IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Designing and pricing guarantee options in definedcontribution pension plans

Andrea Consiglio† Michele Tumminello† Stavros Zenios‡

†University of Palermo, IT‡University of Cyprus, CY

June 20166th International Conference

of the Financial Engineering and Banking Society

1 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Outline

1 Introduction

2 The Mathematics of Guarantee Options

3 The Optimization Model

4 Implementation and ResultsThe effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

5 Conclusions

2 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions

Retirement plans are of two types:

DB -Defined benefits plans shift the risks to the provider, be ita corporate employer or future taxpayersDC -Defined contributions plans pass the risks to retirees.

The retirement income must be “safe”:

DC politically acceptableEncourage participationIncrease savings

Some type of guarantee is needed and the success ofDC hinges upon the design of appropriate guarantees.

3 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions

Retirement plans are of two types:

DB -Defined benefits plans shift the risks to the provider, be ita corporate employer or future taxpayersDC -Defined contributions plans pass the risks to retirees.

The retirement income must be “safe”:

DC politically acceptableEncourage participationIncrease savings

Some type of guarantee is needed and the success ofDC hinges upon the design of appropriate guarantees.

3 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions

Retirement plans are of two types:

DB -Defined benefits plans shift the risks to the provider, be ita corporate employer or future taxpayersDC -Defined contributions plans pass the risks to retirees.

The retirement income must be “safe”:

DC politically acceptableEncourage participationIncrease savings

Some type of guarantee is needed and the success ofDC hinges upon the design of appropriate guarantees.

3 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions / 2

Difficulty in designing the guarantee does not stop to thedefinition of its mechanism.

Guarantees provisions are written on asset portfolio, and thesedecisions need to be “optimised for their safety andperformance”. (European Commission 2012)

Given the complex interactions of financial, economic anddemographic risks, a guarantee may fail as much as a “definedbenefit” may be modified by government legislation.(World Bank 2000).

4 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions / 2

Difficulty in designing the guarantee does not stop to thedefinition of its mechanism.

Guarantees provisions are written on asset portfolio, and thesedecisions need to be “optimised for their safety andperformance”. (European Commission 2012)

Given the complex interactions of financial, economic anddemographic risks, a guarantee may fail as much as a “definedbenefit” may be modified by government legislation.(World Bank 2000).

4 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions / 3

Our contributions:1 Modelling DC plans with alternative guarantee options

2 Optimizing asset allocation to facilitate risk sharing

5 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Motivations and contributions / 3

Our contributions:1 Modelling DC plans with alternative guarantee options2 Optimizing asset allocation to facilitate risk sharing

5 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

DB vs DC pension plans in the OECD countries

0

20

40

60

80

100

Chile

Czech

Rep

ublic

Estonia

Franc

e

Greec

e

Hunga

ry

Poland

Slovak

Rep

ublic

Sloven

ia

Denm

ark

Italy

Austra

lia (1

)

Mex

ico

New Z

ealan

d (1

)

Icelan

dSpa

in

United

Sta

tes (

2)

Turk

eyIsr

ael

Korea

Luxe

mbo

urg

(3)

Portu

gal

Canad

a (2

)

Germ

any

Finlan

d

Norway

Switzer

land

Defined Contribution Defined Benefit / Hybrid Mixed

6 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

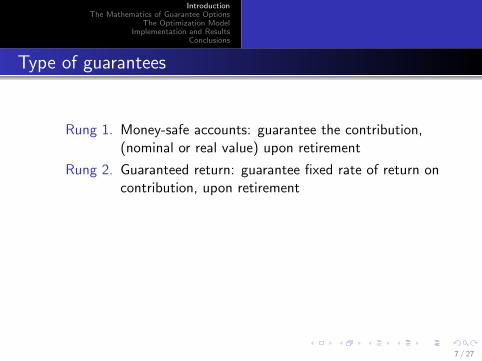

Type of guarantees

Rung 1. Money-safe accounts: guarantee the contribution,(nominal or real value) upon retirement

Rung 2. Guaranteed return: guarantee fixed rate of return oncontribution, upon retirement

