CREDIT RISK MEASUREMENT

Classes #14; Chap 11

Lecture Outline

Purpose: Gain a basic understanding of credit risk. Specifically, how it is measured

Measuring Credit Risk Qualitative Factors Quantitative Models

Credit Score Models Value-at-Risk (VaR) RAROC Other models (if time permits)

2

Measuring Loan Credit Risk

3

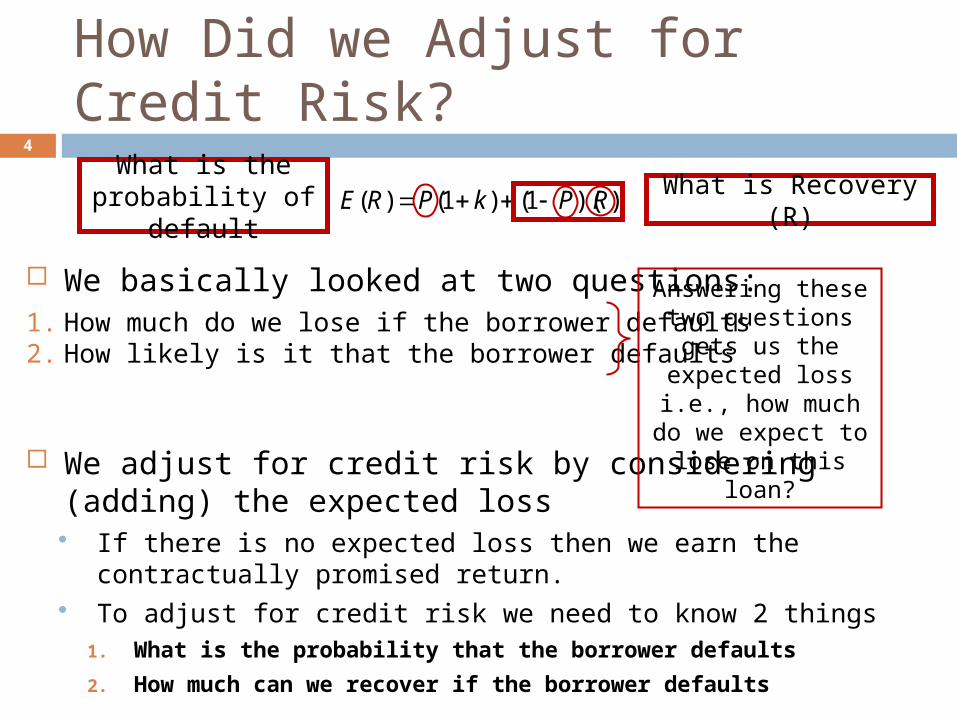

How Did we Adjust for Credit Risk?

We basically looked at two questions:1. How much do we lose if the borrower defaults2. How likely is it that the borrower defaults

We adjust for credit risk by considering (adding) the expected loss If there is no expected loss then we earn the contractually promised return. To adjust for credit risk we need to know 2 things

1. What is the probability that the borrower defaults

2. How much can we recover if the borrower defaults

4

))(1()1()( RPkPRE

Answering these two questions gets us the

expected loss i.e., how much do we expect to

lose on this loan?

What is Recovery (R)What is the

probability of default

Adjusting for Credit Risk

In the credit risk game we need good estimates of:

1.The loan’s probability of default

2.The recovery in default

3.The expected loss Instead of estimating the probability of default and recovery separately

we can take them together and estimate the expected loss directly

5

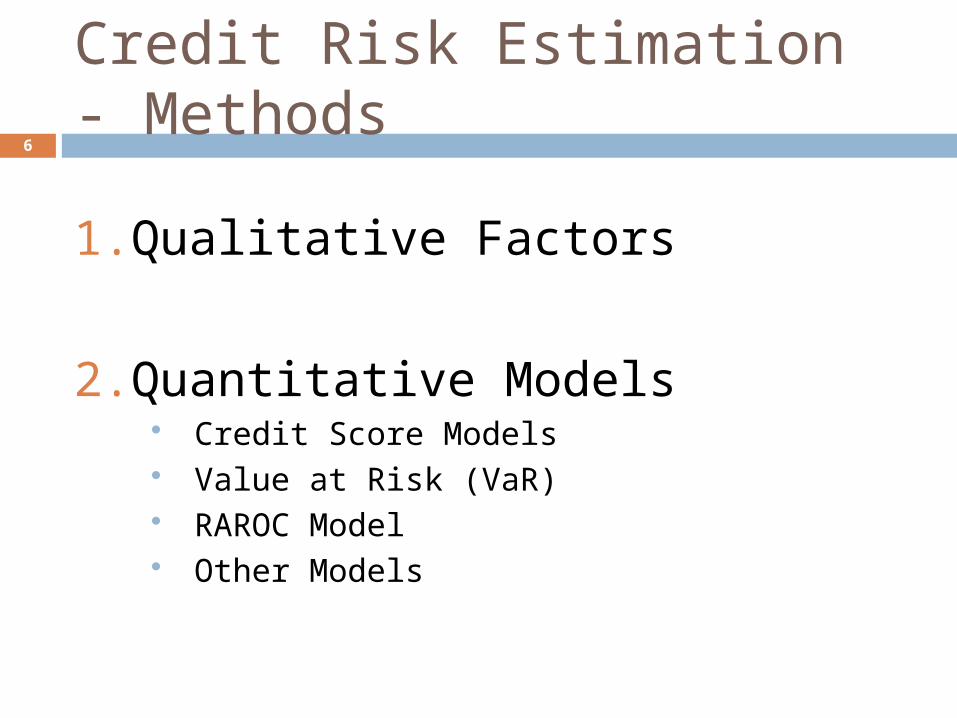

Credit Risk Estimation - Methods

1.Qualitative Factors

2.Quantitative Models Credit Score Models Value at Risk (VaR) RAROC Model Other Models

6

Qualitative Factors

7

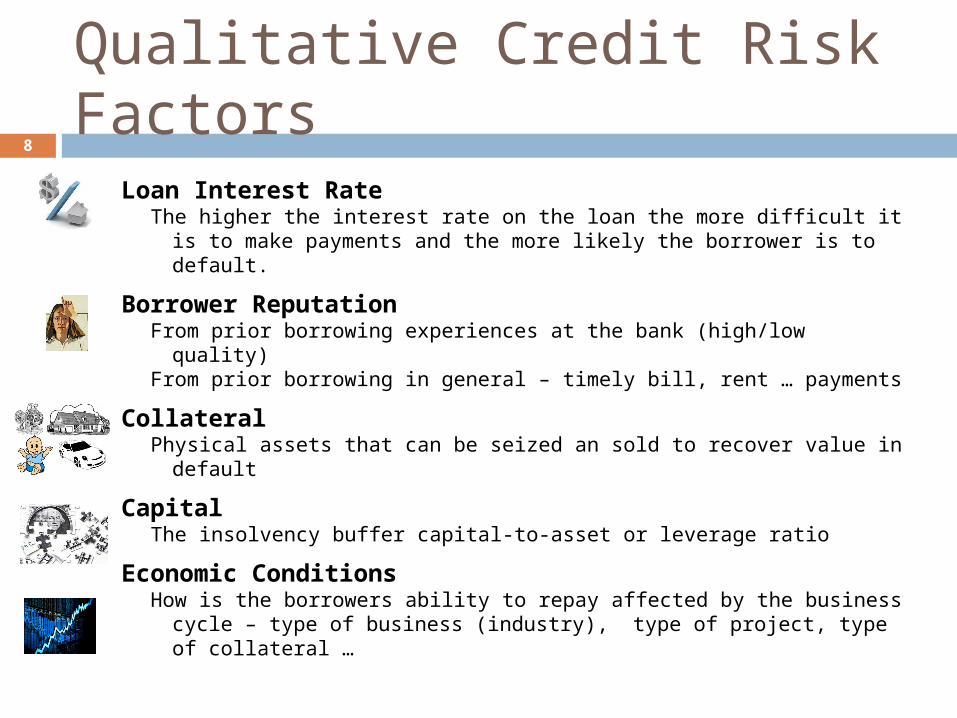

Qualitative Credit Risk Factors

Loan Interest RateThe higher the interest rate on the loan the more difficult it is to make

payments and the more likely the borrower is to default.

Borrower ReputationFrom prior borrowing experiences at the bank (high/low quality)From prior borrowing in general – timely bill, rent … payments

CollateralPhysical assets that can be seized an sold to recover value in default

CapitalThe insolvency buffer capital-to-asset or leverage ratio

Economic ConditionsHow is the borrowers ability to repay affected by the business cycle –

type of business (industry), type of project, type of collateral …

8

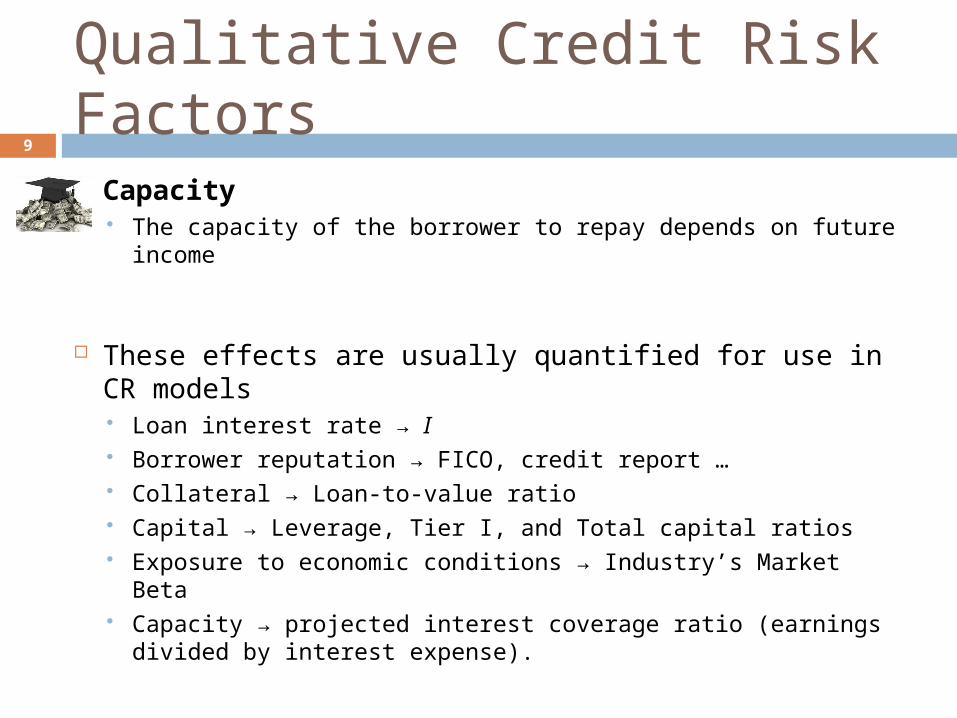

Capacity The capacity of the borrower to repay depends on future income

These effects are usually quantified for use in CR models Loan interest rate → I Borrower reputation → FICO, credit report … Collateral → Loan-to-value ratio Capital → Leverage, Tier I, and Total capital ratios Exposure to economic conditions → Industry’s Market Beta Capacity → projected interest coverage ratio (earnings divided by

interest expense).

