Master thesis I, 15 credits Master’s program in Economics, 120 credits

Spring term 2021

DETERMINANTS OF FOREIGN

DIRECT INVESTMENT IN

RWANDA

Renson Gatsinzi

1

ACKNOWLEDGEMENT

First and fore most, I thank the Almighty God for granting me life, protecting me, and for

His grace and love, without forgetting the wisdom and guidance throughout this study.

Appreciation and gratitude go to everyone who contributed towards my journey of this

research and through my entire education experience so far. However honorable mentions

are extended to the following:

I express my sincere appreciation to Umea University especially the department of

Economics for giving me the opportunity and supporting me to attain my education in

Sweden and to undertake this study.

To my family who have supported and encouraged me especially my Mum, I am very

grateful.

I extend my sincere gratitude to my supervisor Prof. Giovanni Forchini who guided and

advised me throughout this process of my research.

Finally, I thank all my friends and relatives who assisted me in various ways.

May God bless you all.

2

CONTENTS

1: INTRODUCTION ........................................................................................................................ 5

1.1: An overview of FDI in Rwanda ............................................................................................ 6

2. LITERATURE REVIEW ............................................................................................................. 7

2.1: Theoretical Literature ........................................................................................................... 7

2.2: Empirical Literature ............................................................................................................ 10

3.1: Description of data. .............................................................................................................. 14

3.2: Description of variables. ...................................................................................................... 14

3.3: Model specification .............................................................................................................. 15

3.4: Estimation procedures. ........................................................................................................ 16

3.4.1: Stationarity test. ............................................................................................................ 16

3.4.2: Selection of Optimal lag length. ................................................................................... 17

3.4.3: Cointegration test. ......................................................................................................... 17

3.4.4: Vector Error Correction Model (VECM). .................................................................. 18

4. EMPIRICAL RESULTS AND DISCUSSION ......................................................................... 19

4.1: Description statistics. ........................................................................................................... 19

4.2: Trend Analysis. .................................................................................................................... 20

4.3: Augmented Dickey-Fuller Test. .......................................................................................... 22

4.4: Selection of Optimal lag length ........................................................................................... 23

4.6.1: Vector Error Correction Model (VECM). .................................................................. 25

4.6.2: Two Long run equations. ............................................................................................. 27

4.7: VECM Post Estimation Diagnostic Tests........................................................................... 29

4.7.1: Test for Autocorrelation. .............................................................................................. 29

4.7.2: VECM Normality Test. ................................................................................................ 30

4.7.3: VECM Stability test. ..................................................................................................... 31

4.7.4: VECM Impulse Response Function (IRF). ................................................................. 32

5.1: Conclusions ........................................................................................................................... 34

5.3: Limitations and areas for further study. ........................................................................... 35

References. ....................................................................................................................................... 36

3

Abbreviations / Acronyms

FDI: Foreign Direct Investment

UNCTAD: United Nations Conference on Trade and Development

RDB: Rwanda Development Board

ADF: Augmented Dickey Fuller

MNC: Multinational Corporation

OLS: Ordinary Least Squares

SSA: Sub-Saharan Africa

M&A: Merger and Acquisition

BRICS: Brazil, Russia, India, China, South Africa

GDP: Growth Domestic Product

GMM: Generalized Method of Moments

4

ABSTRACT

This study attempts to examine the factors determining foreign direct investment in Rwanda

for the period 1970-2019. The study considers trade openness, market size, and government

expenditure as the determinants of FDI inflows. Time series analysis is used to examine the

significant determinants of FDI inflows in Rwanda. The study employs Johansen

cointegration test and VECM to establish a relationship between FDI and its determinants.

The findings indicate that trade openness (measured by sum of exports and imports as a ratio

of GDP) has a significant long run positive relationship with FDI. This implies that trade

openness is an important determinant of foreign direct investment in Rwanda. On the other

hand, market size and government expenditure are not significant determinants of FDI

inflows in Rwanda. The study concludes that openness of the Rwandan economy to a large

extent explains the direction of FDI inflows in the country and that foreign investors in

Rwanda are not market-seeking.

Key words: Foreign Direct Investment, VECM, Openness, Rwanda.

5

1: INTRODUCTION

Foreign direct investment (FDI) has become an economic buzzword as it has been perceived

by different people across time and space to play a pivotal role in the growth of economies

of both the developed and developing countries. Most developing economies lack enough

capital, and this has dramatically affected their economic growth and development. To

reverse the trend, policymakers have resorted to Investment as the panacea, especially foreign

direct investments, which will not only improve their desired gross domestic Investment and

savings but also boost the economic growth and development of these nations. FDI is

beneficial to the host economies in various ways such as job creation, transfer of knowledge,

technology spillovers, reduced prices by stimulating competition with local firms, among

others (Gichamo, 2012).

The term foreign direct investment refers to net inflows of Investment undertaken to acquire

a lasting management interest (10% or more of stock or voting rights) in a firm conducting

business in any economy other than the investor's home country. In general, an investment is

regarded as FDI when an investor establishes a business operation or acquires assets in a

foreign country. Such kinds of investments may either be in the form of "greenfield"

investment which is the establishment of a new business enterprise, or merger and acquisition

(M&A), which is investing in an already existing firm (Adeolu, 2007).

To attract more FDI, it is important that policymakers identify the factors that determine FDI

inflows in the economy.

Given the above reflections, this study seeks as its objective, to investigate and analyze the

determinants of FDI inflows in Rwanda using time series data from 1970 to 2019. Within the

context of this investigation, the study will answer two fundamental questions viz: “what are

the macroeconomic factors that drive FDI in Rwanda” and “does a reasonably stable long-

run relationship exist among FDI and these factors.”

Essentially, we consider this empirical journey important for the reasons outlined below:

6

1. Only a few studies exist on the determinants of FDI inflows in Rwanda. These studies have

largely used panel data modelling approaches dwelling on the comparative analysis of

Rwanda and other countries that may differ in economic standings.

2. Owing to the remarkably impressive growth of FDI inflows witnessed in the country in

the recent years, it becomes necessary to examine the macroeconomic drivers responsible for

such growth.

The rest of the thesis will be presented in four sections as follows: sections two and three

discuss literature review and methodology, section four contains data analysis and

discussion, section five consists of the conclusion and recommendations.

1.1: An overview of FDI in Rwanda

In the last two decades, the growth of Foreign Direct Investment (as well as Foreign Portfolio

Investment) in Rwanda has been very impressive. Statistical records reveal, for instance, that

FDI inflows increased from USD 382 million in 2018 to whopping USD 420 million in 2019,

and stocks were estimated at USD 2.6 billion at the end of 2019 (UNCTAD). Additionally,

in a report published by Rwanda Development Board (RDB) in 2019, the economy recorded

2.46 billion USD in Investment, which was a record high and of which 37% was in FDI. The

main sectors targeted by investors are Mining, Construction, and real estate, Infrastructure,

and Information and communication technologies, and according to Rwanda Development

Board (RDB) report, the major investing countries are Portugal, the UK, India, and the UAE.

The government of Rwanda has made a significant effort in attracting more FDI through

different measures to improve the investment climate in the country. Different supportive

mechanisms have been put in place, such as a one-stop center where registration of new

businesses and any information regarding Investment can be accessed, exchange platforms

between senior management and business leaders, among others. In 2015, a new investment

code was approved by the policymakers aiming at providing incentives to investors such as

a preferential corporate tax rate of 0% for an international company with its headquarters or

regional office in Rwanda, a preferential corporate tax rate of 15% for any investor, corporate

income tax holiday of up to 7 years, exemption from taxation on capital gains, exemption of

7

customs tax for products used in export processing zones, among others. The government

has also established various special economic zones such as the Kigali free zone and Kigali

industrial park free-trade zone. This has transformed Rwanda into one of the preferred

destinations for investors in recent years, and this is further evidenced by a report by world

bank 2020 in which Rwanda is ranked 38th out of 190 countries in the world in terms of ease

of doing business which makes it the highest-ranked country on the African continent.

