of under 5 MM$ (for an 80 kmta LAB complex)

- Lower normal paraffins requirement can provide yearly feed savings of 3-5 MM$

- Flexibility to “turn on” or “turn off” Transalkylation Reactor to maximize profitability

depending on the HAB-LAB price spread

Ideal for New and Revamp LAB complexes; Ideal for New and Revamp LAB complexes; Increase yield of more valuable LAB Increase yield of more valuable LAB

Profitability Improvement vs.

HAB-LAB Price Spread

Ad

de

d P

rofi

tab

ilit

y

(MM

$/y

r)

HAB Pricing (as % of LAB)

25 50 750

1

3

2

4

5

6

7

UOP 6012-6

© 2013 UOP LLC. All rights reserved.

Kerosene

Benzene

N-Paraffin

Refinery Petrochemical Integration Options

Kerosene n-Paraffin LAB

Benzene

Naphtha pX PTA

Olefins(C2, C3, C4)

Polyolefins(PP, PE, etc.)VGO

UOP 6012-7

Polyester/

PET

© 2013 UOP LLC. All rights reserved.

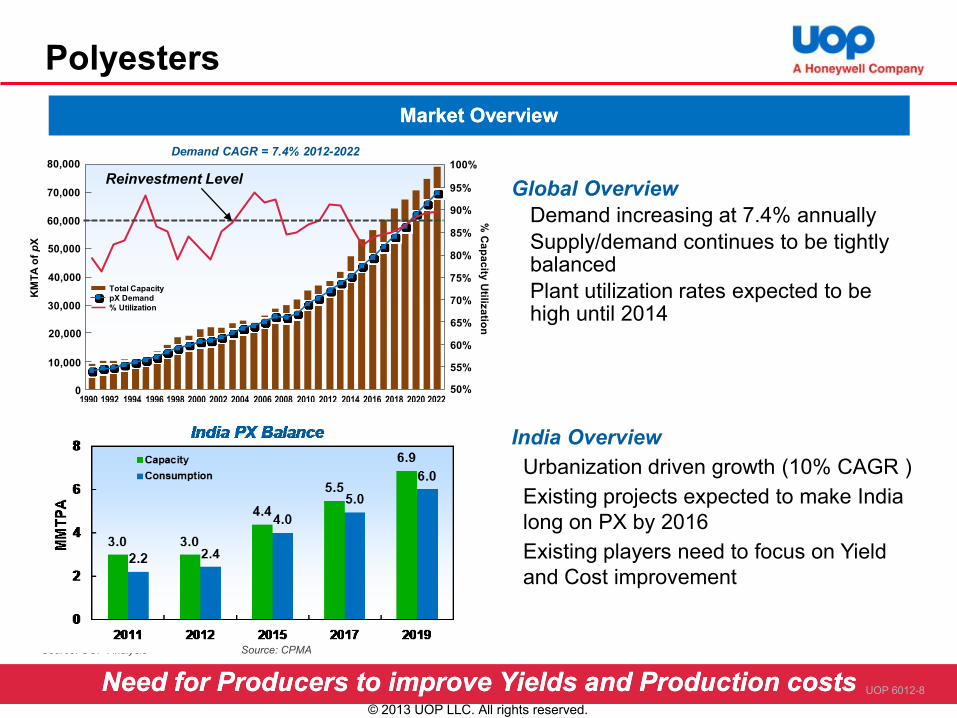

Polyesters

India Overview

Urbanization driven growth (10% CAGR )

Existing projects expected to make India

long on PX by 2016

Existing players need to focus on Yield

and Cost improvement

Market OverviewMarket Overview

Source: UOP Analysis

Source: CPMA IndiaNeed for Producers to improve Yields and Production costsNeed for Producers to improve Yields and Production costs

Source: CPMA

Global Overview

Demand increasing at 7.4% annually

Supply/demand continues to be tightly balanced

Plant utilization rates expected to be high until 2014

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

01990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Demand CAGR = 7.4% 2012-2022

KM

TA

of

pX

% C

ap

ac

ity U

tiliza

tion

Total Capacity

pX Demand

% Utilization

Source: UOP (SBA-CCI & PCI)

Reinvestment Level

UOP 6012-8

© 2013 UOP LLC. All rights reserved.