9

Qualitative Credit Risk Factors

Quantitative Models of Credit Risk Credit Score Models Value at Risk (VaR) RAROC Model Other Models

10

Credit Score Model Linear Probability Model Logit Analysis Linear Discriminate Model

11

Credit Score Model

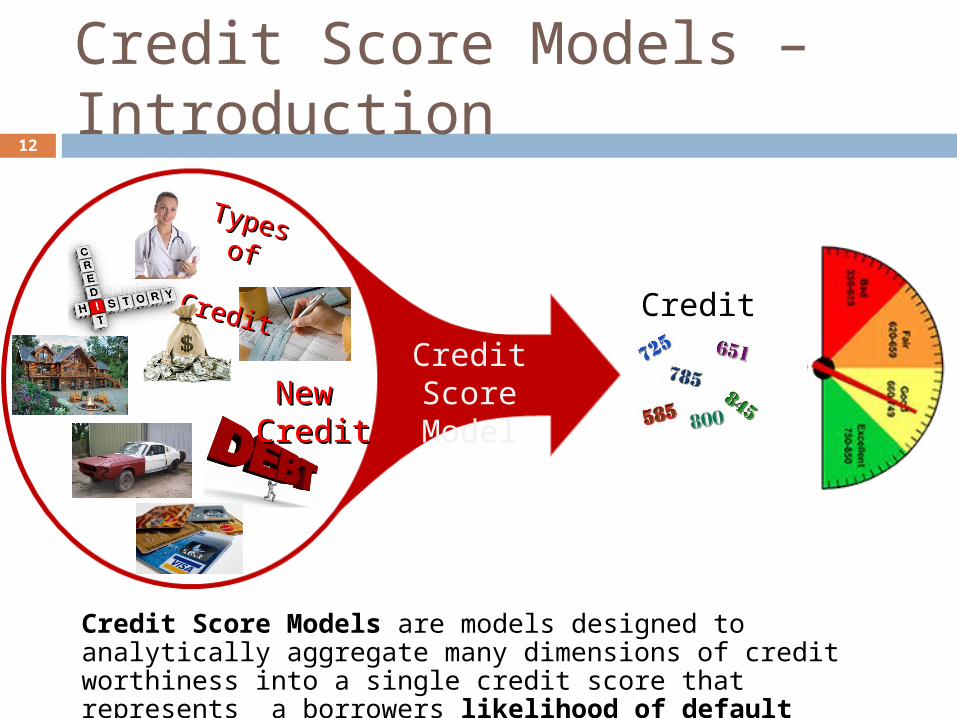

Credit Score Models – Introduction12

Types ofTypes of CreditCredit

Credit Score Models are models designed to analytically aggregate many dimensions of credit worthiness into a single credit score that represents a borrowers likelihood of default

New New CreditCredit

Credit Score

13

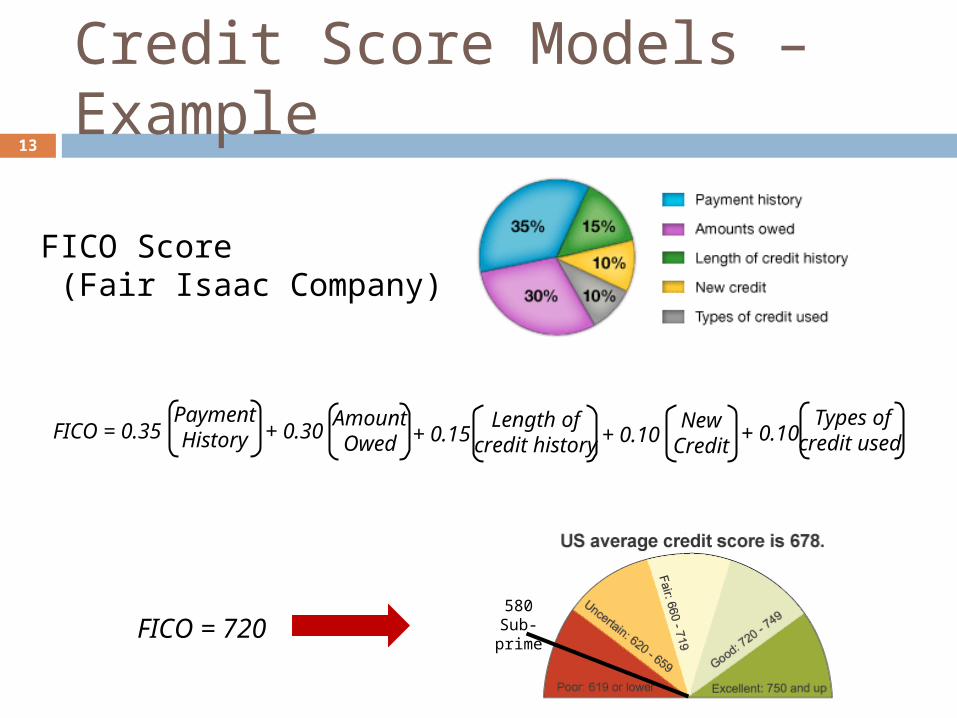

Credit Score Models – Example

FICO Score (Fair Isaac Company)

FICO = 0.35Payment History + 0.30

Amount Owed + 0.15 + 0.10 + 0.10

New Credit

Length of credit history

Types of credit used

FICO = 720580

Sub-prime

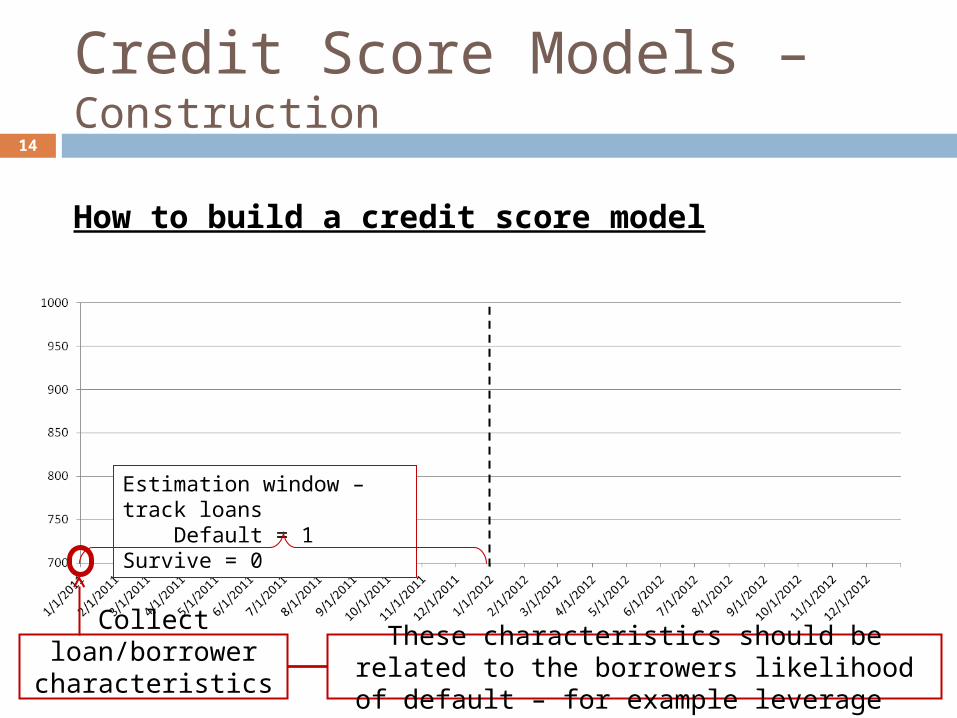

How to build a credit score model

14

Credit Score Models – Construction

Estimation window – track loans Default = 1 Survive = 0

These characteristics should be related to the borrowers likelihood of default – for example leverage

Collect loan/borrower characteristics

What do you want to know about the loan/borrower?

Loan/borrower characteristics:Reputation: Years at the bank, borrowing history, # of loans repaid … Leverage: Leverage ratio, Tier I and Total capital ratios Future income: Earnings volatility (repayment capacity)Collateral: Market value of physical assets backing the loanLoan characteristics: Term, interest rate, type …Business cycle effects: market beta, earnings sensitivity to GDP or other economic indicatorsInterest rates: earnings, profitability, investment … sensitivity to interest rates .