Rung 3. Guaranteed return: equal to some industry averageupon retirement

Rung 4. Guaranteed return: for each time period untilretirement

Rung 5. Guaranteed income past retirement

7 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Type of guarantees

Rung 1. Money-safe accounts: guarantee the contribution,(nominal or real value) upon retirement

Rung 2. Guaranteed return: guarantee fixed rate of return oncontribution, upon retirement

Rung 3. Guaranteed return: equal to some industry averageupon retirement

Rung 4. Guaranteed return: for each time period untilretirement

Rung 5. Guaranteed income past retirement

7 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Type of guarantees

Rung 1. Money-safe accounts: guarantee the contribution,(nominal or real value) upon retirement

Rung 2. Guaranteed return: guarantee fixed rate of return oncontribution, upon retirement

Rung 3. Guaranteed return: equal to some industry averageupon retirement

Rung 4. Guaranteed return: for each time period untilretirement

Rung 5. Guaranteed income past retirement

7 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Type of guarantees

Rung 1. Money-safe accounts: guarantee the contribution,(nominal or real value) upon retirement

Rung 2. Guaranteed return: guarantee fixed rate of return oncontribution, upon retirement

Rung 3. Guaranteed return: equal to some industry averageupon retirement

Rung 4. Guaranteed return: for each time period untilretirement

Rung 5. Guaranteed income past retirement

7 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Type of guarantees

Rung 1. Money-safe accounts: guarantee the contribution,(nominal or real value) upon retirement

Rung 2. Guaranteed return: guarantee fixed rate of return oncontribution, upon retirement

Rung 3. Guaranteed return: equal to some industry averageupon retirement

Rung 4. Guaranteed return: for each time period untilretirement

Rung 5. Guaranteed income past retirement

7 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

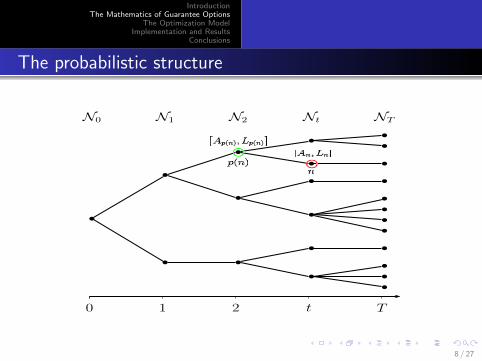

The probabilistic structure

Tt210

NTNtN2N1N0

8 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The basic minimum guarantee option

Model the minimum guarantee provision as an option writtenon a reference fund, with value An at time T for each n ∈ NT ;

We assume a closed fund with initial contribution L0 andregulatory equity requirement E0 = (1− α)A0, α < 1

L0 = αA0 and A0 = L0 + E0

A0 is invested in a reference portfolio with proportions xj , and∑j∈J xj = 1.

9 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The basic minimum guarantee option

Model the minimum guarantee provision as an option writtenon a reference fund, with value An at time T for each n ∈ NT ;

We assume a closed fund with initial contribution L0 andregulatory equity requirement E0 = (1− α)A0, α < 1

L0 = αA0 and A0 = L0 + E0

A0 is invested in a reference portfolio with proportions xj , and∑j∈J xj = 1.

9 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The basic minimum guarantee option

Model the minimum guarantee provision as an option writtenon a reference fund, with value An at time T for each n ∈ NT ;

We assume a closed fund with initial contribution L0 andregulatory equity requirement E0 = (1− α)A0, α < 1

L0 = αA0 and A0 = L0 + E0

A0 is invested in a reference portfolio with proportions xj , and∑j∈J xj = 1.