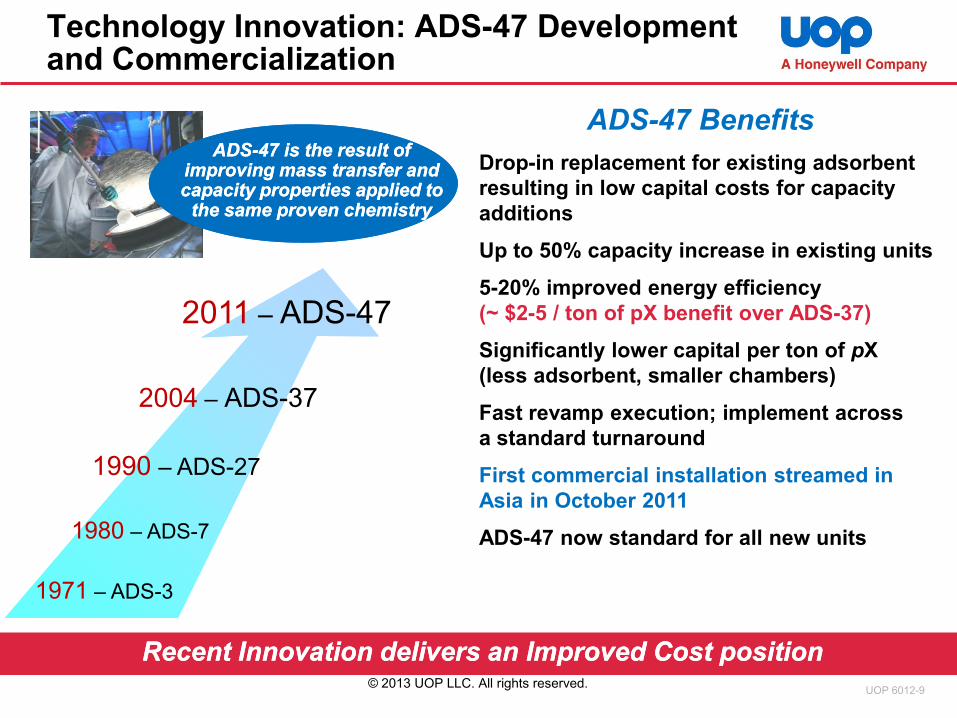

Technology Innovation: ADS-47 Development and Commercialization

Drop-in replacement for existing adsorbent

resulting in low capital costs for capacity

additions

Up to 50% capacity increase in existing units

5-20% improved energy efficiency

(~ $2-5 / ton of pX benefit over ADS-37)

Significantly lower capital per ton of pX

(less adsorbent, smaller chambers)

Fast revamp execution; implement across

a standard turnaround

First commercial installation streamed in

Asia in October 2011

ADS-47 now standard for all new units

ADS-47 Benefits

1971 – ADS-3

1980 – ADS-7

1990 – ADS-27

2004 – ADS-37

2011 – ADS-47

Recent Innovation delivers an Improved Cost positionRecent Innovation delivers an Improved Cost position

ADSADS--47 is the result of 47 is the result of improving mass transfer and improving mass transfer and capacity properties applied to capacity properties applied to

the same proven chemistry the same proven chemistry

UOP 6012-9© 2013 UOP LLC. All rights reserved.

Kerosene

Benzene

N-Paraffin

Refinery Petrochemical Integration Options

Kerosene n-Paraffin LAB

Benzene

Naphtha pX PTA

Olefins(C2, C3, C4)

Polyolefins(PP, PE, etc.)VGO

UOP 6012-10

Polyester/

PET

© 2013 UOP LLC. All rights reserved.