15

Credit Score Models – Construction(Loan\Borrower Characteristics)

16

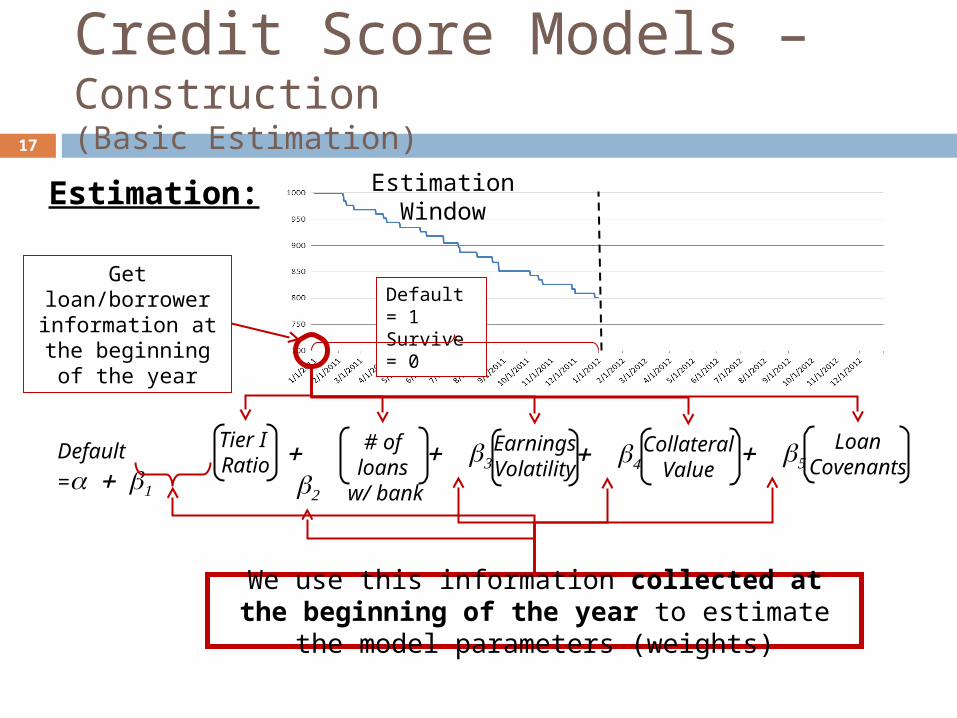

Credit Score Models – Construction(Basic Estimation)

Default = 1Survive = 0

Estimation: Estimation Window

Object is to build a model that we can use to predict default in the next period

17

Credit Score Models – Construction(Basic Estimation)

Default = 1Survive = 0

Estimation: Estimation Window

We use this information collected at the beginning of the year to estimate the model parameters (weights)

Tier I Ratio

# of loans w/ bank

Collateral Value

Earnings Volatility

Loan Covenants

Default

=

Get loan/borrower information at the

beginning of the year

18

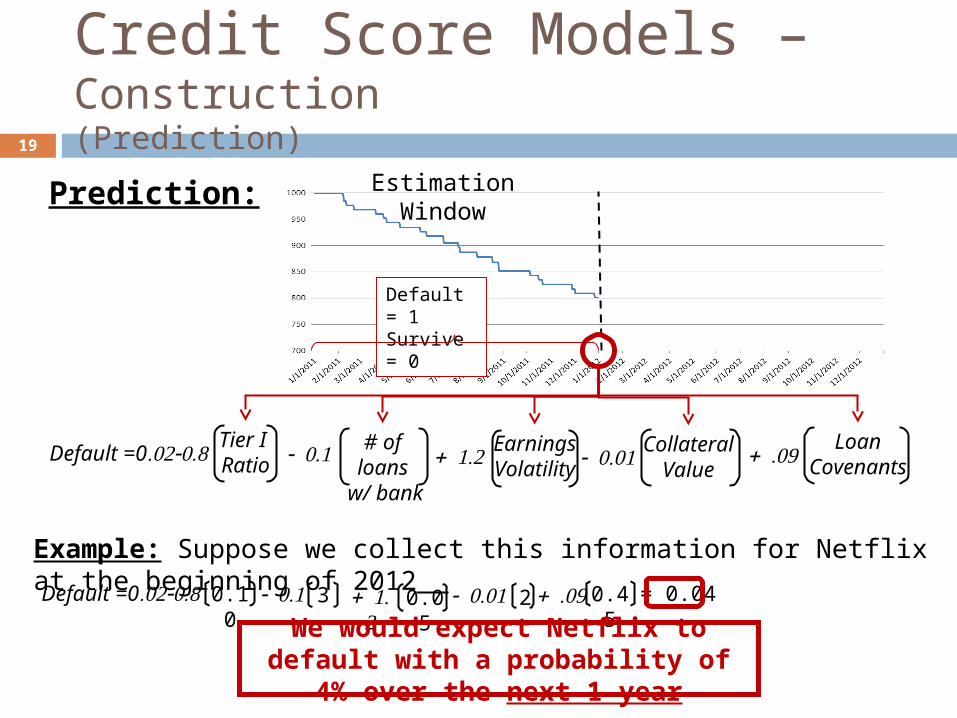

Credit Score Models – Construction (Prediction)

Default = 1Survive = 0

Prediction: Estimation Window

Tier I Ratio

# of loans w/ bank

Collateral Value

Earnings Volatility

Loan Covenants

Default

=

Default =0

After estimating the model, we can fill in the parameters and the model can be used to forecast loan/borrower defaults

19

Credit Score Models – Construction(Prediction)

Default = 1Survive = 0

Prediction: Estimation Window

Tier I Ratio

# of loans w/ bank

Collateral Value

Earnings Volatility

Loan Covenants

Default =0

Default =0

0.10 3 0.05 2 0.45 = 0.04

Example: Suppose we collect this information for Netflix at the beginning of 2012

We would expect Netflix to default with a probability of 4% over the next 1 year

20

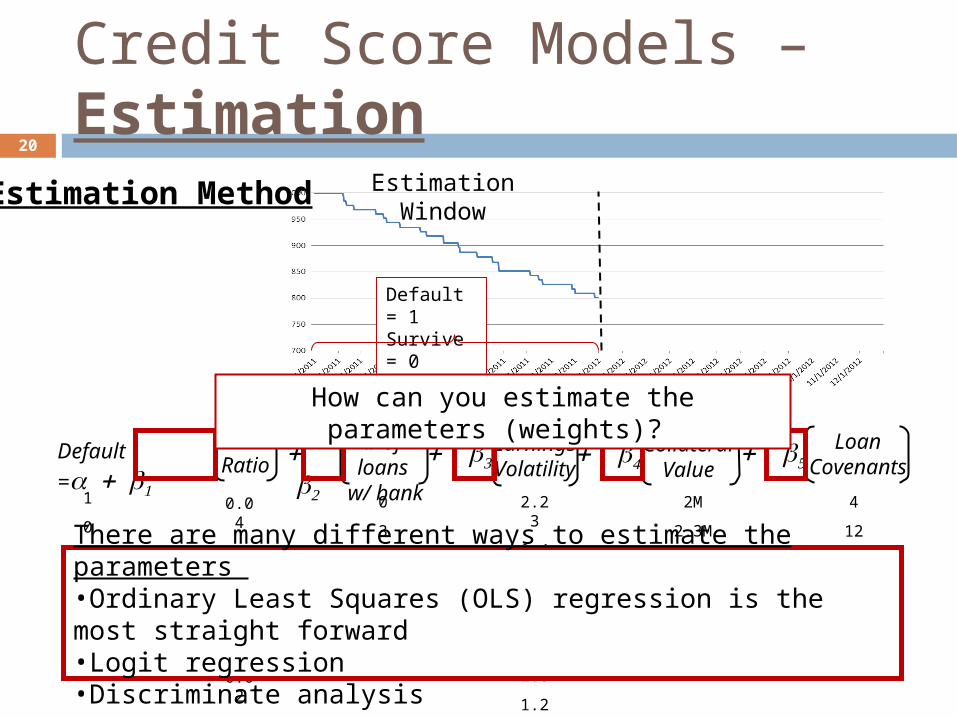

Credit Score Models – Estimation

Default = 1Survive = 0

Estimation Method Estimation Window

Default

=

Tier I Ratio

# of loans w/ bank

Collateral Value

Earnings Volatility

Loan Covenants

1

0

⁞

1

0

0

0.04

0.07

⁞

0.10

0.02

0.05

0

3

⁞

7

2

0

2.23

0.45

⁞

1.23

2.8

1.2

2M

2.3M

⁞

0.32M

0.8M

5.2M

4

12

⁞

8

6

3

How can you estimate the parameters (weights)?

There are many different ways to estimate the parameters •Ordinary Least Squares (OLS) regression is the most straight forward•Logit regression•Discriminate analysis

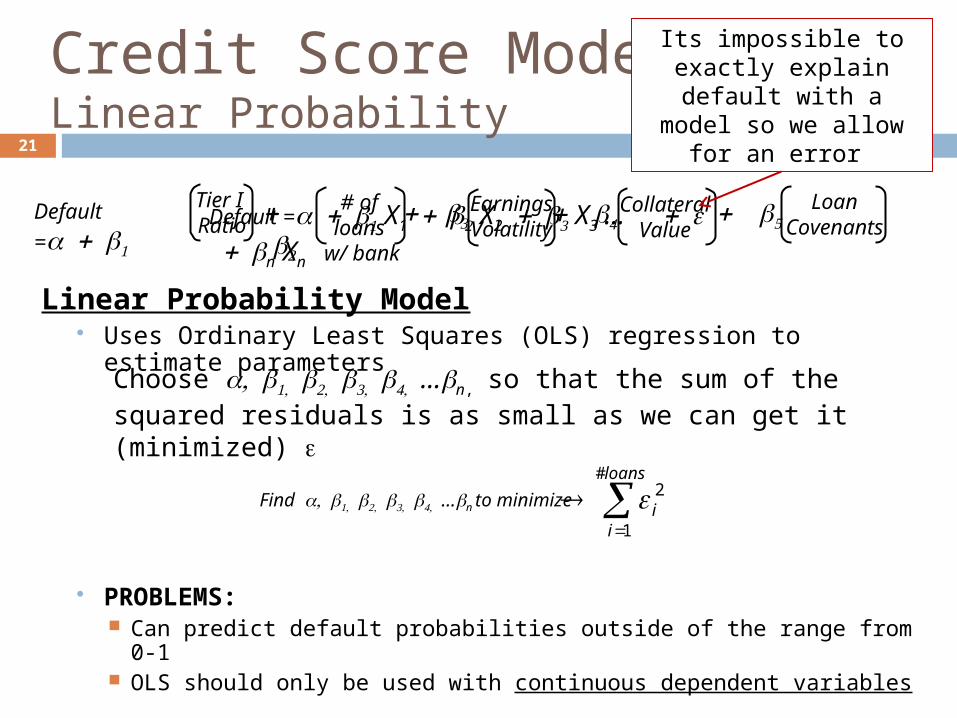

Linear Probability Model Uses Ordinary Least Squares (OLS) regression to estimate parameters

PROBLEMS: Can predict default probabilities outside of the range from 0-1 OLS should only be used with continuous dependent variables