Ameliorating Investment is seen as one of the strategies to guide the economy of Rwanda to

achieving its target of becoming a middle-income country by 2035 and a high-income

country by 2050.

2. LITERATURE REVIEW

Considerable amount of research on the determinants of FDI exist in the literature although

with differing conclusions ( see Asiedo, 2002 and Mijiyawa, 2015). An attempt is made in

this section to critically review some of these earlier studies under the broad headings of

theoretical and empirical literature.

2.1: Theoretical Literature

From the theoretical point of view, there are many scholars and schools of thought that have

come up with different theories to explain the phenomenon of FDI. Notably, in post-World

War II, some prominent theories have surfaced discussing this subject, such as Hymer (1976),

Aliber (1970), Kindleberger (1969), Knickberger (1973), Buckey and Casson (1976),

Wilhems & Witter (1998), Dunning (1974), Popovic & Calin (2014) among others. However,

there has been no consensus on a general theory that better explains FDI. These theories can

be examined from two economic perspectives, that is, the macroeconomic and

microeconomic points of view (Makoni, 2015).

The macroeconomic perspective is that FDI is a type of capital flow across borders, that is

between origin and host countries, and is captured in the balance of payments statement of

countries with the variables of interest being capital flows and stocks and revenues obtained

from those investments. The microeconomic perspective, on the other hand, relates to the

motives for investments across national boundaries, as seen from the investor's point of view

(Denisia, 2010).

FDI theories based on macroeconomic point of view include:

8

The capital market theory is also known as the "currency area theory." This theory was

based on the works of Aliber (1970), who claimed that foreign Investment came because of

imperfections in the capital market and FDI, in particular, because of differences in the

strength of currencies in the nations of origin and host nations. He argued that weaker

currencies in host nations compared to stronger currencies of the investing nations had higher

chances of attracting FDI compared to host nations with stronger currencies. Even though

the theory was proved consistent in developed countries like the USA, United Kingdom, and

Canada, it was criticized for not providing a sound explanation about Investment between

countries with equally strong currencies. Moreover, the theory did not explain the Investment

of Multinational Corporations (MNCs) from nations with weaker currencies in countries with

stronger currencies, with an example of MNCs from China and India investing in the UK and

USA (Nayak & Choudhury, 2014).

Location-based approach to FDI theory. The theory was developed by (Popovici & Calin,

2014), who articulated that the success of FDI among countries depended on factors such as

natural resource endowment, local market size, availability of labor, infrastructure, and

government policy in the country. The Authors went on to argue through their gravity

approach to FDI, which is a subsidiary to the location-based theory that FDI is more

successful if the countries involved are similar Geographically, Culturally, and economically.

Gravity variables such as size, level of development, distance, common language, and

additional institutional aspects like shareholder protection and trade openness were

considered as important determinants of FDI flows. However, the theory was criticized as

FDI flows are a more complicated theme than just similarities between countries and being

neighbours geographically may reduce transport costs but not essentially labor costs,

additionally sharing the same culture may not automatically mean increased profitability or

trade between two nations (Makoni, 2015).

Institutional FDI fitness theory. It was developed (Wilhems & Witter,1998), and the

theory focused on a country's ability to attract, absorb and retain FDI. The theory was based

on a pyramid with four fundamental pillars is Government, Market, education, and socio-

cultural fitness, which were regarded as the main determinants of the country's ability to

attract FDI inflows. The authors argued that it is not about how large the country is but how

able it is to use its macroeconomic factors such as government size, GDP, Inflation, market

9

size, among others, to fit in the required conditions to attract more FDI. The theory has been

tested empirically and proved relevant in the context of developing economies and Africa in

particular, where various studies have been conducted on FDI based on the above-mentioned

factors such as (Ho, 2011), (Amendolagine et al., 2013).

FDI theories based on microeconomic perspective discuss the motivations of FDI flows

from the investor's point of view, which implies that decision is made at the firm- level or

industry level.

Hymer (1976) developed firm-specific advantage theory in which he argued that the MNCs

decision to invest abroad is influenced by some sort of market power in the form of

advantages such as patent-protected superior technology, brand names, marketing and

management skills, economies of scale, and cheaper sources of finance (Nayak &

Choudhury, 2014). Hymer's theory laid a foundation in explaining international production,

and it was supported by scholars such as Kindleberger (1969) in his monopolistic power

model, Knickerbocker's (1973) oligopolistic theory of following the market leader, the

internalization theory of Buckley and Casson (1976) in an international context, among

others.

All microeconomic-based FDI theories are based on the same fundamental principle of the

existence of market imperfections. Dunning (1980), in his award-winning FDI theory,

combined these theories by introducing an eclectic paradigm that contextualized ownership,

internalization, and localizing advantages attained by MNCs as a three-tier masterpiece for

the engagement of FDI and international production. Dunning asserted that a firm must

satisfy three conditions simultaneously to take part in FDI.

Firstly, a firm must possess specific and exclusive ownership advantages such as trademarks,

patents, information, and technology over other rival firms to serve a particular market. Such

advantages would enable the firm to outcompete its rival in a foreign country.

Secondly, these advantages must be more profitable to the firm possessing them to use them

than to lease or sell them to a foreign firm in the form of licensing or management contracts.

Finally, suppose the above two conditions are met, the firm must benefit more from utilizing

the advantages in production in combination with other factor inputs like labor, natural

resources in a foreign country (Makoni, 2015).

10

To sum up, what has been discussed, having analysed different theories of FDI, there is no

single theory that comprehensively explains FDI. It is therefore up to the researcher to choose

which theory to base on while discussing FDI. However, Dunning's theory of the Electric

paradigm is the most recognized theory of FDI.

2.2: Empirical Literature

Several studies have been conducted to examine the determinants of FDI on the continental,

regional, and country levels. Different results were obtained, and varying conclusions were

made about what factors are more significant in determining FDI flows.

In one of the earliest studies on the subject in Africa, Morisset (2000) analyzed what

determines FDI in Africa. Using cross-section and panel data from 29 Sub-Sahara African

(SSA) countries, he asserted that FDI in African countries is determined by factors such as

natural resources, market size, economic growth, trade liberalization, macroeconomic

stability, political stability. The author also concluded that Africa could capture more

attention of foreign investors not only based on Natural resources or targeting the local

market size but also with the implementation of some visible and pro-active policy reforms

and improving their business climate.

In a contradicting fashion, Asiedu (2004) conducted a study on policy reforms and Foreign

Direct Investment in Africa. The author found out that, despite making some policy

improvements and reforming their institutions, improving their infrastructures, and

liberalizing their FDI regulatory framework, developing countries in Sub-Sahara Africa

(SSA) have continued to have a small share of FDI compared with developing countries in

other regions. She asserted that the cause for SSA being less competitive in attracting FDI is

due to mediocre reforms in comparison with the implemented reforms by other developing

countries in other regions.

In a similar study, Investigating 71 developing countries (32 Sub- Saharan African countries

and 39 non-Sub- Saharan African countries) (Asiedu, 2002), used cross-sectional data

analysis for the period1988-1997 and found that developing countries in SSA differ from

developing countries in other regions in what attracts FDI. According to the author, the

results showed that Trade openness attracts FDI to developing countries in both SSA and

11

non-SSA regions. However, the marginal effect of trade openness in SSA is lower. She

further illustrated that Infrastructure development and a higher return to Investment

positively influence FDI to non-SSA, but that is not the case for developing countries in SSA.

Using the fixed effect model, Suliman & Mollick (2009) investigated determinants of FDI

for 29 SSA countries using panel data collected between 1980 and 2003. They discovered

that GDP per capita growth, Human capital, openness, and infrastructure development have

a positive effect on FDI. On the other hand, political rights and civil rights, and liquidity size

of the market all exert a negative impact on FDI.