9 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The dynamics of the asset and liability account

Given a family of stochastic processes {Rt}t∈T defined as aJ-dimensional vector of returns, Rn ≡

(R1n , . . . ,R

Jn

)

The asset account for each n ∈ N\{0} is

An = Ap(n)eRAn

whereRAn =

∑j∈J

xjRjn

The liability account is Ln = Lp(n) exp[g + max

(δRA

n − g , 0)]

10 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The dynamics of the asset and liability account

Given a family of stochastic processes {Rt}t∈T defined as aJ-dimensional vector of returns, Rn ≡

(R1n , . . . ,R

Jn

)The asset account for each n ∈ N\{0} is

An = Ap(n)eRAn

whereRAn =

∑j∈J

xjRjn

The liability account is Ln = Lp(n) exp[g + max

(δRA

n − g , 0)]

10 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The dynamics of the asset and liability account

Given a family of stochastic processes {Rt}t∈T defined as aJ-dimensional vector of returns, Rn ≡

(R1n , . . . ,R

Jn

)The asset account for each n ∈ N\{0} is

An = Ap(n)eRAn

whereRAn =

∑j∈J

xjRjn

The liability account is Ln = Lp(n) exp[g + max

(δRA

n − g , 0)]

10 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The objective function

We assume that shareholders cover shortfalls

A rational strategy for the fund manager is to minimize theexpected value of shortfalls:

Γ = e−rT∑n∈NT

qn max (Ln − An, 0)]

where the qn are the risk neutral probabilities.

The cost of the guarantee is the cost of a put optionwritten on the value of the asset An with a stochasticstrike price Ln

11 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The objective function

We assume that shareholders cover shortfalls

A rational strategy for the fund manager is to minimize theexpected value of shortfalls:

Γ = e−rT∑n∈NT

qn max (Ln − An, 0)]

where the qn are the risk neutral probabilities.

The cost of the guarantee is the cost of a put optionwritten on the value of the asset An with a stochasticstrike price Ln

11 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The objective function

We assume that shareholders cover shortfalls

A rational strategy for the fund manager is to minimize theexpected value of shortfalls:

Γ = e−rT∑n∈NT

qn max (Ln − An, 0)]

where the qn are the risk neutral probabilities.

The cost of the guarantee is the cost of a put optionwritten on the value of the asset An with a stochasticstrike price Ln

11 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Bilinear constraints

Denote by wn and zn the final cumulative returns of the assetand liability accounts An and Ln.For all n ∈ NT , we have:

wn =∑

i∈P(n)

RAi ,

zn =∑

i∈P(n)

g + max(δRA

i − g , 0),

Discontinuous nonlinear programming problem (DNLP)

12 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Bilinear constraints

Denote by wn and zn the final cumulative returns of the assetand liability accounts An and Ln.For all n ∈ NT , we have:

wn =∑

i∈P(n)

RAi ,

zn =∑

i∈P(n)

g + max(δRA

i − g , 0),

Discontinuous nonlinear programming problem (DNLP)

12 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Bilinear constraints / 2

Introduce the set of equations to define the max operator:

δRAn − g = ε+

n − ε−n ,ε+n ε−n = 0,

ε+n , ε

−n ≥ 0.

13 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Bilinear constraints / 3

Similarly, for the max operator in the objective function:

lnα + zn − wn = H+n − H−n ,

H+n H−n = 0,

H+n ,H

−n ≥ 0,

The cost of the guarantee becomes:

Γ(x1, x2, . . . , xJ) = e−rTA0

∑n∈NT

qnewn

(eH

+n − 1

).

14 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Bilinear constraints / 3

Similarly, for the max operator in the objective function:

lnα + zn − wn = H+n − H−n ,

H+n H−n = 0,

H+n ,H

−n ≥ 0,

The cost of the guarantee becomes:

Γ(x1, x2, . . . , xJ) = e−rTA0

∑n∈NT

qnewn

(eH

+n − 1

).

14 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Convex Put Option Model (CPOM)

Minimizex1,...,xJ

e−rTA0

∑n∈NT

qnewn

(eH

+n − 1

)(1)

s.t.

lnα + zn − wn = H+n − H−n , n ∈ NT , (2)

δRAn − g = ε+

n − ε−n , n ∈ N\{0}, (3)

zn = g T +∑

i∈P(n)

ε+i , n ∈ N\{0}, (4)

wn =∑

i∈P(n)

RAi , n ∈ N\{0}, (5)

RAn =

∑j∈J

xjRjn, n ∈ N\{0}, (6)

∑j∈J

xj = 1 (7)

15 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Lemma

Let us assume that x∗1 , x∗2 , . . . , x

∗J is an optimal portfolio choice for

the CPOM. Then,H+n H−n = 0,

for all n ∈ NT .