21

Credit Score Models – Linear Probability

Default

=

Tier I Ratio

# of loans w/ bank

Collateral Value

Earnings Volatility

Loan Covenants

Default =X1X2X3 …nXn

Choose …n,so that the sum of the squared residuals is as small as we can get it (minimized)

loans

ii

#

1

2Find…n to minimize

Its impossible to exactly explain default with a model

so we allow for an error

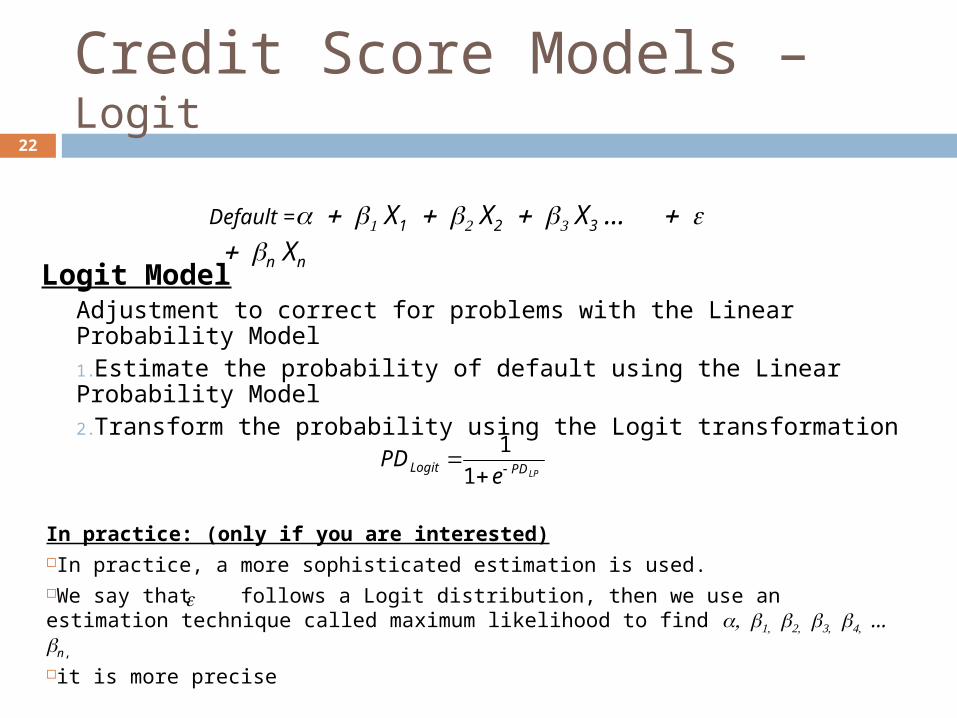

Logit ModelAdjustment to correct for problems with the Linear Probability Model1.Estimate the probability of default using the Linear Probability Model2.Transform the probability using the Logit transformation

22

Credit Score Models – Logit

Default =X1X2X3 …nXn

LPPDLogit ePD

1

1

In practice: (only if you are interested)In practice, a more sophisticated estimation is used.We say that follows a Logit distribution, then we use an estimation technique called maximum likelihood to find …n,it is more precise

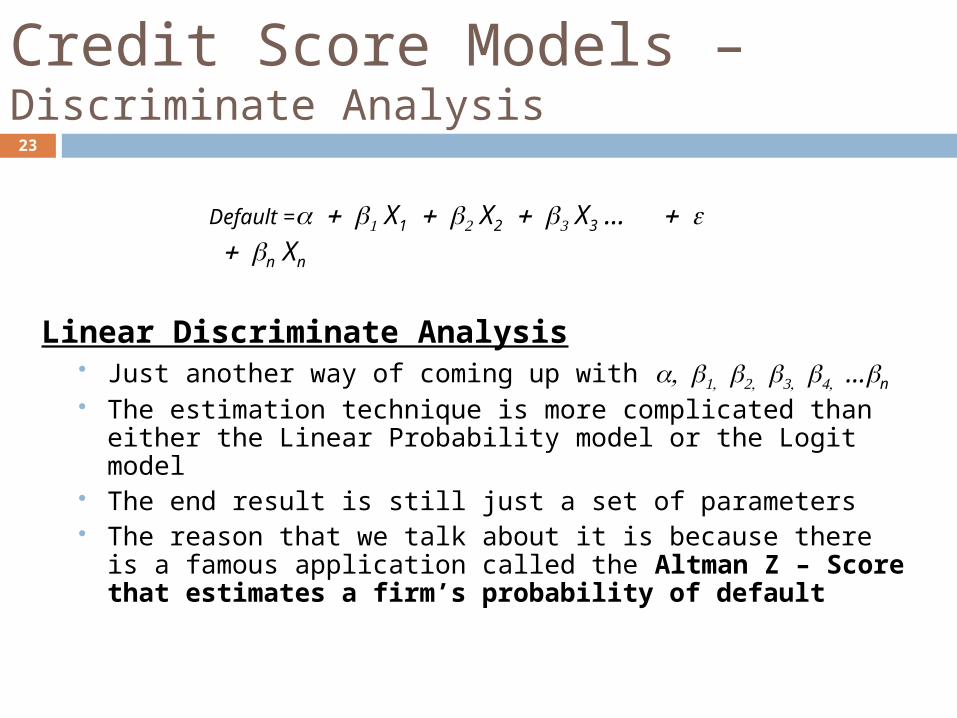

Linear Discriminate Analysis Just another way of coming up with …n The estimation technique is more complicated than either the Linear

Probability model or the Logit model The end result is still just a set of parameters The reason that we talk about it is because there is a famous application

called the Altman Z – Score that estimates a firm’s probability of default

23

Credit Score Models – Discriminate Analysis

Default =X1X2X3 …nXn

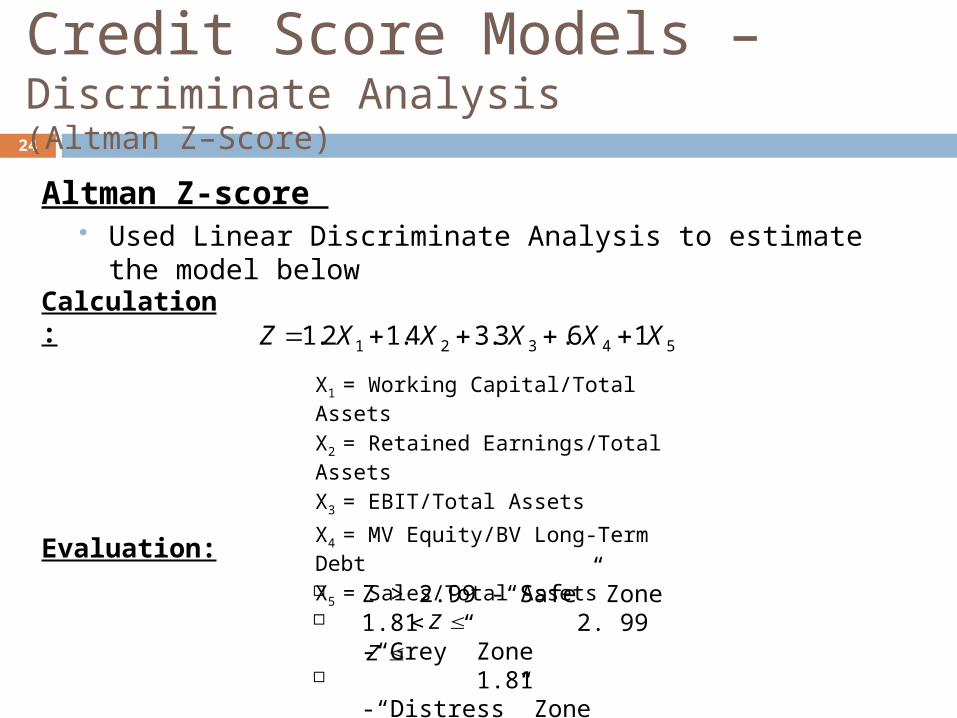

Altman Z-score Used Linear Discriminate Analysis to estimate the model below

24

Credit Score Models – Discriminate Analysis(Altman Z–Score)

54321 16.3.34.12.1 XXXXXZ

X1 = Working Capital/Total Assets

X2 = Retained Earnings/Total Assets

X3 = EBIT/Total Assets

X4 = MV Equity/BV Long-Term Debt

X5 = Sales/Total Assets

Z > 2.99 -“Safe” Zone 1.81 2. 99 -“Grey” Zone 1.81 -“Distress” Zone

Z

Z

Calculation:

Evaluation:

Kaplan Associates has estimated the following linear probability model using loan defaults over the past 4 years.

Suppose that North Star restaurant applies for a loan. They have a leverage ratio of 0.25, a FICO score of 720 and a 10 year credit history.

25

) (032.0)(0085.0)(003.0001.0 historycreditoflengthFICOLeveragePD

a) Calculate the probability that North Star defaults over the next year using the linear probability modelb) Calculate the probability that North Star defaults over the next four years using the linear probability modelc) Calculate the probability that North Star defaults over the next four years using the Logit model

11-26

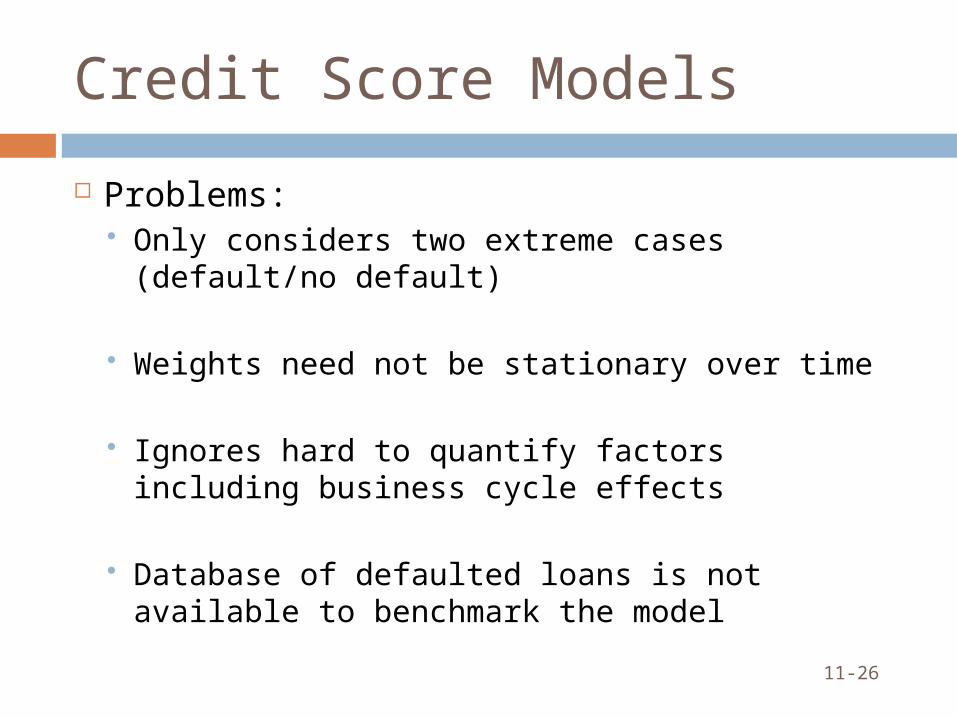

Credit Score Models

Problems: Only considers two extreme cases (default/no default)