(Gichamo, 2012) carried out a study on the determinants of foreign direct investment inflows

in Sub - Saharan Africa, with panel data for the period 1986-2010 from a sample of 14

countries. The author employed pooled OLS, fixed effect, and random effect estimators, and

empirical results showed that gross domestic product, trade openness, Inflation, and a lag of

FDI are the most significant determinants of FDI inflows in Sub-Saharan Africa. The study

also found that the relationship between FDI inflows and telephone lines is insignificant. The

author also highlighted that the significance of variables is differing with countries.

Mijiyawa (2015) agreed with Gichamo (2012) in analyzing what drives FDI in Africa. The

author used panel data on 53 countries for the period 1970-2009 and employed a Fixed effect

estimator and Generalized Method of Moments (GMM) for analysis. The empirical results

showed that lagged FDI inflows, trade openness, political stability, market size, and return

on Investment are the significant determinants of FDI inflows to Africa. The author asserted

that it is not only about how big the country is but also the openness of the economy as well

as how stable the country is political. The study recommended the need to strengthen regional

integration to promote trade and a good political relationship among countries in the region.

For the case of developing countries, (Mottaleb & Kalirajan, 2010) examined the

determinants of FDI in developing countries. Considering factors like GDP size, GDP growth

rate, trade, aid, labor force, days required to start a business, growth rate of industrial value-

added, and the number of telephone users, the study used panel data on 68 low-income and

lower-middle-income countries from Africa, Asia, and Latin America for the period 2005-

2007. The results illustrated that, countries with larger GDP, higher GDP growth rate, a

12

higher proportion of international trade, and a more business-friendly environment attract

more FDI inflows. The study also concluded that small, developing countries could attract

more FDI by implementing more outward-oriented trade policies and providing a more

business-friendly environment to foreign investors.

Similarly, (Kumari & Sharma, 2017) analysed the determinants of FDI in developing

countries using panel data on 20 developing nations for the period 1990-2012. The study

considered factors such as market size, trade openness, infrastructure, Inflation, interest rate,

research and development, and human capital as the potential determinants of FDI and

utilized fixed effect and random effect estimators to analyze the data. The findings

established that market size, trade openness, and human capital are the significant

determinants of FDI in developing countries. The authors also asserted that market size is the

most important factor in attracting FDI in developing economies.

Using a holistic approach, (Jadhav, 2012) conducted a study to examine the economic,

institutional, and political determinants of FDI in Brazil, Russia, India, China, and South

Africa (BRICS). The study used panel data from 2000 to 2009 and employed panel unit root

and multiple regressions. The study considered market size, trade openness, and natural

resources as economic determinants, whilst macroeconomic stability, political stability,

government effectiveness, the rule of law, control of corruption, regulatory policy, and voice

and accountability as institutional and political determinants. The results established that

economic determinants are more significant than institutional and political determinants in

BRICS economies. The findings also indicated that market size and trade openness are

positive and significant determinants of FDI in BRICS whilst natural resources availability

is negatively related to FDI. According to the author, FDI in BRICS is more motivated by

market-seeking purposes and not resource-seeking.

In a similar study, Labes (2015) attempted to analyse FDI determinants in BRICS economies.

The study used panel data from 1992 to 2012. Considering factors such as Trade openness,

GDP per capita, population, exchange rate, and human capital as potential determinants, the

study employed pooled OLS, fixed effect, and random effect estimators. The findings found

13

that trade openness, GDP per capita, and exchange rate are the significant determinants of

FDI in BRICS economies. Narayanamurthy et al. (2017) examined the determinants of FDI

for BRICS countries using fixed effects and random effects estimators on panel data collected

from 1975 to 2007. The authors found that FDI in BRICS is determined by market size,

Industrial production, Labour cost, infrastructure facilities, Growth capital formation. On the

contrary, economic stability, growth prospects, and Trade openness have no significant

impact on FDI flows.

Meanwhile, Ang (2008) utilized the two-stage least squares methodology to analyze the

determinants of FDI in Malaysia using data collected from 1960-2005. According to the

Author, financial development, Infrastructure development, GDP growth, trade openness,

government size, and macroeconomic uncertainty all have a positive impact on FDI.

However, real exchange rates and taxation are negatively related to FDI.

Analyzing the determinants of FDI in Afghanistan, Wani & Tahiri (2017) used OLS on time

series data collected from 2005 to 2015, and the results revealed that total debt service, total

external debt, gross domestic product, and gross fixed capital formation positively affect FDI.

Inflation, on the other hand, negatively impacts FDI.

Dondashe & Phiri (2018) investigated the determinants of FDI for the South African

economy using time series data collected between 1994 and 2016. They deployed ARDL and

found that GDP per capita, Government size, real interest rate, and terms of trade are positive

determinants of FDI. On the other hand, the inflation rate negatively affects FDI.

(Habimana, 2018) examined the determinants of FDI in Rwanda. He established that GDP

as a proxy for the size of the economy and Inflation as a proxy for the stability of the economy

are significant factors in determining FDI inflows in Rwanda. The findings established that

GDP affected FDI positively whilst Inflation exerted a negative impact on FDI. The study

also found out that Exchange was not a significant determinant for FDI flows in Rwanda.

Sajilan et al. (2019), utilizing data on 42 countries, analyzed the determinants of FDI in

Organization of Islamic countries (OIC) countries. Panel data from 1996 to 2013 were

analyzed using fixed effect and random effect estimators, and the results showed that the size

14

of the economy, infrastructure, and trade openness exert a positive impact on FDI. On the

other hand, Institutional quality was negatively related to FDI, and the impact of Inflation on

FDI is mixed.

In summary, different researchers utilized various econometric methods such as Fixed and

random effect estimators on different kinds of data such as cross-section, panel, and time

series to analyze the determinants of FDI and achieved different conflicting results. However,

GDP, trade openness, and market size have been found to be the most significant

determinants of FDI by most of the studies.

3. RESEARCH METHODOLOGY

This chapter discusses the methodology used by the research to collect, process, and analyze

data. Annual time series data are used in this study, and an econometric model is developed

to examine how GDP per capita, trade openness, and Government Expenditure determine

Foreign Direct Investment (FDI) inflows in Rwanda in the period 1970 to 2019.

3.1: Description of data.

Annual time series data are collected on FDI net inflows, GDP per capita, trade openness,

and government expenditure for the period 1970 to 2019 to analyze the determinants of FDI

in Rwanda. The Source of the data on all variables was the World Bank (World Development

Indicators, 2020). More details about the relevant variables are explained in section 3.2

below.

3.2: Description of variables.

Foreign Direct Investment (FDI). It measures the net inflows of investment to acquire a

lasting management interest (10 percent or more of voting stock) in an existing enterprise in

any economy other than that of the investor. The series shows net inflows of investment to

an economy from the rest of the world as a percentage of GDP. The unit of measurement is

percent.

15

Gross Domestic Product per capita (GDPPC). It measures gross domestic product divided

by mid-year population. It determines the income earned per person in the economy. Other

factors being constant, GDPPC determines the demand of all individuals in the economy. In

this study, GDPPC is used as the proxy for market size, and a higher GDP per capita implies

a large market which is an incentive to attract foreign Investment. It is expected to be a

positive and significant determinant of FDI inflows. Some previous researchers used the

same variable, such as (Dondashe & Phiri, 2018). The unit for GDP per capita in this study

is USD millions (constant 2010).

Trade openness (TRDOP). It indicates the level of restrictions on trade activities in the host

economy. Investors prefer a more open economy which will allow them to export their

products to the markets abroad and import some intermediate goods that are used as raw

materials during production. This study used "Volume of Trade as a ratio of GDP," which is

measured by the sum of exports and imports of goods and services as a ratio of GDP to proxy

trade openness. It is expected to be a positive and significant determinant of FDI inflows.

(Mijiyawa, 2015), (Asiedu, 2002) and (Kumari & Sharma, 2017), among others, used the

same variable. The unit of measurement is percentage.