Lemma

Let us assume that x∗1 , x∗2 , . . . , x

∗J is an optimal portfolio choice for

CPOM. Then, it exists a non empty subset of nodes B ⊂ N suchthat ∀n ∈ B we have

ε+n ε−n = 0.

16 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Lemma

Let us assume that x∗1 , x∗2 , . . . , x

∗J is an optimal portfolio choice for

the CPOM. Then,H+n H−n = 0,

for all n ∈ NT .

Lemma

Let us assume that x∗1 , x∗2 , . . . , x

∗J is an optimal portfolio choice for

CPOM. Then, it exists a non empty subset of nodes B ⊂ N suchthat ∀n ∈ B we have

ε+n ε−n = 0.

16 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Corollary

Let x∗1 , x∗2 , . . . , x

∗J be an optimal portfolio choice for the CPOM, if

ε+k ε−k > 0, for any k ∈ N , then it exists n ∈ NT such that

k ∈ P(n) andH−n > 0 or H−n = H+

n = 0.

Theorem

Let x∗1 , x∗2 , . . . , x

∗J be an optimal portfolio choice for the CPOM,

with optimal objective value Γ∗. Let x∗∗1 , x∗∗2 , . . . , x∗∗J be anoptimal portfolio choice of the NCPOM, with optimal objectivevalue Γ∗∗. Then

Γ∗ = Γ∗∗.

17 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Corollary

Let x∗1 , x∗2 , . . . , x

∗J be an optimal portfolio choice for the CPOM, if

ε+k ε−k > 0, for any k ∈ N , then it exists n ∈ NT such that

k ∈ P(n) andH−n > 0 or H−n = H+

n = 0.

Theorem

Let x∗1 , x∗2 , . . . , x

∗J be an optimal portfolio choice for the CPOM,

with optimal objective value Γ∗. Let x∗∗1 , x∗∗2 , . . . , x∗∗J be anoptimal portfolio choice of the NCPOM, with optimal objectivevalue Γ∗∗. Then

Γ∗ = Γ∗∗.

17 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

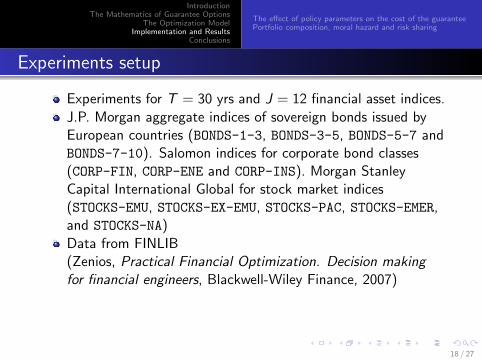

Experiments setup

Experiments for T = 30 yrs and J = 12 financial asset indices.

J.P. Morgan aggregate indices of sovereign bonds issued byEuropean countries (BONDS-1-3, BONDS-3-5, BONDS-5-7 andBONDS-7-10). Salomon indices for corporate bond classes(CORP-FIN, CORP-ENE and CORP-INS). Morgan StanleyCapital International Global for stock market indices(STOCKS-EMU, STOCKS-EX-EMU, STOCKS-PAC, STOCKS-EMER,and STOCKS-NA)Data from FINLIB(Zenios, Practical Financial Optimization. Decision makingfor financial engineers, Blackwell-Wiley Finance, 2007)Simulate risk-neutral process of asset returns using standardMontecarlo approachModel implemented simulating fan of 1000 risk-neutral paths

18 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Experiments setup

Experiments for T = 30 yrs and J = 12 financial asset indices.J.P. Morgan aggregate indices of sovereign bonds issued byEuropean countries (BONDS-1-3, BONDS-3-5, BONDS-5-7 andBONDS-7-10). Salomon indices for corporate bond classes(CORP-FIN, CORP-ENE and CORP-INS). Morgan StanleyCapital International Global for stock market indices(STOCKS-EMU, STOCKS-EX-EMU, STOCKS-PAC, STOCKS-EMER,and STOCKS-NA)