Weights need not be stationary over time

Ignores hard to quantify factors including business cycle effects

Database of defaulted loans is not available to benchmark the model

Value at Risk (VaR)

27

Thinking About Credit Risk

What have we done so far: Followed a group of firms – some defaulted and some did not. Used the actual defaults vs. non-default to try to understand, in

general, what causes a firm to default on its loans. Problem - we have to wait for firms to default to understand what

causes default

Another way of thinking: If no firms defaulted would that mean that there is no credit risk? The value of a loan can change simply because the probability of

default or what we expect to recover in default changes. This is credit risk! It exists even if no firms default Value-at-Risk is one method used to measure this

28

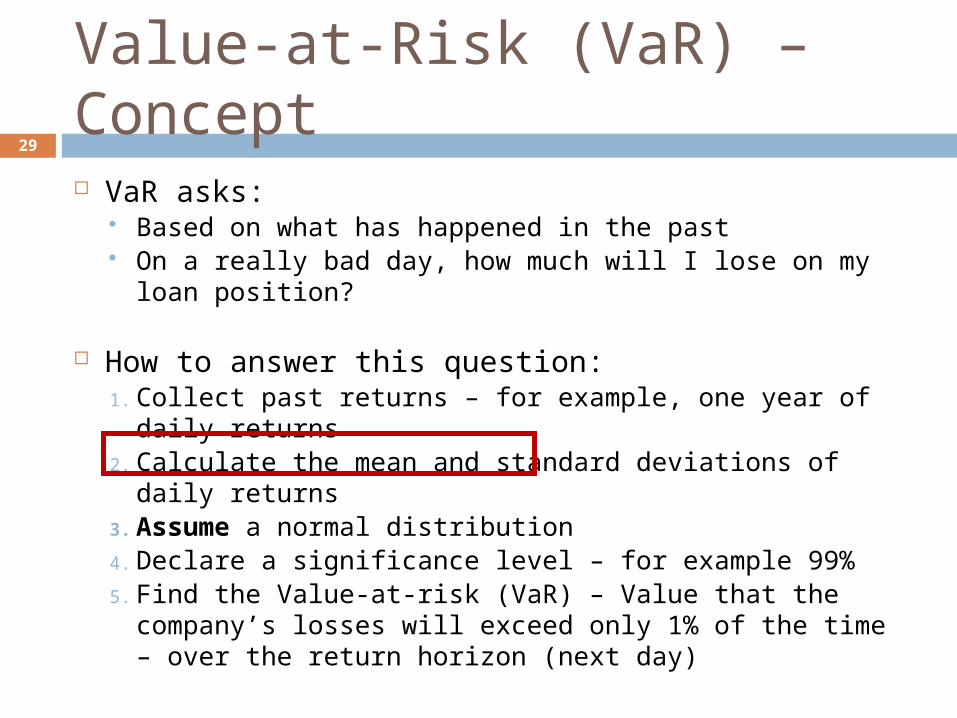

VaR asks: Based on what has happened in the past On a really bad day, how much will I lose on my loan position?

How to answer this question:1. Collect past returns – for example, one year of daily returns2. Calculate the mean and standard deviations of daily returns3. Assume a normal distribution4. Declare a significance level – for example 99%5. Find the Value-at-risk (VaR) – Value that the company’s losses will

exceed only 1% of the time – over the return horizon (next day)

29

Value-at-Risk (VaR) – Concept

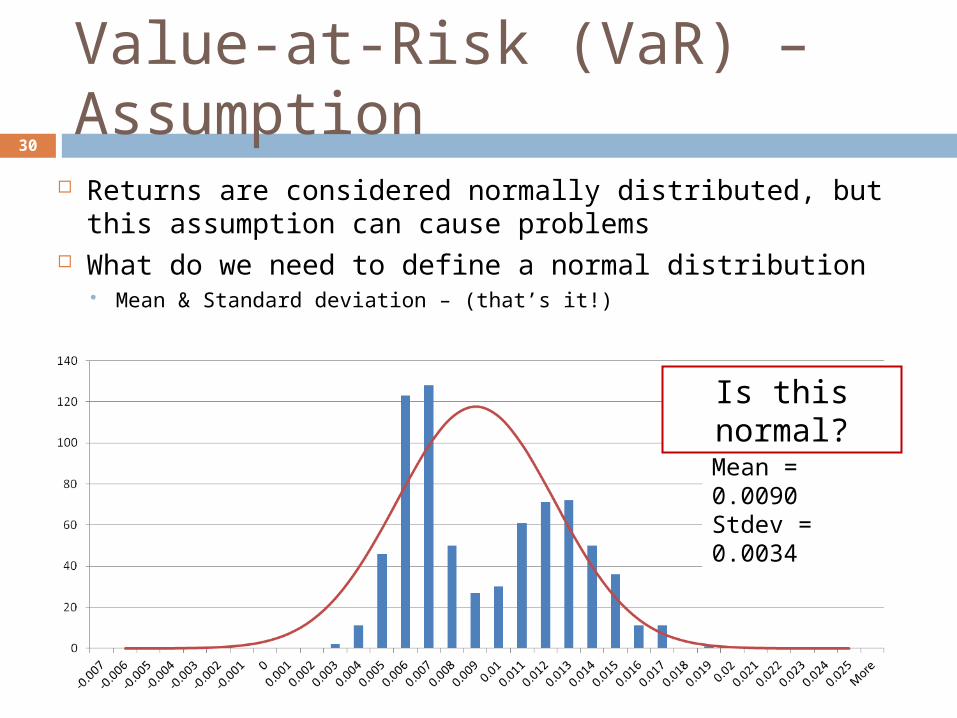

Returns are considered normally distributed, but this assumption can cause problems

What do we need to define a normal distribution Mean & Standard deviation – (that’s it!)

30

Value-at-Risk (VaR) – Assumption

Mean = 0.0090Stdev = 0.0034

Is this normal?

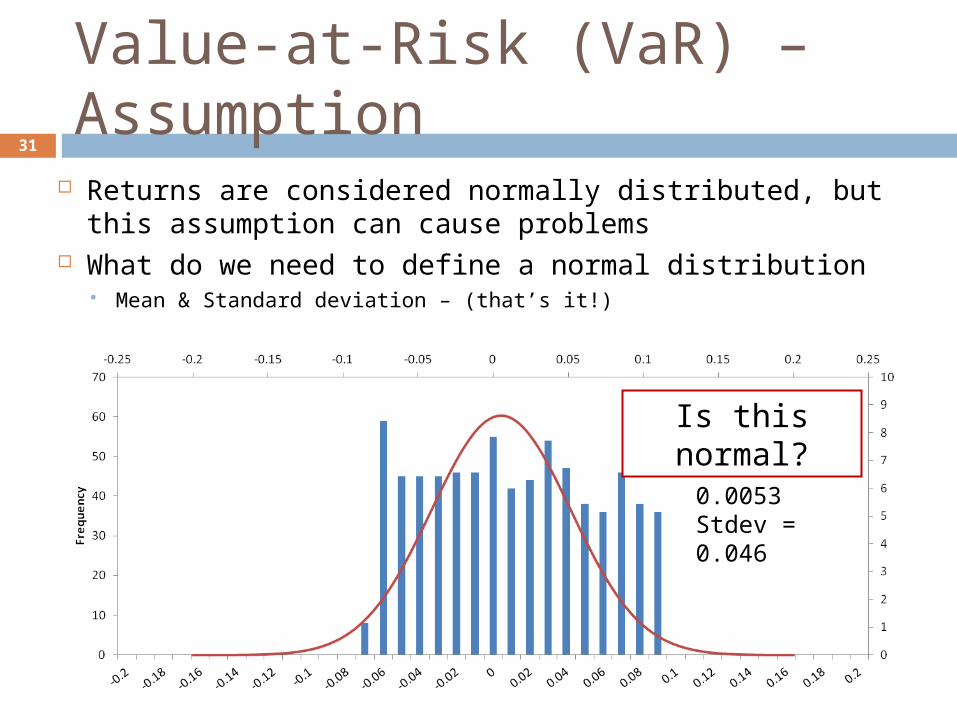

Returns are considered normally distributed, but this assumption can cause problems

What do we need to define a normal distribution Mean & Standard deviation – (that’s it!)

31

Value-at-Risk (VaR) – Assumption

Mean = 0.0053Stdev = 0.046

Is this normal?