Government Expenditure (GE). It measures government consumption, investment, and

transfer payments. Expenditure on infrastructure such as roads, electricity, education acts as

an incentive to FDI. The study used general government final consumption expenditure as a

proxy for Government expenditure. Therefore, we expect a positive and significant

relationship between government expenditure and FDI. Some previous pieces of literature

utilized the same variable, such as (Adeolu, 2007) ( Norashida et al., 2016). The unit of

measure is USD millions (constant 2010).

3.3: Model specification

This study is built on the assumption that GDP per capita, trade openness, and Government

Expenditure determine Foreign Direct Investment (FDI) inflows. The groundbreaking work

of (Sims, 1980) laid a foundation for the study of how macroeconomic series are interrelated.

It is upon this background that economic theory developed Vector autoregressive (VAR)

model as an essential tool for analyzing empirically how economic variables are interrelated

16

in the short run. The phenomenon of VAR is further well described by (Levendis, 2018) in

his own words,

"If we take the notion of general equilibrium seriously, then everything in the economy is

related to everything else. For this reason, it is impossible to say which variable is exogenous.

It is possible that all variables are endogenous: they can all be caused and simultaneously be

the cause of some other variables".

Based on previous literature such as (Seetanah & Rojid, 2011), this study specified a vector

autoregressive model to analyze the relationship between FDI and its determinants in

Rwanda, and it is presented as:

𝑌𝑡 = 𝛽 + ∑ 𝛾𝑖𝑝𝑖=1 𝑌𝑡−1 + 𝑢𝑡 (1)

Where:

𝑌𝑡= (FDI, GDPPC, TRDOP, GE) represents a kx1 vector of endogenous variables

FDI= Foreign Direct Investment Net Inflows

GDPPC= Gross Domestic Product per capita

TRDOP= Trade Openness

GE= Government Expenditure

𝛾𝑖 (𝑖 = 1,2 3, … , 𝑝) represents a k x k matrix of autoregressive coefficients.

𝑢𝑡 It is a k x 1 vector of error terms that is identically and independently distributed.

3.4: Estimation procedures.

3.4.1: Stationarity test.

The stationarity test is essential when dealing with time-series data. In general, time series

are characterized by unit-roots, and therefore they are nonstationary. When a nonstationary

time series variable is regressed on another time series, it leads to a spurious regression. The

results from the regression might report significant coefficients with a remarkably high R2

even though there is no meaningful relationship between the two variables. These results

17

from such regression may be biased and misleading. A nonstationary time series is less

considered in forecasting as its behaviour is suited for a study only for the time under

consideration (Gujarati & Porter, 2009).

The presence of a unit root in a time series indicates that the series under study is

nonstationary. This study employed Augmented Dickey-Fuller (ADF) test to conduct the

stationarity test of the variables and determine their order of integration.

3.4.2: Selection of Optimal lag length.

The optimal number of lags is a requirement to carry out a cointegration test as well as to

estimate a well-established VAR model. Choosing the number of lags to include in the model

is difficult because the inclusion of too many lags may lead to loss of degrees of freedom and

risk facing a problem of multicollinearity whilst including too few lags may lead to

misspecification of the model and omission of important lagged variables. However, there

is no economic theory that explains the exact number of lags that should be in our model.

The choice of the optimal lag length is empirical, and there are various lag selection criteria

utilized in determining the optimal lag length for our VAR model, such as Final Prediction

Error (FPE), Schwarz Bayesian Information Criterion (SBIC), Akaike information criterion

(AIC), Hannan-Quinn information criterion (HQIC), Likelihood Ratio, etc. The most notable

and used among these are the Akaike information criterion (AIC) and Schwartz Bayesian

Information Criterion (SBIC), but the choice on which one to use between the two is

discretionary and exigent on the model, but the one with a lower value is preferred.

Furthermore, it is advisable to consider AIC when one has a small sample that is 60 or fewer

observations as it minimizes the chances of underestimating the true number of lags (Liew,

2006). This study employed AIC given that the number of observations is 50, and it has the

lowest value in comparison with the rest of the criteria.

3.4.3: Cointegration test.

Two or more nonstationary economic variables are cointegrated if they have a common

stochastic trend. This implies that a linear combination of them is stationary (Lutkepohl &

Kratzig, 2004). In which case, if variables are cointegrated, they have a long-run or

equilibrium relationship (Gujarati & Porter, 2009). There are two common approaches

utilized in cointegration testing. These are the Engle-Granger approach and the Johansen

18

cointegration test approach. Engle-Granger's approach is suitable for a univariate model with

only two variables, whereas the Johansen approach is well suited for a multivariate model as

it allows for simultaneous estimation of all the cointegrating relationships in the model under

study (Levendis, 2018). The fact that our model has four variables, this study utilized the

Johansen Cointegration test approach.

3.4.4: Vector Error Correction Model (VECM).

When relevant variables in the model are not cointegrated, it is recommended to use Vector

Autoregressive (VAR) model to analyze the short-run economic relationship among

variables. However, if the variables are I (1) and cointegrated, it is appropriate to estimate

Vector Error Correction Model (VECM) to analyze the short-run dynamics and long-run

cointegrating relationships among the variables (Kilian & Lutkepohl, 2016).

VECM is a special type of VAR model that is specified with cointegration restrictions which

limit the long-run behaviour of the endogenous variables to converge to cointegrating

relationships by an Error correction term (Stock &Watson, 2011). Since VECM is a

differenced VAR, it is specified and estimated with (p-1) lags, and the dependent variable is

a function of its lagged value, lagged values of other explanatory variables in the model, the

ECT, and a stochastic error term or impulse which is independent and identically distributed.

Given that the variables in our model are I (1) and cointegrated, this study applied VECM.

The VECM approach is usually modelled in the way:

∆Yt = β + ∑ Γ𝑖𝑝−1𝑖=1 ∆Yt-i + ПEt-1 + 𝑢𝑡 (2)

Where,

∆𝑌𝑡= 𝑌𝑡 - 𝑌𝑡−1

Et-1 represents the Error Correction Term (ECT) which is the lagged value of the residuals

obtained from the cointegrating regression of the dependent variable on the regressors. It

contains long-run information obtained from the long-run cointegrating relationship, П is

the speed of adjustment parameter which measures the speed at which the variables re-

establish equilibrium after deviations in the short run.

19

4. EMPIRICAL RESULTS AND DISCUSSION

4.1: Description statistics.

This section presents a summary of the data, and the results are reported in Table1. The

number of observations is 50 years from 1970 to 2019. The mean values of variables, Foreign

Direct Investment net inflows (FDI), Gross Domestic Product Per capita (GDPPC), Trade

Openness (TRDOP), and Government Expenditure (GE), is 1.166%, 467m USD, 34.6%, and

467 million USD, respectively. Interestingly, it is noted that mean values for all variables are

positive. This indicates that FDI inflows in Rwanda increased during most of the time under

study. The median values for FDI, GDPPC, TRDOP, and GE are 0.78%, 416.8m USD,

32.5%, and 304 million USD, respectively. Notably, the maximum and minimum values for

all variables indicate a large dispersion, and this is further shown by the high standard

deviation for all the variables, which indicates the deviation from their mean.