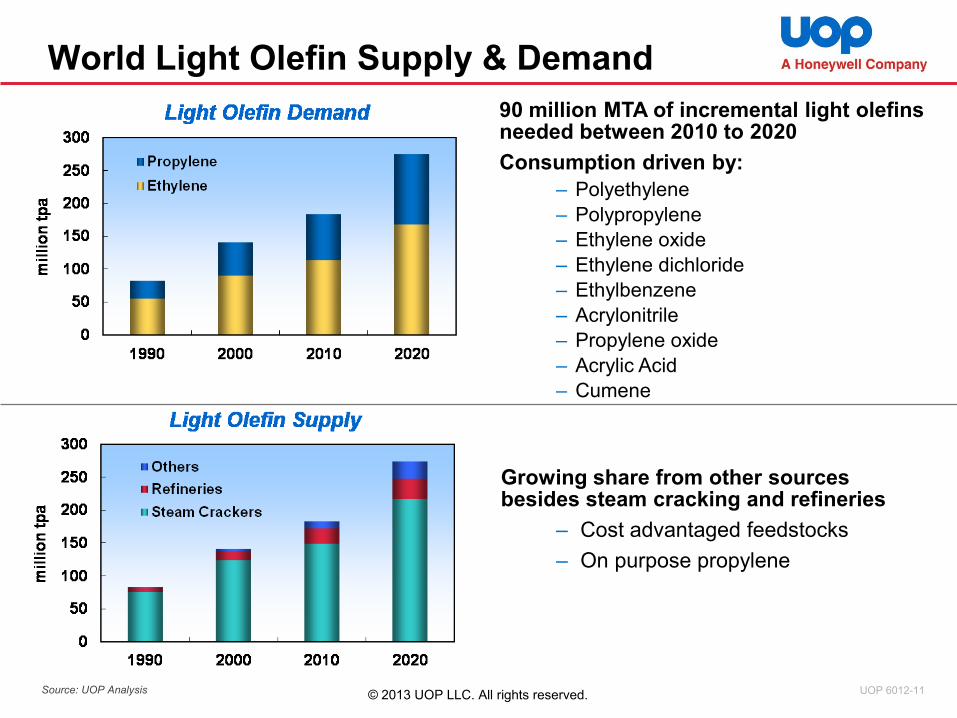

World Light Olefin Supply & Demand

90 million MTA of incremental light olefins needed between 2010 to 2020

Consumption driven by:

– Polyethylene

– Polypropylene

– Ethylene oxide

– Ethylene dichloride

– Ethylbenzene

– Acrylonitrile

– Propylene oxide

– Acrylic Acid

– Cumene

Growing share from other sources besides steam cracking and refineries

– Cost advantaged feedstocks

– On purpose propylene

Source: UOP Analysis UOP 6012-11© 2013 UOP LLC. All rights reserved.

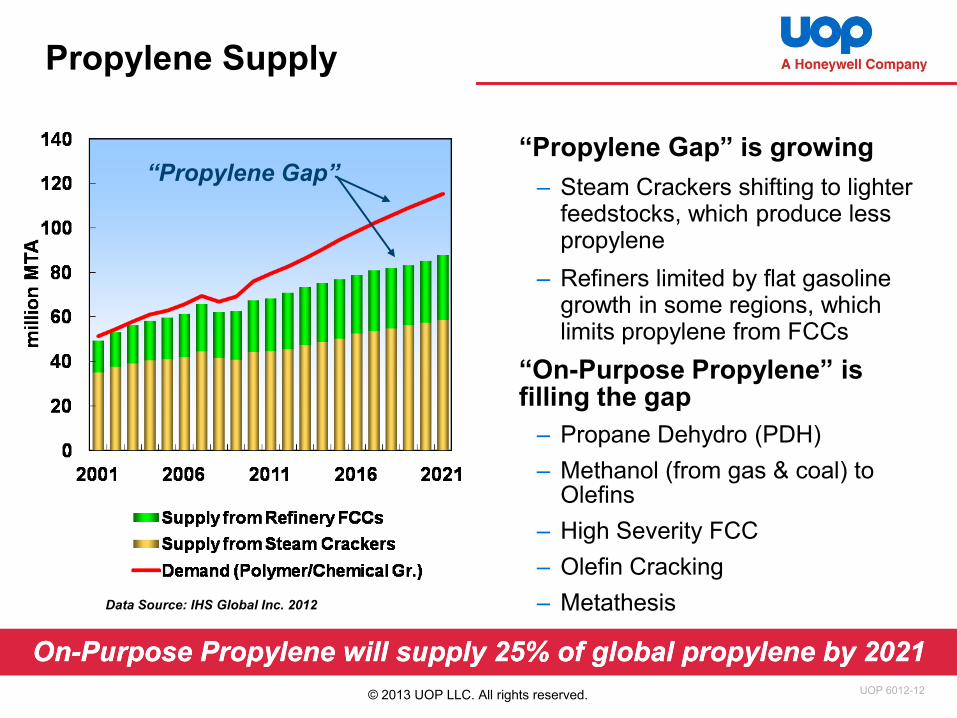

“Propylene Gap” is growing

– Steam Crackers shifting to lighter feedstocks, which produce less propylene

– Refiners limited by flat gasoline growth in some regions, which limits propylene from FCCs