Data from FINLIB(Zenios, Practical Financial Optimization. Decision makingfor financial engineers, Blackwell-Wiley Finance, 2007)Simulate risk-neutral process of asset returns using standardMontecarlo approachModel implemented simulating fan of 1000 risk-neutral paths

18 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Experiments setup

Experiments for T = 30 yrs and J = 12 financial asset indices.J.P. Morgan aggregate indices of sovereign bonds issued byEuropean countries (BONDS-1-3, BONDS-3-5, BONDS-5-7 andBONDS-7-10). Salomon indices for corporate bond classes(CORP-FIN, CORP-ENE and CORP-INS). Morgan StanleyCapital International Global for stock market indices(STOCKS-EMU, STOCKS-EX-EMU, STOCKS-PAC, STOCKS-EMER,and STOCKS-NA)Data from FINLIB(Zenios, Practical Financial Optimization. Decision makingfor financial engineers, Blackwell-Wiley Finance, 2007)

Simulate risk-neutral process of asset returns using standardMontecarlo approachModel implemented simulating fan of 1000 risk-neutral paths

18 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Experiments setup

Experiments for T = 30 yrs and J = 12 financial asset indices.J.P. Morgan aggregate indices of sovereign bonds issued byEuropean countries (BONDS-1-3, BONDS-3-5, BONDS-5-7 andBONDS-7-10). Salomon indices for corporate bond classes(CORP-FIN, CORP-ENE and CORP-INS). Morgan StanleyCapital International Global for stock market indices(STOCKS-EMU, STOCKS-EX-EMU, STOCKS-PAC, STOCKS-EMER,and STOCKS-NA)Data from FINLIB(Zenios, Practical Financial Optimization. Decision makingfor financial engineers, Blackwell-Wiley Finance, 2007)Simulate risk-neutral process of asset returns using standardMontecarlo approach

Model implemented simulating fan of 1000 risk-neutral paths

18 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Experiments setup

Experiments for T = 30 yrs and J = 12 financial asset indices.J.P. Morgan aggregate indices of sovereign bonds issued byEuropean countries (BONDS-1-3, BONDS-3-5, BONDS-5-7 andBONDS-7-10). Salomon indices for corporate bond classes(CORP-FIN, CORP-ENE and CORP-INS). Morgan StanleyCapital International Global for stock market indices(STOCKS-EMU, STOCKS-EX-EMU, STOCKS-PAC, STOCKS-EMER,and STOCKS-NA)Data from FINLIB(Zenios, Practical Financial Optimization. Decision makingfor financial engineers, Blackwell-Wiley Finance, 2007)Simulate risk-neutral process of asset returns using standardMontecarlo approachModel implemented simulating fan of 1000 risk-neutral paths

18 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Minimum guarantee rate (g)

Min

imum

gua

rant

ee c

ost

0.0

0.5

1.0

1.5

2.0

2.5

0

0.01

0.02

0.03

0.04

0.05

0.7

0

0.01

0.02

0.03

0.04

0.05

0.8

0

0.01

0.02

0.03

0.04

0.05

1

alpha0.7 0.8 1

19 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

delta

Min

imum

gua

rant

ee c

ost

0.0

0.2

0.4

0.6

0.8

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9 1

alpha0.7 1

20 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Minimum guarantee rate (g)

Min

imum

gua

rant

ee c

ost

0.0

0.5

1.0

1.5

2.0

2.5

0

0.01

0.02

0.03

0.04

0.05

alpha0.7 0.8 0.9 1

21 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Portfolio percentages

BONDS_1_3

CORP_FIN

CORP_INS

STOCKS_EMER

STOCKS_EMU

STOCKS_PAC

0.0 0.2 0.4 0.6 0.8

0.7

0.0 0.2 0.4 0.6 0.8

0.9

g0 0.01 0.03 0.05

22 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Years

Year

ly r

etur

ns (

%)