Table 1: Summary of descriptive statistics (1970-2019)

Variable Obs Mean Std. Dev. Median Min Max

FDI 50 1.166181 1.142797 .7879802 .0001327 3.807796

GDPPC 50 467.0239 158.0846 416.8239 219.6367 901.3044

TRDOP 50 34.62947 9.970366 32.5398 19.6842 71.0956

GE 50 467.08 423.13 304.32 481.53 1,770

Source: Author’s computation from Stata 16.4

For ease of interpretation and to account for influence of outliers that might characterize our

data, all variables are transformed into their natural logarithmic forms. Additionally,

transforming the series into logs ensures stable variance of the variables in the model. So, the

next tests will use the variables in their natural logarithm form. The variables will be:

lnFDI = Natural logarithm of FDI

20

lnGDPPC = Natural logarithm of GDPPC

lnTRDOP = Natural logarithm of TRDOP

lnGE = Natural logarithm of GE

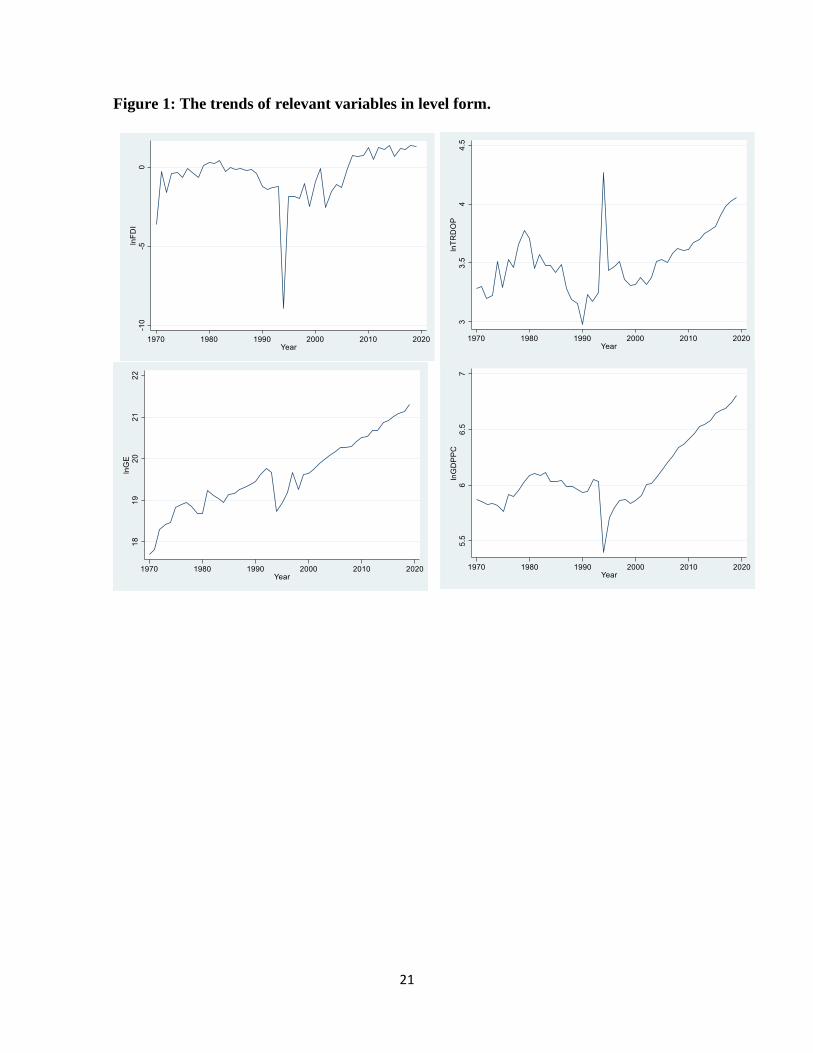

4.2: Trend Analysis.

Figure1 below shows the individual trends of all the relevant variables over the period of

study (1970-2019). The trends of all the variables show fluctuations in the same direction.

Additionally, there is a sharp decline in all the variables between 1990 and 1995. This is

reasonable because it was during the period of war, instability, and the infamous 1994

Genocide in Rwanda. However, after 1995 all the variables show a gradual increase which

implies that the economy was under-recovery and new policies being implemented. After the

year 2000 up to 2019, GDPPC, TRDOP, and GE are observed to be increasing at a high rate.

FDI, however, has been increasing but still volatile. It is noted that trends of relevant

variables in their levels presented in figure 1 show a tendency of fluctuating away from the

mean, suggesting that the mean is not constant; therefore, we suspect that all the variables

are nonstationary at levels. Figure 2, on the other hand, shows the first difference of all the

variables, and their trend shows a tendency to fluctuate around the mean, suggesting that

variables are stationary at their first difference.

Figures 1 and 2 depict the trends of the variables in their levels and at their first difference,

respectively.

21

Figure 1: The trends of relevant variables in level form.

22

Figure 2: The trends of the first difference of the relevant variables.

4.3: Augmented Dickey-Fuller Test.

To test the stationarity of the relevant variables and determine their order of integration,

Augmented Dickey-Fuller (ADF) was used, and the results are reported in Table4.2. The

number of lags was determined based on Ng and Perron (1995), with a maximum lag of 10

set based on the rule of thumb suggested by Schwert (1989). It is noted that FDI and TRDOP

were tested at lag 1, GDPPC was tested at lag 0, and GE was tested at lag 2. The test was

performed on all the variables in their natural logarithm (ln) form to account for the possible

presence of heteroskedasticity. The results from the test gave enough evidence to accept the

null hypothesis of unit root for lnFDI, lnGDPPC, lnTRDOP, lnGE, given that the t-statistics

23

in absolute value were less than the critical value at a 5% significance level, which means

that all the variables are nonstationary in their level form.

However, at their first difference, all the variables are stationary. This implies that all the

relevant variables are integrated of order one, that is, they are I (1).

Table 2: ADF Unit Root Test Results.

Variable ADF Statistics Order of Integration

Level First Diff Lags I(d)

lnFDI -2.571 -8.071*** 1 I (1)

lnGDPPC -1.649 -8.633 *** 0 I (1)

lnTRDOP -2.293 -7.114*** 1 I (1)

lnGE -2.588 -6.049 *** 2 I (1)

Source: Author's computation from Stata 16.4

Note: *** Implies significant at 1% level of significance. The critical values at 1%, 5% and

10% significance levels are -4.168, -3.508, and -3.185 respectively.

4.4: Selection of Optimal lag length

Before conducting a cointegration test and estimating the VAR model, it is appropriate to

select the number of lags to utilize in the estimation. Choosing the number of lags to include

in the model is difficult because the inclusion of too many lags may lead to loss of degrees

of freedom and risk facing a problem of multicollinearity whilst including too few lags may

lead to misspecification of the model and omission of important lagged variables. However,

there is no economic theory that explains the exact number of lags that should be included in

the model under study.

The choice of the optimal lag length is empirical, and there are various lag selection criteria

considered in determining the optimal lag length for our model, such as Final Prediction Error

(FPE), Akaike Information Criterion (AIC), Hannan-Quinn Information Criterion (HQIC),

and Schwartz and Bayesian Information Criterion (SBIC). Among all the Information

24

criteria, it is the choice of the researcher to choose which one to use. However, the criterion

with the lowest value is preferred. All the criteria suggested one lag as the optimal lag length

for the model under study, as shown by the results reported in Table4.3 below. This study

utilized AIC, given that it has the lowest value.

Table 3: Results for the lag selection test.

Lag LL LR FPE AIC HQIC SBIC

0 -

74.4961

NA .000357 3.41287 3.47244 3.57188

1 49.8661 248.72 3.2e-06* -1.29852* -1.00069* -.503463*

2 58.7226 17.713 4.5e-06 -.987939 -.451836 .443172

3 74.1468 30.848 4.8e-06 -.962906 -.188535 1.10425

4 94.3093 40.325* 4.3e-06 -1.14388 -.131246 1.55932

Source: Author’s computation from Stata 16.4

4.5: Johansen Cointegration Test.

After establishing that all the variables are integrated of order one and determining the

optimal lag length, it is appropriate to test for cointegration to discover if the relevant

variables have a long-run relationship. Johansen cointegration test was employed to

determine the possible number of cointegrating equations in the model. The decision criteria

is that Trace statistics and max statistics are compared to their respective 5% critical value.

If the trace statistics and max statistics are greater than critical value, null hypothesis of (no

cointegration) is rejected and vice versa.

The optimal lag length of one suggested by AIC in Table 3 above was utilized in the test, and

the results are reported in Table 4 below. From the results, both Trace statistics and Max

statistics suggested two cointegrating equations in the model. This indicates that there is a

long-run or equilibrium relationship among the relevant variables in the model under

consideration.