“On-Purpose Propylene” is filling the gap

– Propane Dehydro (PDH)

– Methanol (from gas & coal) to Olefins

– High Severity FCC

– Olefin Cracking

– Metathesis

Propylene Supply

“Propylene Gap”

OnOn--Purpose Propylene will supply 25% of global propylene by 2021Purpose Propylene will supply 25% of global propylene by 2021

Data Source: IHS Global Inc. 2012

UOP 6012-12© 2013 UOP LLC. All rights reserved.

Pathways to Olefins

Naphtha Cracker // Gas Cracker

India is long Naphtha and short on Natural Gas

Naphtha prices linked to Crude –challenging economics

India Relevance Routes

India is short LPG

Most imported LPG allocated for domestic use

Abundant Coal offers opportunities for CTO

Surplus Methanol capacity in Region- potential for MTO

Propane Dehydrogenation

Coal / Methanol to Olefins

Limited by FCC capacityHi severity FCC of VGO

10%

90%

0%

0%

Share of Production in

India

Need for India to explore new pathwaysNeed for India to explore new pathwaysUOP 6012-13

© 2013 UOP LLC. All rights reserved.

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

100

90

80

70

60

50

40

30

20

10

0

94 93

74

8589

93

8189 89

(„000 t

on

nes

)

2008-2009

2009-2010 E

2010-2011

2011-2012 E

2012-2013 F

2013-2014 F

2014-2015 F

2015-2016 F

2016-2017 F

%

Capacity Consumption Operating Rate (per cent)

Olefins in India

Ethylene Supply / Demand (MMTPA)Ethylene Supply / Demand (MMTPA)

Key HighlightsKey Highlights

High growth expected across all Olefin derivatives– driven by increasing middle class growth and urbanization

Supply gap expected to grow

– Slowdown in FCC investments -

Limited new refining capacities

expected

– Limited new investments in cracking –

driven by high Naphtha prices and

slowdown in domestic gas production

Propylene Supply / Demand (MMTPA)Propylene Supply / Demand (MMTPA)

Potential to meet the gap through alternatives Potential to meet the gap through alternatives –– PDH & MTOPDH & MTOSource: CRISIL Research,2012 UOP 6012-14

5,000

4,500

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

0

100

90

80

70

60

50

40

30

20

10

0

8388 85

95

79

88 8995 97

(„000 t

on

ne

s)

2008-2009

2009-2010 E

2010-2011

2011-2012 E

2012-2013 F

2013-2014 F

2014-2015 F

2015-2016 F

2016-2017 F

%

Capacity Consumption Operating Rate (per cent)

© 2013 UOP LLC. All rights reserved.

Propane Dehydro with UOP Oleflex Technology

A UOP Oleflex plant converts one feed (C3 LPG) …into one primary product (propylene) …

with the option to export by-product hydrogen

C3 LPG Propylene

Hydrogen

One feed – one productSimple back integrationProven Investment

Low Capital IntensityHighest Yield of PropyleneAttractive Rate of Return

Key Features …

UOP 6012-17© 2013 UOP LLC. All rights reserved.