−40

−20

0

20

40

1995 2000 2005 2010

10−Year T−Bond 3−Month T−Bill

Portfolio

1995 2000 2005 2010

−40

−20

0

20

40S&P500

23 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Minimum guarantee rate (g)

Min

imum

gua

rant

ee c

ost

0

1

2

3

4

5

0

0.01

0.02

0.03

0.04

0.05

Benchmark portfolio

0 0.01

0.02

0.03

0.04

0.05

Optimal reference portfolio

alpha0.7 0.8 0.9 1

24 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Risk Sharing

Cost of guarantee can be used to set risk sharing premia.E.g., for g=3% and α = 1 (zero equity) we have cost 0.84.

Case 1. The pension fund bears the risk of the guarantee. Thebeneficiary will pay 1.84 and will get a return only on 1 euro.

Case 2. Risk sharing between the beneficiary and a thirdparty. For example, the cost of sharing consist in paying 0.3 ofequity (α = 0.7), and investing it in the reference portfolio.The cost of the guarantee is 0.09.

25 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Risk Sharing

Cost of guarantee can be used to set risk sharing premia.E.g., for g=3% and α = 1 (zero equity) we have cost 0.84.

Case 1. The pension fund bears the risk of the guarantee. Thebeneficiary will pay 1.84 and will get a return only on 1 euro.

Case 2. Risk sharing between the beneficiary and a thirdparty. For example, the cost of sharing consist in paying 0.3 ofequity (α = 0.7), and investing it in the reference portfolio.The cost of the guarantee is 0.09.

25 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

The effect of policy parameters on the cost of the guaranteePortfolio composition, moral hazard and risk sharing

Risk Sharing

Cost of guarantee can be used to set risk sharing premia.E.g., for g=3% and α = 1 (zero equity) we have cost 0.84.

Case 1. The pension fund bears the risk of the guarantee. Thebeneficiary will pay 1.84 and will get a return only on 1 euro.

Case 2. Risk sharing between the beneficiary and a thirdparty. For example, the cost of sharing consist in paying 0.3 ofequity (α = 0.7), and investing it in the reference portfolio.The cost of the guarantee is 0.09.

25 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Concluding remarks

A general and computationally tractable model for pricing thecost of alternative embedded guarantee options in DC pensionfunds.

Model to determine the asset allocation choice that is optimalfor a given guarantee, in that it minimizes the cost of theguarantee.

Can be used to benchmark existing portfolios by applying it totest portfolios of State and local government pension funds.

Can be used to calculate risk premia for risk sharing.

26 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Concluding remarks

A general and computationally tractable model for pricing thecost of alternative embedded guarantee options in DC pensionfunds.

Model to determine the asset allocation choice that is optimalfor a given guarantee, in that it minimizes the cost of theguarantee.

Can be used to benchmark existing portfolios by applying it totest portfolios of State and local government pension funds.

Can be used to calculate risk premia for risk sharing.

26 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Concluding remarks

A general and computationally tractable model for pricing thecost of alternative embedded guarantee options in DC pensionfunds.

Model to determine the asset allocation choice that is optimalfor a given guarantee, in that it minimizes the cost of theguarantee.

Can be used to benchmark existing portfolios by applying it totest portfolios of State and local government pension funds.

Can be used to calculate risk premia for risk sharing.

26 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Concluding remarks

A general and computationally tractable model for pricing thecost of alternative embedded guarantee options in DC pensionfunds.

Model to determine the asset allocation choice that is optimalfor a given guarantee, in that it minimizes the cost of theguarantee.

Can be used to benchmark existing portfolios by applying it totest portfolios of State and local government pension funds.

Can be used to calculate risk premia for risk sharing.

26 / 27

IntroductionThe Mathematics of Guarantee Options

The Optimization ModelImplementation and Results

Conclusions

Reference

A. Consiglio, M. Tumminlello and S.A. Zenios, Designing andpricing guarantee options in defined contributions pension plans,Insurance: Mathematics and Economics, 65:267–279, 2015.

27 / 27