25

Table 4: Johansen Cointegration Test results.

Maxi.

Rank

Parms

Trace

Statistics

5% Crit.

Value

Max Statistic

5% Crit. Value

0 4 90.3725 47.21 45.185 27.07

1 11 35.8540 29.68 27.8762 20.97

2 16 7.9778* 15.41 7.8540 14.07

3 19 0.1238 3.76 0.1238 3.76

4 20

Source: Author's computation from Stata 16.4

4.6.1: Vector Error Correction Model (VECM).

This section intends to analyse the short-run dynamics in the relevant variables in the model.

The most important part of the short-run analysis of a VECM is the Error Correction Term

(ECT) which estimates the speed at which variables return to equilibrium in case of

deviations in the short run. More so, it indicates that the deviations of the variables from the

equilibrium are gradually corrected through the adjustments. It is very important when the

coefficient of the ECT is negative and statistically significant.

The ECTs are denoted as ECT1 and ECT2 for every variable in the model, and the results

are shown in Table 5. The results are explained in detail below, with much emphasis on the

FDI model.

VECM is specified and estimated with (p-1) lags, the optimal lag length (p) for the model

under study was 1 as suggested by AIC in optimal lag selection test above. For this reason,

the results from VECM estimation did not generate parameters for short run dynamics of the

relevant variables in the model. Only the coefficients estimating speed of adjustments to re-

establish equilibrium in case of deviations in the short run were generated. However, this is

26

not problematic because the objective of the study is to establish a long run relationship

among the variables in the model. The speed of adjustment for all the relevant variables is

discussed in detail below.

Foreign Direct Investment (FDI).

The coefficient for ECT1 has a negative sign and is statistically significant. The speed of

adjustment is approximately 74% per year towards the equilibrium. This implies that FDI has

a relatively high speed of adjustment to converge to the equilibrium in case of any

unanticipated shocks or innovations. On the other hand, the coefficient for ECT2 indicates

that the speed of adjustment for FDI is 227% per year. However, it has a positive sign and is

statistically insignificant.

Gross domestic product per capita (GDPPC)

The results show that the coefficient for ECT1 is 0.009, which implies that the speed of

adjustment for GDPPC is approximately 0.9% per year towards equilibrium. It is positive

and statistically insignificant. Whilst the coefficient of ECT2 illustrates that the speed of

adjustment for GDPPC is 12.7% every year towards equilibrium.

Trade openness (TRDOP)

The coefficient of ECT1 shows that TRDOP adjusts at a speed of 2.5% per to return to

equilibrium, whilst ECT2 indicates that the speed of adjustment for TRDOP towards

equilibrium is 29.7% per year. However, both coefficients are positive and statistically

insignificant.

Government expenditure (GE)

Empirical results indicate that from the coefficient of ECT1, the speed of adjustment for GE

is 0.06% per year towards equilibrium, while the coefficient of ECT2 illustrates that GE

adjusts at 6.2% per year to return to equilibrium in case of a shock in the independent

variables. However, the coefficients are statistically insignificant.

27

Table 5: VECM Estimation results.

Coef. Std. Err. P-value

∆lnFDI

ECT1 -.7455105 .1859339 0.000

ECT2 2.278555 1.637923 0.164

∆lnGDPPC

ECT1 .0091554 .0145099 0.528

ECT2 -.2956986 .1278197 0.021

∆lnTRDOP

ECT1 .025997 .0260177 0.318

ECT2 .2974828 .2291942 0.194

∆lnGE

ECT1 -.006356 .0316 0.841

ECT2 -.0629743 .2783697 0.821

Source: Author’s computation from Stata 16.4

The fact that all the relevant variables are nonstationary at levels and only become stationary

after the first difference and they are cointegrated puts the focus of this study to investigate

the long-run relationship among the variables in the model. The next section describes the

long-run relationships in the model under study.

4.6.2: Two Long run equations.

Levendis (2018) suggested that the most important part of the VECM economically is the

cointegrating equations. It indicates the cointegrating relationships among the variables of

interest. From Table 6 below, _ce1 and _ce2 show that there are two cointegrating equations

in the model.

28

The Johansen identification scheme placed four constraints on the parameters in the two

cointegrating equations. In the first cointegrating equation, lnFDI was normalized to one

while lnGDPPC was normalized to zero implying that market size does not have a long run

relationship with FDI inflows in Rwanda. Similarly, in the second cointegrating equation,

lnFDI was normalized to zero whereas, lnGDPPC was normalized to one.

Table 6: Normalized Cointegration Coefficients.

_ce1 Beta Coef. Std. Err. P-value

lnFDI 1 .

lnGDPPC 0 (Omitted)

lnTRDOP -6.20824 1.440296 0.000

lnGE .3950569 .4227777 0.350

_cons 14.36179 .

_ce2

lnFDI 0 (Omitted)

lnGDPPC 1 .

lnTRDOP -1.058901 .1881433 0.000

lnGE -.1457104 .0552267 0.008

_cons .4517458 .

Source: Author's computation from Stata 16.4

It is noted that all the variables are in log form, so the coefficients can be interpreted as long-

run elasticity.

The first long run equation is therefore presented as:

lnFDI = 0.62lnTRDOP – 0.395lnGE – 14.36 (6)

29

This implies that Foreign Direct Investment is a function of Trade Openness and Government

expenditure.

The positive cointegrating coefficient for trade openness is 0.62, indicating a positive

relationship between trade openness and FDI inflows, implying that a 1% increase in Trade

openness increases FDI inflows by 0.62%. The results confirm the prior expectations, and

this implies that trade openness is an important factor in attracting FDI into Rwanda.

The empirical results show a negative relationship between government expenditure and FDI

inflows, meaning a 1% increase in government expenditure results in a decrease in Foreign

Direct Investment by 0.39%. Though the coefficient is statistically insignificant, and the

result is inconsistent with the prior expectations.

The second long run equation is presented as:

lnGDPPC = 1.059lnTRDOP + 0.146lnGE – 0.45 (7)

This means that GDP per capita is a function of trade openness and government expenditure.

The coefficient 1.059 is positive, which implies a positive relationship between trade

openness and market size in Rwanda. When trade openness increases by 1%, GDP per capita

increases by 1.059%.

According to the results, the cointegrating coefficient for government expenditure is 0.146

illustrating a positive relationship between government expenditure and market size,

meaning that a 1% increase in government expenditure increases market size by 0.146%.

4.7: VECM Post Estimation Diagnostic Tests.

Post-estimation tests are conducted to ensure that the fitted model is valid. These tests are

intended to check stochastic properties of the model, such as normal distribution of the

residuals, presence of serial correlation in the error terms, stability of the model.