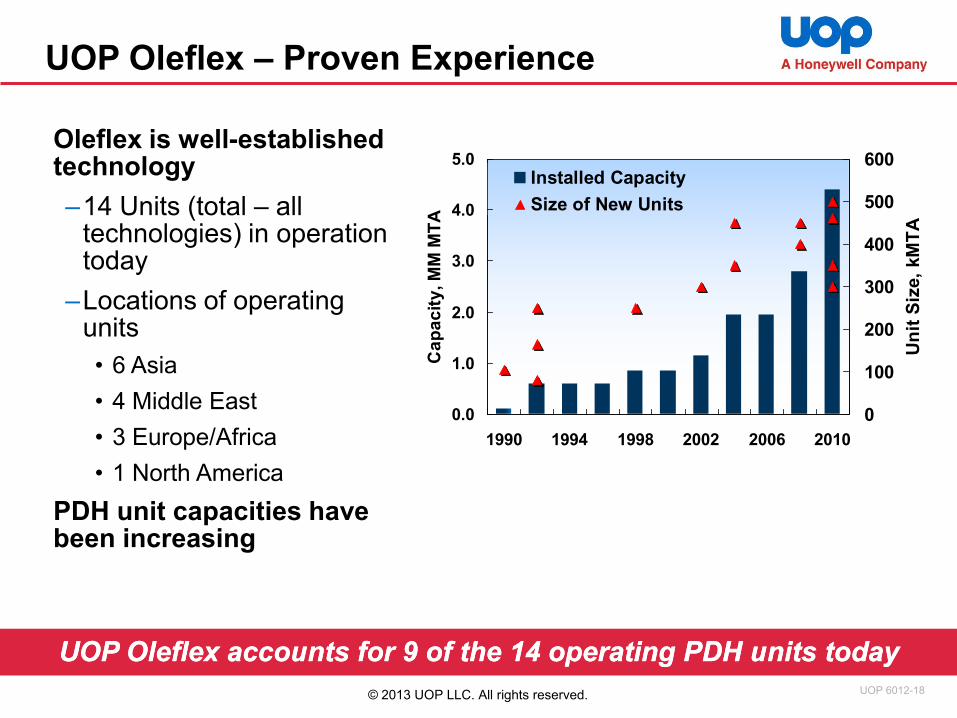

Oleflex is well-established technology

–14 Units (total – all technologies) in operation today

–Locations of operating units

• 6 Asia

• 4 Middle East

• 3 Europe/Africa

• 1 North America

PDH unit capacities have been increasing

UOP Oleflex – Proven Experience

UOP UOP OleflexOleflex accounts for 9 of the 14 operating PDH units todayaccounts for 9 of the 14 operating PDH units today

0.0

1.0

2.0

3.0

4.0

5.0

1990 1994 1998 2002 2006 2010C

ap

ac

ity

, M

M M

TA

0

100

200

300

400

500

600

Un

it S

ize,

kM

TA

Installed Capacity

Size of New Units

UOP 6012-18© 2013 UOP LLC. All rights reserved.

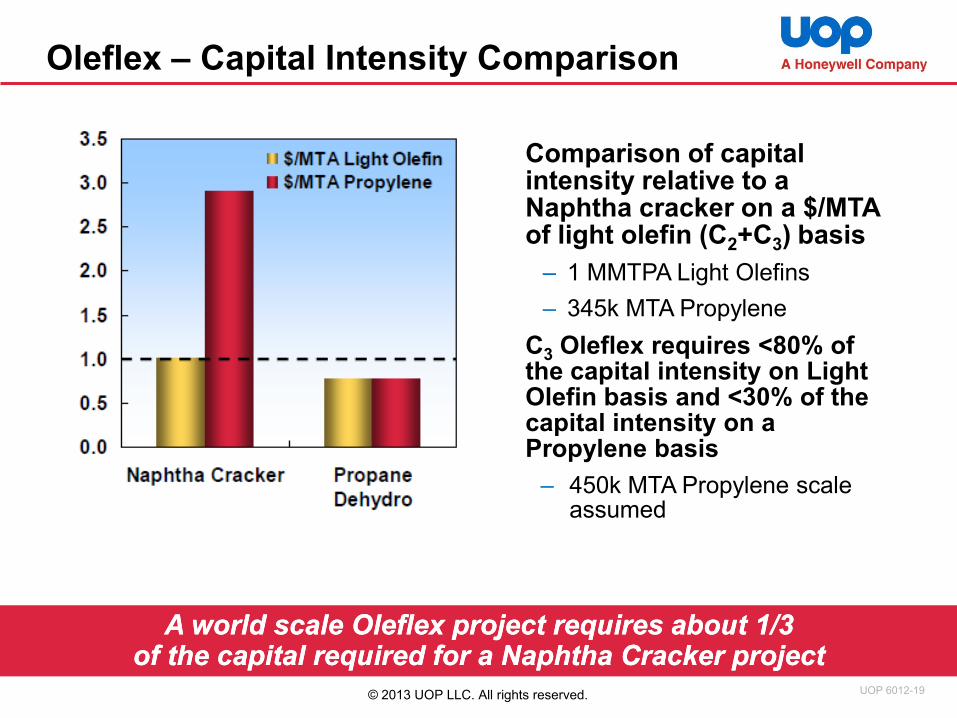

Oleflex – Capital Intensity Comparison

Comparison of capital intensity relative to a Naphtha cracker on a $/MTA of light olefin (C2+C3) basis