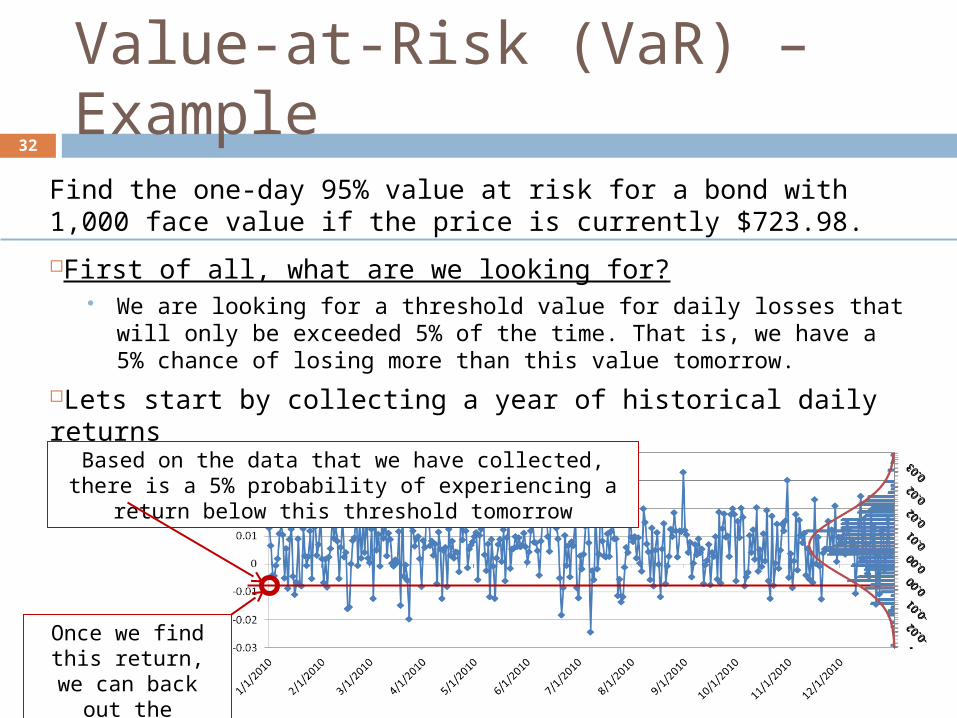

Find the one-day 95% value at risk for a bond with 1,000 face value if the price is currently $723.98.

First of all, what are we looking for? We are looking for a threshold value for daily losses that will only be exceeded 5% of

the time. That is, we have a 5% chance of losing more than this value tomorrow.

Lets start by collecting a year of historical daily returns We work with returns because they are usually normally distributed – prices are not!

32

Value-at-Risk (VaR) – Example

Based on the data that we have collected, there is a 5% probability of experiencing a return below this threshold tomorrow

Once we find this return, we can back out the VaR(95%)

Find the one-day 95% value at risk for a bond with 1,000 face value if the price is currently $723.98.

Step #1: Calculate the mean and standard deviation

Step #2: Find the 95% VaR

33

Value-at-Risk (VaR) – Example

Mean = 0.005473Stdev = 0.009128

Mean = 0.005473Stdev = 0.009128

We want to find the return that gives us 5% of the area under the curve in the tail

5%How do you do it?

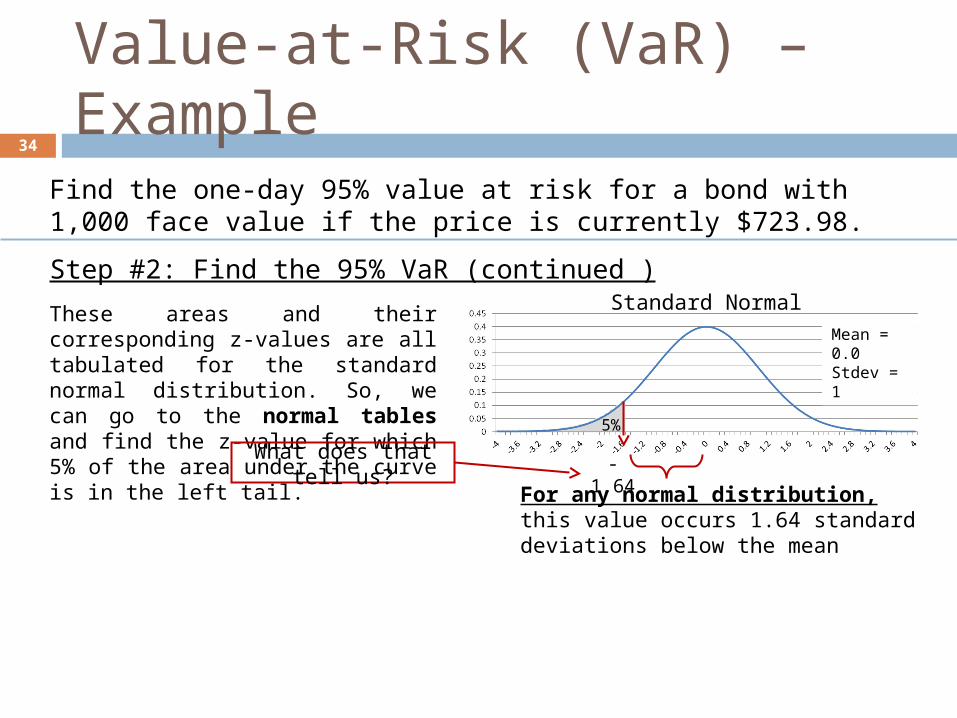

Find the one-day 95% value at risk for a bond with 1,000 face value if the price is currently $723.98.

Step #2: Find the 95% VaR (continued )Standard Normal

5%

Mean = 0.0Stdev = 1

34

Value-at-Risk (VaR) – Example

These areas and their corresponding z-values are all tabulated for the standard normal distribution. So, we can go to the normal tables and find the z-value for which 5% of the area under the curve is in the left tail.

-1.64What does that tell us?

For any normal distribution, this value occurs 1.64 standard deviations below the mean

Find the one-day 95% value at risk for a bond with 1,000 face value if the price is currently $723.98.

Step #2: Find the 95% VaR (continued )Standard Normal

5%

Mean = 0.0Stdev = 1

35

Value-at-Risk (VaR) – Example

These areas and their corresponding z-values are all tabulated for the standard normal distribution. So, we can go to the normal tables and find the z-value for which 5% of the area under the curve is in the left tail.

-1.64

Mean = 0.005473Stdev = 0.009128

5%

Our Distribution

X

We know that “X” is 1.64 standard deviations below the mean

X = 0.005473

Start at the mean subtract 1.64 Standard deviations in this case 0.009128

– 1.64(0.009128) = -0.0095

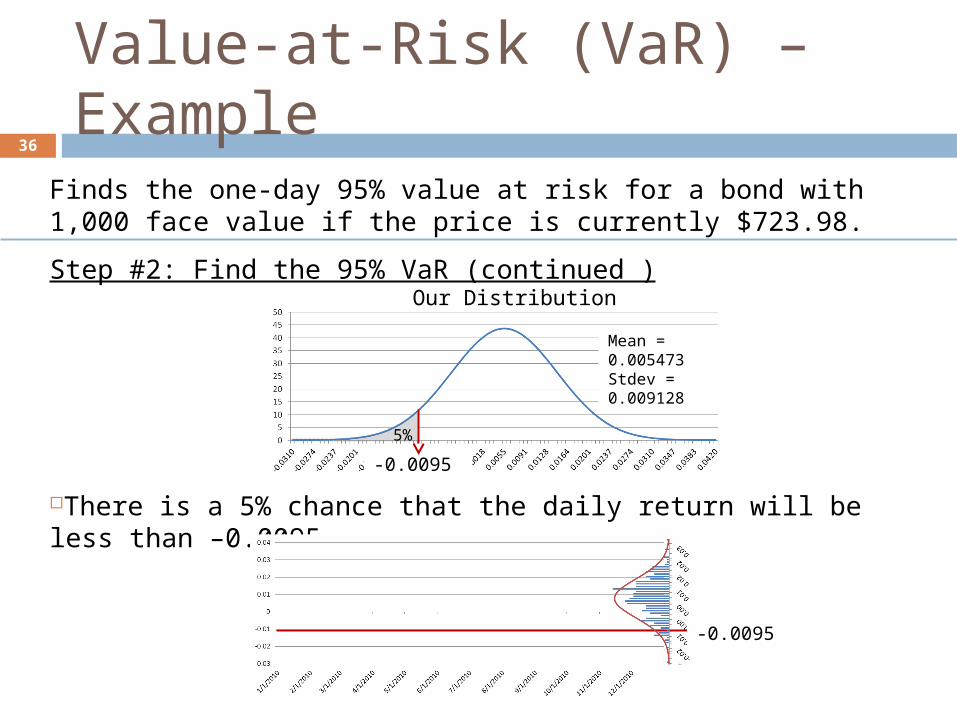

Finds the one-day 95% value at risk for a bond with 1,000 face value if the price is currently $723.98.

Step #2: Find the 95% VaR (continued )

There is a 5% chance that the daily return will be less than –0.0095

36

Value-at-Risk (VaR) – Example

Mean = 0.005473Stdev = 0.009128

5%

Our Distribution

X-0.0095

-0.0095

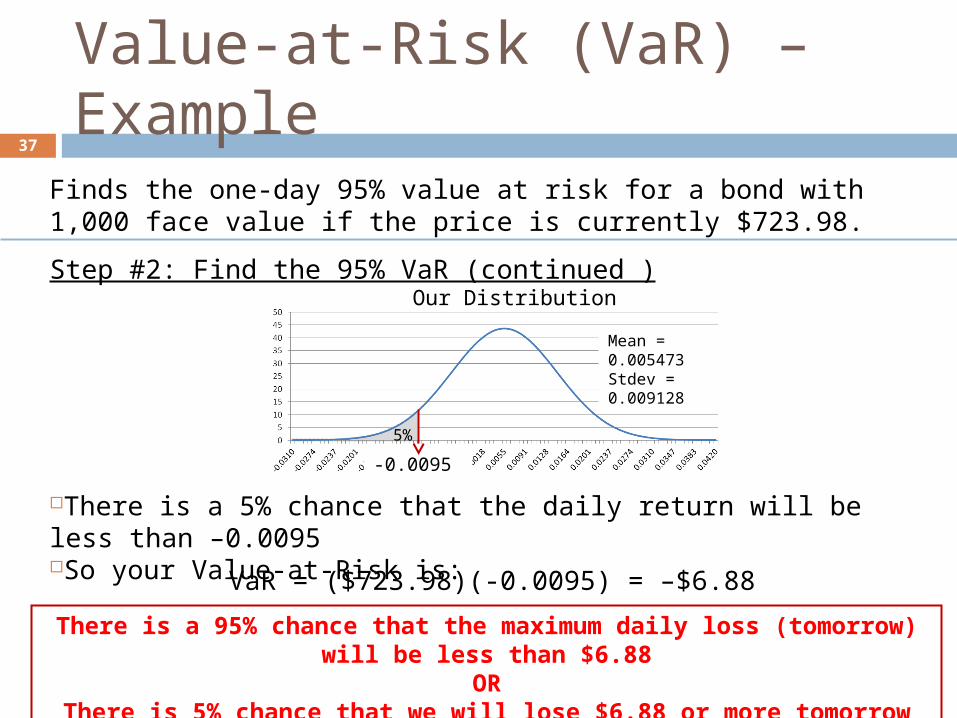

Finds the one-day 95% value at risk for a bond with 1,000 face value if the price is currently $723.98.