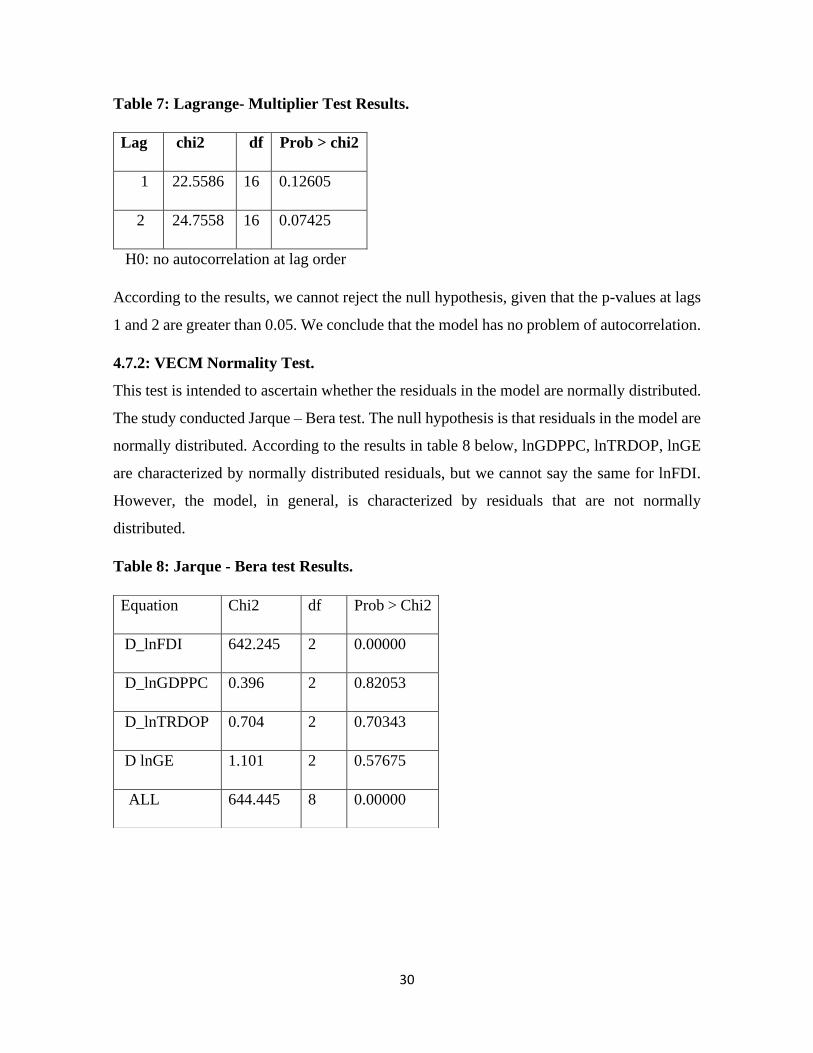

4.7.1: Test for Autocorrelation.

It is essential to test for serial correlation in the residuals after estimating a VECM. We

conducted Lagrange -multiplier test, and the null hypothesis is that there is no autocorrelation

at lag order d, and the results are reported in Table 7.

30

Table 7: Lagrange- Multiplier Test Results.

Lag chi2 df Prob > chi2

1 22.5586 16 0.12605

2 24.7558 16 0.07425

H0: no autocorrelation at lag order

According to the results, we cannot reject the null hypothesis, given that the p-values at lags

1 and 2 are greater than 0.05. We conclude that the model has no problem of autocorrelation.

4.7.2: VECM Normality Test.

This test is intended to ascertain whether the residuals in the model are normally distributed.

The study conducted Jarque – Bera test. The null hypothesis is that residuals in the model are

normally distributed. According to the results in table 8 below, lnGDPPC, lnTRDOP, lnGE

are characterized by normally distributed residuals, but we cannot say the same for lnFDI.

However, the model, in general, is characterized by residuals that are not normally

distributed.

Table 8: Jarque - Bera test Results.

Equation Chi2 df Prob > Chi2

D_lnFDI 642.245 2 0.00000

D_lnGDPPC 0.396 2 0.82053

D_lnTRDOP 0.704 2 0.70343

D lnGE 1.101 2 0.57675

ALL 644.445 8 0.00000

31

4.7.3: VECM Stability test.

The stability test for VEM is conducted to check that the model is unbiased and that we have

correctly specified the number of cointegrating equations in the model. To check the stability

condition, the companion matrix of a VECM with K variables and r integrating equations has

K-r unit eigenvalues. The model is stable if the moduli of the remaining r eigenvalues are

strictly less than one. However, there is no general distribution theory to back up the

statement (Brinkgreve & Kumarswamy, 2008).

Table 9: Eigenvalue Stability Condition.

Eigenvalue Modulus

1 1

1 1

.3733731 .373373

.1156825 .115682

The VECM specification imposes 2 unit moduli.

Figure 3: Roots of the companion matrix.

32

The results reported in Table 9 show that the specified VECM imposes 2 unit moduli on the

companion matrix and the remaining eigenvalues are less than 1. It is further observed on the

footer in Figure 3 that none of the remaining eigenvalues are closer to the unit circle. This

implies that the model meets the stability condition and therefore it is robust.

4.7.4: VECM Impulse Response Function (IRF).

IRF describes the effect of impulses, innovations, or shocks in one time series variable on

another variable after a given number of periods (steps). It shows the responsiveness of a

dependent variable in case of unanticipated shock in the independent variable, the sign of the

effect, and how long it takes for the dependent variable to respond to the shock.

Unlike shocks in VAR models which vanish over time, shocks in VECM do not diminish

and therefore are either permanent or transitory. This study estimated a VECM impulse

response function to examine the impact of shocks in trade openness, market size, and

government expenditure on Foreign Direct Investment in Rwanda for 15 years to check the

persistence of the shock in the long run, and the results are shown in figure 4 below. The

response is statistically significant if the responses are above the zero line, and it is

statistically insignificant if it is below the zero line (Ahmad, 2015).

33

Figure 4: Results of the Impulse Response Function of VECM.

According to the results in figure 4, a one-time shock in trade openness has a permanent

positive effect on foreign direct investment inflows in Rwanda, whilst a shock in government

expenditure exerts a negative impact on FDI inflows in Rwanda. On the other hand, a shock

in market size has a transitory effect on foreign direct investment inflows in Rwanda. It is

further noted from figure 4 that FDI responds immediately to the shocks in the explanatory

variables because the change starts in the first period.

From figure 4 FDI responds in a mixed manner to a shock in GDP per capita. The response

is negative in the first two years, it increases after that up until the fourth year and the impact

of the shock stabilizes after four years. However, it noted from the figure that the response is

minimal because the deviation of the graph from zero line is small both positively and

negatively.

The response of FDI inflows to a shock in government expenditure is negative and decreasing

although it stabilizes after two years. This is surprising given that an increase in government

expenditure is expected to have a positive impact on FDI inflows. This could be because the

34

government of Rwanda spends on activities that are not related to promotion of FDI.

However, the response is statistically insignificant as it is below the zero line.

Foreign Direct Investment responds positively to a shock in trade openness. From the

beginning, a shock in trade openness leads to a rapid increase in FDI inflows. When the

economy is more liberalized, the country is engaged in more international trade activities and

increase foreign investors are induced to invest more.

5. Conclusions and recommendations

This section presents a summary of findings and conclusions from the study,

recommendations to the policymakers, as well as suggestions for further studies about the

same subject that would yield better outcomes.

5.1: Conclusions

This study provided a time series analysis of the determinants of FDI in Rwanda from 1970

to 2019. Variables such as trade openness, market size and government expenditure were

considered by the study as the potential determinants of FDI inflows in Rwanda. Johansen

cointegration test and VECM were employed to establish the long run relationship between

FDI and its determinants. Results from a unit root test using ADF established that all the

variables were nonstationary at levels but stationary in their first difference. This implies that

all the variables are integrated of order one. It was also shown that variables in the model

were cointegrated, suggesting a long-run equilibrium relationship among the relevant

variables.

Findings from VECM model showed that there is a long-run positive relationship between

trade openness which is measured by the sum of exports and imports as a ratio of GDP and

FDI, implying that trade openness is an important factor in determining FDI in Rwanda.

These results indicate that foreign investors in Rwanda are attracted by openness of the

economy and the good exporting policy in the country. On the other hand, market size is

found not to be a significant determinant of FDI inflows in Rwanda. This could be related to

the small population size of the country, which was 12.63 million in 2019. This implies that

MNCs in Rwanda are not market-seeking. Similarly, government expenditure is reported not

35

to be an important determinant of foreign direct investment in Rwanda despite a sound

theoretical argument.

Furthermore, results also established that approximately 74% of discrepancies between

equilibrium and short-run FDI are corrected per year.

Results from IRF showed that a shock in trade openness had a permanent positive impact on

FDI inflow in Rwanda, whilst a shock in government expenditure had a permanent negative

effect on FDI. A shock in market size, on the other hand, had a transitory impact on FDI

inflows.

5.2: Recommendations.