– 1 MMTPA Light Olefins

– 345k MTA Propylene

C3 Oleflex requires <80% of the capital intensity on Light Olefin basis and <30% of the capital intensity on a Propylene basis

– 450k MTA Propylene scale assumed

A world scale A world scale OleflexOleflex project requires about 1/3 project requires about 1/3 of the capital required for a Naphtha Cracker projectof the capital required for a Naphtha Cracker project

UOP 6012-19© 2013 UOP LLC. All rights reserved.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Ole

fin

Ca

pa

cit

y,

kM

TA

Award, Design or Construction

Commissioned

iC4 DehydroC3 Dehydro

5units

8units

3 units

C3/iC4 Dehydro

UOP Oleflex Capacity

4 units

1 unit

14units

UOP has been awarded 19 of the last 22 dehydro projects

world-wide since 2011

2 PDH Projects at 750 kmta propylene capacity

UOP 5881-20

High market activity in response to end-product demand and feedstock availability

© 2013 UOP LLC. All rights reserved.

UOP Methanol-to-Olefins (MTO)

EthylenePropylene

UOP MTOMethanol to Olefins

SynGas MethanolReformer Converter

Olefin DerivativeUnits

Methanol

Products (examples)

PolyethylenePolypropyleneEthylene DichlorideEthylene OxideEthyl BenzeneAcrylonitrilePropylene OxideAcrylic AcidOthers

Feedstocks

Natural gas orCoal orPetroleum Coke orBiomass

Commercial Technologies

New Feedstock and Catalyst using Commercially Proven Equipment

Commercial Technologies

(By Others)

UOP 6012-21© 2013 UOP LLC. All rights reserved.

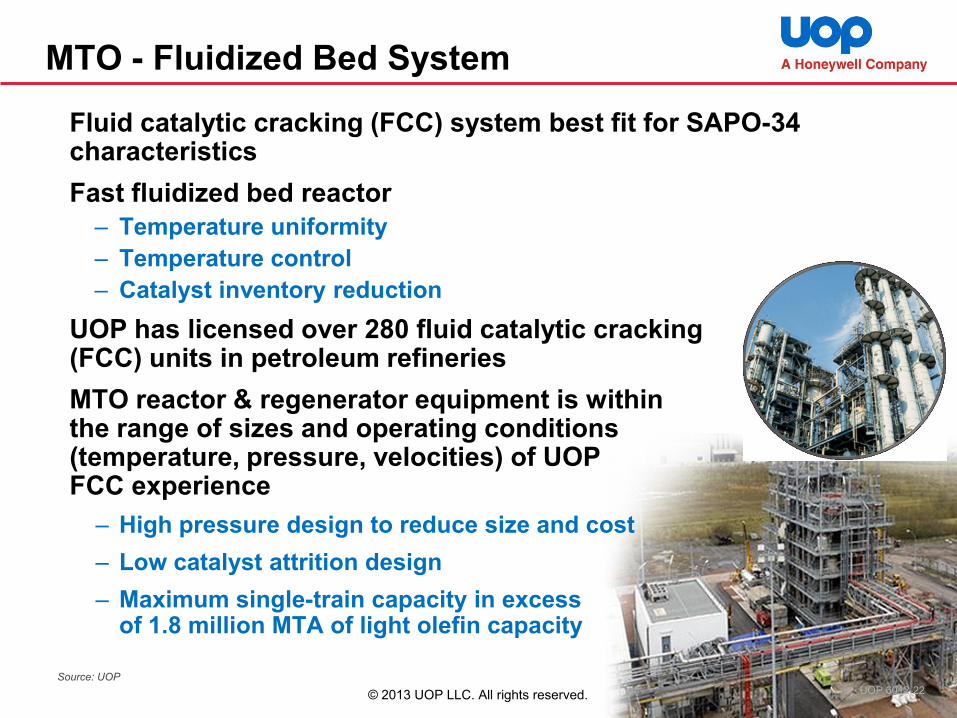

Fluid catalytic cracking (FCC) system best fit for SAPO-34 characteristics

Fast fluidized bed reactor

– Temperature uniformity

– Temperature control

– Catalyst inventory reduction

UOP has licensed over 280 fluid catalytic cracking (FCC) units in petroleum refineries