Step #2: Find the 95% VaR (continued )

There is a 5% chance that the daily return will be less than –0.0095 So your Value-at-Risk is:

37

Value-at-Risk (VaR) – Example

Mean = 0.005473Stdev = 0.009128

5%

Our Distribution

X-0.0095

VaR = ($723.98)(-0.0095) = –$6.88

There is a 95% chance that the maximum daily loss (tomorrow) will be less than $6.88OR

There is 5% chance that we will lose $6.88 or more tomorrow

Lorden Investments has a loan portfolio with a current value of $172M . The mean an variance of the value weighted daily return on their portfolio is 0.0181 and 0.0004 respectively. Find the 99% value at risk for the loan portfolio

38

2.33

RAROC Model

39

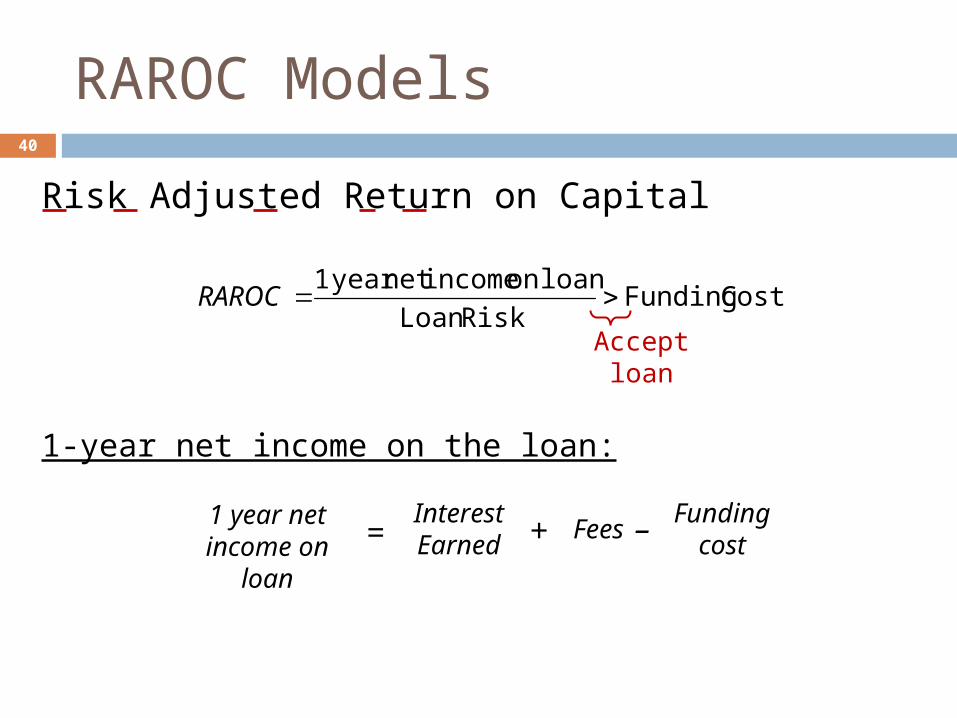

RAROC Models

Risk Adjusted Return on Capital

1-year net income on the loan:

40

1 year net income on loan

Interest Earned

FeesFunding

cost= – +

Costs FundingRiskLoan

loan on incomenet year 1RAROC

Accept loan

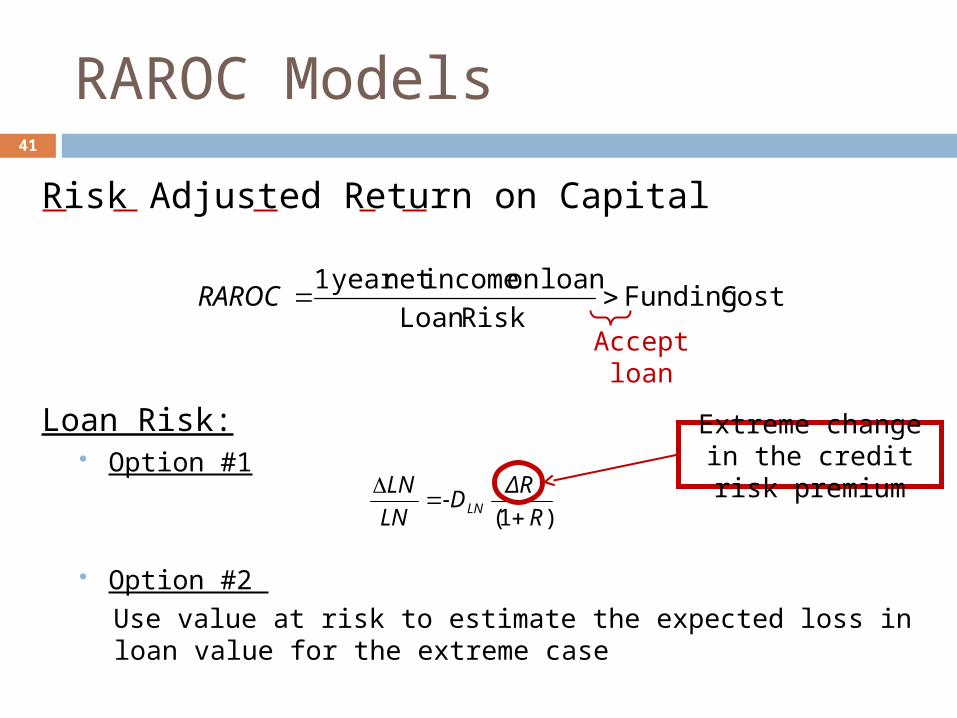

RAROC Models

Risk Adjusted Return on Capital

Loan Risk: Option #1

Option #2

Use value at risk to estimate the expected loss in loan value for the extreme case

41

)1( R

ΔR -D

LN

LNLN

Extreme change in the credit risk premium

Costs FundingRiskLoan

loan on incomenet year 1RAROC

Accept loan

42

The Lucre Island Community Bank (LICB) is planning to make a loan of $5,000,000 to the Dunder-Mifflin Paper Company. It will charge a servicing fee of 50 bps, the loan will have a maturity of 8 years, and a duration of 7.5 years. The cost of funds (RAROC benchmark) for the bank is 10%. Assume that LICB has estimated the maximum change in the risk premium on the paper processing sector to be approximately 4.2%, The current market interest rate for loans in this sector is 12

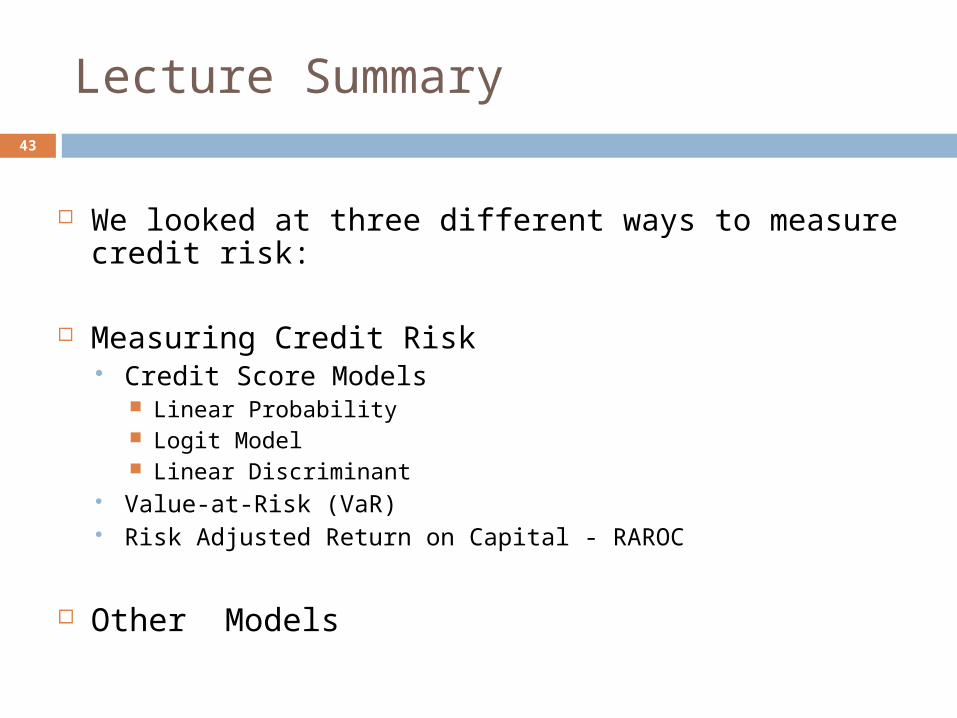

Lecture Summary43

We looked at three different ways to measure credit risk:

Measuring Credit Risk Credit Score Models

Linear Probability Logit Model Linear Discriminant

Value-at-Risk (VaR) Risk Adjusted Return on Capital - RAROC

Other Models

AppendixOther Models

44

11-45

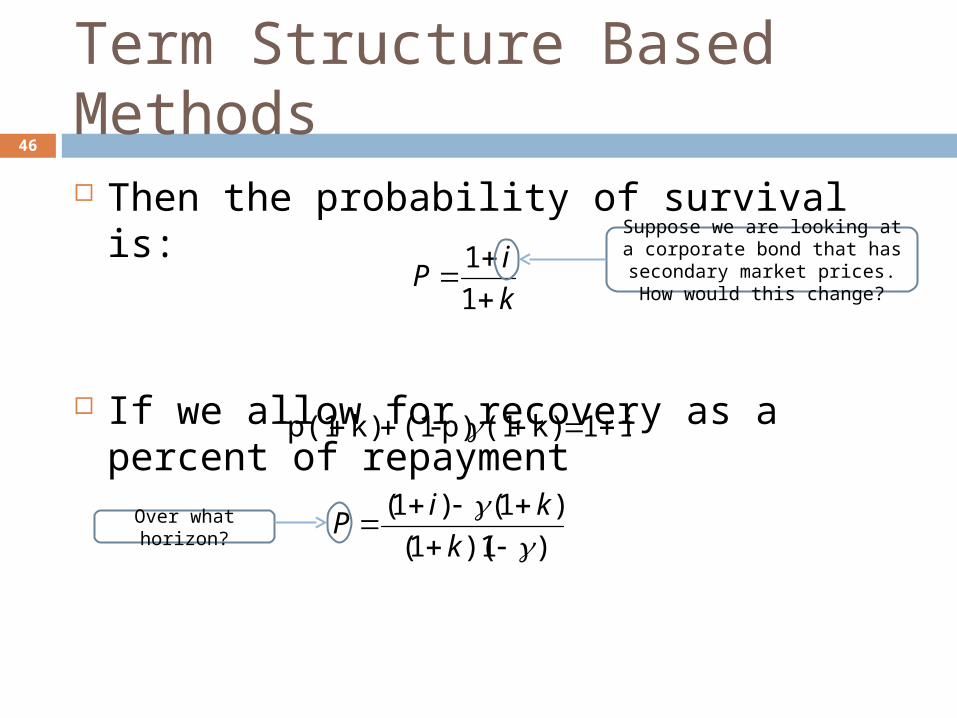

Term Structure Based Methods

We can use the credit spread in the market to determine the level of risk probability of default using zero coupons and strips

Suppose the contractual promised return on a corporate bond is k –the expected return is then

p (1+ k)+(1-p)(0)

Assuming zero recovery

Suppose the FI require a return equal to the risk free rate i

p (1+ k)+(1-p)(0)= 1+i

Term Structure Based Methods

Then the probability of survival is:

If we allow for recovery as a percent of repayment

46

k

iP

1

1

i1 k)(1p)-(1k)p(1

)1)(1(

)1()1(

k

kiP

Suppose we are looking at a corporate bond that has

secondary market prices. How would this change?

Over what horizon?

11-47

Term Structure Based Methods

May be generalized to loans with any maturity or to adjust for varying default recovery rates

The loan can be assessed using the inferred probabilities from comparable quality bonds

11-48

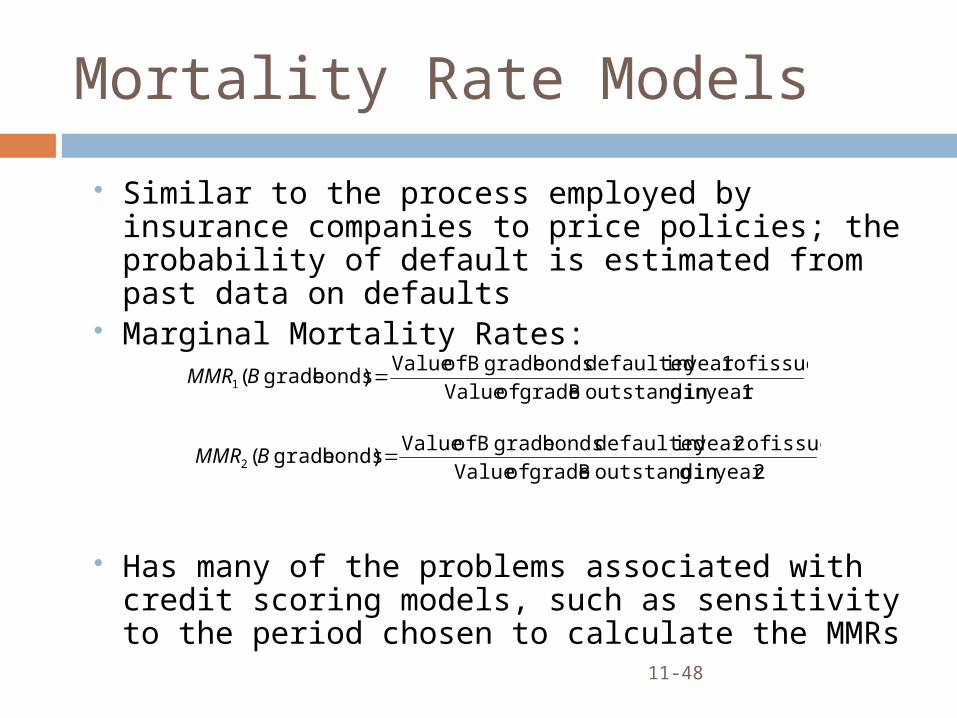

Mortality Rate Models

Similar to the process employed by insurance companies to price policies; the probability of default is estimated from past data on defaults

Marginal Mortality Rates:

Has many of the problems associated with credit scoring models, such as sensitivity to the period chosen to calculate the MMRs

1year in goutstandin B grade of Value

issue of 1year in defaulted bonds grade B of Value)bonds grade (1 BMMR

2year in goutstandin B grade of Value

issue of 2year in defaulted bonds grade B of Value)bonds grade (2 BMMR

11-49

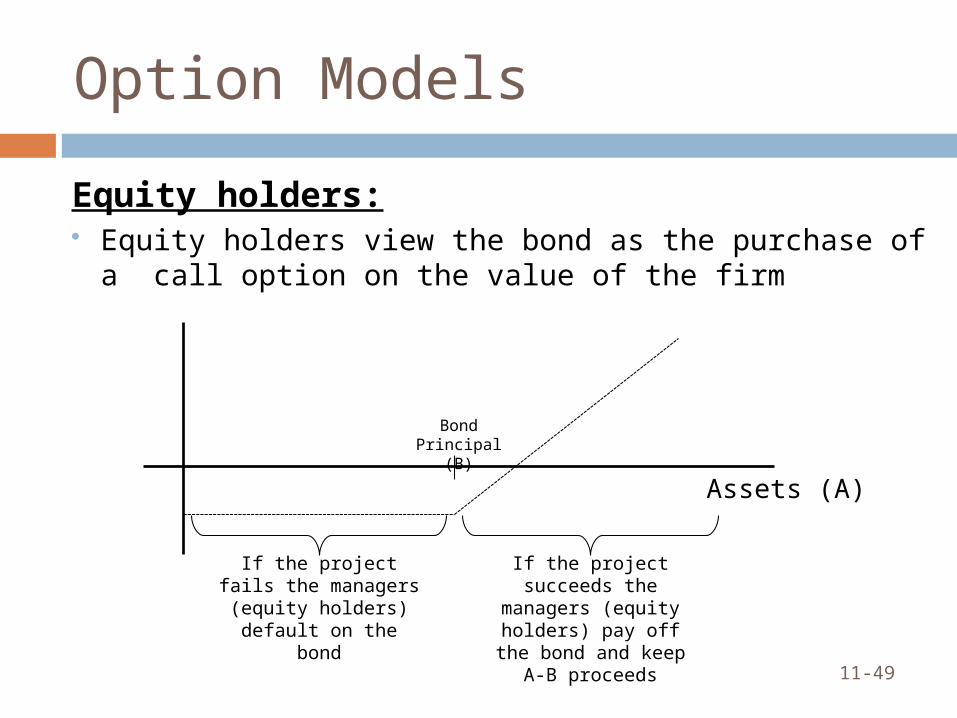

Option Models

Equity holders: Equity holders view the bond as the purchase of a call option on the

value of the firm

Bond Principal (B)

If the project fails the managers (equity holders)

default on the bond

If the project succeeds the managers (equity holders) pay off the bond and keep

A-B proceeds

Assets (A)

11-50

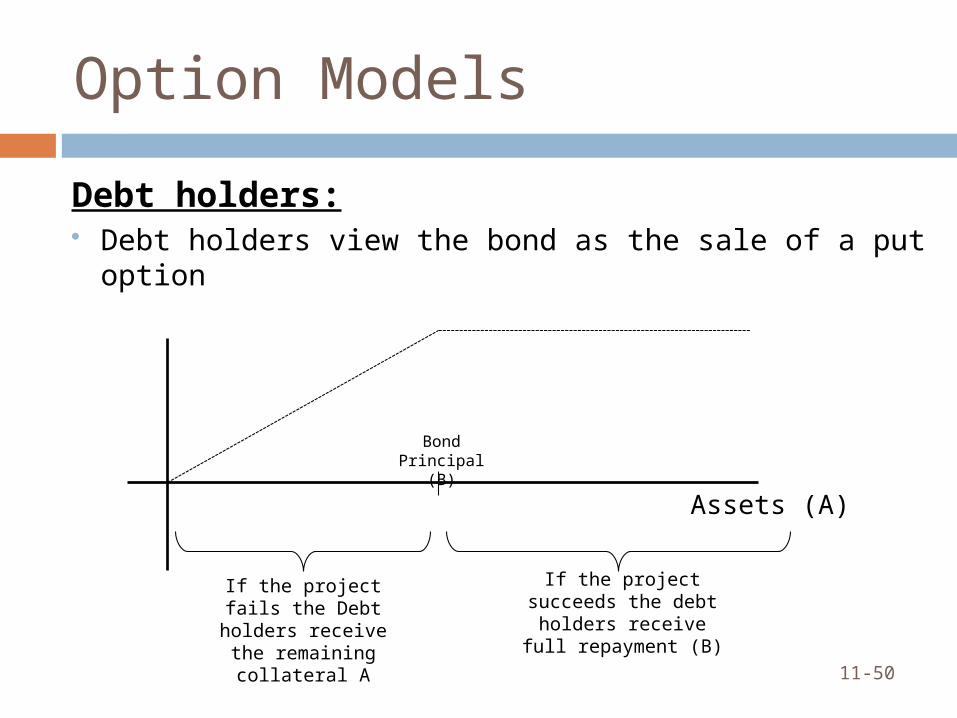

Option Models

Debt holders: Debt holders view the bond as the sale of a put option

Bond Principal (B)

If the project fails the Debt holders receive the

remaining collateral A

If the project succeeds the debt holders receive full

repayment (B)

Assets (A)

11-51

Applying Option Valuation Model

Merton showed value of a risky loan:

where

F() = value of risky debt

ln = Natural logarithm

i = Risk-free rate on debt of equivalent maturity

remaining time to maturity

B = principal amount on the bond

)()()( 21 hNhNBeBeF ii

)/ln(2

1

ABeh

i

)/ln(2

2

ABeh

i