The results suggested that trade openness is a very important factor in determining FDI

inflows in Rwanda. This implies that the policymakers should formulate and implement more

policies aimed at liberalizing the economy and making it more open to international trade to

induce more foreign investors into the country. Engaging in more economic integrations

would be a good strategy to make the economy more involved in international trade there by

opening more doors for FDI inflows.

5.3: Limitations and areas for further study.

The study was restricted to a few variables, especially on the economic determinants of FDI,

due to the availability of data. Further studies with the inclusion of political and institutional

determinants may yield better results.

Conducting a similar study using different proxies for variables like government expenditure

and market size may provide different and significant results.

36

References.

Adeolu, B. A. (2007). FDI and Economic Growth: Evidence from Nigeria. In AERC

ResearchPaper(Vol.165,IssueApril).

https://publications.aercafricalibrary.org/bitstream/handle/123456789/22/RP_165.pdf?

sequence=1&isAllowed=y

Ahmad, F. (2015). Determinants of savings behavior in Pakistan: Long run-short run

association and causality. Timisoara Journal of Economics and Business, 8(1), 103-136.

Aliber, R.Z. 1970, "A theory of direct foreigninvestment", The international corporation, pp.

17-34.

Amendolagine, V., Boly, A., Coniglio, N. D., Prota, F., & Seric, A. (2013). FDI and Local

Linkages in Developing Countries: Evidence from Sub-Saharan Africa. World

Development, 50, 41–56. https://doi.org/10.1016/j.worlddev.2013.05.001

Ang, J. B. (2008). Determinants of foreign direct investment in Malaysia. Journal of Policy

Modeling, 30(1), 185–189. https://doi.org/10.1016/j.jpolmod.2007.06.014

Asiedu, E. (2002). On the determinants of foreign direct investment to developing countries:

Is Africa different? World Development, 30(1), 107–119.

https://doi.org/10.1016/S0305-750X(01)00100-0

Asiedu, E. (2004). Policy Reform and Foreign Direct Investment in Africa: Absolute

Progress but Relative Decline. In Development Policy Review (Vol. 22, Issue 1).

Overseas Development Institute. www.avmedia.at/nepad/

Brinkgreve, R. B. J., & Kumarswamy, S. (2008). Reference Manual Reference Manual. In

Technology (Vol. 1, Issue November).

Buckley P. and Casson M. (1976), “The Future of the Multinational Enterprise”, London,

37

MacMillan.

Denisia, V. (2010). Dunning OLI paradigm theory. European Journal of Interdisciplinary

Studies, 2(2), 104–110.

Dondashe, N., & Phiri, A. (2018). Munich Personal RePEc Archive Determinants of FDI in

South Africa : Do macroeconomic variables matter ? Munich Personal RePEc Archive,

83636.

Dunning, J.H. 1980, "Toward an eclectic theory of international production", The

International Executive, vol. 22, no. 3, pp. 1-3.

Dunning, J.H. 1980, "Towards an eclectic theory ofinternational production: some empirical

tests",

Journal of International Business Studies, vol. 11, no.1, pp. 9-31.

Gichamo, T. Z. (2012). Determinants of Foreign Direct Investment Inflows to Sub-Saharan

Africa: a panel data analysis. 2012.

Habimana, S. (2018). Analysis of the Determinants of Foreign Direct Investment in Rwanda

( Period of 1970-2010 ): Econometric Approach. 6, 1–26.

Ho, C. S. F. (2011). Macroeconomic and Country Specific Determinants of FDI Panel Error

Correction Model View project Event Study View project. September 2011.

https://www.researchgate.net/publication/278390346

Hymer, S.H. 1976, The international operations ofnational firms: A study of direct foreign

investment,MIT press Cambridge, MA.

Jadhav, P. (2012). Determinants of foreign direct investment in BRICS economies: Analysis

of economic, institutional and political factor. Procedia - Social and Behavioral

Sciences, 37, 5–14. https://doi.org/10.1016/j.sbspro.2012.03.270

Kindelberger C. (1969), “American Business Abroad: Six lectures on direct investment”,

NewHaven: Yale University Press.

Knickerbockers F. (1973), “Oligopolistic reaction and multinational enterprise”,

ThunderbirdInternational Business Review, 15(2), 7-9.

38

Kumari, R., & Sharma, A. K. (2017). Determinants of foreign direct investment in

developing countries: a panel data study. International Journal of Emerging Markets,

12(4), 658–682. https://doi.org/10.1108/IJoEM-10-2014-0169

Labes,S.-A.(2015).FDI Determinants in BRICS. VII(2), 296–308.

http://ceswp.uaic.ro/articles/CESWP2015_VII2_LAB.pdf

Levendis, J. D. (2018). Time Series Econometrics: Learning Through Replication. In

Springer Texts in Business and Economics. https://doi.org/10.1007/978-3-319-98282-

3%0Ahttp://link.springer.com/10.1007/978-3-319-98282-3

Liew, V. K. (2006). Which Lag Length Selection Criteria Should We Employ. Economics

Bulletin, 3(33), 1–9.

Lütkepohl, H. & Krätzig, M.,. (2004). Applied time series econometrics (No. 04; HA30. 3,

A6.). Cambridge/MA: Cambridge University Press.

Makoni, P. L. (2015). 10-22495_Rgcv5I2C1Art1.Pdf. 5(2), 77–83.

Mijiyawa, A. G. (2015). What Drives Foreign Direct Investment in Africa? An Empirical

Investigation with Panel Data. African Development Review, 27(4), 392–402.

https://doi.org/10.1111/1467-8268.12155

Morisset, J. (2000). Foreign Direct Investment in Africa: Policies Also Matter (Google

eBook). May, 20.

http://books.google.com/books?hl=en&lr=&id=rRzktbMMWmQC&pgis=1

Mottaleb, K. A., & Kalirajan, K. (2010). Determinants of Foreign Direct Investment in

Developing Countries: A Comparative Analysis. Margin, 4(4), 369–404.

https://doi.org/10.1177/097380101000400401

Narayanamurthy, V., Sridharan, P., & Rao, K. C. sekhara. (2017). Determinants of FDI in

BRICS Countries: A panel analysis. Int. Journal of Business Science and Applied

Management, 5(3). http://www.sussex.ac.uk/spru/

Nayak, D. & Choudhury, R.N. 2014, A selective review of foreign direct investment theories,

(No.143), ARTNeT Working Paper Series.

39

Othman, Norashida; Yusop, Zulkornain; Andaman, Gul; Ismail, M. M. (2016). Impact of

Government Spending on Small. International Journal of Business and Society, 1(2),

41–56.

Popovici, O.C. & Călin, A.C. 2014, "FDI theories. Alocation-based approach", Romanian

EconomicJournal, vol. 17, no. 53, pp. 3-24.

Sajilan, S., Islam, M. U., Ali, M., & Anwar, U. (2019). The determinants of FDI in OIC

countries. International Journal of Financial Research, 10(5), 466–473.

https://doi.org/10.5430/ijfr.v10n5p466

Seetanah, B., & Rojid, S. (2011). The determinants of FDI in Mauritius: a dynamic time

series investigation. African Journal of Economic and Management Studies, 2(1), 24–

41. https://doi.org/10.1108/20400701111110759

Sims, C. A. (1980). Macroeconomics and Reality. Econometrica, 48(1), 1.

https://doi.org/10.2307/1912017

Stock, J. H., & Watson, M. W. (2012). Introduction to econometrics. Pearson Education

Limited. Third Edition.

Suliman, A. H., & Mollick, A. V. (2009). Human capital development, war and foreign direct

investment in sub-Saharan Africa. Oxford Development Studies, 37(1), 47–61.

https://doi.org/10.1080/13600810802660828

Wani, N. U. H., & Tahiri, N. R. (2017). Determinants of FDI in Afghanistan: An Empirical

Analysis. Journal of International Business and Economies, 2(2), 61–70.

Wilhelms S., Stanley M. and Witter D. (1998), “Foreign direct investment and its

determinantsin emerging economies”, African Economic Policy Discussion Paper No.

9, July.