MTO reactor & regenerator equipment is within the range of sizes and operating conditions (temperature, pressure, velocities) of UOP FCC experience

– High pressure design to reduce size and cost

– Low catalyst attrition design

– Maximum single-train capacity in excess of 1.8 million MTA of light olefin capacity

MTO - Fluidized Bed System

Source: UOP

UOP 6012-22© 2013 UOP LLC. All rights reserved.

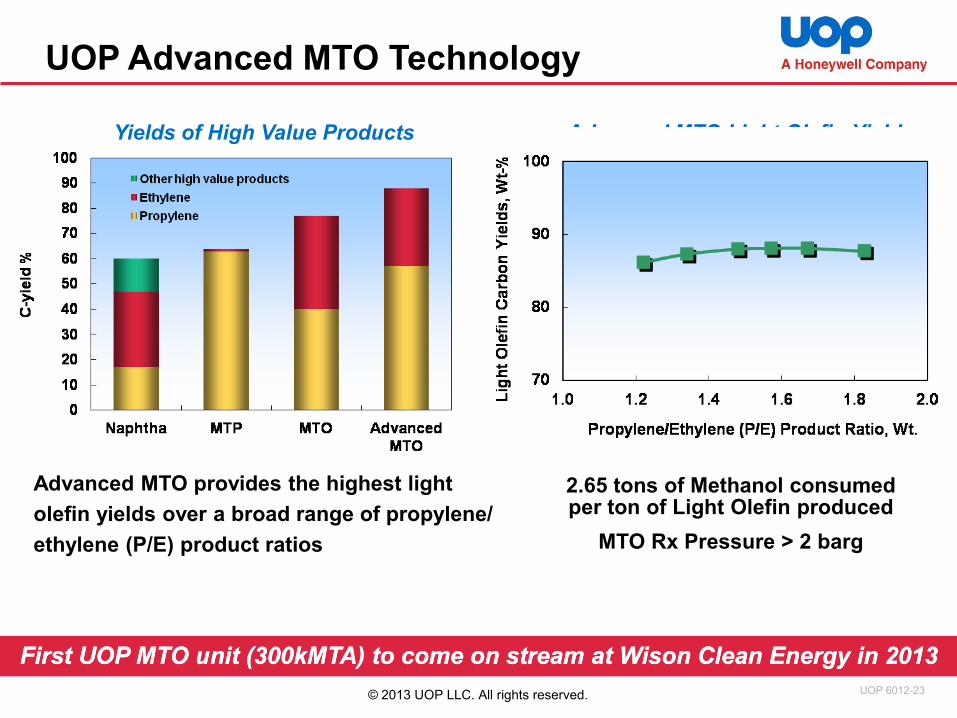

UOP Advanced MTO Technology

Advanced MTO Light Olefin Yields

Advanced MTO provides the highest light

olefin yields over a broad range of propylene/

ethylene (P/E) product ratios

Yields of High Value Products

2.65 tons of Methanol consumed per ton of Light Olefin produced

MTO Rx Pressure > 2 barg

First UOP MTO unit (300kMTA) to come on stream at Wison Clean Energy in 2013First UOP MTO unit (300kMTA) to come on stream at Wison Clean Energy in 2013

UOP 6012-23© 2013 UOP LLC. All rights reserved.

Summary

Petrochemical integration offers a proven route

to enhancing Refinery Profitability over the long

term

Expensive feedstock (Naphtha, India Gas pricing)

represents a challenge to Conventional

petrochemical processes

Novel technologies processing cost advantaged

feedstocks provide a profitable alternative to

traditional Petrochemical integration schemes

UOP 6012-24© 2013 UOP LLC. All rights reserved.

THANK YOU

UOP 6012-25© 2013 UOP LLC. All rights reserved.